Laguerre Multi-Filter [DW]This is an experimental study designed to identify underlying price activity using a series of Laguerre Filters.

Two different modes are included within this script:

-Ribbon Mode - A ribbon of 18 Laguerre Filters with separate Gamma values is calculated.

-Band Mode - An average of the 18 filters generates the basis line. Then, Golden Mean ATR over the specified sampling period multiplied by 1 and 2 are added and subtracted to the basis line to generate the bands.

Multi-Timeframe functionality is included. You can choose any timeframe that TradingView supports as the basis resolution for the script.

Custom bar colors are included. Bar colors are based on the direction of any of the 18 filters, or the average filter's direction in Ribbon Mode. In Band Mode, the colors are based solely on the average filter's direction.

Filter

Price Action Volatility FilterThis creates a none oscillating histogram that shows price action without lower time frame volatility to help show bias for use with macd or entries with other trending indicators.

Function Savitzky Golay Filter with 7 Vectors V0EXPERIMENTAL:

updated code for duo, triple and multipass

Trend FilterThe indicator colours the candles either Green or Red depending on the following conditions:-

If the N Bar Average Close > N Bar Average Open, the Bars are coloured Green.

If the N Bar Average Close < N Bar Average Open, the Bars are coloured Red.

hecate chop filterChop Filter to remove lateral trade under a threshold. Change the FilterOut parameter to filter all you want. Example of a model using it with a filtering of 0.003 (use to filter out to the level you prefer):

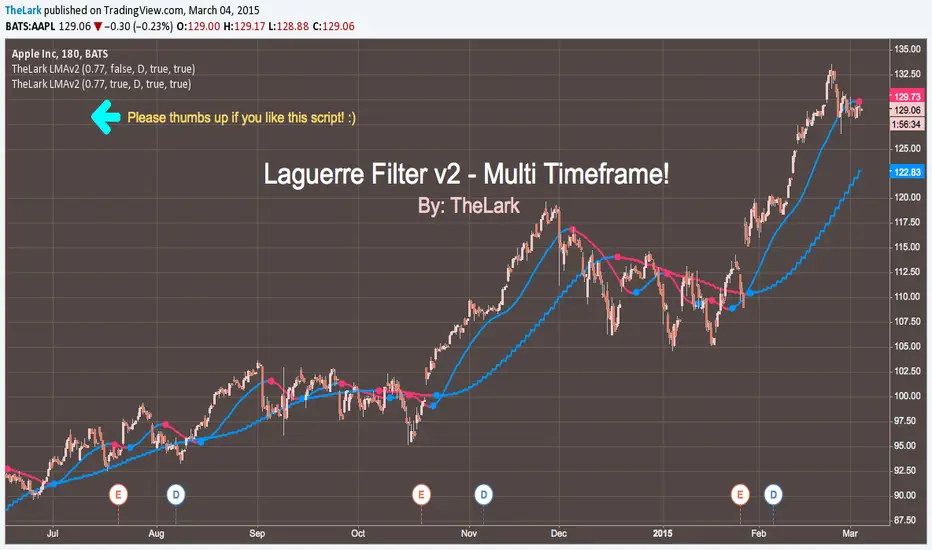

TheLark LMA (Laguerre) v2 - multi timeframeWhat's new?

v2 has added multi timeframe support.

Blatantly stole Chris Moody's code for multi timeframe, because why re-invent the wheel? Thanks Chris ;P

BUT -- modified the coloring to work correctly with higher timeframes, just another Lark hack, so it's a give and take :)

_____________________________

The Laguerre Average (filter) was discovered by John Ehlers.

It's a newer type of averaging that is meant to take out as much of the

inherent lag that your typical EMA and SMA's give at the start of a major trend change.

So what you get is an average that turns more quickly at major trend changes,

and doesn't get tripped up on the noise (as much).

_____________________________

Please thumbs up/ star/ whatever this script if you like it & use it!

See my profile for more scripts, & be sure to follow for future releases.

Sorry for my hiatus, extremely busy these days working on both my own and client work.

This script was a user request.

Bandpass Filter Strategy The related article is copyrighted material from

Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

Bandpass Filter The related article is copyrighted material from

Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

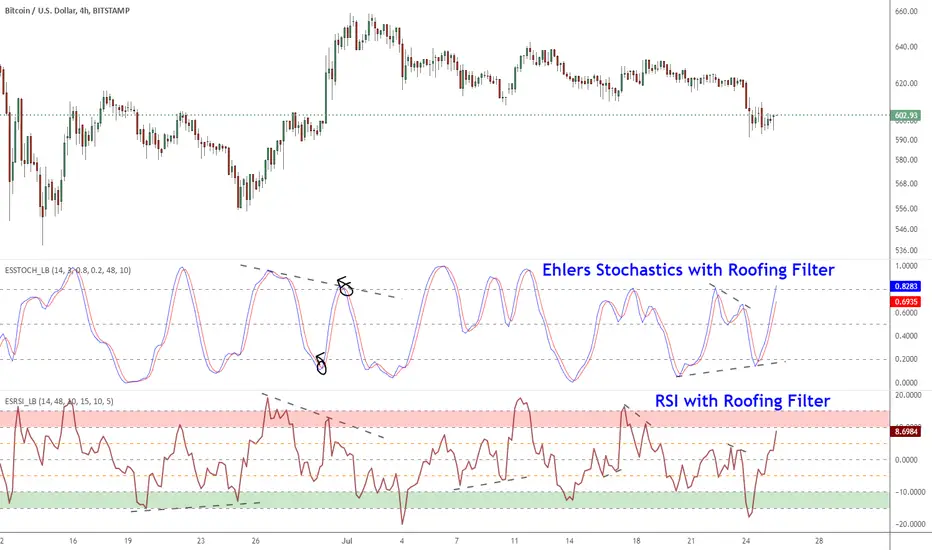

Ehlers Smoothed Stochastic & RSI with Roofing FiltersRoofing filters, first discussed by Mr.John Ehlers, act as a passband, filtering out unwanted noise from market data and accentuating turning points.

I have included 2 indicators with filters enabled. Both support double smoothing via options page. All the parameters are configurable.

Info on Roofing Filter and Ehlers Super Smoother:

----------------------------------------------------

The Ehlers' Roofing Filter is an expansion on Ehlers Super Smoother Filter, both being smoothing techniques based on analog filters. This filter aims at reducing noise in price data.

In Super Smoother Filter, regardless of the time frame used, all waves having cycles of less than 10 bars are considered noise (customizable via options page). The Roofing Filter uses this principle, however, it also creates a so-called "roof" by eliminating wave components having cycles greater than 48 bars which are perceived as "spectral dilation". Thus, the filter only passes those spectral components whose periods are between 10 and 48 bars. This technique noticeably reduces indicator lag and also helps assess turning points more accurately.

More info:

- Spectral dilation paper: www.mesasoftware.com

- John Ehlers presentation: www.youtube.com

------------------------------------------------------

If you want to use RSI %B and Bandwidth, follow this guide to "Make mine" this chart and get access to the source:

drive.google.com

For the complete list of my indicators, check this post:

CMO Oscillator with FilterHi

Let me introduce my CMO Oscillator with Filter script.

This indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.