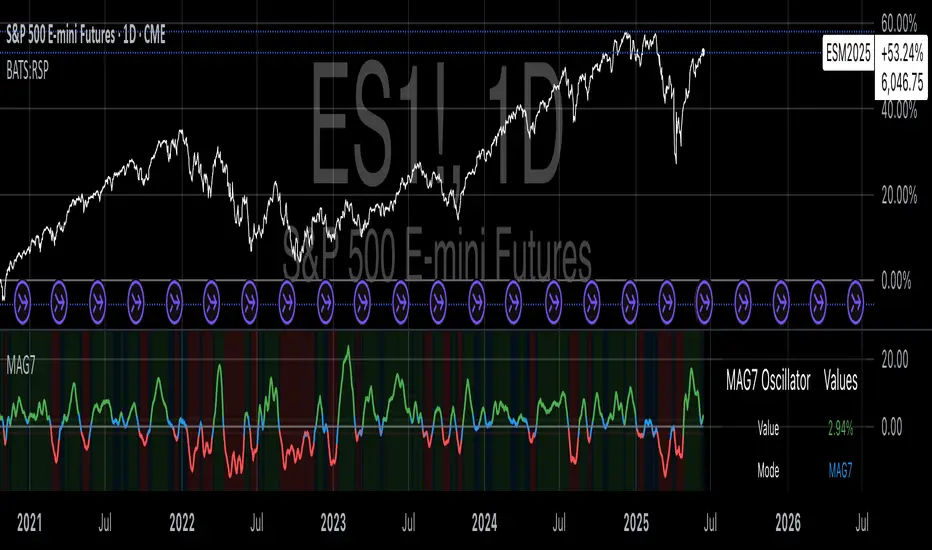

Magnificent 7 OscillatorThe Magnificent 7 Oscillator is a sophisticated momentum-based technical indicator designed to analyze the collective performance of the seven largest technology companies in the U.S. stock market (Apple, Microsoft, Alphabet, Amazon, NVIDIA, Tesla, and Meta). This indicator incorporates established momentum factor research and provides three distinct analytical modes: absolute momentum tracking, equal-weighted market comparison, and relative performance analysis. The tool integrates five different oscillator methodologies and includes advanced breadth analysis capabilities.

Theoretical Foundation

Momentum Factor Research

The indicator's foundation rests on seminal momentum research in financial markets. Jegadeesh and Titman (1993) demonstrated that stocks with strong price performance over 3-12 month periods tend to continue outperforming in subsequent periods¹. This momentum effect was later incorporated into formal factor models by Carhart (1997), who extended the Fama-French three-factor model to include a momentum factor (UMD - Up Minus Down)².

The momentum calculation methodology follows the academic standard:

Momentum(t) = / P(t-n) × 100

Where P(t) is the current price and n is the lookback period.

The focus on the "Magnificent 7" stocks reflects the increasing market concentration observed in recent years. Fama and French (2015) noted that a small number of large-cap stocks can drive significant market movements due to their substantial index weights³. The combined market capitalization of these seven companies often exceeds 25% of the total S&P 500, making their collective momentum a critical market indicator.

Indicator Architecture

Core Components

1. Data Collection and Processing

The indicator employs robust data collection with error handling for missing or invalid security data. Each stock's momentum is calculated independently using the specified lookback period (default: 14 periods).

2. Composite Oscillator Calculation

Following Fama-French factor construction methodology, the indicator offers two weighting schemes:

- Equal Weight: Each active stock receives identical weighting (1/n)

- Market Cap Weight: Reserved for future enhancement

3. Oscillator Transformation Functions

The indicator provides five distinct oscillator types, each with established technical analysis foundations:

a) Momentum Oscillator (Default)

- Pure rate-of-change calculation

- Centered around zero

- Direct implementation of Jegadeesh & Titman methodology

b) RSI (Relative Strength Index)

- Wilder's (1978) relative strength methodology

- Transformed to center around zero for consistency

- Scale: -50 to +50

c) Stochastic Oscillator

- George Lane's %K methodology

- Measures current position within recent range

- Transformed to center around zero

d) Williams %R

- Larry Williams' range-based oscillator

- Inverse stochastic calculation

- Adjusted for zero-centered display

e) CCI (Commodity Channel Index)

- Donald Lambert's mean reversion indicator

- Measures deviation from moving average

- Scaled for optimal visualization

Operational Modes

Mode 1: Magnificent 7 Analysis

Tracks the collective momentum of the seven constituent stocks. This mode is optimal for:

- Technology sector analysis

- Growth stock momentum assessment

- Large-cap performance tracking

Mode 2: S&P 500 Equal Weight Comparison

Analyzes momentum using an equal-weighted S&P 500 reference (typically RSP ETF). This mode provides:

- Broader market momentum context

- Size-neutral market analysis

- Comparison baseline for relative performance

Mode 3: Relative Performance Analysis

Calculates the momentum differential between Magnificent 7 and S&P 500 Equal Weight. This mode enables:

- Sector rotation analysis

- Style factor assessment (Growth vs. Value)

- Relative strength identification

Formula: Relative Performance = MAG7_Momentum - SP500EW_Momentum

Signal Generation and Thresholds

Signal Classification

The indicator generates three signal states:

- Bullish: Oscillator > Upper Threshold (default: +2.0%)

- Bearish: Oscillator < Lower Threshold (default: -2.0%)

- Neutral: Oscillator between thresholds

Relative Performance Signals

In relative performance mode, specialized thresholds apply:

- Outperformance: Relative momentum > +1.0%

- Underperformance: Relative momentum < -1.0%

Alert System

Comprehensive alert conditions include:

- Threshold crossovers (bullish/bearish signals)

- Zero-line crosses (momentum direction changes)

- Relative performance shifts

- Breadth Analysis Component

The indicator incorporates market breadth analysis, calculating the percentage of constituent stocks with positive momentum. This feature provides insights into:

- Strong Breadth (>60%): Broad-based momentum

- Weak Breadth (<40%): Narrow momentum leadership

- Mixed Breadth (40-60%): Neutral momentum distribution

Visual Design and User Interface

Theme-Adaptive Display

The indicator automatically adjusts color schemes for dark and light chart themes, ensuring optimal visibility across different user preferences.

Professional Data Table

A comprehensive data table displays:

- Current oscillator value and percentage

- Active mode and oscillator type

- Signal status and strength

- Component breakdowns (in relative performance mode)

- Breadth percentage

- Active threshold levels

Custom Color Options

Users can override default colors with custom selections for:

- Neutral conditions (default: Material Blue)

- Bullish signals (default: Material Green)

- Bearish signals (default: Material Red)

Practical Applications

Portfolio Management

- Sector Allocation: Use relative performance mode to time technology sector exposure

- Risk Management: Monitor breadth deterioration as early warning signal

- Entry/Exit Timing: Utilize threshold crossovers for position sizing decisions

Market Analysis

- Trend Identification: Zero-line crosses indicate momentum regime changes

- Divergence Analysis: Compare MAG7 performance against broader market

- Volatility Assessment: Oscillator range and frequency provide volatility insights

Strategy Development

- Factor Timing: Implement growth factor timing strategies

- Momentum Strategies: Develop systematic momentum-based approaches

- Risk Parity: Use breadth metrics for risk-adjusted portfolio construction

Configuration Guidelines

Parameter Selection

- Momentum Period (5-100): Shorter periods (5-20) for tactical analysis, longer periods (50-100) for strategic assessment

- Smoothing Period (1-50): Higher values reduce noise but increase lag

- Thresholds: Adjust based on historical volatility and strategy requirements

Timeframe Considerations

- Daily Charts: Optimal for swing trading and medium-term analysis

- Weekly Charts: Suitable for long-term trend analysis

- Intraday Charts: Useful for short-term tactical decisions

Limitations and Considerations

Market Concentration Risk

The indicator's focus on seven stocks creates concentration risk. During periods of significant rotation away from large-cap technology stocks, the indicator may not represent broader market conditions.

Momentum Persistence

While momentum effects are well-documented, they are not permanent. Jegadeesh and Titman (1993) noted momentum reversal effects over longer time horizons (2-5 years).

Correlation Dynamics

During market stress, correlations among the constituent stocks may increase, reducing the diversification benefits and potentially amplifying signal intensity.

Performance Metrics and Backtesting

The indicator includes hidden plots for comprehensive backtesting:

- Individual stock momentum values

- Composite breadth percentage

- S&P 500 Equal Weight momentum

- Relative performance calculations

These metrics enable quantitative strategy development and historical performance analysis.

References

¹Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. Journal of Finance, 48(1), 65-91.

Carhart, M. M. (1997). On persistence in mutual fund performance. Journal of Finance, 52(1), 57-82.

Fama, E. F., & French, K. R. (2015). A five-factor asset pricing model. Journal of Financial Economics, 116(1), 1-22.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

ابحث في النصوص البرمجية عن "backtest"

System 0530 - Stoch RSI Strategy with ATR filterStrategy Description: System 0530 - Multi-Timeframe Stochastic RSI with ATR Filter

Overview:

This strategy, "System 0530," is designed to identify trading opportunities by leveraging the Stochastic RSI indicator across two different timeframes: a shorter timeframe for initial signal triggers (assumed to be the chart's current timeframe, e.g., 5-minute) and a longer timeframe (15-minute) for signal confirmation. It incorporates an ATR (Average True Range) filter to help ensure trades are taken during periods of adequate market volatility and includes a cooldown mechanism to prevent rapid, successive signals in the same direction. Trade exits are primarily handled by reversing signals.

How It Works:

1. Signal Initiation (e.g., 5-Minute Timeframe):

Long Signal Wait: A potential long entry is considered when the 5-minute Stochastic RSI %K line crosses above its %D line, AND the %K value at the time of the cross is at or below a user-defined oversold level (default: 30).

Short Signal Wait: A potential short entry is considered when the 5-minute Stochastic RSI %K line crosses below its %D line, AND the %K value at the time of the cross is at or above a user-defined overbought level (default: 70). When these conditions are met, the strategy enters a "waiting state" for confirmation from the 15-minute timeframe.

2. Signal Confirmation (15-Minute Timeframe):

Once in a waiting state, the strategy looks for confirmation on the 15-minute Stochastic RSI within a user-defined number of 5-minute bars (wait_window_5min_bars, default: 5 bars).

Long Confirmation:

The 15-minute Stochastic RSI %K must be greater than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be below a user-defined threshold (stoch_15min_long_entry_level, default: 40).

Short Confirmation:

The 15-minute Stochastic RSI %K must be less than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be above a user-defined threshold (stoch_15min_short_entry_level, default: 60).

3. Filters:

ATR Volatility Filter: If enabled, trades are only confirmed if the current ATR value (converted to ticks) is above a user-defined minimum threshold (min_atr_value_ticks). This helps to avoid taking signals during periods of very low market volatility. If the ATR condition is not met, the strategy continues to wait for the condition to be met within the confirmation window, provided other conditions still hold.

Signal Cooldown Filter: If enabled, after a signal is generated, the strategy will wait for a minimum number of bars (min_bars_between_signals) before allowing another signal in the same direction. This aims to reduce overtrading.

4. Entry and Exit Logic:

Entry: A strategy.entry() order is placed when all trigger, confirmation, and filter conditions are met.

Exit: This strategy primarily uses reversing signals for exits. For example, if a long position is open, a confirmed short signal will close the long position and open a new short position. There are no explicit take profit or stop loss orders programmed into this version of the script.

Key User-Adjustable Parameters:

Stochastic RSI Parameters: RSI Length, Stochastic RSI Length, %K Smoothing, %D Smoothing.

Signal Trigger & Confirmation:

5-minute %K trigger levels for long and short.

15-minute %K confirmation thresholds for long and short.

Wait window (in 5-minute bars) for 15-minute confirmation.

Filters:

Enable/disable and configure the Signal Cooldown filter (minimum bars between signals).

Enable/disable and configure the ATR Volatility filter (ATR period, minimum ATR value in ticks).

Strategy Parameters:

Leverage Multiplier (Note: This primarily affects theoretical position sizing for backtesting calculations in TradingView and does not simulate actual leveraged trading risks).

Recommendations for Users:

Thorough Backtesting: Test this strategy extensively on historical data for the instruments and timeframes you intend to trade.

Parameter Optimization: Experiment with different parameter settings to find what works best for your trading style and chosen markets. The default values are starting points and may not be optimal for all conditions.

Understand the Logic: Ensure you understand how each component (Stochastic RSI on different timeframes, ATR filter, cooldown) interacts to generate signals.

Risk Management: Since this version does not include explicit stop-loss orders, ensure you have a clear risk management plan in place if trading this strategy live. You might consider manually adding stop-loss orders through your broker or using TradingView's separate strategy order settings for stop-loss if applicable.

Disclaimer:

This strategy description is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Trading involves significant risk of loss. Always do your own research and understand the risks before trading.

AutoFib Breakout Strategy for Uptrend AssetsThis trading strategy is designed to help you catch powerful upward moves on assets that are in a long-term uptrend, such as Gold (XAUUSD). It uses a popular technical tool called the Fibonacci Extension, combined with a trend filter and a risk-managed exit system.

✅ When to Use This Strategy

• Works best on higher timeframes: Daily (1D), 3-Day (3D), or Weekly (W).

• Best used on uptrending assets like Gold.

• Designed for swing trading – holding trades from a few days to weeks.

📊 How It Works

1. Find the Trend

We only want to trade in the direction of the trend.

• The strategy uses the 200-period EMA (Exponential Moving Average) to identify if the market is in an uptrend.

• If the price is above the 200 EMA, we consider it an uptrend and allow long trades.

2. Identify Breakout Levels

• The strategy detects recent high and low pivot points to draw Fibonacci extension levels.

• It focuses on the 1.618 Fibonacci level, which is often a target in strong trends.

• When the price breaks above this level in an uptrend, it signals a potential momentum breakout – a good time to buy.

3. Enter a Trade

• The strategy enters a long (buy) position when the price closes above the 1.618 Fibonacci level and the market is in an uptrend (above the 200 EMA).

4. Manage Risk Automatically

• The trade includes a stop-loss set to 1x the ATR (Average True Range) below the entry price – this protects against sudden drops.

• It sets a take-profit at 3x the ATR above the entry – aiming for higher rewards than risks.

⚠️ Important Notes

• 📈 Higher Timeframes Preferred: This strategy works best on Daily (D), 3-Day (3D), and Weekly (W) charts, especially on Gold (XAUUSD).

• 🧪 Not for Deep Backtesting: Due to the nature of how pivot points and Fib levels are calculated, this strategy may not perform well in backtesting simulations (because the historical calculations can shift). It is better used for live analysis and forward testing.

[blackcat] L3 Projected Magic-9 SequenceOVERVIEW

The L3 Projected Magic-9 Sequence indicator is a sophisticated tool designed to help traders identify potential trend reversals through a unique sequence of price movements. By calculating projected highs and lows based on previous bar conditions, this script provides valuable insights into possible future market directions. It plots these key levels on the chart and highlights specific sequential patterns that often precede significant reversals, offering traders a visual advantage in their decision-making process 📈💡.

FEATURES

Projections: Calculates and plots projected highs and lows based on intricate conditions derived from previous bars' open, close, high, and low prices. These projections serve as dynamic support and resistance levels, helping traders anticipate potential turning points in the market 📊.

Sequential Patterns:

Identifies various sequential patterns known as "Magic" sequences, such as Magic-9 and Magic-13.

Labels these sequences directly on the chart for easy identification: 5, 6, 7, 8, 9, 12, 13 for both bullish and bearish trends.

Provides additional labels when these sequences align with projected highs or lows, enhancing the reliability of the signal 🏷️.

Differentiates between trend and sideways phases using the Magic-9 Project Range. Traditional sequences generating buy and sell signals of 9 and 13 during sideways swings are displayed indistinguishably from other numbers. However, the 9 and 13 generated by breakouts are highlighted with red and green labels for better visibility 🚦.

Project Range Adjustment:

The Project Range is automatically adjusted by Multiple Time Frame (MTF).

A higher cycle is selected as the baseline of the Project Range based on the current operating cycle, ensuring adaptability to varying market conditions ⏳.

Customization:

Offers customizable colors for plotted lines and labels, allowing users to tailor the appearance to their preferences 🎨.

Adjustable settings for lookback periods and other parameters to fine-tune the indicator according to individual trading styles.

Automatic Timeframe Selection:

Automatically selects the most suitable timeframe for data fetching, ensuring optimal performance across different chart intervals ⏳.

Ensures compatibility with various trading strategies, whether short-term intraday or long-term positional trading.

HOW TO USE

Adding the Indicator:

Open your TradingView platform and navigate to the chart where you want to apply the indicator.

Click on the "Indicators" button at the top of the screen and search for L3 Projected Magic-9 Sequence.

Select the indicator from the list and add it to your chart.

Understanding Projections:

Once added, observe the plotted projected highs and lows on your chart.

These lines represent anticipated support and resistance levels based on complex calculations involving previous bar data.

Identifying Sequential Patterns:

Look for labels such as 5, 6, 7, 8, 9, 12, and 13 appearing on the chart.

These labels signify specific sequential patterns that often precede market reversals.

Pay special attention to labels that include arrows (e.g., 9▼, 13▲), indicating alignment with projected highs or lows.

Note the differentiation between trend and sideways phases:

During sideways swings, traditional sequences generating buy and sell signals of 9 and 13 are displayed indistinguishably from other numbers.

Breakout-generated 9 and 13 are highlighted with red and green labels for clear identification.

Combining with Other Tools:

While the L3 Projected Magic-9 Sequence offers powerful insights, it is essential to combine its signals with other technical analysis tools.

Use moving averages, volume indicators, or candlestick patterns to confirm the validity of the identified sequences before executing trades.

LIMITATIONS

Market Conditions: The indicator performs best in trending markets but may generate false signals during periods of consolidation or range-bound movement 🌐.

Complexity: Due to its reliance on specific sequential patterns, some traders might find the concept challenging to grasp initially. Thorough testing and understanding are crucial before deploying it in live trading environments.

Data Dependency: Accurate projections depend on having sufficient historical data. Insufficient data may lead to less reliable results.

NOTES

Backtesting: Before implementing the indicator in real-time trading, conduct extensive backtesting to evaluate its effectiveness under various market conditions.

Risk Management: Always adhere to proper risk management principles, even when relying on robust indicators like this one. Set stop-loss orders and position sizes accordingly to protect your capital 🛡️.

Continuous Learning: Stay updated with the latest developments and adjustments made to the indicator by following community discussions and official updates from the author.

BIN Based Support and Resistance [SS]This indicator presents a version of an alternative way to determine support and resistance, using a method called "Bins".

Bins provide for a flexible and interesting way to determine support and resistance levels.

First off, let's discuss BINS:

Bins are ranges or containers into which your data points can be sorted. For example, if you're grouping ages, you might have bins like 0–18, 19–35, 36–50, and 51+. Any data point within these intervals gets placed in the corresponding bin.

Binning simplifies complex data sets by grouping values into categories. This is useful for such things as

Visualizing data in histograms or bar charts.

Reducing noise and highlighting trends.

This indicator groups the price action into 10 separate bins. It determines the Support / Resistance level by averaging the values in the Bins to find an iteration of the "central tendency" or average reoccurring value.

Pros and Cons

Since this is a different approach to support and resistance, I think its important to highlight some of the pros and advantages, but also be open about the cons.

First off the PROS

Bin Based Support and Resistance Levels dynamically adjust to ranges as opposed to hard / fast peaks and valleys. This makes them better at analyzing price action vs simply drawing lines at random peaks and valleys.

Because Bins are analyzing ALL PA within a period's max and min range, Bin Support and Resistance can actually be used similar to Volume profile, where you are able to identify a pseudo-POC, or areas where price tends to consolidate. Take a look at this example on SPY:

You can see these 2 SR lines are close together. This represents that this general price range is an area where price likes to accumulate/consolidate. You can see the SPY ended up coming back to this range and consolidating there for a bit.

This is a strength of using a BIN based approach to calculating support and resistance, because as indicated before, it looks at price action vs peaks and valleys.

As a tip, these areas are areas you want to wait for a break in one direction or the other.

The indicator provides for backtest results of the support and resistance lines, to see how many times certain areas acted as resistance or support. Because this is analyzing and distributing PA evenly throughout the period's max and min, the indicator can tell you which areas tend to have higher rejection zones and which have higher support zones.

Now the CONS

Because bin based SR take an average approach, the SR lines can sometimes be slightly broken before the ticker finds rejection:

To combat this, make sure there is confirmed support. How the indicator actually backtests these lines is by waiting to see if the ticker has 3 consecutive closes above the support line or below the resistance line. So these are things to be mindful of.

It doesn't consider pivots. Most support and resistance indicators either identify max and min peaks and valleys or use pivot points. Pivot points are a great way to identify peaks and valleys and thus by extension support and resistance. However, this is also somewhat of a strength, as using BINS forces the indicator to consider ALL price action and not just the extremes (highs and lows).

Can be slightly skewed in highly volatile environments. Any time there is a massive drop or rally, it can skew the indicator to give extreme ranges to both ends. For example, the Tariff news collapse on ES1!:

Owning to limitations in lookback length, sometimes the min and max range can be exceeded and other traditional areas of support / resistance is where a ticker will find support.

Using the indicator

Here are some basic use/functionalities of the indicator:

Selecting display of backtest results: You can select to have the backtest results shown in a table:

Or directly on the lines:

Inversely, you can toggle them off completely:

You can modify the lookback length. The suggested lookback length is between 250 to 500 candles on smaller timeframes. I also suggest 252 on daily timeframes (which represents 1 trading year).

And that's the indicator!

It is very easy to use, so you should pick it up in no time!

Enjoy and as always, 🚀🚀 safe trades! 🚀🚀

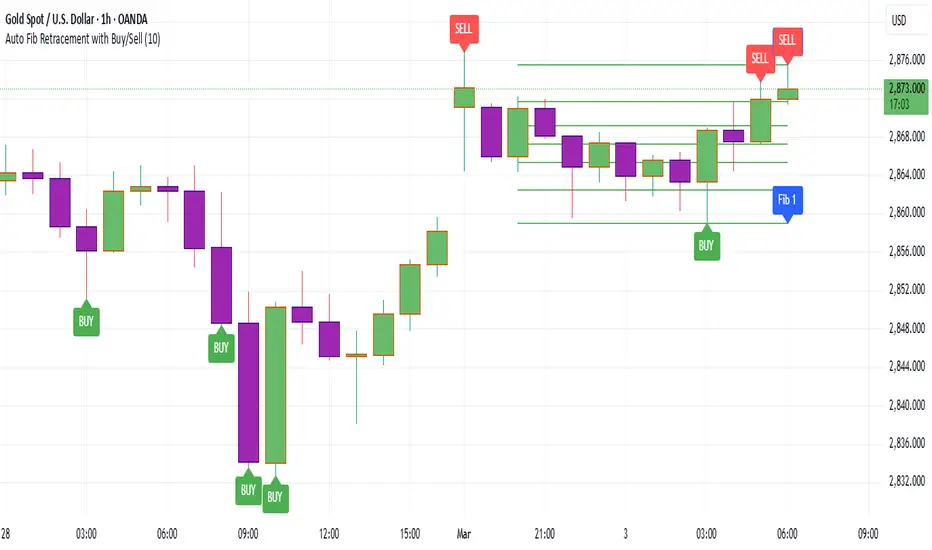

Auto Fib Retracement with Buy/SellKey Features of the Advanced Script:

Multi-Timeframe (MTF) Analysis:

We added an input for the higher timeframe (higher_tf), where the trend is checked on a higher timeframe to confirm the primary trend direction.

Complex Trend Detection:

The trend is determined not only by the current timeframe but also by the trend on the higher timeframe, giving a more comprehensive and reliable signal.

Dynamic Fibonacci Levels:

Fibonacci lines are plotted dynamically, extending them based on price movement, with the Fibonacci retracement drawn only when a trend is identified.

Background Color & Labels:

A background color is added to give a clear indication of the trend direction. Green for uptrend, red for downtrend. It makes it visually easier to understand the current market structure.

"Buy" or "Sell" labels are shown directly on the chart to mark possible entry points.

Strategy and Backtesting:

The script includes strategy commands (strategy.entry and strategy.exit), which allow for backtesting the strategy in TradingView.

Stop loss and take profit conditions are added (loss=100, profit=200), which can be adjusted according to your preferences.

Next Steps:

Test with different timeframes: Try changing the higher_tf to different timeframes (like "60" or "240") and see how it affects the trend detection.

Adjust Fibonacci settings: Modify how the Fibonacci levels are calculated or add more Fibonacci levels like 38.2%, 61.8%, etc.

Optimize Strategy Parameters: Fine-tune the entry/exit logic by adjusting stop loss, take profit, and other strategy parameters.

This should give you a robust foundation for creating advanced trend detection strategies

Custom Buy and Sell Signal with Body Ratio and RSI

Indicator Overview:

Name: Custom Buy and Sell Signal with Body Ratio and RSI

Description: This indicator is designed to detect buy and sell opportunities by analyzing the body size and wicks of candles in combination with the RSI indicator and volume. It helps identify trend reversals under high-volume market conditions, which enhances the reliability of the signals.

Indicator Features:

RSI (Relative Strength Index): The RSI indicator is used to assess oversold (RSI < 40) or overbought (RSI > 60) conditions. These zones signal potential reversals when combined with other technical signals.

Candle Body Analysis:

The indicator compares the size of the current and previous candles to validate signals.

For a buy signal, the current candle must be bullish and have a body size proportional to that of the previous bearish candle.

Similarly, for a sell signal, the current candle must be bearish with a body size comparable to the previous bullish candle.

Wick Validation:

The indicator analyzes the wick length to reinforce or exclude signals.

For a buy signal, the lower wick of the bullish candle must be shorter than that of the previous bearish candle.

For a sell signal, the upper wick of the bearish candle must be shorter than that of the previous bullish candle and smaller than 30% of the candle's body.

High Volume:

Signals are only generated when the volume exceeds a certain threshold, ensuring that signals are issued in active market conditions.

The minimum volume should be adjusted based on the asset. For example, for gold, a minimum volume of 9000 is recommended.

Trading Strategy:

Buy Signals:

A bearish (red) candle is followed by a bullish (green) candle with a body size that is comparable to the previous candle (0.9 to 3 times the body size).

The lower wick of the bullish candle is shorter than that of the previous bearish candle, confirming the validity of the signal.

The RSI must be below 40, indicating an oversold condition.

The volume must exceed the defined threshold (e.g., > 9000 for gold) to confirm an active market.

Sell Signals:

A bullish (green) candle is followed by a bearish (red) candle with a comparable body size.

The upper wick of the bearish candle must be shorter than that of the previous bullish candle and must not exceed 30% of the body size.

The RSI must be above 60, indicating an overbought condition.

The volume must also exceed the minimum threshold for a valid signal.

Usage Guidelines:

Volume Adjustment: It is crucial to adjust the volume threshold depending on the asset you're trading. For example, for assets like gold, a minimum volume of 9000 is recommended to filter out weak signals. Each asset has a different volume dynamic, so test different thresholds on historical data to find the optimal setting.

Time Frame:

It is recommended to use this indicator on a 1-hour (1H) chart for the best signal relevance. This time frame provides a good balance between reactivity and filtering false signals.

Confluence:

Combine the signals from this indicator with other tools like support and resistance levels, moving averages, or chart patterns to increase your chances of success. Confluence of indicators improves the reliability of signals.

Risk Management:

Implement strict risk management. Use stop-losses based on volatility, such as ATR (Average True Range), or the wick size to determine exit points.

Backtesting:

Before using it live, conduct backtesting on various assets to fine-tune the parameters, especially the volume threshold, and to verify performance across different market conditions.

This indicator is an excellent tool for traders looking to identify trend reversals based on solid technical criteria such as RSI, candle structure, and volume. It is particularly effective on volatile assets with precise volume adjustment.

Multi-Moving Average Buy/Sell IndicatorThis Multi-Moving Average Buy/Sell Indicator is a powerful and customizable tool designed to help traders identify potential buy and sell signals based on the interaction between price and multiple moving averages. Whether you're a day trader, swing trader, or long-term investor, this indicator provides clear visual cues and alerts to help you make informed trading decisions.

Key Features

1. Multiple Moving Averages

The indicator calculates four key moving averages:

9-period MA

20-period MA

50-period MA

180-period MA

You can choose the type of moving average:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

2. Custom Timeframe

Select a custom timeframe from a user-friendly dropdown menu:

1 Minute

5 Minutes

15 Minutes

30 Minutes

1 Hour

4 Hours

Daily

Weekly

The indicator dynamically adjusts to the selected timeframe, making it suitable for all trading styles.

3. Buy/Sell Signals

Buy Signal: Triggered when the price crosses above any of the moving averages.

Sell Signal: Triggered when the price crosses below any of the moving averages.

Signals are displayed as labels on the chart:

Green "BUY" Label: Below the bar when a buy signal is triggered.

Red "SELL" Label: Above the bar when a sell signal is triggered.

4. Visualization

Toggle the visibility of all moving averages using the showAllMAs input.

Moving averages are plotted with distinct colors for easy identification:

9 MA: Blue

20 MA: Orange

50 MA: Purple

180 MA: Teal

5. Alerts

The indicator generates alerts for buy and sell signals, which can be used for notifications or automated trading.

How to Use

Add the Indicator:

Open TradingView and go to the Pine Script Editor.

Copy and paste the script into the editor.

Click Add to Chart.

Configure Inputs:

maType: Choose the type of moving average (SMA, EMA, WMA).

timeframe: Select a custom timeframe (e.g., "1 Minute", "Daily").

showSignals: Toggle to show or hide buy/sell signals.

showAllMAs: Toggle to show or hide all moving averages.

Interpret the Signals:

Look for green "BUY" labels below the bars for potential buy opportunities.

Look for red "SELL" labels above the bars for potential sell opportunities.

Set Alerts:

Use the built-in alert system to get notified when buy or sell signals are triggered.

Example Use Cases

Day Trading

Use a 1-minute or 5-minute timeframe with an EMA for quick signals.

Example Inputs:

maType = "EMA"

timeframe = "5 Minutes"

showAllMAs = true

Swing Trading

Use a daily timeframe with an SMA for longer-term signals.

Example Inputs:

maType = "SMA"

timeframe = "Daily"

showAllMAs = false

Why Use This Indicator?

Versatility: Suitable for all trading styles and timeframes.

Customization: Choose your preferred moving average type and timeframe.

Clear Signals: Easy-to-read buy/sell labels and moving averages.

Alerts: Never miss a trading opportunity with built-in alerts.

Limitations

False Signals:

The indicator may generate false signals in choppy or sideways markets. Always combine it with other tools (e.g., RSI, volume analysis) for better accuracy.

Timeframe Dependency:

The effectiveness of the signals depends on the selected timeframe. Shorter timeframes may produce more signals but with higher noise.

No Backtesting:

The script does not include backtesting functionality. Test the strategy manually on historical data.

Customization Options

Add More Moving Averages: Modify the script to include additional moving averages (e.g., 200 MA).

Change Signal Logic: Adjust the conditions for buy/sell signals (e.g., require confirmation from multiple moving averages).

Add Alerts for Specific MAs: Create separate alerts for signals based on specific moving averages (e.g., only 9 MA or 50 MA).

High-Probability IndicatorExplanation of the Code

Trend Filter (EMA):

A 50-period Exponential Moving Average (EMA) is used to determine the overall trend.

trendUp is true when the price is above the EMA.

trendDown is true when the price is below the EMA.

Momentum Filter (RSI):

A 14-period RSI is used to identify overbought and oversold conditions.

oversold is true when RSI ≤ 30.

overbought is true when RSI ≥ 70.

Volatility Filter (ATR):

A 14-period Average True Range (ATR) is used to measure volatility.

ATR is multiplied by a user-defined multiplier (default: 2.0) to set a volatility threshold.

Ensures trades are only taken during periods of sufficient volatility.

Entry Conditions:

Long Entry: Price is above the EMA (uptrend), RSI is oversold, and the candle range exceeds the ATR threshold.

Short Entry: Price is below the EMA (downtrend), RSI is overbought, and the candle range exceeds the ATR threshold.

Exit Conditions:

Take Profit: A fixed percentage above/below the entry price.

Stop Loss: A fixed percentage below/above the entry price.

Visualization:

The EMA is plotted on the chart.

Background colors highlight uptrends and downtrends.

Buy and sell signals are displayed as labels on the chart.

Alerts:

Alerts are triggered for buy and sell signals.

How to Use the Indicator

Trend Filter:

Only take trades in the direction of the trend (e.g., long in an uptrend, short in a downtrend).

Momentum Filter:

Look for oversold conditions in an uptrend for long entries.

Look for overbought conditions in a downtrend for short entries.

Volatility Filter:

Ensure the candle range exceeds the ATR threshold to avoid low-volatility trades.

Risk Management:

Use the built-in take profit and stop loss levels to manage risk.

Optimization Tips

Backtesting:

Test the indicator on multiple timeframes and assets to evaluate its performance.

Adjust the input parameters (e.g., EMA length, RSI length, ATR multiplier) to optimize for specific markets.

Combination with Other Strategies:

Add additional filters, such as volume analysis or support/resistance levels, to improve accuracy.

Risk Management:

Use proper position sizing and risk-reward ratios to maximize profitability.

Disclaimer

No indicator can guarantee an 85% win ratio due to the inherent unpredictability of financial markets. This script is provided for educational purposes only. Always conduct thorough backtesting and paper trading before using any strategy in live trading.

Let me know if you need further assistance or enhancements!

PDF MA For Loop [BackQuant]PDF MA For Loop

Introducing the PDF MA For Loop, an innovative trading indicator that combines Probability Density Function (PDF) smoothing with a dynamic for-loop scoring mechanism. This advanced tool provides traders with precise trend-following signals, helping to identify long and short opportunities with improved clarity and adaptability to market conditions.

If you would like to check out the stand alone PDF Moving Average:

Core Concept: Probability Density Function (PDF) Smoothing

The PDF smoothing method is a unique approach that applies adaptive weights to price data based on a Probability Density Function. This ensures that recent data points receive appropriate emphasis while maintaining a smooth transition across the data set. The result is a moving average that is not only smoother but also more responsive to market changes.

Key parameters in PDF smoothing:

Variance : Controls the spread of the PDF, where a higher value results in broader smoothing and a lower value makes the moving average more sensitive.

Mean : Centers the PDF around a specific value, influencing the weighting and responsiveness of the smoothing process.

By combining PDF smoothing with traditional moving averages (EMA or SMA), the indicator creates a hybrid signal that balances responsiveness and reliability.

For-Loop Scoring Mechanism

At the heart of this indicator is the for-loop scoring mechanism, which evaluates the smoothed PDF moving average over a defined range of historical data points. This process assigns a score to the current market condition based on whether the PDF moving average is greater than or less than previous values.

Long Signal: A long signal is generated when the score exceeds the Long Threshold (default set at 40), indicating upward momentum.

Short Signal: A short signal is triggered when the score crosses below the Short Threshold (default set at -10), suggesting potential downward momentum.

This dynamic scoring system ensures that the indicator remains adaptive, capturing trends and shifts in market sentiment effectively.

Customization Options

The PDF MA For Loop includes a variety of customizable settings to fit different trading styles and strategies:

Calculation Settings

Price Source : Select the input price for the calculation (default is the close price).

Smoothing Method : Choose between EMA or SMA for the additional smoothing layer, providing flexibility to adapt to market conditions.

Smoothing Period : Adjust the lookback period for the smoothing function, with shorter periods providing more sensitivity and longer periods offering greater stability.

Variance & Mean : Fine-tune the PDF function parameters to control the weighting of the smoothing process.

Signal Settings

Thresholds : Customize the upper and lower thresholds to define the sensitivity of the long and short signals.

For Loop Range : Set the range of historical data points analyzed by the for-loop, influencing the depth of the scoring mechanism.

UI Settings

Signal Line Width: Adjust the thickness of the plotted signal line for better visibility.

Candle Coloring: Enable or disable the coloring of candlesticks based on trend direction (green for long, red for short, gray for neutral).

Background Coloring: Add background shading to highlight long and short signals for an enhanced visual experience.

Alerts and Automation

The indicator includes built-in alert conditions to notify traders of important market events:

Long Signal Alert: Notifies when the score exceeds the upper threshold, indicating a bullish trend.

Short Signal Alert: Notifies when the score crosses below the lower threshold, signaling a bearish trend.

These alerts can be configured for real-time notifications, allowing traders to respond quickly to market changes without constant chart monitoring.

Trading Applications

The PDF MA For Loop is versatile and can be applied across various trading strategies and market conditions:

Trend Following: The PDF smoothing method combined with for-loop scoring makes this indicator particularly effective for identifying and following trends.

Reversal Trading: By observing the thresholds and score, traders can anticipate potential reversals when the trend shifts from long to short (or vice versa).

Risk Management: The dynamic thresholds and scoring provide clear signals, allowing traders to enter and exit trades with greater confidence and precision.

Final Thoughts

The PDF MA For Loopis merges advanced mathematical concepts with practical trading tools. By leveraging Probability Density Function smoothing and a dynamic for-loop scoring system, it provides traders with clear, actionable signals while adapting to market conditions.

Whether you’re looking for an edge in trend-following strategies or seeking precision in identifying reversals, this indicator offers the flexibility and power to enhance your trading decisions

As always, backtesting and integrating the PDF MA For Loop into a comprehensive trading strategy is recommended for optimal performance, as no single indicator should be used in isolation.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

FS Scorpion TailKey Features & Components:

1. Custom Date & Chart-Based Controls

The software allows users to define whether they want signals to start on a specific date (useSpecificDate) or base calculations on the visible chart’s range (useRelativeScreenSumLeft and useRelativeScreenSumRight).

Users can input the number of stocks to buy/sell per signal and decide whether to sell only for profit.

2. Technical Indicators Used

EMA (Exponential Moving Average): Users can define the length of the EMA and specify if buy/sell signals should occur when the EMA is rising or falling.

MACD (Moving Average Convergence Divergence): MACD crossovers, slopes of the MACD line, signal line, and histogram are used for generating buy/sell signals.

ATR (Average True Range): Signals are generated based on rising or falling ATR.

Aroon Indicator: Buy and sell signals are based on the behavior of the Aroon upper and lower lines.

RSI (Relative Strength Index): Tracks whether the RSI and its moving average are rising or falling to generate signals.

Bollinger Bands: Buy/sell signals depend on the basis, upper, and lower band behavior (rising or falling).

3. Signal Detection

The software creates arrays for each indicator to store conditions for buy/sell signals.

The allTrue() function checks whether all conditions for buy/sell signals are true, ensuring that only valid signals are plotted.

Signals are differentiated between buy-only, sell-only, and both buy and sell (dual signal).

4. Visual Indicators

Vertical Lines: When buy, sell, or dual signals are detected, vertical lines are drawn at the corresponding bar with configurable colors (green for buy, red for sell, silver for dual).

Buy/Sell Labels: Visual labels are plotted directly on the chart to denote buy or sell signals, allowing for clear interpretation of the strategy.

5. Cash Flow & Metrics Display

The software maintains an internal ledger of how many stocks are bought/sold, their prices, and whether a profit is being made.

A table is displayed at the bottom right of the chart, showing:

Initial investment

Current stocks owned

Last buy price

Market stake

Net profit

The table background turns green for profit and red for loss.

6. Dynamic Decision Making

Buy Condition: If a valid buy signal is generated, the software decrements the cash balance and adds stocks to the inventory.

Sell Condition: If the sell signal is valid (and meets the profit requirement), stocks are sold, and cash is incremented.

A fallback check ensures the sell logic prevents selling more stocks than are available and adjusts stock holding appropriately (e.g., sell half).

Customization and Usage

Indicator Adjustments: The user can choose which indicators to activate (e.g., EMA, MACD, RSI) via input controls. Each indicator has specific customizable parameters such as lengths, slopes, and conditions.

Signal Flexibility: The user can adjust conditions for buying and selling based on various technical indicators, which adds flexibility in implementing trading strategies. For example, users may require the RSI to be higher than its moving average or trigger sales only when MACD crosses under the signal line.

Profit Sensitivity: The software allows the option to sell only when a profit is assured by checking if the current price is higher than the last buy price.

Summary of Usage:

Indicator Selection: Enable or disable technical indicators like EMA, MACD, RSI, Aroon, ATR, and Bollinger Bands to fit your trading strategy.

Custom Date/Chart Settings: Choose whether to calculate based on specific time ranges or visible portions of the chart.

Dynamic Signal Plotting: Once buy or sell conditions are met, the software will visually plot signals on your chart, giving clear entry and exit points.

Investment Tracking: Real-time tracking of stock quantities, investments, and profit ensures a clear view of your trading performance.

Backtesting: Use this software for backtesting your strategy by analyzing how buy and sell signals would have performed historically based on the chosen indicators.

Conclusion

The FS Scorpion Tail software is a robust and flexible trading tool, allowing traders to develop custom strategies based on multiple well-known technical indicators. Its visual aid, coupled with real-time investment tracking, makes it valuable for systematic traders looking to automate or refine their trading approach.

Savitzky Golay Median Filtered RSI [BackQuant]Savitzky Golay Median Filtered RSI

Introducing BackQuant's Savitzky Golay Median Filtered RSI, a cutting-edge indicator that enhances the classic Relative Strength Index (RSI) by applying both a Savitzky-Golay filter and a median filter to provide smoother and more reliable signals. This advanced approach helps reduce noise and captures true momentum trends with greater precision. Let’s break down how the indicator works, the features it offers, and how it can improve your trading strategy.

Core Concept: Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a widely used momentum oscillator that measures the speed and change of price movements. It oscillates between 0 and 100, with levels above 70 typically indicating overbought conditions and levels below 30 indicating oversold conditions. However, the standard RSI can sometimes generate noisy signals, especially in volatile markets, making it challenging to identify reliable entry and exit points.

To improve upon the traditional RSI, this indicator introduces two powerful filters: the Savitzky-Golay filter and a median filter.

Savitzky-Golay Filter: Smoothing with Precision

The Savitzky-Golay filter is a digital filtering technique used to smooth data while preserving important features, such as peaks and trends. Unlike simple moving averages that can distort important price data, the Savitzky-Golay filter uses polynomial regression to fit the data, providing a more accurate and less lagging result.

In this script, the Savitzky-Golay filter is applied to the RSI values to smooth out short-term fluctuations and provide a more reliable signal. By using a window size of 5 and a polynomial degree of 2, the filter effectively reduces noise without compromising the integrity of the underlying price movements.

Median Filter: Reducing Outliers

After applying the Savitzky-Golay filter, the median filter is applied to the smoothed RSI values. The median filter is particularly effective at removing short-lived outliers, further enhancing the accuracy of the RSI by reducing the impact of sudden and temporary price spikes or drops. This combination of filters creates an ultra-smooth RSI that is better suited for detecting true market trends.

Long and Short Signals

The Savitzky Golay Median Filtered RSI generates long and short signals based on user-defined threshold levels:

Long Signals: A long signal is triggered when the filtered RSI exceeds the Long Threshold (default set at 176). This indicates that momentum is shifting upward, and it may present a good buying opportunity.

Short Signals: A short signal is generated when the filtered RSI falls below the Short Threshold (default set at 162). This suggests that momentum is weakening, potentially signaling a selling opportunity or exit from a long position.

These threshold levels can be adjusted to suit different market conditions and timeframes, allowing traders to fine-tune the sensitivity of the indicator.

Customization and Visualization Options

The Savitzky Golay Median Filtered RSI comes with several customization options, enabling traders to tailor the indicator to their specific needs:

Calculation Source: Select the price source for the RSI calculation (default is OHLC4, but it can be changed to close, open, high, or low prices).

RSI Period: Adjust the lookback period for the RSI calculation (default is 14).

Median Filter Length: Control the length of the median filter applied to the smoothed RSI, affecting how much noise is removed from the signal.

Threshold Levels: Customize the long and short thresholds to define the sensitivity for generating buy and sell signals.

UI Settings: Choose whether to display the RSI and thresholds on the chart, color the bars according to trend direction, and adjust the line width and colors used for long and short signals.

Visual Feedback: Color-Coded Signals and Thresholds

To make the signals easier to interpret, the indicator offers visual feedback by coloring the price bars and the RSI plot according to the current market trend:

Green Bars indicate long signals when momentum is bullish.

Red Bars indicate short signals when momentum is bearish.

Gray Bars indicate neutral or undecided conditions when no clear signal is present.

In addition, the Long and Short Thresholds can be plotted directly on the chart to provide a clear reference for when signals are triggered, allowing traders to visually gauge the strength of the RSI relative to its thresholds.

Alerts for Automation

For traders who prefer automated notifications, the Savitzky Golay Median Filtered RSI includes built-in alert conditions for long and short signals. You can configure these alerts to notify you when a buy or sell condition is met, ensuring you never miss a trading opportunity.

Trading Applications

This indicator is versatile and can be used in a variety of trading strategies:

Trend Following: The combination of Savitzky-Golay and median filtering makes this RSI particularly useful for identifying strong trends without being misled by short-term noise. Traders can use the long and short signals to enter trades in the direction of the prevailing trend.

Reversal Trading: By adjusting the threshold levels, traders can use this indicator to spot potential reversals. When the RSI moves from overbought to oversold levels (or vice versa), it may signal a shift in market direction.

Swing Trading: The smoothed RSI provides a clear signal for short to medium-term price movements, making it an excellent tool for swing traders looking to capitalize on momentum shifts.

Risk Management: The filtered RSI can be used as part of a broader risk management strategy, helping traders avoid false signals and stay in trades only when the momentum is strong.

Final Thoughts

The Savitzky Golay Median Filtered RSI takes the classic RSI to the next level by applying advanced smoothing techniques that reduce noise and improve signal reliability. Whether you’re a trend follower, swing trader, or reversal trader, this indicator provides a more refined approach to momentum analysis, helping you make better-informed trading decisions.

As with all indicators, it is important to backtest thoroughly and incorporate sound risk management strategies when using the Savitzky Golay Median Filtered RSI in your trading system.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Chande Momentum Oscillator StrategyThe Chande Momentum Oscillator (CMO) Trading Strategy is based on the momentum oscillator developed by Tushar Chande in 1994. The CMO measures the momentum of a security by calculating the difference between the sum of recent gains and losses over a defined period. The indicator offers a means to identify overbought and oversold conditions, making it suitable for developing mean-reversion trading strategies (Chande, 1997).

Strategy Overview:

Calculation of the Chande Momentum Oscillator (CMO):

The CMO formula considers both positive and negative price changes over a defined period (commonly set to 9 days) and computes the net momentum as a percentage.

The formula is as follows:

CMO=100×(Sum of Gains−Sum of Losses)(Sum of Gains+Sum of Losses)

CMO=100×(Sum of Gains+Sum of Losses)(Sum of Gains−Sum of Losses)

This approach distinguishes the CMO from other oscillators like the RSI by using both price gains and losses in the numerator, providing a more symmetrical measurement of momentum (Chande, 1997).

Entry Condition:

The strategy opens a long position when the CMO value falls below -50, signaling an oversold condition where the price may revert to the mean. Research in mean-reversion, such as by Poterba and Summers (1988), supports this approach, highlighting that prices often revert after sharp movements due to overreaction in the markets.

Exit Conditions:

The strategy closes the long position when:

The CMO rises above 50, indicating that the price may have become overbought and may not provide further upside potential.

Alternatively, the position is closed 5 days after the buy signal is triggered, regardless of the CMO value, to ensure a timely exit even if the momentum signal does not reach the predefined level.

This exit strategy aligns with the concept of time-based exits, reducing the risk of prolonged exposure to adverse price movements (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages the well-known phenomenon of mean-reversion in financial markets. According to research by Jegadeesh and Titman (1993), prices tend to revert to their mean over short periods following strong movements, creating opportunities for traders to profit from temporary deviations.

The CMO captures this mean-reversion behavior by monitoring extreme price conditions. When the CMO reaches oversold levels (below -50), it signals potential buying opportunities, whereas crossing overbought levels (above 50) indicates conditions for selling.

Market Efficiency and Overreaction:

The strategy takes advantage of behavioral inefficiencies and overreactions, which are often the drivers behind sharp price movements (Shiller, 2003). By identifying these extreme conditions with the CMO, the strategy aims to capitalize on the market’s tendency to correct itself when price deviations become too large.

Optimization and Parameter Selection:

The 9-day period used for the CMO calculation is a widely accepted timeframe that balances responsiveness and noise reduction, making it suitable for capturing short-term price fluctuations. Studies in technical analysis suggest that oscillators optimized over such periods are effective in detecting reversals (Murphy, 1999).

Performance and Backtesting:

The strategy's effectiveness is confirmed through backtesting, which shows that using the CMO as a mean-reversion tool yields profitable opportunities. The use of time-based exits alongside momentum-based signals enhances the reliability of the strategy by ensuring that trades are closed even when the momentum signal alone does not materialize.

Conclusion:

The Chande Momentum Oscillator Trading Strategy combines the principles of momentum measurement and mean-reversion to identify and capitalize on short-term price fluctuations. By using a widely tested oscillator like the CMO and integrating a systematic exit approach, the strategy effectively addresses both entry and exit conditions, providing a robust method for trading in diverse market environments.

References:

Chande, T. S. (1997). The New Technical Trader: Boost Your Profit by Plugging into the Latest Indicators. John Wiley & Sons.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Volume-Supported Linear Regression Trend TableThe "Volume-Supported Linear Regression Trend Table" (VSLRT Table) script helps traders identify buy and sell opportunities by analyzing price trends and volume dynamics across multiple timeframes. It uses linear regression to calculate the trend direction and volume strength, visually representing this data with color-coded signals on the chart and in a table. Green signals indicate buying opportunities, while red signals suggest selling, with volume acting as confirmation of trend strength. Traders can use these signals for both short and long positions, with additional risk management and multi-timeframe validation to enhance the strategy.

------------------------------------------------------------------------------

To use the "Volume-Supported Linear Regression Trend Table" (VSLRT Table) script in a trading strategy, you would incorporate it into your decision-making process to identify potential buy and sell opportunities based on the trend and volume dynamics. Here’s how you could apply it for trading:

1. Understanding the Key Elements:

Trend Direction (Slope of Price): The script uses linear regression to assess the trend direction of the price. If the price slope is positive, the asset is likely in an uptrend; if it's negative, the asset is in a downtrend.

Volume-Backed Signals: The buy or sell signal is not only based on the price trend but also on volume. Volume is crucial in validating the strength of a trend; large volume often indicates strong interest in a direction.

2. Interpreting the Table and Signals:

The table displayed at the bottom-right of your TradingView chart gives you a clear overview of the trends across different timeframes:

Trend Colors:

Green hues (e.g., ccol11, ccol12, etc.): Indicate a buying trend supported by volume.

Red hues (e.g., ccol21, ccol22, etc.): Indicate a selling trend supported by volume.

Gray: Indicates weak or unclear trends where no decisive direction is present.

Buy/Sell Signals:

The script plots triangles on the chart:

Upward triangle below the bar signals a potential buy.

Downward triangle above the bar signals a potential sell.

3. Building a Trading Strategy:

Here’s how you can incorporate the script’s information into a trading strategy:

Buy Signal (Long Entry):

Look for green triangles (indicating a buy signal) below a bar.

Confirm that the trend color in the table for the relevant timeframe is green, which shows that the buy signal is supported by strong volume.

Ensure that the price is in an uptrend (positive slope) and that volume is increasing on upward moves, as this indicates buying interest.

Execute a long position when these conditions align.

Sell Signal (Short Entry):

Look for red triangles (indicating a sell signal) above a bar.

Confirm that the trend color in the table for the relevant timeframe is red, which shows that the sell signal is supported by strong volume.

Ensure that the price is in a downtrend (negative slope) and that volume is increasing on downward moves, indicating selling pressure.

Execute a short position when these conditions align.

Exiting the Trade:

Exit a long position when a sell signal (red triangle) appears, or when the trend color in the table shifts to red.

Exit a short position when a buy signal (green triangle) appears, or when the trend color in the table shifts to green.

4. Multi-Timeframe Confirmation:

The script provides trends across multiple timeframes (tf1, tf2, tf3), which can help in validating your trade:

Short-Term Trading: Use shorter timeframes (e.g., 3, 5 minutes) for intraday trades. If both short and medium timeframes align in trend direction (e.g., both showing green), it strengthens the signal.

Longer-Term Trading: If you are trading on a higher timeframe (e.g., daily or weekly), confirm that the lower timeframes align with your intended trade direction.

5. Adding Risk Management:

Stop-Loss: Place stop-losses below recent lows (for long trades) or above recent highs (for short trades) to minimize risk.

Take Profit: Consider taking profit at key support/resistance levels or based on a fixed risk-to-reward ratio (e.g., 2:1).

Example Strategy Flow:

For Long (Buy) Trade:

Signal: A green triangle appears below a candle (Buy signal).

Trend Confirmation: Check that the color in the table for your selected timeframe is green, confirming the trend is supported by volume.

Execute Long: Enter a long trade if the price is trending upward (positive price slope).

Exit Long: Exit when a red triangle appears above a candle (Sell signal) or if the trend color shifts to red in the table.

For Short (Sell) Trade:

Signal: A red triangle appears above a candle (Sell signal).

Trend Confirmation: Check that the color in the table for your selected timeframe is red, confirming the trend is supported by volume.

Execute Short: Enter a short trade if the price is trending downward (negative price slope).

Exit Short: Exit when a green triangle appears below a candle (Buy signal) or if the trend color shifts to green in the table.

6. Fine-Tuning:

Backtesting: Before trading live, use TradingView’s backtesting features to test the strategy on historical data and optimize the settings (e.g., length of linear regression, timeframe).

Combine with Other Indicators: Use this strategy alongside other technical indicators (e.g., RSI, MACD) for better confirmation.

In summary, the script helps identify trends with volume support, giving more confidence in buy/sell decisions. Combining these signals with risk management and multi-timeframe analysis can create a solid trading strategy.

Two Pole Butterworth For Loop [BackQuant]Two Pole Butterworth For Loop

PLEASE read the following carefully, as understanding the underlying concepts and logic behind the indicator is key to incorporating it into your trading system in a sound and methodical manner.

Introducing BackQuant's Two Pole Butterworth For Loop (2P BW FL) — an advanced indicator that fuses the power of the Two Pole Butterworth filter with a dynamic for-loop scoring mechanism. This unique approach is designed to extract actionable trading signals by smoothing out price data and then analyzing it using a comparative scoring method. Let's delve into how this indicator works, why it was created, and how it can be used in various trading scenarios.

Understanding the Two Pole Butterworth Filter

The Butterworth filter is a signal processing tool known for its smooth response and minimal distortion. It's often used in electronic and communication systems to filter out unwanted noise. In trading, the Butterworth filter can be applied to price data to smooth out the volatility, providing traders with a clearer view of underlying trends without the whipsaws often associated with market noise.

The Two Pole Butterworth variant further enhances this effect by applying the filter with two poles, effectively creating a sharper transition between the passband and stopband. In simple terms, this allows the filter to follow the price action more closely, reacting to changes while maintaining smoothness.

In this script, the Two Pole Butterworth filter is applied to the Calculation Source (default is set to the closing price), creating a smoothed price series that serves as the foundation for further analysis.

Why Use a Two Pole Butterworth Filter?

The Two Pole Butterworth filter is chosen for its ability to reduce lag while maintaining a smooth output. This makes it an ideal choice for traders who want to capture trends without being misled by short-term volatility or market noise. By filtering the price data, the Two Pole Butterworth enables traders to focus on the broader market movements and avoid false signals.

The For-Loop Scoring Mechanism

In addition to the Butterworth filter, this script uses a for-loop scoring system to evaluate the smoothed price data. The for-loop compares the current value of the filtered price (referred to as "subject") to previous values over a defined range (set by the start and end input). The score is calculated based on whether the subject is higher or lower than the previous points, and the cumulative score is used to determine the strength of the trend.

Long and Short Signal Logic

Long Signals: A long signal is triggered when the score surpasses the Long Threshold (default set at 40). This suggests that the price has built sufficient upward momentum, indicating a potential buying opportunity.

Short Signals: A short signal is triggered when the score crosses under the Short Threshold (default set at -10). This indicates weakening price action or a potential downtrend, signaling a possible selling or shorting opportunity.

By utilizing this scoring system, the indicator identifies moments when the price momentum is shifting, helping traders enter positions at opportune times.

Customization and Visualization Options

One of the strengths of this indicator is its flexibility. Traders can customize various settings to fit their personal trading style or adapt it to different markets and timeframes:

Calculation Periods: Adjust the lookback period for the Butterworth filter, allowing for shorter or longer smoothing depending on the desired sensitivity.

Threshold Levels: Set the long and short thresholds to define when signals should be triggered, giving you control over the balance between sensitivity and specificity.

Signal Line Width and Colors: Customize the visual presentation of the indicator on the chart, including the width of the signal line and the colors used for long and short conditions.

Candlestick and Background Colors: If desired, the indicator can color the candlesticks or the background according to the detected trend, offering additional clarity at a glance.

Trading Applications

This Two Pole Butterworth For Loop indicator is versatile and can be adapted to various market conditions and trading strategies. Here are a few use cases where this indicator shines:

Trend Following: The Butterworth filter smooths the price data, making it easier to follow trends and identify when they are gaining or losing strength. The for-loop scoring system enhances this by providing a clear indication of how strong the current trend is compared to recent history.

Mean Reversion: For traders looking to identify potential reversals, the indicator’s ability to compare the filtered price to previous values over a range of periods allows it to spot moments when the trend may be losing steam, potentially signaling a reversal.

Swing Trading: The combination of smoothing and scoring allows swing traders to capture short to medium-term price movements by filtering out the noise and focusing on significant shifts in momentum.

Risk Management: By providing clear long and short signals, this indicator helps traders manage their risk by offering well-defined entry and exit points. The smooth nature of the Butterworth filter also reduces the risk of getting caught in false signals due to market noise.

Final Thoughts

The Two Pole Butterworth For Loop indicator offers traders a powerful combination of smoothing and scoring to detect meaningful trends and shifts in price momentum. Whether you are a trend follower, swing trader, or someone looking to refine your entry and exit points, this indicator provides the tools to make more informed trading decisions.

As always, it's essential to backtest the indicator on historical data and tailor the settings to your specific trading style and market. While the Butterworth filter helps reduce noise and smooth trends, no indicator can predict the future with absolute certainty, so it should be used in conjunction with other tools and sound risk management practices.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Bitcoin CME-Spot Z-Spread - Strategy [presentTrading]This time is a swing trading strategy! It measures the sentiment of the Bitcoin market through the spread of CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. By applying Bollinger Bands to the spread, the strategy seeks to capture mean-reversion opportunities when prices deviate significantly from their historical norms

█ Introduction and How it is Different

The Bitcoin CME-Spot Bollinger Bands Strategy is designed to capture mean-reversion opportunities by exploiting the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. The strategy uses Bollinger Bands to detect when the spread between these two correlated assets has deviated significantly from its historical norm, signaling potential overbought or oversold conditions.

What sets this strategy apart is its focus on spread trading between futures and spot markets rather than price-based indicators. By applying Bollinger Bands to the spread rather than individual prices, the strategy identifies price inefficiencies across markets, allowing traders to take advantage of the natural reversion to the mean that often occurs in these correlated assets.

BTCUSD 8hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy relies on Bollinger Bands to assess the volatility and relative deviation of the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. Bollinger Bands consist of a moving average and two standard deviation bands, which help measure how much the spread deviates from its historical mean.

🔶 Spread Calculation:

The spread is calculated by subtracting the Bitfinex spot price from the CME Bitcoin futures price:

Spread = CME Price - Bitfinex Price

This spread represents the difference between the futures and spot markets, which may widen or narrow based on supply and demand dynamics in each market. By analyzing the spread, the strategy can detect when prices are too far apart (potentially overbought or oversold), indicating a trading opportunity.

🔶 Bollinger Bands Calculation:

The Bollinger Bands for the spread are calculated using a simple moving average (SMA) and the standard deviation of the spread over a defined period.

1. Moving Average (SMA):

The simple moving average of the spread (mu_S) over a specified period P is calculated as:

mu_S = (1/P) * sum(S_i from i=1 to P)

Where S_i represents the spread at time i, and P is the lookback period (default is 200 bars). The moving average provides a baseline for the normal spread behavior.

2. Standard Deviation:

The standard deviation (sigma_S) of the spread is calculated to measure the volatility of the spread:

sigma_S = sqrt((1/P) * sum((S_i - mu_S)^2 from i=1 to P))

3. Upper and Lower Bollinger Bands:

The upper and lower Bollinger Bands are derived by adding and subtracting a multiple of the standard deviation from the moving average. The number of standard deviations is determined by a user-defined parameter k (default is 2.618).

- Upper Band:

Upper Band = mu_S + (k * sigma_S)

- Lower Band:

Lower Band = mu_S - (k * sigma_S)

These bands provide a dynamic range within which the spread typically fluctuates. When the spread moves outside of these bands, it is considered overbought or oversold, potentially offering trading opportunities.

Local view

🔶 Entry Conditions:

- Long Entry: A long position is triggered when the spread crosses below the lower Bollinger Band, indicating that the spread has become oversold and is likely to revert upward.

Spread < Lower Band

- Short Entry: A short position is triggered when the spread crosses above the upper Bollinger Band, indicating that the spread has become overbought and is likely to revert downward.

Spread > Upper Band

🔶 Risk Management and Profit-Taking:

The strategy incorporates multi-step take profits to lock in gains as the trade moves in favor. The position is gradually reduced at predefined profit levels, reducing risk while allowing part of the trade to continue running if the price keeps moving favorably.

Additionally, the strategy uses a hold period exit mechanism. If the trade does not hit any of the take-profit levels within a certain number of bars, the position is closed automatically to avoid excessive exposure to market risks.

█ Trade Direction

The trade direction is based on deviations of the spread from its historical norm:

- Long Trade: The strategy enters a long position when the spread crosses below the lower Bollinger Band, signaling an oversold condition where the spread is expected to narrow.

- Short Trade: The strategy enters a short position when the spread crosses above the upper Bollinger Band, signaling an overbought condition where the spread is expected to widen.

These entries rely on the assumption of mean reversion, where extreme deviations from the average spread are likely to revert over time.

█ Usage

The Bitcoin CME-Spot Bollinger Bands Strategy is ideal for traders looking to capitalize on price inefficiencies between Bitcoin futures and spot markets. It’s especially useful in volatile markets where large deviations between futures and spot prices occur.

- Market Conditions: This strategy is most effective in correlated markets, like CME futures and spot Bitcoin. Traders can adjust the Bollinger Bands period and standard deviation multiplier to suit different volatility regimes.

- Backtesting: Before deployment, backtesting the strategy across different market conditions and timeframes is recommended to ensure robustness. Adjust the take-profit steps and hold periods to reflect the trader’s risk tolerance and market behavior.

█ Default Settings

The default settings provide a balanced approach to spread trading using Bollinger Bands but can be adjusted depending on market conditions or personal trading preferences.

🔶 Bollinger Bands Period (200 bars):

This defines the number of bars used to calculate the moving average and standard deviation for the Bollinger Bands. A longer period smooths out short-term fluctuations and focuses on larger, more significant trends. Adjusting the period affects the responsiveness of the strategy:

- Shorter periods (e.g., 100 bars): Makes the strategy more reactive to short-term market fluctuations, potentially generating more signals but increasing the risk of false positives.