Risk Management & Position Size Dashboard ProThis version of the dashboard system factors in trading fees to your max risk to account per trade. This comes in handy when trading very low timeframes where trade risk can be tiny and leverage high where traditional position size calculations can yield huge position sizes where just the fees can far exceed your risk appetite. This system calculates your position size factoring in fees so you will never exceed your risk settings. Details below.

****

This indicator is designed to assist traders by instantly providing the necessary information to execute orders based on defined risk parameters. This is not an indicator that tells you WHEN to buy or sell, but HOW MUCH to buy or sell based on your risk appetite. The indicator is compatible with any strategy and any instrument

The indicator uses some great pinescript features, allowing you to drag and drop your levels directly on the chart for instant feedback from the risk management dashboard. Huge timesaver.

Instructions:

1. The first time you add the indicator to your chart, you will be asked to identify your Entry, Stop and Target levels by clicking on them directly on the chart. You can at any point adjust these levels directly on the chart, or you can manually enter them in settings

2. Setup your risk profile in the indicator settings:

(a) Current Capital: Enter the current value of your trading account

(b) Max Risk Per Trade: Enter the maximum % of your Capital you want to risk per trade

(c) Max Leverage: Enter the maximum leverage you want applied to your account. This comes in handy when you trade on very low timeframes where position sizes can become very large. No matter what you enter here, position size will never exceed Max Risk Per Trade

(d) Stop Ticks: Number of ticks to use above/below the identified high/low for stops

(e) % fee per trade: enter your brokers fees here to ensure the system takes this into consideration while calculating position size

(e) Use Current Price as Entry (Market Orders): By default, the system will use the entry level you have selected for limit orders. If you want to use the system to display data based on current price for market orders, select “Use Current Price as Entry (Market Orders)”

(f) number of TP levels: enter the number of TP levels you are planning to use to ensure the fees are calculated for them

3. Based on your stop and target levels, the system will automatically determine if you're looking to long or short and accordingly display all relevant data to you.

4. Display Free Trade Level: toggle this on to display the level you should exit 50% of your position to make the trade risk free

5. Dashboard / Text size / level colours and positions are customisable

The Dashboard displays the following information at all times:

1. Entry

2. Stop

3. Trade Risk (%): Percentage price difference between Entry and Stop

4. Max Risk ($): Currency value of loss if the trade is stopped out

5. Size: Position Size to execute your trade based on your risk profile/appetite

6. Size($): Position Size in currency value

7. Total Fees: Total fees for the trade based on settings above

7. P&L($): Potential profit to your Capital in currency value

8. P&L(%): Potential profit to your Capital in %

9. Risk to account: % risk to account - used as confirmation that the max risk to your account, factoring fees is circa your risk appetite

10. R:R: Risk to Reward Ratio

11. % to Target: Percent price needs to move to achieve your target

Hope this helps you with your trading. I built this as I was tired of wasting time opening up spreadsheets or calculators to execute trades - especially on lower timeframes. Making the code open source so if you do make improvements to this I'd love to hear from you. Also open to suggestions.

Happy Trading!

Risk

Koalafied Risk ManagementTables and labels/lines showing trade levels and risk/reward. Use to manage trade risk compared to portfolio size.

Initial design optimised for tickers denominated against USD.

PrimeTrading ExposureThis indicator helps traders staying on the right side of the market and increasing their portfolio exposure as the market health improves.

Nothing kills more accounts than trying to pick a bottom by loading positions below all kma’s. What if the market rollover? Then you take a major hit on your p&l.

The goal is to increase your maximum allowable exposure as the market confirms his way above key moving averages (kma’s).

Market based maximum exposure PT rules:

■ Price < 50dma & Price > 5dma = 20%

■ Price < 50dma & Price > 21dma = 40%

■ Price > 50dma = 60%

■ Price > 50dma & Price > 21dma = 80%

■ Price > 50dma & Price > 21dma & Price > 10dma = 100%

Features

■ You can select the indices reference you prefer to calculate the max exposure ( IWM , QQQ , SPY )

■ You can see the price extension for kma’s (5,10,21,50 dma)

■ Use the current symbol or lock on your preferred reference indices

RealTime Max LeverageEver wanted a script that could tell you what is the maximum reasonably safe leverage if you were to open a trade and hold it for a given number of candles? This is it!

Using rate of change based volatility and the maximum expected number of candles/periods you will hold your trade for, based on your risk profile this indicator will tell you what is the maximum reasonable leverage.

Stop losses / take profits or some other prudent exit strategy should not be avoided. The idea is effectively to prevent yourself from using leverage that is too risky for the current market conditions on whatever timeframe you are entering your trade based on.

If you have any suggestions on how to improve the indicator, please leave a comment below!

NDS RISK MANAGEMENT (V1.0)Here is a Risk Management Program that calculates stop loss and position sizing based on NDS analysis.

Inputs:

Entry: The First Symmetry Level T1.

Entry: The Second Symmetry Level T2.

Entry: The Node 1 Level

Entry: The Node 2 Level

Entry: The 86% Level

Target: The First Symmetry Level T1

Target: The Second Symmetry Level T2.

Target:

The Node 1 Level

Target: The Node 2 Level

Target: The 86% Level

Balance: Balance Amount

Risk Level: Percent that is risked of the Balance for one Trade

Output:

Risk Per Point

Stop Loss Price

Take Profit Price

Low Risk Entry Zone

Take Profit Zone

Disclaimer

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such.

You declare to know the principles and risks of the financial markets. Therefore, you declare that you are aware of the financial risks involved in trading.

In this sense, the author can not be held responsible for errors, omissions, inappropriate investment, technical problems, events beyond his control, and, more generally, financial losses that you may realize, or results obtained in the practice of trading resulting from the markets.

Trading involves a high level of financial risk, and may not be appropriate because you may experience losses greater than your deposit. Leverage can be against you.

Do not trade with capital that you can not afford to lose. You must be aware and have a complete understanding of all the risks associated with the market and trading. We can not be held responsible for any loss you incur.

Trading also involves risks of gambling addiction.

سلب مسئولیت

این اندیکاتور /کد به منظور توصیه یا توصیه رسمی سرمایهگذاری توسط سازنده طراحی نشده است ، و همچنین نباید چنین تفسیر شود.

شما اعلام می کنید که از اصول و ریسک های بازارهای مالی مطلع هستید. بنابراین، شما اعلام میکنید که از ریسکهای مالی موجود در معاملات آگاه هستید.

در نتیجه، طراح در قبال اشتباهات، خطاها ، سرمایه گذاری نامناسب، مشکلات فنی، رویدادهای خارج از کنترل خود، و به طور کلی، خسارات مالی که ممکن است متحمل شوید هیچونگه مسیولیتی ندارد

معاملات دارای سطح بالایی از ریسک مالی است و ممکن است مناسب نباشد زیرا ممکن است زیان هایی بیشتر از سپرده خود داشته باشید. اهرم می تواند علیه شما باشد.

با سرمایه ای که نمی توانید از دست بدهید معامله نکنید. شما باید آگاه باشید و درک کاملی از تمام ریسک های مرتبط با بازار و معامله داشته باشید. ما نمی توانیم در قبال ضرر و زیان شما مسئولیتی داشته باشیم.

ترید یا معامله خطرات اعتیاد به قمار را نیز در بر دارد

trailing_drawdown

Description:

Drawdown was a tool to measure historical risk, derived from measuring current wealth from its previous peak, casually from portfolio construction (weights allocation), will consider to having a minimum drawdown. In this indicator, the drawdown for individual assets is utilized to measure its value or percentage from its trailing peak (default to 1-yr period).

Drawdown:

drawdown = (price/peaks)-1

Feature:

Static: display drawdown as percentage

Dynamic: display drawdown as value

PhinkTrade Risk Manager EssentialsHello there, fellow traders!

So, happy to bring you a new, free tool: my Risk Manager Essentials .

(To use it, click on "Add to favorite indicators" below, and then look for it in your charts’ "Indicators & Strategies" dialog window, inside "Favorites" tab.)

The main objective of this indicator is to help and incentivize as many traders as possible to adopt essential risk management practices .

First and foremost, it helps you define how much you can buy or sell, at your chosen price levels, in order to keep your risk always under control (in other words: in order to limit the amount you can potentially lose with a trade if your stop loss order is hit).

This is fundamental if you want to have a lasting and successful trading career: protect your capital, always . Because without it, you know: it’s game over.

Indicator also helps you visualize where minimum ideal target / take profit level is , given your risk, using the popular 3:1 Return/Risk ratio (R/R) .

3:1 R/R ratio is popular because with it you only need to “be right” (have price reach your targets) about 33% of the time, in order to be profitable : in other words, the fewer successful trades will pay you more than the sum of your unsuccessful ones will take from you.

So, make sure your strategy has a success rate greater than 33% and apply 3:1 R/R to your trades . This indicator will help you that, and with developing the necessary discipline . For example, by knowing where the ideal target should be, given your choices, you can assess the likelihood of it being reached in current price context. If that would look like a hard to happen scenario, it would probably be a good idea to avoid taking that particular trade.

Now, let’s see how it works:

When you deploy the indicator to the chart for the first time, you’ll be asked to define:

Your 1st entry price (interactively: you can define and adjust levels directly on the chart, thanks to the new Interactive Mode introduced by TradingView (ty, TV team!))

Your stop loss price (likewise)

Your 1st target price (likewise)

Your starting capital (via initial Input dialog)

Your risk (likewise)

Your risk is how much of your starting capital you are willing to lose if your stop loss is hit (define it as a % of your starting capital).

There’s a good practice here too: to risk only 1 percent of your capital per trade . This way, you can reinforce the odds of making more money than you lose and keep your peace of mind in all trades – and avoid messing up with your plans – and statistics – along the way.

Successful trading is a statistics-based endeavor. So, you want to implement and maintain consistency. Again, this indicator helps with that.

After initial setup:

You can also define additional entries and targets (up to 3 each) . Just open indicator’s Settings window and adjust accordingly.

If you have more than one entry – or target, the amounts involved will be split evenly between them. You can also enable the display of the Average Entry and Average Target labels , to see the equivalent, should you have taken (or take) a single order for each.

You can also define (via Settings, then interactively) a particular date and time for the trade . This way, labels will be presented near that moment, instead of constantly show near the latest bar.

Finally, you can personalize some other display settings: levels precision (number of decimal places), labels positions , and labels colors .

In conclusion:

You are very welcome to check it out – and adopt it on your daily use!

Please let me know your feedbacks as well. If you find any issues, or have any suggestions, I’ll be glad to hear. You can contact me here, via TradingView, or Telegram.

Finally, check the updates section below , as new stuff may show from time to time.

Thank you very much for your attention, and enjoy!

PhinkTrade

UTG Trade Manager [V1]Position Sizing and Risk Management tool

See your trading plan directly on your chart . Enter >> Entry price, Take profit, Stoploss, capital, leverage, and see liquidation prices directly in association with entrys and stop losses

[TTI] Position Sizing Calculatorb]HISTORY AND CREDITS –––––––––––––––––––––––––––––––––––––––––––––––––––––––

"Perhaps the greatest secret to top trading and investing success is appropriate money management or what we now call POSITION SIZING" - Dr. Van Tharp, Definite Guide to Position Sizing (Market Wizard Book #1)

For those of you who have studied position sizing you know the power it can have to the bottom line of your portfolio.

WHAT IT DOES ––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

The indicator allows you to quickly determine your position size after you decide to open a trading or investing position. Additionally, it gives you targets in terms of R-multiples (R) that tell you at what price level you achieve 2R or 200% return to a given risk.

The indicator also has the option to print these levels on chart for you.

You can use the calculator for the loaded ticker or other ticker that you wish.

1️⃣ Percent Calculator

👉 Choose position size (%) of total trading portfolio. General guideline here is 25% to be maximum (as per Mark Minervini criteria)

👉 Choose stop loss (%) of total position. This means that if you have 100k portfolio and your position size is 25% (25k), how much of that 25k are you willing to lose in order to asses you are wrong.

OR

2️⃣ Dollar Value Calculator

👉 Choose Stop Price ($) - general guidance is to use technical stop price.

👉 Choose Amount to risk ($) - this is the absolute amount of money you are willing to risk on a position

Both 1️⃣ & 2️⃣ calculate the targets and the target prices in order to determine where to take profits

Additionally, you get instant information for:

👉 How many shares you ought to buy

👉 What is the total size of the position to open

👉 What is your stop amount (either in $ terms or in $ of portfolio)

👉 What is the Risk to Total Equity with the current parameters.

HOW TO USE IT –––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

✅ STEP 1

Choose ticker and input the price at which you open a position

✅ STEP 2

Choose 1️⃣ Percent Calculator OR 2️⃣ Dollar Value Calculator

Depending on the parameters you use to open a position

✅ STEP 3

Review the table and the Additional data section to see how much Shares you ought to buy and what is the Risk To Total Equity

✅ STEP 4

Put Alerts for Stop Loss and Take Profits

Sell Half On DoubleNotes:

- In settings leave 0 for actual price, or set a new price and the SHOD levels will change too.

ADR in 0.5 / 1 / 3 / 5top of the morning!

This indicator is a tiny bit different then the previous one i published.

As per my little study into the ATR, i have decided to remove it out of my indicator and instead put in a half an ADR in dollar vallue.

For me, i can use this value to check at what level i would like my stop. The next evolvement of this indicator might be a total new one since i'd be one for a lower timeframe with the 0.5 and 0.3 adr down from current high otd.

Hope you enjoy it,

Peace

Bitcoin Risk Long Term indicatorOBJECTIVE:

The purpose of this indicator is to synthesize via an average several indicators from a wide choice with in order to simplify the reading of the bitcoin price and that on a long term vision.

Useful for those who want to see things simply, typically to make a smart DCA based on risk.

I originally used this script as a sandbox to understand and test the usefulness of several indicators, and to develop my PineScript skills, but finally the Risk Indicator output seems relevant so I decided to share it.

USAGE:

The selected indicators are the ones that I think give the best market bottoms, but the idea here is that anyone can try and use any set of indicators based on those preferences (post in comments if you find a relevant config)

Most of the indicator inputs are configurable. And some are not taken into account in the calculation of the Risk indicator because I consider them not relevant, this script is also a test more than a final version.

NOTES :

If you have any idea of adding an indicator, modification, criticism, bug found: share them, it is appreciated!

In the future I will create another more versatile Risk indicator that will not be focused on bitcoin in weekly. (this indicator is still usable on other assets and timeframe)

THANKS:

to Benjamin Cowen for inspiring me with his Bitcoin Risk metric

to Lazybear for his Wavetrend Indicator and all the scripts he shares

to Mabonyi for his Bitcoin Logarithmic Growth Curves & Zones script

to VuManChu for his VMC Cypher B Divergence

to the Trading view team for developing TV and PineScript

And to all the community for all the published codes that allowed me to progress and create this script

---- FR ----

OBJECTIF :

L'objectif de cet indicateur est de synthétiser via une moyenne plusieurs indicateurs parmi un large choix avec afin de simplifier la lecture du cours de bitcoin et cela sur une vision longue terme.

Utile pour ceux qui veulent voir les choses simplement, typiquement faire un DCA intelligent en fonction du risque.

À la base j'ai utilisé ce script comme un bac à sable pour comprendre puis tester l'utilité de plusieurs indicateurs, et développer mes compétences PineScript, mais finalement l'output Risk Indicateur me semble pertinent donc autant le partager.

UTILISATION :

Les indicateurs sélectionnés sont ceux qui permettent selon moi d'avoir les meilleurs point bas de marché, mais l'idée ici est que chacun puisse essayer et utiliser n'importe quel ensemble d'indicateur en fonction de ces préférences (poster en commentaire si vous trouvez une configuration pertinente)

La plupart des inputs indicateurs sont paramétrables. Et certains ne sont pas pris en compte dans le calcul du Risk indicateur car je les estime non pertinent, ce script est aussi un essai plus qu'une version finale.

NOTES :

Si vous avez la moindre idée d'ajout d'indicateur, modification, critique, bug trouvé : partagez-les, c'est apprécié !

à l'avenir je créerais un autre Risk indicator plus polyvalent qui ne sera pas focalisé sur bitcoin en weekly. (cet indicateur est tout de même utilisable sur d'autre actif et timeframe)

REMERCIEMENT :

à Benjamin Cowen pour m'avoir inspiré avec son Bitcoin Risk metric

à Lazybear pour son Wavetrend Indicator et globalement tout les scripts qu'il partage

à Mabonyi pour son script Bitcoin Logarithmic Growth Curves & Zones

à VuManChu pour son VMC Cypher B Divergence

à l'équipe Trading view pour avoir développé TV et PineScript

Et à toute la communauté pour tous les codes publiés qui m'ont permis de progresser et de créer ce script

VIX Strategy : Risk-ON, Risk-OFF

VRatio is the ratio of VIX3M and VIX. This ratio rises above 1.1; in a bear market, it decreases and goes below 1. VRatio=VIX3M/VIX. More details in Part 2.

VRatio > 1: Risk-On signal

Contango is the ratio of VX2 (first back-month contract) and VX1 (front-month contract) minus one. In a bull market, this indicator rises above 5%’ in a downtrend market, this indicator goes below -5%. More details in Part 2.

Contango > -5%: Risk-On signal

Contango Roll is the ratio of VX2 first back-month contract) and the VIX minus one. In a bull market, this indicator rises above 10%’ in a downtrend market, this indicator goes below -10%. More details in Part 2.

Contango Roll > 10%: Risk-On signal

Volatility Risk Premium (VRP) compares the implied volatility to the recent realized volatility; it attempts to quantify how much “extra” premium (in volatility term) S&P500 option sellers are charging investors for the protection of their portfolio. It can be seen as an insurance premium. A simple way to compute the VRP is VRP= VIX -HV10 where HV10 is the 10-day historical volatility of S&P500. Some people also look at the 5-day moving average of the VRP to smooth this indicator.

VRP > 0: Risk-On signal

Fast Volatility Risk Premium (FVRP) is a variant of the VRP. FVRP=EMA(VIX,7)-HV5 where HV5 the 5-day historical volatility of S&P500.

FVRP > 0: Risk-On signal

Volatility Momentum compares today’s VIX to last 50 days. It has, therefore, quite a bit of lag but it is a useful measure when combined with other indicators. Volatility Momentum=SMA(VIX,50) -VIX.

Volatility Momentum > 0: Risk-On signal

VIX Mean Reversion looks at today’s VIX compared to certain thresholds. We avoid investing in the S&P500 when the VIX is too high (above 20) or too low (below 12).

VIX Mean Reversion > 12 and VIX Mean Reversion < 20: Risk-On signal

VIX3M Mean Reversion works the same way as VIX Mean Reversion.

VIX3M Mean Reversion > 12 and VIX3M Mean Reversion < 20: Risk-On signal

Position Sizing CalculatorThis is an intuitive risk management tool with a minimalist design.

This calculator will determine your position size per trade, profit, loss, risk/reward ratio and leverage if any.

It will calculate your leverage if you are trading financial instruments e.g. Mini Futures , Turbo Warrants etc. that have a financing level.

Tip: Use this as a complement to the Long/Short Position tool.

Provide the following inputs to get a calculation:

- Position type

- Account balance

- Risk per trade percentage

- Financing level (if any for leveraged instruments), else let it be 0

- Entry price

- Target price

- Stopp loss price

You can also choose the color of the output text, its background and position in the chart window.

Enjoy!

Risk AssistAs the profit level increases, the amount of profit taking required to avoid risk asymptotically reaches zero.

This indicator displays the % of the established position required to exit in order to ensure the trade is not a loss if the stop is hit.

Values in green (at or below 100%) indicate a winning position.

Values in red (above 100%) indicate a losing position.

Alert Examples:

If you are intent on "selling half" to avoid risk, you can set an alert on the value of this indicator for 50.

If you are intent on "selling a 3rd" to avoid risk, you can set an alert on the value of this indicator for 33.3.

Market Risk IndicatorThere are many tools for swing traders. Position traders have not as much, perhaps because they live in the fringe zone between fundamental analysis and trend following.

In order to bridge this gap between fundamental analysis and technical analysis on large timeframes, we decided to work on building a market indicator that assesses its risk and quantifies it on a single dimension number.

The challenge is to consider as input different assets, that individually are themselves often market driving forces, and collectively, more often than not, are sufficient to determine the market status quo.

We came up with DXY , US10Y , HYG and WTI. The latter, the bigger the better; the former, vice versa.

Each asset is evaluated against its recent max/min range, percentually. The positive ones add up and vice versa.

This is still ongoing work. the math and code are simple. the heart of the matter is selecting the proper assets and processing them even better.

Thank you.

TDR (Trend Direction & Risk) IndicatorIntroduction

The TDR (Trend Direction & Risk) Indicator combines two of my previous indicators into one. TDR helps to visually identify price trends and also measures the risk of entering a position during that trend. This indicator is a combination of Ichimoku cloud techniques, particularly the Kijun-Sen and the percentage price oscillator (PPO) to measure a risk score.

Using the TDR Indicator

There are two main indicator lines, the blue line represents a moving average which can act as support or resistance and the orange and red line is called the trend base. When price crosses the trend base and the moving average also crosses then a change in trend direction is confirmed. This is confirmed with either a Buy or Sell signal.

In between these signals there are also Dollar Cost Average and Take Profit signals based on the current trend direction. Each of these signals gives a warning, indicated with an x above or below the candle accompanied with a b for (buy) or an (s) for sell. The next candle will display a small triangle as confirmation of this signal. These signals are based on a cross of the Advance Signal Price which is show at the current price candle.

The future base level can be set to show a larger macro trend than the current timeframe. An example of this is the 3 day timeframe which I use to determine if Bitcoin is in either a bull or bear market.

The Dollar Cost Average and Take Profit signals recommend to buy or remove a percentage of your position at these points. This percentage is completely down to personal preference.

Risk & Information Box

At the bottom right of the chart there is an information box which contains some Information. It shows the current recommended position based on the signals mentioned above. It also shows a risk score which ranges from -100 to 100. This can be used in combination with the signals and trend above for additional entry points. There are three levels, Low, Neutral and High. Buying a percentage of a position at a low risk level and selling a percentage of a position at a high risk level in combination with the trend signals is recommended.

S/R and Base Percentage

These boxes show the price percentage distance from the blue S/R line and the Trend Base Line. These larger these percentages the more likely a snap back in price towards these lines is likely. In my testing once these get above 20% or -20% the chance the price will move back towards those lines is more likely.

Users who have access to my other scripts will be given access to this one and those old ones will no longer me maintained or updated.

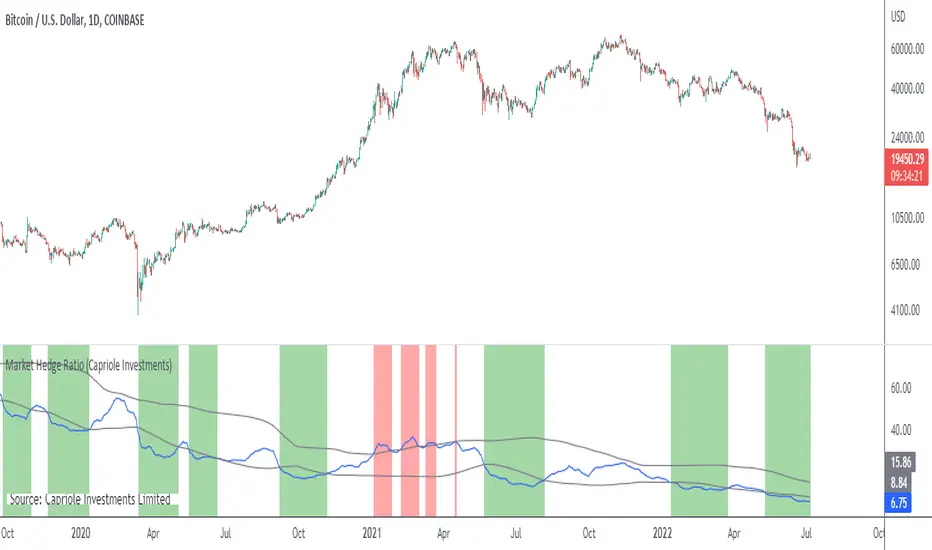

Market Hedge RatioRatio of crypto (total, Bitcoin, or Ethereum market cap) to major stable coins.

A low ratio suggests a lot of people are sitting in cash (sidelined if crypto rallies).

A high ratio suggests possible demand saturation.

Modified Mannarino Market Risk IndicatorThis indicator is meant to give an overall indication of risk and a very basic implementation of the modified mannarino market risk indicator. I take no credit for the original formula, and just decided to hack this together so that it could be useful to the community

Zeal Trade HelperOnce you have mastered a trading strategy, risk management is the most important aspect of trading that will enable and long and successful trading career. The Zeal Trade Helper is based on Van Tharp's theory of R. It provides an immediate visual trading plan, as well as sizing parameters for trading equity and options (.25 and .50 deltas) based on a number of inputs to help you avoid needing to do quick mental math in the moment of taking a trade.

HOW TO USE

- First, you will need to input your R value. To find your R value, divide your **average green day** by the **average number of trades you take in a day**. Once you have this number, enter it into the "Your R Value" field in the indicator settings.

- The indicator settings then provides you with 5 different setup entries. When you have your watchlist ready for the day, simply go through and choose the specific stock, enter your entry price, stop loss, target, and setup type (build, short, bounce, or reject).

OUTPUTS

**Trading Plan**

The indicator will display a visual trading plan based on the inputs you entered on each individual stock's chart. The trading plan will have a green box and red box to represent your entry, target, and stop loss.

**Risk Parameters**

The indicator will also display text outlining what your risk parameters and sizing should be for the trade based on your R value. You will see 3 different lines: the first line showing the number of shares you can trade, the second line showing the number of option contracts you can trade at .50 delta, and the third line showing the number of option contracts you can trade at .25 delta. For reference, at the money options are .50 deltas. Even if you aren't trading exactly .50 or .25 deltas, these values will still help as a frame of reference in the moment of putting on the trade.

**Note that you can toggle the appearance of either of these outputs by checking/un-checking the boxes next to "Display trading plan" and "Display risk parameters" in the indicator settings.

Examples:

1. "**240 shares with $1.25 risk**" means you can take 240 shares and risk $1.25 on the share's price based on your R value

2. "**4.8 Cons @ .50 delta with $0.62 risk**" means you can take either 4 or 5 at the money option contracts and risk $0.62 **on the option contract's value** based on your R value

3. "**9.8 Cons @ .50 delta with $0.31 risk**" means you can take either 9 or 10 option contracts that have a .25 delta (a bit out of the money) and risk $0.31 **on the option contract's value** based on your R value

Happy Trading!

Value-at-Risk Value-at-Risk is a risk measurement tool widely used by banks and institutions.

This script uses historical simulation method for the calculation of VaR. The default settings are 250-days period. 1 percentile (or 99 percentile confidence level.)

This means the daily loss for the past 250 days should not exceed the risk measure 99% of the time.

traders can calculate the desired level of risk by converting the timeframe OR by multiplying the square root (expected holding period) to find out the VaR value for 5 days, 25 days, 250 days etc.

Do take note that the default assumes a long position, if you are taking a short position, the percentile value has to be adjusted accordingly (to find the worst 1 percent loss for shorts will require changing the input to 99)

R-Calculator

Visualise your possible 1R to 6R prices, based on your Risk($), entry and stoploss price, and see the distance until the goal is fulfilled.

It also provides you with a suggested amount of stocks to buy, so if you lose, it will match -1R.

SignalsThis script allows you to calculate position size, and future profit, loses.

- You can add 3 target values and 1 stop loss

- Optionally you can display table, position it as you like, and see risk ratio

Plans:

- add profit loss to the labels