MACD + RSI + ADX Strategy (ChatGPT-powered) by TradeSmartThis is a trading strategy made by TradeSmart, using the recommendations given by ChatGPT . As an experiment, we asked ChatGPT on which indicators are the most popular for trading. We used all of the recommendations given, and added more. We ended up with a strategy that performs surprisingly well on many crypto and forex assets. See below for exact details on what logic was implemented and how you can change the parameters of the strategy.

The strategy is a Christmas special , this is how we would like to thank the support of our followers.

The strategy has performed well on Forex, tested on 43 1-hour pairs and turned a profit in 21 cases. Also it has been tested on 51 crypto pairs using the 1-hour timeframe, and turned a profit in 45 cases with a Profit Factor over 1.4 in the top-5 cases. Tests were conducted without commission or slippage, unlike the presented result which uses 0.01% commission and 5 tick slippage.

Some of the top performers were:

SNXUSDT

SOLUSDT

CAKEUSDT

LINKUSDT

EGLDUSDT

GBPJPY

TRYJPY

USDJPY

The strategy was implemented using the following logic:

Entry strategy:

Long entry:

Price should be above the Simple Moving Average (SMA)

There should be a cross up on the MACD (indicated by the color switch on the histogram, red to green)

RSI should be above the 50 level

Volume is above the selected volume-based Exponential Moving Average (EMA)

ADX should also agree to this position: below 50 and over 20, and above the Regularized Moving Average (REMA)

Short entry:

Price should be under the Simple Moving Average (SMA)

There should be a cross down on the MACD (indicated by the color switch on the histogram, red to green)

RSI should be below the 50 level

Volume is above the selected volume-based Exponential Moving Average (EMA)

ADX should also agree to this position: below 50 and over 20, and above the Regularized Moving Average (REMA)

Exit strategy:

Stop Loss will be placed based on ATR value (with 1.5 Risk)

Take profit level will be placed with a 2.5 Risk/Reward Ratio

Open positions will be closed early based on the Squeeze Momentum (Long: change to red, Short: change to green)

NOTE! : The position sizes used in the example is with 'Risk Percentage (current)', according which the position size will be determined such

that the potential loss is equal to % of the current available capital. This means that in most of the cases, the positions are calculated using leverage.

Parameters of every indicator used in the strategy can be tuned in the strategy settings as follows:

Plot settings:

Plot Signals: true by default, Show all Long and Short signals on the signal candle

Allow early TP/SL plots: false by default, Checking this option will result in the TP and SL lines to be plotted also on the signal candle rather than just the entry candle. Consider this only when manual trading, since backtest entries does not happen on the signal candle.

Entry Signal:

Fast Length: 12 by default

Slow Length: 26 by default

Source: hlcc4 by default

Signal Smoothing: 9 by default

Oscillator MA Type: EMA by default

Signal Line MA Type: EMA by default

Exit Strategy:

ATR Based Stop Loss: true by default

ATR Length (of the SL): 14 by default

ATR Smoothing (of the SL): EMA by default

Candle Low/High Based Stop Loss: false by default, recent lowest or highest point (depending on long/short position) will be used to calculate stop loss value. Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier. Please select only one active stop loss. Default value (if nothing or multiple stop losses are selected) is the 'ATR Based Stop Loss'.

Candle Lookback (of the SL): 10 by default

Base Risk Multiplier: 1.5 by default, the stop loss will be placed at this risk level (meaning in case of ATR SL that the ATR value will be multiplied by this factor and the SL will be placed that value away from the entry level)

Risk to Reward Ratio: 2.5 by default, the take profit level will be placed such as this Risk/Reward ratio is met

Force Exit based on Squeeze Momentum: true by default, a Long position will be closed when Squeeze Momentum turns red inside an open position and a Short position will be closed when Squeeze Momentum turns green inside an open position

BB Length: 20 by default

BB Mult Factor: 1.0 by default

KC Length: 20 by default

KC Mult Factor: 1.5 by default

Use True Range (KC): Yes by default

Base Setups:

Allow Long Entries: true by default

Allow Short Entries: true by default

Order Size: 1.5 by default

Order Type: Risk Percentage (current) by default, allows adjustment on how the position size is calculated: Cash: only the set cash ammount will be used for each trade Contract(s): the adjusted number of contracts will be used for each trade Capital Percentage: a % of the current available capital will be used for each trade Risk Percentage (current): position size will be determined such that the potential loss is equal to % of the current available capital Risk Percentage (initial): position size will be determined such that the potential loss is equal to % of the initial capital

Trend Filter:

Use long trend filter: true by default, only enter long if price is above Long MA

Show long trend filter: true by default, plot the selected MA on the chart

MA Type (Long): SMA by default

MA Length (Long): 100 by default

MA Source (Long): close by default

Use short trend filter: true by default, only enter long if price is under Short MA

Show short trend filter: false by default, plot the selected MA on the chart

MA Type (Short): SMA by default

MA Length (Short): 100 by default

MA Source (Short): close by default

Simple RSI Limiter:

Limit using Simple RSI: true by default, if set to 'Normal', only enter long when Simple RSI is lower then Long Boundary, and only enter short when Simple RSI is higher then Short Boundary. If set to 'Reverse', only enter long when Simple RSI is higher then Long Boundary, and only enter short when Simple RSI is lower then Short Boundary.

Simple RSI Limiter Type:

RSI Length: 14 by default

RSI Source: hl2 by default

Simple RSI Long Boundary: 50 by default

Simple RSI Short Boundary: 50 by default

ADX Limiter:

Use ADX Limiter: true by default, only enter into any position (long/short) if ADX value is higher than the Low Boundary and lower than the High Boundary.

ADX Length: 5 by default

DI Length: 5 by default

High Boundary: 50 by default

Low Boundary: 20 by default

Use MA based calculation: Yes by default, if 'Yes', only enter into position (long/short) if ADX value is higher than MA (ADX as source).

MA Type: REMA by default

MA Length: 5 by default

Volume Filter:

Only enter trades where volume is higher then the volume-based MA: true by default, a set type of MA will be calculated with the volume as source, and set length

MA Type: EMA by default

MA Length: 10 by default

Session Limiter:

Show session plots: false by default, show crypto market sessions on chart: Sidney (red), Tokyo (orange), London (yellow), New York (green)

Use session limiter: false by default, if enabled, trades will only happen in the ticked sessions below.

Sidney session: false by default, session between: 15:00 - 00:00 (EST)

Tokyo session: false by default, session between: 19:00 - 04:00 (EST)

London session: false by default, session between: 03:00 - 11:00 (EST)

New York session: false by default, session between: 08:00 - 17:00 (EST)

Date Range:

Limit Between Dates: false by default

Start Date: Jul 01 2021 00:00:00 by default

End Date: Dec 31 2022 00:00:00 by default

Trading Time:

Limit Trading Time: false by default, tick this together with the options below to enable limiting based on day and time

Valid Trading Days Global: 1234567 by default, if the Limit Trading Time is on, trades will only happen on days that are present in this field. If any of the not global Valid Trading Days is used, this field will be neglected. Values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) To trade on all days use: 123457

(1) Valid Trading Days: false, 1234567 by default, values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) The script will trade on days that are present in this field. Please make sure that this field and also (1) Valid Trading Hours Between is checked

(1) Valid Trading Hours Between: false, 0930-1600 by default, hours between which the trades can happen. The time is always in the exchange's timezone

Fine-tuning is highly recommended when using other asset/timeframe combinations.

ابحث في النصوص البرمجية عن "ema"

Trend ShotBTCUSD -- 5 min or 15 min (recommended)

BUY POSITION

1 : Ema 50 must be above ema 200

2 : The macd should show a buy sign

3 : Multiple RSI should show a buy sign

4 : Multiple fast EMA should show a sign of buy

SELL POSITION

1 : Ema 50 must be below ema 200

2 : The macd should show a sell sign

3 : Multiple RSI should show a sell sign

4 : Multiple fast EMA should show a sell sign

action zone - ATR stop reverse order strategy v0.1 by 9nckACTION ZONE-ATR MOD v0.1 DOCUMENTATION

Overview

This tradingview pine script strategy is mainly created to enrich my coding skill. It is a combination of “CDC-ACTIONZONE” and my personal studies of trading techniques in various sources e.g.book, course or blog. This strategy purposefully built to connect with my automatic trading bot. However, It will be very useful to aid your trading routine by diminishing mental distraction which possibly leads to bad trades.

How does it work?

This strategy will do a basic simple thing that most traders do by creating entry signals on both sides long/short and also set the stop loss. Furthermore, It will also reverse the order (from long to short and vice versa (if long/short conditions are met). Finally, it will recalculate the stop loss/take profit price in every complete bar to increase the chance of winning and limit our loss.

Entry rules(Long/Short)

If you have no open order, an order will be created when a fast EMA crosses(up(long)/down(short) the slow EMA(It’s as simple as that).

If you have an open order, the current order will be (sold if long, covered if short) and the opposite side order will be created.

Exit and Reverse rules(Long/Short)

If fast EMA cross (DOWN(long), UP(short)), the current order will be closed, THE OPPOSITE SIDE ORDER WILL ALSO BE CREATED.

Risk management

FLEX STOP PRICE : initial value will be set at the bar which order created. It is a fast ema (+/-) MIDDLE ATR value.

If MIDDLE ATR value rises, it will be our new stop price.

If MIDDLE ATR value falls, stop price unchanged

If Price OVERBOUGHT(long)/SOLD(short), LOW of that bar will be a new stop price.

Minimum position hold period

In order to eliminate risk of repeatedly open, close orders in sideway trends. Minimum hold period must be passed to start exit our position. However, It always respects stop loss prices. The value refers to the number of bars.

MUST READ!!!

This strategy uses only MARKET ORDER. If you trade with a bot, make sure you choose only enormous market cap tokens.

This strategy is bi-direction strategy. It will work best in the DERIVATIVE market.

It was initially designed to compete in the cryptocurrency market which has very high volume and volatility.

I only use this strategy in 1HR (acceptable change rate, optimum trade frequency)

How (should) we use it?

Choose crypto future pairs (recommend only top 10-15 market volume pairs in Binance, let’s say 1000M+ trade value)

Choose your time frame (1H is strongly recommended)

Setup your portfolio profile (Setting->Properties) such as Initial cap, order size, commission. DO NOT USE CAL ON EVERY TICK IT WILL CAUSE REPAINTING AND YOUR CAPITAL IS BLEEDING !!!

BACKTEST FIRST!! Back test is a combination of art, math and statis(and a bit of luck). You can apply to train and test methods or whatever you are familiar with. In my opinion, your test period should include UPTREND, SIDEWAY, DOWNTREND. Fine tune fast, slow ema first(my best ema length of 1H timeframe around 7-10, 17-22). Try to eliminate fault breakout trade and use other options only necessary. Hopefully we can use automatic optimization on Pine Script soon.

Don’t forget to turn off using a specific backtest date option to start your strategy.A

THIS IS NOT A PERFECT (OR EVEN PROFITABLE) STRATEGY. USE AT YOUR OWN RISK AND TRADE RESPONSIBLY. DYOR DUDE.

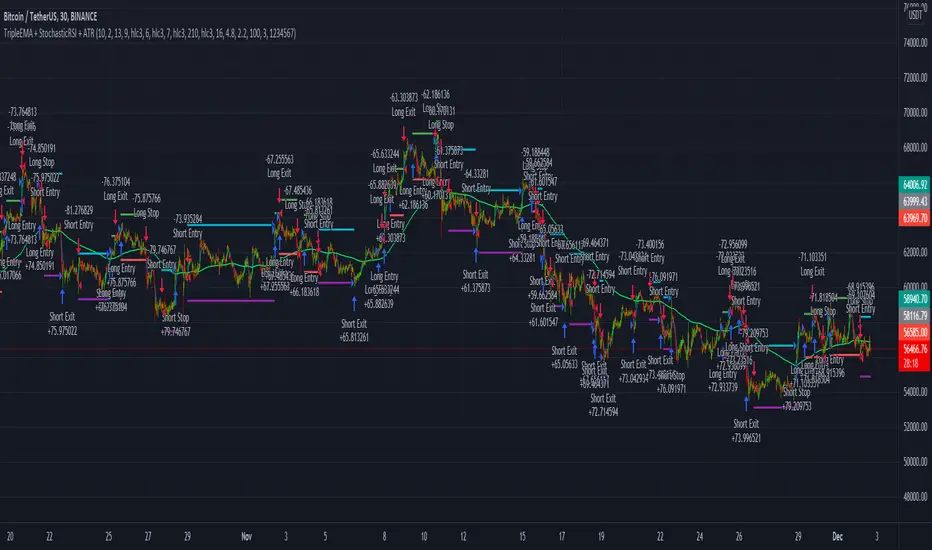

TripleEMA + StochasticRSI + ATR Scalping Strategy by TradeSmartCOINBASE:BTCUSD Hello everyone and welcome to our second script release!

This script is one of many upcoming scripts. This one is a test for us, how it works, how you guys like this kind of stuff, and for feedback what we should change/improve at.

So feel free to comment any suggestions you have.

SCRIPT IS OPTIMIZED FOR:

BTC/USD (Coinbase) 15 minute timeframe

(Keep in mind default settings does not include trading fees, you can set it at the properties)

I recommend using this script on a trading exchange where the fees are extremely low or on an exchange where you get paid to place limit orders.

(I am not a financial avdvisor and none of this is financial advice.)

Now you can modify the following:

Stochastic RSI

3 different EMA

Length of ATR (for stop loss and take profit)

Stop Loss and Take Profit Risk to Reward ratio

Choice between Capital Risk on each trade or Risk of % of Capital

Allowing Short/Long entries only

Limit between dates

Trading days 1-7

We will update the script with more and more features taking in consideration your requests.

Hope you like it! Don't forget to let us know what we should change or improve. Thanks, and have a great day!

STRATEGY ENTRY RULES

LONG

When EMAs are lining up (meaning for ex. 400 < 13 < 7), and the Stochastic RSI crosses upwards (meaning blue line crosses orange upwards), then go long.

SHORT

When EMAs are lining down (meaning for ex. 7 < 13 < 400), and the Stochastic RSI crosses downwards (meaning blue line crosses orange downwards), then go short.

TAKE PROFIT

When price hits the exit price (calculated from stop loss with the risk ratio)

STOP LOSS

When price hits stop loss then exit the position.

QUANTITY TO BUY (Risk per Trade % or Capital %)

Risk Per Trade % attribute: we can set how much money we want to risk on one trade. Meaning that if we lose that particular position, then a Risk Per Trade % value of our equity will be lost.

Example: if you set the Risk Per Trade % to 1 % and you have a 100$ account balance, then if you loose the trade you will loose 1$ max.

Capital % we can set with how big % of our capital we want to enter into a position. Meaning that we enter with a set % of our capital.

Example: if you set the Capital % to 1 % and you have a 100$ account balance, then you will enter the position with 1$.

First Release Settings: (2021-10-25) for BTC/USD (Coinbase) 15 minute timeframe

Stochastic RSI settings: (Not displayed in the script. If you want to see it you have to add it separately.)

K: 3

D: 2

RSI Length: 6

Stochastic Length: 16

RSI Source: hlc3

EMA 1: 5

Source One: Close

EMA 2: 12

Source Two: Close

EMA 3: 215

Source Three: Close

Length of ATR: 16

Stop Loss Multiplier (risk): 3.6

Exit Price Multiplier (reward): 1

Risk Percentage: 3

Allow Long Entries: yes

Allow Short Entries: yes

Valid Trading Days: 1234567

The valid trading days of the Limit Trading Time feature. Numbers represent the days: Sunday (1), Monday (2), Tuesday (3), …, Saturday (7)

If you like this one, follow for more scripts! Thank you for your support!

Ultimate Bollinger Bands by @DaviddTechThis strategy uses the Ultimate Bollinger and Aroon indicator.

The logic behind the code is

* Enter long :

Aroon up is below the 20 or lower line in settings.

Aroon down is above 70 or above line in settings.

When close crossover the lower Bollinger Band we take an entry

SL is %

TP is % of if Aroon up is below the 70 or lower line in settings.

Aroon down is above 20 or above line in settings.

When close crossover the upper Bollinger Band

* Short :

Aroon down is below the 20 or lower line in settings.

Aroon up is above 70 or above line in settings.

When close crossunder the upper Bollinger Band we take an entry

SL is %

TP is % of if Aroon up is below the 20 or lower line in settings.

Aroon down is above 70 or above line in settings.

When close crossover the lower Bollinger Band

Settings I used to get the results below :

====================

** Ultimate Bollinger Bands by @DaviddTech **

====================

Enable Repainting? = False

Enable LONG entries? = True

Enable SHORT entries? = True

lengthBB = 20

Source = close

StdDev = 2

Offset = 0

Aroon Length = 14

Aroon Enter upper band = 85

Aroon Enter lower band = 5

Aroon Exit upper band = 70

Aroon Exit lower band = 20

Restrict Entries to Date Range? = False

From : = 1611100800000

To : = 1613779200000

Show Liquadation line (BETA) = False

Leverage Amount = 25

Maintenance Margin Rate = 0.5

Type of Exit / Entry = Enter New Trade Only if NO running Trades

Type of Take Profit = Custom Stoploss

Type of Stoploss = Custom Stoploss

Stop Loss % = 4

Take Profit % = 6

Highest High lookback = 50

Lowest Low Lookback = 60

Profitfactor Long (Risk to Reward) = 2

Profitfactor Short (Risk to Reward) = 0.5

Stoploss Factor: LONG = 4

SHORT = 4

Profit Factor: LONG = 2

SHORT = 2

ATR Length = 11

Length = 200

Source = hlc3

Multiplier = 3

Level = 764

Take Multi Profit X3 = False

% to take at First TP = 33

% to take at Second TP = 33

% to take at Third TP = 100

Use Strategy Alerts? - Please read the tooltip = False

Show S/R Levels = False

Use MFI + RSI = False

RSI Source = close

RSI Length = 14

RSI Oversold = 30

RSI Overbought = 60

MFI Period = 60

MFI Area multiplier = 150

MFI Area Y Pos = 2.5

Use vWap = False

vWap Source = close

vWap2 Source = close

Vwap Length = 3

EMA Breakout = False

EMA Length = 100

Use MTF EMA cross = False

MTF = 5

EMA Period = 5

MTF = 5

EMA Period = 30

WARNING:

- For purpose educate only - My mission is to debunk fake strategies with code to find THE ONE.

- Plots EMAs and other values on chart.

- This script to change bars colors.

If you have any questions or feedback, please let me know in the comments.

Combo Backtest 123 Reversal & T3 Averages This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the moving average described in the January, 1998 issue

of S&C, p.57, "Smoothing Techniques for More Accurate Signals", by Tim Tillson.

This indicator plots T3 moving average presented in Figure 4 in the article.

T3 indicator is a moving average which is calculated according to formula:

T3(n) = GD(GD(GD(n))),

where GD - generalized DEMA (Double EMA) and calculating according to this:

GD(n,v) = EMA(n) * (1+v)-EMA(EMA(n)) * v,

where "v" is volume factor, which determines how hot the moving average’s response

to linear trends will be. The author advises to use v=0.7.

When v = 0, GD = EMA, and when v = 1, GD = DEMA. In between, GD is a less aggressive

version of DEMA. By using a value for v less than1, trader cure the multiple DEMA

overshoot problem but at the cost of accepting some additional phase delay.

In filter theory terminology, T3 is a six-pole nonlinear Kalman filter. Kalman

filters are ones that use the error — in this case, (time series - EMA(n)) —

to correct themselves. In the realm of technical analysis, these are called adaptive

moving averages; they track the time series more aggres-sively when it is making large

moves. Tim Tillson is a software project manager at Hewlett-Packard, with degrees in

mathematics and computer science. He has privately traded options and equities for 15 years.

WARNING:

- For purpose educate only

- This script to change bars colors.

Traffic Lights Strategy4HS Crypto Market Strategy

This strategy uses 4 ema to get Long or Short Signals

Length are: 4, 9, 18, 100

We take long positions when the order of the emas is the following:

green > yellow > red (As the color of Traffic Lights) and they are above white ema (Used as a filter for long positions)

We take short positions when the order of the emas is the following:

green < yellow < red (As the color of inverse Traffic Lights) and they are below white ema (Used as a filter for short positions)

Enable Long and/or Short Positions in settings

Enable Profit and Stop in strategy settings with different percentage to backtest the strategy. Also if it is better to use a Traditional Stop Loss or a Trailing Stop Loss based on ATR

Change ema filter resolution in settings for better strategy performance

This Strategy was tested on Crypto Market with good results in assets as BTC, ETH, BNB, ADA, LTC, XLM, BCH, among others

Feel free to optimize this strategy, optimizing its parameters. Each asset has its own "personality".

Amazing Crossover System - 100+ pips per day!I got the main concept for this system on another site. While I have made one important change, I must stress that the heart of this system was created by someone else! We must give credit where credit is due!

Y'all know baby pips. @ForexPhantom published about this system and did both back and forward test around 10 years ago.

I found it on the sit and now I put it to code to see how it performs. I assume 10 points spread for every trade. I use Renesource or AxiTrader to get the low spreads.

There are 2 mods, the single trades and constant trading on the direction.

Main concept

Indicators

5 EMA -- YELLOW

10 EMA -- RED

RSI (10 - Apply to Median Price: HL/2) -- One level at 50.

TIME FRAME

1 Hour Only (very important!)

PAIRS

Virtually any pair seems to work as this is strictly technical analysis.

I recommend sticking to the main currencies and avoiding cross currencies (just his preference).

WHEN TO ENTER A TRADE

Enter LONG when the Yellow EMA crosses the Red EMA from underneath.

RSI must be approaching 50 from the BOTTOM and cross 50 to warrant entry.

Enter SHORT when the Yellow EMA crosses the Red EMA from the top.

RSI must be approaching 50 from the TOP and cross 50 to warrant entry.

I've attached a picture which demonstrates all these conditions.

That's it!

f.bpcdn.co

GoldenCross by PuffyThis is a simple trading strategy that seeks the Golden Cross and Death Cross on the 4HR chart. The fast moving indicator in this strategy is the EMA 50 and the slow moving indicator is the EMA 200. When the EMA 50 crosses over the EMA 200 the strategy indicates a buy. When the EMA 50 crosses below the EMA 200 the strategy indicates a sell. This strategy averages trades in the 40 - 50 day range and as such should not be used with heavy leverage.

T3 Averages Backtest This indicator plots the moving average described in the January, 1998 issue

of S&C, p.57, "Smoothing Techniques for More Accurate Signals", by Tim Tillson.

This indicator plots T3 moving average presented in Figure 4 in the article.

T3 indicator is a moving average which is calculated according to formula:

T3(n) = GD(GD(GD(n))),

where GD - generalized DEMA (Double EMA) and calculating according to this:

GD(n,v) = EMA(n) * (1+v)-EMA(EMA(n)) * v,

where "v" is volume factor, which determines how hot the moving average’s response

to linear trends will be. The author advises to use v=0.7.

When v = 0, GD = EMA, and when v = 1, GD = DEMA. In between, GD is a less aggressive

version of DEMA. By using a value for v less than1, trader cure the multiple DEMA

overshoot problem but at the cost of accepting some additional phase delay.

In filter theory terminology, T3 is a six-pole nonlinear Kalman filter. Kalman

filters are ones that use the error — in this case, (time series - EMA(n)) —

to correct themselves. In the realm of technical analysis, these are called adaptive

moving averages; they track the time series more aggres-sively when it is making large

moves. Tim Tillson is a software project manager at Hewlett-Packard, with degrees in

mathematics and computer science. He has privately traded options and equities for 15 years.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Cowabunga System from babypips.comPlease do read the information below as well, especially if you are new to Forex.

The Cowabunga System is a type of Mechanical Trading System that filters trades based on the trend of the 4 hour chart with EMAs and some other familiar indicators (RSI, Stochastics and MACD) while entering trades base on 15 minute chart.

I have coded (quite amateurishly) the basic system onto a 15 minute chart (the 4 hour settings are coded as well). The author says the system is to be traded off the 15 minute chart with the 4 hour chart only as a reference for trend direction.

4 Hour Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

Then we move onto the 15 minute chart, where he gives us the trade entry rules.

15 Minute Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

MACD (12,26,9)

Entry Rules - long entry rules used, obviously reverse these for shorting.

1. EMA must cross above the 10 EMA.

2. RSI must be greater than 50 and not overbought.

3. Stochastic must be headed up and not be in overbought territory.

4. MACD histogram must go from negative to positive OR be negative and start to increase in value.

What I did.

1. Set the RSI and Stochastic levels to avoid entries when they indicate overbought conditions for long and oversold conditions for short (80 and 20 levels).

2. Users can input specific times they want to backtest.

3. User's can configure profit targets, trailing stops and stops. Default is set it to was 100 pips profit target with a 40 pip trailing stop. (Note, when you are changing these values, please note that each pip is worth 10, so 100 pips is entered as 1000.)

The Cowabunga System from babypips.com is another popular and active system. The author, Pip Surfer, continues to post wins and losses with this system. It shows there is a lot of honesty and integrity with this system if the author keeps up to date even 10 years later and is not afraid of sharing the times the system causes losses.

As an example of this, here is post he shared just last week . It's almost like a journal, he gives specific times and reasons why he entered, lets the readers know when he was stopped out, etc. I think that what he does is equally important as his system.

To read more about this system, visit the thread on babypips.com, click here.

Optimized BTC Mean Reversion (RSI 20/65)📈 Optimized BTC Mean Reversion (RSI 20/65)

Optimized BTC Mean Reversion (RSI 20/65) is a rule-based trading strategy designed to capture mean-reversion moves in strong market structures, primarily optimized for Bitcoin, but adaptable to other liquid cryptocurrencies.

The strategy combines RSI extremes, Stochastic momentum, and EMA trend filtering to identify high-probability reversal zones while maintaining strict risk management.

🔍 Strategy Logic

This system focuses on entering trades when price temporarily deviates from equilibrium, while still respecting the broader trend.

✅ Long Conditions

RSI below 20 (oversold)

Stochastic below 25

Price trading above the 200 EMA (or within a controlled deviation)

Designed to buy sharp pullbacks in bullish conditions

❌ Short Conditions

RSI above 65 (overbought)

Stochastic above 75

Price trading below the 200 EMA

Designed to sell relief rallies in bearish conditions

🛡 Risk Management

Fixed Stop Loss: 4%

Fixed Take Profit: 6%

Risk/Reward: 1 : 1.5

No pyramiding (single position at a time)

Full equity position sizing (adjustable)

All exits are predefined at entry, ensuring consistency and emotional discipline.

📊 Indicators Used

200 EMA – Trend direction filter

RSI (14) – Mean-reversion trigger (20 / 65 levels)

Stochastic Oscillator – Momentum confirmation

👁 Visual Features

EMA plotted directly on chart

Real-time Stop Loss, Take Profit, and Entry Price lines

Clear long/short entry markers

Works on all timeframes (optimized for intraday and swing trading)

🔔 Alerts

Long entry alerts

Short entry alerts

(Perfect for automation or discretionary execution)

⚠️ Disclaimer

This strategy is intended for educational and research purposes only. Past performance does not guarantee future results. Always test on a demo account and adjust risk parameters to your own trading plan.

Capitulation Detector StrategyA multi-factor capitulation detector designed to identify exhaustion points in extended trends. It focuses on fading capitulation moves after multi-leg trends with extreme volume and price extension.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE CONCEPT

Capitulation occurs when the last holders give up — panic selling into lows or euphoric buying into highs. These moments create asymmetric opportunities because:

Sentiment becomes maximally skewed

Weak hands are flushed out

Price deviates far from equilibrium

The "fuel" for continuation is exhausted

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE 6 FACTORS

Trend Persistence — Price stays on one side of 38 EMA for 12+ bars, confirming a sustained directional move

Acceleration — Price stays on one side of 5 EMA for 3+ bars, showing the move is accelerating into exhaustion

Volume Spike — Current bar volume ≥ 2x the 20-bar average

Body Expansion — Candle body ≥ 1.5x average, showing conviction/panic in the move

Extension — Price is 2+ ATR away from the 38 EMA, indicating overextension from equilibrium

Multi-Leg Structure — At least 3 consecutive lower lows (for longs) or higher highs (for shorts)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SIGNAL LOGIC

Bullish Capitulation: 4+ factors align + price below 38 EMA + down candle + volume spike

Bearish Capitulation: 4+ factors align + price above 38 EMA + up candle + volume spike

The strategy enters counter-trend, fading the exhaustion move.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

EXIT OPTIONS

ATR-based stop loss (default: 2 ATR)

ATR-based take profit (default: 3 ATR)

Optional trailing stop

Time filter for session-specific trading

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BEST PRACTICES

Works best on liquid instruments with clean trends

More reliable after 3+ legs in the trend

Higher conviction when daily AND intraday timeframes align

"The bigger and more extended, the better"

Consider VWAP as additional confirmation (not coded here)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SETTINGS GUIDE

Min Score: Increase for fewer, higher-quality signals

Volume Spike Multiplier: 2x; increase for stricter filter

Extension ATR: Higher values = more overextended setups only

Trend Bars Min: Higher values = longer established trends required

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ALERTS

Bullish Capitulation (potential long)

Bearish Capitulation (potential short)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This is a counter-trend strategy — inherently higher risk than trend-following. Always use proper position sizing and risk management. Backtest thoroughly on your specific instruments and timeframes.

Stratégie SMC V18.2 (BTC/EUR FINAL R3 - Tendance)This strategy is an automated implementation of Smart Money Concepts (SMC), designed to operate on the Bitcoin/Euro (BTC/EUR) chart using the 15-minute Timeframe (M15).It focuses on identifying high-probability zones (Order Blocks) after a confirmed Break of Structure (BOS) and a Liquidity Sweep, utilizing an H1/EMA 200 trend filter to only execute trades in the direction of the dominant market flow.Risk management is strict: every trade uses a fixed Risk-to-Reward Ratio (R:R) of 1:3.🧱 Core Logic Components

1. Trend Filter (H1/EMA 200)Objective: To avoid counter-trend entries, which has allowed the success rate to increase to nearly $65\%$ in backtests.Mechanism: A $200$-period EMA is plotted on a higher timeframe (Default: H1/60 minutes).Long (Buy): Entry is only permitted if the current price (M15) is above the trend EMA.Short (Sell): Entry is only permitted if the current price (M15) is below the trend EMA.

2. Order Block (OB) DetectionA potential Order Block is identified on the previous candle if it is

accompanied by an inefficiency (FVG - Fair Value Gap).

3. Advanced SMC ValidationBOS (Break of Structure): A recent BOS must be confirmed by breaking the swing high/low defined by the swing length (Default: 4 M15 candles).Liquidity (Liquidity Sweep): The Order Block zone must have swept recent liquidity (defined by the Liquidity Search Length) within a certain tolerance (Default: $0.1\%$).Point of Interest: The OB must form in a premium zone (for shorts) or a discount zone (for longs) relative to the current swing range (above or below the $50\%$ level of the range).

4. Execution and Risk ManagementEntry: The trade is triggered when the price touches the active Order Block (mitigation).Stop Loss (SL): The SL is fixed at the low of the OB (for longs) or the high of the OB (for shorts).Take Profit (TP): The TP is strictly set at a level corresponding to 3 times the SL distance (R:R 1:3).Lot Sizing: The trade quantity is calculated to risk a fixed amount (Default: 2.00 Euros) per transaction, capped by a Lot Max and Lot Min defined by the user.

Input Parameters (Optimized for BTC/EUR M15)Users can adjust these parameters to modify sensitivity and risk profile. The default values are those optimized for the high-performing backtest (Profit Factor $> 3$).ParameterDescriptionDefault Value (M15)Long. Swing (BOS)Candle length used to define the swing (and thus the BOS).4Long. Recherche Liq.Number of candles to scan to confirm a liquidity sweep.7Tolérance Liq. (%)Price tolerance to validate the liquidity sweep (as a percentage of price).0.1Timeframe TendanceChart timeframe used for the EMA filter (e.g., 60 = H1).60 (H1)Longueur EMA TendancePeriods used for the trend EMA.200Lot Max (Quantité Max BTC)Maximum quantity of BTC the strategy is allowed to trade.0.01Lot Min Réel (Exigence Broker)Minimum quantity required by the broker/exchange.0.00001

Seawolf Pivot Hunter [Strategy]Overview

Seawolf Pivot Hunter is a practical trading strategy that enhances the classic pivot-box breakout system with a structured risk-management framework. Using ATR-based stop loss and take-profit calculations, position sizing, multi-layer filtering, and daily loss-limit protection, it provides a stable and sustainable trading environment. It preserves the strengths of the original version while adding systems designed to manage real-market risks more effectively.

Core Philosophy

The most important element in trading is not generating profits but controlling losses. Even the best entry signals cannot compensate for a single large loss that wipes out accumulated gains. This strategy precisely calculates the risk exposure for every trade and includes multiple layers of protection to safeguard the account under worst-case scenarios.

Indicator Setup Link

kr.tradingview.com

Example of Optimal Parameter Settings

Asset (Exchange): ETH/USDT (Binance)

Timeframe: 15-minute chart

Pivot Detection Length: 5

Upper Box Width: 2

Lower Box Width: 2

Enable Risk Management: False

Use Trailing Stop: False

Use Volume Filter

-Min Buy Volume % for Long: 50

-Min Sell Volume % for Short: 50

Use Trend Filter (EMA): False

Enable Max Loss Protection

-Max Daily Loss ($): 200

-Max Trades Per Day: 10

Calculated Bars: 50,000

Risk-Management System

Every trade automatically receives a stop-loss level at the moment of entry. The stop is calculated using ATR, adjusting dynamically to market volatility. When volatility increases, the stop widens; in stable conditions, it tightens to reduce unnecessary exits. The default distance is set to twice the ATR.

The standard take-profit level is set to four times the ATR, providing a 1:2 risk-reward structure. With this ratio, even a 50 percent win rate can produce profitability—while the typical trade structure aims for small losses and larger gains to support long-term performance.

A trailing-stop option is also available. Once the trade moves into profit, the stop level automatically trails behind price action, protecting gains while allowing the position to expand when momentum continues.

Position size is calculated automatically based on the selected risk percentage. For example, with a 2 percent risk setting, each stop-loss hit would result in exactly 2 percent of the account balance being lost. This ensures a consistent risk profile regardless of account size.

The daily loss-limit function prevents excessive drawdown by halting new trades once a predefined loss threshold is reached. This helps avoid emotional decision-making after consecutive losses.

A daily trade-limit feature is included as well. The default is 10 trades per day, protecting traders from overtrading and unnecessary fees.

Filtering System

The volume filter analyzes buying and selling pressure within the pivot box. Long trades are allowed only when buy volume exceeds a specified percentage; shorts require sell-volume dominance. The default threshold is 55 percent.

The trend filter uses an EMA to determine market direction. When price is above the 200-EMA, only long signals are permitted; when below, only shorts are allowed. This ensures alignment with the broader trend and reduces counter-trend risk.

Each filter can be toggled independently. More filters generally reduce trade frequency but improve signal quality.

Real-Time Monitoring

A real-time statistics panel displays daily profit/loss, the number of trades taken, the maximum allowed trades, and whether new trades are currently permitted. When daily limits are reached, the panel provides clear visual warnings.

Entry Logic

A trade is validated only after a pivot-box breakout occurs and all active filters—volume, trend, daily loss limit, and daily trade limit—are satisfied. Position size, stop loss, and take-profit levels are then calculated automatically. Entry arrows and labels on the chart help with later review and analysis.

Setup Guide

Risk percentage is the most critical setting. Beginners should start at 1 percent. Anything above 3 percent becomes aggressive.

ATR stop-loss multipliers should reflect asset volatility.

ATR take-profit multipliers determine reward ratio; 4.0 is the standard.

Volume thresholds are typically set between 50–60 percent depending on market conditions.

Daily loss limits are typically 2–5 percent of the account.

Trading Strategy

This strategy performs best in trending environments and works especially well on the 4-hour and daily charts. New users should begin with all filters enabled and trade conservatively. A minimum of one month of paper trading is recommended before committing real capital.

Suitable Users

The strategy is ideal for beginners who lack risk-management experience as well as advanced traders seeking a customizable structure. It is particularly helpful for traders who struggle with emotional decision-making, as pre-defined limits and rules enforce discipline.

Backtesting Guide

Use at least 2–3 years of historical data that includes bullish, bearish, and sideways conditions.

Target metrics:

Sharpe ratio: 1.5 or higher

Maximum drawdown: below 25 percent

Win rate: 40 percent or higher

Total trades: at least 100 for statistical relevance

Optimization Precautions

Avoid over-fitting parameters. Always test values around the “best” setting to verify stability.

Out-of-sample testing is essential for confirming robustness.

Test across multiple assets and timeframes to ensure consistency.

Live Deployment Roadmap

After successful backtesting, follow a gradual rollout:

Paper trading for at least one month

Small-account live testing

Slow scaling as performance stabilizes

Continuous Improvement

Keep a detailed trading journal and evaluate performance each quarter using recent data.

Adapt settings as market conditions evolve.

Conclusion

Seawolf Pivot Hunter aims to provide more than simple trade signals—it is designed to create a stable and sustainable trading system built on disciplined risk management. No strategy is perfect, and long-term success depends on consistency, patience, and strict adherence to rules. Start small, verify results, and scale progressively.

Disclaimer

This strategy is for educational and research purposes only. Past performance does not guarantee future results. All trading decisions are the responsibility of the user.

개요

Seawolf Pivot Hunter는 기본 피봇 박스 브레이크아웃 전략에 전문적인 리스크 관리 시스템을 더한 실전형 트레이딩 전략입니다. ATR 기반의 손절매와 목표가 설정, 포지션 사이징, 다층 필터링 시스템, 일일 손실 제한 기능을 통해 안정적이고 지속 가능한 트레이딩 환경을 제공합니다. 기본 버전의 장점은 유지하면서 실제 시장에서 발생할 수 있는 위험을 체계적으로 관리할 수 있도록 설계되었습니다.

핵심 철학

트레이딩에서 가장 중요한 것은 수익이 아니라 손실 관리입니다. 아무리 훌륭한 진입 조건이 있어도 한 번의 큰 손실로 모든 수익이 사라질 수 있습니다. 이 전략은 각 거래마다 감수할 리스크를 명확히 계산하고, 최악의 상황에서도 계좌를 보호하기 위한 다양한 안전장치를 제공합니다.

지표 적용 링크 공유

kr.tradingview.com

최적 조건값 설정(예시)

"종목(거래소): ETH/USDT(Binance)", "15 분봉 기준"

-Pivot Detection Length: 5

-Upper Box width: 2

-Lower Box width: 2

-Enable Risk Management: False

-Use Trailing Stop: False

-Use Volume Filter

-Min Buy Volume % for Long: 50

-Min Buy Volume % for Long: 50

-Use Trend Filter(EMA): False

-Enable Max Loss Protection

-Max Daily Loss($): 200

-Max Trades Per Day: 10

-Calucated bars: 50000

리스크 관리 시스템

모든 거래는 진입과 동시에 손절매 주문이 자동 설정됩니다. 손절가는 ATR을 기준으로 계산되며, 시장의 변동성에 따라 자동으로 조정됩니다. 변동성이 큰 시장에서는 넓은 손절폭을, 안정적인 시장에서는 좁은 손절폭을 사용해 불필요한 청산을 줄입니다. 기본값은 ATR의 2배입니다.

목표가는 ATR의 4배를 기본값으로 설정하여 손익비 1:2 구조를 유지합니다. 승률이 50퍼센트만 되어도 수익성이 가능하며, 실제로는 손절은 짧고 이익은 길게 가져가는 방식으로 장기 성과를 확보합니다.

트레일링 스톱 기능도 제공됩니다. 포지션이 수익 구간에 들어서면 손절가가 자동으로 함께 움직이며 수익을 보호합니다. 이 기능은 사용자가 켜거나 끌 수 있습니다.

포지션 크기는 리스크 퍼센트 기반으로 자동 계산됩니다. 예를 들어 리스크를 2퍼센트로 설정하면 손절 시 계좌 자산의 2퍼센트만 잃도록 수량이 조절됩니다. 계좌 크기와 무관하게 항상 일정한 비율의 리스크만 감수하게 되는 방식입니다.

일일 손실 제한 기능은 하루에 허용 가능한 최대 손실을 초과하지 않도록 합니다. 지정 금액에 도달하면 당일 거래는 더 이상 실행되지 않습니다. 감정적 거래를 막고 일정한 규율을 유지하도록 돕습니다.

일일 거래 횟수 제한 기능도 제공됩니다. 기본값은 하루 10회로, 과매매와 수수료 증가를 방지합니다.

필터링 시스템

볼륨 필터는 박스 구간 내 매수·매도 압력을 분석해 진입 신호를 검증합니다. 롱은 매수 볼륨이 일정 비율 이상일 때, 숏은 매도 볼륨이 우세할 때만 진입합니다. 기본값은 55퍼센트입니다.

추세 필터는 EMA를 사용하며, 가격이 200EMA 위에 있을 때는 롱 신호만, 아래에서는 숏 신호만 허용합니다. 큰 추세 방향에만 거래하여 역추세 리스크를 줄입니다.

필터는 독립적으로 켜고 끌 수 있으며, 필터가 많을수록 거래 횟수는 줄지만 신호 품질은 향상됩니다.

실시간 모니터링

화면에 실시간 통계 테이블이 표시되며, 일일 손익, 거래 횟수, 최대 허용 횟수, 현재 거래 가능 여부가 즉시 확인됩니다. 손실 제한 또는 거래 제한 도달 시 시각적으로 표시됩니다.

진입 로직

피봇 박스 브레이크아웃 발생 후 볼륨 필터, 추세 필터, 일일 손실·거래 제한을 모두 통과하면 포지션 크기를 계산하고 손절·목표가를 설정한 뒤 진입합니다. 진입 지점에는 화살표와 레이블이 표시되어 분석에 도움을 줍니다.

설정 가이드

리스크 퍼센트는 가장 중요한 설정입니다. 초보자는 1퍼센트를 추천하며 3퍼센트 이상은 위험합니다.

손절 ATR 배수는 자산 특성에 맞게 조절합니다.

목표가 ATR 배수는 손익비를 결정하며 기본값은 4.0입니다.

볼륨 비율은 시장 상황에 따라 50~60퍼센트 내외로 조정합니다.

일일 손실 제한은 계좌의 2~5퍼센트 수준이 적절합니다.

사용 전략

추세가 명확한 시장에서 가장 효과적이며, 4시간봉 또는 일봉을 추천합니다. 초반에는 모든 필터를 켜고 보수적으로 시작하며, 최소 한 달간 페이퍼 트레이딩을 권장합니다.

적합한 사용자

리스크 관리 경험이 부족한 초보자부터, 커스터마이징을 원하는 경험자까지 폭넓게 적합합니다. 감정적 트레이딩을 억제하는 기능이 있어 규율 유지가 어렵던 트레이더에게 특히 유용합니다.

백테스트 가이드

최소 2~3년 데이터로 테스트하며, 상승·하락·횡보 모두 포함해야 합니다.

샤프비율 1.5 이상, 최대 낙폭 25퍼센트 이하를 목표로 합니다.

승률은 40퍼센트 이상이면 충분합니다.

최소 100회 이상 거래가 있어야 통계적으로 의미가 있습니다.

최적화 주의사항

과최적화를 피하고 주변 값도 테스트해야 합니다.

샘플 외 기간 검증은 필수입니다.

여러 자산·여러 시간대에서 테스트하여 일관성을 확인해야 합니다.

실전 적용 로드맵

백테스트 후 바로 실전 투입하지 말고, 한 달 이상의 페이퍼 트레이딩 → 소액 실전 → 점진적 확대 순으로 진행합니다.

지속적 개선

일지를 기록하고 분기마다 최신 데이터로 점검합니다.

시장 변화에 따라 유연하게 조정해야 합니다.

마치며

Seawolf Pivot Hunter는 단순 신호 제공을 넘어, 안전하고 지속 가능한 트레이딩 환경 구축을 목표로 합니다. 어떤 전략도 완벽할 수 없으며, 장기적 성공을 위해서는 규칙 준수와 인내가 가장 중요합니다. 충분한 검증을 거쳐 작은 금액으로 시작하고 점진적으로 확장해나가는 접근을 추천합니다.

면책 조항

이 전략은 교육 및 연구 목적이며, 과거 성과는 미래를 보장하지 않습니다. 모든 투자 결정은 본인의 판단과 책임 하에 이루어져야 합니다.

Futures Fighter MO: Multi-Confluence Day Trading System ADX/SMI👋 Strategy Overview: The Multi-Confluence Mashup

The Futures Fighter MO is a comprehensive, multi-layered day trading strategy designed for experienced traders focusing on high-liquidity futures contracts (e.g., NQ, ES, R2K).

This strategy is a sophisticated mashup that uses the 1-minute chart for surgical entries while enforcing strict environmental filtering through higher-timeframe data. We aim to capture high-conviction moves only when multiple, uncorrelated signals align.

🧠 How the Logic Works (Concepts & Confluence)

Our logic is built on four pillars, which must align for a trade to be executed:

Primary Trend Filter

Indicators :

ADX/DMI (15-Minute Lookback)

Role :

Price action is filtered to ensure the ADX (17/14) is above 25, confirming a strong, prevailing market trend (Bullish or Bearish). Trades are strictly rejected during "Flat" (sideways) market regimes.

Entry Signal Types

The system uses multiple entry types:

- 🟢 Trend Long/Short: A breakout/rejection near the 200-Period EMA is confirmed by the primary ADX trend.

- 🔴 Engulfing Rejection: A strong signal when a Bullish/Bearish Engulfing or Doji prints near the long-term 500-Period EMA (emaGOD) while the Stochastic Momentum Index (SMI on 30M) is in an extreme overbought/oversold state (below $-40$ or above $40$).

Volatility & Volume Confirmation

Indicators: Average True Range (ATR) and 20-Period SMA of Volume

Role: Every entry requires a volume spike (Current Volume $> 1.5 \times$ SMA Volume) to confirm that the move is supported by significant liquidity. Volatility is tracked via ATR to define bar range and stop boundaries.

Structural Guardrails

Indicators: Daily Pivot Points (PP, S1-S3, R1-R3)

Role: Trades are disabled if the current bar's price range intersects with a Daily Pivot Point. This is a critical filter to avoid high-chop consolidation zones near key structural levels.

📊 Strategy Results & Required Disclosures

I strive to publish backtesting results that are transparent and realistic for the retail futures trader.

- Initial Capital: $50,000 - A realistic base for Mini/Micro futures contracts.

- Order Size: 1 Contract (Pyramiding up to 3) - Conservative risk relative to the account size.

- Commission: $0.11 USD per order - Represents realistic costs for low-cost brokers.

- Slippage: 2 Ticks - Accounts for expected market friction.

⚠️ Risk Management & Deviations

Stop-Loss: The strategy uses a dynamic stop-loss system where positions are closed upon a reversal (e.g., breaking the 50-Period EMA or failure to hold a Pivot Point), rather than a fixed tick-based stop. This is suited for experienced traders using a low relative risk (single Micro-contract entry) on a larger account. Users must confirm that the first entry's maximum potential loss remains below $10\%$ of their capital for compliance.

Trade Sample Size: Due to data limitations of the TradingView Essential plan (showing $\approx 50$ trades over 2 weeks), the sample size is under the ideal $100+$ target. Justification: This system is designed to generate signals across a portfolio of correlated futures markets (NQ, ES, R2K, Gold, Crude), meaning the real sample size for a user tracking the portfolio is significantly higher.

Drawdown Control: This strategy is designed for manual management. It requires the user to turn the script/alerts OFF after a significant drawdown and only reactivate it once a recovery trend is established externally.

The strategy uses a combination of dynamic trailing stops, structural support/resistance zones, and a fixed profit target to manage open positions.

🛑 Strategy Exit Logic

1. General Stop-Loss (Dynamic Trailing Stop)

These conditions act as the primary dynamic stop, closing the position if the market reverses past a key Moving Average (MA):

- Long Positions Closed When: The current bar's close crosses under the 50-Period EMA (emaLong).

- Short Positions Closed When: The current bar's close crosses above the 50-Period EMA (emaLong).

2. Profit Target (Fixed Percentage)

The script includes a general exit based on a user-defined profit percentage:

Take Profit Trigger: The position is closed when the currentProfitPercent meets or exceeds the input Profit Target (%) (default is 1.0% of the entry price).

3. Structural Exits (Daily Pivot Points)

These exits are high-priority, "close all" orders that trigger when the price fails to hold or reclaims a recent Daily Pivot Point, suggesting a failure of the current move.

- VR Close All - Long ($\sym{size} > 0$) - Price crosses under a Daily Resistance Level (R1, R2, or R3) minus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Resistance as support.

- VS Close All - Short ($\sym{size} < 0$) - Price crosses above a Daily Support Level (S1, S2, or S3) plus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Support as resistance.

4. Trend Failure Exit (Trend-Following Signals Only)

This exit protects against holding a position when the primary high-timeframe trend used for the entry has failed:

- Long Positions Closed When: The primary trend is no longer "bullish" for more than 2 consecutive bars (i.e., it turned "bearish" or "flat").

- Short Positions Closed When: The primary trend is no longer "bearish" for more than 2 consecutive bars (i.e., it turned "bullish" or "flat").

5. End of Day (EOD) Session Control

The final hard exits based on time:

- End of Session (EoS): At 11:30 AM, new trades are disabled (TradingDay := false). Open positions are kept.

- End of Day (EoD): At 1:30 PM, all remaining open positions are closed (strategy.close_all).

🤝 Development & Disclaimer

This script and description were created with assistance from Gemini and GitHub Copilot. My focus is on helping fellow real estate investors and day traders develop mechanically sound systems.

Disclaimer: This is for educational purposes only and does not constitute financial advice. Always abide by the Realtor Code and manage your own risk.

Gold 15m: Trend + S/R + Liquidity Sweep (RR 1:2)This strategy is designed for short-term trading on XAUUSD (Gold) using the 15-minute timeframe. It combines trend direction, support/resistance pivots, liquidity sweep detection, and momentum confirmation to identify high-probability reversal setups in line with the dominant market trend.

⚙️ Core Logic:

Trend Filter (EMA 200):

The strategy only takes long positions when price is above the 200 EMA and short positions when price is below it.

Support/Resistance via Pivots:

Dynamic swing highs and lows are identified using pivot points. These act as local supply and demand levels where liquidity is likely to accumulate.

Liquidity Sweep Detection:

A bullish liquidity sweep occurs when price briefly breaks below the last pivot low (grabbing liquidity) and then closes back above it.

A bearish sweep occurs when price breaks above the last pivot high and then closes back below.

Momentum & Candle Strength:

The strategy filters signals based on candle range and body size to ensure entries occur during strong price reactions, not weak retracements.

Risk Management (1:2 RR):

Stop-loss is placed slightly beyond the last pivot level using ATR-based buffers, and take-profit is set at 2× the risk distance, maintaining a reward-to-risk ratio of 1:2.

💼 Trade Logic Summary:

Long Entry:

After a bullish liquidity sweep & reclaim, momentum confirmation, and trend alignment (above EMA 200).

Short Entry:

After a bearish sweep & reclaim, momentum confirmation, and trend alignment (below EMA 200).

Exit:

Automated via ATR-based Stop Loss and Take Profit targets.

📊 Customization Options:

Adjustable EMA length, pivot settings, ATR multipliers, and RR ratio.

Option to enable/disable trend filter.

Toggle display of S/R zones on chart.

🧠 Best Use:

Works best during London and New York sessions when Gold shows strong momentum.

Can be adapted for forex pairs and indices by tuning ATR and pivot parameters.

AVGO Advanced Day Trading Strategy📈 Overview

The AVGO Advanced Day Trading Strategy is a comprehensive, multi-timeframe trading system designed for active day traders seeking consistent performance with robust risk management. Originally optimized for AVGO (Broadcom), this strategy adapts well to other liquid stocks and can be customized for various trading styles.

🎯 Key Features

Multiple Entry Methods

EMA Crossover: Classic trend-following signals using fast (9) and medium (16) EMAs

MACD + RSI Confluence: Momentum-based entries combining MACD crossovers with RSI positioning

Price Momentum: Consecutive price action patterns with EMA and RSI confirmation

Hybrid System: Advanced multi-trigger approach combining all methodologies

Advanced Technical Arsenal

When enabled, the strategy analyzes 8+ additional indicators for confluence:

Volume Price Trend (VPT): Measures volume-weighted price momentum

On-Balance Volume (OBV): Tracks cumulative volume flow

Accumulation/Distribution Line: Identifies institutional money flow

Williams %R: Momentum oscillator for entry timing

Rate of Change Suite: Multi-timeframe momentum analysis (5, 14, 18 periods)

Commodity Channel Index (CCI): Cyclical turning points

Average Directional Index (ADX): Trend strength measurement

Parabolic SAR: Dynamic support/resistance levels

🛡️ Risk Management System

Position Sizing

Risk-based position sizing (default 1% per trade)

Maximum position limits (default 25% of equity)

Daily loss limits with automatic position closure

Multiple Profit Targets

Target 1: 1.5% gain (50% position exit)

Target 2: 2.5% gain (30% position exit)

Target 3: 3.6% gain (20% position exit)

Configurable exit percentages and target levels

Stop Loss Protection

ATR-based or percentage-based stop losses

Optional trailing stops

Dynamic stop adjustment based on market volatility

📊 Technical Specifications

Primary Indicators

EMAs: 9 (Fast), 16 (Medium), 50 (Long)

VWAP: Volume-weighted average price filter

RSI: 6-period momentum oscillator

MACD: 8/13/5 configuration for faster signals

Volume Confirmation

Volume filter requiring 1.6x average volume

19-period volume moving average baseline

Optional volume confirmation bypass

Market Structure Analysis

Bollinger Bands (20-period, 2.0 multiplier)

Squeeze detection for breakout opportunities

Fractal and pivot point analysis

⏰ Trading Hours & Filters

Time Management

Configurable trading hours (default: 9:30 AM - 3:30 PM EST)

Weekend and holiday filtering

Session-based trade management

Market Condition Filters

Trend alignment requirements

VWAP positioning filters

Volatility-based entry conditions

📱 Visual Features

Information Dashboard

Real-time display of:

Current entry method and signals

Bullish/bearish signal counts

RSI and MACD status

Trend direction and strength

Position status and P&L

Volume and time filter status

Chart Visualization

EMA plots with customizable colors

Entry signal markers

Target and stop level lines

Background color coding for trends

Optional Bollinger Bands and SAR display

🔔 Alert System

Entry Alerts

Customizable alerts for long and short entries

Method-specific alert messages

Signal confluence notifications

Advanced Alerts

Strong confluence threshold alerts

Custom alert messages with signal counts

Risk management alerts

⚙️ Customization Options

Strategy Parameters

Enable/disable long or short trades

Adjustable risk parameters

Multiple entry method selection

Advanced indicator on/off toggle

Visual Customization

Color schemes for all indicators

Dashboard position and size options

Show/hide various chart elements

Background color preferences

📋 Default Settings

Initial Capital: $100,000

Commission: 0.1%

Default Position Size: 10% of equity

Risk Per Trade: 1.0%

RSI Length: 6 periods

MACD: 8/13/5 configuration

Stop Loss: 1.1% or ATR-based

🎯 Best Use Cases

Day Trading: Designed for intraday opportunities

Swing Trading: Adaptable for longer-term positions

Momentum Trading: Excellent for trending markets

Risk-Conscious Trading: Built-in risk management protocols

⚠️ Important Notes

Paper Trading Recommended: Test thoroughly before live trading

Market Conditions: Performance varies with market volatility

Customization: Adjust parameters based on your risk tolerance

Educational Purpose: Use as a learning tool and customize for your needs

🏆 Performance Features

Detailed performance metrics

Trade-by-trade analysis capability

Customizable risk/reward ratios

Comprehensive backtesting support

This strategy is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and consider your financial situation before trading.

LP Sweep / Reclaim & Breakout Grading: Long-onlySignals

1) LP Sweep & Reclaim (mean-reversion entry)

Compute LP bounds from prior-bar window extremes:

lpLL_prev = lowest low of the last N bars (offset 1).

lpHH_prev = highest high of the last N bars (offset 1).

Sweep long trigger: current low dips below lpLL_prev and closes back above it.

Real-time quality grading (A/B/C) for sweep:

Trend filter & slope via EMA(88).

BOS bonus: close > last confirmed swing high.

Body size vs ATR, location above a long EMA, headroom to swing high (penalty if too close), and multi-sweep count bonus.

Sum → score → grade A/B/C; A or B required for sweep entry.

2) Trend Breakout (momentum entry)

Core trigger: close > previous Donchian high (length boLen) + ATR buffer.

Optional filter: close must be above the default EMA.

Breakout grading (A/B/C) in real time combining:

Trend up (price > EMA and EMA rising),

Body/ATR, Gap above breakout level (in ATR),

Volume vs MA,

Upper-wick penalty,

Position-in-Score: headroom to last swing high (penalty if too near) + EMA slope bonus.

Sum → score → A or B required if grading enabled.

Lavender Multi-Signal Momentum StrategyOverview

The Lavender strategy is a sophisticated momentum-based trading system specifically optimized for Tesla (TSLA) on the 15-minute timeframe. It combines multiple technical signals to identify high-probability long entries during strong trending conditions.

Key Features

🎯 Multi-Signal Entry System

The strategy uses 4 distinct signal types that can be enabled/disabled individually:

Supertrend Pullback (Default: ON)

Identifies pullbacks in uptrends using Supertrend (ATR: 9, Factor: 0.5)

Enters when price retests EMA9-20 zone during bullish Supertrend

Donchian Breakout + Z-Score Momentum (Default: ON)

53-period Donchian channel breakouts

Combined with 35-period Z-Score momentum filter

Only triggers with positive momentum confirmation

Keltner Squeeze Expansion (Default: OFF)

Detects volatility squeeze conditions

Enters on breakout above Keltner Channel after compression

Opening Range Breakout (ORB) (Default: ON)

Tracks first hour range (9:30-10:30 AM)

Triggers on breakout above opening range high

🧭 Trend Regime Filter

EMA Trend Filter: 20 EMA > 100 EMA (Default: ON)

ADX Strength Filter: ADX > 22 with 15/13 smoothing (Default: ON)

Only trades when both trend conditions align

💵 Advanced Risk Management

Risk per Trade: 2.0% of capital (Default)

ATR-Based Stop Loss: 15-period ATR × 1.6 multiplier

Risk/Reward Ratio: 4:1 (Default)

Position Sizing: Automatic based on stop distance

Capital Options: Dynamic equity or fixed capital ($200,000 default)

⚙️ Execution Control

Candle Close Entries: Prevents intrabar noise (Default: ON)

Candle Close Exits: Stop loss and take profit only at bar close (Default: ON)

Trading Session: 9:00 AM - 4:00 PM (Default)

Trading Days: Monday-Saturday (Default: 123456)

Default Settings Summary

ParameterDefault ValuePurposeRisk per Trade2.0%Capital risk percentageATR Length15Stop loss calculationATR Multiplier1.6Stop distance factorRisk/Reward4.0Take profit multiplierEMA Fast20Short-term trendEMA Slow100Long-term trendADX Threshold22Minimum trend strengthMin Signals Required1Entry trigger thresholdInitial Capital$200,000Backtesting capital

How It Works

Trend Confirmation: Checks EMA alignment and ADX strength

Signal Generation: Scans for active momentum signals

Entry Execution: Enters when minimum signal threshold is met

Risk Management: Calculates position size based on ATR stop

Exit Management: Manages trades with 4:1 risk/reward ratio

Best Use Cases

Tesla (TSLA) on 15-minute charts

Trending market conditions

Intraday momentum trading

Markets with clear directional bias

Visual Indicators

Blue Line: 100-period EMA (trend filter)

Green/Red Line: Supertrend indicator

Teal Line: Donchian channel high

Purple Triangles: Keltner breakout signals

Orange Arrows: Opening range breakouts

Green Dots: Combined entry signals

Red/Green Lines: Active stop loss and take profit levels

Risk Disclaimer

This strategy is optimized for Tesla's specific price behavior on 15-minute timeframes. Past performance does not guarantee future results. Always test thoroughly and manage risk appropriately.

Created by kevloewe - Specialized for TSLA 15M momentum trading

AVWAP+RSI Confluence — 1R TesterRSI + 1R ATR - Monthly P\&L (v4)

WHAT THIS STRATEGY DOES (OVERVIEW)

* Pine strategy (v4) that combines a simple momentum trigger with a symmetric 1R ATR risk model and an on-chart Monthly/Yearly P\&L table.

* Momentum filter: trades only when RSI crosses its own SMA in the direction of the trend (price vs Trend EMA).

* Risk engine: exits use fixed 1R ATR brackets captured at entry (no drifting targets/stops).

* Accounting: the table aggregates percentage returns by month and year using strategy equity.

ENTRY LOGIC (LONGS & OPTIONAL SHORTS)

Indicators used:

* RSI(rsiLen) and its SMA: SMA(RSI, rsiMaLen)

* Trend filter: EMA(emaTrendLen) on price

Longs:

1. RSI crosses above its RSI SMA

2. RSI > rsiBuyThr (filters weak momentum)

3. Close > EMA(emaTrendLen)

Shorts (optional via enableShort):

1. RSI crosses below its RSI SMA

2. RSI < rsiSellThr

3. Close < EMA(emaTrendLen)

EXIT LOGIC AND RISK MODEL (1R ATR)

* On entry, snapshot ATR(atrLen) into atrAtEntry and the average fill price into entryPx.

* Longs: stop = entryPx - ATR \* atrMult; target = entryPx + ATR \* atrMult

* Shorts: mirrored.

* Stops and targets are posted immediately and remain fixed for the life of the trade.

POSITION SIZING AND COSTS

* Default position size: 25% of equity per trade (adjustable in Properties/inputs).

* Commission percent and a small slippage are set in strategy() so backtests include friction by default.

MONTHLY / YEARLY P\&L TABLE (HOW IT WORKS)

* Uses strategy equity to compute bar returns: equity / equity\ - 1.

* Compounds bar returns into current month and current year; commits each finished period at month/year change (or last bar).

* Renders rows as years; columns Jan..Dec plus a Year total column.

* Cells colored by sign; precision and maximum rows are controlled by inputs.

* Values represent percentage returns, not currency P\&L.

VISUAL AIDS

* Two pivot trails (pivot high/low) are plotted for context only; they do not affect entries or exits.

CUSTOMIZATION TIPS

* Raise rsiBuyThr (long) or lower rsiSellThr (short) to filter weak momentum.

* Increase emaTrendLen to tighten trend alignment.

* Adjust atrLen and atrMult to fit your timeframe/instrument volatility.

* Leave enableShort = false if you prefer long-only behavior or shorting is constrained.

NON-REPAINTING AND BACKTEST NOTES

* Signals use bar-close crosses of built-in indicators (RSI, EMA, ATR); no future bars are referenced.

* calc\_on\_every\_tick = true for responsive visuals; Strategy Tester evaluates on bar close in history.

* Backtest stop/limit fills are simulated and may differ from live execution/liquidity.

DISCLAIMERS

* Educational use only. This is not financial advice. Markets involve risk. Past performance does not guarantee future results.

INPUTS (QUICK REFERENCE)

* rsiLen, rsiMaLen, rsiBuyThr, rsiSellThr

* emaTrendLen

* atrLen, atrMult, enableShort

* leftBars, rightBars, prec, showTable, maxYearsRows

SHORT TAGLINE

RSI momentum with 1R ATR brackets and a built-in Monthly/Yearly P\&L table.

TAGS

strategy, RSI, ATR, trend, risk-management, backtest, Pine-v4

RSI + MACD Long-Only StrategyRSI + MACD Long-Only Strategy

Overview: Momentum-based, long-only strategy combining RSI and MACD. Entries favor upside momentum; exits trigger on momentum fades or risk targets. Signals are state-gated so you get one exit per entry (no multiple exits without a prior entry).

Entry conditions:

RSI crosses above the midline (default 50) while MACD is bullish (MACD > Signal, optionally MACD > 0), OR

MACD crosses above its Signal while RSI is at/above the midline.

Optional filters:

EMA trend filter: only enter if price > EMA(n).

Oversold context: only enter within N bars after RSI dipped below the oversold threshold.

Exit conditions:

RSI crosses below the midline, OR

MACD crosses below its Signal with MACD histogram ≤ 0.

Optional risk exit: Take Profit / Stop Loss based on percentage from average entry price.

Risk management:

Inputs: Use TP/SL (on/off), TP% (default 3.0), SL% (default 1.5).

Implements protective strategy.exit (limit/stop) while in position.

Signal-based exit uses strategy.close to flatten.

Position management:

Long-only, no pyramiding (single position at a time).

Internal state ensures entries occur only when flat and exits only when in a position.

Inputs you can tune:

RSI: length, overbought, oversold, midline.

MACD: fast length, slow length, signal length; toggle “Require MACD > 0”.

Signals: oversold lookback window; EMA trend on/off and EMA length.

Risk: TP% and SL%.

Visuals: show entry/exit markers, bar coloring; optional debug background on raw triggers.

Visuals and alerts:

Plots EMA (optional), draws entry/exit markers, optional bar coloring, and a faint background on raw long triggers to aid tuning.

Alert conditions provided for entries and exits.

Notes:

Designed for bar-close evaluation; performance varies by symbol/timeframe—tune inputs accordingly.

Long-only; intended for trend-following momentum with basic risk control.

Not financial advice.

Vegas Tunnel StrategyVegas Tunnel Strategy is a trend-following breakout system based on exponential moving averages (EMAs). It uses a "tunnel" formed by the 144 EMA and 169 EMA to identify the market's long-term trend direction. Entry signals are generated when a shorter-term EMA (12 EMA) breaks above or below this tunnel, confirming momentum alignment.

Long Setup: Price and EMA12 are above the tunnel (EMA144 < EMA169); entry on pullback near the tunnel.

Short Setup: Price and EMA12 are below the tunnel (EMA144 > EMA169); entry on rebound near the tunnel.

Exit Rules: Fixed stop loss below/above the tunnel or based on ATR; take profit at 1.5–2× the risk.

This strategy works best on 4H or daily charts and is suitable for trending assets like FX pairs, gold, oil, or indices.