Support & Resistance ZonesTitle: A Comprehensive Guide to the Support & Resistance Zones Indicator

Introduction

In the world of technical analysis, the Support & Resistance Zones indicator plays a crucial role in identifying potential trading opportunities. These zones are essential for traders looking to capitalize on bounces or break and retests. In this article, we will delve into the specifics of the Support & Resistance Zones indicator, outlining how it works, how it finds and marks zones, and the various options available for traders.

What the indicator is about

The Support & Resistance Zones indicator, developed by @HarryCTC, is a powerful tool for detecting areas of potential price reversal or consolidation in a financial market. These zones are significant as they can act as a guide for traders to make informed decisions on entering or exiting positions. Specifically, the indicator helps identify:

1. Support Zones: Areas where the price has a tendency to bounce back up after falling, indicating a potential buying opportunity.

2. Resistance Zones: Areas where the price has a tendency to reverse after rising, indicating a potential selling opportunity.

How the indicator finds its zones

The Support & Resistance Zones indicator utilizes pivot points to identify potential support and resistance levels. By analyzing the fractal structure of the price chart, the indicator identifies key turning points, known as bull and bear fractals. The bull fractal is a high pivot point, while the bear fractal is a low pivot point.

The fractal structure is determined by the 'Switch Zone Period' input, which can be adjusted to suit the trader's preferences. A higher value will result in fewer zones being identified, while a lower value will result in more zones.

How it marks zones and why it marks zones

The indicator marks the support and resistance zones by creating rectangular boxes around the identified fractal points. The zones are extended horizontally from the fractal point, allowing traders to visualize the potential areas of price reversal.

The zones are marked for the following reasons:

1. To provide a clear visual representation of potential support and resistance levels.

2. To help traders identify potential entry and exit points based on the price's reaction to these zones.

3. To serve as a reference for stop-loss and take-profit levels when planning trades.

The indicator's for traders trading bounces or break and retests

Traders who focus on trading bounces or break and retests can benefit immensely from the Support & Resistance Zones indicator. By providing a visual representation of key support and resistance levels, the indicator enables traders to:

1. Identify potential buying opportunities at support zones where the price is likely to bounce back up.

2. Identify potential selling opportunities at resistance zones where the price is likely to reverse after rising.

3. Make informed decisions on stop-loss and take-profit levels based on the price's proximity to support and resistance zones.

4. Monitor the market for potential breakouts or breakdowns when the price breaches these zones.

Indicator options

The Support & Resistance Zones indicator offers several customizable options to suit the trader's preferences. These options include:

1. Switch Zone Period: Adjusts the number of periods used to calculate the fractal structure, influencing the number of identified zones.

2. No. of Displayed Zones: Determines the maximum number of zones displayed on the chart, ranging from 1 to 8.

3. Zone Extension: Adjusts the horizontal extension of the support and resistance zones.

4. Resistance Zone Color: Customizes the color of the resistance zone boxes.

5. Support Zone Color: Customizes the color of the support zone boxes.

6. Zone Border Color: Customizes the color of the zone box borders.

Conclusion

The Support & Resistance Zones indicator is a valuable tool for traders looking to identify potential trading opportunities based on the price's interaction with support and resistance levels. By providing a clear visual representation of these zones, the

indicator allows traders to make informed decisions on entry and exit points, stop-loss, and take-profit levels. With customizable options, the indicator can be tailored to suit individual trading preferences and strategies.

ابحث في النصوص البرمجية عن "zone"

Supply Demand Zones ProSupply Demand Zones PRO

Version: 1.0

Built with: Pine Script v6

________________________________________

🧭 HOW TO USE Start Here

🧠 What it does default behavior

• ✅ Automatically identifies Supply & Demand zones on your chart

• ✅ Automatically ranks each zone from 0 to 10 higher = stronger

• ✅ Works across most TradingView symbols and timeframes with default settings

⚙️ Default settings recommended for most instruments

Use the default settings for:

• 💱 Forex

• 🪙 Crypto

• 📊 Indices

• 🛢️ Commodities

• 🏛️ Stocks

Defaults are tuned to provide a balanced mix of quality zones + clean charts.

🎯 How to trade with it high-level workflow

1. 🥇 Prioritize strong zones

o Focus on higher scores commonly 7–10 for best reversal potential.

2. 🔄 Wait for a reversal setup at the zone

o Example triggers: rejection wick, engulfing candle, strong reaction candle, structure shift.

3. ✅ Confirm with other indicators before entering

o Use confirmation tools (your choice), such as:

📈 Trend filter (MA / market structure)

🧪 Momentum (RSI / Stoch / MACD)

📉 Volume / volatility tools

o Then take BUY from demand or SELL from supply *only when confirmation aligns

🧩🖤 Executive Summary: PRO Features Overview

The Supply Demand Zones PRO indicator is a professional-grade tool built on the latest Pine Script v6, designed to automatically identify and score high-probability supply and demand zones.

It moves beyond simple zone plotting by incorporating a suite of advanced features that provide a deeper, more actionable market context. This helps traders filter out noise, focus on significant levels, and make more informed decisions.

The indicator is universally compatible and works seamlessly across all major asset classes and timeframes:

• Forex: EURUSD, GBPUSD, USDJPY

• Commodities: Gold/XAUUSD, Silver, Oil

• Indices: NQ, ES, DAX, FTSE

• Cryptocurrencies: Bitcoin, Ethereum, Altcoins

• Stocks: Individual equities

Most symbols available on TradingView are fully supported.

Notice on repainting 🕯️⬛

Active zones won’t repaint unless they are invalidated. Gray/Historic zones may repaint, and that’s fine—this script only displays the most recent and stronger historic zones (if historic zones are enabled).

________________________________________

⬛🛠️Key PRO Features Overview

⚙️ Feature 📌 Description

Zone Strength Ranking ||| Each zone is dynamically scored from 1–10 based on its age and number of retests. Fresher, less-tested zones are stronger, helping prioritize high-impact levels.

Real-Time Distance ||| Each active zone’s info label shows the exact distance (in pips) from current price to the zone edge for quick risk/opportunity assessment.

Trading Session Tracking ||| Zones are tagged by formation session (Asian / London / New York) for added context—high-volume session zones often matter more.

Automated Retest Markers ||| The script tracks retests and places an “R” marker for each retest, giving a clear visual history of price interaction.

Advanced ATR Filtering ||| Volatility-based filters control zone quality: set min/max zone height and optionally enforce a consistent zone height using ATR.

Minimum Zone Distance ||| Reduces clutter by requiring a minimum number of bars between new zones, ensuring zones are distinct and well-separated.

Dual Label Controls Independently toggle info labels for Active vs Historic zones to keep charts clean while preserving key detail.

Built on Pine Script v6 ||| Uses the newest Pine Script version for better efficiency, reliability, and smoother handling of complex logic/drawings.

________________________________________

Detailed Feature Breakdown ⬛

Zone Strength Ranking ⬛

The strength score is a proprietary calculation that helps traders instantly gauge the potential of a supply or demand zone. It is calculated in real time using:

1. Age of the Zone: As zones age, they may lose relevance. Strength decreases as the number of bars since creation increases.

2. Number of Retests: The first test is often the highest-probability reaction. Each retest reduces strength as liquidity is absorbed.

✅ A high score (7/10+) indicates a fresh, less-tested zone that may produce a strong reaction.

⚠️ A low score suggests a zone is old and/or heavily tested—use extra caution.

________________________________________

🧱⬛Invalidation & Historic Zones

A zone becomes invalidated broken when price closes beyond its outer boundary or wicks beyond it, depending on settings. Once broken, it becomes a Historic Zone and turns gray.

This matters for structure: a broken supply zone can become future demand a flip zone, and vice versa.

________________________________________

🧪⬛Advanced Filtering Explained

Three ATR-based filters control zone quality:

• Max Zone Height (ATR Multiplier): Blocks zones that are too large to trade effectively. Example: 1.0 ignores zones taller than 1× ATR.

• Min Zone Height (ATR Multiplier): Filters out zones that are too thin and likely noise. Example: 1.0 rejects zones smaller than 1× ATR.

• Force Zone Height (ATR Multiplier): Normalizes zone heights by expanding smaller valid zones up to the minimum ATR target. Example: 1.0 expands zones to at least 1× ATR.

________________________________________

🧾⬛Configuration Guide

⚙️⬛Zone Detection

⚙️ Setting 🔧 Default 📝 Description

Swing Length (Sensitivity) 12 Lookback bars for pivot high/low detection. Higher = fewer, stronger zones.

Max Zones to Display 10 Max number of active Supply + Demand zones shown.

Max Zone Height (ATR) 1.0 Rejects zones taller than this ATR multiplier.

Min Zone Height (ATR) 1.0 Rejects zones smaller than this ATR multiplier.

Force Zone Height (ATR) 1.0 Expands valid zones to be at least this ATR multiplier.

Min Distance Between Zones 44 Minimum bars required between consecutive zones of the same type.

________________________________________

🧱⬛Zone Settings

⚙️ Setting 🔧 Default 📝 Description

Zone Invalidation Close “Close” = candle must close past zone; “Wick” = wick past zone breaks it.

Show Historic Zones On Toggles visibility of broken (historic) zones.

Active Zones Lookback 1000 Hides active zones older than this many bars.

Historic Zones Lookback 1000 Hides historic zones older than this many bars.

________________________________________

🖥️⬛Display

⚙️ Setting 🔧 Default 📝 Description

Show Active Zone Info On Toggles text labels for active (unbroken) zones.

Show Historic Zone Info Off Toggles text labels for historic (broken) zones.

Label Size Small Adjusts the font size of zone info labels.

Interest ZonesThis indicator automatically identifies and plots "Interest Zones" around significant pivot highs and lows, representing potential areas of institutional interest, support/resistance, or accumulation/distribution. Zones are dynamically merged when pivots cluster near the same price level and extended for visibility.

How It Works (Technical Methodology)

Pivot Point Detection

The indicator uses Pine Script's ta.pivothigh() and ta.pivotlow() with asymmetric left/right lengths (default left=20, right=13) to detect swing highs and lows. This allows for customizable sensitivity – longer left for stronger confirmation, shorter right for faster detection.

Zone Start Condition (Filtering)

Multiple modes control from which point in history zones begin to be drawn:

"None": All historical pivots (limited by max zones).

"Auto (Start of Day)": Zones only from the beginning of the current trading day (resets daily).

"Manual Date": User-defined fixed date.

"Interactive (Chart)": User-confirmed date via input (useful for backtesting specific periods).

"Last X Bars": Only pivots within the last user-defined number of bars (default 400).

A vertical line marks the start point in date-based modes for visual reference.

Zone Construction

For each valid pivot:

Zone thickness is based on ATR(14) × user-defined multiplier (default 0.3) for dynamic, volatility-adjusted height.

Pivot High zones: Centered below the high (potential supply/resistance).

Pivot Low zones: Centered above the low (potential demand/support).

Zones are drawn as boxes extending to the right, with gray fill and border.

Merge & Overlap Logic

When a new pivot falls inside an existing zone or is very close (within user-defined "Proximity Sensitivity %" of the zone's midpoint, default 1.1%):

The new pivot is merged into the existing zone.

A counter ("x2", "x3", etc.) is displayed on the zone, indicating how many pivots have clustered there.

The zone is strengthened visually (counter text) and extended further right.

This highlights high-interest levels where price repeatedly reversed.

Zone Management

In "None" mode: Only the most recent user-defined max zones are kept (default 5) – oldest deleted automatically.

In other modes: Up to ~490 zones (performance limit), oldest pruned if exceeded.

All zones auto-extend to the right on the last bar for continuous visibility.

Visual Elements

Uniform gray color for all zones (configurable).

Transparent background fill (adjustable).

Counter text in white (configurable) when zones have multiple touches.

Clean, non-directional design – focuses purely on clustered reversal points.

How to Use

Interest Zones highlight price levels where the market has shown repeated respect through multiple swing pivots – often coinciding with institutional order clusters, psychological levels, or hidden support/resistance.

Higher counter values ("x3+", "x5+"): Stronger zones – higher probability of reaction on retest.

Use for:

Potential reversal or bounce areas when price approaches a zone.

Confluence with other tools (order blocks, FVG, volume profile, etc.).

Stop-loss placement beyond zones or take-profit at opposite zones.

Daily reset ("Auto Start of Day"): Ideal for intraday trading – fresh zones each session.

Backtesting: Use "Manual" or "Interactive" date modes to analyze specific historical periods.

"Last X Bars": Good for medium-term swing analysis without full history clutter.

Adjust ATR multiplier for tighter (lower) or wider (higher) zones based on asset volatility. Increase proximity sensitivity for more aggressive merging in ranging markets.

Combine with trend direction, volume, or higher-timeframe structure for best results.

Disclaimer

This indicator is a technical analysis tool and should be used in conjunction with other forms of analysis. Past performance does not guarantee future results. Always use proper risk management.

High Volume Zones with Signals – HVZ█ OVERVIEW

"High Volume Zones with Signals – HVZ" is a technical analysis indicator that identifies High Volume Zones (HVZ) on the chart and draws them as fully customizable boxes. Perfect for traders using price action, ICT, and Smart Money Concepts. The indicator highlights key volume-based support/resistance levels, detects potential consolidation zones (very large candles), and generates precise breakout and exit signals. Flexible volume filters, ATR filter, and visual styling options ensure a clean and highly effective chart.

█ CONCEPTS

The indicator detects candles with volume significantly above the average (default ≥ 2× SMA of volume over 20 periods). Such candles often signal institutional activity and create strong supply/demand zones.

The ATR filter additionally identifies very large candles – frequently a sign of market capitulation (panic buying/selling). Within the range of such a candle, prolonged consolidation often occurs, especially on higher timeframes (e.g., 4H and above).

Why are HVZ important? High-volume zones are areas where the market has left a large number of orders – institutions return there to “refresh” liquidity before the next move. A breakout against the zone’s character triggers a Break signal:

- Bullish HVZ broken downward (close below the lower boundary) → Break Down (sell),

- Bearish HVZ broken upward (close above the upper boundary) → Break Up (buy).

Note: The indicator requires real exchange volume – it will not work correctly on instruments without reported volume (e.g., certain CFDs or forex).

█ FEATURES

- HVZ Detection: Automatic identification of high-volume zones with Volume SMA Length and Volume Multiplier filters; historical initialization up to 500 candles back.

- ATR Filter: Optional detection of very large candles (potential consolidation/capitulation) using - ATR Length and ATR Multiplier; three action modes:

Skip Zone – large candle creates no zone,

Separate Color – zone is drawn in a distinct style (gray by default),

Normal Zone – treated like a regular HVZ.

- Gray zones (large candles, Separate Color): generate exactly the same Break signals as regular zones – based solely on the original candle direction (bullish → Break Down on lower break, bearish → Break Up on upper break). Gray color is only a visual marker for potential consolidation/capitulation zones.

- Customizable Boxes: Separate styles for bullish and bearish zones (border color, background gradient, line thickness and style); adjustable background and 50 % midline transparency.

- Break & Exit Signals:

Break Up/Down – green/red triangle after a candle closes outside the zone (zone disappears, triangle remains as a trace).

Exit Up/Down – green/red circle when price leaves the zone without a full breakout.

Signal Type option: Break, Exit, or Both.

- Midline: Automatic dashed line at the 50 % zone level with independent transparency control.

- Chart Cleanup: Automatic removal of inactive zones older than 500 candles (max_boxes_count=500).

- Alerts: Built-in alerts for Break Up and Break Down with clear messages.

█ HOW TO USE

Add to Chart: Paste the script in Pine Editor or find it in TradingView’s indicator library.

Configure Settings:

- Volume Filter: Volume SMA Length (default 20) and Volume Multiplier (default 2.0) – higher multiplier = fewer but stronger zones.

- ATR Filter: Enable/disable, set ATR Length (14) and ATR Multiplier (3.5); choose action for very large candles (Skip Zone / Separate Color / Normal Zone).

- Box Style: Background transparency (90) and midline transparency (70).

- Bull/Bear Box Style: Border and gradient colors, line thickness (1-5).

- ATR Style: Separate colors for large-candle zones (gray by default).

- Signal Settings: Choose Signal Type (Break/Exit/Both) and signal colors.

Signal Interpretation:

- Break Up (green triangle below bar): Bearish HVZ broken upward → buy signal, continuation of uptrend.

- Break Down (red triangle above bar): Bullish HVZ broken downward → sell signal, continuation of downtrend.

- Exit Up/Down (circles): Price leaves zone without breakout – may signal end of correction or reversal setup.

- HVZ Zones: Price often returns to high-volume zones to clear orders. An unfilled zone remains a price magnet.

- 50 % Level (midline): Ideal target for partial take-profit or reaction point inside the zone.

Combine signals with other tools (e.g., RSI, MACD, higher timeframes) for higher confidence.

█ APPLICATIONS

- Price Action & ICT: HVZ act as dynamic S/R; in an uptrend look for buys after breaking a bearish HVZ, in a downtrend look for sells after breaking a bullish HVZ. If you trade retests instead of breakouts, increase Volume Multiplier to 2.5-3.0 – fewer zones but much stronger. Note that after breaking a very strong zone, price often pulls back deeply before continuing.

- Breakout Strategies: For maximum Break signals, lower Volume Multiplier to 1.5-1.8 – gives many high-quality entries in trending markets. Always trade in the direction of the prevailing trend (e.g., only longs in uptrends). Enter after a Break signal with confirmation from volume or momentum (MACD above zero, RSI >50 for longs, <50 for shorts).

█ NOTES

- The indicator requires real exchange volume – it will not function properly on instruments without reported volume (e.g., certain CFDs, forex).

- Always confirm signals with additional context (market structure, higher timeframe).

Quantura - Supply & Demand Zone DetectionIntroduction

“Quantura – Supply & Demand Zone Detection” is an advanced indicator designed to automatically detect and visualize institutional supply and demand zones, as well as breaker blocks, directly on the chart. The tool helps traders identify key areas of market imbalance and potential reversal or continuation zones, based on price structure, volume, and ATR dynamics.

Originality & Value

This indicator provides a unique and adaptive method of zone detection that goes beyond simple pivot or candle-based logic. It merges multiple layers of confirmation—volume sensitivity, ATR filters, and swing structure—while dynamically tracking how zones evolve as the market progresses. Unlike traditional supply and demand indicators, this script also detects and plots Breaker Zones when previous imbalances are violated, giving traders an extra layer of market context.

The key values of this tool include:

Automated detection of high-probability supply and demand zones.

Integration of both volume and ATR filters for precision and adaptability.

Dynamic zone merging and updating based on price evolution.

Identification of breaker blocks (invalidated zones) to visualize market structure shifts.

Optional bullish and bearish trade signals when zones are retested.

Clear, visually optimized plotting for efficient chart interpretation.

Functionality & Core Logic

The indicator continuously scans recent price data for swing highs/lows and combines them with optional volume and ATR conditions to validate potential zones.

Demand Zones are formed when price action indicates accumulation or a strong bullish rejection from a low area.

Supply Zones are created when distribution or strong bearish rejection occurs near local highs.

Breaker Blocks appear when existing zones are invalidated by price, helping traders visualize potential market structure shifts.

Bullish and bearish signals appear when price re-enters an active zone or breaks through a breaker block.

Parameters & Customization

Demand Zones / Supply Zones: Enable or disable each individually.

Breaker Zones: Activate breaker block detection for invalidated zones.

Volume Filter: Optional filter to only confirm zones when volume exceeds its long-term average by a user-defined multiplier.

ATR Filter: Optional filter for volatility confirmation, ensuring zones form under strong momentum conditions.

Swing Length: Controls the number of bars used to detect structural pivots.

Sensitivity Controls: Adjustable ATR and volume multipliers to fine-tune detection responsiveness.

Signals: Toggle for on-chart bullish (▲) and bearish (▼) signal plotting when price interacts with zones.

Color Customization: User-defined bullish and bearish colors for both standard and breaker zones.

Core Calculations

Zones are detected using pivot highs and lows with a defined lookback and lookahead period.

Additional filters apply if ATR and volume are enabled, requiring conditions like “ATR > average * multiplier” and “Volume > average * multiplier.”

Detected zones are merged if overlapping, keeping the chart clean and logical.

When price breaks through a zone, the original box is closed, and a new breaker zone is plotted automatically.

Bullish and bearish markers appear when zones are retested from the opposite side.

Visualization & Display

Demand zones are shaded in semi-transparent bullish color (default: blue).

Supply zones are shaded in semi-transparent bearish color (default: red).

Breaker zones appear when previous imbalances are broken, helping to spot structural shifts.

Optional arrows (▲ / ▼) indicate potential buy or sell reactions on zone interaction.

Use Cases

Identify institutional areas of accumulation (demand) or distribution (supply).

Detect potential breakout traps and market structure shifts using breaker zones.

Combine with other tools such as volume profile, EMA, or liquidity indicators for deeper confirmation.

Observe retests and reactions of zones to anticipate possible reversals or continuations.

Apply multi-timeframe analysis to align higher timeframe zones with lower timeframe entries.

Limitations & Recommendations

The indicator does not predict future price movement; it highlights structural imbalances only.

Performance depends on chosen swing length and sensitivity—users should optimize parameters for each market.

Works best in volatile markets where supply and demand imbalances are clearly expressed.

Should be used as part of a broader trading framework, not as a standalone signal generator.

Markets & Timeframes

The “Quantura – Supply & Demand Zone Detection” indicator is suitable for all asset classes including cryptocurrencies, Forex, indices, commodities, and equities. It performs reliably across multiple timeframes, from intraday scalping to higher timeframe swing analysis.

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Important

This description complies with TradingView’s Script Publishing and House Rules. It clearly explains the indicator’s originality, underlying logic, functionality, and intended use without unrealistic claims or performance guarantees.

Adaptive Pivot Zones█ OVERVIEW

The "Adaptive Pivot Zones" indicator is a versatile tool designed to identify and visualize key pivot levels directly on the price chart. By detecting pivot highs and lows, the indicator calculates dynamic support and resistance zones based on user-defined levels (default: 0.382, 0.5, 0.618). These zones adapt to market volatility, providing traders with clear visual cues for potential reversal or continuation points. The indicator offers extensive customization options, such as adjusting colors, smoothing lines, and setting fill transparency, making it highly adaptable to various trading styles.

█ CONCEPTS

The "Adaptive Pivot Zones" indicator simplifies the identification of significant price levels by plotting three dynamic pivot lines, which can be smoothed to reduce market noise. The indicator dynamically changes the colors of the lines and fill zones based on price action, using bullish, bearish, or neutral colors to reflect market sentiment.

█ CALCULATIONS

The indicator relies on the following calculations:

- Pivot Detection: Pivot highs (ta.pivothigh) and pivot lows (ta.pivotlow) are identified using a user-defined pivot length (default: 10). Pivots represent significant price peaks and troughs. Higher pivot length values produce more stable levels but introduce a delay equal to the set value. For more aggressive strategies, the pivot length can be reduced.

- Pivot Levels: When both a pivot high and low are detected, the range between them is calculated (rng = drHigh - drLow). Three pivot levels are computed as:

Line 1: drLow + rng * pivotLevel1

Line 2: drLow + rng * pivotLevel2

Line 3: drLow + rng * pivotLevel3

- Smoothing: Pivot lines can be smoothed using a simple moving average (SMA) with a user-defined smoothing length (default: 1) to reduce noise and improve readability.

- Color Logic: Lines and fill zones are colored based on the price position relative to the pivot zones:

If the price is below the lowest pivot line, a bearish color is used (default: red).

If the price is above the highest pivot line, a bullish color is used (default: green).

If the price is within the pivot zones and the neutral color option is enabled, a neutral color is used (default: gray); otherwise, the previous color is retained.

- Fill Zones: The areas between pivot lines are filled with a user-defined transparency level (default: 80) to visually highlight support and resistance zones.

█ INDICATOR FEATURES

- Dynamic Pivot Lines: Three adaptive pivot lines (default levels: 0.382, 0.5, 0.618) are plotted on the price chart, adjusting to market volatility.

- Smoothing: User-defined smoothing length (default: 1) for pivot lines to reduce noise and enhance signal clarity.

- Dynamic Coloring: Lines and fill zones change color based on price action (bullish, bearish, or neutral when the price moves within the zone), reflecting market sentiment.

- Fill Zones: Transparent fills between pivot lines to visually highlight support and resistance zones.

- Customization: Options to adjust pivot length, pivot levels, smoothing, colors, transparency, and enable/disable neutral color logic.

█ HOW TO SET UP THE INDICATOR

- Add the "Adaptive Pivot Zones" indicator to your TradingView chart.

- Configure parameters in the settings, such as pivot length, pivot levels, smoothing length, and colors, to align with your trading strategy. Without smoothing, lines behave like levels; with smoothing, they act like bands. All three levels can be set to the same value to obtain a single level or a line behaving like a moving average derived from pivots.

- Enable or disable the neutral color option (for prices moving within the zone) and adjust fill transparency for optimal visualization.

- Adjust line thickness and style in the "Style" section to improve chart readability.

Example of bands – lines behave like support/resistance zones.

Example of a moving average derived from pivots – line behaves like a pivot-based MA.

█ HOW TO USE

Add the indicator to your chart, adjust the settings, and observe price interactions with the pivot lines and zones to identify potential trading opportunities. Key signals include:

- Price Interaction with Pivot Lines: When the price approaches or crosses a pivot line, it may indicate a potential support or resistance level. A bounce from a pivot line could signal a reversal, while a breakout might suggest trend continuation.

- Zone-Based Signals and Trend Line Usage: Price movement within or outside the filled zones can indicate market sentiment. Price below the lowest pivot line suggests bearish momentum, price above the highest pivot line suggests bullish momentum, and price within the zones may indicate consolidation. With higher pivot length values, the indicator can be used as a trend line, particularly during clear market movements.

- Color Changes: Shifts in line and fill colors (bullish, bearish, or neutral) provide visual cues about changing market conditions.

- Confirmation with Other Tools: Combine the indicator with tools like RSI or Bollinger Bands to validate signals and improve trade accuracy. For example, a buy signal from RSI in the oversold zone combined with a bounce from the lowest pivot line may indicate a strong entry point.

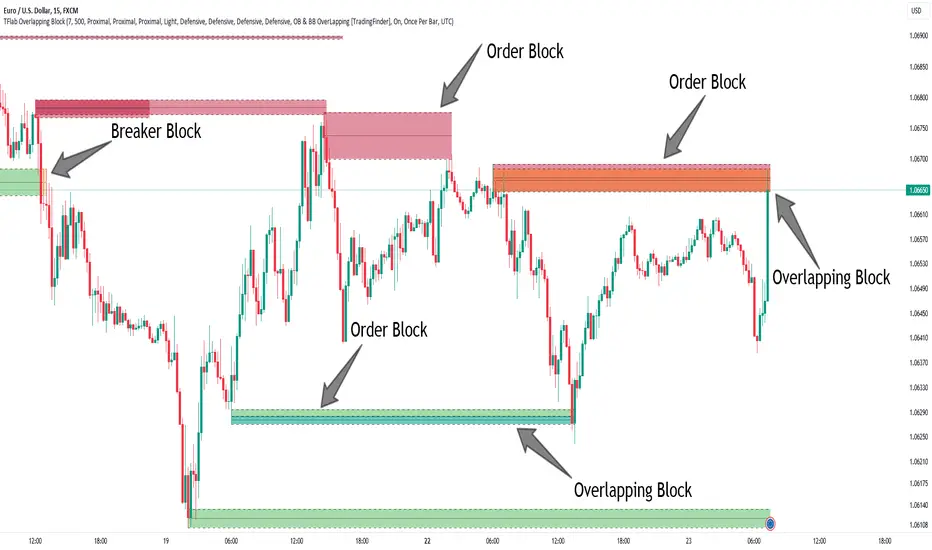

Breaker Blocks + Order Blocks confirm [TradingFinder] BBOB Alert🔵 Introduction

In the realm of technical analysis, various tools and concepts are employed to identify key levels on price charts. These tools assist traders in analyzing market trends with greater precision, enabling them to optimize their trading decisions. Among these tools, the Order Block and Breaker Block hold a significant place, serving as effective instruments for analyzing market structure.

🟣 Order Block

An Order Block refers to zones on a chart where large financial institutions and high-volume traders place their orders. Due to the substantial volume of buy or sell orders in these areas, they are often regarded as pivotal points for potential price reversals or temporary pauses in a trend. Order Blocks are particularly crucial when prices react to these zones after a strong market move, acting as strong support or resistance levels.

🟣 Breaker Block

On the other hand, a Breaker Block refers to areas on a chart that previously functioned as Order Blocks but where the price has managed to break through and continue in the opposite direction. These zones are typically recognized as key points where market trends might shift, helping traders identify potential reversal points in the market.

🟣 Overlapping Block (BBOB)

Now, imagine a scenario where these two essential concepts in technical analysis—Order Blocks and Breaker Blocks—overlap on a chart. Although this overlap is not specifically discussed within the ICT (Inner Circle Trader) trading framework, exploring and utilizing this overlap can provide traders with powerful insights into strong support and resistance zones. The combination of these two robust concepts can highlight critical areas in trading, potentially offering significant advantages in making informed trading decisions.

In this article, we will delve into the concept of this overlap, explaining how to utilize it in trading strategies. Additionally, we will analyze the potential outcomes and benefits of incorporating this concept into your trading decisions.

Bullish Overlapping Block (BBOB) :

Bearish Overlapping Block (BBOB) :

🔵 How to Use

The overlap between Order Blocks and Breaker Blocks is a compelling and powerful concept that can help traders identify key levels on the chart with a high probability of success. This overlap is particularly valuable because it combines two well-regarded concepts in technical analysis—zones of high order volume and critical market shifts.

🟣 Here’s how to effectively use this overlap in your trading

1. Dentifying the Overlapping Block : To make the most of the overlap between Order Blocks and Breaker Blocks, begin by identifying these zones separately. Order Blocks are areas where price typically reacts and reverses after a strong market move.

Breaker Blocks are areas where a previous Order Block has been breached, and the price continues in the opposite direction. When these two zones overlap on a chart, it’s crucial to pay close attention to this area, as it represents a high-probability reaction zone.

2. Analyzing the Overlapping Block : After identifying the overlap zone, carefully analyze price action within this region. Candlestick patterns and price behavior can provide essential clues.

If the price reaches this overlap zone and strong reversal patterns such as Pin Bars or Engulfing patterns are observed, it’s likely that this zone will act as a pivotal reversal point. In such cases, entering a trade with confidence becomes more feasible.

3. Entering the Trade : When sufficient signs of price reaction are present in the overlap zone, you can proceed to enter the trade. If the overlap zone is within an uptrend and bullish reversal signals are evident, a long position might be appropriate.

Conversely, if the overlap zone is in a downtrend and bearish reversal signals are observed, a short position would be more suitable.

4. Risk Management : One of the most critical aspects of trading in overlap zones is managing risk. To protect your capital, place your stop loss near the lowest point of the Order Block (for buy trades) or the highest point (for sell trades). This approach minimizes potential losses if the overlap zone fails to hold.

5. Price Targets : After entering the trade, set your price targets based on other key levels on the chart. These targets could include other support and resistance zones, Fibonacci levels, or pivot points.

Bullish Overlapping Block :

Bearish Overlapping Block :

🟣 Benefits of the Overlapping Block Between Order Block and Breaker Block

1. Enhanced Precision in Identifying Key Levels : The overlap between these two zones usually acts as a highly reliable area for price reactions, increasing the accuracy of identifying entry and exit points.

2. Reduced Trading Risk : Given the high importance of the overlap zone, the likelihood of making incorrect decisions is reduced, contributing to overall lower trading risk.

3. Increased Probability of Success : The overlap between Order Blocks and Breaker Blocks combines two powerful concepts, enhancing the likelihood of success in trades, as multiple indicators confirm the importance of the area.

4. Creation of Better Trading Opportunities : Overlap zones often provide traders with more robust trading opportunities, as these areas typically represent strong reversal points in the market.

5. Compatibility with Other Technical Tools : This concept seamlessly integrates with other technical analysis tools such as Fibonacci retracements, trend lines, and chart patterns, offering a more comprehensive market analysis.

🔵 Setting

🟣 Global Setting

Pivot Period of Order Blocks Detector : Enter the desired pivot period to identify the Order Block.

Order Block Validity Period (Bar) : You can specify the maximum time the Order Block remains valid based on the number of candles from the origin.

Mitigation Level Order Block : Determining the basic level of a Order Block. When the price hits the basic level, the Order Block due to mitigation.

Mitigation Level Breaker Block : Determining the basic level of a Breaker Block. When the price hits the basic level, the Breaker Block due to mitigation.

Mitigation Level Overlapping Block : Determining the basic level of a Overlapping Block. When the price hits the basic level, the Overlapping Block due to mitigation.

🟣 Overlapping Block Display

Show All Overlapping Block : If it is turned off, only the last Order Block will be displayed.

Demand Overlapping Block : Show or not show and specify color.

Supply Overlapping Block : Show or not show and specify color.

🟣 Order Block Display

Show All Order Block : If it is turned off, only the last Order Block will be displayed.

Demand Main Order Block : Show or not show and specify color.

Demand Sub (Propulsion & BoS Origin) Order Block : Show or not show and specify color.

Supply Main Order Block : Show or not show and specify color.

Supply Sub (Propulsion & BoS Origin) Order Block : Show or not show and specify color.

🟣 Breaker Block Display

Show All Breaker Block : If it is turned off, only the last Breaker Block will be displayed.

Demand Main Breaker Block : Show or not show and specify color.

Demand Sub (Propulsion & BoS Origin) Breaker Block : Show or not show and specify color.

Supply Main Breaker Block : Show or not show and specify color.

Supply Sub (Propulsion & BoS Origin) Breaker Block : Show or not show and specify color.

🟣 Order Block Refinement

Refine Order Blocks : Enable or disable the refinement feature. Mode selection.

🟣 Alert

Alert Name : The name of the alert you receive.

Alert Overlapping Block Mitigation :

On / Off

Message Frequency :

This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone :

The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

🔵 Conclusion

The overlap between Order Blocks and Breaker Blocks represents a critical and powerful area in technical analysis that can serve as an effective tool for determining entry and exit points in trading.

These zones, due to the combination of two key concepts in technical analysis, hold significant importance and can help traders make more confident trading decisions.

Although this concept is not specifically discussed in the ICT framework and is introduced as a new idea, traders can achieve better results in their trades through practice and testing.

Utilizing the overlap between Order Blocks and Breaker Blocks, in conjunction with other technical analysis tools, can significantly improve the chances of success in trading.

Best Buying & Selling Flip Zone @MaxMaserati 3.0Best Buying & Selling Flip Zone 3.0 🐂🐻

Best Buying & Selling Flip Zone 3.0 is an advanced, multi-timeframe Price Action tool designed to identify high-probability institutional supply and demand zones.

By analyzing candle range and body size (Expander vs. Normal candles), this indicator categorizes market structure shifts into three distinct tiers of strength (A+++, A++, A+). It includes a built-in Trade Manager, Volume Tracking, and a unique "Defender/Attacker" Multi-Timeframe (MTF) entry confirmation system.

🚀 Key Features

Multi-Timeframe Analysis: Monitor Higher Timeframe (HTF) zones while trading on a Lower Timeframe (LTF).

Tiered Setup Grading: Automatically classifies zones based on the strength of the candle engulfing action (King Slayer, Crusher, Drift).

Smart Entry Confirmation: The script can wait for price to tap an HTF zone and then automatically search for a confirmation pattern on the current timeframe before signaling a trade.

Built-in Trade Management: Visualizes Entry, Stop Loss (SL), and Take Profit (TP) levels with customizable Risk:Reward ratios.

Volume Tracking: Monitors the volume utilized to create a zone and tracks "remaining" volume as price tests the zone.

Zone Deletion Logic: Automatically removes zones that have been invalidated by either a wick or a candle close.

🧠 How It Works: The "A-Grade" Logic

The indicator analyzes candles based on their body-to-range ratio to define "Expander" (Explosive move) vs. "Normal" candles. It then looks for engulfing behaviors to create zones:

A+++ (King Slayer):

Logic: A Bullish Expander engulfs a Bearish Expander (or vice versa).

Significance: This is the strongest signal, indicating a massive shift in momentum where aggressive buyers completely overwhelmed aggressive sellers.

A++ (Crusher):

Logic: A Bullish Expander engulfs a Bearish Normal candle.

Significance: Strong momentum overcoming standard price action. High probability.

A+ (Drift):

Logic: A Bullish Normal candle engulfs a Bearish Normal candle.

Significance: A standard flip zone. Good for continuation plays but less aggressive than KS or CR setups.

🛠️ Functionality Guide

1. General Filters & Timeframes

Higher Timeframe: Select a timeframe higher than your chart (e.g., Select 4H while trading on 15m). The indicator will draw the major zones from the 4H.

Deletion Logic:

Wick (Hard): Zone is removed immediately if price touches the invalidation level.

Close (Soft): Zone is removed only if a candle closes past the invalidation level.

2. LTF Entry Confirmation (The "Master" Switch)

When Show LTF Entry Logic is enabled, the indicator does not signal immediately upon an HTF zone creation. Instead:

It waits for the price to retraced and touch the HTF zone.

Once touched, it scans the current timeframe for a valid flip setup (KS, CR, or DR).

It creates a tighter entry box and draws trade lines only when this confirmation occurs.

3. Trade Management

Risk:Reward: Set your desired RR (e.g., 2.0).

SL Padding: Add breathing room (ticks) to your Stop Loss.

SL Source: Choose between a safer Stop Loss (based on the HTF zone) or a tighter Stop Loss (based on the LTF confirmation candle).

4. Volume Stats

Labels display the volume involved in the zone's creation. As price taps the zone, the volume is "depleted" from the label, giving you insight into the remaining order flow absorption.

🎨 Visual Customization

Colors: Fully customizable colors for Buyers (Green) and Sellers (Red) zones across all three strength tiers.

Labels: Toggle technical names, touch counts, and timeframe labels.

Lines: Option to show "Aggressive Open Lines" to mark the exact opening price of the flip zone extended forward.

⚠️ Disclaimer

This tool is for educational purposes and chart analysis assistance only. Past performance of a setup (A+++/King Slayer) does not guarantee future results. Always manage risk and use this in conjunction with your own trading strategy.

Smart Money Zones (FVG + OB) + MTF Trend Panel## Overview

Professional-grade institutional trading zones indicator that identifies **Fair Value Gaps (FVG)** and **Order Blocks (OB)** - key price inefficiencies where smart money operates. Includes a comprehensive **Multi-Timeframe Trend Panel** for complete market context at a glance.

## Core Features

### 🎯 Fair Value Gaps (FVG)

Fair Value Gaps occur when price moves so aggressively that it leaves an "imbalance" or "gap" in the market structure. These zones often act as magnets where price returns to find liquidity.

**Detection Logic:**

- **Bullish FVG**: When current candle's low is above the high of the candle 2 bars ago

- **Bearish FVG**: When current candle's high is below the low of the candle 2 bars ago

- Requires strong impulse candle (configurable body percentage threshold)

- Color-coded zones: Green for bullish, Red for bearish

### 📦 Order Blocks (OB)

Order Blocks represent the last opposite candle before a significant price move - the zone where institutional orders were placed before the breakout.

**Detection Logic:**

- Identifies the last bearish candle before a strong bullish breakout (Bullish OB)

- Identifies the last bullish candle before a strong bearish breakout (Bearish OB)

- Validates breakout strength using ATR multiplier (1.2x default)

- Color-coded zones: Blue for bullish, Orange for bearish

### 📊 Multi-Timeframe Trend Panel

Real-time trend analysis across **7 timeframes** displayed in an elegant dashboard:

- **1 Minute** - Ultra short-term scalping

- **5 Minutes** - Short-term momentum

- **15 Minutes** - Intraday swings

- **30 Minutes** - Session trends

- **1 Hour** - Multi-session trends

- **4 Hours** - Daily structure

- **Daily** - Long-term direction

**Visual Indicators:**

- 🟢 Green circle = Bullish trend

- 🔴 Red circle = Bearish trend

- Clean, professional table design with customizable position and size

## Intelligence Features

### 🧠 Zone Strength Rating

Every zone is automatically classified by strength based on size relative to ATR:

- **VERY STRONG** - 2.0x ATR or more (major institutional zones)

- **STRONG** - 1.5x to 2.0x ATR (significant zones)

- **MEDIUM** - 1.0x to 1.5x ATR (moderate zones)

- **WEAK** - Below 1.0x ATR (minor zones)

Strength rating helps you prioritize which zones to trade from!

### 📉 Smart Mitigation Tracking

Zones automatically track how much they've been "filled" or mitigated:

- Calculates penetration percentage as price enters the zone

- Zones turn **gray** when 50%+ mitigated or fully filled

- Option to **auto-delete** mitigated zones to keep chart clean

- Live zones extend dynamically with price action

### 🎨 Trend Filter (Optional)

When enabled, only shows zones aligned with the current trend:

- Uses customizable MA period (default 50)

- Bullish zones only appear in uptrend

- Bearish zones only appear in downtrend

- Reduces noise and false signals significantly

## Customization Options

### Display Settings

- Toggle FVGs and OBs independently

- Adjust max zones per type (5-200)

- Choose to remove or gray out mitigated zones

- Color customization for all zone types

### Detection Parameters

- **Min Impulse Body %**: Controls how strong the impulse candle must be (0.3-1.0)

- **Order Block Lookback**: How many bars to look back for OB validation (5-50)

- **ATR Length**: Period for ATR calculation (5-50)

### Trend Filter

- Enable/disable trend filtering

- Adjustable MA period for trend determination

### MTF Panel

- Show/hide the trend panel

- 4 position options: Top Right, Top Left, Bottom Right, Bottom Left

- 3 size options: Small, Normal, Large

- Customizable MA period for trend calculation across all timeframes

## Trading Applications

### 1. **Liquidity Grab Entries**

Wait for price to sweep a zone (50%+ mitigation) then enter on reversal. Smart money often "hunts" these zones before the real move begins.

### 2. **Confluence Trading**

Look for zones that align with:

- Multiple timeframe trends showing same direction

- Multiple FVGs/OBs stacking in same area

- Key support/resistance levels

### 3. **Breakout Confirmation**

Use Order Blocks to confirm the strength of breakouts. Strong OBs indicate institutional participation.

### 4. **Retracement Entries**

Enter when price returns to a fresh, unmitigated zone in the direction of the higher timeframe trend.

### 5. **Range Trading**

Identify FVG zones at range extremes - price often reverses at these inefficiencies.

## How It Works

**Fair Value Gaps** form when the middle candle creates such aggressive movement that it leaves a price gap between the high/low of surrounding candles. Institutional traders know these gaps get filled.

**Order Blocks** mark the origin of major moves. The last opposite-colored candle before a breakout is where large orders were placed. Price often returns to these zones for "retests" before continuing.

**Mitigation** happens when price returns to fill these zones. The indicator tracks this automatically, showing you which zones are still "fresh" and which have been used up.

## Best Practices

✅ **Use higher timeframe trends** - Always check the MTF panel before taking trades

✅ **Trade fresh zones** - Unmitigated zones (not gray) have the highest probability

✅ **Combine with price action** - Look for rejection wicks and engulfing candles at zones

✅ **Respect zone strength** - VERY STRONG and STRONG zones are most reliable

✅ **Use trend filter** - Especially on lower timeframes to reduce false signals

❌ **Don't overtrade** - Not every zone will react, wait for confirmation

❌ **Don't ignore context** - Check the MTF panel for conflicting trends

❌ **Don't chase** - Wait for price to come to the zone, don't enter mid-zone

## Technical Details

- **Non-repainting**: All zones are drawn on confirmed candles only

- **Performance optimized**: Uses efficient array management with per-type caps

- **Real-time updates**: Zones extend and track mitigation as price moves

- **Universal compatibility**: Works on all markets and timeframes

## Recommended Settings by Style

**Scalping (1m-5m charts):**

- Max zones: 10-15

- Use trend filter: ON

- MTF Panel: Focus on 1m-15m trends

- Remove mitigated: ON (keep chart clean)

**Day Trading (5m-1H charts):**

- Max zones: 15-20

- Use trend filter: ON

- MTF Panel: Focus on 15m-4H trends

- Remove mitigated: OFF (track zone history)

**Swing Trading (1H-D charts):**

- Max zones: 20+

- Use trend filter: Optional

- MTF Panel: Focus on 1H-1D trends

- Remove mitigated: OFF (important zones persist)

---

## Perfect For

- Smart Money Concept (SMC) traders

- ICT methodology followers

- Institutional order flow traders

- Price action traders seeking key zones

- Multi-timeframe analysis enthusiasts

**Compatible with all markets:** Forex, Crypto, Stocks, Indices, Commodities, Futures

*Trade where the institutions trade. Follow the smart money.*

Smart Money Zones (FVG + OB) + MTF Trend Panel## Overview

Professional-grade institutional trading zones indicator that identifies **Fair Value Gaps (FVG)** and **Order Blocks (OB)** - key price inefficiencies where smart money operates. Includes a comprehensive **Multi-Timeframe Trend Panel** for complete market context at a glance.

## Core Features

### 🎯 Fair Value Gaps (FVG)

Fair Value Gaps occur when price moves so aggressively that it leaves an "imbalance" or "gap" in the market structure. These zones often act as magnets where price returns to find liquidity.

**Detection Logic:**

- **Bullish FVG**: When current candle's low is above the high of the candle 2 bars ago

- **Bearish FVG**: When current candle's high is below the low of the candle 2 bars ago

- Requires strong impulse candle (configurable body percentage threshold)

- Color-coded zones: Green for bullish, Red for bearish

### 📦 Order Blocks (OB)

Order Blocks represent the last opposite candle before a significant price move - the zone where institutional orders were placed before the breakout.

**Detection Logic:**

- Identifies the last bearish candle before a strong bullish breakout (Bullish OB)

- Identifies the last bullish candle before a strong bearish breakout (Bearish OB)

- Validates breakout strength using ATR multiplier (1.2x default)

- Color-coded zones: Blue for bullish, Orange for bearish

### 📊 Multi-Timeframe Trend Panel

Real-time trend analysis across **7 timeframes** displayed in an elegant dashboard:

- **1 Minute** - Ultra short-term scalping

- **5 Minutes** - Short-term momentum

- **15 Minutes** - Intraday swings

- **30 Minutes** - Session trends

- **1 Hour** - Multi-session trends

- **4 Hours** - Daily structure

- **Daily** - Long-term direction

**Visual Indicators:**

- 🟢 Green circle = Bullish trend

- 🔴 Red circle = Bearish trend

- Clean, professional table design with customizable position and size

## Intelligence Features

### 🧠 Zone Strength Rating

Every zone is automatically classified by strength based on size relative to ATR:

- **VERY STRONG** - 2.0x ATR or more (major institutional zones)

- **STRONG** - 1.5x to 2.0x ATR (significant zones)

- **MEDIUM** - 1.0x to 1.5x ATR (moderate zones)

- **WEAK** - Below 1.0x ATR (minor zones)

Strength rating helps you prioritize which zones to trade from!

### 📉 Smart Mitigation Tracking

Zones automatically track how much they've been "filled" or mitigated:

- Calculates penetration percentage as price enters the zone

- Zones turn **gray** when 50%+ mitigated or fully filled

- Option to **auto-delete** mitigated zones to keep chart clean

- Live zones extend dynamically with price action

### 🎨 Trend Filter (Optional)

When enabled, only shows zones aligned with the current trend:

- Uses customizable MA period (default 50)

- Bullish zones only appear in uptrend

- Bearish zones only appear in downtrend

- Reduces noise and false signals significantly

## Customization Options

### Display Settings

- Toggle FVGs and OBs independently

- Adjust max zones per type (5-200)

- Choose to remove or gray out mitigated zones

- Color customization for all zone types

### Detection Parameters

- **Min Impulse Body %**: Controls how strong the impulse candle must be (0.3-1.0)

- **Order Block Lookback**: How many bars to look back for OB validation (5-50)

- **ATR Length**: Period for ATR calculation (5-50)

### Trend Filter

- Enable/disable trend filtering

- Adjustable MA period for trend determination

### MTF Panel

- Show/hide the trend panel

- 4 position options: Top Right, Top Left, Bottom Right, Bottom Left

- 3 size options: Small, Normal, Large

- Customizable MA period for trend calculation across all timeframes

## Trading Applications

### 1. **Liquidity Grab Entries**

Wait for price to sweep a zone (50%+ mitigation) then enter on reversal. Smart money often "hunts" these zones before the real move begins.

### 2. **Confluence Trading**

Look for zones that align with:

- Multiple timeframe trends showing same direction

- Multiple FVGs/OBs stacking in same area

- Key support/resistance levels

### 3. **Breakout Confirmation**

Use Order Blocks to confirm the strength of breakouts. Strong OBs indicate institutional participation.

### 4. **Retracement Entries**

Enter when price returns to a fresh, unmitigated zone in the direction of the higher timeframe trend.

### 5. **Range Trading**

Identify FVG zones at range extremes - price often reverses at these inefficiencies.

## How It Works

**Fair Value Gaps** form when the middle candle creates such aggressive movement that it leaves a price gap between the high/low of surrounding candles. Institutional traders know these gaps get filled.

**Order Blocks** mark the origin of major moves. The last opposite-colored candle before a breakout is where large orders were placed. Price often returns to these zones for "retests" before continuing.

**Mitigation** happens when price returns to fill these zones. The indicator tracks this automatically, showing you which zones are still "fresh" and which have been used up.

## Best Practices

✅ **Use higher timeframe trends** - Always check the MTF panel before taking trades

✅ **Trade fresh zones** - Unmitigated zones (not gray) have the highest probability

✅ **Combine with price action** - Look for rejection wicks and engulfing candles at zones

✅ **Respect zone strength** - VERY STRONG and STRONG zones are most reliable

✅ **Use trend filter** - Especially on lower timeframes to reduce false signals

❌ **Don't overtrade** - Not every zone will react, wait for confirmation

❌ **Don't ignore context** - Check the MTF panel for conflicting trends

❌ **Don't chase** - Wait for price to come to the zone, don't enter mid-zone

## Technical Details

- **Non-repainting**: All zones are drawn on confirmed candles only

- **Performance optimized**: Uses efficient array management with per-type caps

- **Real-time updates**: Zones extend and track mitigation as price moves

- **Universal compatibility**: Works on all markets and timeframes

## Recommended Settings by Style

**Scalping (1m-5m charts):**

- Max zones: 10-15

- Use trend filter: ON

- MTF Panel: Focus on 1m-15m trends

- Remove mitigated: ON (keep chart clean)

**Day Trading (5m-1H charts):**

- Max zones: 15-20

- Use trend filter: ON

- MTF Panel: Focus on 15m-4H trends

- Remove mitigated: OFF (track zone history)

**Swing Trading (1H-D charts):**

- Max zones: 20+

- Use trend filter: Optional

- MTF Panel: Focus on 1H-1D trends

- Remove mitigated: OFF (important zones persist)

---

## Perfect For

- Smart Money Concept (SMC) traders

- ICT methodology followers

- Institutional order flow traders

- Price action traders seeking key zones

- Multi-timeframe analysis enthusiasts

**Compatible with all markets:** Forex, Crypto, Stocks, Indices, Commodities, Futures

*Trade where the institutions trade. Follow the smart money.*

Time-Decay Liquidity Zones [BackQuant]Time-Decay Liquidity Zones

A dynamic liquidity map that turns single-bar exhaustion events into fading, color-graded zones, so you can see where trapped traders and unfinished business still matter, and when those areas have finally stopped pulling price.

What this is

This indicator detects unusually strong impulsive moves into wicks, converts them into supply or demand “zones,” then lets those zones decay over time. Each zone carries a strength score that fades bar by bar. Zones that stop attracting or rejecting price are gradually de-emphasized and eventually removed, while the most relevant areas stay bright and obvious.

Instead of static rectangles that live forever, you get a living liquidity map where:

Zones are born from objective criteria: volatility, wick size, and optional volume spikes.

Zones “age” using a configurable decay factor and maximum lifetime.

Zone color and opacity reflect current relative strength on a unified clear → green → red gradient.

Zones freeze when broken, so you can distinguish “active reaction areas” from “historical levels that have already given way”.

Conceptual idea

Large wicks with strong volatility often mark areas where aggressive orders met hidden liquidity and got absorbed. Price may revisit these areas to test leftover interest or to relieve trapped positions. However, not every wick matters for long. As time passes and more bars print, the market “forgets” some areas.

Time-Decay Liquidity Zones turns that idea into a rule-based system:

Find bars that likely reflect strong aggressive flows into liquidity.

Mark a zone around the wick using ATR-based thickness.

Assign a strength score of 1.0 at birth.

Each bar, reduce that score by a decay factor and remove zones that fall below a threshold or live too long.

Color all surviving zones from weak to strong using a single gradient scale and a visual legend.

How events are detected

Detection lives in the Event Detection group. The script combines range, wick size, and optional volume filters into simple rules.

Volatility filter

ATR Length — computes a rolling ATR over your chosen window. This is the volatility baseline.

Min range in ATRs — bar range (High–Low) must exceed this multiple of ATR for an event to be considered. This avoids tiny bars triggering zones.

Wick filters

For each bar, the script splits the candle into body and wicks:

Upper wick = High minus the max(Open, Close).

Lower wick = min(Open, Close) minus Low.

Then it tests:

Upper wick condition — upper wick must be larger than Min wick size in ATRs × ATR.

Lower wick condition — lower wick must be larger than Min wick size in ATRs × ATR.

Only bars with a sufficiently long wick relative to volatility qualify as candidate “liquidity events”.

Volume filter

Optionally, the script requires a volume spike:

Use volume filter — if enabled, volume must exceed a rolling volume SMA by a configurable multiplier.

Volume SMA length — period for the volume average.

Volume spike multiplier — how many times above the SMA current volume needs to be.

This lets you focus only on “heavy” tests of liquidity and ignore quiet bars.

Event types

Putting it together:

Upper event (potential supply / long liquidation, etc.)

Occurs when:

Upper wick is large in ATR terms.

Full bar range is large in ATR terms.

Volume is above the spike threshold (if enabled).

Lower event (potential demand / short liquidation, etc.)

Symmetric conditions using the lower wick.

How zones are constructed

Zone geometry lives in Zone Geometry .

When an event is detected, the script builds a rectangular box that anchors to the wick and extends in the appropriate direction by an ATR-based thickness.

For upper (supply-type) zones

Bottom of the zone = event bar high.

Top of the zone = event bar high + Zone thickness in ATRs × ATR.

The zone initially spans only the event bar on the x-axis, but is extended to the right as new bars appear while the zone is active.

For lower (demand-type) zones

Top of the zone = event bar low.

Bottom of the zone = event bar low − Zone thickness in ATRs × ATR.

Same extension logic: box starts on the event bar and grows rightward while alive.

The result is a band around the wick that scales with volatility. On high-ATR charts, zones are thicker. On calm charts, they are narrower and more precise.

Zone lifecycle, decay, and removal

All lifecycle logic is controlled by the Decay & Lifetime group.

Each zone carries:

Score — a floating-point “importance” measure, starting at 1.0 when created.

Direction — +1 for upper zones, −1 for lower zones.

Birth index — bar index at creation time.

Active flag — whether the zone is still considered unbroken and extendable.

1) Active vs broken

Each confirmed bar, the script checks:

For an upper zone , the zone is counted as “broken” when the close moves above the top of the zone.

For a lower zone , the zone is counted as “broken” when the close moves below the bottom of the zone.

When a zone breaks:

Its right edge is frozen at the previous bar (no further extension).

The zone remains on the chart, but is no longer updated by price interaction. It still decays in score until removal.

This lets you see where a major level was overrun, while naturally fading its influence over time.

2) Time decay

At each confirmed bar:

Score := Score × Score decay per bar .

A decay value close to 1.0 means very slow decay and long-lived zones.

Lower values (closer to 0.9) mean faster forgetting and more current-focused zones.

You are controlling how quickly the market “forgets” past events.

3) Age and score-based removal

Zones are removed when either:

Age in bars exceeds Max bars a zone can live .

This is a hard lifetime cap.

Score falls below Minimum score before removal .

This trims zones that have decayed into irrelevance even if their age is still within bounds.

When a zone is removed, its box is deleted and all associated state is freed to keep performance and visuals clean.

Unified gradient and color logic

Color control lives in Gradient & Color . The indicator uses a single continuous gradient for all zones, above and below price, so you can read strength at a glance without guessing what palette means what.

Base colors

You set:

Mid strength color (green) — used for mid-level strength zones and as the “anchor” in the gradient.

High strength color (red) — used for the strongest zones.

Max opacity — the maximum visual opacity for the solid part of the gradient. Lower values here mean more solid; higher values mean more transparent.

The script then defines three internal points:

Clear end — same as mid color, but with a high alpha (close to transparent).

Mid end — mid color at the strongest allowed opacity.

High end — high color at the strongest allowed opacity.

Strength normalization

Within each update:

The script finds the maximum score among all existing zones.

Each zone’s strength is computed as its score divided by this maximum.

Strength is clamped into .

This means a zone with strength 1.0 is currently the strongest zone on the chart. Other zones are colored relative to that.

Piecewise gradient

Color is assigned in two stages:

For strength between 0.0 and 0.5: interpolate from “clear” green to solid green.

Weak zones are barely visible, mid-strength zones appear as solid green.

For strength between 0.5 and 1.0: interpolate from solid green to solid red.

The strongest zones shift toward the red anchor, clearly separating them from everything else.

Strength scale legend

To make the gradient readable, the indicator draws a vertical legend on the right side of the chart:

About 15 cells from top (Strong) to bottom (Weak).

Each cell uses the same gradient function as the zones themselves.

Top cell is labeled “Strong”; bottom cell is labeled “Weak”.

This legend acts as a fixed reference so you can instantly map a zone’s color to its approximate strength rank.

What it plots

At a glance, the indicator produces:

Upper liquidity zones above price, built from large upper wick events.

Lower liquidity zones below price, built from large lower wick events.

All zones colored by relative strength using the same gradient.

Zones that freeze when price breaks them, then fade out via decay and removal.

A strength scale legend on the right to interpret the gradient.

There are no extra lines, labels, or clutter. The focus is the evolving structure of liquidity zones and their visual strength.

How to read the zones

Bright red / bright green zones

These are your current “major” liquidity areas. They have high scores relative to other zones and have not yet decayed. Expect meaningful reactions, absorption attempts, or spillover moves when price interacts with them.

Faded zones

Pale, nearly transparent zones are either old, decayed, or minor. They can still matter, but priority is lower. If these are in the middle of a long consolidation, they often become background noise.

Broken but still visible zones

Zones whose extension has stopped have been overrun by closing price. They show where a key level gave way. You can use them as context for regime shifts or failed attempts.

Absence of zones

A chart with few or no zones means that, under your current thresholds, there have not been strong enough liquidity events recently. Either tighten the filters or accept that recent price action has been relatively balanced.

Use cases

1) Intraday liquidity hunting

Run the indicator on lower timeframes (e.g., 1–15 minute) with moderately fast decay.

Use the upper zones as potential sell reaction areas, the lower zones as potential buy reaction areas.

Combine with order flow, CVD, or footprint tools to see whether price is absorbing or rejecting at each zone.

2) Swing trading context

Increase ATR length and range/wick multipliers to focus only on major spikes.

Set slower decay and higher max lifetime so zones persist across multiple sessions.

Use these zones as swing inflection areas for larger setups, for example anticipating re-tests after breakouts.

3) Stop placement and invalidation

For longs, place invalidation beyond a decaying lower zone rather than in the middle of noise.

For shorts, place invalidation beyond strong upper zones.

If price closes through a strong zone and it freezes, treat that as additional evidence your prior bias may be wrong.

4) Identifying trapped flows

Upper zones formed after violent spikes up that quickly fail can mark trapped longs.

Lower zones formed after violent spikes down that quickly reverse can mark trapped shorts.

Watching how price behaves on the next touch of those zones can hint at whether those participants are being rescued or squeezed.

Settings overview

Event Detection

Use volume filter — enable or disable the volume spike requirement.

Volume SMA length — rolling window for average volume.

Volume spike multiplier — how aggressive the volume spike filter is.

ATR length — period for ATR, used in all size comparisons.

Min wick size in ATRs — minimum wick size threshold.

Min range in ATRs — minimum bar range threshold.

Zone Geometry

Zone thickness in ATRs — vertical size of each liquidity zone, scaled by ATR.

Decay & Lifetime

Score decay per bar — multiplicative decay factor for each zone score per bar.

Max bars a zone can live — hard cap on lifetime.

Minimum score before removal — score cut-off at which zones are deleted.

Gradient & Color

Mid strength color (green) — base color for mid-level zones and the lower half of the gradient.

High strength color (red) — target color for the strongest zones.

Max opacity — controls the most solid end of the gradient (0 = fully solid, 100 = fully invisible).

Tuning guidance

Fast, session-only liquidity

Shorter ATR length (e.g., 20–50).

Higher wick and range multipliers to focus only on extreme events.

Decay per bar closer to 0.95–0.98 and moderate max lifetime.

Volume filter enabled with a decent multiplier (e.g., 1.5–2.0).

Slow, structural zones

Longer ATR length (e.g., 100+).

Moderate wick and range thresholds.

Decay per bar very close to 1.0 for slow fading.

Higher max lifetime and slightly higher min score threshold so only very weak zones disappear.

Noisy, high-volatility instruments

Increase wick and range ATR multipliers to avoid over-triggering.

Consider enabling the volume filter with stronger settings.

Keep decay moderate to avoid the chart getting overloaded with old zones.

Notes

This is a structural and contextual tool, not a complete trading system. It does not account for transaction costs, execution slippage, or your specific strategy rules. Use it to:

Highlight where liquidity has recently been tested hard.

Rank these areas by decaying strength.

Guide your attention when layering in separate entry signals, risk management, and higher-timeframe context.

Time-Decay Liquidity Zones is designed to keep your chart focused on where the market has most recently “cared” about price, and to gradually forget what no longer matters. Adjust the detection, geometry, decay, and gradient to fit your product and timeframe, and let the zones show you which parts of the tape still have unfinished business.

Thrax - Intraday Market Pressure ZonesTHRAX - INTRADAY MARKET PRESSURE ZONES

This indicator identifies potential support and resistance zones based on areas of significant market pressure. It dynamically plots these zones and adjusts their visibility based on real-time price action and user-defined thresholds. The indicator is useful for traders seeking to understand intraday market pressure, visualize zones of potential price reversals, and analyze volume imbalances at critical levels.

1. Support/Resistance Zones: Wherever the price retraces significantly from its high a support zone is drawn and when it retraces significantly from it low a resistance zone is drawn. The significant retracing is measured by the wick threshold percentage. For instance, if set to 75%, it implies price retracement of 75% either from high or from low for a particular candel

Volume delat: Displays volume delta information where the zones are formed. This can be used by trader to consider only those zones where delta is significant.

2. Breakout Detection: Monitors for price breakouts beyond established zones, deleting zones that are invalidated by price movement. when the price breaks a given zone with the threshold, it is considered to be mitigated and chances of trend continuation is decent.

Candle Coloring: Uses color codes (green, red, and yellow) to represent bullish, bearish, and indecisive (doji) candles, aiding quick visual assessment.

INPUTS

1. Wick Threshold (%) : Sets the minimum wick percentage required for a candle to be considered a support or resistance candidate.

2. Breakout Threshold (%) : Determines the percentage above or below a support or resistance zone that defines a breakout condition. if breaks a zone with the set threshold then the zone will be considered mititgated.

3. Max Number of Support/Resistance Zones : Limits the maximum number of support/resistance zones displayed on the chart, ranging from 1 to 5.

4. Show Wick Percentage Labels : Toggles the display of percentage values for upper and lower wicks on each candle.

TRADE SETUP

Identifying Entry Points: Look for the formation of support or resistance zones. Wait for price to retrace to these zones. if you are willing to take risk, you can consider even zones with low delta. If you want to be more cautious you should consider zones with high delta.

Volume Confirmation: Use the volume information to confirm the strength of the zone. Strong volume differences (displayed as labels) can indicate significant market pressure at these levels.

Breakout Trades: If price breaks through a support/resistance zone by more than the breakout threshold, consider this a signal for a potential trend continuation in the breakout direction.

Risk Management: Set stop-loss levels slightly outside of the identified zones to minimize risk in case of false breakouts. This can be set in input setting for breakout threshold.

Bonus Tip : Mark your significant highs and lows from where prices have retraced multiple times in the near past and if the zone is near these levels it can serve s a strong candidate of support or resistance

Therefore, in conclusion monitor the zones, based on delta and volume presence filter out the zone, wait for price retracement to the zone, intiate the trade with stop loss below zone with a set percentage.

Liquidity Zones [BigBeluga]This indicator is designed to detect liquidity zones on the chart by identifying significant pivot highs and lows filtered by volume strength. It plots these zones as boxes, highlighting areas where liquidity is likely to accumulate. The indicator also draws lines extending from these boxes, marking the levels where price may "grab" this liquidity. The size of these boxes can be dynamic, adjusting based on the volume size, offering a visual representation of market areas where traders might expect significant price reactions.

🔵 IDEA