Intraday Volatility Bands [Honestcowboy]The Intraday Volatility Bands aims to provide a better alternative to ATR in the calculation of targets or reversal points.

How are they different from ATR based bands?

While ATR and other measures of volatility base their calculations on the previous bars on the chart (for example bars 1954 to 1968). The volatility used in these bands measure expected volatility during that time of the day.

Why would you take this approach?

Markets behave different during certain times of the day, also called sessions.

Here are a couple examples.

Asian Session (generally low volatility)

London Session (bigger volatility starts)

New York Session (overlap of New York with London creates huge volatility)

Generally when using bands or channel type indicators intraday they do not account for the upcoming sessions. On London open price will quickly spike through a bollinger band and it will take some time for the bands to adjust to new volatility.

This script will show expected volatility targets at the start of each new bar and will not adjust during the bar. It already knows what price is expected to do at this time of day.

Script also plots arrows when price breaches either the top or bottom of the bands. You can also set alerts for when this occurs. These are non repainting as the script knows the level at start of the bar and does not change.

🔷 CALCULATION

Think of this script like an ATR but instead it uses past days data instead of previous bars data. Charts below should visualise this more clearly:

The scripts measure of volatility is based on a simple high-low.

The script also counts the number of bars that exist in a day on your current timeframe chart. After knowing that number it creates the matrix used in it's calculations and data storage.

See how it works perfectly on a lower timeframe chart below:

Getting this right was the hardest part, check the coding if you are interested in this type of stuff. I commented every step in the coding process.

🔷 SETTINGS

Every setting of the script has a tooltip but I provided a breakdown here:

Some more examples of different charts:

ابحث في النصوص البرمجية عن "Volatility"

Breaks and Retests with Volatility Stop [HG]The "Breaks and Retests with Volatility Stop " indicator is a powerful tool designed to assist traders in identifying key support and resistance levels, breakouts, retests, and potential trend reversals. This indicator combines two essential components: support and resistance detection, and a Volatility Stop indicator for improved risk management. Below are the key features of this indicator:

**Support and Resistance Detection:**

- **Lookback Range:** Users can customize the lookback range, determining how many bars are considered when identifying support and resistance levels. This allows for flexibility in capturing short-term or longer-term levels.

- **Bars Since Breakout:** The indicator helps traders spot retests by allowing them to specify the number of bars that should occur since a breakout before considering it a potential retest.

- **Retest Detection Limiter:** Traders can set a limit on how many bars should be actively checked during a potential retest event. This feature prevents retest alerts from occurring too late, ensuring more accurate results.

- **Breakouts and Retests:** Users can choose to display or hide breakout and retest events separately, tailoring the indicator to their specific trading strategy.

- **Repainting Options:** The indicator offers three repainting options: "On," "Off: Candle Confirmation," and "Off: High & Low." This provides flexibility in choosing the repainting behavior that suits your trading style.

**Styling Options:**

- **Outline and Extend:** Traders can customize the appearance of support and resistance boxes by selecting outline styles and extension preferences.

- **Label Types and Sizes:** The indicator offers two label types, "Full" and "Simple," allowing traders to choose the level of detail displayed on the chart. Additionally, users can adjust the label size for better visibility.

- **Customizable Colors:** Support and resistance levels can be color-coded to match your preferred charting style, enhancing visibility and clarity.

- **Override Text Color:** If desired, traders can override the text color for labels, providing further customization of the indicator's appearance.

**Alerts and Notifications:**

- The indicator generates various alerts and notifications to keep traders informed about critical market events, including:

- New Support and Resistance Levels

- Support and Resistance Breakouts

- Support and Resistance Retests

- Potential Support and Resistance Retests

**Volatility Stop Indicator:**

- The "Breaks and Retests with Volatility Stop " indicator also includes a Volatility Stop component, which helps traders manage risk by indicating potential stop-loss levels based on market volatility. The Volatility Stop is color-coded to reflect the current trend direction, making it easy to identify potential trend reversals.

In summary, this TradingView indicator is a comprehensive tool designed to enhance your technical analysis and trading decisions. It provides support and resistance levels, breakout and retest alerts, and incorporates a Volatility Stop indicator for risk management, making it a valuable addition to any trader's toolkit.

VWMA/SMA Delta Volatility (Statistical Anomaly Detector)The "VWMA/SMA Delta Volatility (Statistical Anomaly Detector)" indicator is a tool designed to detect and visualize volatility in a financial market's price data. The indicator calculates the difference (delta) between two moving averages (VWMA/SMA) and uses statistical analysis to identify anomalies or extreme price movements. Here's a breakdown of its components:

Hypothesis:

The hypothesis behind this indicator is that extreme price movements or anomalies in the market can be detected by analyzing the difference between two moving averages and comparing it to a statistically derived normal distribution. When the MA delta (the difference between two MAs: VWMA/SMA) exceeds a certain threshold based on standard deviation and the Z-score coefficient, it may indicate increased market volatility or potential trading opportunities.

Calculation of MA Delta:

The indicator calculates the MA delta by subtracting a simple moving average (SMA) from a volume-weighted moving average (VWMA) of a selected price source. This calculation represents the difference in the market's short-term and long-term trends.

Statistical Analysis:

To detect anomalies, the indicator performs statistical analysis on the MA delta. It calculates a moving average (MA) of the MA delta and its standard deviation over a specified sample size. This MA acts as a baseline, and the standard deviation is used to measure how much the MA delta deviates from the mean.

Delta Normalization:

The MA delta, lower filter, and upper filter are normalized using a function that scales them to a specific range, typically from -100 to 100. Normalization helps in comparing these values on a consistent scale and enhances their visual representation.

Visual Representation:

The indicator visualizes the results through histograms and channels:

The histogram bars represent the normalized MA delta. Red bars indicate negative and below-lower-filter values, green bars indicate positive and above-upper-filter values, and silver bars indicate values within the normal range.

It also displays a Z-score channel, which represents the upper and lower filters after normalization. This channel helps traders identify price levels that are statistically significant and potentially indicative of market volatility.

In summary, the "MA Delta Volatility (Statistical Anomaly Detector)" indicator aims to help traders identify abnormal price movements in the market by analyzing the difference between two moving averages and applying statistical measures. It can be a valuable tool for traders looking to spot potential opportunities during periods of increased volatility or to identify potential market anomalies.

Fierytrading: Volatility DepthDear Tradingview community,

I'd like to share one of my staple indicators with you. The volatility depth indicator calculates the volatility over a 7-day period and plots it on your chart.

This indicator only works for the DAILY chart on BTC/USD.

Colors

I've color coded the indicator as follows:

- Red: Extreme Volatility

- Orange: High Volatility

- Yellow: Normal Volatility

- Green: Low Volatility

Red: extreme changes in price. Often during local tops and bottoms.

Orange: higher than average moves in price. Often before or after a "red" period. Often seen in the middle of bear or bull markets.

Yellow: normal price action. Often seen during early stage bull-markets and late stage bear-markets.

Green: very low price movement. Often during times of indecision. Once this indicator becomes green, you can expect a big move in either direction. Low volatility is always followed by high volatility.

In a long-term uptrend, a green period often signals a bullish break out. In a long-term downtrend it often signals a bearish break out.

How to use

Save the indicator and apply it to your chart. You can change the length in the settings, but it's optimized for 7 days, so no need to change it.

I've build in alerts for all 4 different volatility periods. In most cases, the low volatility alert is enough.

Good luck!

GKD-C Volatility Quality Index [Loxx]Giga Kaleidoscope Volatility Quality Index is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ Giga Kaleidoscope Modularized Trading System

What is Loxx's "Giga Kaleidoscope Modularized Trading System"?

The Giga Kaleidoscope Modularized Trading System is a trading system built on the philosophy of the NNFX (No Nonsense Forex) algorithmic trading.

What is an NNFX algorithmic trading strategy?

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends.

4. Confirmation 2 - a technical indicator used to identify trends.

5. Continuation - a technical indicator used to identify trends.

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown.

7. Exit - a technical indicator used to determine when a trend is exhausted.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v1.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data between modules. Data is passed between each module as described below:

GKD-B => GKD-V => GKD-C(1) => GKD-C(2) => GKD-C(Continuation) => GKD-E => GKD-BT

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Strategy with 1-3 take profits, trailing stop loss, multiple types of PnL volatility, and 2 backtesting styles

Baseline: Hull Moving Average as shown on the chart above

Volatility/Volume: Average Directional Index (ADX) as shown on the chart above

Confirmation 1: Volatility Quality Index as shown on the chart above

Confirmation 2: Williams Percent Range

Continuation: Fisher Transform

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD protocol chain.

Giga Kaleidoscope Modularized Trading System Signals (based on the NNFX algorithm)

Standard Entry

1. GKD-C Confirmation 1 Signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Continuation Entry

1. Standard Entry, Baseline Entry, or Pullback; entry triggered previously

2. GKD-B Baseline hasn't crossed since entry signal trigger

3. GKD-C Confirmation Continuation Indicator signals

4. GKD-C Confirmation 1 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 2 agrees

1-Candle Rule Standard Entry

1. GKD-C Confirmation 1 signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

1-Candle Rule Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

PullBack Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is beyond 1.0x Volatility of Baseline

Next Candle:

1. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

█ Volatility Quality Index

What is Volatility Quality Index?

The original volatility quality index was invented by Thomas Stridsman. This version doesn't use averages for trend estimation, but instead uses the slope of the Volatility quality. In order to lessen the number of signals (which can be enormous if the VQ is not filtered), some versions similar to this use pips filters. This version is uses a % ATR ( Average True Range ) filter instead.

The reason for that is that:

-Using fixed pips value as a filter will work on one symbol and will not work on another

-Changing time frames will render the filter worthless since the ranges of higher time frames are much greater than those at lower time frames, and, when you set your filter on one time frame and then try it on another, it is almost certain that it will have to be adjusted again

Additionally, this version is made to oscillate around zero line (which makes the potential levels, which are even in the original Stridsman's version doubtful, unnecessary)

Requirements

Inputs

Confirmation 1 and Solo Confirmation: GKD-V Volatility / Volume indicator

Confirmation 2: GKD-C Confirmation indicator

Outputs

Confirmation 2 and Solo Confirmation: GKD-E Exit indicator

Confirmation 1: GKD-C Confirmation indicator

Continuation: GKD-E Exit indicator

Additional features will be added in future releases.

This indicator is only available to ALGX Trading VIP group members . You can see the Author's Instructions below to get more information on how to get access.

NEXT Volatility-Momentum Moving Average (VolMo MA)Overview

Volatility-Momentum Moving Average (VolMo MA) incorporates two key market dynamics into its price averaging formula: volatility and momentum. Traditional MAs, like EMA, often lag in volatile markets or during strong price moves. By integrating volatility (price range variability) and momentum (rate of price change), we developed a more adaptive and responsive MA.

Key Concepts

Volatility Calculation: Average True Range (ATR) used to quantify market volatility. ATR measures the average price range over a specified period.

Momentum Calculation: Relative Strength Index (RSI) applied to assess market momentum. RSI evaluates the speed and magnitude of price movements.

Moving Average Adjustment: Dynamically weight EMA based on volatility and momentum metrics. When volatility is high, the MA's responsiveness increases. Similarly, strong momentum accelerates the MA adjustment.

Input Parameters:

Length - length of Volatility-Momentum Moving Average (VolMo MA). This input also affects how far back momentum and volatility are considered. Experimentation is highly encouraged.

Sensitivity - controls the Volatility-Momentum adjustment rate applied to the MA. Default is 50, but experimentation is highly encouraged.

Source - data used for calculating the MA, typically Close, but can be used with other price formats and data sources as well. A lot of potential here.

Note: The VolMo MA Indicator plots, both, the Volatility-Momentum Moving Average and EMA for base comparison. You can disable EMA by unticking it under Style tab.

NASDAQ 100 Futures ( CME_MINI:NQ1! ) 1-minute

The following example compares VolMo MA (blue) to EMA (green). Length set to 34, Sensitivity to 40. Notice the difference in responsiveness as price action consolidates and breaks out. The VolMo MA can be used for scalping at lower Length values and 40-60 Sensitivity or as a dynamic support/resistance line at higher Length values.

Alerts

Here is how to set price crossing VolMo MA alerts: open a TradingView chart, attach NEXT NEXT Volatility-Momentum Moving Average (VolMo MA), right-click on chart -> Add Alert. Condition: Symbol (e.g. NQ) >> Crossing >> NEXT Volatility-Momentum Moving Average (VolMo MA) >> VolMo MA >> Once Per Bar Close.

Development Roadmap

Our initial research shows plenty of edge potential for the VolMo MA when used, both, by itself, or interacting with other indicators. To that end, we'll be adding the following features over the next few months:

Visual signal generation via interaction with EMA, price action, and other MAs and indicators - you can already do alerts with TradingView's built-in Alert functionality

Addition of a second, fully configurable VolMo MA for a Double VolMo MA cross strategy

VolMo MA MACD

Automation and Backtesting via Strategy

ATR-Based Volatility SL/Target Planner (MTF Table)✅ ATR SL & Target Planner (MTF Table – Chart, 10m, 15m)

This indicator provides a clean multi-timeframe ATR table showing:

✅ ATR (Chart / 10m / 15m)

✅ Entry price (manual or auto)

✅ ATR-based Stop-Loss

✅ Target 1 & Target 2

✅ MTF level comparison

✅ High-contrast color-coded SL (Red) + Targets (Green)

✅ Selected timeframe highlighted automatically

Designed for intraday traders, positional traders, and volatility-based strategies.

✅ How to Use It

✅ 1. Choose Entry Mode

Manual Entry ON → Type your entry price

Manual Entry OFF → Last candle close is used

The script calculates ATR(14) on:

Current chart timeframe

10-minute timeframe

15-minute timeframe

Then it uses standard volatility-based formulas:

Stop-Loss = Entry ± (ATR × SL Multiplier)

Target 1 = Entry ± (ATR × T1 Multiplier)

Target 2 = Entry ± (ATR × T2 Multiplier)

Direction depends on Long/Short mode.

You can switch which ATR timeframe becomes active (affecting plotted lines + alerts).

✅ Why This Indicator Is Useful

This script solves 3 common problems:

✅ 1. “How wide should my stop-loss be?”

ATR automatically adjusts the SL to market volatility.

✅ 2. “Which timeframe ATR should I trust?”

You can compare Chart, 10m, and 15m in one panel.

✅ 3. “The table is too big in other indicators.”

This is compact, clean, color-coded, and readable.

Happy Trading :)

Adaptive Jurik Filter Volatility Oscillator [Loxx]Adaptive Jurik Filter Volatility Oscillator uses Jurik Volty and Adaptive Double Jurik Filter Moving Average (AJFMA) to derive Jurik Filter smoothed volatility.

What is Jurik Volty?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

That's why investors, banks and institutions worldwide ask for the Jurik Research Moving Average ( JMA ). You may apply it just as you would any other popular moving average. However, JMA's improved timing and smoothness will astound you.

What is adaptive Jurik volatility?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

- UI options to color bars

(FVC) Fractal Volatility Compression (DAFE) (FVC) Fractal Volatility Compression

See the Market’s Volatility DNA.

The Fractal Volatility Compression (FVC) is a next-generation tool for traders who want to see volatility compression and expansion across multiple timeframes and volatility engines—not just price, but the very structure of volatility itself.

What Makes FVC Unique?

Dual-Engine Volatility:

Plots both classic price-based (Stdev) and meta-volatility (VoVix) compression/expansion, so you can see when the market is “coiling” or “exploding” on multiple levels.

Fractal, Multi-Timeframe Analysis:

Measures volatility on short, medium, and long timeframes, then normalizes each as a Z-score. The result: a true “coiled spring” detector that works on any asset, any timeframe.

Threshold Lines You Control:

Yellow center line: Your neutral baseline.

Green compression line: When crossed, the market is “spring-loading.”

Red expansion line: When crossed, volatility is breaking out.

All lines are solid, clean, and end before the dashboard for a professional look.

Agreement Fill: When both engines agree (both above or both below the center line), a bright fill highlights the zone—red for expansion, green for compression.

Signature Dashboard & Info Line:

Dashboard (right-middle) shows all Z-scores and FVC values, color-coded for instant clarity.

Compact info label for mobile or minimalist users.

Inputs & Customization

Thresholds: Set the yellow, green, and red lines to match your asset, timeframe, and risk tolerance.

Timeframes & Lengths: Tune the short, medium, and long volatility windows for your style.

Toggle Lines: Show/hide Stdev or VoVix FVC lines independently.

Dashboard & Info Line: Toggle for your workflow and screen size.

How to Use

Compression (below green): Market is “coiling” across timeframes—watch for explosive moves.

Expansion (above red): Volatility is breaking out—expect regime shifts or trend acceleration.

Agreement Fill: When both lines agree, the signal is strongest.

Not a Buy/Sell Signal: These are regime and structure signals—combine with your own

strategy and risk management.

Why should you use FVC?

See what others can’t:

Most tools show only one dimension of volatility. FVC reveals the fractal DNA of market compression and expansion. Works on any asset, any timeframe. Professional, clean, and fully customizable.

Fractal Volatility Compression (FVC):

Because the next big move is born in the market’s hidden compression.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

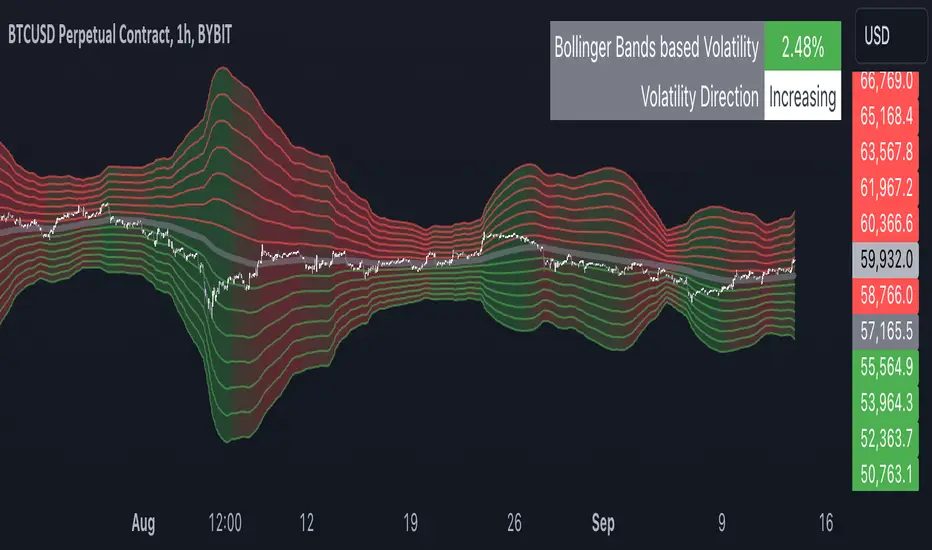

Multiple Bollinger Bands + Volatility [AlgoTraderPro]This indicator helps traders visualize price ranges and volatility changes. Designed to assist in identifying potential consolidation zones, the indicator uses multiple layers of Bollinger Bands combined with volatility-based shading. This can help traders spot periods of reduced price movement, which are often followed by breakouts or trend reversals.

█ FEATURES

Multiple Bollinger Bands: Displays up to seven bands with customizable standard deviations, providing a layered view of price range activity.

Volatility Measurement: Tracks changes in Bollinger Band width to display volatility percentage and direction (increasing, decreasing, or neutral).

Volatility Shading: Uses color-coded shading between the outermost bands to indicate changes in volatility, helping to visualize potential consolidation zones.

Customizable Inputs: Modify lookback periods, moving average lengths, and standard deviations for each band to tailor the analysis to your strategy.

Volatility Table: Displays a table on the chart showing real-time volatility data and direction for quick reference.

█ HOW TO USE

Add the Indicator: Apply it to your TradingView chart.

Adjust Settings: Customize the Bollinger Bands’ parameters to suit your trading timeframe and strategy.

Analyze Consolidation Zones: Use the multiple bands and volatility shading to identify areas of reduced price activity, signaling potential breakouts.

Monitor Volatility: Refer to the volatility table to track real-time shifts in market volatility.

Use in Different Markets: Adapt the settings for various assets and timeframes to assess market conditions effectively.

█ NOTES

• The indicator is useful in consolidating markets where price movement is limited, offering insights into potential breakout areas.

• Adjust the settings based on asset and market conditions for optimal results.

RaymondRatio [Qanexra] - Volatility with Doji Noise CancellationThe Problem with Standard Volatility: Most volatility indicators force a calculation on every single candle, regardless of quality. This means that during periods of market indecision (Dojis), your indicators are digesting "noise," leading to lag and false signals when the market finally moves.

The Solution: RaymondRatio Developed by Qanexra, the RaymondRatio is a sophisticated volatility gauge that introduces a proprietary "Doji Pause" mechanism. Instead of smoothing over noise, this indicator intelligently ignores it.

How It Works:

Volatility Engine: The core calculates the Raymond Trending value derived from a composite of short-term compare with the long-term volatility.

The Doji Pause: The indicator constantly monitors the Body-to-Range ratio of every candle. If a candle is detected as a Doji (indecision), the indicator freezes its calculation. It retains the last known "valid" volatility state.

The Ratio: The output is a ratio.

> 1.0: Volatility is expanding relative to the baseline (Active Market).

< 1.0: Volatility is compressing (Squeeze/Consolidation).

Key Features:

Smart Filtering: Background highlights in Gray indicate "Paused" zones where the market is undecided.

Clean Data: Prevents the baseline from being dragged down by low-quality price action.

Customizable Threshold: Users can define what constitutes a "Doji" (e.g., body is less than 30% of the range).

How to Trade: Use this as a filter for your existing strategy.

Green Light: When the Ratio is above 1.0 and rising, the market is in a valid expansion phase.

Red Light: When the Ratio is below 1.0 or "flatlining" during Doji Pauses, stay out of the market to avoid chop.

Multi-Timeframe Bias Dashboard + VolatilityWhat it is: A corner table (overlay) that gives a quick higher-timeframe read for Daily / 4H / 1H using EMA alignment, MACD, RSI, plus a volatility gauge.

How it works (per timeframe):

EMA block (50/100/200): “Above/Below/Mixed” based on price vs all three EMAs.

MACD: “Bullish/Bearish/Neutral” from MACD line vs Signal and histogram sign.

RSI: Prints the value and an ↑/↓ based on 50 line.

Volatility: Compares ATR(14) to its SMA over 20 bars → High (>*1.2), Normal, Low (<*0.8).

Bias: Combines three votes (EMA, MACD, RSI):

Bullish if ≥2 bullish, Bearish if ≥2 bearish, else Mixed.

Display:

Rows: D / 4H / 1H.

Columns: Bias, EMA(50/100/200), RSI, MACD, Volatility.

Bias cell is color-coded (green/red/gray).

Position setting lets you park the table in Top Right / Bottom Right / Bottom Left (works on mobile too).

Use it for:

Quickly aligning intraday setups with higher-TF direction.

Skipping low-volatility periods.

Confirming momentum (MACD/RSI) when price returns to your OB/FVG zones.

Chande Volatility-Based Trailing Stops This indicator is developed from a description outlined in the Chande - Kroll book, "The New Technical Trader". It is designed to help control risk by plotting two lines that function as long and short trailing stops.

How does it work?

"These stops are derived from recent highest high or lowest low. They adjust based on volatility. However, to avoid giving up a sizable chunk of profit before the stop is hit, it is modified in such a way that the stop can only advance with price, not retreat. This will lock in a greater portion of potential profits..."

Settings:

The default settings are those described in the book. They are described as being best for intermediate term trades. Use the multiplier to tighten or loosen the stop. A smaller multiplier will result in tighter stops. It is recommended to adjust this value for your preferred timeframe. You can toggle the trailing stop lines on or off as well as cross over marker.

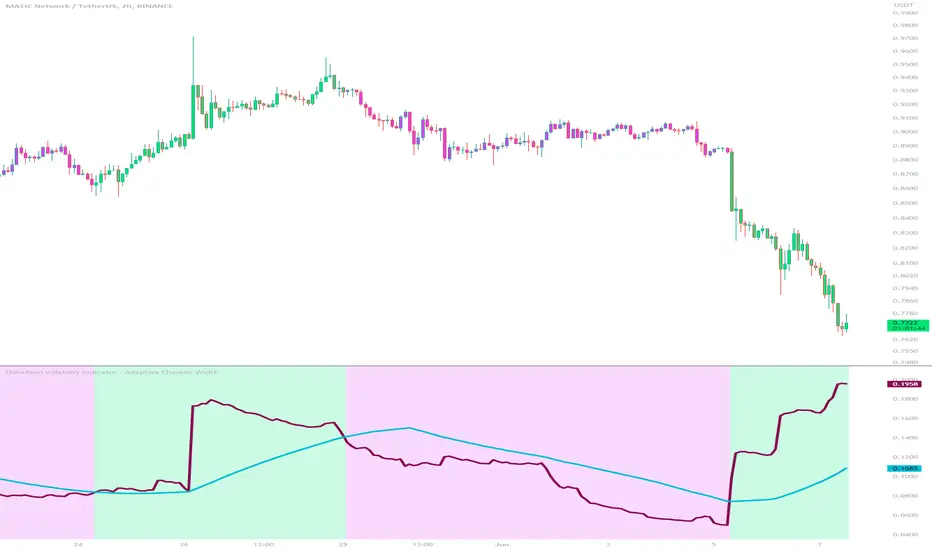

Donchian Volatility Indicator - Adaptive Channel WidthThis indicator is designed to help traders assess and analyze market volatility. By calculating the width of the Donchian channels, it provides valuable insights into the range of price movements over a specified period. This indicator helps traders identify periods of high and low volatility, enabling them to make more informed trading decisions.

The indicator is based on the concept of Donchian channels, which consist of the highest high and lowest low over a specified lookback period. The channel width is calculated as the difference between the upper and lower channels. A wider channel indicates higher volatility, suggesting potentially larger price movements and increased trading opportunities. On the other hand, a narrower channel suggests lower volatility, indicating a relatively calmer market environment with potentially fewer trading opportunities.

The adaptive aspect of the indicator refers to its ability to adjust the width of the channels dynamically based on market conditions. The indicator calculates the width of the channels using the Average True Range (ATR) indicator, which measures the average range of price movements over a specified period. By multiplying the ATR value with the user-defined ATR multiplier, the indicator adapts the width of the channels to reflect the current level of volatility. During periods of higher volatility, the channels expand to accommodate larger price movements, providing a broader range for assessing volatility. Conversely, during periods of lower volatility, the channels contract, reflecting the narrower price ranges and signaling a decrease in volatility. This adaptive nature allows traders to have a flexible and responsive measure of volatility, ensuring that the indicator reflects the current market conditions accurately.

To provide further insights, the indicator includes a signal line. The signal line is derived from the channel width and is calculated as a simple moving average over a specified signal period. This signal line acts as a reference level, allowing traders to compare the current channel width with the average width over a given time frame. By assessing whether the current channel width is above or below the signal line, traders can gain additional context on the volatility level in the market.

The colors used in the Donchian Volatility Indicator - Adaptive Channel Width play a vital role in visualizing the volatility levels:

-- Lime Color : When the channel width is above the signal line, it is colored lime. This color signifies that volatility has entered the market, indicating potentially higher price movements and increased trading opportunities. Traders can pay closer attention to the lime-colored channel width as it may suggest favorable conditions for trend-following or breakout trading strategies.

-- Fuchsia Color : When the channel width is below the signal line, it is colored fuchsia. This color represents relatively low volatility, suggesting a calmer market environment with potentially fewer trading opportunities. Traders may consider adjusting their strategies during periods of low volatility, such as employing range-bound or mean-reversion strategies.

-- Aqua Color : The signal line is represented by the aqua color. This color allows traders to easily identify the signal line amidst the channel width. The aqua color provides a visual reference for the average channel width and helps traders assess whether the current width is above or below this average.

The Donchian Volatility Indicator - Adaptive Channel Width has several practical applications for traders:

-- Volatility Assessment : Traders can use this indicator to assess the level of volatility in the market. By observing the width of the Donchian channels and comparing it to the signal line, they can determine whether the current volatility is relatively high or low. This information helps traders set appropriate expectations and adjust their trading strategies accordingly.

-- Breakout Trading : Wide channel widths may indicate an increased likelihood of price breakouts. Traders can use the Donchian Volatility Indicator - Adaptive Channel Width to identify potential breakout opportunities. When the channel width exceeds the signal line, it suggests a higher probability of significant price movements, potentially signaling a breakout. Traders may consider entering trades in the direction of the breakout.

-- Risk Management : The indicator can assist in setting appropriate stop-loss levels based on the current volatility. During periods of high volatility (lime-colored channel width), wider stop-loss orders may be warranted to account for larger price swings. Conversely, during periods of low volatility (fuchsia-colored channel width), narrower stop-loss orders may be appropriate to limit risk in a more range-bound market.

While the Donchian Volatility Indicator - Adaptive Channel Width is a valuable tool, it is important to consider its limitations:

-- Lagging Indicator : The indicator relies on historical price data, making it a lagging indicator. It provides insights based on past price movements and may not capture sudden changes or shifts in volatility. Traders should be aware that the indicator may not generate real-time signals and should be used in conjunction with other indicators and analysis tools.

-- False Signals : Like any technical indicator, the Donchian Volatility Indicator - Adaptive Channel Width is not immune to generating false signals. Traders should exercise caution and use additional analysis to confirm the signals generated by the indicator. Considering the broader market context and employing risk management techniques can help mitigate the impact of false signals.

-- Market Conditions : Market conditions can vary, and volatility levels can differ across different assets and timeframes. Traders should adapt their strategies and consider other market factors when interpreting the signals provided by the indicator. It is crucial to avoid relying solely on the indicator and to incorporate a comprehensive analysis of the market environment.

In conclusion, this indicator is a powerful tool for assessing market volatility. By examining the width of the Donchian channels and comparing it to the signal line, traders can gain insights into the level of volatility and adjust their trading strategies accordingly. The color-coded representation of the channel width and signal line allows for easy visualization and interpretation of the volatility dynamics. Traders should utilize this indicator as part of a broader trading approach, incorporating other technical analysis tools and considering market conditions for a comprehensive assessment of market volatility.

DXY Volatility Ranges TableThe Dollar Index (DXY) measures the US dollar's value against a basket of six major currencies, including the Euro, Japanese Yen, British Pound, Canadian Dollar, Swedish Krona, and Swiss Franc. Here are some key ranges for the DXY:

- Historical Highs and Lows:

- All-time high: 164.720 in February 1985

- All-time low: 70.698 on March 16, 2008

- Recent Trends:

- Current value: around 99.603 (as of December 5, 2025)

- 52-week high: 129.670 (November 8, 1985)

- 52-week low: 94.650 (projected target by some analysts)

- Volatility Ranges:

- Low volatility: DXY < 95

- Moderate volatility: DXY between 95-105

- High volatility: DXY > 105

- Support and Resistance Levels:

- Support: around 94.650 and 90.00

- Resistance: around 100.15/35 and 105.00

Uber VQ (Lite) - Volatility Quality Index [UTS]Name: Uber VQI (Lite) - Volatility Quality Index

Created: 2022/11/22

Copyright: © UberTradingSystems

Description:

The volatility quality index was first introduced by Thomas Stridsman in Technical Analysis of Stocks and Commodities magazine in the August 2002 edition.

This powerful indicator points out the difference between bad and good volatility in order to identify better trade opportunities in the market.

It is suggested to use this indicator as a confirmation signal together with the other indicators in your system.

Lite Version

Please note that this "Lite" version offers full functionality but is constrained to Euro / US-Dollar trading pairs only.

You can find it as "EURUSD" on many providers such as FXCM, Oanda, Capital.com, Currency.com etc.

If you like this indicator, consider checking out the original. More details under "Author's instructions" and "Signature" sections below.

General Usage

Stridsman suggested buying (or "to go long") when VQ has increased in the previous 10 bars and selling (or "to go short") when it has decreased in the previous 10 bars.

This indicator has been updated to reflect its modern iterations. One of the following signals are choosable trading signal generator:

VQ Sum

Short MA

Long MA

All three signal triggering conditions can selectively be drawn on the indicator for study and reference purposes.

In addition, generated buy and sell signals can be drawn on the indicator and are modifiable too.

Alerts

To allow alert notifications, generated signals are connected as selectable "Long Signal" and "Short Signal" to the indicator alerts.

The conditions can be found on the alert sections of the indicator.

In the menu right to the indicator name, press the three dots and select "Add alert on ...".

Under condition options select one of the following:

Long Signal

Short Signal

It is advised to select "Once per bar close" as alert execution option.

Moving Averages

To fine-tune the "Short MA" and "Long MA" calculation, 16 different Moving Averages are available to choose from:

ALMA (Arnaud Legoux Moving Average)

DEMA (Double Exponential Moving Average)

EMA (Exponential Moving Average)

FRAMA (Fractal Adaptive Moving Average)

HMA (Hull Moving Average)

JURIK (Jurik Moving Average)

KAMA (Kaufman Adaptive Moving Average)

Kijun (Kijun-sen / Tenkan-sen of Ichimoku)

LSMA (Least Square Moving Average)

RMA (Running Moving Average)

SMA (Simple Moving Average)

SuperSmoothed (Super Smoothed Moving Average)

TEMA (Triple Exponential Moving Average)

VWMA (Volume Weighted Moving Average)

WMA (Weighted Moving Average)

ZLEMA (Zero Lag Moving Average)

A freely determinable length allows for sensitivity adjustments that fit your own requirements.

Multi-Volatility Adjusted Moving Average🎯 Core Concept

The Multi-Volatility Adjusted Moving Average (MVAMA) is an advanced technical indicator that creates an adaptive moving average with a built-in upward bias. Unlike traditional moving averages that simply follow price, this indicator adjusts upward based on market volatility, making it particularly useful for identifying dynamic resistance levels and trend strength.

🔧 How It Works

Key Principle: Upward Volatility Bias

Base Calculation: Starts with your chosen moving average (EMA, SMA, etc.)

Volatility Measurement: Calculates market volatility using one of 5 different methods

Upward Adjustment: Always adds volatility adjustment upward: Adaptive MA = Base MA + Volatility Adjustment

Dynamic Resistance: Creates a moving resistance level that adapts to market conditions

📊 5 Volatility Calculation Methods

1. Simple (High-Low Range)

Method: (High - Low) / Close × 100

Best For: Clean, straightforward volatility measurement

Use Case: General purpose, all market conditions

2. Parkinson (Range-Based Log Volatility)

Method: √(ln(High/Low)²) with safety bounds

Best For: Intraday volatility without using open/close gaps

Use Case: Choppy markets, day trading

3. ATR (Average True Range)

Method: Traditional ATR as percentage of price

Best For: Handling gaps and limit moves

Use Case: Swing trading, gap-prone markets

4. Standard Deviation (Statistical)

Method: Standard deviation of price returns

Best For: Academic/statistical approach

Use Case: Backtesting, quantitative analysis

5. Garman-Klass (OHLC Optimized)

Method: 0.5×ln(H/L)² - (2ln2-1)×ln(C/O)²

Best For: Most comprehensive volatility using all OHLC data

Use Case: Professional trading, maximum accuracy

🎛️ 12 Moving Average Types

Fast & Responsive:

HMA (Hull): Minimal lag, very responsive

DEMA/TEMA: Double/Triple exponential for speed

WMA: Weighted for recent price emphasis

Balanced:

EMA: Classic exponential (default)

ALMA: Arnaud Legoux for balanced response

LSMA: Linear regression trend following

Smooth & Stable:

SMA: Simple moving average

SMMA/RMA: Smoothed for noise reduction

TRIMA: Triangular for maximum smoothness

VWMA: Volume-weighted for market participation

💡 Practical Applications

Trading Uses:

Dynamic Resistance: Acts as adaptive resistance level

Trend Strength: Higher volatility = stronger adjustment = more significant level

Entry Timing: Price touching the adaptive MA can signal rejection points

Risk Management: Volatility bands show market uncertainty

Market Analysis:

Low Volatility: Adaptive MA stays close to base MA (consolidation)

High Volatility: Adaptive MA moves significantly above base MA (trending/breakout)

Trend Confirmation: Sustained distance between price and adaptive MA shows trend strength

⚙️ Key Features

Risk Management:

Volatility Capping: Prevents extreme adjustments (default 15% max)

Safety Bounds: All calculations protected against infinite/NaN values

Parameter Limits: Sensible ranges for all inputs

Visualization Options:

Base MA Display: Show underlying moving average

Volatility Bands: Visual representation of volatility adjustment

Custom Colors: Professional color schemes

Clean Interface: Organized input groups

Professional Features:

Multi-timeframe Support: Works on any timeframe

Alert Framework: Ready-to-enable price crossover alerts

🎯 Ideal For:

Traders Who Want:

Dynamic support/resistance levels

Volatility-aware trend analysis

Adaptive position sizing based on market conditions

Professional-grade technical analysis tools

Market Conditions:

Trending Markets: Volatility creates meaningful resistance levels

Volatile Markets: Adaptive adjustment handles changing conditions

All Timeframes: From scalping to position trading

🔍 Unique Advantages:

Always Upward Bias: Unlike oscillating indicators, always provides clear directional bias

Multi-Volatility Support: Choose the best volatility method for your market/style

Comprehensive MA Library: 12 different moving average types

Built-in Risk Management: Prevents extreme values that break other indicators

Professional Implementation: Publication-ready code with proper documentation

This script transforms traditional moving averages into intelligent, volatility-aware tools that adapt to market conditions while maintaining a consistent upward bias for clear directional guidance.

HMA Gaussian Volatility AdjustedOverview

The "HMA Gaussian Volatility Adjusted" indicator introduces a unique combination of HMA smoothing with a Gaussian filter and two components to measure volatility (Average True Range (ATR) and Standard Deviation (SD)). This tool provides traders with a stable and accurate measure of price trends by integrating a Gaussian Filter smoothed using HMA with a customized calculation of volatility. This innovative approach allows for enhanced sensitivity to market fluctuations while filtering out short-term price noise.

Technical Composition and Calculation

The "HMA Gaussian Volatility Adjusted" indicator incorporates HMA smoothing and dynamic standard deviation calculations to build upon traditional volatility measures.

HMA & Gaussian Smoothing:

HMA Calculation (HMA_Length): The script applies a Hull Moving Average (HMA) to smooth the price data over a user-defined period, reducing noise and helping focus on broader market trends.

Gaussian Filter Calculation (Length_Gaussian): The smoothed HMA data is further refined by putting it into a Gaussian filter to incorporate a normal distribution.

Volatility Measurement:

ATR Calculation (ATR_Length, ATR_Factor): The indicator incorporates the Average True Range (ATR) to measure market volatility. The user-defined ATR multiplier is applied to this value to calculate upper and lower trend bands around the Gaussian, providing a dynamic measure of potential price movement based on recent volatility.

Standard Deviation Calculation (SD_Length): The script calculates the standard deviation of the price over a user-defined length, providing another layer of volatility measurement. The upper and lower standard deviation bands (SDD, SDU) act as additional indicators of price extremes.

Momentum Calculation & Scoring

When the indicator signals SHORT:

Diff = Price - Upper Boundary of the Standard Deviation (calculated on a Gaussian filter).

When the indicator signals LONG:

Diff = Price - Upper Boundary of the ATR (calculated on a Gaussian filter).

The calculated Diff signals how close the indicator is to changing trends. An EMA is applied to the Diff to smooth the data. Positive momentum occurs when the Diff is above the EMA, and negative momentum occurs when the Diff is below the EMA.

Trend Detection

Trend Logic: The indicator uses the calculated bands to identify whether the price is moving within or outside the standard deviation and ATR bands. Crosses above or below these bands, combined with positive/negative momentum, signals potential uptrends or downtrends, offering traders a clear view of market direction.

Features and User Inputs

The "HMA Gaussian Volatility Adjusted" script offers a variety of user inputs to customize the indicator to suit traders' styles and market conditions:

HMA Length: Allows traders to adjust the sensitivity of the HMA smoothing to control the amount of noise filtered from the price data.

Gaussian Length: Users can define the length at which the Gaussian filter is applied.

ATR Length and Multiplier: These inputs let traders fine-tune the ATR calculation, affecting the size of the dynamic upper and lower bands to adjust for price volatility.

Standard Deviation Length: Controls how the standard deviation is calculated, allowing further customization in detecting price volatility.

EMA Confluence: This input lets traders determine the length of the EMA used to calculate price momentum.

Type of Plot Setting: Allows users to determine how the indicator signal is plotted on the chart (Background color, Trend Lines, BOTH (backgroung color and Trend Lines)).

Transparency: Provides users with customization of the background color's transparency.

Color Long/Short: Offers users the option to choose their preferred colors for both long and short signals.

Summary and Usage Tips

The "HMA Gaussian Volatility Adjusted" indicator is a powerful tool for traders looking to refine their analysis of market trends and volatility. Its combination of HMA smoothing, Gaussian filtering, and standard deviation analysis provides a nuanced view of market movements by incorporating various metrics to determine direction, momentum, and volatility. This helps traders make better-informed decisions. It's recommended to experiment with the various input parameters to optimize the indicator for specific needs.

GKD-C Volatility-Adaptive Rapid RSI T3 [Loxx]Giga Kaleidoscope GKD-C Volatility-Adaptive Rapid RSI T3 is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-C Volatility-Adaptive Rapid RSI T3

Adaptive Momentum: Mastering Market Dynamics with Advanced RSI Techniques

The Volatility-Adaptive Rapid RSI T3 is a sophisticated technical indicator that combines the concepts of Rapid RSI, Volatility Adaptation, and T3 smoothing. This combination results in a more responsive, accurate, and adaptable momentum oscillator compared to the regular RSI.

The Rapid RSI is a variation of the RSI designed to provide faster and more responsive signals. It does this by modifying the way average gains and losses are calculated, using a simple moving average (SMA) instead of an exponential moving average (EMA). This makes the Rapid RSI more sensitive to recent price changes, allowing traders to identify overbought and oversold conditions more quickly.

Volatility adaptation is a concept that adjusts the parameters of an indicator based on the current market volatility. In the context of the Volatility-Adaptive Rapid RSI T3, the volatility is calculated using the standard deviation of price changes over a specified period. This value is then used to adjust the T3 smoothing period, making the indicator more adaptive to changing market conditions. When the market is volatile, the indicator will respond more quickly to price changes, while in less volatile markets, the indicator will be less sensitive, reducing the likelihood of false signals.

T3 smoothing, developed by Tim Tilson, is a powerful and flexible moving average technique that aims to reduce lag and improve the responsiveness of an indicator. It utilizes a combination of multiple exponential moving averages with varying degrees of weighting to create a smoother and more accurate representation of the underlying data. The T3 smoothing method is applied to the price data before the Rapid RSI calculation, enhancing the overall responsiveness of the indicator.

By combining these three concepts, the Volatility-Adaptive Rapid RSI T3 offers several advantages over the regular RSI:

1. Faster and more responsive signals: The Rapid RSI and T3 smoothing components allow the indicator to respond more quickly to price changes, potentially leading to earlier entry and exit points.

2. Adaptability to market conditions: The volatility adaptation feature enables the indicator to adjust its sensitivity based on the current market volatility. This helps to reduce false signals in less volatile markets and increase responsiveness in more volatile markets.

2. Smoother representation of price data: The T3 smoothing technique provides a more accurate and smoother representation of the underlying data, making it easier to identify trends and potential reversals.

In conclusion, the Volatility-Adaptive Rapid RSI T3 is a powerful technical indicator that offers several improvements over the regular RSI. Its responsiveness, adaptability, and smoothing capabilities make it a valuable tool for traders seeking to identify overbought and oversold conditions more accurately. However, it is essential to remember that no indicator is perfect, and using the Volatility-Adaptive Rapid RSI T3 in conjunction with other technical indicators and analysis tools can provide more reliable trading signals.

Additional Features

This indicator allows you to select from 33 source types. They are as follows:

Close

Open

High

Low

Median

Typical

Weighted

Average

Average Median Body

Trend Biased

Trend Biased (Extreme)

HA Close

HA Open

HA High

HA Low

HA Median

HA Typical

HA Weighted

HA Average

HA Average Median Body

HA Trend Biased

HA Trend Biased (Extreme)

HAB Close

HAB Open

HAB High

HAB Low

HAB Median

HAB Typical

HAB Weighted

HAB Average

HAB Average Median Body

HAB Trend Biased

HAB Trend Biased (Extreme)

What are Heiken Ashi "better" candles?

Heiken Ashi "better" candles are a modified version of the standard Heiken Ashi candles, which are a popular charting technique used in technical analysis. Heiken Ashi candles help traders identify trends and potential reversal points by smoothing out price data and reducing market noise. The "better formula" was proposed by Sebastian Schmidt in an article published by BNP Paribas in Warrants & Zertifikate, a German magazine, in August 2004. The aim of this formula is to further improve the smoothing of the Heiken Ashi chart and enhance its effectiveness in identifying trends and reversals.

Standard Heiken Ashi candles are calculated using the following formulas:

Heiken Ashi Close = (Open + High + Low + Close) / 4

Heiken Ashi Open = (Previous Heiken Ashi Open + Previous Heiken Ashi Close) / 2

Heiken Ashi High = Max (High, Heiken Ashi Open, Heiken Ashi Close)

Heiken Ashi Low = Min (Low, Heiken Ashi Open, Heiken Ashi Close)

The "better formula" modifies the standard Heiken Ashi calculation by incorporating additional smoothing, which can help reduce noise and make it easier to identify trends and reversals. The modified formulas for Heiken Ashi "better" candles are as follows:

Better Heiken Ashi Close = (Open + High + Low + Close) / 4

Better Heiken Ashi Open = (Previous Better Heiken Ashi Open + Previous Better Heiken Ashi Close) / 2

Better Heiken Ashi High = Max (High, Better Heiken Ashi Open, Better Heiken Ashi Close)

Better Heiken Ashi Low = Min (Low, Better Heiken Ashi Open, Better Heiken Ashi Close)

Smoothing Factor = 2 / (N + 1), where N is the chosen period for smoothing

Smoothed Better Heiken Ashi Open = (Better Heiken Ashi Open * Smoothing Factor) + (Previous Smoothed Better Heiken Ashi Open * (1 - Smoothing Factor))

Smoothed Better Heiken Ashi Close = (Better Heiken Ashi Close * Smoothing Factor) + (Previous Smoothed Better Heiken Ashi Close * (1 - Smoothing Factor))

The smoothed Better Heiken Ashi Open and Close values are then used to calculate the smoothed Better Heiken Ashi High and Low values, resulting in "better" candles that provide a clearer representation of the market trend and potential reversal points.

It's important to note that, like any other technical analysis tool, Heiken Ashi "better" candles are not foolproof and should be used in conjunction with other indicators and analysis techniques to make well-informed trading decisions.

Heiken Ashi "better" candles, as mentioned previously, provide a clearer representation of market trends and potential reversal points by reducing noise and smoothing out price data. When using these candles in conjunction with other technical analysis tools and indicators, traders can gain valuable insights into market behavior and make more informed decisions.

To effectively use Heiken Ashi "better" candles in your trading strategy, consider the following tips:

Trend Identification: Heiken Ashi "better" candles can help you identify the prevailing trend in the market. When the majority of the candles are green (or another color, depending on your chart settings) and there are no or few lower wicks, it may indicate a strong uptrend. Conversely, when the majority of the candles are red (or another color) and there are no or few upper wicks, it may signal a strong downtrend.

Trend Reversals: Look for potential trend reversals when a change in the color of the candles occurs, especially when accompanied by longer wicks. For example, if a green candle with a long lower wick is followed by a red candle, it could indicate a bearish reversal. Similarly, a red candle with a long upper wick followed by a green candle may suggest a bullish reversal.

Support and Resistance: You can use Heiken Ashi "better" candles to identify potential support and resistance levels. When the candles are consistently moving in one direction and then suddenly change color with longer wicks, it could indicate the presence of a support or resistance level.

Stop-Loss and Take-Profit: Using Heiken Ashi "better" candles can help you manage risk by determining optimal stop-loss and take-profit levels. For instance, you can place your stop-loss below the low of the most recent green candle in an uptrend or above the high of the most recent red candle in a downtrend.

Confirming Signals: Heiken Ashi "better" candles should be used in conjunction with other technical indicators, such as moving averages, oscillators, or chart patterns, to confirm signals and improve the accuracy of your analysis.

In this implementation, you have the choice of AMA, KAMA, or T3 smoothing. These are as follows:

Kaufman Adaptive Moving Average (KAMA)

The Kaufman Adaptive Moving Average (KAMA) is a type of adaptive moving average used in technical analysis to smooth out price fluctuations and identify trends. The KAMA adjusts its smoothing factor based on the market's volatility, making it more responsive in volatile markets and smoother in calm markets. The KAMA is calculated using three different efficiency ratios that determine the appropriate smoothing factor for the current market conditions. These ratios are based on the noise level of the market, the speed at which the market is moving, and the length of the moving average. The KAMA is a popular choice among traders who prefer to use adaptive indicators to identify trends and potential reversals.

Adaptive Moving Average

The Adaptive Moving Average (AMA) is a type of moving average that adjusts its sensitivity to price movements based on market conditions. It uses a ratio between the current price and the highest and lowest prices over a certain lookback period to determine its level of smoothing. The AMA can help reduce lag and increase responsiveness to changes in trend direction, making it useful for traders who want to follow trends while avoiding false signals. The AMA is calculated by multiplying a smoothing constant with the difference between the current price and the previous AMA value, then adding the result to the previous AMA value.

T3

The T3 moving average is a type of technical indicator used in financial analysis to identify trends in price movements. It is similar to the Exponential Moving Average (EMA) and the Double Exponential Moving Average (DEMA), but uses a different smoothing algorithm.

The T3 moving average is calculated using a series of exponential moving averages that are designed to filter out noise and smooth the data. The resulting smoothed data is then weighted with a non-linear function to produce a final output that is more responsive to changes in trend direction.

The T3 moving average can be customized by adjusting the length of the moving average, as well as the weighting function used to smooth the data. It is commonly used in conjunction with other technical indicators as part of a larger trading strategy.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v1.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data between modules. Data is passed between each module as described below:

GKD-B => GKD-V => GKD-C(1) => GKD-C(2) => GKD-C(Continuation) => GKD-E => GKD-BT

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Strategy with 1-3 take profits, trailing stop loss, multiple types of PnL volatility, and 2 backtesting styles

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Volatility-Adaptive Rapid RSI T3 as shown on the chart above

Confirmation 2: Williams Percent Range

Continuation: Volatility-Adaptive Rapid RSI T3

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD protocol chain.

Giga Kaleidoscope Modularized Trading System Signals (based on the NNFX algorithm)

Standard Entry

1. GKD-C Confirmation 1 Signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Continuation Entry

1. Standard Entry, Baseline Entry, or Pullback; entry triggered previously

2. GKD-B Baseline hasn't crossed since entry signal trigger

3. GKD-C Confirmation Continuation Indicator signals

4. GKD-C Confirmation 1 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 2 agrees

1-Candle Rule Standard Entry

1. GKD-C Confirmation 1 signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

1-Candle Rule Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

1-Candle Rule Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close)

2. GKD-B Volatility/Volume agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

PullBack Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is beyond 1.0x Volatility of Baseline

Next Candle:

1. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

2. GKD-C Confirmation 1 agrees

3. GKD-C Confirmation 2 agrees

4. GKD-V Volatility/Volume Agrees

]█ Setting up the GKD

The GKD system involves chaining indicators together. These are the steps to set this up.

Use a GKD-C indicator alone on a chart

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

Use a GKD-V indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Use a GKD-B indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Baseline (Baseline, Backtest)

1. Import the GKD-B Baseline into the GKD-BT Backtest: "Input into Volatility/Volume or Backtest (Baseline testing)"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline"

Volatility/Volume (Volatility/Volume, Backte st)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Solo"

2. Inside the GKD-V indicator, change the "Signal Type" setting to "Crossing" (neither traditional nor both can be backtested)

3. Import the GKD-V indicator into the GKD-BT Backtest: "Input into C1 or Backtest"