Relative Historical Volatility MCMRelative Historical Volatility

Historical Volatility is relative to it's doubled lookback period of the historical volatility to calculate relative historical volatility.

Including a standard deviation to calculate the volatility value itself is useless. It filters out 32% of the most volatile movements of the asset that you are observing.

Example of RHV:

Period of Volatility Value (POVV) : 10

Relative Historical Volatility : POVV / POVV*2

Historical Volatility of past 10 Bars is compared to the historical volatility of the bast 20 bars to show real growth/decrease of volatility relative to the time of the performing asset.

Comparing historical volatility to the current bar includes much more noise, the relative historical volatility can be perceived as a smoothed historical volatility ind.

Marginal notes:

Added standard deviations adjusted to the relative volatility value to predict probable future volatility of the stock.

ابحث في النصوص البرمجية عن "Volatility"

Volatility Adjusted Moving Average - JD@version=3

This indicator gives an adjusted moving average, based on the volatility of the past x amount of bars, measured against the ema of a certain length.

The idea came out of my VA adjusted Bands indicator where the VAMA is actually the center line.

I scripted the moving average as a function so it is easy to inport into other scripts,

Feel free to use it in your scripts and experiment with it,

of cousre, if you want to publish your script, a little mention in the notes is always appreciated.

At first view I might add some smoothing otions and

a couple of different ma options as a base anchor in future releases.

If you have any other ideas for further development,... let me know!!

JD.

#NotTradingAdvice #DYOR

I build these indicators for myself and provide them open source, to use for free to use and improve upon,

as I believe the best way to learn is toghether.

OHLC Volatility Estimators by @Xel_arjonaDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is by Creative-Commons as TradingView's regulations. Any use, copy or re-use of this code should mention it's origin as it's authorship.

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS DEBUGING CODE The models included in the function have been taken from openly sources on the web so they could have some errors as in the calculation scheme and/or in it's programatic scheme. Debugging are welcome.

WHAT'S THIS?

Here's a full collection of candle based (compressed tick) Volatility Estimators given as a function, openly available for free, it can print IMPLIED VOLATILITY by an external symbol ticker like INDEX:VIX.

Models included in the volatility calculation function:

CLOSE TO CLOSE: This is the classic estimator by rule, sometimes referred as HISTORICAL VOLATILITY and is the must common, accepted and widely used out there. Is based on traditional Standard Deviation method derived from the logarithm return of current close from yesterday's.

ELASTIC WEIGHTED MOVING AVERAGE: This estimator has been used by RiskMetriks®. It's calculation is based on an ElasticWeightedMovingAverage Standard Deviation method derived from the logarithm return of current close from yesterday's. It can be viewed or named as an EXPONENTIAL HISTORICAL VOLATILITY model.

PARKINSON'S: The Parkinson number, or High Low Range Volatility, developed by the physicist, Michael Parkinson, in 1980 aims to estimate the Volatility of returns for a random walk using the high and low in any particular period. IVolatility.com calculates daily Parkinson values. Prices are observed on a fixed time interval. n=10, 20, 30, 60, 90, 120, 150, 180 days.

ROGERS-SATCHELL: The Rogers-Satchell function is a volatility estimator that outperforms other estimators when the underlying follows a Geometric Brownian Motion (GBM) with a drift (historical data mean returns different from zero). As a result, it provides a better volatility estimation when the underlying is trending. However, this Rogers-Satchell estimator does not account for jumps in price (Gaps). It assumes no opening jump. The function uses the open, close, high, and low price series in its calculation and it has only one parameter, which is the period to use to estimate the volatility.

YANG-ZHANG: Yang and Zhang were the first to derive an historical volatility estimator that has a minimum estimation error, is independent of the drift, and independent of opening gaps. This estimator is maximally 14 times more efficient than the close-to-close estimator.

LOGARITHMIC GARMAN-KLASS: The former is a pinescript transcript of the model defined as in iVolatility . The metric used is a combination of the overnight, high/low and open/close range. Such a volatility metric is a more efficient measure of the degree of volatility during a given day. This metric is always positive.

Volatility Momentum Score | Lyro RSVolatility Momentum Score | Lyro RS

Overview

The Volatility Momentum Score (VMS) combines price movement and volatility into a single, easy-to-read signal. Using z-scores, standard deviation bands, and flexible display modes, it helps traders identify trends, overbought/oversold conditions, and potential reversals quickly and effectively.

Key Features

Price + Volatility Blend

Tracks price action and volatility with separate z-scores and merges them into a unified momentum score.

Standard Deviation Bands

Upper and lower bands highlight extreme readings.

Adjustable multipliers allow for fine-tuning sensitivity.

Two Signal Modes

Trend Mode: Plots “Long” and “Short” signals when momentum crosses bands.

Reversion Mode: Colors the chart background when the score indicates stretched conditions.

Overbought & Oversold Alerts

▲ markers indicate oversold conditions.

▼ markers indicate overbought conditions.

Custom Colors

Four preset color themes or fully customizable bullish/bearish colors.

Clear Visuals

Dynamic line coloring based on momentum.

Candles recolored at signal points.

Background shading for quick visual assessment.

How It Works

Calculates z-scores for both price and volatility.

Blends the z-scores into a single average score.

Compares the score against dynamic upper and lower bands.

Triggers signals, markers, or background shading depending on the chosen display mode.

Practical Use

Ride trends: Follow Trend Mode signals to align with momentum.

Spot reversals: Watch ▲ and ▼ markers when markets are overextended.

Stay aware: Background shading highlights potentially overheated conditions.

Customization

Set lookback lengths for price, volatility, and bands.

Adjust band multipliers for more or less sensitive signals.

Choose between Trend or Reversion mode based on trading style.

Select color themes or create custom palettes.

⚠️ Disclaimer

This indicator is a technical analysis tool and does not guarantee results. It should be used alongside other methods and proper risk management. The creators are not responsible for any financial decisions based on its signals.

30D Vs 90D Historical VolatilityVolatility equals risk for an underlying asset's price meaning bullish volatility is bearish for prices while bearish volatility is bullish. This compares 30-Day Historical Volatility to 90-Day Historical Volatility.

When the 30-Day crosses under the 90-day, this is typically when asset prices enter a bullish trend.

Conversely, When the 30-Day crosses above the 90-Day, this is when asset prices enter a bearish trend.

Peaks in volatility are bullish divergences while troughs are bearish divergences.

Volatility Gaussian Bands [BigBeluga]The Volatility Gaussian Bands indicator is a cutting-edge tool designed to analyze market trends and volatility with high precision. By applying a Gaussian filter to smooth price data and implementing dynamic bands based on market volatility, this indicator provides clear signals for trend direction, strength, and potential reversals. With updated volatility calculations, it enhances the accuracy of trend detection, making it a powerful addition to any trader's toolkit.

⮁ KEY FEATURES & USAGE

● Gaussian Filter Trend Bands:

The Gaussian Filter forms the foundation of this indicator by smoothing price data to reveal the underlying trend. The trend is visualized through upper and lower bands that adjust dynamically based on market volatility. These bands provide clear visual cues for traders: a crossover above the upper band indicates a potential uptrend, while a cross below the lower band signals a potential downtrend. This feature allows traders to identify trends with greater accuracy and act accordingly.

● Dynamic Trend Strength Gauges:

The indicator includes trend strength gauges positioned at the top and bottom of the chart. These gauges dynamically measure the strength of the uptrend and downtrend, based on the middle Gaussian line. Even if the trend is downward, a rising midline will cause the upward trend strength gauge to show an increase, offering a nuanced view of the market’s momentum.

Weakening of the trend:

● Fast Trend Change Indicators:

Triangles with a "+" symbol appear on the chart to signal rapid changes in trend direction. These indicators are particularly useful when the trend changes swiftly while the midline continues to grow in its previous direction. For instance, during a downtrend, if the trend suddenly shifts upward while the midline is still declining, a triangle with a "+" will indicate this quick reversal. This feature is crucial for traders looking to capitalize on rapid market movements.

● Retest Signals:

Retest signals, displayed as triangles, highlight potential areas where the price may retest the Gaussian line during a trend. These signals provide an additional layer of analysis, helping traders confirm trend continuations or identify possible reversals. The retest signals can be customized based on the trader’s preferences.

⮁ CUSTOMIZATION

● Length Adjustment:

The length of the Gaussian filter can be customized to control the sensitivity of trend detection. Shorter lengths make the indicator more responsive, while longer lengths offer a smoother, more stable trend line.

● Volatility Calculation Mode:

Traders can select from different modes (AVG, MEDIAN, MODE) to calculate the Gaussian filter, allowing for flexibility in how trends are detected and analyzed.

● Retest Signals Toggle:

Enable or disable the retest signals based on your trading strategy. This toggle allows traders to choose whether they want these additional signals to appear on the chart, providing more control over the information displayed during their analysis.

⮁ CONCLUSION

The Volatility Gaussian Bands indicator is a versatile and powerful tool for traders focused on trend and volatility analysis. By combining Gaussian-filtered trend lines with dynamic volatility bands, trend strength gauges, and rapid trend change indicators, this tool provides a comprehensive view of market conditions. Whether you are following established trends or looking to catch early reversals, the Volatility Gaussian Bands offers the precision and adaptability needed to enhance your trading strategy.

volatility-weighted price change divergenceEMA of intrabar-volatility-weighted price change minus EMA of price change. It puts more weights on candles that have large volatility inside, and assumes that the direction of those high-volatility candles are more meaningful than low-volatility ones. Therefore, we take the difference between the volatility-weighted price change and the regular price change and plot the EMA. The indicator may be used as a tool to find divergence and potential reversal, or hints of continuation of a strong trend. Note that this indicator can change a lot with different time frames and settings, so take care to backtest before using. Recommended settings are 15m resolution for time frames longer than 4H and 1m resolution (with 200 EMA length) for time frames below 4H. The resolution is used to find the intrabar volatility.

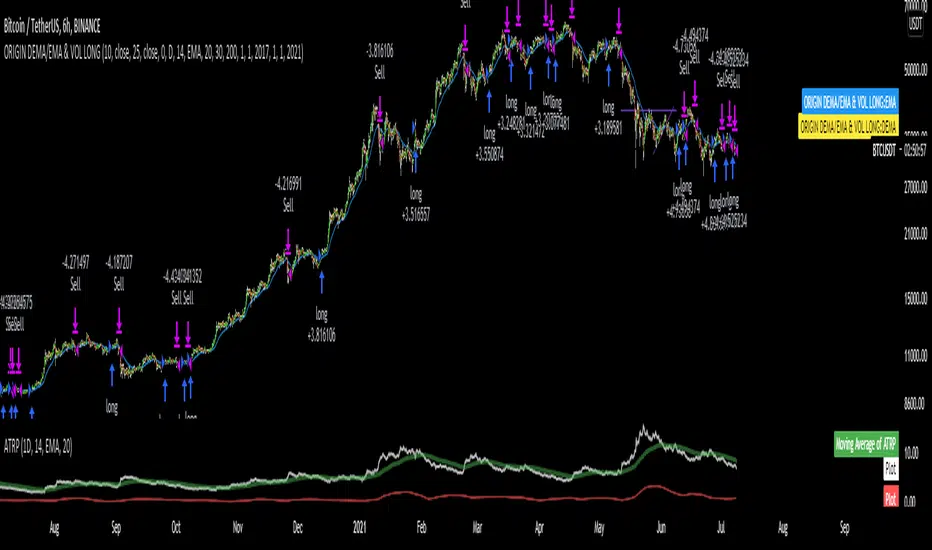

DEMA/EMA & VOLATILITY (VAMS)The biggest issue with momentum following strategies is over signaling during whipsaw periods. I created this strategy that measure momentum with DEMA (Fast Moving) and EMA (Slow moving). In order to mitigate over signaling during whipsaw periods I implemented the average true range percentage (ATRP) to measure realized volatility. If momentum is picking up while volatility is under a certain threshold it purchases the security. If momentum slows while volatility picks up it sells the security. Additionally, if momentum picks up, but volatility is high, it stays out of the security. This follows the theory that during sustained uptrends volatility will decrease, and during market corrections the volatility picks up. Following the old adage that markets climb up the stairs, and fall out the window. Note that this strategy does repaint due to it entering and closing positions at the close of the bars. I forgot to mention how volatility is measured high vs low. If the ATRP is above the EMA of the ATRP the strategy interprets the volatility is increasing and does not enter the security & Vice Versa for selling (with momentum signal of MAs)

This is just my first strategy, any feedback would be much appreciated.

Historical Volatility Percentile: Price and VolumeThis is an expansion of the Historical Volatility scripts to include both price and volume volatility.

As Tradingview states :

Historical Volatility is a measure of how much price (and now volume ) deviates from its average in a specific time period that can be set. The more price (or/and volume ) fluctuates, the higher the indicator value. Please note it does not measure the direction of price (and volume ) changes, just how volatile price/ volume has become. There are several reasons to care about volatility but it's mainly a risk measure. As volatility increases, so does risk and uncertainty and vice versa. Traders can use the indicator to flag instruments with high volatility which could point to a trend change. It is often used in combination with other signals.

Example options

Example formats

Link back to some other great ideas:

@Cheatcountry with his prolific sharing , what a great inspiration.

@Picte and his inspired idea .

@Balipour and his great script

Comparing this to other significant HVP indicators

Realized VolatilityRealized / Historical Volatility

Calculates historical, i.e. realized volatility of any underlying. If frequency is not the daily, but for example 6h, 30min, weeks or months, it scales the initial setting to be suitable for the different time frame.

Examples with default settings (30 day volatility, 365 days per year):

A) Frequency = Daily:

Returns 30 day historical volatility, under the assumption that there are 365 trading days in a year.

B) Frequency = 6h:

Still returns 30 day historical volatility, under the assumption that there are 365 trading days in a year. However, since 6h granularity fits 4 times in 24 hours, it rescales the look back period to rather 30*4 = 120 units to still reflect 30 day historical volatility.

Closed Form Distance VolatilityIntroduction

Calculating distances in signal processing/statistics/time-series analysis imply measuring the distance between two probability distribution, i am not really familiar with distances but since some formulas are in closed form they can be easily used for volatility estimation. This volatility indicator will use three methods originally made to measure the distance of gaussian copulas, using those methods for volatility estimation is fairly easy and provide a different approach to statistical dispersion.

The indicator have a length parameter and a method parameter to select the method used for volatility estimation, i describe each methods below.

Hellinger Method

Each method will use the rolling sum of the low price and the rolling sum of the high price instead of probability distributions. The Hellinger method have many application from the measurement of distances to the use as a cost function for neural networks.

Its closed form is defined as the square root of 1 - a^0.25b^0.25/(0.5a + 0.5b)^0.5 where a and b are both positive series. In our indicator a is the rolling sum of the high price and b the rolling sum of the low price. This method give a classic estimation of volatility.

Bhattacharyya Method

The Bhattacharyya method is another method who use a natural logarithm, this method can visually filter small volatility variation. It is defined as 0.5 * log((0.5a+0.5b)/√(ab)) .

Wasserstein Method

This method was originally using a trimmed mean for its calculation. The original method is defined as the square of the trimmed mean of a + b - 2√(a^0.5ba^0.5) , a median has been used instead of a trimmed mean for efficiency sake, both central tendency estimators are robust to outliers.

Conclusion

I showed that closed form formulas for distance calculation could be derived into volatility estimators with different properties. They could be used with series in a range of (0,1) to provide a smoothing variable for exponential smoothing.

Rogers & Satchell Volatility EstimationFirst off, a huge thank you to the following people:

theheirophant: www.tradingview.com

alexgrover: www.tradingview.com

NGBaltic: www.tradingview.com

The Rogers & Satchell function is a volatility estimator that outperforms other estimators when the underlying follows a geometric Brownian motion with a drift (historical data mean returns different from zero). As a result, it provides a better volatility estimation when the underlying is trending. However, the Rogers & Satchell estimator does not account for jumps in price (gaps). It assumes no opening jump. The function uses the open, close, high, and low price series in its calculation and it has only one parameter, which is the period to use to estimate the volatility.

This script allows you to transform the volatility reading. The intention of this is to be able to compare volatility across different assets and timeframes. Having a relative reading of volatility also allows you to better gauge volatility within the context of current market conditions.

For the signal lie I chose a repulsion moving average to remove choppy crossovers of the estimator and the signal. This may have been a mistake, so in the near-future I might update so that the MA can be selected. Let me know if you have any opinions either way.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Up Down VolatilityThis is just experimental. I wanted the flexibility in looking at volatility and this indicator gives you several ways to do so.

I haven't figured out the best way to use this yet but I suspect that as a form of entry confirmation indicator would be best.

If you find a way this works well for you please drop me a note. It would nice know someone found a way to use it successfully!

The options available are:

* Your source can be price or the ATR.

* It allows you to separate the volatility of the bearish and bullish candles and even allows you to produce differential.

* You can choose to run the result through any one of many smoothers.

With the above options you can look at:

* The normal volatility. That is not split into bearish and bullish components.

* The bearish and bullish volatility and the difference between them.

* The relative bearish and bullish volatility and the difference between them.

The "The relative bearish and bullish" is each one divided into the source before it was split into Up and Down or low/high divided by close which should make the max value roughly around 1.

The code is structured to easily drop into a bigger system so use it as a lone indicator or add the code to some bigger project you are creating. If you do integrate it into something else then send me a note as it would be nice to know it's being well used.

Enjoy and good luck!

Historical Volatility Percentile FilterThis indicator provides a simple market regime filter for Historical Volatility. Depending on the strategy that you are using, it is useful to know how your strategy will perform at different

ranges of volatility, as this can greatly impact your performance. For instance, some of my long-only mean reversion strategies will only take trades where the volatility percentile is not extremely high, as this can often indicate fundamental changes in the security or the start of a big market correction. Some strategies may work better when volatility is higher

Feel free to use the following code along with your strategies to help improve performance and reduce the volatility of your gains in the long term.

Historical Volatility Percentile + SMAHistorical Volatility Percentile tells you the percentage of the days from the past year (252 trading days) that have lower volatility than the current volatility.

I included a simple moving average as a signal line to show you how volatile the stock is at the moment.

I have included simple colors to let you know when to enter or exit a position.

Buy when price higher than EMA & historical volatility higher than SMA

Sell when price lower than EMA & historical volatility higher than SMA

Please let me know if you would like me to publish any other indicators! I always love to hear from you guys.

Scott’s volatility histogramATR shows volatility. SMA of ATR measures the average volatility over a chosen look-back period (default 200).

Divergence of ATR and sma is represented as a histogram.

Low periods of volatility are below the zero line. High periods of volatility are above the zero line.

Average volatility over a 200 period look-back is the zero value.

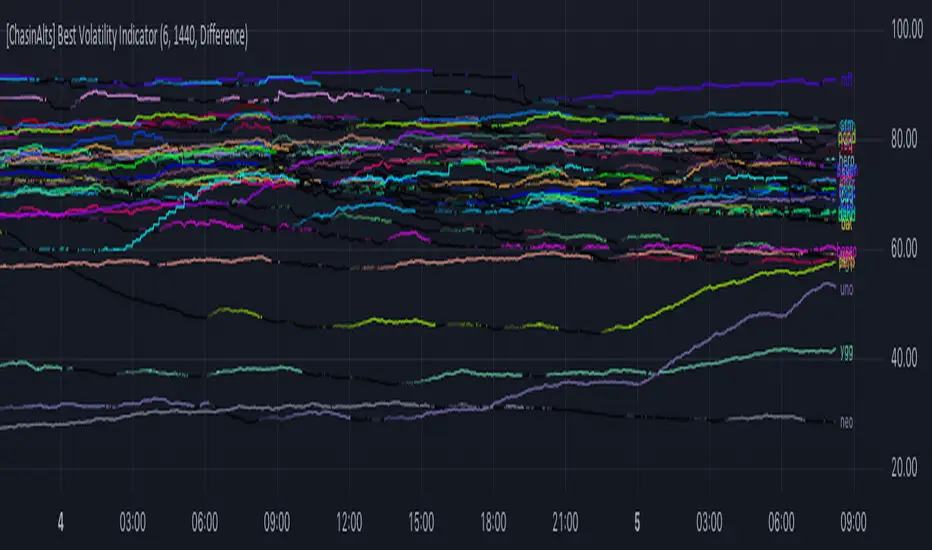

[ChasinAlts] Best Volatility Indicator I hope you all enjoy this one as it does a great job at finding runners I did try to search for an example script to reference for quite a while when i first dreamt up this idea bc needed assistance implementing it. This script in particular was one that I began long ago but got put on the back-burner because I couldn't figure out how to implement the flow of logic until I came across a library titled 'Conditional Averages' and published by the “Pinecoders" account. Thus, the logic in this code is partially derived from that () . To understand what the functions/logic do in the beginning of the 'Functions'' section, you must understand how TV presents it's data through the charts.

Wether on the 1sec TF or the 1day (or ANY other), the only time TV prints a bar/candle is when a trade occurs for that asset (i.e. a change in volume). Even if Open=Close on the same candle, the candle will print with the updated price. The % of candles printed out of the TOTAL possible amount that COULD HAVE been printed is the ultimate output that’s calculated in the script. So, if the lookback setting=10min on the 1min TF and only 7 out of the last 10 candles have printed then the value will appear as 70(%). There are MANY benefits to using this method to measure volatility but its vital to recall that the indicator does nothing to provide the direction of future price movement. One thing I’ve noticed is that when a coin is just beginning it’s ascent and its move is considerably larger/longer than all the other coins OR the plots angle is very steep, it is usually the end of a move and the direction is about to abruptly reverse, continuing with it’s volatility. As volatility increases more and more the plot gets brighter and brighter…and also vise versa.

The settings are as follows:

1) which set of Kucoin’s Margin Coins to use (8 possible sets with 32 coins in each set).

2) input how many minutes ago to start counting the total printed candles from (i.e. if setting is input as 1440, count begins from exactly 24hrs(1440min) ago to present candle.

3) there are 3 different lines to choose from to be able to plot:

i. ‘Includes Open==Close’ = adds to count when bar prints but price does NOT change (=t1)

ii. ‘Does NOT include Open==Close’ = count ONLY updates upon price movement (=t2)

iii. ‘Difference’ = (( t1 - t2 ) / t1 ) *100

*** I’ve got some more great ones I will be uploading soon. Just have to create a description for them

Peace out,

- ChasinAlts

MACD + DMI Scalping with Volatility Stop by (Coinrule)Trend-following strategies are cool because they allow you to catch potential high returns.

The main limit of such strategies are:

False signals > the asset is not experiencing a strong trend. The strategy gets stuck with a sideways move or, worst, with the beginning of a downtrend.

The sell signal may come later than the actual top, leading in some cases to turn a trade in profit into a loss.

This strategy tries to address these limitations to develop a trading system that optimises the entry and closes trade once the profit achieves a pre-set level.

ENTRY

The trading system uses the MACD and the DMI to confirm when is the best time for buying. Combining these two indicators prevents trading during downtrends and reduces the likelihood of getting stuck in a market with low volatility.

The system confirms the entry when:

The MACD histogram turns bullish.

When the positive DMI is greater than the negative DMI, there are more chances that the asset is trading in a sustained uptrend.

EXIT

The strategy comes with a fixed take profit combined with a volatility stop, which acts as a trailing stop to adapt to the trend's strength. Depending on your long term confidence in the asset, you can edit the fixed take profit to be more conservative or aggressive.

The position is closed when:

The price increases by 3%

The price crosses below the volatility stop.

The best time frame for this strategy based on our backtest is the 3-hr . The 4-hr can work well. In general, this approach suits medium to long term strategies

The strategy assumes each order to trade 30% of the available capital to make the results more realistic. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Statistical Volatility - Extreme Value Method Backtest This indicator used to calculate the statistical volatility, sometime

called historical volatility, based on the Extreme Value Method.

Please use this link to get more information about Volatility.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Statistical Volatility - Extreme Value Method This indicator used to calculate the statistical volatility, sometime

called historical volatility, based on the Extreme Value Method.

Please use this link to get more information about Volatility.

Historical Volatility MA - LayeringProvides a historical volatility moving average to show trends in volatility. Meant to be used with Volume MA, and Vol of Vol MA, layered on top of eachother.

Volatility Based Momentum Oscillator (VBMO)There is a frequent and definitive pattern in price movement, whereby price will steadily drift lower, then accelerate before bottoming out. Similarly, price will often steadily rise, then accelerate into a climax top.

The Volatility Based Momentum Oscillator (VBMO) is designed to delineate between steady versus more accelerated and climactic price movements.

VBMO is calculated using a short-term moving average, the distance of price from this moving average, and the trading instrument’s historical volatility. Even though VBMO’s calculation is relatively simple, the resulting values can help traders identify, analyze and act upon many scenarios, such as climax tops, reversals, and capitulation. Moreover, since the units and scale for VBMO are always the same, the indicator can be used in a consistent manner across multiple timeframes and instruments.

For more details, there is an article further describing VBMO and its applicability.