IDX - 5UPThe UDX-5UP is a custom indicator designed to assist traders in identifying trends, entry and exit signals, and market reversal moments with greater accuracy. It combines price analysis, volume, and momentum (RSI) to provide clear buy ("Buy") and sell ("Sell") signals across any asset and timeframe, whether you're a scalper on the 5M chart or a swing trader on the 4H chart. Inspired by robust technical analysis strategies, the UDX-5UP is ideal for traders seeking a reliable tool to operate in volatile markets such as cryptocurrencies, forex, stocks, and futures.

Components of the UDX-5UP

The UDX-5UP consists of three main panels that work together to provide a comprehensive view of the market:

Main Panel (Price):

Pivot Supertrend: A dynamic line that changes color to indicate the trend. Green for an uptrend (look for buys), red for a downtrend (look for sells).

SMAs (Simple Moving Averages): Two SMAs (8 and 21 periods) to confirm the trend direction. When the SMA 8 crosses above the SMA 21, it’s a bullish signal; when it crosses below, it’s a bearish signal.

Entry/Exit Signals: "Buy" (green) and "Sell" (red) labels are plotted on the chart when entry or exit conditions are met.

Volume Panel:

Colored Volume Bars: Green bars indicate dominant buying volume, while red bars indicate dominant selling volume.

Volume Moving Average (MA 20): A blue line that helps identify whether the current volume is above or below the average, confirming the strength of the movement.

RSI Panel:

RSI (Relative Strength Index): Calculated with a period of 14, with overbought (70) and oversold (30) lines to identify momentum extremes.

Divergences: The indicator detects divergences between the RSI and price, plotting signals for potential reversals.

How the UDX-5UP Works

The UDX-5UP uses a combination of rules to generate buy and sell signals:

Buy Signal ("Buy"):

The Pivot Supertrend changes from red to green.

The SMA 8 crosses above the SMA 21.

The volume is above the MA 20, with green bars (indicating buying pressure).

The RSI is rising and, ideally, below 70 (not overbought).

Example: On the 4H chart, the price of Tether (USDT) is at 0.05515. The Pivot Supertrend turns green, the SMA 8 crosses above the SMA 21, the volume shows green bars above the MA 20, and the RSI is at 46. The UDX-5UP plots a "Buy".

Sell Signal ("Sell"):

The Pivot Supertrend changes from green to red.

The SMA 8 crosses below the SMA 21.

The volume is above the MA 20, with red bars (indicating selling pressure).

The RSI is falling and, ideally, above 70 (overbought).

Example: On the 4H chart, the price of Tether rises to 0.05817. The Pivot Supertrend turns red, the SMA 8 crosses below the SMA 21, the volume shows red bars, and the RSI is above 70. The UDX-5UP plots a "Sell".

RSI Divergences:

The indicator identifies bullish divergences (price makes a lower low, but RSI makes a higher low) and bearish divergences (price makes a higher high, but RSI makes a lower high), plotting alerts for potential reversals.

Adjustable Settings

The UDX-5UP is highly customizable to suit your trading style:

Pivot Supertrend Period: Default is 2. Increase to 3 or 4 for more conservative signals (fewer false positives, but more lag).

SMA Periods: Default is 8 and 21. Adjust to 5 and 13 for smaller timeframes (e.g., 5M) or 13 and 34 for larger timeframes (e.g., 1D).

RSI Period: Default is 14. Reduce to 10 for greater sensitivity or increase to 20 for smoother signals.

Overbought/Oversold Levels: Default is 70/30. Adjust to 80/20 in volatile markets.

Display Panels: You can enable/disable the volume and RSI panels to simplify the chart.

How to Use the UDX-5UP

Identify the Trend:

Use the Pivot Supertrend and SMAs to determine the market direction. Uptrend: look for buys. Downtrend: look for sells.

Confirm with Volume and RSI:

For buys: Volume above the MA 20 with green bars, RSI rising and below 70.

For sells: Volume above the MA 20 with red bars, RSI falling and above 70.

Enter the Trade:

Enter a buy when the UDX-5UP plots a "Buy" and all conditions are aligned.

Enter a sell when the UDX-5UP plots a "Sell" and all conditions are aligned.

Plan the Exit:

Use Fibonacci levels or support/resistance on the price chart to set targets.

Exit the trade when the UDX-5UP plots an opposite signal ("Sell" after a buy, "Buy" after a sell).

Tips for Beginners

Start with Larger Timeframes: Use the 4H or 1D chart for more reliable signals and less noise.

Combine with Other Indicators: Use the UDX-5UP with tools like Fibonacci or the Candles RSI (another powerful indicator) to confirm signals.

Practice in Demo Mode: Test the indicator in a demo account before using real money.

Manage Risk: Always use a stop-loss and don’t risk more than 1-2% of your capital per trade.

Why Use the UDX-5UP?

Simplicity: Clear "Buy" and "Sell" signals make trading accessible even for beginners.

Versatility: Works on any asset (crypto, forex, stocks) and timeframe.

Multiple Confirmations: Combines price, volume, and momentum to reduce false signals.

Customizable: Adjust the settings to match your trading style.

Author’s Notes

The UDX-5UP was developed based on years of trading and technical analysis experience. It is an evolution of tested strategies, designed to help traders navigate volatile markets with confidence. However, no indicator is infallible. Always combine the UDX-5UP with proper risk management and fundamental analysis, especially in unpredictable markets. Feedback is welcome – leave a comment or reach out with suggestions for improvements!

ابحث في النصوص البرمجية عن "Futures"

Modified RSIModified RSI (Round Number RSI)

Category: Oscillator / Momentum

Description

The Modified RSI (Round Number RSI) is an enhanced version of the classic Relative Strength Index (RSI), designed to provide clearer and more structured signals by rounding its values to whole numbers. This modification helps traders filter out noise, making trend analysis and overbought/oversold conditions easier to interpret.

Key Features:

✔ Rounded RSI Values – Instead of fluctuating with decimals, this RSI rounds values to whole numbers (e.g., 30, 50, 70) for clearer decision-making.

✔ Easier Signal Interpretation – Helps traders identify key RSI levels without distractions from small fluctuations.

✔ Customizable Lookback Period – Allows adjustment of RSI sensitivity to fit different trading strategies.

✔ Works on All Timeframes & Assets – Can be applied to stocks, forex, crypto, and futures.

How to Use It:

📌 Overbought & Oversold Levels:

RSI ≥ 70 → Market may be overbought (potential reversal or correction).

RSI ≤ 30 → Market may be oversold (potential buying opportunity).

📌 Trend Confirmation:

RSI staying above 50 signals bullish momentum.

RSI staying below 50 signals bearish momentum.

📌 Divergence Trading:

Price makes a new high, but RSI does not → Bearish Divergence (Possible Downtrend).

Price makes a new low, but RSI does not → Bullish Divergence (Possible Uptrend).

Best Used For:

📈 Day Traders & Swing Traders looking for simplified RSI signals.

📉 Trend Confirmation with moving averages or volume analysis.

⚡ Confluence Trading with support/resistance zones.

Why Use This Over Traditional RSI?

🔹 Removes unnecessary noise by rounding RSI values.

🔹 Helps traders focus on key levels (30, 50, 70).

🔹 Reduces decision fatigue for fast-paced trading.

Volatility-Enhanced Williams %R [AIBitcoinTrend]👽 Volatility-Enhanced Williams %R (AIBitcoinTrend)

The Volatility-Enhanced Williams %R takes the classic Williams %R oscillator to the next level by incorporating volatility-adaptive smoothing, making it significantly more responsive to market dynamics. Unlike the traditional version, which uses a fixed calculation method, this indicator dynamically adjusts its smoothing factor based on market volatility, helping traders capture trends more effectively while filtering out noise.

Additionally, the indicator includes real-time divergence detection and an ATR-based trailing stop system, providing traders with enhanced risk management tools and early reversal signals.

👽 What Makes the Volatility-Enhanced Williams %R Unique?

Unlike the standard Williams %R, which applies a simple lookback-based formula, this version integrates adaptive smoothing and volatility-based filtering to refine its signals and reduce false breakouts.

✅ Volatility-Adaptive Smoothing – Adjusts dynamically based on standard deviation, enhancing signal accuracy.

✅ Real-Time Divergence Detection – Identifies bullish and bearish divergences for early trend reversal signals.

✅ Crossovers & Trailing Stops – Implements Williams %R crossovers with ATR-based trailing stops for intelligent trade management.

👽 The Math Behind the Indicator

👾 Volatility-Adaptive Smoothing

The indicator smooths the Williams %R calculation by applying an adaptive filtering mechanism, which adjusts its responsiveness based on market conditions. This helps to eliminate whipsaws and makes trend-following strategies more reliable.

The smoothing function is defined as:

clamp(x, lo, hi) => math.min(math.max(x, lo), hi)

adaptive(src, prev, len, divisor, minAlpha, maxAlpha) =>

vol = ta.stdev(src, len)

alpha = clamp(vol / divisor, minAlpha, maxAlpha)

prev + alpha * (src - prev)

Where:

Volatility Factor (vol) measures price dispersion using standard deviation.

Adaptive Alpha (alpha) dynamically adjusts smoothing strength.

Clamped Output ensures that the smoothing factor remains within a stable range.

👽 How Traders Can Use This Indicator

👾 Divergence Trading Strategy

Bullish Divergence Setup:

Price makes a lower low, while Williams %R forms a higher low.

Buy signal is confirmed when Williams %R reverses upward.

Bearish Divergence Setup:

Price makes a higher high, while Williams %R forms a lower high.

Sell signal is confirmed when Williams %R reverses downward.

👾 Trailing Stop & Signal-Based Trading

Bullish Setup:

✅ Williams %R crosses above trigger level → Buy signal.

✅ A bullish trailing stop is placed at Low - (ATR × Multiplier).

✅ Exit if price crosses below the stop.

Bearish Setup:

✅ Williams %R crosses below trigger level → Sell signal.

✅ A bearish trailing stop is placed at High + (ATR × Multiplier).

✅ Exit if price crosses above the stop.

👽 Why It’s Useful for Traders

Adaptive Filtering Mechanism – Avoids excessive noise while maintaining responsiveness.

Real-Time Divergence Alerts – Helps traders anticipate market reversals before they occur.

ATR-Based Risk Management – Stops dynamically adjust based on market volatility.

Multi-Market Compatibility – Works effectively across stocks, forex, crypto, and futures.

👽 Indicator Settings

Smoothing Factor – Controls how aggressively the indicator adapts to volatility.

Enable Divergence Analysis – Activates real-time divergence detection.

Lookback Period – Defines the number of bars for detecting pivot points.

Enable Crosses Signals – Turns on Williams %R crossover-based trade signals.

ATR Multiplier – Adjusts trailing stop sensitivity.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

CCI with Signals & Divergence [AIBitcoinTrend]👽 CCI with Signals & Divergence (AIBitcoinTrend)

The Hilbert Adaptive CCI with Signals & Divergence takes the traditional Commodity Channel Index (CCI) to the next level by dynamically adjusting its calculation period based on real-time market cycles using Hilbert Transform Cycle Detection. This makes it far superior to standard CCI, as it adapts to fast-moving trends and slow consolidations, filtering noise and improving signal accuracy.

Additionally, the indicator includes real-time divergence detection and an ATR-based trailing stop system, helping traders identify potential reversals and manage risk effectively.

👽 What Makes the Hilbert Adaptive CCI Unique?

Unlike the traditional CCI, which uses a fixed-length lookback period, this version automatically adjusts its lookback period using Hilbert Transform to detect the dominant cycle in the market.

✅ Hilbert Transform Adaptive Lookback – Dynamically detects cycle length to adjust CCI sensitivity.

✅ Real-Time Divergence Detection – Instantly identifies bullish and bearish divergences for early reversal signals.

✅ Implement Crossover/Crossunder signals tied to ATR-based trailing stops for risk management

👽 The Math Behind the Indicator

👾 Hilbert Transform Cycle Detection

The Hilbert Transform estimates the dominant market cycle length based on the frequency of price oscillations. It is computed using the in-phase and quadrature components of the price series:

tp = (high + low + close) / 3

smooth = (tp + 2 * tp + 2 * tp + tp ) / 6

detrender = smooth - smooth

quadrature = detrender - detrender

inPhase = detrender + quadrature

outPhase = quadrature - inPhase

instPeriod = 0.0

deltaPhase = math.abs(inPhase - inPhase ) + math.abs(outPhase - outPhase )

instPeriod := nz(3.25 / deltaPhase, instPeriod )

dominantCycle = int(math.min(math.max(instPeriod, cciMinPeriod), 500))

Where:

In-Phase & Out-Phase Components are derived from a detrended version of the price series.

Instantaneous Frequency measures the rate of cycle change, allowing the CCI period to adjust dynamically.

The result is bounded within a user-defined min/max range, ensuring stability.

👽 How Traders Can Use This Indicator

👾 Divergence Trading Strategy

Bullish Divergence Setup:

Price makes a lower low, while CCI forms a higher low.

Buy signal is confirmed when CCI shows upward momentum.

Bearish Divergence Setup:

Price makes a higher high, while CCI forms a lower high.

Sell signal is confirmed when CCI shows downward momentum.

👾 Trailing Stop & Signal-Based Trading

Bullish Setup:

✅ CCI crosses above -100 → Buy signal.

✅ A bullish trailing stop is placed at Low - (ATR × Multiplier).

✅ Exit if the price crosses below the stop.

Bearish Setup:

✅ CCI crosses below 100 → Sell signal.

✅ A bearish trailing stop is placed at High + (ATR × Multiplier).

✅ Exit if the price crosses above the stop.

👽 Why It’s Useful for Traders

Hilbert Adaptive Period Calculation – No more fixed-length periods; the indicator dynamically adapts to market conditions.

Real-Time Divergence Alerts – Helps traders anticipate market reversals before they occur.

ATR-Based Risk Management – Stops automatically adjust based on volatility.

Works Across Multiple Markets & Timeframes – Ideal for stocks, forex, crypto, and futures.

👽 Indicator Settings

Min & Max CCI Period – Defines the adaptive range for Hilbert-based lookback.

Smoothing Factor – Controls the degree of smoothing applied to CCI.

Enable Divergence Analysis – Toggles real-time divergence detection.

Lookback Period – Defines the number of bars for detecting pivot points.

Enable Crosses Signals – Turns on CCI crossover-based trade signals.

ATR Multiplier – Adjusts trailing stop sensitivity.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

MACD & Bollinger Bands Overbought OversoldMACD & Bollinger Bands Reversal Detector

This indicator combines the power of MACD divergence analysis with Bollinger Bands to help traders identify potential reversal points in the market.

Key Features:

MACD Calculation & Divergence:

The script calculates the standard MACD components (MACD line, Signal line, and Histogram) using configurable fast, slow, and signal lengths. It includes a simplified divergence detection mechanism that flags potential bearish divergence—when the price makes a new swing high but the MACD fails to confirm the move. This divergence can serve as an early warning that the bullish momentum is waning.

Bollinger Bands:

A 20-period simple moving average (SMA) is used as the basis, with upper and lower bands drawn at 2 standard deviations. These bands help visualize overbought and oversold conditions. For example, a close at or above the upper band suggests the market may be overextended (overbought), while a close at or below the lower band may indicate oversold conditions.

Visual Alerts:

The indicator plots the Bollinger Bands on the chart along with labels marking overbought and oversold conditions. Additionally, it marks potential bearish divergence with a downward triangle, providing a quick visual cue to traders.

Usage Suggestions:

Confluence with Other Signals:

Use the divergence signals and Bollinger Band conditions as filters. For example, even if another indicator suggests a long entry, you might avoid it if the price is overbought or if MACD divergence warns of weakening momentum.

Customization:

All key parameters, such as the MACD lengths, Bollinger Band period, and multiplier, are fully configurable. This flexibility allows you to adjust the indicator to suit different markets or trading styles.

Disclaimer:

This script is provided for educational purposes only. Always perform your own analysis and backtesting before trading with live capital.

9-20 EMA Crossover with TP and SL9-20 EMA Crossover: This script tracks the crossover of the 9-period EMA and the 20-period EMA.

When the 9 EMA crosses above the 20 EMA, a buy signal is triggered.

When the 9 EMA crosses below the 20 EMA, a sell signal is triggered.

Take Profit and Stop Loss Levels:

The take profit for a long position is set at 3% above the entry price (close * 1.03).

The stop loss for a long position is set at 1% below the entry price (close * 0.99).

The take profit for a short position is set at 3% below the entry price (close * 0.97).

The stop loss for a short position is set at 1% above the entry price (close * 1.01).

Leverage: The strategy uses 20x leverage for both long and short positions (leverage=20).

Alerts: Alerts are set up for the buy signal when the 9 EMA crosses above the 20 EMA and the sell signal when the 9 EMA crosses below the 20 EMA. These alerts can be used with a webhook to trigger trades on Binance Futures.

Strategy:

For long trades: The strategy enters a long position and sets a take profit at 3% above the entry price and a stop loss at 1% below the entry price.

For short trades: The strategy enters a short position and sets a take profit at 3% below the entry price and a stop loss at 1% above the entry price.

Adaptive Volatility-Scaled Oscillator [AVSO] (Zeiierman)█ Overview

The Adaptive Volatility-Scaled Oscillator (AVSO) is a dynamic trading indicator that measures and visualizes volatility-adjusted market behavior. By scaling various metrics (such as volume, price changes, standard deviation, ATR, and Yang-Zhang volatility) and applying adaptive smoothing, AVSO helps traders identify market conditions where volatility deviates significantly from the norm.

This indicator uses standardized scaling (Z-Score logic) to highlight periods of abnormally high or low volatility relative to recent history. With gradient coloring and clear volatility zones, AVSO provides a visually intuitive way to analyze market volatility and adapt trading strategies accordingly.

█ How It Works

⚪ Scaling Metrics: The indicator scales user-selected metrics (e.g., volume, ATR, standard deviation) relative to the market and price, providing a standardized volatility measure.

⚪ Z-Score Standardization: The scaled metric is normalized using a Z-Score to measure how far current volatility deviates from its recent mean.

Positive Z-Score: Above-average volatility.

Negative Z-Score: Below-average volatility.

⚪ Adaptive Smoothing: An Adaptive EMA smooths the Z-Score, dynamically adjusting its length based on the strength of the volatility. Stronger deviations result in shorter smoothing, increasing responsiveness.

█ Unique Feature: Yang-Zhang Volatility

The Yang-Zhang volatility estimator sets this indicator apart by providing a more robust and accurate measure of volatility compared to traditional methods like ATR or standard deviation.

⚪ What Makes Yang-Zhang Volatility Unique?

Comprehensive Calculation: It combines overnight price gaps (log returns from the previous close to the current open) and intraday price movements (high, low, and close).

Accurate for Gapped Markets: Traditional volatility measures can misrepresent price movement when significant gaps occur between sessions. Yang-Zhang accounts for these gaps, making it highly reliable for assets prone to overnight price jumps, such as stocks, cryptocurrencies, and futures.

Adaptable to Real Market Conditions : By including both close-to-open returns and intraday volatility, it provides a balanced and adaptive measure that captures the full volatility picture.

⚪ Why This Matters to Traders

Better Volatility Insights: Yang-Zhang offers a clearer view of true market volatility, especially in markets with price gaps or uneven trading sessions.

Improved Trade Timing: By identifying volatility spikes and calm periods more effectively, traders can time their entries and exits with greater confidence.

█ How to Use

Identify High and Low Volatility

A high Z-Score (>2) indicates significant market volatility. This can signal momentum-driven moves, breakouts, or areas of increased risk.

A low Z-Score (<-2) suggests low volatility or a calm market environment. This often occurs before a potential breakout or reversal.

Trade Signals

High Volatility Zones (background highlight): Monitor for potential breakouts, trend continuations, or reversals.

Low Volatility Zones: Anticipate range-bound conditions or upcoming volatility spikes.

█ Settings

Source: Select the price source for scaling calculations (close, high, low, open).

Metric Measure: Choose the volatility measure:

Volume: Scales raw volume.

Close: Uses closing price changes.

Standard Deviation: Price dispersion.

ATR: Average True Range.

Yang: Yang-Zhang volatility estimate.

Bars to Analyze: Number of historical bars used to calculate the mean and standard deviation of the scaled metric.

ATR / Standard Deviation Period: Lookback period for ATR or Standard Deviation calculation.

Yang Volatility Period: Period for the Yang-Zhang volatility estimator.

Smoothing Period: Base smoothing length for the adaptive smoothing line.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Enhanced Market Influence DashboardDescription

The "Enhanced Market Influence Dashboard" (EMID) is a sophisticated trading indicator developed in Pine Script, designed to provide traders with a comprehensive view of the market's influences by analyzing a diverse set of financial instruments. This script integrates various market data, calculates dynamic weights based on volatility, and combines them into a composite score to help traders identify significant market movements.

Concept and Methodology

The EMID indicator aggregates data from multiple financial instruments, including forex pairs, commodities, indices, and ETFs. By calculating the median and volatility of these instruments over user-defined timelines, it dynamically adjusts their weights to reflect current market conditions. The composite score generated from these weighted values helps traders understand the overall market influence and detect significant movements.

Key Features

Market Data Integration: The script fetches real-time data from various symbols such as USD/JPY, Gold, Dollar Index (DXY), US Treasury Rate, VIX Index, Crude Oil, EUR/USD, Emerging Market Index, QYLD ETF, and Nasdaq 100 Futures.

1. Dynamic Weight Calculation: The script calculates dynamic weights for each instrument based on their volatility relative to their simple moving average. This approach ensures that more volatile instruments have a proportionally higher impact on the composite score.

2. Median and Volatility Analysis: It uses the median value and standard deviation over specified timelines to gauge the central tendency and volatility of each instrument.

3. Composite Score Generation: By normalizing the difference between current prices and their respective medians, and applying dynamic weights, the script generates a composite score that reflects the overall market sentiment.

4. Baseline Calculation: A dynamic baseline is computed as the median of the composite score over the lookback period, providing a reference point for identifying significant deviations.

5. Alerts: The script includes alert conditions to notify traders of significant market movements, either above or below the baseline by a threshold value.

Usage

To use the EMID indicator, follow these steps:

1. Input Configuration: Adjust the input parameters to suit your trading strategy. The key inputs include:

-Median Timeline: The period for calculating the median values.

-Volatility Timeline: The period for calculating volatility.

-Base Weights: Set the base weights for each financial instrument according to their perceived influence on the market.

-Adding the Indicator: Apply the EMID indicator to your chart in TradingView. Ensure that the symbols used in the script are relevant to your trading strategy and available in your TradingView subscription.

2. Interpreting the Composite Score: The composite score plotted on the chart gives an aggregated view of market influences. Compare the composite score with the baseline to identify significant market movements.

-A composite score significantly above the baseline indicates a potential market uptrend.

-A composite score significantly below the baseline indicates a potential market downtrend.

-Setting Alerts: Use the alert conditions to set up notifications for significant market movements. These alerts help you stay informed about critical changes in market sentiment.

Underlying Calculations

1. Median Calculation: The median function is applied to each instrument's price data over the specified timeline.

2. Volatility Calculation: Volatility is calculated as the standard deviation divided by the simple moving average over the volatility timeline.

3. Dynamic Weight Application: Base weights are multiplied by the respective volatility values to get dynamic weights.

4. Normalized Scores: The script normalizes the difference between current prices and their medians, then multiplies by the dynamic weights to get individual scores.

5. Composite Score: Summing all normalized and weighted scores results in the composite score.

6. Baseline: The baseline is the median of the composite score over the median timeline.

By integrating multiple market influences and dynamically adjusting weights based on volatility, the EMID indicator provides a robust tool for traders to analyze market conditions and make informed trading decisions.

HT: Weekly LevelsIndicator draws several most important weekly levels on the lower timeframe: last week high/low, halfback, week close and current week open. These levels often act as support/resistance for price movements. Also, they can help to assess week character and control of power.

Indicator can be used on any timeframe, lower than weekly, for any type of instrument, including futures. It also provides an option to draw levels for any selected week back in time.

Important notes:

• Levels for the last week are drawn after the new week opens.

• Half-back is calculated as a middle line between week High and Low.

Parameters:

Date – user can select date, belonging to week, for which levels will be plotted. Works only if “Use” check box is on. Otherwise, levels will be plotted for the last week. (“time” value doesn’t matter; unfortunately, there is no way to hide the input box)

Time zone – your chart time zone (as UTC offset). Only needed if you use “Date” parameter.

Visuals – controls visibility and colors

Script is published as an open source. It uses two libraries: Levels Lib and Functions Lib. First one demonstrates how to work with pine-script object model and arrays. You can also reuse it in your custom scripts where there is need to construct any support/resistance levels. The second library contains some useful functions for working with time and dates.

Disclaimer

This indicator should not be used as a standalone tool to make trading decisions but only in conjunction with other technical analysis methods.

Gabriels Trend Regularity Adaptive Moving Average Dragon This is an improved version of the trend following Williams Alligator, through the use of five Trend Regularity Adaptive Moving Averages (TRAMA) instead of three smoothed averages (SMMA). This indicator can double as a TRAMA Ribbon indicator by reducing the offset to zero. Whereas the active offset can double as a forecasting indicator for options and futures.

This indicator uses five TRAMAs, set at 8, 21, 55, 144, and 233 periods. They make up the Lips, Teeth, Jaws, Wings, and Tail of the Dragon. This indicator uses convergence-divergence relationships to build trading signals, with the Tail making the slowest turns and the Lips making the fastest turns. The Lips crossing downwards through the other lines signal a short opportunity, whereas Lips crossing upwards through other lines signal a buying opportunity. The downward cross can be referred to as the Dragon "Sleeping" , and the upward cross as the Dragon "Awakening" .

In particular, but not limited to, the Wings and Tail movements possess a Roar-like forecast effect on the market. Respectively, they can be referred to as the Dragon "Spreading its Wings" or "Swinging its Tail" .

The first three lines, stretching apart and constantly moving higher or lower, denote periods in which long or short equity positions should be managed and maintained. This can be referred to as the Dragon "Eating with a mouth wide open" . Whereas indicator lines converging into narrow bands and shifting into a horizontal position can denote a trending period coming to an end, signaling the need for profit-taking and position realignment. Conversely, a previous flat line moving can denote a new trending period starting.

This indicator can double as a Multiple TRAMAs indicator by reducing the offset to zero. As such, very interesting results can be observed when used in a moving average crossover system such as the Williams Alligator or as trailing support and resistance.

The following moving average adapts to the average of the highest high and lowest low made over a specific period, thus adapting to trend strength. The TRAMA can be used like most moving averages, with the advantage of being smoother during ranging markets because it is calculated through exponential averaging.

It is calculating, using a smoothing factor, the squared simple moving average of the number of highest highs or lowest lows previously made. Where the highest highs and lowest lows are calculated using rolling maximums and minimums. Therefore, squaring allows the moving average to penalize lower values, thus appearing stationary during ranging markets.

As with all moving averages, it is still a lagging indicator, and it can suffer whipsaws when the market moves too violently or when it consolidates in ranging conditions. Despite it working in all timeframes, it won't be as formidable in the 1–5-minute scalping timeframes due to that. I would suggest 5 to 45 minutes if you are a swing trader, or hourly, daily, and weekly if you are a long-term investor.

I hope you enjoy this indicator! It's the first indicator I made, so constructive criticism would be appreciated. Thanks!

Crypto Candlestick Patterns - CN VersionIntroduction:

The candlestick chart has been used for centuries since the Japanese applications. Based on the candlestick charting, people developed candle pattern analysis. Now we have tons of books or articles illustrating the usage of reversal patterns and continuation patterns, and computers provide a faster and preciser way to recognize these pattern.

Originally we have a common *All Candlestick Patterns* indicator to use. This indicator works well for most of the markets or commodities including stocks and futures. However, for cryptocurrency market, quite a few patterns are not suitable anymore. For example, crypto markets are continuously running 7x24hrs and the big coins with good volume tend to have almost continuous price in commonly used time periods. Hence, original patterns with "window" or "jump" concepts are usually not applied to crypto.

For these issues, I modified the original *All Candlestick Patterns* indicator and introduced the Chinese version for people speaking such language.

Like most of the other indicators, I personally do not recommend anyone to simply follow the patterns it shows to enter the market. You may take these recognized patterns as a reference, and further actions on trading should be done with several other tools, such as MACD, RSI, Stochastic and etc.

Usage:

The application of this indicator is basically the same as the original *All Candlestick Patterns* and you will get an automatically generated pattern recognition by your computer system.

There are a few parameters to adjust for the indicator:

Trending Detection Settings: Here you can choose SMA-Fast, SMA-Fast/Slow or None detecting options to recognize the current market trend. This is a minor improvement from the original indicator and you can choose your preferred trending detecting settings by changing the length of SMA.

Candlestick Settings: You may adjust the rules to recognize the properties of candlesticks. I add a "perturbation" parameter here, which actually is an error tolerance for pattern recognition. Some seemingly pattern may not fulfill the strict rules of classic candlestick patterns, but we may recognize them by watch the charting on our own. Hence this error tolerance may show more potential patterns from the charting.

Plot Settings: It is the usually colour choice and providing options for bullish/bearish.

Pattern Settings: Here you can select the patterns that you would like to see from the charting. You can pick the preferred reversal patterns or choose to show all the patterns. It's all up to you!

Features:

Language Translation: Since this is a Chinese language version. I have replaced all the English explanation of patterns to Chinese ones. Move your mouse to the label, you will find a brief intro of the pattern and a notice about bullish or bearish signals it indicates.

Alerts: As the same as the original one, we will have the alert options from this indicator. All the alerts and their messages are Chinese. You can activate alerts based on this indicator from the alert management section, as the same as many other indicators you have used before.

Future Improvements:

For now I am satisfied with the work I have done, and I may apply it to several charts. It's welcome for any users to take a look at the codes and put modifications or improvements towards it. Currently most of the comments in the code are in Chinese language, since basically it's for Chinese speaking users, while the code itself and the parameter names should be pretty easy to understand in English. (I have been using English for writing in the past 8 years, hence this introduction is in English as well.)

Monthly Performance Table by Dr. MauryaWhat is this ?

This Strategy script is not aim to produce strategy results but It aim to produce monthly PnL performance Calendar table which is useful for TradingView community to generate a monthly performance table for Own strategy.

So make sure to read the disclaimer below.

Why it is required to publish?:

I am not satisfied with the monthly performance available on TV community script. Sometimes it is very lengthy in code and sometimes it showing the wrong PNL for current month.

So I have decided to develop new Monthly performance or return in value as well as in percentage with highly flexible to adjust row automatically.

Features :

Accuracy increased for current month PnL.

There are 14 columns and automatically adjusted rows according to available trade years/month.

First Column reflect the YEAR, from second column to 13 column reflect the month and 14 column reflect the yearly PnL.

In tabulated data reflects the monthly PnL (value and (%)) in month column and Yearly PnL (value and (%)) in Yearly column.

Various color input also added to change the table look like background color, text color, heading text color, border color.

In tabulated data, background color turn green for profit and red for loss.

Copy from line 54 to last line as it is in your strategy script.

Credit: This code is modified and top up of the open-source code originally written by QuantNomad. Thanks for their contribution towards to give base and lead to other developers. I have changed the way of determining past PnL to array form and keep separated current month and year PnL from array. Which avoid the false pnl in current month.

Strategy description:

As in first line I said This strategy is aim to provide monthly performance table not focused on the strategy. But it is necessary to explain strategy which I have used here. Strategy is simply based on ADX available on TV community script. Long entry is based on when the difference between DIPlus and ADX is reached on certain value (Set value in Long difference in Input Tab) while Short entry is based on when the difference between DIMinus and ADX is reached on certain value (Set value in Short difference in Input Tab).

Default Strategy Properties used on chart(Important)

This script backtest is done on 1 hour timeframe of NSE:Reliance Inds Future cahrt, using the following backtesting properties:

Balance (default): 500 000 (default base currency)

Order Size: 1 contract

Comission: 20 INR per Order

Slippage: 5 tick

Default setting in Input tab

Len (ADX length) : 14

Th (ADX Threshhold): 20

Long Difference (DIPlus - ADX) = 5

Short Difference (DIMinus - ADX) = 5

We use these properties to ensure a realistic preview of the backtesting system, do note that default properties can be different for various reasons described below:

Order Size: 1 contract by default, this is to allow the strategy to run properly on most instruments such as futures.

Comission: Comission can vary depending on the market and instrument, there is no default value that might return realistic results.

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from the strategies built are realistic.

Disclaimer:

This script not provide indicative of any future results.

This script don’t provide any financial advice.

This strategy is only for the readymade snippet code for monthly PnL performance calender table for any own strategy.

Spongebob [TFO]This Spongebob indicator is an experiment with the newly released polyline drawing features in Pine Script. As someone that enjoys a challenge, I thought of a complex subject to draw with polylines, and Spongebob was one of the first things that came to mind due to his wavy body shape. Although, other features like the shoulders, shoes, and hands proved to be much more difficult than the body shape itself.

With this indicator enabled, Spongebob will be automatically be drawn on the last confirmed bar of the current chart, and should mostly auto-fit to any symbol's price axis through use of the Average True Range (ATR) function. ATR allows us to get the average range of the most recent bars (in this case I used 50 bars). I used this as a base value from which to scale and determine various heights of each body shape, like the radius of the eyes, the length of the pants, etc. - that way, it would scale to any price axis, from forex to index futures.

Attached is a picture of the indicator (left) compared to my subject reference (right). I'm honestly surprised at how well it came out, and how intuitive it was to form the majority of my shapes using polylines. I'm really happy with how this project turned out, and may have to attempt more drawings in the future!

REMA CROSSOVER BY JUGNUThis indicator triggers alerts for long and short positions on DAILY TIME FRAME for SWING trades based on the conditions which described below. This script will generate alerts when the following conditions are met:

LONG POSITION:

RSI(14) above 50.

EMA(5) crosses above EMA(10).

Indicator Triangle Green below price bars

SHORT POSITION:

RSI(14) below 50.

EMA(5) crosses down EMA(10).

Indicator Triangle RED above price bars

This script plots green and red triangles below and above the price bars to indicate long and short alert conditions, respectively. It also triggers alerts when these conditions are met.

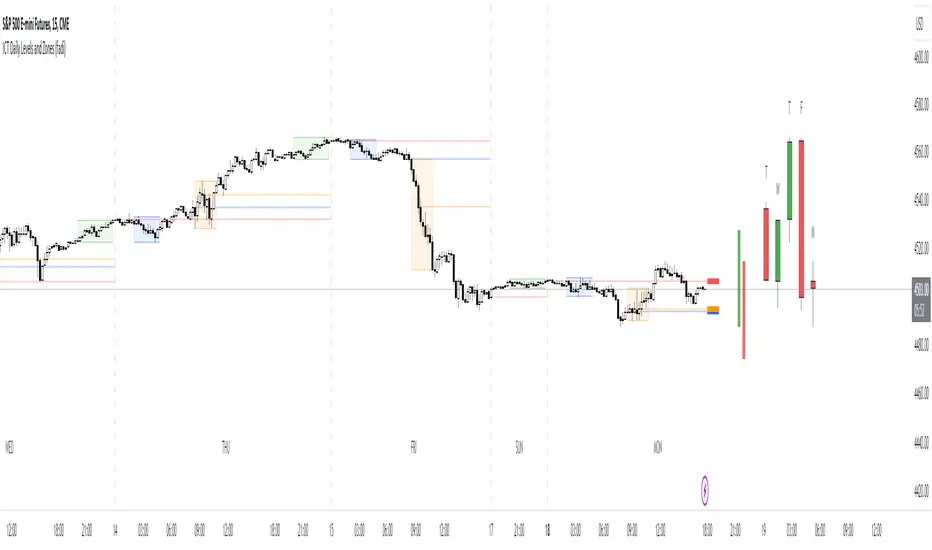

ICT Daily Levels and Zones (fadi)ICT Daily Levels and Zones indicator provides some of the relevant zones and levels for ICT type analysis. The purpose of this indicator is to provide consolidated way of automatically highlighting and identifying relevant levels for ICT type traders.

Daily Separator and Day of Week

Display a separator based on NY Midnight and day of week.

Killzones

Highlight ICT Asia, London, and NY killzones. Please note that the default times are based on Index Futures. Update the times of day if you plan on using it for other instruments such as Forex.

Open Range

The 9:30am to 10:00am open range

(Shown with Extend setting on)

Open Range Gap

The open range Gap is the difference between the 4:15pm close and the 9:30am open.

(Shown with Extend setting on)

Time of Day Levels

The Midnight, 8:30am, and 9:30am open levels.

Daily Midnight Candle

ICT style Daily candle formation based on Midnight open

BB_MDL_V1Simple indicator that is based on the average line of the bollinger bands and the exponential average of 200 periods.

The customizable variable is bollinger bands length, currently the default is 35, you can tweak it to your liking and see how trend identification changes.

My recommendation is to work in 5-minute time frames in values such as SOL, FTM or MASK (cryptos)

This simple strategy can be combined with many others to gain more insight and get better market entries and exits.

3Commas Bot DCA Backtester & Signals FREEThis is a DCA Strategy backtester + signals, built to emulate the 3Commas DCA bots. It uses your choice of 4 different buy signals, 2 of which can be adjusted in the settings. Everything is customizable so you can backtest specific settings with different buy signals and find the best performing strategy for your risk tolerance and capital. It can be used to backtest strategies on stocks as well, but just make sure your base order is larger than the share price for the entire backtesting range or it will not calculate properly.

You can use this template to code your own buy signals and then backtest them as a DCA strategy if you know some basic pine script.

The indicator shows all of your backtesting orders on the chart. The red line is your take profit level, the blue line is your average price level, the white line is your first order and the green lines are your average down orders. If you enable a stop loss in the settings your stop loss will be shown as an orange line once all of your average down orders have been hit, it will not be set until price has dipped below your covered trading range.

These levels update when things change during backtesting so you can visualize your strategy and how it would perform as well as see if your percentage deviation is large enough to cover dips. When backtesting trades are taken, the chart will show where they were taken(in backtesting) along with info on those trades such as the number each order is, the size of that order and the percentage deviation that order is from the initial buy.

SENDING SIGNALS TO 3COMMAS

Tradingview cannot sync this backtester to 3Commas and with the way alerts are setup for strategies on Tradingview, the best option for you to give signals to your bot would be to use this backtester to figure out what trigger you want to use and then setup that indicator separately to send alerts to your bot. All of the indicators used for signals in this backtester are available for free and can be configured to match this backtester and send alerts to 3Commas for you. Just make sure you set your alerts to once per bar close and don’t use less than a 15 second timeframe because then you could trigger the Tradingview threshold for alerts and get your alerts shut off.

You can also use this backtester with your own buy triggers if you know a little pine script. Just make copy of the script and code in your own buy signals and see how it backtests.

INFO PANEL FOR ANALYZING YOUR STRATEGY

The right hand side of the screen will show an info panel that shows a lot of different information so you can quickly see your bot settings and how it performed right on the screen.

In the top right corner you will see in purple your bot settings. These include your stoploss % if turned on, take profit %, average down order %, average down order % multiplier, volume multiplier, max number of orders allowed and size of your base order.

The top section of the first column “Current Trade” shows these stats: the open trade’s average price, the open trade’s take profit price, the open trade’s PNL, how far price is from your open tarde’s take profit level in percentage, your open position size and number of open orders.

The bottom section of the first column “Overall Performance” shows these stats: total number of trades taken during backtesting range, the largest amount of trades that were open at one time during backtesting, the max drawdown, the average number of bars per trade, gross profit, net profit, percent profit from your initial capital, current portfolio value and your initial capital.

CUSTOMIZABLE OPTIONS TO FIND THE PERFECT STRATEGY

Stoploss On/Off

This will turn your stoploss on or off. By default it is set to off and will not affect anything unless turned on.

Stoploss Percentage

This is the percentage below your final average down order price that will be set as a stoploss to keep your account from going too far in the red on big dips.

Take Profit Percentage - This is the percentage of profit you want the trade to hit before taking profit on your entire DCA trade. This level updates everytime you average down.

Average Down Percentage - This is the percentage that price has to drop from your initial order to initiate your first safety order. If the Average Down Percent Multiplier is set to 1 then this percentage will be the same for every average down order.

Average Down Percentage Multiplier - This multiplies your Average Down Percentage so each safety order needs a larger percentage deviation than the previous one. This keeps your buys closer together at the beginning and further apart when you hit more orders so you can extend your trading range but still be aggressive when price is going sideways.

Volume Multiplier Per New Order - This multiplies the size of each trade based on your base order. If you set it to a 2x multiplier then each average down order will be 2 times the size of the last one. So for example, a $100 base order with a 2x multiplier would have these values for the first 3 average down orders: 200, 400, 800.

Size Of Base Order - This is the size of your first position entry and will be used as a starting point for the volume multiplier. If your base order is $100 then it will buy $100 worth of whatever crypto you are backtesting this on. If you are looking at stock charts, you need to make sure your base order is higher than the share price across the entire backtesting range or it will not perform correctly.

Max Number Of Orders - This is the maximum number of orders the bot can take, including your base order. Adjust this to suit the amount of capital you are willing to allocate to your bot based on how much money it will require to run according to your bot settings.

TIPS ON HOW TO USE FOR BEST RESULTS

If you don’t have a lot of capital to work with, then use longer timeframes with a reasonable take profit percentage so that you don’t need a lot of average down orders. You can also try keeping the volume multiplier close to 1.

You can use the 3Commas dca bot settings page to see how much capital you will need for your strategy if you match it to the settings you have on this indicator. You can also check to see how much of a percentage deviation your bot is covering to make sure you have a reasonable range to trade in and orders to cover big dips. You can also check your coverage by seeing how far down the chart the green lines cover, which are your average down orders.

Make sure the initial capital in the properties tab of the settings has enough to cover all of your orders otherwise you will get unrealistic backtesting results. Also, make sure you leave the order size in the properties tab on contracts so it calculates your trades correctly. The only settings you need to touch in the properties tab is the initial capital. Unless you are trading somewhere that has lower commission fees, then you can change that to match, but leave all the other settings as is for it to function properly.

Increasing the volume multiplier will make your average price and take profit target follow the price action a lot closer as price falls, but it can also lead to having very large orders very quickly once you get into the 1.5-3x multiple range. Try using a high volume multiplier with less safety orders and you will get better results, however you need to have money on the sidelines to add on major dips to keep your bot turning a profit. Be very careful with this as greed and impatience will hurt your overall performance. This bot is meant to make money with lots of small wins so don’t get greedy and make sure you have enough money to cover large dips. If you are being aggressive with your bot, then I recommend only using 25% or less of your portfolio to trade aggressively and then use the smart trade feature on 3commas to add chunks of funds to your trades when price dips below your last safety order. Or if you want it to run without any supervision, then use lower volume multipliers and have lots of safety orders that can cover entire bear markets and still keep buying lower.

It’s a good idea to have some capital on the sidelines that you can add in when price dips quickly. This will help lower your average price and allow your bot to get out in profit quicker. 3Commas bot has a smart trade feature that will allow you to track your average price when adding extra funds and it will automatically update your other orders which is very convenient. Look at the longer timeframes when price dips and only add chunks at major areas where price is very likely to bounce. Or you can be aggressive when trading and add to your position when price dips and is at a likely bounce zone to maximize profits.

Only trade coins that have a good amount of liquidity as the larger your orders get, the harder it will be to sell if there isn’t much liquidity. Also, beware of how large your first order is as it will usually be a market order and can move the market if there is not much liquidity.

Since this bot takes a lot of trades and performs best when taking small profits consistently, you will need to factor in exchange fees. The bot is set to .5% commission(you can change this) on the buy and sell orders as most exchanges charge that amount. Some exchanges offer no fee trading on certain coins so be sure to look around for those so you can keep the commissions and maximize profits.

I strongly encourage you to try out a lot of different setting combinations across multiple different coins and do it across a few months to see how it would have performed under various market conditions. This will help you get a better idea of how much of a percentage deviation you’ll need to be able to cover to keep your bot running and making constant profits. You can also use the deep backtesting feature of the strategy panel to see how it would have done, but just beware that the info panel of the indicator will not reflect deep backtesting results, only the normal backtesting range.

MARKETS

This backtester can be used on any market including crypto, stocks, forex & futures. You just need to make sure your base order is larger than the share price when using this on things besides crypto.

TIMEFRAMES

This backtester can be used on all timeframes.

Daily/Weekly ExtremesBACKGROUND

This indicator calculates the daily and weekly +-1 standard deviation of the S&P 500 based on 2 methodologies:

1. VIX - Using the market's expectation of forward volatility, one can calculate the daily expectation by dividing the VIX by the square root of 252 (the number of trading days in a year) - also know as the "rule of 16." Similarly, dividing by the square root of 50 will give you the weekly expected range based on the VIX.

2. ATR - We also provide expected weekly and daily ranges based on 5 day/week ATR.

HOW TO USE

- This indicator only has 1 option in the settings: choosing the ATR (default) or the VIX to plot the +-1 standard deviation range.

- This indicator WILL ONLY display these ranges if you are looking at the SPX or ES futures. The ranges will not be displayed if you are looking at any other symbols

- The boundaries displayed on the chart should not be used on their own as bounce/reject levels. They are simply to provide a frame of reference as to where price is trading with respect to the market's implied expectations. It can be used as an indicator to look for signs of reversals on the tape.

- Daily and Weekly extremes are plotted on all time frames (even on lower time frames).

WSTF RSI2 IndicatorThis is the Indicator replicating the basic RSI(2) created by Wilders.

Buy condition:

(RSI(2) crossed under 10) & (close > EMA(200)) & (EMA(5) > close)

Sell condition:

(RSI(2) crossed over 90) & (close < EMA(200)) & (EMA(5) < close)

You can play around with the script by adjusting the RSI Values, EMA values and crossover & crossunder threshold.

We will update the script with new features in the futures.

Please don't hesitate to share some Ideas or Feedbacks, we would be happy to improve the script for you !

Have fun !

WS TradingFactory

Future PreviewFuture Preview

Calculate real-time future order profit with open price, leverage and commission fee. Simple and straight forward. If you need any additional feature, please leave a comment below. I am glad to help.

Usage:

When adding Future Preview to chart, it will ask order open time and open price on the chart by clicking with left mouse on the desired value. These value can be changed lately, as well as the leverage and commission fee. Default leverage is 10 and default commission fee is 0.06% (taker).

There will be two horizontal lines. The solid longer line is the open price line, it shows the order open price. The shorter line moving with real-time price is the current price line, it shows the current price. There will be preview data shows on top or below the price line. Open price line is red for short order and green for long order. The current price line is red when the order is losing and it is green when it profiting. The back ground color follows the color of current price line. Background color transparency and gain/loss color can be changed in options.

There will be one horizontal line on the left if the option of showing open time is on (default is on). It shows the time stamp when current order opened.

After adding Future Preview to chart, there is option to add Taking Profit(TP) or Stop Loss(SL) to the chart.

Font size can be changed in option

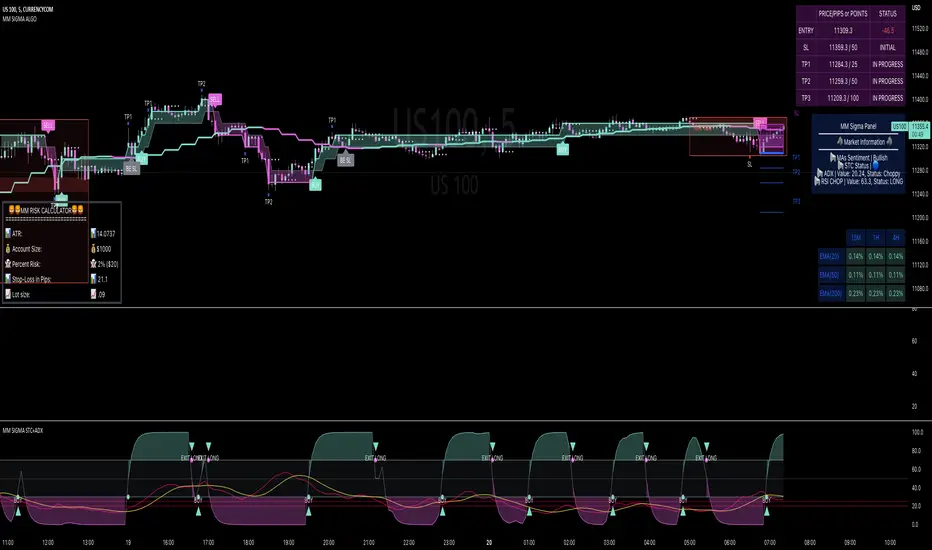

MM SIGMA STC+ADXThe Schaff Trend Cycle (STC) is a charting indicator that is commonly used to identify market trends and provide buy and sell signals to traders. Developed in 1999 by noted currency trader Doug Schaff, STC is a type of oscillator and is based on the assumption that, regardless of time frame, currency trends accelerate and decelerate in cyclical patterns.12

How STC Works

Many traders are familiar with the moving average convergence/divergence (MACD) charting tool, which is an indicator that is used to forecast price action and is notorious for lagging due to its slow responsive signal line . By contrast, STC’s signal line enables it to detect trends sooner. In fact, it typically identifies up and downtrends long before MACD indicator.

While STC is computed using the same exponential moving averages as MACD, it adds a novel cycle component to improve accuracy and reliability. While MACD is simply computed using a series of moving average, the cycle aspect of STC is based on time (e.g., number of days).

It should also be noted that, although STC was developed primarily for fast currency markets, it may be effectively employed across all markets, just like MACD. It can be applied to intraday charts, such as five minutes or one-hour charts, as well as daily, weekly, or monthly time frames.

Introduction to ADX

ADX is used to quantify trend strength. ADX calculations are based on a moving average of price range expansion over a given period of time. The default setting is 14 bars, although other time periods can be used.1 ADX can be used on any trading vehicle such as stocks, mutual funds, exchange-traded funds and futures.

ADX is plotted as a single line with values ranging from a low of zero to a high of 100. ADX is non-directional; it registers trend strength whether price is trending up or down.2 The indicator is usually plotted in the same window as the two directional movement indicator (DMI) lines, from which ADX is derived (shown below).Quantifying Trend Strength

ADX values help traders identify the strongest and most profitable trends to trade. The values are also important for distinguishing between trending and non-trending conditions. Many traders will use ADX readings above 25 to suggest that the trend is strong enough for trend-trading strategies. Conversely, when ADX is below 25, many will avoid trend-trading strategies.

ADX Value Trend Strength

0-25 Absent or Weak Trend

25-50 Strong Trend

50-75 Very Strong Trend

75-100 Extremely Strong Trend

Low ADX is usually a sign of accumulation or distribution. When ADX is below 25 for more than 30 bars, price enters range conditions, and price patterns are often easier to identify. Price then moves up and down between resistance and support to find selling and buying interest, respectively. From low ADX conditions, price will eventually break out into a trend. Below, the price moves from a low ADX price channel to an uptrend with strong ADX.

Added Buy/Sell alerts

ADX filters based on the threshold you put in the settings.

great for trend and trade confirmation

Cipher B divergencies for Crypto (Finandy support)Hello Traders!

In times of high volatility, it is important to follow a market-neutral strategy to protect your hard-earned assets. The simple script employs common buy/sell and/or divergencies signals from the VuManChu Cipher B indicator with fixed stop losses and takes profits. The signals are filtered by a local trend of a coin of interest and the global trend of Bitcoin. These trends-filtered signals demonstrated better performance on most of the back- and forward- tests for USDT cryptocurrency futures. The strategy is based on my real experience, it's a diamond I want to share with you.

In terms of visualization if the background is red and the price is below the yellow line then only a short position can be opened. Conversely, if the price is above the yellow line AND the background is green only a long position can be opened.

Inputs from VuManChu you can find on the top. Frankly, I do not know how they can help you to improve the performance of the strategy. My inputs of the script you can find in "Trend Settings" and "TP/SL Settings" at the bottom.

The checkbox "Only divergencies" lets to broadcast only more reliable buy/sell signals for a cost of rare deals.

The checkbox "Cancel all positions if price crosses local sma?" makes additional trailing stop loss. Usually, this function increases the win rate by "smoothing" the risk/reward ratio, as a usual stop loss does.

You can tune SL/TP based on backtesting.

To connect the script to Finandy just edit "name" and "secret" to connect your webhook (see the bottom of the script).

The rule of thumb for the strategy is "only divergencies" - ON, high reward/risk (TP/SL) ratio, 5 min timeframe on chart help with performance.

Finally, I am looking forward to feedback from you. If you have some cool features for my script in your mind, do not hesitate to leave them in the comments.

Good luck!

SGX Nifty Movement During Indian Market HoursSGX Nifty or Singapore Nifty is a derivative contract of the Nifty 50 index which is the benchmark index of NSE in India. SGX Nifty trades for 21 hours in a day while Nifty 50 trades only for 6 hours and 15 minutes. Traders in India miss out on a lot of price action which happens on the Singapore Nifty. This code which is originally inspired from @Gustavorubi has been modified to track SGX Nifty's movements outside Indian market hours. This will help intraday traders to identify support and resistance levels which are not seen on Nifty 50 futures.

This source code is inspired from GustavoRubi's code on FX Sessions.