ANN Trend PredictionThis trend indicator utilizes an artificial neural network (ANN) to predict the next market reversal within a certain range of previous candles. The larger the range of previous candles you set, the fewer reversals will be predicted, and trends will tend to last longer.

The ANN is trained on the BTCUSD 4-hour chart, so using it on other assets or timeframes may yield suboptimal results. It takes three input values: the closing price, the Stochastic RSI, and a Choppiness Indicator. Based on these inputs, the ANN categorizes the current candle as part of an uptrend, downtrend, or as undefined.

Compared to an EMA-based trend indicator, this ANN identifies reversals several candles earlier. It achieves this by detecting subtle patterns in the input values that typically appear before a market turnaround. These patterns are somewhat specific to that chosen asset and timeframe.

The results are displayed using rows of triangles that indicate the predicted price direction. The price levels of the triangles correspond to the closing price at the last reversal. The area between the triangle row and the price is colored green if the ANN correctly predicted the move, and red if it did not.

This indicator is designed to showcase the capabilities and potential of ANNs, and is not intended for actual trading use. The ANN can be trained on any other input values, assets and timeframes for several predictions tasks.

You can use the Predicted_Trend_Signal of this Indicator in any backtest indicator. In the Backtester just grap the Predicted_Trend_Signal. downtrend = 1, uptrend = -1, undefined = 0

Feel free to write me a comment.

Prediction

[DarkTrader] Intersection Level & PredictionLinear Regression Function Reference by @RicardoSantos :

The Intersection Level Calculation process identifies critical price levels where significant market reactions are expected. It starts by analyzing historical price action and technical indicators to pinpoint key support and resistance levels.

Price Forecast Min represents the predicted lowest price level that the asset might reach, while Price Forecast Max indicates the anticipated highest price level. These projections are calculated using statistical methods and historical price patterns, allowing traders to anticipate potential support and resistance zones. By providing these forecasts, traders can better manage their risk and set more informed entry and exit points based on projected price movements.

Example Of Prediction (Before & After)

Predicting Future Price Movements :

Once the intersection levels are identified, the indicator uses various predictive models to forecast what price might do next when it approaches these levels. Here’s a breakdown of how it achieves this :

Price Reaction Analysis: The indicator assesses how price has historically reacted to similar intersection levels. For instance, if price has reversed from a certain support level multiple times, the indicator can predict a potential reversal or bounce when price approaches that level again.

Trend Continuation or Reversal: It examines the strength of the current trend by analyzing momentum indicators, volume, and the angle or direction of trendlines. Based on this, it can predict whether price is likely to break through an intersection level, signaling trend continuation, or bounce off it, indicating a potential reversal.

Confluence of Factors: The prediction mechanism becomes more accurate when multiple factors converge at the same intersection level. For example, if a trendline, moving average, and support zone all intersect at the same price point, the indicator predicts a stronger likelihood of significant price movement.

Market Volatility and Momentum: The indicator also considers current market volatility and momentum in its prediction. For example, if price approaches an intersection level with high momentum, it might predict a breakout, whereas low momentum might suggest consolidation or a weaker price reaction.

In this indicator, I utilize Linear Regression to forecast price movements by analyzing historical data trends. Linear Regression involves fitting a straight line to past price data, enabling me to model and project future price levels based on identified trends. This method calculates a trend line that best represents the historical price behavior, providing a foundation for predicting future price points. By extending this trend line, I can estimate where prices might move, incorporating a range to account for potential deviations. This approach helps in identifying both minimum and maximum forecasted prices, offering valuable insights into potential market directions.

Viking Fun PredictОсобая благодарность за оригинальную идею Александру Горчакову

Индикатор предсказывает вырастет или упадет цена на следующей свече

Индикатор отображает красные или зеленые кружки над каждой из свечей

Зеленый кружок прогноз роста

Красный кружок прогноз падения

Индикатор выдает прогноз для шестой свечи на основе пяти свечей

Индикатор берет цены максимумов и минимумов пяти свечей и усредняет их, получая 5 значений. На основе полученных 5 значений строится линейная регрессия

Если линия линейной регрессии возрастает, то индикатор прогнозирует рост (зеленый кружок)

Если линия линейной регрессии возрастает, то индикатор прогнозирует падение (красный кружок)

Компания Викинг предоставляет профессиональный сервис, позволяющий реализовать арбитражные стратегии и маркет-мейкинг, осуществляет обучение трейдеров-арбитражеров.

---------------------------

Special thanks for the original idea to Alexander Gorchakov

The indicator predicts whether the price will rise or fall on the next candle

The indicator displays red or green circles above each of the candles

Green circle growth forecast

Red circle forecast of the fall

The indicator gives a forecast for the sixth candle based on five candles

The indicator takes the prices of the highs and lows of five candles and averages them, getting 5 values. Based on the obtained 5 values, a linear regression is constructed

If the linear regression line increases, the indicator predicts growth (green circle)

If the linear regression line increases, the indicator predicts a fall (red circle)

Viking provides a professional service that allows you to implement arbitrage strategies and market making, and provides training for arbitrage traders.

Moving Average Cross Probability [AlgoAlpha]Moving Average Cross Probability 📈✨

The Moving Average Cross Probability by AlgoAlpha calculates the probability of a cross-over or cross-under between the fast and slow values of a user defined Moving Average type before it happens, allowing users to benefit by front running the market.

✨ Key Features:

📊 Probability Histogram: Displays the Probability of MA cross in the form of a histogram.

🔄 Data Table: Displays forecast information for quick analysis.

🎨 Customizable MAs: Choose from various moving averages and customize their length.

🚀 How to Use:

🛠 Add Indicator: Add the indicator to favorites, and customize the settings to suite your trading style.

📊 Analyze Market: Watch the indicator to look for trend shifts early or for trend continuations.

🔔 Set Alerts: Get notified of bullish/bearish points.

✨ How It Works:

The Moving Average Cross Probability Indicator by AlgoAlpha determines the probability by looking at a probable range of values that the price can take in the next bar and finds out what percentage of those possibilities result in the user defined moving average crossing each other. This is done by first using the HMA to predict what the next price value will be, a standard deviation based range is then calculated. The range is divided by the user defined resolution and is split into multiple levels, each of these levels represent a possible value for price in the next bar. These possible predicted values are used to calculate the possible MA values for both the fast and slow MAs that may occur in the next bar and are then compared to see how many of those possible MA results end up crossing each other.

Stay ahead of the market with the Moving Average Cross Probability Indicator AlgoAlpha! 📈💡

ATR Price Range Prediction V.2### ATR Price Range Prediction V.2

This script calculates the expected high and low prices for the current day based on the Average True Range (ATR) and displays the proportion of days where the daily range (high - low) is greater than or equal to the ATR. Additionally, the script provides an option to adjust the size of the text displayed in the top-right corner of the chart.

#### How It Works

1. **ATR Calculation**: The script calculates the ATR for a specified period (`atrPeriod`). ATR is a measure of volatility that represents the average range between the high and low prices over a specified number of periods.

2. **Expected High and Low Calculation**:

- **Expected High**: Calculated by adding the ATR value to the low price of the current day.

- **Expected Low**: Calculated by subtracting the ATR value from the high price of the current day.

3. **Proportion Calculation**: The script calculates the proportion of days where the daily range (high - low) is greater than or equal to the ATR value. This proportion is updated in real-time as new data comes in.

4. **Table Display**: Instead of displaying labels on each candle, the script shows the expected high, expected low, and the calculated proportion in a table located at the top-right corner of the chart. The size of the text in this table can be adjusted using the `Table Size` input.

5. **Color Coding**: The script changes the color of the bars to yellow if the daily range is greater than or equal to the ATR value, making it easy to identify these bars visually.

#### How to Use

- **ATR Period (`atrPeriod`)**: Adjust the period for the ATR calculation using the input parameter. The default value is 14.

- **Table Size (`tableSizeOption`)**: Choose the size of the text displayed in the table. Options include `tiny`, `small`, `normal`, `large`, and `huge`.

- **Expected High and Low**: Use the green and red lines to identify potential target prices or stop-loss levels for your trades. The green line represents the expected high, and the red line represents the expected low.

- **Proportion**: The table in the top-right corner of the chart shows the proportion of days where the daily range is greater than or equal to the ATR value. This can provide insight into the volatility of the asset.

- **Color Coding**: Yellow bars indicate days where the daily range is greater than or equal to the ATR value.

---

### ภาษาไทย

### ATR คาดการณ์ราคาสูงสุดและต่ำสุด พร้อมสัดส่วน

สคริปต์นี้คำนวณราคาสูงสุดและต่ำสุดที่คาดการณ์สำหรับวันปัจจุบันโดยอิงจากค่าเฉลี่ยช่วงที่แท้จริง (ATR) และแสดงสัดส่วนของวันที่ช่วงราคาต่อวัน (สูง - ต่ำ) มากกว่าหรือเท่ากับค่า ATR นอกจากนี้ยังมีตัวเลือกในการปรับขนาดข้อความที่แสดงในกล่องข้อความมุมขวาบนของกราฟ

#### วิธีการทำงาน

1. **การคำนวณ ATR**: สคริปต์คำนวณค่า ATR สำหรับช่วงเวลาที่กำหนด (`atrPeriod`) ATR เป็นมาตรวัดความผันผวนที่แสดงช่วงเฉลี่ยระหว่างราคาสูงสุดและต่ำสุดในช่วงเวลาที่กำหนด

2. **การคำนวณราคาสูงสุดและต่ำสุดที่คาดการณ์**:

- **ราคาสูงสุดที่คาดการณ์**: คำนวณโดยการบวกค่า ATR กับราคาต่ำสุดของวันปัจจุบัน

- **ราคาต่ำสุดที่คาดการณ์**: คำนวณโดยการลบค่า ATR จากราคาสูงสุดของวันปัจจุบัน

3. **การคำนวณสัดส่วน**: สคริปต์คำนวณสัดส่วนของวันที่ช่วงราคาต่อวัน (สูง - ต่ำ) มากกว่าหรือเท่ากับค่า ATR สัดส่วนนี้จะอัปเดตแบบเรียลไทม์เมื่อมีข้อมูลใหม่เข้ามา

4. **การแสดงผลในตาราง**: แทนที่จะแสดงป้ายกำกับบนแท่งเทียนแต่ละแท่ง สคริปต์จะแสดงราคาสูงสุดที่คาดการณ์ ราคาต่ำสุดที่คาดการณ์ และสัดส่วนที่คำนวณในตารางที่มุมขวาบนของกราฟ โดยสามารถปรับขนาดข้อความในตารางได้

5. **การใช้สี**: สคริปต์จะเปลี่ยนสีของแท่งเทียนเป็นสีเหลืองหากช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR ทำให้สามารถระบุแท่งเทียนเหล่านี้ได้ง่ายขึ้น

#### วิธีการใช้งาน

- **ATR Period (`atrPeriod`)**: ปรับช่วงเวลาสำหรับการคำนวณ ATR โดยใช้พารามิเตอร์การป้อนค่า ค่าเริ่มต้นคือ 14

- **Table Size (`tableSizeOption`)**: เลือกขนาดข้อความที่แสดงในตาราง ตัวเลือกได้แก่ `tiny`, `small`, `normal`, `large`, และ `huge`

- **ราคาสูงสุดและต่ำสุดที่คาดการณ์**: ใช้เส้นสีเขียวและสีแดงเพื่อระบุราคาที่เป็นเป้าหมายหรือระดับการหยุดขาดทุนสำหรับการซื้อขายของคุณ เส้นสีเขียวแสดงถึงราคาสูงสุดที่คาดการณ์และเส้นสีแดงแสดงถึงราคาต่ำสุดที่คาดการณ์

- **สัดส่วน**: ตารางที่มุมขวาบนของกราฟแสดงสัดส่วนของวันที่ช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR ซึ่งสามารถให้ข้อมูลเชิงลึกเกี่ยวกับความผันผวนของสินทรัพย์

- **การใช้สี**: แท่งเทียนสีเหลืองบ่งบอกถึงวันที่ช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR

_____

M Farm Scalper v4"M Farm Scalper v2" Trading Indicator on TradingView

Overview

This script uses a combination of indicators to help attempt the best view of when to exit and enter markets. The author has seen that usage of multiple indicators combined provided value and create profit.

1. Improved Signal Reliability

Combining swing highs and lows with Swing Failure Patterns (SFP) increases the reliability of the signals. Each indicator contributes different insights into market behavior:

Swing Highs and Lows: These help identify key support and resistance levels.

Swing Failure Patterns: These provide early warning signs of potential trend reversals when price fails to maintain new highs or lows.

2. Comprehensive Market Analysis

Using multiple indicators allows for a more comprehensive analysis of market conditions:

Trend Analysis: Swing highs and lows can indicate the overall trend direction.

Reversal Signals: SFPs highlight potential reversal points where the current trend might be weakening.

3. Enhanced Signal Strength

The script not only detects basic SFPs but also evaluates their strength by considering the number of failures within a specified range:

Strength of SFPs: By quantifying the strength of SFPs, the script can distinguish between weak and strong reversal signals. This helps traders prioritize stronger signals, reducing false positives.

4. Visual and Alert-based Trading

The combined use of these indicators improves both visual analysis and automated alert systems:

Visual Representation: Plotting different characters for swing points and SFPs makes it easier for traders to quickly interpret the chart.

Alerts: Automated alerts for specific conditions (like swing high/low failures) enable traders to respond promptly to significant market movements without constantly monitoring the charts.

5. Flexibility and Customization

The script includes parameters that allow traders to customize the behavior of the indicators based on their trading preferences:

Customization of Lookback Period (swingHistory): Traders can adjust this to fine-tune the sensitivity of swing point detection.

Selective Plotting (plotSwings, plotFirstSFPOnly, plotStrongerSFPs): These options provide flexibility in how much information is displayed on the chart, preventing clutter and focusing on relevant signals.

6. Minimized Noise and False Signals

By using a combination of indicators, the strategy aims to filter out market noise and reduce the likelihood of false signals:

Confluence of Signals: When multiple indicators align to provide a signal, it generally indicates a higher probability setup, thus reducing the chances of acting on false or less significant market moves.

7. Contextual Market Understanding

Combining indicators offers a more contextual understanding of market dynamics:

Market Context: Identifying both support/resistance levels (via swing points) and potential trend reversals (via SFPs) provides a fuller picture of market conditions, allowing traders to make more informed decisions.

Conclusion

Combining multiple indicators in the "M Farm Scalper v2" script is a strategic choice designed to enhance the robustness, reliability, and actionable quality of the trading signals. This approach leverages the strengths of each indicator to provide a well-rounded, comprehensive trading tool that aids traders in identifying high-probability trade setups and minimizing the risk of false signals.

ChatGPT can make mistakes. Check important info.

Introducing "M Farm Scalper v2" – an advanced proprietary trading indicator designed exclusively for the TradingView platform. This tool excels in identifying key swing points and Swing Failure Patterns (SFPs), offering traders unique visual and auditory cues to enhance decision-making. It's particularly tailored for the 5-minute timeframe but adaptable to suit a variety of trading styles.

Unique Features

Advanced Swing Point Detection: Leverages a sophisticated algorithm to detect swing highs and lows, integrating predictive analytics to forecast potential market reversals.

Dynamic Swing Failure Pattern Analysis: Employs a real-time analysis combining price action and volume data to pinpoint bullish and bearish reversal opportunities with high precision.

Innovative Visual and Auditory Cues: Features unique, easy-to-understand icons such as animals and fruits to represent market signals, simplifying complex market data into actionable insights.

Functionality

"M Farm Scalper v2" is crafted to deliver:

Configurable Parameters: Users can adjust settings including Swing History, visibility of swing points, and sensitivity for detecting stronger SFPs, making it highly customizable to fit individual trading strategies.

Clear, Actionable Outputs: Designed to offer straightforward visual signals directly on the trading chart, facilitating quick and effective decision-making.

Compliance and Originality

Original Integration of Features: This script combines several analytical techniques into a cohesive unit that surpasses the capabilities of existing open-source scripts in both originality and functionality.

Justification for Closed-Source: The proprietary nature of the algorithms and the unique method of data presentation are maintained as closed-source to protect the integrity and effectiveness of the tool, providing users with a reliable competitive advantage.

Application Instructions

To apply "M Farm Scalper v2," add it from the TradingView "Indicators" menu by searching for our script. Adjust the customizable settings as per your trading requirements and observe how the indicator’s outputs make market dynamics easy to interpret and act upon.

Chart Presentation

The accompanying chart is presented cleanly, focusing solely on the outputs of "M Farm Scalper v2." Each visual cue is annotated to demonstrate its relevance, ensuring that traders can easily understand and utilize the information provided without distraction.

Conclusion

"M Farm Scalper v2" is not just an indicator but an essential trading tool for those seeking precision and efficiency in their trading operations. Its advanced features and user-friendly design make it a valuable addition to any trader’s arsenal, especially for those involved in scalping and short-term trading.

Protected script

This script is published closed-source but you may use it freely. You can favorite it to use it on a chart. You cannot view or modify its source code.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Correlated Movement Indicator V2Hello!

This script was briefly known as as Bing Chilling. I converted this to Pine Script V5 to ensure compliance with publishing requirements.

This script tracks RSI and inserts an indicator when correlated movement is detected. Proximity of current tick to indicator origin tick determines freshness of the indicator.

DO NOT sit on the indicator for a long time. This is not a magic solution. It is very accurate but, not always precise. Ensure that you use other factors to determine the relevance of the indicator on current tick. This script can technically be used on any security/commodity/currency. Your Mileage May Vary! Proceed with caution as always.

General Workflow:

Look at proximity to where the flag is placed, general volatility, and other indicators and you can potentially determine the direction/strength. Not always the duration. The indicator could be for 30s, 1hr, 1 day, or whatever the market feels like. It depends on precision/quantity of pricing data. ex. 30min tick rate pricing vs. 1 day tick rate pricing will change the scope.

So if the time scope shows all sell from 1 week -> 3 months except for a couple recent buy indicators on the day, then it may be a bad call long term but, might be good for a short term play. Very volatile. Careful.

If it was all green with long term indicators such as 1 month -> 1 year, then it looks more like a buy and forget type strategy.

If it's all green with a recent red then you can try and figure out what the relative the bottom is so you can buy for long term at a slightly more favorable price.

Flip all that for shorting. I highly recommend AGAINST shorting since the stakes are very different and usually involves taking out what is essentially a loan to bet against the market.

This script pairs nicely with the top pick indicator when you search "Heiken Ashi". I use that to determine peaks and pits to better guess a good time to open a position.

This should be used alongside other indicators. Good for short term day trading and long term hold and forget. (Don't actually forget. Set some alerts periodically.)

Please use caution. Please do not take what I've said here as fact and diamond pepe hands bet all on green to the moon. This, like all the other strategies and indicators on this site, are used as tools to inform you about potential and to categorize/depict data in a more human recognizable way. If you have access to a paper account try there first.

Happy trading!

- Zetsu

Monte Carlo Shuffled Projection [LuxAlgo]The Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made within a user-selected window.

The tool shows potential paths price might take in the future, as well as highlighting potential support/resistance levels.

Note that simulations and their resulting elements are subject to slight changes over time.

🔶 USAGE

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing a large number of simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window)

This constraint will cause the simulations to always display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range as seen below:

🔶 DETAILS

The Monte Carlo Shuffled Projection tool creates simulations based on the most recent prices within a user-set window. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation, for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar with a maximum of 1000 simulations.

To get a glimpse behind the scenes each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options as seen below.

Because the script holds the full simulation data, the script can also do calculations on this data, such as calculating standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Color and Toggle Options are Provided throughout.

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however only the last 99 simulations will be visualized.

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

Entry FraggerEntry Fragger is a simple buy signal indicator.

It is most suitable for cryptocurrency, especially for altcoins on the 5 minute to daily timeframe and is based on simple volume calculations, in combination with EMA's.

Main Signal Logic explained:

A buy signal is generated by counting candles with an above average sell volume of 130% to 170%, taking into account the candles position below and above the 50 and 200 EMA.

If criteria meet, the first green candle above the 50 EMA's suggests upcoming higher prices.

The indicator has 2 input variables.

"Signal Confirmations (0 - 7):" Changes signal accuracy by a defining an ammount of high sell volume candles necessary below the 50 EMA.

"Volume Calculation Base (9 - 200):" Sets the exponential volume multiplier, this affects candle coloring and the volume calculation inside the candle.

"Style Settings": Turn ON/OFF Signals, Cloud, Bar Coloring, EMA's, etc...

There are no generally suitable default numbers for those 2 inputs, those have to be tested out, depending on cryptocurrency and timeframe.

The calculation is very basic, the underlying idea being, market maker initiating range breakouts through rapid increase of volume above or below the EMA's .

Example settings:

SOLUSDT: Signal Confirmations: 2, Volume Calculation Base 13.

SOLUSDT: Signal Confirmations: 0, Volume Calculation Base 20.

As you can see it affects signals quite a lot, but staying accurate.

Finetune the inputs to your preference.

Risk to Reward, Stoploss, Take Profit, position sizing, etc... is up to the user.

Recommended entry is to wait for following candle closes, entering half of the candle size and setting Stoploss outside the structure, like this:

Or right below the candles open, for safety.

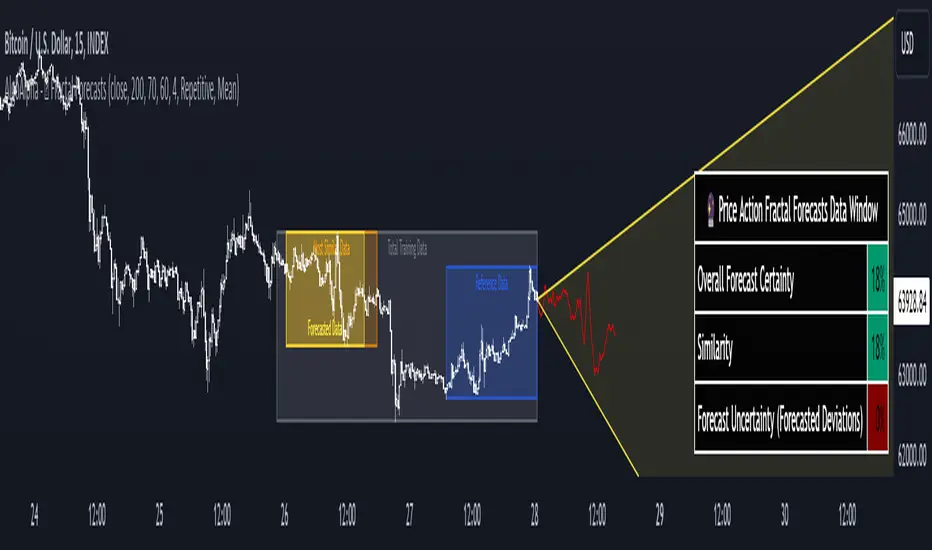

Price Action Fractal Forecasts [AlgoAlpha]🔮 Price Action Fractal Forecasts - Unleash the Power of Historical Patterns! 🌌✨

Dive into the future with AlgoAlpha's Price Action Fractal Forecasts ! This innovative indicator utilizes the mesmerizing complexity of fractals to predict future price movements, offering traders a unique edge in the market. By analyzing historical price action and identifying repeating patterns, this tool forecasts future price trends, providing visually engaging and actionable insights.

Key Features:

🔄 Flexible Data Series Selection: Choose your preferred data series for precise analysis.

🕰 Flexible Training and Reference Data Windows: Customize the length of training data and reference periods to match your trading style.

📈 Custom Forecast Length: Adjust the forecast horizon to suit your strategic objectives.

🌈 Customizable Visual Elements: Tailor the colors of forecast deviation cones, data reference areas, and more for optimal chart readability.

🔄 Anticipatory and Repetitive Forecast Modes: Select between anticipating future trends or identifying repetitive patterns for forecasts.

🔎 Enhanced Similarity Search: Leverages correlation metrics to find the most similar historical data segments.

📊 Forecast Deviation Cone: Visualize potential price range deviations with adjustable multipliers.

🚀 Quick Guide to Maximizing Your Trading with Price Action Fractal Forecasts:

🛠 Add the Indicator: Search for "Price Action Fractal Forecasts" in TradingView's Indicators & Strategies. Customize settings according to your trading strategy.

📊 Strategic Forecasting: Monitor the forecast deviation cone and forecast directional changes for insights into potential future price movements.

🔔 Alerts for Swift Action: Set up notifications based on forecast changes to stay ahead of market movements without constant monitoring.

Behind the Magic: How It Works

The core of the Price Action Fractal Forecasts lies in its ability to compare current market behavior with historical data to unearth similar patterns. It first establishes a training data window to analyze historical prices. Within this window, it then defines a reference length to identify the most recent price action that will serve as the basis for comparison. The indicator searches through the historical data within the training window to find segments that closely match the recent price action in the reference period.

Depending on whether you choose the anticipatory or repetitive forecast mode, the indicator either looks ahead to predict future prices based on past outcomes following similar patterns or focuses on the repeating patterns within the reference period itself for forecasts. The forecast's direction can be configured to reflect the mean average of forecasted prices or the end-point relative to the start-point of the forecast, offering flexibility in how forecasts are interpreted.

To enhance the comprehensiveness and visualization, the indicator features a forecast deviation cone. This cone represents the potential range of price movements, providing a visual cue for volatility and uncertainty in the forecasted prices. The intensity of this cone can be adjusted to suit individual preferences, offering a visual guide to the level of risk and uncertainty associated with the forecasted price path.

Embrace the fractal magic of markets with AlgoAlpha's Price Action Fractal Forecasts and transform your trading today! 🌟🚀

Forecast: PastFluxDelta PredictionThe theory is that time periods and the conditions during these periods repeat themselves. Especially if it is the same day of the week in the past, there is a high probability that price fluctuations will roughly repeat themselves.

Eternal return (or eternal recurrence) is a philosophical concept which states that time repeats itself in an infinite loop, and that exactly the same events will continue to occur in exactly the same way, over and over again, for eternity.

History does repeat itself.

The stock market is a manifest example.

Chief market strategist at Miller Tabak + Co. Matt Maley pointed out the strong resemblance between the stock market recently and that in the past.

Various scientific studies and articles show that there could be something to this theory

Most of the investors are ignoring the parallels between stocks today and "heady" years 1929, 1999 and 2007…

Post Labor Day sees investors returning to the S&P 500 near all-time highs and some dark economic shadows lurking …

So how should we regard these inescapable results?

Nietzsche said we should embrace them, accept them, and love them. Once they stop, expect them to start again.

But remember that the future is fundamentally uncertain and that past results are by no means a guarantee of future performance.

Based on this, this indicator uses historical trading data from a year, a week or a day ago and compares price fluctuations in the past with current conditions.

"Bars to predict" can be used to indicate how far into the future the indicator is looking.

"Amount of bars to show" determines how many bars are generally displayed. A high value allows you to see how accurate the method was in the past.

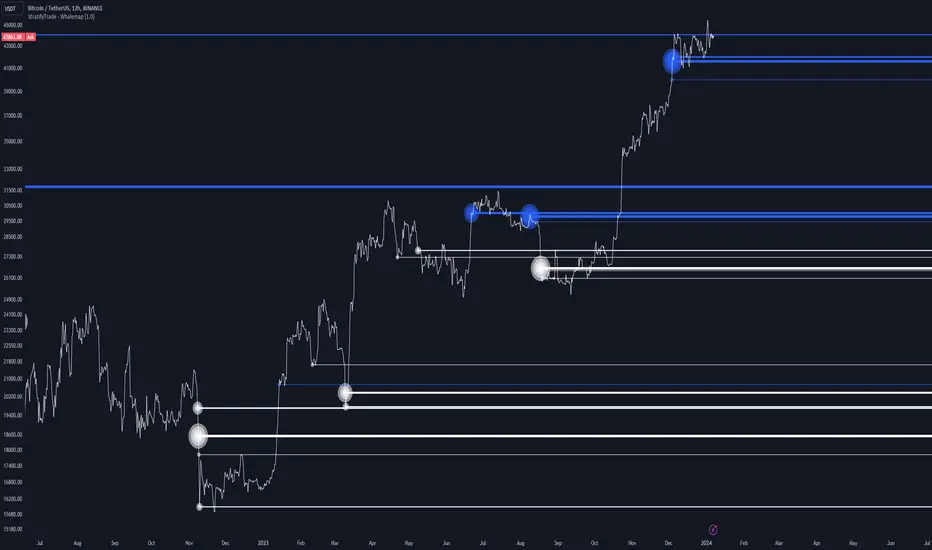

Whalemap [BigBeluga]The Whalemap indicator aims to spot big buying and selling activity represented as big orders for a possible bottom or top formation on the chart.

🔶 CALCULATION

The indicator uses volume to spot big volume activity represented as big orders in the market.

for i = 0 to len - 1

blV.vol += (close > close ? volume : 0)

brV.vol += (close < close ? volume : 0)

When volume exceeds its own threshold, it is a sign that volume is exceeding its normal value and is considered as a "Whale order" or "Whale activity," which is then plotted on the chart as circles.

🔶 DETAILS

The indicator plots Bubbles on the chart with different sizes indicating the buying or selling activity. The bigger the circle, the more impact it will have on the market.

On each circle is also plotted a line, and its own weight is also determined by the strength of its own circle; the bigger the circle, the bigger the line.

Old buying/selling activity can also be used for future support and resistance to spot interesting areas.

The more price enters old buying/selling activity and starts producing orders of the same direction, it might be an interesting point to take a closer look.

🔶 EXAMPLES

The chart above is showing us price reacting to big orders, finding good bottoms in price and good tops in confluence with old activity.

🔶 SETTINGS

Users will have the options to:

Filter options to adjust buying and selling sensitivity.

Display/Hide Lines

Display/Hide Bubbles

Choose which orders to display (from smallest to biggest)

BTC Halving [YinYangAlgorithms]This Indicator not only estimates what it thinks may be the PRICE for the Start, High and Low of the Halving, but likewise estimates WHEN the Start, High and Low of Halving may be. It then creates Trend Lines based on these predictions so that you may get an evaluation towards if the Price is currently Overbought or Oversold. These Trend Lines may be very useful for seeing the Slope in which the Price may move if it is to reach the estimated Price by the estimated Date. By evaluating the Prices location based on these Trend Lines we may determine if the Price is currently Overbought or Oversold.

These Trend Lines likewise may help identify locations of Support and Resistance. If the Price is much higher than its current Trend Line it is Overbought. There is a chance it will Consolidate back to the Trend Line or it may even correct with a dump all the way back to it; the opposite is true if it is much lower than its current Trend Line.

Trend Lines and Estimates are not all that is featured within this Indicator however. There are also Price Zones which may help identify if the price is currently:

Very Overbought (Red)

Slightly Overbought (Orange)

Neutral (Yellow)

Slightly Oversold (Teal)

Very Oversold (Green)

These zones may help give you an idea of how the price is currently fairing and its potential for movement. Likewise, it may help define where Support and Resistance may be found.

The trend line estimates are done with an algorithm created to evaluate the difference between price and % change that has occurred between the Start, High and Low of all the halvings over how many days between each data type. This may allow us to make an educated estimate towards what Price and Date the Start, High and Low will occur at.

Our Zones are created by evaluating the current Market Cap and circulating supply vs Max Supply of BTC. This may help give us an evaluation of what Price may be considered to be Overbought and Oversold; and likewise may help with estimations of where there may be Support and Resistance based on these Zones.

Tutorial:

In the example above we’re displaying the Halving Start Trend Line, our Information Tables and our Estimated Halving Vertical Marker. This Trend Line may help to display not only the trajectory and slope the Price needs to take to reach the Estimated Halving Price by the Estimated Halving Date; but it may also help to show if the price is Overvalued or Undervalued based on its position above or below this Trend Line.

Based on the Trajectory of the Estimated High Upward Trend Line (Green Line) in the photo above and from the ‘High Date’ estimated in the Information tables; we may attempt to estimate the location the ATH of this Bull Market will create and the price slope it may follow in doing so. This Trajectory may be very useful for understanding the price action that may occur for it to reach the High estimated Price by the High estimated Date.

We currently allow for two different types of zones within our Settings, one called ‘Fast’ displayed in the example above; and the other called ‘Slow’ displayed in the example below.

Our Fast Zone aims to move the Zone Levels Faster in an attempt to move with volatility and parabolic movement. This may help to keep the Very Overbought (Red) and Very OverSold (Green) Levels more accurate by attempting to keep the price within them. By doing so, we may aim to keep all of the Slightly Overbought, Slightly Oversold and Neutral Levels more accurate as well.

The Levels within these zones are defined by the Bright (less transparent) Lines. Whereas the Darker (more transparent) lines represent the Basis Lines between two different levels. These Basis lines may likewise act as a Support and Resistance Location too, but generally hold less weight than the actual Levels themselves.

What you may see is that during the Bull Market, the price is within the very Overbought Zones and even touches again the Very Overbought Level a few times. Likewise, during the Bear Market, the price is within the very Oversold Zones and even slightly drops below the Very Oversold Level. This may be expected and likewise may help to give estimates at potential for growth and decay within the Price based on which condition the Market is within.

Slow Zones move a little slower than Fast Zones, however they may still be accurate. Likewise, it is up to you to decide which Zone works better for your specific Trading Style; however, by default, the Zone type is set to Fast.

If you refer to both the Fast and Slow examples above, you may notice in the Fast the Price is only slightly above the ‘Slightly Oversold’ (Teal) line. Also, In the Fast, the Price where the ‘Very Overbought’ Level is 100k. This is one of the many reasons we’ve opted for ‘Fast’ as the default, and it is because it allows more room for movement; and in our opinion, potentially accuracy as well.

If you refer to the Slow example, you’ll see that the price is currently facing the Neutral Level as a Resistance location. However, if you refer to the price residing at the Slows ‘Very Overbought’ Level, it is only 81.5k, compared to the 100k of Fast.

The BTC Halving is a major event that takes place roughly every 4 years. It historically has a major impact on the market, and some may even say it signifies the Start, or close to start of the Bull Market. Therefore, since historically there may be cycles that BTC and potentially crypto itself follows, we’ve developed this Indicator in hopes that it may solve one of the biggest questions traders face. What Date will the Start, High and Low of the Halving occur and also at what Price.

Hopefully this Tutorial has given you some guidance as to how this Indicator may be used to help identify some of these key levels; including the slope at which the price may have to move if it is to reach its projection Price by its projected Date.

Settings:

1. Show Prediction Trend Lines:

- Options:

All

Start + High

Start + Low

High + Low

Start

High

Low

None

- Description:

Prediction Trend Lines may be an important way to see the Slope the Price needs to take to reach the Predicted Price by the Predicted Date. This may be useful for identifying if the Price is currently Overbought or Oversold.

2. Zone Type:

- Options:

Fast

Slow

- Description:

Zone types change the way the Zones expand.

3. Show Zones:

- Options:

All

Zones

Basis

None

- Description:

Zones are a way of seeing Overbought and Oversold Price locations based on Market Cap and Circulating Supply vs Max Supply.

4. Vertical Markers:

- Options:

All

Line

Label

None

- Description:

Vertical Markers display where the Halving has occurred with a Vertical Line and Label.

5. Show Tables:

Tables may be useful for seeing the Price and Date for when the Start, High and Low of the Halving may occur.

6. Fill Zones:

Filling in Zones may help to identify which Zone the Price is currently in.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Machine Learning: Gaussian Process Regression [LuxAlgo]We provide an implementation of the Gaussian Process Regression (GPR), a popular machine-learning method capable of estimating underlying trends in prices as well as forecasting them.

While this implementation is adapted to real-time usage, do remember that forecasting trends in the market is challenging, do not use this tool as a standalone for your trading decisions.

🔶 USAGE

The main goal of our implementation of GPR is to forecast trends. The method is applied to a subset of the most recent prices, with the Training Window determining the size of this subset.

Two user settings controlling the trend estimate are available, Smooth and Sigma . Smooth determines the smoothness of our estimate, with higher values returning smoother results suitable for longer-term trend estimates.

Sigma controls the amplitude of the forecast, with values closer to 0 returning results with a higher amplitude. Do note that due to the calculation of the method, lower values of sigma can return errors with higher values of the training window.

🔹 Updating Mechanisms

The script includes three methods to update a forecast. By default a forecast will not update for new bars (Lock Forecast).

The forecast can be re-estimated once the price reaches the end of the forecasting window when using the "Update Once Reached" method.

Finally "Continuously Update" will update the whole forecast on any new bar.

🔹 Estimating Trends

Gaussian Process Regression can be used to estimate past underlying local trends in the price, allowing for a noise-free interpretation of trends.

This can be useful for performing descriptive analysis, such as highlighting patterns more easily.

🔶 SETTINGS

Training Window: Number of most recent price observations used to fit the model

Forecasting Length: Forecasting horizon, determines how many bars in the future are forecasted.

Smooth: Controls the degree of smoothness of the model fit.

Sigma: Noise variance. Controls the amplitude of the forecast, lower values will make it more sensitive to outliers.

Update: Determines when the forecast is updated, by default the forecast is not updated for new bars.

Machine Learning: Support and Resistance [YinYangAlgorithms]Overview:

Support and Resistance is normally based upon Pivot Points and Highest Highs and Lowest Lows. Many times coders even incorporate Volume, RSI and other factors into the equation. However there may be a downside to doing a pure technical approach based on historical levels. We live in a time where Machine Learning is becoming more and more used; thus we have decided to create a Machine Learning Support and Resistance Projection based Indicator. Rather than using traditional Support and Resistance calculations using historical data, we have taken a rather different approach. This Indicator instead attempts to Predict and Project where Support and Resistance locations will be based on a Machine Learning Model using a form of KNN (k-Nearest Neighbors).

Since this indicator creates a Projection of where it deems Support and Resistance will be, it has the ability to move its Support and Resistance before the price even gets to it if it believes it will surpass its projections. This may create a more accurate placement of Support and Resistance as they’re not based on historical levels.

This Indicator does not Repaint.

How it works:

This Indicator makes its projections based on the source you provide (by default close) of the previous bar and submits the source, RSI and EMA to our Projection Function to get its projection of the current bar.

The Projection function essentially calculates potential movement after finding the differences between the source the MA from the current bar, previous bar and average over the span of Machine Learning Length.

Potential movement is defined as:

Average Difference + Average(Machine Learning Average, Average Last Distance)

Average Difference: (Absolute value of Current Source - Current MA) - (Absolute value of Machine Learning Average - Machine Learning MA)

Average Last Distance: Average(Current Source - Current MA, Previous Source - Previous MA)

It then predicts the next bars directional movement (bullish or bearish bar) using several factors:

Previous Source > Previous MA

Current Source - Current MA > Average Source - Average MA

Current RSI > Previous RSI

Current RSI > 30 and Previous RSI <= 30

Current RSI < 70 and Previous RSI >= 70

This helps us to predict the direction the next bar may move.

We then calculate a multiplier that we apply to our Potential Movement value to get our final result which is our Current Bars Close Projection.

Our multiplier is calculated using:

(Current RSI > 30 and Previous RSI <= 30) OR (Current RSI < 70 and Previous RSI >= 70)

Current Source - Current MA > Previous Source - Previous MA

We then create an array and fill it with the previous X projections (Machine Learning Length) and send it to another function. This function, if told to, will sort the data accordingly and then output the KNN average of the length given.

We calculate and plot various KNN lengths to create different Zones:

Strong Support: Length of 2 but sort the data Ascending (low to high)

Strong Resistance: Length of 2 but sort the data Descending (high to low)

Support: Length of Machine Length Length / 10 or Min of 2 sorted by Ascending

Resistance: Length of Machine Length Length / 10 or Min of 2 sorted by Descending

There are also 4 other plots you may be wondering what they are, there is your AVG, VWMA, Long Term Memory and Current Projection.

By default your Current Projection is disabled in settings but you can enable it if you are curious to see how the projections for each close are calculated. It is, however, not a crucial point of interest (white line).

The average is simply the average value of the Machine Learning Data (purple line).

The VWMA is a VWMA calculation applied to our Data over a length specified in settings (by default 1)(blue line). The VWMA is crucial when combined with the Avg as they can cross over and under each other. These crosses represent potential Bullish and Bearish zones.

Lastly, but certainly not least, we have the Long Term Memory (maroon line). The Long Term Memory can be displayed either as an ‘Average’, ‘Hard Line’ or ‘None’. The Long Term Average is only updated every Machine Learning Length Bar Index’s and is populated with the average of the Machine Learning Data. For Instance, if Machine Learning Length is set to 100, the Long Term Memory is only updated every 100 bars, and since its length is the same as the Machine Learning Length, that means its data is composed of 10,000 bars worth of data. The Long Term Memory may be very beneficial for determining where Support and Resistance lie over the Long Term within a Machine Learning Algorithm. When set to ‘Average’ it plots the connection lines diagonally, and although they may be more visually appealing, they’re less useful when it comes to actually seeing support and resistance as generally speaking, support and resistance lie on the horizontal. When set to ‘Hard Line’ the Long Term Memory is connected with hard lines and holds the price value until the next time it is updated. This makes it much more useful for potentially identifying Support and Resistance.

Tutorial:

Here is an overview of what the Indicator looks like, now let's start to dissect it.

In the example above we can see how all of the lines between the Major Support and Resistance zones may act as BOTH Support and Resistance depending on which side the price is currently on. In the circle on the left, we can see how it can fluctuate between the two. If you look at the circle on the right, we can see how the Average line acts as a strong support before it fails to maintain it. Generally speaking, most Support and Resistance locations may potentially fail to hold after 3 tests, as the Average did in this example.

As you can see, the Support and Resistance doesn’t wait to be tested before adjusting, which is why there are 2 lines which create their zones. The inner line is the Support/Resistance and the outer line is the Strong Support/Resistance. The Yellow Circle shows the inner line was able to calculate the moving resistance correctly and then adjusted accordingly as it was projecting the price to keep increasing. However, if you look at the White Circle, you can see that since there was first a crash, and then parabolic movement, that the inner zone could not move and predict the resistance as well as the outer zone could.

We consider the price to be ‘Overvalued’ when it is above the VWMA (blue line) and ‘Undervalued’ when it is below the VWMA. It is considered ‘fair’ price when it is within the VWMA to Average zone (between the blue and purple lines). If you look at the example above, you’ll notice where the two yellow circles are, it is not only considered ‘Overvalued’, but it then proceeds to ride the inner resistance line upwards. This is common when the market is overly bullish and vice versa when it is bearish. Please keep in mind, although it is common, it doesn’t mean a correction can’t happen.

In this example above we look at the last bull run that may have started due to the halving. This bull run was very bullish as you can see in the example above. The price was constantly sitting within the Resistance Zone and the VWMA that was very close to it was constantly acting as a Support. Naturally, due to the Algorithm used in this Indicator, as the momentum starts to slow down, the VWMA (blue line) will start to space out more and more from the Resistance Zone. This doesn’t mean the momentum is gone, it just means it may be slowing down.

Unfortunately we have to study the Bear Market with a different perspective than the Bull Market. However, there are still some similarities within the two. If you refer to the example above and the previous example, you can clearly see that the Bull Market loves to stay with the Resistance Zone and use the VWMA as a Support. However, the Bear Market does not. This is a normal occurrence, however we can see from the example above you may see a correction / horizontal movement when the Outer Support Line is touched. If you look at all 3 yellow circles, the Outer Support Line was touched, then either a small correction or horizontal consolidation occurred.

We will conclude our Tutorial here, hopefully you’ll be able to benefit from a moving Support and Resistance calculated with Machine Learning that projects its locations, rather than using traditional calculations.

Settings:

Source: This source is the base for all our calculations

Machine Learning Length: How much projection data are we storing and using to make calculations.

Smoothing Length: We need to smooth calculations such as RSI, EMA and VWMA. What length are we smoothing it with?

VWMA ML Projection Length: How far into our Machine Learning data should we average for our VWMA. Please note the 'Smoothing Length' is still applied here after getting the Projection Average.

Long Term Memory: Long term memory has the same storage length but is only updated once per Machine Learning Length. For instance, if Machine Learning Length is 100, it will save the Average of our data once every 100 bars. This means its memory is an average of 10,000 bars of Machine Learning. 'Average' connects its values diagonally whereas 'Hard Line' holds its value until it changes.

Use Average Last Distance In Potential Movement: This can help accuracy but generally also displaces the Support and Resistance by projecting it further.

Show Current Projection: Projections occur for each bar, and our Machine Learning utilizes these projections by storing and evaluating them. This toggle will display the Current Projection Line which is used to create all our Projections.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

YinYang Bar ForecastOverview:

YinYang Bar Forecast is a prediction indicator. It predicts the movement for High, Low, Open and Close for up to 13 bars into the future. We created this Indicator as we felt the TradingView community could benefit from a bar forecast as there wasn’t any currently available.

Our YinYang Bar Forecast is something we plan on continuously working on to better improve it, but at its current state it is still very useful and decently accurate. It features many calculations to derive what it thinks the future bars will hold. Let’s discuss some of the logic behind it:

Each bar has its High, Low, Open and Close calculated individually for highest accuracy. Within these calculations we first check which bar it is we are calculating and base our span back length that we are getting our data from based on the bar index we are generating. This helps us get a Moving Average for this bar index.

We take this MA and we apply our Custom Volume Filter calculation on it, which is essentially us dividing the current bars volume over the average volume in the last ‘Filtered Length’ (Setting) length. We take this decimal and multiply it on our MA and smooth it out with a VWMA.

We take the new Volume Filtered MA and apply a RSI Filter calculation on it. RSI Filter is where we take the difference between the high and low of this bar and we multiply it with an RSI calculation using our Volume Filtered MA. We take the result of that multiplication and either add or subtract it from the Volume Filtered MA based on if close > open. This makes our RSI Filtered MA.

Next, we do an EMA Strength Calculation which is where we check if close > ema(close, ‘EMA Averaged Length’) (Setting). Based on this condition we assign a multiplier that is applied to our RSI Filtered MA. We divide by how many bars we are predicting and add a bit to each predictive bar so that the further we go into the future the stronger the strength is.

Next we check RSI and RSI MA levels and apply multiplications based on its RSI levels and if it is greater than or less than the MA. Also it is affected by if the RSI is <= 30 and >= 70.

Finally we check the MFI and MFI MA levels and like RSI we apply multiplications based on its MFI levels and if it is greater than or less than the MA. It is also affected by if the MFI is <= 30 and >= 70.

Please note the way we calculate this may change in the future, this is just currently what we deemed works best for forecasting the future bars. Also note this script uses MA calculations out of scope for efficiency but there is potential for inconsistencies.

Innately it’s main use is the projection it provides. It only draws the bars for realtime bars and not historical ones, so the best way to backtest it is with TradingView’s Replay Tool.

Well, enough of the logic behind it, let's get to understanding how to use it:

Tutorial:

So unfortunately we aren’t able to plot legit bars/candles into the future so we’ve had to do a bit of a work around using lines and fills. As you can see here we have 4 Lines and 3 Zones:

Lines:

Green: Represents the High

Orange: Represents the Open

Teal: Represents the Close

Red: Represents the Low

Zones:

High Zone: This zone is from either Open or Close to the High and is ALWAYS filled with Green.

Open/Close Zone: This zone is from the Open to the Close and is filled with either Green or Red based on if it's greater than the previous bar (real or forecasted).

Low Zone: This zone is from either Open or Close to the Low and is ALWAYS filled with Red.

As you can see generally the Forecasted bars are generally within strong pivot locations and are a good estimation of what will likely go on. Please note, the WHOLE structure of the prediction can change based on the current bars movements and the way it affects the calculations.

Let's look 1 bar back from the current bar just so we can see what it used to Forecast:

As you can see it has changed quite a bit from the previous bar, but if you look close, we drew horizontal lines around where its projecting the next bar to be (our current realtime bar), if we go back to the live chart:

Its projections were pretty close for the high and low. Generally, right now at least, it does a much better job at predicting the high and low than it does the open and close, however we will do our best to fine tune that in future updates.

Remember, this indicator is not meant to base your trades on, but rather give you a Forecast towards the general direction of the next few bars. Somewhat like weather, the farther the bar (or day for weather), the harder it is to predict. For this reason we recommend you focusing on the first few bars as they are more accurate, but review the further ones as they may help show the trend and the way that pair will move.

We will conclude this tutorial here, hopefully this Predictive Indicator can be of some help and use to you. If you have any questions, comments, ideas or concerns please let us know.

Settings:

Forecast Length: How many bars should we predict into the Future? Max 13

Each Bar Length Multiplier: For each new Forecast bar, how many more bars are averaged? Min 2

VWMA Averaged Length: All Forecast bars are put into a VWMA, what length should we use?

EMA Averaged Length: All Forecast bars are put into a EMA, what length should we use?

Filtered Length: What length should we use for Filtered Volume and RSI?

EMA Strength Length: What length should we use for the EMA Strength

HAPPY TRADING!

Liquidity Heatmap [BigBeluga]The Liquidity Heatmap is an indicator designed to spot possible resting liquidity or potential stop loss using volume or Open interest.

The Open interest is the total number of outstanding derivative contracts for an asset—such as options or futures—that have not been settled. Open interest keeps track of every open position in a particular contract rather than tracking the total volume traded.

The Volume is the total quantity of shares or contracts traded for the current timeframe.

🔶 HOW IT WORKS

Based on the user choice between Volume or OI, the idea is the same for both.

On each candle, we add the data (volume or OI) below or above (long or short) that should be the hypothetical liquidation levels; More color of the liquidity level = more reaction when the price goes through it.

Gradient color is calculated between an average of 2 points that the user can select. For example: 500, and the script will take the average of the highest data between 500 and 250 (half of the user's choice), and the gradient will be based on that.

If we take volume as an example, a big volume spike will mean a lot of long or short activity in that candle. A liquidity level will be displayed below/above the set leverage (4.5 = 20x leverage as an example) so when the price revisits that zone, all the 20x leverage should be liquidated.

Huge volume = a lot of activity

Huge OI = a lot of positions opened

More volume / OI will result in a stronger color that will generate a stronger reaction.

🔶 ROUTE

Here's an example of a route for long liquidity:

Enable the filter = consider only green candles.

Set the leverage to 4.5 (20x).

Choose Data = Volume.

Process:

A green candle is formed.

A liquidity level is established.

The level is placed below to simulate the 20x leverage.

Color is applied, considering the average volume within the chosen area.

Route completed.

🔶 FEATURE

Possibility to change the color of both long and short liquidity

Manual opacity value

Manual opacity average

Leverage

Autopilot - set a good average automatically of the opacity value

Enable both long or short liquidity visualization

Filtering - grab only red/green candle of the corresponding side or grab every candle

Data - nzVolume - Volume - nzOI - OI

🔶 TIPS

Since the limit of the line is 500, it's best to plot 2 scripts: one with only long and another with only short.

🔶 CONCLUSION

The liquidity levels are an interesting way to think about possible levels, and those are not real levels.

BE - Spread_IndicatorSpread Indicator: An Overview Driven by the concept of forethought. The indicator predicts the range for the day and divides it into two or three Levels (upper, middle, and lower).

These ranges are drawn from possible supply and demand zones as well as potential price consolidation zones which has happend in the rolling number of days in the past.

It's true that market respects history. Which means the zones which are untested and created new in recent past shall be respected in the future days. Also the most respected Zones switch between support and resistance based on the price and volume pumped into the market.

Calucations Involved In the Indicator:

Indicator takes into account Factrol points, Fibonachi and its Retracements along with Channel and Candle Ranges to calculate the levels accordingly.

Levels Information:

Levels should be Treated and Traded the way like POC (Point Of Control). Price within the levels are basically controled by the levels above and underneath.

Converting idea to TradeOpportunity:

One can look into deploying IronCondor, while it is within the Zone also One Can deploy Long Straddle when the levels are Tested.

My personal Observation not a Trade Recommendation

With an Option Buyer view, I have been testing this indicator on the Index (BankNifty, FinNifty & Nifty) on 5 Min TF and 15 Min TF. Banknifty Works Well with Bull & Bear Spreads and FinNifty along with Nifty Works Well with Long Straddle & Long Strangle.

Happy to receive Suggesstions and feedback to improvise it with better option strategy.

Features:

1. Integrated with NLB for AlgoTrading.

2. Timely Alerts for Levels, Formation, Breach, TestOf Levels, CrossOvers.

3. Position Can be traded as CarryForward or Intraday.

Predictive Ranges [LuxAlgo]The Predictive Ranges indicator aims to efficiently predict future trading ranges in real-time, providing multiple effective support & resistance levels as well as indications of the current trend direction.

Predictive Ranges was a premium feature originally released by LuxAlgo in 2020.

The feature was discontinued & made legacy, however, due to its popularity and reproduction attempts, we deemed it necessary to release it open source to the community.

🔶 USAGE

The primary purpose of this indicator is to provide potential support & resistance levels on the chart by estimating future trading ranges.

When the price reaches one of the upper/lower levels of the Predictive Ranges we can expect the price to reverse.

If the price exits the predicted range, new levels are given in real-time & they do not repaint. Higher "Factor" values allow returning longer term and wider ranges less susceptible to be exited.

🔹 Estimating Trend Directions

Users are able to easily estimate trend directions by looking at the central levels of the predictive ranges, which represent an estimate of the price central tendency.

If this central level increases it means the price is up-trending, if it is decreasing price is down-trending.

🔶 SETTINGS

Length: ATR Length used for the indicator calculation. Higher values will tend to return ranges of equal width.

Factor: Control the ranges width. Higher values will return less frequent ranges, each having a higher width.

Timeframe: Indicator timeframe output.

Source: Input source of the indicator. It is recommended to use input sources on the same scale as the price.

Monte Carlo Price ProbabilitiesMonte Carlo simulations have been a popular tool in the world of finance, risk analysis, and decision making for decades. In this post, I will take you through the history of Monte Carlo simulations and explain how I implemented this powerful technique in Pine Script. This implementation can help traders and investors in various time frames to better understand the potential future price movements of financial instruments based on historical data.

History of Monte Carlo Simulations

The Monte Carlo method was named after the famous Monte Carlo Casino in Monaco, as the technique involves using random sampling to approximate solutions to mathematical problems. The method was first introduced by Stanislaw Ulam, a mathematician working on the Manhattan Project in the 1940s. Ulam realized that using random sampling could provide approximate solutions to complex problems that were otherwise difficult or impossible to solve analytically.

Over the years, Monte Carlo simulations have found applications in various fields, including physics, engineering, and finance. In the world of finance, the method has been used to model stock price movements, option pricing, portfolio optimization, and risk management.

Implementation in Pine

In my implementation of Monte Carlo simulations in Pine, I created a script that allows users to input several parameters such as the arbitrary price, number of simulations, number of steps into the future, and the start bar index. The start bar index is a crucial setting for running the script on lower time frames, as it helps to ensure that the script runs smoothly for a given symbol.

The script then calculates the log return of each bar and categorizes them into green (positive) or red (negative) moves. It uses these historical price movements to calculate the probabilities of future price movements for each step in the simulation.

The core of the Monte Carlo simulation lies in the `monte()` function, which generates random numbers to determine if the next price movement will be green or red, and then selects a move size based on its probability. The `sim()` function runs multiple simulations using the `monte()` function and stores the results in an array.

Finally, the script calculates the probability of the arbitrary price being reached in the future based on the results of the simulations. It also plots the probability on the chart, allowing users to visually assess the potential future price movements of the financial instrument.

Using the Monte Carlo Simulation

To use the Monte Carlo simulation in Pine, you need to input the desired parameters such as the arbitrary price, number of simulations, number of steps into the future, and the start bar index. For some symbols, you may need to set the start bar index to around 10k to ensure that the script runs smoothly.

Once you have input the parameters and run the script, you will see the probability of reaching the arbitrary price plotted on the chart. This can provide a valuable insight into the potential future price movements of the financial instrument based on historical data, helping you make more informed trading and investment decisions.

Conclusion

Monte Carlo simulations have a rich history and have proven to be a valuable tool in various fields, including finance. My implementation of Monte Carlo simulations in Pine allows traders and investors to better understand the potential future price movements of financial instruments in various time frames. By evaluating the probabilities of reaching specific price levels, users can make more informed decisions and better manage their risk.

Bayesian predictive leading indicator--------- ENGLISH ---------

This is a predictive indicator ( leading indicator ) that uses Bayes' formula to calculate the conditional probability of price increases given the angular coefficient. The indicator calculates the angular coefficient and its regression and uses it to predict prices.

Bayes' theorem is a fundamental result of probability theory and is used to calculate the probability of a cause causing the verified event. In other words, for our indicator, Bayes' theorem is used to calculate the conditional probability of one event (price event in this case) with respect to another event by calculating the probabilities of the two events (past price) and the conditional probability of the second event (future price) with respect to the first event.

The red line represents the angular coefficient. The blue line represents the normalized expected price. Finally, the yellow line represents the conditional probability that the price will increase or decrease.

How to use it. In addition to the convenient histogram, which follows the angular coefficient, another practical operational application might be to go long when the blue line is above the red and yellow lines. Conversely short when the blue is below the red and yellow.

When the yellow line passes above all others, a reversal in the long direction is imminent and vice versa.

The extent of the reversal depends on how far the yellow line will be away in price from the other 2 lines.

This indicator is in its embryonic state and updates will follow to make it more graphically readable, add alerts, etc.

Stay tuned! Leave a boost and comment or write to me if you wish.

--------- ITALIANO ---------

Questo è un indicatore predittivo ( leading indicator ) che utilizza la formula di Bayes per calcolare la probabilità condizionata che il prezzo aumenti dato il coefficiente angolare. L’indicatore calcola il coefficiente angolare e la sua regressione e lo utilizza per prevedere i prezzi.

Il teorema di Bayes è un risultato fondamentale della teoria della probabilità e viene impiegato per calcolare la probabilità di una causa che ha provocato l’evento verificato. In altre parole, per il nostro indicatore, il teorema di Bayes serve per calcolare la probabilità condizionata di un evento (di prezzo in questo caso) rispetto a un altro evento, calcolando le probabilità dei due eventi (prezzo passato) e la probabilità condizionata del secondo evento (prezzo futuro) rispetto al primo.

La linea rossa rappresenta il coefficiente angolare. La linea blu rappresenta il prezzo previsto normalizzato. Infine la linea gialla rappresenta la probabilità condizionata che il prezzo aumenti o diminuisca.

Come si usa? Oltre al comodo istogramma, che segue il coefficiente angolare, un'altra applicazione operativa pratica potrebbe essere di andare long quando la linea blu è sopra la linea rossa e gialla. Viceversa short quando la blu è sotto la rossa e la gialla.

Quando la linea gialla passa sopra tutte le altre è imminente un'inversione in direzione long e viceversa.

L'entità dell'inversione dipende da quanto la linea gialla sarà distante di prezzo dalle altre 2 linee.

Questo indicatore è al suo stato embrionale e seguiranno aggiornamenti per renderlo graficamente più leggibile, aggiungere alert, ecc.

Stay tuned! Lascia un boost e commenta o scrivimi se desideri.

Acceleration-Based MA Slope PredictionHello traders,

I developed this indicator while working on a trading strategy using moving average slope and acceleration, and I found the concept interesting enough to share it.

Let me briefly explain this indicator.

----About White Plot----

1. Calculate the first derivative approximation at the current point of the Moving Average, and then calculate the second derivative approximation to obtain the 'Acceleration'.

2. Where the acceleration is 0, it signifies a change in the force of the moving average.

3. Therefore, by drawing a parabola based on the acceleration at that time, can depict the parabolic shape of the moving average.

This is represented as a white circle on the indicator.

4. These circles are reset at the next point where the acceleration is 0, indicating a change in the parabolic force.

If the moving average rises more sharply than the predicted value of the rising parabola, a more drastic increase is expected.

5. In this case, you can start risk management around the time the drawn parabola breaks.

(The actual MA is represented by green/red lines)

6. Before the trend changes, i.e., before the direction of the moving average changes, there is a section where the acceleration is 0, and this is represented on the chart as follows.

(The lower indicator shows the acceleration of the corresponding parabola)

----About Red Plot----

1. Calculate the first derivative approximation of the moving average value, the 'slope'.

2. Where the slope is 0, it represents the extreme point of the parabola.

3. Therefore, by using the acceleration at that point as the coefficient of the quadratic function and setting the extreme point as a vertex, we can draw a quadratic function. This is represented as a red circle on the indicator.

(Keep in mind that the actual moving average is not a quadratic function; this is a "forced" quadratic function assuming the parabola is maintained)

4. These circles are reset at the next extreme point where the slope is 0, and a new quadratic function is created.

Based on the formula obtained in the above process, you can predict the future moving average through 'offset'.

5. That is, if the x value at the current point is 'k', you can predict the moving average one candle ahead by substituting (k+1) into the quadratic function.

The predicted value at the past position is shown as a red circle.

6. The smoother the chosen moving average, the fewer extreme points will appear, and the higher the likelihood of the parabola fitting.

For the T3 set as the default value, it shows very high accuracy even when predicting about 20 candles ahead.

On the other hand, rough moving averages like SMA have limited prediction value.

(SMA 60, offset = 10)

--------

The moving average with a very high level of accuracy is JMA (Jurik Moving Average). However, since the code for this moving average is not public, I recommend those interested to check it through my code.

Additionally, I believe the code of this indicator I've uploaded has significant utility.

As an example, you can use the breaking point of the parabola predicted by the acceleration to determine when the force changes again for entries/losses. There are many other possible applications as well.

I look forward to seeing more excellent results from this indicator.

--------

안녕하세요 트레이더여러분.

이 지표는, 제가 이동평균선의 기울기와 가속도를 이용하여 매매를 하기 위한 지표를 개발하다가, 흥미로운 내용이라고 판단하여 만들게 되었습니다.

이 지표에 대해 간단히 설명드리겠습니다.

----하얀색 플롯에 대해----

1. 이동평균선이 진행되는 현재 시점에서 미분의 근사값을 구하고, 다시 한 번 미분의 근사값을 구해서 '가속도'를 얻습니다.

2. 가속도가 0이 되는 곳은, 곧 해당 이동평균선의 힘이 바뀌는 곳을 의미합니다.

3. 따라서, 그 당시 시점 기준으로 포물선을 그려낸다면, 가속도를 이용하여 해당 이동평균선의 포물선을 그려낼 수 있습니다. 이것은 지표의 하얀색점로서 표기됩니다.

4. 이 때, 이러한 점들은 다음의 가속도가 0이 되는 지점, 즉 포물선의 힘이 바뀌는 곳에서 다시 초기화됩니다.

5. 올라가고 있던 포물선에서의 예측치보다 이동평균선이 더 급하게 올라간다면, 더욱 급격한 상승이 예상됩니다. 이 경우, 그려지고있는 포물선이 깨질 때쯤부터 리스크 관리를 시작할 수 있습니다.

(녹색/빨간색의 선으로 실제 MA를 표현했습니다. 거슬리시면 '모습'가셔서 끄셔도 좋습니다. )

6. 추세가 변경되기 전, 즉 이동평균선의 방향이 바뀌기 전에는 가속도가 0이 되는 구간이 존재하고, 그것이 차트 위에 다음과같이 표현됩니다.

(하단의 지표는, 해당 포물선의 가속도을 나타냅니다)

----붉은색 플롯에 대해----

1. 이동평균선 값을 미분 근사값 즉, '기울기'를 구합니다.

2. 기울기가 0이 되는 곳은, 포물선이 극점이 되는 곳을 뜻합니다.

3. 따라서, 해당 시점의 가속도를 2차함수의 계수로 하여, 또한 해당 극점을 하나의 꼭지점으로 설정하여,이차함수를 그려낼 수 있습니다. 이것은 지표의 빨간색점으로서 표현됩니다.

(실제 이동평균선은 2차함수가 아니기에, 포물선이 유지된다는 가정 하에 "억지로"만들어낸 이차함수입니다)

4. 이 때, 이러한 점은 다음 극점이 0이 되는 곳에서 초기화되고 이차함수가 만들어집니다.

5. 위의 과정에서 얻은 식을 바탕으로 'offset'을 통해 미래의 이동평균선을 예측할 수 있습니다.

즉, 현재시점의 x값을 'k'라고 한다면, (k+1)을 이차함수에 대입하여 1캔들 앞의 이동평균선을 예측할 수 있습니다.

해당 예측치가 지나간 자리는, 빨간색점을 통해 보여집니다.

6. 선택한 이동평균선이 스무스할수록 극점은 덜 등장하게되고, 포물선의 위치가 맞아들어갈 가능성이 높습니다.

현재 디폴트값으로 설정된 T3의 경우, 약 20캔들 앞을 예측해도 매우 높은 정확도를 보여줍니다.

반면에, SMA와 같이 울퉁불퉁한 이동평균선은 가능한 예측치가 크지 않습니다.

(SMA 60, offset=10)

--------

매우 높은 수준의 정확도를 보여준 이동평균선은 JMA(Jurik Moving Average)입니다. 다만 이 이동평균선은 코드가 공개되지 않았기때문에, 관심있으신 분은 저의 코드를 통해 한번 확인해보시길 권장드립니다.

추가로, 제가 올린 이 지표의 코드는 이용가치가 높다고 생각합니다.

하나의 예시로서, 가속도로 예측한 포물선이 깨지는 곳을 기준으로, 힘이 다시 한 번 바뀌는 것을 이용해 진입/로스를 할 수 있습니다. 그 외에도 매우 다양한 활용이 가능합니다.

이 지표를 통해 더욱 좋은 새로운 결과물이 나오길 기대해봅니다.

High and Low PredictorWhat can I Do:

Update at 12:01 AM everyday.

Predict the Highest and the Lowest price of each day.

Color of the lines: the red color suggests downward while the green color suggests upward.

It is able to predict the highest and the lowest price of each day by calculating the history prices,

but please notice this is only prediction! Not one hundred percent correct!

The data suggests chances to buy and to sell, and the history data is also available for review.

If the switch of resistance is turned on, the resistance will be displayed on the chart directly for reference.

How to use it?

First, choose the period of 60 minutes/1 hour,

Second, add alerts, when price hits the predicted prices, it will send you alert alarm.