Juiced Ichimoku StratI saw this indicator and thought I'd try to make it into a script. I can't get an exit when the EMA is between signal lines so it's a long/short strategy until I can figure that part out.

Strategy

Recursive Moving Trend Average Strategy Taken from an article "The Yen Recused" in the December 1998 issue of TASC,

written by Dennis Meyers. He describes the Recursive MA in mathematical terms

as "recursive polynomial fit, a technique that uses a small number of past values

of the estimated price and today's price to predict tomorrows price."

Red bars color - short position. Green is long.

Glory Hole with SMA + ADX - StrategyHere you get a script with the rules for "Glory Hole"-Strategy from Linda Raschke.

In Addition, I choose the SMA - not the EMA for this script.

MY RECOMMONDATION:

If you get a trade Signal, then set an sell- oder buy-order on the high or low. If the next bar doesn't touch into the trade, then delete your order.

Have fun and good look.

HiLoHi Everyone,

Do you guys know how can I add an exit strategy to this hilo.

I would like it to exit either with hilo invertion (already does) or with profit/loss (it doesn't work)

Thank you

Indecision Candle IdentifierThis script helps identify indecision candles on for better entries into trade reversals. Note that I don't believe this signal/indicator should be used as a sole basis for entering/exiting a trade. This is simply to help you have an edge in terms of your chart/candle analysis when your brain fails to keep up with your trades.

Empirical Mode Decomposition Strategy Backtest The related article is copyrighted material from Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

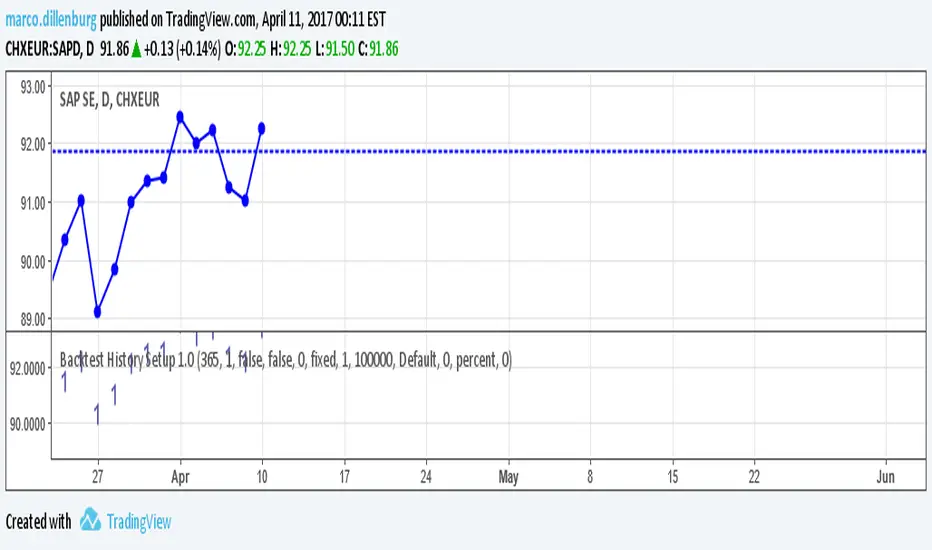

Backtest History Setup 1.0Script of strategy component to setup the backtext lookback. You setup the maximum days back in the history, which will be used for backtest.

Empirical Mode Decomposition Strategy The related article is copyrighted material from Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

FX Sniper: T3-CCI Strategy With Alerts This simple indicator gives you a lot of useful information - when to enter, when to exit

and how to reduce risks by entering a trade on a double confirmed signal.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

Added Alerts when signal changes.

Dynamo Strategy Backtest In July 1996 Futures magazine, E. Marshall Wall introduces the

Dynamic Momentum Oscillator (Dynamo). Please refer to this article

for interpretation.

The Dynamo oscillator is a normalizing function which adjusts the

values of a standard oscillator for trendiness by taking the difference

between the value of the oscillator and a moving average of the oscillator

and then subtracting that value from the oscillator midpoint.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading

Dynamo Strategy In July 1996 Futures magazine, E. Marshall Wall introduces the

Dynamic Momentum Oscillator (Dynamo). Please refer to this article

for interpretation.

The Dynamo oscillator is a normalizing function which adjusts the

values of a standard oscillator for trendiness by taking the difference

between the value of the oscillator and a moving average of the oscillator

and then subtracting that value from the oscillator midpoint.

DSS Bressert (Double Smoothed Stochastic) Strategy Backtest Double Smoothed Stochastics (DSS) is designed by William Blaw.

It attempts to combine moving average methods with oscillator principles.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

DSS Bressert (Double Smoothed Stochastic) Strategy Double Smoothed Stochastics (DSS) is designed by William Blaw.

It attempts to combine moving average methods with oscillator principles.

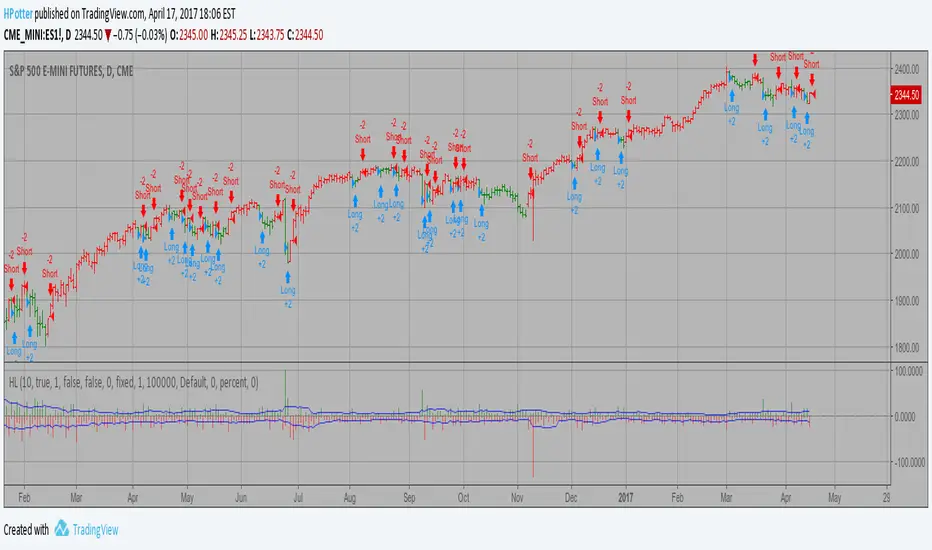

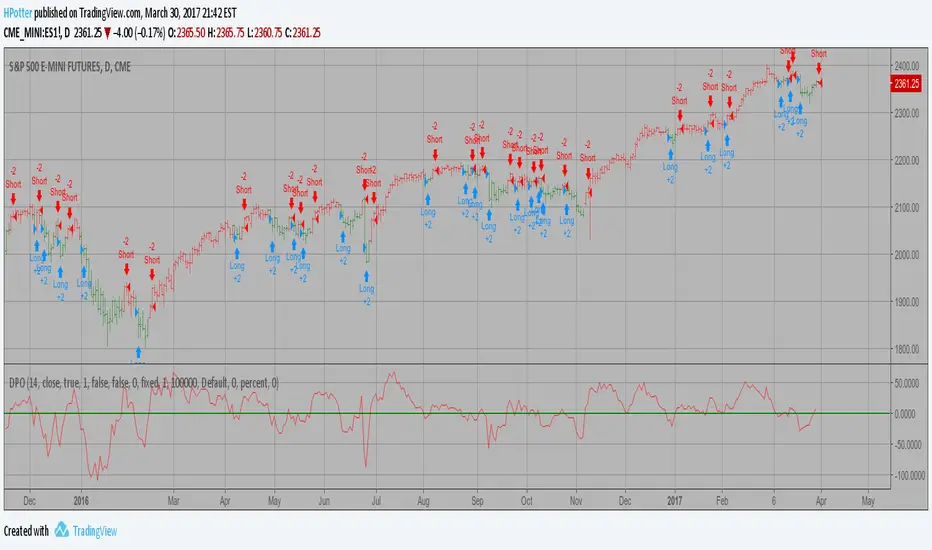

Detrended Price Oscillator Strategy Backtest The Detrend Price Osc indicator is similar to a moving average,

in that it filters out trends in prices to more easily identify

cycles. The indicator is an attempt to define cycles in a trend

by drawing a moving average as a horizontal straight line and

placing prices along the line according to their relation to a

moving average. It provides a means of identifying underlying

cycles not apparent when the moving average is viewed within a

price chart. Cycles of a longer duration than the Length (number

of bars used to calculate the Detrend Price Osc) are effectively

filtered or removed by the oscillator.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Detrended Price Oscillator Strategy The Detrend Price Osc indicator is similar to a moving average,

in that it filters out trends in prices to more easily identify

cycles. The indicator is an attempt to define cycles in a trend

by drawing a moving average as a horizontal straight line and

placing prices along the line according to their relation to a

moving average. It provides a means of identifying underlying

cycles not apparent when the moving average is viewed within a

price chart. Cycles of a longer duration than the Length (number

of bars used to calculate the Detrend Price Osc) are effectively

filtered or removed by the oscillator.