Multi Rolling VWAPMulti Rolling VWAP Indicator

Displays 4 volume-weighted average price (VWAP) levels on your chart:

7D VWAP - Weekly rolling average

30D VWAP - Monthly rolling average

90D VWAP - Quarterly rolling average

365D VWAP - Yearly rolling average

Each VWAP shows where the average price is, weighted by volume. Institutional traders often use these levels as support/resistance.

Optional Features:

Bands show volatility zones (Value Area High/Low)

Anchor modes: Reset weekly, monthly, quarterly, or yearly instead of rolling

Crypto volume aggregation from 15+ exchanges for accurate calculations

Clean, minimal design for white background charts.

Rvwap

30-Day Rolling VWAP30-Day Rolling VWAP (30-RVWAP)

Overview:

The 30-Day Rolling VWAP is an advanced technical analysis tool designed for crypto traders that combines Volume Weighted Average Price over a 30-day rolling window with sophisticated volume analysis to generate high-probability trading signals.

Key Features:

1. Dynamic Color-Coded VWAP Line

Green glow = Strong bullish pressure

Red glow = Strong bearish pressure

Gray = Neutral/balanced market

The line changes color based on volume-weighted directional pressure

2. Volume Pressure Zones

Multi-layered glowing fill effect around VWAP

Expands/contracts based on volatility and volume

Shows potential support/resistance zones

3. Smart Alert System

Buy/Sell alerts based on VWAP color change

Cross above/below VWAP alerts

Confidence levels based on pressure strength

How to Use:

1. Color Signals

When VWAP turns green: Consider buying (bullish pressure)

When VWAP turns red: Consider selling (bearish pressure)

Gray color indicates consolidation/neutral market

2. Alert Structure

Buy/Sell alerts include confidence percentage (0-100%)

Higher confidence = stronger directional pressure

Cross alerts notify when price crosses VWAP with distance

3. Volume Pressure Zones

Wider zones = higher volatility/volume

Use zones as dynamic support/resistance levels

Watch for price reactions at zone boundaries

4. Trading Strategy

Enter long when VWAP turns green with high confidence (60%+)

Enter short when VWAP turns red with high confidence

Use VWAP as trailing stop (exit when cross alerts trigger)

Use pressure zones for profit targets

5. Alert Messages

Buy Signal: "BTCUSDT | 15m | BUY Signal | Price: 42380.00 | VWAP: 42350.00 | Distance: 0.07% | Confidence: 78% due to strong bullish pressure"

Cross Alert: "BTCUSDT | 15m | CROSS ABOVE VWAP | Price: 42360.00 | VWAP: 42350.00 | Distance: 0.02%"

Best Practices:

Use higher timeframes (4H+) for trend direction; preferably **daily timeframe**

Combine with other indicators for confirmation

Monitor volume for signal validation

Consider market context when entering trades

The indicator combines multiple volume metrics to filter out false signals and provides clear visual and alert-based trading signals.

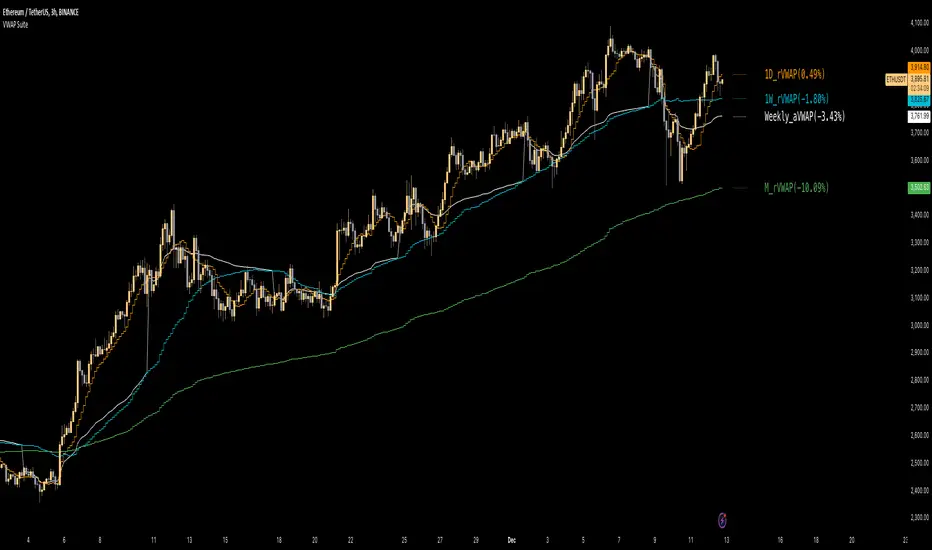

Multiple VWAP SuiteThe VWAP Suite is a tool I created to streamline VWAP analysis for traders. By integrating Anchored and Rolling VWAPs into a single indicator, it eliminates the need for multiple separate tools, keeping charts clean and organized without sacrificing flexibility or functionality. The goal was to simplify VWAP management by combining six different configurations into one intuitive and highly customizable indicator. It’s designed for traders who utilize VWAP-based strategies for trend analysis, support/resistance identification, or mean-reversion setups.

Features:

1. Integrated Anchored VWAPs:

Includes three customizable Anchored VWAPs, each tied to a specific timeframe such as Session, Weekly, Monthly, or even Decade.

Standard deviation bands can provide visual cues for dynamic support/resistance or volatility ranges.

Each VWAP can be toggled on/off and customized for color and band appearance.

2. Rolling VWAPs:

Includes three independently configurable Rolling VWAPs for dynamic timeframe analysis (Daily, Weekly, Monthly).

Rolling VWAPs feature optional deviation bands to gauge price action within a defined volatility range.

Smooth visualization using stepline plots for better trend identification.

3. Labeling System:

Labels show the VWAP levels and percentage deviations from the current price for easy reference.

Adjustable text size for improved chart readability.

4. Customizability:

Fully adjustable input sources for both Anchored and Rolling VWAPs, allowing you to tailor the indicator to your strategy.

Ability to enable or disable specific VWAPs, deviation bands, or labels depending on your focus.

Why Did I Make This?

Managing multiple VWAP indicators often leads to cluttered charts and inefficient workflows. I created the VWAP Suite to address this issue, combining Anchored and Rolling VWAPs into a single, powerful tool. Whether you’re a scalper, swing trader, or long-term trend follower, this script keeps everything you need in one place, simplifying your workflow and enhancing your ability to make informed trading decisions.

Feel free to comment any suggestions or questions! Enjoy!

Moving Averages + BB & R.VWAP StDev (multi-tf)█ Moving Averages + Bollinger Bands and Rolling Volume Weighted Average Price with Standard Deviation Bands (Multi Timeframe)

Multiple moving averages can be independently applied.

The length , type and timeframe of each moving average are configurable .

The lines and colors are customizable too.

This script can display:

Moving Averages

Bollinger Bands

Rolling VWAP and Standard Deviation Bands

Types of Moving Averages:

Simple Moving Average (SMA)

Exponential Moving Average (EMA)

Smoothed Moving Average (SMMA)

Weighted Moving Average (WMA)

Volume Weighted Moving Average (VWMA)

Least Squares Moving Average (LSMA)

Hull Moving Average (HMA)

Arnaud Legoux Moving Average (ALMA)

█ Moving Average

Moving Averages are price based, lagging (or reactive) indicators that display the average price of a security over a set period of time.

A Moving Average is a good way to gauge momentum as well as to confirm trends, and define areas of support and resistance.

█ Bollinger Bands

Bollinger Bands consist of a band of three lines which are plotted in relation to security prices.

The line in the middle is usually a Simple Moving Average (SMA) set to a period of 20 days (the type of trend line and period can be changed by the trader, a 20 day moving average is by far the most popular).

The SMA then serves as a base for the Upper and Lower Bands which are used as a way to measure volatility by observing the relationship between the Bands and price.

█ Rolling VWAP

The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day.

Such VWAPs cannot be used on daily, weekly or monthly charts. Instead, this rolling VWAP uses a time period that automatically adjusts to the chart's timeframe.

You can thus use the rolling VWAP on any chart that includes volume information in its data feed.

Because the rolling VWAP uses a moving window, it does not exhibit the jumpiness of VWAP plots that reset.

Based on the previous script :

MTF MA Ribbon and Bands + BB, Gaussian F. and R. VWAP with StDev█ Multi Timeframe Moving Average Ribbon and Bands + Bollinger Bands, Gaussian Filter and Rolling Volume Weighted Average Price with Standard Deviation Bands

Up to 9 moving averages can be independently applied.

The length , type and timeframe of each moving average are configurable .

The lines, colors and background fill are customizable too.

This script can also display:

Moving Average Bands

Bollinger Bands

Gaussian Filter

Rolling VWAP and Standard Deviation Bands

Types of Moving Averages:

Simple Moving Average (SMA)

Exponential Moving Average (EMA)

Smoothed Moving Average (SMMA)

Weighted Moving Average (WMA)

Volume Weighted Moving Average (VWMA)

Least Squares Moving Average (LSMA)

Hull Moving Average (HMA)

Arnaud Legoux Moving Average (ALMA)

█ Moving Average

Moving Averages are price based, lagging (or reactive) indicators that display the average price of a security over a set period of time.

A Moving Average is a good way to gauge momentum as well as to confirm trends, and define areas of support and resistance.

█ Bollinger Bands

Bollinger Bands consist of a band of three lines which are plotted in relation to security prices.

The line in the middle is usually a Simple Moving Average (SMA) set to a period of 20 days (the type of trend line and period can be changed by the trader, a 20 day moving average is by far the most popular).

The SMA then serves as a base for the Upper and Lower Bands which are used as a way to measure volatility by observing the relationship between the Bands and price.

█ Gaussian Filter

Gaussian filter can be used for smoothing.

It rejects high frequencies (fast movements) better than an EMA and has lower lag.

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve.

In the case of low-pass filters, only the upper half of the curve describes the filter.

The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

█ Rolling VWAP

The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day.

Such VWAPs cannot be used on daily, weekly or monthly charts. Instead, this rolling VWAP uses a time period that automatically adjusts to the chart's timeframe.

You can thus use the rolling VWAP on any chart that includes volume information in its data feed.

Because the rolling VWAP uses a moving window, it does not exhibit the jumpiness of VWAP plots that reset.

Made with the help from scripts of: adam24x, VishvaP, loxx and pmk07.

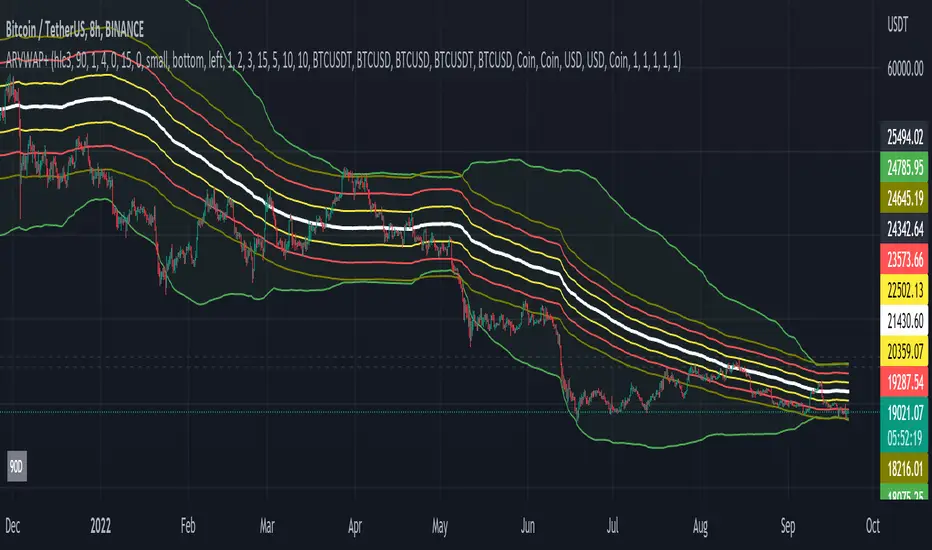

Aggregated Rolling VWAP +Edit of TradingView's original Rolling VWAP

Edit log:

Added Volume Aggregation Capabilities to the Script

- Price Action is impacted by volume executed in all exchanges. Even though a single exchange RVWAP can be useful, using aggregated data makes it more accurate and saves time in symbol switching.

- Aggregation is preset to be done for Bitcoin Spot Pairs. However this can be changed to Aggregate Volume from any other symbol at the bottom of the setup menu.

Added Symmetrical Deviations to the Script

- Symmetrical deviations create range of "tolerance" around the RVWAP at a fixed % distance. This helps in situations when price does not respect the exact RVWAP level and goes slightly above/under.

- Adding multiple Symmetrical Deviations at different percentage values can give relevant levels for scalping, entries and range trading.

Switched default option to manual TF instead of automatic TF

Added TF Presets for quick switching between different settings. (Feature intended for mobile charting)

Added ON/OFF Switch to all individual deviations to make it easier, faster and cleaner to display different data. (Feature intended for mobile charting)