Stochastic Ensembling of OutputsStochastic Ensembling of Outputs

🙏🏻 This is a simple tool/method that would solve naturally many well known problems:

“Price reversed 1 tick before the actual level, not executing my limit order”

“I consider intraday trend change by checking whether price is above/below VWAP, but is 1 tick enough? What to do, price is now whipsawing around vwap...”.

“I want to gradually accumulate a position around a chosen anchor. But where exactly should I put my orders? And I want to automate it ofc.“

“All these DSP adepts are telling you about some kind of noise in the markets… But how can I actually see it?”

The easy fix is to make things more analog less digital, by synthesizing numerous noise instances & adding it to any price-applied metric of yours. The ones who fw techno & psytrance, and other music, probably don’t need any more explanations. Then by checking not just 2 lines or 1 process against another one, you will be checking cloud vs cloud of lines, even allowing you to introduce proxies of probabilities. More crosses -> more confirmation to act.

How-to use:

The tool has 2 inputs: source and target:

Sources should always be the underlying process. If you apply the tool to price based metric, leave it hlcc4 unless you have a better one point estimate for each bar;

Target is your target, e.g if you want to apply it to VWAP, pick VWAP as target. You can thee on the chart above how trading activity recently never exactly touched VWAP, however noised instances of VWAP 'were' touched

The code is clean and written in modular form, you can simply copy paste it to any script of yours if you don't want to have multiple study-on-study script pairs.

^^ applied to prev days highs and lows

^^ applied to MBAD extensions and basis

^^ applied to input series itself

Here’s how it works, no ML, no “AI”, no 1k lines of code, just stats:

The problem with metrics, even if they are time aware like WMA, is that they still do not directly gain information about “changes” between datapoints. If we pick noise characteristics to match these changes, we’d effectively introduce this info into our ops.

^^ this screenshot represents 2 very different processes: a sine wave and white noise, see how the noise instances learned from each process differ significantly.

Changes can be represented as AR1 process . It’s dead simple, no PHD needed, it’s just how the current datapoint is related (or not) to the previous datapoint, no more than 1, and how this relationship holds/evolves over time. Unlike the mainstream approach like MLE, I estimate this relationship (phi parameter) via MoM but giving more weights to more recent datapoints via exponential smoothing over all the data available on your charts (so I encode temporal information), algocomplexity is O(1), lighting fast, just one pass. <- that gives phi , we’d use it as color for our noise generator

Then we just need to estimate noise amplitude ( gamma ) via checking what AR1 model actually thought vs the reality, variance of these innovations. Same via exponential smoothing, time aware, O(1), one pass, it’s all it does.

Then we generate white gaussian noise, and apply 2 estimated parameters (phi and gamma), and that’s all.

Omg, I think I just made my first real DSP script xd

Just like Monte Carlo for risk management, this is so simple and natural I can’t believe so many “pros” hide it and never talk about it in open access. Sharing it here on TradingView would’ve not done anything critical for em, but many would’ve benefited.

∞

Noise

Kalman Adaptive Score Overlay [BackQuant]Kalman Adaptive Score Overlay

A powerful indicator that uses adaptive scoring to assess market conditions and trends, utilizing advanced filtering techniques to smooth price data, enhance trend-following precision, and predict future price movements based on past data. It is ideal for traders who need a dynamic and responsive trend analysis tool that adjusts to market fluctuations.

What is Adaptive Scoring?

Adaptive scoring is a technique that adjusts the weight or importance of certain price movements over time based on an ongoing assessment of market behavior. This indicator uses dynamic scoring to assess the strength and direction of price movements, providing insight into whether a trend is likely to continue or reverse. The score is recalculated continuously to reflect the most up-to-date market conditions, offering a responsive approach to trend-following.

How It Works

The core of this indicator is built on advanced filtering methods that smooth price data, adjusting the response to recent price changes. The filtering mechanism incorporates a Kalman filter to reduce noise and improve the accuracy of price signals. Combined with adaptive scoring, this creates a robust framework that automatically adjusts to both short-term fluctuations and long-term trends.

The indicator also uses a dynamic trend-following component that updates its analysis based on the direction of the market, with the option to visualize it through colored candles. When a strong trend is identified, the candles are painted to reflect the prevailing trend, helping traders quickly identify whether the market is in a bullish or bearish state.

Why Adaptive Scoring Is Important

Dynamic Response: Adaptive scoring allows the indicator to respond to changing market conditions. By adjusting its sensitivity to price fluctuations, it ensures that trends are captured accurately, without being overly influenced by short-term noise.

Trend Precision: By combining Kalman filtering with adaptive scoring, the indicator offers a precise and smooth trend-following mechanism. It helps traders stay aligned with the market direction and avoid false signals.

Versatility: The indicator works across multiple timeframes, making it adaptable to different trading strategies, from scalping to long-term trend-following.

Confidence in Market Moves: The adaptive scoring component provides traders with confidence in the strength of the trend, helping them determine when to enter or exit positions with greater certainty.

How Traders Use It

Trend-Following Strategy: Traders can use this indicator to confirm trends and refine their entries and exits. The colored candles and adaptive scoring offer a visual cue of trend strength and direction, making it easier to follow the prevailing market movement.

Multi-Timeframe Analysis: The script supports multi-timeframe analysis, allowing traders to analyze trends and scores across different timeframes (e.g., 1m, 5m, 15m, 30m, 1h, 4h, 12h). This is useful for traders who want to confirm trends on both short and long-term charts before making a trade.

Refining Entry Points: By utilizing the adaptive scoring, traders can identify potential entry points where the score indicates a high probability of trend continuation. Higher scores signal stronger trends, guiding decision-making.

Managing Risk: Traders can use the adaptive scoring system to assess trend stability and adjust their risk management strategies accordingly. For example, higher confidence in the trend allows for larger positions, while lower confidence may require smaller, more cautious trades.

Key Features and Benefits

Kalman Filter for Noise Reduction: The Kalman filter helps to smooth out market noise and allows for a clearer understanding of the underlying price movements. This is particularly useful in volatile markets where short-term fluctuations can cloud trend analysis.

Adaptive Scoring for Flexibility: Adaptive scoring ensures that the indicator remains responsive to changing market conditions. It automatically adjusts to the strength of price movements, enabling better detection of trends and reversals.

Visual Trend Signals: The indicator provides visual signals through candle coloring, making it easier to identify whether the market is in a bullish, neutral, or bearish phase.

Multi-Timeframe Display: The indicator’s multi-timeframe feature allows traders to see the trend and adaptive score on different timeframes simultaneously, providing a comprehensive view of the market.

Customizable Settings: Traders can customize the indicator’s settings, such as the filter parameters, scoring thresholds, and visualization options, tailoring it to their specific trading style and strategy.

Why This is Important for Traders

Improved Decision Making: The adaptive nature of the scoring system allows traders to make more informed decisions based on real-time market data, without being influenced by past volatility.

Market Clarity: By smoothing out price movements and scoring trends adaptively, the indicator provides a clearer picture of market behavior, which is essential for effective trend-following and timing entries and exits.

Increased Confidence in Signals: Adaptive scoring ensures that signals are based on the current market structure, reducing the likelihood of false positives. This boosts traders' confidence when acting on signals.

Conclusion

The Kalman Adaptive Score Overlay offers a dynamic and responsive trend-following tool that integrates Kalman filtering with adaptive scoring. By adjusting to market fluctuations in real time, it allows traders to identify and follow trends with greater precision. Whether you are trading on short or long timeframes, this tool helps you stay aligned with market momentum, ensuring that your entries and exits are based on the most up-to-date and reliable data available.

Volume Sampled Supertrend [BackQuant]Volume Sampled Supertrend

A Supertrend that runs on a volume sampled price series instead of fixed time. New synthetic bars are only created after sufficient traded activity, which filters out low participation noise and makes the trend much easier to read and model.

Original Script Link

This indicator is built on top of my volume sampling engine. See the base implementation here:

Why Volume Sampling

Traditional charts print a bar every N minutes regardless of how active the tape is. During quiet periods you accumulate many small, low information bars that add noise and whipsaws to downstream signals.

Volume sampling replaces the clock with participation. A new synthetic bar is created only when a pre-set amount of volume accumulates (or, in Dollar Bars mode, when pricevolume reaches a dollar threshold). The result is a non-uniform time series that stretches in busy regimes and compresses in quiet regimes. This naturally:

filters dead time by skipping low volume chop;

standardizes the information content per bar, improving comparability across regimes;

stabilizes volatility estimates used inside banded indicators;

gives trend and breakout logic cleaner state transitions with fewer micro flips.

What this tool does

It builds a synthetic OHLCV stream from volume based buckets and then applies a Supertrend to that synthetic price. You are effectively running Supertrend on a participation clock rather than a wall clock.

Core Features

Sampling Engine - Choose Volume buckets or Dollar Bars . Thresholds can be dynamic from a rolling mean or median, or fixed by the user.

Synthetic Candles - Plots the volume sampled OHLC candles so you can visually compare against regular time candles.

Supertrend on Synthetic Price - ATR bands and direction are computed on the sampled series, not on time bars.

Adaptive Coloring - Candle colors can reflect side, intensity by volume, or a neutral scheme.

Research Panels - Table shows total samples, current bucket fill, threshold, bars-per-sample, and synthetic return stats.

Alerts - Long and Short triggers on Supertrend direction flips for the synthetic series.

How it works

Sampling

Pick Sampling Method = Volume or Dollar Bars.

Set the dynamic threshold via Rolling Lookback and Filter (Mean or Median), or enable Use Fixed and type a constant.

The script accumulates volume (or pricevolume) each time bar. When the bucket reaches the threshold, it finalizes one or more synthetic candles and resets accumulation.

Each synthetic candle stores its own OHLCV and is appended to the synthetic series used for all downstream logic.

Supertrend on the sampled stream

Choose Supertrend Source (Open, High, Low, Close, HLC3, HL2, OHLC4, HLCC4) derived from the synthetic candle.

Compute ATR over the synthetic series with ATR Period , then form upperBand = src + factorATR and lowerBand = src - factorATR .

Apply classic trailing band and direction rules to produce Supertrend and trend state.

Because bars only come when there is sufficient participation, band touches and flips tend to align with meaningful pushes, not idle prints.

Reading the display

Synthetic Volume Bars - The non-uniform candles that represent equal information buckets. Expect more candles during active sessions and fewer during lulls.

Volume Sampled Supertrend - The main line. Green when Trend is 1, red when Trend is -1.

Markers - Small dots appear when a new synthetic sample is created, useful for aligning activity cycles.

Time Bars Overlay (optional) - Plot regular time candles to compare how the synthetic stream compresses quiet chop.

Settings you will use most

Data Settings

Sampling Method - Volume or Dollar Bars.

Rolling Lookback and Filter - Controls the dynamic threshold. Median is robust to outliers, Mean is smoother.

Use Fixed and Fixed Threshold - Force a constant bucket size for consistent sampling across regimes.

Max Stored Samples - Ring buffer limit for performance.

Indicator Settings

SMA over last N samples - A moving average computed on the synthetic close series. Can be hidden for a cleaner layout.

Supertrend Source - Price field from the synthetic candle.

ATR Period and Factor - Standard Supertrend controls applied on the synthetic series.

Visuals and UI

Show Synthetic Bars - Turn synthetic candles on or off.

Candle Color Mode - Green/Red, Volume Intensity, Neutral, or Adaptive.

Mark new samples - Puts a dot when a bucket closes.

Show Time Bars - Overlay regular candles for comparison.

Paint candles according to Trend - Colors chart candles using current synthetic Supertrend direction.

Line Width , Colors , and Stats Table toggles.

Some workflow notes:

Trend Following

Set Sampling Method = Volume, Filter = Median, and a reasonable Rolling Lookback so busy regimes produce more samples.

Trade in the direction of the Volume Sampled Supertrend. Because flips require real participation, you tend to avoid micro whipsaws seen on time bars.

Use the synthetic SMA as a bias rail and trailing reference for partials or re-entries.

Breakout and Continuation

Watch for rapid clustering of new sample markers and a clean flip of the synthetic Supertrend.

The compression of quiet time and expansion in busy bursts often makes breakouts more legible than on uniform time charts.

Mean Reversion

In instruments that oscillate, faded moves against the synthetic Supertrend are easier to time when the bucket cadence slows and Supertrend flattens.

Combine with the synthetic SMA and return statistics in the table for sizing and expectation setting.

Stats table (top right)

Method and Total Samples - Sampling regime and current synthetic history length.

Current Vol or Dollar and Threshold - Live bucket fill versus the trigger.

Bars in Bucket and Avg Bars per Sample - How much time data each synthetic bar tends to compress.

Avg Return and Return StdDev - Simple research metrics over synthetic close-to-close changes.

Why this reduces noise

Time based bars treat a 5 minute print with 1 percent of average participation the same as one with 300 percent. Volume sampling equalizes bar information content. By advancing the bar only when sufficient activity occurs, you skip low quality intervals that add variance but little signal. For banded systems like Supertrend, this often means fewer false flips and cleaner runs.

Notes and tips

Use Dollar Bars on assets where nominal price varies widely over time or across symbols.

Median filter can resist single burst outliers when setting dynamic thresholds.

If you need a stable research baseline, set Use Fixed and keep the threshold constant across tests.

Enable Show Time Bars occasionally to sanity check what the synthetic stream is compressing or stretching.

Link again for reference

Original Volume Based Sampling engine:

Bottom line

When you let participation set the clock, your Supertrend reacts to meaningful flow instead of idle prints. The result is a cleaner state machine, fewer micro whipsaws, and a trend read that respects when the market is actually trading.

Volatility & Market Regimes [AlgoXcalibur]Analyze Market Conditions Like a Pro.

Volatility & Market Regimes is a specialized, institution-inspired indicator designed to help traders instantly identify the current conditions of the market with clarity and confidence.

By combining a real-time Volatility Histogram and Strength Line with a compact Regime Table, this tool reveals four essential market dimensions—Volatility, Strength, Participation, and Noise—in a clean and intuitive format. Whether you’re confirming trade setups or managing risk, knowing the current regimes enhances awareness across all assets and timeframes.

🧠 Algorithm Logic

This sophisticated tool continuously monitors four independent regimes, each reflecting a distinct dimension of market behavior:

• Volatility – Gauges how active or dormant the market is by comparing current price action movement to historical averages. A dynamic, color-gradient Volatility Histogram transitions from Low (ice blue/white) to Medium (green/yellow) to High (orange/red), giving you an immediate assessment of volatility and risk.

• Strength – Measures directional intensity by assessing trend momentum, pressure, and persistence. A color-gradient Strength Line ranges from weak (red) to strong (green), helping traders determine if directional strength is trending, weakening, or consolidating.

• Participation – Analyzes relative volume to assess the level of trader engagement. Higher volume indicates stronger participation and conviction, while low volume may signal uncertainty, fading momentum, or even liquidity traps.

• Noise – Evaluates structural stability by measuring how orderly or chaotic the price action is. High noise suggests choppy, unstable conditions, while low noise reflects clean, stable moves.

Each regime includes a High / Medium / Low classification and a color-coded directional arrow to indicate whether condition parameters are increasing or decreasing. Together, these components deliver real-time market context—helping you stay grounded in logic, not emotion.

⚙️ User-Selectable Features

Each component of the indicator—the Volatility Histogram, Strength Line, and Regime Table—can be independently made visible or hidden to match your preference. This flexibility allows you to display only the Regime Table and move it directly to your main chart, where it auto-positions to the center-right and integrates seamlessly with other AlgoXcalibur indicators that also use data tables for a cohesive and refined experience.

📊 Clarity, Not Guesswork

Volatility & Market Regimes is a unique, institution-inspired algorithm rarely seen in retail trading. Not only does it clearly display volatility—it translates complex market behavior into a clear context to reveal what’s happening behind the candles. By decoding core regimes in real-time, this tool transforms uncertainty into structured insight—empowering traders to act with clarity, not guesswork.

🔐 To get access or learn more, visit the Author’s Instructions section.

Quick scan for signal🙏🏻 Hey TV, this is QSFS, following:

^^ Quick scan for drift (QSFD)

^^ Quick scan for cycles (QSFC)

As mentioned before, ML trading is all about spotting any kind of non-randomness, and this metric (along with 2 previously posted) gonna help ya'll do it fast. This one will show you whether your time series possibly exhibits mean-reverting / consistent / noisy behavior, that can be later confirmed or denied by more sophisticated tools. This metric is O(n) in windowed mode and O(1) if calculated incrementally on each data update, so you can scan Ks of datasets w/o worrying about melting da ice.

^^ windowed mode

Now the post will be divided into several sections, and a couple of things I guess you’ve never seen or thought about in your life:

1) About Efficiency Ratios posted there on TV;

Some of you might say this is the Efficiency Ratio you’ve seen in Perry's book. Firstly, I can assure you that neither me nor Perry, just as X amount of quants all over the world and who knows who else, would say smth like, "I invented it," lol. This is just a thing you R&D when you need it. Secondly, I invite you (and mods & admin as well) to take a lil glimpse at the following screenshot:

^^ not cool...

So basically, all the Efficiency Ratios that were copypasted to our platform suffer the same bug: dudes don’t know how indexing works in Pine Script. I mean, it’s ok, I been doing the same mistakes as well, but loxx, cmon bro, you... If you guys ever read it, the lines 20 and 22 in da code are dedicated to you xD

2) About the metric;

This supports both moving window mode when Length > 0 and all-data expanding window mode when Length < 1, calculating incrementally from the very first data point in the series: O(n) on history, O(1) on live updates.

Now, why do I SQRT transform the result? This is a natural action since the metric (being a ratio in essence) is bounded between 0 and 1, so it can be modeled with a beta distribution. When you SQRT transform it, it still stays beta (think what happens when you apply a square root to 0.01 or 0.99), but it becomes symmetric around its typical value and starts to follow a bell-shaped curve. This can be easily checked with a normality test or by applying a set of percentiles and seeing the distances between them are almost equal.

Then I noticed that on different moving window sizes, the typical value of the metric seems to slide: higher window sizes lead to lower typical values across the moving windows. Turned out this can be modeled the same way confidence intervals are made. Lines 34 and 35 explain it all, I guess. You can see smth alike on an autocorrelogram. These two match the mean & mean + 1 stdev applied to the metric. This way, we’ve just magically received data to estimate alpha and beta parameters of the beta distribution using the method of moments. Having alpha and beta, we can now estimate everything further. Btw, there’s an alternative parameterization for beta distributions based on data length.

Now what you’ll see next is... u guys actually have no idea how deep and unrealistically minimalistic the underlying math principles are here.

I’m sure I’m not the only one in the universe who figured it out, but the thing is, it’s nowhere online or offline. By calculating higher-order moments & combining them, you can find natural adaptive thresholds that can later be used for anomaly detection/control applications for any data. No hardcoded thresholds, purely data-driven. Imma come back to this in one of the next drops, but the truest ones can already see it in this code. This way we get dem thresholds.

Your main thresholds are: basis, upper, and lower deviations. You can follow the common logic I’ve described in my previous scripts on how to use them. You just register an event when the metric goes higher/lower than a certain threshold based on what you’re looking for. Then you take the time series and confirm a certain behavior you were looking for by using an appropriate stat test. Or just run a certain strategy.

To avoid numerous triggers when the metric jitters around a threshold, you can follow this logic: forget about one threshold if touched, until another threshold is touched.

In general, when the metric gets higher than certain thresholds, like upper deviation, it means the signal is stronger than noise. You confirm it with a more sophisticated tool & run momentum strategies if drift is in place, or volatility strategies if there’s no drift in place. Otherwise, you confirm & run ~ mean-reverting strategies, regardless of whether there’s drift or not. Just don’t operate against the trend—hedge otherwise.

3) Flex;

Extension and limit thresholds based on distribution moments gonna be discussed properly later, but now you can see this:

^^ magic

Look at the thresholds—adaptive and dynamic. Do you see any optimizations? No ML, no DL, closed-form solution, but how? Just a formula based on a couple of variables? Maybe it’s just how the Universe works, but how can you know if you don’t understand how fundamentally numbers 3 and 15 are related to the normal distribution? Hm, why do they always say 3 sigmas but can’t say why? Maybe you can be different and say why?

This is the primordial power of statistical modeling.

4) Thanks;

I really wanna dedicate this to Charlotte de Witte & Marion Di Napoli, and their new track "Sanctum." It really gets you connected to the Source—I had it in my soul when I was doing all this ∞

Noise Footprint ImbalanceNoise Footprint Imbalance Indicator

The Noise Footprint Imbalance Indicator highlights areas of imbalance in price action, marking potential zones of support and resistance. This indicator helps traders visualize "footprints" of imbalance on the chart, allowing for better identification of areas where price moves significantly away from equilibrium. This can help traders pinpoint potential reversal points or zones where buyers or sellers may step in.

Features

Customizable Box Count: Choose the maximum number of imbalance zones displayed on the chart, keeping your workspace clear and focused.

Imbalance Detection: Highlights both top and bottom imbalances, identifying them based on price discrepancies between open/close and high/low levels.

Dynamic Zone Boxes: Draws boxes around imbalance zones with customizable colors and transparency, providing visual clarity without overwhelming the chart.

Usage

This indicator is beneficial for traders who:

Use imbalance zones as potential areas of interest for entries or exits.

Want to combine it with other indicators or price action analysis to improve trade setups.

Customization Options

Maximum Imbalance Zones: Adjusts the maximum number of imbalance boxes shown.

Imbalance Box Color: Customize the color and transparency of the imbalance zones to suit your chart's theme.

Add this script to your chart to enhance your technical analysis and bring more structure to your trading approach with the Noise Footprint Imbalance Indicator.

Total Death and Golden Crosses Calculator The Indicator calculates the total number of the death and golden crosses in the total chart which can help the moving average user to compare the number of signals generated by the moving average pair in the given timeframe.

All you need is to plot any two moving average then change the source of the indicator to get the total number of crosses.

If Indicator is not plotting anything then right click on the indicator's scale and click on "Auto(data fits the screen" option.

Signal to Noise TrendSignal to Noise Ratio

The Signal to Noise Ratio or SNR is used to assess the quality of information or data by comparing the strength of a useful signal to the presence of background noise or random variations.

In Finance the SNR refers to the ratio of strength of a trading signal to the background noise. A high SNR suggest a clear and reliable signal, meanwhile a low SNR indicates more noise (random fluctuations, volatility, or randomness).

Signal To Noise Trend

This indicator basically calculates the signal to noise of returns and then gets the Z-Score of the signal to noise ratio to find extremes levels of signal and noise. The Lines basically are standard deviations from the mean. 1,2,3 Are standard deviations same with the -1,-2,-3 Lines.

The signal is expressed as the positive Z-Score value, and the Noise is the negative Z-Score Value.

The moving average enhances the indicator ability to display the trend of returns and the trend strength. It provides a smooth representation of the Signal to Nose Ratio values.

There are more trending conditions when there is a higher signal, and there is more "ranging" conditions when there is more noise present in the markets.

The Standard deviations help find extreme levels of signal and noise. If the noise reaches the standard deviation of -3 then that means that there is a extreme negative deviation from the mean, and this would be a rare occurrence, with a lot of noise. This could indicate a potential reversion in market states, and could be followed by a trending move.

Another example is that if the Z-Score value reaches a Standard deviation of 3, this could mean that there is extremely strong and rare signal, and could potentially mean a change to a more noisy environment soon.

White NoiseThe "White Noise" indicator is designed to visualize the dispersion of price movements around a moving average, providing insights into market noise and potential trend changes. It highlights periods of increased volatility or noise compared to the underlying trend.

Code Explanation:

Inputs:

mlen: Input for the length of the noise calculation.

hlen: Input for the length of the Hull moving average.

col_up: Input for the color of the up movement.

col_dn: Input for the color of the down movement.

Calculations:

ma: Calculate the simple moving average of the high, low, and close prices (hlc3) over the specified mlen period.

dist: Calculate the percentage distance between the hlc3 and the moving average ma, then scale it by 850. This quantifies the deviation from the moving average as a value.

sm: Smooth the calculated dist values using a weighted moving average (WMA) twice, with different weights, and subtract one from the other. This provides a smoothed representation of the dispersion.

Coloring:

col_wn: Determine the color of the bars based on whether dist is positive or negative and whether it's greater or less than the smoothed sm value. This creates color-coded columns indicating upward or downward movements with varying opacity.

col_switch: Define the color for the current trend state. It switches color when the smoothed sm crosses above or below its previous value, indicating potential trend changes.

col_switch2: Define the color for the horizontal line that separates the two trend states. It switches color based on the same crossover and crossunder conditions as col_switch.

Plots:

plot(dist): Plot the dispersion values as columns with color defined by col_wn.

plot(sm): Plot the smoothed dispersion line with a white color and thicker linewidth.

plot(sm ): Plot the previous smoothed dispersion value with a lighter white color to create a visual distinction.

Usage:

This indicator can help traders identify periods of increased market noise, visualize potential trend reversals, and assess the strength of price movements around the moving average. The colored columns and smoothed line offer insights into the ebb and flow of market sentiment, aiding in decision-making.

ps. This can be used as a long-term TPI component if you dabble in Modern Portfolio Theory (MPT)

Recommended for timeframes on the 1D or above:

NET on Variety Moving Averages [Loxx]NET (Noise Elimination Technology) on Variety Moving Averages is a moving average indicator that applies John Ehlers' NET (Noise Elimination Technology) to your choice of 36 different moving averages.

█ What is NET (Noise Elimination Technology)?

Noise Elimination Technology (NET) is a method introduced by John Ehlers to enhance the clarity of technical indicators by removing noise without resorting to filtering. Here's a more detailed explanation:

Purpose of Technical Indicators: Technical indicators aim to provide insights into market inefficiencies, assisting traders in making informed decisions. However, many indicators are inherently noisy due to their reliance on a limited amount of data.

Traditional Noise Removal: Noise in indicators is typically removed using smoothing filters. While these filters can reduce noise, they introduce lag, leading to potentially delayed trading decisions which can be costly.

NET's Approach: NET offers a solution to this problem by using the nonlinearity of a rank-ordered Kendall correlation. Instead of filtering, NET clarifies indicators by focusing on their main direction and stripping out noise components.

Kendall Correlation: This is a statistical method that compares the ranked order of two sets of random variables. These pairs of ranked variables can be either concordant or discordant. In the context of NET:

The "y" variable represents a straight line with a positive slope.

The "x" variable is the output of the technical indicator.

When applied, the Kendall correlation in this configuration removes noise components that don't align with the primary direction of the indicator.

NET's Mechanism:

The "y" variable (a straight line with a positive slope) and the "x" variable (indicator output) are used in the Kendall correlation.

This correlation essentially removes noise components not aligned with the main direction of the indicator in a nonlinear manner.

The effectiveness of NET lies in its ability to reduce noise without introducing lag.

Flexibility: NET is designed to be versatile and can be applied to various technical indicators. It doesn't necessarily replace traditional smoothing filters but can complement them to provide a clearer visual representation of the indicator's behavior.

In essence, NET offers a novel approach to refining technical indicators by removing noise using the principles of Kendall correlation, without the drawbacks associated with traditional smoothing filters.

█ Moving Average Types

ADXvma - Average Directional Volatility Moving Average

Ahrens Moving Average

Alexander Moving Average - ALXMA

Double Exponential Moving Average - DEMA

Double Smoothed Exponential Moving Average - DSEMA

Exponential Moving Average - EMA

Fast Exponential Moving Average - FEMA

Fractal Adaptive Moving Average - FRAMA

Hull Moving Average - HMA

IE/2 - Early T3 by Tim Tilson

Integral of Linear Regression Slope - ILRS

Instantaneous Trendline

Laguerre Filter

Leader Exponential Moving Average

Linear Regression Value - LSMA (Least Squares Moving Average)

Linear Weighted Moving Average - LWMA

McGinley Dynamic

McNicholl EMA

Non-Lag Moving Average

Parabolic Weighted Moving Average

Recursive Moving Trendline

Simple Moving Average - SMA

Sine Weighted Moving Average

Smoothed Moving Average - SMMA

Smoother

Super Smoother

Three-pole Ehlers Butterworth

Three-pole Ehlers Smoother

Triangular Moving Average - TMA

Triple Exponential Moving Average - TEMA

Two-pole Ehlers Butterworth

Two-pole Ehlers smoother

Volume Weighted EMA - VEMA

Zero-Lag DEMA - Zero Lag Double Exponential Moving Average

Zero-Lag Moving Average

Zero Lag TEMA - Zero Lag Triple Exponential Moving Average

█ Included

Bar coloring

Alerts

Channels fill

Loxx's Expanded Source Types

█ Libraries included

loxxmas - moving averages used in Loxx's indis & strats

loxxexpandedsourcetypes

Opal - Aggr.Crypto█ OVERVIEW

The Multi-Exchange Crypto Aggregator is a unique concept ticker that gathers up to 10 tickers into one. A new OPAL Chart is created as an indicator, with its own candles and information. This information is meant to be interpreted as average information in order to reduce noise from a single ticker only. Everything is automated between assets. Our script will always check and ensure that data is received for calculations; otherwise, invalid tickers are ignored. This version is designed for Crypto Perpetual markets.

█ HOW DATA SLIPPAGE/DIFFERENCE IMPACT NOISE

This new average ticker aims to reduce noise in your candles and their live movements, avoiding most of the minor/last-second spikes, especially when they don't happen on every desired exchange at the same time. Our candles have different behaviors and highlight close-open slippage/gaps, as it seems to provide a strong reaction. Those gaps represent average slippage.

█ HOW TO USE

This should help you visualize market behaviors. Volume pressures are the origin of a lot of misunderstood things. Data analysis and observations show that makers target liquidity on both sides. Time and sessions have their own logic and will always need experience, as it is basically a gigantic Tetris game. Anyway, this should help with timing confirmations or bring confidence.

█ FEATURES

Aggregated (Tickers) Candles ▸ Aggregated OHLC candles, the idea behind the script. Set desired tickers to automate in settings. Value and Var% are displayed right next to the current candle.

Aggr. Dynamics/Levels ▸ Plot some strong levels as landmarks calculated on modified price, from Volume Weighted Average Price (VWAP) to Daily aggregated Open Price. The previous day's key level is included.

Aggr. Data Markers ▸ Plot some key markers on the chart, such as Open Pressure gaps, or estimated 3-scale liquidation bubbles with 2 confirmation modes (using different filters).

Aggr. Averages ▸ Plot up to 3 averages or HLC channels for visual ease.

█ SIGN

All of our contents are shared for educational purposes only.

Wishing you success;

OPAL - Strive for Greatness

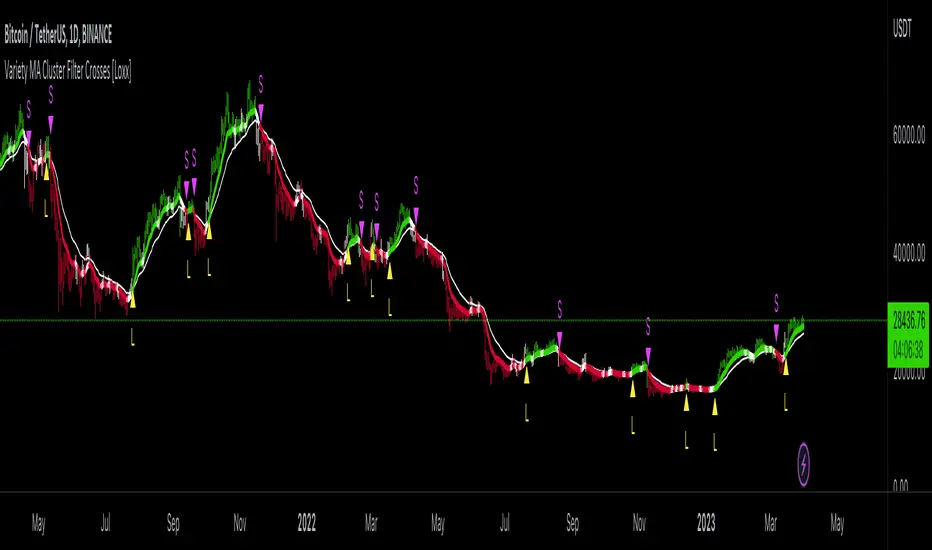

Variety MA Cluster Filter Crosses [Loxx]What is a Cluster Filter?

One of the approaches to determining a useful signal (trend) in stream data. Small filtering (smoothing) tests applied to market quotes demonstrate the potential for creating non-lagging digital filters (indicators) that are not redrawn on the last bars.

Standard Approach

This approach is based on classical time series smoothing methods. There are lots of articles devoted to this subject both on this and other websites. The results are also classical:

1. The changes in trends are displayed with latency;

2. Better indicator (digital filter) response achieved at the expense of smoothing quality decrease;

3. Attempts to implement non-lagging indicators lead to redrawing on the last samples (bars).

And whereas traders have learned to cope with these things using persistence of economic processes and other tricks, this would be unacceptable in evaluating real-time experimental data, e.g. when testing aerostructures.

The Main Problem

It is a known fact that the majority of trading systems stop performing with the course of time, and that the indicators are only indicative over certain intervals. This can easily be explained: market quotes are not stationary. The definition of a stationary process is available in Wikipedia:

A stationary process is a stochastic process whose joint probability distribution does not change when shifted in time.

Judging by this definition, methods of analysis of stationary time series are not applicable in technical analysis. And this is understandable. A skillful market-maker entering the market will mess up all the calculations we may have made prior to that with regard to parameters of a known series of market quotes.

Even though this seems obvious, a lot of indicators are based on the theory of stationary time series analysis. Examples of such indicators are moving averages and their modifications. However, there are some attempts to create adaptive indicators. They are supposed to take into account non-stationarity of market quotes to some extent, yet they do not seem to work wonders. The attempts to "punish" the market-maker using the currently known methods of analysis of non-stationary series (wavelets, empirical modes and others) are not successful either. It looks like a certain key factor is constantly being ignored or unidentified.

The main reason for this is that the methods used are not designed for working with stream data. All (or almost all) of them were developed for analysis of the already known or, speaking in terms of technical analysis, historical data. These methods are convenient, e.g., in geophysics: you feel the earthquake, get a seismogram and then analyze it for few months. In other words, these methods are appropriate where uncertainties arising at the ends of a time series in the course of filtering affect the end result.

When analyzing experimental stream data or market quotes, we are focused on the most recent data received, rather than history. These are data that cannot be dealt with using classical algorithms.

Cluster Filter

Cluster filter is a set of digital filters approximating the initial sequence. Cluster filters should not be confused with cluster indicators.

Cluster filters are convenient when analyzing non-stationary time series in real time, in other words, stream data. It means that these filters are of principal interest not for smoothing the already known time series values, but for getting the most probable smoothed values of the new data received in real time.

Unlike various decomposition methods or simply filters of desired frequency, cluster filters create a composition or a fan of probable values of initial series which are further analyzed for approximation of the initial sequence. The input sequence acts more as a reference than the target of the analysis. The main analysis concerns values calculated by a set of filters after processing the data received.

In the general case, every filter included in the cluster has its own individual characteristics and is not related to others in any way. These filters are sometimes customized for the analysis of a stationary time series of their own which describes individual properties of the initial non-stationary time series. In the simplest case, if the initial non-stationary series changes its parameters, the filters "switch" over. Thus, a cluster filter tracks real time changes in characteristics.

Cluster Filter Design Procedure

Any cluster filter can be designed in three steps:

1. The first step is usually the most difficult one but this is where probabilistic models of stream data received are formed. The number of these models can be arbitrary large. They are not always related to physical processes that affect the approximable data. The more precisely models describe the approximable sequence, the higher the probability to get a non-lagging cluster filter.

2. At the second step, one or more digital filters are created for each model. The most general condition for joining filters together in a cluster is that they belong to the models describing the approximable sequence.

3. So, we can have one or more filters in a cluster. Consequently, with each new sample we have the sample value and one or more filter values. Thus, with each sample we have a vector or artificial noise made up of several (minimum two) values. All we need to do now is to select the most appropriate value.

An Example of a Simple Cluster Filter

For illustration, we will implement a simple cluster filter corresponding to the above diagram, using market quotes as input sequence. You can simply use closing prices of any time frame.

1. Model description. We will proceed on the assumption that:

The aproximate sequence is non-stationary, i.e. its characteristics tend to change with the course of time.

The closing price of a bar is not the actual bar price. In other words, the registered closing price of a bar is one of the noise movements, like other price movements on that bar.

The actual price or the actual value of the approximable sequence is between the closing price of the current bar and the closing price of the previous bar.

The approximable sequence tends to maintain its direction. That is, if it was growing on the previous bar, it will tend to keep on growing on the current bar.

2. Selecting digital filters. For the sake of simplicity, we take two filters:

The first filter will be a variety filter calculated based on the last closing prices using the slow period. I believe this fits well in the third assumption we specified for our model.

Since we have a non-stationary filter, we will try to also use an additional filter that will hopefully facilitate to identify changes in characteristics of the time series. I've chosen a variety filter using the fast period.

3. Selecting the appropriate value for the cluster filter.

So, with each new sample we will have the sample value (closing price), as well as the value of MA and fast filter. The closing price will be ignored according to the second assumption specified for our model. Further, we select the МА or ЕМА value based on the last assumption, i.e. maintaining trend direction:

For an uptrend, i.e. CF(i-1)>CF(i-2), we select one of the following four variants:

if CF(i-1)fastfilter(i), then CF(i)=slowfilter(i);

if CF(i-1)>slowfilter(i) and CF(i-1)slowfilter(i) and CF(i-1)>fastfilter(i), then CF(i)=MAX(slowfilter(i),fastfilter(i)).

For a downtrend, i.e. CF(i-1)slowfilter(i) and CF(i-1)>fastfilter(i), then CF(i)=MAX(slowfilter(i),fastfilter(i));

if CF(i-1)>slowfilter(i) and CF(i-1)fastfilter(i), then CF(i)=fastfilter(i);

if CF(i-1)

KERPD Noise Filter - Kaufman Efficiency Ratio and Price DensityThis indicator combines Kaufman Efficiency Ratio (KER) and Price Density theories to create a unique market noise filter that is 'right on time' compared to using KER or Price Density alone. All data is normalized and merged into a single output. Additionally, this indicator provides the ability to consider background noise and background noise buoyancy to allow dynamic observation of noise level and asset specific calibration of the indicator (if desired).

The basic theory surrounding usage is that: higher values = lower noise, while lower values = higher noise in market.

Notes: NON-DIRECTIONAL Kaufman Efficiency Ratio used. Threshold period of 30 to 40 applies to Kaufman Efficiency Ratio systems if standard length of 20 is applied; maintained despite incorporation of Price Density normalized data.

TRADING USES:

-Trend strategies, mean reversion/reversal/contrarian strategies, and identification/avoidance of ranging market conditions.

-Trend strategy where KERPD is above a certain value; generally a trend is forming/continuing as noise levels fall in the market.

-Mean reversion/reversal/contrarian strategies when KERPD exits a trending condition and falls below a certain value (additional signal confluence confirming for a strong reversal in price required); generally a reversal is forming as noise levels increase in the market.

-A filter to screen out ranging/choppy conditions where breakouts are frequently fake-outs and or price fails to move significantly; noise level is high, in addition to the background buoyancy level.

-In an adaptive trading systems to assist in determining whether to apply a trend following algorithm or a mean reversion algorithm.

THEORY / THOUGHT SPACE:

The market is a jungle. When apex predators are present it often goes quiet (institutions moving price), when absent the jungle is loud.

There is always background noise that scales with the anticipation of the silence, which has features of buoyancy that act to calibrate the beginning of the silence and return to background noise conditions.

Trend traders hunt in low noise conditions. Reversion traders hunt in the onset of low noise into static conditions. Ranges can be avoided during high noise and buoyant background noise conditions.

Distance between the noise line and background noise can help inform decision making.

CALIBRATION:

- Set the Noise Threshold % color change line so that the color cut off is where your trend/reversion should begin.

- Set the Background Noise Buoyancy Calibration Decimal % to match the beginning/end of the color change Noise Threshold % line. Match the Background Noise Baseline Decimal %' to the number set for buoyancy.

- Additionally, create your own custom settings; 33/34 and 50 length also provides interesting results.

- A color change tape option can be enabled by un-commenting the lines at the bottom of this script.

Market Usage:

Stock, Crypto, Forex, and Others

Excellent for: NDQ, J225, US30, SPX

Market Conditions:

Trend, Reversal, Ranging

Adaptive ATR Keltner Channels [Loxx]Adaptive ATR Channels are adaptive Keltner channels. ATR is calculated using a rolling signal-to-noise ratio making this indicator flex more to changes in price volatility than the fixed Keltner Channels.

What is Average True Range (ATR)?

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.1

The true range is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close. The ATR is then a moving average, generally using 14 days, of the true ranges.

What are Keltner Channel (ATR)?

Keltner Channels are volatility-based bands that are placed on either side of an asset's price and can aid in determining the direction of a trend.

The Keltner channel uses the average-true range (ATR) or volatility, with breaks above or below the top and bottom barriers signaling a continuation.

Parabolic SAR of KAMA [Loxx]Parabolic SAR of KAMA attempts to reduce noise and volatility from regular Parabolic SAR in order to derive more accurate trends. In addition, and to further reduce noise and enhance trend identification, PSAR of KAMA includes two calculations of efficiency ratio: 1) price change adjusted for the daily volatility; or, 2) Jurik Fractal Dimension Adaptive (explained below)

What is PSAR?

The parabolic SAR indicator, developed by J. Wells Wilder, is used by traders to determine trend direction and potential reversals in price. The indicator uses a trailing stop and reverse method called "SAR," or stop and reverse, to identify suitable exit and entry points. Traders also refer to the indicator as to the parabolic stop and reverse, parabolic SAR, or PSAR.

What is KAMA?

Developed by Perry Kaufman, Kaufman's Adaptive Moving Average (KAMA) is a moving average designed to account for market noise or volatility. KAMA will closely follow prices when the price swings are relatively small and the noise is low. KAMA will adjust when the price swings widen and follow prices from a greater distance. This trend-following indicator can be used to identify the overall trend, time turning points and filter price movements.

What is the efficiency ratio?

In statistical terms, the Efficiency Ratio tells us the fractal efficiency of price changes. ER fluctuates between 1 and 0, but these extremes are the exception, not the norm. ER would be 1 if prices moved up 10 consecutive periods or down 10 consecutive periods. ER would be zero if price is unchanged over the 10 periods.

What is Jurik Fractal Dimension?

There is a weak and a strong way to measure the random quality of a time series.

The weak way is to use the random walk index (RWI). You can download it from the Omega web site. It makes the assumption that the market is moving randomly with an average distance D per move and proposes an amount the market should have changed over N bars of time. If the market has traveled less, then the action is considered random, otherwise it's considered trending.

The problem with this method is that taking the average distance is valid for a Normal (Gaussian) distribution of price activity. However, price action is rarely Normal, with large price jumps occuring much more frequently than a Normal distribution would expect. Consequently, big jumps throw the RWI way off, producing invalid results.

The strong way is to not make any assumption regarding the distribution of price changes and, instead, measure the fractal dimension of the time series. Fractal Dimension requires a lot of data to be accurate. If you are trading 30 minute bars, use a multi-chart where this indicator is running on 5 minute bars and you are trading on 30 minute bars.

Conclusion from the combined efforts explained above:

-PSAR is a tool that identifies trends

-To reduce noise and identify trends during periods of low volatility, we calculate a PSAR on KAMA

-To enhance noise and reduction and trend identification, we attempt to derive an efficiency ratio that is less reliant on a Normal (Gaussian) distribution of price

Included:

-Customization of all variables

-Select from two different ER calculation styles

-Multiple timeframe enabled

FiboBars ExtendedA trend indicator FiboBars Extended , the main purpose of which is to confirm the trend and cut off market noise. In his logic, he uses the Fibonacci sequence.

Two settings are used to account for noise suppression accuracy:

Period - number of calculation bars

Level - Fibonacci number selection

Trend-Quality IndicatorBINANCE:BTCUSDT

Open source version of the Trend-Quality Indicator as described by David Sepiashvili in [ Stocks & Commodities V. 22:4 (14-20) ]

Q-Indicator and B-Indicator are available both separately or together

█ OVERVIEW

The Trend-Quality indicator is a trend detection and estimation tool that is based on a two-step filtering technique. It measures cumulative price changes over term-oriented semicycles and relates them to “noise”. The approach reveals congestion and trending periods of the price movement and focuses on the most important trends, evaluating their strength in the process. The indicator is presented in a centered oscillator (Q-Indicator) and banded oscillator format (B-Indicator).

Semicycles are determined by using a short term and a longer term EMAs. The starting points for the cycles are determined by the moving averages crossover.

Cumulative price change (CPC) indicator measures the amount that the price has changed from a fixed starting point within a given semicycle. The CPC indicator is calculated as a cumulative sum of differences between the current and previous prices over the period from the fixed starting point.

The trend within the given semicycle can be found by calculating the moving average of the cumulative price change.

The noise can be defined as the average deviation of the cumulative price change from the trend. To determine linear noise, we calculate the absolute value of the difference between CPC and trend, and then smooth it over the n-point period. The root mean square noise, similar to the conventional standard deviation, can be derived by summing the squares of the difference between CPC and trend over each of the preceding n-point periods, dividing the sum by n, and calculating the square root of the result.

█ Q-INDICATOR

The Q-Indicator is a centered oscillator that fluctuates around a zero line with no upper or lower limits, is calculated by dividing trend by noise.

The Q-Indicator is intended to measure trend activity. The further the Q is from 0, the less the risk of trading with a trend, and the more reliable the trading opportunity. Values exceeding +2 or -2 can be qualified as promising

Values:

in the -1 to +1 range (GRAY) indicate that the trend is buried beneath noise. It is preferable to stay out of this zone

in the +1 to +2 or -1 to -2 range (YELLOW) indicate weak trending

in the +2 to +5 range (BLUE) or -2 to -5 range (ORANGE) indicate moderate trending

above +5 range (GREEN) or below -5 (RED) indicate strong trending

Readings exceeding strong trending levels can indicate overbought or oversold conditions and signal that price action should be monitored closely.

█ B-INDICATOR

The B-Indicator is a banded oscillator that fluctuates between 0 and 100, is calculated by dividing the absolute value of trend by noise added to absolute value of trend, and scaling the result appropriately.

The B-indicator doesn’t show the direction of price movement, but only the existence of the trend and its strength. It requires additional tools for reversal manifestations.

The indicator’s interpretation is simple. The central line suggests that the trend and noise are in equilibrium (trend is equal to noise).

Values:

below 50 (GRAY) indicate ranging market

in the 50 to 65 range (YELLOW) indicate weak trending

in the 65 to 80 range (BLUE) indicate moderate trending

above 80 (GREEN) indicate strong trending

The 65 level can be thought of as the demarcation line of trending and ranging markets and can help determine which type of technical analysis indicator (lagging or leading) is better suited to current market conditions. Readings exceeding strong trending levels can indicate overbought or oversold conditions.

Cyclic RSI High Low With Noise Filter█ OVERVIEW

This indicator displays Cyclic Relative Strength Index based on Decoding the Hidden Market Rhythm, Part 1 written by Lars von Thienen.

To determine true or false for Overbought / Oversold are unnecessary, therefore these should be either strong or weak.

Noise for weak Overbought / Oversold can be filtered, especially for smaller timeframe.

█ FEATURES

Display calculated Cyclic Relative Strength Index.

Zigzag high low based on Cyclic Relative Strength Index.

Able to filter noise for high low.

█ LEGENDS

◍ Weak Overbought / Oversold

OB ▼ = Strong Overbought

OS ▲ = Strong Oversold

█ USAGE / TIPS

Recommend to be used for Harmonic Patterns such as XABCD and ABCD.

Condition 1 (XABCD) : When ▼ and ▲ exist side by side, usually this outline XA, while the next two ◍ can be BC.

Condition 2 (ABCD) : When ▼ and ▲ exist side by side, usually this outline AB, while the next one ◍ can be BC, strong ABCD.

Condition 3 (ABCD) : When ▼ or ▲ exist at Point A, the next two ◍ can be Point B and Point C, medium ABCD.

Condition 4 (ABCD) : When ◍ exist at Point a, the next two ◍ can be Point b and Point c, weak ABCD usually used as lower case as abcd.

█ CREDITS

LoneSomeTheBlue

WhenToTrade

Rebalance OscillatorRebalancing is a common strategy to reduce risk and achieve a constant portfolio ratio between two tokens. It shifts between two values in order to keep a static ratio between them as their value oscillates.

However what is less known about rebalancing is that it provides a way to remove the noise from a signal, effectively showing us the points where to buy and to sell.

This works best in highly volatile tickers, between two tokens that are not correlated and show a high std deviation between them (i.e. XTZUSD is a better signal for this than XTZBTC).

The buying bars are marked in blue, and the selling bars are marked in red, in a similar fashion to Trading View strategy orders.

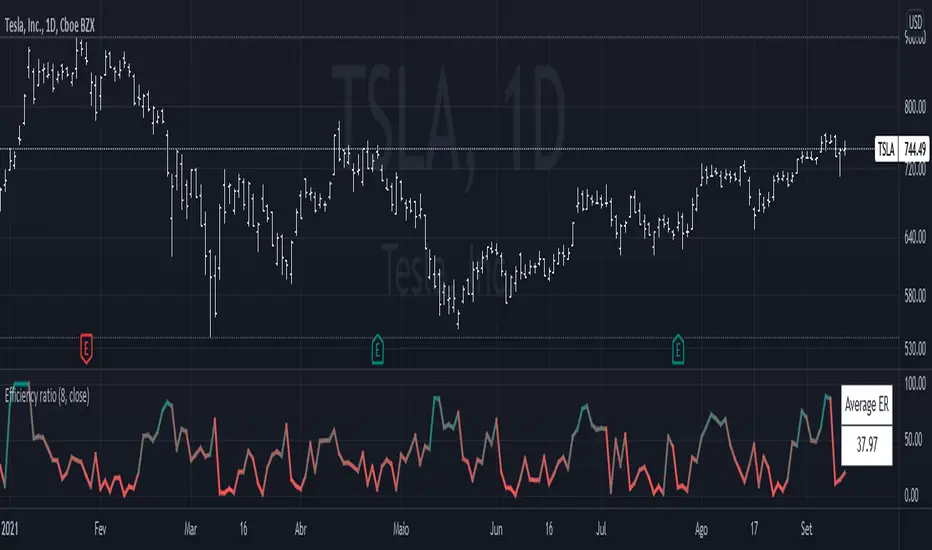

Efficiency RatioThe efficiency ratio (ER) is described by Perry Kaufman in his book, Trading Systems and Methods.

It works by measuring the momentum of the market, that is, the absolute change from the current price to a past price, and divides it by the volatility, which is the sum of the absolute changes of each bar. That makes this a bounded indicator, going from 0 to 100, like an oscillator. Higher values mean less noise, while lower values mean more.

Eg.: if the market moves from 10.0 to 15.0 in a directional manner, with every bar up, the ER is going to be at 100. However, if it moves up and down, and goes all over the place until finally reaching 15.0, the ER is going to be at around 20. It is very difficult for the ER to be at zero, because that would require 0 volatility, which is almost impossible to occur.

This indicator is useful when planning for trades. If you notice the ER being higher than average, you may choose to increase the position size, because that would mean that the market is directional and has less chance of a whipsaw.

Ehlers Noise Elimination Technology [CC]The Noise Elimination Technology Indicator was created by John Ehlers (Stocks and Commodities Dec 2020 pg 17) and he created this indicator to be used with his version of RSI but I think it works well with any price data or any indicator really.

I'm trying a new signal system due to a request from @luckyCamel58789 so let me know what you think. I now differentiate between a buy and a strong buy when the indicator increases over itself twice and vice versa. Dark green is a strong buy and light green is a regular buy. Dark red is a strong sell and light red is a regular sell.

Let me know what indicators you would like to see me publish!

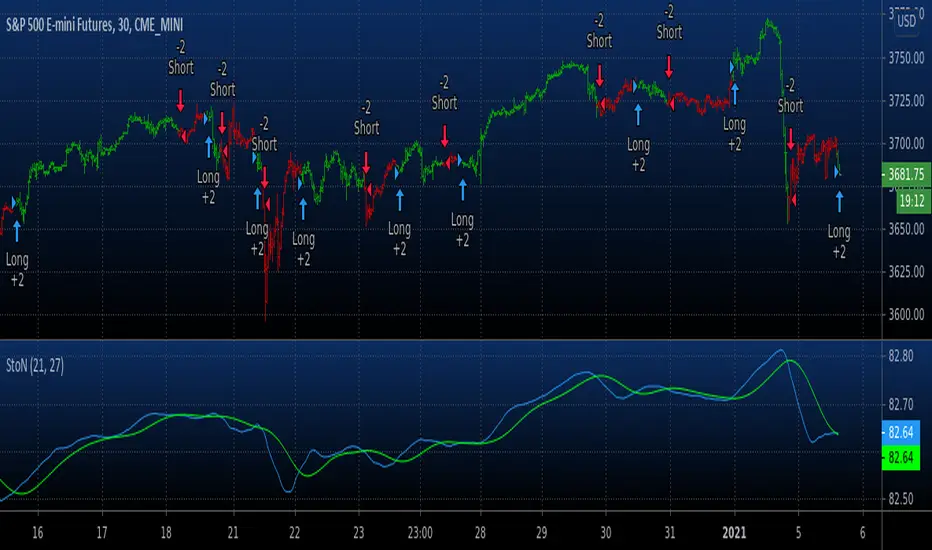

Combo Backtest 123 Reversal & Signal To Noise This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The signal-to-noise (S/N) ratio.

And Simple Moving Average.

WARNING:

- For purpose educate only

- This script to change bars colors.

Backtest Signal To Noise This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

© HPotter 05/01/2021

The signal-to-noise (S/N) ratio.

And Simple Moving Average.

Thank you for idea BlockchainYahoo

WARNING:

- For purpose educate only

- This script to change bars colors.