utilitiesLibrary "utilities"

toPercentageString(x, decimals)

: Converts a decimal number into a string formatted as percentage.

Parameters:

x (float) : (simple float): Float number to be converted

decimals (int) : (simple int): Number of decimals to apply

Returns: : Returns a string with x as percentage.

toFactorString(x, decimals)

: Converts a decimal number into a string formatted as Factor.

Parameters:

x (float) : (simple float): Float number to be converted

decimals (int) : (simple int): Number of decimals to apply

Returns: : Returns a string with x as a Factor.

toCurrencyString(x, decimals)

: Converts a decimal number into a string formatted as currency.

Parameters:

x (float) : (simple float): Float number to be converted

decimals (int) : (simple int): Number of decimals to apply

Returns: : Returns a string with x as currency.

toNumberString(x, decimals)

: Converts a decimal number into a string formatted as decimal.

Parameters:

x (float) : (simple float): Float number to be converted

decimals (int) : (simple int): Number of decimals to apply

Returns: : Returns a string with x as a decimal.

المؤشرات والاستراتيجيات

bollingerBandsLibrary "bollingerBands"

Bollinger bands related functions

get_multiple_bollinger_bands(stdv1, stdv2, stdv3, stdv4, stdv5, stdv6, stdv7, length, source)

Parameters:

stdv1 (int)

stdv2 (int)

stdv3 (int)

stdv4 (int)

stdv5 (int)

stdv6 (int)

stdv7 (int)

length (simple int)

source (float)

get_bb_volatility(bb_highest, bb_lowest, ma_length, lookback)

Parameters:

bb_highest (float)

bb_lowest (float)

ma_length (simple int)

lookback (int)

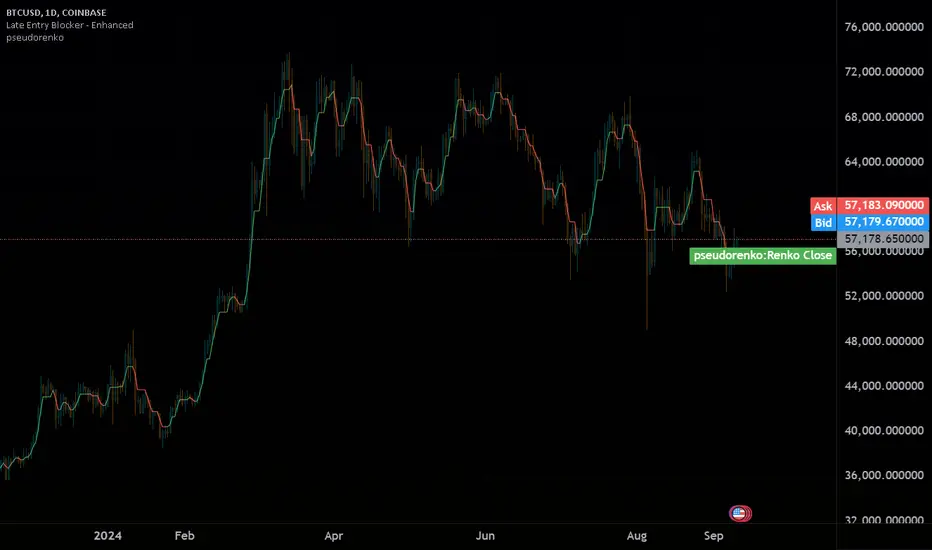

pseudorenko█ CALCULATE PSEUDO-RENKO VALUE

Calculates and returns the Pseudo-Renko Stabilized value (or close price) based on a given input value, along with the direction of the current Renko brick. This function adapts the traditional Renko brick size dynamically based on the volatility of the input value using a combination of SMA and EMA calculations. The calculated price represents the closing price of the most recent Pseudo-Renko brick, while the direction indicates the trend ( 1 for uptrend, -1 for downtrend).

Parameters:

* `val` :

* Type: ` float `

* Description: The input value upon which the Pseudo-Renko calculations are performed. You can use any price series or custom value as input.

* `sensitivity` :

* Type: ` float `

* Default Value: ` 1.0 `

* Description: Controls the sensitivity of the brick size to the volatility of the `val`. Higher values lead to larger bricks, resulting in a smoother Renko chart. Lower values produce smaller bricks, leading to a more reactive chart.

* Possible Values: Any positive float.

* `length` :

* Type: ` int `

* Default Value: ` 7 `

* Description: The length used for calculating the EMA and SMA in the dynamic brick size calculation. It influences how quickly the brick size adapts to changing volatility of the `val`.

* Possible Values: Any positive integer.

Return Values:

* `lastRenkoClose` :

* Type: ` float `

* Description: The closing price of the last completed Pseudo-Renko brick based on the `val`.

* `renkoDirection` :

* Type: ` int `

* Description: The direction of the current Pseudo-Renko brick based on the `val`:

* ` 1 `: Uptrend

* ` -1 `: Downtrend

* ` 0 `: No change (initially, or no brick change since the previous bar)

Example Usage:

//@version=5

indicator("Pseudo-Renko Stabilized (Val)", overlay=true)

// Get user inputs

sensitivityInput = input.float(0.1, "Sensitivity",0.01,step=0.01)

lengthInput = input.int(5, "Length",2)

// Example usage with the 'close' price as the input value

= pseudo_renko(math.avg(close,open), sensitivityInput, lengthInput)

// Plot the Renko close price

plot(renkoClose, "Renko Close", renkoDirection>0?color.aqua:color.orange,2)

// You can also use other values as input, such as:

// = pseudo_renko(high, sensitivityInput, lengthInput)

// = pseudo_renko(low, sensitivityInput, lengthInput)

This example demonstrates how to use the `pseudo_renko` function within an indicator. It takes user inputs for `sensitivity` and `length`, then calculates the Pseudo-Renko values using the average of the `close` and `open` prices as the `val`. The resulting `renkoClose` price is plotted on the chart, with a color change based on the `renkoDirection`. It also illustrates how you can use other values, like `high` and `low`, as input to the function.

Note: The Pseudo-Renko algorithm is based on adapting the Renko brick size dynamically based on the input `val`. This provides more flexibility compared to the normal, but is experimental. The `sensitivity` and `length` parameters, along with the choice of the `val`, offer further customization to tune the algorithm's behavior to your preference and trading style.

JordanSwindenLibraryLibrary "JordanSwindenLibrary"

TODO: add library description here

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

getPipSize(multiplier)

Calculates the pip size of the current market

Parameters:

multiplier (int) : The mintick point multiplier (1 by default, 10 for FX/Crypto/CFD but can be used to override when certain markets require)

Returns: The pip size for the current market

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float) : The number to truncate

decimalPlaces (simple float) : (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float) : The pip number to convert into a whole number

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float) : The whole number to convert into pips

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float) : The first value to reference

value2 (float) : The second value to reference

lookback (int) : The lookback period to analyze

Returns: The percent change over the two values and lookback period

random(minRange, maxRange)

Wichmann–Hill Pseudo-Random Number Generator

Parameters:

minRange (float) : The smallest possible number (default: 0)

maxRange (float) : The largest possible number (default: 1)

Returns: A random number between minRange and maxRange

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(length, maType)

Gets a Moving Average based on type (! MUST BE CALLED ON EVERY TICK TO BE ACCURATE, don't place in scopes)

Parameters:

length (simple int) : The MA period

maType (string) : The type of MA

Returns: A moving average with the given parameters

barsAboveMA(lookback, ma)

Counts how many candles are above the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(lookback, ma)

Counts how many candles are below the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently (based on closing prices)

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA (based on closing prices)

getPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

lookback (int) : The lookback period to look back over

direction (int) : The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize()

Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent()

Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(fib, colorMatch)

Checks if the current bar is a hammer candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(fib, colorMatch)

Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(wickSize, bodySize)

Checks if the current bar is a doji candle based on the given parameters

Parameters:

wickSize (float) : (default=2) The maximum top wick size compared to the bottom (and vice versa)

bodySize (float) : (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bullish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bearish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar()

Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar()

Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range

Parameters:

startTime (int) : The UNIX date timestamp to begin searching from

endTime (int) : the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze

Parameters:

monday (bool) : Should the script analyze this day? (true/false)

tuesday (bool) : Should the script analyze this day? (true/false)

wednesday (bool) : Should the script analyze this day? (true/false)

thursday (bool) : Should the script analyze this day? (true/false)

friday (bool) : Should the script analyze this day? (true/false)

saturday (bool) : Should the script analyze this day? (true/false)

sunday (bool) : Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter(atrValue, maxSize)

Parameters:

atrValue (float)

maxSize (float)

tradeCount()

Calculate total trade count

Returns: Total closed trade count

isLong()

Check if we're currently in a long trade

Returns: True if our position size is positive

isShort()

Check if we're currently in a short trade

Returns: True if our position size is negative

isFlat()

Check if we're currentlyflat

Returns: True if our position size is zero

wonTrade()

Check if this bar falls after a winning trade

Returns: True if we just won a trade

lostTrade()

Check if this bar falls after a losing trade

Returns: True if we just lost a trade

maxDrawdownRealized()

Gets the max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

Returns: The max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

totalPipReturn()

Gets the total amount of pips won/lost (as a whole number)

Returns: Total amount of pips won/lost (as a whole number)

longWinCount()

Count how many winning long trades we've had

Returns: Long win count

shortWinCount()

Count how many winning short trades we've had

Returns: Short win count

longLossCount()

Count how many losing long trades we've had

Returns: Long loss count

shortLossCount()

Count how many losing short trades we've had

Returns: Short loss count

breakEvenCount(allowanceTicks)

Count how many break-even trades we've had

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even count

longCount()

Count how many long trades we've taken

Returns: Long trade count

shortCount()

Count how many short trades we've taken

Returns: Short trade count

longWinPercent()

Calculate win rate of long trades

Returns: Long win rate (0-100)

shortWinPercent()

Calculate win rate of short trades

Returns: Short win rate (0-100)

breakEvenPercent(allowanceTicks)

Calculate break even rate of all trades

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even win rate (0-100)

averageRR()

Calculate average risk:reward

Returns: Average winning trade divided by average losing trade

unitsToLots(units)

(Forex) Convert the given unit count to lots (multiples of 100,000)

Parameters:

units (float) : The units to convert into lots

Returns: Units converted to nearest lot size (as float)

getFxPositionSize(balance, risk, stopLossPips, fxRate, lots)

(Forex) Calculate fixed-fractional position size based on given parameters

Parameters:

balance (float) : The account balance

risk (float) : The % risk (whole number)

stopLossPips (float) : Pip distance to base risk on

fxRate (float) : The conversion currency rate (more info below in library documentation)

lots (bool) : Whether or not to return the position size in lots rather than units (true by default)

Returns: Units/lots to enter into "qty=" parameter of strategy entry function

EXAMPLE USAGE:

string conversionCurrencyPair = (strategy.account_currency == syminfo.currency ? syminfo.tickerid : strategy.account_currency + syminfo.currency)

float fx_rate = request.security(conversionCurrencyPair, timeframe.period, close )

if (longCondition)

strategy.entry("Long", strategy.long, qty=zen.getFxPositionSize(strategy.equity, 1, stopLossPipsWholeNumber, fx_rate, true))

skipTradeMonteCarlo(chance, debug)

Checks to see if trade should be skipped to emulate rudimentary Monte Carlo simulation

Parameters:

chance (float) : The chance to skip a trade (0-1 or 0-100, function will normalize to 0-1)

debug (bool) : Whether or not to display a label informing of the trade skip

Returns: True if the trade is skipped, false if it's not skipped (idea being to include this function in entry condition validation checks)

fillCell(tableID, column, row, title, value, bgcolor, txtcolor, tooltip)

This updates the given table's cell with the given values

Parameters:

tableID (table) : The table ID to update

column (int) : The column to update

row (int) : The row to update

title (string) : The title of this cell

value (string) : The value of this cell

bgcolor (color) : The background color of this cell

txtcolor (color) : The text color of this cell

tooltip (string)

Returns: Nothing.

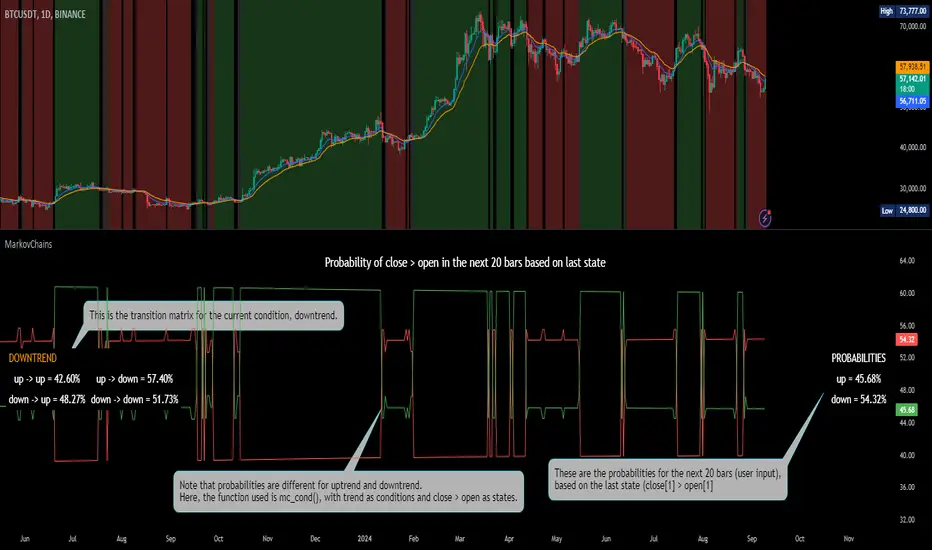

[ALGOA+] Markov Chains Library by @metacamaleoLibrary "MarkovChains"

Markov Chains library by @metacamaleo. Created in 09/08/2024.

This library provides tools to calculate and visualize Markov Chain-based transition matrices and probabilities. This library supports two primary algorithms: a rolling window Markov Chain and a conditional Markov Chain (which operates based on specified conditions). The key concepts used include Markov Chain states, transition matrices, and future state probabilities based on past market conditions or indicators.

Key functions:

- `mc_rw()`: Builds a transition matrix using a rolling window Markov Chain, calculating probabilities based on a fixed length of historical data.

- `mc_cond()`: Builds a conditional Markov Chain transition matrix, calculating probabilities based on the current market condition or indicator state.

Basically, you will just need to use the above functions on your script to default outputs and displays.

Exported UDTs include:

- s_map: An UDT variable used to store a map with dummy states, i.e., if possible states are bullish, bearish, and neutral, and current is bullish, it will be stored

in a map with following keys and values: "bullish", 1; "bearish", 0; and "neutral", 0. You will only use it to customize your own script, otherwise, it´s only for internal use.

- mc_states: This UDT variable stores user inputs, calculations and MC outputs. As the above, you don´t need to use it, but you may get features to customize your own script.

For example, you may use mc.tm to get the transition matrix, or the prob map to customize the display. As you see, functions are all based on mc_states UDT. The s_map UDT is used within mc_states´s s array.

Optional exported functions include:

- `mc_table()`: Displays the transition matrix in a table format on the chart for easy visualization of the probabilities.

- `display_list()`: Displays a map (or array) of string and float/int values in a table format, used for showing transition counts or probabilities.

- `mc_prob()`: Calculates and displays probabilities for a given number of future bars based on the current state in the Markov Chain.

- `mc_all_states_prob()`: Calculates probabilities for all states for future bars, considering all possible transitions.

The above functions may be used to customize your outputs. Use the returned variable mc_states from mc_rw() and mc_cond() to display each of its matrix, maps or arrays using mc_table() (for matrices) and display_list() (for maps and arrays) if you desire to debug or track the calculation process.

See the examples in the end of this script.

Have good trading days!

Best regards,

@metacamaleo

-----------------------------

KEY FUNCTIONS

mc_rw(state, length, states, pred_length, show_table, show_prob, table_position, prob_position, font_size)

Builds the transition matrix for a rolling window Markov Chain.

Parameters:

state (string) : The current state of the market or system.

length (int) : The rolling window size.

states (array) : Array of strings representing the possible states in the Markov Chain.

pred_length (int) : The number of bars to predict into the future.

show_table (bool) : Boolean to show or hide the transition matrix table.

show_prob (bool) : Boolean to show or hide the probability table.

table_position (string) : Position of the transition matrix table on the chart.

prob_position (string) : Position of the probability list on the chart.

font_size (string) : Size of the table font.

Returns: The transition matrix and probabilities for future states.

mc_cond(state, condition, states, pred_length, show_table, show_prob, table_position, prob_position, font_size)

Builds the transition matrix for conditional Markov Chains.

Parameters:

state (string) : The current state of the market or system.

condition (string) : A string representing the condition.

states (array) : Array of strings representing the possible states in the Markov Chain.

pred_length (int) : The number of bars to predict into the future.

show_table (bool) : Boolean to show or hide the transition matrix table.

show_prob (bool) : Boolean to show or hide the probability table.

table_position (string) : Position of the transition matrix table on the chart.

prob_position (string) : Position of the probability list on the chart.

font_size (string) : Size of the table font.

Returns: The transition matrix and probabilities for future states based on the HMM.

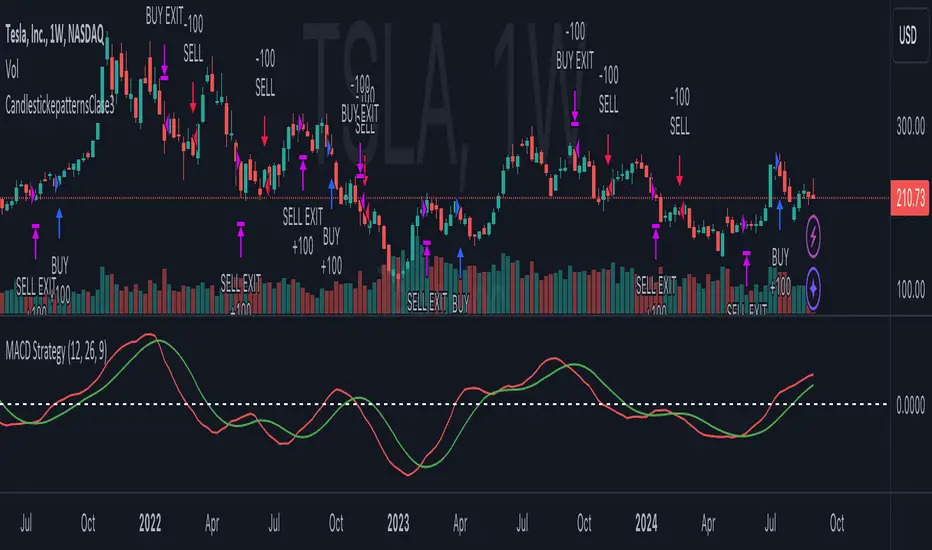

Candlestick_patternsLibrary "CandlestickepatternsClase3"

TODO: add library description here

bullish_engulfing()

bearish_engulfing()

LinTrendLibLibrary "LinTrendLib"

TODO: add library description here

ema_trend(twz, ema_length, cross_ratio, multiplier)

Given Bullish / Bearish / side-way market jugement

Parameters:

twz (int)

ema_length (simple int)

cross_ratio (float)

multiplier (float)

Returns: 1 --> bullish trend, -1 --> bearish trend, 0 --> sideway market

Color Library // AlgoFyreAlgoFyre's Color Library is a Pine Script v5 library offering fire-themed palettes with light and dark modes. It helps traders easily integrate consistent, visually appealing color schemes into TradingView indicators. Used in AlgoFyre's Scripts and Indicators.

Color Overview

The AlgoFyreColorLibrary includes a comprehensive set of colors inspired by fire, ranging from light reds and oranges to dark browns and deep reds. The library is divided into two main themes:

Light Theme:

Includes lighter shades of red, orange, and brown, suitable for use on light backgrounds.

Dark Theme:

Includes darker shades of red, orange, and brown, suitable for use on dark backgrounds.

How to Use

To use the AlgoFyreColorLibrary in your Pine Script indicators and strategies, follow these steps:

Import the Library:

Import the AlgoFyreColorLibrary at the beginning of your script.

Call the getColor Function:

Use the getColor function to retrieve the desired color with the specified transparency.

Example

//@version=5

import "AF-L-0001" as af

// Example usage of getColor function

color primaryColor = af.getColor("af_primary1", 50)

color signalColor = af.getColor("af_green", 80)

// Plotting example

plot(close, color=primaryColor, linewidth=2, title="Primary Color Line")

plot(close, color=signalColor, linewidth=2, title="Signal Color Line")

The library AF-L-0001 is imported with the alias af.

The getColor function is used to get colors with specified transparency.

The colors are then used to plot lines on the chart.

StyleLibraryLibrary "StyleLibrary"

A small library of Pine Script functions that return built-in style variables.

method sizeStyle(size)

Takes a `string` that returns the corresponding built-in size style variable.

Namespace types: series string, simple string, input string, const string

Parameters:

size (string) : A `string` representing a built-in size style: `"Tiny"`, `"Small"`, `"Normal"`, `"Large"`,

`"Huge"`, `"Auto"`.

Returns: The respective built-in size style variable.

method sizeStyle(size)

Takes a `sizeStyle` that returns the corresponding built-in size style variable.

Namespace types: series sizeStyle

Parameters:

size (series sizeStyle) : A `sizeStyle` representing a built-in size style variable.

Returns: The respective built-in size style variable.

method lineStyle(style)

Takes a `string` that returns the corresponding built-in line style variable.

Namespace types: series string, simple string, input string, const string

Parameters:

style (string) : A `string` representing a built-in line style: `"Dashed"`, `"Dotted"`, `"Solid"`.

Returns: The respective built-in line style variable.

method lineStyle(style)

Takes a `lineStyle` that returns the corresponding built-in line style variable.

Namespace types: series lineStyle

Parameters:

style (series lineStyle) : A `lineStyle` representing a built-in line style variable.

Returns: The respective built-in line style variable.

method labelStyle(style)

Takes a `string` that returns the corresponding built-in label style variable.

Namespace types: series string, simple string, input string, const string

Parameters:

style (string) : A `string` representing a built-in label style:

`"Arrow Down"`, `"Arrow Up"`, `"Circle"`, `"Cross"`, `"Diamond"`, `"Flag"`,

`"Label Center"`, `"Label Down"`, `"Label Left"`, `"Label Lower Left"`,

`"Label Lower Right"`, `"Label Right"`, `"Label Up"`, `"Label Upper Left"`,

`"Label Upper Right"`, `"None"`, `"Square"`, `"Text Outline"`, `"Triangle Down"`,

`"Triangle Up"`, `"XCross"`.

Returns: The respective built-in label style variable.

method labelStyle(style)

Takes a `labelStyle` that returns the corresponding built-in label style variable.

Namespace types: series labelStyle

Parameters:

style (series labelStyle) : A `labelStyle` representing a built-in label style variable.

Returns: The respective built-in label style variable.

method fontStyle(font)

Takes a `string` that returns the corresponding built-in font style variable.

Namespace types: series string, simple string, input string, const string

Parameters:

font (string) : A `string` representing a built-in font style: `"Default"`, `"Monospace"`.

Returns: The respective built-in font style variable.

method positionStyle(position)

Takes a `string` that returns the corresponding built-in position style variable.

Namespace types: series string, simple string, input string, const string

Parameters:

position (string) : A `string` representing a built-in position style:

`"Bottom Center", `"Bottom Left", `"Bottom Right", `"Middle Center", `"Middle Left",

`"Middle Right", `"Top Center", `"Top Left", `"Top Right".

Returns: The respective built-in position style variable.

method displayStyle(display)

Takes a `simple string` that returns the corresponding built-in display style variable.

Namespace types: simple string, input string, const string

Parameters:

display (simple string) : A `simple string` representing a built-in display style: `"All"`, `"Data Window"`,

`"None"`, `"Pane"`, `"Price Scale"`, `"Status Line"`.

Returns: The respective built-in display style variable.

WavesLibrary "Waves"

Methods for elliot wave detection

method delete(this)

deletes the subwave drawing

Namespace types: Subwave

Parameters:

this (Subwave) : Subwave object to be deleted

Returns: deleted subwave object

method delete(this)

deletes the wave drawing and the corresponding subwaves

Namespace types: Wave

Parameters:

this (Wave) : Wave object to be deleted

Returns: deleted wave object

method createWave(pivot, lineColor, waves, limit)

Create wave object

Namespace types: zg.Pivot

Parameters:

pivot (Pivot type from Trendoscope/Zigzag/7) : pivot object where the wave needs to be created

lineColor (color) : color of the wave to be drawn

waves (array) : array of existing waves

limit (int) : max number of waves to be shown in the chart

Returns: wave object created

method createSubWaves(wave, subwavePivots)

Create sub waves for the wave

Namespace types: Wave

Parameters:

wave (Wave)

subwavePivots (array) : array of sub wave pivots

Returns: wave object created

method draw(subWave)

Draw subwave

Namespace types: Subwave

Parameters:

subWave (Subwave)

Returns: subwsubWave object

method draw(wave, limitSubwaves)

Draw Wave

Namespace types: Wave

Parameters:

wave (Wave) : Wave object to be drawn

limitSubwaves (bool) : limit the number of subwave combinations within the wave

Returns: wave object

method checkMotiveWave(prices)

based on the price array, check if there is motive wave and identify the type

Namespace types: array

Parameters:

prices (array) : float array of prices

Returns: WaveType representing the identified wave type. na otherwise

method scanMotiveWave(pivot, lastPivot, existingWaves, allowedTypes)

Scan for motive wave

Namespace types: zg.Pivot

Parameters:

pivot (Pivot type from Trendoscope/Zigzag/7) : Zigzag pivot that will be checked for motive wave

lastPivot (Pivot type from Trendoscope/Zigzag/7) : previous Zigzag pivot

existingWaves (array) : array of existing waves

allowedTypes (array) : allowed Wave types to filter them

Returns: array of subwave pivots

SubwavePivots

SubwavePivots represents the sub pivots of the main wave

Fields:

waveType (series WaveType) : Type of the Wave

indices (array) : Bar index values of sub waves

subPivots (array type from Trendoscope/Zigzag/7) : sub pivot objects of the wave

Subwave

Subwave represents the drawing of sub waves

Fields:

waves (array type from Trendoscope/Drawing/1) : array of sub wave lines

points (array type from Trendoscope/Drawing/1) : Array of subwave pivot labels

subwavePivots (SubwavePivots) : array of subwave pivots being drawn

Wave

Wave object type

Fields:

pivot (Pivot type from Trendoscope/Zigzag/7) : starting point of the wave

wave (Line type from Trendoscope/Drawing/1) : Line representing the wave

waveLabel (Label type from Trendoscope/Drawing/1) : label containing wave details

subWaves (array) : array of sub waves

DrawingLibrary "Drawing"

User Defined types and methods for basic drawing structure. Consolidated from the earlier libraries - DrawingTypes and DrawingMethods

method get_price(this, bar)

get line price based on bar

Namespace types: Line

Parameters:

this (Line) : (series Line) Line object.

bar (int) : (series/int) bar at which line price need to be calculated

Returns: line price at given bar.

method init(this)

Namespace types: PolyLine

Parameters:

this (PolyLine)

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Point object to string representation

Namespace types: chart.point

Parameters:

this (chart.point) : DrawingTypes/Point object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Point

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LineProperties object to string representation

Namespace types: LineProperties

Parameters:

this (LineProperties) : DrawingTypes/LineProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LineProperties

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Line object to string representation

Namespace types: Line

Parameters:

this (Line) : DrawingTypes/Line object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Line

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LabelProperties object to string representation

Namespace types: LabelProperties

Parameters:

this (LabelProperties) : DrawingTypes/LabelProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LabelProperties

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Label object to string representation

Namespace types: Label

Parameters:

this (Label) : DrawingTypes/Label object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Label

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Linefill object to string representation

Namespace types: Linefill

Parameters:

this (Linefill) : DrawingTypes/Linefill object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Linefill

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/BoxProperties object to string representation

Namespace types: BoxProperties

Parameters:

this (BoxProperties) : DrawingTypes/BoxProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/BoxProperties

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/BoxText object to string representation

Namespace types: BoxText

Parameters:

this (BoxText) : DrawingTypes/BoxText object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/BoxText

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Box object to string representation

Namespace types: Box

Parameters:

this (Box) : DrawingTypes/Box object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Box

method delete(this)

Deletes line from DrawingTypes/Line object

Namespace types: Line

Parameters:

this (Line) : DrawingTypes/Line object

Returns: Line object deleted

method delete(this)

Deletes label from DrawingTypes/Label object

Namespace types: Label

Parameters:

this (Label) : DrawingTypes/Label object

Returns: Label object deleted

method delete(this)

Deletes Linefill from DrawingTypes/Linefill object

Namespace types: Linefill

Parameters:

this (Linefill) : DrawingTypes/Linefill object

Returns: Linefill object deleted

method delete(this)

Deletes box from DrawingTypes/Box object

Namespace types: Box

Parameters:

this (Box) : DrawingTypes/Box object

Returns: DrawingTypes/Box object deleted

method delete(this)

Deletes lines from array of DrawingTypes/Line objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Line objects

Returns: Array of DrawingTypes/Line objects

method delete(this)

Deletes labels from array of DrawingTypes/Label objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Label objects

Returns: Array of DrawingTypes/Label objects

method delete(this)

Deletes linefill from array of DrawingTypes/Linefill objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Linefill objects

Returns: Array of DrawingTypes/Linefill objects

method delete(this)

Deletes boxes from array of DrawingTypes/Box objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Box objects

Returns: Array of DrawingTypes/Box objects

method clear(this)

clear items from array of DrawingTypes/Line while deleting underlying objects

Namespace types: array

Parameters:

this (array) : array

Returns: void

method clear(this)

clear items from array of DrawingTypes/Label while deleting underlying objects

Namespace types: array

Parameters:

this (array) : array

Returns: void

method clear(this)

clear items from array of DrawingTypes/Linefill while deleting underlying objects

Namespace types: array

Parameters:

this (array) : array

Returns: void

method clear(this)

clear items from array of DrawingTypes/Box while deleting underlying objects

Namespace types: array

Parameters:

this (array) : array

Returns: void

method draw(this)

Creates line from DrawingTypes/Line object

Namespace types: Line

Parameters:

this (Line) : DrawingTypes/Line object

Returns: line created from DrawingTypes/Line object

method draw(this)

Creates lines from array of DrawingTypes/Line objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Line objects

Returns: Array of DrawingTypes/Line objects

method draw(this)

Creates label from DrawingTypes/Label object

Namespace types: Label

Parameters:

this (Label) : DrawingTypes/Label object

Returns: label created from DrawingTypes/Label object

method draw(this)

Creates labels from array of DrawingTypes/Label objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Label objects

Returns: Array of DrawingTypes/Label objects

method draw(this)

Creates linefill object from DrawingTypes/Linefill

Namespace types: Linefill

Parameters:

this (Linefill) : DrawingTypes/Linefill objects

Returns: linefill object created

method draw(this)

Creates linefill objects from array of DrawingTypes/Linefill objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Linefill objects

Returns: Array of DrawingTypes/Linefill used for creating linefills

method draw(this)

Creates box from DrawingTypes/Box object

Namespace types: Box

Parameters:

this (Box) : DrawingTypes/Box object

Returns: box created from DrawingTypes/Box object

method draw(this)

Creates labels from array of DrawingTypes/Label objects

Namespace types: array

Parameters:

this (array) : Array of DrawingTypes/Label objects

Returns: Array of DrawingTypes/Label objects

method createLabel(this, lblText, tooltip, properties)

Creates DrawingTypes/Label object from DrawingTypes/Point

Namespace types: chart.point

Parameters:

this (chart.point) : DrawingTypes/Point object

lblText (string) : Label text

tooltip (string) : Tooltip text. Default is na

properties (LabelProperties) : DrawingTypes/LabelProperties object. Default is na - meaning default values are used.

Returns: DrawingTypes/Label object

method createLine(this, other, properties)

Creates DrawingTypes/Line object from one DrawingTypes/Point to other

Namespace types: chart.point

Parameters:

this (chart.point) : First DrawingTypes/Point object

other (chart.point) : Second DrawingTypes/Point object

properties (LineProperties) : DrawingTypes/LineProperties object. Default set to na - meaning default values are used.

Returns: DrawingTypes/Line object

method createLinefill(this, other, fillColor, transparency)

Creates DrawingTypes/Linefill object from DrawingTypes/Line object to other DrawingTypes/Line object

Namespace types: Line

Parameters:

this (Line) : First DrawingTypes/Line object

other (Line) : Other DrawingTypes/Line object

fillColor (color) : fill color of linefill. Default is color.blue

transparency (int) : fill transparency for linefill. Default is 80

Returns: Array of DrawingTypes/Linefill object

method createBox(this, other, properties, textProperties)

Creates DrawingTypes/Box object from one DrawingTypes/Point to other

Namespace types: chart.point

Parameters:

this (chart.point) : First DrawingTypes/Point object

other (chart.point) : Second DrawingTypes/Point object

properties (BoxProperties) : DrawingTypes/BoxProperties object. Default set to na - meaning default values are used.

textProperties (BoxText) : DrawingTypes/BoxText object. Default is na - meaning no text will be drawn

Returns: DrawingTypes/Box object

method createBox(this, properties, textProperties)

Creates DrawingTypes/Box object from DrawingTypes/Line as diagonal line

Namespace types: Line

Parameters:

this (Line) : Diagonal DrawingTypes/PoLineint object

properties (BoxProperties) : DrawingTypes/BoxProperties object. Default set to na - meaning default values are used.

textProperties (BoxText) : DrawingTypes/BoxText object. Default is na - meaning no text will be drawn

Returns: DrawingTypes/Box object

LineProperties

Properties of line object

Fields:

xloc (series string) : X Reference - can be either xloc.bar_index or xloc.bar_time. Default is xloc.bar_index

extend (series string) : Property which sets line to extend towards either right or left or both. Valid values are extend.right, extend.left, extend.both, extend.none. Default is extend.none

color (series color) : Line color

style (series string) : Line style, valid values are line.style_solid, line.style_dashed, line.style_dotted, line.style_arrow_left, line.style_arrow_right, line.style_arrow_both. Default is line.style_solid

width (series int) : Line width. Default is 1

Line

Line object created from points

Fields:

start (chart.point) : Starting point of the line

end (chart.point) : Ending point of the line

properties (LineProperties) : LineProperties object which defines the style of line

object (series line) : Derived line object

LabelProperties

Properties of label object

Fields:

xloc (series string) : X Reference - can be either xloc.bar_index or xloc.bar_time. Default is xloc.bar_index

yloc (series string) : Y reference - can be yloc.price, yloc.abovebar, yloc.belowbar. Default is yloc.price

color (series color) : Label fill color

style (series string) : Label style as defined in Tradingview Documentation. Default is label.style_none

textcolor (series color) : text color. Default is color.black

size (series string) : Label text size. Default is size.normal. Other values are size.auto, size.tiny, size.small, size.normal, size.large, size.huge

textalign (series string) : Label text alignment. Default if text.align_center. Other allowed values - text.align_right, text.align_left, text.align_top, text.align_bottom

text_font_family (series string) : The font family of the text. Default value is font.family_default. Other available option is font.family_monospace

Label

Label object

Fields:

point (chart.point) : Point where label is drawn

lblText (series string) : label text

tooltip (series string) : Tooltip text. Default is na

properties (LabelProperties) : LabelProperties object

object (series label) : Pine label object

Linefill

Linefill object

Fields:

line1 (Line) : First line to create linefill

line2 (Line) : Second line to create linefill

fillColor (series color) : Fill color

transparency (series int) : Fill transparency range from 0 to 100

object (series linefill) : linefill object created from wrapper

BoxProperties

BoxProperties object

Fields:

border_color (series color) : Box border color. Default is color.blue

bgcolor (series color) : box background color

border_width (series int) : Box border width. Default is 1

border_style (series string) : Box border style. Default is line.style_solid

extend (series string) : Extend property of box. default is extend.none

xloc (series string) : defines if drawing needs to be done based on bar index or time. default is xloc.bar_index

BoxText

Box Text properties.

Fields:

boxText (series string) : Text to be printed on the box

text_size (series string) : Text size. Default is size.auto

text_color (series color) : Box text color. Default is color.yellow.

text_halign (series string) : horizontal align style - default is text.align_center

text_valign (series string) : vertical align style - default is text.align_center

text_wrap (series string) : text wrap style - default is text.wrap_auto

text_font_family (series string) : Text font. Default is

Box

Box object

Fields:

p1 (chart.point) : Diagonal point one

p2 (chart.point) : Diagonal point two

properties (BoxProperties) : Box properties

textProperties (BoxText) : Box text properties

object (series box) : Box object created

PolyLineProperties

Fields:

curved (series bool)

closed (series bool)

xloc (series string)

lineColor (series color)

fillColor (series color)

lineStyle (series string)

lineWidth (series int)

PolyLine

Fields:

points (array)

properties (PolyLineProperties)

object (series polyline)

lib_no_delayLibrary "lib_no_delay"

This library contains modifications to standard functions that return na before reaching the bar of their 'length' parameter.

That is because they do not compromise speed at current time for correct results in the past. This is good for live trading in short timeframes but killing applications on Monthly / Weekly timeframes if instruments, like in crypto, do not have extensive history (why would you even trade the monthly on a meme coin ... not my decision).

Also, some functions rely on source (value at previous bar), which is not available on bar 1 and therefore cascading to a na value up to the last bar ... which in turn leads to a non displaying indicator and waste of time debugging this)

Anyway ... there you go, let me know if I should add more functions.

sma(source, length)

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars (length).

Returns: Simple moving average of source for length bars back.

ema(source, length)

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars (length).

Returns: (float) The exponentially weighted moving average of the source.

rma(source, length)

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars (length).

Returns: Exponential moving average of source with alpha = 1 / length.

atr(length)

Function atr (average true range) returns the RMA of true range. True range is max(high - low, abs(high - close ), abs(low - close )). This adapted version extends ta.atr to start without delay at first bar and deliver usable data instead of na by averaging ta.tr(true) via manual SMA.

Parameters:

length (simple int) : Number of bars back (length).

Returns: Average true range.

rsi(source, length)

Relative strength index. It is calculated using the ta.rma() of upward and downward changes of source over the last length bars. This adapted version extends ta.rsi to start without delay at first bar and deliver usable data instead of na.

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars back (length).

Returns: Relative Strength Index.

ToClrToStrContains functions for conversion of color to string and vice versa:

method toClr( string this ) - converts string reperesentation of color (in hex format) to color

method toHex( color this ) - converts color to string (hex form)

method toRgb( color this ) - converts color to string ("rgb(11,11,11,0)" form)

Thanks to @ImmortalFreedom for his `color_tostring()` function from "RGB Color Fiddler"

Time Zone CorrectorThe Time Zone Corrector library provides a utility function designed to adjust time based on the user's current time zone. This library supports a wide range of time zones across the Americas, Europe, Asia, and Oceania, making it highly versatile for traders around the world. It simulates a switch-case structure using ternary operators to output the appropriate time offset relative to UTC.

Whether you're dealing with market sessions in New York, Tokyo, London, or other major trading hubs, this library helps ensure your trading algorithms can accurately account for time differences. The library is particularly useful for strategies that rely on precise timing, as it dynamically adjusts the time zone offset depending on the symbol being traded.

SessionLibrary "Session"

Helper functions for trading sessions. TradingView doesn't provide correct data when

calling some of the convenience methods like session.ismarket when you are looking at futures charts. This library corrects those mistakes by providing functions with the same names as the TradingView default properties. that reference a custom defined set of session hours for futures. It also provides a way for consumers to customize the map values by calling getSessionMap() and then overwriting (or adding) custom session definitions.

getSessionMap()

Returns a map of the futures rth & eth session hours. The map is keyed with symbol:session format (eg. ES:market or ES:overnight).

Returns: A map of futures symbols and their associated session hours.

getSessionString(session, symbol, sessionMap)

Returns a session string representing the session hours (and days) for the requested symbol (or the chart's symbol if the symbol value is not provided). If the session string is not found in the collection, it will return a blank string.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

symbol (string) : The symbol to check. Optional. Defaults to chart symbol.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

inSession(session, sessionMap, barsBack)

Returns true if the current symbol is currently in the session parameters defined by sessionString.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

barsBack (int) : Private. Only used by futures to check islastbar. Optional. The default is 0.

ismarket(sessionMap)

Returns true if the current bar is a part of the regular trading hours (i.e. market hours), false otherwise. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar()

Returns true if the current bar is the first bar of the day's session, false otherwise. If extended session information is used, only returns true on the first bar of the pre-market bars. Works for futures (TradingView's methods do not).

Returns: bool

islastbar()

Returns true if the current bar is the last bar of the day's session, false otherwise. If extended session information is used, only returns true on the last bar of the post-market bars. Works for futures (TradingView's methods do not).

Returns: bool

ispremarket(sessionMap)

Returns true if the current bar is a part of the pre-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

ispostmarket(sessionMap)

Returns true if the current bar is a part of the post-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar_regular(sessionMap)

Returns true on the first regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

islastbar_regular(sessionMap)

Returns true on the last regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isovernight(sessionMap)

Returns true if the current bar is a part of the pre-market or post-market, false otherwise. On non-intraday charts always returns false.

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

getSessionHighAndLow(session, sessionMap)

Returns a tuple containing the high and low print during the specified session.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: A tuple containing

TradingHook_LibraryLibrary "TradingHook_Library"

This library is a client script for making a webhook signal formatted string to TradingHook webhook server.

buy_message(password, amount, order_name)

Make a buy Message for TradingHook.

Parameters:

password (string) : (string) password that you set in .env file.

amount (float) : (float) amount. If not set, your strategy qty will be sent.

order_name (string) : (string) order_name. The default name is "Order".

Returns: (string) A string containing the formatted webhook message.

sell_message(password, percent, order_name)

Make a sell message for TradingHook.

Parameters:

password (string) : (string) password that you set in .env file.

percent (string) : (string) what percentage of your quantity you want to sell.

order_name (string) : (string) order_name. The default name is "Order".

Returns: (string) A string containing the formatted webhook message.

entry_message(password, amount, leverage, order_name)

Make a Entry Message for TradingHook.

Parameters:

password (string) : (string) password that you set in .env file.

amount (float) : (float) amount. If not set, your strategy qty will be sent.

leverage (int) : (int) leverage. If not set, your leverage doesn't change.

order_name (string) : (string) order_name. The default name is "Order".

Returns: (string) A string containing the formatted webhook message.

close_message(password, percent, amount, order_name)

Make a close message for TradingHook.

Parameters:

password (string) : (string) password that you set in .env file.

percent (string) : (string) what percentage of your quantity you want to close.

amount (float) : (float) quantity you want to close.

order_name (string) : (string) order_name. The default name is "Order".

Returns: (string) A string containing the formatted webhook message.

iteratorThe "Iterator" library is designed to provide a flexible way to work with sequences of values. This library offers a set of functions to create and manage iterators for various data types, including integers, floats, and more. Whether you need to generate an array of values with specific increments or iterate over elements in reverse order, this library has you covered.

Key Features:

Array Creation: Easily generate arrays of integers or floats with customizable steps, both inclusive and exclusive of the end values.

Flexible Iteration: Includes methods to iterate over arrays of different types, such as booleans, integers, floats, strings, colors, and drawing objects like lines and labels.

Reverse Iteration: Support for reverse iteration, giving you control over the order in which elements are processed.

Automatic Loop Control: One of the key advantages of this library is that when using the .iterate() method, it only loops over the array when there are values present. This means you don’t have to manually check if the array is populated before iterating, simplifying your code and reducing potential errors.

Versatile Use Cases: Ideal for scenarios where you need to loop over an array without worrying about empty arrays or checking conditions manually.

This library is particularly useful in cases where you need to perform operations on each element in an array, ensuring that your loops are efficient and free from unnecessary checks.

Library "iterator"

The "iterator" library provides a versatile and efficient set of functions for creating and managing iterators.

It allows you to generate arrays of integers or floats with customizable steps, both inclusive and exclusive of the end values.

The library also includes methods for iterating over various types, including booleans, integers, floats, strings, colors,

and drawing objects like lines and labels. With support for reverse iteration and flexible customization options.

iterator(stop, start, step)

Creates an array of integers from start to stop with a specified step, excluding the stop value.

Parameters:

stop (int) : The end value of the iterator, exclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop. Will return and empty array if start = stop.

iterator(stop, start, step)

Creates an array of floats from start to stop with a specified step, excluding the stop value.

Parameters:

stop (float) : The end value of the iterator, exclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop. Will return and empty array if start = stop.

iterator_inclusive(stop, start, step)

Creates an array of integers from start to stop with a specified step, including the stop value.

Parameters:

stop (int) : The end value of the iterator, inclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop, including the stop value.

iterator_inclusive(stop, start, step)

Creates an array of floats from start to stop with a specified step, including the stop value.

Parameters:

stop (float) : The end value of the iterator, inclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop, including the stop value.

itr(stop, start, step)

Creates an array of integers from start to stop with a specified step, excluding the stop value.

Parameters:

stop (int) : The end value of the iterator, exclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop.

itr(stop, start, step)

Creates an array of floats from start to stop with a specified step, excluding the stop value.

Parameters:

stop (float) : The end value of the iterator, exclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop.

itr_in(stop, start, step)

Creates an array of integers from start to stop with a specified step, including the stop value.

Parameters:

stop (int) : The end value of the iterator, inclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop, including the stop value.

itr_in(stop, start, step)

Creates an array of floats from start to stop with a specified step, including the stop value.

Parameters:

stop (float) : The end value of the iterator, inclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop, including the stop value.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

whookLibrary "whook"

This library provides functions for generating trading alerts for `whook`

check this -> github.com

Currently supported exchanges:

Kucoin futures

Bitget futures

Coinex futures

Bingx

OKX futures ( also its demo mode )

Bybit futures ( also Bybit testnet )

Binance futures ( also Binance futures testnet )

Phemex futures ( also Phemex testnet )

Kraken futures ( also Kraken futures testnet )

# --- Test Cases ---

Note: These test cases are for demonstration purposes only and may not cover all scenarios.

// buy(string account, float amount, string unit = "units", float leverage = 1)

buy("MyAccount", 100, "units", 1)

buy("MyAccount", 1000, "USDT", 5)

buy("MyAccount", 50, "percent", 2)

// sell(string account, float amount, string unit = "units", float leverage = 1)

sell("MyAccount", 50, "units", 1)

sell("MyAccount", 500, "USDT", 3)

sell("MyAccount", 25, "percent", 2)

// set_position(string account, float amount, string unit = "units", float leverage = 1)

set_position("MyAccount", 100, "units", 1)

set_position("MyAccount", 1000, "USDT", 5)

set_position("MyAccount", 50, "percent", 2)

// limit_buy(string account, float amount, float price, string unit = "units", float leverage = 1, string id = "")

limit_buy("MyAccount", 100, 10000, "units", 1, "MyBuyOrder")

limit_buy("MyAccount", 1000, 10500, "USDT", 5)

limit_buy("MyAccount", 50, 11000, "percent", 2)

// limit_sell(string account, float amount, float price, string unit = "units", float leverage = 1, string id = "")

limit_sell("MyAccount", 50, 10000, "units", 1, "MySellOrder")

limit_sell("MyAccount", 500, 9500, "USDT", 3)

limit_sell("MyAccount", 25, 9000, "percent", 2)

// close_percent(string account, float pct = 100)

close_percent("MyAccount", 100)

close_percent("MyAccount", 50)

buy(account, amount, unit, leverage)

Sends a trading alert to execute a market buy order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to buy (can be in USD, units, or percentage).

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

sell(account, amount, unit, leverage)

Sends a trading alert to execute a market sell order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to sell (can be in USD, units, or percentage).

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

set_position(account, amount, unit, leverage)

Sends a trading alert to set a position.

Parameters:

account (string) : The account ID.

amount (float) : The amount to set the position to (can be in USD, units, or percentage).

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

limit_buy(account, amount, price, unit, leverage, id)

Sends a trading alert to place a limit buy order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to buy (can be in USD, units, or percentage).

price (float) : The limit price.

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

id (string) : An optional custom ID for the limit order.

limit_sell(account, amount, price, unit, leverage, id)

Sends a trading alert to place a limit sell order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to sell (can be in USD, units, or percentage).

price (float) : The limit price.

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

id (string) : An optional custom ID for the limit order.

close_percent(account, pct)

Sends an alert to close a position on Phemex.

Parameters:

account (string) : The account ID.

pct (float) : The percentage of the position to close (optional, defaults to 100%).

csv_series_libraryThe CSV Series Library is an innovative tool designed for Pine Script developers to efficiently parse and handle CSV data for series generation. This library seamlessly integrates with TradingView, enabling the storage and manipulation of large CSV datasets across multiple Pine Script libraries. It's optimized for performance and scalability, ensuring smooth operation even with extensive data.

Features:

Multi-library Support: Allows for distribution of large CSV datasets across several libraries, ensuring efficient data management and retrieval.

Dynamic CSV Parsing: Provides robust Python scripts for reading, formatting, and partitioning CSV data, tailored specifically for Pine Script requirements.

Extensive Data Handling: Supports parsing CSV strings into Pine Script-readable series, facilitating complex financial data analysis.