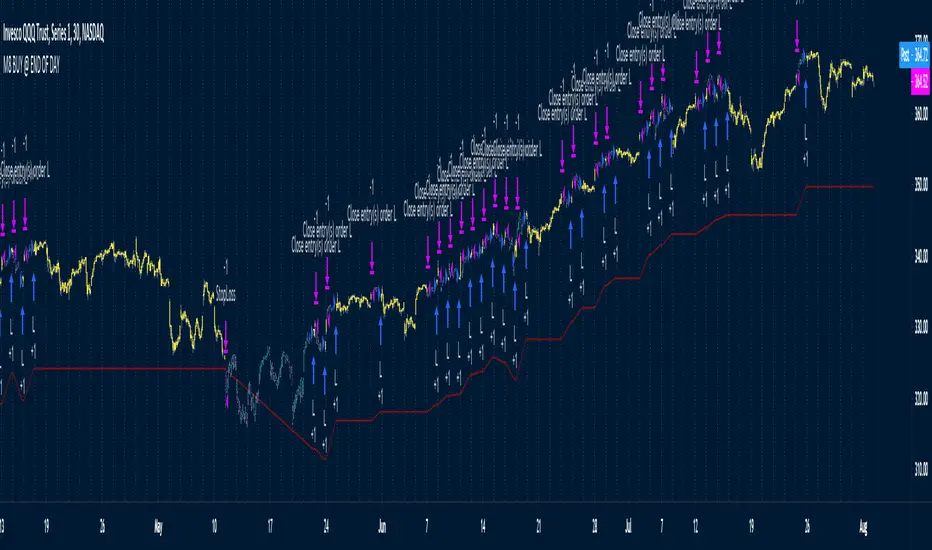

M8 BUY @ END OF DAYI've read a couple of times at a couple of different places that most of the move in the market happens after hours, meaning during non-standard trading hours.

After-market and pre-market hours and have seen data presented showing that systems which bought just before end normal market hours and sold the next morning had really amazing resutls.

But when testing those I found the results to be quite poor compared to the pretty graphs I saw, and after much tweaking and trying different ideas I gave up on the idea until I recently decided to try a new position management system.

The System

Buys at the end of the trading day before the close

Sells the next morning at the open IF THE CLOSE OF THE CURRENT BAR IS HIGHER THAN THE ENTRY PRICE

When the current price is not higher, the system will keep the position open until it EITHER gets stops out or closes on profit <<< this is WHY it has the high win %

The system has a high win ratio because it will keep that one position open until it either reaches profit or stops out

This "system" of waiting, and keeping the trade open, actually turned out to be a fantastic way to kind of put the complete trading strategy in a kind of limbo mode. It either waits for market failure or for a profit.

I don't really care about win % at all, almost always high win % ratio systems are just nonsense. What I look for is a PF -- profit factor of 1.5 or above, and a relatively smooth equity curve. -- This has both.

The Stop Loss setting is set @ .95, meaning a 5% stop loss. The Red Line on the chart is the stop loss line.

There is no set profit target -- it simply takes what the market gives.

Non-Repainting System

This does use a 200D Simple Moving Average as a filter. Like a Green Light / Red Light traffic light, the system will only trade long when the price is above its 200 Moving average.

Here is the code: "F1 = close > sma(security(syminfo.tickerid, "D", close ), MarketFilterLen) // HIGH OF OLD DATA -- SO NO REPAINTING"

I use "close ", so that's data from two days ago, it's fixed, confirmed, non-repainting data from the higher timeframe.

-- I would only suggest using this on direction tickers like SPY, QQQ, SSO, TQQQ, market sectors with additional filters in place.

Strategy!

Day of Week Custom Buy/Sell StrategyThis strategy was made for bitcoin and allows you to back test longing or shorting for various days of the week. The price may tend to go in one direction or another for each week day, and this strategy allows you to test days across a range of dates to capitalize on this.

Make sure you are on the daily time frame while viewing the performance and trade history to ensure the script works as intended and you have the most historical data as possible from Trading View.

Custom Date Buy/Sell StrategyThis strategy allows you to back test longing or shorting during a period of time between two dates.

Make sure you are in the daily time frame while viewing the performance and trade history to ensure you have the most historical data as possible from Trading View.

Finally, due to the way Trading View enters trades at the end of a candle, you must subtract one day from your starting and your end dates.

Three (3)-Bar and Four (4)-Bar Plays StrategyThis strategy analyzes the three and four-bar play which is when price action has a wide igniting bar that has a full body, then one or two narrow bars which have a relatively equal high for long plays and relatively equal low for short plays, then a continuation bar. You should not take plays that will encounter resistance. The stop loss is placed for long plays below the 2nd bar (or 3rd bar for 4-bar play).

This is commonly used on 1m, 2m, 5m, and 10m charts.

Jared Wesley is one of the more notable traders that use this setup. You can edit as an input the start date, end date, igniting bar size, the body percentage of the igniting bar, the relative equality of the 2nd bar (and 3rd bar for 4-bar play) compared to the igniting bar, and profit multiplier.

7-RSI strategyHello, I've only been trying to learn PineScript for two months on my own, here I am posting a version of the strategy for a grid bot with 20 orders, order size 5%, earlier I tried to find something similar, but could not. Perhaps others, those who, like me, are just starting to learn PineScript, will find something useful. In the process of using grid bots, I noticed that the RSI indicator is sufficient, so the strategy uses 7 RSI indicators on different timeframes, but it is not necessary to use all 7, usually 3 is enough, therefore, by default, the RSI values are set to limit so that there is no effect on the settings of others. The step between bot orders is set in the settings. The code can of course be simplified, but it's better for understanding, I think.

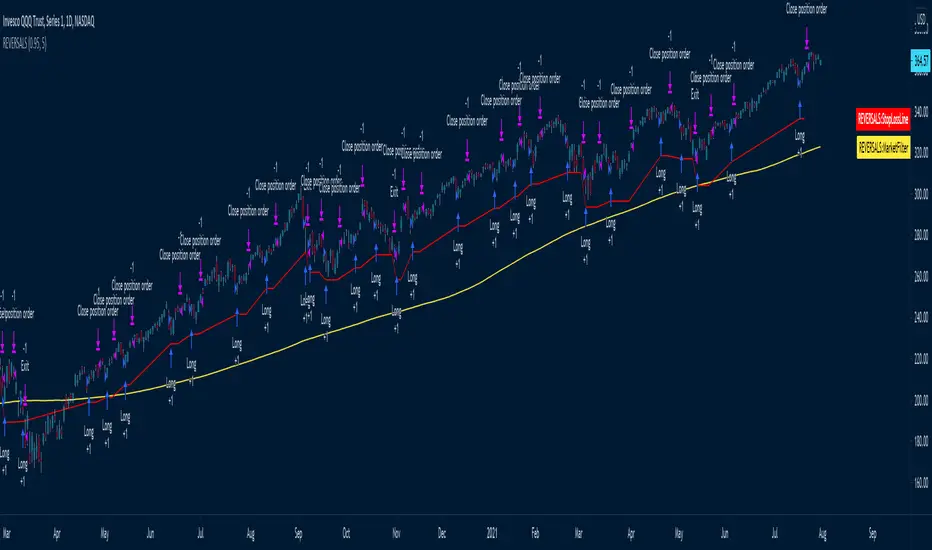

REVERSALS

The systems basically play reversals, it enters when the close is lower than its low of 5 bars ago to enter

It exits when the price is higher than the high of 5 days ago

Uses a 200 MA as a market filter, does not trade when the price is below its 200 Moving average

Uses a 5% stop, as per the red Stop Loss Line -- can be adjusted

The amount of bars it uses to look for reversals is set to 5 by default, but can be adjusted in settings.

Best to use on directional instruments where you know that the long term direction is up, for example:

TQQQ, SSO, SPX, SPY, or sector tickers -- but it would be best to include some more advanced filtering for sectors

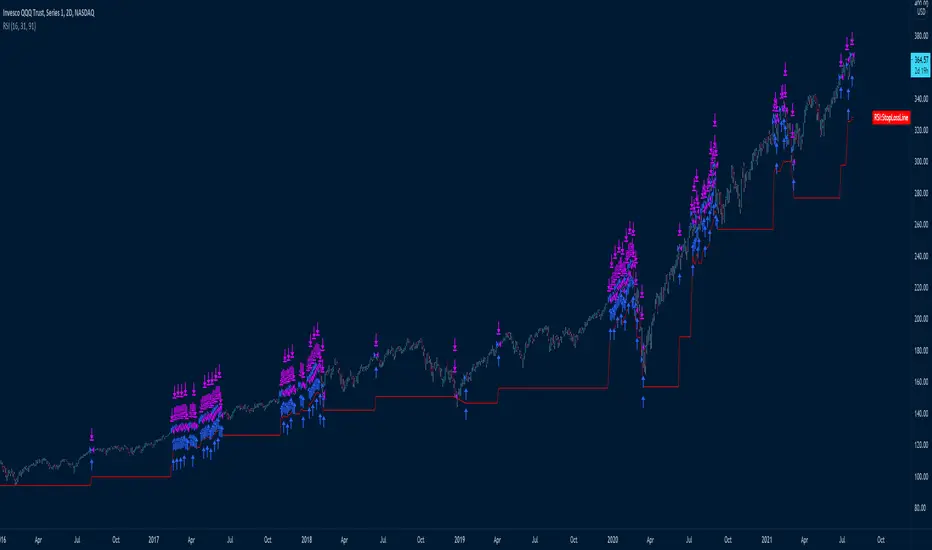

DUAL RSI

This system uses two RSI's with different settings

Fast RSI Lenght is 16, buys when RSI price is oversold @ 91 or lower, and sells when RSI price is overbought at 70

Slow RSI Lenght is 31, buys when RSI price is oversold @ 91 or lower, and sells when RSI price is overbought at 68

Pyramiding is set to 2 since each system should be able to trade in the same direction on the same day

The Red StopLine is a stop loss of 10% based on the combined strategic position average entry price.

I've used a 2D chart because I prefer longer-term charts for higher quality signals

The way I trade all the systems is to set up alerts to let me know when to look at what setups

The system also has a market filter and does not trade when the close is lower than its 200 days moving average

10PreBuyerQuite a simple system

Uses a moving average, the blue line to try and get filled at favorable prices

The MA is multiplied by a number (e.g. .90) which means the system tries to get filled at a 10% lower price (on the Blue MA line)

This means that stop limit buy orders have to be set in advance on the blue line and hope that they would get filled when there is a temporary drop in price

This obviously works best on tickers with a clear long-term up direction

The multiplier can be set to .95 to try and get in on 5% drops instead of 10% drops

"Prof TRG %" determines what profit target you'd like the system to use, default is 1.2 meaning a 20% target, but 1.05, 1.10, and 1.30 would also be good considerations

"Loss TRG %" determines what stop-loss target you'd like the system to use, default is 0.90, meaning 10% stop loss, but, .95, and .85 would also be good considerations

The Profit Target line is green

The Stop Loss target line is red

Using the combination of the Stop Loss inputs and Profit Target inputs you can determine your own RR (Risk to reward ratios), for example, 1:1, 2:1, 3:1, 5:1

Let me know if anything is unclear and I'll try to clarify.

Again, this system assumes that you'll have waiting stop limit orders that are trying to get filled on the blue line, is below price most of the time -- so it's trying to get in on temporary drops on instruments that have a long term uptrend.

1:1 RR ratio would mean high win %

1:5 RR ratios would mean low win %

Not that win % matters, the important things IMO to pay attention to is Profit Factor and a relatively smooth equity cruve

Simple Buy/Sell StrategyThis is the strategy version of the original 'Simple Buy/Sell Indicator' by @Shizaru .

The original indicator description explains the logic behind the strategy:

"The original script was posted on ProRealCode by user Doctrading.

This little and simple code allows you to draw an indicator, which show you when buy or sell conditions are met.

For "buy" conditions, I did just set :

close > MM200

close > Parabolic SAR

MACD > 0

RSI7 > 50

For "sell" conditions : the opposite.

Of course, you can set what you want, in order to test your strategies.

Of course, to be profitable, you must also set your trading rules (entry, stop loss, trailing stop, take profit, etc.)

It's only an indicator, which doesn't show entry or exit rules."

Hope this helps someone!

Multi-X by HamidBoxHello to All, introducing Multi Types Crossover strategy,

simply the best way of trading with Crossover and Crossunder Strategy, How it Works???

I added 5 types of Moving Averages,

1: Simple Moving Average ( SMA )

2: Exponential Moving Average ( EMA )

3: Weighted Moving Average ( WMA )

4: Volume Weighted Moving Average ( VWMA )

5: Relative Moving Average (RMA)

With this indicator, you can do scalping, You can trade not only with similar types of Moving Average indicators but also with different types of Moving Average indicators.

what is mean? like: Normal Condition is:

( Simple Moving Average ) Crossover to ( Simple Moving Average ), SMA x SMA

( Exponential Moving Average ) Crossover to ( Exponential Moving Average ), EMA x EMA

But we can Crossover with:

( Exponential Moving Average ) Crossover to ( Simple Moving Average ), EMA x SMA

( Simple Moving Average ) Crossover to ( Weighted Moving Average ), SMA x WMA

( Weighted Moving Average ) Crossover to ( Weighted Moving Average ), WMA x WMA

( Simple Moving Average ) Crossover to (Relative Moving Average), WMA x RMA

and also I added Moving Average ZONE in this tool, What does it work???

The zone will tell us what type of direction the market has, if the market is above the zone, it's mean we have a Bullish Trend, and if the market is below the zone, it means the market has a Bearish Trend,

so if you want to play on the safe side, never trade when the market is in Bearish Trend, and if you want to play on aggressive mood, you can skip Moving Average Zone section.

Binary Options Strategy TemplateWith the hype around Binary Options trading (more like gambling instead of trading) it is good to be able to backtest a strategy before using it in the live markets.

In a Binary Options trade the trade get's closed after a specific amount of time and the only thing that matters is if the market has increased in price or decreased after that amount of time.

Because of this a strategy backtest should close all positions after a specific amount of time. In this super small script the number of bars since the trade was opened is used as a way to close the position. So for example if you use this strategy on the 1 minute charts with number of bars set to 5 it will close the position 5 minutes after opening it. Purpose of this script is using it as a strategy on already existing scripts to check viability for options trading.

With the limited pine knowledge that I have I do not know if it is possible to create a more realistic binary options strategy which also calculated the profit. If someone knows a more advanced version of this please let me know.

LargestMarketCapsThis trading system uses a MA to check if the LARGEST CAP stocks are above or below the MA.

You can see from the indicator below how well it manages to capture big moves.

It aggregates the data of all the tickers to create the histogram indicator at the bottom of the chart called MarketLeaders.

If a ticker is above its moving average, then the output will increase by +1 and -1 if a ticker is below its moving average.

This is a powerful system because it uses not only data from one stock but from the stocks that really affect the market big time. If those stocks don't do well, the market won't do well either.

Basically if all the market leaders are doing well, then this system will buy those 20 tickers and keep positions open until the MarketLeaders indicator crosses below 0 -- meaning red.

It also has a red stop loss line, with a wide 15% stop loss to keep us in the trades for the long term.

I've used a 5-day chart because I wanted fewer signals, but higher quality signals.

There are no profit targets, this exits when the indicator turns red -- meaning below 0 or if a position falls 15% in price.

The MA setting is adjustable, the default is 20

These are the tickers that the strategy and indicator currently looks at

The tickers will need to be updated every 6-12 months to remove and ad those who have dropped out of the largest 20 stocks.

It would be a good idea to create a watchlist and alerts for the Large Cap tickers so you can scroll through to see how the system performed on each ticker

"SPX"

"QQQ"

"AAPL"

"MSFT"

"GOOG"

"FB"

"BRK.A"

"TSLA"

"V"

"JPM"

"WMT"

"UNH"

"MA"

"KO"

"PYPL"

"PG"

"HD"

"DIS"

"BAC"

"ADBE"

"CMCSA"

"NKE"

RELATED IDEAS / Indicators

Market Leaders Ribbon

Market Leaders Large Performance Table

EMA StrategyThis is a simple EMA cross strategy. This script was published by CaptJava. I added in the ability to check off a box and allow shorting, the ability to select a back testing date range and also the ability to enter the buy message and sell message in the properties. You then create the webhook alert and put only this in the message:

{{strategy.order.alert_message}}

That will pull in your alert message dynamically.

I may add more features to this over time.

Chaikin Money Flow + MACD + ATRHere I present you on of Trade Pro's Trading Idea: Chaikin Money Flow + MACD + ATR.

This strategy is not as profitable as it can be seen in one of his videos. In the forex market, the strategy could reach a maximum of 35% profitability.

I have, as some of my followers have requested, created an overview of the current position, risk and leverage settings in the form of a table.

Furthermore, one can again swap between short and long positions.

It is now possible to select or deselect individual indicators.

I have chosen the ATR alone as a take profit stop loss, as in his strategy.

A position is only triggered as soon as all prerequisites have been fulfilled and a command is executed. This prevents false triggering by bots and repainting.

-----------------------------------------------------------------------------------

How does the strategy work?

ENTRY

Long

The MACD indicator must be above the zero line.

Then the K line must cross the D line.

Finally, when this happens, the Money Flow Index must be above the zero line.

Short

Contrary to the premise of long positions.

EXIT

ATR Exit

The value of ATR at the time of buying is multiplied by the value entered in "Profit factor ATR" and "Stop factor ATR". As soon as the price reaches this value, it is closed.

Important

The script must be optimized for each coin or currency pair.

I will publish a guide to the strategy shortly. There I will explain how the table works and how to set the strategy correctly.

The results of the strategy are without commissions and leverage.

If you have any questions or feedback, please let me know in the comments.

CCI & EMA strategy by TradeswithashishThis strategy is extremely useful for positional traders or traders using timeframe 15-minute of higher. It uses following combo of values:

VWAP, CCI, Volume and Moving average (simple and exponential)

Caution:

Avoid taking trade if candle size is greater than twice the average candle size. for that wait for the retracement to near trailing stoploss

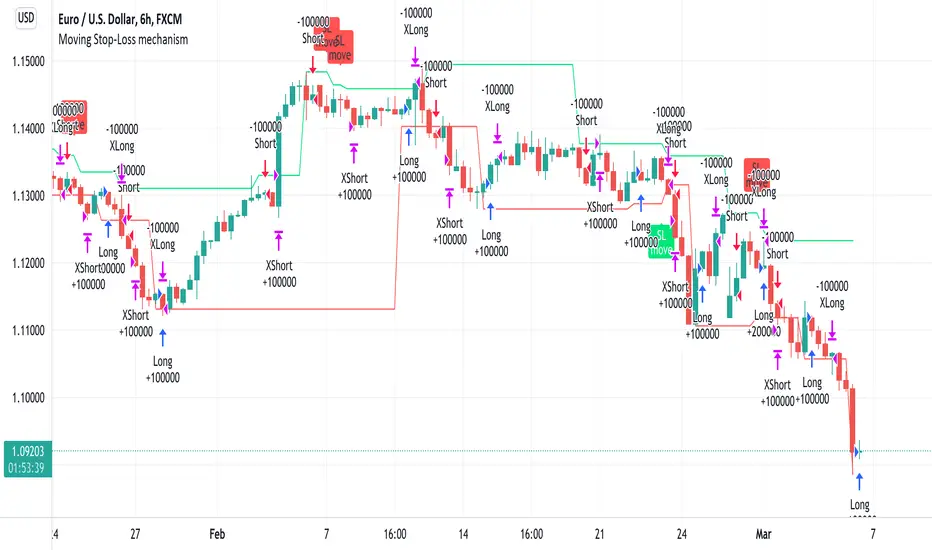

Moving Stop-Loss mechanism + alerts to MT4/MT5"How to code moving stop-loss mechanism", is one of the most often repeating questions in private messages I receive, so just to focus on this mechanism, I made a spin-off from my previous script: TradingView-Alerts-to-MT4-MT5-dynamic-variables-NON-REPAINTING .

The logic here moves the stop-loss each time a trade is running and a new pivot high/low is detected. When such event occurs (UpdateLongStopLoss or UpdateShortStopLoss), stoploss_long or stoploss_short mutable variable is modified. And it needs to be coded inside strategy.exit() line as "stop=stoploss_long" or "stop=stoploss_short". Entries are pretty straightforward - on Stoch crosses.

Last lines of the script show how to wrap information about such updates and send send alerts to MetaTrader via TradingConnector for execution in Forex/indices/commodities/crypto markets via MetaTrader. Please note that "tradeid=" variable must be passed with each alert, to let MetaTrader know which trade to modify. SLMOD, TPMOD are recently added commands, along with BE (as in "move stop-loss to breakeven" - but that's another topic).

Please disregard strategy backtest results, as this script is for coding education purposes only. However, it seems with the stop-loss mechanism enabled, the results are even better, than in original version of the script :)

RSI Cross [xaurr]This is simple but profitable rsi cross strategy, to find optimal values you can change rsi and ema periods.

Good Luck!

TradePro's Trading Idea Cipher Divergence EMA Pb StrategyHere I present you on of Trade Pro's Trading Idea: Cipher B+ Divergence EMA Pullback Strategy.

Optimized the crypto pairBTC/USDT in the 30 minute chart.

There is the possibility to switch between short and long positions.

You can choose between 2 different take profit/stop loss types: The Lowest Low/ Highest High Stop Loss/ Take Profit and the ATR Take Profit/ Stop Loss.

-----------------------------------------------------------------------------------

How does the strategy work?

ENTRY

Long

The price must be above the 200 EMA .

The price needs to make a pullback into the 50 EMA .

Right after that, the Cipher B indicator must give a buy signal, it must be below the zero line and the Money Flow cloud must be green.

Short

Contrary to the premise of long positions.

EXIT

Lowest Low/ Highest High Exit

The Lowest Low (long) / highest high (short) serves as the stop loss. The TP is formed on the basis of a factor.

(Long for example: *Lowest Low* multiplied by *Profitfactor* = TP).

ATR Exit

The value of ATR at the time of buying is multiplied by the value entered in "Profit factor ATR" and "Stop factor ATR". As soon as the price reaches this value, it is closed.

Important

The script must be optimized for each coin or currency pair. However, only the values for the profit factor, the stop loss and Lowest Low / Highest High are relevant.

Also, by changing the Chanel Length and the Chanel Average, you can create strong profit changes.

The results of the strategy are without commissions and leverage.

If you have any questions or feedback, please let me know in the comments.

If you need more information about the strategy and want to know exactly how to apply it, check out my profile. There I have created a tutorial for the function of the script.

BTC Volatility Band StrategyThis script/strategy is a pullback system designed for securities with high volatility so naturally Bitcoin is an excellent choice for trading this. This could be used both on a daily chart or on lower timeframes (I found good results on 3hr timeframe but haven't tested it on anything under 1hr).

A volatility band is created by comparing the candle close price of the previous 2 candles and and it uses this change in price to create a moving average. A band is wrapped around the moving average with a standard deviation of 1 for the inner band and 2 for the outer band. If the price is above a pre-set MA (moving average filter) then it is determined we are in an uptrend so the strategy will issue a buy signal when we are in an uptrend and there is a pullback which causes the lower inner deviation band to be spiked, but if the price continues and falls through the outer deviation band then a buy signal will not issue as this detriments that the volatility spike is to great. You can see a spike "buy" event occur on the indicator where the background is coloured green. For a short/sell then there will be a spike on the upper inner band and we are below the pre-set MA filter, for this it shows with red background on the indicator.

The user can change the date range they wish to test, the moving average period for the volatility tracking and the inner and outer band deviations. On BTC I left the inner deviation and outer deviation bands on standard settings but found the 3 period volatility tracking to be good for trading 1 day chart and the 5 period volatility tracking good for the 3hr chart. Since this is not a buy and hold strategy then for trading you would probably want to stick with the most liquid coins so you can get in and out very fast on any exchange. If you wanted to tray this on less volatile markets then changing the inner deviation band to ~0.75 would work okay in various futures markets likely stocks as well. The take profit and stop loss levels are based on a multiple of the trading range looking back the past 7 candles.

Attached result is trading 1 BTCUSDT contract on Binance.

Trade Vertex - Bank Nifty Volume IndicatorNSE:BANKNIFTY

We all know that the value of an Bank Nifty is derived from top banking sector underlying stocks.

The value of Bank Nifty is calculated from free float market capitalization.

Using the same formula, I made an indicator on the bases of weighted volume of each stock.

This indicator will help you to plot Volume on Bank Nifty.

PMax on Rsi w/T3 *Strategy*Profit Maximizer Indicator on RSI with Tillson T3 Moving Average:

PMax uses ATR calculation inside, for this reason users couldn't manage to use PMax on RSI because RSI indicator doesn't have High and Low values in bars, but ATR needs that values. So I personally calculate RSI in a different way to have High and Low values of RSI wrt price bars.

IMPORTANT:

Because of the sudden movements and divergences on RSI , this indicator must firstly optimized for the charts before using. Optimization can be held by users for the meaningful parameters for each chart.

3 parameters are critical when optimizing:

First: Multiplier

Second: Tillson T3 Length

Third: T3 Volume Factor

Says, Kıvanç Özbilgiç. Here's the strategy version for you to backtest & optimize properly.

Enjoy.

Martingale TemplateA template example on how to apply the famous Martingale gambling strategy. When your strategy gets an exit signal for your long position that leaves you without profit, you re-enter on the next entry long condition with double the capital of the previous amount entered with. You keep doubling the amount of capital entered with until you finally exit with a profit. If the strategy isn't sound enough then it could take several attempts and it can take only as much as a dozen tries to eat away at all your capital as the capital required to double on the next entry increases greatly over time by consecutive products of 2.

The strategy used is just a simple moving average crossover, above the moving average is going long, below the moving average is going short. It can be replaced with whatever strategy that you want. The colored vertical bars show long and short positions and exits. The default option on the tick box under the settings show the number of attempts at entering before finally exiting with a profit, the other option shows the amount of capital it took starting from 1.

Know Sure Thing and EMA Strategy by JLXThis is a simple strategy based in Know Sure Thing indicator and an Exponential moving average,

Rules are as follow:

- You can go long when the KST cross signal bellow 0 and price closes above the target EMA

- You can go short when the KST cross signal above 0 and price closes bellow the target EMA

I include a trailing stop loss, default its 0.5%

Hope you enjoy it