IU Opening range Breakout StrategyIU Opening Range Breakout Strategy

This Pine Script strategy is designed to capitalize on the breakout of the opening range, which is a popular trading approach. The strategy identifies the high and low prices of the opening session and takes trades based on price crossing these levels, with built-in risk management and trade limits for intraday trading.

Key Features:

1. Risk Management:

- Risk-to-Reward Ratio (RTR):

Set a customizable risk-to-reward ratio to calculate target prices based on stop-loss levels.

Default: 2:1

- Max Trades in a Day:

Specify the maximum number of trades allowed per day to avoid overtrading.

Default: 2 trades in a day.

- End-of-Day Close:

Automatically closes all open positions at a user-defined session end time to ensure no overnight exposure.

Default: 3:15 PM

2. Opening Range Identification

- Opening Range High and Low:

The script detects the high and low of the first trading session using Pine Script's session functions.

These levels are plotted as visual guides on the chart:

- High: Lime-colored circles.

- Low: Red-colored circles.

3. Trade Entry Logic

- Long Entry:

A long trade is triggered when the price closes above the opening range high.

- Entry condition: Crossover of the price above the opening range high.

-Short Entry:

A short trade is triggered when the price closes below the opening range low.

- Entry condition: Crossunder of the price below the opening range low.

Both entries are conditional on the absence of an existing position.

4. Stop Loss and Take Profit

- Long Position:

- Stop Loss: Previous candle's low.

- Take Profit: Calculated based on the RTR.

- **Short Position:**

- **Stop Loss:** Previous candle's high.

- **Take Profit:** Calculated based on the RTR.

The strategy plots these levels for visual reference:

- Stop Loss: Red dashed lines.

- Take Profit: Green dashed lines.

5. Visual Enhancements

-Trade Level Highlighting:

The script dynamically shades the areas between the entry price and SL/TP levels:

- Red shading for the stop-loss region.

- Green shading for the take-profit region.

- Entry Price Line:

A silver-colored line marks the average entry price for active trades.

How to Use:

1.Input Configuration:

Adjust the Risk-to-Reward ratio, max trades per day, and session end time to suit your trading preferences.

2.Visual Cues:

Use the opening range high/low lines and shading to identify potential breakout opportunities.

3.Execution:

The strategy will automatically enter and exit trades based on the conditions. Review the plotted SL and TP levels to monitor the risk-reward setup.

Important Notes:

- This strategy is designed for intraday trading and works best in markets with high volatility during the opening session.

- Backtest the strategy on your preferred market and timeframe to ensure compatibility.

- Proper risk management and position sizing are essential when using this strategy in live markets.

ابحث في النصوص البرمجية عن "entry"

Turtle Trade Channels Indicator with EMATurtle Trade Channels Indicator with EMA (TuTCI + EMA)

This custom indicator combines the classic Turtle Trading Channel strategy with an Exponential Moving Average (EMA) filter to provide clear entry and exit signals, as well as trend direction guidance.

Features:

Turtle Channels: The indicator calculates the upper and lower Turtle Trading Channels based on the highest and lowest values over a user-defined period ( Entry Length for the channel).

Entry/Exit Signals: Alerts you to potential buy and sell opportunities with visual signals on the chart.

Long Entry: When the price crosses above the upper channel.

Short Entry: When the price crosses below the lower channel.

Long Exit: When the price breaks below the exit line.

Short Exit: When the price breaks above the exit line.

EMA Filter: A 50-period Exponential Moving Average (EMA) is included to identify the overall trend. The background color turns green when the price is above the EMA (bullish trend) and red when the price is below the EMA (bearish trend).

Highlighter: Optional background highlighting for the most relevant signals, such as when the price crosses the upper or lower Turtle Channel. This feature helps to easily identify key market movements.

Visual Customization: Customize the EMA length, Entry/Exit lengths, and toggle signals and highlighting to suit your preferences.

How It Works:

The Turtle Trade Channels are designed to capture breakouts by identifying key price levels (highest high and lowest low) over a specified period. By combining this strategy with an EMA, the indicator ensures trades are aligned with the broader trend, increasing the probability of successful trades.

Uptrend: When the price is above the EMA, the indicator considers the trend to be bullish, and it highlights long entry signals.

Downtrend: When the price is below the EMA, the trend is considered bearish, and short entries are emphasized.

Customization:

Entry Length: Adjusts the period for calculating the Turtle Channel's entry levels.

Exit Length: Defines the period for calculating the exit levels.

EMA Length: The period for the Exponential Moving Average (default is set to 50).

Show Entry/Exit Signals: Toggle the visibility of entry/exit signals on the chart.

Highlighter On/Off: Toggle background highlighting for key signals.

This indicator is suitable for traders who follow trend-following strategies, particularly those influenced by the Turtle Trading methodology, and wish to use an EMA filter for better trend confirmation.

Use Cases:

Trend-following traders looking for clear entry/exit signals.

Breakout traders using the Turtle Trading concept to identify price breakouts.

Swing traders who want to incorporate trend analysis with price levels.

MERCURY by DrAbhiramSivprasad"MERCURY by DrAbhiramSivprasad"

Developed from over 10 years of personal trading experience, the Mercury Indicator is a strategic tool designed to enhance accuracy in trading decisions. Think of it as a guiding light—a supportive tool that helps traders refine and build more robust strategies by integrating multiple powerful elements into a single indicator. I’ll be sharing some examples to illustrate how I use this indicator in my own trading journey, highlighting its potential to improve strategy accuracy.

Reason behind the combination of emas , cpr and vwap is it provides very good support and resistance in my trading carrier so now i brought them together in one plate

How It Works:

Mercury combines three essential elements—EMA, VWAP, and CPR—each of which plays a vital role in detecting support and resistance:

Exponential Moving Averages (EMAs): Known for their strength in providing dynamic support and resistance levels, EMAs help in identifying trends and shifts in momentum. This indicator includes a dashboard with up to nine customizable EMAs, showing whether each is acting as support or resistance based on real-time price movement.

Volume Weighted Average Price (VWAP): VWAP also provides valuable support and resistance, often regarded as a fair price level by institutional traders. Paired with EMAs, it forms a dual-layered support/resistance system, adding an additional level of confirmation.

Central Pivot Range (CPR): By combining CPR with EMAs and VWAP, Mercury highlights “traffic blocks” in your target journey. This means it identifies zones where price is likely to stall or reverse, providing additional guidance for navigating entries and exits.

Why This Combination Matters:

Using these three tools together gives you a more complete view of the market. VWAP and EMAs offer dynamic trend direction and support/resistance, while CPR pinpoints critical price zones. This combination helps you find high-probability trades, adding clarity to complex market situations and enabling stronger confirmation on trend or reversal decisions.

How to Use:

Trend Confirmation: Check if all EMAs are aligned (green for uptrend, red for downtrend), which is visible in the EMA dashboard. An alignment across VWAP, CPR, and EMAs signifies high confidence in trend direction.

Breakouts & Breakdowns: Mercury has an alert system to signal when a price breakout or breakdown occurs across VWAP, EMA1, and EMA2. This can help in spotting strong directional moves.

Example Application: In my trading, I use Mercury to identify support/resistance zones, confirming trends with EMA/VWAP alignment and using CPR as a checkpoint. I find this especially useful for day trading and swing setups.

Recommended Timeframes:

Day Trading: 5 to 15-minute charts for swift, actionable insights.

Swing Trading: 1-hour or 4-hour charts for broader trend analysis.

Note:

The Mercury Indicator should be used as a supportive tool rather than a standalone strategy, guiding you toward informed decisions in line with your trading style and goals.

EXAMPLE OF TRADE

you can see the cart of XAUUSD on 11th nov 2024

1.SHORT POSITION - TIME FRAME 15 MIN

So here for a short position you need to wait for a breakdown candle which will print in orange post the candle you need to check ema dashboard is completly red that indicates no traffic blocks in your journey to destiny target from ema's and you can take the target from nearest cpr support line

TAKEN IN XAUUSD you can see in chart of XAUUSD on 7th nov

2.LONG POSITION - TIME FRAME 15 MIN -

So here for long position you need to wait for a breakout candle from indicator thats here is blue and check all ema boxes are green and candle body should close above all the 3 lines here it is the both ema 1 and 2 and the vwap line then you can take and entry and your target will be the nearest resistance from the daily cpr

3. STOP LOSS CRITERIA

After the entry any candle close below any of the last line from entry for example we have 3 lines vwap and ema 1 and 2 lines and u have made an entry and the last line before the entry is vwap then if any candle closes below vwap can be considered as stoploss like wise in any lines

The MERCURY indicator is a comprehensive trading tool designed to enhance traders' ability to identify trends, breakouts, and reversals effectively. Created by Dr. Abhiram Sivprasad, this indicator integrates several technical elements, including Central Pivot Range (CPR), EMA crossovers, VWAP levels, and a table-based EMA dashboard, to offer a holistic trading view.

Core Components and Functionality:

Central Pivot Range (CPR):

The CPR in MERCURY provides a central pivot level along with Below Central (BC) and Top Central (TC) pivots. These levels act as potential support and resistance, useful for identifying reversal points and zones where price may consolidate.

Exponential Moving Averages (EMAs):

MERCURY includes up to nine EMAs, with a customizable EMA crossover alert system. This feature enables traders to see shifts in trend direction, especially when shorter EMAs cross longer ones.

VWAP (Volume-Weighted Average Price):

VWAP is incorporated as a dynamic support/resistance level and, combined with EMA crossovers, helps refine entry and exit points for higher probability trades.

Breakout and Breakdown Alerts:

MERCURY monitors conditions for upside and downside breakouts. For an upside breakout, all EMAs turn green and a candle closes above VWAP, EMA1, and EMA2. Similarly, all EMAs turning red, combined with a close below VWAP and EMA1/EMA2, signals a downside breakdown. Continuous alerts are available until the trend shifts.

Real-Time EMA Dashboard:

A table displays each EMA’s relative position (Above or Below), helping traders quickly gauge trend direction. Colors in the table adjust to long/short conditions based on EMA alignment.

Usage Recommendations:

Trend Confirmation:

Use the CPR, EMA alignments, and VWAP to confirm uptrends and downtrends. The table highlights trends, making it easy to spot long or short setups at a glance.

Breakout and Breakdown Alerts:

The alert system is customizable for continuous notifications on critical price levels. When all EMAs align in one direction (green for long, red for short) and the close is above or below VWAP and key EMAs, the indicator confirms a breakout/breakdown.

Adaptable for Different Styles:

Day Trading: Traders can set shorter EMAs for quick insights.

Swing Trading: Longer EMAs combined with CPR offer insights into sustained trends.

Recommended Settings:

Timeframes: MERCURY is suitable for timeframes as low as 5 minutes for intraday traders, up to daily charts for trend analysis.

Symbols: Works across forex, stocks, and crypto. Adjust EMA lengths for asset volatility.

Example Strategy:

Long Entry: When the price crosses above CPR and closes above both EMA1 and EMA2.

Short Entry: When the price falls below CPR with a close below both EMA1 and EMA2.

Austin's Apex AcceleratorIndicator Name: Austin’s Apex Accelerator

Overview

The Austin’s Apex Accelerator is a highly aggressive trading indicator designed specifically for high-frequency Forex trading. It combines several technical analysis tools to identify rapid entry and exit points, making it well-suited for intraday or even lower timeframe trades. The indicator leverages a combination of exponential moving averages (EMAs), Bollinger Bands, volume filters, and volatility-adjusted ranges to detect breakout opportunities and manage risk with precision.

Core Components

Fast and Slow EMAs: The two EMAs act as trend and momentum indicators. When the shorter EMA crosses the longer EMA, it signals a change in momentum. The crossover of these EMAs often indicates a potential entry point, especially when combined with volume and volatility filters.

ATR-Based Range Filter: Using the Average True Range (ATR) for dynamic range calculation, the indicator adapts to market volatility. Higher ATR values widen the range, helping the indicator adjust for volatile conditions.

Volume Filter: A volume condition ensures that buy and sell signals only trigger when there’s significant market interest, reducing the likelihood of false signals in low-liquidity environments.

Bollinger Bands: The Bollinger Bands provide additional context for potential overbought or oversold conditions, highlighting opportunities for price reversals or trend continuations.

Key Features

Aggressive Buy and Sell Signals:

Buy Signal: A buy signal is generated when the fast EMA crosses above the slow EMA, confirming bullish momentum, and the volume condition is met. If the price is also near the lower Bollinger Band, it adds further confirmation of an oversold condition.

Sell Signal: A sell signal is generated when the fast EMA crosses below the slow EMA, confirming bearish momentum, with sufficient trading volume. If the price is near the upper Bollinger Band, it signals a potential overbought condition, which supports the sell signal.

Dynamic Range with ATR:

The indicator uses a volatility-based range, derived from the ATR, to adjust the signal sensitivity based on recent price fluctuations. This dynamic range ensures that signals are responsive in both high and low volatility conditions.

The range’s upper and lower bands act as thresholds, with trades often occurring when the price breaches these levels, signaling momentum shifts or trend reversals.

Trend Background Color:

A green background highlights bullish trends when the fast EMA is above the slow EMA.

A red background signifies bearish trends when the fast EMA is below the slow EMA, providing a visual indication of the overall market trend direction.

Trend Line:

The indicator plots a dynamic trend line that changes color based on the price's relationship to the EMAs, helping traders quickly assess the current trend’s strength and direction.

Alerts:

The indicator includes configurable alerts for buy and sell signals, allowing traders to be notified of entry opportunities without needing to monitor the chart continuously.

How to Use Austin’s Apex Accelerator

Identify Entry Points:

Buy Entry: When the fast EMA crosses above the slow EMA, a buy signal is triggered. Confirm this signal by checking if the price is near or below the lower Bollinger Band (indicating an oversold condition) and if trading volume meets the set threshold.

Sell Entry: When the fast EMA crosses below the slow EMA, a sell signal is triggered. Confirm the signal by ensuring the price is near or above the upper Bollinger Band (suggesting an overbought condition) and that volume is sufficient.

Exit Strategy:

Take Profit: The take profit level is calculated as 1.5 times the ATR from the entry point. This ensures that each trade aims to achieve a positive risk/reward ratio.

Stop Loss: The stop loss is set at 1 ATR from the entry, providing a tight risk control mechanism that limits potential losses on each trade.

Trend Identification and Background Colors:

Use the background colors to assess the trend direction. A green background indicates a bullish trend, while a red background suggests a bearish trend. These colors can help you filter signals that go against the trend, increasing the chances of a successful trade.

Volume Confirmation:

This indicator has an inbuilt volume filter to prevent trading in low-volume conditions. Look for signals only when volume exceeds the average volume threshold, which is set by the multiplier. This helps avoid trading during quieter times when false signals are more likely.

Alerts:

Set up alerts for buy and sell signals to be notified in real-time whenever a new trading opportunity arises, so you can act on high-quality signals promptly.

Practical Tips for Using Austin’s Apex Accelerator

Timeframe: Best suited for short timeframes such as 5-minute or 15-minute charts for high-frequency trading.

Trend Magic with EMA, SMA, and Auto-TradingRelease Notes

Strategy Name: Trend Magic with EMA, SMA, and Auto-Trading

Purpose: This strategy is designed to capture entry and exit points in the market using the Trend Magic indicator and three moving averages (EMA45, SMA90, and SMA180). Specifically, it uses the perfect order of the moving averages and the color changes in Trend Magic to identify trend reversals and potential trading opportunities.

Uniqueness and Usefulness

Uniqueness: The strategy utilizes the Trend Magic indicator, which is based on price and volatility, along with three moving averages to assess the strength of trends. The signals are generated only when the moving averages are in perfect order, and the Trend Magic color changes, ensuring that the entry is made during established trends. This combination provides a higher degree of reliability compared to strategies that rely solely on price action or single indicators.

Usefulness: This strategy is particularly useful for traders looking to capture trends over longer periods. It is effective at reducing noise in the market, only providing signals when the moving averages align and the Trend Magic indicator confirms a trend reversal. It works well in both trending and volatile markets.

Entry Conditions

Long Entry:

Condition: A perfect order (EMA45 > SMA90 > SMA180) is established, and Trend Magic changes color from red to blue.

Signal: A buy signal is generated, indicating the start of an uptrend.

Short Entry:

Condition: A perfect order (EMA45 < SMA90 < SMA180) is established, and Trend Magic changes color from blue to red.

Signal: A sell signal is generated, indicating the start of a downtrend.

Exit Conditions

Exit Strategy:

This strategy automatically enters and exits trades based on signals, but traders are encouraged to manage exits manually according to their own risk management preferences. The strategy includes stop loss and take profit settings based on risk-to-reward ratios for better risk management.

Risk Management

The strategy includes built-in risk management by using the SMA90 level at the time of entry as the stop-loss point and setting the take profit at a 1:1.5 risk-to-reward ratio. The stop-loss level is fixed at the entry point and does not move as the market progresses. Traders are advised to implement additional risk management, such as trailing stops, for added protection.

Account Size: ¥100,000

Commissions and Slippage: Assumes 94 pips for commissions and 1 pip for slippage per trade

Risk per Trade: 10% of account equity (adjust this based on personal risk tolerance)

Configurable Options

Configurable Options:

CCI Period: Set the period for the CCI used to calculate the Trend Magic indicator (default is 21).

ATR Multiplier: Set the multiplier for ATR used in the Trend Magic calculation (default is 1.0).

EMA/SMA Periods: The periods for the three moving averages (default is EMA45, SMA90, and SMA180).

Signal Display Control: An option to toggle the display of buy and sell signals on the chart.

Adequate Sample Size

To ensure the robustness and reliability of this strategy, it is recommended to backtest it with a sufficiently long period of historical data. Testing across different market conditions, including high and low volatility periods, is also advised.

Credits

Acknowledgments:

This strategy is based on the Trend Magic indicator combined with moving averages and draws on contributions from the technical analysis and trading community.

Clean Chart Description

Chart Appearance:

To maintain a clean and simple chart, this strategy includes options to turn off the display of Trend Magic, moving averages, and entry signals. Traders can adjust these display settings as needed to minimize visual clutter and focus on effective trend analysis.

Addressing the House Rule Violations

Omissions and Unrealistic Claims

Clarification:

This strategy does not make any unrealistic or unsupported claims about its performance. All signals are intended for educational purposes only and do not guarantee future results. It is important to note that past performance does not guarantee future outcomes, and proper risk management is crucial.

Monthly Day Long Strategy with VIX and Risk ManagementThis trading strategy is designed to open long positions on a specific day of the month, with the conditions for entry and exit based on the VIX index and additional risk management techniques. The strategy includes stop-loss and take-profit features to manage risk and lock in profits.

Inputs:

Entry Day of the Month (entry_day): Specifies which day of the month to consider for initiating a trade. The default value is the 27th.

Hold Duration (Days) (hold_duration_days): Defines how many days to hold the position after opening. The default value is 4 days.

VIX Threshold (vix_threshold): Sets the maximum acceptable value for the VIX index to consider an entry. If the VIX is below this threshold, it signals a potential trade. The default value is 20.0.

Stop Loss (%) (stop_loss_percentage): Determines the percentage below the entry price where the stop-loss will be triggered. The default value is 2.0%.

Take Profit (%) (take_profit_percentage): Sets the percentage above the entry price where the take-profit will be triggered. The default value is 5.0%.

Functions:

next_weekday(date): Adjusts the entry date to the next Monday if it falls on a weekend (Saturday or Sunday). This ensures trades do not occur on non-trading days.

Logic:

Entry Conditions:

Date Check: Opens a long position if the current date matches the adjusted entry date (the 27th or the next Monday if the 27th falls on a weekend).

VIX Filter: The VIX index value must be below the specified threshold (e.g., 20.0) to consider an entry.

Exit Conditions:

Time-Based Exit: Closes the position after the hold duration of 4 days.

Stop-Loss: Automatically closes the position if the price drops to a level that is a specified percentage below the entry price (e.g., 2.0%).

Take-Profit: Closes the position if the price rises to a level that is a specified percentage above the entry price (e.g., 5.0%).

Plots:

VIX Plot: Displays the VIX index on the chart for visual reference.

VIX Threshold Line: A horizontal line representing the VIX threshold value.

Summary:

The strategy aims to take advantage of specific entry days while filtering trades based on VIX levels to ensure market conditions are favorable. Risk management is enhanced through stop-loss and take-profit settings, which help in controlling potential losses and securing profits. The strategy ensures trades are only made on trading days and not on weekends, adjusting automatically to the next Monday if needed.

ChatGPT kann Fehler machen. Überprüfe wichtige Informationen.

Fibo Level DailyOverview

The "Fibo Level Daily" strategy is designed for trading Bitcoin (BTC) using the 1-hour timeframe. This strategy relies on Fibonacci levels calculated from the previous day's range and determines entry and exit points based on whether the previous daily candle was bullish or bearish.

How It Works

Fibonacci Levels Calculation:

The indicator calculates Fibonacci levels (0.8, 0.5, and 0.2) based on the high and low of the previous day.

The levels are calculated as follows:

0.8: This level is calculated by multiplying the difference between the previous day's high and low by 0.8 and adding the result to the previous day's low.

0.5: This is the midpoint of the previous day's range.

0.2: This level is calculated by multiplying the difference between the previous day's high and low by 0.2 and adding the result to the previous day's low.

Identifying the Previous Day's Trend:

The indicator checks if the previous daily candle closed bullish (close greater than open) or bearish (close less than open).

Setting Entry and Take Profit Levels:

If the previous daily candle was bearish:

Sell Entry: Wait for the price to rise to the 0.5 level (midpoint of the previous day's range) to enter a sell position.

Take Profit: The profit target is set at the 0.2 level.

If the previous daily candle was bullish:

Buy Entry: Wait for the price to drop to the 0.5 level (midpoint of the previous day's range) to enter a buy position.

Take Profit: The profit target is set at the 0.8 level.

Visual Representation on the Chart:

The indicator draws horizontal lines on the chart representing the Fibonacci levels (0.8, 0.5, and 0.2) from the previous day. These lines help visualize entry and exit points clearly.

Additionally, the last 15 minutes of the daily session are highlighted with a light red background to indicate the session's end.

Conditions of Use:

Timeframe: This indicator is specifically designed for use on the 1-hour timeframe.

Assets: While it can be used on any asset, it is optimized for trading Bitcoin (BTC).

Steps to Use the Indicator

Add the Indicator:

Insert the "Fibo Level Daily" indicator script into your trading platform (such as TradingView).

Select Timeframe:

Change the chart timeframe to 1 hour.

Interpret the Levels:

Observe the horizontal lines drawn on the chart representing the Fibonacci levels.

Identify whether the previous daily candle was bullish or bearish.

Wait for the Entry Price:

For a bearish previous daily candle: Wait for the price to rise to the 0.5 level to enter a sell position.

For a bullish previous daily candle: Wait for the price to drop to the 0.5 level to enter a buy position.

Set the Profit Target:

For a sell: Set your profit target at the 0.2 level.

For a buy: Set your profit target at the 0.8 level.

Execute the Trade:

Initiate the trade once the price reaches the entry level and set your take profit according to the identified trend from the previous day.

Conclusion

The "Fibo Level Daily" strategy provides a clear and precise methodology for identifying entry and exit points in Bitcoin using Fibonacci levels. By following this step-by-step guide, any trader can take advantage of market movements based on the previous day's price action, optimizing their trading opportunities on the 1-hour timeframe.

Triple MA HTF strategy - Dynamic SmoothingThe triple MA strategy is a simple but effective method to trade the trend. The advantage of this script over the existing triple MA strategies is that the user can open a lower time frame chart and select higher time frame inputs for different MA types mainting the visibility on the chart. The dynamic smoothing code makes sure the HTF trendlines are not jagged, but a fluid line visiable on the lower time frame chart. The script comes with a MA crossover and crossunder strategy explained below.

Moving Averages (MA) Crossover for Entry:

Long Entry: A long entry signal is triggered when the moving average line 1 crosses above the moving average line 2. This crossover indicates a potential shift in market sentiment towards the upside. However, to validate this signal, the strategy checks if the moving average 3 on a higher time frame (eg. 4 hour) is in an upward trend. This additional filter ensures that the trade aligns with the prevailing trend on a broader time scale, increasing the probability of success.

Short Entry: Conversely, a short entry signal occurs when the moving average line 1 crosses below the moving average line 2. This crossover suggests a possible downturn in market momentum. However, for a short trade to be confirmed, the strategy verifies that the moving average 3 on the higher time frame is in a downward trend. This confirmation ensures that the trade is in harmony with the overarching market direction.

Exit from Long Position: The strategy triggers an exit signal from a long position when the moving average line 1 crosses below the moving average line 2. This crossover indicates a potential reversal in the market trend, prompting the trader to close their long position and take profits or minimize losses.

Exit from Short Position: Similarly, an exit signal from a short position occurs when the moving average line 1 crosses above the moving average line 2. This crossover suggests a potential shift in market sentiment towards the upside, prompting the trader to exit their short position and manage their risk accordingly.

Features of the script

This Triple MA Strategy is basically the HTF Trend Filter displayed 3 times on the chart. For more infomation on how the MA with dynamic smoothing is calculated I recommend reading the following script:

For risk management I included a simple script to opt for % of eauity or # of contracts of in the instrument. For explanation on how the risk management settings work I refer to my ealier published script:

The strategy is a simplified example for setting up an entry and exit logic based on multiple moving avarages. Hence the script is meant for educational purposes only.

Three Candle Rolling Pivot Range**Strategy Description: Three Previous Candle Rolling Pivot Range**

**Introduction:**

This trading strategy is based on the concept of the rolling pivot range calculated from the high, low, and close prices of the three previous candles. The rolling pivot range serves as a dynamic support and resistance level, and this strategy aims to capture potential trading opportunities based on the price relationship with this range.

**Strategy Components:**

**1. Rolling Pivot Range Calculation:**

- **Rolling Pivot:** Calculate the rolling pivot by averaging the high, low, and close prices of the three previous candles.

- **Second Number:** Find the midpoint between the high and low of the three previous candles.

- **Pivot Differential:** Measure the difference between the rolling pivot and the second number.

- **Rolling Pivot Range High:** Set as rolling pivot + pivot differential.

- **Rolling Pivot Range Low:** Set as rolling pivot - pivot differential.

**2. Entry Rules:**

- **Long Entry:**

- Initiate a long entry when the current close is above both the rolling pivot range high and the rolling pivot.

- Continue the long entry as long as both the rolling pivot range high and low are higher than the corresponding values of the previous candle.

- **Short Entry:**

- Start a short entry when the current close is below both the rolling pivot range high and the rolling pivot.

- Continue the short entry as long as both the rolling pivot range high and low are lower than the corresponding values of the previous candle.

**Visualization:**

- **Plotting:**

- The rolling pivot range high, rolling pivot, and rolling pivot range low are plotted on the chart for visual reference.

- Long entry points are marked with a green triangle below the corresponding candle.

- Short entry points are marked with a red triangle above the corresponding candle.

**Conclusion:**

This strategy leverages the rolling pivot range to identify potential reversal points in the market. By considering the relative position of the current price compared to the dynamic support and resistance levels, the strategy aims to capture favorable trading opportunities. However, like all trading strategies, it should be used cautiously and backtested thoroughly on historical data to ensure its effectiveness before implementation in a live trading environment. Additionally, risk management techniques should always be applied to safeguard trading capital.

TradeTrackerLibrary "TradeTracker"

Simple Library for tracking trades

method track(this)

tracks trade when called on every bar

Namespace types: Trade

Parameters:

this (Trade) : Trade object

Returns: current Trade object

Trade

Has the constituents to track trades generated by any method.

Fields:

id (series int)

direction (series int) : Trade direction. Positive values for long and negative values for short trades

initialEntry (series float) : Initial entry price. This value will not change even if the entry is changed in the lifecycle of the trade

entry (series float) : Updated entry price. Allows variations to initial calculated entry. Useful in cases of trailing entry.

initialStop (series float) : Initial stop. Similar to initial entry, this is the first calculated stop for the lifecycle of trade.

stop (series float) : Trailing Stop. If there is no trailing, the value will be same as that of initial trade

targets (float ) : array of target values.

startBar (series int) : bar index of starting bar. Set by default when object is created. No need to alter this after that.

endBar (series int) : bar index of last bar in trade. Set by tracker on each execution

startTime (series int) : time of the start bar. Set by default when object is created. No need to alter this after that.

endTime (series int) : time of the ending bar. Updated by tracking method.

status (series int) : Integer parameter to track the status of the trade

retest (series bool) : Boolean parameter to notify if there was retest of the entry price

peterzorve-libraryLibrary "library"

is_bullish_engulfing()

is_bearish_engulfing()

is_hammer(fib_level)

Parameters:

fib_level (float)

is_shooting_star(fib_level)

Parameters:

fib_level (float)

is_hammer_and_star(fib_level)

Parameters:

fib_level (float)

is_star_and_hammer(fib_level)

Parameters:

fib_level (float)

is_dogi(dogi_body_ratio)

Parameters:

dogi_body_ratio (float)

is_bear_bear_bullish_engulf()

is_atr_stoploss_takeprofit(atr_multiplier, atr_length, reward_ratio)

Parameters:

atr_multiplier (float)

atr_length (simple int)

reward_ratio (float)

is_fixed_stoploss_takeprofit(stoploss_pips, reward_ratio)

Parameters:

stoploss_pips (float)

reward_ratio (float)

is_step_trailing_stoploss(stoploss_pips)

Parameters:

stoploss_pips (float)

is_atr_trailing_stoploss(atr_multiplier, break_even_pip)

Parameters:

atr_multiplier (float)

break_even_pip (int)

is_pull_back_strategy(length)

Parameters:

length (simple int)

is_trade_statistics(condition, entrypoint, stoploss, takeprofit)

Parameters:

condition (bool)

entrypoint (float)

stoploss (float)

takeprofit (float)

is_table_of_statistics(win_trades, lost_trades, even_trades, pips_won, pips_lost)

Parameters:

win_trades (int)

lost_trades (int)

even_trades (int)

pips_won (float)

pips_lost (float)

is_pine_info(lotsize, stoploss, takeprofit)

Parameters:

lotsize (float)

stoploss (float)

takeprofit (float)

is_support_and_resistance_strategy(look_back, look_forward)

Parameters:

look_back (int)

look_forward (int)

is_choral_strategy(smoothing_period, constant_d)

Parameters:

smoothing_period (int)

constant_d (float)

is_bollinger_band_strategy(length, dev_entry, dev_stoploss, dev_takeprofit)

Parameters:

length (int)

dev_entry (simple float)

dev_stoploss (simple float)

dev_takeprofit (simple float)

PlurexSignalCoreLibrary "PlurexSignalCore"

General purpose functions and helpers for use in more specific Plurex Signal alerting scripts and libraries

plurexMarket()

Build a Plurex market string from a base and quote asset symbol.

Returns: A market string that can be used in Plurex Signal messages.

tickerToPlurexMarket()

Builds Plurex market string from the syminfo

Returns: A market string that can be used in Plurex Signal messages.

simpleMessage(secret, action, marketOverride)

Builds Plurex Signal Message json to be sent to a Signal webhook

Parameters:

secret : The secret for your Signal on plurex

action : The action of the message. One of .

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

entryMessage(secret, isLong, budgetPercentage, priceLimit, marketOverride)

Builds Plurex Signal Entry Message json to be sent to a Signal webhook with optional parameters for budget and price limits.

Parameters:

secret : The secret for your Signal on plurex

isLong : The action of the message. true for LONG, false for SHORT.

budgetPercentage : Optional, The percentage of budget to use in the entry.

priceLimit : Optional, The worst price to accept for the entry.

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

long(secret, budgetPercentage, priceLimit, marketOverride)

Builds Plurex Signal LONG Message json to be sent to a Signal webhook with optional parameters for budget and price limits.

Parameters:

secret : The secret for your Signal on plurex

budgetPercentage : Optional, The percentage of budget to use in the entry.

priceLimit : Optional, The worst price to accept for the entry.

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

short(secret, budgetPercentage, priceLimit, marketOverride)

Builds Plurex Signal SHORT Message json to be sent to a Signal webhook with optional parameters for budget and price limits.

Parameters:

secret : The secret for your Signal on plurex

budgetPercentage : Optional, The percentage of budget to use in the entry.

priceLimit : Optional, The worst price to accept for the entry.

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeAll(secret, marketOverride)

Builds Plurex Signal CLOSE_ALL Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeShorts(secret, marketOverride)

Builds Plurex Signal CLOSE_SHORTS Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeLongs(secret, marketOverride)

Builds Plurex Signal CLOSE_LONGS Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeFirstLong(secret, marketOverride)

Builds Plurex Signal CLOSE_FIRST_LONG Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeLastLong(secret, marketOverride)

Builds Plurex Signal CLOSE_LAST_LONG Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeFirstShort(secret, marketOverride)

Builds Plurex Signal CLOSE_FIRST_SHORT Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

closeLastShort(secret, marketOverride)

Builds Plurex Signal CLOSE_LAST_SHORT Message json to be sent to a Signal webhook.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

SSL + Wave Trend StrategyStrategy incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Based on strategy conditions below

Trade exit:

Based on strategy conditions below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Alerting:

Alerts on LONG and SHORT trade entries

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: SSL Hybrid baseline is BLUE

C2: SSL Channel crosses up (green above red)

C3: Wave Trend crosses up (represented by pink candle body)

C4: Entry candle height is not greater than configured threshold

C5: Entry candle is inside Keltner Channel (wicks or body depending on configuration)

C6: Take Profit target does not touch EMA (represents resistance)

SHORT

C1: SSL Hybrid baseline is RED

C2: SSL Channel crosses down (red above green)

C3: Wave Trend crosses down (represented by orange candle body)

C4: Entry candle height is not greater than configured threshold

C5: Entry candle is inside Keltner Channel (wicks or body depending on configuration)

C6: Take Profit target does not touch EMA (represents support)

Trade exit:

Stop Loss: Size configurable with NNFX ATR multiplier

Take Profit: Calculated from Stop Loss using R:R ratio

Credits

Strategy is based on the YouTube video "This Unique Strategy Made 47% Profit in 2.5 Months " by TradeSmart.

It combines the following indicators to determine trade entry/exit conditions:

Wave Trend: Indicator: WaveTrend Oscillator by @LazyBear

SSL Channel: SSL channel by @ErwinBeckers

SSL Hybrid: SSL Hybrid by @Mihkel00

Keltner Channels: Keltner Channels Bands by @ceyhun

Candle Height: Candle Height in Percentage - Columns by @FreeReveller

NNFX ATR: NNFX ATR by @sueun123

[MT Trader] Backtest template w/ Supertrend Strategy---EN: In this strategy template you will find some functions already pre-programmed to be used in your strategies to speed up the programming process, among them we can highlight the default stop loss and take profit functions, which will help to set easily and quickly, defining the price range in which we want to prevent large losses or protect our profits from unexpected market movements.

🔴 Stop Loss: Among the functions of the stop loss are the 4 most known, first we have the fixed percentage range (%) and price ($), when the price reaches this fixed price will limit the losses of the operation avoiding larger losses, then we have the average true range (ATR), a moving average of true range and X period that can give us good reference points to place our stop loss, finally the last point higher or lower is the most used by traders to place their stop loss.

In addition, the price range between the entry and stop loss can be converted into a trailing stop loss.

🟢 Take Profit: We have 3 options for take profit, just like stop loss, the fixed range of percentage(%) and price($), are available, in addition to this we have the 1:# ratio option, which multiplies by X number the range between the entry and stop loss to use it as take profit, perfect for strategies that use ATR or last high/low point for their strategy.

📈 Heikin Ashi Entrys: The heikin ashi entries are trades that are calculated based on heikin ashi candles but their price is executed in Japanese candles, thus avoiding the false results that occur in heikin candlestick charts, making that in certain cases better results are obtained in the strategies that are executed with this option compared to Japanese candlesticks.

📊 Dashboard: A more visual and organized way to see the results and data needed for our strategy.

Feel free to use this template to program your own strategies, if you find bugs or want to request a new feature let me know in the comments or through my telegram @hvert_mt

__________________________________________________________________________________________________________________________________________________

---ES: En esta plantilla de estrategia podrás encontrar algunas funciones ya pre-programadas para ser usadas en tus estrategias para acelerar procesos de programación, entre ellas podemos destacar las funciones por defecto de stop loss y take profit, que ayudaran a establecer de manera fácil y rápida, definiendo los rango de precio en los que queremos prevenirnos de perdidas grandes o proteger nuestras ganancias de movimientos inesperados del mercado.

🔴 Stop Loss: Entre las funciones del stop loss están las 4 más conocidas, en primer lugar tenemos el rango de porcentaje fijo(%) y el precio($), cuando el precio alcance este precio fijo se limitaran las perdidas de la operación evitando perdidas mas grandes, después tenemos el promedio de rango verdadero(ATR), una media móvil del rango verdadero y X periodo que nos puede dar buenos puntos de referencia para colocar nuestro stop loss, por ultimo el ultimo punto mas alto o mas bajo es de los mas usados por los traders para colocar su stop loss.

Adicional a esto, el rango de precio entre la entrada y el stop loss se puede convertir en un trailing stop loss.

🟢 Take Profit: Tenemos 3 opciones para take profit, al igual que en el stop loss, el rango fijo de porcentaje(%) y precio($) se encuentran disponibles, adicional a esto tenemos la opción de ratio 1:#, que multiplica por X numero el rango entre la entrada y el stop loss para usarlo como take profit, perfecto para estrategias que usen ATR o ultimo punto alto/bajo.

📈 Entradas Heikin Ashi: Las entradas Heikin Ashi son trades que son calculados en base a las velas Aeikin Ashi pero su precio esta ejecutado a velas japonesas, evitando así los falsos resultados que se producen en graficas de velas Heikin, esto haciendo que en ciertos casos se obtengan mejores resultados en las estrategias que son ejecutadas con esta opción en comparación con las velas japonesas.

📊 Panel de Control: Una manera mas visual y organizada de ver los resultados y datos necesarios de nuestra estrategia.

Siéntete libre de usar esta plantilla para programar tus propias estrategias, si encuentras errores o quieres solicitar una nueva función házmelo saber en los comentarios o a través de mi Telegram: @hvert_mt

Rainbow Oscillator The Rainbow Oscillator is a technical indicator that shows prices in overbought or oversold areas. That allows you to catch the price reversal point.

---------------

FEATURES

---------------

.:: Dynamic levels ::.

The indicator levels are divided into several zones, which have a fibonacci ratio. Zones determine the overbought/oversold level. Blue and green level zones are better for buying, red and orange for selling. Dynamic levels are used as replacements for classic levels such as -100 and 100 for the CCI indicator or 30 and 70 for the RSI indicator. Dynamic levels work much better than static levels, as they are more adaptive to the current market situation.

.:: Composite oscillator (3 in 1) ::.

The main signal line of the indicator includes all three oscillators RSI, CCI, Stoch in different ratios. In the settings, you can change the proportions or completely remove one of the oscillators by setting its weight to 0

.:: CCI + RSI + Stoch ratio setting ::.

Each of the oscillators has its own weight in the calculation formula: w2 * cci ( + w1 * ( rsi - 50) + (1 - w2 - w1) * ( stoch - 50), this allows you to create the resulting oscillator from all indicators, depending on the weight of each of them. Each weight value must be between 0 and 1 so that the sum of all weights does not exceed 1.

.:: Smoothing levels and lines of the oscillator ::.

Smoothing the oscillator readings allows you to filter out the noise and get more accurate data. Level offset allows you to customize the support for inputs.

.:: Market Flat ::.

Dynamic creation of levels allows you to find in the price reversal zone, even when the price is in a flat

.:: Sources ::.

You can change the data source for the indicator to the number of longs and shorts for the selected asset. For example, BTCUSDLONGS / BTCUSDSHORTS is perfect for Bitcoin, then the oscillator will work on this data and will not use the quote price.

.:: Trend Detection ::.

The main line of the oscillator has 2 colors - green and red. Red means downtrend, green means uptrend. Trend reversal points are most often found in overbought and oversold zones.

.:: Alerts ::.

Alerts inside for next events: Buy (blue point) Sell (red point) and TrendReversal (change line color)

----------------

TRADING

—-------------

There are several possible entry points for the indicator, let's consider them all.

1) Trend reversal.

Long entry: The indicator line is in the green zone below 0 (oversold), while the line changes color from red (downward) to green (upward)

Short entry: The indicator line is in the red zone above the 0 (overbought) mark, while the line changes color from green to red.

2) Red and blue dots.

Long entry: Blue dot

Short Entry: Red Dot

I prefer to use the first trading method.

----------------

SETTINGS

----------------

.:: Trend Filter (checkbox) ::.

Use trend confirmation for red/blue dots. When enabled, the blue dot requires an uptrend, red dot requires downtrend confirmation before appearing.

.:: Use long/shorts (checkbox) ::.

Change formula to use longs and shorts positions as data source (instead of quote price)

.:: RSI weight / CCI weight / Stoch weight ::.

Weight control coefficients for RSI and CCI indicators, respectively. When you set RSI Weight = 0, equalize the combo of CCI and Stoch , when RSI Weight is zero and CCI Weight is equal to the oscillator value will be plotted

only from Stoch . Intermediate values have a high degree of measurement of each of the three oscillators in percentage terms from 0 to 100. The calculation uses the formula: w2 * cci ( + w1 * ( rsi - 50) + (1 - w2 - w1) * ( stoch - 50),

where w1 is RSI Weight and w2 is CCI Weight, Stoch weight is calculated on the fly as (1 - w2 - w1), so the sum of w1 + w2 should not exceed 1, in this case Stoch will work as opposed to CCI and RSI .

.:: Oscillograph fast and slow periods ::.

The fast period is the period for the moving average used to smooth CCI, RSI and Stoch. The slow period is the same. The fast period must always be less than the slow period.

.:: Oscillograph samples period::.

The period of smoothing the total values of indicators - creates a fast and slow main lines of the oscillator.

.:: Oscillograph samples count::.

How many times smoothing applied to source data.

.:: Oscillator samples type ::.

Smoothing line type e.g. EMA, SMA, RMA …

.:: Level period ::.

Periodically moving averages used to form the levels (zone) of the Rainbow Oscillator indicator

.:: Level offset ::.

Additional setting for shifting levels from zero points. Can be useful for absorbing levels and filtering input signals. The default is 0.

.:: Level redundant ::.

It characterizes the severity of the state at each iteration of the level of the disease. If set to 1 - the levels will not decrease when the oscillator values fall. If it has a value of 0.99 - the levels are reduced by 0.01

each has an oscillator in 1% of cases and is pressed to 0 by more aggressive ones.

.:: Level smooth samples ::.

setting allows you to set the number of strokes per level. Measuring the number of averages with the definition of the type of moving averages

.:: Level MA Type ::.

Type of moving average, average for the formation of a smoothing overbought and oversold zone

Trending Bar SRTrending Bar SR is a simple script define a Bar called "Trending Bar".

Depend on direction of Trending Bar, if Trending Bar is UpTrend then this indicator plot Bar's Low Price as Support and if Trending Bar is DownTrend then it plot Bar's High Price as Resistance.

Beside, this indicaor also plot 4 levels retracement of Trending Bar for trading.

1. Define Trending Bar

1.1 Uptrend Bar

+ Close Price higher than previous High Price

+ Body greater than sum of shadows (up and down)

+ Color: A green dot is plotted at bottom chart.

1.2 Downtrend Bar

+ Close Price lower than previous Low Price

+ Body greater than sum of shadows (up and down)

+ Color: A red dot is plotted at bottom chart.

2. Retracement Level

+ Trending Bar Retracement 0.5 is called Equerium.

+ Trending Bar Retracement 0.618 is called Perfect Entry.

+ Trending Bar Retracement 0.705 is called Optimal Entry.

+ Trending Bar Retracement 0.79 is called Max Entry.

3. Trading

+ When Price crossed Equerium, consider open position at Perfect Entry, Optimal Entry with stoploss place at Max Entry.

+ If place order at Max Entry, stoploss can place at Support or Resistance.

Double SupertrendThis strategy is based on a custom indicator that was created based on the Supertrend indicator. At its core, there are always 2 super trend indicators with different factors to reduce market noise (false signals).

The strategy/indicator has some parameters to improve the signals and filters.

TECHNICAL ANALYSIS

☑ Show Indicators

This option will enable/disable the Supertrend indicators on the chart.

☑ Length

The length will be used on the Supertrend Indicator to calculate its values.

☑ Dev Fast

The fast deviation or factor from one of the super trend indicators. This will be the leading indicator for entry signals, as well as for the exit signals.

☑ Dev Slow

The slow deviation or factor from one of the super trend indicators. This will be the confirmation indicator for entry and exit signals.

☑ Exit Type

It's possible to select from 4 options for the exit signals. Exit signals always take profit target.

☑ ⥹ Reversals

This option will make the strategy/indicator calculate the exit signals based on the difference between the given period's highest and lowest candle value (see Period on this list). It's displayed on the chart with the cross. As it's possible to verify in the image below, there are multiple exit spots for every entry.

☑ ⥹ ATR

Using ATR as a base indicator for exit signals will make the strategy/indicator place limit/stop orders. Candle High + ATR for longs, Candle Low - ATR for shorts. The strategy will show the ATR level for take profit and stick with it until the next signal. This way, the take profit value remains based on the candle of the entry signal.

☑ ⥹ Fast Supertrend

With this option selected, the exit signals will be based on the Fast Supertsignal value, mirrored to make a profit.

☑ ⥹ Slow Supertrend

With this option selected, the exit signals will be based on the Slow Supertsignal value, which is mirrored to take profit.

☑ Period

This will represent the number of candles used on the exit signals when Reversals is selected as Exit Type. It's also used to calculate the gradient used on the Fills and Supertrend signals.

☑ Multiplier

It's used on the take profit when the ATR option is selected on the Exit Type.

STRATEGY

☑ Use The Strategy

This will enable/disable the strategy to show the trades calculations.

☑ Show Use Long/Short Entries

Option to make the strategy show/use Long or Short signals. Available only if Use The Strategy is enabled

☑ Show Use Exit Long/Short

Option to make the strategy show/use Exit Long or Short signals (valid when Reversals option is selected on the Exit Type). Available only if Use The Strategy is enabled

☑ Show Use Add Long/Short

Option to make the strategy show/use Add Long or Short signals. With this option enabled, the strategy will place multiple trades in the same direction, almost the same concept as a pyramiding parameter. It's based on the Fast Supersignal when the candle fails to cross and reverses. Available only if Use The Strategy is enabled

☑ Trades Date Start/End

The date range that the strategy will check the market data and make the trades

HOW TO USE

It's very straightforward. A long signal will appear as a green arrow with a text Long below it. A short signal will appear as a red arrow with a text Short above it. It's ideal to wait for the candle to finish to validate the signal.

The exit signals are optional but give a good idea of the configuration used when backtesting. Each market and timeframe will have its own configuration for the best results. On average, sticking to ATR as an exit signal will have less risk than the other options.

☑ Entry Signals

Follow the arrows with Long/Short texts on them. Wait for the signal candle to close to validate the entry.

☑ Exit Signals

Use them to close your position or to trail stop your orders and maximize profits. Select the exit type suitable for each timeframe and market

☑ Add Entries

It's possible to increase the position following the add margin/contracts based on the Add signals. Not mandatory, but may work as reentries or late entries using the same signal.

☑ What about Stop Loss?

The stop-loss levels were not included as a separated signal because it's already in the chart. There are some possible ideas for the stop loss:

☑⥹ Candle High/Low (2nd recommend option)

When it's a Long signal from the entry signal candle, the stop loss can be the Low value of the same candle. Very tight stop loss in some cases, depending on the candle range

☑⥹ Local Top/Bottom

Selecting the local top/bottom as stop loss will give the strategy more room for false breakouts or reversals, keeping the trade open and minimizing noises. Increases the risk

☑⥹ Fast Supertrend (1st recommend option)

The fast supertrend can be used as stop-loss as well. making it a moving level and working close to trail stop management

☑⥹ Fixed Percentage

It's possible to use a fixed risk percentage for the trades, making the risk easier to control and project. Since the market volatility is not fixed, this may affect the accuracy of the trades

☑⥹ Based on the ATR (3rd recommend option)

When the exit type option ATR is selected, it will display the take profit level for that entry. Just mirror that value and put it as stop-loss, or multiply that amount by 1.5 to have more room for market noise.

EXAMPLE CONFIGURATIONS

Here are some configuration ideas for some markets (all of them are from crypto, especially futures markets)

BTCUSDT 15min - Default configuration

BTCUSDT 1h - Length 10 | Dev Fast 3 | Dev Slow 4 | Exit Type ATR | Period 50 | Multiplier 1

BTCUSDT 4h - Length 10 | Dev Fast 2 | Dev Slow 4 | Exit Type ATR | Period 50 | Multiplier 1

ETHUSDT 15min - Length 20 | Dev Fast 1 | Dev Slow 3 | Exit Type Fast Supertrend | Period 50 | Multiplier 1

IOTAUSDT 15min - Length 10 | Dev Fast 1 | Dev Slow 2 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

OMGUSDT 15min - Length 10 | Dev Fast 1 | Dev Slow 4 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

VETUSDT 15min - Length 10 | Dev Fast 3 | Dev Slow 4 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

HOW TO FIND OTHER CONFIGURATIONS

Here are some steps to find suitable configurations

select a market and time frame

enable the Use This Strategy option on the strategy

open the strategy tester panel and select the performance summary

open the strategy configuration and go to properties

change the balance to the same price of the symbol (example: BTCUSDT 60.000, use 60.000 as balance)

go back to the inputs tab and keep changing the parameters until you see the net profit be positive and bigger than the absolute value of the drawdown

in case you can't find a suitable configuration, try other timeframes

Since the tester reflects what happened in the past candles, it's not guaranteed to give the same results. However, this indicator/Strategy can be used with other indicators as a leading signal or confirmation signal.

Forex Scalping 1min Bollinger Bands, RSI and ADX Trading SystemThis is a Forex Scalping Trading Sytem based on the Bollinger Bands.

Its suited for major pairs, with lowest possible comission (below 1 pip) and with timeframes ranging between 1-15 min.

Indicators:

Bollinger bands

ADX

RSI

Rules for entry:

Long Entry: price to move below the upper Bollinger Bands RSI raise above the 30 line and ADX<32 at the same time.

Short Entry: price to move above the upper Bollinger Bands, RSI raise below the 70 line and ADX<32 at the same time.

Rules for exit

Profit Exit: 3 options: 1, exit position when the price touches the middle band, 2) when the price touches the opposite band, X pips target profit.

Loss Exit: X pips loss

Altered True Strength Indicator (TSI) Reupload-

Altered TSI provides a slightly more volatile signal that demonstrates extremities in price action with greater success than standard TSI. In addition, I added bull/bear cross indicators (green/red) to make it easier to notice the crosses to save time when the market is moving fast (I couldn't find a regular TSI script with this addition). Finally, the signal also has overextension parameters (red and green lines)

I think this is best used on Intraday time frames as the signals respond to volatility very well and using Heikin Ashi candles, trend is more visual. In this particular example, I am showing SPY on the 3m time chart (my favorite short time frame) and the signal alone provided many opportunities for trades when using simple divergences and countering overextension direction when short term (blue) signal crosses either

In the first example (purple lines), SPY ramps but it was a dull signal given the signal strength flatlining- we would be looking for a short entry. When the signal fires, it provides a clean $1.50 move down in spy.

In the second example (orange), the blue signal provides a nice V shape (rebound signal) in which we are looking for a long entry. 390.50 is a strong SPY support in confluence with 2nd std dev VWAP extension, but disregarding that bull signal fires resulting in a 2 dollar move upwards. Exit is provided when blue line crosses green overextension.

In the third example (white), we are searching for a short entry at 392.5 resistance in confluence with divergently higher highs. Bear cross signal when fired and a significant cross is visible provides a $2.50 move to the downside with a potential exit provided when blue line crosses red overextension line in confluence with previous LOD area.

In the fourth example (green), we watch as the blue line provides a V pattern, we are searching for a long entry. If you didn't take a riskier long at 2nd std dev VWAP overextension with V recovery on blue line at red overextension for a ride to vwap, then you are looking for a secondary entry long as you wouldn't take the trade at resistance (vwap). Bullishly divergent lows provide this entry and the signal does not bear cross at all (but looking for significant crosses is more important even if the signal were to make a minor bear cross). Bullishly divergent double bottom provides a long entry to end of day with a nice clean signal for a $5.00 move until eod or when signal crosses overextension range.

Ideally, close to the money options or SPY/SPXS/SPXL are best used in the intraday time frame.

Again, this is not a standalone indicator but it's best used in conjunction with other indicators/trading strategies

Any questions feel free to comment

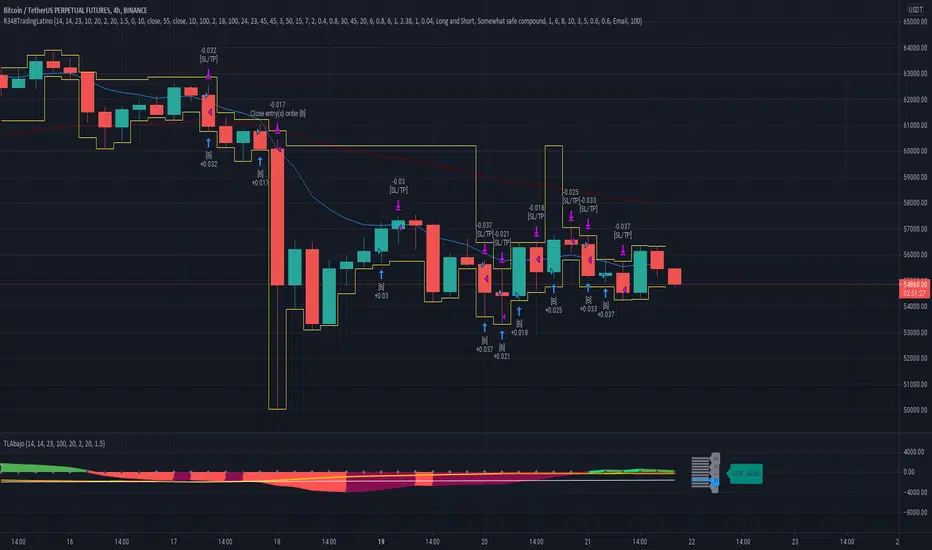

Ruckard TradingLatinoThis strategy tries to mimic TradingLatino strategy.

The current implementation is beta.

Si hablas castellano o espanyol por favor consulta MENSAJE EN CASTELLANO más abajo.

It's aimed at BTCUSDT pair and 4h timeframe.

STRATEGY DEFAULT SETTINGS EXPLANATION

max_bars_back=5000 : This is a random number of bars so that the strategy test lasts for one or two years

calc_on_order_fills=false : To wait for the 4h closing is too much. Try to check if it's worth entering a position after closing one. I finally decided not to recheck if it's worth entering after an order is closed. So it is false.

calc_on_every_tick=false

pyramiding=0 : We only want one entry allowed in the same direction. And we don't want the order to scale by error.

initial_capital=1000 : These are 1000 USDT. By using 1% maximum loss per trade and 7% as a default stop loss by using 1000 USDT at 12000 USDT per BTC price you would entry with around 142 USDT which are converted into: 0.010 BTC . The maximum number of decimal for contracts on this BTCUSDT market is 3 decimals. E.g. the minimum might be: 0.001 BTC . So, this minimal 1000 amount ensures us not to entry with less than 0.001 entries which might have happened when using 100 USDT as an initial capital.

slippage=1 : Binance BTCUSDT mintick is: 0.01. Binance slippage: 0.1 % (Let's assume). TV has an integer slippage. It does not have a percentage based slippage. If we assume a 1000 initial capital, the recommended equity is 142 which at 11996 USDT per BTC price means: 0.011 BTC. The 0.1% slippage of: 0.011 BTC would be: 0.000011 . This is way smaller than the mintick. So our slippage is going to be 1. E.g. 1 (slippage) * 0.01 (mintick)

commission_type=strategy.commission.percent and commission_value=0.1 : According to: binance . com / en / fee / schedule in VIP 0 level both maker and taker fees are: 0.1 %.

BACKGROUND

Jaime Merino is a well known Youtuber focused on crypto trading

His channel TradingLatino

features monday to friday videos where he explains his strategy.

JAIME MERINO STANCE ON BOTS

Jaime Merino stance on bots (taken from memory out of a 2020 June video from him):

'~

You know. They can program you a bot and it might work.

But, there are some special situations that the bot would not be able to handle.

And, I, as a human, I would handle it. And the bot wouldn't do it.

~'

My long term target with this strategy script is add as many

special situations as I can to the script

so that it can match Jaime Merino behaviour even in non normal circumstances.

My alternate target is learn Pine script

and enjoy programming with it.

WARNING

This script might be bigger than other TradingView scripts.

However, please, do not be confused because the current status is beta.

This script has not been tested with real money.

This is NOT an official strategy from Jaime Merino.

This is NOT an official strategy from TradingLatino . net .

HOW IT WORKS

It basically uses ADX slope and LazyBear's Squeeze Momentum Indicator

to make its buy and sell decisions.

Fast paced EMA being bigger than slow paced EMA

(on higher timeframe) advices going long.

Fast paced EMA being smaller than slow paced EMA

(on higher timeframe) advices going short.

It finally add many substrats that TradingLatino uses.

SETTINGS

__ SETTINGS - Basics

____ SETTINGS - Basics - ADX

(ADX) Smoothing {14}

(ADX) DI Length {14}

(ADX) key level {23}

____ SETTINGS - Basics - LazyBear Squeeze Momentum

(SQZMOM) BB Length {20}

(SQZMOM) BB MultFactor {2.0}

(SQZMOM) KC Length {20}

(SQZMOM) KC MultFactor {1.5}

(SQZMOM) Use TrueRange (KC) {True}

____ SETTINGS - Basics - EMAs

(EMAS) EMA10 - Length {10}

(EMAS) EMA10 - Source {close}

(EMAS) EMA55 - Length {55}

(EMAS) EMA55 - Source {close}

____ SETTINGS - Volume Profile

Lowest and highest VPoC from last three days

is used to know if an entry has a support

VPVR of last 100 4h bars

is also taken into account

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC

(VP) Show tick difference from current price {False}: BETA . Might be useful for actions some day.

(VP) Number of bars {100}: If 'Use number of bars (not VP timeframe)' is turned on this setting is used to calculate session VPoC.

(VP) Volume Profile timeframe {1 day}: If 'Use number of bars (not VP timeframe)' is turned off this setting is used to calculate session VPoC.

(VP) Row width multiplier {0.6}: Adjust how the extra Volume Profile bars are shown in the chart.

(VP) Resistances prices number of decimal digits : Round Volume Profile bars label numbers so that they don't have so many decimals.

(VP) Number of bars for bottom VPOC {18}: 18 bars equals 3 days in suggested timeframe of 4 hours. It's used to calculate lowest session VPoC from previous three days. It's also used as a top VPOC for sells.

(VP) Ignore VPOC bottom advice on long {False}: If turned on it ignores bottom VPOC (or top VPOC on sells) when evaluating if a buy entry is worth it.

(VP) Number of bars for VPVR VPOC {100}: Number of bars to calculate the VPVR VPoC. We use 100 as Jaime once used. When the price bounces back to the EMA55 it might just bounce to this VPVR VPoC if its price it's lower than the EMA55 (Sells have inverse algorithm).

____ SETTINGS - ADX Slope

ADX Slope

help us to understand if ADX

has a positive slope, negative slope

or it is rather still.

(ADXSLOPE) ADX cut {23}: If ADX value is greater than this cut (23) then ADX has strength

(ADXSLOPE) ADX minimum steepness entry {45}: ADX slope needs to be 45 degrees to be considered as a positive one.

(ADXSLOPE) ADX minimum steepness exit {45}: ADX slope needs to be -45 degrees to be considered as a negative one.

(ADXSLOPE) ADX steepness periods {3}: In order to avoid false detection the slope is calculated along 3 periods.

____ SETTINGS - Next to EMA55

(NEXTEMA55) EMA10 to EMA55 bounce back percentage {80}: EMA10 might bounce back to EMA55 or maybe to 80% of its complete way to EMA55

(NEXTEMA55) Next to EMA55 percentage {15}: How much next to the EMA55 you need to be to consider it's going to bounce back upwards again.

____ SETTINGS - Stop Loss and Take Profit

You can set a default stop loss or a default take profit.

(STOPTAKE) Stop Loss % {7.0}

(STOPTAKE) Take Profit % {2.0}

____ SETTINGS - Trailing Take Profit

You can customize the default trailing take profit values

(TRAILING) Trailing Take Profit (%) {1.0}: Trailing take profit offset in percentage

(TRAILING) Trailing Take Profit Trigger (%) {2.0}: When 2.0% of benefit is reached then activate the trailing take profit.

____ SETTINGS - MAIN TURN ON/OFF OPTIONS

(EMAS) Ignore advice based on emas {false}.

(EMAS) Ignore advice based on emas (On closing long signal) {False}: Ignore advice based on emas but only when deciding to close a buy entry.

(SQZMOM) Ignore advice based on SQZMOM {false}: Ignores advice based on SQZMOM indicator.

(ADXSLOPE) Ignore advice based on ADX positive slope {false}

(ADXSLOPE) Ignore advice based on ADX cut (23) {true}

(STOPTAKE) Take Profit? {false}: Enables simple Take Profit.

(STOPTAKE) Stop Loss? {True}: Enables simple Stop Loss.

(TRAILING) Enable Trailing Take Profit (%) {True}: Enables Trailing Take Profit.

____ SETTINGS - Strategy mode

(STRAT) Type Strategy: 'Long and Short', 'Long Only' or 'Short Only'. Default: 'Long and Short'.

____ SETTINGS - Risk Management

(RISKM) Risk Management Type: 'Safe', 'Somewhat safe compound' or 'Unsafe compound'. ' Safe ': Calculations are always done with the initial capital (1000) in mind. The maximum losses per trade/day/week/month are taken into account. ' Somewhat safe compound ': Calculations are done with initial capital (1000) or a higher capital if it increases. The maximum losses per trade/day/week/month are taken into account. ' Unsafe compound ': In each order all the current capital is gambled and only the default stop loss per order is taken into account. That means that the maximum losses per trade/day/week/month are not taken into account. Default : 'Somewhat safe compound'.

(RISKM) Maximum loss per trade % {1.0}.

(RISKM) Maximum loss per day % {6.0}.

(RISKM) Maximum loss per week % {8.0}.

(RISKM) Maximum loss per month % {10.0}.

____ SETTINGS - Decimals

(DECIMAL) Maximum number of decimal for contracts {3}: How small (3 decimals means 0.001) an entry position might be in your exchange.

EXTRA 1 - PRICE IS IN RANGE indicator

(PRANGE) Print price is in range {False}: Enable a bottom label that indicates if the price is in range or not.

(PRANGE) Price range periods {5}: How many previous periods are used to calculate the medians

(PRANGE) Price range maximum desviation (%) {0.6} ( > 0 ): Maximum positive desviation for range detection

(PRANGE) Price range minimum desviation (%) {0.6} ( > 0 ): Mininum negative desviation for range detection

EXTRA 2 - SQUEEZE MOMENTUM Desviation indicator

(SQZDIVER) Show degrees {False}: Show degrees of each Squeeze Momentum Divergence lines to the x-axis.

(SQZDIVER) Show desviation labels {False}: Whether to show or not desviation labels for the Squeeze Momentum Divergences.

(SQZDIVER) Show desviation lines {False}: Whether to show or not desviation lines for the Squeeze Momentum Divergences.

EXTRA 3 - VOLUME PROFILE indicator

WARNING: This indicator works not on current bar but on previous bar. So in the worst case it might be VP from 4 hours ago. Don't worry, inside the strategy calculus the correct values are used. It's just that I cannot show the most recent one in the chart.

(VP) Print recent profile {False}: Show Volume Profile indicator

(VP) Avoid label price overlaps {False}: Avoid label prices to overlap on the chart.

EXTRA 4 - ZIGNALY SUPPORT

(ZIG) Zignaly Alert Type {Email}: 'Email', 'Webhook'. ' Email ': Prepare alert_message variable content to be compatible with zignaly expected email content format. ' Webhook ': Prepare alert_message variable content to be compatible with zignaly expected json content format.

EXTRA 5 - DEBUG

(DEBUG) Enable debug on order comments {False}: If set to true it prepares the order message to match the alert_message variable. It makes easier to debug what would have been sent by email or webhook on each of the times an order is triggered.

HOW TO USE THIS STRATEGY