MW+MA Cross StrategyThe strategy uses WMA and SMA indicators with certain algorithm in order to create signals when they cross.

ابحث في النصوص البرمجية عن "the strat"

Gidra's SRSI strategy v0.1The strategy uses the Gidra SRSI indicator and MTF Supertrend indicator.

It can be used with 1h (1st timeframe) / 1D (2nd timeframe), for example, or you can choose your own parameters

The Ultimate TripleX Trading StrategyThe strategy is now set to wor with the 15 Minutes timeframe, but you can adjust it to work with any timeframe.

Sb_Rate_Of_Change_BB_Band_strategy Version 1.0The strategy couples the concept of rate of change along with the Bollinger bands.

Along with it LazyBear's RSI/MFI with Volatility Indicator is also taken to reduce the number of trades and improve efficiency.

Strategy (in Layman terms):

If in the past 10 candles RSI/MFI with Volatility Indicator has printed a red/green colour and the roc has gone above/below the Bollinger bands then the short/long order is placed respectively.

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

SB_Compliment_RSI StrategyThe strategy modifies the original rsi strategy with the addition of compliment si (i.e. 100-rsi).

Strategy Idea: Previous rsi high and low value is recorded when the rsi crosses overBought(70) and OverSold(30) values.

Now when the rsi crosses above the overSold range, the rsi is matched with the compliment of previous high rsi value. If the compliment i.e.(100-prev_rsi_high) is less than or equal to rsi then long position is taken.

For short position, when the rsi crosses below the overBought range, the rsi is matched with the compliment of previous low rsi value. If compliment i.e.(100-prev_rsi_low) is greater than or equal to rsi.

Below s the code for the indicator present in the chart.

//@version=3

study(title="SB_Compliment_Relative Strength Index", shorttitle="RSI")

src = close, len = input(14, minval=1, title="Length")

up = rma(max(change(src), 0), len)

down = rma(-min(change(src), 0), len)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

plot(rsi, color=purple)

plot(100-rsi, color=orange)

band1 = hline(70)

band0 = hline(30)

fill(band1, band0, color=purple, transp=90)

The code also has switch code also which means it will enter the overBrought or overSold block one after the other.

Future modifications: Currently the value of rsi tracked is the one in which it crosses the overSold or OverBought range and not the highest/lowest value when the value is above/below OverBought/OverSold range.

Comment the perfect combination of indicators for it and will try to incorporate those indicators into it in the next version.

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

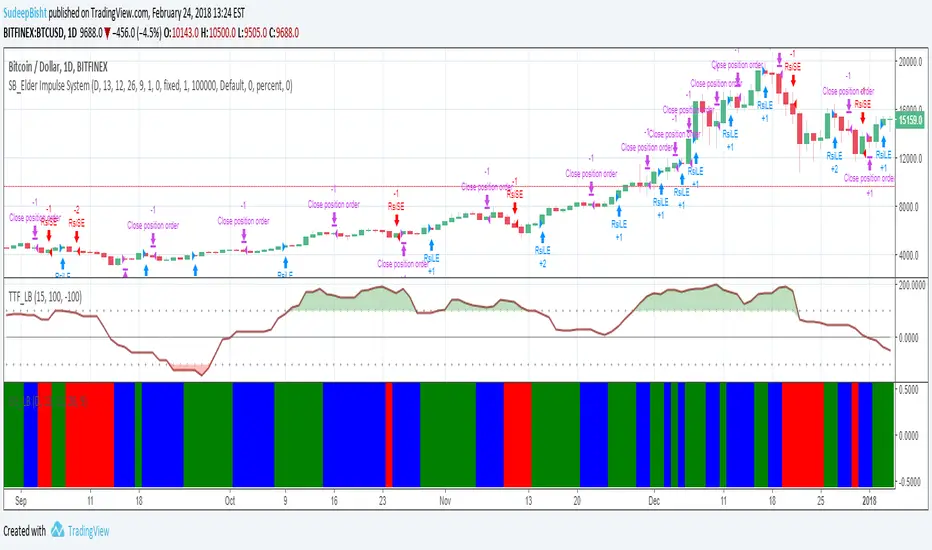

SB_Elder Impulse SystemThe strategy is based on LazyBear's Elder Impulse System

Strategy(in layman terms):

Long: When the green bar in the Elder Impulse System's indicator shows up

Short: When the red bar in the Elder Impulse System's indicator shows up

Close trade/Profit booking: When the blue bar in the Elder Impulse System's indicator shows up

Original Idea:

Message in the script if you think of any modifications/ enhancements.

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Rainbow StrategyThe strategy is based on the following idea:

www.youtube.com

Not a fan of this but no script was present to show this idea's performance.

Best suitable for the 1-minute chart. You can change the ema values as per your needs.

For Tips to continue :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

SB_CM_RSI_2_Strategy_Version 1.0The strategy is based on the indicator posted by @ChrisMoody "CM RSI-2 Strategy Lower Indicator" which is based on "Larry Connors RSI-2 Strategy - Lower RSI"

In this strategy the longs are placed when a green color is encountered in the rsi and short when red color is encountered in the rsi.

Although the profits can be booked at different interval.

Just message in the script if you have any different idea regarding this indicator.

For the original indicator you can refer to :

For Tips to continue :) :

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Free Strategy #01 (ES / SPY)The strategy was designed to be traded based on daily data on the ES and SPY--the strategy was originally developed on NinjaTrader using approximately 50% out of sample data with a slippage of 1 tick on the ES. This is our first strategy that we converted from NinjaTrader to TradingView, so if you see any issues with our conversion, please let us know as we are still learning TradingView Pine Script.

Rawa_Trade_System_Vol_AdxThe strategy must be configured for each instrument separately; the basic configuration uses a trailing stop, a 4H timeframe, and excludes margin trading.

CE+ZLSMA RovTrading StrateryThe strategy is optimized for scalping in small timeframes like M15 and M30, as well as M5.

It combines two indicators: CE and ZLSMA.

Try it now!

dabilThe strategy is probably to go short or long with the trend depending on the case, but if all time units 1 minute then 3 minutes then 5 minutes then 15 minutes then 1 hour all show the same direction, but first the 1 hour must be bullish in which the 1 hour candle closes above the previous one, for example if the trend is bearish then the market wants to change direction, then a 1 hour bullish close must then be followed by a 1 hour bearish close below the bullish candle, then another bullish candle must shoot above the previous bullish candle, then 15 minutes also shoot above the previous 15 bullish candles, then 1 and 2...3.5. Then I can rise with the market by only covering the last 15 bullish candles with my stop loss, if my SL is 50 pips then I want 100 pips and then I'm out.

MomentumThe strategy uses EMA200, ADX/DMI, RSI, and volume. Pivot levels and Heikin-Ashi ensure safe entries, while cooldowns and opposite-locks prevent overtrading. Exits are managed with ATR trailing stops and trend-reversal signals.

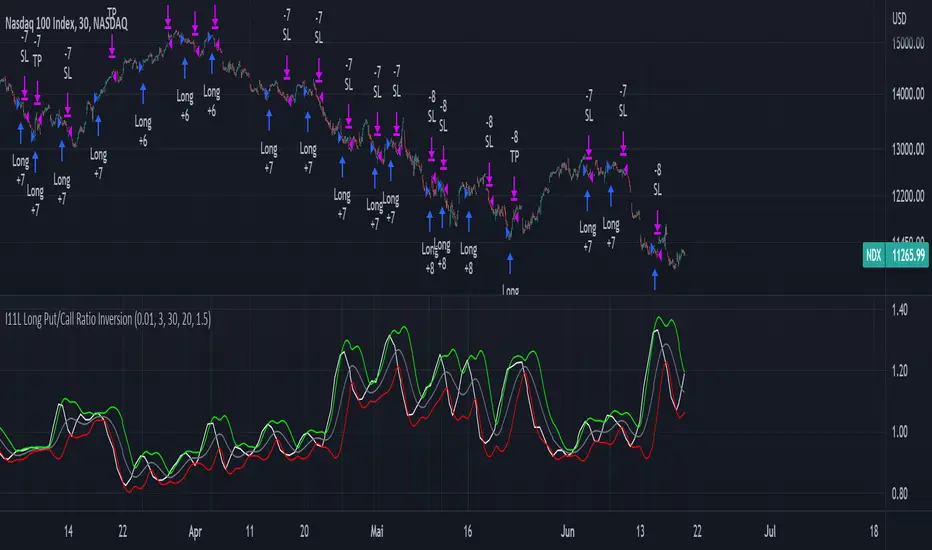

I11L Long Put/Call Ratio InversionThe Strategy uses the Put/Call Options Ratio Inversaion as a Signal and Implements simple Money Management rules.

It is adjusted for the NDX and for the SPX in the 30min Range.

The Oscilation has to be finetuned to reflect the correct Reversal point.

A good indicator of the correct Reversal Point is a solid range of good backtesting results..

The strategy example. Close position by timeoutThis is an example how to close open entries by timeout for educational purpose.

Arjun_Bhatia_Alligator_StrategyThe strategy utilizes the alligator indicator on bank nifty HA candles and bank nifty futures charts.

Trend Following or Mean RevertingThe strategy checks nature of the instruments. It Buys if the close is greater than yesterday's high, reverse the position if the close is lower than yesterday's low and repeat the process.

1. If it is trend following then the equity curve will be in uptrend

2. If it is mean reverting then the equity curve will be downtrend

Thanks to Rayner Teo.

Bollinger and Tendencies (Bollinger e Tendências )The strategy consists of buying when the price breaks up (crossover) the bottom line of the Bollinger and selling when the price breaks down (crossunder) to your top line.

The chart still shows trends clearly, with the fill between the exponential average and the closing value of the canlestick, green at high, red at low (this part of the script is based on the code: "Pivot Daily Price Color" by Rimko).

It also places notes on the high and low candlesticks (based on the code: "Candlesticks Pattern Identified" by Repo32).

It is recommended to use it in conjunction with the "IFR and Storage" script (also available to me), and some volume script.

A estratégia consiste em comprar quando o preço rompe para cima (crossover) a linha inferior do Bollinger e vender quando o preço rompe para baixo (crossunder) a sua linha superior.

O gráfico ainda mostra as tendências de forma clara, com o preenchimento entre a média exponencial e o valor de fechamento do canlestick, verde em alta, vermelho em baixa (essa parte do script é baseada no código: "Pivot Daily Price Color" do usuário: Rimko).

Também, coloca apontamentos nos candlesticks de alta e de baixa (baseado no código: "Candlesticks Pattern Identified" do usuário Repo32).

Recomenda-se a utilização em conjunto com o script "IFR e Estocagem" (também por mim disponibilizado), e algum script de volume.

SB_Volume_oscillator_Prev_high_lowThe strategy is a take on traditional volume oscillator.

In Layman terms:

The script places an order when the oscillator crosses the zero mark in the volume oscillator.

If the previous high is greater than the absolute value of previous low then a long order is placed

And if the absolute previous low is greater than the previous high then a shrt order is placed.

Last script (bandwidth focus on other monetary works. If you have any opportunities ping me)

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

NQ Conservative MTF FINAL (1m + 15m) [Risk-Controlled]Strategy Description

This is a conservative multi-timeframe futures strategy designed for the NASDAQ-100 (NQ). Trades are taken on the 1-minute chart only in the direction of the confirmed 15-minute trend, defined by moving averages and momentum strength. Entries occur after short-term pullbacks, using EMA alignment and RSI confirmation to avoid chasing price. Risk is managed with an ATR-based stop loss and take-profit, limiting per-trade risk while allowing larger trend winners to run. The strategy emphasizes capital preservation, controlled drawdowns, and consistency over high trade frequency.

HYE Combo Market [Strategy] (Vwap Mean Reversion + Trend Hunter)In this strategy, I used a combination of trend hunter and vwap mean reversion strategies that I published before.

Trend Hunter Strategy:

Mean Reversion Vwap Strategy:

The results are quite impressive, especially for bitcoin.

While the hodl return for bitcoin was 13419%, the strategy's return in the same period was about 5 times (65000%) of this.

s3.tradingview.com

In this combo strategy, I made some changes to the original settings of the strategies used together and added some more new features.

Trend Hunter Strategy Settings: (Original / Combo)

- Slow Tenkansen Period : 9 / 9

- Slow Kijunsen Period : 26 / 13

- Fast Tenkansen Period : 5 / 3

- Fast Kijunsen Period : 13 / 7

- BB Length : 20 / 20

- BB Stdev : 2 / 2

- TSV Length : 13 / 20

- TSV Ema Length : 7 / 7

* I also added a "vidya moving average" to be used as a confirmation tool to open a long position. (Candle close must be above the vidya line.)

Vwap Mean Reversion Strategy Settings: (Original / Combo)

- Small Vwap : 2 / 8

- Big Vwap : 5 / 10

- Percent Below to Buy : 3 / 2

- RSI Period : 2 / 2

- RSI Ema Period : 5 / 5

- Maximum RSI Level for Buy : 30

* I also added a "mean vwap line" to be used for exits in this part of the strategy. In the original version, when small vwap crossovers big vwap, we close the position, but in this strategy we will wait for the close above the mean vwap.

TIPS AND WARNINGS

1-) The standard settings of this combo strategy is designed and tested with daily timeframe. For lower timeframes, you should change the strategy settings and find the best value for yourself.

2-) Only the mean vwap line is displayed on the graph. For a detailed view, you can delete the "//" marks from the plot codes in the strategy code.

3-) This is a strategy for educational and experimental purposes. It cannot be considered as investment advice. You should be careful and make your own risk assessment when opening real market trades using this strategy.

________________________________________________________

Bu stratejide, daha önce yayınladığım trend avcısı ve vwap ortalamaya geri dönüş stratejilerinin bir kombinasyonunu kullandım.

Sonuçlar özellikle bitcoin için oldukça etkileyici.

Bitcoin için hodl getirisi %13419 iken, stratejinin aynı dönemdeki getirisi bunun yaklaşık 5 katı (%65000) idi.

Bu kombo stratejide, birlikte kullanılan stratejilerin orijinal ayarlarında bazı değişiklikler yaptım ve bazı yeni özellikler ekledim.

Trend Avcısı Strateji Ayarları: (Orijinal / Combo)

- Yavaş Tenkansen Periyodu : 9 / 9

- Yavaş Kijunsen Periyodu : 26 / 13

- Hızlı Tenkansen Periyodu : 5 / 3

- Hızlı Kijunsen Periyodu : 13 / 7

- BB Uzunluğu : 20 / 20

- BB Standart Sapması : 2 / 2

- TSV Uzunluğu : 13 / 20

- TSV Ema Uzunluğu : 7 / 7

* Ayrıca long pozisyon açmak için onay aracı olarak kullanılmak üzere "vidya hareketli ortalama" ekledim. (Mum kapanışı vidya çizgisinin üzerinde olmalıdır.)

Vwap Ortalamaya Dönüş Stratejisi Ayarları: (Orijinal / Combo)

- Küçük Vwap : 2 / 8

- Büyük Vwap : 5 / 10

- Alış İçin Gerekli Fark Oranı : 3 / 2

- RSI Periyodu : 2 / 2

- RSI Ema Periyodu: 5 / 5

- Alış için gerekli maksimum RSI seviyesi : 30

* Stratejinin bu bölümünde pozisyondan çıkışlar için kullanılacak bir "ortalama vwap çizgisi" de ekledim. Orijinal versiyonda, küçük vwap, büyük vwap'ı yukarı kestiğinde pozisyonu kapatıyoruz, ancak bu stratejide, ortalama vwap'ın üzerindeki kapanışı bekleyeceğiz.

İPUÇLARI VE UYARILAR

1-) Bu birleşik stratejinin standart ayarları, günlük zaman dilimi ile tasarlanmış ve test edilmiştir. Daha düşük zaman dilimleri için strateji ayarlarını değiştirmeli ve kendiniz için en iyi değeri bulmalısınız.

2-) Grafikte sadece ortalama vwap çizgisi görüntülenir. Ayrıntılı bir görünüm için strateji kodundaki "plot" ile başlayan satırlarda grafikte görünmesini istediğiniz özelliğin önündeki "//" işaretlerini silebilirsiniz.

3-) Eğitim ve deneysel amaçlı bir stratejidir. Yatırım tavsiyesi olarak değerlendirilemez. Bu stratejiyi kullanarak gerçek piyasa işlem açarken dikkatli olmalı ve kendi risk değerlendirmenizi yapmalısınız.

Buy The Dip - ENGThis script implements a grid trading strategy for long positions in the USDT market. The core idea is to place a series of buy limit orders at progressively lower prices below an initial entry point, aiming to lower the average entry price as the price drops. It then aims to exit the entire position when the price rises a certain percentage above the average entry price.

Here's a detailed breakdown:

1. Strategy Setup (`strategy` function):

`'거미줄 자동매매 250227'`: The name of the strategy.

`overlay = true`: Draws plots and labels directly on the main price chart.

`pyramiding = 15`: Allows up to 15 entries in the same direction (long). This is essential for grid trading, as it needs to open multiple buy orders.

`initial_capital = 600`: Sets the starting capital for backtesting to 600 USDT.

`currency = currency.USDT`: Specifies the account currency as USDT.

`margin_long/short = 0`: Doesn't define specific margin requirements (might imply spot trading logic or rely on exchange defaults if used live).

`calc_on_order_fills = false`: Strategy calculations happen on each bar's close, not just when orders fill.

2. Inputs (`input`):

Core Settings:

`lev`: Leverage (default 10x). Used to calculate position sizes.

`Investment Percentage %`: Percentage of total capital to allocate to the initial grid (default 80%).

`final entry Percentage %`: Percentage of the *remaining* capital (100 - `Investment Percentage %`) to use for the "semifinal" entry (default 50%). The rest goes to the "final" entry.

`Price Adjustment Length`: Lookback period (default 4 bars) to determine the initial `maxPrice`.

`price range`: The total percentage range downwards from `maxPrice` where the grid orders will be placed (default -10%, meaning 10% down).

`tp`: Take profit percentage above the average entry price (default 0.45%).

`semifinal entry price percent`: Percentage drop from `maxPrice` to trigger the "semifinal" larger entry (default -12%).

`final entry price percent`: Percentage drop from `maxPrice` to trigger the "final" larger entry (default -15%).

Rounding & Display:

`roundprice`, `round`: Decimal places for rounding price and quantity calculations.

`texts`, `label_style`: User interface preferences for text size and label appearance on the chart.

Time Filter:

`startTime`, `endTime`: Defines the date range for the backtest.

3. Calculations & Grid Setup:

`maxPrice`: The highest price point for the grid setup. Calculated as the lowest low of the previous `len` bars only if no trades are open. If trades are open, it uses the entry price of the very first order placed in the current sequence (`strategy.opentrades.entry_price(0)`).

`minPrice`: The lowest price point for the grid, calculated based on `maxPrice` and `range1`.

`totalCapital`: The amount of capital (considering leverage and `per1`) allocated for the main grid orders.

`coinRatios`: An array ` `. This defines the *relative* size ratio for each of the 11 grid orders. Later orders (at lower prices) will be progressively larger.

`totalRatio`: The sum of all ratios (66).

`positionSizes`: An array calculated based on `totalCapital` and `coinRatios`. It determines the actual quantity (size) for each of the 11 grid orders.

4. Order Placement Logic (`strategy.entry`):

Initial Grid Orders:

Runs only if within the specified time range and no position is currently open (`strategy.opentrades == 0`).

A loop places 11 limit buy orders (`Buy 1` to `Buy 11`).

Prices are calculated linearly between `maxPrice` and `minPrice`.

Order sizes are taken from the `positionSizes` array.

Semifinal & Final Entries:

Two additional, larger limit buy orders are placed simultaneously with the grid orders:

`semifinal entry`: At `maxPrice * (1 - semifinal / 100)`. Size is based on `per2`% of the capital *not* used by the main grid (`1 - per1`).

`final entry`: At `maxPrice * (1 - final / 100)`. Size is based on the remaining capital (`1 - per2`% of the unused portion).

5. Visualization (`line.new`, `label.new`, `plot`, `plotshape`, `plotchar`):

Grid Lines & Labels:

When a position is open (`strategy.opentrades > 0`), horizontal lines and labels are drawn for each of the 11 grid order prices and the "final" entry price.

Lines extend from the bar where the *first* entry occurred.

Labels show the price and planned size for each level.

Dynamic Coloring: If the price drops below a grid level, the corresponding line turns green, and the label color changes, visually indicating that the level has been reached or filled.

Plotted Lines:

`maxPrice` (initial high point for the grid).

`strategy.position_avg_price` (current average entry price of the open position, shown in red).

Target Profit Price (`strategy.position_avg_price * (1 + tp / 100)`, shown in green).

Markers:

A flag marks the `startTime`.

A rocket icon (`🚀`) appears below the bar where the `final entry` triggers.

A stop icon (`🛑`) appears below the bar where the `semifinal entry` triggers.

6. Exit Logic (`strategy.exit`, `strategy.entry` with `qty=0`):

Main Take Profit (`Full Exit`):

Uses `strategy.entry('Full Exit', strategy.short, qty = 0, limit = target2)`. This places a limit order to close the entire position (`qty=0`) at the calculated take profit level (`target2 = avgPrice * (1 + tp / 100)`). Note: Using `strategy.entry` with `strategy.short` and `qty=0` is a way to close a long position, though `strategy.exit` is often clearer. This exit seems intended to apply whenever any part of the grid position is open.

First Order Trailing Stop (`1st order Full Exit`):

Conditional: Only active if `trail` input is true AND the *last* order filled was "Buy 1" (meaning only the very first grid level was entered).

Uses `strategy.exit` with `trail_points` and `trail_offset` based on ATR values to implement a trailing stop loss/profit mechanism for this specific scenario.

This trailing stop order is cancelled (`strategy.cancel`) if any subsequent grid orders ("Buy 2", etc.) are filled.

Final/Semifinal Take Profit (`final Full Exit`):

Conditional: Only active if more than 11 entries have occurred (meaning either the "semifinal" or "final" entry must have triggered).

Uses `strategy.exit` to place a limit order to close the entire position at the take profit level (`target3 = avgPrice * (1 + tp / 100)`).

7. Information Display (Tables & UI Label):

`statsTable` (Top Right):

A comprehensive table displaying grouped information:

Market Info (Entry Point, Current Price)

Position Info (Avg Price, Target Price, Unrealized PNL $, Unrealized PNL %, Position Size, Position Value)

Strategy Performance (Realized PNL $, Realized PNL %, Initial/Total Balance, MDD, APY, Daily Profit %)

Trade Statistics (Trade Count, Wins/Losses, Win Rate, Cumulative Profit)

`buyAvgTable` (Bottom Left):

* Shows the *theoretical* entry price and average position price if trades were filled sequentially up to each `buy` level (buy1 to buy10). It uses hardcoded percentage drops (`buyper`, `avgper`) based on the initial `maxPrice` and `coinRatios`, not the dynamically changing actual average price.

`uiLabel` (Floating Label on Last Bar):

Updates only on the most recent bar (`barstate.islast`).

Provides real-time context when a position is open: Size, Avg Price, Current Price, Open PNL ($ and %), estimated % drop needed for the *next* theoretical buy (based on `ui_gridStep` input), % rise needed to hit TP, and estimated USDT profit at TP.

Shows "No Position" and basic balance/trade info otherwise.

In Summary:

This is a sophisticated long-only grid trading strategy. It aims to:

1. Define an entry range based on recent lows (`maxPrice`).

2. Place 11 scaled-in limit buy orders within a percentage range below `maxPrice`.

3. Place two additional, larger buy orders at deeper percentage drops (`semifinal`, `final`).

4. Calculate the average entry price as orders fill.

5. Exit the entire position for a small take profit (`tp`) above the average entry price.

6. Offer a conditional ATR trailing stop if only the first order fills.

7. Provide extensive visual feedback through lines, labels, icons, and detailed information tables/UI elements.

Keep in mind that grid strategies can perform well in ranging or slowly trending markets but can incur significant drawdowns if the price trends strongly against the position without sufficient retracements to hit the take profit. The leverage (`lev`) input significantly amplifies both potential profits and losses.