Previous Quarterly, Monthly, Weekly, Daily Candle Open, Close.This script marks the Previous Quarterly, Monthly, Weekly, and Daily Candle Open and Closes. Colors can be changed as needed.

ابحث في النصوص البرمجية عن "weekly"

Custom Time ranges. Daily price ranges.Addition to previous time range script, now containing daily ranges. You can select a day of the week, and have it show the high, low, mid, and open of that day.

For the time bands:

Monday = 2

Tuesday = 3

Wednesday = 4

Thursday = 5

Friday = 6

Saturday = 7

Sunday = 1

Example 1:

1500-1800:2

This will colour the background between 3pm and 6pm on Mondays.

Example 2:

0000-0600:247

This will colour the background between midnight and 6am on Mondays, Wednesdays, and Saturdays.

For the Daily price ranges:

Just select the tick-box forthe day, and then the price levels you'd like to see.

I want to add specific weekly levels to this, for example: week 06 of year 2020, but I've not figured out how to do it yet. If anyone knows, I'd appreciate it if you let me know. I'll then update this script.

As always, any questions you may have, please leave in comments below and I'll respond when I have time.

If you notice anything good with this indicator, let me know. We are all in this to make money after all! ;)

MultiTimeFrame Fractals D W M [xdecow]This indicator shows fractals in different timeframes. With the possibility of coloring the bars with any combination of current, daily, weekly and monthly timeframes.

The return points are calculated as follows:

high > last 3 highs and close above highest low

low < last 3 lows and closes below lowest high

The direction of higher timeframes fractals tend to be more durable and reliable. This indicator helps to find the fractal alignment of different timeframes, so that you can look for trade opportunities in the same direction as the higher timeframes and improve your chances.

Moving Average ChannelIntended for use on BTC long term (BNC:BLX Weekly) with Logarithmic charts only

As Bitcoin is adopted, it moves through market cycles. These are created by periods where market participants are over-excited causing the price to over-extend, and periods where they are overly pessimistic where the price over-contracts. Identifying and understanding these periods can be beneficial to the long term investor. This long term investment tool is a simple and effective way to highlight those periods.

Buying Bitcoin when the price drops below the green line has historically generated outsized returns. Selling Bitcoin when price goes above the red line has been historically effective for taking profits.

NOTE: 144 Week = 2¾ Years. 104 Weeks = 2 Years. Originally created by Philip Swift

camarilla - Daily,Weekly,Monthly by Ganeshcamarilla - Daily,Weekly,Monthly levels in one chart for support and resitance

14-RSI minus 36-MFI (weekly)On the weekly chart of BTC/USD, the difference between the 14-RSI and the 36-MFI, combined with the 14-RSI alone, gives good buy and sell signals.

sma 50 100 200 multi Timframes actual daily weekly monthlysma 50-100-200

Just 3 sma from actual,daily,weekly and monthly timeframe

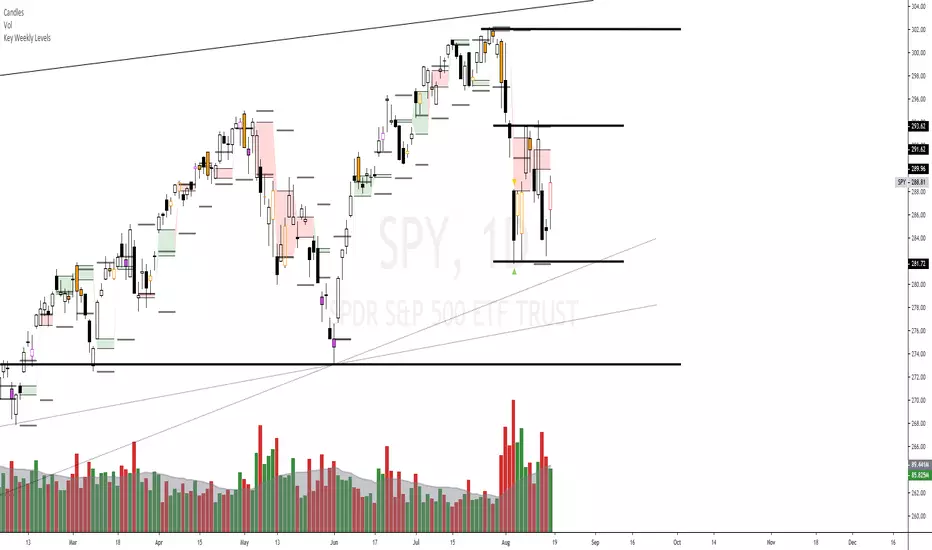

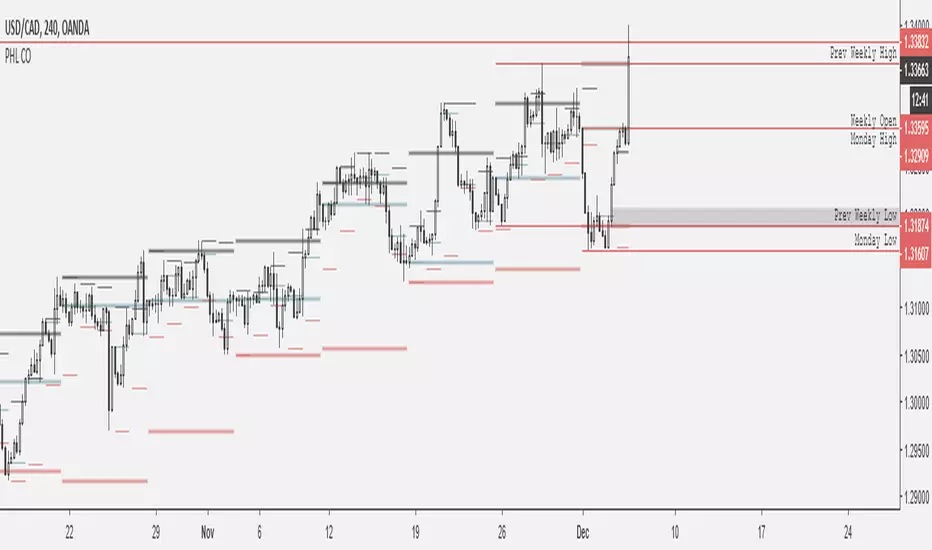

Key Weekly LevelsIncluded is the current weekly open, previous high, Low, Close, and the gap is highlighted.

Ema Weekly In current TimeframeThis simple indicator shows the Ema with data extracted from weekly timeframe in your current displayed timeframe.

Due to Tradingview working restrictions, this indicator only works if is used in a timeframe lower (or equal) to one week, otherways shows an error red label showing this error.

All my scripts:

es.tradingview.com

TKP Weekly, Monthly and Yearly Fib Pivot PointsThis script allows you to plot Weekly, Monthly and Yearly Fibonacci Pivot Points. I used templates from others I found on TradingView, special thanks given in the Script. I prefer Longer time frames, especially yearly Pivots, to predict reversals and places to trim risk, so this was tailored to my needs. Hope this helps!

Close of relevant previous periodThis indicator puts the previous close value of a higher relevant time frame on the chart, it adepts to the period of the chart. Relevant means that it puts:

Close of previous year in monthly chart

Close of previous month in weekly chart

Close of either previous month of week in daily chart, default setting is week

Close of previous week in 4hourly and 3hourly charts

Close of previous day in 30minute and higher intraday charts

Not bother the user below 30 minutes.

Pivots Daily Weekly Monthly YearlyDaily, Weekly, Monthly and yearly pivot lines

Just the pivot lines without the support and resistance lines

Eminaest Pivots V2Simple Pivot Points plotting script.

You can choose to plot Daily, Weekly and Monthly Pivot Points. Separate or two of them or all together.