TCP | Money Management indicator | Crypto Version📌 TCP | Money Management Indicator | Crypto Version

A robust, multi-target risk and capital management indicator tailored for crypto traders. Whether you're trading spot, perpetual futures, or leverage tokens, this tool empowers you with precise control over risk, reward, and position sizing—directly on your chart. Eliminate guesswork and trade with confidence.

🔰 Introduction: Master Your Capital, Master Your Trades

Poor money management is the number one reason traders lose their accounts, even with solid strategies. The TCP Money Management Indicator, built by Trade City Pro (TCP), solves this problem by providing a structured, rule-based approach to capital allocation.

Want to dive deeper into the concept of money management? Check out our comprehensive tutorial on TradingView, " TradeCityPro Academy: Money Management ", to understand the principles that power this indicator and transform your trading mindset.

This indicator equips you to:

• Calculate optimal position sizes based on your capital, risk percentage, and leverage

• Set up to 5 customizable take-profit targets with partial close percentages

• Access real-time metrics like Risk-to-Reward (R/R), USD profit, and margin usage

• Trade with discipline, avoiding emotional or inconsistent decisions

💸 Money Management Formula

The indicator uses a professional capital allocation model:

Position Size = (Capital × Risk %) ÷ (Stop Loss % × Leverage)

From this, it calculates:

• Total risk amount in USD

• Optimal position size for your trade

• Margin required for each take-profit target

• Adjusted R/R for each target, accounting for partial position closures

🛠 How to Use

Enter Trade Parameters: Input your capital, risk %, leverage, entry price, and stop-loss price.

Set Take-Profit Targets: Enable 1 to 5 take-profit levels and specify the percentage of the position to close at each.

Real-Time Calculations: The indicator automatically computes:

• R/R ratio for each target

• Profit in USD for each partial close

• Margin used per target (in % and USD)

Visualize Your Trade:

• Price levels for entry, stop-loss, and take-profits are plotted on the chart.

• A dynamic info panel on the left side displays all key metrics.

🔄 Dynamic Adjustments: As each take-profit target is hit and a portion of the position is closed, the indicator recalculates the remaining position size, expected profit, R/R, and margin for subsequent targets. This ensures accuracy and reflects real-world trade behavior.

📊 Table Overview

The left-side panel provides a clear snapshot:

• Trade Setup: Capital, entry price, stop-loss, risk amount, and position size

• Per Target: Percentage closed, R/R, profit in USD, and margin used

• Summary: Total expected profit across all targets

⚙️ Settings Panel

• Total Capital ($): Your account size for the trade

• Risk per Trade (%): The percentage of capital you’re willing to risk

• Leverage: The leverage applied to the trade

• Entry/Stop-Loss Prices: Define your trade’s risk zone

• Take-Profit Targets (1–5): Set price levels and percentage to close at each

🔍 Use Case Example

Imagine you have $1,000 capital, risking 1%, using 10x leverage:

• Entry: $100 | Stop-Loss: $95

• TP1: $110 (close 50%) | TP2: $115 (close 50%)

The indicator calculates the exact position size, profit at each target, and margin allocation in real time, with all metrics displayed on the chart.

✅ Why Traders Love It

• Precision: No more manual calculations or guesswork

• Versatility: Works on all crypto pairs (BTC, ETH, altcoins, etc.)

• Flexibility: Perfect for scalping, swing trading, or futures strategies

• Universal: Compatible with all timeframes

• Transparency: Fully manual, with clear and reliable outputs

🧩 Built by Trade City Pro (TCP)

Developed by TCP, a trusted name in trading tools, used by over 150,000 traders worldwide. This indicator is coded in Pine Script v5, ensuring compatibility with TradingView’s platform.

🧾 Final Notes

• No Auto-Trading: This is a manual tool for disciplined traders

• No Repainting: All calculations are accurate and non-repainting

• Tested: Rigorously validated across major crypto pairs

• Publish-Ready: Built for seamless use on TradingView

🔗 Resources

• Money Management Tutorial: Learn the fundamentals of capital management with our detailed guide: TradeCityPro Academy: Money Management

• TradingView Profile: Explore more tools by TCP on TradingView

ابحث في النصوص البرمجية عن "Futures"

Adaptive ATR Limits█ OVERVIEW

This indicator plots adaptive ATR limits for intraday trading. A key feature of this indicator, which makes it different from other ATR limit indicators, is that the top and bottom ATR limit lines are always exactly one ATR apart from each other (in "auto" mode; there is also a "basic" mode, which plots the limits in the more traditional way—i.e., one ATR above the low and one ATR below the high at all times—and this can be used for comparison).

█ FEATURES

Provides an algorithm to plot the most reasonable intraday ATR top/bottom limits based on currently available information

Dynamically adapts limits as the price evolves during the day

Works correctly and consistently on both RTH and ETH charts

Has a user-selected ADR mode to base the limits on ADR instead of ATR

Option to include the current pre-market and previous day's post-market range in the calculation

Configurable ATR/ADR averaging length

Provides a visual smoothing option

Provides an information box showing the current numerical ATR/ADR values

Reasonable defaults that work well if the user changes nothing

Well-documented, high-quality, open-source code for those interested

█ HOW TO USE

At a minimum, there is nothing that needs to be set. The defaults work well. The ATR top line (red, configurable) gives you the most reasonable move given the currently available information. The line will move away from the price as the price approaches it; that is normal—it is reacting to new information. This happens until the ATR bottom limit hits the lower of the daily low and the previous day's close (in ATR mode). The ATR bottom line (green, configurable) works the same way, with reversed logic.

There is an option to use ADR instead of ATR. The ATR includes the previous day's RTH close in the range, whereas ADR does not. Another option allows the user to add the current day's pre-market range or the previous day's post-market into the current day's range, which has an effect if either of those went outside of today's RTH range, plus yesterday's RTH close (in the default ATR mode). Pre-market and post-market range is not typically included in the daily true range, so only change it if you really know you want it.

█ CONCEPTS

Most traditional ATR limit indicators plot the top ATR limit one ATR above the current daily low, and the bottom ATR limit one ATR below the current daily high. This indicator can also do that (in "basic" mode), but its value lies in its default "auto" mode, which uses an algorithm to dynamically adapt the ATR limits throughout the day, keeping them one ATR apart at all times. It tries to plot the most sensible ATR limits based on the current daily ATR, in order to provide a reasonable visual intraday target, given the available information at that point in time.

"Auto" mode is actually a weighted average of two methods: midpoint and relative (both of which can also be explicitly selected). The midpoint method places the midpoint of the ATR limit equal to the midpoint of the currently established daily range. The relative method measures the currently established daily range and calculates the position of the current price within it (as a ratio between 0 and 1). It then uses that value as a weight in a weighted average of extreme locations for the ATR limits, which are: the ATR top anchored to one ATR above the daily low, and the ATR bottom anchored to one ATR below the daily high.

The relative method is more advanced and better for most of the day; however, it can cause wild swings in the early market or pre-market before a reasonable range (as a percentage of ATR) has been established. "Auto" mode therefore takes another weighted average between the two methods, with the weight determined by the percentage of the ATR currently established within the day, more strongly weighting the calmer midpoint method before a good range is established. Once the full ATR has been achieved, the algorithm in "auto" mode will have fully switched to the relative method and will remain with that method for the rest of the day.

To explain the effect further, as an example, imagine that the price is approaching the full ATR range on the high side. At this point, the indicator will have almost fully transitioned to the second (relative) method. The lower ATR limit will now be anchored to the daily low as the price hits the upper ATR limit. If the price goes beyond the upper ATR, the lower ATR limit will stay anchored to the daily low, and the upper limit will stay anchored to one ATR above the lower limit. This allows you to see how far the price is going beyond the upper ATR limit. If the price then returns and backs off the upper ATR limit, the lower ATR limit will un-anchor from the daily low (it will actually rise, since the daily ATR range has been exceeded, so the lower ATR limit needs to come up because the actual daily range can’t fit into the ATR range anymore). The overall effect is to give you the best visual indication of where the price is in relation to a possible upper ATR-based target. Reverse this example for when the price low approaches the ATR range on the low side.

Care was taken so that the code uses no hard-coded time zones, exchanges, or session times. For this reason, it can in principle work globally. However, it very much depends on the information provided by the exchange, which is reflected in built-in Pine Script variables (see Limitations below).

█ LIMITATIONS

The indicator was developed for US/European equities and is tested on them only. It is also known to work on US futures; in this case, the whole 23-hour session is used, and the "Sessions to include in range" setting has no effect. It may or may not work as intended on security types and equities/futures for other countries.

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

AlphaTrend++AlphaTrend++

Overview

The AlphaTrend++ is an advanced Pine Script indicator designed to help traders identify buy and sell opportunities in trending and volatile markets. Building on trend-following principles, it uses a modified Average True Range (ATR) calculation combined with volume or momentum data to plot a dynamic trend line. The indicator overlays on the price chart, displaying a colored trend line, a filled trend zone, buy/sell signals, and optional stop-loss tick labels, making it ideal for day trading or swing trading, particularly in markets like futures (e.g., MES).

What It Does

This indicator generates buy and sell signals based on the direction and momentum of a custom trend line, filtered by optional time restrictions and signal frequency logic. The trend line adapts to price action and volatility, with a filled zone highlighting trend strength. Buy/sell signals are plotted as labels, and stop-loss distances are displayed in ticks (customizable for instruments like MES). The indicator supports standard chart types for realistic signal generation.

How It Works

The indicator employs the following components:

Trend Line Calculation: A dynamic trend line is calculated using ATR adjusted by a user-defined multiplier, combined with either Money Flow Index (MFI) or Relative Strength Index (RSI) depending on volume availability. The line tracks price movements, adjusting upward or downward based on trend direction and volatility.

Trend Zone: The area between the current trend line and its value two bars prior is filled, colored green for bullish trends (upward movement) or red for bearish trends (downward movement), providing a visual cue of trend strength.

Signal Generation: Buy signals occur when the trend line crosses above its value two bars ago, and sell signals occur when it crosses below, with optional filtering to reduce signal noise (based on bar timing logic). Signals can be restricted to a 9:00–15:00 UTC trading window.

Stop-Loss Ticks: For each signal, the indicator calculates the distance to the trend line (acting as a stop-loss level) in ticks, using a user-defined tick size (default 0.25 for MES). These are displayed as labels below/above the signal.

Time Filter: An optional filter limits signals to 9:00–15:00 UTC, aligning with active trading sessions like the US market open.

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to avoid unrealistic results associated with non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Multiplier: Adjust the ATR multiplier (default 1.0) to control trend line sensitivity. Higher values widen the stop-loss distance.

Common Period: Set the ATR and MFI/RSI period (default 14) for trend calculations.

No Volume Data: Enable if volume data is unavailable (e.g., for certain forex pairs), switching from MFI to RSI.

Tick Size: Set the tick size for stop-loss calculations (default 0.25 for MES futures).

Show Buy/Sell Signals: Toggle signal labels (default enabled).

Show Stop Loss Ticks: Toggle stop-loss tick labels (default enabled).

Use Time Filter: Restrict signals to 9:00–15:00 UTC (default disabled).

Use Filtered Signals: Enable to reduce signal frequency using bar timing logic (default enabled).

Interpret Signals:

Buy Signal: A blue “BUY” label below the bar indicates a potential long entry (trend line crossover, passing filters).

Sell Signal: A red “SELL” label above the bar indicates a potential short entry (trend line crossunder, passing filters).

Trend Zone: Green fill suggests bullish momentum; red fill suggests bearish momentum.

Stop-Loss Ticks: Gray labels show the stop-loss distance in ticks, helping with risk management.

Monitor Context: Use the trend line and filled zone to confirm the market’s direction before acting on signals.

Unique Features

Adaptive Trend Line: Combines ATR with MFI or RSI to create a responsive trend line that adjusts to volatility and market conditions.

Tick-Based Stop-Loss: Displays stop-loss distances in ticks, customizable for specific instruments, aiding precise risk management.

Signal Filtering: Optional bar timing logic reduces false signals, improving reliability in choppy markets.

Trend Zone Visualization: The filled zone between trend line values enhances trend clarity, making it easier to assess momentum.

Time-Restricted Trading: Optional 9:00–15:00 UTC filter aligns signals with high-liquidity sessions.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume spikes) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in highly volatile or low-liquidity markets due to ATR-based calculations.

The 9:00–15:00 UTC time filter may not suit all markets; disable it for 24-hour assets like forex or crypto.

Stop-loss tick calculations assume consistent tick sizes; verify compatibility with your instrument.

This indicator is designed for traders seeking a robust, trend-following tool with customizable risk management and signal filtering, optimized for active trading sessions.

EXODUS EXODUS by (DAFE) Trading Systems

EXODUS is a sophisticated trading algorithm built by Dskyz (DAFE) Trading Systems for competitive and competition purposes, designed to identify high-probability trades with robust risk management. this strategy leverages a multi-signal voting system, combining three core components—SPR, VWMO, and VEI—alongside ADX, choppiness filters, and ATR-based volatility gates to ensure trades are taken only in favorable market conditions. the algo uses a take-profit to stop-loss ratio, dynamic position sizing, and a strict voting mechanism requiring all signals to align before entering a trade.

EXODUS was not overfitted for any specific symbol. instead, it uses a generic tuned setting, making it versatile across various markets. while it can trade futures, it’s not currently set up for it but has the potential to do more with further development. visuals are intentionally minimal due to its competition focus, prioritizing performance over aesthetics. a more visually stunning version may be released in the future with enhanced graphics.

The Unique Core Components Developed for EXODUS

SPR (Session Price Recalibration)

SPR measures momentum during regular trading hours (RTH, 0930-1600, America/New_York) to catch session-specific trends.

spr_lookback = input.int(15, "SPR Lookback") this sets how many bars back SPR looks to calculate momentum (default 15 bars). it compares the current session’s price-volume score to the score 15 bars ago to gauge momentum strength.

how it works: a longer lookback smooths out the signal, focusing on bigger trends. a shorter one makes SPR more sensitive to recent moves.

how to adjust: on a 1-hour chart, 15 bars is 15 hours (about 2 trading days). if you’re on a shorter timeframe like 5 minutes, 15 bars is just 75 minutes, so you might want to increase it to 50 or 100 to capture more meaningful trends. if you’re trading a choppy stock, a shorter lookback (like 5) can help catch quick moves, but it might give more false signals.

spr_threshold = input.float (0.7, "SPR Threshold")

this is the cutoff for SPR to vote for a trade (default 0.7). if SPR’s normalized value is above 0.7, it votes for a long; below -0.7, it votes for a short.

how it works: SPR normalizes its momentum score by ATR, so this threshold ensures only strong moves count. a higher threshold means fewer trades but higher conviction.

how to adjust: if you’re getting too few trades, lower it to 0.5 to let more signals through. if you’re seeing too many false entries, raise it to 1.0 for stricter filtering. test on your chart to find a balance.

spr_atr_length = input.int(21, "SPR ATR Length") this sets the ATR period (default 21 bars) used to normalize SPR’s momentum score. ATR measures volatility, so this makes SPR’s signal relative to market conditions.

how it works: a longer ATR period (like 21) smooths out volatility, making SPR less jumpy. a shorter one makes it more reactive.

how to adjust: if you’re trading a volatile stock like TSLA, a longer period (30 or 50) can help avoid noise. for a calmer stock, try 10 to make SPR more responsive. match this to your timeframe—shorter timeframes might need a shorter ATR.

rth_session = input.session("0930-1600","SPR: RTH Sess.") rth_timezone = "America/New_York" this defines the session SPR uses (0930-1600, New York time). SPR only calculates momentum during these hours to focus on RTH activity.

how it works: it ignores pre-market or after-hours noise, ensuring SPR captures the main market action.

how to adjust: if you trade a different session (like London hours, 0300-1200 EST), change the session to match. you can also adjust the timezone if you’re in a different region, like "Europe/London". just make sure your chart’s timezone aligns with this setting.

VWMO (Volume-Weighted Momentum Oscillator)

VWMO measures momentum weighted by volume to spot sustained, high-conviction moves.

vwmo_momlen = input.int(21, "VWMO Momentum Length") this sets how many bars back VWMO looks to calculate price momentum (default 21 bars). it takes the price change (close minus close 21 bars ago).

how it works: a longer period captures bigger trends, while a shorter one reacts to recent swings.

how to adjust: on a daily chart, 21 bars is about a month—good for trend trading. on a 5-minute chart, it’s just 105 minutes, so you might bump it to 50 or 100 for more meaningful moves. if you want faster signals, drop it to 10, but expect more noise.

vwmo_volback = input.int(30, "VWMO Volume Lookback") this sets the period for calculating average volume (default 30 bars). VWMO weights momentum by volume divided by this average.

how it works: it compares current volume to the average to see if a move has strong participation. a longer lookback smooths the average, while a shorter one makes it more sensitive.

how to adjust: for stocks with spiky volume (like NVDA on earnings), a longer lookback (50 or 100) avoids overreacting to one-off spikes. for steady volume stocks, try 20. match this to your timeframe—shorter timeframes might need a shorter lookback.

vwmo_smooth = input.int(9, "VWMO Smoothing")

this sets the SMA period to smooth VWMO’s raw momentum (default 9 bars).

how it works: smoothing reduces noise in the signal, making VWMO more reliable for voting. a longer smoothing period cuts more noise but adds lag.

how to adjust: if VWMO is too jumpy (lots of false votes), increase to 15. if it’s too slow and missing trades, drop to 5. test on your chart to see what keeps the signal clean but responsive.

vwmo_threshold = input.float(10, "VWMO Threshold") this is the cutoff for VWMO to vote for a trade (default 10). above 10, it votes for a long; below -10, a short.

how it works: it ensures only strong momentum signals count. a higher threshold means fewer but stronger trades.

how to adjust: if you want more trades, lower it to 5. if you’re getting too many weak signals, raise it to 15. this depends on your market—volatile stocks might need a higher threshold to filter noise.

VEI (Velocity Efficiency Index)

VEI measures market efficiency and velocity to filter out choppy moves and focus on strong trends.

vei_eflen = input.int(14, "VEI Efficiency Smoothing") this sets the EMA period for smoothing VEI’s efficiency calc (bar range / volume, default 14 bars).

how it works: efficiency is how much price moves per unit of volume. smoothing it with an EMA reduces noise, focusing on consistent efficiency. a longer period smooths more but adds lag.

how to adjust: for choppy markets, increase to 20 to filter out noise. for faster markets, drop to 10 for quicker signals. this should match your timeframe—shorter timeframes might need a shorter period.

vei_momlen = input.int(8, "VEI Momentum Length") this sets how many bars back VEI looks to calculate momentum in efficiency (default 8 bars).

how it works: it measures the change in smoothed efficiency over 8 bars, then adjusts for inertia (volume-to-range). a longer period captures bigger shifts, while a shorter one reacts faster.

how to adjust: if VEI is missing quick reversals, drop to 5. if it’s too noisy, raise to 12. test on your chart to see what catches the right moves without too many false signals.

vei_threshold = input.float(4.5, "VEI Threshold") this is the cutoff for VEI to vote for a trade (default 4.5). above 4.5, it votes for a long; below -4.5, a short.

how it works: it ensures only strong, efficient moves count. a higher threshold means fewer trades but higher quality.

how to adjust: if you’re not getting enough trades, lower to 3. if you’re seeing too many false entries, raise to 6. this depends on your market—fast stocks like NQ1 might need a lower threshold.

Features

Multi-Signal Voting: requires all three signals (SPR, VWMO, VEI) to align for a trade, ensuring high-probability setups.

Risk Management: uses ATR-based stops (2.1x) and take-profits (4.1x), with dynamic position sizing based on a risk percentage (default 0.4%).

Market Filters: ADX (default 27) ensures trending conditions, choppiness index (default 54.5) avoids sideways markets, and ATR expansion (default 1.12) confirms volatility.

Dashboard: provides real-time stats like SPR, VWMO, VEI values, net P/L, win rate, and streak, with a clean, functional design.

Visuals

EXODUS prioritizes performance over visuals, as it was built for competitive and competition purposes. entry/exit signals are marked with simple labels and shapes, and a basic heatmap highlights market regimes. a more visually stunning update may be released later, with enhanced graphics and overlays.

Usage

EXODUS is designed for stocks and ETFs but can be adapted for futures with adjustments. it performs best in trending markets with sufficient volatility, as confirmed by its generic tuning across symbols like TSLA, AMD, NVDA, and NQ1. adjust inputs like SPR threshold, VWMO smoothing, or VEI momentum length to suit specific assets or timeframes.

Setting I used: (Again, these are a generic setting, each security needs to be fine tuned)

SPR LB = 19 SPR TH = 0.5 SPR ATR L= 21 SPR RTH Sess: 9:30 – 16:00

VWMO L = 21 VWMO LB = 18 VWMO S = 6 VWMO T = 8

VEI ES = 14 VEI ML = 21 VEI T = 4

R % = 0.4

ATR L = 21 ATR M (S) =1.1 TP Multi = 2.1 ATR min mult = 0.8 ATR Expansion = 1.02

ADX L = 21 Min ADX = 25

Choppiness Index = 14 Chop. Max T = 55.5

Backtesting: TSLA

Frame: Jan 02, 2018, 08:00 — May 01, 2025, 09:00

Slippage: 3

Commission .01

Disclaimer

this strategy is for educational purposes. past performance is not indicative of future results. trading involves significant risk, and you should only trade with capital you can afford to lose. always backtest and validate any strategy before using it in live markets.

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

About the Author

Dskyz (DAFE) Trading Systems is dedicated to building high-performance trading algorithms. EXODUS is a product of rigorous research and development, aimed at delivering consistent, and data-driven trading solutions.

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Overnight ES Strategy: CBC + Fractal + RSI + ATR FilterThis script is designed for overnight trading of the E-mini S&P 500 futures (ES) between 6 PM and 11 PM EST.

It combines multiple technical confluences to generate high-probability buy and sell signals, focusing on volatility-rich, low-liquidity evening sessions.

Key Features:

Candle Body Confluence (CBC) Approximation:

Identifies candles with small real bodies compared to total range, simulating consolidation zones where price is likely to reverse.

Williams Fractal Confirmation:

Detects local tops and bottoms based on 5-bar fractal reversal patterns, helping validate breakout or reversal points.

RSI Filter:

Ensures momentum is supportive — buys only when RSI < 35 (oversold) and sells only when RSI > 65 (overbought).

ATR Volatility Filter:

Trades are only allowed if the Average True Range (ATR) exceeds a user-defined threshold, filtering out low-volatility, risky environments.

Time Session Control:

Signals are only generated during the user-defined evening session (default: 6 PM to 11 PM EST) to match market behavior.

Real-Time Alerts Enabled:

Alerts can be set for BUY or SELL conditions, enabling mobile notifications, emails, or pop-ups without constant chart monitoring.

Recommended Settings:

Chart Timeframe: 15-minute or 30-minute candles

Assets: ES Mini (ES1!), NQ Mini, or other CME futures

Session: New York Time (EST)

ATR Threshold: Adjust based on market conditions; 5.0 suggested starting point for ES Mini on 15m.

Important:

This script only plots signals, it does not auto-execute trades.

Always backtest and paper trade before using live capital.

Volatility can vary; consider adjusting RSI and ATR filters based on market environment.

Credits:

Script designed based on confluence of price action, momentum, reversal structure, and volatility filtering principles used by professional traders.

Inspired by Candle Body Confluence (CBC) theory and Williams fractal techniques.

Multi-Factor Reversal AnalyzerMulti-Factor Reversal Analyzer – Quantitative Reversal Signal System

OVERVIEW

Multi-Factor Reversal Analyzer is a comprehensive technical analysis toolkit designed to detect market tops and bottoms with high precision. It combines trend momentum analysis, price action behavior, wave oscillation structure, and volatility breakout potential into one unified indicator.

This indicator is not a random mix of tools — each module is carefully selected for a specific purpose. When combined, they form a multi-dimensional view of the market, merging trend analysis, momentum divergence, and volatility compression to produce high-confidence signals.

Why Combine These Modules?

Module Combination Ideas & How to Use Them

Factor A: Trend Detector + Gold Zone

Concept:

• The Trend Detector (light yellow histogram) evaluates market strength:

• Histogram trending downward or staying below 50 → bearish conditions;

• Trending upward or staying above 50 → bullish conditions.

• The Gold Zone identifies areas of volatility compression — typically a prelude to explosive market moves.

Practical Application:

• When the Gold Zone appears and the Trend Detector is bearish → likely downside move;

• When the Gold Zone appears and the Trend Detector is bullish → likely upside breakout.

• Note: The Gold Zone does not mean the bottom is in. It is not a buy signal on its own — always combine it with other modules for directional bias.

Factor B: PAI + Wave Trend

Concept:

• PAI (Price Action Index) is a custom oscillator that combines price momentum with volatility dispersion, displaying strength zones:

• Green area → bullish dominance;

• Red area → bearish pressure.

• Wave Trend offers smoothed crossover signals via the main and signal lines.

Practical Application:

• When PAI is in the green zone and Wave Trend makes a bullish crossover → potential reversal to the upside;

• When PAI is in the red zone and Wave Trend shows a bearish crossover → potential start of a downtrend.

Factor C: Trend Detector + PAI

Concept:

• Combines directional trend strength with price action strength to confirm setups via confluence.

Practical Application:

• Trend Detector histogram bottoms out + PAI enters the green zone → high chance of upward reversal;

• Histogram tops out + PAI in the red zone → increased likelihood of downside continuation.

Multi-Factor Confluence (Advanced Use)

• When Trend Detector, PAI, and Wave Trend all align in the same direction (bullish or bearish), the directional signal becomes significantly more reliable.

• This setup is especially useful for trend-following or swing trade entries.

KEY FEATURES

1. Multi-Layer Reversal Logic

• Combines trend scoring, oscillator divergence, and volatility squeezes for triangulated reversal detection.

• Helps traders distinguish between trend pullbacks and true reversals.

2. Advanced Divergence Detection

• Detects both regular and hidden divergences using pivot-based confirmation logic.

• Customizable lookback ranges and pivot sensitivity provide flexible tuning for different market styles.

3. Gold Zone Volatility Compression

• Highlights pre-breakout zones using custom oscillation models (RSI, harmonic, Karobein, etc.).

• Improves anticipation of breakout opportunities following low-volatility compressions.

4. Trend Direction Context

• PAI and Trend Score components provide top-down insight into prevailing bias.

• Built-in “Straddle Area” highlights consolidation zones; breakouts from this area often signal new trend phases.

5. Flexible Visualization

• Color-coded trend bars, reversal markers, normalized oscillator plots, and trend strength labels.

• Designed for both visual discretionary traders and data-driven system developers.

USAGE GUIDELINES

1. Applicable Markets

• Suitable for stocks, crypto, futures, and forex

• Supports reversal, mean-reversion, and breakout trading styles

2. Recommended Timeframes

• Short-term traders: 5m / 15m / 1H — use Wave Trend divergence + Gold Zone

• Swing traders: 4H / Daily — rely on Price Action Index and Trend Detector

• Macro trend context: use PAI HTF mode for higher timeframe overlays

3. Reversal Strategy Flow

• Watch for divergence (WT/PAI) + Gold Zone compression

• Confirm with Trend Score weakening or flipping

• Use Straddle Area breakout for final trigger

• Optional: enable bar coloring or labels for visual reinforcement

• The indicator performs optimally when used in conjunction with a harmonic pattern recognition tool

4. Additional Note on the Gold Zone

The “Gold Zone” does not directly indicate a market bottom. Since it is displayed at the bottom of the chart, it may be misunderstood as a bullish signal. In reality, the Gold Zone represents a compression of price momentum and volatility, suggesting that a significant directional move is about to occur. The direction of that move—upward or downward—should be determined by analyzing the histogram:

• If histogram momentum is weakening, the Gold Zone may precede a downward move.

• If histogram momentum is strengthening, it may signal an upcoming rebound or rally.

Treat the Gold Zone as a warning of impending volatility, and always combine it with trend indicators for accurate directional judgment.

RISK DISCLAIMER

• This indicator calculates trend direction based on historical data and cannot guarantee future market performance. When using this indicator for trading, always combine it with other technical analysis tools, fundamental analysis, and personal trading experience for comprehensive decision-making.

• Market conditions are uncertain, and trend signals may result in false positives or lag. Traders should avoid over-reliance on indicator signals and implement stop-loss strategies and risk management techniques to reduce potential losses.

• Leverage trading carries high risks and may result in rapid capital loss. If using this indicator in leveraged markets (such as futures, forex, or cryptocurrency derivatives), exercise caution, manage risks properly, and set reasonable stop-loss/take-profit levels to protect funds.

• All trading decisions are the sole responsibility of the trader. The developer is not liable for any trading losses. This indicator is for technical analysis reference only and does not constitute investment advice.

• Before live trading, it is recommended to use a demo account for testing to fully understand how to use the indicator and apply proper risk management strategies.

CHANGELOG

v1.0: Initial release featuring integrated Price Action Index, Trend Strength Scoring, Wave Trend Oscillator, Gold Zone Compression Detection, and dual-type divergence recognition. Supports higher timeframe (HTF) synchronization, visual signal markers, and diversified parameter configurations.

ES1! vs ZB1! Exponentially Weighted CorrelationES1! vs ZB1! Exponentially Weighted Correlation

This indicator calculates and visualizes the exponentially weighted correlation between the S&P 500 E-mini futures (ES1!) and the 30-Year U.S. Treasury Bond futures (ZB1!) over a user-defined lookback period. By using an exponential moving average (EMA) approach, it emphasizes recent price movements, providing a dynamic view of the relationship between these two key financial instruments.

Features:

- Customizable Inputs: Adjust the lookback length (default: 60) and alpha (default: 0.1) to fine-tune the sensitivity of the correlation calculation.

- Exponentially Weighted Correlation: Measures the strength and direction of the relationship between ES1! and ZB1! prices, with more weight given to recent data.

- Visual Clarity: Displays correlation as colored bars (green for positive, red for negative) for quick interpretation, with reference lines at 0, +1, and -1 for context.

- Non-Overlay Design: Plotted in a separate panel below the chart to avoid cluttering price data.

How It Works:

The indicator fetches closing prices for ES1! and ZB1!, applies an EMA to smooth the data, and computes the exponentially weighted covariance and variances. The correlation is then derived and plotted as a histogram, helping traders identify whether the two markets are moving together (positive correlation), in opposite directions (negative correlation), or independently.

Use Cases:

- Market Analysis: Gauge the relationship between equity and bond markets to inform trading strategies.

- Risk Management: Monitor correlation shifts to adjust portfolio exposure.

- Intermarket Insights: Identify trends or divergences in the stock-bond dynamic for macroeconomic analysis.

Ideal for traders and analysts tracking intermarket relationships, this indicator offers a clear, responsive tool for understanding ES1! and ZB1! correlation in real-time.

Failed Breakout DetectionThis indicator is a reverse-engineered copy of the FBD Detection indicator published by xfuturesgod. The original indicator aimed at detecting "Failed Breakdowns". This version tracks the opposite signals, "Failed Breakouts". It was coded with the ES Futures 15 minute chart in mind but may be useful on other instruments and time frames.

The original description, with terminology reversed to explain this version:

'Failed Breakouts' are a popular set up for short entries.

In short, the set up requires:

1) A significant high is made ('initial high')

2) Initial high is undercut with a new high

3) Price action then 'reclaims' the initial high by moving +8-10 points from the initial high

This script aims at detecting such set ups. It was coded with the ES Futures 15 minute chart in mind but may be useful on other instruments and time frames.

Business Logic:

1) Uses pivot highs to detect 'significant' initial highs

2) Uses amplitude threshold to detect a new high above the initial high; used /u/ben_zen script for this

3) Looks for a valid reclaim - a red candle that occurs within 10 bars of the new high

4) Price must reclaim at least 8 points for the set up to be valid

5) If a signal is detected, the initial high value (pivot high) is stored in array that prevents duplicate signals from being generated.

6) FBO Signal is plotted on the chart with "X"

7) Pivot high detection is plotted on the chart with "P" and a label

8) New highs are plotted on the chart with a red triangle

Notes:

User input

- My preference is to use the defaults as is, but as always feel free to experiment

- Can modify pivot length but in my experience 10/10 work best for pivot highs

- New high detection - 55 bars and 0.05 amplitude work well based on visual checks of signals

- Can modify the number of points needed to reclaim a high, and the # of bars limit over which this must occur.

Alerts:

- Alerts are available for detection of new highs and detection of failed breakouts

- Alerts are also available for these signals but only during 7:30PM-4PM EST - 'prime time' US trading hours

Limitations:

- Current version of the script only compares new highs to the most recent pivot high, does not look at anything prior to that

- Best used as a discretionary signal

Rolling ATR Momentum

Rolling ATR Momentum Indicator – User Manual

---

🔍 Overview

The Rolling ATR Momentum Indicator is a simple yet powerful tool designed to detect shifts in market volatility. It compares the current Average True Range (ATR) with the ATR from a previous point in time to measure how market volatility is changing.

This indicator is especially useful for:

- Spotting the beginning or fading of a momentum phase

- Filtering out low-volatility market conditions

- Enhancing timing for entries and exits in trending or breakout trades

---

📊 Key Components

✅ ATR Delta (Rolling)

- Definition: `ATR Delta = Current ATR - Past ATR`

- Inputs:

- ATR Period (default: 14): The base ATR calculation window

- Lookback Period (default: 5): How many bars ago to compare ATR

- Interpretation:

- Positive ATR Delta (Green Line): Market volatility is increasing

- Negative ATR Delta (Red Line): Market volatility is decreasing

📈 Zero Line

- A horizontal baseline at zero helps you easily see when ATR momentum shifts from negative to positive (or vice versa).

🟩/🟥 Background Color

- Green Background: ATR Delta is positive (rising volatility)

- Red Background: ATR Delta is negative (falling volatility)

🔵 Optional: ATR Reference Lines

- You can optionally display raw Current ATR and Past ATR by changing their visibility settings.

---

✅ How to Use It

Entry Timing (Futures/Options)

- Use ATR Delta as a filter:

- Only take trades when ATR Delta is positive → confirms momentum is building

- Avoid trades when ATR Delta is negative → market might be slow, sideways, or losing steam

Breakout Anticipation

- A rising ATR Delta after a tight range or consolidation can suggest that a breakout is underway

Stop-loss Strategy

- Use high ATR periods for wider stops (to avoid noise)

- Use low ATR periods for tighter stops or skip trading

---

🧠 Pro Tips

- This indicator doesn’t predict direction—combine with trend or price structure tools (like EMA, PPMA, candlesticks)

- Works best in trending or breakout environments

- Add it to multi-timeframe layouts to see volatility buildup on higher timeframes

---

⚙️ Settings

| Parameter | Description |

|----------|-------------|

| ATR Period | Length of the ATR calculation (default 14) |

| Lookback Period | How many bars back to compare ATR values |

---

🧭 Best For:

- Index futures (Nifty, BankNifty)

- Option buyers needing volatility confirmation

- Intraday & swing traders looking to trade momentum setups

---

Use the Rolling ATR Momentum indicator as your volatility radar—simple, clean, and highly effective for staying on the right side of market energy.

End of Manual

Nasdaq Risk Calculator - DTFXNasdaq Risk Calculator

This Pine Script (v5) indicator provides a dashboard-style tool for calculating trading risk based on manually input tick measurements for Nasdaq futures contracts (NQ and MNQ). Designed as an overlay on the main chart, it displays key risk metrics in a fixed-position table, allowing traders to assess contract type, lot size, risk ticks, and actual risk in dollars relative to a user-defined risk amount.

Features:

Manual Tick Input: Enter the number of ticks (e.g., from a ruler measurement) to define the price range for risk calculation.

Risk Calculation: Computes the optimal contract (NQ or MNQ), number of lots, risk ticks (half the input range), and actual risk in dollars, targeting the specified risk amount (default: $100).

Customizable Dashboard: Displays results in a single-cell table with a semi-transparent white background and gray border, positioned in one of four chart corners (Top Left, Top Right, Bottom Left, Bottom Right) via user selection.

Reset Option: Includes a toggle to clear the dashboard and start anew.

How to Use:

Add the indicator to your chart (best suited for NQ or MNQ futures).

In the settings, input your "Risk Amount ($)" and "Ticks" (e.g., 400 for a 100-point range on NQ).

Select the "Dashboard Corner" to position the table.

View the calculated risk details in the chosen corner.

Adjust inputs or reset as needed.

Notes:

NQ tick value is $5.00 (NQ_MULTIPLIER = 5.0), and MNQ tick value is $0.50 (MNQ_MULTIPLIER = 0.5).

Ideal for traders planning risk based on measured price ranges, such as support/resistance zones.

ES vs Bond ROCThis Pine Script plots the Relative Rate of Change (ROC) between the S&P 500 E-mini Futures (ES) and 30-Year Treasury Bond Futures (ZB) over a specified period. It helps identify when equities are overperforming or underperforming relative to long-term bonds—an insight often used to detect risk-on/risk-off sentiment shifts in the market.

Volume Weighted RSI (VW RSI)The Volume Weighted RSI (VW RSI) is a momentum oscillator designed for TradingView, implemented in Pine Script v6, that enhances the traditional Relative Strength Index (RSI) by incorporating trading volume into its calculation. Unlike the standard RSI, which measures the speed and change of price movements based solely on price data, the VW RSI weights its analysis by volume, emphasizing price movements backed by significant trading activity. This makes the VW RSI particularly effective for identifying bullish or bearish momentum, overbought/oversold conditions, and potential trend reversals in markets where volume plays a critical role, such as stocks, forex, and cryptocurrencies.

Key Features

Volume-Weighted Momentum Calculation:

The VW RSI calculates momentum by comparing the volume associated with upward price movements (up-volume) to the volume associated with downward price movements (down-volume).

Up-volume is the volume on bars where the closing price is higher than the previous close, while down-volume is the volume on bars where the closing price is lower than the previous close.

These volumes are smoothed over a user-defined period (default: 14 bars) using a Running Moving Average (RMA), and the VW RSI is computed using the formula:

\text{VW RSI} = 100 - \frac{100}{1 + \text{VoRS}}

where

\text{VoRS} = \frac{\text{Average Up-Volume}}{\text{Average Down-Volume}}

.

Oscillator Range and Interpretation:

The VW RSI oscillates between 0 and 100, with a centerline at 50.

Above 50: Indicates bullish volume momentum, suggesting that volume on up bars dominates, which may signal buying pressure and a potential uptrend.

Below 50: Indicates bearish volume momentum, suggesting that volume on down bars dominates, which may signal selling pressure and a potential downtrend.

Overbought/Oversold Levels: User-defined thresholds (default: 70 for overbought, 30 for oversold) help identify potential reversal points:

VW RSI > 70: Overbought, indicating a possible pullback or reversal.

VW RSI < 30: Oversold, indicating a possible bounce or reversal.

Visual Elements:

VW RSI Line: Plotted in a separate pane below the price chart, colored dynamically based on its value:

Green when above 50 (bullish momentum).

Red when below 50 (bearish momentum).

Gray when at 50 (neutral).

Centerline: A dashed line at 50, optionally displayed, serving as the neutral threshold between bullish and bearish momentum.

Overbought/Oversold Lines: Dashed lines at the user-defined overbought (default: 70) and oversold (default: 30) levels, optionally displayed, to highlight extreme conditions.

Background Coloring: The background of the VW RSI pane is shaded red when the indicator is in overbought territory and green when in oversold territory, providing a quick visual cue of potential reversal zones.

Alerts:

Built-in alerts for key events:

Bullish Momentum: Triggered when the VW RSI crosses above 50, indicating a shift to bullish volume momentum.

Bearish Momentum: Triggered when the VW RSI crosses below 50, indicating a shift to bearish volume momentum.

Overbought Condition: Triggered when the VW RSI crosses above the overbought threshold (default: 70), signaling a potential pullback.

Oversold Condition: Triggered when the VW RSI crosses below the oversold threshold (default: 30), signaling a potential bounce.

Input Parameters

VW RSI Length (default: 14): The period over which the up-volume and down-volume are smoothed to calculate the VW RSI. A longer period results in smoother signals, while a shorter period increases sensitivity.

Overbought Level (default: 70): The threshold above which the VW RSI is considered overbought, indicating a potential reversal or pullback.

Oversold Level (default: 30): The threshold below which the VW RSI is considered oversold, indicating a potential reversal or bounce.

Show Centerline (default: true): Toggles the display of the 50 centerline, which separates bullish and bearish momentum zones.

Show Overbought/Oversold Lines (default: true): Toggles the display of the overbought and oversold threshold lines.

How It Works

Volume Classification:

For each bar, the indicator determines whether the price movement is upward or downward:

If the current close is higher than the previous close, the bar’s volume is classified as up-volume.

If the current close is lower than the previous close, the bar’s volume is classified as down-volume.

If the close is unchanged, both up-volume and down-volume are set to 0 for that bar.

Smoothing:

The up-volume and down-volume are smoothed using a Running Moving Average (RMA) over the specified period (default: 14 bars) to reduce noise and provide a more stable measure of volume momentum.

VW RSI Calculation:

The Volume Relative Strength (VoRS) is calculated as the ratio of smoothed up-volume to smoothed down-volume.

The VW RSI is then computed using the standard RSI formula, but with volume data instead of price changes, resulting in a value between 0 and 100.

Visualization and Alerts:

The VW RSI is plotted with dynamic coloring to reflect its momentum direction, and optional lines are drawn for the centerline and overbought/oversold levels.

Background coloring highlights overbought and oversold conditions, and alerts notify the trader of significant crossings.

Usage

Timeframe: The VW RSI can be used on any timeframe, but it is particularly effective on intraday charts (e.g., 1-hour, 4-hour) or daily charts where volume data is reliable. Shorter timeframes may require a shorter length for increased sensitivity, while longer timeframes may benefit from a longer length for smoother signals.

Markets: Best suited for markets with significant and reliable volume data, such as stocks, forex, and cryptocurrencies. It may be less effective in markets with low or inconsistent volume, such as certain futures contracts.

Trading Strategies:

Trend Confirmation:

Use the VW RSI to confirm the direction of a trend. For example, in an uptrend, look for the VW RSI to remain above 50, indicating sustained bullish volume momentum, and consider buying on pullbacks when the VW RSI dips but stays above 50.

In a downtrend, look for the VW RSI to remain below 50, indicating sustained bearish volume momentum, and consider selling on rallies when the VW RSI rises but stays below 50.

Overbought/Oversold Conditions:

When the VW RSI crosses above 70, the market may be overbought, suggesting a potential pullback or reversal. Consider taking profits on long positions or preparing for a short entry, but confirm with price action or other indicators.

When the VW RSI crosses below 30, the market may be oversold, suggesting a potential bounce or reversal. Consider entering long positions or covering shorts, but confirm with additional signals.

Divergences:

Look for divergences between the VW RSI and price to spot potential reversals. For example, if the price makes a higher high but the VW RSI makes a lower high, this bearish divergence may signal an impending downtrend.

Conversely, if the price makes a lower low but the VW RSI makes a higher low, this bullish divergence may signal an impending uptrend.

Momentum Shifts:

A crossover above 50 can signal the start of bullish momentum, making it a potential entry point for long trades.

A crossunder below 50 can signal the start of bearish momentum, making it a potential entry point for short trades or an exit for long positions.

Example

On a 4-hour SOLUSDT chart:

During an uptrend, the VW RSI might rise above 50 and stay there, confirming bullish volume momentum. If it approaches 70, it may indicate overbought conditions, as seen near a price peak of 145.08, suggesting a potential pullback.

During a downtrend, the VW RSI might fall below 50, confirming bearish volume momentum. If it drops below 30 near a price low of 141.82, it may indicate oversold conditions, suggesting a potential bounce, as seen in a slight recovery afterward.

A bullish divergence might occur if the price makes a lower low during the downtrend, but the VW RSI makes a higher low, signaling a potential reversal.

Limitations

Lagging Nature: Like the traditional RSI, the VW RSI is a lagging indicator because it relies on smoothed data (RMA). It may not react quickly to sudden price reversals, potentially missing the start of new trends.

False Signals in Ranging Markets: In choppy or ranging markets, the VW RSI may oscillate around 50, generating frequent crossovers that lead to false signals. Combining it with a trend filter (e.g., ADX) can help mitigate this.

Volume Data Dependency: The VW RSI relies on accurate volume data, which may be inconsistent or unavailable in some markets (e.g., certain forex pairs or futures contracts). In such cases, the indicator’s effectiveness may be reduced.

Overbought/Oversold in Strong Trends: During strong trends, the VW RSI can remain in overbought or oversold territory for extended periods, leading to premature exit signals. Use additional confirmation to avoid exiting too early.

Potential Improvements

Smoothing Options: Add options to use different smoothing methods (e.g., EMA, SMA) instead of RMA for the up/down volume calculations, allowing users to adjust the indicator’s responsiveness.

Divergence Detection: Include logic to detect and plot bullish/bearish divergences between the VW RSI and price, providing visual cues for potential reversals.

Customizable Colors: Allow users to customize the colors of the VW RSI line, centerline, overbought/oversold lines, and background shading.

Trend Filter: Integrate a trend strength filter (e.g., ADX > 25) to ensure signals are generated only during strong trends, reducing false signals in ranging markets.

The Volume Weighted RSI (VW RSI) is a powerful tool for traders seeking to incorporate volume into their momentum analysis, offering a unique perspective on market dynamics by emphasizing price movements backed by significant trading activity. It is best used in conjunction with other indicators and price action analysis to confirm signals and improve trading decisions.

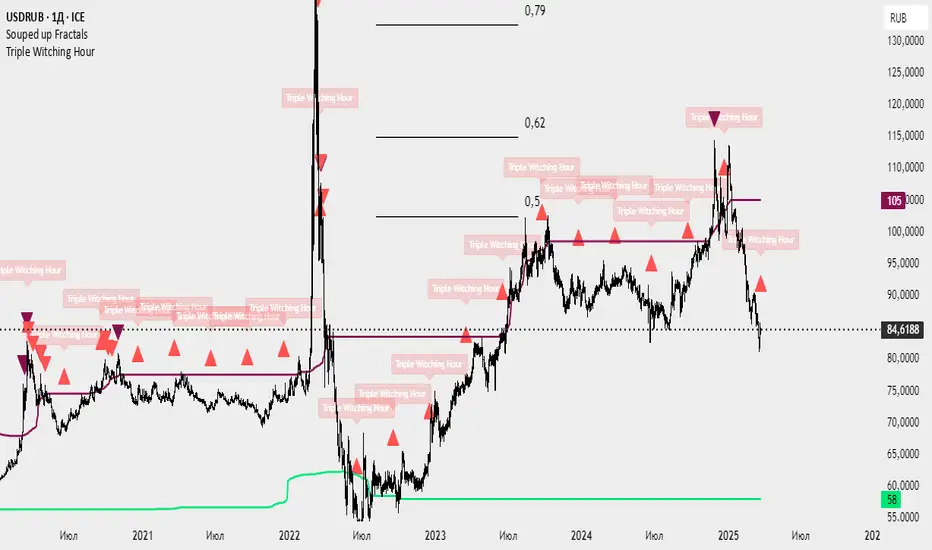

Triple Witching HourThe "Triple Witching Hour" indicator highlights the days when the quarterly expiration of stock index futures, options on futures, and options on stocks occurs simultaneously. These events, known as "Triple Witching Days," typically happen on the third Friday of March, June, September, and December. The indicator marks these days on the chart with a red triangle below the price bars and displays a label with the text "Triple Witching Hour." Traders can use this tool to identify periods of potential market volatility and adjust their strategies accordingly.

BTC: Open InterestThis indicator tracks the 7-day (default) percentage change in open interest (OI), providing insights into market participation trends. It includes customizable periods and colors, allowing traders to adjust settings for better visualization.

Open interest (OI) is the total number of active contracts (futures or options) that haven’t been closed or settled. It represents the total open positions in the market.

Thus when OI increases, more traders are entering new positions, signaling growing market interest. Conversely, when OI decreases, positions are being closed, suggesting lower trader participation or liquidation.

Attributes & Features:

Open Interest Percentage Change – Measures the 7-day % change in open interest to track market participation.

Customizable Calculation Period – Users can adjust the period (default: 7 days) for more flexible analysis.

Adjustable Colors – Allows modification of colors for better visualization.

Trend Identification – Highlights rising vs. falling open interest trends.

Works Across Assets – Can be used for cryptos, stocks, and futures with open interest data.

Overlay or Separate Panel – Can be plotted on price chart or as a separate indicator.

How It Works:

Fetches Open Interest Data – Retrieves open interest values for each day for USD, USDT, and USDC Bitcoin Perpetual Derivitives.

Calculates Percentage Change – Compares current open interest to its value X days ago (Default = 7 days).

Standard Deviation – Applies standard deviation ranging from -2 to +2 deviations to identify large shifts in OI.

Visual Alerts – Can highlight extreme increases or decreases signaling potential market shifts.

NOTE: THE INDICATOR DATA ONLY GOES BACK TO START OF 2022

TJR SEEK AND DESTROYTJR SEEK AND DESTROY – Intraday ICT Trading Tool

Built for day traders, TJR SEEK AND DESTROY combines Smart Money concepts like order blocks, fair value gaps, and liquidity sweeps with structure breaks and daily bias to pinpoint high-probability trades during US market hours (9:30–16:00). Ideal for scalping or intraday strategies on stocks, futures, or forex.

What Makes It Unique?

Unlike standalone ICT indicators, this script integrates:

Order Blocks with volume and range filters for precise support/resistance zones.

Fair Value Gaps (FVG) to spot pre-market price imbalances.

Break of Structure (BOS) and Liquidity Sweeps for trend and reversal signals.

A 1H MA-based Bias to align trades with the day’s direction.

BUY/SELL Labels triggered only when bias, BOS, and sweeps align, reducing noise.

How Does It Work?

Order Blocks: Marks zones with high volume (>1.5x 20-period SMA) and low range (<0.5x ATR20) as teal boxes—potential reversal points.

Fair Value Gap: Compares the prior day’s close to the current open (pre- or post-9:30), shown as a purple line and label (e.g., "FVG: 0.005").

Pivot Point: Calculates (prevHigh + prevLow + prevClose) / 3 from the prior day, plotted as an orange line for equilibrium.

Break of Structure: Detects crossovers of 5-bar highs/lows (gray lines), marked with red triangles.

Liquidity Sweeps: Tracks breaches of the prior day’s high/low (yellow lines), marked with yellow triangles.

Daily Bias: Uses 1H close vs. 20-period MA (blue line) for bullish (green background), bearish (red), or neutral (gray) context.

Signals: BUY (green label) when bias is bullish, price breaks up, and sweeps the prior high; SELL (red label) when bias is bearish, price breaks down, and sweeps the prior low.

How to Use It

Setup: Apply to 1M–15M charts for US session trading (9:30–16:00 EST).

Trading:

Wait for a BUY label after a yellow sweep triangle above the prior day’s high in a green (bullish) background.

Wait for a SELL label after a yellow sweep triangle below the prior day’s low in a red (bearish) background.

Use order blocks (teal boxes) as support/resistance for stop-loss or take-profit.

Markets: Best for SPY, ES futures, or forex pairs with US session volatility.

Underlying Concepts

Order Blocks: High-volume, low-range bars suggest institutional activity.

FVG: Gaps between close and open indicate imbalance to be filled.

BOS & Sweeps: Price breaking key levels signals momentum or stop-hunting.

Bias: 1H MA filters trades by broader trend.

Chart Setup

Displays order blocks (teal boxes), pivot (orange), open (purple), bias (colored background), BOS/sweeps (triangles), and signals (labels). Keep other indicators off for clarity.

Casa_VolumeProfileSessionLibrary "Casa_VolumeProfileSession"

Analyzes price and volume during regular trading hours to provide a session volume profile,

including Point of Control (POC), Value Area High (VAH), and Value Area Low (VAL).

Calculates and displays these levels historically and for the developing session.

Offers customizable visualization options for the Value Area, POC, histogram, and labels.

Uses lower timeframe data for increased accuracy and supports futures sessions.

The number of rows used for the volume profile can be fixed or dynamically calculated based on the session's price range and the instrument's minimum tick increment, providing optimal resolution.

calculateEffectiveRows(configuredRows, dayHigh, dayLow)

Determines the optimal number of rows for the volume profile, either using the configured value or calculating dynamically based on price range and tick size

Parameters:

configuredRows (int) : User-specified number of rows (0 means auto-calculate)

dayHigh (float) : Highest price of the session

dayLow (float) : Lowest price of the session

Returns: The number of rows to use for the volume profile

debug(vp, position)

Helper function to write some information about the supplied SVP object to the screen in a table.

Parameters:

vp (Object) : The SVP object to debug

position (string) : The position.* to place the table. Defaults to position.bottom_center

getLowerTimeframe()

Depending on the timeframe of the chart, determines a lower timeframe to grab volume data from for the analysis

Returns: The timeframe string to fetch volume for

get(volumeProfile, lowerTimeframeHigh, lowerTimeframeLow, lowerTimeframeVolume, lowerTimeframeTime, lowerTimeframeSessionIsMarket)

Populated the provided SessionVolumeProfile object with vp data on the session.

Parameters:

volumeProfile (Object) : The SessionVolumeProfile object to populate

lowerTimeframeHigh (array) : The lower timeframe high values

lowerTimeframeLow (array) : The lower timeframe low values

lowerTimeframeVolume (array) : The lower timeframe volume values

lowerTimeframeTime (array) : The lower timeframe time values

lowerTimeframeSessionIsMarket (array) : The lower timeframe session.ismarket values (that are futures-friendly)

drawPriorValueAreas(todaySessionVolumeProfile, extendYesterdayOverToday, showLabels, labelSize, pocColor, pocStyle, pocWidth, vahlColor, vahlStyle, vahlWidth, vaColor)

Given a SessionVolumeProfile Object, will render the historical value areas for that object.

Parameters:

todaySessionVolumeProfile (Object) : The SessionVolumeProfile Object to draw

extendYesterdayOverToday (bool) : Defaults to true

showLabels (bool) : Defaults to true

labelSize (string) : Defaults to size.small

pocColor (color) : Defaults to #e500a4

pocStyle (string) : Defaults to line.style_solid

pocWidth (int) : Defaults to 1

vahlColor (color) : The color of the value area high/low lines. Defaults to #1592e6

vahlStyle (string) : The style of the value area high/low lines. Defaults to line.style_solid

vahlWidth (int) : The width of the value area high/low lines. Defaults to 1

vaColor (color) : The color of the value area background. Defaults to #00bbf911)

drawHistogram(volumeProfile, bgColor, showVolumeOnHistogram)

Given a SessionVolumeProfile object, will render the histogram for that object.

Parameters:

volumeProfile (Object) : The SessionVolumeProfile object to draw

bgColor (color) : The baseline color to use for the histogram. Defaults to #00bbf9

showVolumeOnHistogram (bool) : Show the volume amount on the histogram bars. Defaults to false.

Object

Object Contains all settings and calculated values for a Volume Profile Session analysis

Fields:

numberOfRows (series int) : Number of price levels to divide the range into. If set to 0, auto-calculates based on price range and tick size

valueAreaCoverage (series int) : Percentage of total volume to include in the Value Area (default 70%)

trackDevelopingVa (series bool) : Whether to calculate and display the Value Area as it develops during the session

valueAreaHigh (series float) : Upper boundary of the Value Area - price level containing specified % of volume

pointOfControl (series float) : Price level with the highest volume concentration

valueAreaLow (series float) : Lower boundary of the Value Area

startTime (series int) : Session start time in Unix timestamp format

endTime (series int) : Session end time in Unix timestamp format

dayHigh (series float) : Highest price of the session

dayLow (series float) : Lowest price of the session

step (series float) : Size of each price row (calculated as price range divided by number of rows)

pointOfControlLevel (series int) : Index of the row containing the Point of Control

valueAreaHighLevel (series int) : Index of the row containing the Value Area High

valueAreaLowLevel (series int) : Index of the row containing the Value Area Low

lastTime (series int) : Tracks the most recent timestamp processed

volumeRows (map) : Stores volume data for each price level row (key=row number, value=volume)

ltfSessionHighs (array) : Stores high prices from lower timeframe data

ltfSessionLows (array) : Stores low prices from lower timeframe data

ltfSessionVols (array) : Stores volume data from lower timeframe data

Delta VolDelta Volume BTC - Multi Pair

Description The Delta Volume BTC - Multi Pair indicator visualizes the balance between buying and selling volume across multiple Bitcoin exchanges. By analyzing price action within each bar, it provides insight into underlying market pressure that traditional volume indicators miss. This indicator allows traders to:

Compare volume flow across Coinbase, Binance, and Binance Perpetual markets

Identify divergences between exchanges that may signal market shifts

Detect accumulation or distribution patterns through volume imbalances

View exchanges individually or in aggregate for comprehensive analysis

Calculation Methods The indicator offers three volume delta calculation methods:

VWAP Based (default):

price_range = high - low

buy_percent = (close - low) / price_range

sell_percent = (high - close) / price_range

delta = volume * (buy_percent - sell_percent)

This method distributes volume based on where price closed within the bar's range, providing a nuanced view of buying/selling pressure.

Tick Based :

delta = volume * sign(hlc3 - previous_hlc3)

This approach assigns volume based on the direction of typical price movement between bars, capturing momentum between periods.

Simple :

delta = close > open ? volume : close < open ? -volume : 0

A straightforward method that assigns positive volume to up bars and negative volume to down bars.

When Aggregate Mode is enabled, the indicator sums the volume deltas from all selected exchanges:

aggregate_delta = coinbase_delta + binance_delta + binance_perp_delta

Features

Multi-Exchange Support : Track volume delta across Coinbase, Binance, and Binance Perpetual futures

Advanced Calculation Methods : Choose between VWAP-based, tick-based, or simple volume delta algorithms

Flexible Display Options : Visualize as histogram, columns, area, or line charts

Customizable Colors : Distinct color schemes for each exchange and direction

Smoothing Options : Apply EMA, SMA, or WMA to reduce noise

Aggregate Mode : Combine all exchanges to see total market flow

How to Use

Individual Exchange Analysis : Uncheck "Aggregate Mode" to see each exchange separately, revealing where smart money may be positioning

Divergence Detection : Watch for one exchange showing buying while others show selling

Volume Trend Confirmation : Strong price moves should be accompanied by strong delta in the same direction

Liquidity Analysis : Compare spot vs futures volume delta to identify market sentiment shifts

The Delta Volume BTC - Multi Pair indicator helps identify the "hidden" buying and selling pressure that may not be apparent from price action alone, giving you an edge in understanding market dynamics across the Bitcoin ecosystem.

Trending Market Toolkit [LuxAlgo]The Trending Market Toolkit focuses exclusively on trending market structures and high-confluence, high-risk-to-reward entry models. It is designed to complement discretionary trading by offering different entry strategies based on market structure.

🔶 USAGE

In the chart above we can see how the tool detects several reversals, draws the broken trendlines, the reversal areas from which the tool starts looking for a trigger, and when it finally happens, a potential trade with risk and reward areas and the risk/reward ratio.

🔹 Detection Mode

Traders can choose between three different modes: trend only, reversal only, or both.

If both are active, reversals have priority over trends, so the tool will not detect a trend if a reversal is active.

In the chart above we can see all three modes.

🔹 Detection on Higher Timeframes

Traders can choose to identify structures on the chart timeframe or on a higher timeframe.

In the chart above, we have the SP500 futures on the 5m timeframe with different settings: chart timeframe, 30m, and 1H.

🔹 Risk And Targets

Depending on whether the high-risk/reward parameter is enabled, traders can choose between three different targets and two different stops.

The chart above shows how different choices affect the risk/reward ratio for the same potential trade on the Gold Futures 2m chart.

🔶 SETTINGS

Show: Traders can choose between Trends, Reversals or Both.

🔹 Structures

Swing Length: Number of candles to confirm a swing high or swing low. A higher number detects larger swings.

Custom Timeframe: Traders can make use of the current chart timeframe, or choose a custom timeframe.

Reversal Area Threshold: A higher number increases the reversal area.

🔹 Trades

Trade Trigger Length: Number of candles to confirm an internal high or internal low. A lower number detects smaller swings. It must be the same size or smaller than the swing length.

Target: Traders can choose between the default target (0) or two extended targets (0.27 or 0.618).

Risk to Reward Threshold: Set the minimum risk-to-reward ratio to detect trades. Use the 0 value to detect all trades.

High Risk to Reward: Enable/Disable the high risk to reward mode.

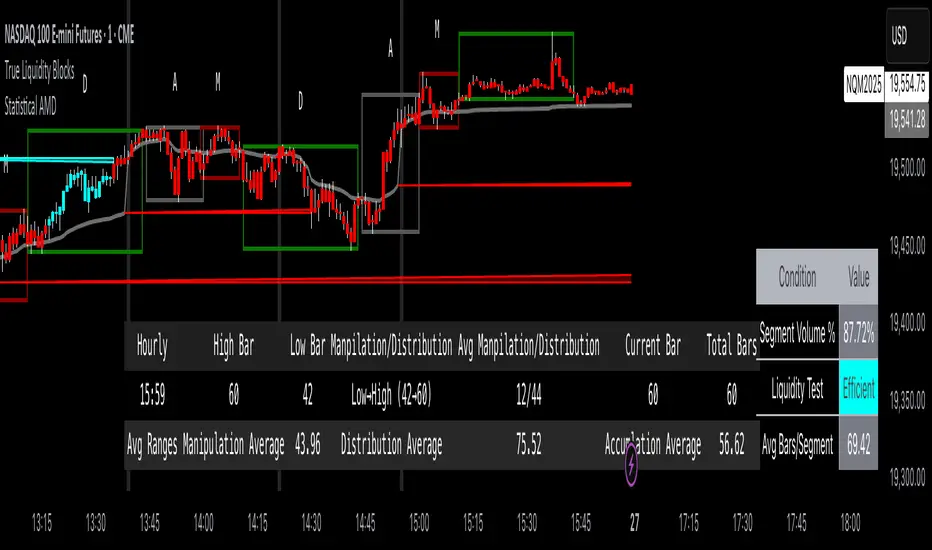

True Liquidity BlocksSo basically I've been deep diving into liquidity trading concepts similar to ICT (Inner Circle Trader) and developed an indicator that breaks down market movement through a volume-centric lens.

Key Concept:

Markets move not just by price, but by resolving trapped positions

Volume segments, not time intervals, show true market dynamics

VWAP (Volume Weighted Average Price) becomes a key structural reference

What Makes This Different:

Tracks volume segments instead of fixed time frames

Identifies "trapped" trader positions

Measures liquidity level efficiency

Color-codes bars based on nearest liquidity zone

Indicator Features:

Cyan/Red liquidity levels showing buy/sell pressure

Efficiency tracking for each level

Dynamic volume-based segmentation

Bar coloring to show nearest liquidity zone

Theoretical Inspiration: Viewed markets as energy systems where:

Positions create potential energy

Price movement resolves this energy

Trends form through systematic position liquidation

VWAP Recalculation in Each Segment:

Segment Start:

VWAP resets when volume threshold User Inputtable (600,000) is reached

Uses the last 4 price values (High, Low, Close, Close) for calculation

Weighted by volume traded during that segment

Calculation Method:

pineCopy = ta.vwap(hlcc4, na(segment_start) ? true : na, 1)

hlcc4: Combines high, low, close prices

na(segment_start): Ensures reset at new segment

Weighted by volume, not equal time intervals

Key Points:

Dynamic recalculation each segment

Reflects most recent trading activity

Provides real-time fair price reference