PROTECTED SOURCE SCRIPT

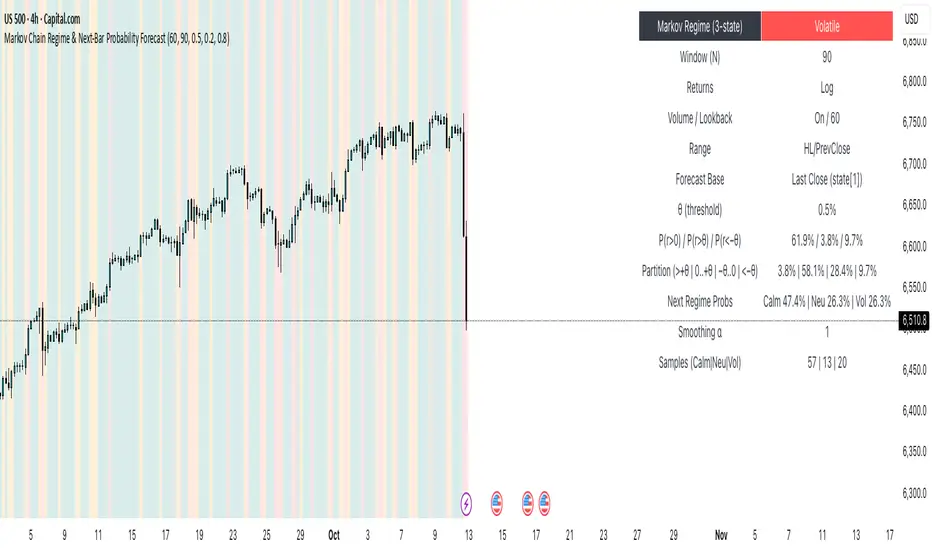

Markov Chain Regime & Next‑Bar Probability Forecast

✨ What it is

A regime-aware, math-driven panel that forecasts the odds for the very next candle. It shows:

• P(next r > 0)

• P(next r > +θ)

• P(next r < −θ)

• A 4-bucket split of next-bar outcomes (>+θ | 0..+θ | −θ..0 | <−θ)

• Next-regime probabilities: Calm | Neutral | Volatile

🧠 Why the math is strong

• Markov regimes: Markets cluster in volatility “moods.” We learn a 3-state regime S∈{Calm, Neutral, Volatile} with a transition matrix A, where A[i,j] = P(Sₜ₊₁=j | Sₜ=i).

• Condition on the future state: We estimate event odds given the next regime j—

q_pos(j)=P(rₜ₊₁>0 | Sₜ₊₁=j), q_gt(j)=P(rₜ₊₁>+θ | Sₜ₊₁=j), q_lt(j)=P(rₜ₊₁<−θ | Sₜ₊₁=j)—

and mix them with transitions from the current (or frozen) state sNow:

P(event) = Σⱼ A[sNow,j] · q(event | j).

This mixture-of-regimes view (HMM-style one-step prediction) ties next-bar outcomes to where volatility is likely headed.

• Statistical hygiene: Laplace/Beta smoothing, minimum-sample gating, and unconditional fallbacks keep estimates stable. Heavy computations run on confirmed bars; “Freeze at close” avoids intrabar flicker.

📊 What each value means

• Regime label & background: 🟩 Calm, 🟧 Neutral, 🟥 Volatile — quick read of market context.

• P(next r > 0): Directional tilt for the very next bar.

• P(next r > +θ): Odds of an outsized positive move beyond θ.

• P(next r < −θ): Odds of an outsized negative move beyond −θ.

• Partition row: Distributes next-bar probability across four intuitive buckets; they ≈ sum to 100%.

• Next Regime Probs: Likelihood of switching to Calm/Neutral/Volatile on the next bar (row of A for the current/frozen state).

• Samples row: How many next-bar samples support each next-state estimate (a confidence cue).

• Smoothing α: The Laplace prior used to stabilize binary event rates.

⚙️ Inputs you control

• Returns: Log (default) or %

• Include Volume (z-score) + lookback

• Include Range (HL/PrevClose)

• Rolling window N (transitions & estimates)

• θ as percent (e.g., 0.5%)

• Freeze forecast at last close (recommended)

• Display toggles (plots, partition, samples)

🎯 How to use it

• Volatility awareness & sizing: Rising P(next regime = Volatile) → consider smaller size, wider stops, or skipping marginal entries.

• Breakout preparation: Elevated P(next r > +θ) highlights environments where range expansion is more likely; pair with your setup/trigger.

• Defense for mean-reversion: If P(next r < −θ) lifts while you’re late long (or P(next r > +θ) lifts while late short), tighten risk or wait for better context.

• Calibration tip: Start θ near your market’s typical bar size; adjust until “>+θ” flags truly meaningful moves for your timeframe.

📝 Method notes & limits

Activity features (|r|, volume z, range) are standardized; only positive z’s feed the composite activity score. Estimates adapt to instrument/timeframe; rare regimes or small windows increase variance (hence smoothing, sample gating, fallbacks). This is a context/forecast tool, not a standalone signal—combine with your entry/exit rules and risk management.

🧩 Strategies too

We also develop full strategy versions that use these probabilities for entries, filters, and position sizing. Like this publication if you’d like us to release the strategy edition next.

⚠️ Disclaimer

Educational use only. Not financial advice. Markets involve risk. Past performance does not guarantee future results.

A regime-aware, math-driven panel that forecasts the odds for the very next candle. It shows:

• P(next r > 0)

• P(next r > +θ)

• P(next r < −θ)

• A 4-bucket split of next-bar outcomes (>+θ | 0..+θ | −θ..0 | <−θ)

• Next-regime probabilities: Calm | Neutral | Volatile

🧠 Why the math is strong

• Markov regimes: Markets cluster in volatility “moods.” We learn a 3-state regime S∈{Calm, Neutral, Volatile} with a transition matrix A, where A[i,j] = P(Sₜ₊₁=j | Sₜ=i).

• Condition on the future state: We estimate event odds given the next regime j—

q_pos(j)=P(rₜ₊₁>0 | Sₜ₊₁=j), q_gt(j)=P(rₜ₊₁>+θ | Sₜ₊₁=j), q_lt(j)=P(rₜ₊₁<−θ | Sₜ₊₁=j)—

and mix them with transitions from the current (or frozen) state sNow:

P(event) = Σⱼ A[sNow,j] · q(event | j).

This mixture-of-regimes view (HMM-style one-step prediction) ties next-bar outcomes to where volatility is likely headed.

• Statistical hygiene: Laplace/Beta smoothing, minimum-sample gating, and unconditional fallbacks keep estimates stable. Heavy computations run on confirmed bars; “Freeze at close” avoids intrabar flicker.

📊 What each value means

• Regime label & background: 🟩 Calm, 🟧 Neutral, 🟥 Volatile — quick read of market context.

• P(next r > 0): Directional tilt for the very next bar.

• P(next r > +θ): Odds of an outsized positive move beyond θ.

• P(next r < −θ): Odds of an outsized negative move beyond −θ.

• Partition row: Distributes next-bar probability across four intuitive buckets; they ≈ sum to 100%.

• Next Regime Probs: Likelihood of switching to Calm/Neutral/Volatile on the next bar (row of A for the current/frozen state).

• Samples row: How many next-bar samples support each next-state estimate (a confidence cue).

• Smoothing α: The Laplace prior used to stabilize binary event rates.

⚙️ Inputs you control

• Returns: Log (default) or %

• Include Volume (z-score) + lookback

• Include Range (HL/PrevClose)

• Rolling window N (transitions & estimates)

• θ as percent (e.g., 0.5%)

• Freeze forecast at last close (recommended)

• Display toggles (plots, partition, samples)

🎯 How to use it

• Volatility awareness & sizing: Rising P(next regime = Volatile) → consider smaller size, wider stops, or skipping marginal entries.

• Breakout preparation: Elevated P(next r > +θ) highlights environments where range expansion is more likely; pair with your setup/trigger.

• Defense for mean-reversion: If P(next r < −θ) lifts while you’re late long (or P(next r > +θ) lifts while late short), tighten risk or wait for better context.

• Calibration tip: Start θ near your market’s typical bar size; adjust until “>+θ” flags truly meaningful moves for your timeframe.

📝 Method notes & limits

Activity features (|r|, volume z, range) are standardized; only positive z’s feed the composite activity score. Estimates adapt to instrument/timeframe; rare regimes or small windows increase variance (hence smoothing, sample gating, fallbacks). This is a context/forecast tool, not a standalone signal—combine with your entry/exit rules and risk management.

🧩 Strategies too

We also develop full strategy versions that use these probabilities for entries, filters, and position sizing. Like this publication if you’d like us to release the strategy edition next.

⚠️ Disclaimer

Educational use only. Not financial advice. Markets involve risk. Past performance does not guarantee future results.

نص برمجي محمي

تم نشر هذا النص البرمجي كمصدر مغلق. ومع ذلك، يمكنك استخدامه بحرية ودون أي قيود - تعرف على المزيد هنا.

📊 Access & Subscription → algorific.gumroad.com/

💬 After purchase, DM @Algorific on TradingView for invite-only access.

💬 After purchase, DM @Algorific on TradingView for invite-only access.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView. اقرأ المزيد في شروط الاستخدام.

نص برمجي محمي

تم نشر هذا النص البرمجي كمصدر مغلق. ومع ذلك، يمكنك استخدامه بحرية ودون أي قيود - تعرف على المزيد هنا.

📊 Access & Subscription → algorific.gumroad.com/

💬 After purchase, DM @Algorific on TradingView for invite-only access.

💬 After purchase, DM @Algorific on TradingView for invite-only access.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView. اقرأ المزيد في شروط الاستخدام.