13/48 EMA Trading Scalper (ATR TP/SL)13/48 EMA Trading Scalper (ATR TP/SL)

What it does:

This tool looks for price “touches” of the 13-EMA, only takes CALL entries when the 13 is above the 48 (uptrend) and PUT entries when the 13 is below the 48 (downtrend), and confirms with a simple candle pattern (green > red with expansion for calls, inverse for puts). Touch sensitivity is ATR-scaled, so signals adapt to volatility. Each trade gets auto-drawn entry, TP, and SL lines, colored labels with $ / % distance from entry, plus optional TP/SL hit alerts. A rotating color palette and per-bar label staggering help keep the chart readable. Old objects are auto-pruned via maxTracked.

How it works

Trend filter: 13-EMA vs 48-EMA.

Entry: ATR-scaled touch of the 13-EMA + candle confirmation.

Risk: TP/SL = ATR multiples you control.

Visuals: Entry/TP/SL lines (extend right), vertical entry marker (optional), multi-line labels.

Hygiene: maxTracked keeps only the last N trades’ objects; labels are staggered to reduce overlap.

Alerts: Buy Call, Buy Put, Take Profit Reached, Stop Loss Hit.

Key Inputs

Fast EMA (13), Trend EMA (48), ATR Length (14)

Touch Threshold (x ATR) – how close price must come to the EMA

Take Profit (x ATR), Stop Loss (x ATR)

maxTracked – number of recent trades to keep on chart

Tips

Start with Touch = 0.10–0.20 × ATR; TP=2×ATR, SL=1×ATR, then tune per symbol/timeframe.

Works on intraday and higher TFs; fewer, cleaner signals on higher TFs.

This is an indicator, not a broker—always backtest and manage risk.

Options

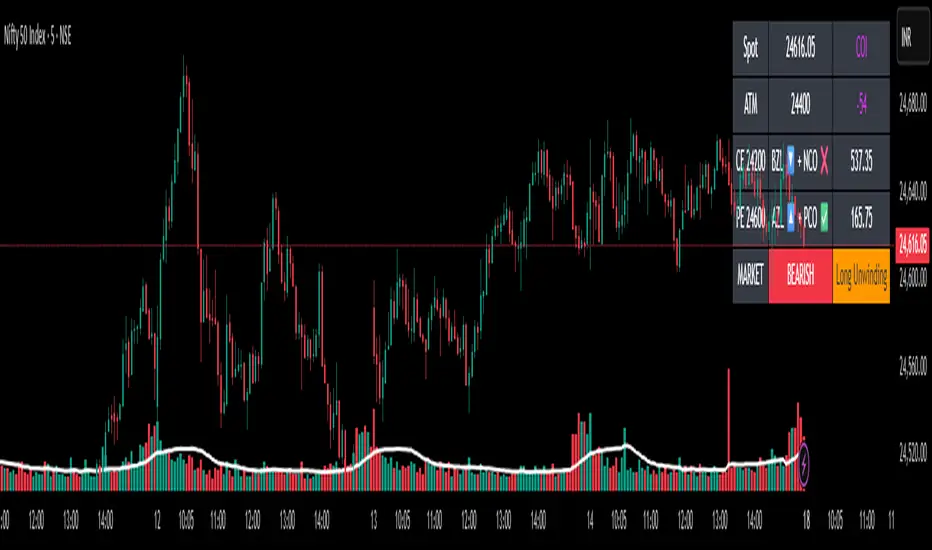

✨Smart Option MACD: Bullish, Bearish, Neutral Logic by AKM ✨The **Smart Option MACD: Bullish, Bearish, Neutral Logic by AKM** is an advanced indicator designed for TradingView, tailored for option traders on indices like NIFTY. It automates options trend scanning by applying MACD analysis to both Call (CE) and Put (PE) options near the ATM (At-The-Money) strike, providing actionable market states—Bullish, Bearish, or Neutral—using distinct logic for both strikes and overall market context.

***

### Core Features

- **Option Selection Logic:** The script dynamically calculates ATM, CE, and PE strike prices based on the underlying index spot price and customizable user inputs for expiry, strike distance, and OTM/ITM shift.

- **MACD on Option Prices:** For both CE and PE symbols, the indicator computes the MACD (Moving Average Convergence Divergence) and Signal lines. It uses standard MACD settings: 12-period EMA (fast), 26-period EMA (slow), and 9-period Signal.

- **Strike Status Classification:**

- AZL 🔼: Indicates MACD > 0 for that option, signifying positive momentum.

- BZL 🔽: Indicates MACD 0 & crossover up), PE is bearish (MACD<0 & crossover down).

- **Bearish:** PE is bullish & crossover up, CE is bearish & crossover down.

- **Neutral:** All other scenarios—including mixed or undefined signals.

***

### Table Output

A real-time table is displayed on the chart (top-right) with key option and market details:

- Spot price

- ATM Strike

- CE/PE strike status (momentum + crossover logic)

- Option prices

- Overall market state, color-coded for clarity

***

### How to Use This Indicator

- **Entry Signal:** Use the Bullish/Bearish status for directional trades or option strategies. Bullish calls for buying or selling upward momentum options; Bearish favors downside trades. Neutral advises caution or range-bound trades.

- **Customizability:** Expiry, strike width, OTM/ITM offset, and chart resolution are user-controlled, allowing adaptation to different market contexts.

- **Best Practice:** Use alongside price action, support/resistance zones and other indicators to confirm options momentum, as MACD is powerful yet not infallible.

***

### Who Is It For?

- **Option traders** who want to automate trend/momentum detection for CE/PE strikes instead of manual chart switching.

- **Index traders** (NIFTY, BANKNIFTY...) seeking systematic edge in intraday/positional strategies tied to option momentum.

- **Technical analysts** interested in visual, rule-based signals combining options data and classic MACD logic.

***

The Smart Option MACD indicator streamlines multi-strike, multi-option momentum analysis and presents clear actionable logic directly on your chart for enhanced decision-making. Use it as a core part of your TradingView toolkit for options-focused market views.

RSI 20/80 Arrows + AlertsRSI 20/80 Arrows + Alerts

This indicator is a modified Relative Strength Index (RSI) tool designed to help traders spot potential overbought and oversold conditions using customizable threshold levels (default 80 for overbought, 20 for oversold).

Features:

Custom RSI Levels – Default to 80/20 instead of the standard 70/30, but fully adjustable by the user.

Visual Signals –

Blue Arrow Up appears below the bar when RSI crosses up from below the oversold level (potential buy zone).

Red Arrow Down appears above the bar when RSI crosses down from above the overbought level (potential sell zone).

Alerts Built In – Receive notifications when either signal occurs, with the option to confirm signals only on bar close for reduced noise.

Guide Levels – Optionally display overbought/oversold reference lines on the chart for quick visual reference.

Overlay Mode – Signals are plotted directly on the price chart, so you don’t need to switch between chart windows.

Use Case:

Ideal for traders who want quick, visual confirmation of potential turning points based on RSI, especially in strategies where more extreme levels (like 20/80) help filter out weaker signals. Works well across all markets and timeframes.

Price Level Alert System

Price Level Alert System - Manage Multiple Price Alerts in One

This indicator is designed to simplify price level monitoring by allowing you to manage up to 5 different price alerts through a single, unified alert system. Instead of creating multiple separate alerts for different price levels, you can now monitor all your key levels with just one alert subscription.

Key Benefits:

Unified Alert Management - Monitor 5 price levels with a single alert, saving your valuable alert slots

Clean Chart Interface - Toggle price levels on/off without cluttering your chart

Smart Alert Types - Get notified for price crosses (above/below) and approaching alerts

Customizable Appearance - Adjust colors, transparency, and line width for each level individually

Efficient Workflow - Inline controls make setup quick and intuitive

Perfect For:

Traders monitoring multiple support/resistance levels

Swing traders tracking key price targets

Day traders needing quick alert setup

Anyone wanting to maximize their TradingView alert efficiency

How It Works:

Simply enter your desired price levels, check the boxes to enable them, and click the bell icon to activate alerts. The indicator will monitor all enabled levels and send notifications through a single alert when price action occurs at any of your specified levels.

Features:

5 independent price levels

Individual on/off toggles

Approaching distance alerts (customizable percentage)

Cross above/below notifications

Professional line styling options

Status line price display

Save your alert slots and streamline your trading workflow with this efficient price level monitoring solution. Whether you're tracking support/resistance, psychological levels, or price targets, this indicator helps you stay informed without the complexity of managing multiple individual alerts.

ICT/SMC Liquidity Map V3 KyroowThe indicator is designed to map liquidity on the chart following the ICT/SMC logic, with the added feature of precise tracking of the Asian session.

It shows you:

PDH / PDL → Previous Day High & Low, automatically removed once taken out.

EQH / EQL → Equal Highs & Equal Lows (double tops/bottoms), with pip tolerance and a check to ensure no candle has already "cleared" the range.

ASH / ASL → Asian Session High & Low (the highs/lows of each closed Asian session).

Asian Session → Displayed as a box or shaded area, with visual history.

Dynamic tolerance management → EQH/EQL can have different tolerances depending on the timeframe.

Automatic removal → Levels are removed once the market takes them (via wick or body, configurable).

💡 In practice:

It helps you quickly identify likely liquidity grab zones, whether they come from the previous day, the Asian session, or equal highs/lows. This allows you to anticipate market reactions around these levels.

GLD GC Price Converter Its primary function is to fetch the prices of the Gold ETF (ticker: GLD) and Gold Futures (ticker: GC1!) and then project significant price levels from one or both of these assets onto the chart of whatever instrument you are currently viewing.

Core Functionality & Features

Dual Asset Tracking: The script simultaneously tracks the prices of GLD and Gold Futures (GC).

Dynamic Price Level Projection: The script's main feature is its ability to calculate and draw horizontal price levels. It determines a "base price" (e.g., the nearest $100 level for GC) and then draws lines at specified increments above and below it. The key is that these levels are projected onto the current chart's price scale.

On-Chart Information Display:

Price Table: A customizable table can be displayed in any corner of the chart, showing the current prices of GLD and GC. It can also show the daily percentage change for GC, colored green for positive changes and red for negative ones.

Last Price Label: It can show a label next to the most recent price bar that displays the current prices of both GLD and GC.

Extensive Customization: The user has significant control over the indicator's appearance and behavior through the settings panel.

This includes:

Toggling the display for GLD and GC levels independently.

Adjusting the multiplier for the price levels (e.g., show levels every $100 or $50 for GC).

Changing the colors, line styles (solid, dashed, dotted), and horizontal offset for the labels.

Defining the number of price levels to display.

Controlling the text size for labels and the table.

Choosing whether the script updates on every tick or only once per candle close for better performance.

💎 ENJOYBLUE ⏰ Open Price AlertThis Pine Script (version 6) is designed for TradingView to monitor the closing of a user-selected Timeframe (TF) — for example, M30, H1, H4, or D1 — and trigger an alert immediately when that TF’s candle closes. Along with the alert, it displays the current open prices from four higher-level timeframes:

Open MN: Open price of the current monthly candle

Open W1: Open price of the current weekly candle

Open D1: Open price of the current daily candle

Open H4: Open price of the current 4-hour candle

The alert message is formatted into a single compact line to ensure it is fully visible on mobile devices!

~ENJOYBLUE 💎

TCP | Market Session | Session Analyzer📌 TCP | Market Session Indicator | Crypto Version

A powerful, real-time market session visualization tool tailored for crypto traders. Track the heartbeat of Asia, Europe, and US trading hours directly on your chart with live session boxes, behavioral analysis, liquidity grab detection, and countdown timers. Know when the action starts, how the market behaves, and where the traps lie.

🔰 Introduction:

Trade the Right Hours with the Right Tools

Time matters in trading. Most significant moves happen during key sessions—and knowing when and how each session unfolds can give you a sharp edge. The TCP Market Session Indicator, developed by Trade City Pro (TCP), puts professional session tracking and behavioral insights at your fingertips.

Whether you're a scalper or swing trader, this indicator gives you the timing context to enter and exit trades with greater confidence and clarity.

🕒 Core Features

• Live Session Boxes :

Highlight active ranges during Asia, Europe, and US sessions with dynamic high/low updates.

• Session Start/End Labels :

Know exactly when each session begins and ends plotted clearly on your chart with context.

• Session Behavior Analysis :

At the end of each session, the indicator classifies the price action as:

- Trend Up

- Trend Down

- Consolidation

- Manipulation

• Liquidity Grab Detection: Automatically detects possible stop hunts (fake breakouts) and marks them on the chart with precision filters (volume, ATR, reversal).

• Session Countdown Table: A live dashboard showing:

- Current active session

- Time left in session

- Upcoming session and how many minutes until it starts

- Utility time converter (e.g. 90 min = 01:30)

• Vertical Session Lines: Visualize past and upcoming session boundaries with customizable history and future range.

• Multi-Day Support: Draw session ranges for previous, current, and future days for better backtesting and forecasting.

⚙️ Settings Panel

Customize everything to fit your trading style and schedule:

• Session Time Settings:

Set the opening and closing time for each session manually using UTC-based minute inputs.

→ For example, enter Asia Start: 0, Asia End: 480 for 00:00–08:00 UTC.

This gives full flexibility to adjust session hours to match your preferred market behavior.

• Enable or Disable Elements:

Toggle the visibility of each session (Asia, Europe, US), as well as:

- Session Boxes

- Countdown Table

- Session Lines

- Liquidity Grab Labels

• Timezone Selection:

Choose between using UTC or your chart’s local timezone for session calculations.

• Customization Options:

Select number of past and future days to draw session data

Adjust vertical line transparency

Fine-tune label offset and spacing for clean layout

📊 Smart Session Boxes

Each session box tracks high, low, open, and close in real time, providing visual clarity on market structure. Once a session ends, the box closes, and the behavior type is saved and labeled ideal for spotting patterns across sessions.

• Asia: Green Box

• Europe: Orange Box

• US: Blue Box

💡 Why Use This Tool?

• Perfect Timing: Don’t get chopped in low-liquidity hours. Focus on sessions where volume and volatility align.

• Pattern Recognition: Study how price behaves session-to-session to build better strategies.

• Trap Detection: Spot manipulation moves (liquidity grabs) early and avoid common retail pitfalls.

• Macro Session Mapping: Use as a foundational layer to align trades with market structure and news cycles.

🔍 Example Use Case

You're watching BTC at 12:45 UTC. The indicator tells you:

The Asia session just ended (label shows “Asia Session End: Trend Up”)

Europe session starts in 15 minutes

A liquidity grab just triggered at the previous high—label confirmed

Now you know who’s active, what the market just did, and what’s about to start—all in one glance.

✅ Why Traders Trust It

• Visual & Intuitive: Fully chart-based, no clutter, no guessing

• Crypto-Focused: Designed specifically for 24/7 crypto markets (not outdated forex models)

• Non-Repainting: All labels and boxes stay as printed—no tricks

• Reliable: Tested across multiple exchanges, pairs, and timeframes

🧩 Built by Trade City Pro (TCP)

The TCP Market Session Indicator is part of a suite of professional tools used by over 150,000 traders. It’s coded in Pine Script v6 for full compatibility with TradingView’s latest capabilities.

🔗 Resources

• Tutorial: Learn how to analyze sessions like a pro in our TradingView guide:

"TradeCityPro Academy: Session Mapping & Liquidity Traps"

• More Tools: Explore our full library of indicators on

SquirrelofwallstreetAlien technologia

possible strategic entrie

English:

This content is provided for informational purposes only. We disclaim any responsibility for how it may be used. Please consult a qualified professional for any specific advice.

Ayman – Full Smart Suite Auto/Manual Presets + PanelIndicator Name

Ayman – Full Smart Suite (OB/BoS/Liq/FVG/Pin/ADX/HTF) + Auto/Manual Presets + Panel

This is a multi-condition trading tool for TradingView that combines advanced Smart Money Concepts (SMC) with classic technical filters.

It generates BUY/SELL signals, draws Stop Loss (SL) and Take Profit (TP1, TP2) levels, and displays a control panel with all active settings and conditions.

1. Main Features

Smart Money Concepts Filters:

Order Block (OB) Zones

Break of Structure (BoS)

Liquidity Sweeps

Fair Value Gaps (FVG)

Pin Bar patterns

ADX filter

Higher Timeframe EMA filter (HTF EMA)

Two Operating Modes:

Auto Presets: Automatically adjusts all settings (buffers, ATR multipliers, RR, etc.) based on your chart timeframe (M1/M5/M15).

Manual Mode: Fully customize all parameters yourself.

Trade Management Levels:

Stop Loss (SL)

TP1 – partial profit

TP2 – full profit

Visual Panel showing:

Current settings

Filter status

Trend direction

Last swing levels

SL/TP status

Alerts for BUY/SELL conditions

2. Entry Conditions

A BUY signal is generated when all these are true:

Trend: Price above EMA (bullish)

HTF EMA: Higher timeframe trend also bullish

ADX: Trend strength above threshold

OB: Price in a valid bullish Order Block zone

BoS: Structure break to the upside

Liquidity Sweep: Sweep of recent lows in bullish context

FVG: A bullish Fair Value Gap is present

Pin Bar: Bullish Pin Bar pattern detected (if enabled)

A SELL signal is generated when the opposite conditions are met.

3. Stop Loss & Take Profits

SL: Placed just beyond the last swing low (BUY) or swing high (SELL), with a small ATR buffer.

TP1: Partial profit target, defined as a ratio of the SL distance.

TP2: Full profit target, based on Reward:Risk ratio.

4. How to Use

Step 1 – Apply Indicator

Open TradingView

Go to your chart (recommended: XAUUSD, M1/M5 for scalping)

Add the indicator script

Step 2 – Choose Mode

AUTO Mode: Leave “Use Auto Presets” ON – parameters adapt to your timeframe.

MANUAL Mode: Turn Auto OFF and adjust all lengths, buffers, RR, and filters.

Step 3 – Filters

In the Filters On/Off section, enable/disable specific conditions (OB, BoS, Liq, FVG, Pin Bar, ADX, HTF EMA).

Step 4 – Trading the Signals

Wait for a BUY or SELL arrow to appear.

SL and TP levels will be plotted automatically.

TP1 can be used for partial close and TP2 for full exit.

Step 5 – Alerts

Set alerts via BUY Signal or SELL Signal to receive notifications.

5. Best Practices

Scalping: Use M1 or M5 with AUTO mode for gold or forex pairs.

Swing Trading: Use M15+ and adjust buffers/ATR manually.

Combine with price action confirmation before entering trades.

For higher accuracy, wait for multiple filter confirmations rather than acting on the first arrow.

6. Summary Table

Feature Purpose Can Disable?

Order Block Finds key supply/demand zones ✅

Break of Structure Detects trend continuation ✅

Liquidity Sweep Finds stop-hunt moves ✅

Fair Value Gap Confirms imbalance entries ✅

Pin Bar Price action reversal filter ✅

ADX Trend strength filter ✅

HTF EMA Higher timeframe confirmation ✅

Crypto Options Greeks & Volatility Analyzer [BackQuant]Crypto Options Greeks & Volatility Analyzer

Overview

The Crypto Options Greeks & Volatility Analyzer is a comprehensive analytical tool that calculates Black-Scholes option Greeks up to the third order for Bitcoin and Ethereum options. It integrates implied volatility data from VOLMEX indices and provides multiple visualization layers for options risk analysis.

Quick Introduction to Options Trading

Options are financial derivatives that give the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (strike price) within a specific time period (expiration date). Understanding options requires grasping two fundamental concepts:

Call Options : Give the right to buy the underlying asset at the strike price. Calls increase in value when the underlying price rises above the strike price.

Put Options : Give the right to sell the underlying asset at the strike price. Puts increase in value when the underlying price falls below the strike price.

The Language of Options: Greeks

Options traders use "Greeks" - mathematical measures that describe how an option's price changes in response to various factors:

Delta : How much the option price moves for each $1 change in the underlying

Gamma : How fast delta changes as the underlying moves

Theta : Daily time decay - how much value erodes each day

Vega : Sensitivity to implied volatility changes

Rho : Sensitivity to interest rate changes

These Greeks are essential for understanding risk. Just as a pilot needs instruments to fly safely, options traders need Greeks to navigate market conditions and manage positions effectively.

Why Volatility Matters

Implied volatility (IV) represents the market's expectation of future price movement. High IV means:

Options are more expensive (higher premiums)

Market expects larger price swings

Better for option sellers

Low IV means:

Options are cheaper

Market expects smaller moves

Better for option buyers

This indicator helps you visualize and quantify these critical concepts in real-time.

Back to the Indicator

Key Features & Components

1. Complete Greeks Calculations

The indicator computes all standard Greeks using the Black-Scholes-Merton model adapted for cryptocurrency markets:

First Order Greeks:

Delta (Δ) : Measures the rate of change of option price with respect to underlying price movement. Ranges from 0 to 1 for calls and -1 to 0 for puts.

Vega (ν) : Sensitivity to implied volatility changes, expressed as price change per 1% change in IV.

Theta (Θ) : Time decay measured in dollars per day, showing how much value erodes with each passing day.

Rho (ρ) : Interest rate sensitivity, measuring price change per 1% change in risk-free rate.

Second Order Greeks:

Gamma (Γ) : Rate of change of delta with respect to underlying price, indicating how quickly delta will change.

Vanna : Cross-derivative measuring delta's sensitivity to volatility changes and vega's sensitivity to price changes.

Charm : Delta decay over time, showing how delta changes as expiration approaches.

Vomma (Volga) : Vega's sensitivity to volatility changes, important for volatility trading strategies.

Third Order Greeks:

Speed : Rate of change of gamma with respect to underlying price (∂Γ/∂S).

Zomma : Gamma's sensitivity to volatility changes (∂Γ/∂σ).

Color : Gamma decay over time (∂Γ/∂T).

Ultima : Third-order volatility sensitivity (∂²ν/∂σ²).

2. Implied Volatility Analysis

The indicator includes a sophisticated IV ranking system that analyzes current implied volatility relative to its recent history:

IV Rank : Percentile ranking of current IV within its 30-day range (0-100%)

IV Percentile : Percentage of days in the lookback period where IV was lower than current

IV Regime Classification : Very Low, Low, High, or Very High

Color-Coded Headers : Visual indication of volatility regime in the Greeks table

Trading regime suggestions based on IV rank:

IV Rank > 75%: "Favor selling options" (high premium environment)

IV Rank 50-75%: "Neutral / Sell spreads"

IV Rank 25-50%: "Neutral / Buy spreads"

IV Rank < 25%: "Favor buying options" (low premium environment)

3. Gamma Zones Visualization

Gamma zones display horizontal price levels where gamma exposure is highest:

Purple horizontal lines indicate gamma concentration areas

Opacity scaling : Darker shading represents higher gamma values

Percentage labels : Shows gamma intensity relative to ATM gamma

Customizable zones : 3-10 price levels can be analyzed

These zones are critical for understanding:

Pin risk around expiration

Potential for explosive price movements

Optimal strike selection for gamma trading

Market maker hedging flows

4. Probability Cones (Expected Move)

The probability cones project expected price ranges based on current implied volatility:

1 Standard Deviation (68% probability) : Shown with dashed green/red lines

2 Standard Deviations (95% probability) : Shown with dotted green/red lines

Time-scaled projection : Cones widen as expiration approaches

Lognormal distribution : Accounts for positive skew in asset prices

Applications:

Strike selection for credit spreads

Identifying high-probability profit zones

Setting realistic price targets

Risk management for undefined risk strategies

5. Breakeven Analysis

The indicator plots key price levels for options positions:

White line : Strike price

Green line : Call breakeven (Strike + Premium)

Red line : Put breakeven (Strike - Premium)

These levels update dynamically as option premiums change with market conditions.

6. Payoff Structure Visualization

Optional P&L labels display profit/loss at expiration for various price levels:

Shows P&L at -2 sigma, -1 sigma, ATM, +1 sigma, and +2 sigma price levels

Separate calculations for calls and puts

Helps visualize option payoff diagrams directly on the chart

Updates based on current option premiums

Configuration Options

Calculation Parameters

Asset Selection : BTC or ETH (limited by VOLMEX IV data availability)

Expiry Options : 1D, 7D, 14D, 30D, 60D, 90D, 180D

Strike Mode : ATM (uses current spot) or Custom (manual strike input)

Risk-Free Rate : Adjustable annual rate for discounting calculations

Display Settings

Greeks Display : Toggle first, second, and third-order Greeks independently

Visual Elements : Enable/disable probability cones, gamma zones, P&L labels

Table Customization : Position (6 options) and text size (4 sizes)

Price Levels : Show/hide strike and breakeven lines

Technical Implementation

Data Sources

Spot Prices : INDEX:BTCUSD and INDEX:ETHUSD for underlying prices

Implied Volatility : VOLMEX:BVIV (Bitcoin) and VOLMEX:EVIV (Ethereum) indices

Real-Time Updates : All calculations update with each price tick

Mathematical Framework

The indicator implements the full Black-Scholes-Merton model:

Standard normal distribution approximations using Abramowitz and Stegun method

Proper annualization factors (365-day year)

Continuous compounding for interest rate calculations

Lognormal price distribution assumptions

Alert Conditions

Four categories of automated alerts:

Price-Based : Underlying crossing strike price

Gamma-Based : 50% surge detection for explosive moves

Moneyness : Deep ITM alerts when |delta| > 0.9

Time/Volatility : Near expiration and vega spike warnings

Practical Applications

For Options Traders

Monitor all Greeks in real-time for active positions

Identify optimal entry/exit points using IV rank

Visualize risk through probability cones and gamma zones

Track time decay and plan rolls

For Volatility Traders

Compare IV across different expiries

Identify mean reversion opportunities

Monitor vega exposure across strikes

Track higher-order volatility sensitivities

Conclusion

The Crypto Options Greeks & Volatility Analyzer transforms complex mathematical models into actionable visual insights. By combining institutional-grade Greeks calculations with intuitive overlays like probability cones and gamma zones, it bridges the gap between theoretical options knowledge and practical trading application.

Whether you're:

A directional trader using options for leverage

A volatility trader capturing IV mean reversion

A hedger managing portfolio risk

Or simply learning about options mechanics

This tool provides the quantitative foundation needed for informed decision-making in cryptocurrency options markets.

Remember that options trading involves substantial risk and complexity. The Greeks and visualizations provided by this indicator are tools for analysis - they should be combined with proper risk management, position sizing, and a thorough understanding of options strategies.

As crypto options markets continue to mature and grow, having professional-grade analytics becomes increasingly important. This indicator ensures you're equipped with the same analytical capabilities used by institutional traders, adapted specifically for the unique characteristics of 24/7 cryptocurrency markets.

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

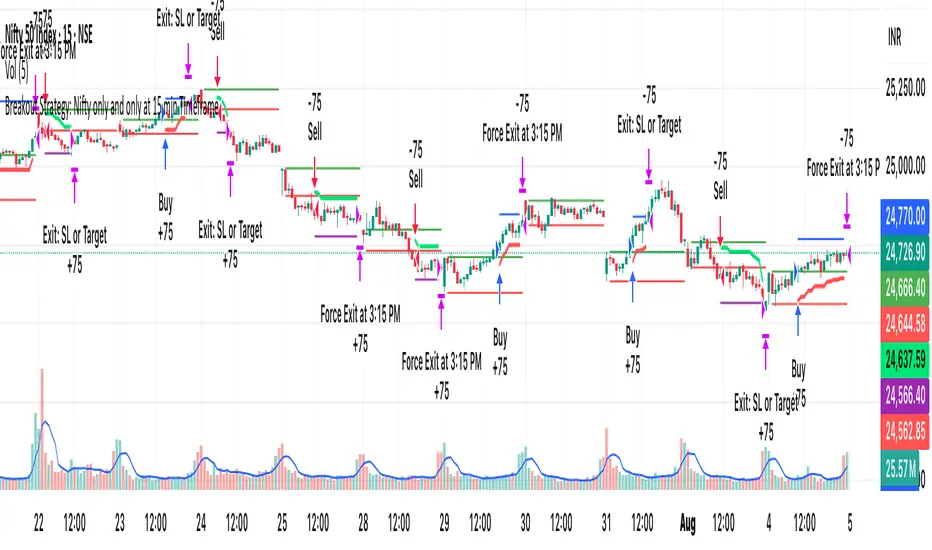

[PS]Breakout Strategy: Nifty/BN only at 15 min TimeframeIt only works on 15 min timeframe for nifty and Bank nifty.

VIX Sentiment Table – ResolutionThis indicator provides verbal representation of the current VIX value and likely market trend for easy to view and interpret

Max Profit Min Loss Options Strategyoption when to buy and sell calls and puts indicator. it uses the rsi macd and volume indicators. it has high profit and low loses

NY/LDN/TOK Stock Exchange Opening HoursThis indicator displays vertical dotted lines marking the exact opening times of the three major global stock exchanges: New York (NYSE), London (LSE), and Tokyo (TSE). Perfect for traders who need to track market opening sessions across different time zones.

Features:

New York Stock Exchange (NYSE): 9:30 AM EST/EDT

London Stock Exchange (LSE): 8:00 AM GMT/BST

Tokyo Stock Exchange (TSE): 9:00 AM JST

Key Highlights:

✓ Automatic daylight saving time adjustments for NY and London

✓ Individual color customization for each market

✓ Toggle on/off functionality for each exchange

✓ Clean vertical dotted lines (1-pixel width) that extend across the entire chart

✓ Interactive legend in bottom-right corner showing active markets

✓ Weekdays only (Monday-Friday) - no weekend lines

✓ Uses official local time zones for accurate timing

Customizable Settings:

Enable/disable individual exchanges

Custom color selection for each market line

Dynamic legend that shows only enabled markets

Time Zone Handling:

The indicator automatically handles daylight saving time transitions using official time zones:

America/New_York (EST/EDT)

Europe/London (GMT/BST)

Asia/Tokyo (JST - no DST)

Perfect for:

Multi-market traders

Session overlap analysis

Global market timing coordination

Institutional trading schedules

Simply add to your chart and customize colors/visibility in the indicator settings. The legend will automatically update to show your active markets in their respective colors.

🟡🔵🟢🔴Beginner's Assistant by carljchapman🟡🔵🟢🔴

Overview

This indicator dynamically marks highs and lows of the premarket (4:00am-9:30amEST) and opening range. It displays Fair Value Gaps, 9 and 21 period Exponential Moving Averages (EMA) and the Volume Weighted Average Price (VWAP). To really help beginners, it marks suggested entry points on the chart with green or red triangles, when a reasonable trend appears.

Features

Automatically draws blue lines for Premarket High and Low values

Dynamically marks the opening Range region

Visual entry signals for long and short opportunities

Primarily used for stocks/funds , but works with forex and crypto

Quick configuration settings to tailor details for your experience level

Mobile friendly mode

Supports alerts

How To Use

Open your chart, and select a 1 or 2 minute timeframe.

Watch for green triangles and red triangles, hinting at entries for long or short positions. Pay particular attention to the price action as it approaches the bounds of the opening range and the premarket levels. I suggest also using a MACD indicator for confirmation of the trend.

For scalping 0dte Options, switch frequently between the 1 ,2 and 5 minute or higher timeframes. Do this so you will not miss an entry opportunity or be unaware of the overall trend.

As a beginner, until you have refined your strategy and develop risk management, take profits as low as 10%. A small profit can quickly become a much larger loss. With 0dte options, time will devour your profits even when the price doesn’t budge.

What makes this indicator so beginner friendly?

Charts with too many lines and colors are are a nightmare for beginners! And empty charts do not tell the whole story. Simple checkboxes in the configuration settings let you turn on and off features to match your comfort level. As you become more familiar you might try turning off the suggested entries to see if you would have selected the same or better ones yourself. Just one example of how you will learn and verify your knowledge. You will quickly spot Opening Range Breakouts and more.

Why are the triangle pointers not simply above or below the bars?

As a beginner, I like to review charts to see how much the price changed, then estimate how much a contract would move based on its delta. A mouthful, I know. But what price does an arrow pointing up below a bar reflect? Would I have entered at the open or close, low or high? This indicator helps by putting the marker close to the price when indicated. It can even display the actual price on the bar. This is helpful for you to make fast calculations without a measuring tool.

I am an experienced trader. Can this help me make winning trades?

Sure. It can also help you make losing ones! Profit is not guaranteed with any indicator or strategy. This indicator is designed to assist you as you learn and while you trade. You won't see the words BUY or SELL. This is not a signal bot! It is merely a tool to assist you. You can learn a lot by spending time observing price movement using this indicator without ever making a single trade.

🟡🔵🟢🔴

Position Size Calculator with Fees# Position Size Calculator with Portfolio Management - Manual

## Overview

The Position Size Calculator with Portfolio Management is an advanced Pine Script indicator designed to help traders calculate optimal position sizes based on their total portfolio value and risk management strategy. This tool automatically calculates your risk amount based on portfolio allocation percentages and determines the exact position size needed while accounting for trading fees.

## Key Features

- **Portfolio-Based Risk Management**: Calculates risk based on total portfolio value

- **Tiered Risk Allocation**: Separates trading allocation from total portfolio

- **Automatic Trade Direction Detection**: Determines long/short based on entry vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Factor Adjustment**: Allows scaling of position size up or down

- **Visual Display**: Shows all calculations in a clear, color-coded table

- **Automatic Risk Calculation**: No need to manually input risk amount

## Input Parameters

### Total Portfolio ($)

- **Purpose**: The total value of your investment portfolio

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If your total portfolio is worth $100,000, enter 100000

### Trading Portfolio Allocation (%)

- **Purpose**: The percentage of your total portfolio allocated to active trading

- **Default**: 20.0%

- **Range**: 0.0% to 100.0%

- **Step**: 0.01

- **Example**: If you allocate 20% of your portfolio to trading, enter 20

### Risk from Trading (%)

- **Purpose**: The percentage of your trading allocation you're willing to risk per trade

- **Default**: 0.1%

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If you risk 0.1% of your trading allocation per trade, enter 0.1

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit if the trade goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How Risk Amount is Calculated

The script automatically calculates your risk amount using this formula:

```

Risk Amount = Total Portfolio × Trading Allocation (%) × Risk % ÷ 10,000

```

### Example Calculation:

- Total Portfolio: $100,000

- Trading Allocation: 20%

- Risk per Trade: 0.1%

**Risk Amount = $100,000 × 20 × 0.1 ÷ 10,000 = $20**

This means you would risk $20 per trade, which is 0.1% of your $20,000 trading allocation.

## Portfolio Structure Example

Let's say you have a $100,000 portfolio:

### Allocation Structure:

- **Total Portfolio**: $100,000

- **Trading Allocation (20%)**: $20,000

- **Long-term Investments (80%)**: $80,000

### Risk Management:

- **Risk per Trade (0.1% of trading)**: $20

- **Maximum trades at risk**: Could theoretically have 1,000 trades before risking entire trading allocation

## How Position Size is Calculated

### Trade Direction Detection

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Formulas

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

## Output Display

The indicator displays a comprehensive table with color-coded sections:

### Portfolio Information (Light Blue Background)

- **Portfolio (USD)**: Your total portfolio value

- **Trading Portfolio Allocation (%)**: Percentage allocated to trading

- **Risk as % of Trading**: Risk percentage per trade

### Trade Setup (Gray Background)

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: Trading fee percentage

- **Risk Factor**: Position size multiplier

### Risk Analysis (Red Background)

- **Risk Amount**: Automatically calculated dollar risk

- **Effective Entry**: Actual entry cost including fees

- **Effective Exit**: Actual exit value including fees

- **Expected Loss**: Calculated loss if stop loss is hit

- **Deviation from Risk %**: Accuracy of risk calculation

### Final Result (Blue Background)

- **Position Size**: Number of shares/units to trade

## Usage Examples

### Example 1: Conservative Long Trade

- **Total Portfolio**: $50,000

- **Trading Allocation**: 15%

- **Risk per Trade**: 0.05%

- **Entry Price**: $25.00

- **Stop Loss**: $24.00

- **Risk Factor**: 1.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $50,000 × 15% × 0.05% ÷ 100 = $3.75

### Example 2: Aggressive Short Trade

- **Total Portfolio**: $200,000

- **Trading Allocation**: 30%

- **Risk per Trade**: 0.2%

- **Entry Price**: $150.00

- **Stop Loss**: $155.00

- **Risk Factor**: 2.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $200,000 × 30% × 0.2% ÷ 100 = $120

**Actual Risk**: $120 × 2.0 = $240 (due to risk factor)

## Color Coding System

- **Green/Red Header**: Trade direction (Long/Short)

- **Light Blue**: Portfolio management parameters

- **Gray**: Trade setup parameters

- **Red**: Risk-related calculations and results

- **Blue**: Final position size result

## Best Practices

### Portfolio Management

1. **Keep trading allocation reasonable** (typically 10-30% of total portfolio)

2. **Use conservative risk percentages** (0.05-0.2% per trade)

3. **Don't risk more than you can afford to lose**

### Risk Management

1. **Start with small risk factors** (1.0 or less) until comfortable

2. **Monitor your total exposure** across all open positions

3. **Adjust risk based on market conditions**

### Trade Execution

1. **Always validate calculations** before placing trades

2. **Account for slippage** in volatile markets

3. **Consider position size relative to liquidity**

## Risk Management Guidelines

### Conservative Approach

- Trading Allocation: 10-20%

- Risk per Trade: 0.05-0.1%

- Risk Factor: 0.5-1.0

### Moderate Approach

- Trading Allocation: 20-30%

- Risk per Trade: 0.1-0.15%

- Risk Factor: 1.0-1.5

### Aggressive Approach

- Trading Allocation: 30-40%

- Risk per Trade: 0.15-0.25%

- Risk Factor: 1.5-2.0

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Verify all portfolio inputs are greater than 0

- Check that entry price differs from stop loss

- Ensure calculated risk amount is positive

2. **Very small position sizes**

- Increase risk percentage or risk factor

- Check if your risk amount is too small for the price difference

3. **Large risk deviation**

- Normal for very small positions

- Consider adjusting entry/stop loss levels

### Validation Checklist

- Total portfolio value is realistic

- Trading allocation percentage makes sense

- Risk percentage is conservative

- Entry and stop loss prices are valid

- Trade direction matches your intention

## Advanced Features

### Risk Factor Usage

- **Scaling up**: Use risk factors > 1.0 for high-confidence trades

- **Scaling down**: Use risk factors < 1.0 for uncertain trades

- **Never exceed**: Risk factors that would risk more than your comfort level

### Multiple Timeframe Analysis

- Use different risk factors for different timeframes

- Consider correlation between positions

- Adjust trading allocation based on market conditions

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and correlation between positions. The automated risk calculation assumes you're comfortable with the mathematical relationship between portfolio allocation and individual trade risk. Past performance doesn't guarantee future results, and all trading involves risk of loss.

MA Crossover Strategy with TP/SL (5 EMA Filter)How the Strategy Works on a 5-Minute Chart:

Data Input (5-Minute Candles):

Every single data point (candle) on your chart will represent 5 minutes of price action (Open, High, Low, Close for that 5-minute period).

All calculations (MAs, EMA, signals) will be based on these 5-minute price data points.

Moving Average Calculations:

Fast MA (10-period SMA): This will be the Simple Moving Average of the closing prices of the last 10 five-minute candles. It reacts relatively quickly to recent price changes.

Slow MA (30-period SMA): This will be the Simple Moving Average of the closing prices of the last 30 five-minute candles. It represents a slightly longer-term trend compared to the Fast MA.

5 EMA (5-period EMA): This is the Exponential Moving Average of the closing prices of the last 5 five-minute candles. Being an EMA, it gives more weight to the most recent 5-minute prices, making it very responsive to immediate price action.

Signal Generation (Entry Conditions):

Long Entry Signal:

The 10-period SMA crosses above the 30-period SMA (indicating a potential bullish shift in the short-to-medium term trend).

AND the current 5-minute candle's closing price is above the 5-period EMA (confirming that the immediate price momentum is also bullish and supporting the crossover).

If both conditions are met at the close of a 5-minute candle, a "Buy" signal is generated.

Short Entry Signal:

The 10-period SMA crosses below the 30-period SMA (indicating a potential bearish shift).

AND the current 5-minute candle's closing price is below the 5-period EMA (confirming immediate bearish momentum).

If both conditions are met at the close of a 5-minute candle, a "Sell" signal is generated.

Trade Execution:

When a signal is triggered, the strategy enters a trade (long or short) at the closing price of that 5-minute candle.

Immediately upon entry, it places two contingent orders:

Take Profit (Target): Set at 2% (by default) away from your entry price. For a long trade, it's 2% above; for a short trade, 2% below.

Stop Loss: Set at 1% (by default) away from your entry price. For a long trade, it's 1% below; for a short trade, 1% above.

The trade will remain open until either the Take Profit or Stop Loss price is hit by subsequent 5-minute candles.

Implications for Trading on a 5-Minute Chart:

Increased Trade Frequency: You will likely see many more signals and trades compared to higher timeframes (like 1-hour or daily charts). This means more potential opportunities but also more transaction costs (commissions, slippage).

Sensitivity to Noise: Lower timeframes are more prone to "market noise" – small, random price fluctuations that don't indicate a true trend. While the 5 EMA filter helps, some false signals might still occur.

Faster Price Action: Price movements can be very rapid on a 5-minute chart. Your take profit or stop loss levels might be hit very quickly, sometimes within the same or next few candles.

Parameter Optimization is Crucial: The default MA lengths (10, 30) and EMA (5) might not be optimal for every asset or market condition on a 5-minute chart. You'll need to backtest extensively and potentially adjust these lengths, as well as the targetPerc and stopPerc, to find what works best for the specific instrument you're trading.

Risk Management: The fixed percentage stop loss is vital on a 5-minute chart due to its volatility. Without it, a few unfavorable moves could lead to significant losses.

Easy Position Size Calculator with Fees# Easy Position Size Calculator with Fees - Manual

## Overview

The Easy Position Size Calculator is a Pine Script indicator designed to help traders calculate the optimal position size for their trades while accounting for trading fees. This tool automatically determines whether you're planning a long or short position and calculates the exact position size needed to risk a specific dollar amount.

## Key Features

- **Automatic Trade Direction Detection**: Determines if you're going long or short based on entry price vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Management**: Calculates position size based on your specified risk amount

- **Risk Factor Adjustment**: Allows you to scale your position size up or down

- **Visual Display**: Shows all calculations in a clear, organized table

## Input Parameters

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit the trade if it goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk ($)

- **Purpose**: The maximum dollar amount you're willing to lose on this trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction (buy/sell)

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How It Works

### Trade Direction Detection

The script automatically determines your trade direction:

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Calculation

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

### Fee Adjustment

The script accounts for fees on both entry and exit:

- **Long trades**: You pay fees when buying (entry) and selling (exit)

- **Short trades**: You pay fees when shorting (entry) and covering (exit)

## Output Display

The indicator displays a table with the following information:

### Trade Information

- **Trade Type**: Shows whether it's a LONG, SHORT, or INVALID trade

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: The fee percentage being used

### Risk Parameters

- **Risk Amount**: The dollar amount you're willing to risk

- **Risk Factor**: The multiplier being applied

### Calculated Values

- **Effective Entry**: The actual cost per share including fees

- **Effective Exit**: The actual exit value per share including fees

- **Expected Loss**: The calculated loss if stop loss is hit

- **Deviation from Risk %**: Shows how close the expected loss is to your target risk

- **Position Size**: The number of shares/units to trade

## Usage Examples

### Example 1: Long Trade

- Entry Price: $100.00

- Stop Loss: $95.00

- Risk Amount: $500.00

- Risk Factor: 1.0

- Fee: 0.01%

**Result**: The script will calculate how many shares to buy so that if the stop loss is hit, you lose approximately $500 (accounting for fees). Position Size: 99.61152

### Example 2: Short Trade

- Entry Price: $50.00

- Stop Loss: $55.00

- Risk Amount: $300.00

- Risk Factor: 1.0

- Fee: 0.01%

**Result**: The script will calculate how many shares to short so that if the stop loss is hit, you lose approximately $300 (accounting for fees). Position Size: 59.87426

## Important Notes

### Validation Requirements

For the script to work properly, all of the following must be true:

- Entry price > 0

- Stop loss > 0

- Risk amount > 0

- Entry price ≠ Stop loss (to determine direction)

### Negative Position Sizes

The script may show negative position sizes, which is normal:

- **Negative values for long trades**: Represents shares to buy

- **Negative values for short trades**: Represents shares to short

### Risk Deviation

The "Deviation from Risk %" shows how closely the calculated position size matches your target risk. Small deviations are normal due to:

- Fee calculations

- Rounding

- Market precision

## Color Coding

The table uses color coding for easy identification:

- **Green**: Long trade information

- **Red**: Short trade information

- **Gray**: Invalid trade (when inputs are incorrect)

- **Blue**: Final position size

- **Red background**: Risk-related calculations

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Check that all inputs are greater than 0

- Ensure entry price is different from stop loss

2. **Trade Type shows INVALID**

- Verify that entry price and stop loss are both positive

- Make sure entry price ≠ stop loss

3. **Large Risk Deviation**

- This is normal for very small position sizes

- Consider adjusting your risk amount or price levels

## Best Practices

1. **Always validate your inputs** before placing actual trades

2. **Double-check the trade direction** shown in the table

3. **Review the expected loss** to ensure it aligns with your risk management

4. **Consider the effective entry/exit prices** which include fees

5. **Use appropriate risk factors** - avoid extreme values that could lead to overexposure

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and other factors before placing actual trades. The script assumes that fees are charged on both entry and exit transactions.

Option Maxpain & WallsThis simple script plots three lines on your chart based on options data: Call Wall, Put Wall and Max Pain. These three numbers must be obtained elsewhere. While Tradingview has delayed options data, to my knowledge Pinescript does not allow looping through this data to calculate the numbers within the script. So the user must obtain or calculate them elsewhere then type them into the input dialog. Labels and alerts are included as user options.