【MasterHSC】CCI Mean Derivative Smart Strategy🧾 Strategy Description (English)

CCI Mean Slope Smart Strategy

This strategy is built on the derivative slope behavior of the Commodity Channel Index (CCI) mean line.

It identifies key turning points or trend continuations based on how the smoothed CCI (mean value) changes direction after reaching overbought or oversold zones.

Core Idea:

When the CCI mean reverses slope after exceeding ±100, it signals a potential mean reversion (range-trading opportunity).

When the CCI mean remains above +100 or below −100 with a consistent slope, it indicates a strong trending phase (momentum continuation).

The strategy dynamically adapts between these two behaviors depending on market conditions.

Modes:

🌀 Range Reversal Mode — Focuses on slope reversals after overbought/oversold conditions.

🚀 Trend Following Mode — Captures strong momentum when the CCI mean stays extended.

🧠 Auto Mode — Automatically switches between Range and Trend logic based on CCI mean volatility.

Key Features:

Dual-direction toggle: Enable or disable long/short entries independently.

Adjustable tolerance: Choose fixed or dynamic thresholds for flexibility.

Automatic mode label and visual buy/sell markers on the chart.

Pure CCI-based system — no external filters or indicators required.

Purpose:

This system is designed to reduce false signals in sideways markets while preventing missed opportunities during strong directional trends, offering a clean balance between precision and adaptability.

ابحث في النصوص البرمجية عن "Candlestick"

Empire OS Trading Fully Automated Prop Firm Ready💎 Prop-Firm-Ready Momentum System v3 — The Gold-Mine Algorithm 💎

Engineered for the same standards that top prop firms demand — minimal drawdown, consistent equity growth, and precision-based execution. This isn’t a basic indicator; it’s a refined momentum engine built for traders who scale capital and manage risk like professionals.

Performance Snapshot

• Profit Factor 2.26 • Win Rate 33 % • Max Drawdown 0.9 % • Total P/L + $447 • W/L Ratio 4.6 : 1

Stress-tested on Gold (XAUUSD) across live-market conditions, it stays composed under volatility and delivers structured, data-driven consistency.

⚡ See it. Test it. Scale it.

Built for prop-firm precision — from $10 K to $300 K and beyond.

AIBTC Automated Trading Strategy🧠 AIBTC Automated Trading Strategy

Overview:

The AIBTC Automated Trading Strategy is a fully autonomous system designed for 4-hour timeframes (4H). It dynamically identifies support and resistance levels based on price action, and automatically executes trades when valid breakouts occur above resistance or below support. The system adapts in real time to changing market volatility, ensuring stable performance across different market conditions.

⚙️ Strategy Logic

Dynamic Support & Resistance Detection

The strategy uses an adaptive Pivot Point algorithm that adjusts parameters according to market volatility (ATR) and price deviation (Standard Deviation).

When volatility increases, the algorithm automatically widens its detection range and recalibrates channel width for better accuracy.

All support and resistance levels are detected dynamically — no manual configuration is required.

Trend & Volatility Filtering

The system applies ADX (Average Directional Index) to measure trend strength.

When ADX > 25, only strong levels are considered valid to avoid noise during weak trends.

ATR-based volatility adjustments automatically optimize lookback periods and detection sensitivity.

Breakout Signal Detection

A long position is triggered when price breaks above resistance with a valid breakout margin (default filter: 0.1%).

A short position is triggered when price breaks below support with the same breakout filter applied.

This breakout filter effectively minimizes false breakouts and improves signal quality.

Fully Automated Execution

The system is designed for both backtesting and live simulation.

All buy/sell entries are executed automatically without manual input once conditions are met.

🕒 Recommended Timeframe

4-hour (4H) candles

Suitable for short-to-medium term swing trading, balancing signal precision and trade frequency.

📊 Key Features

✅ Fully Automated — Executes long/short positions on valid breakouts

✅ Adaptive Parameters — Automatically adjusts to changing volatility

✅ Trend-Aware Filtering — Uses ADX to avoid false signals in ranging markets

✅ Multi-Asset Compatibility — Works on BTC, ETH, or any high-liquidity instrument

⚠️ Disclaimer

This strategy is a technical and algorithmic tool, not financial advice.

Always backtest and simulate before using it on live markets.

During periods of extreme volatility, signals may delay or show false breakouts — consider using stop-loss mechanisms accordingly.

EMA 9/50 News Confirmation Strategy v3 (Trend Aligned 3 bMin) “EMA 9/50 crossover strategy with trend filter and ATR-based targets”)

ApexSignalsIve been working with pine code for a really long time now, took me about 6 months to build this script, hopefully it works well for you.very good for trading. will help you out a lot

Cybertrading-Insidebar hunter pro robotThe Cybertrading-Inside Pro strategy is an advanced version of Cyber-Inside.

It automates ATR-based inside-bar trading with optional pullback entries, full risk/reward visualization, time filtering, pending-order handling, and fixed chart watermark branding (“CollegePips / CyberTrading”).

⚙️ Technical Overview

1. Core Structure

Uses ATR(14) to measure volatility and classify candle ranges.

Candles are labeled as Spinning, Standard, Long, or Huge based on their range vs. ATR.

Only valid candles (Standard or Long) qualify to confirm a setup.

2. Inside-Bar Logic

The setup requires the current candle’s high/low to be fully contained inside the previous candle (an inside bar).

A wick-break must occur — the wick slightly breaks the previous inside bar’s range while the body remains inside.

This pattern forms a Pierce-Only signal.

Direction:

Wick down → potential Long entry

Wick up → potential Short entry

3. Timing and Entry Conditions

With the time filter enabled, trades trigger only between defined hours (e.g., 07–22).

If Enable Pullback is on, the entry is placed using a limit order offset by pullbackATR × ATR from the signal candle.

If the pullback entry isn’t triggered within pullbackMaxBars, the pending order is canceled automatically.

You can also enable display-only entries without execution (Enable Entry Without Pullback).

4. Risk & Target Management

Stop loss is placed beyond the second-previous candle’s high/low ± stopBuffer × ATR.

Take-profit is based on the chosen risk/reward multiple (RR) or the previous candle’s high/low.

Position size auto-adjusts to keep total risk equal to riskPercent of equity.

5. Visual Components

Dynamic chart objects include:

Red box: risk zone (entry → stop)

Green/blue box: reward zone (entry → target)

Dotted diagonal line: risk-to-reward path

Arrows: actual fill points

6. Order Management System

Each signal creates a unique order ID (pendingId) and exit ID (planExitId).

On a valid fill (newLong / newShort), real stop, target, and position size are applied.

If an order isn’t filled within the timeout window, it’s canceled and reset automatically.

7. Advantages

✅ Smart inside-bar pattern recognition

✅ Automated risk control and dynamic sizing

✅ Clear visual feedback for analysis

✅ Fully backtest-ready for research or education

CBC Flip StrategyThe CBC Flip Strategy is a momentum-based trading system that identifies shifts in market control by monitoring price closes relative to previous bars' highs and lows: it flips to bullish mode when the close exceeds the prior high (indicating bulls in control) and enters a long position, or to bearish mode when the close falls below the prior low (indicating bears in control) and enters a short position, all while incorporating optional confluences like higher timeframe CBC alignment, RSI thresholds (above 50 + offset for longs, below 50 - offset for shorts), and EMA positioning (above for longs, below for shorts) to filter entries; trades are restricted to a user-defined session window and direction preferences, with exits handled via tick-based TP/SL, reversal on chart or higher timeframe CBC flips, and an optional flatten at a specified time to close all positions.

Number of Contracts: Adjust the quantity of contracts per trade (default: 1).

SL and TP Ticks: Set stop-loss (default: 12 ticks) and take-profit (default: 24 ticks) distances from entry.

Exit Strategy: Choose from TP/SL in ticks, exit on chart CBC flip (reverses on opposite signal), or exit on higher timeframe CBC flip.

Flatten All: Enable/disable flattening all positions at a customizable time (default: 16:00, with adjustable hour/minute).

Trading Session: Define the time window for allowing entries (default: 0800-1700).

Trade Direction: Select "Both" (longs and shorts), "Only Long", "Only Short", or "Towards Daily Open" (longs if below daily open, shorts if above).

Higher Timeframe CBC Confluence: Toggle use of HTF CBC alignment (default: enabled, with customizable HTF like "240").

RSI Confluence: Toggle RSI filter (default: enabled, with adjustable length=14, offset=20 for thresholds).

EMA Confluence: Toggle EMA filter (default: enabled, with adjustable length=200 for position relative to price).

Enhanced OB Retest Strategy v7.0The OB Retest Strategy is a full Order Block retest trading system that detects, plots, and trades OB zones across multiple timeframes. It uses structure breaks, retrace depth, and ATR filters to identify strong reversal or continuation setups.

⸻

⚙️ Core Features

• Multi-timeframe OB detection using break-of-structure (BOS) logic

• Automatic zone creation for bullish and bearish order blocks

• Smart merging of overlapping OB zones

• Dynamic flip-zone logic that turns invalidated OBs into new zones

• Wick zone detection for high-precision entries

• ATR-based trailing stop and optional breakeven

• Adjustable retrace depth, breakout %, and ATR filters

• Built-in performance table showing PnL, win rate, and total trades

• Fully backtestable with date range and commission control

⸻

🧠 Logic Summary

1. Detects a BOS on the higher timeframe.

2. Identifies the last opposing candle as the valid OB.

3. Validates the OB based on ATR size and breakout strength.

4. Waits for price to retest the zone to a set depth.

5. Executes trades and manages exits using trailing stop or breakeven.

6. Flips invalidated zones automatically.

⸻

💡 Usage Tips

• Best used on 1H to 4H charts for swing setups.

• Tune ATR and breakout thresholds for your market’s volatility.

• Combine with higher-timeframe bias or liquidity levels for better accuracy.

⸻

⚠️ Notes

• For educational and testing purposes only.

• Backtested results do not predict future performance.

• Always test before live use.

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

Crypto Pro Strategy (Entry Model + Risk)Imma try to use this on a prop firm but if you want to use it itss free or im going to try to make it free

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

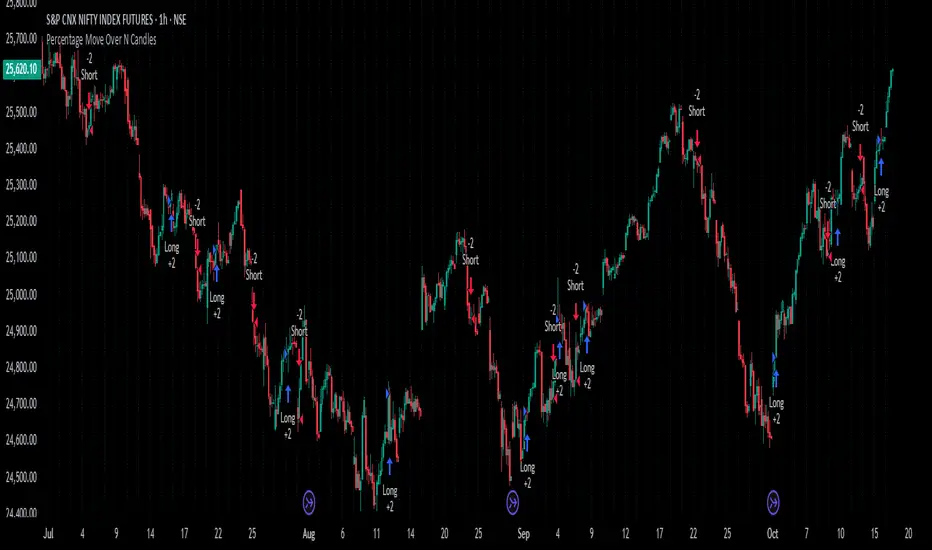

Percentage Move Over N CandlesThis strategy enters long/short trades if the price goes up/down by a certain defined percentage of the price, over a previous certain number of candles. Can be run on any time frame and on any instrument and alerts can be enabled.

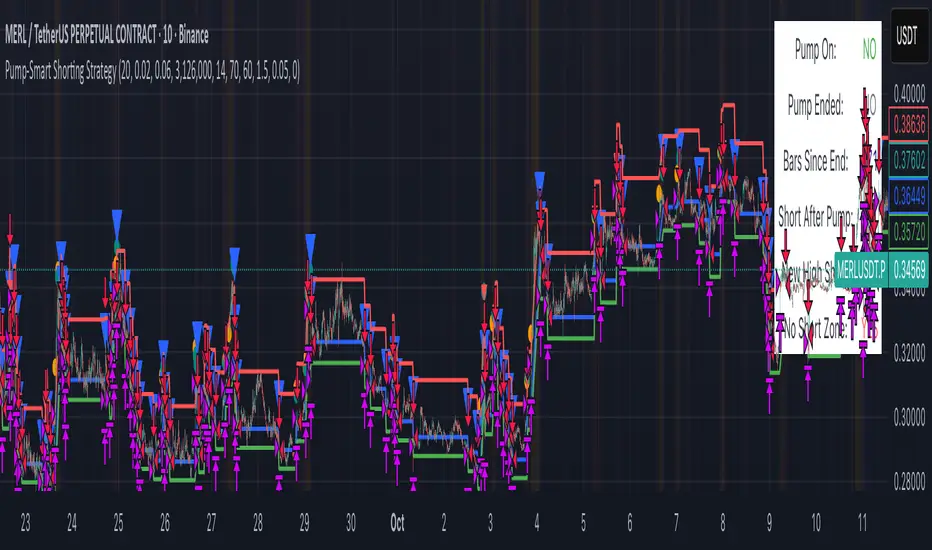

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

MAUL RSI Gaussian Filter MACD Gaussian Filter MACD — Strategy (with RSI Gate)

A momentum-first, chop-aware strategy built on a Gaussian-smoothed MACD with an optional RSI threshold filter. It looks for clean transitions in trend and ignores half-hearted wiggles around the zero line. You choose how signals are confirmed and whether shorts are allowed—no clutter, just deliberate entries and exits.

What it does (at a glance)

Confirms momentum using a smoothed MACD and a selectable signal mode.

Optional RSI gate to avoid low-quality breakouts.

Flexible source options (incl. Heikin-Ashi families) to match your charting style.

Long-only by default; shorts are an option.

Built-in alerts for entries/exits.

How to use

Add to chart and select your preferred signal mode.

Toggle the RSI gate and set your threshold to filter weak setups.

Forward-test across symbols/timeframes; then walk it into live with conservative sizing.

Notes

The parameters and internals are intentionally locked to protect IP and avoid over-fitting by casual copycats.

Works best on liquid symbols with consistent session structure.

Risk

Backtests are not a promise. Markets are noisy, slippage is real, and capital at risk should be sized accordingly. Use with sound risk management and a clear exit plan.

4hr / BTCBTCUSDT.P / 4hr

趨勢線交易策略

設定可以如我圖表

也可以自己找合適的

測試請用最大虧損的三倍金額下去打

圖以含手續費(0.06%)

可以用小金額去打

最大淨利與最大虧損績效比 1:10

平均獲利/虧損盈虧比 2.135

長期放保證獲利

沒獲利或獲利較小的那年通常是大事件

如2022

有問題私訊 謝謝

BTCUSDT.P / 4hr

Trendline Trading Strategy

You can set it up the same way as shown on my chart,

or find your own suitable setup.

For testing, please use three times the maximum loss as your trading capital.

The chart should include fees (0.06%).

You can trade with a small amount.

Performance:

Maximum profit to maximum loss ratio: 1:10

Average profit/loss ratio: 2.135

Guaranteed profit in the long term

Years with no profit or smaller profit are usually caused by major events,

such as 2022.

If you have any questions, please DM me. Thank you.

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

Larry Williams Oops StrategyThis strategy is a modern take on Larry Williams’ classic Oops setup. It trades intraday while referencing daily bars to detect opening gaps and align entries with the prior day’s direction. Risk is managed with day-based stops, and—unlike the original—all positions are closed at the end of the session (or at the last bar’s close), not at a fixed profit target or the first profitable open.

Entry Rules

Long setup (bullish reversion): Today opens below yesterday’s low (down gap) and yesterday’s candle was bearish. Place a buy stop at yesterday’s low + Filter (ticks).

Short setup (bearish reversion): Today opens above yesterday’s high (up gap) and yesterday’s candle was bullish. Place a sell stop at yesterday’s high − Filter (ticks).

Longs are only taken on down-gap days; shorts only on up-gap days.

Protective Stop

If long, stop loss trails the current day’s low.

If short, stop loss trails the current day’s high.

Exit Logic

Positions are force-closed at the end of the session (in the last bar), ensuring no overnight exposure. There is no take-profit; only stop loss or end-of-day flat.

Notes

This strategy is designed for intraday charts (minutes/seconds) using daily data for gaps and prior-day direction.

Longs/shorts can be enabled or disabled independently.

SHALOM TRADING HUB – Bollinger Band SystemSHALOM TRADING HUB – Bollinger Band System (Strategy)

All-in-one BB system with both Breakout and Mean-Reversion modes.

Automatic ENTRY / EXIT / STOP-LOSS, optional Mid-Band Exit, ATR or % risk, and built-in alerts. Backtest-ready.

What it does

Bollinger Bands: Basis = SMA(length); Upper/Lower = ±(mult × StDev).

Signals

Breakout mode

LONG → price crosses above Upper

SHORT → price crosses below Lower

Mean-Reversion mode

LONG → price re-enters above Lower

SHORT → price re-enters below Upper

Risk / Exits

ATR mode: SL = ATR × Mult, TP = SL × Risk:Reward

% mode: SL = %Stop, TP = %Take Profit

Optional Mid-Band (Basis) cross exit.

Visuals: BB lines + active Entry / SL / TP overlays + last-bar price labels.

Alerts: Breakout / Mean-Reversion signals and TP/SL hits.

Inputs (Settings)

Source, Length, Multiplier – BB calculation.

Signal Mode – Breakout or Mean Reversion.

Use ATR Stop/Target? – On = ATR; Off = %.

ATR Length, ATR Mult (SL), Risk:Reward (TP)

% Stop, % Take Profit (when ATR is Off)

Also exit on Mid-Band cross? – On/Off.

Alerts only on bar close? – Filters to confirmed bars.

Entry / Exit / Stop

Entry: Auto when the chosen signal condition triggers.

Stop-Loss: Placed from ATR or % settings.

Take-Profit: Set by R:R or % settings.

Mid-Band Exit (optional):

LONG → exit if close < Basis

SHORT → exit if close > Basis

Alerts (How-to)

Add the strategy to the chart → click Alerts (⚠️).

Condition: “SHALOM BB System” → choose:

BB Breakout LONG / SHORT

BB Mean-Reversion LONG / SHORT

Long TP Hit / Long SL Hit / Short TP Hit / Short SL Hit

Choose Once per bar or Once per bar close.

Backtest Tips

Match timeframe to your instrument.

Tune ATR/Mult, R:R, % to volatility.

Session filter (e.g., 09:20–15:20 IST) can be added easily in code.

Default pyramiding = 0; raise if you want multiple entries.

Trend Catcher and Mean ReversionPlease DM if you want to use this strategy.

it took long time to make this code profitable using 3 parameters only!

it allow you to:

1- Pyramid as you see fit.

2- allow option to use trend catching strategy ( while keeping mean reversion strategy)

3- Time filter to limit trading and exit at your preferred time.

4- it works for long, short or both positions.

5- has trailing tp as an option as well while keeping initial sl as hard stop

6- tp multiple (of stop loss) is optional

ongoing working for alerts and automation. More on that for subscribers only.

i will charge the minimum fee to utilize this code as we don't need your money but we need people to support our vision.

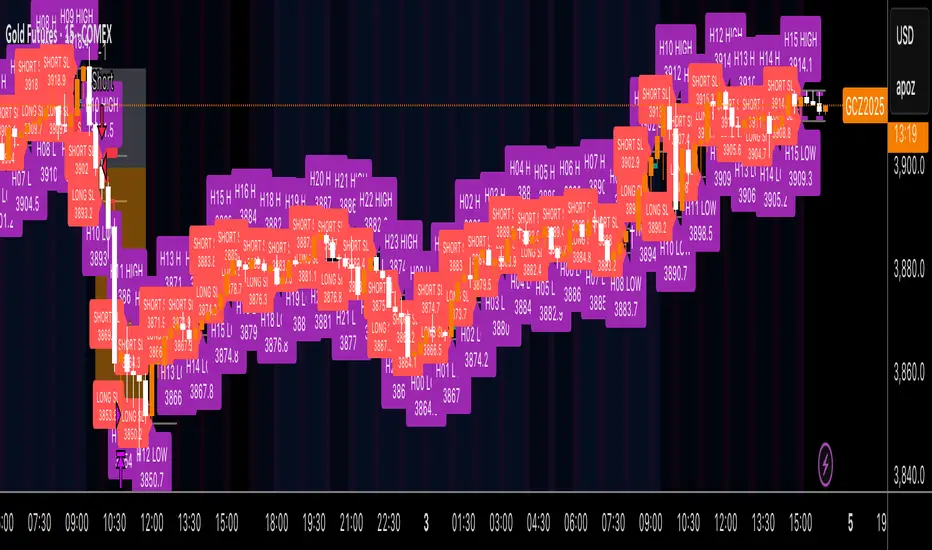

Kz GC1! ORBStrategy that trades breakouts on GC1! futures on the 5min timeframe. It also works on MGC1! for lower drawdown and to manage Apex and Top Step accounts with the lower risk.

Risk Disclaimer:

Past results as well as strategy tester reports do not indicate future performance. Guarantees do not exist in trading. By using this strategy you risk losing all your money.

Important:

It trades all days that markets are open. Set times may be seen on settings. Trades multiple times a day sometimes.

It works on the 5 and 15min timeframe only. Results are better on 5min timeframe.

The settings are optimized already for GC1! on the 5min timeframe.

How it works:

Every trading day it measures the range of the first 15min candle of pre-selected hours. As soon as price closes above or below on the 15min timeframe, it will trade the breakout targeting a set risk to reward ratio. SL on the opposite side of the range.

Settings:

Hourly Trading Hours: These are the times that worked best for this strategy. All boxes should be checked for best results. Excluded times were when it performed bad which is why those times have been left out.

ORB Formation Period: This setting determines on which timeframe candle has to close outside the opening range box in order to take a trade. It's set to 15min by default because this is what worked by far the best

Entry Type: Entries are immediate instead of waiting for a pull back to enter on a limit order.

Limit Orders: If enabled, the strategy will place a pending order x points from the current price, instead of a market order. Immediate orders are enabled by default for a better performance. Important: It doesn't actually place a limit order. The strategy will just wait for a pullback and then enter with a market order. It's more like a hidden limit order.

Limit Order Offset Points: If you have limit orders enabled, this setting determines how many points from the current price the limit order will be placed.

FVG Detection Type: How fast it detects the fair value gaps. Standard detection over immediate had better performance

Risk Type: You can chose either between Fixed USD Amount, Risk per Trade in % or Fixed Contract Size. By default it's set to fixed contract size.

Risk Amount (USD or Contracts): This setting is to set how many USD or how many contracts you want to risk per trade. Make sure to check which risk type you have selected before you choose the risk amount.

Take Profit Multiplier: This is simply the total SL size in points multiplied by x.

Example: If you put 2, you get a 2:1 Risk to Reward Ratio. By Default it's set to 2.5 because this gave the best results in backtests.

Stop Loss Padding: This is simply the buffer in points that is added to the SL for safety reasons. If you have it on 0, the SL will be at the exact price of the opposite side of the range. By default it's set to 5 because this is what delivered the best results in backtests.

Stop Loss Placement: This determines where the stop loss gets placed for the order. It has been set to ORB Range by default as this delivered the best results.

Max Trades Per Hour: This allows the user to decide how many trades are taken an hour. 1 is been set to default for best results

Visual Settings: Check boxes to show orb range, FVG's, Entry points, and trade visualization boxes.

Backtest Settings:

For the backtest the commissions were set to 1.29USD per contract and .35USD for micros which is the highest amount Tradovate charges Margin was not accounted for because typically on prop accounts you can use way more contracts than you need for the extremely low max drawdown. Margin would be important on personal accounts but even there typically it's not an issue at all especially because this strategy runs on the 15min timeframe so it won't use a lot of contracts anyways.

Why the source code is hidden:

The source code is hidden because I invested a lot of time and money into developing this strategy and optimizing it with paid 3rd party software.

TPFX - Unified Strategy v8.1 (COT + Valuation + S/D + Seasonal)

TPFX - Unified Strategy v8.1: A 5-in-1 Confluence Model

The TPFX Unified Strategy is a comprehensive trading model that integrates five distinct market analysis modules into a single indicator. Its primary function is to generate high-confluence entry and exit signals by requiring validation across multiple layers of market analysis. This approach aims to minimize noise and focus trading activity on moments of strong directional agreement.

Core Analytical Modules:

1. COT Index (Commitment of Traders): Quantifies the relative extreme positioning of major market participants (Commercials, Large Speculators) over a user-defined lookback period to identify overextended sentiment.

2. COT Momentum: Utilizes Commercial net positioning to detect momentum shifts, based on either a new high/low logic or a Moving Average crossover.

3. Valuation Trigger: Compares the relative performance of the current symbol against a reference asset (e.g., DXY) to determine periods of comparative overvaluation or undervaluation.

4. Supply and Demand (S/D) Zones: Automatically identifies and plots institutional S/D zones based on specific candle patterns. These zones provide precise entry, stop-loss, and dynamic take-profit targets upon activation and retest.

5. Seasonal Filter: Applies a calendar-based constraint to limit trade entry to historically favorable or unfavorable periods for the specific asset.

Key Strategy Features:

* Modular Control: All five modules can be independently enabled or disabled via input settings, allowing the user to customize the required confluence level for signal generation.

* Flexible Exit Management: The strategy supports four primary exit methodologies:

* Fixed TP/SL: Standard point or percentage-based risk management.

* Dynamic (S/D Zones): Uses the S/D zone boundaries for stop-loss and either a fixed R:R ratio or the nearest opposite zone for take-profit.

* Opposite Signal: Closes a position when a full, confirmed signal in the opposite direction is generated.

* Mean Reversion: Closes the position when the COT Index or Valuation Line reverts to a defined mean level.

* Risk Parameters: Includes configurable order size, trade direction filtering (Long, Short, Both), and adjustable parameters for S/D zone detection logic.

v8.1 Update: This version features a syntax correction within the Supply/Demand Zones calculation block to ensure reliable zone detection and trigger logic.

This tool is designed for systematic traders seeking to align their decisions with fundamental flows and order book imbalances.

(Note: Full functionality relies on access to the Commitment of Traders data feed, which may require a subscription.)

高频策略优化版-空头Open Condition Reversal: Change the condition of the TEMA fast line above the slow line to the condition of the fast line below the slow line RSI condition from " buy above the threshold " to " short below the threshold ", and adjust the default threshold from 30 to 70 (more suitable for shorting overbought area) moving average direction judgment from up to down stop-loss direction adjustment: Short stop-loss Settings above the entry price (entry price * (1 + i _ sl) ) Short stop-loss set below the entry price (entry price * (1-tp) Tracking stop-loss level adjusted to below the entry price MACD logic adjustment: Preferred use of the bearish pattern as a short signal bullish pattern for closing risk management: Maintained a dynamic stop-loss mechanism, adjusted to protect the market from the bottom of the visual stop-loss strategy: The visual marking of the ACD energy column is convenient for monitoring signals to be fully tested before use, especially for adjusting RSI thresholds and stop-loss parameters to suit the characteristics of specific trading varieties.

AstraAlgo BacktesterOVERVIEW

The AstraAlgo Backtester allows traders to simulate and evaluate trading strategies directly on TradingView. By simulating trades across different timeframes and markets, it provides valuable insights into win rates, drawdowns, and overall strategy effectiveness.

SIGNAL MODES

Signal Modes generate proprietary trade signals based on live price data. Users can choose between Off, Basic, Advanced, or Custom modes to evaluate strategies under different conditions and refine their trading approach.

ADJUSTABLE BACKTESTING

Parameters for historical simulations can be customized to test different market conditions and trading scenarios. This allows traders to measure strategy performance, including win rate, profit/loss, and risk/reward ratios, helping refine and optimize strategies before live execution.

BAR COLORING

Bar Coloring highlights bullish and bearish bars on historical charts, allowing traders to visually assess trend direction and trade outcomes during backtesting. This makes it easier to analyze momentum and strategy effectiveness at a glance.

ASTRA CLOUD

Astra Cloud overlays dynamic support and resistance levels on live price data. These zones adapt automatically to past market movements, helping traders identify areas where trades would have reacted, aiding strategy evaluation and optimization.