RS Rating Multi-TimeframeRS Rating Multi-Timeframe (IBD-Style Relative Strength)

Short Description:

IBD-style Relative Strength Rating (1-99) comparing any stock's performance vs the S&P 500 across multiple timeframes.

Full Description:

Overview

This indicator calculates an IBD-style Relative Strength (RS) Rating that measures a stock's price performance relative to the S&P 500 over the past 12 months. The rating scale ranges from 1 (weakest) to 99 (strongest), telling you how a stock ranks against all other stocks in terms of relative performance.

How It Works

The RS Rating uses a weighted formula based on quarterly performance:

Last 63 days (1 quarter): 40% weight

Last 126 days (2 quarters): 20% weight

Last 189 days (3 quarters): 20% weight

Last 252 days (4 quarters): 20% weight

This weighting emphasizes recent performance while still accounting for longer-term strength.

Rating Interpretation

90-99 (Elite): Top 10% of all stocks - exceptional relative strength

80-89 (Excellent): Top 20% - strong leadership candidates

50-79 (Average): Middle of the pack

30-49 (Below Average): Underperforming the market

1-29 (Weak): Bottom 30% - avoid or consider shorting

Features

Multi-Timeframe: Works on any timeframe from 1-hour to weekly (always uses daily data for calculation)

Moving Average: Optional EMA or SMA of the RS Rating to smooth signals

Visual Zones: Color-coded zones for quick identification of strength/weakness

Signal Markers: Triangles appear when RS crosses key levels (80 and 30)

Info Table: Displays current RS Rating, change, MA value, and raw score

Alerts: Built-in alerts for key crossover events

Settings

Show Moving Average: Toggle MA line on/off

MA Length: Period for the moving average (default: 10)

MA Type: Choose between EMA or SMA

Benchmark Index: Change the comparison index (default: SP:SPX)

Show Rating Table: Toggle the info table on/off

How To Use

Buy candidates: Look for stocks with RS Rating above 80, ideally rising

Avoid: Stocks with RS Rating below 30 or falling rapidly

Confirmation: Use RS above its moving average as additional confirmation

Divergence: Watch for RS making new highs before price (bullish) or new lows before price (bearish)

Credits

RS Rating calculation methodology inspired by Investor's Business Daily (IBD) and adapted from Fred6724's RS Rating script. Percentile calibration based on analysis of ~6,600 US stocks.

Tags: relative strength, RS rating, IBD, momentum, CAN SLIM, benchmark, SPX, market leaders, stock ranking

Category: Relative Strength

ابحث في النصوص البرمجية عن "Table"

RSI HTF Hardcoded (A/B Presets) + Regimes [CHE]RSI HTF Hardcoded (A/B Presets) + Regimes — Higher-timeframe RSI emulation with acceptance-based regime filter and on-chart diagnostics

Summary

This indicator emulates a higher-timeframe RSI on the current chart by resolving hardcoded “HTF-like” lengths from a time-bucket mapping, avoiding cross-timeframe requests. It computes RSI on a resolved length, smooths it with a resolved moving average, and derives a histogram-style difference (RSI minus its smoother). A four-state regime classifier is gated by a dead-band and an acceptance filter requiring consecutive bars before a regime is considered valid. An on-chart table reports the active preset, resolved mapping tag, resolved lengths, and the current filtered regime.

Pine version: v6

Overlay: false

Primary outputs: RSI line, SMA(RSI) line, RSI–SMA histogram columns, reference levels (30/50/70), regime-change alert, info table

Motivation

Cross-timeframe RSI implementations often rely on `request.security`, which can introduce repaint pathways and additional update latency. This design uses deterministic, on-series computation: it infers a coarse target bucket (or uses a forced bucket) and resolves lengths accordingly. The dead-band reduces noise at the decision boundaries (around RSI 50 and around the RSI–SMA difference), while the acceptance filter suppresses rapid flip-flops by requiring sustained agreement across bars.

Differences

Baseline: Standard RSI with a user-selected length on the same timeframe, or HTF RSI via cross-timeframe requests.

Key differences:

Hardcoded preset families and a bucket-based mapping to resolve “HTF-like” lengths on the current chart.

No `request.security`; all calculations run on the chart’s own series.

Regime classification uses two independent signals (RSI relative to 50 and RSI–SMA difference), gated by a configurable dead-band and an acceptance counter.

Always-on diagnostics via a persistent table (optional), showing preset, mapping tag, resolved lengths, and filtered regime.

Practical effect: The oscillator behaves like a slower, higher-timeframe variant with more stable regime transitions, at the cost of delayed recognition around sharp turns (by design).

How it works

1. Bucket selection: The script derives a coarse “target bucket” from the chart timeframe (Auto) or uses a user-forced bucket.

2. Length resolution: A chosen preset defines base lengths (RSI length and smoothing length). A bucket/timeframe mapping resolves a multiplier, producing final lengths used for RSI and smoothing.

3. Oscillator construction: RSI is computed on the resolved RSI length. A moving average of RSI is computed on the resolved smoothing length. The difference (RSI minus its smoother) is used as the histogram series.

4. Regime classification: Four regimes are defined from:

RSI relative to 50 (bullish above, bearish below), with a dead-band around 50

Difference relative to 0 (positive/negative), with a dead-band around 0

These two axes produce strong/weak bull and bear states, plus a neutral state when inside the dead-band(s).

5. Acceptance filter: The raw regime must persist for `n` consecutive bars before it becomes the filtered regime. The alert triggers when the filtered regime changes.

6. Diagnostics and visualization: Histogram columns change shade based on sign and whether the difference is rising/falling. The table displays preset, mapping tag, resolved lengths, and the filtered regime description.

Parameter Guide

Source — Input series for RSI — Default: Close — Smoother sources reduce noise but add lag.

Preset — Base lengths family — Default: A(14/14) — Switch presets to change RSI and smoothing responsiveness.

Target Bucket — Auto or forced bucket — Default: Auto — Force a bucket to lock behavior across chart timeframe changes.

Table X / Table Y — Table anchor — Default: right / top — Move to avoid covering content.

Table Size — Table text size — Default: normal — Increase for presentations, decrease for dense layouts.

Dark Mode — Table theme — Default: enabled — Match chart background for readability.

Show Table — Toggle diagnostics table — Default: enabled — Disable for a cleaner pane.

Epsilon (dead-band) — Noise gate for decisions — Default: 1.0 — Raise to reduce flips near boundaries; lower to react faster.

Acceptance bars (n) — Bars required to confirm a regime — Default: 3 — Higher reduces whipsaw; lower increases reactivity.

Reading

Histogram (RSI–SMA):

Above zero indicates RSI is above its smoother (positive momentum bias).

Below zero indicates RSI is below its smoother (negative momentum bias).

Darker/lighter shading indicates whether the difference is increasing or decreasing versus the previous bar.

RSI vs SMA(RSI):

RSI’s position relative to 50 provides broad directional bias.

RSI’s position relative to its smoother provides momentum confirmation/contra-signal.

Regimes:

Strong bull: RSI meaningfully above 50 and difference meaningfully above 0.

Weak bull: RSI above 50 but difference below 0 (pullback/transition).

Strong bear: RSI meaningfully below 50 and difference meaningfully below 0.

Weak bear: RSI below 50 but difference above 0 (pullback/transition).

Neutral: inside the dead-band(s).

Table:

Use it to validate the active preset, the mapping tag, the resolved lengths, and the filtered regime output.

Workflows

Trend confirmation:

Favor long bias when strong bull is active; favor short bias when strong bear is active.

Treat weak regimes as pullback/transition context rather than immediate reversals, especially with higher acceptance.

Structure + oscillator:

Combine regimes with swing structure, breakouts, or a baseline trend filter to avoid trading against dominant structure.

Use regime change alerts as a “state change” notification, not as a standalone entry.

Multi-asset consistency:

The bucket mapping helps keep a consistent “feel” across different chart timeframes without relying on external timeframe series.

Behavior/Constraints

Intrabar behavior:

No cross-timeframe requests are used; values can still evolve on the live bar and settle at close depending on your chart/update timing.

Warm-up requirements:

Large resolved lengths require sufficient history to seed RSI and smoothing. Expect a warm-up period after loading or switching symbols/timeframes.

Latency by design:

Dead-band and acceptance filtering reduce noise but can delay regime changes during sharp reversals.

Chart types:

Intended for standard time-based charts. Non-time-based or synthetic chart types (e.g., Heikin-Ashi, Renko, Kagi, Point-and-Figure, Range) can distort oscillator behavior and regime stability.

Tuning

Too many flips near decision boundaries:

Increase Epsilon and/or increase Acceptance bars.

Too sluggish in clean trends:

Reduce Acceptance bars by one, or choose a faster preset (shorter base lengths).

Too sensitive on lower timeframes:

Choose a slower preset (longer base lengths) or force a higher Target Bucket.

Want less clutter:

Disable the table and keep only the alert + plots you need.

What it is/isn’t

This indicator is a regime and visualization layer for RSI using higher-timeframe emulation and stability gates. It is not a complete trading system and does not provide position sizing, risk management, or execution rules. Use it alongside structure, liquidity/volatility context, and protective risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino.

Tchwella Stocks Custom WatermarkThis Pine Script v5 indicator adds a customizable watermark to TradingView charts, displaying key stock information while allowing for flexible positioning and formatting.

📌 Features & Functionality:

✅ Custom Positioning:

• Fixed to the top-left corner.

• Adjustable spacing ensures the text is properly aligned.

✅ Displayed Information (Configurable):

• Company Name & Market Cap (Optional: Shows dynamically calculated market cap)

• Stock Ticker & Timeframe

• Industry & Sector

✅ Customization Options:

• Font Size: Huge, Large, Normal, Small

• Text Color & Transparency: Adjustable

• Proper Left Alignment for a clean, structured display

• Vertical Offset Tweaks to move text down for better visibility

✅ Optimized Table Layout:

• Uses table.new() for persistent placement.

• Added an empty row to fine-tune positioning, ensuring the watermark doesn’t overlap key chart areas.

🔧 Use Case:

Designed for traders who want a clear, customizable stock watermark to enhance their charting experience without obstructing price action.

Feb 1

Release Notes

Updated version: now you can decide your location for the watermark

Micha Stocks Custom Watermark (MSWM) – TradingView Script

This Pine Script v5 indicator adds a customizable watermark to TradingView charts, displaying key stock information while allowing for flexible positioning and formatting.

📌 Features & Functionality:

✅ Custom Positioning:

• Fixed to the top-left corner.

• Adjustable spacing ensures the text is properly aligned.

✅ Displayed Information (Configurable):

• Company Name & Market Cap (Optional: Shows dynamically calculated market cap)

• Stock Ticker & Timeframe

• Industry & Sector

✅ Customization Options:

• Font Size: Huge, Large, Normal, Small

• Text Color & Transparency: Adjustable

• Proper Left Alignment for a clean, structured display

• Vertical Offset Tweaks to move text down for better visibility

✅ Optimized Table Layout:

• Uses table.new() for persistent placement.

• Added an empty row to fine-tune positioning, ensuring the watermark doesn’t overlap key chart areas.

🔧 Use Case:

Designed for traders who want a clear, customizable stock watermark to enhance their charting experience without obstructing price action.

Feb 7

Release Notes

Micha Stocks Custom Watermark – Updated Version 🚀

This updated Micha Stocks Custom Watermark script enhances your TradingView experience by adding an ATR-based volatility signal alongside the existing customizable stock watermark.

🆕 New Features & Improvements:

✅ ATR (14-Day) with Dynamic Volatility Indicator

• Displays the ATR value and its percentage relative to price.

• Includes a color-coded volatility signal:

• 🔴 High Volatility (Above user-defined Red Threshold)

• 🟡 Moderate Volatility (Between Red & Yellow Thresholds)

• 🟢 Low Volatility (Below user-defined Yellow Threshold)

✅ Fully Customizable ATR Thresholds

• Users can set their own ATR % levels for Red, Yellow, and Green signals.

✅ Improved Watermark Customization

• Users can still adjust the position, size, and color of the watermark.

• Includes Company Name, Ticker, Market Cap, Industry, and Sector.

• ATR can be turned on/off in settings for flexibility.

🔧 How to Use:

1️⃣ Go to Indicator Settings → Enable or Disable ATR Display

2️⃣ Adjust ATR % Thresholds to fit your volatility preference

3️⃣ Customize Text Position, Color, and Size to match your chart setup

This update makes it easier to quickly assess market volatility while keeping a clean and professional chart layout.

💡 Why Use This Indicator?

• Effortlessly track key stock info without cluttering your chart.

• Quickly identify volatile conditions using ATR percentage signals.

• Adjust settings on the fly to match your trading strategy.

📢 Update Now & Enjoy a Smarter Charting Experience!

Buyer vs Seller ControlBuyer vs Seller Control Analysis

Technical indicator measuring market participation through candlestick wick analysis

Overview:

This indicator analyzes the relationship between closing prices and candlestick wicks to measure buying and selling pressure. It calculates two key metrics and displays their moving averages to help identify market sentiment shifts.

Calculation Method:

The indicator measures two distinct values for each candle:

Buyer Control Value: Distance from candle low to closing price (close - low)

Seller Control Value: Distance from candle high to closing price (high - close)

Both values are then smoothed using a Simple Moving Average (default period: 20) to reduce noise and show clearer trends.

Visual Components:

Lime Line: 20-period SMA of buyer control values

Fuchsia Line: 20-period SMA of seller control values

Area Fill: Colored region between the two lines

Histogram: Difference between buyer and seller control SMAs

Zero Reference Line: Horizontal line at zero level

Information Table: Current numerical values (optional display)

Interpretation:

When the lime line (buyer control) is above the fuchsia line (seller control), it indicates that recent candles have been closing closer to their highs than to their lows on average.

When the fuchsia line is above the lime line, recent candles have been closing closer to their lows than to their highs on average.

Fill Color Logic:

Lime (green) fill appears when buyer control SMA > seller control SMA

Fuchsia (red) fill appears when seller control SMA > buyer control SMA

Fill transparency adjusts based on the magnitude of difference between the two SMAs

Stronger differences result in more opaque fills

Settings:

Moving Average Period: Adjustable from 1-200 periods (default: 20)

Show Info Table: Toggle to display/hide the numerical values table

Technical Notes:

The indicator works on any timeframe

Values are displayed in the same units as the underlying asset's price

The histogram shows the mathematical difference between the two SMA lines

Transparency calculation uses a 50-period lookback for dynamic scaling

This indicator provides a quantitative approach to analyzing candlestick patterns by focusing on where prices close relative to their intraday ranges.

Kelly Optimal Leverage IndicatorThe Kelly Optimal Leverage Indicator mathematically applies Kelly Criterion to determine optimal position sizing based on market conditions.

This indicator helps traders answer the critical question: "How much capital should I allocate to this trade?"

Note that "optimal position sizing" does not equal the position sizing that you should have. The Optima position sizing given by the indicator is based on historical data and cannot predict a crash, in which case, high leverage could be devastating.

Originally developed for gambling scenarios with known probabilities, the Kelly formula has been adapted here for financial markets to dynamically calculate the optimal leverage ratio that maximizes long-term capital growth while managing risk.

Key Features

Kelly Position Sizing: Uses historical returns and volatility to calculate mathematically optimal position sizes

Multiple Risk Profiles: Displays Full Kelly (aggressive), 3/4 Kelly (moderate), 1/2 Kelly (conservative), and 1/4 Kelly (very conservative) leverage levels

Volatility Adjustment: Automatically recommends appropriate Kelly fraction based on current market volatility

Return Smoothing: Option to use log returns and smoothed calculations for more stable signals

Comprehensive Table: Displays key metrics including annualized return, volatility, and recommended exposure levels

How to Use

Interpret the Lines: Each colored line represents a different Kelly fraction (risk tolerance level). When above zero, positive exposure is suggested; when below zero, reduce exposure. Note that this is based on historical returns. I personally like to increase my exposure during market downturns, but this is hard to illustrate in the indicator.

Monitor the Table: The information panel provides precise leverage recommendations and exposure guidance based on current market conditions.

Follow Recommended Position: Use the "Recommended Position" guidance in the table to determine appropriate exposure level.

Select Your Risk Profile: Conservative traders should follow the Half Kelly or Quarter Kelly lines, while more aggressive traders might consider the Three-Quarter or Full Kelly lines.

Adjust with Volatility: During high volatility periods, consider using more conservative Kelly fractions as recommended by the indicator.

Mathematical Foundation

The indicator calculates the optimal leverage (f*) using the formula:

f* = μ/σ²

Where:

μ is the annualized expected return

σ² is the annualized variance of returns

This approach balances potential gains against risk of ruin, offering a scientific framework for position sizing that maximizes long-term growth rate.

Notes

The Full Kelly is theoretically optimal for maximizing long-term growth but can experience significant drawdowns. You should almost never use full kelly.

Most practitioners use fractional Kelly strategies (1/2 or 1/4 Kelly) to reduce volatility while capturing most of the growth benefits

This indicator works best on daily timeframes but can be applied to any timeframe

Negative Kelly values suggest reducing or eliminating market exposure

The indicator should be used as part of a complete trading system, not in isolation

Enjoy the indicator! :)

P.S. If you are really geeky about the Kelly Criterion, I recommend the book The Kelly Capital Growth Investment Criterion by Edward O. Thorp and others.

regressionUtilitiesLibrary "regressionUtilities"

get_linear_regression(bar_index_array, prices_array, stdDev_mult)

: Generates the linear regression channel for an array of values.

Parameters:

bar_index_array (array) : (array): Array with bar indexes

prices_array (array) : (array): Array with prices

stdDev_mult (float) : (float): Standard deviation multiple for the channels

Returns: : Returns x1, x2, y1_mid, y2_mid, y1_up, y2_up, y1_dn, y2_dn, m, b, R2, stdDev

get_optimal_linearRegression_channel(max_length, min_length, source, stdDev_mult, show_data_table, tableYpos, tableXpos, table_textSize, barsToRight, plot_labels, include_levels)

: Gets the best fitting linear regression using optimum length

Parameters:

max_length (int) : (int): Maximum bar length

min_length (int) : (int): Minimum bar length

source (float) : (float): Source for the regression

stdDev_mult (float) : (float): Array with prices

show_data_table (bool) : (bool): Activates and shows the data table

tableYpos (string)

tableXpos (string)

table_textSize (string)

barsToRight (int)

plot_labels (bool)

include_levels (bool)

Returns: : Returns three line objects that conform the regression channel, plus the optimal length and maximum r2

get_regressionChannel_data(max_length, min_length, source, stdDev_mult, plot_linearRegression, plot_labels, include_levels, barsToRight)

: Gets data for the linear regression channel

Parameters:

max_length (int) : (int): Maximum length for the linear regression.

min_length (int) : (int): Minimum length for the linear regression.

source (float) : (float): Source for the linear regression

stdDev_mult (float) : (float): Multiple for the standar deviations for the linear regression channel.

plot_linearRegression (bool)

plot_labels (bool)

include_levels (bool)

barsToRight (int)

Returns: : Returns a maps with the regression levels, the direction flag and the datatable map.

get_regressionChannel_data_v2(max_length, min_length, source, stdDev_mult, plot_linearRegression, plot_labels, include_levels, barsToRight)

Parameters:

max_length (int)

min_length (int)

source (float)

stdDev_mult (float)

plot_linearRegression (bool)

plot_labels (bool)

include_levels (bool)

barsToRight (int)

get_cuadratic_regression(x_array, y_array, bars_to_project, max_length)

: Gets the best fitting linear regression using optimum length

Parameters:

x_array (array) : (array): Maximum bar length

y_array (array) : (array): Minimum bar length

bars_to_project (int) : (int): Array with prices

max_length (int)

Returns: : Returns three line objects

Indicator DashboardThis script creates an 'Indicator Dashboard' designed to assist you in analyzing financial markets and making informed decisions. The indicator provides a summary of current market conditions by presenting various technical analysis indicators in a table format. The dashboard evaluates popular indicators such as Moving Averages, RSI, MACD, and Stochastic RSI. Below, we'll explain each part of this script in detail and its purpose:

### Overview of Indicators

1. **Moving Averages (MA)**:

- This indicator calculates Simple Moving Averages (“SMA”) for 5, 14, 20, 50, 100, and 200 periods. These averages provide a visual summary of price movements. Depending on whether the price is above or below the moving average, it determines the market direction as either “Bullish” or “Bearish.”

2. **RSI (Relative Strength Index)**:

- The RSI helps identify overbought or oversold market conditions. Here, the RSI is calculated for a 14-period window, and this value is displayed in the table. Additionally, the 14-period moving average of the RSI is also included.

3. **MACD (Moving Average Convergence Divergence)**:

- The MACD indicator is used to determine trend strength and potential reversals. This script calculates the MACD line, signal line, and histogram. The MACD condition (“Bullish,” “Bearish,” or “Neutral”) is displayed alongside the MACD and signal line values.

4. **Stochastic RSI**:

- Stochastic RSI is used to identify momentum changes in the market. The %K and %D lines are calculated to determine the market condition (“Bullish” or “Bearish”), which is displayed along with the calculated values for %K and %D.

### Table Layout and Presentation

The dashboard is presented in a vertical table format in the top-right corner of the chart. The table contains two columns: “Indicator” and “Status,” summarizing the condition of each technical indicator.

- **Indicator Column**: Lists each of the indicators being tracked, such as SMA values, RSI, MACD, etc.

- **Status Column**: Displays the current status of each indicator, such as “Bullish,” “Bearish,” or specific values like the RSI or MACD.

The table also includes rounded indicator values for easier interpretation. This helps traders quickly assess market conditions and make informed decisions based on multiple indicators presented in a single location.

### Detailed Indicator Status Calculations

1. **SMA Status**: For each moving average (5, 14, 20, 50, 100, 200), the script checks if the current price is above or below the SMA. The status is determined as “Bullish” if the price is above the SMA and “Bearish” if below, with the value of the SMA also displayed.

2. **RSI and RSI Average**: The RSI value for a 14-period is displayed along with its 14-period SMA, which provides an average reading of the RSI to smooth out volatility.

3. **MACD Indicator**: The MACD line, signal line, and histogram are calculated using standard parameters (12, 26, 9). The status is shown as “Bullish” when the MACD line is above the signal line, and “Bearish” when it is below. The exact values for the MACD line, signal line, and histogram are also included.

4. **Stochastic RSI**: The %K and %D lines of the Stochastic RSI are used to determine the trend condition. If %K is greater than %D, the condition is “Bullish,” otherwise it is “Bearish.” The actual values of %K and %D are also displayed.

### Conclusion

The 'Indicator Dashboard' provides a comprehensive overview of multiple technical indicators in a single, easy-to-read table. This allows traders to quickly gauge market conditions and make more informed decisions. By consolidating key indicators like Moving Averages, RSI, MACD, and Stochastic RSI into one dashboard, it saves time and enhances the efficiency of technical analysis.

This script is particularly useful for traders who prefer a clean and organized overview of their favorite indicators without needing to plot each one individually on the chart. Instead, all the crucial information is available at a glance in a consolidated format.

Sri Yantra MTF - AynetSri Yantra MTF - Aynet Script Overview

This Pine Script generates a Sri Yantra-inspired geometric pattern overlay on price charts. The pattern is dynamically updated based on multi-timeframe (MTF) inputs, utilizing high and low price ranges, and adjusting its size relative to a chosen multiplier.

The Sri Yantra is a sacred geometric figure used in various spiritual and mathematical contexts, symbolizing the interconnectedness of the universe. Here, it is applied to visualize structured price levels.

Scientific and Technical Explanation

Multi-Timeframe Integration:

Base Timeframe (baseRes): This is the primary timeframe for the analysis. The opening price and ATR (Average True Range) are calculated from this timeframe.

Pattern Timeframe (patternRes): Defines the granularity of the pattern. It ensures synchronization with price movements on specific time intervals.

Geometric Construction:

ATR-Based Scaling: The script uses ATR as a volatility measure to dynamically size the geometric pattern. The sizeMult input scales the pattern relative to price volatility.

Pattern Width (barOffset): Defines the horizontal extent of the pattern in terms of bars. This ensures the pattern is aligned with price movements and scales appropriately.

Sri Yantra-Like Geometry:

Outer Square: A bounding box is drawn around the price level.

Triangles: Multiple layers of triangles (primary, secondary, and tertiary) are calculated and drawn to mimic the structure of the Sri Yantra. These triangles converge and diverge based on price levels.

Horizontal Lines: Added at key levels to provide additional structure and aesthetic alignment.

Dynamic Updates:

The pattern recalculates and redraws itself on the last bar of the selected timeframe, ensuring it adapts to real-time price data.

A built-in check identifies new bars in the chosen timeframe (patternRes), ensuring accurate updates.

Information Table:

Displays the selected base and pattern timeframes in a table format on the top-right corner of the chart.

Allows traders to see the active settings for quick adjustments.

Key Inputs

Style Settings:

Pattern Color: Customize the color of the geometric patterns.

Size Multiplier (sizeMult): Adjusts the size of the pattern relative to price movements.

Line Width: Controls the thickness of the geometric lines.

Timeframe Settings:

Base Resolution (baseRes): Timeframe for calculating the pattern's anchor (default: daily).

Pattern Resolution (patternRes): Timeframe granularity for the pattern’s formation.

Geometric Adjustments:

Pattern Width (barOffset): Horizontal width in bars.

ATR Multiplier (rangeSize): Vertical size adjustment based on price volatility.

Scientific Concepts

Volatility Representation:

ATR (Average True Range): A standard measure of market volatility, representing the average range of price movements over a defined period. Here, ATR adjusts the vertical height of the geometric figures.

Geometric Symmetry:

The script emulates symmetry similar to the Sri Yantra, aligning with the principles of sacred geometry, which often appear in nature and mathematical constructs. Symmetry in financial data visualizations can aid in intuitive interpretation of price movements.

Multi-Timeframe Fusion:

Synchronizing patterns with multiple timeframes enhances the relevance of overlays for different trading strategies. For example, daily trends combined with hourly patterns can help traders optimize entries and exits.

Visual Features

Outer Square:

Drawn to encapsulate the geometric structure.

Represents the broader context of price levels.

Triangles:

Three layers of interlocking triangles create a fractal pattern, providing a visual alignment to price dynamics.

Horizontal Lines:

Emphasize critical levels within the pattern, offering visual cues for potential support or resistance areas.

Information Table:

Displays the active timeframe settings, helping traders quickly verify configurations.

Applications

Trend Visualization:

Patterns overlay on price movements provide a clearer view of trend direction and potential reversals.

Volatility Mapping:

ATR-based scaling ensures the pattern adjusts to varying market conditions, making it suitable for different asset classes and trading strategies.

Multi-Timeframe Analysis:

Integrates higher and lower timeframes, enabling traders to spot confluences between short-term and long-term price levels.

Potential Enhancements

Add Fibonacci Levels: Overlay Fibonacci retracements within the pattern for deeper price level insights.

Dynamic Alerts: Include alert conditions when price intersects key geometric lines.

Custom Labels: Add text descriptions for critical intersections or triangle centers.

This script is a unique blend of technical analysis and sacred geometry, providing traders with an innovative way to visualize market dynamics.

Stationarity Test: Dickey-Fuller & KPSS [Pinescriptlabs]

📊 Kwiatkowski-Phillips-Schmidt-Shin Model Indicator & Dickey-Fuller Test 📈

This algorithm performs two statistical tests on the price spread between two selected instruments: the first from the current chart and the second determined in the settings. The purpose is to determine if their relationship is stationary. It then uses this information to generate **visual signals** based on how far the current relationship deviates from its historical average.

⚙️ Key Components:

• 🧪 ADF Test (Augmented Dickey-Fuller):** Checks if the spread between the two instruments is stationary.

• 🔬 KPSS Test (Kwiatkowski-Phillips-Schmidt-Shin):** Another test for stationarity, complementing the ADF test.

• 📏 Z-Score Calculation:** Measures how many standard deviations the current spread is from its historical mean.

• 📊 Dynamic Threshold:** Adjusts the trading signal threshold based on recent market volatility.

🔍 What the Values Mean:

The indicator displays several key values in a table:

• 📈 ADF Stationarity:** Shows "Stationary" or "Non-Stationary" based on the ADF test result.

• 📉 KPSS Stationarity:** Shows "Stationary" or "Non-Stationary" based on the KPSS test result.

• 📏 Current Z-Score:** The current Z-score of the spread.

• 🔗 Hedge Ratio:** The relationship coefficient between the two instruments.

• 🌐 Market State:** Describes the current market condition based on the Z-score.

📊 How to Interpret the Chart:

• The main chart displays the Z-score of the spread over time.

• The green and red lines represent the upper and lower thresholds for trading signals.

• The area between the **Z-score** and the thresholds is filled when a trading signal is active.

• Additional charts show the **statistics of the ADF and KPSS tests** and their critical values.

**📉 Practical Example: NVIDIA Corporation (NVDA)**

Looking at the chart for **NVIDIA Corporation (NVDA)**, we can see how the indicator applies in a real case:

1. **Main Chart (Top):**

• Shows the **historical price** of NVIDIA on a weekly scale.

• A general **uptrend** is observed with periods of consolidation.

2. **KPSS & ADF Indicator (Bottom):**

• The lower chart shows the KPSS & ADF Model indicator applied to NVIDIA.

• The **green line** represents the Z-score of the spread.

• The **green shaded areas** indicate periods where the Z-score exceeded the thresholds, generating trading signals.

3. **📋 Current Values in the Table:**

• **ADF Stationarity:** Non-Stationary

• **KPSS Stationarity:** Non-Stationary

• **Current Z-Score:** 3.45

• **Hedge Ratio:** -164.8557

• **Market State:** Moderate Volatility

4. **🔍 Interpretation:**

• A Z-score of **3.45** suggests that NVIDIA’s price is significantly above its historical average relative to **EURUSD**.

• Both the **ADF** and **KPSS** tests indicate **non-stationarity**, suggesting **caution** when using mean reversion signals at this moment.

• The market state "Moderate Volatility" indicates noticeable deviation, but not extreme.

---

**💡 Usage:**

• **When Both Tests Show Stationarity:**

• **🔼 If Z-score > Upper Threshold:** Consider **buying the first instrument** and **selling the second**.

• **🔽 If Z-score < Lower Threshold:** Consider **selling the first instrument** and **buying the second**.

• **When Either Test Shows Non-Stationarity:**

• Wait for the relationship to become **stationary** before trading.

• **Market State:**

• Use this information to evaluate **general market conditions** and adjust your trading strategy accordingly.

**Mirror Comparison of the Same as Symbol 2 🔄📊**

**📊 Table Values:**

• **Extreme Volatility Threshold:** This value is displayed when the **Z-score** exceeds **100%**, indicating **extreme deviation**. It signals a potential **trading opportunity**, as the spread has reached unusually high or low levels, suggesting a **reversion or correction** in the market.

• **Mean Reversion Threshold:** Appears when the **Z-score** begins returning towards the mean after a period of **high or extreme volatility**. It indicates that the spread between the assets is returning to normal levels, suggesting a phase of **stabilization**.

• **Neutral Zone:** Displayed when the **Z-score** is near **zero**, signaling that the spread between assets is within expected limits. This indicates a **balanced market** with no significant volatility or clear trading opportunities.

• **Low Volatility Threshold:** Appears when the **Z-score** is below **70%** of the dynamic threshold, reflecting a period of **low volatility** and market stability, indicating fewer trading opportunities.

Español:

📊 Indicador del Modelo Kwiatkowski-Phillips-Schmidt-Shin & Prueba de Dickey-Fuller 📈

Este algoritmo realiza dos pruebas estadísticas sobre la diferencia de precios (spread) entre dos instrumentos seleccionados: el primero en el gráfico actual y el segundo determinado en la configuración. El objetivo es determinar si su relación es estacionaria. Luego utiliza esta información para generar señales visuales basadas en cuánto se desvía la relación actual de su promedio histórico.

⚙️ Componentes Clave:

• 🧪 Prueba ADF (Dickey-Fuller Aumentada): Verifica si el spread entre los dos instrumentos es estacionario.

• 🔬 Prueba KPSS (Kwiatkowski-Phillips-Schmidt-Shin): Otra prueba para la estacionariedad, complementando la prueba ADF.

• 📏 Cálculo del Z-Score: Mide cuántas desviaciones estándar se encuentra el spread actual de su media histórica.

• 📊 Umbral Dinámico: Ajusta el umbral de la señal de trading en función de la volatilidad reciente del mercado.

🔍 Qué Significan los Valores:

El indicador muestra varios valores clave en una tabla:

• 📈 Estacionariedad ADF: Muestra "Estacionario" o "No Estacionario" basado en el resultado de la prueba ADF.

• 📉 Estacionariedad KPSS: Muestra "Estacionario" o "No Estacionario" basado en el resultado de la prueba KPSS.

• 📏 Z-Score Actual: El Z-score actual del spread.

• 🔗 Ratio de Cobertura: El coeficiente de relación entre los dos instrumentos.

• 🌐 Estado del Mercado: Describe la condición actual del mercado basado en el Z-score.

📊 Cómo Interpretar el Gráfico:

• El gráfico principal muestra el Z-score del spread a lo largo del tiempo.

• Las líneas verdes y rojas representan los umbrales superior e inferior para las señales de trading.

• El área entre el Z-score y los umbrales se llena cuando una señal de trading está activa.

• Los gráficos adicionales muestran las estadísticas de las pruebas ADF y KPSS y sus valores críticos.

📉 Ejemplo Práctico: NVIDIA Corporation (NVDA)

Observando el gráfico para NVIDIA Corporation (NVDA), podemos ver cómo se aplica el indicador en un caso real:

Gráfico Principal (Superior): • Muestra el precio histórico de NVIDIA en escala semanal. • Se observa una tendencia alcista general con períodos de consolidación.

Indicador KPSS & ADF (Inferior): • El gráfico inferior muestra el indicador Modelo KPSS & ADF aplicado a NVIDIA. • La línea verde representa el Z-score del spread. • Las áreas sombreadas en verde indican períodos donde el Z-score superó los umbrales, generando señales de trading.

📋 Valores Actuales en la Tabla: • Estacionariedad ADF: No Estacionario • Estacionariedad KPSS: No Estacionario • Z-Score Actual: 3.45 • Ratio de Cobertura: -164.8557 • Estado del Mercado: Volatilidad Moderada

🔍 Interpretación: • Un Z-score de 3.45 sugiere que el precio de NVIDIA está significativamente por encima de su promedio histórico en relación con EURUSD. • Tanto la prueba ADF como la KPSS indican no estacionariedad, lo que sugiere precaución al usar señales de reversión a la media en este momento. • El estado del mercado "Volatilidad Moderada" indica una desviación notable, pero no extrema.

💡 Uso:

• Cuando Ambas Pruebas Muestran Estacionariedad:

• 🔼 Si Z-score > Umbral Superior: Considera comprar el primer instrumento y vender el segundo.

• 🔽 Si Z-score < Umbral Inferior: Considera vender el primer instrumento y comprar el segundo.

• Cuando Alguna Prueba Muestra No Estacionariedad:

• Espera a que la relación se vuelva estacionaria antes de operar.

• Estado del Mercado:

• Usa esta información para evaluar las condiciones generales del mercado y ajustar tu estrategia de trading en consecuencia.

Comparativo en Espejo del Mismo Como Símbolo 2 🔄📊

📊 Valores de la Tabla:

• Umbral de Volatilidad Extrema: Este valor se muestra cuando el Z-score supera el 100%, indicando desviación extrema. Señala una posible oportunidad de trading, ya que el spread entre los activos ha alcanzado niveles inusualmente altos o bajos, lo que podría indicar una reversión o corrección en el mercado.

• Umbral de Reversión a la Media: Aparece cuando el Z-score comienza a volver hacia la media tras un período de alta o extrema volatilidad. Indica que el spread entre los activos está regresando a niveles normales, sugiriendo una fase de estabilización.

• Zona Neutral: Se muestra cuando el Z-score está cerca de cero, señalando que el spread entre activos está dentro de lo esperado. Esto indica un mercado equilibrado con ninguna volatilidad significativa ni oportunidades claras de trading.

• Umbral de Baja Volatilidad: Aparece cuando el Z-score está por debajo del 70% del umbral dinámico, reflejando un período de baja volatilidad y estabilidad del mercado, indicando menos oportunidades de trading.

ChartUtilsLibrary "ChartUtils"

Library for chart utilities, including managing tables

initTable(rows, cols, bgcolor)

Initializes a table with specific dimensions and color

Parameters:

rows (int) : (int) Number of rows in the table

cols (int) : (int) Number of columns in the table

bgcolor (color) : (color) Background color of the table

Returns: (table) The initialized table

updateTable(tbl, is_price_below_avg, current_investment_USD, strategy_position_size, strategy_position_avg_price, strategy_openprofit, strategy_opentrades, isBullishRate, isBearishRate, mlRSIOverSold, mlRSIOverBought)

Updates the trading table

Parameters:

tbl (table) : (table) The table to update

is_price_below_avg (bool) : (bool) If the current price is below the average price

current_investment_USD (float) : (float) The current investment in USD

strategy_position_size (float) : (float) The size of the current position

strategy_position_avg_price (float) : (float) The average price of the current position

strategy_openprofit (float) : (float) The current open profit

strategy_opentrades (int) : (int) The number of open trades

isBullishRate (bool) : (bool) If the current rate is bullish

isBearishRate (bool) : (bool) If the current rate is bearish

mlRSIOverSold (bool) : (bool) If the ML RSI is oversold

mlRSIOverBought (bool) : (bool) If the ML RSI is overbought

updateTableNoPosition(tbl)

Updates the table when there is no position

Parameters:

tbl (table) : (table) The table to update

Index Generator [By MUQWISHI]▋ INTRODUCTION :

The “Index Generator” simplifies the process of building a custom market index, allowing investors to enter a list of preferred holdings from global securities. It aims to serve as an approach for tracking performance, conducting research, and analyzing specific aspects of the global market. The output will include an index value, a table of holdings, and chart plotting, providing a deeper understanding of historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom index. I created this index and named it “My Oil & Gas Index”. The index comprises several global energy companies. Essentially, the indicator weights each company by collecting the number of shares and then computes the market capitalization before sorting them as seen in the table.

_______________________

▋ OUTPUTS:

The output can be divided into 3 sections:

1. Index Title (Name & Value).

2. Index Holdings.

3. Index Chart.

1. Index Title , displays the index name at the top, and at the bottom, it shows the index value, along with the daily change in points and percentage.

2. Index Holdings , displays list the holding securities inside a table that contains the ticker, price, daily change %, market cap, and weight %. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

3. Index Chart , display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

(1) Naming the index.

(2) Entering a currency. To unite all securities in one currency.

(3) Table location on the chart.

(4) Table’s cells size.

(5) Table’s colors.

(6) Sorting table. By securities’ (Market Cap, Change%, Price, or Ticker Alphabetical) order.

(7) Plotting formation (Candle, Bar, or Line)

(8) To show/hide any indicator’s components.

(9) There are 34 fields where user can fill them with symbols.

Please let me know if you have any questions.

arraysLibrary "arraymethods"

Supplementary array methods.

delete(arr, index)

remove int object from array of integers at specific index

Parameters:

arr : int array

index : index at which int object need to be removed

Returns: void

delete(arr, index)

remove float object from array of float at specific index

Parameters:

arr : float array

index : index at which float object need to be removed

Returns: float

delete(arr, index)

remove bool object from array of bool at specific index

Parameters:

arr : bool array

index : index at which bool object need to be removed

Returns: bool

delete(arr, index)

remove string object from array of string at specific index

Parameters:

arr : string array

index : index at which string object need to be removed

Returns: string

delete(arr, index)

remove color object from array of color at specific index

Parameters:

arr : color array

index : index at which color object need to be removed

Returns: color

delete(arr, index)

remove line object from array of lines at specific index and deletes the line

Parameters:

arr : line array

index : index at which line object need to be removed and deleted

Returns: void

delete(arr, index)

remove label object from array of labels at specific index and deletes the label

Parameters:

arr : label array

index : index at which label object need to be removed and deleted

Returns: void

delete(arr, index)

remove box object from array of boxes at specific index and deletes the box

Parameters:

arr : box array

index : index at which box object need to be removed and deleted

Returns: void

delete(arr, index)

remove table object from array of tables at specific index and deletes the table

Parameters:

arr : table array

index : index at which table object need to be removed and deleted

Returns: void

delete(arr, index)

remove linefill object from array of linefills at specific index and deletes the linefill

Parameters:

arr : linefill array

index : index at which linefill object need to be removed and deleted

Returns: void

popr(arr)

remove last int object from array

Parameters:

arr : int array

Returns: int

popr(arr)

remove last float object from array

Parameters:

arr : float array

Returns: float

popr(arr)

remove last bool object from array

Parameters:

arr : bool array

Returns: bool

popr(arr)

remove last string object from array

Parameters:

arr : string array

Returns: string

popr(arr)

remove last color object from array

Parameters:

arr : color array

Returns: color

popr(arr)

remove and delete last line object from array

Parameters:

arr : line array

Returns: void

popr(arr)

remove and delete last label object from array

Parameters:

arr : label array

Returns: void

popr(arr)

remove and delete last box object from array

Parameters:

arr : box array

Returns: void

popr(arr)

remove and delete last table object from array

Parameters:

arr : table array

Returns: void

popr(arr)

remove and delete last linefill object from array

Parameters:

arr : linefill array

Returns: void

shiftr(arr)

remove first int object from array

Parameters:

arr : int array

Returns: int

shiftr(arr)

remove first float object from array

Parameters:

arr : float array

Returns: float

shiftr(arr)

remove first bool object from array

Parameters:

arr : bool array

Returns: bool

shiftr(arr)

remove first string object from array

Parameters:

arr : string array

Returns: string

shiftr(arr)

remove first color object from array

Parameters:

arr : color array

Returns: color

shiftr(arr)

remove and delete first line object from array

Parameters:

arr : line array

Returns: void

shiftr(arr)

remove and delete first label object from array

Parameters:

arr : label array

Returns: void

shiftr(arr)

remove and delete first box object from array

Parameters:

arr : box array

Returns: void

shiftr(arr)

remove and delete first table object from array

Parameters:

arr : table array

Returns: void

shiftr(arr)

remove and delete first linefill object from array

Parameters:

arr : linefill array

Returns: void

push(arr, val, maxItems)

add int to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : int array

val : int object to be pushed

maxItems : max number of items array can hold

Returns: int

push(arr, val, maxItems)

add float to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : float array

val : float object to be pushed

maxItems : max number of items array can hold

Returns: float

push(arr, val, maxItems)

add bool to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : bool array

val : bool object to be pushed

maxItems : max number of items array can hold

Returns: bool

push(arr, val, maxItems)

add string to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : string array

val : string object to be pushed

maxItems : max number of items array can hold

Returns: string

push(arr, val, maxItems)

add color to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : color array

val : color object to be pushed

maxItems : max number of items array can hold

Returns: color

push(arr, val, maxItems)

add line to the end of an array with max items cap. Objects are removed and deleted from start to maintain max items cap

Parameters:

arr : line array

val : line object to be pushed

maxItems : max number of items array can hold

Returns: line

push(arr, val, maxItems)

add label to the end of an array with max items cap. Objects are removed and deleted from start to maintain max items cap

Parameters:

arr : label array

val : label object to be pushed

maxItems : max number of items array can hold

Returns: label

push(arr, val, maxItems)

add box to the end of an array with max items cap. Objects are removed and deleted from start to maintain max items cap

Parameters:

arr : box array

val : box object to be pushed

maxItems : max number of items array can hold

Returns: box

push(arr, val, maxItems)

add table to the end of an array with max items cap. Objects are removed and deleted from start to maintain max items cap

Parameters:

arr : table array

val : table object to be pushed

maxItems : max number of items array can hold

Returns: table

push(arr, val, maxItems)

add linefill to the end of an array with max items cap. Objects are removed and deleted from start to maintain max items cap

Parameters:

arr : linefill array

val : linefill object to be pushed

maxItems : max number of items array can hold

Returns: linefill

unshift(arr, val, maxItems)

add int to the beginning of an array with max items cap. Objects are removed from end to maintain max items cap

Parameters:

arr : int array

val : int object to be unshift

maxItems : max number of items array can hold

Returns: int

unshift(arr, val, maxItems)

add float to the beginning of an array with max items cap. Objects are removed from end to maintain max items cap

Parameters:

arr : float array

val : float object to be unshift

maxItems : max number of items array can hold

Returns: float

unshift(arr, val, maxItems)

add bool to the beginning of an array with max items cap. Objects are removed from end to maintain max items cap

Parameters:

arr : bool array

val : bool object to be unshift

maxItems : max number of items array can hold

Returns: bool

unshift(arr, val, maxItems)

add string to the beginning of an array with max items cap. Objects are removed from end to maintain max items cap

Parameters:

arr : string array

val : string object to be unshift

maxItems : max number of items array can hold

Returns: string

unshift(arr, val, maxItems)

add color to the beginning of an array with max items cap. Objects are removed from end to maintain max items cap

Parameters:

arr : color array

val : color object to be unshift

maxItems : max number of items array can hold

Returns: color

unshift(arr, val, maxItems)

add line to the beginning of an array with max items cap. Objects are removed and deleted from end to maintain max items cap

Parameters:

arr : line array

val : line object to be unshift

maxItems : max number of items array can hold

Returns: line

unshift(arr, val, maxItems)

add label to the beginning of an array with max items cap. Objects are removed and deleted from end to maintain max items cap

Parameters:

arr : label array

val : label object to be unshift

maxItems : max number of items array can hold

Returns: label

unshift(arr, val, maxItems)

add box to the beginning of an array with max items cap. Objects are removed and deleted from end to maintain max items cap

Parameters:

arr : box array

val : box object to be unshift

maxItems : max number of items array can hold

Returns: box

unshift(arr, val, maxItems)

add table to the beginning of an array with max items cap. Objects are removed and deleted from end to maintain max items cap

Parameters:

arr : table array

val : table object to be unshift

maxItems : max number of items array can hold

Returns: table

unshift(arr, val, maxItems)

add linefill to the beginning of an array with max items cap. Objects are removed and deleted from end to maintain max items cap

Parameters:

arr : linefill array

val : linefill object to be unshift

maxItems : max number of items array can hold

Returns: linefill

flush(arr)

remove all int objects in an array

Parameters:

arr : int array

Returns: int

flush(arr)

remove all float objects in an array

Parameters:

arr : float array

Returns: float

flush(arr)

remove all bool objects in an array

Parameters:

arr : bool array

Returns: bool

flush(arr)

remove all string objects in an array

Parameters:

arr : string array

Returns: string

flush(arr)

remove all color objects in an array

Parameters:

arr : color array

Returns: color

flush(arr)

remove and delete all line objects in an array

Parameters:

arr : line array

Returns: line

flush(arr)

remove and delete all label objects in an array

Parameters:

arr : label array

Returns: label

flush(arr)

remove and delete all box objects in an array

Parameters:

arr : box array

Returns: box

flush(arr)

remove and delete all table objects in an array

Parameters:

arr : table array

Returns: table

flush(arr)

remove and delete all linefill objects in an array

Parameters:

arr : linefill array

Returns: linefill

Price Cross Time Custom Range Interactive█ OVERVIEW

This indicator was a time-based indicator and intended as educational purpose only based on pine script v5 functions for ta.cross() , ta.crossover() and ta.crossunder() .

I realised that there is some overlap price with the cross functions, hence I integrate them into Custom Range Interactive with value variance and overlap displayed into table.

This was my submission for Pinefest #1 , I decided to share this as public, I may accidentally delete this as long as i keep as private.

█ INSPIRATION

Inspired by design, code and usage of CAGR. Basic usage of custom range / interactive, pretty much explained here . Credits to TradingView.

█ FEATURES

1. Custom Range Interactive

2. Label can be resize and change color.

3. Label show tooltip for price and time.

4. Label can be offset to improve readability.

5. Table can show price variance when any cross is true.

6. Table can show overlap if found crosss is overlap either with crossover and crossunder.

7. Table text color automatically change based on chart background (light / dark mode).

8. Source 2 is drawn as straight line, while Source 1 will draw as label either above line for crossover, below line for crossunder and marked 'X' if crossing with Source 2's line.

9. Cross 'X' label can be offset to improve readability.

10. Both Source 1 and Source 2 can select Open, Close, High and Low, which can be displayed into table.

█ LIMITATIONS

1. Table is limited to intraday timeframe only as time format is not accurate for daily timeframe and above. Example daily timeframe will give result less 1 day from actual date.

2. I did not include other sources such external source or any built in sources such as hl2, hlc3, ohlc4 and hlcc4.

█ CODE EXPLAINATION

I pretty much create custom function with method which returns tuple value.

method crossVariant(float price = na, chart.point ref = na) =>

cross = ta.cross( price, ref.price)

over = ta.crossover( price, ref.price)

under = ta.crossunder(price, ref.price)

Unfortunately, I unable make the labels into array which i plan to return string value by getting the text value from array label, hence i use label.all and add incremental int value as reference.

series label labelCross = na, labelCross.delete()

var int num = 0

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

I realised cross value can be overlap with crossover and crossunder, hence I add bool to enable force overlap and add additional bools.

series label labelCross = na, labelCross.delete()

var int num = 0

if forceOverlap

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

else

if cross and over

num += 1

labelCross := label.new()

if cross and under

num += 1

labelCross := label.new()

if cross and not over and not under

num += 1

labelCross := label.new()

█ USAGE / EXAMPLES

Major and Minor Trend Indicator by Nikhil34a V 2.2Title: Major and Minor Trend Indicator by Nikhil34a V 2.2

Description:

The Major and Minor Trend Indicator v2.2 is a comprehensive technical analysis script designed for use with the TradingView platform. This powerful tool is developed in Pine Script version 5 and helps traders identify potential buying and selling opportunities in the stock market.

Features:

SMA Trend Analysis: The script calculates two Simple Moving Averages (SMAs) with user-defined lengths for major and minor trends. It displays these SMAs on the chart, allowing traders to visualize the prevailing trends easily.

Surge Detection: The indicator can detect buying and selling surges based on specific conditions, such as volume, RSI, MACD, and stochastic indicators. Both Buying and Selling surges are marked in black on the chart.

Option Buy Zone Detection: The script identifies the option buy zone based on SMA crossovers, RSI, and MACD values. The buy zone is categorized as "CE Zone" or "PE Zone" and displayed in the table along with the trigger time.

Two-Day High and Low Range: The script calculates the highest high and lowest low of the previous two trading days and plots them on the chart. The area between these points is shaded in semi-transparent green and red colors.

Crossover Analysis: The script analyzes moving average crossovers on multiple timeframes (2-minute, 3-minute, and 5-minute) and displays buy and sell signals accordingly.

Trend Identification: The script identifies the major and minor trends as either bullish or bearish, providing valuable insights into the overall market sentiment.

Usage:

Customize Major and Minor SMA Periods: Adjust the lengths of major and minor SMAs through input parameters to suit your trading preferences.

Enable/Disable Moving Averages: Choose which SMAs to display on the chart by toggling the "showXMA" input options.

Set Surge and Option Buy Zone Thresholds: Modify the surgeThreshold, volumeThreshold, RSIThreshold, and StochThreshold inputs to refine the surge and buy zone detection.

Analyze Crossover Signals: Monitor the crossover signals in the table, categorized by timeframes (2-minute, 3-minute, and 5-minute).

Explore Market Bias and Distance to 2-Day High/Low: The table provides information on market bias, current price movement relative to the previous two-day high and low, and the option buy zone status.

Additional Use Cases:

Surge Indicator:

The script includes a Surge Indicator that detects sudden buying or selling surges in the market. When a buying surge is identified, the "BSurge" label will appear below the corresponding candle with black text on a white background. Similarly, a selling surge will display the "SSurge" label in white text on a black background. These indicators help traders quickly spot strong buying or selling activities that may influence their trading decisions. These surges can be used to identify sudden premium dump zones.

Option Buy Zone:

The Option Buy Zone is an essential feature that identifies potential zones for buying call options (CE Zone) or put options (PE Zone) based on specific technical conditions. The indicator evaluates SMA crossovers, RSI, and MACD values to determine the current market sentiment. When the option buy zone is triggered, the script will display the respective zone ("CE Zone" or "PE Zone") in the table, highlighted with a white background. Additionally, the time when the buy zone was triggered will be shown under the "Option Buy Zone Trigger Time" column.

Price Movement Relative to 2-Day High/Low:

The script calculates the highest high and lowest low of the previous two trading days (high2DaysAgo and low2DaysAgo) and plots these points on the chart. The area between these two points is shaded in semi-transparent green and red colors. The green region indicates the price range between the highpricetoconsider (highest high of the previous two days) and the lower value between highPreviousDay and high2DaysAgo. Similarly, the red region represents the price range between the lowpricetoconsider (lowest low of the previous two days) and the higher value between lowPreviousDay and low2DaysAgo.

Entry Time and Current Zone:

The script identifies potential entry times for trades within the option buy zone. When a valid buy zone trigger occurs, the script calculates the entryTime by adding the durationInMinutes (user-defined) to the startTime. The entryTime will be displayed in the "Entry Time" column of the table. Depending on the comparison between optionbuyzonetriggertime and entryTime, the background color of the entry time will change. If optionbuyzonetriggertime is greater than entryTime, the background color will be yellow, indicating that a new trigger has occurred before the specified duration. Otherwise, the background color will be green, suggesting that the entry time is still within the defined duration.

Current Zone Indicator:

The script further categorizes the current zone as either "CE Zone" (call option zone) or "PE Zone" (put option zone). When the market is trending upwards and the minor SMA is above the major SMA, the currentZone will be set to "CE Zone." Conversely, when the market is trending downwards and the minor SMA is below the major SMA, the currentZone will be "PE Zone." This information is displayed in the "Current Zone" column of the table.

These additional use cases empower traders with valuable insights into market trends, buying and selling surges, option buy zones, and potential entry times. Traders can combine this information with their analysis and risk management strategies to make informed and confident trading decisions.

Note:

The script is optimized for identifying trends and potential trade opportunities. It is crucial to perform additional analysis and risk management before executing any trades based on the provided signals.

Happy Trading!

Price Legs: Average Heights; 'Smart ATR'Price Legs: Average Heights; 'Smart ATR'. Consol Range Gauge

~~ Indicator to show small and large price legs (based on short and long input pivot lengths), and calculating the average heights of these price legs; counting legs from user-input start time ~~

//Premise: Wanted to use this as something like a 'Smart ATR': where the average/typical range of a distinct & dynamic price leg could be calculated based on a user-input time interval (as opposed to standard ATR, which is simply the average range over a consistent repeating period, with no regard to market structure). My instinct is that this would be most useful for consolidated periods & range trading: giving the trader an idea of what the typical size of a price leg might be in the current market state (hence in the title, Consol Range gauge)

//Features & User inputs:

-Start time: confirm input when loading indicator by clicking on the chart. Then drag the vertical line to change start time easily.

-Large Legs (toggle on/off) and user-input pivot lookback/lookforward length (larger => larger legs)

-Small Legs (toggle on/off) and user-input pivot lookback/lookforward length (smaller => smaller legs)

-Display Stats table: toggle on/off: simple view- shows the averages of large (up & down), small (up & down), and combined (for each).

-Extended stats table: toggle on/off option to show the averages of the last 3 legs of each category (up/down/large/small/combined)

-Toggle on/off Time & Price chart text labels of price legs (time in mins/hours/days; price in $ or pips; auto assigned based on asset)

-Table position: user choice.

//Notes & tips:

-Using custom start time along with replay mode, you can select any arbitrary chunk of price for the purpose of backtesting.

-Play around with the pivot lookback lengths to find price legs most suitable to the current market regime (consolidating/trending; high volatility/ low volatility)

-Single bar price legs will never be counted: they must be at least 2 bars from H>>L or L>>H.

//Credits: Thanks to @crypto_juju for the idea of applying statistics to this simple price leg indicator.

Simple View: showing only the full averages (counting from Start time):

View showing ONLY the large legs, with Time & Price labels toggled ON:

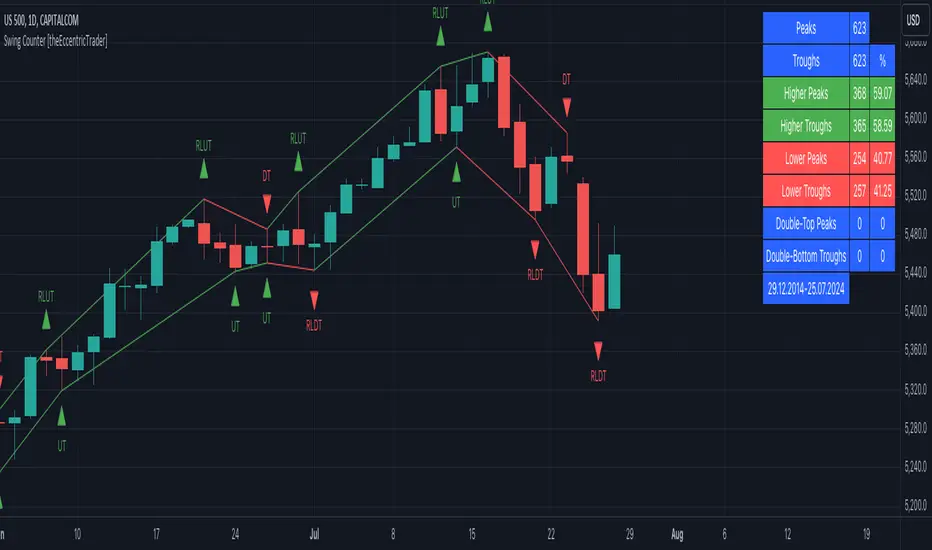

Swing Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed swing high and swing low scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a high price equal to or above the price it opened.

• A red candle is one that closes with a low price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Peak and Trough Prices (Advanced)

• The advanced peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the highest preceding green candle high price, depending on which is higher.

• The advanced trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the lowest preceding red candle low price, depending on which is lower.

Green and Red Peaks and Troughs

• A green peak is one that derives its price from the green candle/s that constitute the swing high.

• A red peak is one that derives its price from the red candle that completes the swing high.

• A green trough is one that derives its price from the green candle that completes the swing low.

• A red trough is one that derives its price from the red candle/s that constitute the swing low.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

█ FEATURES

Inputs

• Start Date

• End Date

• Position

• Text Size

• Show Sample Period

• Show Plots

• Show Lines

Table

The table is colour coded, consists of three columns and nine rows. Blue cells denote neutral scenarios, green cells denote return line uptrend and uptrend scenarios, and red cells denote downtrend and return line downtrend scenarios.

The swing scenarios are listed in the first column with their corresponding total counts to the right, in the second column. The last row in column one, row nine, displays the sample period which can be adjusted or hidden via indicator settings.

Rows three and four in the third column of the table display the total higher peaks and higher troughs as percentages of total peaks and troughs, respectively. Rows five and six in the third column display the total lower peaks and lower troughs as percentages of total peaks and troughs, respectively. And rows seven and eight display the total double-top peaks and double-bottom troughs as percentages of total peaks and troughs, respectively.

Plots

I have added plots as a visual aid to the swing scenarios listed in the table. Green up-arrows with ‘HP’ denote higher peaks, while green up-arrows with ‘HT’ denote higher troughs. Red down-arrows with ‘LP’ denote higher peaks, while red down-arrows with ‘LT’ denote lower troughs. Similarly, blue diamonds with ‘DT’ denote double-top peaks and blue diamonds with ‘DB’ denote double-bottom troughs. These plots can be hidden via indicator settings.

Lines

I have also added green and red trendlines as a further visual aid to the swing scenarios listed in the table. Green lines denote return line uptrends (higher peaks) and uptrends (higher troughs), while red lines denote downtrends (lower peaks) and return line downtrends (lower troughs). These lines can be hidden via indicator settings.

█ HOW TO USE

This indicator is intended for research purposes and strategy development. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe. It can, for example, give you an idea of any inherent biases such as a greater proportion of higher peaks to lower peaks. Or a greater proportion of higher troughs to lower troughs. Such information can be very useful when conducting top down analysis across multiple timeframes, or considering entry and exit methods.

What I find most fascinating about this logic, is that the number of swing highs and swing lows will always find equilibrium on each new complete wave cycle. If for example the chart begins with a swing high and ends with a swing low there will be an equal number of swing highs to swing lows. If the chart starts with a swing high and ends with a swing high there will be a difference of one between the two total values until another swing low is formed to complete the wave cycle sequence that began at start of the chart. Almost as if it was a fundamental truth of price action, although quite common sensical in many respects. As they say, what goes up must come down.

The objective logic for swing highs and swing lows I hope will form somewhat of a foundational building block for traders, researchers and developers alike. Not only does it facilitate the objective study of swing highs and swing lows it also facilitates that of ranges, trends, double trends, multi-part trends and patterns. The logic can also be used for objective anchor points. Concepts I will introduce and develop further in future publications.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.