Buy/Sell StratThis strategy will produce a buy or sell signal when the following criteria are met:

9 EMA crosses 21 EMA

Recently closed candlestick has 15% higher average volume than previous 5 candles

A candlestick reversal pattern

Price crosses 9 EMA

Feel free to use and modify as you see fit. Happy trading!

ابحث في النصوص البرمجية عن "Candlestick"

ONWAY Indicator PV6The ONWAY indicator is a comprehensive and earnestly designed tool aimed to increase confidence in a traders market bias. ONWAY analyzes market trends, market strength, and price action near key pivot levels to form a bias on future price action. Of course, it is fundamentally impossible to predict the future, but we all try it now don't we. Gain an edge in the markets and add ONWAY to your tool box.

ONWAY Functionality

Confirmation Signals: ONWAY provides real-time, non-repaint BUY and SELL signals upon the active timeframes candle close.

Targets and Stops: ONWAY will, upon signal confirmation, set a target and stop loss.

Position Management: ONWAY will monitor its current position, if one exists, and attempt to tighten the stop loss if possible.

ONWAY Details

Symbols and Timeframes: ONWAY is restricted to approved symbols and timeframes indicated by the 🟢 icon next to "Optimized:" and "ONWAY Timeframe:" on the dashboard. If an unapproved combination of symbol and timeframe is in use, ONWAY will be disabled (no signals will be visible). See author's instructions for the current ONWAY watchlist or to submit a symbol/timeframe request.

Position Details: Apart from the on chart signals and position plot, the ONWAY dashboard will indicate the current position, entry price, target price, and stop price.

Stop Loss: ONWAY has a unique stop loss/exit strategy that has proved, based on our calculations, to be advantageous. If price reaches or exceeds the stop loss, ONWAY will not close the position unless there is a candle close on the active timeframe exceeding the stop level. This is known as a soft stop loss and identified on the dashboard as "(Soft)" next to the stop price. Additionally, the stop loss will change throughout the position, following the low, for a long position or high, for a short position, within a given period, but the soft stop loss will not exceed beyond a 1:1 risk to reward ratio (the risk will always be equal to or less than the potential reward). It is importance to be aware that the soft stop is utilized at this 1:1 threshold as well. On the plus side, the changing stop loss will impose a risk free position if it finds itself between the entry price and target price. At this stage the soft stop is no longer utilized, the stop loss can only approach the target price, and profit is uhhh.....certain (I don't think the mods will like that word 😉). If the soft stop is no longer in use, the dashboard will indicate this with "(Hard)" next to the stop price.

Position Sizing: The position sizing used for the backtested results is displayed on the dashboard next to "Strategy Lot Size:". This position size is provided solely as a reference for the backtest results. The choice of a position size is left to the users discretion.

Backtest Results: With any strategy, backtesting is an excellent way to judge performance and viability, but it is important to recognize that past performance does not confirm repeatability in future market conditions.

Updates: ONWAY updates its acceptable symbols frequently to account for everchanging market conditions. This includes adding new symbols, rejecting previously compatible symbols, and modifying the optimal window for current symbols.

Acceptability Criteria: The criteria for a symbol to be deemed acceptable requires that its backtested results deliver a win rate greater than 70%, profit factor greater than 1.2, and its equity chart appear favorable. These metrics are available to users by clicking on "Strategy Tester" located on the bottom panel of the chart view.

Accessibility: To gain access to ONWAY, see the author's instructions below.

Use of this script implies that you acknowledge that past performance does not necessarily indicate future results and that guarantees are not possible in this trading realm.

Reversal with Bollinger Bands + RSI + ADX + ATR (Upgraded)Hi,

Welcome to my 4th script.

Someone asked me some questions about the Bollinger Band strategy I previously published. When I went back to my published script I couldn't help myself but simply try and make it better. Which I did.

Since I've published that script, I've gained much more knowledge about how Pinescript functions. As well as gaining more and more knowledge about how the markets are structered etc.

In this reversal script we use 4 indicators to determine good entry signals, we determine whether the market is ranging or trending and we still only want to take trades in the direction of the "trend".

Bollinger Bands are used for our entry signal. When price hits either side of the band, we wait for a reverse candlestick before we enter a position.

RSI is used to determine if we're in a trending market or in a ranging market. You can adjust the values in the inputs. You can determine the minimum RSI value and the maximum RSI value.

ADX is used the same way as RSI, you can adjust the value in the inputs. You can determine the minimum ADX value.

Last but not least we use two EMA's, a 200 EMA and 100 EMA. Both are adjustable through the inputs. I used two EMA's because I noticed when using this strategy that we'd enter a new position often after having a bad trade. Using two EMA's might clean up some signals, in my case with EUR/USD on a 15m timeframe, it didn't clean up enough signals.

All the default values are pretty decent but might require some finetuning on a certain instrument. Don't overfit the strategy though, that'll only give you bad signals in the future.

Then we are off to our exit signals.

Initially I wanted to incorporate my previous Bollinger Band exit signals as well, but it was too much of a hassle to make the script work as intended so I left it out. If you want to use those exit signals, just find my other script.

When we're in a position and price crosses the opposite band, we wait for a reverse candlestick before we exit the position.

Additionally we want our losses to be as small as possible, so we use RSI to signal us when the market is, or starts to, trend against us. This is where you use the minimum and maximum exit values. So when RSI crosses over or under that value, it'll exit the position.

Furthermore, we use the ATR indicator to set our stop loss, which is pretty basic stuff. You can adjust the ATR multiplier in the inputs. Disabling "Use Trailing Stop?" is really inadvisable unless you know this script inside out as your only exit signals will be opposite Bollinger Band Cross and RSI overbought / oversold areas.

[BTCUSD] DinhChienFX [2 orders]* Historical statistics from 2018:

* Strategy will enter 2 orders, Order 2 will appear only when there is Order 1:

- Percent profitable of 1st order: 64.76%.

- Percent profitable of 2nd order: 49.86%.

- Average percent profitable: 57.31%.

- 14 consecutive wins.

- 4 consecutive losses.

Order 1: risk / reward ratio 1/1 used to determine if this rule is effective or not?

Order 2: Appears when there is order 1, Use take-profit and take-loss level of order 1 at Fibonacci 75%.

. * 1st Order conditions:

- Buy: When the ADX index cuts up to 45, check earlier if the closing price has cut up and is above the Upper 2 line, enter the Buy order.

- Sell: when the ADX indicator cuts up to 45, check before that if the closing price has cut down and is above Lower 2 then enter a Sell order.

* How to enter Order 2: When order 1 appears, there are always Stoploss and Takeprofit levels. Draw Fibonacci from take-profit and take-loss prices, Fibonacci retracement level = 75%

----------------

1. Trend identification:

- Channel Keltner:

... Uptrend: when the closing candlestick cuts up and is above the Keltner channel, the Upper Line 2

... Down trend: when the candle closes and falls above the Keltner Line Lower 2

2. Rules of entry:

- Channel Keltner:

... Buy: Candlestick closing price cuts up and above the Keltner Upper 2.

... Sell: The closing price of the candle cuts down and is lower than the Keltner Below 2.

ADX indicator:

... Buy: The ADX value crossed to 45 and the close of the candle was higher than Keltner Upper 2.

... Sell: ADX value cuts to 45 and the close of the candle is lower than Keltner Below 2.

3. Stoploss and Profit = atr (20) * 2.

Heikin-Ashi MACD"Heikin-Ashi, also sometimes spelled Heiken-Ashi, means "average bar" in Japanese. The Heikin-Ashi technique can be used in conjunction with candlestick charts when trading securities to spot market trends and predict future prices. It's useful for making candlestick charts more readable and trends easier to analyze. For example, traders can use Heikin-Ashi charts to know when to stay in trades while a trend persists but get out when the trend pauses or reverses. Most profits are generated when markets are trending, so predicting trends correctly is necessary."

HA bars help us to smooth the price action, and I think MACD gives me a lot of signals and I need to eliminate them and add MACD strategy on Heiken-Ashi candles to look performance.

Mostly, it eliminates %75 of the signals, and most of the time it did increase backtest performance significantly.

There is still a way to it to combine other indicators for complete strategy, but at least We can achieve better MACD with this approach.

Simple Heiken Ashi Stop and Reverse Trading on FuturesThis is the initial version of the Heikein Ashi Strategy.

It calculates the Heiken Ashi values for the candlestick charts displayed on the screen and generates alerts/trades based on the actual value in the candlestick chart.

MOM+RSI StrategyThis is a momentum based strategy which generates signals when the price moves with momentum in either direction. This strategy works well on liquid stocks. Its not necessary to close the trade as soon as the close signal is generated and one can wait for the price to move in the direction as indicated by the prior signal unless price starts to go in the opposite direction. The best set up for a trader is his/her own set up and hence it is recommended to use this strategy with your set up/research.

[New series!] [Consistent Losing Strategies] 34 EMA Scalping//---------------------------INTRO------------------------------

Hi All!

Let me introduce myself as a semi-successful forex trader & lover of automation.

I've taken to algo trading and have been hunting down strategies (that usually use indicators) to automate, backtest, and hopefully implement in MT4.

Unfortunately, most strategies are complete bulls*** and the select cases that are shown to "prove" success are limited.

These strategy sources often do not provide useful analytics either.

I want to change that approach to trading! We can really benefit each other and the community by being methodical about backtesting

as well as evaluating our results with some kind of scoring heuristic.

As for what that standardized process looks like..well I'm still working on it.

I'm pretty much on Tv for multiple hours of the day, screening strategies via Pinescript and I'd like to start sharing my progress!

This is a new series I'd like to start on consistently losing strategies. I'll make all the code public, so if you think I've made a blunder

or approached a problem the wrong way, then drop me a DM or paste your fix into the comments.

//---------------------------STRAT------------------------------

34 EMA Scalping strategy (ref. forextradingstrategies4u )

How you're supposed to trade it:

BUY:

1. Market is in an down trend as shown by the 34 EMA

2. Price breaks above a downwards trend line

3. Price breaks above the 34 EMA

4. Look for a very bullish candlestick or chart pattern

SELL:

1. Look for the 34 EMA to show we are in an uptrend

2. Price breaks below an upwards sloping trend line

3. Price breaks below 34 EMA

4. Look for a bearish candlestick or a chart pattern

//---------------------------CONC------------------------------

Q: Why does it fail?

A: I believe this strategy relies too much on subjective input (aka, trendlines).

Q: Why does it fail as an algo?

A: The 34 EMA is no more predictive than any other EMA, although it does a good job at filtering out noise.

Q: Should I try it out?

A: No, it's trash. This is the proof that it is trash.

[Autoview][BackTest]Dual MA Ribbons R0.12 by JustUncleLThis is an implementation of a strategy based on two MA Ribbons, a Fast Ribbon and a Slow Ribbon. This strategy can be used on Normal candlestick charts or Renko charts (if you are familiar with them).

The strategy revolves around a pair of scripts: One to generate alerts signals for Autoview and one for Backtesting, to tune your settings.

The risk management options are performed within the script to set SL(StopLoss), TP(TargetProfit), TSL(Trailing Stop Loss) and TTP (Trailing Target Profit). The only requirement for Autoview is to Buy and Sell as directed by this script, no complicated syntax is required.

The Dual Ribbons are designed to capture the inferred behavior of traders and investors by using two groups of averages:

> Traders MA Ribbon: Lower MA and Upper MA (Aqua=Uptrend, Blue=downtrend, Gray=Neutral), with center line Avg MA (Orange dotted line).

> Investors MAs Ribbon: Lower MA and Upper MA (Green=Uptrend, Red=downtrend, Gray=Neutral), with center line Avg MA (Fuchsia dotted line).

> Anchor time frame (0=current). This is the time frame that the MAs are calculated for. This way 60m MA Ribbons can be viewed on a 15 min chart to establish tighter Stop Loss conditions.

Trade Management options:

Option to specify Backtest start and end time.

Trailing Stop, with Activate Level (as % of price) and Trailing Stop (as % of price)

Target Profit Level, (as % of price)

Stop Loss Level, (as % of price)

BUY green triangles and SELL dark red triangles

Trade Order closed colour coded Label:

>> Dark Red = Stop Loss Hit

>> Green = Target Profit Hit

>> Purple = Trailing Stop Hit

>> Orange = Opposite (Sell) Order Close

Trade Management Indication:

Trailing Stop Activate Price = Blue dotted line

Trailing Stop Price = Fuschia solid stepping line

Target Profit Price = Lime '+' line

Stop Loss Price = Red '+' line

Dealing With Renko Charts:

If you choose to use Renko charts, make sure you have enabled the "IS This a RENKO Chart" option, (I have not so far found a way to Detect the type of chart that is running).

If you want non-repainting Renko charts you MUST use TRADITIONAL Renko Bricks. This type of brick is fixed and will not change size.

Also use Renko bricks with WICKS DISABLED. Wicks are not part of Renko, the whole idea of using Renko bricks is not to see the wick noise.

Set you chart Time Frame to the lowest possible one that will build enough bricks to give a reasonable history, start at 1min TimeFrame. Renko bricks are not dependent on time, they represent a movement in price. But the chart candlestick data is used to create the bricks, so lower TF gives more accurate Brick creation.

You want to size your bricks to 2/1000 of the pair price, so for ETHBTC the price is say 0.0805 then your Renko Brick size should be about 2*0.0805/1000 = 0.0002 (round up).

You may find there is some slippage in value, but this can be accounted for in the Backtest by setting your commission a bit higher, for Binance for example I use 0.2%

Special thanks goes to @CryptoRox for providing the initial Risk management Framework in his "How to automate this strategy for free using a chrome extension" example.

Trend Flow & Volatility Guard Strategy [ROSTOK V5]Description:

This strategy is a comprehensive trend-following system designed to identify high-probability entries by aligning long-term market direction with short-term momentum, while strictly filtering out low-quality "choppy" market conditions.

How it Works:

The strategy operates on a multi-stage logic system:

Trend Identification: The core direction is determined by a customizable Main Trend Line (selectable between a long-period EMA or Supertrend). Trades are only taken in the direction of the dominant trend.

Signal Generation: Entries are triggered when a fast-moving Signal Line crosses the Main Trend Line, confirmed by specific candlestick price action (Close > Open).

Advanced Filtering (Confluence): To avoid false signals, the strategy employs a robust set of filters. A trade is only valid if:

Momentum: RSI is within safe operating zones (avoiding extreme overbought/oversold unless a strong trend override is active).

Cycle: CCI and MACD histograms align with the trade direction.

Volatility: The ADX is analyzed to ensure sufficient trend strength, while a Choppiness Index filter blocks trades during sideways/ranging markets.

Risk Management & Recovery: The strategy features built-in money management tools, including:

ADR (Average Daily Range) Filter: Prevents entering trades when the asset has already moved its expected daily distance.

Daily Limits: Hard stops for Max Daily Loss and Target Daily Profit to preserve capital.

Recovery Logic: An optional mechanism to manage drawdowns on difficult days using calculated recovery targets.

Settings & Customization: Users can toggle individual filters (Volume, Choppiness, ADX) and adjust the sensitivity of the trend lines to fit different assets and timeframes (e.g., EURAUD 15m).

Disclaimer: Past performance is not indicative of future results. This script is for educational purposes and backtesting analysis.

TH E9M Larry Williams EMA9 Strategy with Trend Filter"Larry's Improved Trading Strategy Using EMA9

"When a trend is in place and the EMA9 starts to slope against it, enter at the EMA9 level when the candlestick breaks out in the direction of the trend."

CDC Action Zone V.2 strategy — Updated v6Making a profit with a candlestick structure compared to the MA course 25 line with nine intersecting to find. Buy in the market.

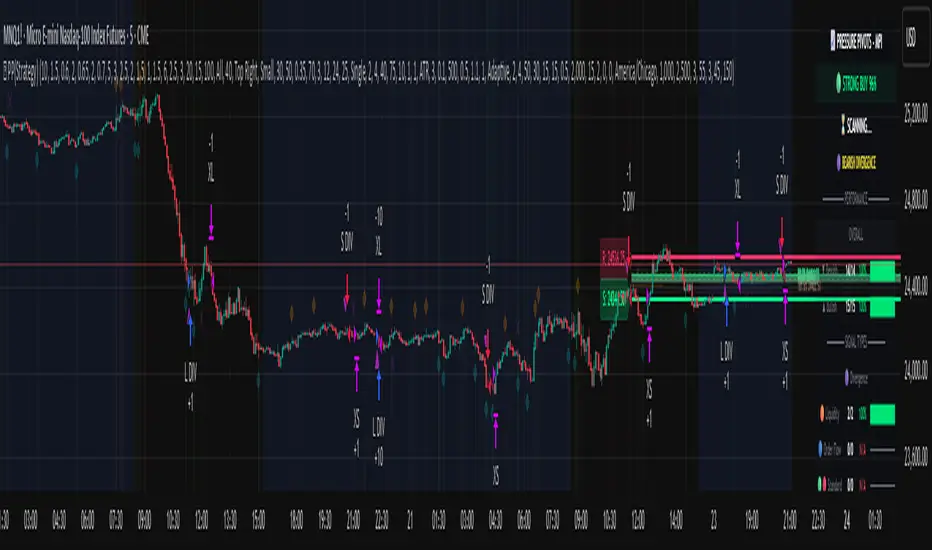

Pressure Pivots - MPI (Strategy)⇋ PRESSURE PIVOTS — MARKET PRESSURE INDEX STRATEGY

A comprehensive reversal trading system that combines order flow pressure analysis, multi-factor confluence detection, and adaptive machine learning to identify high-probability turning points in liquid markets.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

CORE INNOVATION: MARKET PRESSURE INDEX (MPI)

Traditional indicators measure price movement. The Market Pressure Index measures the force behind the movement.

How MPI Works:

Every bar tells two stories through volume distribution:

• Buy Pressure: Volume × (Close - Low) / (High - Low)

• Sell Pressure: Volume × (High - Close) / (High - Low)

• Net Pressure: Buy Pressure - Sell Pressure

This raw pressure is then normalized against baseline activity to create the bounded MPI (-1.0 to +1.0):

• Smooth Pressure: EMA(Net Pressure, period)

• Baseline Activity: SMA(|Net Pressure|, period × 2)

• MPI: (Smooth Pressure / Baseline) × Sensitivity

What MPI Reveals:

MPI > +0.7: Extreme buy pressure → Exhaustion potential

MPI = +0.2 to +0.7: Healthy bullish momentum

MPI = -0.2 to +0.2: Neutral/balanced pressure

MPI = -0.7 to -0.2: Healthy bearish momentum

MPI < -0.7: Extreme sell pressure → Exhaustion potential

Why It Works:

Two bars can both move 10 points, but if one closes at the high on high volume (aggressive buying) and the other closes mid-range on average volume (weak buying), only MPI distinguishes between sustainable momentum and exhaustion. This volume-weighted pressure analysis reveals conviction behind price moves—the key to timing reversals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SEVEN-FACTOR CONFLUENCE SYSTEM

MPI extremes alone aren't enough. The system requires multiple independent confirmations through weighted scoring:

1. DIVERGENCE (Weight: 3.0) — Premium Signal Type: DIV

Price makes new high but MPI makes lower high (or inverse for bullish)

• Detection: Tracks pivots with 5-bar lookback, compares price vs MPI at pivot points

• Signal: Purple triangles, highest weight (pressure weakening while price extends)

2. LIQUIDITY SWEEP (Weight: 2.5) — Premium Signal Type: LIQ

Price breaks swing high/low within 0.3 ATR then reverses

• Detection: Break within tolerance + close back through level

• Signal: Orange triangles, second-highest weight (stop hunt reversal)

3. ORDER FLOW IMBALANCE (Weight: 2.0) — Premium Signal Type: OF

Aggressive buying/selling 50% above normal

• Detection: EMA(aggressive volume) vs SMA(imbalance) threshold

• Signal: Aqua triangles, institutional positioning

4. VELOCITY EXHAUSTION (Weight: 1.5)

Parabolic move (2+ ATRs in 3 bars) + extreme MPI

• Detection: |3-bar price change / ATR| > threshold + MPI > ±0.5

• Indicates: Momentum deceleration, blow-off top/bottom

5. WICK REJECTION (Weight: 1.5)

Single bar: wick > 60% of range, or sequence: 2 bars with 40% + 30% wicks

• Detection: Shooting stars (bearish) or hammers (bullish)

• Indicates: Intrabar rejection, battle won by opposing side

6. VOLUME SPIKE (Weight: 1.0)

Volume > 20-bar average × multiplier (default: 2.0x)

• Detection: Participation surge confirmation

• Lowest weight: Can be manipulated, better as confirmation

7. POSITION FACTOR (Weight: 1.0)

At 10-bar highest (bearish) or lowest (bullish)

• Detection: Structural positioning for reversal

• Base requirement: Must be at extreme to score

Scoring Logic:

Premium Signals (DIV/LIQ/OF): Must score ≥6.0 (default premiumThreshold)

Standard Signals (STD): Must score ≥4.0 (default standardThreshold)

Example Scoring:

Divergence (3.0) + Liquidity Sweep (2.5) + Volume (1.0) = 6.5 → FIRES (DIV signal)

Recent High (1.0) + Wick (1.5) + Volume (1.0) + Velocity (1.5) = 5.0 → FIRES (STD signal)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ADAPTIVE LEARNING ENGINE

Unlike static strategies, this system learns from every trade and optimizes itself.

Performance Tracking:

Every trade records:

• Entry Score: Confluence level at entry

• Signal Type: DIV / LIQ / OF / STD

• Win/Loss: Boolean outcome

• R-Multiple: (Exit - Entry) / (Entry - Stop)

• MAE: Maximum Adverse Excursion (worst drawdown)

• MFE: Maximum Favorable Excursion (best profit reached)

Three Adaptive Parameters:

1. Signal Threshold Adaptation

If Win Rate < Target (45%): RAISE threshold → fewer signals, better quality

If Win Rate > Target + 10% AND good R: LOWER threshold → more signals, profitable

2. Stop Distance Adaptation

If Avg MAE > 0.85 AND WR < 50%: WIDEN stops → reduce premature exits

If Avg MAE < 0.4 AND WR > 55%: TIGHTEN stops → reduce risk

3. Target Distance Adaptation

If Avg MFE > Target × 1.5: EXTEND targets → capture more of runners

If Avg MFE < Target × 0.7: SHORTEN targets → take profits faster

Signal Type Filtering:

The system tracks performance by type (DIV/LIQ/OF/STD):

• If Type WR < 40% AND Avg R < 0.8: Type DISABLED

• If Type WR ≥ 40% OR Avg R ≥ 0.8: Type RE-ENABLED

Example: If OF signals consistently lose while DIV signals win, system automatically stops taking OF signals and focuses on DIV.

Warmup Period:

First 30 trades (default) gather baseline data with relaxed thresholds. After warmup, full adaptation activates.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPLETE POSITION MANAGEMENT

Dynamic Position Sizing:

Base Contracts = (Equity × Risk%) / (Stop Distance × Point Value)

Then multiplied by:

• Score Bonus: Up to +50% for highest-scoring signals

• Signal Type Bonus: DIV signals +50%, LIQ signals +30%

• Streak Multiplier: After 3 losses: 50% reduction, After 3 wins: 25% increase

Example: High-scoring DIV signal on winning streak = 3-4× larger position than weak STD signal on losing streak

Entry Modes:

Single Entry: Full size at once, exit at TP2 (or partial at TP1)

Tiered Entry: 40% at TP1 (2R), 60% at TP2 (4R adaptive)

Stop Management (3 Modes):

Structural: Beyond recent 20-bar swing high/low + buffer

ATR: Fixed ATR multiplier (default: 2.0 ATR, then adapts)

Hybrid: Attempt structural, fallback to ATR if invalid

Plus:

• Breakeven: Move stop to entry ± 1 tick when 1R reached

• Trailing: Activate when 1.5R reached, trail 0.8R behind price

• Max Loss Override: Cap dollar risk regardless of calculation

Target Management:

Fixed Mode: TP1 = 2R, TP2 = 4R

Adaptive Mode: TP1 = 2R fixed, TP2 adapts based on MFE analysis

Partial Exits: Default 50% at TP1, remainder at TP2 or trailing stop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPREHENSIVE RISK CONTROLS

Daily Limits:

• Max Daily Loss: $2,000 default → HALT trading

• Max Daily Trades: 15 default → prevent overtrading

• Max Concurrent: 2 positions → limit correlation risk

Session Controls:

• Trading Hours: Specify start/end times + timezone

• Weekend Block: Optional (avoid crypto weekend volatility)

Prop Firm Protection (Live Trading Only):

• Daily Loss Limit: Stricter of general or prop limit ($1,000 default)

• Trailing Drawdown: Tracks high water mark, HALTS if breach ($2,500 default)

• Reset on Reload: Optional high water mark reset

Liquidity Filter (Optional):

• Time-Based: Avoid first/last X minutes of session

• Volume-Based: Require minimum volume ratio (0.5× average default)

Market Regime Filter (Optional):

• ADX-Based: Only trade when ADX > threshold (trending)

• Block: Consolidation (ADX < 20) or Transitional regimes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

REAL-TIME DASHBOARD

MPI Gauge Section:

Shows current pressure: 🟢 STRONG BUY (+0.5 to +1.0), 🟩 BUY PRESSURE (+0.2 to +0.5), ⚪ NEUTRAL (-0.2 to +0.2), 🟥 SELL PRESSURE (-0.5 to -0.2), 🔴 STRONG SELL (-1.0 to -0.5)

Signal Status Section:

• Active Signals: "🔴 DIV SELL" (purple background), "🟢 LIQ BUY" (orange), "🔵 OF SELL" (aqua), "🟢 STD BUY" (green)

• Warnings: "⚠️ BEAR WARNING" / "⚠️ BULL WARNING" (yellow) — setup forming, not full signal

• Scanning: "⏳ SCANNING..." (gray) — no signal active

• Confidence Bar: Visual score display "██████░░░░" showing confluence strength

Divergence Indicator:

"🟣 BEARISH DIVERGENCE" or "🟡 BULLISH DIVERGENCE" when detected

Performance Statistics:

• Overall Win Rate: Wins/Total with visual bar (lime ≥70%, yellow 50-70%, red <50%)

• Directional: Bearish vs Bullish win rates separately

• By Signal Type: DIV / LIQ / OF / STD individual performance tracking

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY PARAMETERS EXPLAINED

🎯 Pressure Engine:

• MPI Period (5-50, default: 14): Smoothing period — lower for scalping, higher for position trading

• MPI Sensitivity (0.5-5.0, default: 1.5): Amplification — lower compresses range, higher more extremes

🔍 Detection:

• Wick Threshold (0.3-0.9, default: 0.6): Minimum wick-to-range ratio for rejection

• Volume Spike (1.2-3.0x, default: 2.0): Multiplier above average for spike

• Aggressive Ratio (0.5-0.9, default: 0.65): Close position in range for aggressive orders

• Velocity Threshold (1.0-5.0 ATR, default: 2.0): ATR-normalized move for exhaustion

• MPI Extreme (0.5-0.95, default: 0.7): Level considered overbought/oversold

⚖️ Weights:

• Divergence: 3.0 (highest — pressure weakening)

• Liquidity: 2.5 (second — stop hunts)

• Order Flow: 2.0 (institutional positioning)

• Velocity: 1.5 (momentum exhaustion)

• Wick: 1.5 (rejection patterns)

• Volume: 1.0 (lowest — can be manipulated)

🎚️ Thresholds:

• Premium (4.0-15.0, default: 6.0): Score for DIV/LIQ/OF signals

• Standard (2.0-8.0, default: 4.0): Score for STD signals

• Warning Confluence (1-4, default: 2): Factors for yellow diamond warnings

🧬 Adaptive:

• Enable (true/false, default: true): Master learning switch

• Warmup Trades (5-100, default: 30): Data collection before adaptation

• Lookback (20-200, default: 50): Recent trades for performance calculation

• Adapt Speed (0.05-0.50, default: 0.15): Parameter adjustment rate

• Target Win Rate (30-70%, default: 45%): Optimization goal

• Target R-Multiple (0.5-5.0, default: 1.5): Risk/reward goal

💼 Position:

• Base Risk (0.1-10.0%, default: 1.5%): Equity risked per trade

• Max Contracts (1-100, default: 10): Hard position limit

• DIV Bonus (1.0-3.0x, default: 1.5): Size multiplier for divergence signals

• LIQ Bonus (1.0-3.0x, default: 1.3): Size multiplier for liquidity signals

🛡️ Stops:

• Mode (Structural/ATR/Hybrid, default: ATR): Stop placement method

• ATR Multiplier (0.5-5.0, default: 2.0): Stop distance in ATRs (adapts)

• Breakeven at (0.3-3.0R, default: 1.0R): When to move stop to entry

• Trail Trigger (0.5-5.0R, default: 1.5R): When to activate trailing

• Trail Offset (0.3-3.0R, default: 0.8R): Distance behind price

🎯 Targets:

• Mode (Fixed/Adaptive, default: Fixed): Target placement method

• TP1 (0.5-10.0R, default: 2.0R): First target for partial exit

• TP2 (1.0-15.0R, default: 4.0R): Final target (adapts in adaptive mode)

• Partial % (0-100%, default: 50%): Position percentage to exit at TP1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PROFESSIONAL USAGE PROTOCOL

Phase 1: Paper Trading (Weeks 1-4)

• Setup: Default settings, all adaptive features ON, 0.5% base risk

• Goal: 30+ trades for warmup, observe MPI behavior and signal frequency

• Adjust: MPI sensitivity if stuck near neutral or always at extremes

• Threshold: Raise/lower if too many/few signals

Phase 2: Micro Live (Weeks 5-8)

• Requirements: WR >43%, at least one type >55%, Avg R >0.8

• Setup: 10-25% intended size, 0.5-1.0% risk, 1 position max

• Focus: Execution quality, match dashboard performance

• Journal: Screenshot every signal, track outcomes

Phase 3: Full Scale (Month 3+)

• Requirements: WR >45% over 50+ trades, Avg R >1.2, drawdown <15%

• Progression: Months 3-4 (1.0-1.5% risk), 5-6 (1.5-2.0%), 7+ (1.5-2.5%)

• Maintenance: Weekly dashboard review, monthly deep analysis

• Warnings: Reduce size if WR drops >10%, consecutive losses >7, or drawdown >20%

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DEVELOPMENT INSIGHTS

The Pressure Insight: Emerged from analyzing intrabar volume distribution. Within every candlestick, volume accumulates at different price levels. MPI deconstructs this to reveal conviction behind moves.

The Confluence Challenge: Early versions using MPI extremes alone achieved only 42% win rate. The seven-factor confluence system emerged from testing which combinations produced reliable reversals. Divergence + liquidity sweep became the strongest setup (68% win rate in isolation).

The Adaptive Breakthrough: Per-signal-type performance tracking revealed DIV signals winning at 71% while OF signals languished at 38%. Adaptive filtering disabled weak types automatically, recovering win rate from 39% to 54% during the 2022 volatility spike.

The Position Sizing Revelation: Dynamic sizing based on signal quality and recent performance increased Sharpe ratio from 1.2 to 1.9 while decreasing max drawdown from 18% to 12% over 500 trades. Bigger positions on better signals = geometric edge amplification.

The Risk Control Lesson: Testing with $50K accounts revealed catastrophic failure modes: daily loss cascades, overtrading commission bleed, weekend gap blowouts. Multi-layer controls (daily limits, concurrent caps, prop firm protection) became essential.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

LIMITATIONS & ASSUMPTIONS

What This Is NOT:

• NOT a Holy Grail: Typical performance 52-58% WR, 1.3-1.8 avg R, probabilistic edge

• NOT Predictive: Identifies high-probability conditions, doesn't forecast prices

• NOT Market-Agnostic: Best on liquid auction-driven markets (futures, forex, major crypto)

• NOT Hands-Off: Requires oversight for news events, gaps, system anomalies

• NOT Immune to Regime Changes: Adaptive engine helps but cannot predict black swans

Critical Assumptions:

1. Volume reflects intent (valid for regulated markets, violated by wash trading)

2. Pressure extremes mean-revert (true in ranging/exhaustion, fails in paradigm shifts)

3. Stop hunts exist (valid in liquid markets, less in thin/random walk periods)

4. Past patterns persist (valid in stable regimes, fails when structure fundamentally changes)

Works Best On: Major futures (ES, NQ, CL), liquid forex pairs (EUR/USD, GBP/USD), large-cap stocks, BTC

Performs Poorly On: Low-volume stocks, illiquid crypto pairs, news-driven headline events

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK DISCLOSURE

Trading futures, forex, and leveraged instruments involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational purposes only and should not be construed as financial advice.

The adaptive engine learns from historical data—there is no guarantee that past relationships will persist. Market conditions change, volatility regimes shift, and black swan events occur. No strategy can eliminate the risk of loss.

Users must validate performance on their specific instruments and timeframes before risking capital. The developer makes no warranties regarding profitability or suitability. Users assume all responsibility for trading decisions and outcomes.

"The market doesn't care about your indicators. It only cares about pressure—who's willing to pay more, who's desperate to sell. Find the exhaustion. Trade the reversal. Let the system learn the rest."

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Paulinho Signals – Cripto 5m/15m com Filtro de LateralidadeThis script is an automated Pine Script v6 strategy designed for short-term cryptocurrency trading, especially on 5-minute and 15-minute timeframes. It combines moving average crossovers, trend strength (ADX), volatility (ATR), and candlestick patterns to generate buy and sell signals with a fixed risk/reward management system.

How to Use:

- Apply to cryptocurrency charts on 5m or 15m timeframes.

- Adjust parameters to fit your preferences (EMA, RSI, ADX, ATR).

- Use for backtesting or as a decision-support tool.

Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Always test on demo accounts before applying to live trading.

ORBSMMAATRVOLREENTRY2Contracts📈 Opening Range Fibonacci Breakout (TradingView Strategy)

Overview:

The Opening Range Fibonacci Breakout strategy is designed to capture high-probability intraday moves by combining the power of the 15-minute opening range, trend confirmation via SMMA, and volume-based momentum filtering.

At the start of each trading session, the script automatically plots the Opening Range Box based on the first 15 minutes of price action — highlighting key intraday support and resistance levels.

How It Works:

Opening Range Setup

The first 15 minutes of the session define the range high and low.

A visual box marks this zone on the chart for easy reference.

Signal Generation

A Smoothed Moving Average (SMMA) with a user-defined period determines overall trend bias.

Candle volume is analyzed to confirm momentum strength.

Long Signal: Price breaks above the opening range high, SMMA trending up, and volume supports the move.

Short Signal: Price breaks below the opening range low, SMMA trending down, and volume supports the move.

Take Profit & Targets

Fibonacci extension levels are automatically plotted from the opening range.

These dynamic levels serve as structured Take Profit (TP) zones for partial or full exits.

Features:

✅ 15-Minute Opening Range Box

✅ Adjustable SMMA period

✅ Volume-based confirmation filter

✅ Automatic Fibonacci profit targets

✅ Visual Long/Short alerts & signals

Ideal For:

Scalpers and intraday traders who rely on early-session momentum, breakout confirmation, and precision exit targets.

Backtested for MNQ/NQ futures trading

BankNifty Etharia Aggresive Buyer / SellerOverview

Professional intraday trading strategy for BankNifty Futures that identifies high-probability setups by combining multiple technical indicators. Works in BOTH directions - LONG and SHORT.

Best Timeframe: 5-Minute Chart

Key Features:

✅ Multi-Confluence Entry System - All indicators must align for signal

✅ Bidirectional Trading - Captures both uptrends and downtrends

✅ Advanced Risk Management - Daily loss limits, consecutive loss protection

✅ Smart Exit System - Partial profit taking + trailing stops

✅ Session-Based Trading - Avoids opening and closing volatility

Entry Logic:

LONG Signals:

Price above Kernel Regression (trend confirmation)

Price above VWAP with positive slope (momentum)

Cumulative Volume Delta bullish (buying pressure)

Volume spike or increasing volume (strength confirmation)

Strong bullish candle with 60%+ body ratio

RSI filter to avoid overbought entries

SHORT Signals:

Price below Kernel Regression (downtrend confirmation)

Price below VWAP with negative slope (bearish momentum)

CVD bearish (selling pressure dominates)

High volume confirmation

Strong bearish candle pattern

RSI filter to avoid oversold entries

Exit Management:

🎯 Target 1: 1.5 R:R (50% position exit)

🎯 Target 2: 2.5 R:R (full exit)

🛡️ Stop Loss Options: ATR-based, Swing-based, or Fixed

🟡 Trailing Stop: Activates after 1.2 R:R, trails at 0.8 R:R

⏰ Time-Based Exit: Closes all positions 5 mins before session end

Risk Controls:

Maximum trades per day (default: 5)

Consecutive loss limit (default: 2)

Daily loss limit: 2.5% of capital

Daily profit target: 5% (stops trading when reached)

Position sizing based on account risk percentage

Recommended Settings:

Asset: BankNifty Futures (NSE:BANKNIFTY1!)

Timeframe: 5-minute

Initial Capital: ₹1,00,000

Risk per trade: 1%

Commission: 0.05%

Slippage: 5 points

Performance Expectations:

Win Rate: 55-65%

Profit Factor: 1.5-2.0

Average Trades/Day: 3-8

Risk:Reward: 1:1.8 average

Customizable Parameters:

Trading direction (Long Only / Short Only / Both)

Indicator lengths and thresholds

Stop loss type and targets

Risk management limits

Trading session hours

Best For:

Intraday traders seeking systematic, rule-based entries with strong confluence, proper risk management, and the ability to profit from both bullish and bearish market conditions.

30分钟事件合约策略(Q群956383880)This strategy is applicable to the Binance ETHUSDT spot 1-minute candlestick chart, and the order size can be adjusted based on the security level. Theoretically, the higher the security level, the smaller the order size and the higher the win rate.

本策略适用于币安ETHUSDT现货1分钟k线图,可以通过安全等级自行调节单量。理论上,安全等级越高,单量越少,胜率越高。

The Best Strategy Template[LuciTech]Hello Traders,

This is a powerful and flexible strategy template designed to help you create, backtest, and deploy your own custom trading strategies. This template is not a ready-to-use strategy but a framework that simplifies the development process by providing a wide range of pre-built features and functionalities.

What It Does

The LuciTech Strategy Template provides a robust foundation for building your own automated trading strategies. It includes a comprehensive set of features that are essential for any serious trading strategy, allowing you to focus on your unique trading logic without having to code everything from scratch.

Key Features

The LuciTech Strategy Template integrates several powerful features to enhance your strategy development:

•

Advanced Risk Management: This includes robust controls for defining your Risk Percentage per Trade, setting a precise Risk-to-Reward Ratio, and implementing an intelligent Breakeven Stop-Loss mechanism that automatically adjusts your stop to the entry price once a specified profit threshold is reached. These elements are crucial for capital preservation and consistent profitability.

•

Flexible Stop-Loss Options: The template offers adaptable stop-loss calculation methods, allowing you to choose between ATR-Based Stop-Loss, which dynamically adjusts to market volatility, and Candle-Based Stop-Loss, which uses structural price points from previous candles. This flexibility ensures the stop-loss strategy aligns with diverse trading styles.

•

Time-Based Filtering: Optimize your strategy's performance by restricting trading activity to specific hours of the day. This feature allows you to avoid unfavorable market conditions or focus on periods of higher liquidity and volatility relevant to your strategy.

•

Customizable Webhook Alerts: Stay informed with advanced notification capabilities. The template supports sending detailed webhook alerts in various JSON formats (Standard, Telegram, Concise Telegram) to external platforms, facilitating real-time monitoring and potential integration with automated trading systems.

•

Comprehensive Visual Customization: Enhance your analytical clarity with extensive visual options. You can customize the colors of entry, stop-loss, and take-profit lines, and effectively visualize market inefficiencies by displaying and customizing Fair Value Gap (FVG) boxes directly on your chart.

How It Does It

The LuciTech Strategy Template is meticulously crafted using Pine Script, TradingView's powerful and expressive programming language. The underlying architecture is designed for clarity and modularity, allowing for straightforward integration of your unique trading signals. At its core, the template operates by taking user-defined entry and exit conditions and then applying a sophisticated layer of risk management, position sizing, and trade execution logic.

For instance, when a longCondition or shortCondition is met, the template dynamically calculates the appropriate position size. This calculation is based on your specified risk_percent of equity and the stop_distance (the distance between your entry price and the calculated stop-loss level). This ensures that each trade adheres to your predefined risk parameters, a critical component of disciplined trading.

The flexibility in stop-loss calculation is achieved through a switch statement that evaluates the sl_type input. Whether you choose an ATR-based stop, which adapts to market volatility, or a candle-based stop, which uses structural price points, the template seamlessly integrates these methods. The ATR calculation itself is further refined by allowing various smoothing methods (RMA, SMA, EMA, WMA), providing granular control over how volatility is measured.

Time-based filtering is implemented by comparing the current bar's time with user-defined start_hour, start_minute, end_hour, and end_minute inputs. This allows the strategy to activate or deactivate trading during specific market sessions or periods of the day, a valuable tool for optimizing performance and avoiding unfavorable conditions.

Furthermore, the template incorporates advanced webhook alert functionality. When a trade is executed, a customizable JSON message is formatted based on your webhook_format selection (Standard, Telegram, or Concise Telegram) and sent via alert function. This enables seamless integration with external services for real-time notifications or even automated trade execution through third-party platforms.

Visual feedback is paramount for understanding strategy behavior. The template utilizes plot and fill functions to clearly display entry prices, stop-loss levels, and take-profit targets directly on the chart. Customizable colors for these elements, along with dedicated options for Fair Value Gap (FVG) boxes, enhance the visual analysis during backtesting and live trading, making it easier to interpret the strategy's actions.

How It's Original

The LuciTech Strategy Template distinguishes itself in the crowded landscape of TradingView scripts through its unique combination of integrated, advanced risk management features, highly flexible stop-loss methodologies, and sophisticated alerting capabilities, all within a user-friendly and modular framework. While many templates offer basic entry/exit signal integration, LuciTech goes several steps further by providing a robust, ready-to-use infrastructure for managing the entire trade lifecycle once a signal is generated.

Unlike templates that might require users to piece together various risk management components or code complex stop-loss logic from scratch, LuciTech offers these critical functionalities out-of-the-box. The inclusion of dynamic position sizing based on a user-defined risk percentage, a configurable risk-to-reward ratio, and an intelligent breakeven mechanism significantly elevates its utility. This comprehensive approach to capital preservation and profit targeting is a cornerstone of professional trading and is often overlooked or simplified in generic templates.

Furthermore, the template's provision for multiple stop-loss calculation types—ATR-based for volatility adaptation, and candle-based for structural support/resistance—demonstrates a deep understanding of diverse trading strategies. The underlying code for these calculations is already implemented, saving developers considerable time and effort. The subtle yet powerful inclusion of FVG (Fair Value Gap) related inputs also hints at advanced price action concepts, offering a sophisticated layer of analysis and execution that is not commonly found in general-purpose templates.

The advanced webhook alerting system, with its support for various JSON formats tailored for platforms like Telegram, showcases an originality in catering to the needs of modern, automated trading setups. This moves beyond simple TradingView pop-up alerts, enabling seamless integration with external systems for real-time trade monitoring and execution. This level of external connectivity and customizable data output is a significant differentiator.

In essence, the LuciTech Strategy Template is original not just in its individual features, but in how these features are cohesively integrated to form a powerful, opinionated, yet highly adaptable system. It empowers traders to focus their creative energy on developing their core entry/exit signals, confident that the underlying framework will handle the complexities of risk management, trade execution, and external communication with precision and flexibility. It's a comprehensive solution designed to accelerate the development of robust and professional trading strategies.

How to Modify the Logic to Apply Your Strategy

The LuciTech Strategy Template is designed with modularity in mind, making it exceptionally straightforward to integrate your unique trading strategy logic. The template provides a clear separation between the core strategy management (risk, position sizing, exits) and the entry signal generation. This allows you to easily plug in your own buy and sell conditions without altering the robust underlying framework.

Here’s a step-by-step guide on how to adapt the template to your specific trading strategy:

1.

Locate the Strategy Logic Section:

Open the Pine Script editor in TradingView and navigate to the section clearly marked with the comment //Strategy Logic Example:. This is where the template’s placeholder entry conditions (a simple moving average crossover) are defined.

2.

Define Your Custom Entry Conditions:

Within this section, you will find variables such as longCondition and shortCondition. These are boolean variables that determine when a long or short trade should be initiated. Replace the existing example logic with your own custom buy and sell conditions. Your conditions can be based on any combination of indicators, price action patterns, candlestick formations, or other market analysis techniques. For example, if your strategy involves a combination of RSI and MACD, you would define longCondition as (rsi > 50 and macd_line > signal_line) and shortCondition as (rsi < 50 and macd_line < signal_line).

3.

Leverage the Template’s Built-in Features:

Once your longCondition and shortCondition are defined, the rest of the template automatically takes over. The integrated risk management module will calculate the appropriate position size based on your Risk % input and the chosen Stop Loss Type. The Risk:Reward ratio will determine your take-profit levels, and the Breakeven at R feature will manage your stop-loss dynamically. The time filter (Use Time Filter) will ensure your trades only occur within your specified hours, and the webhook alerts will notify you of trade executions.

Momentum Breakout StrategyBacktest a strategy where, when a candlestick on a timeframe rises more than a certain %, it enters a trade.

LANZ Strategy 6.0 [Backtest]🔷 LANZ Strategy 6.0 — Precision Backtesting Based on 09:00 NY Candle, Dynamic SL/TP, and Lot Size per Trade

LANZ Strategy 6.0 is the simulation version of the original LANZ 6.0 indicator. It executes a single LIMIT BUY order per day based on the 09:00 a.m. New York candle, using dynamic Stop Loss and Take Profit levels derived from the candle range. Position sizing is calculated automatically using capital, risk percentage, and pip value — allowing accurate trade simulation and performance tracking.

📌 This is a strategy script — It simulates real trades using strategy.entry() and strategy.exit() with full money management for risk-based backtesting.

🧠 Core Logic & Trade Conditions

🔹 BUY Signal Trigger:

At 09:00 a.m. NY (New York time), if:

The current candle is bullish (close > open)

→ A BUY order is placed at the candle’s close price (EP)

Only one signal is evaluated per day.

⚙️ Stop Loss / Take Profit Logic

SL can be:

Wick low (0%)

Or dynamically calculated using a % of the full candle range

TP is calculated using the user-defined Risk/Reward ratio (e.g., 1:4)

The TP and SL levels are passed to strategy.exit() for each trade simulation.

💰 Risk Management & Lot Size Calculation

Before placing the trade:

The system calculates pip distance from EP to SL

Computes the lot size based on:

Account capital

Risk % per trade

Pip value (auto or manual)

This ensures every trade uses consistent, scalable risk regardless of instrument.

🕒 Manual Close at 3:00 p.m. NY

If the trade is still open by 15:00 NY time, it will be closed using strategy.close().

The final result is the actual % gain/loss based on how far price moved relative to SL.

📊 Backtest Accuracy

One trade per day

LIMIT order at the candle close

SL and TP pre-defined at execution

No repainting

Session-restricted (only runs on 1H timeframe)

✅ Ideal For:

Traders who want to backtest a clean and simple daily entry system

Strategy developers seeking reproducible, high-conviction trades

Users who prefer non-repainting, session-based simulations

👨💻 Credits:

💡 Developed by: LANZ

🧠 Logic & Money Management Engine: LANZ

📈 Designed for: 1H charts

🧪 Purpose: Accurate simulation of LANZ 6.0's NY Candle Entry system

Quantum Reversal Engine [ApexLegion]Quantum Reversal Engine

STRATEGY OVERVIEW

This strategy is constructed using 5 custom analytical filters that analyze different market dimensions - trend structure, momentum expansion, volume confirmation, price action patterns, and reversal detection - with results processed through a multi-component scoring calculation that determines signal generation and position management decisions.

Why These Custom Filters Were Independently Developed:

This strategy employs five custom-developed analytical filters:

1. Apex Momentum Core (AMC) - Custom oscillator with volatility-scaled deviation calculation

Standard oscillators lag momentum shifts by 2-3 bars. Custom calculation designed for momentum analysis

2. Apex Wick Trap (AWT) - Wick dominance analysis for trap detection

Existing wick analysis tools don't quantify trap conditions. Uses specific ratios for wick dominance detection

3. Apex Volume Pulse (AVP) - Volume surge validation with participation confirmation

Volume indicators typically use simple averages. Uses surge multipliers with participation validation

4. Apex TrendGuard (ATG) - Angle-based trend detection with volatility band integration

EMA slope calculations often produce false signals. Uses angle analysis with volatility bands for confirmation

5. Quantum Composite Filter (QCF) - Multi-component scoring and signal generation system

Composite scoring designed to filter noise by requiring multiple confirmations before signal activation.

Each filter represents mathematical calculations designed to address specific analytical requirements.

Framework Operation: The strategy functions as a scoring framework where each filter contributes weighted points based on market conditions. Entry signals are generated when minimum threshold scores are met. Exit management operates through a three-tier system with continued signal strength evaluation determining position holds versus closures at each TP level.

Integration Challenge: The core difficulty was creating a scoring system where five independent filters could work together without generating conflicting signals. This required backtesting to determine effective weight distributions.

Custom Filter Development:

Each of the five filters represents analytical approaches developed through testing and validation:

Integration Validation: Each filter underwent individual testing before integration. The composite scoring system required validation to verify that filters complement rather than conflict with each other, resulting in a cohesive analytical framework that was tested during the development period.

These filters represent custom-developed components created specifically for this strategy, with each component addressing different analytical requirements through testing and parameter adjustment.

Programming Features:

Multi-timeframe data handling with backup systems

Performance optimization techniques

Error handling for live trading scenarios

Parameter adaptation based on market conditions

Strategy Features:

Uses multi-filter confirmation approach

Adapts position holding based on continued signal strength

Includes analysis tools for trade review and optimization

Ongoing Development: The strategy was developed through testing and validation processes during the creation period.

COMPONENT EXPLANATION

EMA System

Uses 8 exponential moving averages (7, 14, 21, 30, 50, 90, 120, 200 periods) for trend identification. Primary signals come from 8/21 EMA crossovers, while longer EMAs provide structural context. EMA 1-4 determine short-term structure, EMA 5-8 provide long-term trend confirmation.

Apex Momentum Core (AMC)

Built custom oscillator mathematics after testing dozens of momentum calculation methods. Final algorithm uses price deviation from EMA baseline with volatility scaling to reduce lag while maintaining accuracy across different market conditions.

Custom momentum oscillator using price deviation from EMA baseline:

apxCI = 100 * (source - emaBase) / (sensitivity * sqrt(deviation + 1))

fastLine = EMA(apxCI, smoothing)

signalLine = SMA(fastLine, 4)

Signals generate when fastLine crosses signalLine at +50/-50 thresholds.

This identifies momentum expansion before traditional oscillators.

Apex Volume Pulse (AVP)

Created volume surge analysis that goes beyond simple averages. Extensive testing determined 1.3x multiplier with participation validation provides reliable confirmation while filtering false volume spikes.

Compares current volume to 21-period moving average.

Requires 1.3x average volume for signal confirmation. This filters out low-volume moves during quiet periods and confirms breakouts with actual participation.

Apex Wick Trap (AWT)

Developed proprietary wick trap detection through analysis of failed breakout patterns. Tested various ratio combinations before settling on 60% wick dominance + 20% body limit as effective trap identification parameters.

Analyzes candle structure to identify failed breakouts:

candleRange = math.max(high - low, 0.00001)

candleBody = math.abs(close - open)

bodyRatio = candleBody / candleRange

upperWick = high - math.max(open, close)

lowerWick = math.min(open, close) - low

upperWickRatio = upperWick / candleRange

lowerWickRatio = lowerWick / candleRange

trapWickLong = showAWT and lowerWickRatio > minWickDom and bodyRatio < bodyToRangeLimit and close > open

trapWickShort = showAWT and upperWickRatio > minWickDom and bodyRatio < bodyToRangeLimit and close < open This catches reversals after fake breakouts.

Apex TrendGuard (ATG)

Built angle-based trend detection after standard EMA crossovers proved insufficient. Combined slope analysis with volatility bands through iterative testing to eliminate false trend signals.

EMA slope analysis with volatility bands:

Fast EMA (21) vs Slow EMA (55) for trend direction

Angle calculation: atan(fast - slow) * 180 / π

ATR bands (1.75x multiplier) for breakout confirmation

Minimum 25° angle for strong trend classification

Core Algorithm Framework

1. Composite Signal Generation

calculateCompositeSignals() =>

// Component Conditions

structSignalLong = trapWickLong

structSignalShort = trapWickShort

momentumLong = amcBuySignal

momentumShort = amcSellSignal

volumeSpike = volume > volAvg_AVP * volMult_AVP

priceStrength_Long = close > open and close > close

priceStrength_Short = close < open and close < close

rsiMfiComboValue = (ta.rsi(close, 14) + ta.mfi(close, 14)) / 2

reversalTrigger_Long = ta.crossover(rsiMfiComboValue, 50)

reversalTrigger_Short = ta.crossunder(rsiMfiComboValue, 50)

isEMACrossUp = ta.crossover(emaFast_ATG, emaSlow_ATG)

isEMACrossDown = ta.crossunder(emaFast_ATG, emaSlow_ATG)

// Enhanced Composite Score Calculation

scoreBuy = 0.0

scoreBuy += structSignalLong ? scoreStruct : 0.0

scoreBuy += momentumLong ? scoreMomentum : 0.0

scoreBuy += flashSignal ? weightFlash : 0.0

scoreBuy += blinkSignal ? weightBlink : 0.0

scoreBuy += volumeSpike_AVP ? scoreVolume : 0.0

scoreBuy += priceStrength_Long ? scorePriceAction : 0.0

scoreBuy += reversalTrigger_Long ? scoreReversal : 0.0

scoreBuy += emaAlignment_Bull ? weightTrendAlign : 0.0

scoreBuy += strongUpTrend ? weightTrendAlign : 0.0

scoreBuy += highRisk_Long ? -1.2 : 0.0

scoreBuy += signalGreenDot ? 1.0 : 0.0

scoreBuy += isAMCUp ? 0.8 : 0.0

scoreBuy += isVssBuy ? 1.5 : 0.0

scoreBuy += isEMACrossUp ? 1.0 : 0.0

scoreBuy += signalRedX ? -1.0 : 0.0

scoreSell = 0.0

scoreSell += structSignalShort ? scoreStruct : 0.0

scoreSell += momentumShort ? scoreMomentum : 0.0

scoreSell += flashSignal ? weightFlash : 0.0

scoreSell += blinkSignal ? weightBlink : 0.0

scoreSell += volumeSpike_AVP ? scoreVolume : 0.0

scoreSell += priceStrength_Short ? scorePriceAction : 0.0

scoreSell += reversalTrigger_Short ? scoreReversal : 0.0

scoreSell += emaAlignment_Bear ? weightTrendAlign : 0.0

scoreSell += strongDownTrend ? weightTrendAlign : 0.0

scoreSell += highRisk_Short ? -1.2 : 0.0

scoreSell += signalRedX ? 1.0 : 0.0

scoreSell += isAMCDown ? 0.8 : 0.0

scoreSell += isVssSell ? 1.5 : 0.0

scoreSell += isEMACrossDown ? 1.0 : 0.0

scoreSell += signalGreenDot ? -1.0 : 0.0

compositeBuySignal = enableComposite and scoreBuy >= thresholdCompositeBuy

compositeSellSignal = enableComposite and scoreSell >= thresholdCompositeSell

if compositeBuySignal and compositeSellSignal

compositeBuySignal := false

compositeSellSignal := false

= calculateCompositeSignals()

// Final Entry Signals

entryCompositeBuySignal = compositeBuySignal and ta.rising(emaFast_ATG, 2)

entryCompositeSellSignal = compositeSellSignal and ta.falling(emaFast_ATG, 2)

Calculates weighted scores from independent modules and activates signals only when threshold requirements are met.

2. Smart Exit Hold Evaluation System

evaluateSmartHold() =>

compositeBuyRecentCount = 0

compositeSellRecentCount = 0

for i = 0 to signalLookbackBars - 1

compositeBuyRecentCount += compositeBuySignal ? 1 : 0

compositeSellRecentCount += compositeSellSignal ? 1 : 0

avgVolume = ta.sma(volume, 20)

volumeSpike = volume > avgVolume * volMultiplier

// MTF Bull/Bear conditions

mtf_bull = mtf_emaFast_final > mtf_emaSlow_final

mtf_bear = mtf_emaFast_final < mtf_emaSlow_final

emaBackupDivergence = math.abs(mtf_emaFast_backup - mtf_emaSlow_backup) / mtf_emaSlow_backup

emaBackupStrong = emaBackupDivergence > 0.008

mtfConflict_Long = inLong and mtf_bear and emaBackupStrong

mtfConflict_Short = inShort and mtf_bull and emaBackupStrong

// Layer 1: ATR-Based Dynamic Threshold (Market Volatility Intelligence)

atr_raw = ta.atr(atrLen)

atrValue = na(atr_raw) ? close * 0.02 : atr_raw

atrRatio = atrValue / close

dynamicThreshold = atrRatio > 0.02 ? 1.0 : (atrRatio > 0.01 ? 1.5 : 2.8)

// Layer 2: ROI-Conditional Time Intelligence (Selective Pressure)

timeMultiplier_Long = realROI >= 0 ? 1.0 : // Profitable positions: No time pressure

holdTimer_Long <= signalLookbackBars ? 1.0 : // Loss positions 1-8 bars: Base

holdTimer_Long <= signalLookbackBars * 2 ? 1.1 : // Loss positions 9-16 bars: +10% stricter

1.3 // Loss positions 17+ bars: +30% stricter

timeMultiplier_Short = realROI >= 0 ? 1.0 : // Profitable positions: No time pressure

holdTimer_Short <= signalLookbackBars ? 1.0 : // Loss positions 1-8 bars: Base

holdTimer_Short <= signalLookbackBars * 2 ? 1.1 : // Loss positions 9-16 bars: +10% stricter

1.3 // Loss positions 17+ bars: +30% stricter

// Dual-Layer Threshold Calculation

baseThreshold_Long = mtfConflict_Long ? dynamicThreshold + 1.0 : dynamicThreshold

baseThreshold_Short = mtfConflict_Short ? dynamicThreshold + 1.0 : dynamicThreshold

timeAdjustedThreshold_Long = baseThreshold_Long * timeMultiplier_Long

timeAdjustedThreshold_Short = baseThreshold_Short * timeMultiplier_Short

// Final Smart Hold Decision with Dual-Layer Intelligence

smartHold_Long = not mtfConflict_Long and smartScoreLong >= timeAdjustedThreshold_Long and compositeBuyRecentCount >= signalMinCount

smartHold_Short = not mtfConflict_Short and smartScoreShort >= timeAdjustedThreshold_Short and compositeSellRecentCount >= signalMinCount

= evaluateSmartHold()

Evaluates whether to hold positions past TP1/TP2/TP3 levels based on continued signal strength, volume confirmation, and multi-timeframe trend alignment

HOW TO USE THE STRATEGY

Step 1: Initial Setup

Apply strategy to your preferred timeframe (backtested on 15M)

Enable "Use Heikin-Ashi Base" for smoother signals in volatile markets

"Show EMA Lines" and "Show Ichimoku Cloud" are enabled for visual context

Set default quantities to match your risk management (5% equity default)

Step 2: Signal Recognition

Visual Signal Guide:

Visual Signal Guide - Complete Reference:

🔶 Red Diamond: Bearish momentum breakdown - short reversal signal

🔷 Blue Diamond: Strong bullish momentum - long reversal signal

🔵 Blue Dot: Volume-confirmed directional move - trend continuation

🟢 Green Dot: Bullish EMA crossover - trend reversal confirmation

🟠 Orange X: Oversold reversal setup - counter-trend opportunity

❌ Red X: Bearish EMA breakdown - trend reversal warning

✡ Star Uprising: Strong bullish convergence

💥 Ultra Entry: Ultra-rapid downward momentum acceleration

▲ VSS Long: Velocity-based bullish momentum confirmation

▼ VSS Short: Velocity-based bearish momentum confirmation

Step 3: Entry Execution

For Long Positions:

1. ✅ EMA1 crossed above EMA2 exactly 3 bars ago [ta.crossover(ema1,ema2) ]

2. ✅ Current EMA structure: EMA1 > EMA2 (maintained)

3. ✅ Composite score ≥ 5.0 points (6.5+ for 5-minute timeframes)

4. ✅ Cooldown period completed (no recent stop losses)

5. ✅ Volume spike confirmation (green dot/blue dot signals)

6. ✅ Bullish candle closes above EMA structure

For Short Positions:

1. ✅ EMA1 crossed below EMA2 exactly 3 bars ago [ta.crossunder(ema1,ema2) ]

2. ✅ Current EMA structure: EMA1 < EMA2 (maintained)

3. ✅ Composite score ≥ 5.4 points (7.0+ for 5-minute timeframes)

4. ✅ Cooldown period completed (no recent stop losses)

5. ✅ Momentum breakdown (red diamond/red X signals)

6. ✅ Bearish candle closes below EMA structure

🎯 Critical Timing Note: The strategy requires EMA crossover to have occurred 3 bars prior to entry, not at the current bar. This attempts to avoid premature entries and may improve signal reliability.

Step 4: Reading Market Context

EMA Ribbon Interpretation:

All EMAs ascending = Strong uptrend context

EMAs 1-3 above EMAs 4-8 = Bullish structure

Tight EMA spacing = Low volatility/consolidation

Wide EMA spacing = High volatility/trending

Ichimoku Cloud Context:

Price above cloud = Bullish environment

Price below cloud = Bearish environment

Cloud color intensity = Momentum strength

Thick cloud = Strong support/resistance

THE SMART EXIT GRID SYSTEM

Smart Exit Grid Approach:

The Smart Exit Grid uses dynamic hold evaluation that continuously analyzes market conditions after position entry. This differs from traditional fixed profit targets by adapting exit timing based on real-time signal strength.

How Smart Exit Grid System Works

The system operates through three evaluation phases:

Smart Score Calculation:

The smart score calculation aggregates 22 signal components in real-time, combining reversal warnings, continuation signals, trend alignment indicators, EMA structural analysis, and risk penalties into a numerical representation of market conditions. MTF analysis provides additional confirmation as a separate validation layer.

Signal Stack Management:

The per-tick signal accumulation system monitors 22 active signal types with MTF providing trend validation and conflict detection as a separate confirmation layer.

Take Profit Progression:

Smart Exit Activation:

The QRE system activates Smart Exit Grid immediately upon position entry. When strategy.entry() executes, the system initializes monitoring systems designed to track position progress.

Upon position opening, holdTimer begins counting, establishing the foundation for subsequent decisions. The Smart Exit Grid starts accumulating signals from entry, with all 22 signal components beginning real-time tracking when the trade opens.

The system operates on continuous evaluation where smartScoreLong and smartScoreShort calculate from the first tick after entry. QRE's approach is designed to capture market structure changes, trend deteriorations, or signal pattern shifts that can trigger protective exits even before the first take profit level is reached.

This activation creates a proactive position management framework. The 8-candle sliding window starts from entry, meaning that if market conditions change rapidly after entry - due to news events, liquidity shifts, or technical changes - the system can respond within the configured lookback period.

TP Markers as Reference Points:

The TP1, TP2, and TP3 levels function as reference points rather than mandatory exit triggers. When longTP1Hit or shortTP1Hit conditions activate, they serve as profit confirmation markers that inform the Smart Exit algorithm about achieved reward levels, but don't automatically initiate position closure.

These TP markers enhance the Smart Exit decision matrix by providing profit context to ongoing signal evaluation. The system recognizes when positions have achieved target returns, but the actual exit decision remains governed by continuous smart score evaluation and signal stack analysis.

TP2 Reached: Enhanced Monitoring

TP2 represents significant profit capture with additional monitoring features:

This approach is designed to help avoid premature profit-taking during trending conditions. If TP2 is reached but smartScoreLong remains above the dynamic threshold and the 8-candle sliding window shows persistent signals, the position continues holding. If market structure deteriorates before reaching TP2, the Smart Exit can trigger closure based on signal analysis.

The visual TP circles that appear when levels are reached serve as performance tracking tools, allowing users to see how frequently entries achieve various profit levels while understanding that actual exit timing depends on market structure analysis.

Risk Management Systems:

Operating independently from the Smart Exit Grid are two risk management systems: the Trap Wick Detection Protocol and the Stop Loss Mechanism. These systems maintain override authority over other exit logic.

The Trap Wick System monitors for conditionBearTrapExit during long positions and conditionBullTrapExit during short positions. When detected, these conditions trigger position closure with state reset, bypassing Smart Exit evaluations. This system recognizes that certain candlestick patterns may indicate reversal risk.

Volatility Exit Monitoring: The strategy monitors for isStrongBearCandle combined with conditionBearTrapExit, recognizing when market structure may be shifting.

Volume Validation: Before exiting on volatility, the strategy requires volume confirmation: volume > ta.sma(volume, 20) * 1.8. This is designed to filter exits on weak, low-volume movements.

The Stop Loss Mechanism operates through multiple triggers including traditional price-based stops (longSLHit, shortSLHit) and early exit conditions based on smart score deterioration combined with negative ROI. The early exit logic activates when smartScoreLong < 1.0 or smartScoreShort < 1.0 while realROI < -0.9%.

These risk management systems are designed so that risk scenarios can trigger protective closure with state reset across all 22 signal counters, TP tracking variables, and smart exit states.

This architecture - Smart Exit activation, TP markers as navigation tools, and independent risk management - creates a position management system that adapts to market conditions while maintaining risk discipline through dedicated protection protocols.

TP3 Reached: Enhanced Protection

Once TP3 is hit, the strategy shifts into enhanced monitoring:

EMA Structure Monitoring: isEMAStructureDown becomes a primary exit trigger

MTF Alignment: The higher timeframe receives increased consideration

Wick Trap Priority: conditionBearTrapExit becomes an immediate exit signal

Approach Differences:

Traditional Fixed Exits:

Exit at predetermined levels regardless of market conditions

May exit during trend continuation

May exit before trend completion

Limited adaptation to changing volatility

Smart Exit Grid Approach:

Adaptive timing based on signal conditions

Exits when supporting signals weaken

Multi-timeframe validation for trend confirmation

Volume confirmation requirements for holds

Structural monitoring for trend analysis

Dynamic ATR-Based Smart Score Threshold System

Market Volatility Adaptive Scoring

// Real-time ATR Analysis

atr_raw = ta.atr(atrLen)

atrValue = na(atr_raw) ? close * 0.02 : atr_raw

atrRatio = atrValue / close

// Three-Tier Dynamic Threshold Matrix

dynamicThreshold = atrRatio > 0.02 ? 1.0 : // High volatility: Lower threshold

(atrRatio > 0.01 ? 1.5 : // Medium volatility: Standard

2.8) // Low volatility: Higher threshold

The market volatility adaptive scoring calculates real-time ATR with a 2% fallback for new markets. The atrRatio represents the relationship between current volatility and price, creating a foundation for threshold adjustment.

The three-tier dynamic threshold matrix responds to market conditions by adjusting requirements based on volatility levels: lowering thresholds during high volatility periods above 2% ATR ratio to 1.0 points, maintaining standard requirements at 1.5 points for medium volatility between 1-2%, and raising standards to 2.8 points during low volatility periods below 1%.

Profit-Loss Adaptive Management:

The system applies different evaluation criteria based on position performance:

Winning Positions (realROI ≥ 0%):

→ timeMultiplier = 1.0 (No additional pressure)

→ Maintains base threshold requirements

→ Allows natural progression to TP2/TP3 levels

Losing Positions (realROI < 0%):

→ Progressive time pressure activated

→ Increasingly strict requirements over time

→ Faster decision-making on underperforming trades

ROI-Adaptive Smart Hold Decision Process:

The strategy uses a profit-loss adaptive system:

Winning Position Management (ROI ≥ 0%):

✅ Standard threshold requirements maintained

✅ No additional time-based pressure applied

✅ Allows positions to progress toward TP2/TP3 levels

✅ timeMultiplier remains at 1.0 regardless of hold duration

Losing Position Management (ROI < 0%):

⚠️ Time-based threshold adjustments activated

⚠️ Progressive increase in required signal strength over time

⚠️ Earlier exit evaluation on underperforming positions

⚠️ timeMultiplier increases from 1.0 → 1.1 → 1.3 based on hold duration

Real-Time Monitoring:

Monitor Analysis Table → "Smart" filter → "Score" vs "Dynamic Threshold"

Winning positions: Evaluation based on signal strength deterioration only

Losing positions: Evaluation considers both signal strength and progressive time adjustments

Breakeven positions (0% ROI): Treated as winning positions - no time adjustments

This approach differentiates between winning and losing positions in the hold evaluation process, requiring higher signal thresholds for extended holding of losing positions while maintaining standard requirements for winning ones.

ROI-Conditional Decision Matrix Examples:

Scenario 1 - Winning Position in Any Market:

Position ROI: +0.8% → timeMultiplier = 1.0 (regardless of hold time)

ATR Medium (1.2%) → dynamicThreshold = 1.5

Final Threshold = 1.5 × 1.0 = 1.5 points ✅ Position continues

Scenario 2 - Losing Position, Extended Hold:

Position ROI: -0.5% → Time pressure activated

Hold Time: 20 bars → timeMultiplier = 1.3

ATR Low (0.8%) → dynamicThreshold = 2.8

Final Threshold = 2.8 × 1.3 = 3.64 points ⚡ Enhanced requirements

Scenario 3 - Fresh Losing Position:

Position ROI: -0.3% → Time pressure activated

Hold Time: 5 bars → timeMultiplier = 1.0 (still early)

ATR High (2.1%) → dynamicThreshold = 1.0

Final Threshold = 1.0 × 1.0 = 1.0 points 📊 Recovery opportunity

Scenario 4 - Breakeven Position:

Position ROI: 0.0% → timeMultiplier = 1.0 (no pressure)

Hold Time: 15 bars → No time penalty applied

Final Threshold = dynamicThreshold only ⚖️ Neutral treatment

🔄8-Candle Sliding Window Signal Rotation System

Composite Signal Counting Mechanism

// Dynamic Lookback Window (configurable: default 8)

signalLookbackBars = input.int(8, "Composite Lookback Bars", minval=1, maxval=50)

// Rolling Signal Analysis

compositeBuyRecentCount = 0

compositeSellRecentCount = 0

for i = 0 to signalLookbackBars - 1

compositeBuyRecentCount += compositeBuySignal ? 1 : 0

compositeSellRecentCount += compositeSellSignal ? 1 : 0

Candle Flow Example (8-bar window):

→

✓ ✓ ✗ ✓ ✗ ✓ ✗ ✓ 🗑️

New Signal Count = 5/8 signals in window

Threshold Check: 5 ≥ signalMinCount (2) = HOLD CONFIRMED

Signal Decay & Refresh Mechanism

// Signal Persistence Tracking

if compositeBuyRecentCount >= signalMinCount

smartHold_Long = true

else

smartHold_Long = false

The composite signal counting operates through a configurable sliding window. The system maintains rolling counters that scan backward through the specified number of candles.

During each evaluation cycle, the algorithm iterates through historical bars, incrementing counters when composite signals are detected. This creates a dynamic signal persistence measurement where recent signal density determines holding decisions.