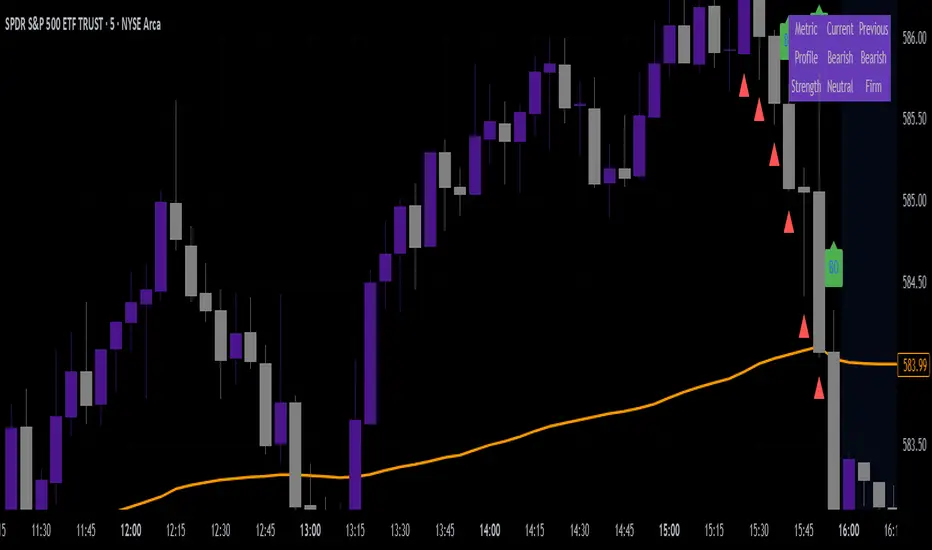

VWAP & Breakout Volume ConfirmHow the TradingView Indicator Works (Explained Simply)

VWAP Line (Orange)

It plots the Volume Weighted Average Price for the day.

Price above VWAP = bullish zone

Price below VWAP = bearish zone

Volume Spike Detection (Red Triangle)

It calculates the average volume over the last 20 candles.

If the current volume is 1.5× that average, it plots a red triangle under the candle.

Helps confirm if a move has real momentum or not.

Breakout Confirmation (Green Label ‘BO’)

Checks if price breaks above the last 10-bar high (for upside breakout) or below the last 10-bar low (for downside breakout).

If a breakout happens and the volume spike is present, it plots a green “BO” label above the candle.

This tells you the breakout is strong and likely to follow through.

ابحث في النصوص البرمجية عن "VWAP"

VWAP ROC Weighted AverageThe VWAP ROC Weighted Average indicator combines the concepts of Volume Weighted Average Price (VWAP) and Rate of Change (ROC) to create a unique and versatile tool for traders. The indicator calculates the average VWAP and average ROC over a specified period (default: 200 bars) and then creates a weighted average of these two values. This provides a single line that can help traders identify potential entry and exit points in a market.

How it can be used in trading:

Trend Confirmation: The VWAP_ROC_WA can be used to confirm the prevailing trend of an asset. If the weighted average line is moving upward, it indicates a bullish trend, while a downward-moving line suggests a bearish trend. Traders can use this information to enter trades in the direction of the trend to improve their odds of success.

Support and Resistance: The VWAP_ROC_WA line can act as dynamic support and resistance levels. When the price is above the weighted average line, it can act as a support level, and when the price is below the line, it can serve as a resistance level. Traders can use these levels to set stop-loss and take-profit orders or to identify potential entry and exit points.

Divergences: Traders can look for divergences between the price and the VWAP_ROC_WA line to identify potential reversals. For instance, if the price is making higher highs while the weighted average line is making lower highs, it may signal a bearish divergence, indicating a potential reversal to the downside. Conversely, if the price is making lower lows while the weighted average line is making higher lows, it may signal a bullish divergence, indicating a potential reversal to the upside.

Crossovers: Traders can monitor crossovers between the price and the VWAP_ROC_WA line. A bullish crossover occurs when the price crosses above the weighted average line, suggesting a potential long entry point. A bearish crossover occurs when the price crosses below the line, suggesting a potential short entry point.

Koalafied RVWAPThis indicator shows both the Rolling VWAP and Standard Deviations as set by the user. The Rolling VWAP calculation is similar to the standard VWAP although it calculates the volume weighted average price over the specified period of time (lookback), resetting for each subsequent bar.

The unique aspect of this indicator is that instead of calculating the RVWAP over the current timeframes lookback period, the option is available to select a High-Time-Frame setting instead.

This has two different methods of calculation

1 - Based on HTF security requests (both repainting and non-repainting)

2 - Automatic calculation of number of current timeframe bars that make up the HTF lookback period (smoother and non-repainting plot)

Additionally a smooth function is included for the HTF input setting.

VWAP-RSI Using the script that i put here before

we can play with the Z function and make this nice indicator

which is hybrid of VWAP and RSI

it look cool

red is bearish

green is bullish

low points are bellow 20

high points above 80

you can change the length of different vwap or RSI for your purpose

the color changes are based on vwap

VWAP BANDSThis nice script combine VWAP band and trend/forecast system based on it

/ode for band take from linear regression script from pine script manual and adopted to VWAP

Trend lines based on VWAP and forecast using Alex grover method with his approval for script

Together it a great too for detection of trend and high and low

for forecast use the trend option

I set length to 100. in daily chart I use 20 . in lower TF I prefer longer 50 or above as it better fit this system

VWAP Stdev Bands v2 Mod UPDATE

Vwap + standard deviation bands. Good for reversal trading among other things. Used intraday.

Very useful when price is ranging.

I added:

- Option to fill the spaces between the deviation lines with color.

- Option to add some extra bands. Color/length/style etc is customizable.

Made a quick update to prev version:

- Added bar/candle coloring

- You can change the colors to whatever you want.

- Or turn them off completely.

Ex:

If the candle is above vwap and below standard deviation 1 its white

If the candle is below vwap and above standard deviation 1 its black

If the candle is below std 2and above std3 its green

And so on...

original script by /u/SandroTurriate/ - I just made the changes above.

VWAP Adapt ProDescription

VWAPADAPT provides institutional-grade VWAP (Volume Weighted Average Price) analysis with multiple standard deviation bands, session reset options, and slope analysis. VWAP represents the average price weighted by volume - where institutional traders have executed throughout the day.

VWAP Extreme Zones (Elite Style)Short Description

VWAP Extreme Zones (Elite Style) highlights statistically stretched price areas above and below VWAP, helping traders identify potential overextension, mean-reversion zones, and high-risk breakout areas during intraday sessions.

Disclaimer

This indicator is provided for educational and analytical purposes only.

It does not constitute financial advice or trade signals.

All trading involves risk. Always confirm with price action, market context, and proper risk management before taking any trade.

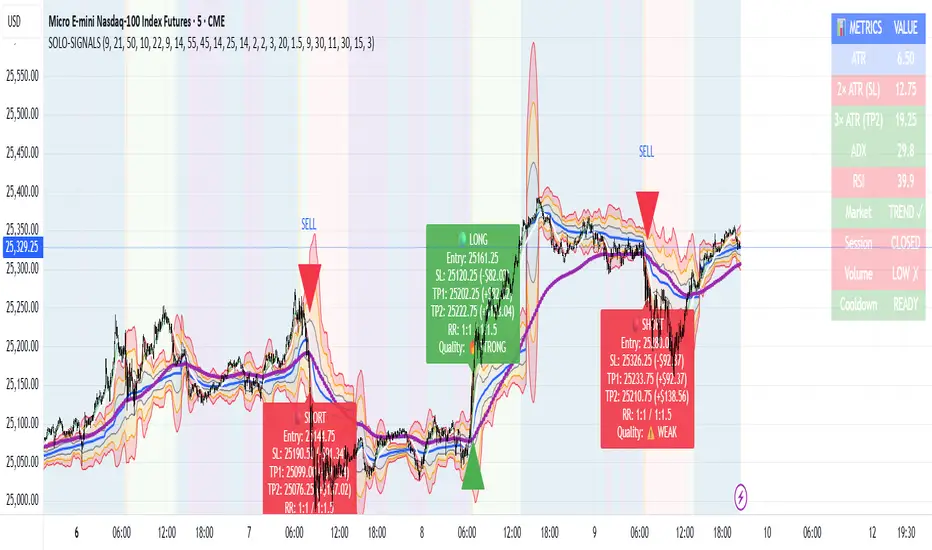

MNQ Morning Indicator | Clean SignalsMNQ Morning Trading Indicator Summary

What It Does

This is a TradingView indicator designed for day trading MNQ (Micro Nasdaq-100 futures) during morning sessions. It generates BUY and SELL signals only when multiple technical conditions align, helping traders identify high-probability trade setups.

Core Strategy

BUY Signal Requirements (All must be true):

✅ Price above VWAP (volume-weighted average price)

✅ Fast EMA (9) above Slow EMA (21) - uptrend confirmation

✅ Price above 15-minute 50 EMA - higher timeframe confirmation

✅ MACD histogram positive - momentum confirmation

✅ RSI above 55 - strength confirmation

✅ ADX above 25 - trending market (not choppy)

✅ Volume 1.5x above average - strong participation

SELL Signal (opposite conditions)

Key Features

🎯 Risk Management

Stop Loss: 2× ATR (Average True Range)

Take Profit 1: 2× ATR (1:2 risk-reward)

Take Profit 2: 3× ATR (1:3 risk-reward)

Dollar values: Calculates P&L based on MNQ's $2/point value

⏰ Session Filter

Default: 9:30 AM - 11:30 AM ET (customizable)

Safety feature: Avoids first 15 minutes (high volatility period)

Won't generate signals outside trading hours

🛡️ Signal Quality

Rates each signal: 🔥 STRONG, ⚡ MEDIUM, or ⚠️ WEAK

Requires minimum 15 bars between signals (prevents overtrading)

📊 Visual Dashboard

Shows real-time metrics:

ATR values

ADX (trend strength)

RSI (momentum)

Market condition (TREND/CHOP)

Session status

Volume status

Signal cooldown timer

Visual Elements

📈 VWAP with standard deviation bands (1σ, 2σ, 3σ)

📉 Multiple EMAs with trend-based coloring

🟢/🔴 Buy/Sell arrows on chart

📋 Detailed trade labels showing entry, SL, TPs, and risk-reward ratios

🎨 Background highlighting for market conditions

Safety Features

Cooldown period between signals

Session restrictions (no trading outside set hours)

First 15-minute avoidance (post-open volatility)

Multi-confirmation requirement (all 7 conditions must align)

Trend filter (ADX minimum to avoid choppy markets)

Best For

Day traders focused on morning sessions

MNQ futures traders

Traders who prefer systematic, rule-based entries

Those wanting pre-calculated risk management levels

Customization

All parameters are adjustable:

EMA periods

MACD settings

RSI thresholds

ADX minimum

ATR multipliers

Session times

Visual preferences

This indicator is designed to be conservative — it waits for strong confirmation before signaling, which means fewer but potentially higher-quality trades.

vwap inside bar jmrjm vwap inside bar which helps to take guage trend with vwap and and help to understand when market taking pause due to bulls and bears fight. Then we can take a trade in trend with winners.

VWAP MTF Scalping ModuleThe VWAP MTF indicator allows you to visualize anchored VWAP across multiple timeframes, while maintaining a clean and responsive display.

Designed for intraday traders, scalpers, and swing traders, this module offers a clear view of volume-weighted average price zones across key timeframes (1m, 5m, 15m, 1h... customizable).

Clean Multi-Indicator Alignment System

Overview

A sophisticated multi-indicator alignment system designed for 24/7 trading across all markets, with pure signal-based exits and no time restrictions. Perfect for futures, forex, and crypto markets that operate around the clock.

Key Features

🎯 Multi-Indicator Confluence System

EMA Cross Strategy: Fast EMA (5) and Slow EMA (10) for precise trend direction

VWAP Integration: Institution-level price positioning analysis

RSI Momentum: 7-period RSI for momentum confirmation and reversal detection

MACD Signals: Optimized 8/17/5 configuration for scalping responsiveness

Volume Confirmation: Customizable volume multiplier (default 1.6x) for signal validation

🚀 Advanced Entry Logic

Initial Full Alignment: Requires all 5 indicators + volume confirmation

Smart Continuation Entries: EMA9 pullback entries when trend momentum remains intact

Flexible Time Controls: Optional session filtering or 24/7 operation

🎪 Pure Signal-Based Exits

No Forced Closes: Positions exit only on technical signal reversals

Dual Exit Conditions: EMA9 breakdown + RSI flip OR MACD cross + EMA20 breakdown

Trend Following: Allows profitable trends to run their full course

Perfect for Swing Scalping: Ideal for multi-session position holding

📊 Visual Interface

Real-Time Status Dashboard: Live alignment monitoring for all indicators

Color-Coded Candles: Instant visual confirmation of entry/exit signals

Clean Chart Display: Toggle-able EMAs and VWAP with professional styling

Signal Differentiation: Clear labels for entries, X-crosses for exits

🔔 Alert System

Entry Notifications: Separate alerts for buy/sell signals

Exit Warnings: Technical breakdown alerts for position management

Mobile Ready: Push notifications to TradingView mobile app

Market Applications

Perfect For:

Gold Futures (GC): 24-hour precious metals trading

NASDAQ Futures (NQ): High-volatility index scalping

Forex Markets: Currency pairs with continuous operation

Crypto Trading: 24/7 cryptocurrency momentum plays

Energy Futures: Oil, gas, and commodity swing trades

Optimal Timeframes:

1-5 Minutes: Ultra-fast scalping during high volatility

5-15 Minutes: Balanced approach for most markets

15-30 Minutes: Swing scalping for trend following

🧠 Smart Position Management

Tracks implied position direction

Prevents conflicting signals

Allows trend continuation entries

State-aware exit logic

⚡ Scalping Optimized

Fast-reacting indicators with shorter periods

Volume-based confirmation reduces false signals

Clean entry/exit visualization

Minimal lag for time-sensitive trades

Configuration Options

All parameters fully customizable:

EMA Lengths: Adjustable from 1-30 periods

RSI Period: 1-14 range for different market conditions

MACD Settings: Fast (1-15), Slow (1-30), Signal (1-10)

Volume Confirmation: 0.5-5.0x multiplier range

Visual Preferences: Colors, displays, and table options

Risk Management Features

Clear visual exit signals prevent emotion-based decisions

Volume confirmation reduces false breakouts

Multi-indicator confluence improves signal quality

Optional time filtering for session-specific strategies

Best Use Cases

Futures Scalping: NQ, ES, GC during active sessions

Forex Swing Trading: Major pairs during overlap periods

Crypto Momentum: Bitcoin, Ethereum trend following

24/7 Automated Systems: Algorithmic trading implementation

Multi-Market Scanning: Portfolio-wide signal monitoring

Fibo_Ma with Toggleable 200 EMA Filter Fibo_MA with Toggleable 200 EMA Filter

Description:

This multi-functional indicator blends Fibonacci-based moving averages with customizable filters and visual enhancements to support various trading strategies. It offers traders the flexibility to analyze trend dynamics and potential reversal zones using multiple tools in one script.

Key Features:

🔹 Fibonacci MA Framework

Leverage a range of Fibonacci numbers (from 1 to 233) to visualize trend-based EMA lines with optional smoothing. Users can choose the moving average method (SMA, EMA, RMA, WMA, VWMA, etc.) and adjust the smoothing length for fine-tuned analysis.

🔹 VWAP and Dynamic EMA Tools

Includes VWAP and a color-coded 200 EMA that updates based on trend slope. These help visualize key dynamic support and resistance levels.

🔹 Multi-Timeframe Support

Option to switch the data source to a higher timeframe for broader trend confirmation.

🔹 Signal Highlights

Bullish and bearish signal markers based on crossovers with optional filters.

Background highlights show whether the current price is above or below a smoothed EMA line.

🔹 Customizable Filters

Enable or disable filters like:

200 EMA Position Filter (only signal when price is above or below the 200 EMA)

ATR Filter (filter out low-volatility candles)

Volume Filter (signal only on sufficient volume)

🔹 Cross Alerts & Labels

Built-in alert conditions for crossovers and customizable signal display options—labels, shapes, and background highlights.

🔹 Advanced Options

Toggle forecast line visibility and offset

Fine-tune alerts using price action relative to the smooth trend line

Optional tail and cross label display for deeper chart customization

How to Use:

This tool can support trend-following, breakout, and pullback strategies. Customize the MA types, filters, and timeframe settings to match your trading style. The script is designed for visual clarity while offering rich configurability for discretionary and system-based traders.

Multi Range Pivots

Multi Range Pivots works by recognizing the high and low of the timeframe selected and plotting range high to MEAN averages and range low to MEAN averages.

This is essentially the VWAP pivots updated to include not only VWAP as a MEAN, but also SMA, EMA, VWMA, DEMA, TEMA, TRIMA, KAMA, MAMA, T3, H/L basis and Donchian basis.

Also, with high and low no longer repainting, I was able to add true reliable signals.

Enjoy

VWAP Bands Team AustraliaThis indicator add 6 configurable vwap bands for each side of the vwap price.

VWAP ATRATR Trailing stoploss with VWAP for confirmation and entry/exit points

VWAP resets on ATR cross

VWAP Enhanced (Visual Feedback)This is the standard Volume-Weighted Average Price (VWAP) indicator, with the addition of an adjustable anchored time point. This modification aligns with the objective of analyzing price action relative to a specific subsequent event.

NY VWAP 2std to 3std Probabilities + Exit ZonesHow it works:

Time buckets

Early: 10:30 – 12:00

Mid: 12:00 – 14:00

Late: 14:00 – 16:00

Bands

2σ band (s2up / s2dn) → this is where the “potential breakout” starts.

3σ band (s3up / s3dn) → this is the “target” for the 2→3σ move.

Counting logic

If during a given bucket, the price touches the 2σ band, it counts as a 2σ hit.

If after that, in the same bucket, the price also touches the 3σ band, it counts as a 3σ hit.

Probability calculation

\text{Probability 2→3σ} = \frac{\text{# of 3σ hits}}{\text{# of 2σ hits}} \times 100

For example, if in the late session the lower 2σ band is hit 10 times, and of those 10 times, 6 eventually hit the lower 3σ band, the script will show 60%.

Labels / lines

On the chart, Upper/Lower 2→3σ probabilities are displayed per bucket.

So yes: “Late Lower 2σ → 3σ: 60%” means: if price touches the lower 2σ band in the late session, historically, 60% of those touches continued to the 3σ band.

⚠ Important caveats:

These are historical probabilities, not predictions.

Small sample sizes in a bucket can make percentages unstable early in the day.

The script only counts session NY bars (0930–1600) and ignores pre-10:30 hits to reduce opening volatility noise.

VWAP Histogram with EMAsBased on VWAP and Moving Averages.

Bias turns +ve if dynamic colour of the moving averages turns green. All moving avaerages are customisable.

VWAP + EMA9 With SignalsThis script is for scalping on the 5 minute timeframe. It contains signals that indicate intersection of VWAP by the EMA9. It contains Buy signals when a candle closes above both lines indicating a quick continuation of a long position (quick scalp) as well as Sell signals when a candle closes below both lines indicating a quick continuation of a short position (quick scalp). Please note that i do not recommend entries at Buy and Sell signals during Accumulation/Consolidation. Positions should be taken with volume.

VWAP & EMA9 Cross AlertAlerts the user when VWAP and EMA 9 cross. It gives a general direction of the market to help make decisions.

VWAP & EMA9 Cross AlertAlerts when EMA9 and VWAP Cross. This provides an indicator of general market direction based on these 2 indicators.