VolatilityIndicatorsLibrary "VolatilityIndicators"

This is a library of Volatility Indicators .

It aims to facilitate the grouping of this category of indicators, and also offer the customized supply of

the parameters and sources, not being restricted to just the closing price.

@Thanks and credits:

1. Dynamic Zones: Leo Zamansky, Ph.D., and David Stendahl

2. Deviation: Karl Pearson (code by TradingView)

3. Variance: Ronald Fisher (code by TradingView)

4. Z-score: Veronique Valcu (code by HPotter)

5. Standard deviation: Ronald Fisher (code by TradingView)

6. ATR (Average True Range): J. Welles Wilder (code by TradingView)

7. ATRP (Average True Range Percent): millerrh

8. Historical Volatility: HPotter

9. Min-Max Scale Normalization: gorx1

10. Mean Normalization: gorx1

11. Standardization: gorx1

12. Scaling to unit length: gorx1

13. LS Volatility Index: Alexandre Wolwacz (Stormer), Fabrício Lorenz, Fábio Figueiredo (Vlad) (code by me)

14. Bollinger Bands: John Bollinger (code by TradingView)

15. Bollinger Bands %: John Bollinger (code by TradingView)

16. Bollinger Bands Width: John Bollinger (code by TradingView)

dev(source, length, anotherSource)

Deviation. Measure the difference between a source in relation to another source

Parameters:

source (float)

length (simple int) : (int) Sequential period to calculate the deviation

anotherSource (float) : (float) Source to compare

Returns: (float) Bollinger Bands Width

variance(src, mean, length, biased, degreesOfFreedom)

Variance. A statistical measurement of the spread between numbers in a data set. More specifically,

variance measures how far each number in the set is from the mean (average), and thus from every other number in the set.

Variance is often depicted by this symbol: σ2. It is used by both analysts and traders to determine volatility and market security.

Parameters:

src (float) : (float) Source to calculate variance

mean (float) : (float) Mean (Moving average)

length (simple int) : (int) The sequential period to calcule the variance (number of values in data set)

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length. Only applies when biased parameter is defined as true.

Returns: (float) Standard deviation

stDev(src, length, mean, biased, degreesOfFreedom)

Measure the Standard deviation from a source in relation to it's moving average.

In this implementation, you pass the average as a parameter, allowing a more personalized calculation.

Parameters:

src (float) : (float) Source to calculate standard deviation

length (simple int) : (int) The sequential period to calcule the standard deviation

mean (float) : (float) Moving average.

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Standard deviation

zscore(src, mean, length, biased, degreesOfFreedom)

Z-Score. A z-score is a statistical measurement that indicates how many standard deviations a data point is from

the mean of a data set. It is also known as a standard score. The formula for calculating a z-score is (x - μ) / σ,

where x is the individual data point, μ is the mean of the data set, and σ is the standard deviation of the data set.

Z-scores are useful in identifying outliers or extreme values in a data set. A positive z-score indicates that the

data point is above the mean, while a negative z-score indicates that the data point is below the mean. A z-score of

0 indicates that the data point is equal to the mean.

Z-scores are often used in hypothesis testing and determining confidence intervals. They can also be used to compare

data sets with different units or scales, as the z-score standardizes the data. Overall, z-scores provide a way to

measure the relative position of a data point in a data

Parameters:

src (float) : (float) Source to calculate z-score

mean (float) : (float) Moving average.

length (simple int) : (int) The sequential period to calcule the standard deviation

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Z-score

atr(source, length)

ATR: Average True Range. Customized version with source parameter.

Parameters:

source (float) : (float) Source

length (simple int) : (int) Length (number of bars back)

Returns: (float) ATR

atrp(length, sourceP)

ATRP (Average True Range Percent)

Parameters:

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

atrp(source, length, sourceP)

ATRP (Average True Range Percent). Customized version with source parameter.

Parameters:

source (float) : (float) Source for ATR

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

historicalVolatility(lengthATR, lengthHist)

Historical Volatility

Parameters:

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

historicalVolatility(source, lengthATR, lengthHist)

Historical Volatility

Parameters:

source (float) : (float) Source for ATR

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

minMaxNormalization(src, numbars)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

minMaxNormalization(src, numbars, minimumLimit, maximumLimit)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

In this implementation, the user explicitly provides the desired minimum (min) and maximum (max) values for the scale,

rather than using the minimum and maximum values from the data.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

minimumLimit (simple float) : (float) Minimum value to scale

maximumLimit (simple float) : (float) Maximum value to scale

Returns: (float) Normalized value

meanNormalization(src, numbars, mean)

Mean Normalization

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

mean (float) : (float) Mean of source

Returns: (float) Normalized value

standardization(src, mean, stDev)

Standardization (Z-score Normalization). How "outside the mean" values relate to the standard deviation (ratio between first and second)

Parameters:

src (float) : (float) Source to normalize

mean (float) : (float) Mean of source

stDev (float) : (float) Standard Deviation

Returns: (float) Normalized value

scalingToUnitLength(src, numbars)

Scaling to unit length

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

lsVolatilityIndex(movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int) : (float) Length for normalization

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

lsVolatilityIndex(sourcePrice, movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

sourcePrice (float) : (float) Source for measure the distance

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int)

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

bollingerBands(src, length, mult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) A tuple of Bollinger Bands, where index 1=basis; 2=basis+dev; 3=basis-dev; and dev=multiplier*stdev

bollingerBands(src, length, aMult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Also, various multipliers can be passed, thus getting more bands (instead of just 2).

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) An array of multiplies used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands, where:

index 1=basis; 2=basis+dev1; 3=basis-dev1; 4=basis+dev2, 5=basis-dev2, 6=basis+dev2, 7=basis-dev2, Nup=basis+devN, Nlow=basis-devN

and dev1, dev2, devN are ```multiplier N * stdev```

bollingerBandsB(src, length, mult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation:

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands %B

bollingerBandsB(src, length, aMult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands %B. The number of results in this array is equal the numbers of multipliers passed via parameter.

bollingerBandsW(src, length, mult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation:

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands Width

bollingerBandsW(src, length, aMult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands Width. The number of results in this array is equal the numbers of multipliers passed via parameter.

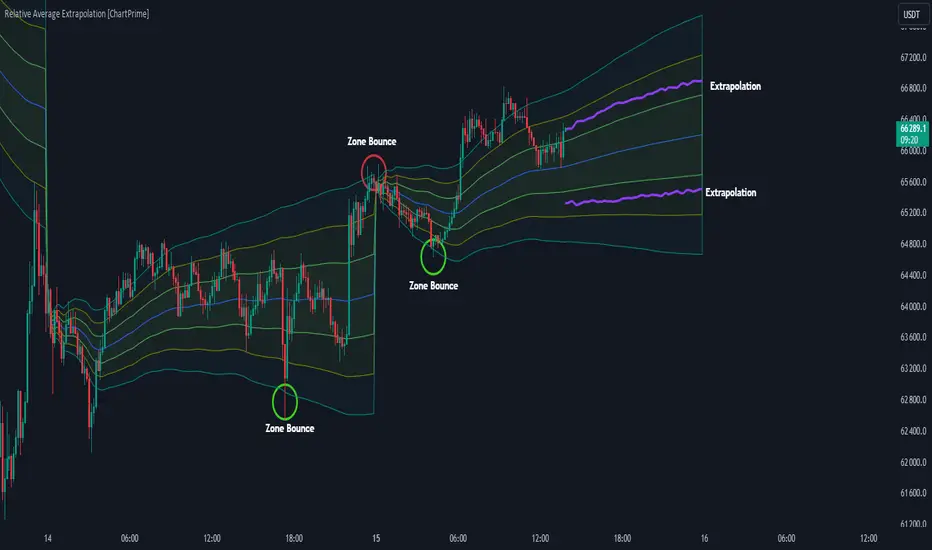

dinamicZone(source, sampleLength, pcntAbove, pcntBelow)

Get Dynamic Zones

Parameters:

source (float) : (float) Source

sampleLength (simple int) : (int) Sample Length

pcntAbove (simple float) : (float) Calculates the top of the dynamic zone, considering that the maximum values are above x% of the sample

pcntBelow (simple float) : (float) Calculates the bottom of the dynamic zone, considering that the minimum values are below x% of the sample

Returns: A tuple with 3 series of values: (1) Upper Line of Dynamic Zone;

(2) Lower Line of Dynamic Zone; (3) Center of Dynamic Zone (x = 50%)

Examples:

ابحث في النصوص البرمجية عن "index"

Simple Moving Average Extrapolation via Monte Carlo (SMAE)In this post, I will dive into my Moving Average Extrapolator, a tool that I created to help traders predict future price movements based on past data. I will discuss the underlying logic, its limitations, and the importance of accounting for delays in the moving average. The following code, my Moving Average Extrapolator, will serve as the basis for our discussion.

The Moving Average Extrapolator uses a simple moving average (SMA) to analyze past price movements and make predictions about future price movements. It uses a Monte Carlo simulation to generate possible future price movements based on historical probabilities.

Let's start by understanding the different components of the code:

The movement_probability function calculates the probability of green and red price movements, where green movements indicate an increase in price, and red movements indicate a decrease in price.

The monte function generates an array of potential price movements using a Monte Carlo simulation.

The sim function uses the generated Monte Carlo array to simulate potential future price movements based on the probabilities calculated earlier.

The draw_lines function draws lines connecting the current price to the extrapolated future price movements.

The extrapolate function calculates the extrapolated future price movements based on the provided source, length, and accuracy.

Limitations of My Moving Average Extrapolator:

Reliance on historical data: My Moving Average Extrapolator relies heavily on historical data to make future price predictions. This can be a limitation, as past performance does not guarantee future results. Market conditions can change, making the extrapolator less reliable in predicting future price movements.

Inherent randomness: The Monte Carlo simulation introduces an element of randomness in the extrapolator's predictions. While this can help in exploring various scenarios, it may not always accurately predict future price movements.

Delay in the moving average: Moving averages inherently have a delay, as they are based on past data. This delay can cause my Moving Average Extrapolator to be less accurate in predicting immediate price movements.

Accounting for Delays in the Moving Average:

It is essential to account for the delay in the moving average to improve the accuracy of my Moving Average Extrapolator. I have taken this into account by introducing a delay variable (delay) in the draw_lines function. The delay variable calculates the delay as half the moving average's length and adjusts the time axis accordingly.

This adjustment helps in reducing the lag in the extrapolator's predictions, making it more accurate and useful for traders. However, it is important to note that even with this adjustment, my Moving Average Extrapolator is still subject to the limitations discussed earlier.

Adding Custom Lookback Period to My Moving Average Extrapolator:

To enhance the functionality and adaptability of my Moving Average Extrapolator, I have implemented an option to set a custom lookback period. The lookback period determines how far back in the historical data the Moving Average Extrapolator should start its analysis.

To achieve this, I have included a method to obtain the current bar index and then calculate the starting bar index by subtracting the desired lookback period.

Here's how to implement the custom lookback period in the Moving Average Extrapolator:

Get the current bar index: I use the bar_index built-in variable to get the current bar index, which represents the current position in the historical data.

Set the start index: To set the start index, you can subtract the desired lookback period from the current bar index. In the code, I have defined a user-input number variable, which can be set to the desired lookback period. By default, it is set to 20800. The starting index for the Moving Average Extrapolator's analysis is calculated as bar_index - number.

Here's the relevant code snippet:

number = input.int(20800, "Bar Start")

And to conditionally run the calculations:

if bar_index > number

draw_lines(avg, extrapolate(close, length, 10), length, extrapolate)

By implementing this custom lookback period, users can easily adjust the starting point of the Moving Average Extrapolator based on their preferences and trading strategies. This allows for more flexibility and adaptability to different market scenarios and ensures that the Moving Average Extrapolator remains a valuable tool for traders.

Conclusion:

My Moving Average Extrapolator can be a valuable tool for traders looking to predict future price movements based on historical data. However, it is essential to understand its limitations and the need to account for the delay in the moving average. By considering these factors, traders can make better-informed decisions and use my Moving Average Extrapolator to complement their trading strategies effectively.

loxxfftLibrary "loxxfft"

This code is a library for performing Fast Fourier Transform (FFT) operations. FFT is an algorithm that can quickly compute the discrete Fourier transform (DFT) of a sequence. The library includes functions for performing FFTs on both real and complex data. It also includes functions for fast correlation and convolution, which are operations that can be performed efficiently using FFTs. Additionally, the library includes functions for fast sine and cosine transforms.

Reference:

www.alglib.net

fastfouriertransform(a, nn, inversefft)

Returns Fast Fourier Transform

Parameters:

a (float ) : float , An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

nn (int) : int, The number of function values. It must be a power of two, but the algorithm does not validate this.

inversefft (bool) : bool, A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

Returns: float , Modifies the input array a in-place, which means that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution. The transformed data will have real and imaginary parts interleaved, with the real parts at even indices and the imaginary parts at odd indices.

realfastfouriertransform(a, tnn, inversefft)

Returns Real Fast Fourier Transform

Parameters:

a (float ) : float , A float array containing the real-valued function samples.

tnn (int) : int, The number of function values (must be a power of 2, but the algorithm does not validate this condition).

inversefft (bool) : bool, A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

Returns: float , Modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

fastsinetransform(a, tnn, inversefst)

Returns Fast Discrete Sine Conversion

Parameters:

a (float ) : float , An array of real numbers representing the function values.

tnn (int) : int, Number of function values (must be a power of two, but the code doesn't validate this).

inversefst (bool) : bool, A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

Returns: float , The output is the transformed array 'a', which will contain the result of the transformation.

fastcosinetransform(a, tnn, inversefct)

Returns Fast Discrete Cosine Transform

Parameters:

a (float ) : float , This is a floating-point array representing the sequence of values (time-domain) that you want to transform. The function will perform the Fast Cosine Transform (FCT) or the inverse FCT on this input array, depending on the value of the inversefct parameter. The transformed result will also be stored in this same array, which means the function modifies the input array in-place.

tnn (int) : int, This is an integer value representing the number of data points in the input array a. It is used to determine the size of the input array and control the loops in the algorithm. Note that the size of the input array should be a power of 2 for the Fast Cosine Transform algorithm to work correctly.

inversefct (bool) : bool, This is a boolean value that controls whether the function performs the regular Fast Cosine Transform or the inverse FCT. If inversefct is set to true, the function will perform the inverse FCT, and if set to false, the regular FCT will be performed. The inverse FCT can be used to transform data back into its original form (time-domain) after the regular FCT has been applied.

Returns: float , The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

fastconvolution(signal, signallen, response, negativelen, positivelen)

Convolution using FFT

Parameters:

signal (float ) : float , This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

response (float ) : float , This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

negativelen (int) : int, This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

positivelen (int) : int, This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

Returns: float , The resulting convolved values are stored back in the input signal array.

fastcorrelation(signal, signallen, pattern, patternlen)

Returns Correlation using FFT

Parameters:

signal (float ) : float ,This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array.

pattern (float ) : float , This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

patternlen (int) : int, This is an integer representing the length of the pattern array.

Returns: float , The signal array containing the correlation values at points from 0 to SignalLen-1.

tworealffts(a1, a2, a, b, tn)

Returns Fast Fourier Transform of Two Real Functions

Parameters:

a1 (float ) : float , An array of real numbers, representing the values of the first function.

a2 (float ) : float , An array of real numbers, representing the values of the second function.

a (float ) : float , An output array to store the Fourier transform of the first function.

b (float ) : float , An output array to store the Fourier transform of the second function.

tn (int) : float , An integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

Returns: float , The a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Detailed explaination of each function

Fast Fourier Transform

The fastfouriertransform() function takes three input parameters:

1. a: An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

2. nn: The number of function values. It must be a power of two, but the algorithm does not validate this.

3. inversefft: A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

The function performs the FFT using the Cooley-Tukey algorithm, which is an efficient algorithm for computing the discrete Fourier transform (DFT) and its inverse. The Cooley-Tukey algorithm recursively breaks down the DFT of a sequence into smaller DFTs of subsequences, leading to a significant reduction in computational complexity. The algorithm's time complexity is O(n log n), where n is the number of samples.

The fastfouriertransform() function first initializes variables and determines the direction of the transformation based on the inversefft parameter. If inversefft is True, the isign variable is set to -1; otherwise, it is set to 1.

Next, the function performs the bit-reversal operation. This is a necessary step before calculating the FFT, as it rearranges the input data in a specific order required by the Cooley-Tukey algorithm. The bit-reversal is performed using a loop that iterates through the nn samples, swapping the data elements according to their bit-reversed index.

After the bit-reversal operation, the function iteratively computes the FFT using the Cooley-Tukey algorithm. It performs calculations in a loop that goes through different stages, doubling the size of the sub-FFT at each stage. Within each stage, the Cooley-Tukey algorithm calculates the butterfly operations, which are mathematical operations that combine the results of smaller DFTs into the final DFT. The butterfly operations involve complex number multiplication and addition, updating the input array a with the computed values.

The loop also calculates the twiddle factors, which are complex exponential factors used in the butterfly operations. The twiddle factors are calculated using trigonometric functions, such as sine and cosine, based on the angle theta. The variables wpr, wpi, wr, and wi are used to store intermediate values of the twiddle factors, which are updated in each iteration of the loop.

Finally, if the inversefft parameter is True, the function divides the result by the number of samples nn to obtain the correct inverse FFT result. This normalization step is performed using a loop that iterates through the array a and divides each element by nn.

In summary, the fastfouriertransform() function is an implementation of the Cooley-Tukey FFT algorithm, which is an efficient algorithm for computing the DFT and its inverse. This FFT library can be used for a variety of applications, such as signal processing, image processing, audio processing, and more.

Feal Fast Fourier Transform

The realfastfouriertransform() function performs a fast Fourier transform (FFT) specifically for real-valued functions. The FFT is an efficient algorithm used to compute the discrete Fourier transform (DFT) and its inverse, which are fundamental tools in signal processing, image processing, and other related fields.

This function takes three input parameters:

1. a - A float array containing the real-valued function samples.

2. tnn - The number of function values (must be a power of 2, but the algorithm does not validate this condition).

3. inversefft - A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

The function modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

The algorithm uses a combination of complex-to-complex FFT and additional transformations specific to real-valued data to optimize the computation. It takes into account the symmetry properties of the real-valued input data to reduce the computational complexity.

Here's a detailed walkthrough of the algorithm:

1. Depending on the inversefft flag, the initial values for ttheta, c1, and c2 are determined. These values are used for the initial data preprocessing and post-processing steps specific to the real-valued FFT.

2. The preprocessing step computes the initial real and imaginary parts of the data using a combination of sine and cosine terms with the input data. This step effectively converts the real-valued input data into complex-valued data suitable for the complex-to-complex FFT.

3. The complex-to-complex FFT is then performed on the preprocessed complex data. This involves bit-reversal reordering, followed by the Cooley-Tukey radix-2 decimation-in-time algorithm. This part of the code is similar to the fastfouriertransform() function you provided earlier.

4. After the complex-to-complex FFT, a post-processing step is performed to obtain the final real-valued output data. This involves updating the real and imaginary parts of the transformed data using sine and cosine terms, as well as the values c1 and c2.

5. Finally, if the inversefft flag is True, the output data is divided by the number of samples (nn) to obtain the inverse DFT.

The function does not return a value explicitly. Instead, the transformed data is stored in the input array a. After the function execution, you can access the transformed data in the a array, which will have the real part at even indices and the imaginary part at odd indices.

Fast Sine Transform

This code defines a function called fastsinetransform that performs a Fast Discrete Sine Transform (FST) on an array of real numbers. The function takes three input parameters:

1. a (float array): An array of real numbers representing the function values.

2. tnn (int): Number of function values (must be a power of two, but the code doesn't validate this).

3. inversefst (bool): A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

The output is the transformed array 'a', which will contain the result of the transformation.

The code starts by initializing several variables, including trigonometric constants for the sine transform. It then sets the first value of the array 'a' to 0 and calculates the initial values of 'y1' and 'y2', which are used to update the input array 'a' in the following loop.

The first loop (with index 'jx') iterates from 2 to (tm + 1), where 'tm' is half of the number of input samples 'tnn'. This loop is responsible for calculating the initial sine transform of the input data.

The second loop (with index 'ii') is a bit-reversal loop. It reorders the elements in the array 'a' based on the bit-reversed indices of the original order.

The third loop (with index 'ii') iterates while 'n' is greater than 'mmax', which starts at 2 and doubles each iteration. This loop performs the actual Fast Discrete Sine Transform. It calculates the sine transform using the Danielson-Lanczos lemma, which is a divide-and-conquer strategy for calculating Discrete Fourier Transforms (DFTs) efficiently.

The fourth loop (with index 'ix') is responsible for the final phase adjustments needed for the sine transform, updating the array 'a' accordingly.

The fifth loop (with index 'jj') updates the array 'a' one more time by dividing each element by 2 and calculating the sum of the even-indexed elements.

Finally, if the 'inversefst' flag is True, the code scales the transformed data by a factor of 2/tnn to get the inverse Fast Sine Transform.

In summary, the code performs a Fast Discrete Sine Transform on an input array of real numbers, either in the direct or inverse direction, and returns the transformed array. The algorithm is based on the Danielson-Lanczos lemma and uses a divide-and-conquer strategy for efficient computation.

Fast Cosine Transform

This code defines a function called fastcosinetransform that takes three parameters: a floating-point array a, an integer tnn, and a boolean inversefct. The function calculates the Fast Cosine Transform (FCT) or the inverse FCT of the input array, depending on the value of the inversefct parameter.

The Fast Cosine Transform is an algorithm that converts a sequence of values (time-domain) into a frequency domain representation. It is closely related to the Fast Fourier Transform (FFT) and can be used in various applications, such as signal processing and image compression.

Here's a detailed explanation of the code:

1. The function starts by initializing a number of variables, including counters, intermediate values, and constants.

2. The initial steps of the algorithm are performed. This includes calculating some trigonometric values and updating the input array a with the help of intermediate variables.

3. The code then enters a loop (from jx = 2 to tnn / 2). Within this loop, the algorithm computes and updates the elements of the input array a.

4. After the loop, the function prepares some variables for the next stage of the algorithm.

5. The next part of the algorithm is a series of nested loops that perform the bit-reversal permutation and apply the FCT to the input array a.

6. The code then calculates some additional trigonometric values, which are used in the next loop.

7. The following loop (from ix = 2 to tnn / 4 + 1) computes and updates the elements of the input array a using the previously calculated trigonometric values.

8. The input array a is further updated with the final calculations.

9. In the last loop (from j = 4 to tnn), the algorithm computes and updates the sum of elements in the input array a.

10. Finally, if the inversefct parameter is set to true, the function scales the input array a to obtain the inverse FCT.

The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

Fast Convolution

This code defines a function called fastconvolution that performs the convolution of a given signal with a response function using the Fast Fourier Transform (FFT) technique. Convolution is a mathematical operation used in signal processing to combine two signals, producing a third signal representing how the shape of one signal is modified by the other.

The fastconvolution function takes the following input parameters:

1. float signal: This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

3. float response: This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

4. int negativelen: This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

5. int positivelen: This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

The function works by:

1. Calculating the length nl of the arrays used for FFT, ensuring it's a power of 2 and large enough to hold the signal and response.

2. Creating two new arrays, a1 and a2, of length nl and initializing them with the input signal and response function, respectively.

3. Applying the forward FFT (realfastfouriertransform) to both arrays, a1 and a2.

4. Performing element-wise multiplication of the FFT results in the frequency domain.

5. Applying the inverse FFT (realfastfouriertransform) to the multiplied results in a1.

6. Updating the original signal array with the convolution result, which is stored in the a1 array.

The result of the convolution is stored in the input signal array at the function exit.

Fast Correlation

This code defines a function called fastcorrelation that computes the correlation between a signal and a pattern using the Fast Fourier Transform (FFT) method. The function takes four input arguments and modifies the input signal array to store the correlation values.

Input arguments:

1. float signal: This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array.

3. float pattern: This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

4. int patternlen: This is an integer representing the length of the pattern array.

The function performs the following steps:

1. Calculate the required size nl for the FFT by finding the smallest power of 2 that is greater than or equal to the sum of the lengths of the signal and the pattern.

2. Create two new arrays a1 and a2 with the length nl and initialize them to 0.

3. Copy the signal array into a1 and pad it with zeros up to the length nl.

4. Copy the pattern array into a2 and pad it with zeros up to the length nl.

5. Compute the FFT of both a1 and a2.

6. Perform element-wise multiplication of the frequency-domain representation of a1 and the complex conjugate of the frequency-domain representation of a2.

7. Compute the inverse FFT of the result obtained in step 6.

8. Store the resulting correlation values in the original signal array.

At the end of the function, the signal array contains the correlation values at points from 0 to SignalLen-1.

Fast Fourier Transform of Two Real Functions

This code defines a function called tworealffts that computes the Fast Fourier Transform (FFT) of two real-valued functions (a1 and a2) using a Cooley-Tukey-based radix-2 Decimation in Time (DIT) algorithm. The FFT is a widely used algorithm for computing the discrete Fourier transform (DFT) and its inverse.

Input parameters:

1. float a1: an array of real numbers, representing the values of the first function.

2. float a2: an array of real numbers, representing the values of the second function.

3. float a: an output array to store the Fourier transform of the first function.

4. float b: an output array to store the Fourier transform of the second function.

5. int tn: an integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

The function performs the following steps:

1. Combine the two input arrays, a1 and a2, into a single array a by interleaving their elements.

2. Perform a 1D FFT on the combined array a using the radix-2 DIT algorithm.

3. Separate the FFT results of the two input functions from the combined array a and store them in output arrays a and b.

Here is a detailed breakdown of the radix-2 DIT algorithm used in this code:

1. Bit-reverse the order of the elements in the combined array a.

2. Initialize the loop variables mmax, istep, and theta.

3. Enter the main loop that iterates through different stages of the FFT.

a. Compute the sine and cosine values for the current stage using the theta variable.

b. Initialize the loop variables wr and wi for the current stage.

c. Enter the inner loop that iterates through the butterfly operations within each stage.

i. Perform the butterfly operation on the elements of array a.

ii. Update the loop variables wr and wi for the next butterfly operation.

d. Update the loop variables mmax, istep, and theta for the next stage.

4. Separate the FFT results of the two input functions from the combined array a and store them in output arrays a and b.

At the end of the function, the a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Example scripts using functions contained in loxxfft

Real-Fast Fourier Transform of Price w/ Linear Regression

Real-Fast Fourier Transform of Price Oscillator

Normalized, Variety, Fast Fourier Transform Explorer

Variety RSI of Fast Discrete Cosine Transform

STD-Stepped Fast Cosine Transform Moving Average

TR_HighLow_LibLibrary "TR_HighLow_Lib"

TODO: add library description here

ShowLabel(_Text, _X, _Y, _Style, _Size, _Yloc, _Color)

TODO: Function to display labels

Parameters:

_Text : TODO: text (series string) Label text.

_X : TODO: x (series int) Bar index.

_Y : TODO: y (series int/float) Price of the label position.

_Style : TODO: style (series string) Label style.

_Size : TODO: size (series string) Label size.

_Yloc : TODO: yloc (series string) Possible values are yloc.price, yloc.abovebar, yloc.belowbar.

_Color : TODO: color (series color) Color of the label border and arrow

Returns: TODO: No return values

GetColor(_Index)

TODO: Function to take out 12 colors in order

Parameters:

_Index : TODO: color number.

Returns: TODO: color code

Tbl_position(_Pos)

TODO: Table display position function

Parameters:

_Pos : TODO: position.

Returns: TODO: Table position

DeleteLine()

TODO: Delete Line

Parameters:

: TODO: No parameter

Returns: TODO: No return value

DeleteLabel()

TODO: Delete Label

Parameters:

: TODO: No parameter

Returns: TODO: No return value

ZigZag(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _Histories, _Provisional_PHiLo, _Provisional_IHiLo, _Color1, _Width1, _Color2, _Width2, _ShowLabel, _ShowHighLowBar, _HighLowBarWidth, _HighLow_LabelSize)

TODO: Draw a zig-zag line.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_Histories : TODO: Array size (High-Low length)

_Provisional_PHiLo : TODO: Provisional High-Low Price

_Provisional_IHiLo : TODO: Provisional High-Low INDEX

_Color1 : TODO: Normal High-Low color

_Width1 : TODO: Normal High-Low width

_Color2 : TODO: Provisional High-Low color

_Width2 : TODO: Provisional High-Low width

_ShowLabel : TODO: Label display flag True: Displayed False: Not displayed

_ShowHighLowBar : TODO: High-Low bar display flag True:Show False:Hide

_HighLowBarWidth : TODO: High-Low bar width

_HighLow_LabelSize : TODO: Label Size

Returns: TODO: No return value

TrendLine(_a_PHiLo, _a_IHiLo, _Histories, _MultiLine, _StartWidth, _EndWidth, _IncreWidth, _StartTrans, _EndTrans, _IncreTrans, _ColorMode, _Color1_1, _Color1_2, _Color2_1, _Color2_2, _Top_High, _Top_Low, _Bottom_High, _Bottom_Low)

TODO: Draw a Trend Line

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_Histories : TODO: Array size (High-Low length)

_MultiLine : TODO: Draw a multiple Line.

_StartWidth : TODO: Line width start value

_EndWidth : TODO: Line width end value

_IncreWidth : TODO: Line width increment value

_StartTrans : TODO: Transparent rate start value

_EndTrans : TODO: Transparent rate finally

_IncreTrans : TODO: Transparent rate increase value

_ColorMode : TODO: 0:Nomal 1:Gradation

_Color1_1 : TODO: Gradation Color 1_1

_Color1_2 : TODO: Gradation Color 1_2

_Color2_1 : TODO: Gradation Color 2_1

_Color2_2 : TODO: Gradation Color 2_2

_Top_High : TODO: _Top_High Value for Gradation

_Top_Low : TODO: _Top_Low Value for Gradation

_Bottom_High : TODO: _Bottom_High Value for Gradation

_Bottom_Low : TODO: _Bottom_Low Value for Gradation

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index, _FrontMargin, _BackMargin)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index : TODO: Where to draw the Fibonacci line

_FrontMargin : TODO: Fibonacci line front-margin

_BackMargin : TODO: Fibonacci line back-margin

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index1, _FrontMargin1, _BackMargin1, _Transparent1, _Index2, _FrontMargin2, _BackMargin2, _Transparent2)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index1 : TODO: Where to draw the Fibonacci line 1

_FrontMargin1 : TODO: Fibonacci line front-margin 1

_BackMargin1 : TODO: Fibonacci line back-margin 1

_Transparent1 : TODO: Transparent rate 1

_Index2 : TODO: Where to draw the Fibonacci line 2

_FrontMargin2 : TODO: Fibonacci line front-margin 2

_BackMargin2 : TODO: Fibonacci line back-margin 2

_Transparent2 : TODO: Transparent rate 2

Returns: TODO: No return value

High_Low_Judgment(_Length, _Extension, _Difference)

TODO: Judges High-Low

Parameters:

_Length : TODO: High-Low Confirmation Length

_Extension : TODO: Length of extension when the difference did not open

_Difference : TODO: Difference size

Returns: TODO: _HiLo=High-Low flag 0:Neither high nor low、1:High、2:Low、3:High-Low

_PHi=high price、_PLo=low price、_IHi=High Price Index、_ILo=Low Price Index、

_Cnt=count、_ECnt=Extension count、

_DiffHi=Difference from Start(High)、_DiffLo=Difference from Start(Low)、

_StartHi=Start value(High)、_StartLo=Start value(Low)

High_Low_Data_AddedAndUpdated(_HiLo, _Histories, _PHi, _PLo, _IHi, _ILo, _DiffHi, _DiffLo, _a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo)

TODO: Adds and updates High-Low related arrays from given parameters

Parameters:

_HiLo : TODO: High-Low flag

_Histories : TODO: Array size (High-Low length)

_PHi : TODO: Price Hi

_PLo : TODO: Price Lo

_IHi : TODO: Index Hi

_ILo : TODO: Index Lo

_DiffHi : TODO: Difference in High

_DiffLo : TODO: Difference in Low

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

Returns: TODO: _PHiLo price array、_IHiLo indexed array、_FHiLo flag array、_DHiLo price-matching array、

Provisional_PHiLo Provisional price、Provisional_IHiLo 暫定インデックス

High_Low(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _a_Fibonacci, _Length, _Extension, _Difference, _Histories, _ShowZigZag, _ZigZagColor1, _ZigZagWidth1, _ZigZagColor2, _ZigZagWidth2, _ShowZigZagLabel, _ShowHighLowBar, _ShowTrendLine, _TrendMultiLine, _TrendStartWidth, _TrendEndWidth, _TrendIncreWidth, _TrendStartTrans, _TrendEndTrans, _TrendIncreTrans, _TrendColorMode, _TrendColor1_1, _TrendColor1_2, _TrendColor2_1, _TrendColor2_2, _ShowFibonacci1, _FibIndex1, _FibFrontMargin1, _FibBackMargin1, _FibTransparent1, _ShowFibonacci2, _FibIndex2, _FibFrontMargin2, _FibBackMargin2, _FibTransparent2, _ShowInfoTable1, _TablePosition1, _ShowInfoTable2, _TablePosition2)

TODO: Draw the contents of the High-Low array.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_a_Fibonacci : TODO: Fibonacci Gnar Matching

_Length : TODO: Length of confirmation

_Extension : TODO: Extension Length of extension when the difference did not open

_Difference : TODO: Difference size

_Histories : TODO: High-Low Length

_ShowZigZag : TODO: ZigZag Display

_ZigZagColor1 : TODO: Colors of ZigZag1

_ZigZagWidth1 : TODO: Width of ZigZag1

_ZigZagColor2 : TODO: Colors of ZigZag2

_ZigZagWidth2 : TODO: Width of ZigZag2

_ShowZigZagLabel : TODO: ZigZagLabel Display

_ShowHighLowBar : TODO: High-Low Bar Display

_ShowTrendLine : TODO: Trend Line Display

_TrendMultiLine : TODO: Trend Multi Line Display

_TrendStartWidth : TODO: Line width start value

_TrendEndWidth : TODO: Line width end value

_TrendIncreWidth : TODO: Line width increment value

_TrendStartTrans : TODO: Starting transmittance value

_TrendEndTrans : TODO: Transmittance End Value

_TrendIncreTrans : TODO: Increased transmittance value

_TrendColorMode : TODO: color mode

_TrendColor1_1 : TODO: Trend Color 1_1

_TrendColor1_2 : TODO: Trend Color 1_2

_TrendColor2_1 : TODO: Trend Color 2_1

_TrendColor2_2 : TODO: Trend Color 2_2

_ShowFibonacci1 : TODO: Fibonacci1 Display

_FibIndex1 : TODO: Fibonacci1 Index No.

_FibFrontMargin1 : TODO: Fibonacci1 Front margin

_FibBackMargin1 : TODO: Fibonacci1 Back Margin

_FibTransparent1 : TODO: Fibonacci1 Transmittance

_ShowFibonacci2 : TODO: Fibonacci2 Display

_FibIndex2 : TODO: Fibonacci2 Index No.

_FibFrontMargin2 : TODO: Fibonacci2 Front margin

_FibBackMargin2 : TODO: Fibonacci2 Back Margin

_FibTransparent2 : TODO: Fibonacci2 Transmittance

_ShowInfoTable1 : TODO: InfoTable1 Display

_TablePosition1 : TODO: InfoTable1 position

_ShowInfoTable2 : TODO: InfoTable2 Display

_TablePosition2 : TODO: InfoTable2 position

Returns: TODO: 無し

TR_HighLowLibrary "TR_HighLow"

TODO: add library description here

ShowLabel(_Text, _X, _Y, _Style, _Size, _Yloc, _Color)

TODO: Function to display labels

Parameters:

_Text : TODO: text (series string) Label text.

_X : TODO: x (series int) Bar index.

_Y : TODO: y (series int/float) Price of the label position.

_Style : TODO: style (series string) Label style.

_Size : TODO: size (series string) Label size.

_Yloc : TODO: yloc (series string) Possible values are yloc.price, yloc.abovebar, yloc.belowbar.

_Color : TODO: color (series color) Color of the label border and arrow

Returns: TODO: No return values

GetColor(_Index)

TODO: Function to take out 12 colors in order

Parameters:

_Index : TODO: color number.

Returns: TODO: color code

Tbl_position(_Pos)

TODO: Table display position function

Parameters:

_Pos : TODO: position.

Returns: TODO: Table position

DeleteLine()

TODO: Delete Line

Parameters:

: TODO: No parameter

Returns: TODO: No return value

DeleteLabel()

TODO: Delete Label

Parameters:

: TODO: No parameter

Returns: TODO: No return value

ZigZag(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _Histories, _Provisional_PHiLo, _Provisional_IHiLo, _Color1, _Width1, _Color2, _Width2, _ShowLabel, _ShowHighLowBar, _HighLowBarWidth, _HighLow_LabelSize)

TODO: Draw a zig-zag line.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_Histories : TODO: Array size (High-Low length)

_Provisional_PHiLo : TODO: Provisional High-Low Price

_Provisional_IHiLo : TODO: Provisional High-Low INDEX

_Color1 : TODO: Normal High-Low color

_Width1 : TODO: Normal High-Low width

_Color2 : TODO: Provisional High-Low color

_Width2 : TODO: Provisional High-Low width

_ShowLabel : TODO: Label display flag True: Displayed False: Not displayed

_ShowHighLowBar : TODO: High-Low bar display flag True:Show False:Hide

_HighLowBarWidth : TODO: High-Low bar width

_HighLow_LabelSize : TODO: Label Size

Returns: TODO: No return value

TrendLine(_a_PHiLo, _a_IHiLo, _Histories, _MultiLine, _StartWidth, _EndWidth, _IncreWidth, _StartTrans, _EndTrans, _IncreTrans, _ColorMode, _Color1_1, _Color1_2, _Color2_1, _Color2_2, _Top_High, _Top_Low, _Bottom_High, _Bottom_Low)

TODO: Draw a Trend Line

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_Histories : TODO: Array size (High-Low length)

_MultiLine : TODO: Draw a multiple Line.

_StartWidth : TODO: Line width start value

_EndWidth : TODO: Line width end value

_IncreWidth : TODO: Line width increment value

_StartTrans : TODO: Transparent rate start value

_EndTrans : TODO: Transparent rate finally

_IncreTrans : TODO: Transparent rate increase value

_ColorMode : TODO: 0:Nomal 1:Gradation

_Color1_1 : TODO: Gradation Color 1_1

_Color1_2 : TODO: Gradation Color 1_2

_Color2_1 : TODO: Gradation Color 2_1

_Color2_2 : TODO: Gradation Color 2_2

_Top_High : TODO: _Top_High Value for Gradation

_Top_Low : TODO: _Top_Low Value for Gradation

_Bottom_High : TODO: _Bottom_High Value for Gradation

_Bottom_Low : TODO: _Bottom_Low Value for Gradation

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index, _FrontMargin, _BackMargin)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index : TODO: Where to draw the Fibonacci line

_FrontMargin : TODO: Fibonacci line front-margin

_BackMargin : TODO: Fibonacci line back-margin

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index1, _FrontMargin1, _BackMargin1, _Transparent1, _Index2, _FrontMargin2, _BackMargin2, _Transparent2)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index1 : TODO: Where to draw the Fibonacci line 1

_FrontMargin1 : TODO: Fibonacci line front-margin 1

_BackMargin1 : TODO: Fibonacci line back-margin 1

_Transparent1 : TODO: Transparent rate 1

_Index2 : TODO: Where to draw the Fibonacci line 2

_FrontMargin2 : TODO: Fibonacci line front-margin 2

_BackMargin2 : TODO: Fibonacci line back-margin 2

_Transparent2 : TODO: Transparent rate 2

Returns: TODO: No return value

High_Low_Judgment(_Length, _Extension, _Difference)

TODO: Judges High-Low

Parameters:

_Length : TODO: High-Low Confirmation Length

_Extension : TODO: Length of extension when the difference did not open

_Difference : TODO: Difference size

Returns: TODO: _HiLo=High-Low flag 0:Neither high nor low、1:High、2:Low、3:High-Low

_PHi=high price、_PLo=low price、_IHi=High Price Index、_ILo=Low Price Index、

_Cnt=count、_ECnt=Extension count、

_DiffHi=Difference from Start(High)、_DiffLo=Difference from Start(Low)、

_StartHi=Start value(High)、_StartLo=Start value(Low)

High_Low_Data_AddedAndUpdated(_HiLo, _Histories, _PHi, _PLo, _IHi, _ILo, _DiffHi, _DiffLo, _a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo)

TODO: Adds and updates High-Low related arrays from given parameters

Parameters:

_HiLo : TODO: High-Low flag

_Histories : TODO: Array size (High-Low length)

_PHi : TODO: Price Hi

_PLo : TODO: Price Lo

_IHi : TODO: Index Hi

_ILo : TODO: Index Lo

_DiffHi : TODO: Difference in High

_DiffLo : TODO: Difference in Low

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

Returns: TODO: _PHiLo price array、_IHiLo indexed array、_FHiLo flag array、_DHiLo price-matching array、

Provisional_PHiLo Provisional price、Provisional_IHiLo 暫定インデックス

High_Low(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _a_Fibonacci, _Length, _Extension, _Difference, _Histories, _ShowZigZag, _ZigZagColor1, _ZigZagWidth1, _ZigZagColor2, _ZigZagWidth2, _ShowZigZagLabel, _ShowHighLowBar, _ShowTrendLine, _TrendMultiLine, _TrendStartWidth, _TrendEndWidth, _TrendIncreWidth, _TrendStartTrans, _TrendEndTrans, _TrendIncreTrans, _TrendColorMode, _TrendColor1_1, _TrendColor1_2, _TrendColor2_1, _TrendColor2_2, _ShowFibonacci1, _FibIndex1, _FibFrontMargin1, _FibBackMargin1, _FibTransparent1, _ShowFibonacci2, _FibIndex2, _FibFrontMargin2, _FibBackMargin2, _FibTransparent2, _ShowInfoTable1, _TablePosition1, _ShowInfoTable2, _TablePosition2)

TODO: Draw the contents of the High-Low array.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_a_Fibonacci : TODO: Fibonacci Gnar Matching

_Length : TODO: Length of confirmation

_Extension : TODO: Extension Length of extension when the difference did not open

_Difference : TODO: Difference size

_Histories : TODO: High-Low Length

_ShowZigZag : TODO: ZigZag Display

_ZigZagColor1 : TODO: Colors of ZigZag1

_ZigZagWidth1 : TODO: Width of ZigZag1

_ZigZagColor2 : TODO: Colors of ZigZag2

_ZigZagWidth2 : TODO: Width of ZigZag2

_ShowZigZagLabel : TODO: ZigZagLabel Display

_ShowHighLowBar : TODO: High-Low Bar Display

_ShowTrendLine : TODO: Trend Line Display

_TrendMultiLine : TODO: Trend Multi Line Display

_TrendStartWidth : TODO: Line width start value

_TrendEndWidth : TODO: Line width end value

_TrendIncreWidth : TODO: Line width increment value

_TrendStartTrans : TODO: Starting transmittance value

_TrendEndTrans : TODO: Transmittance End Value

_TrendIncreTrans : TODO: Increased transmittance value

_TrendColorMode : TODO: color mode

_TrendColor1_1 : TODO: Trend Color 1_1

_TrendColor1_2 : TODO: Trend Color 1_2

_TrendColor2_1 : TODO: Trend Color 2_1

_TrendColor2_2 : TODO: Trend Color 2_2

_ShowFibonacci1 : TODO: Fibonacci1 Display

_FibIndex1 : TODO: Fibonacci1 Index No.

_FibFrontMargin1 : TODO: Fibonacci1 Front margin

_FibBackMargin1 : TODO: Fibonacci1 Back Margin

_FibTransparent1 : TODO: Fibonacci1 Transmittance

_ShowFibonacci2 : TODO: Fibonacci2 Display

_FibIndex2 : TODO: Fibonacci2 Index No.

_FibFrontMargin2 : TODO: Fibonacci2 Front margin

_FibBackMargin2 : TODO: Fibonacci2 Back Margin

_FibTransparent2 : TODO: Fibonacci2 Transmittance

_ShowInfoTable1 : TODO: InfoTable1 Display

_TablePosition1 : TODO: InfoTable1 position

_ShowInfoTable2 : TODO: InfoTable2 Display

_TablePosition2 : TODO: InfoTable2 position

Returns: TODO: 無し

ArrayExtensionLibrary "ArrayExtension"

Functions to extend Arrays.

index_2d_to_1d(dimension_x, dimension_y, index_x, index_y) returns the flatened one dimension index of a two dimension array.

Parameters:

dimension_x : int, dimension of X.

dimension_y : int, dimension of Y.

index_x : int, index of X.

index_y : int, index of Y.

Returns: int, index in 1 dimension

index_3d_to_1d(dimension_x, dimension_y, dimension_z, index_x, index_y, index_z) returns the flatened one dimension index of a three dimension array.

Parameters:

dimension_x : int, dimension of X.

dimension_y : int, dimension of Y.

dimension_z : int, dimension of Z.

index_x : int, index of X.

index_y : int, index of Y.

index_z : int, index of Z.

Returns: int, index in 1 dimension

down_sample(sample, new_size) Down samples a array to a specified size.

Parameters:

sample : float array, array with source data.

new_size : new size of down sampled array.

Returns: float array with down sampled data.

sort_indices_float(sample, order) Sorts array and returns a extra array with sorting indices.

Parameters:

sample : float array with values to be sorted.

order : string, default='forward', options='forward', 'backward'.

Returns: _indices int array with indices.

_ordered float array with ordered values.

sort_indices_int(sample, order) Sorts array and returns a extra array with sorting indices.

Parameters:

sample : int array with values to be sorted.

order : string, default='forward', options='forward', 'backward'.

Returns: _indices int array with indices.

_ordered float array with ordered values.

sort_bool_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : bool array with data sample to be sorted.

Returns: bool array

sort_box_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : box array with data sample to be sorted.

Returns: box array

sort_color_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : color array with data sample to be sorted.

Returns: color array

sort_float_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : float array with data sample to be sorted.

Returns: float array

sort_int_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : int array with data sample to be sorted.

Returns: int array

sort_label_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : label array with data sample to be sorted.

Returns: label array

sort_line_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : line array with data sample to be sorted.

Returns: line array

sort_string_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : string array with data sample to be sorted.

Returns: string array

sort_table_from_indices(indices, sample) Sorts sample array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : table array with data sample to be sorted.

Returns: table array

sort_bool_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : bool array with data sample to be sorted.

Returns: void updates sample array.

sort_box_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : box array with data sample to be sorted.

Returns: void updates sample

sort_color_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : color array with data sample to be sorted.

Returns: void updates sample

sort_float_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : float array with data sample to be sorted.

Returns: void updates sample

sort_int_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : int array with data sample to be sorted.

Returns: void updates sample

sort_label_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : label array with data sample to be sorted.

Returns: void updates sample

sort_line_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : line array with data sample to be sorted.

Returns: void updates sample

sort_string_inplace_from_indices(indices, sample) Sorts sample inplace array using a array with indices.

Parameters:

indices : int array with positional indices.

sample : string array with data sample to be sorted.

Returns: void updates sample

sort_table_inplace_from_indices(indices, sample) Sorts sample array inplace using a array with indices.

Parameters:

indices : int array with positional indices.

sample : table array with data sample to be sorted.

Returns: void updates sample

to_float(sample) Transform a integer array into a float array

Parameters:

sample : int array, sample data to transform.

Returns: float array

to_int(sample, method) Transform a float array into a int array

Parameters:

sample : float array, sample data to transform.

method : string, default="round", options= , aproximation method.

Returns: int array

Bitcoin Expectile Model [LuxAlgo]The Bitcoin Expectile Model is a novel approach to forecasting Bitcoin, inspired by the popular Bitcoin Quantile Model by PlanC. By fitting multiple Expectile regressions to the price, we highlight zones of corrections or accumulations throughout the Bitcoin price evolution.

While we strongly recommend using this model with the Bitcoin All Time History Index INDEX:BTCUSD on the 3 days or weekly timeframe using a logarithmic scale, this model can be applied to any asset using the daily timeframe or superior.

Please note that here on TradingView, this model was solely designed to be used on the Bitcoin 1W chart, however, it can be experimented on other assets or timeframes if of interest.

🔶 USAGE

The Bitcoin Expectile Model can be applied similarly to models used for Bitcoin, highlighting lower areas of possible accumulation (support) and higher areas that allow for the anticipation of potential corrections (resistance).

By default, this model fits 7 individual Expectiles Log-Log Regressions to the price, each with their respective expectile ( tau ) values (here multiplied by 100 for the user's convenience). Higher tau values will return a fit closer to the higher highs made by the price of the asset, while lower ones will return fits closer to the lower prices observed over time.

Each zone is color-coded and has a specific interpretation. The green zone is a buy zone for long-term investing, purple is an anomaly zone for market bottoms that over-extend, while red is considered the distribution zone.

The fits can be extrapolated, helping to chart a course for the possible evolution of Bitcoin prices. Users can select the end of the forecast as a date using the "Forecast End" setting.

While the model is made for Bitcoin using a log scale, other assets showing a tendency to have a trend evolving in a single direction can be used. See the chart above on QQQ weekly using a linear scale as an example.

The Start Date can also allow fitting the model more locally, rather than over a large range of prices. This can be useful to identify potential shorter-term support/resistance areas.

🔶 DETAILS

🔹 On Quantile and Expectile Regressions

Quantile and Expectile regressions are similar; both return extremities that can be used to locate and predict prices where tops/bottoms could be more likely to occur.

The main difference lies in what we are trying to minimize, which, for Quantile regression, is commonly known as Quantile loss (or pinball loss), and for Expectile regression, simply Expectile loss.

You may refer to external material to go more in-depth about these loss functions; however, while they are similar and involve weighting specific prices more than others relative to our parameter tau, Quantile regression involves minimizing a weighted mean absolute error, while Expectile regression minimizes a weighted squared error.

The squared error here allows us to compute Expectile regression more easily compared to Quantile regression, using Iteratively reweighted least squares. For Quantile regression, a more elaborate method is needed.

In terms of comparison, Quantile regression is more robust, and easier to interpret, with quantiles being related to specific probabilities involving the underlying cumulative distribution function of the dataset; on the other expectiles are harder to interpret.

🔹 Trimming & Alterations

It is common to observe certain models ignoring very early Bitcoin price ranges. By default, we start our fit at the date 2010-07-16 to align with existing models.

By default, the model uses the number of time units (days, weeks...etc) elapsed since the beginning of history + 1 (to avoid NaN with log) as independent variable, however the Bitcoin All Time History Index INDEX:BTCUSD do not include the genesis block, as such users can correct for this by enabling the "Correct for Genesis block" setting, which will add the amount of missed bars from the Genesis block to the start oh the chart history.

🔶 SETTINGS

Start Date: Starting interval of the dataset used for the fit.

Correct for genesis block: When enabled, offset the X axis by the number of bars between the Bitcoin genesis block time and the chart starting time.

🔹 Expectiles

Toggle: Enable fit for the specified expectile. Disabling one fit will make the script faster to compute.

Expectile: Expectile (tau) value multiplied by 100 used for the fit. Higher values will produce fits that are located near price tops.

🔹 Forecast

Forecast End: Time at which the forecast stops.

🔹 Model Fit

Iterations Number: Number of iterations performed during the reweighted least squares process, with lower values leading to less accurate fits, while higher values will take more time to compute.

UM VIX status table and Roll Yield with EMA

Description :

This oscillator indicator gives you a quick snapshot of VIX, VIX futures prices, and the related VIX roll yield at a glance. When the roll yield is greater than 0, The front-month VX1 future contract is less than the next-month VX2 contract. This is called Contango and is typical for the majority of the time. If the roll yield falls below zero. This is considered backwardation where the front-month VX1 contract is higher than the value of the next-month VX2 contract. Contango is most common. When Backwardation occurs, there is usually high volatility present.

Features :

The red and green fill indicate the current roll yield with the gray line being zero.

An Exponential moving average is overlaid on the roll yield. It is red when trending down and green when trending up. If you right-click the indicator, you can set alerts for roll yield EMA color transitions green to red or red to green.

Suggested uses:

The author suggests a one hour chart using the 55 period EMA with a 60 minute setting in the indicator. This gives you a visual idea of whether the roll yield is rising or falling. The roll yield will often change directions at market turning points. For example if the roll yield EMA changes from red to green, this indicates a rising roll yield and volatility is subsiding. This could be considered bullish. If the roll yield begins falling, this indicates volatility is rising. This may be negative for stocks and indexes.

I look for short volatility positions (SVIX) when the roll yield is rising. I look for long volatility positions (VXX, UVXY, UVIX) when the roll yield begins falling. The indicator can be added to any chart. I suggest using the VX1, SPY, VIX, or other major stock index.

Set the time frame to your trading style. The default is 60 minutes. Note, the timeframe of the indicator does NOT utilize the current chart timeframe, it must be set to the desired timeframe. I manually input text on the chart indicator for understanding periods of Long and Short Volatility.

Settings and Defaults