Polyline PlusThis library introduces the `PolylinePlus` type, which is an enhanced version of the built-in PineScript `polyline`. It enables two features that are absent from the built-in type:

1. Developers can now efficiently add or remove points from the polyline. In contrast, the built-in `polyline` type is immutable, requiring developers to create a new instance of the polyline to make changes, which is cumbersome and incurs a significant performance penalty.

2. Each `PolylinePlus` instance can theoretically hold up to ~1M points, surpassing the built-in `polyline` type's limit of 10K points, as long as it does not exceed the memory limit of the PineScript runtime.

Internally, each `PolylinePlus` instance utilizes an array of `line`s and an array of `polyline`s. The `line`s array serves as a buffer to store lines formed by recently added points. When the buffer reaches its capacity, it flushes the contents and converts the lines into polylines. These polylines are expected to undergo fewer updates. This approach is similiar to the concept of "Buffered I/O" in file and network systems. By connecting the underlying lines and polylines, this library achieves an enhanced polyline that is dynamic, efficient, and capable of surpassing the maximum number of points imposed by the built-in polyline.

🔵 API

Step 1: Import this library

import algotraderdev/polylineplus/1 as pp

// remember to check the latest version of this library and replace the 1 above.

Step 2: Initialize the `PolylinePlus` type.

var p = pp.PolylinePlus.new()

There are a few optional params that developers can specify in the constructor to modify the behavior and appearance of the polyline instance.

var p = pp.PolylinePlus.new(

// If true, the drawing will also connect the first point to the last point, resulting in a closed polyline.

closed = false,

// Determines the field of the chart.point objects that the polyline will use for its x coordinates. Either xloc.bar_index (default), or xloc.bar_time.

xloc = xloc.bar_index,

// Color of the polyline. Default is blue.

line_color = color.blue,

// Style of the polyline. Default is line.style_solid.

line_style = line.style_solid,

// Width of the polyline. Default is 1.

line_width = 1,

// The maximum number of points that each built-in `polyline` instance can contain.

// NOTE: this is not to be confused with the maximum of points that each `PolylinePlus` instance can contain.

max_points_per_builtin_polyline = 10000,

// The number of lines to keep in the buffer. If more points are to be added while the buffer is full, then all the lines in the buffer will be flushed into the poylines.

// The higher the number, the less frequent we'll need to // flush the buffer, and thus lead to better performance.

// NOTE: the maximum total number of lines per chart allowed by PineScript is 500. But given there might be other places where the indicator or strategy are drawing lines outside this polyline context, the default value is 50 to be safe.

lines_bffer_size = 50)

Step 3: Push / Pop Points

// Push a single point

p.push_point(chart.point.now())

// Push multiple points

chart.point points = array.from(p1, p2, p3) // Where p1, p2, p3 are all chart.point type.

p.push_points(points)

// Pop point

p.pop_point()

// Resets all the points in the polyline.

p.set_points(points)

// Deletes the polyline.

p.delete()

🔵 Benchmark

Below is a simple benchmark comparing the performance between `PolylinePlus` and the native `polyline` type for incrementally adding 10K points to a polyline.

import algotraderdev/polylineplus/2 as pp

var t1 = 0

var t2 = 0

if bar_index < 10000

int start = timenow

var p = pp.PolylinePlus.new(xloc = xloc.bar_time, closed = true)

p.push_point(chart.point.now())

t1 += timenow - start

start := timenow

var polyline pl = na

var points = array.new()

points.push(chart.point.now())

if not na(pl)

pl.delete()

pl := polyline.new(points)

t2 += timenow - start

if barstate.islast

log.info('{0} {1}', t1, t2)

For this benchmark, `PolylinePlus` took ~300ms, whereas the native `polyline` type took ~6000ms.

We can also fine-tune the parameters for `PolylinePlus` to have a larger buffer size for `line`s and a smaller buffer for `polyline`s.

var p = pp.PolylinePlus.new(xloc = xloc.bar_time, closed = true, lines_buffer_size = 500, max_points_per_builtin_polyline = 1000)

With the above optimization, it only took `PolylinePlus` ~80ms to process the same 10K points, which is ~75x the performance compared to the native `polyline`.

MATH

SPTS_StatsPakLibFinally getting around to releasing the library component to the SPTS indicator!

This library is packed with a ton of great statistics functions to supplement SPTS, these functions add to the capabilities of SPTS including a forecast function.

The library includes the following functions

1. Linear Regression (single independent and single dependent)

2. Multiple Regression (2 independent variables, 1 dependent)

3. Standard Error of Residual Assessment

4. Z-Score

5. Effect Size

6. Confidence Interval

7. Paired Sample Test

8. Two Tailed T-Test

9. Qualitative assessment of T-Test

10. T-test table and p value assigner

11. Correlation of two arrays

12. Quadratic correlation (curvlinear)

13. R Squared value of 2 arrays

14. R Squared value of 2 floats

15. Test of normality

16. Forecast function which will push the desired forecasted variables into an array.

One of the biggest added functionalities of this library is the forecasting function.

This function provides an autoregressive, trainable model that will export forecasted values to 3 arrays, one contains the autoregressed forecasted results, the other two contain the upper confidence forecast and the lower confidence forecast.

Hope you enjoy and find use for this!

Library "SPTS_StatsPakLib"

f_linear_regression(independent, dependent, len, variable)

TODO: creates a simple linear regression model between two variables.

Parameters:

independent (float)

dependent (float)

len (int)

variable (float)

Returns: TODO: returns 6 float variables

result: The result of the regression model

pear_cor: The pearson correlation of the regresion model

rsqrd: the R2 of the regression model

std_err: the error of residuals

slope: the slope of the model (coefficient)

intercept: the intercept of the model (y = mx + b is y = slope x + intercept)

f_multiple_regression(y, x1, x2, input1, input2, len)

TODO: creates a multiple regression model between two independent variables and 1 dependent variable.

Parameters:

y (float)

x1 (float)

x2 (float)

input1 (float)

input2 (float)

len (int)

Returns: TODO: returns 7 float variables

result: The result of the regression model

pear_cor: The pearson correlation of the regresion model

rsqrd: the R2 of the regression model

std_err: the error of residuals

b1 & b2: the slopes of the model (coefficients)

intercept: the intercept of the model (y = mx + b is y = b1 x + b2 x + intercept)

f_stanard_error(result, dependent, length)

x TODO: performs an assessment on the error of residuals, can be used with any variable in which there are residual values (such as moving averages or more comlpex models)

param x TODO: result is the output, for example, if you are calculating the residuals of a 200 EMA, the result would be the 200 EMA

dependent: is the dependent variable. In the above example with the 200 EMA, your dependent would be the source for your 200 EMA

Parameters:

result (float)

dependent (float)

length (int)

Returns: x TODO: the standard error of the residual, which can then be multiplied by standard deviations or used as is.

f_zscore(variable, length)

TODO: Calculates the z-score

Parameters:

variable (float)

length (int)

Returns: TODO: returns float z-score

f_effect_size(array1, array2)

TODO: Calculates the effect size between two arrays of equal scale.

Parameters:

array1 (float )

array2 (float )

Returns: TODO: returns the effect size (float)

f_confidence_interval(array1, array2, ci_input)

TODO: Calculates the confidence interval between two arrays

Parameters:

array1 (float )

array2 (float )

ci_input (float)

Returns: TODO: returns the upper_bound and lower_bound cofidence interval as float values

paired_sample_t(src1, src2, len)

TODO: Performs a paired sample t-test

Parameters:

src1 (float)

src2 (float)

len (int)

Returns: TODO: Returns the t-statistic and degrees of freedom of a paired sample t-test

two_tail_t_test(array1, array2)

TODO: Perofrms a two tailed t-test

Parameters:

array1 (float )

array2 (float )

Returns: TODO: Returns the t-statistic and degrees of freedom of a two_tail_t_test sample t-test

t_table_analysis(t_stat, df)

TODO: This is to make a qualitative assessment of your paired and single sample t-test

Parameters:

t_stat (float)

df (float)

Returns: TODO: the function will return 2 string variables and 1 colour variable. The 2 string variables indicate whether the results are significant or not and the colour will

output red for insigificant and green for significant

t_table_p_value(df, t_stat)

TODO: This performs a quantaitive assessment on your t-tests to determine the statistical significance p value

Parameters:

df (float)

t_stat (float)

Returns: TODO: The function will return 1 float variable, the p value of the t-test.

cor_of_array(array1, array2)

TODO: This performs a pearson correlation assessment of two arrays. They need to be of equal size!

Parameters:

array1 (float )

array2 (float )

Returns: TODO: The function will return the pearson correlation.

quadratic_correlation(src1, src2, len)

TODO: This performs a quadratic (curvlinear) pearson correlation between two values.

Parameters:

src1 (float)

src2 (float)

len (int)

Returns: TODO: The function will return the pearson correlation (quadratic based).

f_r2_array(array1, array2)

TODO: Calculates the r2 of two arrays

Parameters:

array1 (float )

array2 (float )

Returns: TODO: returns the R2 value

f_rsqrd(src1, src2, len)

TODO: Calculates the r2 of two float variables

Parameters:

src1 (float)

src2 (float)

len (int)

Returns: TODO: returns the R2 value

test_of_normality(array, src)

TODO: tests the normal distribution hypothesis

Parameters:

array (float )

src (float)

Returns: TODO: returns 4 variables, 2 float and 2 string

Skew: the skewness of the dataset

Kurt: the kurtosis of the dataset

dist = the distribution type (recognizes 7 different distribution types)

implication = a string assessment of the implication of the distribution (qualitative)

f_forecast(output, input, train_len, forecast_length, output_array, upper_array, lower_array)

TODO: This performs a simple forecast function on a single dependent variable. It will autoregress this based on the train time, to the desired length of output,

then it will push the forecasted values to 3 float arrays, one that contains the forecasted result, 1 that contains the Upper Confidence Result and one with the lower confidence

result.

Parameters:

output (float)

input (float)

train_len (int)

forecast_length (int)

output_array (float )

upper_array (float )

lower_array (float )

Returns: TODO: Will return 3 arrays, one with the forecasted results, one with the upper confidence results, and a final with the lower confidence results. Example is given below.

mathLibrary "math"

TODO: Math custom MA and more

pine_ema(src, length)

Parameters:

src (float)

length (int)

pine_dema(src, length)

Parameters:

src (float)

length (int)

pine_tema(src, length)

Parameters:

src (float)

length (int)

pine_sma(src, length)

Parameters:

src (float)

length (int)

pine_smma(src, length)

Parameters:

src (float)

length (int)

pine_ssma(src, length)

Parameters:

src (float)

length (int)

pine_rma(src, length)

Parameters:

src (float)

length (int)

pine_wma(x, y)

Parameters:

x (float)

y (int)

pine_hma(src, length)

Parameters:

src (float)

length (int)

pine_vwma(x, y)

Parameters:

x (float)

y (int)

pine_swma(x)

Parameters:

x (float)

pine_alma(src, length, offset, sigma)

Parameters:

src (float)

length (int)

offset (float)

sigma (float)

EphemerisLibrary "Ephemeris"

TODO: add library description here

mercuryElements()

mercuryRates()

venusElements()

venusRates()

earthElements()

earthRates()

marsElements()

marsRates()

jupiterElements()

jupiterRates()

saturnElements()

saturnRates()

uranusElements()

uranusRates()

neptuneElements()

neptuneRates()

rev360(x)

Normalize degrees to within [0, 360)

Parameters:

x (float) : degrees to be normalized

Returns: Normalized degrees

scaleAngle(longitude, magnitude, harmonic)

Scale angle in degrees

Parameters:

longitude (float)

magnitude (float)

harmonic (int)

Returns: Scaled angle in degrees

julianCenturyInJulianDays()

Constant Julian days per century

Returns: 36525

julianEpochJ2000()

Julian date on J2000 epoch start (2000-01-01)

Returns: 2451545.0

meanObliquityForJ2000()

Mean obliquity of the ecliptic on J2000 epoch start (2000-01-01)

Returns: 23.43928

getJulianDate(Year, Month, Day, Hour, Minute)

Convert calendar date to Julian date

Parameters:

Year (int) : calendar year as integer (e.g. 2018)

Month (int) : calendar month (January = 1, December = 12)

Day (int) : calendar day of month (e.g. January valid days are 1-31)

Hour (int) : valid values 0-23

Minute (int) : valid values 0-60

julianCenturies(date, epoch_start)

Centuries since Julian Epoch 2000-01-01

Parameters:

date (float) : Julian date to conver to Julian centuries

epoch_start (float) : Julian date of epoch start (e.g. J2000 epoch = 2451545)

Returns: Julian date converted to Julian centuries

julianCenturiesSinceEpochJ2000(julianDate)

Calculate Julian centuries since epoch J2000 (2000-01-01)

Parameters:

julianDate (float) : Julian Date in days

Returns: Julian centuries since epoch J2000 (2000-01-01)

atan2(y, x)

Specialized arctan function

Parameters:

y (float) : radians

x (float) : radians

Returns: special arctan of y/x

eccAnom(ec, m_param, dp)

Compute eccentricity of the anomaly

Parameters:

ec (float) : Eccentricity of Orbit

m_param (float) : Mean Anomaly ?

dp (int) : Decimal places to round to

Returns: Eccentricity of the Anomaly

planetEphemerisCalc(TGen, planetElementId, planetRatesId)

Compute planetary ephemeris (longtude relative to Earth or Sun) on a Julian date

Parameters:

TGen (float) : Julian Date

planetElementId (float ) : All planet orbital elements in an array. This index references a specific planet's elements.

planetRatesId (float ) : All planet orbital rates in an array. This index references a specific planet's rates.

Returns: X,Y,Z ecliptic rectangular coordinates and R radius from reference body.

calculateRightAscensionAndDeclination(earthX, earthY, earthZ, planetX, planetY, planetZ)

Calculate right ascension and declination for a planet relative to Earth

Parameters:

earthX (float) : Earth X ecliptic rectangular coordinate relative to Sun

earthY (float) : Earth Y ecliptic rectangular coordinate relative to Sun

earthZ (float) : Earth Z ecliptic rectangular coordinate relative to Sun

planetX (float) : Planet X ecliptic rectangular coordinate relative to Sun

planetY (float) : Planet Y ecliptic rectangular coordinate relative to Sun

planetZ (float) : Planet Z ecliptic rectangular coordinate relative to Sun

Returns: Planet geocentric orbital radius, geocentric right ascension, and geocentric declination

mercuryHelio(T)

Compute Mercury heliocentric longitude on date

Parameters:

T (float)

Returns: Mercury heliocentric longitude on date

venusHelio(T)

Compute Venus heliocentric longitude on date

Parameters:

T (float)

Returns: Venus heliocentric longitude on date

earthHelio(T)

Compute Earth heliocentric longitude on date

Parameters:

T (float)

Returns: Earth heliocentric longitude on date

marsHelio(T)

Compute Mars heliocentric longitude on date

Parameters:

T (float)

Returns: Mars heliocentric longitude on date

jupiterHelio(T)

Compute Jupiter heliocentric longitude on date

Parameters:

T (float)

Returns: Jupiter heliocentric longitude on date

saturnHelio(T)

Compute Saturn heliocentric longitude on date

Parameters:

T (float)

Returns: Saturn heliocentric longitude on date

neptuneHelio(T)

Compute Neptune heliocentric longitude on date

Parameters:

T (float)

Returns: Neptune heliocentric longitude on date

uranusHelio(T)

Compute Uranus heliocentric longitude on date

Parameters:

T (float)

Returns: Uranus heliocentric longitude on date

sunGeo(T)

Parameters:

T (float)

mercuryGeo(T)

Parameters:

T (float)

venusGeo(T)

Parameters:

T (float)

marsGeo(T)

Parameters:

T (float)

jupiterGeo(T)

Parameters:

T (float)

saturnGeo(T)

Parameters:

T (float)

neptuneGeo(T)

Parameters:

T (float)

uranusGeo(T)

Parameters:

T (float)

moonGeo(T_JD)

Parameters:

T_JD (float)

mercuryOrbitalPeriod()

Mercury orbital period in Earth days

Returns: 87.9691

venusOrbitalPeriod()

Venus orbital period in Earth days

Returns: 224.701

earthOrbitalPeriod()

Earth orbital period in Earth days

Returns: 365.256363004

marsOrbitalPeriod()

Mars orbital period in Earth days

Returns: 686.980

jupiterOrbitalPeriod()

Jupiter orbital period in Earth days

Returns: 4332.59

saturnOrbitalPeriod()

Saturn orbital period in Earth days

Returns: 10759.22

uranusOrbitalPeriod()

Uranus orbital period in Earth days

Returns: 30688.5

neptuneOrbitalPeriod()

Neptune orbital period in Earth days

Returns: 60195.0

jupiterSaturnCompositePeriod()

jupiterNeptuneCompositePeriod()

jupiterUranusCompositePeriod()

saturnNeptuneCompositePeriod()

saturnUranusCompositePeriod()

planetSineWave(julianDateInCenturies, planetOrbitalPeriod, planetHelio)

Convert heliocentric longitude of planet into a sine wave

Parameters:

julianDateInCenturies (float)

planetOrbitalPeriod (float) : Orbital period of planet in Earth days

planetHelio (float) : Heliocentric longitude of planet in degrees

Returns: Sine of heliocentric longitude on a Julian date

WIPFunctionLyaponovLibrary "WIPFunctionLyaponov"

Lyapunov exponents are mathematical measures used to describe the behavior of a system over

time. They are named after Russian mathematician Alexei Lyapunov, who first introduced the concept in the

late 19th century. The exponent is defined as the rate at which a particular function or variable changes

over time, and can be positive, negative, or zero.

Positive exponents indicate that a system tends to grow or expand over time, while negative exponents

indicate that a system tends to shrink or decay. Zero exponents indicate that the system does not change

significantly over time. Lyapunov exponents are used in various fields of science and engineering, including

physics, economics, and biology, to study the long-term behavior of complex systems.

~ generated description from vicuna13b

---

To calculate the Lyapunov Exponent (LE) of a given Time Series, we need to follow these steps:

1. Firstly, you should have access to your data in some format like CSV or Excel file. If not, then you can collect it manually using tools such as stopwatches and measuring tapes.

2. Once the data is collected, clean it up by removing any outliers that may skew results. This step involves checking for inconsistencies within your dataset (e.g., extremely large or small values) and either discarding them entirely or replacing with more reasonable estimates based on surrounding values.

3. Next, you need to determine the dimension of your time series data. In most cases, this will be equal to the number of variables being measured in each observation period (e.g., temperature, humidity, wind speed).

4. Now that we have a clean dataset with known dimensions, we can calculate the LE for our Time Series using the following formula:

λ = log(||M^T * M - I||)/log(||v||)

where:

λ (Lyapunov Exponent) is the quantity that will be calculated.

||...|| denotes an Euclidean norm of a vector or matrix, which essentially means taking the square root of the sum of squares for each element in the vector/matrix.

M represents our Jacobian Matrix whose elements are given by:

J_ij = (∂fj / ∂xj) where fj is the jth variable and xj is the ith component of the initial condition vector x(t). In other words, each element in this matrix represents how much a small change in one variable affects another.

I denotes an identity matrix whose elements are all equal to 1 (or any constant value if you prefer). This term essentially acts as a baseline for comparison purposes since we want our Jacobian Matrix M^T * M to be close to it when the system is stable and far away from it when the system is unstable.

v represents an arbitrary vector whose Euclidean norm ||v|| will serve as a scaling factor in our calculation. The choice of this particular vector does not matter since we are only interested in its magnitude (i.e., length) for purposes of normalization. However, if you want to ensure that your results are accurate and consistent across different datasets or scenarios, it is recommended to use the same initial condition vector x(t) as used earlier when calculating our Jacobian Matrix M.

5. Finally, once we have calculated λ using the formula above, we can interpret its value in terms of stability/instability for our Time Series data:

- If λ < 0, then this indicates that the system is stable (i.e., nearby trajectories will converge towards each other over time).

- On the other hand, if λ > 0, then this implies that the system is unstable (i.e., nearby trajectories will diverge away from one another over time).

~ generated description from airoboros33b

---

Reference:

en.wikipedia.org

www.collimator.ai

blog.abhranil.net

www.researchgate.net

physics.stackexchange.com

---

This is a work in progress, it may contain errors so use with caution.

If you find flaws or suggest something new, please leave a comment bellow.

_measure_function(i)

helper function to get the name of distance function by a index (0 -> 13).\

Functions: SSD, Euclidean, Manhattan, Minkowski, Chebyshev, Correlation, Cosine, Camberra, MAE, MSE, Lorentzian, Intersection, Penrose Shape, Meehl.

Parameters:

i (int)

_test(L)

Helper function to test the output exponents state system and outputs description into a string.

Parameters:

L (float )

estimate(X, initial_distance, distance_function)

Estimate the Lyaponov Exponents for multiple series in a row matrix.

Parameters:

X (map)

initial_distance (float) : Initial distance limit.

distance_function (string) : Name of the distance function to be used, default:`ssd`.

Returns: List of Lyaponov exponents.

max(L)

Maximal Lyaponov Exponent.

Parameters:

L (float ) : List of Lyapunov exponents.

Returns: Highest exponent.

Contrast Color LibraryThis lightweight library provides a utility method that analyzes any provided background color and automatically chooses the optimal black or white foreground color to ensure maximum visual contrast and readability.

🟠 Algorithm

The library utilizes the HSP Color Model to calculate the brightness of the background color. The formula for this calculation is as follows:

brightness = sqrt(0.299 * R^2 + 0.587 * G^2 + 0.114 * B^2 )

The library chooses black as the foreground color if the brightness exceeds the threshold (default 0.5), and white otherwise.

two_ma_logicLibrary "two_ma_logic"

The core logic for the two moving average strategy that is used as an example for the internal logic of

the "Template Trailing Strategy" and the "Two MA Signal Indicator"

ma(source, maType, length)

ma - Calculate the moving average of the given source for the given length and type of the average

Parameters:

source (float) : - The source of the values

maType (simple string) : - The type of the moving average

length (simple int) : - The length of the moving average

Returns: - The resulted value of the calculations of the moving average

getDealConditions(drawings, longDealsEnabled, shortDealsEnabled, endDealsEnabled, cnlStartDealsEnabled, cnlEndDealsEnabled, emaFilterEnabled, emaAtrBandEnabled, adxFilterEnabled, adxSmoothing, diLength, adxThreshold)

Parameters:

drawings (TwoMaDrawings)

longDealsEnabled (simple bool)

shortDealsEnabled (simple bool)

endDealsEnabled (simple bool)

cnlStartDealsEnabled (simple bool)

cnlEndDealsEnabled (simple bool)

emaFilterEnabled (simple bool)

emaAtrBandEnabled (simple bool)

adxFilterEnabled (simple bool)

adxSmoothing (simple int)

diLength (simple int)

adxThreshold (simple float)

TwoMaDrawings

Fields:

fastMA (series__float)

slowMA (series__float)

emaLine (series__float)

emaUpperBand (series__float)

emaLowerBand (series__float)

tts_conventionLibrary "tts_convention"

This library can convert the start, end, cancel start, cancel end deal conditions that are used in the

"Template Trailing Strategy" script into a signal value and vice versa. The "two channels mod div" convention is unsed

internaly and the signal value can be composed/decomposed into two channels that contain the afforementioned actions

for long and short positions separetely.

getDealConditions(signal)

getDealConditions - Get the start, end, cancel start and cancel end deal conditions that are used in the "Template Trailing Strategy" script by decomposing the given signal

Parameters:

signal (int) : - The signal value to decompose

Returns: An object with the start, end, cancel start and cancel end deal conditions for long and short

getSignal(dealConditions)

getSignal - Get the signal value from the composition of the start, end, cancel start and cancel end deal conditions that are used in the "Template Trailing Strategy" script

Parameters:

dealConditions (DealConditions) : - The deal conditions object that containd the start, end, cancel start and cancel end deal conditions for long and short

Returns: The composed signal value

DealConditions

Fields:

startLongDeal (series__bool)

startShortDeal (series__bool)

endLongDeal (series__bool)

endShortDeal (series__bool)

cnlStartLongDeal (series__bool)

cnlStartShortDeal (series__bool)

cnlEndLongDeal (series__bool)

cnlEndShortDeal (series__bool)

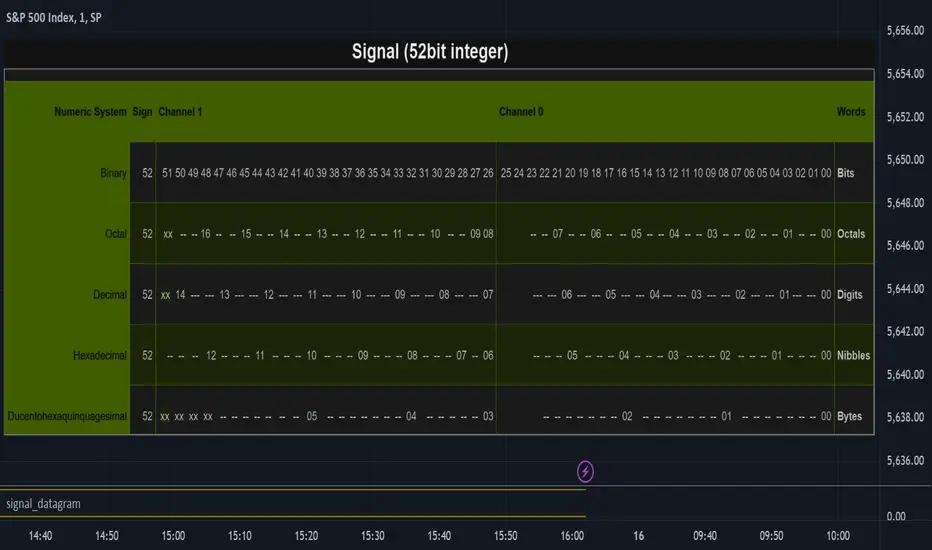

signal_datagramThe purpose of this library is to split and merge an integer into useful pieces of information that can easily handled and plotted.

The basic piece of information is one word. Depending on the underlying numerical system a word can be a bit, octal, digit, nibble, or byte.

The user can define channels. Channels are named groups of words. Multiple words can be combined to increase the value range of a channel.

A datagram is a description of the user-defined channels in an also user-defined numeric system that also contains all runtime information that is necessary to split and merge the integer.

This library simplifies the communication between two scripts by allowing the user to define the same datagram in both scripts.

On the sender's side, the channel values can be merged into one single integer value called signal. This signal can be 'emitted' using the plot function. The other script can use the 'input.source' function to receive that signal.

On the receiver's end based on the same datagram, the signal can be split into several channels. Each channel has the piece of information that the sender script put.

In the example of this library, we use two channels and we have split the integer in half. However, the user can add new channels, change them, and give meaning to them according to the functionality he wants to implement and the type of information he wants to communicate.

Nowadays many 'input.source' calls are allowed to pass information between the scripts, When that is not a price or a floating value, this library is very useful.

The reason is that most of the time, the convention that is used is not clear enough and it is easy to do things the wrong way or break them later on.

With this library validation checks are done during the initialization minimizing the possibility of error due to some misconceptions.

Library "signal_datagram"

Conversion of a datagram type to a signal that can be "send" as a single value from an indicator to a strategy script

method init(this, positions, maxWords)

init - Initialize if the word positons array with an empty array

Namespace types: WordPosArray

Parameters:

this (WordPosArray) : - The word positions array object

positions (int ) : - The array that contains all the positions of the worlds that shape the channel

maxWords (int) : - The maximum words allowed based on the span

Returns: The initialized object

method init(this)

init - Initialize if the channels word positons map with an empty map

Namespace types: ChannelDesc

Parameters:

this (ChannelDesc) : - The channels' descriptor object

Returns: The initialized object

method init(this, numericSystem, channelDesc)

init - Initialize if the datagram

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object

numericSystem (simple string) : - The numeric system of the words to be used

channelDesc (ChannelDesc) : - The channels descriptor that contains the positions of the words that each channel consists of

Returns: The initialized object

method add_channel(this, name, positions)

add_channel - Add a new channel descriptopn with its name and its corresponding word positons to the map

Namespace types: ChannelDesc

Parameters:

this (ChannelDesc) : - The channels' descriptor object to update

name (simple string)

positions (int )

Returns: The initialized object

method set_signal(this, value)

set_signal - Set the signal value

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to update

value (int) : - The signal value to set

method get_signal(this)

get_signal - Get the signal value

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to query

Returns: The value of the signal in digits

method set_signal_sign(this, sign)

set_signal_sign - Set the signal sign

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to update

sign (int) : - The negative -1 or positive 1 sign of the underlying value

method get_signal_sign(this)

get_signal_sign - Get the signal sign

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to query

Returns: The sign of the signal value -1 if it is negative and 1 if it is possitive

method get_channel_names(this)

get_channel_names - Get an array of all channel names

Namespace types: Datagram

Parameters:

this (Datagram)

Returns: An array that has all the channel names that are used by the datagram

method set_channel_value(this, channelName, value)

set_channel_value - Set the value of the channel

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to update

channelName (simple string) : - The name of the channel to set the value to. Then name should be as described int the schemas channel descriptor

value (int) : - The channel value to set

method set_all_channels_value(this, value)

set_all_channels_value - Set the value of all the channels

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to update

value (int) : - The channel value to set

method set_all_channels_max_value(this)

set_all_channels_value - Set the value of all the channels

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to update

method get_channel_value(this, channelName)

get_channel_value - Get the value of the channel

Namespace types: Datagram

Parameters:

this (Datagram) : - The datagram object to query

channelName (simple string)

Returns: Digit group of words (bits/octals/digits/nibbles/hexes/bytes) found at the channel accodring to the schema

WordDesc

Fields:

numericSystem (series__string)

span (series__integer)

WordPosArray

Fields:

positions (array__integer)

ChannelDesc

Fields:

map (map__series__string:|WordPosArray|#OBJ)

Schema

Fields:

wordDesc (|WordDesc|#OBJ)

channelDesc (|ChannelDesc|#OBJ)

Signal

Fields:

value (series__integer)

isNegative (series__bool)

words (array__integer)

Datagram

Fields:

schema (|Schema|#OBJ)

signal (|Signal|#OBJ)

FunctionMatrixCovarianceLibrary "FunctionMatrixCovariance"

In probability theory and statistics, a covariance matrix (also known as auto-covariance matrix, dispersion matrix, variance matrix, or variance–covariance matrix) is a square matrix giving the covariance between each pair of elements of a given random vector.

Intuitively, the covariance matrix generalizes the notion of variance to multiple dimensions. As an example, the variation in a collection of random points in two-dimensional space cannot be characterized fully by a single number, nor would the variances in the `x` and `y` directions contain all of the necessary information; a `2 × 2` matrix would be necessary to fully characterize the two-dimensional variation.

Any covariance matrix is symmetric and positive semi-definite and its main diagonal contains variances (i.e., the covariance of each element with itself).

The covariance matrix of a random vector `X` is typically denoted by `Kxx`, `Σ` or `S`.

~wikipedia.

method cov(M, bias)

Estimate Covariance matrix with provided data.

Namespace types: matrix

Parameters:

M (matrix) : `matrix` Matrix with vectors in column order.

bias (bool)

Returns: Covariance matrix of provided vectors.

---

en.wikipedia.org

numpy.org

Extended Moving Average (MA) LibraryThis Extended Moving Average Library is a sophisticated and comprehensive tool for traders seeking to expand their arsenal of moving averages for more nuanced and detailed technical analysis.

The library contains various types of moving averages, each with two versions - one that accepts a simple constant length parameter and another that accepts a series or changing length parameter.

This makes the library highly versatile and suitable for a wide range of strategies and trading styles.

Moving Averages Included:

Simple Moving Average (SMA): This is the most basic type of moving average. It calculates the average of a selected range of prices, typically closing prices, by the number of periods in that range.

Exponential Moving Average (EMA): This type of moving average gives more weight to the latest data and is thus more responsive to new price information. This can help traders to react faster to recent price changes.

Double Exponential Moving Average (DEMA): This is a composite of a single exponential moving average, a double exponential moving average, and an exponential moving average of a triple exponential moving average. It aims to eliminate lag, which is a key drawback of using moving averages.

Jurik Moving Average (JMA): This is a versatile and responsive moving average that can be adjusted for market speed. It is designed to stay balanced and responsive, regardless of how long or short it is.

Kaufman's Adaptive Moving Average (KAMA): This moving average is designed to account for market noise or volatility. KAMA will closely follow prices when the price swings are relatively small and the noise is low.

Smoothed Moving Average (SMMA): This type of moving average applies equal weighting to all observations and smooths out the data.

Triangular Moving Average (TMA): This is a double smoothed simple moving average, calculated by averaging the simple moving averages of a dataset.

True Strength Force (TSF): This is a moving average of the linear regression line, a statistical tool used to predict future values from past values.

Volume Moving Average (VMA): This is a simple moving average of a volume, which can help to identify trends in volume.

Volume Adjusted Moving Average (VAMA): This moving average adjusts for volume and can be more responsive to volume changes.

Zero Lag Exponential Moving Average (ZLEMA): This type of moving average aims to eliminate the lag in traditional EMAs, making it more responsive to recent price changes.

Selector: The selector function allows users to easily select and apply any of the moving averages included in the library inside their strategy.

This library provides a broad selection of moving averages to choose from, allowing you to experiment with different types and find the one that best suits your trading strategy.

By providing both simple and series versions for each moving average, this library offers great flexibility, enabling users to pass both constant and changing length parameters as needed.

ta_mLibrary "ta_m"

This library is a Pine Script™ programmer’s tool containing calcs for my oscillators and some helper functions.

upDnIntrabarVolumesByPolarity()

Determines if the volume for an intrabar is up or down.

Returns: ( ) A tuple of two values, one of which contains the bar's volume. `upVol` is the positive volume of up bars. `dnVol` is the negative volume of down bars.

Note that when this function is designed to be called with `request.security_lower_tf()`,

which will return a tuple of "array" arrays containing up and dn volume for all the intrabars in a chart bar.

upDnIntrabarVolumesByPrice()

Determines if the intrabar volume is up or down

Returns: ( ) A tuple of two values, one of which contains the bar's volume. `upVol` is the positive volume of up bars. `dnVol` is the negative volume of down bars.

Note that when this function is designed to be called with `request.security_lower_tf()`,

which will return a tuple of "array" arrays containing up and dn volume for all the intrabars in a chart bar.

LibrarySupertrendLibrary "LibrarySupertrend"

selective_ma(condition, source, length)

Parameters:

condition (bool)

source (float)

length (int)

trendUp(source)

Parameters:

source (float)

smoothrng(source, sampling_period, range_mult)

Parameters:

source (float)

sampling_period (simple int)

range_mult (float)

rngfilt(source, smoothrng)

Parameters:

source (float)

smoothrng (float)

fusion(overallLength, rsiLength, mfiLength, macdLength, cciLength, tsiLength, rviLength, atrLength, adxLength)

Parameters:

overallLength (simple int)

rsiLength (simple int)

mfiLength (simple int)

macdLength (simple int)

cciLength (simple int)

tsiLength (simple int)

rviLength (simple int)

atrLength (simple int)

adxLength (simple int)

zonestrength(amplitude, wavelength)

Parameters:

amplitude (int)

wavelength (simple int)

atr_anysource(source, atr_length)

Parameters:

source (float)

atr_length (simple int)

supertrend_anysource(source, factor, atr_length)

Parameters:

source (float)

factor (float)

atr_length (simple int)

lib_drawing_compositesLibrary "lib_drawing_composites"

methods to draw and manage composite obejects. Based on Trendoscope's added Triangle and Polygon composite objects, fixed tostring method output to be actual json

method tostring(this, format_date, format, tz, pretty)

Converts lib_drawing_types/LineProperties object to a json string representation

Namespace types: D.Point

Parameters:

this (Point type from HeWhoMustNotBeNamed/DrawingTypes/2) : lib_drawing_types/LineProperties object

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool) : if true adds a line feed after every property and a space before properties (default: true)

Returns: string representation of lib_drawing_types/LineProperties

method tostring(this, pretty)

Converts lib_drawing_types/LabelProperties object to a json string representation

Namespace types: D.LineProperties

Parameters:

this (LineProperties type from HeWhoMustNotBeNamed/DrawingTypes/2) : lib_drawing_types/LabelProperties object

pretty (simple bool) : if true adds a line feed after every property and a space before properties (default: true)

Returns: string representation of lib_drawing_types/LabelProperties

method tostring(this, format_date, format, tz, pretty)

Converts lib_drawing_types/BoxProperties object to a json string representation

Namespace types: D.Line

Parameters:

this (Line type from HeWhoMustNotBeNamed/DrawingTypes/2) : lib_drawing_types/BoxProperties object

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool) : if true adds a line feed after every property and a space before properties (default: true)

Returns: string representation of lib_drawing_types/BoxProperties

method tostring(this, pretty)

Converts lib_drawing_types/BoxText object to a json string representation

Namespace types: D.LabelProperties

Parameters:

this (LabelProperties type from HeWhoMustNotBeNamed/DrawingTypes/2) : lib_drawing_types/BoxText object

pretty (simple bool) : if true adds a line feed after every property and a space before properties (default: true)

Returns: string representation of lib_drawing_types/BoxText

method tostring(this, format_date, format, tz, pretty)

Converts lib_drawing_types/TriangleProperties object to a json string representation

Namespace types: D.Label

Parameters:

this (Label type from HeWhoMustNotBeNamed/DrawingTypes/2) : lib_drawing_types/TriangleProperties object

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool) : if true adds a line feed after every property and a space before properties (default: true)

Returns: string representation of lib_drawing_types/TriangleProperties

method tostring(this, format_date, format, tz, pretty)

Namespace types: D.Linefill

Parameters:

this (Linefill type from HeWhoMustNotBeNamed/DrawingTypes/2)

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool)

method tostring(this, pretty)

Namespace types: D.BoxProperties

Parameters:

this (BoxProperties type from HeWhoMustNotBeNamed/DrawingTypes/2)

pretty (simple bool)

method tostring(this, pretty)

Namespace types: D.BoxText

Parameters:

this (BoxText type from HeWhoMustNotBeNamed/DrawingTypes/2)

pretty (simple bool)

method tostring(this, format_date, format, tz, pretty)

Namespace types: D.Box

Parameters:

this (Box type from HeWhoMustNotBeNamed/DrawingTypes/2)

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool)

method tostring(this, pretty)

Namespace types: DC.TriangleProperties

Parameters:

this (TriangleProperties type from robbatt/lib_drawing_composite_types/1)

pretty (simple bool)

method tostring(this, format_date, format, tz, pretty)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool)

method tostring(this, format_date, format, tz, pretty)

Namespace types: DC.Trianglefill

Parameters:

this (Trianglefill type from robbatt/lib_drawing_composite_types/1)

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool)

method tostring(this, format_date, format, tz, pretty)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool)

method tostring(this, format_date, format, tz, pretty)

Namespace types: DC.Polygonfill

Parameters:

this (Polygonfill type from robbatt/lib_drawing_composite_types/1)

format_date (simple bool)

format (simple string)

tz (simple string)

pretty (simple bool)

method delete(this)

Namespace types: DC.Trianglefill

Parameters:

this (Trianglefill type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Trianglefill

Parameters:

this (Trianglefill type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Polygonfill

Parameters:

this (Polygonfill type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

method delete(this)

Namespace types: DC.Polygonfill

Parameters:

this (Polygonfill type from robbatt/lib_drawing_composite_types/1)

method clear(this)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

method clear(this)

Namespace types: DC.Trianglefill

Parameters:

this (Trianglefill type from robbatt/lib_drawing_composite_types/1)

method clear(this)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

method clear(this)

Namespace types: DC.Polygonfill

Parameters:

this (Polygonfill type from robbatt/lib_drawing_composite_types/1)

method draw(this, is_polygon_section)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

is_polygon_section (bool)

method draw(this)

Namespace types: DC.Trianglefill

Parameters:

this (Trianglefill type from robbatt/lib_drawing_composite_types/1)

method draw(this, is_polygon)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

is_polygon (bool)

method draw(this)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

method draw(this)

Namespace types: DC.Trianglefill

Parameters:

this (Trianglefill type from robbatt/lib_drawing_composite_types/1)

method draw(this)

Namespace types: DC.Polygonfill

Parameters:

this (Polygonfill type from robbatt/lib_drawing_composite_types/1)

method draw(this)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

method draw(this)

Namespace types: DC.Polygonfill

Parameters:

this (Polygonfill type from robbatt/lib_drawing_composite_types/1)

method createCenter(this, other)

Namespace types: D.Point

Parameters:

this (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

other (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

method createCenter(this)

Namespace types: D.Point

Parameters:

this (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

method createCenter(this, other1, other2)

Namespace types: D.Point

Parameters:

this (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

other1 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

other2 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

method createLabel(this, labeltext, tooltip, properties)

Namespace types: D.Line

Parameters:

this (Line type from HeWhoMustNotBeNamed/DrawingTypes/2)

labeltext (string)

tooltip (string)

properties (LabelProperties type from HeWhoMustNotBeNamed/DrawingTypes/2)

method createLabel(this, labeltext, tooltip, properties)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

labeltext (string)

tooltip (string)

properties (LabelProperties type from HeWhoMustNotBeNamed/DrawingTypes/2)

method createTriangle(this, p2, p3, properties)

Namespace types: D.Point

Parameters:

this (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

p2 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

p3 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

properties (TriangleProperties type from robbatt/lib_drawing_composite_types/1)

method createTrianglefill(this, fill_color, transparency)

Namespace types: DC.Triangle

Parameters:

this (Triangle type from robbatt/lib_drawing_composite_types/1)

fill_color (color)

transparency (int)

method createPolygonfill(this, fill_color, transparency)

Namespace types: DC.Polygon

Parameters:

this (Polygon type from robbatt/lib_drawing_composite_types/1)

fill_color (color)

transparency (int)

method createPolygon(points, properties)

Namespace types: D.Point

Parameters:

points (Point type from HeWhoMustNotBeNamed/DrawingTypes/2)

properties (TriangleProperties type from robbatt/lib_drawing_composite_types/1)

lib_drawing_composite_typesLibrary "lib_drawing_composite_types"

User Defined Types for basic drawing structure. Other types and methods will be built on these. (added type Triangle and Polygon to )

TriangleProperties

TriangleProperties object

Fields:

border_color (series color) : Box border color. Default is color.blue

fill_color (series color) : Fill color

fill_transparency (series int)

border_width (series int) : Box border width. Default is 1

border_style (series string) : Box border style. Default is line.style_solid

xloc (series string) : defines if drawing needs to be done based on bar index or time. default is xloc.bar_index

Triangle

Triangle object

Fields:

p1 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2) : point one

p2 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2) : point two

p3 (Point type from HeWhoMustNotBeNamed/DrawingTypes/2) : point three

properties (TriangleProperties) : Triangle properties

l12 (series line) : line object created

l23 (series line) : line object created

l31 (series line) : line object created

Trianglefill

Trianglefill object

Fields:

triangle (Triangle) : to create a linefill for

fill_color (series color) : Fill color

transparency (series int) : Fill transparency range from 0 to 100

object (series linefill) : linefill object created

Polygon

Polygon object

Fields:

center (Point type from HeWhoMustNotBeNamed/DrawingTypes/2) : Point that triangles are using as common center

triangles (Triangle ) : an array of triangles that form the Polygon

Polygonfill

Polygonfill object

Fields:

_polygon (Polygon) : to create a fill for

_fills (Trianglefill ) : an array of Trianglefill objects that match the array of triangles in _polygon

VolatilityIndicatorsLibrary "VolatilityIndicators"

This is a library of Volatility Indicators .

It aims to facilitate the grouping of this category of indicators, and also offer the customized supply of

the parameters and sources, not being restricted to just the closing price.

@Thanks and credits:

1. Dynamic Zones: Leo Zamansky, Ph.D., and David Stendahl

2. Deviation: Karl Pearson (code by TradingView)

3. Variance: Ronald Fisher (code by TradingView)

4. Z-score: Veronique Valcu (code by HPotter)

5. Standard deviation: Ronald Fisher (code by TradingView)

6. ATR (Average True Range): J. Welles Wilder (code by TradingView)

7. ATRP (Average True Range Percent): millerrh

8. Historical Volatility: HPotter

9. Min-Max Scale Normalization: gorx1

10. Mean Normalization: gorx1

11. Standardization: gorx1

12. Scaling to unit length: gorx1

13. LS Volatility Index: Alexandre Wolwacz (Stormer), Fabrício Lorenz, Fábio Figueiredo (Vlad) (code by me)

14. Bollinger Bands: John Bollinger (code by TradingView)

15. Bollinger Bands %: John Bollinger (code by TradingView)

16. Bollinger Bands Width: John Bollinger (code by TradingView)

dev(source, length, anotherSource)

Deviation. Measure the difference between a source in relation to another source

Parameters:

source (float)

length (simple int) : (int) Sequential period to calculate the deviation

anotherSource (float) : (float) Source to compare

Returns: (float) Bollinger Bands Width

variance(src, mean, length, biased, degreesOfFreedom)

Variance. A statistical measurement of the spread between numbers in a data set. More specifically,

variance measures how far each number in the set is from the mean (average), and thus from every other number in the set.

Variance is often depicted by this symbol: σ2. It is used by both analysts and traders to determine volatility and market security.

Parameters:

src (float) : (float) Source to calculate variance

mean (float) : (float) Mean (Moving average)

length (simple int) : (int) The sequential period to calcule the variance (number of values in data set)

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length. Only applies when biased parameter is defined as true.

Returns: (float) Standard deviation

stDev(src, length, mean, biased, degreesOfFreedom)

Measure the Standard deviation from a source in relation to it's moving average.

In this implementation, you pass the average as a parameter, allowing a more personalized calculation.

Parameters:

src (float) : (float) Source to calculate standard deviation

length (simple int) : (int) The sequential period to calcule the standard deviation

mean (float) : (float) Moving average.

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Standard deviation

zscore(src, mean, length, biased, degreesOfFreedom)

Z-Score. A z-score is a statistical measurement that indicates how many standard deviations a data point is from

the mean of a data set. It is also known as a standard score. The formula for calculating a z-score is (x - μ) / σ,

where x is the individual data point, μ is the mean of the data set, and σ is the standard deviation of the data set.

Z-scores are useful in identifying outliers or extreme values in a data set. A positive z-score indicates that the

data point is above the mean, while a negative z-score indicates that the data point is below the mean. A z-score of

0 indicates that the data point is equal to the mean.

Z-scores are often used in hypothesis testing and determining confidence intervals. They can also be used to compare

data sets with different units or scales, as the z-score standardizes the data. Overall, z-scores provide a way to

measure the relative position of a data point in a data

Parameters:

src (float) : (float) Source to calculate z-score

mean (float) : (float) Moving average.

length (simple int) : (int) The sequential period to calcule the standard deviation

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Z-score

atr(source, length)

ATR: Average True Range. Customized version with source parameter.

Parameters:

source (float) : (float) Source

length (simple int) : (int) Length (number of bars back)

Returns: (float) ATR

atrp(length, sourceP)

ATRP (Average True Range Percent)

Parameters:

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

atrp(source, length, sourceP)

ATRP (Average True Range Percent). Customized version with source parameter.

Parameters:

source (float) : (float) Source for ATR

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

historicalVolatility(lengthATR, lengthHist)

Historical Volatility

Parameters:

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

historicalVolatility(source, lengthATR, lengthHist)

Historical Volatility

Parameters:

source (float) : (float) Source for ATR

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

minMaxNormalization(src, numbars)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

minMaxNormalization(src, numbars, minimumLimit, maximumLimit)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

In this implementation, the user explicitly provides the desired minimum (min) and maximum (max) values for the scale,

rather than using the minimum and maximum values from the data.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

minimumLimit (simple float) : (float) Minimum value to scale

maximumLimit (simple float) : (float) Maximum value to scale

Returns: (float) Normalized value

meanNormalization(src, numbars, mean)

Mean Normalization

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

mean (float) : (float) Mean of source

Returns: (float) Normalized value

standardization(src, mean, stDev)

Standardization (Z-score Normalization). How "outside the mean" values relate to the standard deviation (ratio between first and second)

Parameters:

src (float) : (float) Source to normalize

mean (float) : (float) Mean of source

stDev (float) : (float) Standard Deviation

Returns: (float) Normalized value

scalingToUnitLength(src, numbars)

Scaling to unit length

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

lsVolatilityIndex(movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int) : (float) Length for normalization

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

lsVolatilityIndex(sourcePrice, movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

sourcePrice (float) : (float) Source for measure the distance

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int)

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

bollingerBands(src, length, mult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) A tuple of Bollinger Bands, where index 1=basis; 2=basis+dev; 3=basis-dev; and dev=multiplier*stdev

bollingerBands(src, length, aMult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Also, various multipliers can be passed, thus getting more bands (instead of just 2).

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) An array of multiplies used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands, where:

index 1=basis; 2=basis+dev1; 3=basis-dev1; 4=basis+dev2, 5=basis-dev2, 6=basis+dev2, 7=basis-dev2, Nup=basis+devN, Nlow=basis-devN

and dev1, dev2, devN are ```multiplier N * stdev```

bollingerBandsB(src, length, mult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation:

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands %B

bollingerBandsB(src, length, aMult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands %B. The number of results in this array is equal the numbers of multipliers passed via parameter.

bollingerBandsW(src, length, mult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation:

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands Width

bollingerBandsW(src, length, aMult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands Width. The number of results in this array is equal the numbers of multipliers passed via parameter.

dinamicZone(source, sampleLength, pcntAbove, pcntBelow)

Get Dynamic Zones

Parameters:

source (float) : (float) Source

sampleLength (simple int) : (int) Sample Length

pcntAbove (simple float) : (float) Calculates the top of the dynamic zone, considering that the maximum values are above x% of the sample

pcntBelow (simple float) : (float) Calculates the bottom of the dynamic zone, considering that the minimum values are below x% of the sample

Returns: A tuple with 3 series of values: (1) Upper Line of Dynamic Zone;

(2) Lower Line of Dynamic Zone; (3) Center of Dynamic Zone (x = 50%)

Examples:

Risk ManagementLibrary "RiskManagement"

This library keeps your money in check, and is used for testing and later on webhook-applications too. It has four volatility functions and two of them can be used to calculate a Stop-Loss, like Average True Range. It also can calculate Position Size, and the Risk Reward Ratio. But those calculations don't take leverage into account.

position_size(portfolio, risk, entry, stop_loss, use_leverage, qty_as_integer)

This function calculates the definite amount of contracts/shares/units you should use to buy or sell. This value can used by `strategy.entry(qty)` for example.

Parameters:

portfolio (float) : This is the total amount of the currency you own, and is also used by strategy.initial_capital, for example. The amount is needed to calculate the maximum risk you are willing to take per trade.

risk (float) : This is the percentage of your Portfolio you willing to loose on a single trade. Possible values are between 0.1 and 100%. Same usecase with strategy(default_qty_type=strategy.percent_of_equity,default_qty_value=100), except its calculation the risk only.

entry (float) : This is the limit-/market-price for the investment. In other words: The price per contract/share/unit you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

use_leverage (bool) : This value is optional. When not used or when set to false then this function will let you invest your portfolio at max.

qty_as_integer (bool) : This value is optional. When set to true this function will return a value used with integers. The largest integer less than or equal to the given number. Because some Broker/Exchanges let you trade hole contracts/shares/units only.

Returns: float

position_size_currency(portfolio, risk, entry, stop_loss)

This function calculates the definite amount of currency you should use when going long or short.

Parameters:

portfolio (float) : This is the total amount of the currency you own, and is also used by strategy.initial_capital, for example. The amount is needed to calculate the maximum risk you are willing to take per trade.

risk (float) : This is the percentage of your Portfolio you willing to loose on a single trade. For example: 1 is 100% and 0,01 is 1%. Default amount is 0.02 (2%).

entry (float) : This is the limit-/market-price for the current investment. In other words: The price per contract/share/units you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

Returns: float

rrr(entry, stop_loss, take_profit)

This function calculates the Risk Reward Ratio. Common values are between 1.5 and 2.0 and you should not go lower except for very few special cases.

Parameters:

entry (float) : This is the limit-/market-price for the investment. In other words: The price per contract/share/unit you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

take_profit (float) : This is the limit-/market-price when to take profits.

Returns: float

change_in_price(length)

This function calculates the difference between price now and close price of the candle 'n' bars before that. If prices are very volatile but closed where they began, then this method would show zero volatility. Over many calculations, this method returns a reasonable measure of volatility, but will always be lower than those using the highs and lows.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

maximum_price_fluctuation(length)

This function measures volatility over most recent candles, which could be used as an estimate of risk. It may also be effective as the basis for a stop-loss or take-profit, like the ATR but it ignores the frequency of directional changes within the time interval. In other words: The difference between the highest high and lowest low over 'n' bars.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

absolute_price_changes(length)

This function measures volatility over most recent close prices. This is excellent for comparing volatility. It includes both frequency and magnitude. In other words: Sum of differences between second to last close price and last close price as absolute value for 'n' bars.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

annualized_volatility(length)

This function measures volatility over most recent close prices. Its the standard deviation of close over the past 'n' periods, times the square root of the number of periods in a year.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

AlgebraLibLibrary "AlgebraLib"

f_signaldraw(_side, _date)

: Draw a simple label with Buy or Sell signal

Parameters:

_side (string)

_date (int)

Returns: : VOID, it draws a new label

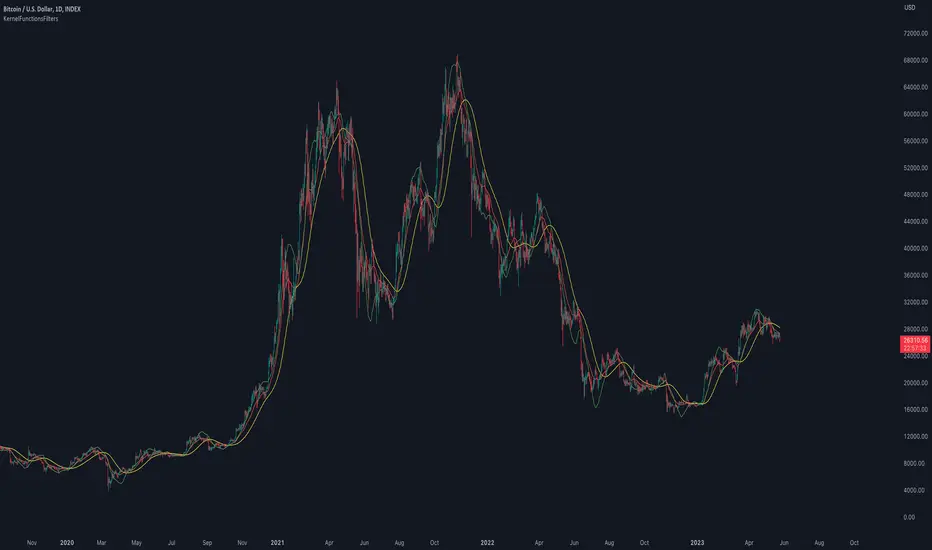

KernelFunctionsFiltersLibrary "KernelFunctionsFilters"

This library provides filters for non-repainting kernel functions for Nadaraya-Watson estimator implementations made by @jdehorty. Filters include a smoothing formula and zero lag formula. You can find examples in the code. For more information check out the original library KernelFunctions.

rationalQuadratic(_src, _lookback, _relativeWeight, startAtBar, _filter)

Parameters:

_src (float)

_lookback (simple int)

_relativeWeight (simple float)

startAtBar (simple int)

_filter (simple string)

gaussian(_src, _lookback, startAtBar, _filter)

Parameters:

_src (float)

_lookback (simple int)

startAtBar (simple int)

_filter (simple string)

periodic(_src, _lookback, _period, startAtBar, _filter)

Parameters:

_src (float)

_lookback (simple int)

_period (simple int)

startAtBar (simple int)

_filter (simple string)

locallyPeriodic(_src, _lookback, _period, startAtBar, _filter)

Parameters:

_src (float)

_lookback (simple int)

_period (simple int)

startAtBar (simple int)

_filter (simple string)

j(line1, line2)

Parameters:

line1 (float)

line2 (float)

Vector3Library "Vector3"

Representation of 3D vectors and points.

This structure is used to pass 3D positions and directions around. It also contains functions for doing common vector operations.

Besides the functions listed below, other classes can be used to manipulate vectors and points as well.

For example the Quaternion and the Matrix4x4 classes are useful for rotating or transforming vectors and points.

___

**Reference:**

- github.com

- github.com

- github.com

- www.movable-type.co.uk

- docs.unity3d.com

- referencesource.microsoft.com

- github.com

\

new(x, y, z)

Create a new `Vector3`.

Parameters:

x (float) : `float` Property `x` value, (optional, default=na).

y (float) : `float` Property `y` value, (optional, default=na).