Uptrick Signal Density Cloud🟪 Introduction

The Uptrick Signal Density Cloud is designed to track market direction and highlight potential reversals or shifts in momentum. It plots two smoothed lines on the chart and fills the space between them (often called a “cloud”). The bars on the chart change color depending on bullish or bearish conditions, and small triangles appear when certain reversal criteria are met. A metrics table displays real-time values for easy reference.

🟩 Why These Features Have Been Linked Together

1) Dual-Line Structure

Two separate lines represent shorter- and longer-term market tendencies. Linking them in one tool allows traders to view both near-term changes and the broader directional bias in a single glance.

2) Smoothed Averages

The script offers multiple smoothing methods—exponential, simple, hull, and an optimized approach—to reduce noise. Using more than one type of moving average can help balance responsiveness with stability.

3) Density Cloud Concept

Shading the region between the two lines highlights the gap or “thickness.” A wider gap typically signals stronger momentum, while a narrower gap could indicate a weakening trend or potential market indecision. When the cloud is too wide and crosses a certain threshold defined by the user, it indicates a possible reversal. When the cloud is too narrow it may indicate a potential breakout.

🟪 Why Use This Indicator

• Trend Visibility: The color-coded lines and bars make it easier to distinguish bullish from bearish conditions.

• Momentum Tracking: Thicker cloud regions suggest stronger separation between the faster and slower lines, potentially indicating robust momentum.

• Possible Reversal Alerts: Small triangles appear within thick zones when the indicator detects a crossover, drawing attention to key moments of potential trend change.

• Quick Reference Table: A metrics table shows line values, bullish or bearish status, and cloud thickness without needing to hover over chart elements.

🟩 Inputs

1) First Smoothing Length (length1)

Default: 14

Defines the lookback period for the faster line. Lower values make the line respond more quickly to price changes.

2) Second Smoothing Length (length2)

Default: 28

Defines the lookback period for the slower line or one of the moving averages in optimized mode. It generally responds more slowly than the faster line.

3) Extra Smoothing Length (extraLength)

Default: 50

A medium-term period commonly seen in technical analysis. In optimized mode, it helps add broader perspective to the combined lines.

4) Source (source)

Default: close

Specifies the price data (for example, open, high, low, or a custom source) used in the calculations.

5) Cloud Type (cloudType)

Options: Optimized, EMA, SMA, HMA

Determines the smoothing method used for the lines. “Optimized” blends multiple exponential averages at different lengths.

6) Cloud Thickness Threshold (thicknessThreshold)

Default: 0.5

Sets the minimum separation between the two lines to qualify as a “thick” zone, indicating potentially stronger momentum.

🟪 Core Components

1) Faster and Slower Lines

Each line is smoothed according to user preferences or the optimized technique. The faster line typically reacts more quickly, while the slower line provides a broader overview.

2) Filled Density Cloud

The space between the two lines is filled to visualize in which direction the market is trending.

3) Color-Coded Bars

Price bars adopt bullish or bearish colors based on which line is on top, providing an immediate sense of trend direction.

4) Reversal Triangles

When the cloud is thick (exceeding the threshold) and the lines cross in the opposite direction, small triangles appear, signaling a possible market shift.

5) Metrics Table

A compact table shows the current values of both lines, their bullish/bearish statuses, the cloud thickness, and whether the cloud is in a “reversal zone.”

🟩 Calculation Process

1) Raw Averages

Depending on the mode, standard exponential, simple, hull, or “optimized” exponential blends are calculated.

2) Optimized Averages (if selected)

The faster line is the average of three exponential moving averages using length1, length2, and extraLength.

The slower line similarly uses those same lengths multiplied by 1.5, then averages them together for broader smoothing.

3) Difference and Threshold

The absolute gap between the two lines is measured. When it exceeds thicknessThreshold, the cloud is considered thick.

4) Bullish or Bearish Determination

If sma1 (the faster line) is above sma2 (the slower line), conditions are deemed bullish; otherwise, they are bearish. This distinction is reflected in both bar colors and cloud shading.

5) Reversal Markers

In thick zones, a crossover triggers a triangle at the point of potential reversal, alerting traders to a possible trend change.

🟪 Smoothing Methods

1) Exponential (EMA)

Prioritizes recent data for quicker responsiveness.

2) Simple (SMA)

Takes a straightforward average of the chosen period, smoothing price action but often lagging more in volatile markets.

3) Hull (HMA)

Employs a specialized formula to reduce lag while maintaining smoothness.

4) Optimized (Blended Exponential)

Combines multiple EMA calculations to strike a balance between responsiveness and noise reduction.

🟩 Cloud Logic and Reversal Zones

Cloud thickness above the defined threshold typically signals exceeding momentum and can lead to a quick reversal. During these thick periods, if the width exceeds the defined threshold, small triangles mark potential reversal points. In order for the reversal shape to show, the color of the cloud has to be the opposite. So, for example, if the cloud is bearish, and exceeds momentum, defined by the user, a bullish signal appears. The opposite conditions for a bullish signal. This approach can help traders focus on notable changes rather than minor oscillations.

🟪 Bar Coloring and Layered Lines

Bars take on bullish or bearish tints, matching the faster line’s position relative to the slower line. The lines themselves are plotted multiple times with varying opacities, creating a layered, glowing look that enhances visibility without affecting calculations.

🟩 The Metrics Table

Located in the top-right corner of the chart, this table displays:

• SMA1 and SMA2 current values.

• Bullish or bearish alignment for each line.

• Cloud thickness.

• Reversal zone status (in or out of zone).

This numeric readout allows for a quick data check without hovering over the chart.

🟪 Why These Specific Moving Average Lengths Are Used

Default lengths of 14, 28, and 50 are common in technical analysis. Fourteen captures near-term price movement without overreacting. Twenty-eight, roughly double 14, provides a moderate smoothing level. Fifty is widely regarded as a medium-term benchmark. Multiplying each length by 1.5 for the slower line enhances separation when combined with the faster line.

🟩 Originality and Usefulness

• Multi-Layered Smoothing. The user can select from several moving average modes, including a unique “optimized” blend, possibly reducing random fluctuations in the market data.

• Combined Visual and Numeric Clarity. Bars, clouds, and a real-time table merge into a single interface, enabling efficient trend analysis.

• Focus on Significant Shifts. Thick cloud zones and triangles draw attention to potentially stronger momentum changes and plausible reversals.

• Flexible Across Markets. The adjustable lengths and threshold can be tuned to different asset classes (stocks, forex, commodities, crypto) and timeframes.

By integrating multiple technical concepts—cloud-based trend detection, color coding, reversal markers, and an immediate reference table—the Uptrick Signal Density Cloud aims to streamline chart reading and decision-making.

🟪 Additional Considerations

• Timeframes. Intraday, daily, and weekly charts each yield different signals. Adjust the smoothing lengths and threshold to suit specific trading horizons.

• Market Types. Though applicable across asset classes, parameters might need tweaking to address the volatility of commodities, forex pairs, or cryptocurrencies.

• Confirmation Tools. Pairing this indicator with volume studies or support/resistance analysis can improve the reliability of signals.

• Potential Limitations. No indicator is foolproof; sudden market shifts or choppy conditions may reduce accuracy. Cautious position sizing and risk management remain essential.

🟩 Disclaimers

The Uptrick Signal Density Cloud relies on historical price data and may lag sudden moves or provide false positives in ranging conditions. Always combine it with other analytical techniques and sound risk management. This script is offered for educational purposes only and should not be considered financial advice.

🟪 Conclusion

The Uptrick Signal Density Cloud blends trend identification, momentum assessment, and potential reversal alerts in a single, user-friendly tool. With customizable smoothing methods and a focus on cloud thickness, it visually highlights important market conditions. While it cannot guarantee predictive accuracy, it can serve as a comprehensive reference for traders seeking both a quick snapshot of the current trend and deeper insights into market dynamics.

ابحث في النصوص البرمجية عن "Table"

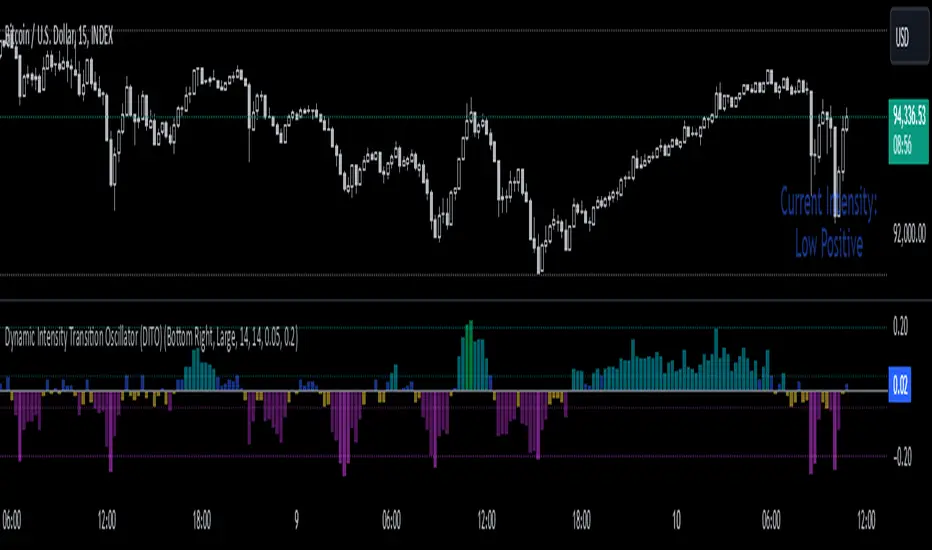

Dynamic Intensity Transition Oscillator (DITO)The Dynamic Intensity Transition Oscillator (DITO) is a comprehensive indicator designed to identify and visualize the slope of price action normalized by volatility, enabling consistent comparisons across different assets. This indicator calculates and categorizes the intensity of price movement into six states—three positive and three negative—while providing visual cues and alerts for state transitions.

Components and Functionality

1. Slope Calculation

- The slope represents the rate of change in price action over a specified period (Slope Calculation Period).

- It is calculated as the difference between the current price and the simple moving average (SMA) of the price, divided by the length of the period.

2. Normalization Using ATR

- To standardize the slope across assets with different price scales and volatilities, the slope is divided by the Average True Range (ATR).

- The ATR ensures that the slope is comparable across assets with varying price levels and volatility.

3. Intensity Levels

- The normalized slope is categorized into six distinct intensity levels:

High Positive: Strong upward momentum.

Medium Positive: Moderate upward momentum.

Low Positive: Weak upward movement or consolidation.

Low Negative: Weak downward movement or consolidation.

Medium Negative: Moderate downward momentum.

High Negative: Strong downward momentum.

4. Visual Representation

- The oscillator is displayed as a histogram, with each intensity level represented by a unique color:

High Positive: Lime green.

Medium Positive: Aqua.

Low Positive: Blue.

Low Negative: Yellow.

Medium Negative: Purple.

High Negative: Fuchsia.

Threshold levels (Low Intensity, Medium Intensity) are plotted as horizontal dotted lines for visual reference, with separate colors for positive and negative thresholds.

5. Intensity Table

- A dynamic table is displayed on the chart to show the current intensity level.

- The table's text color matches the intensity level color for easy interpretation, and its size and position are customizable.

6. Alerts for State Transitions

- The indicator includes a robust alerting system that triggers when the intensity level transitions from one state to another (e.g., from "Medium Positive" to "High Positive").

- The alert includes both the previous and current states for clarity.

Inputs and Customization

The DITO indicator offers a variety of customizable settings:

Indicator Parameters

Slope Calculation Period: Defines the period over which the slope is calculated.

ATR Calculation Period: Defines the period for the ATR used in normalization.

Low Intensity Threshold: Threshold for categorizing weak momentum.

Medium Intensity Threshold: Threshold for categorizing moderate momentum.

Intensity Table Settings

Table Position: Allows you to position the intensity table anywhere on the chart (e.g., "Bottom Right," "Top Left").

Table Size: Enables customization of table text size (e.g., "Small," "Large").

Use Cases

Trend Identification:

- Quickly assess the strength and direction of price movement with color-coded intensity levels.

Cross-Asset Comparisons:

- Use the normalized slope to compare momentum across different assets, regardless of price scale or volatility.

Dynamic Alerts:

- Receive timely alerts when the intensity transitions, helping you act on significant momentum changes.

Consolidation Detection:

- Identify periods of low intensity, signaling potential reversals or breakout opportunities.

How to Use

- Add the indicator to your chart.

- Configure the input parameters to align with your trading strategy.

Observe:

The Oscillator: Use the color-coded histogram to monitor price action intensity.

The Intensity Table: Track the current intensity level dynamically.

Alerts: Respond to state transitions as notified by the alerts.

Final Notes

The Dynamic Intensity Transition Oscillator (DITO) combines trend strength detection, cross-asset comparability, and real-time alerts to offer traders an insightful tool for analyzing market conditions. Its user-friendly visualization and comprehensive alerting make it suitable for both novice and advanced traders.

Disclaimer: This indicator is for educational purposes and is not financial advice. Always perform your own analysis before making trading decisions.

Average Price Range Screener [KFB Quant]Average Price Range Screener

Overview:

The Average Price Range Screener is a technical analysis tool designed to provide insights into the average price volatility across multiple symbols over user-defined time periods. The indicator compares price ranges from different assets and displays them in a visual table and chart for easy reference. This can be especially helpful for traders looking to identify symbols with high or low volatility across various time frames.

Key Features:

Multiple Symbols Supported:

The script allows for analysis of up to 10 symbols, such as major cryptocurrencies and market indices. Symbols can be selected by the user and configured for tracking price volatility.

Dynamic Range Calculation:

The script calculates the average price range of each symbol over three distinct time periods (default are 30, 60, and 90 bars). The price range for each symbol is calculated as a percentage of the bar's high-to-low difference relative to its low value.

Range Visualization:

The results are visually represented using:

- A color-coded table showing the calculated average ranges of each symbol and the current chart symbol.

- A line plot that visually tracks the volatility for each symbol on the chart, with color gradients representing the range intensity from low (red/orange) to high (blue/green).

Customizable Inputs:

- Length Inputs: Users can define the time lengths (default are 30, 60, and 90 bars) for calculating average price ranges for each symbol.

- Symbol Inputs: 10 symbols can be tracked at once, with default values set to popular crypto pairs and indices.

- Color Inputs: Users can customize the color scheme for the range values displayed in the table and chart.

Real-Time Ranking:

The indicator ranks symbols by their average price range, providing a clear view of which assets are exhibiting higher volatility at any given time.

Each symbol's range value is color-coded based on its relative volatility within the selected symbols (using a gradient from low to high range).

Data Table:

The table shows the average range values for each symbol in real-time, allowing users to compare volatility across multiple assets at a glance. The table is dynamically updated as new data comes in.

Interactive Labels:

The indicator adds labels to the chart, showing the average range for each symbol. These labels adjust in real-time as the price range values change, giving users an immediate view of volatility rankings.

How to Use:

Set Time Periods: Adjust the time periods (lengths) to match your trading strategy's timeframe and volatility preference.

Symbol Selection: Add and track the price range for your preferred symbols (cryptocurrencies, stocks, indices).

Monitor Volatility: Use the visual table and plot to identify symbols with higher or lower volatility, and adjust your trading strategy accordingly.

Interpret the Table and Chart: Ranges that are color-coded from red/orange (lower volatility) to blue/green (higher volatility) allow you to quickly gauge which symbols are most volatile.

Disclaimer: This tool is provided for informational and educational purposes only and should not be considered as financial advice. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.

Burst PowerThe Burst Power indicator is to be used for Indian markets where most stocks have a maximum price band limit of 20%.

This indicator is intended to identify stocks with high potential for significant price movements. By analysing historical price action over a user-defined lookback period, it calculates a Burst Power score that reflects the stock's propensity for rapid and substantial moves. This can be helpful for stock selection in strategies involving momentum bursts, swing trading, or identifying stocks with explosive potential.

Key Components

____________________

Significant Move Counts:

5% Moves: Counts the number of days within the lookback period where the stock had a positive close-to-close move between 5% and 10%.

10% Moves: Counts the number of days with a positive close-to-close move between 10% and 19%.

19% Moves: Counts the number of days with a positive close-to-close move of 19% or more.

Maximum Price Move (%):

Identifies the largest positive close-to-close percentage move within the lookback period, along with the date it occurred.

Burst Power Score:

A composite score calculated using the counts of significant moves: Burst Power =(Count5%/5) +(Count10%/2) + (Count19%/0.5)

The score is then rounded to the nearest whole number.

A higher Burst Power score indicates a higher frequency of significant price bursts.

Visual Indicators:

Table Display: Presents all the calculated data in a customisable table on the chart.

Markers on Chart: Plots markers on the chart where significant moves occurred, aiding visual analysis.

Using the Lookback Period

____________________________

The lookback period determines how much historical data the indicator analyses. Users can select from predefined options:

3 Months

6 Months

1 Year

3 Years

5 Years

A shorter lookback period focuses on recent price action, which may be more relevant for short-term trading strategies. A longer lookback period provides a broader historical context, useful for identifying long-term patterns and behaviors.

Interpreting the Burst Power Score

__________________________________

High Burst Power Score (≥15):

Indicates the stock frequently experiences significant price moves.

Suitable for traders seeking quick momentum bursts and swing trading opportunities.

Stocks with high scores may be more volatile but offer potential for rapid gains.

Moderate Burst Power Score (10 to 14):

Suggests occasional significant price movements.

May suit traders looking for a balance between volatility and stability.

Low Burst Power Score (<10):

Reflects fewer significant price bursts.

Stocks are more likely to exhibit longer, sustainable, but slower price trends.

May be preferred by traders focusing on steady growth or longer-term investments.

Note: Trading involves uncertainties, and the Burst Power score should be considered as one of many factors in a comprehensive trading strategy. It is essential to incorporate broader market analysis and risk management practices.

Customisation Options

_________________________

The indicator offers several customisation settings to tailor the display and functionality to individual preferences:

Display Mode:

Full Mode: Shows the detailed table with all components, including significant move counts, maximum price move, and the Burst Power score.

Mini Mode: Displays only the Burst Power score and its corresponding indicator (green, orange, or red circle).

Show Latest Date Column:

Toggle the display of the "Latest Date" column in the table, which shows the most recent occurrence of each significant move category.

Theme (Dark Mode):

Switch between Dark Mode and Light Mode for better visual integration with your chart's color scheme.

Table Position and Size:

Position: Place the table at various locations on the chart (top, middle, bottom; left, center, right).

Size: Adjust the table's text size (tiny, small, normal, large, huge, auto) for optimal readability.

Header Size: Customise the font size of the table headers (Small, Medium, Large).

Color Settings:

Disable Colors in Table: Option to display the table without background colors, which can be useful for printing or if colors are distracting.

Bullish Closing Filter:

Another customisation here is to count a move only when the closing for the day is strong. For this, we have an additional filter to see if close is within the chosen % of the range of the day. Closing within the top 1/3, for instance, indicates a way more bullish day tha, say, closing within the bottom 25%.

Move Markers on chart:

The indicator also marks out days with significant moves. You can choose to hide or show the markers on the candles/bars.

Practical Applications

________________________

Momentum Trading: High Burst Power scores can help identify stocks that are likely to experience rapid price movements, suitable for momentum traders.

Swing Trading: Traders looking for short- to medium-term opportunities may focus on stocks with moderate to high Burst Power scores.

Positional Trading: Lower Burst Power scores may indicate steadier stocks that are less prone to volatility, aligning with long-term investment strategies.

Risk Management: Understanding a stock's propensity for significant moves can aid in setting appropriate stop-loss and take-profit levels.

Disclaimer: Trading involves significant risk, and past performance is not indicative of future results. The Burst Power indicator is intended for educational purposes and should not be construed as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decisions.

US30 Challenge 3.0Purpose of the Script

This script is designed to provide advanced technical analysis for the US30 index by combining moving averages (MA and EMA) on different timeframes and a modified Keltner channel to analyze volatility. It visualizes trends across both daily and hourly charts and displays their relationship in a custom table, helping traders to make informed decisions based on the alignment of these indicators.

Explanation of the Key Features

User Input Parameters:

The script allows users to customize several parameters, such as whether to show the baseline moving average, which type of moving average to use (e.g., EMA, SMA, HMA), and the length of the moving average. These inputs make the script flexible, allowing users to adjust it to their trading style.

Moving Averages (MA and EMA):

Two types of moving averages are calculated: the baseline (which can be any of several moving average types) and two additional moving averages (SMA and EMA) based on user-defined periods. These are plotted on the chart to provide insight into the trend and momentum of the US30 price action.

The baseline moving average is central to the strategy, and its calculation can be customized by selecting different methods (e.g., SMA, EMA, or HMA), making it adaptable to different market conditions.

Volatility Bands (Keltner Channel):

The script calculates volatility bands using a method similar to the Keltner Channel. It can either use the True Range (ATR) or the simple high-low price difference to determine market volatility.

These bands are useful for identifying overbought and oversold conditions, as well as detecting periods of price contraction or expansion. The width of the bands is adjustable via a multiplier, allowing users to fine-tune their analysis.

Security Function for Higher Timeframes:

The script retrieves moving average values for the daily timeframe using the request.security() function, which allows it to display higher-timeframe information on lower-timeframe charts. This gives traders a multi-timeframe perspective, helping them align their shorter-term trades with the broader trend.

Trend and Cross Detection:

The script detects when the EMA crosses below or above the SMA on both the daily and hourly timeframes. These crossovers are significant for trend-following strategies, as they often signal shifts in market momentum.

It visually indicates whether the EMA is above or below the SMA for both timeframes using color-coded panels, providing an easy-to-read summary of market conditions.

Custom Table Display:

A custom table is created to summarize the trend information for both the daily and hourly timeframes. The table shows whether the EMA is above or below the SMA for each timeframe, with green or red background colors indicating bullish or bearish conditions, respectively.

This feature is particularly useful for traders who want a quick, at-a-glance confirmation of the trend across multiple timeframes without having to analyze the chart visually.

Visual Plotting:

The script plots the moving averages and volatility bands directly on the price chart, providing clear visual cues for traders. The baseline and bands help traders identify key support and resistance levels, while the additional moving averages help confirm the current trend direction.

How to Use the Script

Adjust Parameters:

Before using the script, traders can customize the type of baseline moving average, its length, and the volatility band multiplier to suit their specific strategy and market conditions. Users can also choose whether to use the True Range or high-low difference for the volatility calculation.

Multi-Timeframe Analysis:

The script combines information from both daily and hourly charts, making it ideal for traders who prefer to align their short-term trades with the broader market trend. The custom table provides a quick snapshot of the trend on both timeframes, allowing users to see if the EMA is above or below the SMA in both cases.

Visual Cues:

By watching the relationship between price and the plotted bands, traders can identify potential breakouts, consolidations, or reversals. The moving average crossovers provide a simple, yet powerful, signal for entering or exiting trades.

Trend Confirmation:

The color-coded custom table helps traders quickly confirm the trend without having to analyze the price action directly. If both the daily and hourly EMA are above their respective SMA, this indicates a strong bullish trend. Conversely, if the EMA is below the SMA on both timeframes, this signals a bearish trend.

Differences from Other Scripts

Multi-Timeframe Cross Detection: Unlike many scripts, this one focuses on detecting moving average crossovers across multiple timeframes (daily and hourly), providing traders with a more comprehensive view of the market.

Custom Volatility Band Calculation: It includes a customizable Keltner-like channel, offering flexibility in how volatility is calculated, which is not commonly found in standard indicators.

Visual Trend Table: The addition of a custom table to visually display trend confirmation across different timeframes sets this script apart from most others, making it easier for traders to digest the information.

******************************************************************** (Español)

Propósito del Script

Este script está diseñado para proporcionar un análisis técnico avanzado del índice US30, combinando medias móviles (MA y EMA) en diferentes marcos de tiempo y un canal Keltner modificado para analizar la volatilidad. Visualiza las tendencias tanto en gráficos diarios como horarios y muestra su relación en una tabla personalizada, ayudando a los traders a tomar decisiones informadas basadas en la alineación de estos indicadores.

Explicación de las Características Clave

Parámetros de Entrada del Usuario:

El script permite a los usuarios personalizar varios parámetros, como si mostrar la media móvil base, qué tipo de media móvil usar (por ejemplo, EMA, SMA, HMA) y la longitud de la media móvil. Estos inputs hacen que el script sea flexible, permitiendo que los usuarios lo ajusten a su estilo de trading.

Medias Móviles (MA y EMA):

Se calculan dos tipos de medias móviles: la base (que puede ser de varios tipos) y dos medias adicionales (SMA y EMA) basadas en los períodos definidos por el usuario. Estas se trazan en el gráfico para proporcionar información sobre la tendencia y el impulso de la acción del precio del US30.

La media móvil base es central en la estrategia, y su cálculo se puede personalizar seleccionando diferentes métodos (por ejemplo, SMA, EMA, o HMA), lo que la hace adaptable a diferentes condiciones de mercado.

Bandas de Volatilidad (Canal Keltner):

El script calcula bandas de volatilidad usando un método similar al Canal Keltner. Puede usar el Rango Verdadero (ATR) o la simple diferencia entre el alto y el bajo del precio para determinar la volatilidad del mercado.

Estas bandas son útiles para identificar condiciones de sobrecompra y sobreventa, así como para detectar períodos de contracción o expansión del precio.

Función security() para Tiempos Superiores:

El script obtiene los valores de las medias móviles para el marco temporal diario, utilizando la función request.security(), lo que permite mostrar información de marcos temporales más largos en gráficos de marcos más cortos.

Detección de Cruces de Tendencia:

El script detecta cuando la EMA cruza por debajo o por encima de la SMA en los gráficos diarios y horarios. Estos cruces son significativos para estrategias de seguimiento de tendencias, ya que suelen señalar cambios en el impulso del mercado.

Tabla de Tendencias Personalizada:

Se crea una tabla personalizada para resumir la información de la tendencia en los gráficos diarios y horarios, mostrando si la EMA está por encima o por debajo de la SMA.

Trazado Visual:

El script traza las medias móviles y las bandas de volatilidad directamente en el gráfico de precios, proporcionando señales visuales claras para los traders.

Cómo usar el Script

Ajustar Parámetros.

Análisis Multi-Tiempo.

Señales Visuales.

Confirmación de Tendencia.

Diferencias con Otros Scripts

Detección Multi-Tiempo de Cruces.

Cálculo Personalizado de Bandas de Volatilidad.

Tabla Visual de Tendencia.

Saludos

VM y CS

Ticker Tape█ OVERVIEW

This indicator creates a dynamic, scrolling display of multiple securities' latest prices and daily changes, similar to the ticker tapes on financial news channels and the Ticker Tape Widget . It shows realtime market information for a user-specified list of symbols along the bottom of the main chart pane.

█ CONCEPTS

Ticker tape

Traditionally, a ticker tape was a continuous, narrow strip of paper that displayed stock prices, trade volumes, and other financial and security information. Invented by Edward A. Calahan in 1867, ticker tapes were the earliest method for electronically transmitting live stock market data.

A machine known as a "stock ticker" received stock information via telegraph, printing abbreviated company names, transaction prices, and other information in a linear sequence on the paper as new data came in. The term "ticker" in the name comes from the "tick" sound the machine made as it printed stock information. The printed tape provided a running record of trading activity, allowing market participants to stay informed on recent market conditions without needing to be on the exchange floor.

In modern times, electronic displays have replaced physical ticker tapes. However, the term "ticker" remains persistent in today's financial lexicon. Nowadays, ticker symbols and digital tickers appear on financial news networks, trading platforms, and brokerage/exchange websites, offering live updates on market information. Modern electronic displays, thankfully, do not rely on telegraph updates to operate.

█ FEATURES

Requesting a list of securities

The "Symbol list" text box in the indicator's "Settings/Inputs" tab allows users to list up to 40 symbols or ticker Identifiers. The indicator dynamically requests and displays information for each one. To add symbols to the list, enter their names separated by commas . For example: "BITSTAMP:BTCUSD, TSLA, MSFT".

Each item in the comma-separated list must represent a valid symbol or ticker ID. If the list includes an invalid symbol, the script will raise a runtime error.

To specify a broker/exchange for a symbol, include its name as a prefix with a colon in the "EXCHANGE:SYMBOL" format. If a symbol in the list does not specify an exchange prefix, the indicator selects the most commonly used exchange when requesting the data.

Realtime updates

This indicator requests symbol descriptions, current market prices, daily price changes, and daily change percentages for each ticker from the user-specified list of symbols or ticker identifiers. It receives updated information for each security after new realtime ticks on the current chart.

After a new realtime price update, the indicator updates the values shown in the tape display and their colors.

The color of the percentages in the tape depends on the change in price from the previous day . The text is green when the daily change is positive, red when the value is negative, and gray when the value is 0.

The color of each displayed price depends on the change in value from the last recorded update, not the change over a daily period. For example, if a security's price increases in the latest update, the ticker tape shows that price with green text, even if the current price is below the previous day's closing price. This behavior allows users to monitor realtime directional changes in the requested securities.

NOTE: Pine scripts execute on realtime bars when new ticks are available in the chart's data feed. If no new updates are available from the chart's realtime feed, it may cause a delay in the data the indicator receives.

Ticker motion

This indicator's tape display shows a list of security information that incrementally scrolls horizontally from right to left after new chart updates, providing a dynamic visual stream of current market data. The scrolling effect works by using a counter that increments across successive intervals after realtime ticks to control the offset of each listed security. Users can set the initial scroll offset with the "Offset" input in the "Settings/Inputs" tab.

The scrolling rate of the ticker tape display depends on the realtime ticks available from the chart's data feed. Using the indicator on a chart with frequent realtime updates results in smoother scrolling. If no new realtime ticks are available in the chart's feed, the ticker tape does not move. Users can also deactivate the scrolling feature by toggling the "Running" input in the indicator's settings.

█ FOR Pine Script™ CODERS

• This script utilizes dynamic requests to iteratively fetch information from multiple contexts using a single request.security() instance in the code. Previously, `request.*()` functions were not allowed within the local scopes of loops or conditional structures, and most `request.*()` function parameters, excluding `expression`, required arguments of a simple or weaker qualified type. The new `dynamic_requests` parameter in script declaration statements enables more flexibility in how scripts can use `request.*()` calls. When its value is `true`, all `request.*()` functions can accept series arguments for the parameters that define their requested contexts, and `request.*()` functions can execute within local scopes. See the Dynamic requests section of the Pine Script™ User Manual to learn more.

• Scripts can execute up to 40 unique `request.*()` function calls. A `request.*()` call is unique only if the script does not already call the same function with the same arguments. See this section of the User Manual's Limitations page for more information.

• This script converts a comma-separated "string" list of symbols or ticker IDs into an array . It then loops through this array, dynamically requesting data from each symbol's context and storing the results within a collection of custom `Tape` objects . Each `Tape` instance holds information about a symbol, which the script uses to populate the table that displays the ticker tape.

• This script uses the varip keyword to declare variables and `Tape` fields that update across ticks on unconfirmed bars without rolling back. This behavior allows the script to color the tape's text based on the latest price movements and change the locations of the table cells after realtime updates without reverting. See the `varip` section of the User Manual to learn more about using this keyword.

• Typically, when requesting higher-timeframe data with request.security() using barmerge.lookahead_on as the `lookahead` argument, the `expression` argument should use the history-referencing operator to offset the series, preventing lookahead bias on historical bars. However, the request.security() call in this script uses barmerge.lookahead_on without offsetting the `expression` because the script only displays results for the latest historical bar and all realtime bars, where there is no future information to leak into the past. Instead, using this call on those bars ensures each request fetches the most recent data available from each context.

• The request.security() instance in this script includes a `calc_bars_count` argument to specify that each request retrieves only a minimal number of bars from the end of each symbol's historical data feed. The script does not need to request all the historical data for each symbol because it only shows results on the last chart bar that do not depend on the entire time series. In this case, reducing the retrieved bars in each request helps minimize resource usage without impacting the calculated results.

Look first. Then leap.

Uptrick: TimeFrame Trends: Performance & Sentiment Indicator### **Uptrick: TimeFrame Trends: Performance & Sentiment Indicator (TFT) - In-Depth Explanation**

#### **Overview**

The **Uptrick: TimeFrame Trends: Performance & Sentiment Indicator (TFT)** is a sophisticated trading tool designed to provide traders with a comprehensive view of market trends across multiple timeframes, combined with a sentiment gauge through the Relative Strength Index (RSI). This indicator offers a unique blend of performance analysis, sentiment evaluation, and visual signal generation, making it an invaluable resource for traders who seek to understand both the macro and micro trends within a financial instrument.

#### **Purpose**

The primary purpose of the TFT indicator is to empower traders with the ability to assess the performance of an asset over various timeframes while simultaneously gauging market sentiment through the RSI. By analyzing price changes over periods ranging from one week to one year, and complementing this with sentiment signals, TFT enables traders to make informed decisions based on a well-rounded analysis of historical price performance and current market conditions.

#### **Key Components and Features**

1. **Multi-Timeframe Performance Analysis:**

- **Performance Lookback Periods:**

- The TFT indicator calculates the percentage price change over several predefined timeframes: 7 days (1 week), 14 days (2 weeks), 30 days (1 month), 180 days (6 months), and 365 days (1 year). These timeframes provide a layered view of how an asset has performed over short, medium, and long-term periods.

- **Percentage Change Calculation:**

- The indicator computes the percentage change for each timeframe by comparing the current closing price to the closing price at the start of each period. This gives traders insight into the strength and direction of the trend over different periods, helping them identify consistent trends or potential reversals.

2. **Sentiment Analysis Using RSI:**

- **Relative Strength Index (RSI):**

- RSI is a widely-used momentum oscillator that measures the speed and change of price movements. It oscillates between 0 and 100 and is typically used to identify overbought or oversold conditions. In TFT, the RSI is calculated using a 14-period lookback, which is standard for most RSI implementations.

- **RSI Smoothing with EMA:**

- To refine the RSI signal and reduce noise, TFT applies a 10-period Exponential Moving Average (EMA) to the RSI values. This smoothed RSI is then used to generate buy, sell, and neutral signals based on its position relative to the 50 level:

- **Buy Signal:** Triggered when the smoothed RSI crosses above 50, indicating bullish sentiment.

- **Sell Signal:** Triggered when the smoothed RSI crosses below 50, indicating bearish sentiment.

- **Neutral Signal:** Triggered when the smoothed RSI equals 50, suggesting indecision or a balanced market.

3. **Visual Signal Generation:**

- **Signal Plots:**

- TFT provides clear visual cues directly on the price chart by plotting shapes at the points where buy, sell, or neutral signals are generated. These shapes are color-coded (green for buy, red for sell, yellow for neutral) and are positioned below or above the price bars for easy identification.

- **First Occurrence Trigger:**

- To avoid clutter and focus on significant market shifts, TFT only triggers the first occurrence of each signal type. This feature helps traders concentrate on the most relevant signals without being overwhelmed by repeated alerts.

4. **Customizable Performance & Sentiment Table:**

- **Table Display:**

- The TFT indicator includes a customizable table that displays the calculated percentage changes for each timeframe. This table is positioned on the chart according to user preference (top-left, top-right, bottom-left, bottom-right) and provides a quick reference to the asset’s performance across multiple periods.

- **Dynamic Text Color:**

- To enhance readability and provide immediate visual feedback, the text color in the table changes based on the direction of the percentage change: green for positive (upward movement) and red for negative (downward movement). This color-coding helps traders quickly assess whether the asset is in an uptrend or downtrend for each period.

- **Customizable Font Size:**

- Traders can adjust the font size of the table to fit their chart layout and personal preferences, ensuring that the information is accessible without being intrusive.

5. **Flexibility and Customization:**

- **Lookback Period Customization:**

- While the default lookback periods are set for common trading intervals (7 days, 14 days, etc.), these can be adjusted to match different trading strategies or market conditions. This flexibility allows traders to tailor the indicator to focus on the timeframes most relevant to their analysis.

- **RSI and EMA Settings:**

- The length of the RSI calculation and the smoothing EMA can also be customized. This is particularly useful for traders who prefer shorter or longer periods for their momentum analysis, allowing them to fine-tune the sensitivity of the indicator.

- **Table Position and Appearance:**

- The table’s position on the chart, along with its font size and colors, is fully customizable. This ensures that the indicator can be integrated seamlessly into any chart setup without obstructing key price data.

#### **Use Cases and Applications**

1. **Trend Identification and Confirmation:**

- **Short-Term Traders:**

- Traders focused on short-term movements can use the 7-day and 14-day performance metrics to identify recent trends and momentum shifts. The RSI signals provide additional confirmation, helping traders enter or exit positions based on the latest market sentiment.

- **Swing Traders:**

- For those holding positions over days to weeks, the 30-day and 180-day performance data are particularly useful. These metrics highlight medium-term trends, and when combined with RSI signals, they provide a robust framework for swing trading strategies.

- **Long-Term Investors:**

- Long-term investors can benefit from the 1-year performance data to gauge the overall health and direction of an asset. The indicator’s ability to track performance across different periods helps in identifying long-term trends and potential reversal points.

2. **Sentiment Analysis and Market Timing:**

- **Market Sentiment Tracking:**

- By using RSI in conjunction with performance metrics, TFT provides a clear picture of market sentiment. Traders can use this information to time their entries and exits more effectively, aligning their trades with periods of strong bullish or bearish sentiment.

- **Avoiding False Signals:**

- The smoothing of RSI helps reduce noise and avoid false signals that are common in volatile markets. This makes the TFT indicator a reliable tool for identifying true market trends and avoiding whipsaws that can lead to losses.

3. **Comprehensive Market Analysis:**

- **Multi-Timeframe Analysis:**

- TFT’s ability to analyze multiple timeframes simultaneously makes it an excellent tool for comprehensive market analysis. Traders can compare short-term and long-term performance to understand the broader market context, making it easier to align their trading strategies with the overall trend.

- **Performance Benchmarking:**

- The percentage change metrics provide a clear benchmark for an asset’s performance over time. This information can be used to compare the asset against broader market indices or other assets, helping traders make more informed decisions about where to allocate their capital.

4. **Custom Strategy Development:**

- **Tailoring to Specific Markets:**

- TFT can be customized to suit different markets, whether it’s stocks, forex, commodities, or cryptocurrencies. For instance, traders in volatile markets may opt for shorter lookback periods and more sensitive RSI settings, while those in stable markets may prefer longer periods for a smoother analysis.

- **Integrating with Other Indicators:**

- TFT can be used alongside other technical indicators to create a more comprehensive trading strategy. For example, combining TFT with moving averages, Bollinger Bands, or MACD can provide additional layers of confirmation and reduce the likelihood of false signals.

#### **Best Practices for Using TFT**

- **Regularly Adjust Lookback Periods:**

- Depending on the market conditions and the asset being traded, it’s important to regularly review and adjust the lookback periods for the performance metrics. This ensures that the indicator remains relevant and responsive to current market trends.

- **Combine with Volume Analysis:**

- While TFT provides a solid foundation for trend and sentiment analysis, combining it with volume indicators can further enhance its effectiveness. Volume can confirm the strength of a trend or signal potential reversals when divergences occur.

- **Use RSI with Other Momentum Indicators:**

- Although RSI is a powerful tool on its own, using it alongside other momentum indicators like Stochastic Oscillator or MACD can provide additional confirmation and help refine entry and exit points.

- **Customize Table Settings for Clarity:**

- Ensure that the performance table is positioned and sized appropriately on the chart. It should be easily readable without obstructing important price data. Adjust the text size and colors as needed to maintain clarity.

- **Monitor Multiple Timeframes:**

- Utilize the multi-timeframe analysis feature of TFT to monitor trends across different periods. This helps in identifying the dominant trend and avoiding trades that go against the broader market direction.

#### **Conclusion**

The **Uptrick: TimeFrame Trends: Performance & Sentiment Indicator (TFT)** is a comprehensive and versatile tool that combines the power of multi-timeframe performance analysis with sentiment gauging through RSI. Its ability to customize and adapt to various trading strategies and markets makes it a valuable asset for traders at all levels. By offering a clear visual representation of trends and market sentiment, TFT empowers traders to make more informed and confident trading decisions, whether they are focusing on short-term price movements or long-term investment opportunities. With its deep integration of performance metrics and sentiment analysis, TFT stands out as a must-have indicator for any trader looking to gain a holistic understanding of market dynamics.

Uptrick: Volume-Weighted EMA Signal### **Uptrick: Volume-Weighted EMA Signal (UVES) Indicator - Comprehensive Description**

#### **Overview**

The **Uptrick: Volume-Weighted EMA Signal (UVES)** is an advanced, multifaceted trading indicator meticulously designed to provide traders with a holistic view of market trends by integrating Exponential Moving Averages (EMA) with volume analysis. This indicator not only identifies the direction of market trends through dynamic EMAs but also evaluates the underlying strength of these trends using real-time volume data. UVES is a versatile tool suitable for various trading styles and markets, offering a high degree of customization to meet the specific needs of individual traders.

#### **Purpose**

The UVES indicator aims to enhance traditional trend-following strategies by incorporating a critical yet often overlooked component: volume. Volume is a powerful indicator of market strength, providing insights into the conviction behind price movements. By merging EMA-based trend signals with detailed volume analysis, UVES offers a more nuanced and reliable approach to identifying trading opportunities. This dual-layer analysis allows traders to differentiate between strong trends supported by significant volume and weaker trends that may be prone to reversals.

#### **Key Features and Functions**

1. **Dynamic Exponential Moving Average (EMA):**

- The core of the UVES indicator is its dynamic EMA, calculated over a customizable period. The EMA is a widely used technical indicator that smooths price data to identify the underlying trend. In UVES, the EMA is dynamically colored—green when the current EMA value is above the previous value, indicating an uptrend, and red when below, signaling a downtrend. This visual cue helps traders quickly assess the trend direction without manually calculating or interpreting raw data.

2. **Comprehensive Moving Average Customization:**

- While the EMA is the default moving average in UVES, traders can select from various other moving average types, including Simple Moving Average (SMA), Smoothed Moving Average (SMMA), Weighted Moving Average (WMA), and Volume-Weighted Moving Average (VWMA). Each type offers unique characteristics:

- **SMA:** Provides a simple average of prices over a specified period, suitable for identifying long-term trends.

- **EMA:** Gives more weight to recent prices, making it more responsive to recent market movements.

- **SMMA (RMA):** A slower-moving average that reduces noise, ideal for capturing smoother trends.

- **WMA:** Weighs prices based on their order in the dataset, making recent prices more influential.

- **VWMA:** Integrates volume data, emphasizing price movements that occur with higher volume, making it particularly useful in volume-sensitive markets.

3. **Signal Line for Trend Confirmation:**

- UVES includes an optional signal line, which applies a secondary moving average to the primary EMA. This signal line can be used to smooth out the EMA and confirm trend changes. The signal line’s color changes based on its slope—green for an upward slope and red for a downward slope—providing a clear visual confirmation of trend direction. Traders can adjust the length and type of this signal line, allowing them to tailor the indicator’s responsiveness to their trading strategy.

4. **Buy and Sell Signal Generation:**

- UVES generates explicit buy and sell signals based on the interaction between the EMA and the signal line. A **buy signal** is triggered when the EMA transitions from a red (downtrend) to a green (uptrend), indicating a potential entry point. Conversely, a **sell signal** is triggered when the EMA shifts from green to red, suggesting an exit or shorting opportunity. These signals are displayed directly on the chart as upward or downward arrows, making them easily identifiable even during fast market conditions.

5. **Volume Analysis with Real-Time Buy/Sell Volume Table:**

- One of the standout features of UVES is its integration of volume analysis, which calculates and displays the volume attributed to buying and selling activities. This analysis includes:

- **Buy Volume:** The portion of the total volume associated with price increases (close higher than open).

- **Sell Volume:** The portion of the total volume associated with price decreases (close lower than open).

- **Buy/Sell Ratio:** A ratio of buy volume to sell volume, providing a quick snapshot of market sentiment.

- These metrics are presented in a real-time table positioned in the top-right corner of the chart, with customizable colors and formatting. The table updates with each new bar, offering continuous feedback on the strength and direction of the market trend based on volume data.

6. **Customizable Settings and User Control:**

- **EMA Length and Source:** Traders can specify the lookback period for the EMA, adjusting its sensitivity to price changes. The source for EMA calculations can also be customized, with options such as close, open, high, low, or other custom price series.

- **Signal Line Customization:** The signal line’s length, type, and width can be adjusted to suit different trading strategies, allowing traders to optimize the balance between trend detection and noise reduction.

- **Offset Adjustment:** The offset feature allows users to shift the EMA and signal line forward or backward on the chart. This can help align the indicator with specific price action or adjust for latency in decision-making processes.

- **Volume Table Positioning and Formatting:** The position, size, and color scheme of the volume table are fully customizable, enabling traders to integrate the table seamlessly into their chart setup without cluttering the visual workspace.

7. **Versatility Across Markets and Trading Styles:**

- UVES is designed to be effective across a wide range of financial markets, including Forex, stocks, cryptocurrencies, commodities, and indices. Its adaptability to different markets is supported by its comprehensive customization options and the inclusion of volume analysis, which is particularly valuable in markets where volume plays a crucial role in price movement.

#### **How Different Traders Can Benefit from UVES**

1. **Trend Followers:**

- Trend-following traders will find UVES particularly beneficial for identifying and riding trends. The dynamic EMA and signal line provide clear visual cues for trend direction, while the volume analysis helps confirm the strength of these trends. This combination allows trend followers to stay in profitable trades longer and exit when the trend shows signs of weakening.

2. **Volume-Based Traders:**

- Traders who focus on volume as a key indicator of market strength can leverage the UVES volume table to gain insights into the buying and selling pressure behind price movements. By monitoring the buy/sell ratio, these traders can identify periods of strong conviction (high buy volume) or potential reversals (high sell volume) with greater accuracy.

3. **Scalpers and Day Traders:**

- For traders operating on shorter time frames, UVES provides quick and reliable signals that are essential for making rapid trading decisions. The ability to customize the EMA length and type allows scalpers to fine-tune the indicator for responsiveness, while the volume analysis offers an additional layer of confirmation to avoid false signals.

4. **Swing Traders:**

- Swing traders, who typically hold positions for several days to weeks, can use UVES to identify medium-term trends and potential entry and exit points. The indicator’s ability to filter out market noise through the signal line and volume analysis makes it ideal for capturing significant price movements without being misled by short-term volatility.

5. **Position Traders and Long-Term Investors:**

- Even long-term investors can benefit from UVES by using it to identify major trend reversals or confirm the strength of long-term trends. The flexibility to adjust the EMA and signal line to longer periods ensures that the indicator remains relevant for detecting shifts in market sentiment over extended time frames.

#### **Optimal Settings for Different Markets**

- **Forex Markets:**

- **EMA Length:** 9 to 14 periods.

- **Signal Line:** Use VWMA or WMA for the signal line to incorporate volume data, which is crucial in the highly liquid Forex markets.

- **Best Use:** Short-term trend following, with an emphasis on identifying rapid changes in market sentiment.

- **Stock Markets:**

- **EMA Length:** 20 to 50 periods.

- **Signal Line:** SMA or EMA with a slightly longer length (e.g., 50 periods) to capture broader market trends.

- **Best Use:** Medium to long-term trend identification, with volume analysis confirming the strength of institutional buying or selling.

- **Cryptocurrency Markets:**

- **EMA Length:** 9 to 12 periods, due to the high volatility in crypto markets.

- **Signal Line:** SMMA or EMA for smoothing out extreme price fluctuations.

- **Best Use:** Identifying entry and exit points in volatile markets, with the volume table providing insights into market manipulation or sudden shifts in trader sentiment.

- **Commodity Markets:**

- **EMA Length:** 14 to 21 periods.

- **Signal Line:** WMA or VWMA, considering the impact of trading volume on commodity prices.

- **Best Use:** Capturing medium-term price movements and confirming trend strength with volume data.

#### **Customization for Advanced Users**

- **Advanced Offset Usage:** Traders can experiment with different offset values to see how shifting the EMA and signal line impacts the timing of buy/sell signals. This can be particularly useful in markets with known latency or for strategies that require a delayed confirmation of trend changes.

- **Volume Table Integration:** The position, size, and colors of the volume table can be adjusted to fit seamlessly into any trading setup. For example, a trader might choose to position the table in the bottom-right corner and use a smaller size to keep the focus on price action while still having access to volume data.

- **Signal Filtering:** By combining the signal line with the primary EMA, traders can filter out false signals during periods of low volatility or when the market is range-bound. Adjusting the length of the signal line allows for greater control over the sensitivity of the trend detection.

#### **Conclusion**

The **Uptrick: Volume-Weighted EMA Signal (UVES)** is a powerful and adaptable indicator designed for traders who demand more from their technical analysis tools. By integrating dynamic EMA trend signals with real-time volume analysis, UVES offers a comprehensive view of market conditions, making it an invaluable resource for identifying trends, confirming signals, and understanding market sentiment. Whether you are a day trader, swing trader, or long-term investor, UVES provides the versatility, precision, and customization needed to make more informed and profitable trading decisions. With its ability to adapt to various markets and trading styles, UVES is not just an indicator but a complete trend analysis solution.

Bearish vs Bullish ArgumentsThe Bearish vs Bullish Arguments Indicator is a tool designed to help traders visually assess and compare the number of bullish and bearish arguments based on their custom inputs. This script enables users to input up to five bullish and five bearish arguments, dynamically displaying the bias on a clean and customizable table on the chart. This provides traders with a clear, visual representation of the market sentiment they have identified.

Key Features:

Customizable Inputs: Users can input up to five bullish and five bearish arguments, which are displayed in a table on the chart.

Bias Calculation: The script calculates the bias (Bullish, Bearish, or Neutral) based on the number of bullish and bearish arguments provided.

Color Customization: Users can customize the colors for the table background, text, and headers, ensuring the table fits seamlessly into their charting environment.

Reset Functionality: A reset switch allows users to clear all input arguments with a single click, making it easy to start fresh.

How It Works:

Input Fields: The script provides input fields for up to five bullish and five bearish arguments. Each input is a simple text field where users can describe their arguments.

Bias Calculation: The script counts the number of non-empty bullish and bearish arguments and determines the overall bias. The bias is displayed in the table with a dynamically changing color to indicate whether the market sentiment is bullish, bearish, or neutral.

Customizable Table: The table is positioned on the chart according to the user's preference (top-left, top-right, bottom-left, bottom-right) and can be customized in terms of background color and text color.

How to Use:

Add the Indicator: Add the Bearish vs Bullish Arguments Indicator to your chart.

Input Arguments: Enter up to five bullish and five bearish arguments in the provided input fields in the script settings.

Customize Appearance: Adjust the table's background color, text color, and position on the chart to fit your preferences.

Example Use Case:

A trader might use this indicator to visually balance their arguments for and against a particular trade setup. By entering their reasons for a bullish outlook in the bullish argument fields and their reasons for a bearish outlook in the bearish argument fields, they can quickly see which side has more supporting points and make a more informed trading decision.

This script was inspired by Arjoio's concepts

Ohlson O-Score IndicatorThe Ohlson O-Score is a financial metric developed by Olof Ohlson to predict the probability of a company experiencing financial distress. It is widely used by investors and analysts as a key tool for financial analysis.

Inputs:

Period: Select the financial period for analysis, either "FY" (Fiscal Year) or "FQ" (Fiscal Quarter).

Country: Specify the country for Gross Net Product data. This helps in tailoring the analysis to specific economic conditions.

Gross Net Product : Define the number of years back for the index to be set at 100. This parameter provides a historical context for the analysis.

Table Display : Customize the display of various tables to suit your preference and analytical needs.

Key Features:

Predictive Power : The Ohlson O-Score is renowned for its predictive power in assessing the financial health of a company. It incorporates multiple financial ratios and indicators to provide a comprehensive view.

Financial Distress Prediction : Use the O-Score to gauge the likelihood of a company facing financial distress in the future. It's a valuable tool for risk assessment.

Country-Specific Analysis : Tailor the analysis to the economic conditions of a specific country, ensuring a more accurate evaluation of financial health.

Historical Context : Set the Gross Net Product index at a specific historical point, allowing for a deeper understanding of how a company's financial health has evolved over time.

How to Use:

Select Period : Choose either Fiscal Year or Fiscal Quarter based on your preference.

Specify Country : Input the country for country-specific Gross Net Product data.

Set Historical Context : Determine the number of years back for the index to be set at 100, providing historical context to your analysis.

Custom Table Display : Personalize the display of various tables to focus on the metrics that matter most to you.

Calculation and component description

Here is the description of O-score components as found in orginal Ohlson publication :

1. SIZE = log(total assets/GNP price-level index). The index assumes a base value of 100 for 1968. Total assets are as reported in dollars. The index year is as of the year prior to the year of the balance sheet date. The procedure assures a real-time implementation of the model. The log transform has an important implication. Suppose two firms, A and B, have a balance sheet date in the same year, then the sign of PA - Pe is independent of the price-level index. (This will not follow unless the log transform is applied.) The latter is, of course, a desirable property.

2. TLTA = Total liabilities divided by total assets.

3. WCTA = Working capital divided by total assets.

4. CLCA = Current liabilities divided by current assets.

5. OENEG = One if total liabilities exceeds total assets, zero otherwise.

6. NITA = Net income divided by total assets.

7. FUTL = Funds provided by operations divided by total liabilities

8. INTWO = One if net income was negative for the last two years, zero otherwise.

9. CHIN = (NI, - NI,-1)/(| NIL + (NI-|), where NI, is net income for the most recent period. The denominator acts as a level indicator. The variable is thus intended to measure change in net income. (The measure appears to be due to McKibben ).

Interpretation

The foundational model for the O-Score evolved from an extensive study encompassing over 2000 companies, a notable leap from its predecessor, the Altman Z-Score, which examined a mere 66 companies. In direct comparison, the O-Score demonstrates significantly heightened accuracy in predicting bankruptcy within a 2-year horizon.

While the original Z-Score boasted an estimated accuracy of over 70%, later iterations reached impressive levels of 90%. Remarkably, the O-Score surpasses even these high benchmarks in accuracy.

It's essential to acknowledge that no mathematical model achieves 100% accuracy. While the O-Score excels in forecasting bankruptcy or solvency, its precision can be influenced by factors both internal and external to the formula.

For the O-Score, any results exceeding 0.5 indicate a heightened likelihood of the firm defaulting within two years. The O-Score stands as a robust tool in financial analysis, offering nuanced insights into a company's financial stability with a remarkable degree of accuracy.

Price Cross Time Custom Range Interactive█ OVERVIEW

This indicator was a time-based indicator and intended as educational purpose only based on pine script v5 functions for ta.cross() , ta.crossover() and ta.crossunder() .

I realised that there is some overlap price with the cross functions, hence I integrate them into Custom Range Interactive with value variance and overlap displayed into table.

This was my submission for Pinefest #1 , I decided to share this as public, I may accidentally delete this as long as i keep as private.

█ INSPIRATION

Inspired by design, code and usage of CAGR. Basic usage of custom range / interactive, pretty much explained here . Credits to TradingView.

█ FEATURES

1. Custom Range Interactive

2. Label can be resize and change color.

3. Label show tooltip for price and time.

4. Label can be offset to improve readability.

5. Table can show price variance when any cross is true.

6. Table can show overlap if found crosss is overlap either with crossover and crossunder.

7. Table text color automatically change based on chart background (light / dark mode).

8. Source 2 is drawn as straight line, while Source 1 will draw as label either above line for crossover, below line for crossunder and marked 'X' if crossing with Source 2's line.

9. Cross 'X' label can be offset to improve readability.

10. Both Source 1 and Source 2 can select Open, Close, High and Low, which can be displayed into table.

█ LIMITATIONS

1. Table is limited to intraday timeframe only as time format is not accurate for daily timeframe and above. Example daily timeframe will give result less 1 day from actual date.

2. I did not include other sources such external source or any built in sources such as hl2, hlc3, ohlc4 and hlcc4.

█ CODE EXPLAINATION

I pretty much create custom function with method which returns tuple value.

method crossVariant(float price = na, chart.point ref = na) =>

cross = ta.cross( price, ref.price)

over = ta.crossover( price, ref.price)

under = ta.crossunder(price, ref.price)

Unfortunately, I unable make the labels into array which i plan to return string value by getting the text value from array label, hence i use label.all and add incremental int value as reference.

series label labelCross = na, labelCross.delete()

var int num = 0

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

I realised cross value can be overlap with crossover and crossunder, hence I add bool to enable force overlap and add additional bools.

series label labelCross = na, labelCross.delete()

var int num = 0

if forceOverlap

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

else

if cross and over

num += 1

labelCross := label.new()

if cross and under

num += 1

labelCross := label.new()

if cross and not over and not under

num += 1

labelCross := label.new()

█ USAGE / EXAMPLES

dashboard MTF,EMA User Guide: Dashboard MTF EMA

Script Installation:

Copy the script code.

Go to the script window (Pine Editor) on TradingView.

Paste the code into the script window.

Save the script.

Adding the Script to the Chart:

Return to your chart on TradingView.

Look for the script in the list of available scripts.

Add the script to the chart.

Interpreting the Table:

On the right side of the chart, you will see a table labeled "EMA" with arrows.

The rows correspond to different timeframes: 5 minutes (5M), 15 minutes (15M), 1 hour (1H), 4 hours (4H), and 1 day (1D).

Understanding the Arrows:

Each row of the table has two columns: "EMA" and an arrow.

"EMA" indicates the trend of the Exponential Moving Average (EMA) for the specified period.

The arrow indicates the direction of the trend: ▲ for bullish, ▼ for bearish.

Table Colors:

The colors of the table reflect the current trend based on the comparison between fast and slow EMAs.

Blue (▲) indicates a bullish trend.

Red (▼) indicates a bearish trend.

Table Theme:

The table has a dark (Dark) or light (Light) theme according to your preference.

The background, frame, and colors are adjusted based on the selected theme.

Usage:

Use the table as a quick indicator of trends on different timeframes.

The arrows help you quickly identify trends without navigating between different time units.

Designed to simplify analysis and avoid cluttering the chart with multiple indicators.

Major and Minor Trend Indicator by Nikhil34a V 2.2Title: Major and Minor Trend Indicator by Nikhil34a V 2.2

Description:

The Major and Minor Trend Indicator v2.2 is a comprehensive technical analysis script designed for use with the TradingView platform. This powerful tool is developed in Pine Script version 5 and helps traders identify potential buying and selling opportunities in the stock market.

Features:

SMA Trend Analysis: The script calculates two Simple Moving Averages (SMAs) with user-defined lengths for major and minor trends. It displays these SMAs on the chart, allowing traders to visualize the prevailing trends easily.

Surge Detection: The indicator can detect buying and selling surges based on specific conditions, such as volume, RSI, MACD, and stochastic indicators. Both Buying and Selling surges are marked in black on the chart.

Option Buy Zone Detection: The script identifies the option buy zone based on SMA crossovers, RSI, and MACD values. The buy zone is categorized as "CE Zone" or "PE Zone" and displayed in the table along with the trigger time.

Two-Day High and Low Range: The script calculates the highest high and lowest low of the previous two trading days and plots them on the chart. The area between these points is shaded in semi-transparent green and red colors.

Crossover Analysis: The script analyzes moving average crossovers on multiple timeframes (2-minute, 3-minute, and 5-minute) and displays buy and sell signals accordingly.

Trend Identification: The script identifies the major and minor trends as either bullish or bearish, providing valuable insights into the overall market sentiment.

Usage:

Customize Major and Minor SMA Periods: Adjust the lengths of major and minor SMAs through input parameters to suit your trading preferences.

Enable/Disable Moving Averages: Choose which SMAs to display on the chart by toggling the "showXMA" input options.

Set Surge and Option Buy Zone Thresholds: Modify the surgeThreshold, volumeThreshold, RSIThreshold, and StochThreshold inputs to refine the surge and buy zone detection.

Analyze Crossover Signals: Monitor the crossover signals in the table, categorized by timeframes (2-minute, 3-minute, and 5-minute).

Explore Market Bias and Distance to 2-Day High/Low: The table provides information on market bias, current price movement relative to the previous two-day high and low, and the option buy zone status.

Additional Use Cases:

Surge Indicator:

The script includes a Surge Indicator that detects sudden buying or selling surges in the market. When a buying surge is identified, the "BSurge" label will appear below the corresponding candle with black text on a white background. Similarly, a selling surge will display the "SSurge" label in white text on a black background. These indicators help traders quickly spot strong buying or selling activities that may influence their trading decisions. These surges can be used to identify sudden premium dump zones.

Option Buy Zone:

The Option Buy Zone is an essential feature that identifies potential zones for buying call options (CE Zone) or put options (PE Zone) based on specific technical conditions. The indicator evaluates SMA crossovers, RSI, and MACD values to determine the current market sentiment. When the option buy zone is triggered, the script will display the respective zone ("CE Zone" or "PE Zone") in the table, highlighted with a white background. Additionally, the time when the buy zone was triggered will be shown under the "Option Buy Zone Trigger Time" column.

Price Movement Relative to 2-Day High/Low:

The script calculates the highest high and lowest low of the previous two trading days (high2DaysAgo and low2DaysAgo) and plots these points on the chart. The area between these two points is shaded in semi-transparent green and red colors. The green region indicates the price range between the highpricetoconsider (highest high of the previous two days) and the lower value between highPreviousDay and high2DaysAgo. Similarly, the red region represents the price range between the lowpricetoconsider (lowest low of the previous two days) and the higher value between lowPreviousDay and low2DaysAgo.

Entry Time and Current Zone:

The script identifies potential entry times for trades within the option buy zone. When a valid buy zone trigger occurs, the script calculates the entryTime by adding the durationInMinutes (user-defined) to the startTime. The entryTime will be displayed in the "Entry Time" column of the table. Depending on the comparison between optionbuyzonetriggertime and entryTime, the background color of the entry time will change. If optionbuyzonetriggertime is greater than entryTime, the background color will be yellow, indicating that a new trigger has occurred before the specified duration. Otherwise, the background color will be green, suggesting that the entry time is still within the defined duration.

Current Zone Indicator: