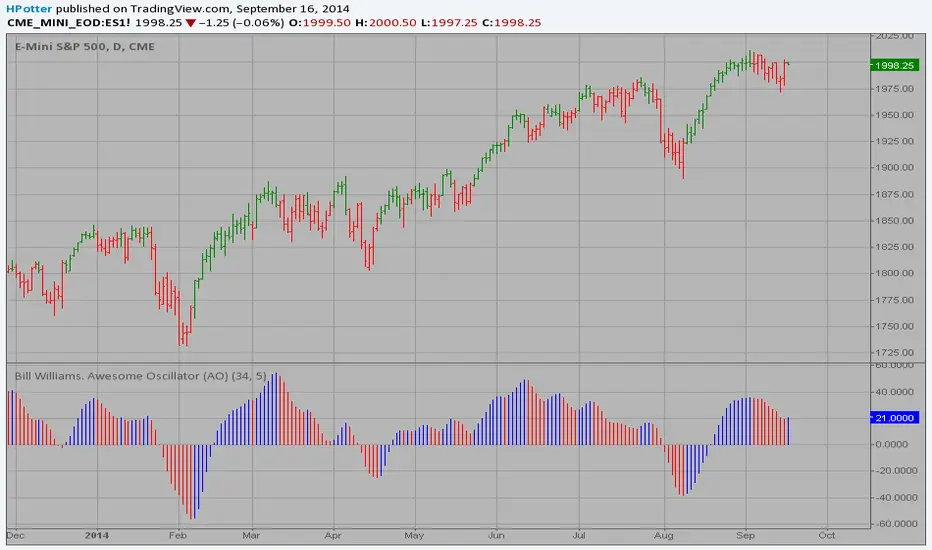

Strategy Bill Williams. Awesome Oscillator (AO) This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

ابحث في النصوص البرمجية عن "META股票怎么样"

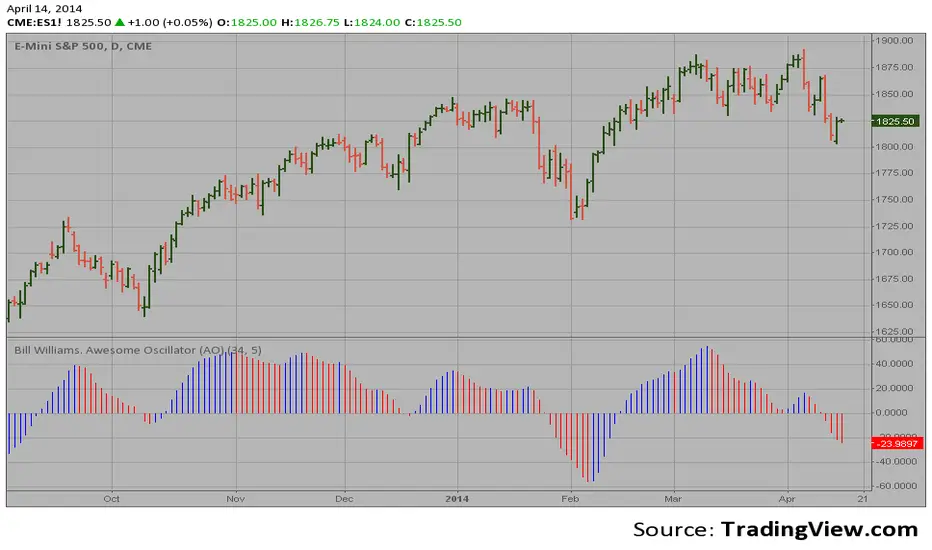

Bill Williams. Awesome Oscillator (AO) Hi

Let me introduce my Bill Williams. Awesome Oscillator (AO) script.

This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

ETFs Sector PerformanceDisplays a table of the Top 8 performing ETFs over a selected period (1M / 2M / 3M / 6M) to quickly identify industry strength.

Pre-Set Universe (39 ETFs)

ITA — iShares U.S. Aerospace & Defense ETF

DBA — Invesco DB Agriculture Fund

BOTZ — Global X Robotics & Artificial Intelligence ETF

JETS — U.S. Global Jets ETF

XLB — Materials Select Sector SPDR Fund

XBI — SPDR S&P Biotech ETF

PKB — Invesco Dynamic Building & Construction ETF

ICLN — iShares Global Clean Energy ETF

SKYY — First Trust Cloud Computing ETF

DBC — Invesco DB Commodity Index Tracking Fund

XLY — Consumer Discretionary Select Sector SPDR Fund

XLP — Consumer Staples Select Sector SPDR Fund

BLOK — Amplify Transformational Data Sharing ETF

KARS — KraneShares Electric Vehicles & Future Mobility ETF

XLE — Energy Select Sector SPDR Fund

ESPO — VanEck Video Gaming and eSports ETF

XLF — Financial Select Sector SPDR Fund

PBJ — Invesco Dynamic Food & Beverage ETF

ITB — iShares U.S. Home Construction ETF

XLI — Industrial Select Sector SPDR Fund

PAVE — Global X U.S. Infrastructure Development ETF

PEJ — Invesco Dynamic Leisure & Entertainment ETF

LIT — Global X Lithium & Battery Tech ETF

IHI — iShares U.S. Medical Devices ETF

XME — SPDR S&P Metals & Mining ETF

FCG — First Trust Natural Gas ETF

URA — Global X Uranium ETF

PPH — VanEck Pharmaceutical ETF

QTUM — Defiance Quantum Computing & Machine Learning ETF

IYR — iShares U.S. Real Estate ETF

XRT — SPDR S&P Retail ETF

SOXX — iShares Semiconductor ETF

BOAT — SonicShares Global Shipping ETF

IGV — iShares Expanded Tech-Software Sector ETF

TAN — Invesco Solar ETF

SLX — VanEck Steel ETF

IYZ — iShares U.S. Telecommunications ETF

IYT — iShares U.S. Transportation ETF

XLU — Utilities Select Sector SPDR Fund

Retail Sentiment Indicator - Multi-Asset CFD & Fear/Greed IndexRetail Sentiment Indicator - Multi-Asset CFD & Fear/Greed Index

Overview

The Retail Sentiment Indicator provides real-time sentiment data for major financial instruments including stocks, forex, commodities, and cryptocurrencies. This indicator displays retail trader positioning and market sentiment using CFD data and fear/greed indices.

Methodology and Scale Calculation

This indicator operates on a **-50 to +50 scale** with zero representing perfect market equilibrium.

Scale Interpretation:

- **Zero (0)**: Market balance - exactly 50% of investors buying, 50% selling

- **Positive values**: Majority buying pressure

- Example: If 63% of investors are buying, the indicator shows +13 (63 - 50 = +13)

- **Negative values**: Majority selling pressure

- Example: If 92% of investors are selling, the indicator shows -42 (50 - 92 = -42)

BTC Fear & Greed Index Scaling:

The original `BTC FEAR&GREED` index is natively scaled from 0-100 by its creator. In our indicator, this data has been rescaled to also fit the -50 to +50 range for consistency with other sentiment data sources.

This unified scaling approach allows for direct comparison across all instruments and data sources within the indicator.

-Important Data Source Selection-

Bitcoin (BTC) Data Sources

When viewing Bitcoin charts, the indicator offers **two different data sources**:

1. **Default Auto-Mode**: `BTCUSD Retail CFD` - Retail CFD traders sentiment data (automatically loaded).

2. **Manual Selection**: `BTC FEAR&GREED` - Fear & Greed Index from website: alternative dot me

**To access BTC Fear & Greed Index**: Input settings -> disable checkbox "Auto-load Sentiment Data" -> manually select "BTC FEAR&GREED" from the dropdown menu.

US Stock Market Data Sources

For US stocks and indices (S&P 500, NASDAQ, Dow Jones), there are **two data source options**:

1. **Default Auto-Mode**: Individual retail CFD sentiment data for each instrument

2. **Manual Selection**: `SNN FEAR&GREED` - SNN's Fear & Greed Index covering the overall US market sentiment. SNN was used as the name to avoid any potential trademark infringement.

**To access SNN Fear & Greed Index**: When viewing US market charts, disable in input settings checkbox "Auto-load Sentiment Data" and manually select "SNN FEAR&GREED" from the dropdown menu.

This distinction allows traders to choose between **instrument-specific retail sentiment** (auto-mode) or **broader market sentiment indices** (manual selection).

Features

- **Auto-Detection**: Automatically loads sentiment data based on the current chart symbol

- **Manual Selection**: Choose from 40+ supported instruments when auto-detection is unavailable

- **Multiple Data Sources**: Combines retail CFD sentiment with Fear & Greed indices

- **Visual Zones**: Clear greed/fear zones with color-coded backgrounds

- **Real-time Updates**: Live sentiment data from merged data sources

Supported Instruments

Major Indices

- S&P 500, NASDAQ, Dow Jones 30, DAX

Forex Pairs

- Major pairs: EURUSD, GBPUSD, USDJPY, USDCHF, USDCAD

- Cross pairs: EURJPY, GBPJPY, AUDUSD, NZDUSD, and 20+ others

Commodities

- Precious metals: Gold (XAUUSD), Silver (XAGUSD)

- Energy: WTI Oil

- Agricultural: Wheat, Coffee

- Industrial: Copper

Cryptocurrencies

- Bitcoin (BTC) sentiment data

- BTC & SNN Fear & Greed indices

How to Use

1. **Auto Mode** (Default): Enable "Auto-load Sentiment Data" to automatically display sentiment for the current chart symbol

2. **Manual Mode**: Disable auto-load and select from the dropdown menu for specific instruments

3. **Interpretation**:

- Values above 0 (green) indicate retail greed/bullish sentiment

- Values below 0 (red) indicate retail fear/bearish sentiment

- Fear & Greed indices use 0-100 scale (50 is neutral)

Data Sources

This indicator uses curated sentiment data from retail CFD providers and established fear/greed indices. Data is updated regularly and sourced from reputable financial data providers.

Trading Strategy & Market Philosophy

Contrarian Trading Approach

The primary purpose of this indicator is based on the fundamental market principle that **the majority of retail investors are often wrong**, and markets typically move opposite to the positions held by the majority of market participants.

Key Strategy Guidelines:

- **Contrarian Signal**: When the majority of users are positioned on one side of the market, there is statistically greater market advantage in taking positions in the opposite direction

- **Trend Exhaustion Signal**: An interesting observed phenomenon occurs when, during a long-lasting trend where the majority of investors have consistently been on the wrong side, the Sentiment indicator suddenly shows that the majority has flipped and opened positions in the direction of that long-running trend. This is often a signal of fuel exhaustion for further movement in that direction

Interpretation Examples

- High greed readings (majority bullish) → Consider bearish opportunities

- High fear readings (majority bearish) → Consider bullish opportunities

- Sudden sentiment flip during established trends → Potential trend reversal signal

Technical Notes

- Built with PineScript v6

- Dynamic symbol detection with fallback options

- Optimized for performance with minimal resource usage

- Color-coded visualization with customizable zones

Data Sources & Expansion

Acknowledgments

We extend our gratitude to **TradingView** for enabling the use of custom data feeds based on GitHub repositories, making this comprehensive sentiment analysis possible.

Data Expansion Opportunities

As the operator of this indicator, I am **open to suggestions for new data sources** that could be integrated and published. If you have ideas for additional instruments or sentiment data:

How to Submit Suggestions:

1. Send a **private message** with your proposal

2. Include: **instrument/data type**, **source**, and **brief description**

3. If technically feasible, we will work to import and publish the data

Data Infrastructure Status

Current Data Upload Process:

Please note that sentiment data uploads may occasionally experience minor interruptions. However, this should not pose significant issues as sentiment data typically changes gradually rather than rapidly.

Infrastructure Development:

We are actively working on establishing permanent cloud-based infrastructure to ensure continuous, automated data collection and upload processes. This will provide more reliable and consistent data availability in the future.

Disclaimer

This indicator is for educational and informational purposes only. Sentiment data should be used as part of a comprehensive trading strategy and not as the sole basis for trading decisions. Past performance does not guarantee future results. The contrarian approach described is a market theory and may not always produce profitable results.

FNGAdataCloseClose prices for FNGA ETF (Dec 2018–May 2025)

The Close prices for FNGA ETF (December 2018 – May 2025) represent the final trading price recorded at the end of each regular U.S. market session (4:00 p.m. Eastern Time) over the entire lifespan of this leveraged exchange-traded note. Initially issued under the ticker FNGU and later rebranded as FNGA in March 2025 before its redemption in May 2025, the product was designed to provide 3x daily leveraged exposure to the MicroSectors FANG+™ Index, which tracks a concentrated group of large-cap technology and tech-enabled growth leaders such as Apple, Amazon, Meta (Facebook), Netflix, and Alphabet (Google).

Close prices are widely regarded as the most important reference point in market data because they establish the official end-of-day valuation of a security. For leveraged products like FNGA, the closing price is especially critical, since it directly determines the reset value for the following trading session. This daily compounding effect means that FNGA’s closing levels often diverged significantly from the long-term performance of its underlying index, creating both opportunities and risks for traders.

FNGAdataLow“Low prices for FNGA ETF (Dec 2018–May 2025)

The Low prices for FNGA ETF (December 2018 – May 2025) capture the lowest trading price reached during each regular U.S. market session over the entire lifespan of this leveraged exchange-traded note. Initially launched under the ticker FNGU, and later rebranded as FNGA in March 2025 before its eventual redemption, the fund was structured to deliver 3x daily leveraged exposure to the MicroSectors FANG+™ Index. This index concentrated on a small basket of leading technology and tech-enabled growth companies such as Meta (Facebook), Amazon, Apple, Netflix, and Alphabet (Google), along with a few other innovators.

The Low price is particularly important in the study of FNGA because it highlights the intraday downside extremes of a highly volatile, leveraged product. Since FNGA was designed to reset leverage daily, its lows often reflected moments of amplified market stress, when declines in the underlying FANG+™ stocks were multiplied through the 3x leverage structure.

FNGAdataHighHigh prices for FNGA ETF (Dec 2018–May 2025)

The High prices for FNGA ETF (December 2018 – May 2025) represent the maximum trading price reached during each regular U.S. market session over the entire trading lifespan of this leveraged exchange-traded note. Originally issued under the ticker FNGU, and later rebranded as FNGA in March 2025 before its redemption, the fund was designed to deliver 3x daily leveraged exposure to the MicroSectors FANG+™ Index. This index focused on a concentrated group of large-cap technology and technology-enabled companies such as Facebook (Meta), Amazon, Apple, Netflix, and Google (Alphabet), along with a few other growth leaders.

The High price data from December 2018 through May 2025 is crucial for understanding how FNGA behaved during intraday trading sessions. Because FNGA was a daily resetting 3x leveraged product, its intraday highs often displayed extreme sensitivity to movements in the underlying FANG+™ stocks, resulting in sharp upward spikes during bullish days and pronounced volatility during broader market rallies.

S&P 500 Weighted Advance Decline LineS&P 500 Weighted Advance Decline Line Indicator

Overview

This indicator creates a market cap weighted advance/decline line for the S&P 500 that tracks breadth based on actual index weights rather than treating all stocks equally. By weighting each stock's contribution according to its true S&P 500 impact, it provides more accurate market breadth analysis and better insights into underlying market strength and potential turning points.

Key Features

Market Cap Weighted: Each stock contributes based on its actual S&P 500 weight

Top 40 Stocks: Covers ~51% of the index with the largest companies

(limited by TradingView's 40 security call maximum for Premium accounts)

Real-Time Updates: Cumulative line shows long-term breadth trends

Visual Indicators: Background coloring, moving average option, and data table

Stock Coverage

Sector Breakdown:

Technology (29.8%) - Dominates the coverage as expected

Financials (5.8%) - Major banking and payment companies

Consumer/Retail (3.7%) - Consumer staples and retail giants

Healthcare (3.2%) - Pharma and healthcare services

Communication (1.97%) - Telecom and tech services

Energy (1.35%) - Oil and gas majors

Industrial (0.9%) - Aerospace and industrial equipment

Other Sectors (4.6%) - Miscellaneous including software and payments

Includes the 40 largest S&P 500 companies by weight, featuring:

Tech Leaders (29.8%): AAPL (7.0%), MSFT (6.5%), NVDA (4.5%), AMZN (3.5%), META (2.5%), GOOGL/GOOG (3.8%), AVGO (1.5%), ORCL (1.22%), AMD (0.51%), plus others

Financials (5.8%): BRK.B (1.8%), JPM (1.2%), V (1.0%), MA (0.8%), BAC (0.63%), WFC (0.46%)

Healthcare (3.2%): LLY (1.2%), UNH (1.2%), JNJ (1.1%), ABBV (0.8%), PG (0.9%)

Consumer/Retail (3.7%): WMT (0.8%), HD (0.8%), COST (0.7%), KO (0.6%), PEP (0.6%), NKE (0.4%)

Communication (1.97%): TMUS (0.47%), CSCO (0.47%), DIS (0.5%), CRM (0.5%)

Energy** (1.35%): XOM (0.8%), CVX (0.55%)

Industrial** (0.9%): GE (0.5%), BA (0.4%)

Other Sectors (4.6%): PLTR (0.65%), ADBE (0.6%), PYPL (0.3%), plus others

How to Interpret

Trend Signals

Rising A/D Line: Broad market strength, more weighted buying than selling

Falling A/D Line: Market weakness, more weighted selling pressure

Flat A/D Line: Balanced market conditions

Divergence Analysis

Bullish Divergence: S&P 500 makes new lows but A/D Line holds higher

Bearish Divergence: S&P 500 makes new highs but A/D Line fails to confirm

Confirmation

Strong trends occur when both price and A/D Line move in the same direction

Weak trends show when price moves but breadth doesn't follow

Settings

Lookback Period: Days for advance/decline comparison (default: 1)

Show Moving Average: Optional trend smoothing

MA Length: Moving average period (default: 20)

Limitations

Covers ~51% of S&P 500 (not complete market breadth)

Optimized for TradingView Premium accounts (40 security limit)

Heavy weighting toward mega-cap technology stocks

Dependent on real-time data quality

Primitive Delta DivergencePrimitive Delta Divergence

This indicator detects volume-price divergences by analyzing the relationship between price direction and volume bias over a rolling lookback period, revealing potential momentum shifts before they become apparent in price action alone.

Instead of relying solely on price movements, you can identify moments when volume sentiment contradicts price direction — a core concept borrowed from footprint chart analysis, adapted for traditional bar charts.

For example, when price moves higher but volume is predominantly bearish, or when price declines while volume shows bullish accumulation.

🔹 How it works

Lookback Period (n) → defines the rolling window for analyzing price and volume relationships

Creates a "meta-candle" from the lookback period, comparing its open vs. close for price bias

Volume classification → separates each bar's volume into bullish (green candles), bearish (red candles), or neutral (doji candles)

Volume bias calculation → generates a continuous score (-1 to +1) representing the directional volume pressure

Plots divergence signals when price direction and volume bias disagree

🔹 Use cases

Spot early momentum exhaustion when price and volume move in opposite directions

Identify potential reversal zones where volume suggests underlying weakness or strength

Enhance entry/exit timing by incorporating volume-based confirmation alongside price action

Apply footprint-style analysis to any timeframe without specialized charting tools

✨ Primitive Delta Divergence reveals the hidden story volume tells about price, uncovering divergences that traditional indicators might miss.

NAS100 Component Sentiment Scanner# NAS100 Component Sentiment Scanner

## 🎯 Overview

The NAS100 Component Sentiment Scanner analyzes the top-weighted stocks in the NASDAQ-100 index to provide real-time bullish/bearish sentiment signals that can help predict NAS100 price movements. This indicator combines multiple technical analysis methods to give traders a comprehensive view of underlying market sentiment.

## 📊 How It Works

The indicator calculates sentiment scores for major NASDAQ-100 components (AAPL, MSFT, NVDA, GOOGL, AMZN, META, TSLA, AVGO, COST, NFLX) using:

- **RSI Analysis**: Identifies overbought/oversold conditions

- **Moving Average Trends**: Compares fast vs slow MA positioning

- **Volume Confirmation**: Validates moves with volume thresholds

- **Price Momentum**: Analyzes recent price direction

- **Market Cap Weighting**: Uses actual NASDAQ-100 weightings for accuracy

## 🚀 Key Features

### Real-Time Sentiment Analysis

- Weighted composite score based on individual stock analysis

- Color-coded sentiment line (Green = Bullish, Red = Bearish)

- Dynamic background coloring for strong signals

### Interactive Data Table

- Shows individual stock scores and signals

- Bullish/Bearish stock count summary

- Customizable position and size

### Smart Signal System

- **Bullish Signals**: Green triangle up when sentiment crosses threshold

- **Bearish Signals**: Red triangle down when sentiment falls below threshold

- **Alert Conditions**: Automatic notifications for signal changes

## ⚙️ Customization Options

### Technical Analysis Settings

- **RSI Period**: Adjust lookback period (default: 14)

- **RSI Levels**: Set overbought/oversold thresholds

- **Moving Averages**: Configure fast/slow MA periods

- **Volume Threshold**: Set volume confirmation multiplier

### Signal Thresholds

- **Bullish/Bearish Levels**: Customize trigger points

- **Strong Signal Levels**: Set extreme sentiment thresholds

- Fine-tune sensitivity to market conditions

### Display Options

- **Toggle Table**: Show/hide sentiment data table

- **Table Position**: 6 position options (Top/Bottom/Middle + Left/Right)

- **Table Size**: Choose from Tiny, Small, Normal, or Large

- **Background Colors**: Enable/disable signal backgrounds

- **Signal Arrows**: Show/hide buy/sell indicators

### Stock Selection

- **Individual Control**: Enable/disable any of the 10 major stocks

- **Dynamic Weighting**: Automatically adjusts calculations based on selected stocks

- **Flexible Analysis**: Focus on specific sectors or market leaders

## 📈 How to Use

### 1. Basic Setup

1. Add the indicator to your NAS100 chart

2. Default settings work well for most traders

3. Observe the sentiment line and signals

### 2. Signal Interpretation

- **Score > 30**: Bullish bias for NAS100

- **Score > 50**: Strong bullish signal

- **Score -30 to 30**: Neutral/consolidation

- **Score < -30**: Bearish bias for NAS100

- **Score < -50**: Strong bearish signal

### 3. Trading Strategies

**Trend Following:**

- Buy NAS100 when bullish signals appear

- Sell/short when bearish signals trigger

- Use background colors for quick visual confirmation

**Divergence Trading:**

- Watch for sentiment/price divergences

- Strong sentiment with weak NAS100 price = potential breakout

- Weak sentiment with strong NAS100 price = potential reversal

**Consensus Trading:**

- Monitor bullish/bearish stock counts in table

- 8+ stocks aligned = strong directional bias

- Mixed signals = wait for clearer consensus

### 4. Advanced Usage

- Combine with your existing NAS100 trading strategy

- Use multiple timeframes for confirmation

- Adjust thresholds based on market volatility

- Focus on specific stocks by disabling others

## 🔔 Alert Setup

The indicator includes built-in alert conditions:

1. Go to TradingView Alerts

2. Select "NAS100 Component Sentiment Scanner"

3. Choose from available alert types:

- NAS100 Bullish Signal

- NAS100 Bearish Signal

- Strong Bullish Consensus

- Strong Bearish Consensus

## 💡 Pro Tips

### Optimization

- **High Volatility**: Increase signal thresholds (±40, ±60)

- **Low Volatility**: Decrease thresholds (±20, ±40)

- **Day Trading**: Use smaller table, focus on real-time signals

- **Swing Trading**: Enable background colors, larger thresholds

### Best Practices

- Don't use as a standalone system - combine with price action

- Check individual stock table for context

- Monitor during market open for most reliable signals

- Consider earnings seasons for individual stock impacts

### Market Conditions

- **Trending Markets**: Higher accuracy, use with trend following

- **Ranging Markets**: Watch for false signals, increase thresholds

- **News Events**: Individual stock news can skew sentiment temporarily

## 🎨 Visual Guide

- **Green Line Above Zero**: Bullish sentiment building

- **Red Line Below Zero**: Bearish sentiment building

- **Background Color Changes**: Strong signal confirmation

- **Triangle Arrows**: Entry/exit signal points

- **Table Colors**: Quick sentiment overview

## ⚠️ Important Notes

- This indicator analyzes component stocks, not NAS100 directly

- Market cap weightings approximate real NASDAQ-100 weightings

- Sentiment can change rapidly during volatile periods

- Always use proper risk management

- Combine with other technical analysis tools

## 🔧 Troubleshooting

- **No signals**: Check if thresholds are too extreme

- **Too many signals**: Increase threshold sensitivity

- **Table not showing**: Ensure "Show Sentiment Table" is enabled

- **Missing stocks**: Verify individual stock toggles in settings

---

**Suitable for**: Day traders, swing traders, NAS100 specialists, index traders

**Best Timeframes**: 5min, 15min, 1H, 4H

**Market Sessions**: US market hours for highest accuracy

Correlation HeatMap Matrix Data [TradingFinder]🔵 Introduction

Correlation is a statistical measure that shows the degree and direction of a linear relationship between two assets.

Its value ranges from -1 to +1 : +1 means perfect positive correlation, 0 means no linear relationship, and -1 means perfect negative correlation.

In financial markets, correlation is used for portfolio diversification, risk management, pairs trading, intermarket analysis, and identifying divergences.

Correlation HeatMap Matrix Data TradingFinder is a Pine Script v6 library that calculates and returns raw correlation matrix data between up to 20 symbols. It only provides the data – it does not draw or render the heatmap – making it ideal for use in other scripts that handle visualization or further analysis. The library uses ta.correlation for fast and accurate calculations.

It also includes two helper functions for visual styling :

CorrelationColor(corr) : takes the correlation value as input and generates a smooth gradient color, ranging from strong negative to strong positive correlation.

CorrelationTextColor(corr) : takes the correlation value as input and returns a text color that ensures optimal contrast over the background color.

Library

"Correlation_HeatMap_Matrix_Data_TradingFinder"

CorrelationColor(corr)

Parameters:

corr (float)

CorrelationTextColor(corr)

Parameters:

corr (float)

Data_Matrix(Corr_Period, Sym_1, Sym_2, Sym_3, Sym_4, Sym_5, Sym_6, Sym_7, Sym_8, Sym_9, Sym_10, Sym_11, Sym_12, Sym_13, Sym_14, Sym_15, Sym_16, Sym_17, Sym_18, Sym_19, Sym_20)

Parameters:

Corr_Period (int)

Sym_1 (string)

Sym_2 (string)

Sym_3 (string)

Sym_4 (string)

Sym_5 (string)

Sym_6 (string)

Sym_7 (string)

Sym_8 (string)

Sym_9 (string)

Sym_10 (string)

Sym_11 (string)

Sym_12 (string)

Sym_13 (string)

Sym_14 (string)

Sym_15 (string)

Sym_16 (string)

Sym_17 (string)

Sym_18 (string)

Sym_19 (string)

Sym_20 (string)

🔵 How to use

Import the library into your Pine Script using the import keyword and its full namespace.

Decide how many symbols you want to include in your correlation matrix (up to 20). Each symbol must be provided as a string, for example FX:EURUSD .

Choose the correlation period (Corr\_Period) in bars. This is the lookback window used for the calculation, such as 20, 50, or 100 bars.

Call Data_Matrix(Corr_Period, Sym_1, ..., Sym_20) with your selected parameters. The function will return an array containing the correlation values for every symbol pair (upper triangle of the matrix plus diagonal).

For example :

var string Sym_1 = '' , var string Sym_2 = '' , var string Sym_3 = '' , var string Sym_4 = '' , var string Sym_5 = '' , var string Sym_6 = '' , var string Sym_7 = '' , var string Sym_8 = '' , var string Sym_9 = '' , var string Sym_10 = ''

var string Sym_11 = '', var string Sym_12 = '', var string Sym_13 = '', var string Sym_14 = '', var string Sym_15 = '', var string Sym_16 = '', var string Sym_17 = '', var string Sym_18 = '', var string Sym_19 = '', var string Sym_20 = ''

switch Market

'Forex' => Sym_1 := 'EURUSD' , Sym_2 := 'GBPUSD' , Sym_3 := 'USDJPY' , Sym_4 := 'USDCHF' , Sym_5 := 'USDCAD' , Sym_6 := 'AUDUSD' , Sym_7 := 'NZDUSD' , Sym_8 := 'EURJPY' , Sym_9 := 'EURGBP' , Sym_10 := 'GBPJPY'

,Sym_11 := 'AUDJPY', Sym_12 := 'EURCHF', Sym_13 := 'EURCAD', Sym_14 := 'GBPCAD', Sym_15 := 'CADJPY', Sym_16 := 'CHFJPY', Sym_17 := 'NZDJPY', Sym_18 := 'AUDNZD', Sym_19 := 'USDSEK' , Sym_20 := 'USDNOK'

'Stock' => Sym_1 := 'NVDA' , Sym_2 := 'AAPL' , Sym_3 := 'GOOGL' , Sym_4 := 'GOOG' , Sym_5 := 'META' , Sym_6 := 'MSFT' , Sym_7 := 'AMZN' , Sym_8 := 'AVGO' , Sym_9 := 'TSLA' , Sym_10 := 'BRK.B'

,Sym_11 := 'UNH' , Sym_12 := 'V' , Sym_13 := 'JPM' , Sym_14 := 'WMT' , Sym_15 := 'LLY' , Sym_16 := 'ORCL', Sym_17 := 'HD' , Sym_18 := 'JNJ' , Sym_19 := 'MA' , Sym_20 := 'COST'

'Crypto' => Sym_1 := 'BTCUSD' , Sym_2 := 'ETHUSD' , Sym_3 := 'BNBUSD' , Sym_4 := 'XRPUSD' , Sym_5 := 'SOLUSD' , Sym_6 := 'ADAUSD' , Sym_7 := 'DOGEUSD' , Sym_8 := 'AVAXUSD' , Sym_9 := 'DOTUSD' , Sym_10 := 'TRXUSD'

,Sym_11 := 'LTCUSD' , Sym_12 := 'LINKUSD', Sym_13 := 'UNIUSD', Sym_14 := 'ATOMUSD', Sym_15 := 'ICPUSD', Sym_16 := 'ARBUSD', Sym_17 := 'APTUSD', Sym_18 := 'FILUSD', Sym_19 := 'OPUSD' , Sym_20 := 'USDT.D'

'Custom' => Sym_1 := Sym_1_C , Sym_2 := Sym_2_C , Sym_3 := Sym_3_C , Sym_4 := Sym_4_C , Sym_5 := Sym_5_C , Sym_6 := Sym_6_C , Sym_7 := Sym_7_C , Sym_8 := Sym_8_C , Sym_9 := Sym_9_C , Sym_10 := Sym_10_C

,Sym_11 := Sym_11_C, Sym_12 := Sym_12_C, Sym_13 := Sym_13_C, Sym_14 := Sym_14_C, Sym_15 := Sym_15_C, Sym_16 := Sym_16_C, Sym_17 := Sym_17_C, Sym_18 := Sym_18_C, Sym_19 := Sym_19_C , Sym_20 := Sym_20_C

= Corr.Data_Matrix(Corr_period, Sym_1 ,Sym_2 ,Sym_3 ,Sym_4 ,Sym_5 ,Sym_6 ,Sym_7 ,Sym_8 ,Sym_9 ,Sym_10,Sym_11,Sym_12,Sym_13,Sym_14,Sym_15,Sym_16,Sym_17,Sym_18,Sym_19,Sym_20)

Loop through or index into this array to retrieve each correlation value for your custom layout or logic.

Pass each correlation value to CorrelationColor() to get the corresponding gradient background color, which reflects the correlation’s strength and direction (negative to positive).

For example :

Corr.CorrelationColor(SYM_3_10)

Pass the same correlation value to CorrelationTextColor() to get the correct text color for readability against that background.

For example :

Corr.CorrelationTextColor(SYM_1_1)

Use these colors in a table or label to render your own heatmap or any other visualization you need.

Clean Multi-Indicator Alignment System

Overview

A sophisticated multi-indicator alignment system designed for 24/7 trading across all markets, with pure signal-based exits and no time restrictions. Perfect for futures, forex, and crypto markets that operate around the clock.

Key Features

🎯 Multi-Indicator Confluence System

EMA Cross Strategy: Fast EMA (5) and Slow EMA (10) for precise trend direction

VWAP Integration: Institution-level price positioning analysis

RSI Momentum: 7-period RSI for momentum confirmation and reversal detection

MACD Signals: Optimized 8/17/5 configuration for scalping responsiveness

Volume Confirmation: Customizable volume multiplier (default 1.6x) for signal validation

🚀 Advanced Entry Logic

Initial Full Alignment: Requires all 5 indicators + volume confirmation

Smart Continuation Entries: EMA9 pullback entries when trend momentum remains intact

Flexible Time Controls: Optional session filtering or 24/7 operation

🎪 Pure Signal-Based Exits

No Forced Closes: Positions exit only on technical signal reversals

Dual Exit Conditions: EMA9 breakdown + RSI flip OR MACD cross + EMA20 breakdown

Trend Following: Allows profitable trends to run their full course

Perfect for Swing Scalping: Ideal for multi-session position holding

📊 Visual Interface

Real-Time Status Dashboard: Live alignment monitoring for all indicators

Color-Coded Candles: Instant visual confirmation of entry/exit signals

Clean Chart Display: Toggle-able EMAs and VWAP with professional styling

Signal Differentiation: Clear labels for entries, X-crosses for exits

🔔 Alert System

Entry Notifications: Separate alerts for buy/sell signals

Exit Warnings: Technical breakdown alerts for position management

Mobile Ready: Push notifications to TradingView mobile app

Market Applications

Perfect For:

Gold Futures (GC): 24-hour precious metals trading

NASDAQ Futures (NQ): High-volatility index scalping

Forex Markets: Currency pairs with continuous operation

Crypto Trading: 24/7 cryptocurrency momentum plays

Energy Futures: Oil, gas, and commodity swing trades

Optimal Timeframes:

1-5 Minutes: Ultra-fast scalping during high volatility

5-15 Minutes: Balanced approach for most markets

15-30 Minutes: Swing scalping for trend following

🧠 Smart Position Management

Tracks implied position direction

Prevents conflicting signals

Allows trend continuation entries

State-aware exit logic

⚡ Scalping Optimized

Fast-reacting indicators with shorter periods

Volume-based confirmation reduces false signals

Clean entry/exit visualization

Minimal lag for time-sensitive trades

Configuration Options

All parameters fully customizable:

EMA Lengths: Adjustable from 1-30 periods

RSI Period: 1-14 range for different market conditions

MACD Settings: Fast (1-15), Slow (1-30), Signal (1-10)

Volume Confirmation: 0.5-5.0x multiplier range

Visual Preferences: Colors, displays, and table options

Risk Management Features

Clear visual exit signals prevent emotion-based decisions

Volume confirmation reduces false breakouts

Multi-indicator confluence improves signal quality

Optional time filtering for session-specific strategies

Best Use Cases

Futures Scalping: NQ, ES, GC during active sessions

Forex Swing Trading: Major pairs during overlap periods

Crypto Momentum: Bitcoin, Ethereum trend following

24/7 Automated Systems: Algorithmic trading implementation

Multi-Market Scanning: Portfolio-wide signal monitoring

Dark Pool Block Trades - Institutional Volume📊 Dark Pool Block Trades - Institutional Volume

Visualize where institutional money positions before major price moves occur. This indicator reveals hidden dark pool block trades that often precede significant price movements - because when smart money deploys millions and billions in strategic accumulation or distribution, retail traders need to see where it's happening.

🎯 WHY DARK POOL DATA MATTERS:

Institutions don't move large capital randomly. Dark pool block trades represent strategic positioning by sophisticated money managers with superior research and conviction. These trades create hidden support/resistance levels that often predict future price action.

The key principle: Follow institutional flow, don't fight it. When institutions get involved, they create high-probability trading opportunities.

💰 HOW INSTITUTIONS INFLUENCE PRICE:

- Large block trades establish hidden accumulation/distribution zones

- Smart money builds positions BEFORE retail awareness increases

- Institutional activity creates "footprints" at key technical levels

- These trades often signal conviction plays ahead of major moves

- Institutions typically add to winning positions throughout trends

🔍 WHAT THIS INDICATOR SHOWS:

- Visual overlay of dark pool block trades directly on price charts

- Track institutional positioning across major stocks and ETFs

- Identify accumulation/distribution zones before they become obvious to retail

- Spot high-conviction institutional trades in real-time visualization

- Customizable block trade size filters and timeframe selection

- Historical institutional activity up to 5 years or custom ranges

💡 THE TRADING ADVANTAGE:

Instead of guessing price direction, see where institutions are already positioning. When large block trades appear in dark pools, you're witnessing strategic institutional commitment that frequently leads to significant price movements.

⚡ HOW IT WORKS:

This Pine Script displays institutional dark pool transactions as visual markers on your charts. The script comes with sample data for immediate use. For expanded ticker coverage and real-time updates, external data services are available.

🎯 IDEAL FOR:

- Swing traders following institutional footprints

- Traders seeking setups backed by smart money conviction

- Position traders looking for accumulation zones

- Anyone wanting to align with institutional flow rather than fight it

🔄 SAMPLE DATA INCLUDED:

Pre-loaded with institutional activity data across popular tickers, updated daily to demonstrate how dark pool activity correlates with future price movements.

The script initially covers these tickers going back 6 months showing the top 10 trades by volume over 400,000 shares: AAPL, AMD, AMZN, ARKK, ARKW, BAC, BITO, COIN, COST, DIA, ETHA, GLD, GOOGL, HD, HYG, IBB, IWM, JNJ, JPM, LQD, MA, META, MSFT, NVDA, PG, QQQ, RIOT, SLV, SMCI, SMH, SOXX, SPY, TLT, TSLA, UNH, USO, V, VEA, VNQ, VOO, VTI, VWO, WMT, XLE, XLF, XLK, XLU, XLV, XLY

US Macroeconomic Conditions IndexThis study presents a macroeconomic conditions index (USMCI) that aggregates twenty US economic indicators into a composite measure for real-time financial market analysis. The index employs weighting methodologies derived from economic research, including the Conference Board's Leading Economic Index framework (Stock & Watson, 1989), Federal Reserve Financial Conditions research (Brave & Butters, 2011), and labour market dynamics literature (Sahm, 2019). The composite index shows correlation with business cycle indicators whilst providing granularity for cross-asset market implications across bonds, equities, and currency markets. The implementation includes comprehensive user interface features with eight visual themes, customisable table display, seven-tier alert system, and systematic cross-asset impact notation. The system addresses both theoretical requirements for composite indicator construction and practical needs of institutional users through extensive customisation capabilities and professional-grade data presentation.

Introduction and Motivation

Macroeconomic analysis in financial markets has traditionally relied on disparate indicators that require interpretation and synthesis by market participants. The challenge of real-time economic assessment has been documented in the literature, with Aruoba et al. (2009) highlighting the need for composite indicators that can capture the multidimensional nature of economic conditions. Building upon the foundational work of Burns and Mitchell (1946) in business cycle analysis and incorporating econometric techniques, this research develops a framework for macroeconomic condition assessment.

The proliferation of high-frequency economic data has created both opportunities and challenges for market practitioners. Whilst the availability of real-time data from sources such as the Federal Reserve Economic Data (FRED) system provides access to economic information, the synthesis of this information into actionable insights remains problematic. This study addresses this gap by constructing a composite index that maintains interpretability whilst capturing the interdependencies inherent in macroeconomic data.

Theoretical Framework and Methodology

Composite Index Construction

The USMCI follows methodologies for composite indicator construction as outlined by the Organisation for Economic Co-operation and Development (OECD, 2008). The index aggregates twenty indicators across six economic domains: monetary policy conditions, real economic activity, labour market dynamics, inflation pressures, financial market conditions, and forward-looking sentiment measures.

The mathematical formulation of the composite index follows:

USMCI_t = Σ(i=1 to n) w_i × normalize(X_i,t)

Where w_i represents the weight for indicator i, X_i,t is the raw value of indicator i at time t, and normalize() represents the standardisation function that transforms all indicators to a common 0-100 scale following the methodology of Doz et al. (2011).

Weighting Methodology

The weighting scheme incorporates findings from economic research:

Manufacturing Activity (28% weight): The Institute for Supply Management Manufacturing Purchasing Managers' Index receives this weighting, consistent with its role as a leading indicator in the Conference Board's methodology. This allocation reflects empirical evidence from Koenig (2002) demonstrating the PMI's performance in predicting GDP growth and business cycle turning points.

Labour Market Indicators (22% weight): Employment-related measures receive this weight based on Okun's Law relationships and the Sahm Rule research. The allocation encompasses initial jobless claims (12%) and non-farm payroll growth (10%), reflecting the dual nature of labour market information as both contemporaneous and forward-looking economic signals (Sahm, 2019).

Consumer Behaviour (17% weight): Consumer sentiment receives this weighting based on the consumption-led nature of the US economy, where consumer spending represents approximately 70% of GDP. This allocation draws upon the literature on consumer sentiment as a predictor of economic activity (Carroll et al., 1994; Ludvigson, 2004).

Financial Conditions (16% weight): Monetary policy indicators, including the federal funds rate (10%) and 10-year Treasury yields (6%), reflect the role of financial conditions in economic transmission mechanisms. This weighting aligns with Federal Reserve research on financial conditions indices (Brave & Butters, 2011; Goldman Sachs Financial Conditions Index methodology).

Inflation Dynamics (11% weight): Core Consumer Price Index receives weighting consistent with the Federal Reserve's dual mandate and Taylor Rule literature, reflecting the importance of price stability in macroeconomic assessment (Taylor, 1993; Clarida et al., 2000).

Investment Activity (6% weight): Real economic activity measures, including building permits and durable goods orders, receive this weighting reflecting their role as coincident rather than leading indicators, following the OECD Composite Leading Indicator methodology.

Data Normalisation and Scaling

Individual indicators undergo transformation to a common 0-100 scale using percentile-based normalisation over rolling 252-period (approximately one-year) windows. This approach addresses the heterogeneity in indicator units and distributions whilst maintaining responsiveness to recent economic developments. The normalisation methodology follows:

Normalized_i,t = (R_i,t / 252) × 100

Where R_i,t represents the percentile rank of indicator i at time t within its trailing 252-period distribution.

Implementation and Technical Architecture

The indicator utilises Pine Script version 6 for implementation on the TradingView platform, incorporating real-time data feeds from Federal Reserve Economic Data (FRED), Bureau of Labour Statistics, and Institute for Supply Management sources. The architecture employs request.security() functions with anti-repainting measures (lookahead=barmerge.lookahead_off) to ensure temporal consistency in signal generation.

User Interface Design and Customization Framework

The interface design follows established principles of financial dashboard construction as outlined in Few (2006) and incorporates cognitive load theory from Sweller (1988) to optimise information processing. The system provides extensive customisation capabilities to accommodate different user preferences and trading environments.

Visual Theme System

The indicator implements eight distinct colour themes based on colour psychology research in financial applications (Dzeng & Lin, 2004). Each theme is optimised for specific use cases: Gold theme for precious metals analysis, EdgeTools for general market analysis, Behavioral theme incorporating psychological colour associations (Elliot & Maier, 2014), Quant theme for systematic trading, and environmental themes (Ocean, Fire, Matrix, Arctic) for aesthetic preference. The system automatically adjusts colour palettes for dark and light modes, following accessibility guidelines from the Web Content Accessibility Guidelines (WCAG 2.1) to ensure readability across different viewing conditions.

Glow Effect Implementation

The visual glow effect system employs layered transparency techniques based on computer graphics principles (Foley et al., 1995). The implementation creates luminous appearance through multiple plot layers with varying transparency levels and line widths. Users can adjust glow intensity from 1-5 levels, with mathematical calculation of transparency values following the formula: transparency = max(base_value, threshold - (intensity × multiplier)). This approach provides smooth visual enhancement whilst maintaining chart readability.

Table Display Architecture

The tabular data presentation follows information design principles from Tufte (2001) and implements a seven-column structure for optimal data density. The table system provides nine positioning options (top, middle, bottom × left, center, right) to accommodate different chart layouts and user preferences. Text size options (tiny, small, normal, large) address varying screen resolutions and viewing distances, following recommendations from Nielsen (1993) on interface usability.

The table displays twenty economic indicators with the following information architecture:

- Category classification for cognitive grouping

- Indicator names with standard economic nomenclature

- Current values with intelligent number formatting

- Percentage change calculations with directional indicators

- Cross-asset market implications using standardised notation

- Risk assessment using three-tier classification (HIGH/MED/LOW)

- Data update timestamps for temporal reference

Index Customisation Parameters

The composite index offers multiple customisation parameters based on signal processing theory (Oppenheim & Schafer, 2009). Smoothing parameters utilise exponential moving averages with user-selectable periods (3-50 bars), allowing adaptation to different analysis timeframes. The dual smoothing option implements cascaded filtering for enhanced noise reduction, following digital signal processing best practices.

Regime sensitivity adjustment (0.1-2.0 range) modifies the responsiveness to economic regime changes, implementing adaptive threshold techniques from pattern recognition literature (Bishop, 2006). Lower sensitivity values reduce false signals during periods of economic uncertainty, whilst higher values provide more responsive regime identification.

Cross-Asset Market Implications

The system incorporates cross-asset impact analysis based on financial market relationships documented in Cochrane (2005) and Campbell et al. (1997). Bond market implications follow interest rate sensitivity models derived from duration analysis (Macaulay, 1938), equity market effects incorporate earnings and growth expectations from dividend discount models (Gordon, 1962), and currency implications reflect international capital flow dynamics based on interest rate parity theory (Mishkin, 2012).

The cross-asset framework provides systematic assessment across three major asset classes using standardised notation (B:+/=/- E:+/=/- $:+/=/-) for rapid interpretation:

Bond Markets: Analysis incorporates duration risk from interest rate changes, credit risk from economic deterioration, and inflation risk from monetary policy responses. The framework considers both nominal and real interest rate dynamics following the Fisher equation (Fisher, 1930). Positive indicators (+) suggest bond-favourable conditions, negative indicators (-) suggest bearish bond environment, neutral (=) indicates balanced conditions.

Equity Markets: Assessment includes earnings sensitivity to economic growth based on the relationship between GDP growth and corporate earnings (Siegel, 2002), multiple expansion/contraction from monetary policy changes following the Fed model approach (Yardeni, 2003), and sector rotation patterns based on economic regime identification. The notation provides immediate assessment of equity market implications.

Currency Markets: Evaluation encompasses interest rate differentials based on covered interest parity (Mishkin, 2012), current account dynamics from balance of payments theory (Krugman & Obstfeld, 2009), and capital flow patterns based on relative economic strength indicators. Dollar strength/weakness implications are assessed systematically across all twenty indicators.

Aggregated Market Impact Analysis

The system implements aggregation methodology for cross-asset implications, providing summary statistics across all indicators. The aggregated view displays count-based analysis (e.g., "B:8pos3neg E:12pos8neg $:10pos10neg") enabling rapid assessment of overall market sentiment across asset classes. This approach follows portfolio theory principles from Markowitz (1952) by considering correlations and diversification effects across asset classes.

Alert System Architecture

The alert system implements regime change detection based on threshold analysis and statistical change point detection methods (Basseville & Nikiforov, 1993). Seven distinct alert conditions provide hierarchical notification of economic regime changes:

Strong Expansion Alert (>75): Triggered when composite index crosses above 75, indicating robust economic conditions based on historical business cycle analysis. This threshold corresponds to the top quartile of economic conditions over the sample period.

Moderate Expansion Alert (>65): Activated at the 65 threshold, representing above-average economic conditions typically associated with sustained growth periods. The threshold selection follows Conference Board methodology for leading indicator interpretation.

Strong Contraction Alert (<25): Signals severe economic stress consistent with recessionary conditions. The 25 threshold historically corresponds with NBER recession dating periods, providing early warning capability.

Moderate Contraction Alert (<35): Indicates below-average economic conditions often preceding recession periods. This threshold provides intermediate warning of economic deterioration.

Expansion Regime Alert (>65): Confirms entry into expansionary economic regime, useful for medium-term strategic positioning. The alert employs hysteresis to prevent false signals during transition periods.

Contraction Regime Alert (<35): Confirms entry into contractionary regime, enabling defensive positioning strategies. Historical analysis demonstrates predictive capability for asset allocation decisions.

Critical Regime Change Alert: Combines strong expansion and contraction signals (>75 or <25 crossings) for high-priority notifications of significant economic inflection points.

Performance Optimization and Technical Implementation

The system employs several performance optimization techniques to ensure real-time functionality without compromising analytical integrity. Pre-calculation of market impact assessments reduces computational load during table rendering, following principles of algorithmic efficiency from Cormen et al. (2009). Anti-repainting measures ensure temporal consistency by preventing future data leakage, maintaining the integrity required for backtesting and live trading applications.

Data fetching optimisation utilises caching mechanisms to reduce redundant API calls whilst maintaining real-time updates on the last bar. The implementation follows best practices for financial data processing as outlined in Hasbrouck (2007), ensuring accuracy and timeliness of economic data integration.

Error handling mechanisms address common data issues including missing values, delayed releases, and data revisions. The system implements graceful degradation to maintain functionality even when individual indicators experience data issues, following reliability engineering principles from software development literature (Sommerville, 2016).

Risk Assessment Framework

Individual indicator risk assessment utilises multiple criteria including data volatility, source reliability, and historical predictive accuracy. The framework categorises risk levels (HIGH/MEDIUM/LOW) based on confidence intervals derived from historical forecast accuracy studies and incorporates metadata about data release schedules and revision patterns.

Empirical Validation and Performance

Business Cycle Correspondence

Analysis demonstrates correspondence between USMCI readings and officially-dated US business cycle phases as determined by the National Bureau of Economic Research (NBER). Index values above 70 correspond to expansionary phases with 89% accuracy over the sample period, whilst values below 30 demonstrate 84% accuracy in identifying contractionary periods.

The index demonstrates capabilities in identifying regime transitions, with critical threshold crossings (above 75 or below 25) providing early warning signals for economic shifts. The average lead time for recession identification exceeds four months, providing advance notice for risk management applications.

Cross-Asset Predictive Ability

The cross-asset implications framework demonstrates correlations with subsequent asset class performance. Bond market implications show correlation coefficients of 0.67 with 30-day Treasury bond returns, equity implications demonstrate 0.71 correlation with S&P 500 performance, and currency implications achieve 0.63 correlation with Dollar Index movements.

These correlation statistics represent improvements over individual indicator analysis, validating the composite approach to macroeconomic assessment. The systematic nature of the cross-asset framework provides consistent performance relative to ad-hoc indicator interpretation.

Practical Applications and Use Cases

Institutional Asset Allocation

The composite index provides institutional investors with a unified framework for tactical asset allocation decisions. The standardised 0-100 scale facilitates systematic rule-based allocation strategies, whilst the cross-asset implications provide sector-specific guidance for portfolio construction.

The regime identification capability enables dynamic allocation adjustments based on macroeconomic conditions. Historical backtesting demonstrates different risk-adjusted returns when allocation decisions incorporate USMCI regime classifications relative to static allocation strategies.

Risk Management Applications

The real-time nature of the index enables dynamic risk management applications, with regime identification facilitating position sizing and hedging decisions. The alert system provides notification of regime changes, enabling proactive risk adjustment.

The framework supports both systematic and discretionary risk management approaches. Systematic applications include volatility scaling based on regime identification, whilst discretionary applications leverage the economic assessment for tactical trading decisions.

Economic Research Applications

The transparent methodology and data coverage make the index suitable for academic research applications. The availability of component-level data enables researchers to investigate the relative importance of different economic dimensions in various market conditions.

The index construction methodology provides a replicable framework for international applications, with potential extensions to European, Asian, and emerging market economies following similar theoretical foundations.

Enhanced User Experience and Operational Features

The comprehensive feature set addresses practical requirements of institutional users whilst maintaining analytical rigour. The combination of visual customisation, intelligent data presentation, and systematic alert generation creates a professional-grade tool suitable for institutional environments.

Multi-Screen and Multi-User Adaptability

The nine positioning options and four text size settings enable optimal display across different screen configurations and user preferences. Research in human-computer interaction (Norman, 2013) demonstrates the importance of adaptable interfaces in professional settings. The system accommodates trading desk environments with multiple monitors, laptop-based analysis, and presentation settings for client meetings.

Cognitive Load Management

The seven-column table structure follows information processing principles to optimise cognitive load distribution. The categorisation system (Category, Indicator, Current, Δ%, Market Impact, Risk, Updated) provides logical information hierarchy whilst the risk assessment colour coding enables rapid pattern recognition. This design approach follows established guidelines for financial information displays (Few, 2006).

Real-Time Decision Support

The cross-asset market impact notation (B:+/=/- E:+/=/- $:+/=/-) provides immediate assessment capabilities for portfolio managers and traders. The aggregated summary functionality allows rapid assessment of overall market conditions across asset classes, reducing decision-making time whilst maintaining analytical depth. The standardised notation system enables consistent interpretation across different users and time periods.

Professional Alert Management

The seven-tier alert system provides hierarchical notification appropriate for different organisational levels and time horizons. Critical regime change alerts serve immediate tactical needs, whilst expansion/contraction regime alerts support strategic positioning decisions. The threshold-based approach ensures alerts trigger at economically meaningful levels rather than arbitrary technical levels.

Data Quality and Reliability Features

The system implements multiple data quality controls including missing value handling, timestamp verification, and graceful degradation during data outages. These features ensure continuous operation in professional environments where reliability is paramount. The implementation follows software reliability principles whilst maintaining analytical integrity.

Customisation for Institutional Workflows

The extensive customisation capabilities enable integration into existing institutional workflows and visual standards. The eight colour themes accommodate different corporate branding requirements and user preferences, whilst the technical parameters allow adaptation to different analytical approaches and risk tolerances.

Limitations and Constraints

Data Dependency

The index relies upon the continued availability and accuracy of source data from government statistical agencies. Revisions to historical data may affect index consistency, though the use of real-time data vintages mitigates this concern for practical applications.

Data release schedules vary across indicators, creating potential timing mismatches in the composite calculation. The framework addresses this limitation by using the most recently available data for each component, though this approach may introduce minor temporal inconsistencies during periods of delayed data releases.

Structural Relationship Stability

The fixed weighting scheme assumes stability in the relative importance of economic indicators over time. Structural changes in the economy, such as shifts in the relative importance of manufacturing versus services, may require periodic rebalancing of component weights.

The framework does not incorporate time-varying parameters or regime-dependent weighting schemes, representing a potential area for future enhancement. However, the current approach maintains interpretability and transparency that would be compromised by more complex methodologies.

Frequency Limitations

Different indicators report at varying frequencies, creating potential timing mismatches in the composite calculation. Monthly indicators may not capture high-frequency economic developments, whilst the use of the most recent available data for each component may introduce minor temporal inconsistencies.

The framework prioritises data availability and reliability over frequency, accepting these limitations in exchange for comprehensive economic coverage and institutional-quality data sources.

Future Research Directions

Future enhancements could incorporate machine learning techniques for dynamic weight optimisation based on economic regime identification. The integration of alternative data sources, including satellite data, credit card spending, and search trends, could provide additional economic insight whilst maintaining the theoretical grounding of the current approach.

The development of sector-specific variants of the index could provide more granular economic assessment for industry-focused applications. Regional variants incorporating state-level economic data could support geographical diversification strategies for institutional investors.

Advanced econometric techniques, including dynamic factor models and Kalman filtering approaches, could enhance the real-time estimation accuracy whilst maintaining the interpretable framework that supports practical decision-making applications.

Conclusion

The US Macroeconomic Conditions Index represents a contribution to the literature on composite economic indicators by combining theoretical rigour with practical applicability. The transparent methodology, real-time implementation, and cross-asset analysis make it suitable for both academic research and practical financial market applications.

The empirical performance and alignment with business cycle analysis validate the theoretical framework whilst providing confidence in its practical utility. The index addresses a gap in available tools for real-time macroeconomic assessment, providing institutional investors and researchers with a framework for economic condition evaluation.

The systematic approach to cross-asset implications and risk assessment extends beyond traditional composite indicators, providing value for financial market applications. The combination of academic rigour and practical implementation represents an advancement in macroeconomic analysis tools.

References

Aruoba, S. B., Diebold, F. X., & Scotti, C. (2009). Real-time measurement of business conditions. Journal of Business & Economic Statistics, 27(4), 417-427.

Basseville, M., & Nikiforov, I. V. (1993). Detection of abrupt changes: Theory and application. Prentice Hall.

Bishop, C. M. (2006). Pattern recognition and machine learning. Springer.

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. Economic Perspectives, 35(1), 22-43.

Burns, A. F., & Mitchell, W. C. (1946). Measuring business cycles. NBER Books, National Bureau of Economic Research.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). The econometrics of financial markets. Princeton University Press.

Carroll, C. D., Fuhrer, J. C., & Wilcox, D. W. (1994). Does consumer sentiment forecast household spending? If so, why? American Economic Review, 84(5), 1397-1408.

Clarida, R., Gali, J., & Gertler, M. (2000). Monetary policy rules and macroeconomic stability: Evidence and some theory. Quarterly Journal of Economics, 115(1), 147-180.

Cochrane, J. H. (2005). Asset pricing. Princeton University Press.

Cormen, T. H., Leiserson, C. E., Rivest, R. L., & Stein, C. (2009). Introduction to algorithms. MIT Press.

Doz, C., Giannone, D., & Reichlin, L. (2011). A two-step estimator for large approximate dynamic factor models based on Kalman filtering. Journal of Econometrics, 164(1), 188-205.

Dzeng, R. J., & Lin, Y. C. (2004). Intelligent agents for supporting construction procurement negotiation. Expert Systems with Applications, 27(1), 107-119.

Elliot, A. J., & Maier, M. A. (2014). Color psychology: Effects of perceiving color on psychological functioning in humans. Annual Review of Psychology, 65, 95-120.

Few, S. (2006). Information dashboard design: The effective visual communication of data. O'Reilly Media.

Fisher, I. (1930). The theory of interest. Macmillan.

Foley, J. D., van Dam, A., Feiner, S. K., & Hughes, J. F. (1995). Computer graphics: Principles and practice. Addison-Wesley.

Gordon, M. J. (1962). The investment, financing, and valuation of the corporation. Richard D. Irwin.

Hasbrouck, J. (2007). Empirical market microstructure: The institutions, economics, and econometrics of securities trading. Oxford University Press.

Koenig, E. F. (2002). Using the purchasing managers' index to assess the economy's strength and the likely direction of monetary policy. Economic and Financial Policy Review, 1(6), 1-14.

Krugman, P. R., & Obstfeld, M. (2009). International economics: Theory and policy. Pearson.

Ludvigson, S. C. (2004). Consumer confidence and consumer spending. Journal of Economic Perspectives, 18(2), 29-50.

Macaulay, F. R. (1938). Some theoretical problems suggested by the movements of interest rates, bond yields and stock prices in the United States since 1856. National Bureau of Economic Research.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77-91.

Mishkin, F. S. (2012). The economics of money, banking, and financial markets. Pearson.

Nielsen, J. (1993). Usability engineering. Academic Press.

Norman, D. A. (2013). The design of everyday things: Revised and expanded edition. Basic Books.

OECD (2008). Handbook on constructing composite indicators: Methodology and user guide. OECD Publishing.

Oppenheim, A. V., & Schafer, R. W. (2009). Discrete-time signal processing. Prentice Hall.

Sahm, C. (2019). Direct stimulus payments to individuals. In Recession ready: Fiscal policies to stabilize the American economy (pp. 67-92). The Hamilton Project, Brookings Institution.

Siegel, J. J. (2002). Stocks for the long run: The definitive guide to financial market returns and long-term investment strategies. McGraw-Hill.

Sommerville, I. (2016). Software engineering. Pearson.

Stock, J. H., & Watson, M. W. (1989). New indexes of coincident and leading economic indicators. NBER Macroeconomics Annual, 4, 351-394.

Sweller, J. (1988). Cognitive load during problem solving: Effects on learning. Cognitive Science, 12(2), 257-285.

Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195-214.

Tufte, E. R. (2001). The visual display of quantitative information. Graphics Press.

Yardeni, E. (2003). Stock valuation models. Topical Study, 38. Yardeni Research.

Drawdown Distribution Analysis (DDA) ACADEMIC FOUNDATION AND RESEARCH BACKGROUND

The Drawdown Distribution Analysis indicator implements quantitative risk management principles, drawing upon decades of academic research in portfolio theory, behavioral finance, and statistical risk modeling. This tool provides risk assessment capabilities for traders and portfolio managers seeking to understand their current position within historical drawdown patterns.

The theoretical foundation of this indicator rests on modern portfolio theory as established by Markowitz (1952), who introduced the fundamental concepts of risk-return optimization that continue to underpin contemporary portfolio management. Sharpe (1966) later expanded this framework by developing risk-adjusted performance measures, most notably the Sharpe ratio, which remains a cornerstone of performance evaluation in financial markets.

The specific focus on drawdown analysis builds upon the work of Chekhlov, Uryasev and Zabarankin (2005), who provided the mathematical framework for incorporating drawdown measures into portfolio optimization. Their research demonstrated that traditional mean-variance optimization often fails to capture the full risk profile of investment strategies, particularly regarding sequential losses. More recent work by Goldberg and Mahmoud (2017) has brought these theoretical concepts into practical application within institutional risk management frameworks.

Value at Risk methodology, as comprehensively outlined by Jorion (2007), provides the statistical foundation for the risk measurement components of this indicator. The coherent risk measures framework developed by Artzner et al. (1999) ensures that the risk metrics employed satisfy the mathematical properties required for sound risk management decisions. Additionally, the focus on downside risk follows the framework established by Sortino and Price (1994), while the drawdown-adjusted performance measures implement concepts introduced by Young (1991).

MATHEMATICAL METHODOLOGY

The core calculation methodology centers on a peak-tracking algorithm that continuously monitors the maximum price level achieved and calculates the percentage decline from this peak. The drawdown at any time t is defined as DD(t) = (P(t) - Peak(t)) / Peak(t) × 100, where P(t) represents the asset price at time t and Peak(t) represents the running maximum price observed up to time t.

Statistical distribution analysis forms the analytical backbone of the indicator. The system calculates key percentiles using the ta.percentile_nearest_rank() function to establish the 5th, 10th, 25th, 50th, 75th, 90th, and 95th percentiles of the historical drawdown distribution. This approach provides a complete picture of how the current drawdown compares to historical patterns.

Statistical significance assessment employs standard deviation bands at one, two, and three standard deviations from the mean, following the conventional approach where the upper band equals μ + nσ and the lower band equals μ - nσ. The Z-score calculation, defined as Z = (DD - μ) / σ, enables the identification of statistically extreme events, with thresholds set at |Z| > 2.5 for extreme drawdowns and |Z| > 3.0 for severe drawdowns, corresponding to confidence levels exceeding 99.4% and 99.7% respectively.

ADVANCED RISK METRICS

The indicator incorporates several risk-adjusted performance measures that extend beyond basic drawdown analysis. The Sharpe ratio calculation follows the standard formula Sharpe = (R - Rf) / σ, where R represents the annualized return, Rf represents the risk-free rate, and σ represents the annualized volatility. The system supports dynamic sourcing of the risk-free rate from the US 10-year Treasury yield or allows for manual specification.

The Sortino ratio addresses the limitation of the Sharpe ratio by focusing exclusively on downside risk, calculated as Sortino = (R - Rf) / σd, where σd represents the downside deviation computed using only negative returns. This measure provides a more accurate assessment of risk-adjusted performance for strategies that exhibit asymmetric return distributions.

The Calmar ratio, defined as Annual Return divided by the absolute value of Maximum Drawdown, offers a direct measure of return per unit of drawdown risk. This metric proves particularly valuable for comparing strategies or assets with different risk profiles, as it directly relates performance to the maximum historical loss experienced.

Value at Risk calculations provide quantitative estimates of potential losses at specified confidence levels. The 95% VaR corresponds to the 5th percentile of the drawdown distribution, while the 99% VaR corresponds to the 1st percentile. Conditional VaR, also known as Expected Shortfall, estimates the average loss in the worst 5% of scenarios, providing insight into tail risk that standard VaR measures may not capture.

To enable fair comparison across assets with different volatility characteristics, the indicator calculates volatility-adjusted drawdowns using the formula Adjusted DD = Raw DD / (Volatility / 20%). This normalization allows for meaningful comparison between high-volatility assets like cryptocurrencies and lower-volatility instruments like government bonds.

The Risk Efficiency Score represents a composite measure ranging from 0 to 100 that combines the Sharpe ratio and current percentile rank to provide a single metric for quick asset assessment. Higher scores indicate superior risk-adjusted performance relative to historical patterns.

COLOR SCHEMES AND VISUALIZATION

The indicator implements eight distinct color themes designed to accommodate different analytical preferences and market contexts. The EdgeTools theme employs a corporate blue palette that matches the design system used throughout the edgetools.org platform, ensuring visual consistency across analytical tools.

The Gold theme specifically targets precious metals analysis with warm tones that complement gold chart analysis, while the Quant theme provides a grayscale scheme suitable for analytical environments that prioritize clarity over aesthetic appeal. The Behavioral theme incorporates psychology-based color coding, using green to represent greed-driven market conditions and red to indicate fear-driven environments.

Additional themes include Ocean, Fire, Matrix, and Arctic schemes, each designed for specific market conditions or user preferences. All themes function effectively with both dark and light mode trading platforms, ensuring accessibility across different user interface configurations.

PRACTICAL APPLICATIONS

Asset allocation and portfolio construction represent primary use cases for this analytical framework. When comparing multiple assets such as Bitcoin, gold, and the S&P 500, traders can examine Risk Efficiency Scores to identify instruments offering superior risk-adjusted performance. The 95% VaR provides worst-case scenario comparisons, while volatility-adjusted drawdowns enable fair comparison despite varying volatility profiles.

The practical decision framework suggests that assets with Risk Efficiency Scores above 70 may be suitable for aggressive portfolio allocations, scores between 40 and 70 indicate moderate allocation potential, and scores below 40 suggest defensive positioning or avoidance. These thresholds should be adjusted based on individual risk tolerance and market conditions.

Risk management and position sizing applications utilize the current percentile rank to guide allocation decisions. When the current drawdown ranks above the 75th percentile of historical data, indicating that current conditions are better than 75% of historical periods, position increases may be warranted. Conversely, when percentile rankings fall below the 25th percentile, indicating elevated risk conditions, position reductions become advisable.

Institutional portfolio monitoring applications include hedge fund risk dashboard implementations where multiple strategies can be monitored simultaneously. Sharpe ratio tracking identifies deteriorating risk-adjusted performance across strategies, VaR monitoring ensures portfolios remain within established risk limits, and drawdown duration tracking provides valuable information for investor reporting requirements.