ZS Master Vision Pro - Advanced Multi-Timeframe Trading SystemZS MASTER VISION PRO - PROFESSIONAL TRADING SUITE

Created by Zakaria Safri

A comprehensive, all-in-one trading system combining multiple proven technical analysis methods into a single, powerful indicator. Designed for traders who demand precision, clarity, and actionable signals across all timeframes.

KEY FEATURES

CORE TREND ALGORITHM

Adaptive ATR-based trend detection with dynamic support and resistance zones. Features Type A and Type B signal modes for different trading styles, strong signal detection in key reversal zones, and optional EMA source smoothing for noise reduction.

MULTI-LAYER EMA CLOUD SYSTEM

Five customizable EMA cloud layers for multi-timeframe analysis with theme-adaptive color coding across five professional themes. Optional line display for detailed MA tracking with configurable periods from scalping to position trading.

WAVE TREND OSCILLATOR

Advanced momentum oscillator with channel-based calculations featuring smart reversal detection at extreme overbought and oversold levels. Includes directional strength confirmation and customizable sensitivity with adjustable reaction periods.

DIVERGENCE SCANNER

Detects four types of divergence automatically:

- Regular Bullish: Price making lower lows while oscillator making higher lows

- Regular Bearish: Price making higher highs while oscillator making lower highs

- Hidden Bullish: Trend continuation signals in uptrends

- Hidden Bearish: Trend continuation signals in downtrends

Automatic fractal-based detection with clear visual labels on chart.

MARKET BIAS INDICATOR

Heikin Ashi-based trend strength analysis with real-time bias calculation showing Bullish or Bearish combined with Strong or Weak conditions. Smoothed for cleaner signals and perfect for trend confirmation.

MOMENTUM SYSTEM

Proprietary momentum calculation using adaptive smoothing with growing and falling state detection. Normalized values for consistent interpretation and responsive to rapid market changes.

DYNAMIC SUPPORT AND RESISTANCE

Automatic pivot-based support and resistance level detection with adjustable left and right bar lookback. Non-repainting levels with visual clarity through color-coded lines.

LIVE INFORMATION DASHBOARD

Real-time market analysis panel displaying current trend direction, market bias based on Heikin Ashi, Wave Trend status and value, and momentum trend with state. Customizable display options with theme-adaptive colors.

VISUAL CUSTOMIZATION

FIVE PROFESSIONAL COLOR THEMES:

Pro - Modern green and red color scheme (default)

Classic - Traditional teal and red combination

Cyberpunk - Neon cyan and magenta contrast

Ocean - Blue and orange contrast

Sunset - Gold and red warmth

SIGNAL STYLES:

Labels with emoji indicators (BUY with rocket, SELL with bear, STRONG with lightning)

Arrows for clean minimal appearance

Triangles for classic approach

DISPLAY OPTIONS:

Color-coded candles following trend direction

Trend background highlighting for instant trend recognition

Optional EMA line display for detailed analysis

Adjustable transparency levels for personal preference

SMART ALERTS

Pre-configured alert conditions for all major signals:

Buy signals for standard entry opportunities

Sell signals for standard exit or short opportunities

Strong buy signals for high-confidence long entries

Strong sell signals for high-confidence short entries

Bullish divergence detection alerts

Bearish divergence detection alerts

Alert messages automatically include ticker symbol, current price, and specific signal type for quick decision making.

HOW TO USE

FOR TREND TRADERS:

Enable EMA Clouds with focus on Cloud 5 featuring 50 and 200 period moving averages. Wait for trend background color change to confirm direction. Enter on STRONG signals aligned with higher timeframe trend direction. Use support and resistance levels for strategic exits.

FOR SWING TRADERS:

Enable Wave Trend Oscillator information display. Look for oversold and overbought reversal setups. Confirm potential reversals with divergence scanner. Enter on smart reversal signals with proper risk management.

FOR SCALPERS:

Use Type B signal mode for more frequent trading signals. Enable Cloud 1 with 5 and 13 periods for quick trend confirmation. Focus on momentum growing and falling states for entry timing. Take quick entries on regular buy and sell signals.

FOR POSITION TRADERS:

Use Type A mode with higher ATR multiplier set to 3.0 or above. Enable only Cloud 5 with 50 and 200 periods for major trend confirmation. Only take STRONG signals for highest probability setups. Hold positions through minor pullbacks and noise.

RECOMMENDED SETTINGS

STOCKS ON DAILY TIMEFRAME:

Trend Period: 180

ATR Period: 155

ATR Multiplier: 2.1

Signal Mode: Type A

FOREX ON HOURLY AND 4-HOUR TIMEFRAMES:

Trend Period: 150

ATR Period: 120

ATR Multiplier: 2.5

Signal Mode: Type A

CRYPTOCURRENCY ON 15-MINUTE AND 1-HOUR TIMEFRAMES:

Trend Period: 100

ATR Period: 80

ATR Multiplier: 3.0

Signal Mode: Type B

SCALPING ON 1-MINUTE AND 5-MINUTE TIMEFRAMES:

Trend Period: 50

ATR Period: 40

ATR Multiplier: 2.0

Signal Mode: Type B

WHAT IS INCLUDED

Trend Analysis using ATR-based adaptive algorithm

Five EMA Cloud Layers for multi-timeframe confluence

Wave Trend Oscillator for momentum and reversal detection

Divergence Scanner detecting four types of divergence

Market Bias using Heikin Ashi-based trend strength

Momentum System with advanced momentum tracking

Support and Resistance Levels with automatic pivot detection

Live Dashboard showing real-time market analysis

Smart Alerts featuring six pre-configured alert types

Five Color Themes offering professional visual options

TECHNICAL DETAILS

CALCULATION METHODS:

Average True Range (ATR) for volatility adaptation

Exponential Moving Average (EMA) and Simple Moving Average (SMA) for trend smoothing

Wave Trend channel oscillator for momentum analysis

Fractal-based divergence detection algorithm

Heikin Ashi transformation for bias calculation

Logarithmic momentum calculation for precision

PERFORMANCE CHARACTERISTICS:

Optimized for maximum speed and efficiency

No repainting signals ensuring reliability

Works on all timeframes from 1 minute to monthly

Compatible with all instruments including stocks, forex, crypto, and futures

RISK DISCLAIMER

This indicator is a technical analysis tool and should not be used as the sole basis for trading decisions. Always use proper risk management and never risk more than you can afford to lose. Combine with other analysis methods and practice on demo accounts first. Past performance does not guarantee future results. Trading carries substantial risk and is not suitable for all investors.

SUPPORT AND UPDATES

Regular updates and continuous improvements

Based on proven technical analysis principles

Developed following Pine Coders best practices and standards

Clean, well-documented, and optimized code structure

WHY CHOOSE ZS MASTER VISION PRO

All-in-one solution eliminating the need for multiple indicators

Highly customizable to adapt to your specific trading style

Professional grade analysis with institutional-quality standards

Clean interface that is not cluttered or confusing

Works everywhere across all markets and all timeframes

Smart signals filtered for quality over quantity

Beautiful design featuring five professional color themes

Active development with regular improvements and updates

Transform your trading with ZS Master Vision Pro today.

Version 2.0 | Created by Zakaria Safri | Pine Script Version 5

ابحث في النصوص البرمجية عن "algo"

T3 [DCAUT]█ T3

📊 INDICATOR OVERVIEW

The T3 Moving Average is a smoothing indicator developed by Tim Tillson and published in Technical Analysis of Stocks & Commodities magazine (January 1998). The algorithm applies Generalized DEMA (Double Exponential Moving Average) recursively three times, creating a six-pole filtering effect that aims to balance noise reduction with responsiveness while minimizing lag relative to price changes.

📐 MATHEMATICAL FOUNDATION

Generalized DEMA (GD) Function:

The core building block is the Generalized DEMA function, which combines two exponential moving averages with weights controlled by the volume factor:

GD(input, v) = EMA(input) × (1 + v) - EMA(EMA(input)) × v

Where v is the volume factor parameter (default 0.7). This weighted combination reduces lag while maintaining smoothness by extrapolating beyond the first EMA using the double-smoothed EMA as a reference.

T3 Calculation Process:

T3 applies the GD function three times recursively:

T3 = GD(GD(GD(Price, v), v), v)

This triple nesting creates a six-pole smoothing effect (each GD applies two EMA operations, resulting in 2 × 3 = 6 total EMA calculations). The cascading refinement progressively filters noise while preserving trend information.

Step-by-Step Breakdown:

First GD application: GD1 = EMA(Price) × (1 + v) - EMA(EMA(Price)) × v - Creates initial smoothed series with lag reduction

Second GD application: GD2 = EMA(GD1) × (1 + v) - EMA(EMA(GD1)) × v - Further refines the smoothing while maintaining responsiveness

Third GD application: T3 = EMA(GD2) × (1 + v) - EMA(EMA(GD2)) × v - Final refinement produces the T3 output

Volume Factor Impact:

The volume factor (v) is the key parameter controlling the balance between smoothness and responsiveness. Tim Tillson recommended v = 0.7 as the optimal default value.

Lower volume factors (v closer to 0.0): Increase the extrapolation effect, making T3 more responsive to price changes but potentially more sensitive to noise.

Higher volume factors (v closer to 1.0): Reduce the extrapolation effect, producing smoother output with less sensitivity to short-term fluctuations but slightly more lag.

The recursive application of the volume factor through three GD stages creates a nonlinear filtering effect that achieves superior lag reduction compared to traditional moving averages of equivalent smoothness.

📊 SIGNAL INTERPRETATION

Trend Direction Signals:

Green Line (T3 Rising): Smoothed trend line is rising, may indicate uptrend, consider bullish opportunities when confirmed by other factors

Red Line (T3 Falling): Smoothed trend line is falling, may indicate downtrend, consider bearish opportunities when confirmed by other factors

Gray Line (T3 Flat): Smoothed trend line is flat, indicates unclear trend or consolidation phase

Price Crossover Signals:

Price Crosses Above T3: Price breaks above smoothed trend line, may be bullish signal, requires confirmation from other indicators

Price Crosses Below T3: Price breaks below smoothed trend line, may be bearish signal, requires confirmation from other indicators

Price Position Relative to T3: Price sustained above T3 may indicate uptrend, sustained below may indicate downtrend

Supporting Analysis Signals:

T3 Slope Angle: Steeper slopes indicate stronger trend momentum, flatter slopes suggest weakening trends

Price Deviation: Significant price separation from T3 may indicate overextension, watch for pullback or reversal

Dynamic Support/Resistance: T3 line can serve as dynamic support (in uptrends) or resistance (in downtrends) reference

🎯 STRATEGIC APPLICATIONS

Common Usage Patterns:

The T3 Moving Average can be incorporated into trading analysis in various ways. These represent common approaches used by market participants, though effectiveness varies by market conditions and requires individual testing:

Trend Filtering:

T3 can be used as a trend filter by observing the relationship between price and the T3 line. The color-coded slope (green for rising, red for falling, gray for sideways) provides visual feedback about the current trend direction of the smoothed series.

Price Crossover Analysis:

Some traders monitor crossovers between price and the T3 line as potential indication points. When price crosses the T3 line, it may suggest a change in the relationship between current price action and the smoothed trend.

Multi-Timeframe Observation:

T3 can be applied to multiple timeframes simultaneously. Observing alignment or divergence between different timeframe T3 indicators may provide context about trend consistency across time scales.

Dynamic Reference Level:

The T3 line can serve as a dynamic reference level for price action analysis. Price distance from T3, price reactions when approaching T3, and the behavior of price relative to the T3 line can all be incorporated into market analysis frameworks.

Application Considerations:

Any trading application should be thoroughly tested on historical data before implementation

T3 performance characteristics vary across different market conditions and asset types

The indicator provides smoothed trend information but does not predict future price movements

Combining T3 with other analytical tools and market context improves analysis quality

Risk management practices remain essential regardless of the analytical approach used

📋 DETAILED PARAMETER CONFIGURATION

Source Selection:

Close Price (Default): Standard choice for end-of-period trend analysis, reduces intrabar noise

HL2 (High+Low)/2: Provides balanced view of price action, considers full bar range

HLC3 or OHLC4: Incorporates more price information, may provide smoother results

Selection Impact: Different sources affect signal timing and smoothness characteristics

Length Configuration:

Shorter periods: More responsive, faster reaction, frequent signals, but higher false signal risk in choppy markets

Longer periods: Smoother output, fewer signals, better for long-term trends, but slower response

Default 14 periods is a common baseline, but optimal length varies by asset, timeframe, and market conditions

Parameter selection should be determined through backtesting rather than general recommendations

Volume Factor Configuration:

Lower values (closer to 0.0): Increase responsiveness but also noise sensitivity

Higher values (closer to 1.0): Increase smoothness but slightly more lag

Default 0.7 (Tim Tillson's recommendation) provides good balance for most applications

Optimal value depends on signal frequency versus reliability preference, test for specific use case

Parameter Optimization Approach:

There are no universal "best" parameter values - optimal settings depend on the specific asset, timeframe, market regime, and trading strategy

Start with default values (Length: 14, Volume Factor: 0.7) and adjust based on observed performance in your target market

Conduct systematic backtesting across different market conditions to evaluate parameter sensitivity

Consider that parameters optimized for historical data may not perform identically in future market conditions

Monitor performance and be prepared to adjust parameters as market characteristics evolve

📈 DESIGN FEATURES & MARKET ADAPTATION

Algorithm Design Features:

Simple Moving Average (SMA): Equal weighting across lookback period

Exponential Moving Average (EMA): Exponentially decreasing weights on historical prices

T3 Moving Average: Recursive Generalized DEMA with adjustable volume factor

Market Condition Adaptation:

Trending markets: Smoothed indicators generally align more closely with sustained directional movement

Ranging markets: All moving averages may generate more crossover signals during non-trending periods

Volatile conditions: Higher smoothing parameters reduce short-term sensitivity but increase lag

Indicator behavior relative to market conditions should be evaluated for specific applications

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. The T3 Moving Average has limitations and should not be used as the sole basis for trading decisions. Like all trend-following indicators, its performance varies with market conditions, and past signal characteristics do not guarantee future results.

Key Points:

T3 is a lagging indicator that responds to price changes rather than predicting future movements

Signals should be confirmed with other technical tools and market context

Parameters should be optimized for specific market and timeframe

Risk management and position sizing are essential

Market regime changes can affect indicator effectiveness

Test strategies thoroughly on historical data before live implementation

Consider broader market context and fundamental factors

MAMA [DCAUT]█ MAMA (MESA Adaptive Moving Average)

📊 OVERVIEW

The MESA Adaptive Moving Average (MAMA) represents an advanced implementation of John F. Ehlers' adaptive moving average system using the Hilbert Transform Discriminator. This indicator automatically adjusts to market cycles, providing superior responsiveness compared to traditional fixed-period moving averages while maintaining smoothness.

MAMA dynamically calculates two lines: the fast-adapting MAMA line and the following FAMA (Following Adaptive Moving Average) line. The system's core strength lies in its ability to automatically detect and adapt to the dominant market cycle, reducing lag during trending periods while providing stability during consolidation phases.

🎯 CORE CONCEPTS

Signal Interpretation:

• MAMA above FAMA: Indicates bullish trend momentum with the fast line leading upward movement

• MAMA below FAMA: Suggests bearish trend momentum with the fast line leading downward movement

• Golden Cross: MAMA crossing above FAMA signals potential upward momentum shift

• Death Cross: MAMA crossing below FAMA indicates potential downward momentum shift

• Line Convergence: MAMA and FAMA approaching each other suggests trend consolidation or potential reversal

Primary Applications:

• Trend Following: Enhanced responsiveness to trend changes compared to traditional moving averages

• Crossover Signals: MAMA/FAMA crossovers for identifying potential entry and exit points

• Cycle Analysis: Automatic adaptation to market's dominant cycle characteristics

• Reduced Lag: Minimized delay in trend detection while maintaining signal smoothness

📐 MATHEMATICAL FOUNDATION

Hilbert Transform Discriminator Technology:

The MAMA system employs John F. Ehlers' Hilbert Transform Discriminator, a sophisticated signal processing technique borrowed from telecommunications engineering. The Hilbert Transform creates a complex representation of the price series by generating a 90-degree phase-shifted version of the original signal, enabling precise cycle measurement.

The discriminator analyzes the instantaneous phase relationships between the original price series and its Hilbert Transform counterpart. This mathematical relationship reveals the dominant cycle period present in the market data at each point in time, forming the foundation for adaptive smoothing.

Instantaneous Period Calculation:

The algorithm computes the instantaneous period using the arctangent of the ratio between the Hilbert Transform and the original price series. This calculation produces a real-time measurement of the market's dominant cycle, typically ranging from short-term noise cycles to longer-term trend cycles.

The instantaneous period measurement undergoes additional smoothing to prevent erratic behavior from single-bar anomalies. This smoothed period value becomes the basis for calculating the adaptive alpha coefficient that controls the moving average's responsiveness.

Dynamic Alpha Coefficient System:

The adaptive alpha calculation represents the core mathematical innovation of MAMA. The alpha coefficient is derived from the instantaneous period measurement and constrained within the user-defined fast and slow limits.

The mathematical relationship converts the measured cycle period into an appropriate smoothing factor: shorter detected cycles result in higher alpha values (increased responsiveness), while longer cycles produce lower alpha values (increased stability). This creates an automatic adaptation mechanism that responds to changing market conditions.

MAMA/FAMA Calculation Process:

The MAMA line applies the dynamically calculated alpha coefficient to an exponential moving average formula: MAMA = alpha × Price + (1 - alpha) × MAMA . The FAMA line then applies a secondary smoothing operation to the MAMA line, creating a following average that provides confirmation signals.

This dual-line approach ensures that the fast-adapting MAMA line captures trend changes quickly, while the FAMA line offers a smoother confirmation signal, reducing the likelihood of acting on temporary price fluctuations.

Cycle Detection Mechanism:

The underlying cycle detection employs quadrature components derived from the Hilbert Transform to measure both amplitude and phase characteristics of price movements. This allows the system to distinguish between genuine trend changes and temporary price noise, automatically adjusting the smoothing intensity accordingly.

The mathematical framework ensures that during strong trending periods with clear directional movement, the algorithm reduces smoothing to minimize lag. Conversely, during consolidation phases with mixed signals, increased smoothing helps filter out false breakouts and whipsaws.

📋 PARAMETER CONFIGURATION

Source Selection Strategy:

• HL2 (High+Low)/2 (Default): Recommended for cycle analysis as it represents the midpoint of each period's trading range, reducing impact of opening gaps and closing spikes

• Close Price: Traditional choice reflecting final market sentiment, suitable for end-of-day analysis

• HLC3 (High+Low+Close)/3: Balanced approach incorporating range information with closing emphasis

• OHLC4 (Open+High+Low+Close)/4: Most comprehensive price representation for complete market view

Fast Limit Configuration (Default 0.5):

Controls the maximum responsiveness of the adaptive system. Higher values increase sensitivity to recent price changes but may introduce more noise. This parameter sets the upper bound for the dynamic alpha calculation.

Slow Limit Configuration (Default 0.05):

Determines the minimum responsiveness, providing stability during uncertain market conditions. Lower values increase smoothing but may cause delayed signals. This parameter sets the lower bound for the dynamic alpha calculation.

Parameter Relationship Considerations:

The fast and slow limits work together to define the adaptive range. The wider the range between these limits, the more dramatic the adaptation between trending and consolidating market conditions. Different market characteristics may benefit from different parameter configurations, requiring individual testing and validation.

📊 COLOR CODING SYSTEM

Line Visualization:

• Green Line (MAMA): The fast-adapting moving average that responds quickly to price changes

• Red Line (FAMA): The following adaptive moving average that provides confirmation signals

The fixed color scheme provides consistent visual identification of each line, enabling clear differentiation between the fast-adapting MAMA and the following FAMA throughout all market conditions.

💡 CORE VALUE PROPOSITION

Advantages Over Traditional Moving Averages:

• Cycle Adaptation: Automatically adjusts to market's dominant cycle rather than using fixed periods

• Reduced Lag: Faster response to genuine trend changes while filtering market noise

• Mathematical Foundation: Based on advanced signal processing techniques from telecommunications engineering

• Dual-Line System: Provides both fast adaptation (MAMA) and confirmation (FAMA) in one indicator

Comparative Performance Characteristics:

Unlike fixed-period moving averages that apply the same smoothing regardless of market conditions, MAMA adapts its behavior based on current market cycle characteristics. This may help reduce whipsaws during consolidation periods while maintaining responsiveness during trending phases.

Usage Considerations:

This indicator is designed for technical analysis purposes. The adaptive nature means that parameter optimization should consider the specific characteristics of the asset and timeframe being analyzed. Like all technical indicators, MAMA should be used as part of a comprehensive analysis approach rather than as a standalone signal generator.

Alert Functionality:

The indicator includes alert conditions for MAMA/FAMA crossovers, enabling automated notification of potential momentum shifts. These alerts can assist in timing analysis but should be combined with other forms of market analysis for decision-making purposes.

Señales de Compra/Venta - KUSKUS + MACD AlgoAlphaseñales de compra/venta con base en la alineación de dos indicadores

Chimera [theUltimator5]In myth, the chimera is an “impossible” hybrid—lion, goat, and serpent fused into one—striking to look at and formidable in presence. The word has come to mean a beautiful, improbable union of parts that shouldn’t work together, yet do.

Chimera is a dual-mode market context tool that blends a multi-input oscillator with classic ADX/DI trend strength, plus optional multi-timeframe “gap-line” tracking. Use it to visualize regime (trend vs. range), momentum swings around an adaptive midline, and higher timeframe (HTF) reference levels that auto-terminate on touch/cross.

Modes

1) Oscillator view

A smoothed composite of five common inputs—RSI, MACD (oscillator), Bollinger position, Stochastic, and an ATR/DI-weighted bias. Each is normalized to a comparable 0–100 style scale, averaged, and plotted as a candle-style oscillator (short vs. long smoothing, wickless for clarity). A dynamic midline with standard-deviation bands frames neutral → bearish/bullish zones. Colors ramp from neutral to your chosen Oversold/Overbought endpoints; consolidation can override to white.

Here is a description of the (5) signals used to calculate the sentiment oscillator:

RSI (14): Measures recent momentum by comparing average gains vs. losses. High = strength after advances; low = weakness after declines. (Z-score normalized to 0–100.)

MACD oscillator (12/26/9): Uses the difference between MACD and its signal (histogram) to gauge momentum shifts. Positive = bullish tilt; negative = bearish. (Z-score normalized.)

Bollinger Bands position (20, 2): Locates price within the bands (0–100 from lower → upper). Near upper suggests strength/expansion; near lower suggests weakness/contraction. (Then normalized.)

Stochastic (14, 3, 3): Shows where the close sits within the recent high-low range, smoothed via %D. Higher values = closes near highs; lower = near lows. (Scaled 0–100.)

ATR/DI composite (14): Volatility-weighted directional bias: (+DI − −DI) amplified by ATR as a % of price and its relative average. Positive = bullish pressure with volatility; negative = bearish. (Rank/scale normalized.)

All five are normalized and averaged into one composite, then smoothed (short/long) and compared to an adaptive midline with bands.

2) ADX view

Shows ADX, +DI, –DI with user-defined High Threshold. Transparency and color shift with regime. When ADX is strong, a directional “fire/ice” gradient fills the area between ADX and the high threshold, biased toward the dominant DI; when ADX is weak, a soft white fade highlights low-trend conditions.

HTF gap-line tracking (optional; both modes)

Detects “gap-like” reference levels after weak-trend consolidation flips into a sudden DI jump.

Anchors a line at the event bar’s open and auto-terminates upon first touch/cross (tick-size tolerance).

Auto-selects up to three higher timeframes suited to your chart resolution and prints non-overlapping lines with labels like 1H / 4H / 1D. Lower-priority duplicates are suppressed to reduce clutter.

Confirmation / repaint notes

Signals and lines finalize on bar close of the relevant timeframe.

HTF elements update only on the HTF bar close. During a forming bar they may appear transiently.

Line removal finalizes after the bar that produced the touch/cross closes.

Visual cues & effects

Oscillator candles: Open/High = long smoothing; Low/Close = short smoothing (no wicks).

Adaptive bands: Midline ± StdDev Multiplier × stdev of the blended series.

Consolidation tint: Optional white backdrop/candles when the consolidation condition is true (balance + low ADX).

Breakout VFX (optional): With strong DI/ADX and Bollinger breaks, renders a subtle “fire” flare above upper-band thrusts or “ice” shelf below lower-band thrusts.

Inputs (high-level)

Visual Style: Oscillator or ADX.

General (Oscillator): Lookback Period, Short/Long Smoothing, Standard Deviation Multiplier.

Color (Oscillator): Oversold/Overbought colors for gradient endpoints.

Plot (Oscillator): Show Candles, Show Slow MA Line, Show Individual Component (RSI/MACD/BB/Stoch/ATR).

Table (Oscillator): Show Information Table & position (compact dashboard of component values + status).

ADX / Gaps / VFX (both modes): ADX High Threshold, Highlight Backgrounds, Show Gap Labels, Visual Overlay Effects, and color choices for current-TF & HTF lines.

HTF selection: Automatic ladder (3 tiers) based on your chart timeframe.

Alerts (built-in)

Buy Signal – Primary: Oscillator exits oversold.

Sell Signal – Primary: Oscillator exits overbought.

Gap Fill Line Created (Any TF)

Gap Fill Line Terminated (Any TF)

ADX Crossed ABOVE/BELOW Low Threshold

ADX Crossed ABOVE/BELOW High Threshold

Consolidation Started

Alerts evaluate on the close of the relevant timeframe.

How to read it (quick guide)

Pick your lens: Oscillator for blended momentum around an adaptive midline; ADX for trend strength and DI skew.

Watch extremes & mean re-entries (Oscillator): Approaches to the top/bottom band show persistent momentum; returns toward the midline show normalization.

Check regime (ADX): Below Low = low-trend; above High = strong trend, with “fire/ice” bias toward +DI/–DI.

Track gap lines: Fresh labels mark new reference levels; lines auto-remove on first interaction. HTF lines add context but finalize only on HTF close.

The uniqueness from this indicator comes from multiple areas:

1. A unique multi-timeframe algorithm detects gap fill zones and plots them on the chart.

2. Visual effects for both visual modes were hand crafted to provide a visually stunning and intuitive interface.

3. The algorithm to determine sentiment uses a unique blend of weight and sensitivity adjustment to create a plot with elastic upper and lower bounds based off historical volatility and price action.

Information Flow Analysis[b🔄 Information Flow Analysis: Systematic Multi-Component Market Analysis Framework

SYSTEM OVERVIEW AND ANALYTICAL FOUNDATION

The Information Flow Kernel - Hybrid combines established technical analysis methods into a unified analytical framework. This indicator systematically processes three distinct data streams - directional price momentum, volume-weighted pressure dynamics, and intrabar development patterns - integrating them through weighted mathematical fusion to produce statistically normalized market flow measurements.

COMPREHENSIVE MATHEMATICAL FRAMEWORK

Component 1: Directional Flow Analysis

The directional component analyzes price momentum through three mathematical vectors:

Price Vector: p = C - O (intrabar directional bias)

Momentum Vector: m = C_t - C_{t-1} (bar-to-bar velocity)

Acceleration Vector: a = m_t - m_{t-1} (momentum rate of change)

Directional Signal Integration:

S_d = \text{sgn}(p) \cdot |p| + \text{sgn}(m) \cdot |m| \cdot 0.6 + \text{sgn}(a) \cdot |a| \cdot 0.3

The signum function preserves directional information while absolute values provide magnitude weighting. Coefficients create a hierarchy emphasizing intrabar movement (100%), momentum (60%), and acceleration (30%).

Final Directional Output: K_1 = S_d \cdot w_d where w_d is the directional weight parameter.

Component 2: Volume-Weighted Pressure Analysis

Volume Normalization: r_v = \frac{V_t}{\overline{V_n}} where \overline{V_n} represents the n-period simple moving average of volume.

Base Pressure Calculation: P_{base} = \Delta C \cdot r_v \cdot w_v where \Delta C = C_t - C_{t-1} and w_v is the velocity weighting factor.

Volume Confirmation Function:

f(r_v) = \begin{cases}

1.4 & \text{if } r_v > 1.2 \

0.7 & \text{if } r_v < 0.8 \

1.0 & \text{otherwise}

\end{cases}

Final Pressure Output: K_2 = P_{base} \cdot f(r_v)

Component 3: Intrabar Development Analysis

Bar Position Calculation: B = \frac{C - L}{H - L} when H - L > 0 , else B = 0.5

Development Signal Function:

S_{dev} = \begin{cases}

2(B - 0.5) & \text{if } B > 0.6 \text{ or } B < 0.4 \

0 & \text{if } 0.4 \leq B \leq 0.6

\end{cases}

Final Development Output: K_3 = S_{dev} \cdot 0.4

Master Integration and Statistical Normalization

Weighted Component Fusion: F_{raw} = 0.5K_1 + 0.35K_2 + 0.15K_3

Sensitivity Scaling: F_{master} = F_{raw} \cdot s where s is the sensitivity parameter.

Statistical Normalization Process:

Rolling Mean: \mu_F = \frac{1}{n}\sum_{i=0}^{n-1} F_{master,t-i}

Rolling Standard Deviation: \sigma_F = \sqrt{\frac{1}{n}\sum_{i=0}^{n-1} (F_{master,t-i} - \mu_F)^2}

Z-Score Computation: z = \frac{F_{master} - \mu_F}{\sigma_F}

Boundary Enforcement: z_{bounded} = \max(-3, \min(3, z))

Final Normalization: N = \frac{z_{bounded}}{3}

Flow Metrics Calculation:

Intensity: I = |z|

Strength Percentage: S = \min(100, I \times 33.33)

Extreme Detection: \text{Extreme} = I > 2.0

DETAILED INPUT PARAMETER SPECIFICATIONS

Sensitivity (0.1 - 3.0, Default: 1.0)

Global amplification multiplier applied to the master flow calculation. Functions as: F_{master} = F_{raw} \cdot s

Low Settings (0.1 - 0.5): Enhanced precision for subtle market movements. Optimal for low-volatility environments, scalping strategies, and early detection of minor directional shifts. Increases responsiveness but may amplify noise.

Moderate Settings (0.6 - 1.2): Balanced sensitivity for standard market conditions across multiple timeframes.

High Settings (1.3 - 3.0): Reduced sensitivity to minor fluctuations while emphasizing significant flow changes. Ideal for high-volatility assets, trending markets, and longer timeframes.

Directional Weighting (0.1 - 1.0, Default: 0.7)

Controls emphasis on price direction versus volume and positioning factors. Applied as: K_{1,weighted} = K_1 \times w_d

Lower Values (0.1 - 0.4): Reduces directional bias, favoring volume-confirmed moves. Optimal for ranging markets where momentum may generate false signals.

Higher Values (0.7 - 1.0): Amplifies directional signals from price vectors and acceleration. Ideal for trending conditions where directional momentum drives price action.

Velocity Weighting (0.1 - 1.0, Default: 0.6)

Scales volume-confirmed price change impact. Applied in: P_{base} = \Delta C \times r_v \times w_v

Lower Values (0.1 - 0.4): Dampens volume spike influence, focusing on sustained pressure patterns. Suitable for illiquid assets or news-sensitive markets.

Higher Values (0.8 - 1.0): Amplifies high-volume directional moves. Optimal for liquid markets where volume provides reliable confirmation.

Volume Length (3 - 20, Default: 5)

Defines lookback period for volume averaging: \overline{V_n} = \frac{1}{n}\sum_{i=0}^{n-1} V_{t-i}

Short Periods (3 - 7): Responsive to recent volume shifts, excellent for intraday analysis.

Long Periods (13 - 20): Smoother averaging, better for swing trading and higher timeframes.

DASHBOARD SYSTEM

Primary Flow Gauge

Bilaterally symmetric visualization displaying normalized flow direction and intensity:

Segment Calculation: n_{active} = \lfloor |N| \times 15 \rfloor

Left Fill: Bearish flow when N < -0.01

Right Fill: Bullish flow when N > 0.01

Neutral Display: Empty segments when |N| \leq 0.01

Visual Style Options:

Matrix: Digital blocks (▰/▱) for quantitative precision

Wave: Progressive patterns (▁▂▃▄▅▆▇█) showing flow buildup

Dots: LED-style indicators (●/○) with intensity scaling

Blocks: Modern squares (■/□) for professional appearance

Pulse: Progressive markers (⎯ to █) emphasizing intensity buildup

Flow Intensity Visualization

30-segment horizontal bar graph with mathematical fill logic:

Segment Fill: For i \in : filled if \frac{i}{29} \leq \frac{S}{100}

Color Coding System:

Orange (S > 66%): High intensity, strong directional conviction

Cyan (33% ≤ S ≤ 66%): Moderate intensity, developing bias

White (S < 33%): Low intensity, neutral conditions

Extreme Detection Indicators

Circular markers flanking the gauge with state-dependent illumination:

Activation: I > 2.0 \land |N| > 0.3

Bright Yellow: Active extreme conditions

Dim Yellow: Normal conditions

Metrics Display

Balance Value: Raw master flow output ( F_{master} ) showing absolute directional pressure

Z-Score Value: Statistical deviation ( z_{bounded} ) indicating historical context

Dynamic Narrative System

Context-sensitive interpretation based on mathematical thresholds:

Extreme Flow: I > 2.0 \land |N| > 0.6

Moderate Flow: 0.3 < |N| \leq 0.6

High Volatility: S > 50 \land |N| \leq 0.3

Neutral State: S \leq 50 \land |N| \leq 0.3

ALERT SYSTEM SPECIFICATIONS

Mathematical Trigger Conditions:

Extreme Bullish: I > 2.0 \land N > 0.6

Extreme Bearish: I > 2.0 \land N < -0.6

High Intensity: S > 80

Bullish Shift: N_t > 0.3 \land N_{t-1} \leq 0.3

Bearish Shift: N_t < -0.3 \land N_{t-1} \geq -0.3

TECHNICAL IMPLEMENTATION AND PERFORMANCE

Computational Architecture

The system employs efficient calculation methods minimizing processing overhead:

Single-pass mathematical operations for all components

Conditional visual rendering (executed only on final bar)

Optimized array operations using direct calculations

Real-Time Processing

The indicator updates continuously during bar formation, providing immediate feedback on changing market conditions. Statistical normalization ensures consistent interpretation across varying market regimes.

Market Applicability

Optimal performance in liquid markets with consistent volume patterns. May require parameter adjustment for:

Low-volume or after-hours sessions

News-driven market conditions

Highly volatile cryptocurrency markets

Ranging versus trending market environments

PRACTICAL APPLICATION FRAMEWORK

Market State Classification

This indicator functions as a comprehensive market condition assessment tool providing:

Trend Analysis: High intensity readings ( S > 66% ) with sustained directional bias indicate strong trending conditions suitable for momentum strategies.

Reversal Detection: Extreme readings ( I > 2.0 ) at key technical levels may signal potential trend exhaustion or reversal points.

Range Identification: Low intensity with neutral flow ( S < 33%, |N| < 0.3 ) suggests ranging market conditions suitable for mean reversion strategies.

Volatility Assessment: High intensity without clear directional bias indicates elevated volatility with conflicting pressures.

Integration with Trading Systems

The normalized output range facilitates integration with automated trading systems and position sizing algorithms. The statistical basis provides consistent interpretation across different market conditions and asset classes.

LIMITATIONS AND CONSIDERATIONS

This indicator combines established technical analysis methods and processes historical data without predicting future price movements. The system performs optimally in liquid markets with consistent volume patterns and may produce false signals in thin trading conditions or during news-driven market events. This indicator is provided for educational and analytical purposes only and does not constitute financial advice. Users should combine this analysis with proper risk management, position sizing, and additional confirmation methods before making any trading decisions. Past performance does not guarantee future results.

Note: The term "kernel" in this context refers to modular calculation components rather than mathematical kernel functions in the formal computational sense.

As quantitative analyst Ralph Vince noted: "The essence of successful trading lies not in predicting market direction, but in the systematic processing of market information and the disciplined management of probability distributions."

— Dskyz, Trade with insight. Trade with anticipation.

Machine Learning-Inspired Supply & Demand Zones [AlgoPoint]This indicator is a Smart Supply & Demand Zone tool, developed with principles inspired by Machine Learning (ML). It intelligently filters out market noise, allowing you to focus only on the most significant zones where institutional order flow is likely present.

💡 How It Works: Why Is This Indicator "Smart"?

Unlike traditional indicators that only measure simple price movements, this script uses an algorithm that asks the same critical questions an experienced market analyst would to qualify a zone:

- 1. Price Imbalance: How fast and aggressively did the price leave the zone? Our algorithm measures the body size of the "departure candle" relative to the current market volatility (ATR). A zone is only considered if it was formed by an explosive move that is statistically significant, indicating a major imbalance between buyers and sellers.

- 2. Volume Confirmation: Did the "smart money" participate in this move? The script checks if the volume on the departure candle was significantly higher than the recent average volume. A spike in volume confirms that the move was backed by institutional interest, adding strength and validity to the zone.

- 3. Valid Pivot Structure: Did the zone originate from a meaningful swing high or low? The algorithm first identifies a valid pivot structure, ensuring that zones are not drawn from insignificant or random price fluctuations.

Only when a potential zone passes these three critical tests—our "quality filter"—is it drawn on your chart.

🚀 Features & How to Use

Using the indicator is straightforward. You will see two primary types of boxes on your chart:

* 🟥 Red Box (Supply Zone): An area of potential resistance where selling pressure is likely to be strong. Look for potential shorting opportunities as the price approaches this zone.

* 🟩 Green Box (Demand Zone): An area of potential support where buying pressure is likely to be strong. Look for potential long opportunities as the price pulls back into this zone.

Dynamic Zone Management

This indicator is not static; it lives and breathes with the market:

- Fresh Zone: A newly formed zone appears in its full, vibrant color. These are the highest-probability zones as they have not yet been re-tested.

- Broken / Flipped Zone: You have full control over what happens when a zone is broken! In the settings, you can choose:

- Delete Zone: The zone will be removed completely when the price closes through it.

- Show as Broken (Flip): When broken, the zone will turn gray, stop extending, and remain on your chart. This is extremely useful for identifying Support/Resistance Flips, where a broken demand zone becomes new resistance, or a broken supply zone becomes new support.

⚙️ Settings & Customization

Fine-tune the indicator to match your personal trading style via the settings menu:

- Breakout Behavior: The most powerful feature. Choose between Delete Zone and Show as Broken (Flip) to customize your chart.

- Zone Finding Logic: Control the indicator's sensitivity.

- Selective: Requires both strong imbalance and high volume. Finds fewer, but higher-quality, zones.

- Moderate: Requires either strong imbalance or high volume. Finds more potential zones.

- Sensitivity Settings: Adjust the ATR Multiplier and Volume Multiplier to make the criteria for a "strong" zone stricter or looser.

Swing Z | Zillennial Technologies Inc.Swing Z by Zillennial Technologies Inc. is an advanced algorithmic framework built specifically for cryptocurrency markets. It integrates multiple layers of technical analysis into a single decision-support tool, generating buy and sell signals only when several independent confirmations align.

Core Concept

Swing Z fuses trend structure, momentum oscillators, volatility signals, and price action tools to capture high-probability trading opportunities in volatile crypto environments.

Trend Structure (EMA 9, 21, 50, 200)

Short-term EMAs (9 & 21) detect immediate momentum shifts.

Longer-term EMAs (50 & 200) define the broader trend and dynamic support/resistance.

Momentum & Confirmation Layer

RSI measures relative strength and market conditions.

MACD crossovers confirm momentum shifts and trend continuations.

Volatility & Market Pressure

TTM Squeeze highlights compression zones likely to precede breakouts.

Volume analysis confirms conviction behind directional moves.

VWAP (Volume Weighted Average Price) establishes intraday value zones and institutional benchmarks.

Price Action Filters

Fibonacci retracements are integrated to identify key reversal and continuation levels.

Signals are produced only when multiple conditions agree, reducing noise and improving reliability in fast-moving crypto markets.

Features

Tailored for cryptocurrency trading across major pairs (BTC, ETH, and altcoins).

Works effectively on swing and trend-based timeframes (1H–1D).

Combines trend, momentum, volatility, and price action into a single framework.

Generates clear Buy/Sell markers and integrates with TradingView alerts.

How to Use

Apply to a clean chart for the clearest visualization.

Use Swing Z as a swing trading tool, aligning entries with both trend structure and momentum confirmation.

Combine with your own stop-loss, take-profit, and position sizing rules.

Avoid application on non-standard chart types such as Renko, Heikin Ashi, or Point & Figure, which may distort results.

Disclaimer

Swing Z is designed as a decision-support tool, not financial advice.

All backtesting should use realistic risk, commission, and slippage assumptions.

Past results do not guarantee future performance.

Signals do not repaint but may adjust as new data develops in real-time.

Why Swing Z is original & useful:

Swing Z unifies EMA trend structure, RSI, MACD, TTM Squeeze, VWAP, Fibonacci retracements, and volume analysis into a single algorithmic framework. This multi-confirmation approach improves accuracy by requiring consensus across trend, momentum, volatility, and price action — a design made specifically for the challenges and volatility of cryptocurrency markets.

Alexmoku Genesis v0.2.6 — Runtime BulletproofAlexmoku Genesis v0.2.6 – Reinventing Ichimoku with Precision and Intelligence

Built by Alex • Engineered for traders who demand more than lagging clouds

🔬 Overview

Alexmoku Genesis is a ground-up reimagining of the traditional Ichimoku system — retaining its philosophical foundations of harmony, balance, and structure, while infusing it with modern logic, advanced volatility modeling, and AI-aligned signal classification.

This is not your grandfather’s Ichimoku. Genesis transforms it into a forward-sensing, volatility-aware system that adapts in real time and guides discretionary and algorithmic traders alike with smarter signals, predictive structure, and built-in trade intelligence.

⚙️ Core Enhancements

📐 Volatility-Responsive Smoothing

Tenkan-sen and Kijun-sen lengths are dynamically adjusted based on recent price volatility (ATR-based).

Prevents overreaction in choppy markets and improves responsiveness during strong trends.

🌀 Adaptive Cloud Projection

Span A and Span B are still projected 52 periods forward — but cloud width adapts to market rhythm, not just static values.

🕵️ Enhanced Chikou Span (CKS+)

Chikou logic is upgraded to emphasize structure interaction, not just simple price overlay.

Useful for identifying support/resistance echoes and divergence validation.

🌐 Multi-Timeframe Cloud Awareness (Genesis Core)

Internal alignment checks between higher and lower timeframe Kumo positioning.

Future module support for overlaying MTF clouds.

🔖 Signal Classifier Engine (Experimental)

Each major structure event is tagged with signal intent:

📦 prep

🚀 launch

🔁 reversion

🪤 trap

Enables faster discretionary reads or future automation.

🧠 Trust Score Logic (Coming soon)

Future versions will assign numerical trust scores (1–10) to trade setups based on confluence.

🧰 Settings

🔧 Volatility Scaling Factor – Adjusts how reactive the indicator is to volatility. Default: 300.

🌫 Displacement (Kumo) – Cloud projection forward. Default (and required): 52.

⛅ Cloud Display Toggle – Show/hide Kumo visuals without affecting logic.

⚡️ Future expansion modules already scaffolded (MTF overlays, color-coded signal classifiers, Trust Score engine, etc.)

🧘 Philosophy Behind the System

"This isn’t just about catching runners — it’s about becoming the kind of person who can trade with clarity, peace, and precision."

Alexmoku Genesis reflects the W.E.A.L.T.H. System's holistic philosophy:

Wealth

Engineered

Algorithmic

Leveraged

Trading

Holistically

Trading isn't just a strategy. It's a mirror. Genesis is designed to train both your execution and your awareness.

⚠️ Disclaimer

This tool is designed for experienced technical traders and is still in active development. Use judgment and proper risk management. This is not financial advice.

ICT Macro Time Window NYThis script highlights the typical ICT “macro” algorithm activity windows on your chart. It marks 10 minutes before to 10 minutes after each full hour, based on New York time (NY). The display is restricted to the 00:00 – 16:00 NY time range.

Overlay on chart with semi-transparent background

Automatically adjusts to the chart timeframe

Customizable: window start/end minutes, hours, and background color

Ideal for traders following ICT concepts to visually identify high-probability algorithm activity periods.

Advanced Volume Profile Pro Delta + POC + VAH/VAL# Advanced Volume Profile Pro - Delta + POC + VAH/VAL Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive volume profile analysis system that combines traditional volume-at-price distribution with delta volume calculations, Point of Control (POC) identification, and Value Area (VAH/VAL) analysis. Unlike standard volume indicators that show only total volume over time, this script analyzes volume distribution across price levels and estimates buying vs selling pressure using multiple calculation methods to provide deeper market structure insights.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Traditional volume indicators show when volume occurs but not where price finds acceptance or rejection. Standalone volume profiles lack directional bias information, while basic delta calculations don't provide structural context. Traders need to understand both volume distribution AND directional sentiment at key price levels.

**The Solution:** This script implements an integrated approach that:

- Maps volume distribution across price levels using configurable row density

- Estimates delta (buying vs selling pressure) using three different methodologies

- Identifies Point of Control (highest volume price level) for key support/resistance

- Calculates Value Area boundaries where 70% of volume traded

- Provides real-time alerts for key level interactions and volume imbalances

**Unique Features:**

1. **Developing POC Visualization**: Real-time tracking of Point of Control migration throughout the session via blue dotted trail, revealing institutional accumulation/distribution patterns before they complete

2. **Multi-Method Delta Calculation**: Price Action-based, Bid/Ask estimation, and Cumulative methods for different market conditions

3. **Adaptive Timeframe System**: Auto-adjusts calculation parameters based on chart timeframe for optimal performance

4. **Flexible Profile Types**: N Bars Back (precise control), Days Back (calendar-based), and Session-based analysis modes

5. **Advanced Imbalance Detection**: Identifies and highlights significant buying/selling imbalances with configurable thresholds

6. **Comprehensive Alert System**: Monitors POC touches, Value Area entry/exit, and major volume imbalances

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Volume Profile Methodology:

**1. Price Level Distribution:**

- Divides price range into user-defined rows (10-50 configurable)

- Calculates row height: `(Highest Price - Lowest Price) / Number of Rows`

- Distributes each bar's volume across price levels it touched proportionally

**2. Delta Volume Calculation Methods:**

**Price Action Method:**

```

Price Range = High - Low

Buy Pressure = (Close - Low) / Price Range

Sell Pressure = (High - Close) / Price Range

Buy Volume = Total Volume × Buy Pressure

Sell Volume = Total Volume × Sell Pressure

Delta = Buy Volume - Sell Volume

```

**Bid/Ask Estimation Method:**

```

Average Price = (High + Low + Close) / 3

Buy Volume = Close > Average ? Volume × 0.6 : Volume × 0.4

Sell Volume = Total Volume - Buy Volume

```

**Cumulative Method:**

```

Buy Volume = Close > Open ? Volume : Volume × 0.3

Sell Volume = Close ≤ Open ? Volume : Volume × 0.3

```

**3. Point of Control (POC) Identification:**

- Scans all price levels to find maximum volume concentration

- POC represents the price level with highest trading activity

- Acts as significant support/resistance level

- **Developing POC Feature**: Tracks POC evolution in real-time via blue dotted trail, showing how institutional interest migrates throughout the session. Upward POC migration indicates accumulation patterns, downward migration suggests distribution, providing early trend signals before price confirmation.

**4. Value Area Calculation:**

- Starts from POC and expands up/down to encompass 70% of total volume

- VAH (Value Area High): Upper boundary of value area

- VAL (Value Area Low): Lower boundary of value area

- Expansion algorithm prioritizes direction with higher volume

**5. Adaptive Range Selection:**

Based on profile type and timeframe optimization:

- **N Bars Back**: Fixed lookback period with performance optimization (20-500 bars)

- **Days Back**: Calendar-based analysis with automatic timeframe adjustment (1-365 days)

- **Session**: Current trading session or custom session times

### Performance Optimization Features:

- **Sampling Algorithm**: Reduces calculation load on large datasets while maintaining accuracy

- **Memory Management**: Clears previous drawings to prevent performance degradation

- **Safety Constraints**: Prevents excessive memory usage with configurable limits

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Profile Configuration**: Select profile type based on trading style:

- N Bars Back: Precise control over data range

- Days Back: Intuitive calendar-based analysis

- Session: Real-time session development

2. **Row Density**: Set number of rows (30 default) - more rows = higher resolution, slower performance

3. **Delta Method**: Choose calculation method based on market type:

- Price Action: Best for trending markets

- Bid/Ask Estimate: Good for ranging markets

- Cumulative: Smoothed approach for volatile markets

4. **Visual Settings**: Configure colors, position (left/right), and display options

### Reading the Profile:

**Volume Bars:**

- **Length**: Represents relative volume at that price level

- **Color**: Green = net buying pressure, Red = net selling pressure

- **Intensity**: Darker colors indicate volume imbalances above threshold

**Key Levels:**

- **POC (Blue Line)**: Highest volume price - major support/resistance

- **VAH (Purple Dashed)**: Value Area High - upper boundary of fair value

- **VAL (Orange Dashed)**: Value Area Low - lower boundary of fair value

- **Value Area Fill**: Shaded region showing main trading range

**Developing POC Trail:**

- **Blue Dotted Lines**: Show real-time POC evolution throughout the session

- **Migration Patterns**: Upward trail indicates bullish accumulation, downward trail suggests bearish distribution

- **Early Signals**: POC movement often precedes price movement, providing advance warning of institutional activity

- **Institutional Footprints**: Reveals where smart money concentrated volume before final POC establishment

### Trading Applications:

**Support/Resistance Analysis:**

- POC acts as magnetic price level - expect reactions

- VAH/VAL provide intermediate support/resistance levels

- Profile edges show areas of low volume acceptance

**Developing POC Analysis:**

- **Upward Migration**: POC moving higher = institutional accumulation, bullish bias

- **Downward Migration**: POC moving lower = institutional distribution, bearish bias

- **Stable POC**: Tight clustering = balanced market, range-bound conditions

- **Early Trend Detection**: POC direction change often precedes price breakouts

**Entry Strategies:**

- Buy at VAL with POC as target (in uptrends)

- Sell at VAH with POC as target (in downtrends)

- Breakout plays above/below profile extremes

**Volume Imbalance Trading:**

- Strong buying imbalance (>60% threshold) suggests continued upward pressure

- Strong selling imbalance suggests continued downward pressure

- Imbalances near key levels provide high-probability setups

**Multi-Timeframe Context:**

- Use higher timeframe profiles for major levels

- Lower timeframe profiles for precise entries

- Session profiles for intraday trading structure

## SCRIPT SETTINGS EXPLANATION

### Volume Profile Settings:

- **Profile Type**: Determines data range for calculation

- N Bars Back: Exact number of bars (20-500 range)

- Days Back: Calendar days with timeframe adaptation (1-365 days)

- Session: Trading session-based (intraday focus)

- **Number of Rows**: Profile resolution (10-50 range)

- **Profile Width**: Visual width as chart percentage (10-50%)

- **Value Area %**: Volume percentage for VA calculation (50-90%, 70% standard)

- **Auto-Adjust**: Automatically optimizes for different timeframes

### Delta Volume Settings:

- **Show Delta Volume**: Enable/disable delta calculations

- **Delta Calculation Method**: Choose methodology based on market conditions

- **Highlight Imbalances**: Visual emphasis for significant volume imbalances

- **Imbalance Threshold**: Percentage for imbalance detection (50-90%)

### Session Settings:

- **Session Type**: Daily, Weekly, Monthly, or Custom periods

- **Custom Session Time**: Define specific trading hours

- **Previous Sessions**: Number of historical sessions to display

### Days Back Settings:

- **Lookback Days**: Number of calendar days to analyze (1-365)

- **Automatic Calculation**: Script automatically converts days to bars based on timeframe:

- Intraday: Accounts for 6.5 trading hours per day

- Daily: 1 bar per day

- Weekly/Monthly: Proportional adjustment

### N Bars Back Settings:

- **Lookback Bars**: Exact number of bars to analyze (20-500)

- **Precise Control**: Best for systematic analysis and backtesting

### Visual Customization:

- **Colors**: Bullish (green), Bearish (red), and level colors

- **Profile Position**: Left or Right side of chart

- **Profile Offset**: Distance from current price action

- **Labels**: Show/hide level labels and values

- **Smooth Profile Bars**: Enhanced visual appearance

### Alert Configuration:

- **POC Touch**: Alerts when price interacts with Point of Control

- **VA Entry/Exit**: Alerts for Value Area boundary interactions

- **Major Imbalance**: Alerts for significant volume imbalances

## VISUAL FEATURES

### Profile Display:

- **Horizontal Bars**: Volume distribution across price levels

- **Color Coding**: Delta-based coloring for directional bias

- **Smooth Rendering**: Optional smoothing for cleaner appearance

- **Transparency**: Configurable opacity for chart readability

### Level Lines:

- **POC**: Solid blue line with optional label

- **VAH/VAL**: Dashed colored lines with value displays

- **Extension**: Lines extend across relevant time periods

- **Value Area Fill**: Optional shaded region between VAH/VAL

### Information Table:

- **Current Values**: Real-time POC, VAH, VAL prices

- **VA Range**: Value Area width calculation

- **Positioning**: Multiple table positions available

- **Text Sizing**: Adjustable for different screen sizes

## IMPORTANT USAGE NOTES

**Realistic Expectations:**

- Volume profile analysis provides structural context, not trading signals

- Delta calculations are estimations based on price action, not actual order flow

- Past volume distribution does not guarantee future price behavior

- Combine with other analysis methods for comprehensive market view

**Best Practices:**

- Use appropriate profile types for your trading style:

- Day Trading: Session or Days Back (1-5 days)

- Swing Trading: Days Back (10-30 days) or N Bars Back

- Position Trading: Days Back (60-180 days)

- Consider market context (trending vs ranging conditions)

- Verify key levels with additional technical analysis

- Monitor profile development for changing market structure

**Performance Considerations:**

- Higher row counts increase calculation complexity

- Large lookback periods may affect chart performance

- Auto-adjust feature optimizes for most use cases

- Consider using session profiles for intraday efficiency

**Limitations:**

- Delta calculations are estimations, not actual transaction data

- Profile accuracy depends on available price/volume history

- Effectiveness varies across different instruments and market conditions

- Requires understanding of volume profile concepts for optimal use

**Data Requirements:**

- Requires volume data for accurate calculations

- Works best on liquid instruments with consistent volume

- May be less effective on very low volume or exotic instruments

This script serves as a comprehensive volume analysis tool for traders who need detailed market structure information with integrated directional bias analysis and real-time POC development tracking for informed trading decisions.

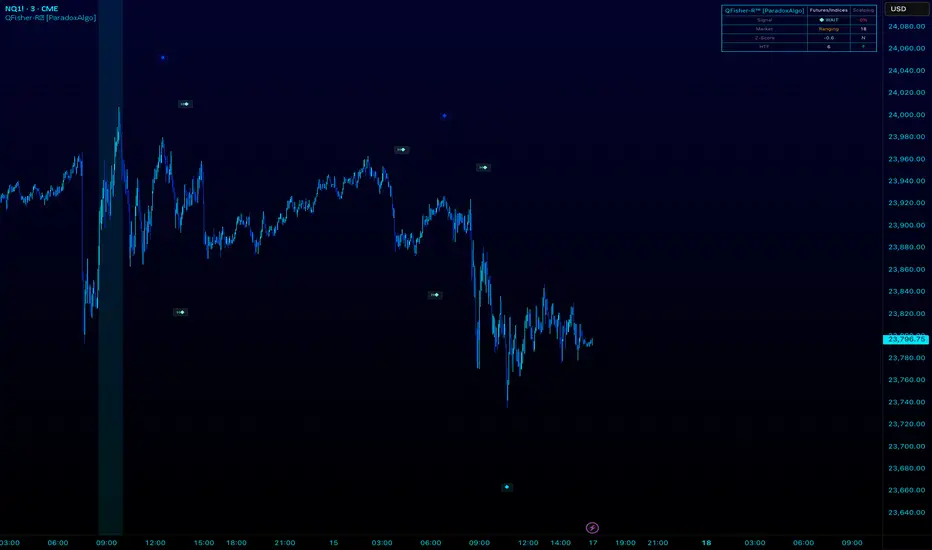

QFisher-R™ [ParadoxAlgo]QFISHER-R™ (Regime-Aware Fisher Transform)

A research/education tool that helps visualize potential momentum exhaustion and probable inflection zones using a quantitative, non-repainting Fisher framework with regime filters and multi-timeframe (MTF) confirmation.

What it does

Converts normalized price movement into a stabilized Fisher domain to highlight potential turning points.

Uses adaptive smoothing, robust (MAD/quantile) thresholds, and optional MTF alignment to contextualize extremes.

Provides a Reversal Probability Score (0–100) to summarize signal confluence (extreme, slope, cross, divergence, regime, and MTF checks).

Key features

Non-repainting logic (bar-close confirmation; security() with no lookahead).

Dynamic exhaustion bands (data-driven thresholds vs fixed ±2).

Adaptive smoothing (efficiency-ratio based).

Optional divergence tags on structurally valid pivots.

MTF confirmation (same logic computed on a higher timeframe).

Compact visuals with subtle plotting to reduce chart clutter.

Inputs (high level)

Source (e.g., HLC3 / Close / HA).

Core lookback, fast/slow range blend, and ER length.

Band sensitivity (robust thresholding).

MTF timeframe(s) and agreement requirement.

Toggle divergence & intrabar previews (default off).

Signals & Alerts

Turn Candidate (Up/Down) when multiple conditions align.

Trade-Grade Turn when score ≥ threshold and MTF agrees.

Divergence Confirmed when structural criteria are met.

Alerts are generated on confirmed bar close by default. Optional “preview” mode is available for experimentation.

How to use

Start on your preferred timeframe; optionally enable an HTF (e.g., 4×) for confirmation.

Look for RPS clusters near the exhaustion bands, slope inflections, and (optionally) divergences.

Combine with your own risk management, liquidity, and trend context.

Paper test first and calibrate thresholds to your instrument and timeframe.

Notes & limitations

This is not a buy/sell signal generator and does not predict future returns.

Readings can remain extreme during strong trends; use HTF context and your own filters.

Parameters are intentionally conservative by default; adjust carefully.

Compliance / Disclaimer

Educational & research tool only. Not financial advice. No recommendation to buy/sell any security or derivative.

Past performance, backtests, or examples (if any) are not indicative of future results.

Trading involves risk; you are responsible for your own decisions and risk management.

Built upon the Fisher Transform concept (Ehlers); all modifications, smoothing, regime logic, scoring, and visualization are original work by Paradox Algo.

Time Window Optimizer [theUltimator5]The Time Window Optimizer is designed to identify the most profitable 30-minute trading windows during regular market hours (9:30 AM - 4:00 PM EST). This tool helps traders optimize their intraday strategies by automatically discovering time periods with the highest historical performance or allowing manual selection for custom analysis. It also allows you to select manual timeframes for custom time period analysis.

🏆 Automatic Window Discovery

The core feature of this indicator is its intelligent Auto-Find Best 30min Window system that analyzes all 13 possible 30-minute time slots during market hours.

How the Algorithm Works:

Concurrent Analysis: The indicator simultaneously tracks performance across all 13 time windows (9:30-10:00, 10:00-10:30, 10:30-11:00... through 15:30-16:00)

Daily Performance Tracking: For each window, it captures the percentage change from window open to window close on every trading day

Cumulative Compounding: Daily returns are compounded over time to show the true long-term performance of each window, starting from a normalized value of 1.0

Dynamic Optimization: The system continuously identifies the window with the highest cumulative return and highlights it as the optimal choice

Statistical Validation: Performance is validated through multiple metrics including average daily returns, win rates, and total sample size

Visual Representation:

Best Window Line: The top-performing window is displayed as a thick colored line for easy identification

All 13 Lines (optional): Users can view performance lines for all time windows simultaneously to compare relative performance

Smart Coloring: Lines are color-coded (green for gains, red for losses) with the best performer highlighted in a user-selected color

📊 Comprehensive Performance Analysis

The indicator provides detailed statistics in an information table:

Average Daily Return: Mean percentage change per trading session

Cumulative Return: Total compounded performance over the analysis period

Win Rate: Percentage of profitable days (colored green if ≥50%, red if <50%)

Buy & Hold Comparison: Shows outperformance vs. simple buy-and-hold strategy

Sample Size: Number of trading days analyzed for statistical significance

🛠️ User Settings

imgur.com

Auto-Optimization Controls:

Auto-Find Best Window: Toggle to enable/disable automatic optimization

Show All 13 Lines: Display all time window performance lines simultaneously

Best Window Line Color: Customize the color of the top-performing window

Manual Mode:

imgur.com

Custom Time Window: Set any desired time range using session format (HHMM-HHMM)

Crypto Support: Built-in timezone offset adjustment for cryptocurrency markets

Chart Type Options: Switch between candlestick and line chart visualization

Visual Customization:

imgur.com

Background Highlighting: Optional background color during active time windows

Candle Coloring: Custom colors for bullish/bearish candles within the time window

Table Positioning: Flexible placement of the statistics table anywhere on the chart

🔧 Technical Features

Market Compatibility:

Stock Markets: Optimized for traditional market hours (9:30 AM - 4:00 PM EST)

Cryptocurrency: Includes timezone offset adjustment for 24/7 crypto markets

Exchange Detection: Automatically detects crypto exchanges and applies appropriate settings

Performance Optimization:

Efficient Calculation: Uses separate arrays for each time block to minimize computational overhead

Real-time Updates: Dynamically updates the best-performing window as new data becomes available

Memory Management: Optimized data structures to handle large datasets efficiently

💡 Use Cases

Strategy Development: Identify the most profitable trading hours for your specific instruments

Risk Management: Focus trading activity during historically successful time periods

Performance Comparison: Evaluate whether time-specific strategies outperform buy-and-hold

Market Analysis: Understand intraday patterns and market behavior across different time windows

📈 Key Benefits

Data-Driven Decisions: Base trading schedules on historical performance data

Automated Analysis: No manual calculation required - the algorithm does the work

Flexible Implementation: Works in both automated discovery and manual selection modes

Comprehensive Metrics: Multiple performance indicators for thorough analysis

Visual Clarity: Clear, color-coded visualization makes interpretation intuitive

This indicator transforms complex intraday analysis into actionable insights, helping traders optimize their time allocation and improve overall trading performance through systematic, data-driven approach to market timing.

Bollinger Heatmap [Quantitative]Overview

The Bollinger Heatmap is a composite indicator that synthesizes data derived from 30 Bollinger bands distributed over multiple time horizons, offering a high-dimensional characterization of the underlying asset.

Algorithm

The algorithm quantifies the current price’s relative position within each Bollinger band ensemble, generating a normalized position ratio. This ratio is subsequently transformed into a scalar heat value, which is then rendered on a continuous color gradient from red to blue. Red hues correspond to price proximity to or extension below the lower band, while blue hues denote price proximity to or extension above the upper band.

Using default parameters, the indicator maps bands over timeframes increasing in a pattern approximating exponential growth, constrained to multiples of seven days. The lower region encodes relationships with shorter-term bands spanning between 1 and 14 weeks, whereas the upper region portrays interactions with longer-term bands ranging from 15 to 52 weeks.

Conclusion

By integrating Bollinger bands across a diverse array of time horizons, the heatmap indicator aims to mitigate the model risk inherent in selecting a single band length, capturing exposure across a richer parameter space.

MTF Dashboard 9 Timeframes + Signals# MTF Dashboard Pro - Multi-Timeframe Confluence Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive dashboard that simultaneously analyzes market conditions across 9 different timeframes (1m, 5m, 15m, 30m, 1H, 4H, Daily, Weekly, Monthly) using a proprietary confluence scoring methodology. Unlike simple multi-timeframe displays that show individual indicators separately, this script combines trend analysis, momentum, volatility signals, and volume analysis into unified confluence scores for each timeframe.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Most traders manually check multiple timeframes and struggle to quickly assess overall market bias when different timeframes show conflicting signals. Existing MTF scripts typically display individual indicators without synthesizing them into actionable intelligence.

**The Solution:** This script implements a mathematical confluence algorithm that:

- Weights each indicator's signal strength (trend direction, RSI momentum, MACD volatility, volume analysis)

- Calculates normalized scores across all active timeframes

- Determines overall market bias with statistical confidence levels

- Provides instant visual feedback through color-coded symbols and star ratings

**Unique Features:**

1. **Confluence Scoring Algorithm**: Mathematically combines multiple indicator signals into a single confidence rating per timeframe

2. **Market Bias Engine**: Automatically calculates overall directional bias with percentage strength across all selected timeframes

3. **Dynamic Display System**: Real-time updates with customizable layouts, color schemes, and selective timeframe activation

4. **Statistical Analysis**: Provides bullish/bearish vote counts and overall confluence percentages

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Calculation Methodology:

**1. Trend Analysis (EMA-based):**

- Fast EMA (default: 9) vs Slow EMA (default: 21) crossover analysis

- Returns values: +1 (bullish), -1 (bearish), 0 (neutral)

**2. Momentum Analysis (RSI-based):**

- RSI levels: >70 (strong bullish +2), >50 (bullish +1), <30 (strong bearish -2), <50 (bearish -1)

- Provides overbought/oversold context for trend confirmation

**3. Volatility Analysis (MACD-based):**

- MACD line vs Signal line positioning

- Histogram strength comparison with previous bar

- Combined score considering both direction and momentum strength

**4. Volume Analysis:**

- Current volume vs 20-period moving average

- Thresholds: >150% MA (strong +2), >100% MA (bullish +1), <50% MA (weak -2)

**5. Confluence Calculation:**

```

Confluence Score = (Trend + RSI + MACD + Volume) / 4.0

```

**6. Market Bias Determination:**

- Counts bullish vs bearish signals across all active timeframes

- Calculates bias strength percentage: |Bullish Count - Bearish Count| / Total Active TFs * 100

- Determines overall market direction: BULLISH, BEARISH, or NEUTRAL

### Multi-Timeframe Implementation:

Uses `request.security()` calls to fetch data from each timeframe, ensuring all calculations are performed on the respective timeframe's data rather than current chart timeframe, providing accurate multi-timeframe analysis.

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Timeframe Selection**: Enable/disable specific timeframes in "Timeframe Selection" group based on your trading style

2. **Indicator Configuration**: Adjust EMA periods (Fast: 9, Slow: 21), RSI length (14), and MACD settings (12/26/9) to match your analysis preferences

3. **Display Options**: Choose table position, text size, and color scheme for optimal visibility

### Reading the Dashboard:

**Symbol Interpretation:**

- ⬆⬆ = Strong bullish signal (score ≥ 2)

- ⬆ = Bullish signal (score > 0)

- ➡ = Neutral signal (score = 0)

- ⬇ = Bearish signal (score < 0)

- ⬇⬇ = Strong bearish signal (score ≤ -2)

**Confluence Stars:**

- ★★★★★ = Very high confidence (score > 0.75)

- ★★★★☆ = High confidence (score > 0.5)

- ★★★☆☆ = Medium confidence (score > 0.25)

- ★★☆☆☆ = Low confidence (score > 0)

- ★☆☆☆☆ = Very low confidence (score > -0.25)

**Market Bias Section:**

- Shows overall market direction across all active timeframes

- Strength percentage indicates conviction level

- Overall confluence score represents average agreement across timeframes

### Trading Applications:

**Entry Signals:**

- Look for high confluence (4-5 stars) across multiple timeframes in same direction

- Higher timeframe alignment provides stronger signal validation

- Use confluence percentage >75% for high-probability setups

**Risk Management:**

- Lower timeframe conflicts may indicate choppy conditions