MAC-Z & MACD Leader signal [ChuckBanger]This is a combination of my MACD Leader script and MAC-Z with option to add Laguerre filter. The advantage of the MAC-Z over MACD is that it is a more accurate and “assumption-free” indicator that can more accurately describe how a market actually perform. But you can use this as a regular MACD indicator.

Crossovers signals

The MAC-Z line and signal line can be utilized in the same way as a stochastic oscillator, with the crossover between the two lines providing buy and sell signals. As with most crossover strategies, a buy signal comes when the shorter-term, more reactive line – in this case the MAC-Z line (blue line) crosses above the slower signal line (orange line). For example, when the MAC-Z line crosses below the signal line it provides a bearish sell signal.

Zero line crossing

The zero cross strategy is based on either of the lines crossing the zero line. If the MAC-Z crosses the zero line from below, it is a signal for a possible new uptrend, while the MAC-Z crossing from above is a signal that a new downtrend may be starting. This is special powerful if the lines has a fast up or down movement but the price action doesn't reflect that movement.

Divergences

Bearish and bullish divergences is my favorite signals. When price action and oscillators follow the same path it is called Convergences, when they don’t, it’s called a Divergence. Don't confuse the two because they have not the same meaning. But be aware that for example during consolidation or low liquidity, some small divergences between price and indicators might form, but that doesn't mean we should consider them as real divergences.

There is many different types of divergences. It is easier to show a picture then explaining it so I recommend you to check out the link below. Especially the top image. It sums this up very well

medium.com

MACD Leader

The MACD leader is only showing the crossing of MACD as a vertical line

Green vertical line = MACD Leader Bullish Cross

Red vertical line = MACD Leader Bearish Cross

MACD Leader:

MAC-Z:

More Information

cssanalytics.wordpress.com

en.wikipedia.org

drive.google.com

ابحث في النصوص البرمجية عن "电力行业+股票+11年涨幅"

Edward EMA 8-21-89-144Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入

14、89-144作为牛熊的分水岭。在89-144区域之下只考虑做空,89-144只考虑做多。如果89-144走横则以位置决定高位倾向空低位倾向多。

15、K线会因为指标的设置自动变成两个颜色块,绿色看涨,红色看跌。做趋势看K线颜色。牛市的红色可以当成入场K熊市绿色当成入场K

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

[astropark] MACD, RSI+, AO, DMI, ADX, OBV, ADI//******************************************************************************

// Copyright by astropark v4.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV, ADI

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

// 14/01/2019 Added Accelerator Decelerator Indicator (ADI)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV//******************************************************************************

// Copyright by astropark v4.0.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Oscillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI with ADX//******************************************************************************

// Copyright by astropark v3.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

//******************************************************************************

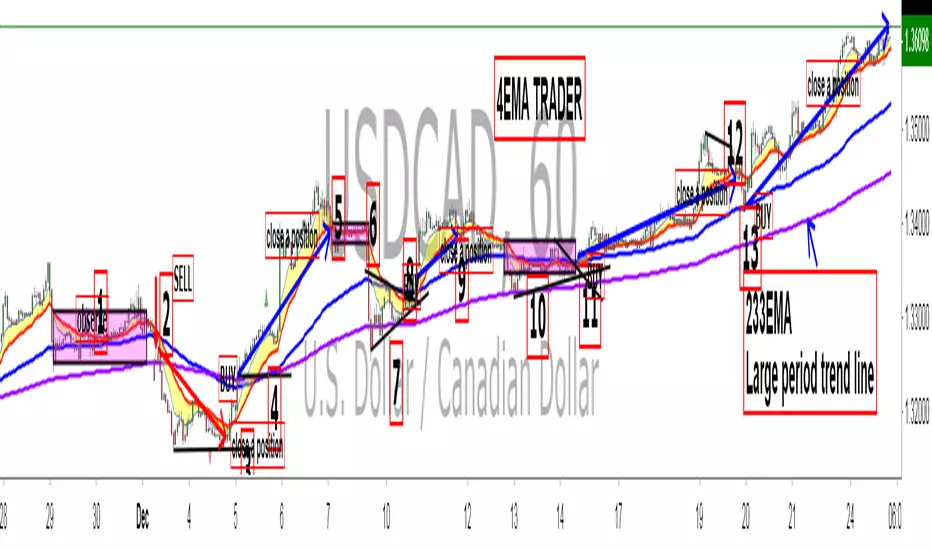

King 4EMA TraderKing 4EMA trader 8/21/89EMA+(233)V3.3

Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入。

Bitfinex Longs/Shorts Multi-Coin [acatwithcharts]This script plots the longs/shorts ratio derived from Bitfinex for BTCUSDLONGS, BTCUSDSHORTS, and similar for 11 top cryptocurrencies chosen selected based on marketcap, trading volume on Bitfinex, and the maximum number of times that TradingView would let me call the "security" function in one script. Included coins:

BTC, ETH, LTC, BCH, XRP, EOS, IOT (IOTA), ETC, ZEC, NEO, XMR

In addition to just plotting the ratios for the individual coins, this script also calculates for a customizable selection of the 11 coins both the average ratio and a weighted average weighted by (USD price of coin * sum of long and short positions).

I wrote it both to use both for a big picture overview of leveraged positions across major coins and to use as a Swiss army knife of longs/shorts ratio indicators for individual coins, most of which do not currently have individual scripts published.

I'm an amateur and you definitely shouldn't take anything I say or use any of my scripts as financial advice. I'd appreciate any feedback.

Stochastic Momentum IndexStochastic Momentum Index indicator script. This indicator was originally developed by William Blau (Stocks & Commodities V. 11:1 (11-18)).

Density Zones (GM Crossing Clusters) + QHO Spin FlipsINDICATOR NAME

Density Zones (GM Crossing Clusters) + QHO Spin Flips

OVERVIEW

This indicator combines two complementary ideas into a single overlay: *this combines my earlier Geometric Mean Indicator with the Quantum Harmonic Oscillator (Overlay) with additional enhancements*

1) Density Zones (GM Crossing Clusters)

A “Density Zone” is detected when price repeatedly crosses a Geometric Mean equilibrium line (GM) within a rolling lookback window. Conceptually, this identifies regions where the market is repeatedly “snapping” across an equilibrium boundary—high churn, high decision pressure, and repeated re-selection of direction.

2) QHO Spin Flips (Regression-Residual σ Breaches)

A “Spin Flip” is detected when price deviates beyond a configurable σ-threshold (κ) from a regression-based equilibrium, using normalized residuals. Conceptually, this marks excursions into extreme states (decoherence / expansion), which often precede a reversion toward equilibrium and/or a regime re-scaling.

These two systems are related but not identical:

- Density Zones identify where equilibrium crossings cluster (a “singularity”/anchor behavior around GM).

- Spin Flips identify when price exceeds statistically extreme displacement from the regression equilibrium (LSR), indicating expansion beyond typical variance.

CORE CONCEPTS AND FORMULAS

SECTION A — GEOMETRIC MEAN EQUILIBRIUM (GM)

We define two moving averages:

(1) MA1_t = SMA(close_t, L1)

(2) MA2_t = SMA(close_t, L2)

We define the equilibrium anchor as the geometric mean of MA1 and MA2:

(3) GM_t = sqrt( MA1_t * MA2_t )

This GM line acts as an equilibrium boundary. Repeated crossings are interpreted as high “equilibrium churn.”

SECTION B — CROSS EVENTS (UP/DOWN)

A “cross event” is registered when the sign of (close - GM) changes:

Define a sign function s_t:

(4) s_t =

+1 if close_t > GM_t

-1 if close_t < GM_t

s_{t-1} if close_t == GM_t (tie-breaker to avoid false flips)

Then define the crossing event indicator:

(5) crossEvent_t = 1 if s_t != s_{t-1}

0 otherwise

Additionally, the indicator plots explicit cross markers:

- Cross Above GM: crossover(close, GM)

- Cross Below GM: crossunder(close, GM)

These provide directional visual cues and match the original Geometric Mean Indicator behavior.

SECTION C — DENSITY MEASURE (CROSSING CLUSTER COUNT)

A Density Zone is based on the number of cross events occurring in the last W bars:

(6) D_t = Σ_{i=0..W-1} crossEvent_{t-i}

This is a “crossing density” score: how many times price has toggled across GM recently.

The script implements this efficiently using a cumulative sum identity:

Let x_t = crossEvent_t.

(7) cumX_t = Σ_{j=0..t} x_j

Then:

(8) D_t = cumX_t - cumX_{t-W} (for t >= W)

cumX_t (for t < W)

SECTION D — DENSITY ZONE TRIGGER

We define a Density Zone state:

(9) isDZ_t = ( D_t >= θ )

where:

- θ (theta) is the user-selected crossing threshold.

Zone edges:

(10) dzStart_t = isDZ_t AND NOT isDZ_{t-1}

(11) dzEnd_t = NOT isDZ_t AND isDZ_{t-1}

SECTION E — DENSITY ZONE BOUNDS

While inside a Density Zone, we track the running high/low to display zone bounds:

(12) dzHi_t = max(dzHi_{t-1}, high_t) if isDZ_t

(13) dzLo_t = min(dzLo_{t-1}, low_t) if isDZ_t

On dzStart:

(14) dzHi_t := high_t

(15) dzLo_t := low_t

Outside zones, bounds are reset to NA.

These bounds visually bracket the “singularity span” (the churn envelope) during each density episode.

SECTION F — QHO EQUILIBRIUM (REGRESSION CENTERLINE)

Define the regression equilibrium (LSR):

(16) m_t = linreg(close_t, L, 0)

This is the “centerline” the QHO system uses as equilibrium.

SECTION G — RESIDUAL AND σ (FIELD WIDTH)

Residual:

(17) r_t = close_t - m_t

Rolling standard deviation of residuals:

(18) σ_t = stdev(r_t, L)

This σ_t is the local volatility/width of the residual field around the regression equilibrium.

SECTION H — NORMALIZED DISPLACEMENT AND SPIN FLIP

Define the standardized displacement:

(19) Y_t = (close_t - m_t) / σ_t

(If σ_t = 0, the script safely treats Y_t = 0.)

Spin Flip trigger uses a user threshold κ:

(20) spinFlip_t = ( |Y_t| > κ )

Directional spin flips:

(21) spinUp_t = ( Y_t > +κ )

(22) spinDn_t = ( Y_t < -κ )

The default κ=3.0 corresponds to “3σ excursions,” which are statistically extreme under a normal residual assumption (even though real markets are not perfectly normal).

SECTION I — QHO BANDS (OPTIONAL VISUALIZATION)

The indicator optionally draws the standard σ-bands around the regression equilibrium:

(23) 1σ bands: m_t ± 1·σ_t

(24) 2σ bands: m_t ± 2·σ_t

(25) 3σ bands: m_t ± 3·σ_t

These provide immediate context for the Spin Flip events.

WHAT YOU SEE ON THE CHART

1) MA1 / MA2 / GM lines (optional)

- MA1 (blue), MA2 (red), GM (green).

- GM is the equilibrium anchor for Density Zones and cross markers.

2) GM Cross Markers (optional)

- “GM↑” label markers appear on bars where close crosses above GM.

- “GM↓” label markers appear on bars where close crosses below GM.

3) Density Zone Shading (optional)

- Background shading appears while isDZ_t = true.

- This is the period where the crossing density D_t is above θ.

4) Density Zone High/Low Bounds (optional)

- Two lines (dzHi / dzLo) are drawn only while in-zone.

- These bounds bracket the full churn envelope during the density episode.

5) QHO Bands (optional)

- 1σ, 2σ, 3σ shaded zones around regression equilibrium.

- These visualize the current variance field.

6) Regression Equilibrium (LSR Centerline)

- The white centerline is the regression equilibrium m_t.

7) Spin Flip Markers

- A circle is plotted when |Y_t| > κ (beyond your chosen σ-threshold).

- Marker size is user-controlled (tiny → huge).

HOW TO USE IT

Step 1 — Pick the equilibrium anchor (GM)

- L1 and L2 define MA1 and MA2.

- GM = sqrt(MA1 * MA2) becomes your equilibrium boundary.

Typical choices:

- Faster equilibrium: L1=20, L2=50 (default-like).

- Slower equilibrium: L1=50, L2=200 (macro anchor).

Interpretation:

- GM acts like a “center of mass” between two moving averages.

- Crosses show when price flips from one side of equilibrium to the other.

Step 2 — Tune Density Zones (W and θ)

- W controls the time window measured (how far back you count crossings).

- θ controls how many crossings qualify as a “density/singularity episode.”

Guideline:

- Larger W = slower, broader density detection.

- Higher θ = only the most intense churn is labeled as a Density Zone.

Interpretation:

- A Density Zone is not “bullish” or “bearish” by itself.

- It is a condition: repeated equilibrium toggling (high churn / high compression).

- These often precede expansions, but direction is not implied by the zone alone.

Step 3 — Tune the QHO spin flip sensitivity (L and κ)

- L controls regression memory and σ estimation length.

- κ controls how extreme the displacement must be to trigger a spin flip.

Guideline:

- Smaller L = more reactive centerline and σ.

- Larger L = smoother, slower “field” definition.

- κ=3.0 = strong extreme filter.

- κ=2.0 = more frequent flips.

Interpretation:

- Spin flips mark when price exits the “normal” residual field.

- In your model language: a moment of decoherence/expansion that is statistically extreme relative to recent equilibrium.

Step 4 — Read the combined behavior (your key thesis)

A) Density Zone forms (GM churn clusters):

- Market repeatedly crosses equilibrium (GM), compressing into a bounded churn envelope.

- dzHi/dzLo show the envelope range.

B) Expansion occurs:

- Price can release away from the density envelope (up or down).

- If it expands far enough relative to regression equilibrium, a Spin Flip triggers (|Y| > κ).

C) Re-coherence:

- After a spin flip, price often returns toward equilibrium structures:

- toward the regression centerline m_t

- and/or back toward the density envelope (dzHi/dzLo) depending on regime behavior.

- The indicator does not guarantee return, but it highlights the condition where return-to-field is statistically likely in many regimes.

IMPORTANT NOTES / DISCLAIMERS

- This indicator is an analytical overlay. It does not provide financial advice.

- Density Zones are condition states derived from GM crossing frequency; they do not predict direction.

- Spin Flips are statistical excursions based on regression residuals and rolling σ; markets have fat tails and non-stationarity, so σ-based thresholds are contextual, not absolute.

- All parameters (L1, L2, W, θ, L, κ) should be tuned per asset, timeframe, and volatility regime.

PARAMETER SUMMARY

Geometric Mean / Density Zones:

- L1: MA1 length

- L2: MA2 length

- GM_t = sqrt(SMA(L1)*SMA(L2))

- W: crossing-count lookback window

- θ: crossing density threshold

- D_t = Σ crossEvent_{t-i} over W

- isDZ_t = (D_t >= θ)

- dzHi/dzLo track envelope bounds while isDZ is true

QHO / Spin Flips:

- L: regression + residual σ length

- m_t = linreg(close, L, 0)

- r_t = close_t - m_t

- σ_t = stdev(r_t, L)

- Y_t = r_t / σ_t

- spinFlip_t = (|Y_t| > κ)

Visual Controls:

- toggles for GM lines, cross markers, zone shading, bounds, QHO bands

- marker size options for GM crosses and spin flips

ALERTS INCLUDED

- Density Zone START / END

- Spin Flip UP / DOWN

- Cross Above GM / Cross Below GM

SUMMARY

This indicator treats the Geometric Mean as an equilibrium boundary and identifies “Density Zones” when price repeatedly crosses that equilibrium within a rolling window, forming a bounded churn envelope (dzHi/dzLo). It also models a regression-based equilibrium field and triggers “Spin Flips” when price makes statistically extreme σ-excursions from that field. Used together, Density Zones highlight compression/decision regions (equilibrium churn), while Spin Flips highlight extreme expansion states (σ-breaches), allowing the user to visualize how price compresses around equilibrium, releases outward, and often re-stabilizes around equilibrium structures over time.

PEAD ScreenerPEAD Screener - Post-Earnings Announcement Drift Scanner

═══════════════════════════════════════════════════════════════

WHY EARNINGS ANNOUNCEMENTS CREATE OPPORTUNITY

═══════════════════════════════════════════════════════════════

The days immediately following an earnings announcement are among the noisiest periods for any stock. Within hours, the market must digest new information about a company's profits, revenue, and future outlook. Analysts scramble to update their models. Institutions rebalance positions. Retail traders react to headlines.

This chaos creates a well-documented phenomenon called Post-Earnings Announcement Drift (PEAD): stocks that beat expectations tend to keep rising, while those that miss tend to keep falling - often for weeks after the initial announcement. Academic research has confirmed this pattern persists across decades and markets.

But not every earnings surprise is equal. A company that beats estimates by 5 cents might move very differently than one that beats by 5 cents with unusually high volume, or one where both earnings AND revenue exceeded expectations. Raw numbers alone don't tell the full story.

═══════════════════════════════════════════════════════════════

HOW "STANDARDIZED UNEXPECTED" METRICS CUT THROUGH THE NOISE

═══════════════════════════════════════════════════════════════

This screener uses a statistical technique to measure how "surprising" a result truly is - not just whether it beat or missed, but how unusual that beat or miss was compared to the company's own history.

The core idea: convert raw surprises into Z-scores.

A Z-score answers the question: "How many standard deviations away from normal is this result?"

- A Z-score of 0 means the result was exactly average

- A Z-score of +2 means the result was unusually high (better than ~95% of historical results)

- A Z-score of -2 means the result was unusually low

By standardizing surprises this way, we can compare apples to apples. A small-cap biotech's $0.02 beat might actually be more significant than a mega-cap's $0.50 beat, once we account for each company's typical variability.

This screener applies this standardization to three dimensions: earnings (SUE), revenue (SURGE), and volume (SUV).

═══════════════════════════════════════════════════════════════

THE 9 SCREENING CRITERIA

═══════════════════════════════════════════════════════════════

─────────────────────────────────────────

1. SUE (Standardized Unexpected Earnings)

─────────────────────────────────────────

WHAT IT IS:

SUE measures how surprising an earnings result was, adjusted for the company's historical forecast accuracy.

Calculation: Take the earnings surprise (actual EPS minus analyst estimate), then divide by the standard deviation of past forecast errors. This uses a rolling window of the last 8 quarters by default.

Formula: SUE = (Actual EPS - Estimated EPS) / Standard Deviation of Past Errors

HOW TO INTERPRET:

- SUE > +2.0: Strongly positive surprise - earnings beat expectations by an unusually large margin. These stocks often continue drifting higher.

- SUE between 0 and +2.0: Modest positive surprise - beat expectations, but within normal range.

- SUE between -2.0 and 0: Modest negative surprise - missed expectations, but within normal range.

- SUE < -2.0: Strongly negative surprise - significant miss. These stocks often continue drifting lower.

For long positions, look for SUE values above +2.0, ideally combined with positive SURGE.

─────────────────────────────────────────

2. SURGE (Standardized Unexpected Revenue)

─────────────────────────────────────────

WHAT IT IS:

SURGE applies the same standardization technique to revenue surprises. While earnings can be manipulated through accounting choices, revenue is harder to fake - it represents actual sales.

Calculation: Take the revenue surprise (actual revenue minus analyst estimate), then divide by the standard deviation of past revenue forecast errors.

Formula: SURGE = (Actual Revenue - Estimated Revenue) / Standard Deviation of Past Errors

HOW TO INTERPRET:

- SURGE > +1.5: Strongly positive revenue surprise - the company sold significantly more than expected.

- SURGE between 0 and +1.5: Modest positive surprise.

- SURGE < 0: Revenue missed expectations.

The most powerful signals occur when BOTH SUE and SURGE are positive and elevated (ideally SUE > 2.0 AND SURGE > 1.5). This indicates the company beat on both profitability AND top-line growth - a much stronger signal than either alone.

When SUE and SURGE diverge significantly (e.g., high SUE but negative SURGE), treat with caution - the earnings beat may have come from cost-cutting rather than genuine growth.

─────────────────────────────────────────

3. SUV (Standardized Unexpected Volume)

─────────────────────────────────────────

WHAT IT IS:

SUV detects unusual trading volume after accounting for how volatile the stock is. More volatile stocks naturally have higher volume, so raw volume comparisons can be misleading.

Calculation: This uses regression analysis to model the expected relationship between price volatility and volume. The "unexpected" volume is the residual - how much actual volume deviated from what the model predicted. This residual is then standardized into a Z-score.

In plain terms: SUV asks "Given how much this stock typically moves, is today's volume unusually high or low?"

HOW TO INTERPRET:

- SUV > +2.0: Exceptionally high volume relative to the stock's volatility. This often signals institutional activity - big players moving in or out.

- SUV between +1.0 and +2.0: Elevated volume - above normal interest.

- SUV between -1.0 and +1.0: Normal volume range.

- SUV < -1.0: Unusually quiet - less activity than expected.

High SUV combined with positive price movement suggests accumulation (buying). High SUV combined with negative price movement suggests distribution (selling).

─────────────────────────────────────────

4. % From D0 Close

─────────────────────────────────────────

WHAT IT IS:

This measures how far the current price has moved from the closing price on its initial earnings reaction day (D0). The "reaction day" is the first trading day that fully reflects the earnings news - typically the day after an after-hours announcement, or the announcement day itself for pre-market releases.

Calculation: ((Current Price - D0 Close) / D0 Close) × 100

HOW TO INTERPRET:

- Positive values: Stock has gained ground since earnings. The higher the percentage, the stronger the post-earnings drift.

- 0% to +5%: Modest positive drift - earnings were received well but momentum is limited.

- +5% to +15%: Strong drift - buyers continue accumulating.

- > +15%: Exceptional drift - significant institutional interest likely.

- Negative values: Stock has given back gains or extended losses since earnings. May indicate the initial reaction was overdone, or that sentiment is deteriorating.

This metric is most meaningful within the first 5-20 trading days after earnings. Extended drift (maintaining gains over 2+ weeks) is a stronger signal than a quick spike that fades.

─────────────────────────────────────────

5. # Pocket Pivots

─────────────────────────────────────────

WHAT IT IS:

Pocket Pivots are a volume-based pattern developed by Chris Kacher and Gil Morales. They identify days where institutional buyers are likely accumulating shares without causing obvious breakouts.

Calculation: A Pocket Pivot occurs when:

- The stock closes higher than it opened (up day)

- The stock closes higher than the previous day's close

- Today's volume exceeds the highest down-day volume of the prior 10 trading sessions

The screener counts how many Pocket Pivots have occurred since the earnings announcement.

HOW TO INTERPRET:

- 0 Pocket Pivots: No detected institutional accumulation patterns since earnings.

- 1-2 Pocket Pivots: Some institutional buying interest - worth monitoring.

- 3+ Pocket Pivots: Strong accumulation signal - institutions appear to be building positions.

Pocket Pivots are most significant when they occur:

- Immediately following earnings announcements

- Near moving average support (10-day, 21-day, or 50-day)

- On above-average volume

- After a period of price consolidation

Multiple Pocket Pivots in a short period suggest sustained institutional demand, not just a one-day event.

─────────────────────────────────────────

6. ADX/DI (Trend Strength and Direction)

─────────────────────────────────────────

WHAT IT IS:

ADX (Average Directional Index) measures trend strength regardless of direction. DI (Directional Indicator) shows whether the trend is bullish or bearish.

Calculation: ADX uses a 14-period lookback to measure how directional (trending) price movement is. Values range from 0 to 100. The +DI and -DI components compare upward and downward movement.

The screener shows:

- ADX value (trend strength)

- Direction indicator: "+" for bullish (price trending up), "-" for bearish (price trending down)

HOW TO INTERPRET:

- ADX < 20: Weak trend - the stock is moving sideways, choppy. Not ideal for momentum trading.

- ADX 20-25: Trend is emerging - potentially starting a directional move.

- ADX 25-40: Strong trend - clear directional movement. Good for momentum plays.

- ADX > 40: Very strong trend - powerful move in progress, but may be extended.

The direction indicator (+/-) tells you which way:

- "25+" means ADX of 25 with bullish direction (uptrend)

- "25-" means ADX of 25 with bearish direction (downtrend)

For post-earnings plays, ideal setups show ADX rising above 25 with positive direction, confirming the earnings reaction is developing into a sustained trend rather than a one-day spike.

─────────────────────────────────────────

7. Institutional Buying PASS

─────────────────────────────────────────

WHAT IT IS:

This proprietary composite indicator detects patterns consistent with institutional accumulation at three stages after earnings:

EARLY (Days 0-4): Looks for "large block" buying on the earnings reaction day (exceptionally high volume with a close in the upper half of the day's range) combined with follow-through buying on the next day.

MID (Days 5-9): Checks for sustained elevated volume (averaging 1.5x the 20-day average) combined with positive drift and consistent upward price movement (more up days than down days).

LATE (Days 10+): Detects either visible accumulation (positive drift with high volume) OR stealth accumulation (positive drift with unusually LOW volume - suggesting smart money is quietly building positions without attracting attention).

HOW TO INTERPRET:

- Check mark/value of '1': Institutional buying pattern detected. The stock shows characteristics consistent with large players accumulating shares.

- X mark/value of '0': No institutional buying pattern detected. This doesn't mean institutions aren't buying - just that the typical footprints aren't visible.

A passing grade here adds conviction to other bullish signals. Institutions have research teams, information advantages, and long time horizons. When their footprints appear in the data, it often precedes sustained moves.

Important: This is a pattern detection tool, not a guarantee. Always combine with other analysis.

─────────────────────────────────────────

8. Strong ATR Drift PASS

─────────────────────────────────────────

WHAT IT IS:

This measures whether the stock has drifted significantly relative to its own volatility. Instead of asking "did it move 10%?", it asks "did it move more than 1.5 ATRs?"

ATR (Average True Range) measures a stock's typical daily movement. A volatile stock might move 5% daily, while a stable stock might move 0.5%. Using ATR normalizes for this difference.

Calculation:

ATR Drift = (Current Close - D0 Close) / D0 ATR in dollars

The indicator passes when ATR Drift exceeds 1.5 AND at least 5 days have passed since earnings.

HOW TO INTERPRET:

- Check mark/value of '1': The stock has drifted more than 1.5 times its average daily range since earnings - a statistically significant move that suggests genuine momentum, not just noise.

- X mark/value of '0': The drift (if any) is within normal volatility bounds - could just be random fluctuation.

Why wait 5 days? The immediate post-earnings reaction (days 0-2) often includes gap fills and noise. By day 5, if the stock is still extended beyond 1.5 ATRs from the earnings close, it suggests real buying pressure, not just a reflexive gap.

A passing grade here helps filter out stocks that "beat earnings" but haven't actually moved meaningfully. It focuses attention on stocks where the market is voting with real capital.

─────────────────────────────────────────

9. Days Since D0

─────────────────────────────────────────

WHAT IT IS:

Simply counts the number of trading days since the earnings reaction day (D0).

HOW TO INTERPRET:

- Days 0-5 (Green): Fresh earnings - the information is new, institutional repositioning is active, and momentum trades are most potent. This is the "sweet spot" for PEAD strategies.

- Days 6-10 (Neutral): Mid-period - some edge remains but diminishing. Good for adding to winning positions, less ideal for new entries.

- Days 11+ (Red): Extended period - most of the post-earnings drift has typically played out. Higher risk that momentum fades or reverses.

Research shows PEAD effects are strongest in the first 5-10 days after earnings, then decay. Beyond 20-30 days, the informational advantage of the earnings surprise is largely priced in.

Use this to prioritize: focus on stocks with strong signals that are still in the early window, and be more selective about entries as days accumulate.

═══════════════════════════════════════════════════════════════

PUTTING IT ALL TOGETHER

═══════════════════════════════════════════════════════════════

You can use this screener in the chart view or in the Screener.

One combination of the above filters to develop a shortlist of positive drift candidates may be:

- SUE > 2.0 (significant earnings beat)

- SURGE > 1.5 (significant revenue beat)

- Positive % From D0 Close (price confirming the good news)

- Institutional Buying PASS (big players accumulating)

- Strong ATR Drift PASS (statistically significant movement)

- Days Since D0 < 10 (still in the active drift window)

No single indicator is sufficient. The power comes from convergence - when multiple independent measures all point the same direction.

═══════════════════════════════════════════════════════════════

SETTINGS

═══════════════════════════════════════════════════════════════

Key adjustable parameters:

- SUE Method: "Analyst-based" uses consensus estimates; "Time-series" uses year-over-year comparison

- Window Size: Number of quarters used for standardization (default: 8)

- ATR Drift Threshold: Minimum ATR multiple for "strong" classification (default: 1.5)

- Institutional Buying thresholds: Adjustable volume and CLV parameters

═══════════════════════════════════════════════════════════════

DISCLAIMER

═══════════════════════════════════════════════════════════════

This screener is a research tool, not financial advice. Past patterns do not guarantee future results. Always conduct your own due diligence and manage risk appropriately. Post-earnings trading involves significant uncertainty and volatility. The 'SUE' in this indicator does not represent a real person; any similarity to actual Sue's (or Susans for that matter) living or dead is quite frankly ridiculous, not to mention coincidental.

Mutanabby_AI | ONEUSDT_MR1

ONEUSDT Mean-Reversion Strategy | 74.68% Win Rate | 417% Net Profit

This is a long-only mean-reversion strategy designed specifically for ONEUSDT on the 1-hour timeframe. The core logic identifies oversold conditions following sharp declines and enters positions when selling pressure exhausts, capturing the subsequent recovery bounce.

Backtested Period: June 2019 – December 2025 (~6 years)

Performance Summary

| Metric | Value |

|--------|-------|

| Net Profit | +417.68% |

| Win Rate | 74.68% |

| Profit Factor | 4.019 |

| Total Trades | 237 |

| Sharpe Ratio | 0.364 |

| Sortino Ratio | 1.917 |

| Max Drawdown | 51.08% |

| Avg Win | +3.14% |

| Avg Loss | -2.30% |

| Buy & Hold Return | -80.44% |

Strategy Logic :

Entry Conditions (Long Only):

The strategy seeks confluence of three conditions that identify exhausted selling:

1. Prior Move Filter:*The price change from 5 bars ago to 3 bars ago must be ≥ -7% (ensures we're not entering during freefall)

2. Current Move Filter: The price change over the last 2 bars must be ≤ 0% (confirms momentum is stalling or reversing)

3. Three-Bar Decline: The price change from 5 bars ago to 3 bars ago must be ≤ -5% (confirms a significant recent drop occurred)

When all three conditions align, the strategy identifies a potential reversal point where sellers are exhausted.

Exit Conditions:

- Primary Exit: Close above the previous bar's high while the open of the previous bar is at or below the close from 9 bars ago (profit-taking on strength)

- Trailing Stop: 11x ATR trailing stop that locks in profits as price rises

Risk Management

- Position Sizing:Fixed position based on account equity divided by entry price

- Trailing Stop:11× ATR (14-period) provides wide enough room for crypto volatility while protecting gains

- Pyramiding:Up to 4 orders allowed (can scale into winning positions)

- **Commission:** 0.1% per trade (realistic exchange fees included)

Important Disclaimers

⚠️ This is NOT financial advice.

- Past performance does not guarantee future results

- Backtest results may contain look-ahead bias or curve-fitting

- Real trading involves slippage, liquidity issues, and execution delays

- This strategy is optimized for ONEUSDT specifically — results may differ on other pairs

- Always test before risking real capital

Recommended Usage

- Timeframe:*1H (as designed)

- Pair: ONEUSDT (Binance)

- Account Size: Ensure sufficient capital to survive max drawdown

Source Code

Feedback Welcome

I'm sharing this strategy freely for educational purposes. Please:

- Drop a comment with your backtesting results any you analysis

- Share any modifications that improve performance

- Let me know if you spot any issues in the logic

Happy trading

As a quant trader, do you think this strategy will survive in live trading?

Yes or No? And why?

I want to hear from you guys

Killzones (EST)Asian Range

19:00 – 00:00 EST

Consolidation, liquidity build

London Open

02:00 – 05:00 EST

Initial expansion, Judas Swing

New York Open

07:00 – 10:00 EST

Main move, SMT, MSS setups

NY Lunch/Reversal

11:30 – 13:00 EST

Rebalancing, exit window

Gyspy Bot Trade Engine - V1.2B - Alerts - 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Alerts & Visualization

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script V6 environment. While most tools rely on a single dominant indicator to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

Note: This is the Indicator / Alerts version of the engine. It is designed for visual analysis and generating live alert signals for automation. If you wish to see Backtest data (Equity Curves, Drawdown, Profit Factors), please use the Strategy version of this script.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only fires a signal plot when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to signal forced exits, preserving capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the charts look perfect in hindsight, only to have the signals fail in live markets because they were tuned to historical noise rather than market structure.

To use this engine successfully:

Visual Verification: Do not just look for "green arrows." Look for signals that occur at logical market structure points.

Stability: Ensure signals are not flickering. This script uses closed-candle logic for key decisions to ensure that once a signal plots, it remains painted.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Gypsy Bot settings should be reviewed and adjusted at regular intervals to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY plot a Buy Signal if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the signal is rejected.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: Filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold.

Module 2: Correlation Trend Indicator (CTI)

Logic: Measures how closely the current price action correlates to a straight line (a perfect trend).

Function: Ensures that we are moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A spectral filter combining High-Pass (trend removal) and Super Smoother (noise removal).

Function: Isolates the "Roof" of price action to catch cyclical turning points before standard moving averages.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: Signals when the regression trend flips. Offers "Aggressive" and "Conservative" calculation modes.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from extremes.

Function: Used as an entry filter. If price is above the Chandelier line, the trend is Bullish.

Module 6: Crypto Market Breadth (CMB)

Logic: Pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts).

Function: Calculates "Market Health." If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator using Advance/Decline and Volume data.

Function: One of the most powerful modules. Confirms that price movement is supported by actual volume flow. Recommended setting: "SSMA" (Super Smoother).

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis.

Function: Checks for a "Kumo Breakout." Price must be fully above/below the Cloud to confirm entry.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes harmonic wave properties to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector.

Module 11: HSRS Compression / Super AO

Logic: Detects volatility compression (HSRS) or Momentum/Trend confluence (Super AO).

Function: Great for catching explosive moves resulting from consolidation.

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. Uses Multi-Timeframe (MTF) logic to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors.

Bitcoin Halving Logic: Prevents trading during chaotic weeks surrounding Halving events (dates projected through 2040).

Miner Capitulation: Uses Hash Rate Ribbons to identify bearish regimes when miners are shutting down.

ADX Filter: Prevents trading in "Flat/Choppy" markets (Low ADX).

CryptoCap Trend: Checks the total Crypto Market Cap chart for broad market alignment.

6. Risk Management & The Dump Protection Team (DPT)

Even in this Indicator version, the RM logic runs to generate Exit Signals.

Dump Protection Team (DPT): Detects "Nuke" (Crash) or "Moon" (Pump) volatility signatures. If triggered, it plots an immediate Exit Signal (Yellow Plot).

Advanced Adaptive Trailing Stop (AATS): Dynamically tightens stops in low volatility ("Dungeon") and loosens them in high volatility ("Penthouse").

Staged Take Profits: Plots TP1, TP2, and TP3 events on the chart for visual confirmation or partial exit alerts.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These filter out bad signals during high volatility.

Tune Module 8 (MTI): Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders to filter out noise.

Alert Setup: Once visually satisfied, use the "Any Alert Function Call" option when creating an alert in TradingView to capture all Buy/Sell/Close events generated by the engine.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This indicator uses Closed Candle data for all Risk Management and Entry decisions. This ensures that signals do not vanish after the candle closes.

Visuals:

Blue Plot: Buy/Sell Signal.

Yellow Plot: Risk Management (RM) / DPT Close Signal.

Green/Lime/Olive Plots: Take Profit hits.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Cryptocurrency trading involves substantial risk of loss. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

Gyspy Bot Trade Engine - V1.2B - Strategy 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Ultimate Strategy & Backtest

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script environment. While most strategies rely on a single dominant indicator (like an RSI cross or a MACD flip) to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only executes a trade entry when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction before capital is committed.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to force-exit positions, overriding standard stops to preserve capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the backtest shows a 100% win rate, only to have the strategy fail immediately in live markets because it was tuned to historical noise rather than market structure.

To use this engine successfully, you must adopt a specific optimization mindset:

Ignore Raw Net Profit: Do not tune for the highest dollar amount. A strategy that makes $1M in the backtest but has a 40% drawdown is useless.

Prioritize Stability: Look for a high Profit Factor (1.5+), a high Percent Profitable, and a smooth equity curve.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Parameters that worked perfectly in 2021 may fail in 2024. Gypsy Bot settings should be reviewed and adjusted at regular intervals (e.g., quarterly) to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY trigger a Buy Entry if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the trade is rejected.

This allows you to mix "Leading" indicators (Oscillators) with "Lagging" indicators (Moving Averages) to create a high-probability entry signal that requires momentum, volume, and trend to all be in alignment.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: It filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold. This helps avoid entering trades during weak drifts that often precede a reversal.

Module 2: Correlation Trend Indicator (CTI)

Logic: Based on John Ehlers' work, this measures how closely the current price action correlates to a straight line (a perfect trend).

Function: It outputs a confidence score (-1 to 1). Gypsy Bot uses this to ensure that we are not just moving up, but moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A sophisticated spectral filter that combines a High-Pass filter (to remove long-term drift) with a Super Smoother (to remove high-frequency noise).

Function: It attempts to isolate the "Roof" of the price action. It is excellent at catching cyclical turning points before standard moving averages react.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: When the Forecast Oscillator crosses its zero line, it indicates that the regression trend has flipped. We offer both "Aggressive" and "Conservative" calculation modes for this module.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from the highest high (for longs) or lowest low (for shorts).

Function: Used here as an entry filter. If price is above the Chandelier line, the trend is Bullish. It also includes a "Bull/Bear Qualifier" check to ensure structural support.

Module 6: Crypto Market Breadth (CMB)

Logic: This is a macro-filter. It pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts) across different exchanges.

Function: It calculates a "Market Health" percentage. If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade, ensuring you don't buy into a "fake" rally driven by a single asset.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding. A buy signal is generated only when the positive directional movement overpowers the negative movement with expanding momentum.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator. It uses Advance/Decline data and Up/Down Volume data.

Function: This is one of the most powerful modules. It confirms that price movement is supported by actual volume flow. We recommend using the "SSMA" (Super Smoother) MA Type for the cleanest signals on the 4H chart.

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis using the Tenkan-sen and Kijun-sen.

Function: Checks for a "Kumo Breakout." Price must be fully above the Cloud (for longs) or below it (for shorts). This is a classic "trend confirmation" module.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes the harmonic wave properties of price action to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector. It tries to identify when a cycle has bottomed out (for buys) or topped out (for sells) before the main trend indicators catch up.

Module 11: HSRS Compression / Super AO

Logic: Two options in one.

HSRS: Hirashima Sugita Resistance Support. Detects volatility compression (squeezes) relative to dynamic support/resistance bands.

Super AO: A combination of the Awesome Oscillator and SuperTrend logic.

Function: Great for catching explosive moves that result from periods of low volatility (consolidation).

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. This module uses Multi-Timeframe (MTF) logic to look at higher-timeframe trends (e.g., looking at the Daily Fisher while trading the 4H chart) to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors. If any of these are triggered, the trade is blocked.

Bitcoin Halving Logic:

Hardcoded dates for past and projected future Bitcoin halvings (up to 2040).

Trading is inhibited or restricted during the chaotic weeks immediately surrounding a Halving event to avoid volatility crushes.

Miner Capitulation:

Uses Hash Rate Ribbons (Moving averages of Hash Rate).

If miners are capitulating (Shutting down rigs due to unprofitability), the engine flags a "Bearish" regime and can flip logic to Short-only or flat.

ADX Filter (Flat Market Protocol):

If the Average Directional Index (ADX) is below a specific threshold (e.g., 20), the market is deemed "Flat/Choppy." The bot will refuse to open trend-following trades in a flat market.

CryptoCap Trend:

Checks the total Crypto Market Cap chart. If the broad market is in a downtrend, it can inhibit Long entries on individual altcoins.

6. Risk Management & The Dump Protection Team (DPT)

Gypsy Bot separates "Entry Logic" from "Risk Management Logic."

Dump Protection Team (DPT)

This is a specialized logic branch designed to save the account during Black Swan events.

Nuke Protection: If the DPT detects a volatility signature consistent with a flash crash, it overrides all other logic and forces an immediate exit.

Moon Protection: If a parabolic pump is detected that violates statistical probability (Bollinger deviations), DPT can force a profit take before the inevitable correction.

Advanced Adaptive Trailing Stop (AATS)

Unlike a static trailing stop (e.g., "trail by 5%"), AATS is dynamic.

Penthouse Level: If price is at the top of the HSRS channel (High Volatility), the stop loosens to allow for wicks.

Dungeon Level: If price is compressed at the bottom, the stop tightens to protect capital.

Staged Take Profits

TP1: Scalp a portion (e.g., 10%) to cover fees and secure a win.

TP2: Take the bulk of profit.

TP3: Leave a "Runner" position with a loose trailing stop to catch "Moon" moves.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Reset: Turn OFF Trailing Stop, Stop Loss, and Take Profits. (We want to see raw entry performance first).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These have the highest impact on net performance.

Tune Module 8 (MTI): This module is a heavy filter. Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules 1-12 based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders. A lower number = More Trades (Aggressive). A higher number = Fewer, higher conviction trades (Conservative).

Final Polish: Re-enable Stop Losses, Trailing Stops, and Staged Take Profits to smooth the equity curve and define your max risk per trade.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This strategy uses Closed Candle data for all Risk Management and Entry decisions. This ensures that Backtest results align closely with real-time behavior (no repainting of historical signals).

Alerts: This script generates Strategy alerts. If you require visual-only alerts, see the source code header for instructions on switching to "Study" (Indicator) mode.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

ShooterViz Lazy Trader EMA SystemShooterViz Lazy Trader EMA System - Complete User Guide

What This Script Does

This is a position scaling indicator that tells you exactly when to enter, add to, and exit trades using a simplified 5-EMA system. It removes the guesswork and decision fatigue from trading by giving you clear visual signals.

The Core Concept

3 entry signals that build your position from 20% → 50% → 100%

2 exit signals that scale you out at 50% → 50% (complete exit)

1 higher timeframe filter that keeps you on the right side of the trend

No Fibonacci calculations, no RSI divergence, no multi-indicator confusion. Just EMAs and price action.

What You'll See On Your Chart

1. Colored EMA Lines

Blue Lines (Entry Zone):

3 EMA (lightest blue) - Early reversal detector

5 EMA (darker blue) - Confirmation line

Green Lines (Add Zone):

21 EMA (bright green) - First add location

34 EMA (lighter green) - Final add location

Red Lines (Exit Zone):

89 EMA (lighter red) - First exit trigger

144 EMA (darker red) - Final exit trigger

Orange Lines (Hyper Frame - optional):

Hyper 21 EMA (from higher timeframe) - Trend direction

Hyper 34 EMA (from higher timeframe) - Bias confirmation

2. Triangle Signals

Green Triangles (Below Price) = BUY/ADD:

Lime triangle with "20%" = Entry 1: Price reclaimed 3→5 EMA (starter position)

Green triangle with "30%" = Entry 2: Price bounced off 21 EMA (first add)

Teal triangle with "50%" = Entry 3: Price broke out from 34 EMA compression (final add)

Red Triangles (Above Price) = SELL:

Orange triangle with "50% OFF" = Exit 1: Price broke below 89 EMA (take half off)

Red triangle with "EXIT ALL" = Exit 2: Price broke below 144 EMA (close remaining position)

3. Background Color (Trend Bias)

Light green background = Hyper frame EMAs trending up (bias LONG)

Light red background = Hyper frame EMAs trending down (bias SHORT)

Gray background = Neutral/choppy (be cautious)

4. Info Table (Top Right Corner)

A live status dashboard showing:

Which entry signals are currently active (✓ or —)

Which exit signals are currently active (⚠ or ⛔)

Current hyper frame bias (🟢 LONG / 🔴 SHORT / ⚪ NEUTRAL)

Which timeframe you're using for hyper frame filtering

How to Install and Set Up

Step 1: Add the Script to TradingView

Open TradingView

Click "Pine Editor" at the bottom of the screen

Copy the entire script code

Paste it into the Pine Editor

Click "Add to Chart"

Step 2: Configure Your Settings

Click the gear icon ⚙️ next to "LazyEMA" in your indicators list.

Critical Settings to Configure:

Hyper Frame Selection (Most Important!)

Location: "Hyper Frame (Pick ONE)" section

Setting: "Timeframe"

What to choose:

Trading 15min or 1H charts? → Use "240" (4-hour)

Trading 4H or Daily charts? → Use "D" (Daily)

Trading Daily or Weekly charts? → Use "W" (Weekly)

Why this matters: This filter keeps you aligned with the bigger trend. Only take longs when this timeframe is green, shorts when it's red.

MA Type (Optional, default is fine)

Location: "MA Config" section

Default: EMA (recommended)

Options: EMA, SMA, WMA, HMA, RMA, VWMA

Most traders should stick with EMA

Visual Toggles (Customize your view)

Entry Zone: Turn individual EMAs on/off (3, 5, 21, 34)

Exit Zone: Turn individual EMAs on/off (89, 144)

Hyper Frame: Toggle the higher timeframe EMAs on/off

Step 3: Clean Up Your Chart

Turn OFF these if visible:

Volume bars (they clutter the view)

Any other indicators you have loaded

Grid lines (optional, but cleaner)

Keep ONLY:

Price candles

Your ShooterViz Lazy Trader EMA System

Maybe support/resistance levels if you manually draw them

How to Trade With This Script

The Basic Workflow

Before the Market Opens:

Check the background color and info table bias

Green background? Look for LONG setups only

Red background? Look for SHORT setups only

Gray background? Stay flat or trade small

During the Trading Session:

LONGS (When hyper frame is bullish):

Wait for Entry 1 signal:

Lime triangle appears with "20%"

Price has reclaimed the 5 EMA after dipping to 3 EMA

Action: Enter 20% of your intended position

Stop loss: Place below the 5 EMA or recent swing low

Wait for Entry 2 signal:

Green triangle appears with "30%"

Price pulled back to 21 EMA and bounced

Action: Add 30% more (you're now at 50% total)

Move stop: Trail it up to below 21 EMA

Wait for Entry 3 signal:

Teal triangle appears with "50%"

Price compressed at 34 EMA and broke out

Action: Add final 50% (you're now 100% loaded)

Move stop: Trail it up to below 34 EMA

Wait for Exit 1 signal:

Orange triangle appears with "50% OFF"

Price broke below 89 EMA

Action: Exit 50% of your position immediately

Move stop on rest: Trail to 89 EMA or lock in profits

Wait for Exit 2 signal:

Red triangle appears with "EXIT ALL"

Price broke below 144 EMA

Action: Exit remaining 50% (you're now flat)

Or: Stop gets hit at 89 EMA (same result)

SHORTS (When hyper frame is bearish):

Same process, but inverted

Triangles appear above price instead of below

Look for breakdowns below EMAs instead of bounces off them

Exit when price reclaims 89 and 144 EMAs

Real-World Example Walkthrough

Setup: Trading ES (S&P 500 Futures) on 1H Chart

Chart Configuration:

Timeframe: 1 Hour

Hyper Frame: 240 (4-hour)

Ticker: ES

Pre-Market Check:

Background is light green

Info table shows "🟢 LONG" for Hyper Bias

Decision: Only look for long entries today

9:30 AM - Market Opens

Price dips and touches 3 EMA

Watch for: Reclaim of 5 EMA

9:45 AM - Entry 1 Triggers

Lime triangle appears below bar

Price closed above 5 EMA at $4,550

Action taken:

Enter long 20% position (2 contracts if targeting 10 total)

Stop loss at $4,545 (below 5 EMA)

Risk: $10 per contract × 2 = $20 risk

10:30 AM - Entry 2 Triggers

Price rallied to $4,565, pulls back

Green triangle appears at 21 EMA ($4,555)

Action taken:

Add 30% (3 more contracts, now have 5 total)

Move stop to $4,550 (below 21 EMA)

Current P/L: +$25 ($5 gain on original 2 contracts, break-even on new 3)

11:15 AM - Entry 3 Triggers

Price consolidates at 34 EMA around $4,560

Teal triangle appears as price breaks to $4,568

Action taken:

Add final 50% (5 more contracts, now have 10 total)

Move stop to $4,555 (below 34 EMA)

Current P/L: +$70

1:00 PM - Price Extends

Price rallies to $4,595 (on track)

89 EMA is at $4,575

No action yet, let it run

2:15 PM - Exit 1 Triggers

Price pulls back from $4,600

Orange triangle appears as price breaks below 89 EMA at $4,580

Action taken:

Exit 50% (5 contracts closed at $4,580)

Keep 5 contracts with stop at 89 EMA ($4,575)

Banked: +$150 average gain on closed 5 contracts

2:45 PM - Exit 2 Triggers

Price continues down

Red triangle appears as price breaks 144 EMA at $4,570

Action taken:

Exit remaining 5 contracts at $4,570

Banked: +$100 on remaining 5 contracts

Final Results:

Total gain: $250 on the trade

Initial risk: $50 (if stopped out at Entry 1)

Risk/Reward: 5:1

Time in trade: ~5 hours

Common Questions

"What if I miss Entry 1? Can I still take Entry 2?"

Yes! Each entry is independent. If you miss the 3→5 reclaim, wait for the 21 EMA bounce. You'll start with a 30% position instead of 20%, but that's fine.

Rule: Never chase. Wait for the next EMA setup.

"What if multiple entry signals trigger at the same bar?"

Rare, but possible. If you see both Entry 1 and Entry 2 trigger together:

Take Entry 1 first (20%)

If the next bar confirms Entry 2 is still valid, add 30%

When in doubt, scale in gradually

"The hyper frame is green but I'm seeing short signals?"

Don't take them. The hyper frame is your bias filter. If it says "go long," ignore short setups. They're usually lower probability and will get stopped out.

"Can I use this for swing trading overnight?"

Absolutely. Just switch your hyper frame:

If you're on Daily charts, use Weekly hyper frame

If you're on 4H charts, use Daily hyper frame

Adjust position sizes for overnight risk

"What if the signal appears right at market close?"

Don't chase it. Wait for the next bar (next day) to confirm. Signals that appear in the last 5 minutes are often noise.

"How do I set up alerts?"

Right-click on the chart

Select "Add Alert"

Choose "LazyEMA" from the condition dropdown

Select which signal you want alerts for:

Entry 1: 3→5 Reclaim

Entry 2: 21 EMA Add

Entry 3: 34 EMA Breakout

Exit 1: 89 EMA Break

Exit 2: 144 EMA Break

Click "Create"

Pro tip: Set up all 5 alerts so you never miss a signal.

Position Sizing Guide see

swingtradenotes.substack.com

Critical Rule: Know your total risk BEFORE you take Entry 1. Don't wing it.

Customization Tips

For Day Traders (Scalpers)

Use 5min or 15min charts

Hyper frame: 1H or 4H

Expect 2-4 setups per day

Tighter stops (0.5% risk per entry)

For Swing Traders

Use 4H or Daily charts

Hyper frame: Daily or Weekly

Expect 1-2 setups per week

Wider stops (1-2% risk per entry)

For Position Traders

Use Daily or Weekly charts

Hyper frame: Weekly or Monthly

Expect 1-2 setups per month

Widest stops (2-3% risk per entry)

The "Don't Be Stupid" Checklist

Before taking ANY signal from this script, ask:

✅ Is the hyper frame bias pointing in my direction?

✅ Is the signal clean (not at a weird time or during news)?

✅ Do I know my stop loss level?

✅ Do I know my position size?

✅ Can I afford to lose if this trade fails?

If you answered "no" to ANY of these, skip the trade.

Troubleshooting

"I'm not seeing any signals"

Possible causes:

The "Show Lazy Trader System" toggle is off (turn it on)

Your chart timeframe is too high (try 1H or 4H)

Market is in a tight range (EMAs are compressed)

You need to refresh the chart

"Too many signals, getting whipsawed"

Fixes:

Increase your chart timeframe (go from 15m to 1H)

Switch to a less volatile ticker

Only trade when hyper frame bias is STRONG (not neutral)

Add a minimum bar count between signals

"The info table is covering my price action"

Fix:

Edit the script