OPEN-SOURCE SCRIPT

3HMA

Introduction

The Hull smoothing method aim to reduce the lag of a moving average by using a simple calculation involving smoothing with a moving average of period √p the subtraction of a moving average of period p/2 multiplied by 2 with another moving average of period p, however it is possible to extend this calculation by introducing more terms thus reducing both the lag and overshoot of the classical HMA.

Comparison

The proposed filter add 1 more term to the classical hull moving average thus ending with : sma(sma(p/3) * 3 - sma(p/2) - sma(p),p), this can be developed as long as every terms add to total unity, more terms will often require more smoothing, this is why i replace √p by p.

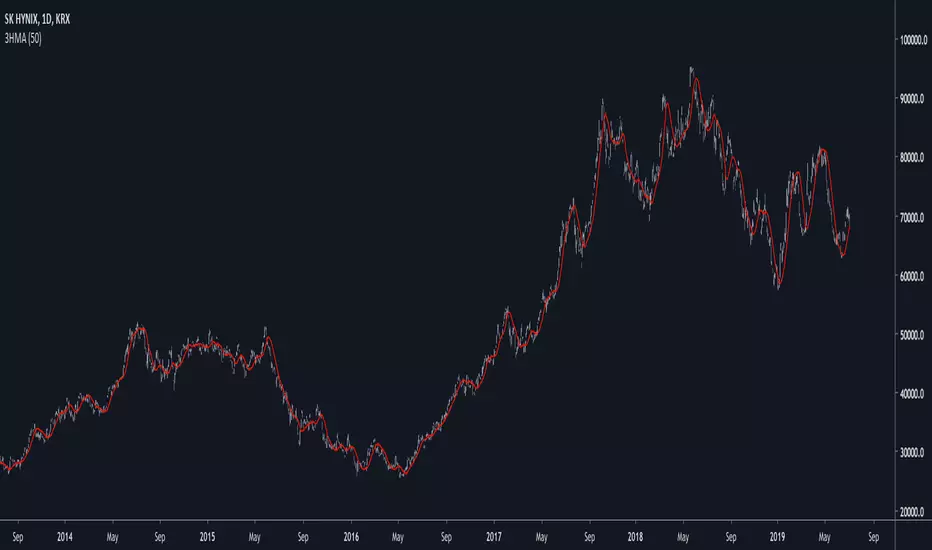

In blue a HMA and in red the proposed filter of both period 50. The third term added allow for more reactivity which sometimes allow for overshoots with lower amplitudes.

Conclusions

Adding more terms to certain filtering methods can correct certain behaviours as well as reducing lag or increasing smoothing.

The Hull smoothing method aim to reduce the lag of a moving average by using a simple calculation involving smoothing with a moving average of period √p the subtraction of a moving average of period p/2 multiplied by 2 with another moving average of period p, however it is possible to extend this calculation by introducing more terms thus reducing both the lag and overshoot of the classical HMA.

Comparison

The proposed filter add 1 more term to the classical hull moving average thus ending with : sma(sma(p/3) * 3 - sma(p/2) - sma(p),p), this can be developed as long as every terms add to total unity, more terms will often require more smoothing, this is why i replace √p by p.

In blue a HMA and in red the proposed filter of both period 50. The third term added allow for more reactivity which sometimes allow for overshoots with lower amplitudes.

Conclusions

Adding more terms to certain filtering methods can correct certain behaviours as well as reducing lag or increasing smoothing.

نص برمجي مفتوح المصدر

بروح TradingView الحقيقية، قام مبتكر هذا النص البرمجي بجعله مفتوح المصدر، بحيث يمكن للمتداولين مراجعة وظائفه والتحقق منها. شكرا للمؤلف! بينما يمكنك استخدامه مجانًا، تذكر أن إعادة نشر الكود يخضع لقواعد الموقع الخاصة بنا.

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView. اقرأ المزيد في شروط الاستخدام.

نص برمجي مفتوح المصدر

بروح TradingView الحقيقية، قام مبتكر هذا النص البرمجي بجعله مفتوح المصدر، بحيث يمكن للمتداولين مراجعة وظائفه والتحقق منها. شكرا للمؤلف! بينما يمكنك استخدامه مجانًا، تذكر أن إعادة نشر الكود يخضع لقواعد الموقع الخاصة بنا.

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView. اقرأ المزيد في شروط الاستخدام.