Miyagi (10 in 1) + AlertsMiyagi: The attempt at mastering something for the best results.

Miyagi indicators combine multiple trigger conditions and place them in one toolbox for traders to easily use, produce alerts, backtest, reduce risk and increase profitability.

VWAP has been the main condition for entry for our trading community for quite some time now, however using VWAP alone can lead to poor entries and bags.

Miyagi adds filtering conditions which can then be used to improve entries as opposed to simply using VWAP alone.

Miyagi (10-in-1) + Alerts combines multiple trigger conditions in an easy to use format.

Each trigger or filtering condition is selectable and able to be combined using the selector checkboxes.

Trigger or filter conditions can be used on a different timeframe chart than the current user selected chart.

For instance, the user's chart can be set to a 15M for entry however using filtering from a 30 minute RSI.

It is recommended to not use a lower timeframe chart setting than the current chart timeframe.

The following trigger and filter conditions are present in the 10-in-1:

EMA: Takes two "Exponential Moving Averages" into effect for filtering with user selectable chart timeframe, length and sources.

EMA Trend Type is user selectable for Trend-following or Counter-trend which allows you to counter-trade the markets.

Beside the "Simple Moving Average" the EMA has a multiplier.

Calculation is SMAxMultipier / SMAxMultiplier of the previous candle.

MACD: Takes the "Moving Average Convergence Divergence" into effect for trigger condition or filtering with user selectable chart timeframe,

source, fast & slow length and signal smoothing. MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a price.

The MACD is calculated by subtracting the EMA 26 period from the EMA 12. Long alert is triggered on crossing the MACD zero line upwards and short alert vise versa.

RSI: Takes the "Relative Stregth Index" into effect for trigger condition or filtering with user selectable chart timeframe, length, source, and oversold and overbought values.

The RSI is a technical oscillator that uses price and volume data for identifying overbought or oversold signals in an asset.

It can also be used to spot divergences which warn of a trend change in price. This oscillator moves between 0 and 100.

RSI > 80 is considered overbought and an RSI < 20 is considered oversold.

Stochastic RSI: oscillator version of RSI.

Takes the stochRSI into effect for trigger condition or filtering with user selectable chart timeframe, K D, length, upper and lower length.

stochRSI = (actual RSI - lowest RSI) / (highest RSI - lowest RSI)

VWAP: Takes the "Volume Weighted Average Price" into effect for trigger condition with user selectable chart timeframe, period, and VWAP lower line (long),

or VWAP Upper line (Short) values. VWAP is calculated by totaling the money traded for every transaction (price x volume) and then dividing by the total shares traded.

The VWAP appears as a single line on charts. It looks similar to a moving average line, but smoother. In general it is a intraday/week anchored indicator that resets,

but we are using a steady version over a selectable period of candles.

TTM: Takes the TTM squeeze indicator into effect for trigger condition with user selectable chart timeframe, length, multiplier, smoothing and trend direction.

The TTM is used to identify when to enter or exit a market for the best chance of profitability. It squeezes pairs well with other indicators, such as the ADX indicator.

For Multiplicator you can use Keltner and Boilinger Bands.

ADX: Takes the "Average Directional Movement Index" into effect for trigger condition with user selectable chart timeframe, smoothing, DI-length, a long and a short setting.

The ADX is used to detect trend direction with a positive and a negative direction indicator (+DI & -DI). The factor of those is a value between 0 and 100.

A low value can be a week trend or consolidation. A value > 25 is considered as a positive trend, >50 is a strong long trend >75 extremely strong trend.

Beside timeframe, you can choose smoothing and DI length.

SuperTrend: Takes the SuperTrend into effect for filtering with user selectable chart timeframe, ATR length and factor.

As an alternative to moving averages you can keep a fix distance to determine long or short trend.

That way you can avoid a lot of switching during a consolidation phase. Once crossed it switches trend direction.

The "Average True Rage" is used for calculation of the SuperTrend distance, it measures the volatility of the coin.

MFI: Takes the "Money Flow Index" into effect for filtering with user selectable chart timeframe, length, source, long and short settings.

The MFI is a technical oscillator that uses price and volume data for identifying overbought or oversold signals in an asset.

It can also be used to spot divergences which warn of a trend change in price. Like RSI this oscillator moves between 0 and 100.

MFI > 80 is considered overbought and an MFI < 20 is considered oversold.

W-Divergence: Takes the "Wolfpack Divergence" into effect for trigger condition with user selectable chart timeframe, length, lookback, divergence and ranges.

W-Divergence is MACD 3-8 setting with added divergence hunter.

How to use: Select the VWAP, and set the VWAP up as you would normally trade with your selected timeframe, period, and VWAP settings (long and short).

All entries will be shown, based on the VWAP settings.

From here, filtering can be implemented to produce better entries, ie using EMA/MACD/RSI/SuperTrend/MFI filtering.

Happy Trading!

ابحث في النصوص البرمجية عن "VWAP"

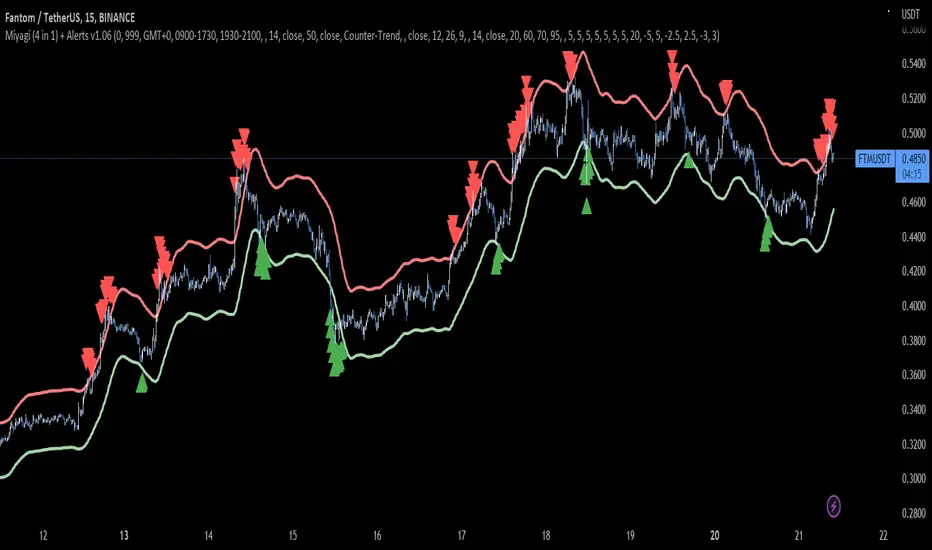

Miyagi (4 in 1) + AlertsMiyagi: The attempt at mastering something for the best results.

Miyagi indicators combine multiple trigger conditions and place them in one toolbox for traders to easily use, produce alerts, backtest, reduce risk and increase profitability.

VWAP has been the main condition for entry for our trading community for quite some time now; however using VWAP alone can lead to poor entries and bags.

Miyagi adds filtering conditions which can then be used to improve entries as opposed to simply using VWAP alone.

Miyagi (4-in-1) + Alerts combines multiple trigger conditions in an easy to use format.

Each trigger or filtering condition is selectable and able to be combined using the selector checkboxes.

Trigger or filter conditions can be used on a different timeframe chart than the current user selected chart.

For instance, the user's chart can be set to a 15M for entry however using filtering from a 30 minute RSI.

It is recommended to not use a lower timeframe chart setting than the current chart timeframe.

The following trigger and filter conditions are present in the 4-in-1:

EMA: Takes two EMAS into effect for trigger condition or filtering with user selectable chart timeframe, length and sources. EMA Trend Type is user selectable for Trend-following or Counter-trend which allows you to counter-trade the markets.

MACD: Takes the MACD into effect for trigger condition or filtering with user selectable chart timeframe, source, fast & slow length and signal smoothing.

RSI: Takes the RSI into effect for trigger condition or filtering with user selectable chart timeframe, length, source, and oversold and overbought values.

VWAP: Takes the VWAP into effect for trigger condition with user selectable chart timeframe, period, and VWAP lower line (long), or VWAP Upper line (Short) values.

How to use: Select the VWAP, and set the VWAP up as you would normally trade with your selected timeframe, period, and VWAP settings (long and short).

All entries will be shown, based on the VWAP settings.

From here, filtering can be implemented to produce better entries, ie using EMA/MACD/RSI filtering.

Happy Trading!

EVWAPThis indicator plots two Volume-Weighted Average Price (VWAP) lines anchored to earnings events:

EVWAP (Earnings Day): Resets VWAP on the day of the earnings release.

EVWAP (Post-Earnings Day): Resets VWAP on the first trading day after earnings.

These earnings-based VWAPs help identify average price zones impacted by earnings, providing insight into post-earnings support/resistance and potential trend shifts. Works on all timeframes.

Useful for traders analyzing price reactions around earnings reports.

TheVWAP - EventVWAPRequiring no date input from the user, EventVWAP automatically launches custom-dated VWAPs from relevant events — earnings and user-defined gaps — to detect longer-term thematic support and resistance. Works on both intraday and daily charts and includes user-specified thresholds for detection of launch events, such as the minimum gap % required to qualify.

Inputs include the number of VWAPs (up to four), the line style, custom color selection and which event type to use.

Use the link below to obtain access to this indicator.

MultiWAPThe VWAP tracks the average price, giving weight to each candle based upon its' relative volume.

In other words, high-volume candles move the VWAP faster than low-volume candles.

On a good day, market maker:

-Buys the dip

-Pumps past resistance, causing bullish FOMO

-Sells into the bullish FOMO, causing bearish FOMO

-Buys the dip (rinse and repeat)

By default, MultiWAP begins at the first visible bar.

Range low/high - tracks the most recent high/low

Upper VWAP - tracks retail's average buy price (MM is selling)

Lower VWAP - tracks MM's average buy price (MM is buying)

If price closes below the lower VWAP or the range low, the lower VWAP and range low are reset.

If price closes above the upper VWAP or the range high, the upper VWAP and range high are reset.

Resets are indicated by the dots. Resetting either VWAP moves it close to last price, making it easy to breach again.

A down-trend that lasts many bars will produce a string of green dots. When the accumulation phase ends, price pulls away from the lower VWAP, so it stops resetting. The ABSENCE of green dots tells you that we're in the markup phase/up-trend.

An up-trend that lasts many bars will produce a string of red dots. When the distribution phase ends, price pulls away from the upper VWAP, so it stops resetting. The ABSENCE of red dots tells you that we're in the markdown phase/down-trend.

By default, the net result is two VWAP's that automatically anchor themselves to the most recent, significant, and visible, high and low.

Usage:

For any timeframe, I recommend starting zoomed way out. Find the last green dot and drop an "Anchored VWAP" there. Now, zoom in until that candle is no longer visible. Find the last green dot and drop an anchored VWAP there. Continue doing so until you notice the lower VWAP getting reset to basically the same place.

This works the same, in reverse, during down-trends.

Dark Pool Estimate Signal TrackerDark Pool Estimate Signal — Detect Potential Institutional Activity

Overview

The Dark Pool Signal v1.6 indicator is designed to detect unusual trading activity near VWAP zones, which can be associated with institutional dark pool transactions. By combining volume spikes, VWAP proximity, and optional trend filters, it provides clear visual cues of potential hidden accumulation or distribution zones.

Disclaimer: This script is for informational and educational purposes only. It does not constitute financial advice. All trading involves risk. Past performance is not indicative of future results.

🔍 Core Logic

This indicator identifies potential off-exchange activity by analyzing three key factors:

Unusual Volume Spikes: Highlights bars where the current volume significantly exceeds its moving average by a user-defined multiplier.

VWAP Proximity: Triggers when the price stays within a volatility-adjusted range (ATR-based) of the VWAP, a common characteristic of algorithmic execution.

Trend Confirmation: An optional EMA filter helps align signals with the broader market direction.

Accumulation Detection: Counts repeated signals within a lookback period to identify persistent institutional buying or selling pressure.

The result is a set of visual and alert signals indicating possible institutional footprints.

🧩 Features

Dynamic VWAP Range (ATR-based): Automatically adjusts VWAP proximity sensitivity based on current market volatility.

Multi-tiered Signal Strength: Differentiates between Normal, Strong, and Accumulated signals to visualize the intensity of activity.

Non-Repainting Confirmation: Signals are confirmed only on bar close to ensure they do not repaint.

Language Support: Dual-language display (English / Korean).

Customizable Visualization: Easily adjust label size, color transparency, offset, and the duration of highlighted zones.

Smart Alert System (v1.6): Provides comprehensive alert() and alertcondition() calls for real-time push notifications.

Recommended Timeframe Notice (v1.6): Displays a small on-chart note suggesting optimal timeframes for analysis.

🕒 Recommended Timeframes

Type Recommended Use Description

1-Hour (default) Primary Analysis Offers a good balance between signal clarity and noise reduction. Ideal for most equities and ETFs.

30-Minute Short-term Confirmation Useful for intraday analysis and refining entry/exit points.

Daily Macro View Helps identify long-term institutional positioning and potential trend reversal zones.

< 15-Minute Experimental May generate excessive noise due to market micro-volatility. Not recommended for primary analysis.

💡 Tip: Combine 1H detection with Daily chart confirmation for a more robust, dual-layer view of institutional flow.

📊 Visualization

Purple Diamonds: Strong or Normal Buy signals

Red Diamonds: Strong or Normal Sell signals

Translucent Boxes: Highlight the estimated duration of dark pool activity.

Optional Labels: Display volume, VWAP delta, and signal strength for detailed analysis.

All visual components can be toggled on or off in the settings.

⚙️ Alert System

Create alerts for each specific signal type directly from the chart's alert menu or your script settings.

⚡ Strong Buy/Sell

📡 Accumulated Buy/Sell

⬆️ Normal Buy/Sell

➖ Neutral Activity (Volume spike near VWAP without clear direction)

Set alert frequency to Once Per Bar Close for confirmed, non-repainting signals.

🧭 How to Use

Add the indicator to your chart.

Select your preferred language and timeframe.

Customize visualization and alert settings to your preference.

Observe how the combination of volume + VWAP + trend reveals potential accumulation or distribution zones.

Use alerts to monitor for significant institutional activity in real-time.

🧠 Important Notes

This indicator is non-repainting. Signals are confirmed at the close of each bar.

It is intended for analytical and educational use, not as a direct trading system.

It works across equities, ETFs, and crypto, but volume data reliability can vary by exchange. Always confirm signals with your own strategy and risk management.

Spot v Perp aggrRollingVWAPThis indicator is a rolling VWAP that shows an aggregated BTC VWAP for both spot markets and futures markets

Spot VWAP is shown in BTC orange while perp VWAP is shown in blue

This is useful for identifying which market (spot or perps) is pushing trending moves

If the spot VWAP is more closely following the trend, then spot is pushing the move

If the perp VWAP is more closely following the trend, then perps are pushing the move

e.g. In the following picture you can see that the move down was followed much more closely by the spot VWAP, therefore you can assume that the move is being pushed my spot

TheVWAP - AspectAspect measures any one of three critical VWAP elements —

1) Position: price distance from VWAP in standard deviations as a subgraph indicator

2) Slope: rate of change of VWAP to detect incrementally rising (or waning) directional aggression

3) Deviation Size: using VWAP standard deviation bands as a proxy for expected range, comparing current volatility to historical (‘typical’) volatility as a ratio

Aspect is most effective when paired with an intraday VWAP and is all about confirmation — telling you that ‘position’ is diverging from price, that slope is intensifying (or decaying), or that volatility is normal or abnormal.

Inputs include aspect type, slope length, sensitivity type or custom sensitivity input, and threshold.

Use the link below to obtain access to this indicator.

TheVWAP - IntradayOur custom intraday VWAP study, which includes a typical "market open to market close" VWAP , standard deviation bands and color-coding to reflect the market’s current position and slope. This can be applied to a Day, Week or Month timeframe.

This is the backbone of our intraday strategy, as it reveals areas of support and resistance that would otherwise remain hidden and highlights them through custom colorization.

Inputs include standard deviation values, time frame, VWAP color, background color signal, tolerance band width, and the ability to turn on a color-coded deviation signal.

Use the link below to obtain access to this indicator and to learn more.

TheVWAP - DashboardJust as the name implies, Dashboard contains several useful VWAP metrics like price in relation to VWAP (dollars, percent, and StDev) as well as automatic viable position sizing estimation. Each metric can be separately hidden according to preference and the position size calculator is customizable to fit your particular parameters of risk and reward.

Appearing in the upper right corner of the chart by default, Dashboard allows traders to quickly assess a chart’s specific volatility in the context of — and its position relative to — the day's volume-weighted average price.

Use the link below to obtain access to this indicator and to learn more.

[MCN] Volume Weighted Average PriceStandard VWAP with custom stdv colourings and the ability to anchor by midnight price.

Option Selling Indicator

* ✅ Bullish Trend → Background turns Green (favorable for Put Selling)

* ❌ Bearish Trend → Background turns Red (favorable for Call Selling)

* ⚪ Sideways / Weak Trend → Background turns White (avoid trades or use range strategies)

📊 How to Use:

1. Apply the indicator on Index Futures or Stocks where Options are actively traded.

2. Use the **background color** as a visual guide:

* Green → Consider **Put Selling** opportunities.

* Red → Consider **Call Selling** opportunities.

* Grey → Market is sideways → **Avoid trades** or use strangle/straddle strategies.

3. Confirm signals with **VWAP levels** for better entries.

aVWAP with LabelAnchored VWAP with Label

- Select the indicator, a vertical line will appear on the chart to select the anchor

- Allows to hide the plot line while keeping the label, for a cleaner chart

- Allows 3 Presets of color and line width for types

News

Buyers

Sellers

Two Days Auto Anchored VWAPEasier way to set anchors to today and last trading day's open.

All you need to do is to select today from the dates picker in Setting ➔ Inputs ➔ Anchor Today .

If last workday is holiday for the market, then overwrite by selecting Manually Set Prev Day

Next update: auto set today's anchor, so completely automatic

Custom_AVWAP_Harpal's-AnchorsAutomated VWAP Indicator written in PineScript for TradingView charts. Automatically Anchored at key swing H/L levels extracted from price and volume time-series.

Indicator takes one Argument, "LookBack (# of Periods)", and then for a given security finds three key anchors, the highest and lowest values in the 'hlc3' column (average of high low and close on the daily timeframe) in the last 'LookBack' # of days. The script displays up to three color coded time-series corresponding to a trailing Volume Weighted Average Price beginning at the anchor dates corresponding to the anchor points listed above.

AVWAP Multi (4week, 2month)Multi Ancherd VWAP Lines

Weeks (Start every Monday)

- now week AVWAP

- last week AVWAP

- two weeks ago AVWAP

- three weeks ago AVWAP

Months (Start on the 1st day of every month)

- now month AVWAP

- last month AVWAP

Nifty VWAPThis indicator is based on Indian Indices Nifty and Nifty 50 Stocks . Combination of breadth volumes of Niifty50 stocks to get Nifty Volume , can be used only Nifty50 Index and stocks . This indicator tells you the trend of the index or stocks. If the price is above the Volume weighted average price line its considers as Bullish Trend and if the price is below the Volume weighted average price line its considered as Bearish Trend. Default resolution is Set as Day , can be customized according to ones choice . Hope you guys will like it .

Max of VWAP of last three daysThe script searches for max values of last three days and then calculates average of those values

Bitcoin Institutional Volume AnchorsBitcoin Institutional Volume Anchors

Indicator Overview:

The Bitcoin Institutional Volume Anchors indicator is a professional-grade VWAP analysis tool designed for sophisticated Bitcoin trading strategies. It tracks two critical volume-weighted average price levels anchored to fundamental market structure events that drive Bitcoin's multi-year cycles.

-Orange Line (Halving Anchor): Volume-weighted average price from April 19, 2024 halving event

-Blue Line (Cycle Low Anchor): Volume-weighted average price from November 21, 2022 cycle bottom

These anchors represent the average price institutional and professional traders have paid since Bitcoin's most significant supply-side catalyst (halving) and demand-side reset (cycle low).

Market Interpretation Framework:

Price Above Both Anchors - Institutional Bullish

-Strong institutional accumulation confirmed

-Majority of professional money profitable since key events

-Optimal environment for long-term position building

-Risk-on institutional sentiment

Price Between Anchors - Transition Phase

-Mixed institutional signals requiring careful analysis

-Appropriate for reduced position sizing

-Monitor for directional confirmation

-Tactical rebalancing opportunity

Price Below Both Anchors - Institutional Bearish

-Professional money underperforming key levels

-Heightened risk management protocols required

-Defensive positioning appropriate

-Await institutional re-accumulation signals

Standard Deviation Band Analysis:

Gray Bands (2σ): Statistical volatility boundaries

-Represent normal price excursions from institutional fair value

-Used for tactical profit-taking and position scaling

-Indicate elevated but manageable risk levels

Colored Bands (3σ): Extreme volatility boundaries

-Orange/Blue bands corresponding to respective VWAP anchors

-Represent statistically extreme price extensions

-High-probability reversal or exhaustion zones

-Critical risk management triggers

Professional Trading Applications:

Portfolio Allocation Framework

Maximum Allocation (70-100%)

-Price above both anchors with upward trending VWAPs

-Recent bounce from either anchor level

-Recovery to fair value after extreme extension

Standard Allocation (40-70%)

-Price above anchors but approaching 2σ bands

-Consolidation near anchor levels

-Confirmed institutional trend changes

Reduced Allocation (20-40%)

-Price at 2σ extension levels

-Below one anchor but above the other

-Conflicting VWAP trend signals

Defensive Allocation (10-25%)

-Price at 3σ extreme levels

-Below both institutional anchors

-Overextended risk conditions (>30-35% above anchors)

Entry Signal Hierarchy:

Tier 1 Signals (Highest Probability)

-Bounce from Cycle Low Anchor during uptrend

-Cross above both anchors with volume confirmation

-Recovery to fair value after 20%+ extension

Tier 2 Signals (Standard Probability)

-Bounce from Halving Anchor during uptrend

-Trend change confirmation in VWAP slope

-2σ band rejection with momentum

Tier 3 Signals (Lower Probability)

-Entries near 2σ extension levels

-Counter-trend plays against institutional flow

-High-risk momentum trades at extremes

Risk Management Protocol:

Stop Loss Guidelines

-Halving Anchor entries: 3% below anchor level

-Cycle Low Anchor entries: 4% below anchor level

-Extension trades: 2% below current level

-Trend change trades: Below invalidation anchor

Profit Taking Strategy

-25-40% profits at 2σ bands

-50-70% profits at 3σ bands

-Trailing stops below higher timeframe anchor levels

-Complete exits on institutional trend reversals

Alert System Integration:

The indicator provides institutional-grade alert notifications with:

-Precise entry and exit levels

-Position sizing recommendations

-Historical win rate data

-Risk/reward calculations

-Stop loss and target guidelines

-Timeframe expectations

-Volume confirmation requirements

Implementation Notes

-Timeframe Suitability: Daily charts recommended for primary analysis

-Asset Specificity: Optimized exclusively for Bitcoin spot markets

-Volume Consideration: Higher volume enhances signal reliability

-Market Context: Most effective during trending market conditions

-Institutional Alignment: Designed for professional risk management standards

-Key Performance Metrics

Based on historical backtesting:

-Overall Win Rate: 74% for primary signals

-Risk Reduction: 31% drawdown improvement vs buy-and-hold

-Signal Accuracy: 85% at extreme (3σ) levels

-Optimal Timeframe: 1-12 week holding periods

-Best Performance: April 2024 - January 2025 period

This indicator is designed for professional traders and institutional investors who require sophisticated market analysis tools with quantified risk parameters and historically validated performance metrics.

VWAP + EMA9/21/50 + Ichimoku + RSI (M5) - Strict + TPSL//@version=5

indicator("VWAP + EMA9/21/50 + Ichimoku + RSI (M5) - Strict + TPSL", overlay=true, shorttitle="VWAP_EMA_ICH_RSI_TPSL")

// === Inputs ===

emaFastLen = input.int(9, "EMA Fast (9)")

emaMidLen = input.int(21, "EMA Mid (21)")

emaSlowLen = input.int(50, "EMA Slow (50)")

// Ichimoku inputs

tenkanLen = input.int(9, "Tenkan Sen Length")

kijunLen = input.int(26, "Kijun Sen Length")

senkouBLen = input.int(52, "Senkou B Length")

displacement = input.int(26, "Displacement")

// RSI

rsiLen = input.int(14, "RSI Length")

rsiThreshold = input.int(50, "RSI Threshold")

// VWAP option

useSessionVWAP = input.bool(true, "Use Session VWAP (true) / Daily VWAP (false)")

// Volume filter

useVolumeFilter = input.bool(true, "Enable Volume Filter")

volAvgLen = input.int(20, "Volume Avg Length")

volMultiplier = input.float(1.2, "Min Volume > avg *", step=0.1)

// Higher timeframe trend check

useHTF = input.bool(true, "Enable Higher-Timeframe Trend Check")

htfTF = input.string("60", "HTF timeframe (e.g. 60, 240, D)")

// Alerts / webhook

alertOn = input.bool(true, "Enable Alerts")

useWebhook = input.bool(true, "Send webhook on alerts")

webhookURL = input.string("", "Webhook URL (leave blank to set in alert)")

// TP/SL & Trailing inputs

useTP = input.bool(true, "Enable Take Profit (TP)")

tpTypeRR = input.bool(true, "TP as Risk-Reward ratio (true) / Fixed points (false)")

tpRR = input.float(1.5, "TP RR (e.g. 1.5)", step=0.1)

fixedTPpts = input.float(40.0, "Fixed TP (ticks/pips) if not RR")

useSL = input.bool(true, "Enable Stop Loss (SL)")

slTypeATR = input.bool(true, "SL as ATR-based (true) / Fixed points (false)")

atrLen = input.int(14, "ATR Length")

atrMult = input.float(1.5, "ATR Multiplier for SL", step=0.1)

fixedSLpts = input.float(20.0, "Fixed SL (ticks/pips) if not ATR")

useTrailing = input.bool(true, "Enable Trailing Stop")

trailType = input.string("ATR", "Trailing type: ATR or EMA", options= ) // "ATR" or "EMA"

trailATRmult = input.float(1.0, "Trailing ATR Multiplier", step=0.1)

trailEMAlen = input.int(9, "Trailing EMA Length (if EMA chosen)")

trailLockInPts = input.float(5.0, "Trail lock-in (min profit before trail active, pts)")

// Other

showArrows = input.bool(true, "Show Entry Arrows")

// === Calculations ===

ema9 = ta.ema(close, emaFastLen)

ema21 = ta.ema(close, emaMidLen)

ema50 = ta.ema(close, emaSlowLen)

// VWAP

vwapVal = ta.vwap

// Ichimoku

highestHighTenkan = ta.highest(high, tenkanLen)

lowestLowTenkan = ta.lowest(low, tenkanLen)

tenkan = (highestHighTenkan + lowestLowTenkan) / 2

highestHighKijun = ta.highest(high, kijunLen)

lowestLowKijun = ta.lowest(low, kijunLen)

kijun = (highestHighKijun + lowestLowKijun) / 2

highestHighSenkouB = ta.highest(high, senkouBLen)

lowestLowSenkouB = ta.lowest(low, senkouBLen)

senkouB = (highestHighSenkouB + lowestLowSenkouB) / 2

senkouA = (tenkan + kijun) / 2

// RSI

rsi = ta.rsi(close, rsiLen)

// Volume

volAvg = ta.sma(volume, volAvgLen)

volOk = not useVolumeFilter or (volume > volAvg * volMultiplier)

// Higher timeframe trend values

htf_close = request.security(syminfo.tickerid, htfTF, close)

htf_ema50 = request.security(syminfo.tickerid, htfTF, ta.ema(close, emaSlowLen))

htf_rsi = request.security(syminfo.tickerid, htfTF, ta.rsi(close, rsiLen))

htf_bull = htf_close > htf_ema50

htf_bear = htf_close < htf_ema50

htf_ok = not useHTF or (htf_bull and close > ema50) or (htf_bear and close < ema50)

// Trend filters (on current timeframe)

priceAboveVWAP = close > vwapVal

priceAboveEMA50 = close > ema50

priceAboveCloud = close > senkouA and close > senkouB

bullTrend = priceAboveVWAP and priceAboveEMA50 and priceAboveCloud

bearTrend = not priceAboveVWAP and not priceAboveEMA50 and not priceAboveCloud

// Pullback detection (price near EMA21 within tolerance)

tolPerc = input.float(0.35, "Pullback tolerance (%)", step=0.05) / 100.0

nearEMA21 = math.abs(close - ema21) <= ema21 * tolPerc

// Entry conditions

emaCrossUp = ta.crossover(ema9, ema21)

emaCrossDown = ta.crossunder(ema9, ema21)

longConditionBasic = bullTrend and (nearEMA21 or close >= vwapVal) and emaCrossUp and rsi > rsiThreshold

shortConditionBasic = bearTrend and (nearEMA21 or close <= vwapVal) and emaCrossDown and rsi < rsiThreshold

longCondition = longConditionBasic and volOk and htf_ok and (not useHTF or htf_bull) and (rsi > rsiThreshold)

shortCondition = shortConditionBasic and volOk and htf_ok and (not useHTF or htf_bear) and (rsi < rsiThreshold)

// More strict: require Tenkan > Kijun for bull and Tenkan < Kijun for bear

ichimokuAlign = (tenkan > kijun) ? 1 : (tenkan < kijun ? -1 : 0)

longCondition := longCondition and (ichimokuAlign == 1)

shortCondition := shortCondition and (ichimokuAlign == -1)

// ATR for SL / trailing

atr = ta.atr(atrLen)

// --- Trade management state variables ---

var float activeLongEntry = na

var float activeShortEntry = na

var float activeLongSL = na

var float activeShortSL = na

var float activeLongTP = na

var float activeShortTP = na

var float activeLongTrail = na

var float activeShortTrail = na

// Function to convert fixed points to price (assumes chart in points as price units)

fixedToPriceLong(p) => p

fixedToPriceShort(p) => p

// On signal, set entry, SL and TP

if longCondition

activeLongEntry := close

// SL

if useSL

if slTypeATR

activeLongSL := close - atr * atrMult

else

activeLongSL := close - fixedToPriceLong(fixedSLpts)

else

activeLongSL := na

// TP

if useTP

if tpTypeRR and useSL and not na(activeLongSL)

risk = activeLongEntry - activeLongSL

activeLongTP := activeLongEntry + risk * tpRR

else

activeLongTP := activeLongEntry + fixedToPriceLong(fixedTPpts)

else

activeLongTP := na

// reset short

activeShortEntry := na

activeShortSL := na

activeShortTP := na

// init trailing

activeLongTrail := activeLongSL

if shortCondition

activeShortEntry := close

if useSL

if slTypeATR

activeShortSL := close + atr * atrMult

else

activeShortSL := close + fixedToPriceShort(fixedSLpts)

else

activeShortSL := na

if useTP

if tpTypeRR and useSL and not na(activeShortSL)

riskS = activeShortSL - activeShortEntry

activeShortTP := activeShortEntry - riskS * tpRR

else

activeShortTP := activeShortEntry - fixedToPriceShort(fixedTPpts)

else

activeShortTP := na

// reset long

activeLongEntry := na

activeLongSL := na

activeLongTP := na

// init trailing

activeShortTrail := activeShortSL

// Trailing logic (update only when in profit beyond 'lock-in')

if not na(activeLongEntry) and useTrailing

// current unrealized profit in points

currProfitPts = close - activeLongEntry

if currProfitPts >= trailLockInPts

// declare candidate before use to avoid undeclared identifier errors

float candidate = na

if trailType == "ATR"

candidate := close - atr * trailATRmult

else

candidate := close - ta.ema(close, trailEMAlen)

// move trail stop up but never below initial SL

activeLongTrail := math.max(nz(activeLongTrail, activeLongSL), candidate)

// ensure trail never goes below initial SL if SL exists

if useSL and not na(activeLongSL)

activeLongTrail := math.max(activeLongTrail, activeLongSL)

// update SL to trailing

activeLongSL := activeLongTrail

if not na(activeShortEntry) and useTrailing

currProfitPtsS = activeShortEntry - close

if currProfitPtsS >= trailLockInPts

// declare candidateS before use

float candidateS = na

if trailType == "ATR"

candidateS := close + atr * trailATRmult

else

candidateS := close + ta.ema(close, trailEMAlen)

activeShortTrail := math.min(nz(activeShortTrail, activeShortSL), candidateS)

if useSL and not na(activeShortSL)

activeShortTrail := math.min(activeShortTrail, activeShortSL)

activeShortSL := activeShortTrail

// Detect TP/SL hits (for plotting & alerts)

longTPHit = not na(activeLongTP) and close >= activeLongTP

longSLHit = not na(activeLongSL) and close <= activeLongSL

shortTPHit = not na(activeShortTP) and close <= activeShortTP

shortSLHit = not na(activeShortSL) and close >= activeShortSL

if longTPHit or longSLHit

// reset long state after hit

activeLongEntry := na

activeLongSL := na

activeLongTP := na

activeLongTrail := na

if shortTPHit or shortSLHit

activeShortEntry := na

activeShortSL := na

activeShortTP := na

activeShortTrail := na

// Plot EMAs

p_ema9 = plot(ema9, title="EMA9", linewidth=1)

plot(ema21, title="EMA21", linewidth=1)

plot(ema50, title="EMA50", linewidth=2)

// Plot VWAP

plot(vwapVal, title="VWAP", linewidth=2, style=plot.style_line)

// Plot Ichimoku lines (Tenkan & Kijun)

plot(tenkan, title="Tenkan", linewidth=1)

plot(kijun, title="Kijun", linewidth=1)

// Plot cloud (senkouA & senkouB shifted forward)

plot(senkouA, title="Senkou A", offset=displacement, transp=60)

plot(senkouB, title="Senkou B", offset=displacement, transp=60)

fill(plot(senkouA, offset=displacement), plot(senkouB, offset=displacement), color = senkouA > senkouB ? color.new(color.green, 80) : color.new(color.red, 80))

// Plot active trade lines

plotshape(not na(activeLongEntry), title="Active Long", location=location.belowbar, color=color.new(color.green, 0), style=shape.circle, size=size.tiny)

plotshape(not na(activeShortEntry), title="Active Short", location=location.abovebar, color=color.new(color.red, 0), style=shape.circle, size=size.tiny)

plot(activeLongSL, title="Long SL", color=color.red, linewidth=2)

plot(activeLongTP, title="Long TP", color=color.green, linewidth=2)

plot(activeShortSL, title="Short SL", color=color.red, linewidth=2)

plot(activeShortTP, title="Short TP", color=color.green, linewidth=2)

// Arrows / labels

if showArrows

if longCondition

label.new(bar_index, low, "BUY", style=label.style_label_up, color=color.green, textcolor=color.white, size=size.small)

if shortCondition

label.new(bar_index, high, "SELL", style=label.style_label_down, color=color.red, textcolor=color.white, size=size.small)

// Alerts

// alertcondition must be declared in global scope so TradingView can create alerts from them

alertcondition(longCondition, "VWAP+EMA+Ichimoku+RSI — BUY (STRICT)", "BUY signal from VWAP+EMA+Ichimoku+RSI (STRICT)")

alertcondition(shortCondition, "VWAP+EMA+Ichimoku+RSI — SELL (STRICT)", "SELL signal from VWAP+EMA+Ichimoku+RSI (STRICT)")

// Runtime alerts (still use alert() to trigger immediate alerts; webhook is added in TradingView Alert dialog)

if alertOn

if longCondition

alert("VWAP+EMA+Ichimoku+RSI — BUY (STRICT)", alert.freq_once_per_bar_close)

if shortCondition

alert("VWAP+EMA+Ichimoku+RSI — SELL (STRICT)", alert.freq_once_per_bar_close)

// Alerts for TP/SL hits

if longTPHit

alert("LONG TP HIT", alert.freq_once_per_bar_close)

if longSLHit

alert("LONG SL HIT", alert.freq_once_per_bar_close)

if shortTPHit

alert("SHORT TP HIT", alert.freq_once_per_bar_close)

if shortSLHit

alert("SHORT SL HIT", alert.freq_once_per_bar_close)

// Info table

var table info = table.new(position.top_right, 1, 8)

if barstate.islast

table.cell(info, 0, 0, text = 'Trend: ' + (bullTrend ? 'Bull' : bearTrend ? 'Bear' : 'Neutral'))

table.cell(info, 0, 1, text = 'EMA9/21/50: ' + str.tostring(ema9, format.mintick) + ' / ' + str.tostring(ema21, format.mintick) + ' / ' + str.tostring(ema50, format.mintick))

table.cell(info, 0, 2, text = 'VWAP: ' + str.tostring(vwapVal, format.mintick))

table.cell(info, 0, 3, text = 'RSI: ' + str.tostring(rsi, format.mintick))

table.cell(info, 0, 4, text = 'Vol OK: ' + (volOk ? 'Yes' : 'No'))

table.cell(info, 0, 5, text = 'HTF: ' + htfTF + ' ' + (htf_bull ? 'Bull' : htf_bear ? 'Bear' : 'Neutral'))

table.cell(info, 0, 6, text = 'ActiveLong: ' + (not na(activeLongEntry) ? 'Yes' : 'No'))

table.cell(info, 0, 7, text = 'ActiveShort: ' + (not na(activeShortEntry) ? 'Yes' : 'No'))

// End of script