Liquidity Levels - PMH/PWH/PDH/HODWhat is it?

An indicator that tracks the main liquidity levels on TradingView, displaying the highs and lows of reference for month, week, previous day and current day.

What's it for?

It identifies price zones where there are many pending orders (liquidity). Traders use it to:

Find support and resistance points

Identify areas where price could bounce or break through

Receive alerts when price touches or breaks these levels

Which levels does it show?

LevelDescriptionColorLinePMH/PMLPrevious month's high and lowPurpleSolidPWH/PWLPrevious week's high and lowBlueSolidPDH/PDLPrevious day's high and lowOrangeSolidHOD/LODCurrent day's high and lowGrayDotted

How to use it?

Apply the indicator to your chart

Customize colors and enable/disable the levels you prefer

Set alerts to receive notifications when price touches or breaks levels

Use the levels to make trading decisions (entry, exit, stop loss)

Perfect for: Scalping, Day Trading, Swing Trading on any asset (forex, crypto, stocks)

حجم التداول

Asia Session High/Low 23:00-00:15This indicator shows highs and lows 1 hour before Asia session and the first 15min of Asia session.

VolumeAnlaysis### Volume Analysis (VA) Indicator

**Overview**

The Volume Analysis (VA) indicator is a dynamic overlay tool designed for traders seeking to identify high-volume breakouts, retests, and multi-timeframe volume-driven price cycles. By combining volume spikes with price action and support/resistance boxes, it highlights potential trend continuations, reversals, and cycle shifts. Ideal for intraday and swing trading on stocks, forex, or crypto, it uses a Fibonacci-inspired 1.618 multiplier to detect significant volume surges, then maps them to visual boxes and key levels for actionable insights.

This indicator draws from volume profile concepts but focuses on **breakout confirmation** and **cycle momentum**, helping you spot when "smart money" volume aligns with price extremes. It's particularly useful in volatile markets where volume precedes price moves.

**How It Works**

1. **Volume Break Detection**:

- Identifies a "Volume Break" when the current bar's volume exceeds 1.618x the highest volume from the prior 5 bars. This signals unusual activity, often preceding breakouts.

- A "Volume Retest" triggers exactly 3 bars after a break if volume has been falling steadily over those 3 bars—indicating a pullback for re-accumulation/distribution.

2. **Visual Annotations**:

- **Labels**: Green/red/yellow labels mark Volume Breaks and Retests, positioned above/below the bar based on candle direction for clarity.

- **Demand/Supply Boxes**:

- Blue semi-transparent boxes form around Retest bars, extending rightward to act as dynamic support/resistance.

- Green (bullish) or red (bearish) boxes draw from Volume Breaks, based on the original candle's open/close, highlighting potential zones for continuation.

- Limited to 5 boxes max to avoid chart clutter; older boxes fade as new ones form.

3. **Box Interaction Signals**:

- When price enters a box:

- **Reversal Hints**: Maroon (bearish rejection) or lime (bullish rejection) labels on closes against the trend with opening price momentum.

- **Breakout Arrows**: Up/down arrows on crossovers/crossunders of box tops/bottoms from Retest boxes.

- Scans all active boxes for interactions, prioritizing recent volume events.

4. **Multi-Timeframe Volume Cycles**:

- Aggregates the "Volume Break Max" level (a proxy for key price extremes tied to volume spikes) across timeframes: 1min, 5min, 10min, 30min, and 65min (using `request.security`).

- Computes **MaxVolBreak** (highest extreme) and **MinVolBreak** (lowest extreme) for trend-following levels.

- Tracks **Percent Volume Greater/Less Than Close**: Sums volumes from TFs where price is below/above these levels, creating a momentum ratio.

- **CrossClose**: Plots the prior close where this ratio crosses (gray line), signaling cycle shifts—bullish below MinVolBreak, bearish above MaxVolBreak.

- **Fills**: Red fill above CrossClose/MaxVolBreak (bearish cycle); green below CrossClose/MinVolBreak (bullish cycle).

5. **Plots**:

- Black lines for MaxVolBreak (⏫) and MinVolBreak (⏬).

- Gray 🔄 for CrossClose.

- Colors dynamically adjust (green/red) based on close relative to levels.

**Key Features**

- **Trend vs. Reversal Modes**: Toggle alerts for trend-following breaks (crosses of Max/MinVolBreak) or reversal signals (crosses of CrossClose).

- **Multi-TF Fusion**: Optionally include the chart's native timeframe in Max/Min calculations for finer tuning.

- **Box Management**: Auto-prunes to 5 boxes; focuses on retest/break alignments for "inside bar" logic.

- **Momentum Filters**: Uses rising/falling opens and crossovers for label precision, reducing noise.

- **Customizable**: Simple inputs for alert visibility and timeframe inclusion.

**Settings**

| Input | Default | Description |

|-------|---------|-------------|

| Show Volume Reversal Breaks | False | Enables alerts/labels for CrossClose crosses (cycle reversals). |

| Show Trend Following Breaks | True | Enables alerts for Max/MinVolBreak crosses (trend signals). |

| Use Current Time | False | Includes chart's native TF in multi-TF Max/Min calculations. |

**Alerts**

- **Reversal Alerts** (if enabled): "Volume Reverse Bullish/Bearish Break of " on close crosses of CrossClose.

- **Trend Alerts** (if enabled): "Trend Volume Bullish/Bearish Signal" on close crosses of Max/MinVolBreak; plus notes if prior low/high aligns with levels.

- All alerts include ticker and level value for easy scanning. Use `alert.freq_once_per_bar` to avoid spam.

**Trading Ideas**

- **Bullish Entry**: Green box formation + price holding MinVolBreak + upward arrow on retest box. Target next resistance.

- **Bearish Entry**: Red box + close above MaxVolBreak + red fill activation. Stop below recent low.

- **Cycle Trading**: Watch CrossClose crosses for regime shifts—fade extremes in overextended cycles.

- **Best Timeframes**: 5-30min for intraday; combine with daily for swings. Works best on liquid assets with reliable volume data.

**Limitations & Notes**

- Relies on accurate volume data (e.g., stocks/forex); less effective on low-volume or synthetic instruments.

- Boxes extend rightward but don't auto-delete—monitor for clutter on long histories (max_bars_back=500).

- Some logic (e.g., exact 3-bar retest) is rigid; backtest for your market.

- Open-source under MPL 2.0—fork and tweak as needed!

For questions or enhancements, drop a comment below. Happy trading! 🚀

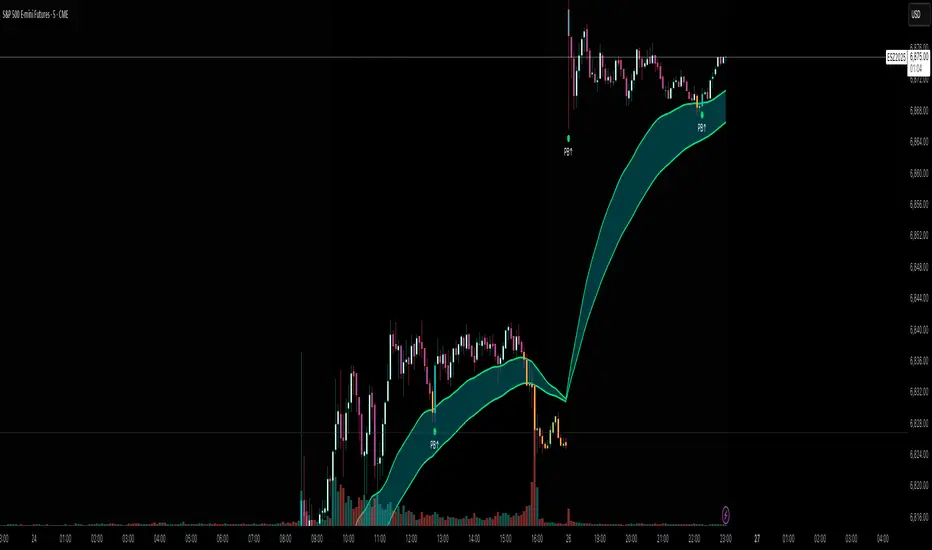

Flux AI PullBack System (Hybrid Pro)Flux AI PullBack System (Hybrid Pro)

//Session-Aware | Adaptive Confluence | Grace Confirm Logic//

Overview:

The Flux AI PullBack System (Hybrid Pro v5) is an adaptive, session-aware pullback indicator designed to identify high-probability continuation setups within trending markets. It automatically adjusts between “Classic” and “Enhanced” logic modes based on volatility, volume, and ATR slope, allowing it to perform seamlessly across different market sessions (Asian, London, and New York).

Core Features:

Hybrid Auto Mode — Dynamically switches between Classic (fast-moving) and Enhanced (strict) modes.

Session-Aware Context — Optimized for intraday trading in ES, NQ, and SPY.

Grace Confirmation Logic — Validates pullbacks with a follow-through condition to reduce noise.

Adaptive EMA Zone (38/62) — Highlights pullback areas with dynamic aqua fill and transparency linked to trend strength.

Noise Suppression Filter — Prevents false pullbacks during EMA crossovers or unstable transitions.

Weighted Confluence Model — Combines trend, ATR, volume, and swing structure for confirmation strength.

Pine v6 Compliant Alerts — Constant-string safe, ready for webhooks and automation.

Visual Elements:

Aqua EMA Zone: Displays the “breathing” pullback band (tightens during volatility spikes).

PB↑ / PB↓ Markers: Confirmed pullbacks with subtle transparency and fixed label size.

Bar Highlights: Yellow for pullbacks; ice-blue for confirmed continuation.

Use Cases

Perfect for:

Intraday trend traders

0DTE SPX / ES scalpers

Futures traders (NQ, MNQ, MES)

Algorithmic strategy builders using webhooks

Recommended Timeframes:

1–15 minute charts (scalping / intraday)

Higher timeframes for swing confirmations.

Attribution:

This open-source script was inspired by Chris Moody’s “CM Slingshot System” and JustUncleL’s Pullback Tools, but it was built from scratch using AI-assisted code refinement (ChatGPT).

All logic and enhancements are original, not derived from proprietary software.

License: MIT (Open Source)

© 2025 Ken Anderson — You may modify, use, or redistribute with credit.

Keywords:

Pullback, Reversal, AI Trading, EMA Zone, Session Aware, Futures Trading, SPX, ES, NQ, ATR Filter, Volume Confirmation, Flux System, Pine Script v6, Non-Repainting, Adaptive Trading Indicator.

Momentum Breakout Filter + ATR ZonesMomentum Breakout Filter + ATR Zones - User Guide

What This Indicator Does

This indicator helps you with your MACD + volume momentum strategy by:

Filtering out fake breakouts - Shows ⚠️ warnings when breakouts lack confirmation

Showing clear entry signals - 🚀 LONG and 🔻 SHORT labels when all conditions align

Automatic stop loss & profit targets - Based on ATR (Average True Range)

Visual trend confirmation - Background color + EMA alignment

Signal Types

🚀 LONG Entry Signal (Green Label)

Appears when ALL conditions met:

✅ MACD crosses above signal line

✅ Volume > 1.5× average

✅ Price > EMA 9 > EMA 21 > EMA 200 (bullish trend)

✅ Price closes above recent 20-bar high

🔻 SHORT Entry Signal (Red Label)

Appears when ALL conditions met:

✅ MACD crosses below signal line

✅ Volume > 1.5× average

✅ Price < EMA 9 < EMA 21 < EMA 200 (bearish trend)

✅ Price closes below recent 20-bar low

⚠️ FAKE Breakout Warning (Orange Label)

Appears when price breaks high/low BUT lacks confirmation:

❌ Low volume (below 1.5× average), OR

❌ Wick break only (didn't close through level), OR

❌ MACD not aligned with direction

Hover over the warning label to see what's missing!

ATR Stop Loss & Targets

When you get a signal, colored lines automatically appear:

Long Position

Red solid line = Stop Loss (Entry - 1.5×ATR)

Green dashed lines = Profit Targets:

Target 1: Entry + 2×ATR

Target 2: Entry + 3×ATR

Target 3: Entry + 4×ATR

Short Position

Red solid line = Stop Loss (Entry + 1.5×ATR)

Green dashed lines = Profit Targets:

Target 1: Entry - 2×ATR

Target 2: Entry - 3×ATR

Target 3: Entry - 4×ATR

The lines move with each bar until you exit the position.

Chart Elements

Moving Averages

Blue line = EMA 9 (fast)

Orange line = EMA 21 (medium)

White line = EMA 200 (trend filter)

Volume

Yellow bars = High volume (above threshold)

Gray bars = Normal volume

Background Color

Light green = Bullish trend (all EMAs aligned up)

Light red = Bearish trend (all EMAs aligned down)

No color = Neutral/mixed

MACD (Bottom Pane)

Green/Red columns = MACD Histogram

Blue line = MACD Line

Orange line = Signal Line

Info Dashboard (Bottom Right)

ItemWhat It ShowsVolumeCurrent volume vs average (✓ HIGH or ✗ Low)MACDDirection (BULLISH or BEARISH)TrendEMA alignment (BULL, BEAR, or NEUTRAL)ATRCurrent ATR value in dollarsPositionCurrent position (LONG, SHORT, or NONE)R:RRisk-to-Reward ratio (shows when in position)

How To Use It

Basic Workflow

Wait for setup

Watch for MACD to approach signal line

Volume should be building

Price should be near EMA structure

Get confirmation

Wait for 🚀 LONG or 🔻 SHORT label

Check dashboard shows "✓ HIGH" volume

Verify trend is aligned (green or red background)

Enter the trade

Enter when signal appears

Note your stop loss (red line)

Note your targets (green dashed lines)

Manage the trade

Exit at first target for partial profit

Move stop to breakeven

Trail remaining position

What To Avoid

❌ Don't trade when you see:

⚠️ FAKE labels (wait for confirmation)

Neutral background (no clear trend)

"✗ Low" volume in dashboard

MACD and Trend not aligned

Settings You Can Adjust

Volume Sensitivity

High Volume Threshold: Default 1.5×

Increase to 2.0× for cleaner signals (fewer trades)

Decrease to 1.2× for more signals (more trades)

Fake Breakout Filters

You can toggle these ON/OFF:

Volume Confirmation: Requires high volume

Close Through: Requires candle close, not just wick

MACD Alignment: Requires MACD direction match

Tip: Turn all three ON for highest quality signals

ATR Stop/Target Multipliers

Default settings (conservative):

Stop Loss: 1.5×ATR

Target 1: 2×ATR (1.33:1 R:R)

Target 2: 3×ATR (2:1 R:R)

Target 3: 4×ATR (2.67:1 R:R)

Aggressive traders might use:

Stop Loss: 1.0×ATR

Target 1: 2×ATR (2:1 R:R)

Target 2: 4×ATR (4:1 R:R)

Conservative traders might use:

Stop Loss: 2.0×ATR

Target 1: 3×ATR (1.5:1 R:R)

Target 2: 5×ATR (2.5:1 R:R)

Example Trade Scenarios

Scenario 1: Perfect Long Setup ✅

Stock consolidating near EMA 21

MACD curling up toward signal line

Volume bar turns yellow (high volume)

🚀 LONG label appears

Red stop line and green target lines appear

Result: High probability trade

Scenario 2: Fake Breakout Avoided ✅

Price breaks above resistance

Volume is normal (gray bar)

⚠️ FAKE label appears (hover shows "Low volume")

No entry signal

Price falls back below breakout level

Result: Avoided losing trade

Scenario 3: Premature Entry ❌

MACD crosses up

Volume is high

BUT trend is NEUTRAL (no background color)

No signal appears (trend filter blocks it)

Result: Avoided choppy/sideways market

Quick Reference

Entry Checklist

🚀 or 🔻 label on chart

Dashboard shows "✓ HIGH" volume

Dashboard shows aligned MACD + Trend

Colored background (green or red)

ATR lines visible

No ⚠️ FAKE warning

Exit Strategy

Target 1 (2×ATR): Take 50% profit, move stop to breakeven

Target 2 (3×ATR): Take 25% profit, trail stop

Target 3 (4×ATR): Take remaining profit or trail aggressively

Stop Loss: Exit entire position if hit

Alerts

Set up these alerts:

Long Entry: Fires when 🚀 LONG signal appears

Short Entry: Fires when 🔻 SHORT signal appears

Fake Breakout Warning: Fires when ⚠️ appears (optional)

Tips for Success

Use on 5-minute charts for day trading momentum plays

Only trade high volume stocks ($5-20 range works best)

Wait for full confirmation - don't jump early

Respect the stop loss - it's calculated based on volatility

Scale out at targets - don't hold for home runs

Avoid trading first 15 minutes - let market settle

Best during 10am-11am and 2pm-3pm - peak momentum times

Common Questions

Q: Why didn't I get a signal even though MACD crossed?

A: All conditions must be met - check dashboard for what's missing (likely volume or trend alignment)

Q: Can I use this on any timeframe?

A: Yes, but it's designed for 5-15 minute charts. On daily charts, adjust ATR multipliers higher.

Q: The stop loss seems too tight, can I widen it?

A: Yes, increase "Stop Loss (×ATR)" from 1.5 to 2.0 or 2.5 in settings.

Q: I keep seeing FAKE warnings but price keeps going - what gives?

A: The filter is conservative. You can disable some filters in settings, but expect more false signals.

Q: Can I use this for swing trading?

A: Yes, but use larger timeframes (1H or 4H) and adjust ATR multipliers up (3× for stops, 6-9× for targets).

Volume Surge by MashrabThe "Volume Surge" indicator is like a simple market health checkup. It looks at how much of an asset (like a stock or crypto) is being traded right now and compares it to the recent past. Think of it as a way to quickly see if interest in that asset is suddenly spiking, fading, or staying the same.

The indicator shows this information in an easy-to-read table right on your chart.

How it works:

The indicator keeps track of two main things for you:

Current Volume: The total trading volume over the last "N" days (or whatever time period you choose).

Previous Volume: The total trading volume over the period right before that

Then, it gives you a summary:

The "Ratio" tells you how many times bigger or smaller the current volume is.

The "Percent Change" shows the percentage jump in volume.

How to use it:

This indicator helps you see when something interesting might be happening. Here are a few ways traders use it:

Confirm Breakouts: If a stock breaks above a key price level and the indicator shows a huge volume surge, it’s a stronger signal that the move is real and not a false alarm.

Spot Reversals: If a stock has been trending up but the volume starts to drop off, it could mean the trend is losing steam. A sudden, massive volume surge on a down day might indicate panic selling, which can sometimes happen right before the price turns around.

Check Trend Strength: A healthy trend usually has increasing volume going in the same direction. For example, if a stock is in an uptrend, you want to see lots of volume on the days it goes up.

This indicator isn't a crystal ball, but it's a great tool for understanding the "who" and "how much" behind a price move. It helps you see when a price change is backed by a lot of market activity, which often makes the move more trustworthy.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

Volume + MA5 & MA10This Volume + MA5 & MA10 (Technical Volume Trend Analysis)

The Volume + MA5 & MA10 indicator provides a precise view of market participation and volume momentum by combining raw volume data with two moving averages (MA5 and MA10). It’s designed for traders who rely on volume-based confirmation to validate price movements, breakouts, and trend reversals.

🔍 Overview

This indicator displays volume bars alongside two smooth volume averages — MA5 (short-term) and MA10 (medium-term) — making it easier to detect shifts in market activity.

When the short-term average crosses above or below the long-term average, it signals a potential change in trading intensity or market sentiment.

⚙️ Key Features

Dual Volume Moving Averages (MA5 & MA10) for short- and medium-term analysis.

Dynamic Bar Coloring based on whether current volume exceeds MA5 or MA10.

Crossover Detection with visual markers for MA5/MA10 intersections.

Alert Conditions to notify you of significant volume trend shifts.

Fully customizable appearance and smoothing options.

📊 How to Interpret

MA5 > MA10 → Increasing short-term volume activity (strengthening momentum).

MA5 < MA10 → Decreasing short-term volume (weakening participation).

Rising volume with price → Confirms trend strength.

Falling volume with rising/falling price → Suggests potential reversal or reduced conviction.

💡 Applications

Confirm breakouts and trend continuations.

Identify momentum divergences between price and volume.

Filter out low-volume or weak-trend setups.

Combine with RSI, MACD, or moving averages for enhanced signal validation.

✅ Advantages

Simple yet powerful structure for clean visual analysis.

Works across all timeframes and markets (crypto, stocks, forex, indices).

No repainting — reliable for both live and historical backtesting.

Use Volume + MA5 & MA10 to strengthen your technical analysis and gain a deeper understanding of how market participation drives price trends.

Simple VWAP + BandsSimple VWAP + Bands

A clean and customizable VWAP (Volume Weighted Average Price) indicator with standard deviation bands and RTH (Regular Trading Hours) session support.

Features:

- VWAP Line: Volume-weighted average price calculation

- Three Standard Deviation Bands: Configurable bands at 1σ, 2σ, and 3σ levels (above and below VWAP)

- RTH Session Support: Option to calculate VWAP only during regular trading hours

- Customizable Session Times: Configure your own trading session hours and timezone

- Clean Visualization: Line breaks between sessions prevent messy connections across non-trading periods

- Toggle Bands: Show/hide individual standard deviation bands as needed

Use Cases:

- Identify overbought/oversold conditions relative to volume-weighted price

- Track price deviation from VWAP during trading sessions

- Support and resistance levels based on standard deviations

- Mean reversion trading strategies

Kalman VWAP Filter [BackQuant]Kalman VWAP Filter

A precision-engineered price estimator that fuses Kalman filtering with the Volume-Weighted Average Price (VWAP) to create a smooth, adaptive representation of fair value. This hybrid model intelligently balances responsiveness and stability, tracking trend shifts with minimal noise while maintaining a statistically grounded link to volume distribution.

If you would like to see my original Kalman Filter, please find it here:

Concept overview

The Kalman VWAP Filter is built on two core ideas from quantitative finance and control theory:

Kalman filtering — a recursive Bayesian estimator used to infer the true underlying state of a noisy system (in this case, fair price).

VWAP anchoring — a dynamic reference that weights price by traded volume, representing where the majority of transactions have occurred.

By merging these concepts, the filter produces a line that behaves like a "smart moving average": smooth when noise is high, fast when markets trend, and self-adjusting based on both market structure and user-defined noise parameters.

How it works

Measurement blend : Combines the chosen Price Source (e.g., close or hlc3) with either a Session VWAP or a Rolling VWAP baseline. The VWAP Weight input controls how much the filter trusts traded volume versus price movement.

Kalman recursion : Each bar updates an internal "state estimate" using the Kalman gain, which determines how much to trust new observations vs. the prior state.

Noise parameters :

Process Noise controls agility — higher values make the filter more responsive but also more volatile.

Measurement Noise controls smoothness — higher values make it steadier but slower to adapt.

Filter order (N) : Defines how many parallel state estimates are used. Larger orders yield smoother output by layering multiple one-dimensional Kalman passes.

Final output : A refined price trajectory that captures VWAP-adjusted fair value while dynamically adjusting to real-time volatility and order flow.

Why this matters

Most smoothing techniques (EMA, SMA, Hull) trade off lag for smoothness. Kalman filtering, however, adaptively rebalances that tradeoff each bar using probabilistic weighting, allowing it to follow market state changes more efficiently. Anchoring it to VWAP integrates microstructure context — capturing where liquidity truly lies rather than only where price moves.

Use cases

Trend tracking : Color-coded candle painting highlights shifts in slope direction, revealing early trend transitions.

Fair value mapping : The line represents a continuously updated equilibrium price between raw price action and VWAP flow.

Adaptive moving average replacement : Outperforms static MAs in variable volatility regimes by self-adjusting smoothness.

Execution & reversion logic : When price diverges from the Kalman VWAP, it may indicate short-term imbalance or overextension relative to volume-adjusted fair value.

Cross-signal framework : Use with standard VWAP or other filters to identify convergence or divergence between liquidity-weighted and state-estimated prices.

Parameter guidance

Process Noise : 0.01–0.05 for swing traders, 0.1–0.2 for intraday scalping.

Measurement Noise : 2–5 for normal use, 8+ for very smooth tracking.

VWAP Weight : 0.2–0.4 balances both price and VWAP influence; 1.0 locks output directly to VWAP dynamics.

Filter Order (N) : 3–5 for reactive short-term filters; 8–10 for smoother institutional-style baselines.

Interpretation

When price > Kalman VWAP and slope is positive → bullish pressure; buyers dominate above fair value.

When price < Kalman VWAP and slope is negative → bearish pressure; sellers dominate below fair value.

Convergence of price and Kalman VWAP often signals equilibrium; strong divergence suggests imbalance.

Crosses between Kalman VWAP and the base VWAP can hint at shifts in short-term vs. long-term liquidity control.

Summary

The Kalman VWAP Filter blends statistical estimation with market microstructure awareness, offering a refined alternative to static smoothing indicators. It adapts in real time to volatility and order flow, helping traders visualize balance, transition, and momentum through a lens of probabilistic fair value rather than simple price averaging.

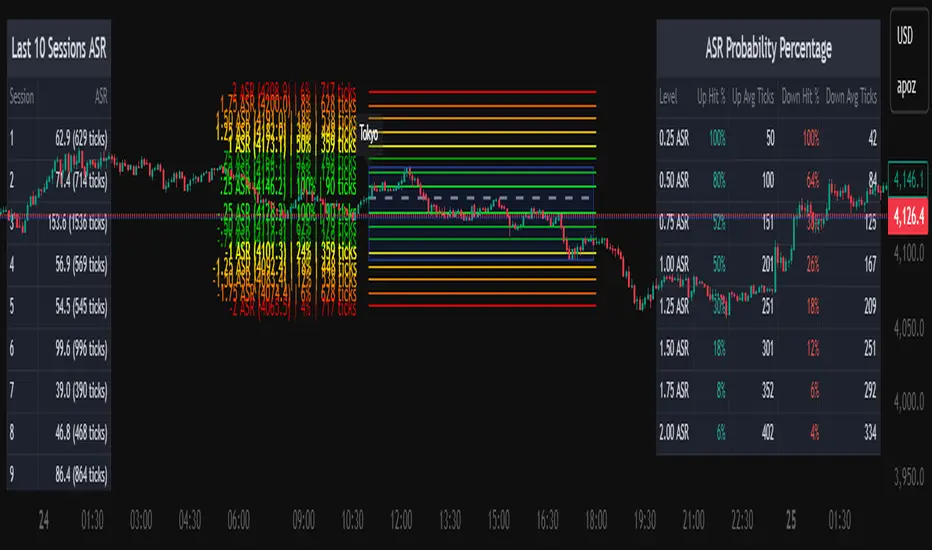

Average Daily Session Range PRO [Capitalize Labs]Average Daily Session Range PRO

The Average Daily Session Range PRO (ADSR PRO) is a professional-grade analytical tool designed to quantify and visualize the probabilistic range behavior of intraday sessions.

It calculates directional range statistics using historical session data to show how far price typically moves up or down from the session open.

This helps traders understand session volatility profiles, range asymmetry, and probabilistic extensions relative to prior performance.

Key Features

Asymmetric Range Modeling: Separately tracks average upside and downside excursions from each session open, revealing directional bias and volatility imbalance.

Probability Engine Modes: Choose between Rolling Window (fixed-length lookback) and Exponential Decay (weighted historical memory) to control how recent or historic data influences probabilities.

Session-Aware Statistics: Calculates values independently for each defined session, allowing region-specific insights (e.g., Tokyo, London, New York).

Dynamic Range Table: Displays key metrics such as average up/down ticks, expected range extensions, and percentage probabilities.

Adaptive Display: Works across timeframes and instruments, automatically aligning with user-defined session start and end times.

Visual Clarity: Includes clean range markers and labels optimized for both backtesting and live-chart analysis.

Intended Use

ADSR PRO is a statistical reference indicator.

It does not generate buy/sell signals or predictive forecasts.

Its purpose is to help users observe historical session behavior and volatility tendencies to support their own discretionary analysis.

Credits

Developed by Capitalize Labs, specialists in quantitative and discretionary market research tools.

Risk Warning

This material is educational research only and does not constitute financial advice, investment recommendation, or a solicitation to buy or sell any instrument.

Foreign exchange and CFDs are complex, leveraged products that carry a high risk of rapid losses; leverage amplifies both gains and losses, and you should not trade with funds you cannot afford to lose.

Market conditions can change without notice, and news or illiquidity may cause gaps and slippage; stop-loss orders are not guaranteed.

The analysis presented does not take into account your objectives, financial situation, or risk tolerance.

Before acting, assess suitability in light of your circumstances and consider seeking advice from a licensed professional.

Past performance and back-tested or hypothetical scenarios are not reliable indicators of future results, and no outcome or level mentioned here is assured.

You are solely responsible for all trading decisions, including position sizing and risk management.

No external links, promotions, or contact details are provided, in line with TradingView House Rules.

Fabio + Waqar SMC AlertThis script is a custom TradingView indicator designed to combine elements of a trend‑following VWAP approach (inspired by the “Fabio” strategy) with a smart‑money‑concepts framework (inspired by Waqar Asim). Here’s what it does:

* **Directional bias:** It calculates a 15‑minute VWAP and compares the current 15‑minute close to it. When price is above the 15‑minute VWAP, the script assumes a long bias; when below, a short bias. This reflects the trend‑following aspect of the Fabio strategy.

* **Liquidity sweeps:** Using recent pivot highs and lows on the current timeframe, it identifies when price takes out a recent high (for potential longs) or low (for potential shorts). This represents a “liquidity sweep” — a fake breakout that collects stops and signals a possible reversal or continuation.

* **Break of structure (BOS):** After a sweep, the script confirms that price is breaking away from the swept level (i.e., higher than recent highs for longs or lower than recent lows for shorts). This BOS confirmation helps avoid false signals.

* **Entry filters:** For a long setup, the bias must be long, there must be a liquidity sweep followed by a BOS, and price must reclaim the current‑timeframe VWAP. For a short setup, the opposite conditions apply (short bias, sweep + BOS to the downside, and price rejecting the VWAP).

* **Alerts and plot:** It provides two alert conditions (“Fabio‑Waqar Long Setup” and “Fabio‑Waqar Short Setup”) that you can attach to notifications. It also plots the intraday VWAP on your chart for visual reference.

In short, this script watches for a confluence of trend direction, liquidity sweeps, structural shifts, and VWAP reclaim/rejection, and then notifies you when those conditions align. You can use it as an alerting tool to identify high‑probability setups based on these combined strategies.

BankNifty Etharia Aggresive Buyer / SellerOverview

Professional intraday trading strategy for BankNifty Futures that identifies high-probability setups by combining multiple technical indicators. Works in BOTH directions - LONG and SHORT.

Best Timeframe: 5-Minute Chart

Key Features:

✅ Multi-Confluence Entry System - All indicators must align for signal

✅ Bidirectional Trading - Captures both uptrends and downtrends

✅ Advanced Risk Management - Daily loss limits, consecutive loss protection

✅ Smart Exit System - Partial profit taking + trailing stops

✅ Session-Based Trading - Avoids opening and closing volatility

Entry Logic:

LONG Signals:

Price above Kernel Regression (trend confirmation)

Price above VWAP with positive slope (momentum)

Cumulative Volume Delta bullish (buying pressure)

Volume spike or increasing volume (strength confirmation)

Strong bullish candle with 60%+ body ratio

RSI filter to avoid overbought entries

SHORT Signals:

Price below Kernel Regression (downtrend confirmation)

Price below VWAP with negative slope (bearish momentum)

CVD bearish (selling pressure dominates)

High volume confirmation

Strong bearish candle pattern

RSI filter to avoid oversold entries

Exit Management:

🎯 Target 1: 1.5 R:R (50% position exit)

🎯 Target 2: 2.5 R:R (full exit)

🛡️ Stop Loss Options: ATR-based, Swing-based, or Fixed

🟡 Trailing Stop: Activates after 1.2 R:R, trails at 0.8 R:R

⏰ Time-Based Exit: Closes all positions 5 mins before session end

Risk Controls:

Maximum trades per day (default: 5)

Consecutive loss limit (default: 2)

Daily loss limit: 2.5% of capital

Daily profit target: 5% (stops trading when reached)

Position sizing based on account risk percentage

Recommended Settings:

Asset: BankNifty Futures (NSE:BANKNIFTY1!)

Timeframe: 5-minute

Initial Capital: ₹1,00,000

Risk per trade: 1%

Commission: 0.05%

Slippage: 5 points

Performance Expectations:

Win Rate: 55-65%

Profit Factor: 1.5-2.0

Average Trades/Day: 3-8

Risk:Reward: 1:1.8 average

Customizable Parameters:

Trading direction (Long Only / Short Only / Both)

Indicator lengths and thresholds

Stop loss type and targets

Risk management limits

Trading session hours

Best For:

Intraday traders seeking systematic, rule-based entries with strong confluence, proper risk management, and the ability to profit from both bullish and bearish market conditions.

VWAP Composites📊 VWAP Composite - Advanced Multi-Period Volume Weighted Average Price Indicator

═══════════════════════════════════════════════════════════════════

🎯 OVERVIEW

VWAP Composite is an advanced volume-weighted average price (VWAP) indicator that goes beyond traditional single-period VWAP calculations by offering composite multi-period analysis and unprecedented customization. This indicator solves a common problem traders face: traditional VWAP resets at arbitrary intervals (session start, day, week), but significant price action and volume accumulation often spans multiple periods. VWAP Composite allows you to anchor VWAP calculations to any timeframe—or combine multiple periods into a single composite VWAP—giving you a true representation of average price weighted by volume across the exact periods that matter to your analysis.

═══════════════════════════════════════════════════════════════════

⚙️ HOW IT WORKS - CALCULATION METHODOLOGY

📌 CORE VWAP CALCULATION

The indicator calculates VWAP using the standard volume-weighted formula:

• Typical Price = (High + Low + Close) / 3

• VWAP = Σ(Typical Price × Volume) / Σ(Volume)

This calculation is performed across user-defined time periods, ensuring each bar's contribution to the average is proportional to its trading volume.

📌 STANDARD DEVIATION BANDS

The indicator calculates volume-weighted standard deviation to measure price dispersion around the VWAP:

• Variance = Σ / Σ(Volume)

• Standard Deviation = √Variance

• Upper Band = VWAP + (StdDev × Multiplier)

• Lower Band = VWAP - (StdDev × Multiplier)

These bands help identify overbought/oversold conditions relative to the volume-weighted mean, with high-volume price excursions having greater impact on band width than low-volume moves.

📌 COMPOSITE PERIOD METHODOLOGY (Auto Mode)

Unlike traditional VWAP that resets at fixed intervals, Auto Mode creates composite VWAPs by combining the current period with N previous periods:

• Period Span = 1: Current period only (standard VWAP behavior)

• Period Span = 2: Current period + 1 previous period combined

• Period Span = 3: Current period + 2 previous periods combined

• And so on...

Example: A 3-period Weekly composite VWAP calculates from the start of 2 weeks ago through the current week's end, creating a single VWAP that represents 21 days of continuous price and volume data. This provides context about where price stands relative to the volume-weighted average over multiple weeks, not just the current week.

═══════════════════════════════════════════════════════════════════

🔧 KEY FEATURES & ORIGINALITY

✅ DUAL OPERATING MODES

1️⃣ MANUAL MODE (5 Independent VWAPs)

Define up to 5 separate VWAP calculations with custom start/end times:

• Perfect for anchoring VWAP to specific events (earnings, Fed announcements, major reversals)

• Each VWAP has independent color settings for lines and deviation band backgrounds

• Individual control over calculation extension and visual extension (explained below)

• Useful for tracking multiple institutional accumulation/distribution zones simultaneously

2️⃣ AUTO MODE (Composite Period VWAP)

Automatically calculates VWAP across combined time periods:

• Supported periods: Daily, Weekly, Monthly, Quarterly, Yearly

• Configurable period span (1-20 periods)

• Always up-to-date, recalculates on each new bar

• Ideal for systematic analysis across consistent timeframes

✅ DUAL EXTENSION SYSTEM (Manual Mode Innovation)

Most VWAP indicators only offer "on/off" for extending calculations. This indicator provides two distinct extension options:

🔹 EXTEND CALCULATION TO CURRENT BAR

When enabled, continues including new bars in the VWAP calculation after the defined end time. The VWAP value updates dynamically as new volume enters the market.

Use case: You anchored VWAP to a major low 3 weeks ago. You want the VWAP to continue evolving with new volume data to track ongoing institutional positioning.

🔹 EXTEND VISUAL LINE ONLY

When enabled (and calculation extension is disabled), projects the "frozen" VWAP value forward as a reference line. The VWAP value remains fixed at what it was at the end time, but the line and deviation bands visually extend to current price.

Use case: You want to see how price is behaving relative to the VWAP that existed at a specific point in time (e.g., "Where is price now vs. the 5-day VWAP that existed at last Friday's close?").

This dual system gives you unprecedented control over whether you're tracking a "living" VWAP that incorporates new data or using historical VWAP levels as static reference points.

✅ CUSTOMIZABLE STANDARD DEVIATION BANDS

• Adjustable multiplier (0.1 to 5.0)

• Independent background colors with opacity control for each VWAP

• Dashed band lines for easy visual distinction from main VWAP

• Bands extend when visual extension is enabled, maintaining zone visibility

✅ COMPREHENSIVE LABELING SYSTEM

Each VWAP displays:

• Current VWAP value

• Upper deviation band value (High)

• Lower deviation band value (Low)

• Extension status indicator (Calc Extended / Visual Extended)

• Color-coded for quick identification

═══════════════════════════════════════════════════════════════════

📖 HOW TO USE THIS INDICATOR

🎯 SCENARIO 1: EVENT-ANCHORED VWAP (Manual Mode)

Use case: A stock gaps down 15% on earnings and you want to track where institutions are positioning during the recovery.

Setup:

1. Switch to Manual Mode

2. Enable VWAP 1

3. Set Start Time to the earnings gap bar

4. Set End Time to current time (or leave far in future)

5. Enable "Extend Calculation to Current Bar"

6. Watch how price respects the VWAP as a dynamic support/resistance

Interpretation:

• Price above VWAP = buyers in control since the event

• Price testing VWAP from above = potential support

• Volume-weighted standard deviation bands show normal price range

• Price outside bands = potential exhaustion/mean reversion setup

🎯 SCENARIO 2: MULTI-WEEK INSTITUTIONAL ACCUMULATION ZONE (Auto Mode)

Use case: You trade swing setups and want to identify where institutions have been accumulating over the past 3 weeks.

Setup:

1. Switch to Auto Mode

2. Select "Weekly" period type

3. Set Period Span to 3

4. Enable standard deviation bands

Interpretation:

• 3-week composite VWAP shows the true average institutional entry

• Price bouncing off VWAP repeatedly = strong support (institutions defending their average)

• Price breaking below VWAP on high volume = potential distribution

• Deviation bands contracting = consolidation; expanding = volatility increase

🎯 SCENARIO 3: COMPARING MULTIPLE TIME HORIZONS (Manual Mode)

Use case: You want to see short-term vs medium-term vs long-term VWAP alignments.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Last 5 trading days (blue)

3. VWAP 2: Last 10 trading days (orange)

4. VWAP 3: Last 20 trading days (purple)

5. Enable "Extend Calculation" for all

6. Set different background colors for visual separation

Interpretation:

• All VWAPs aligned upward = strong trend across all timeframes

• Price between VWAPs = finding equilibrium between different trader timeframes

• Short-term VWAP crossing long-term VWAP = momentum shift

• Price rejecting at higher-timeframe VWAP = that timeframe's traders defending their average

🎯 SCENARIO 4: HISTORICAL VWAP REFERENCE LEVELS (Manual Mode)

Use case: You want to see where the 1-month VWAP was at each month-end as static reference levels.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Set to last month's start/end dates

3. VWAP 2: Set to 2 months ago start/end dates

4. VWAP 3: Set to 3 months ago start/end dates

5. Disable "Extend Calculation"

6. Enable "Extend Visual Line Only"

Interpretation:

• Each VWAP represents the volume-weighted average for that complete month

• These become static support/resistance levels

• Price returning to old monthly VWAPs = institutional memory/gap fill behavior

• Useful for identifying longer-term value areas

═══════════════════════════════════════════════════════════════════

🎨 CUSTOMIZATION OPTIONS

GENERAL SETTINGS

• Show/hide labels

• Line style: Solid, Dashed, or Dotted

• Standard deviation multiplier (impacts band width)

• Toggle standard deviation bands on/off

MANUAL MODE (Per VWAP)

• Custom start and end times

• Line color picker

• Background color picker (with transparency control)

• Extend calculation option

• Extend visual option

• Show/hide individual VWAPs

AUTO MODE

• Period type selection (Daily/Weekly/Monthly/Quarterly/Yearly)

• Period span (1-20 periods)

• Line color

• Background color (with transparency control)

═══════════════════════════════════════════════════════════════════

💡 TRADING APPLICATIONS

✓ Mean Reversion: Use deviation bands to identify stretched prices likely to return to VWAP

✓ Trend Confirmation: Price sustained above VWAP = bullish bias; below = bearish bias

✓ Support/Resistance: VWAP often acts as dynamic S/R, especially on higher volume periods

✓ Institutional Positioning: Multi-day/week VWAPs show where large players have established positions

✓ Entry Timing: Wait for pullbacks to VWAP in trending markets

✓ Stop Placement: Use VWAP ± standard deviation as volatility-adjusted stop levels

✓ Breakout Confirmation: Breakouts from consolidation with price reclaiming VWAP = stronger signal

✓ Multi-Timeframe Analysis: Compare short vs long-period VWAPs to gauge momentum alignment

═══════════════════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

• The indicator redraws on each bar to maintain accurate visual representation (uses `barstate.islast`)

• Maximum lookback is limited to 5000 bars for performance optimization

• Time range calculations work across all timeframes but are most effective on intraday to daily charts

• Standard deviation bands assume volume-weighted distribution; extreme events may violate assumptions

• Auto mode always calculates to current bar; use Manual mode for fixed historical periods

═══════════════════════════════════════════════════════════════════

This indicator is open-source. Feel free to examine the code, learn from it, and adapt it to your needs.

Velocity Pressure Index | AlphaNattVelocity Pressure Index (VPI) | AlphaNatt

A sophisticated momentum oscillator that combines price velocity analysis with volume pressure dynamics to identify high-probability trading opportunities.

📊 KEY FEATURES

Dual Analysis System: Merges price velocity measurement with volume pressure analysis for comprehensive market momentum assessment

Dynamic Normalization: Automatically scales values between -100 and +100 for consistent readings across all market conditions

Adaptive Zones: Self-adjusting overbought/oversold levels based on recent price history

Multi-Layer Confirmation: Combines momentum, acceleration, and crossover signals for robust trade identification

Volume-Weighted Pressure: Differentiates between bullish and bearish volume to gauge true market sentiment

📈 HOW IT WORKS

The VPI calculates price velocity using linear regression of price changes, then weights this velocity by the difference between bullish and bearish volume pressure. This creates a momentum reading that accounts for both price movement speed and the volume conviction behind it.

Signal Generation:

Price velocity is measured over the specified period

Volume is separated into bullish (close > open) and bearish (close < open) pressure

Velocity is amplified or dampened based on volume pressure differential

The resulting index is normalized to oscillate between -100 and +100

A signal line smooths the oscillator for crossover detection

🎯 TRADING SIGNALS

Long Signals (Cyan #00F1FF):

Strong Bull: VPI > Signal with positive momentum and acceleration

Crossover Bull: VPI crosses above signal while above oversold zone

Divergence: Price makes lower low while VPI makes higher low

Short Signals (Magenta #FF019A):

Strong Bear: VPI < Signal with negative momentum and deceleration

Crossover Bear: VPI crosses below signal while below overbought zone

Divergence: Price makes higher high while VPI makes lower high

⚙️ CUSTOMIZABLE PARAMETERS

Velocity Settings:

Velocity Period (14): Lookback for price velocity calculation

Pressure Period (21): Volume analysis window

Smoothing Factor (3): Final oscillator smoothing

Signal Configuration:

Signal Type: Choose between SMA, EMA, or DEMA

Signal Length (9): Signal line smoothing period

Normalization Period (50): Range calculation window

Dynamic Zones:

Zone Lookback (100): Period for adaptive overbought/oversold calculation

Percentiles: 80th/20th percentiles for dynamic zones

📐 VISUAL COMPONENTS

Main Oscillator: Color-coded line showing current momentum state

Signal Line: White line for crossover detection

Momentum Histogram: Shows velocity differential at 50% scale

Dynamic Zones: Self-adjusting overbought/oversold bands

Extreme Levels: ±50 dotted lines marking extreme conditions

Background Shading: Subtle highlighting of overbought/oversold regions

💡 USAGE TIPS

Trend Trading: Use strong bull/bear signals in trending markets for continuation entries

Range Trading: Focus on crossovers near extreme zones for reversal trades

Divergence Trading: Watch for price/oscillator divergences at market extremes

Multi-Timeframe: Combine with higher timeframe VPI for directional bias

Volume Confirmation: Stronger signals occur with aligned volume pressure

⚠️ BEST PRACTICES

The VPI works best in liquid markets with reliable volume data. For optimal results, combine with price action analysis and use appropriate risk management. The indicator is most effective during trending conditions but can identify reversals when divergences occur at extremes.

🔔 ALERTS AVAILABLE

VPI Long/Short Signals

Bullish/Bearish Crossovers

Extreme Overbought/Oversold Conditions

Version 6 | Pine Script™ | © AlphaNatt

Cumulative Volume Delta Divergence Periodic EMACumulative Volume Delta Divergence Periodic EMA

extended indicator

WAD : Whale Activity Detector🐋 WAD: Whale Activity Detector

WAD (Whale Activity Detector) automatically detects periods of abnormally high trading volume compared to the average, identifying potential whale (institutional) buy or sell activity and visualizing it directly on the chart.

🔍 How It Works

1. Buy/Sell Volume Separation

Each candle’s trading volume is categorized based on its direction:

Bullish candle → Buy volume

Bearish candle → Sell volume

This separation helps distinguish the actual strength of buying vs. selling pressure, rather than looking at total volume alone.

2. Average Volume Calculation

Over a user-defined lookback period (default: 34 bars), the indicator calculates the moving average of both buy and sell volumes, establishing a baseline for what constitutes “normal” activity.

3. Whale Activity Detection

When the current volume exceeds n times the average volume (default: 4×), the indicator flags it as a Whale Zone — a potential sign of large player involvement.

Volume surge on a bullish candle → Whale Buy

Volume surge on a bearish candle → Whale Sell

4. Visual Display

🟢 Green bars: Whale buy activity

🔴 Red bars: Whale sell activity

BUY/SELL labels: Appear above the chart when an anomaly is detected

Average line toggle: Users can turn the average volume lines on or off for clarity

5. Alerts

Whenever whale buy/sell signals are detected, real-time alerts are triggered.

Example: 🐋 Whale Buy – NVDA! 🟢

⚙️ Indicator Meaning

Rather than showing raw volume, WAD tracks “abnormal volume relative to the average.”

It filters out noise and highlights the moments where large entities begin to move.

Essentially, it visualizes intentional and impactful trades hidden within standard volume activity.

🚀 Example Use Cases

Whale accumulation tracking – Repeated strong buy signals may indicate sustained institutional accumulation.

Short-term breakout confirmation – Price often rallies shortly after whale buy signals appear.

Support/resistance analysis – Whale sell zones frequently align with short-term resistance areas.

In short:

WAD identifies when trading volume exceeds its historical norm to highlight where big money enters or exits the market.

===============================================================================

🐋 WAD : 세력 매매거래 추적기

WAD(Whale Activity Detector) 는 특정 종목의 거래량 패턴 속에서

‘평균 대비 비정상적으로 큰 거래량이 발생한 구간’을 자동으로 감지해

세력(Whale)의 매수·매도 활동을 시각화하는 지표입니다.

🔍 작동 원리

매수·매도 거래량 분리

각 캔들이 양봉인지, 음봉인지에 따라 거래량을 분리합니다.

양봉 시 발생한 거래량 → 매수 거래량(buy volume)

음봉 시 발생한 거래량 → 매도 거래량(sell volume)

이렇게 분리함으로써 단순 거래량이 아닌,

실제 매수세/매도세의 힘을 구분할 수 있습니다.

평균 거래량 계산

사용자가 지정한 기간(기본 34봉)을 기준으로

매수·매도 거래량의 이동평균선을 각각 계산합니다.

이는 ‘정상적인 거래량 수준’을 판단하는 기준선으로 활용됩니다.

이상치 탐지 (Whale Activity Detection)

현재 거래량이 평균 거래량의 n배(기본 4배)를 초과할 경우,

그 구간을 세력 개입 구간(Whale Zone) 으로 판단합니다.

양봉에서 급증 → 세력 매수 (Whale Buy)

음봉에서 급증 → 세력 매도 (Whale Sell)

시각적 표시

초록색 기둥 : 세력 매수 거래량

빨간색 기둥 : 세력 매도 거래량

라벨 표시 (BUY / SELL) : 이상치 발생 시 차트 상단에 표시

평균선 표시 옵션 : 사용자가 원할 때 평균선을 켜거나 끌 수 있음

알림(Alerts)

세력의 매수·매도 신호가 감지되면,

알림 메시지를 통해 실시간으로 통보받을 수 있습니다.

(예: 🐋 Whale Buy - NVDA! 🟢)

⚙️ 지표의 의미

단순 거래량이 아니라, ‘평균 대비 비정상적 거래량’ 을 추적합니다.

즉, “세력이 본격적으로 움직이기 시작한 구간” 만 걸러내는 지표입니다.

노이즈가 많은 거래량 차트 속에서 의도 있는 거래의 흔적을 포착할 수 있습니다.

🚀 활용 예시

세력 매집 구간 포착 : 큰 매수 시그널이 반복적으로 발생하는 구간은 세력의 누적 매집 가능성을 의미함

단기 급등 신호 확인 : 매수 이상치가 발생한 직후 가격이 급등하는 경우가 많음

지지/저항 분석과 병행 활용 : 세력 매도 구간은 단기 저항으로 작용하는 경향이 있음

copyright @invest_hedgeway

DayFlow VWAP Relay Forex Majors StrategySummary in one paragraph

DayFlow VWAP Relay is a day-trading strategy for major FX pairs on intraday timeframes, demonstrated on EURUSD 15 minutes. It waits for alignment between a daily anchored VWAP regime check, residual percentiles, and lower-timeframe micro flow before suggesting trades. The originality is the fusion of daily VWAP residual percentiles with a live micro-flow score from 1 minute data to switch between fade and breakout behavior inside the same session. Add it to a clean chart and use the markers and alerts.

Scope and intent

• Markets: Major FX pairs such as EURUSD, GBPUSD, USDJPY, AUDUSD, USDCHF, USDCAD

• Timeframes: One minute to one hour

• Default demo in this publication: EURUSD on 15 minutes

• Purpose: Reduce false starts by acting only when context, location and micro flow agree

• Limits: This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Core novelty: Residual percentiles to daily anchored VWAP decide “balanced versus expanding day”. A separate 1 minute micro-flow score confirms direction, so the same model fades extremes in balance and rides range breaks in expansion

• Failure modes addressed: Chop fakeouts and unconfirmed breakouts are filtered by the expansion gate and micro-flow threshold

• Testability: Every input is exposed. Bands, background regime color, and markers show why a suggestion appears

• Portable yardstick: Stops and targets are ATR multiples converted to ticks, which transfer across symbols

• Open source status: No reused third-party code that requires attribution

Method overview in plain language

The day is anchored with a VWAP that updates from the daily session start. Price minus VWAP is the residual. Percentiles of that residual measured over a rolling window define location extremes for the current day. A regime score compares residual volatility to price volatility. When expansion is low, the day is treated as balanced and the model fades residual extremes if 1 minute micro flow points back to VWAP. When expansion is high, the model trades breakouts outside the VWAP bands if slope and micro flow agree with the move.

Base measures

• Range basis: True Range smoothed by ATR for stops and targets, length 14

• Return basis: Not required for signals; residuals are absolute price distance to VWAP

Components

• Daily Anchor VWAP Bands. VWAP with standard-deviation bands. Slope sign is used for trend confirmation on breakouts

• Residual Percentiles. Rolling percentiles of close minus VWAP over Signal length. Identify location extremes inside the day

• Expansion Ratio. Standard deviation of residuals divided by standard deviation of price over Signal length. Classifies balanced versus expanding day

• Micro Flow. Net up minus down closes from 1 minute data across a short span, normalized to −1..+1. Confirms direction and avoids fades against pressure

• Session Window optional. Restricts trading to your configured hours to avoid thin periods

• Cooldown optional. Bars to wait after a position closes to prevent immediate re-entry

Fusion rule

Gating rather than weighting. First choose regime by Expansion Ratio versus the Expansion gate. Inside each regime all listed conditions must be true: location test plus micro-flow threshold plus session window plus cooldown. Breakouts also require VWAP slope alignment.

Signal rule

• Long suggestion on balanced day: residual at or below the lower percentile and micro flow positive above the gate while inside session and cooldown is satisfied

• Short suggestion on balanced day: residual at or above the upper percentile and micro flow negative below the gate while inside session and cooldown is satisfied

• Long suggestion on expanding day: close above the upper VWAP band, VWAP slope positive, micro flow positive, session and cooldown satisfied

• Short suggestion on expanding day: close below the lower VWAP band, VWAP slope negative, micro flow negative, session and cooldown satisfied

• Positions flip on opposite suggestions or exit by brackets

What you will see on the chart

• Markers on suggestion bars: L for long, S for short

• Exit occurs on reverse signal or when a bracket order is filled

• Reference lines: daily anchored VWAP with upper and lower bands

• Optional background: teal for balanced day, orange for expanding day

Inputs with guidance

Setup

• Signal length. Residual and regime window. Typical 40 to 100. Higher smooths, lower reacts faster

Micro Flow

• Micro TF. Lower timeframe used for micro flow, default 1 minute

• Micro span bars. Count of lower-TF bars. Typical 5 to 20

• Micro flow gate 0..1. Minimum absolute flow. Raising it demands stronger confirmation and reduces trade count

VWAP Bands

• VWAP stdev multiplier. Band width. Typical 0.8 to 1.6. Wider bands reduce breakout frequency and increase fade distance

• Expansion gate 0..3. Threshold to switch from fades to breakouts. Raising it favors fades, lowering it favors breakouts

Sessions

• Use session filter. Enable to trade only inside your window

• Trade window UTC. Default 07:00 to 17:00

Risk

• ATR length. Stop and target basis. Typical 10 to 21

• Stop ATR x. Initial stop distance in ATR multiples

• Target ATR x. Profit target distance in ATR multiples

• Cooldown bars after close. Wait bars before a new entry

• Side. Both, long only, or short only

View

• Show VWAP and bands

• Color bars by residual regime

Properties visible in this publication

• Initial capital 10000

• Base currency Default

• request.security uses lookahead off everywhere

• Strategy: Percent of equity with value 3. Pyramiding 0. Commission cash per order 0.0001 USD. Slippage 3 ticks. Process orders on close ON. Bar magnifier ON. Recalculate after order is filled OFF. Calc on every tick OFF. Using standard OHLC fills ON.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Fills and slippage vary by venue. Shapes can move while a bar forms and settle on close. Strategies must run on standard candles for signals and orders.

Honest limitations and failure modes

High impact news, session opens, and thin liquidity can invalidate assumptions. Very quiet days can reduce contrast between residuals and price volatility. Session windows use the chart exchange time. If both stop and target are touched within a single bar, TradingView’s standard OHLC price-movement model decides the outcome.

Expect different behavior on illiquid pairs or during holidays. The model is sensitive to session definitions and feed time. Past results never guarantee future outcomes.

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Stop point MMAAn indicator that determines an important stopping area by overcoming the blue candle. The overriding party is determined by buyers or sellers, as it must be confirmed by two candles closing below

Daily Pivot Points LEVELS S-RThis indicator plots daily pivot points based on the previous day’s high, low, and close. It displays the main pivot line, as well as the first levels of support (S1) and resistance (R1), with optional second levels (R2, S2) for additional reference. Ideal for

Nifty 50 Weighted Volume IndicatorThis takes the volume of the cash market as per the composite weighted average of the Nifty 50 Components.

You can use this at your discretion to take calls on Index trades.

PheeTrades - Value Area Levels (VAH / VAL / POC Visualizer)This script helps traders quickly visualize key Volume Profile–style levels such as Value Area High (VAH), Value Area Low (VAL), and Point of Control (POC) using recent price and volume data.

While TradingView’s built-in Volume Profile tool is great for manual analysis, this indicator automatically calculates and plots approximate value zones directly on your chart — ideal for traders who want to identify high-probability support and resistance areas without drawing a fixed range every time.

Features:

Calculates short-term VAH, VAL, and POC based on a user-defined lookback period.

Plots color-coded levels for quick visual reference.

Helps identify “fair value” zones where most trading activity occurred.

Useful for detecting breakout or mean-reversion opportunities around value extremes.

How to use:

Apply the script to any chart and set your preferred lookback period.

VAH (red line): potential upper resistance or overbought zone.

VAL (green line): potential lower support or accumulation zone.

POC (orange line): price level with the highest traded activity — often a magnet for price.

Note:

This is a simplified Value Area model meant for educational and analytical use. It does not replace TradingView’s official Volume Profile or broker-level volume distribution data.