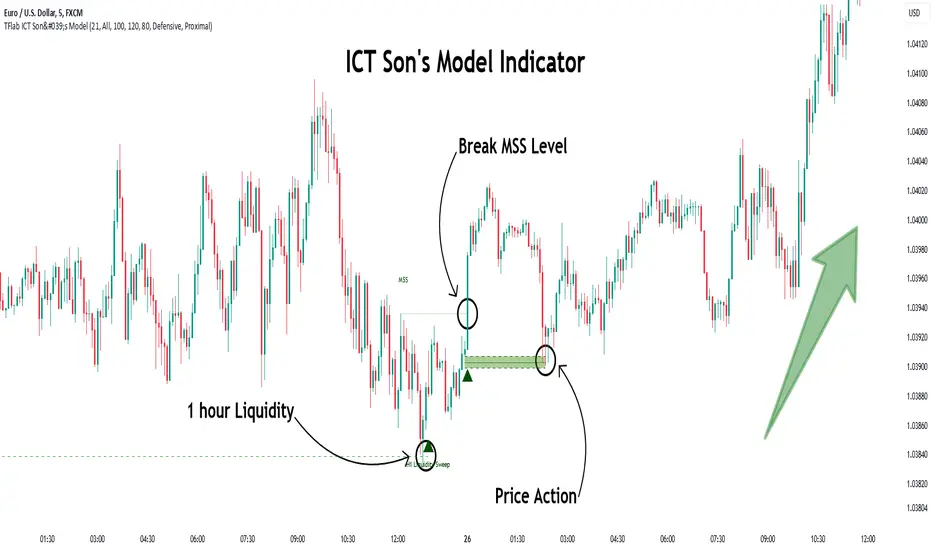

Son Model ICT [TradingFinder] HTF DOL H1 + Sweep M15 + FVG M1🔵 Introduction

The ICT Son Model setup is a precise trading strategy based on market structure and liquidity, implemented across multiple timeframes. This setup first identifies a liquidity level in the 1-hour (1H) timeframe and then confirms a Market Structure Shift (MSS) in the 5-minute (5M) timeframe to validate the trend. After confirmation, the price forms a new swing in the 5-minute timeframe, absorbing liquidity.

Once this level is broken, traders typically drop to the 30-second (30s) timeframe and enter trades based on a Fair Value Gap (FVG). However, since access to the 30-second timeframe is not available to most traders, we take the entry signal directly from the 5-minute timeframe, using the same liquidity zones and confirmed breakouts to execute trades. This approach simplifies execution and makes the strategy accessible to all traders.

This model operates in two setups :

Bullish ICT Son Model and Bearish ICT Son Model. In the bullish setup, liquidity is first accumulated at the lows of the 1-hour timeframe, and after confirming a market structure shift, a long position is initiated. Conversely, in the bearish setup, liquidity is first drawn from higher levels, and upon confirmation of a bearish trend, a short position is executed.

Bullish Setup :

Bearish Setup :

🔵 How to Use

The ICT Son Model setup is designed around liquidity analysis and market structure shifts and can be applied in both bullish and bearish market conditions. The strategy first identifies a liquidity level in the 1-hour (1H) timeframe and then confirms a Market Structure Shift (MSS) in the 5-minute (5M) timeframe.

After this shift, the price forms a new swing, absorbing liquidity. When this level is broken in the 5-minute timeframe, the trader enters based on a Fair Value Gap (FVG). While the ideal entry is in the 30-second (30s) timeframe, due to accessibility constraints, we take entry signals directly from the 5-minute timeframe.

🟣 Bullish Setup

In the Bullish ICT Son Model, the 1-hour timeframe first identifies liquidity at the market lows, where price sweeps this level to absorb liquidity. Then, in the 5-minute timeframe, an MSS confirms the bullish shift.

After confirmation, the price forms a new swing, absorbing liquidity at a higher level. The price then retraces into a Fair Value Gap (FVG) created in the 5-minute timeframe, where the trader enters a long position, placing the stop-loss below the FVG.

🟣 Bearish Setup

In the Bearish ICT Son Model, liquidity at higher market levels is identified in the 1-hour timeframe, where price sweeps these levels to absorb liquidity. Then, in the 5-minute timeframe, an MSS confirms the bearish trend.

After confirmation, the price forms a new swing, absorbing liquidity at a lower level. The price then retraces into a Fair Value Gap (FVG) created in the 5-minute timeframe, where the trader enters a short position, placing the stop-loss above the FVG.

🔵 Settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

FVG Length : Default is 120 Bar.

MSS Length : Default is 80 Bar.

FVG Filter : This refines the number of identified FVG areas based on a specified algorithm to focus on higher quality signals and reduce noise.

Types of FVG filters :

Very Aggressive Filter: Adds a condition where, for an upward FVG, the last candle's highest price must exceed the middle candle's highest price, and for a downward FVG, the last candle's lowest price must be lower than the middle candle's lowest price. This minimally filters out FVGs.

Aggressive Filter: Builds on the Very Aggressive mode by ensuring the middle candle is not too small, filtering out more FVGs.

Defensive Filter: Adds criteria regarding the size and structure of the middle candle, requiring it to have a substantial body and specific polarity conditions, filtering out a significant number of FVGs.

Very Defensive Filter: Further refines filtering by ensuring the first and third candles are not small-bodied doji candles, retaining only the highest quality signals.

🔵 Conclusion

The ICT Son Model setup is a structured and precise method for trade execution based on liquidity analysis and market structure shifts. This strategy first identifies a liquidity level in the 1-hour timeframe and then confirms a trend shift using the 5-minute timeframe.

Trade entries are executed based on Fair Value Gaps (FVGs), which highlight optimal entry points. By applying this model, traders can leverage existing market liquidity to enter high-probability trades. The bullish setup activates when liquidity is swept from market lows and a market structure shift confirms an upward trend, whereas the bearish setup is used when liquidity is drawn from market highs, confirming a downtrend.

This approach enables traders to identify high-probability trade setups with greater precision compared to many other strategies. Additionally, since access to the 30-second timeframe is limited, the strategy remains fully functional in the 5-minute timeframe, making it more practical and accessible for a wider range of traders.

ابحث في النصوص البرمجية عن "欧元汇率走势30天"

Timed Ranges [mktrader]The Timed Ranges indicator helps visualize price ranges that develop during specific time periods. It's particularly useful for analyzing market behavior in instruments like NASDAQ, S&P 500, and Dow Jones, which often show reactions to sweeps of previous ranges and form reversals.

### Key Features

- Visualizes time-based ranges with customizable lengths (30 minutes, 90 minutes, etc.)

- Tracks high/low range development within specified time periods

- Shows multiple cycles per day for pattern recognition

- Supports historical analysis across multiple days

### Parameters

#### Settings

- **First Cycle (HHMM-HHMM)**: Define the time range of your first cycle. The duration of this range determines the length of all subsequent cycles (e.g., "0930-1000" creates 30-minute cycles)

- **Number of Cycles per Day**: How many consecutive cycles to display after the first cycle (1-20)

- **Maximum Days to Display**: Number of historical days to show the ranges for (1-50)

- **Timezone**: Select the appropriate timezone for your analysis

#### Style

- **Box Transparency**: Adjust the transparency of the range boxes (0-100)

### Usage Example

To track 30-minute ranges starting at market open:

1. Set First Cycle to "0930-1000" (creates 30-minute cycles)

2. Set Number of Cycles to 5 (will show ranges until 11:30)

3. The indicator will display:

- Range development during each 30-minute period

- Visual progression of highs and lows

- Color-coded cycles for easy distinction

### Use Cases

- Identify potential reversal points after range sweeps

- Track regular time-based support and resistance levels

- Analyze market structure within specific time windows

- Monitor range expansions and contractions during key market hours

### Tips

- Use in conjunction with volume analysis for better confirmation

- Pay attention to breaks and sweeps of previous ranges

- Consider market opens and key session times when setting cycles

- Compare range sizes across different time periods for volatility analysis

Market Movement After OpenDescription:

This script provides a detailed visualization of market movements during key trading hours: the German market opening (08:00–09:00 UTC+1) and the US market opening (15:30–16:30 UTC+1). It is designed to help traders analyze price behavior in these critical trading periods by capturing and presenting movement patterns and trends directly on the chart and in an interactive table.

Key Features:

Market Movement Analysis:

Tracks the price movement during the German market's first hour (08:00–09:00 UTC+1) and the US market's opening session (15:30–16:30 UTC+1).

Analyzes whether the price moved up or down during these intervals.

Visual Representation:

Dynamically colored price lines indicate upward (green) or downward (red) movement during the respective periods.

Labels ("DE" for Germany and "US" for the United States) mark key moments in the chart.

Historical Data Table:

Displays the past 10 trading days' movement trends in an interactive table, including:

Date: Trading date.

German Market Movement: Up (▲), Down (▼), or Neutral (-) for 08:00–09:00 UTC+1.

US Market Movement: Up (▲), Down (▼), or Neutral (-) for 15:30–16:30 UTC+1.

The table uses color coding for easy interpretation: green for upward movements, red for downward, and gray for neutral.

Real-Time Updates:

Automatically updates during live trading sessions to reflect the most recent movements.

Highlights incomplete periods (e.g., ongoing sessions) to indicate their status.

Customizable:

Suitable for intraday analysis or broader studies of market trends.

Designed to overlay directly on any price chart.

Use Case:

This script is particularly useful for traders who focus on market openings, which are often characterized by high volatility and significant price movements. By providing a clear visual representation of historical and live data, it aids in understanding and capitalizing on market trends during these critical periods.

Notes:

The script works best when the chart is set to the appropriate timezone (UTC+1 for the German market or your local equivalent).

For precise trading decisions, consider combining this script with other technical indicators or trading strategies.

Feel free to share feedback or suggest additional features to enhance the script!

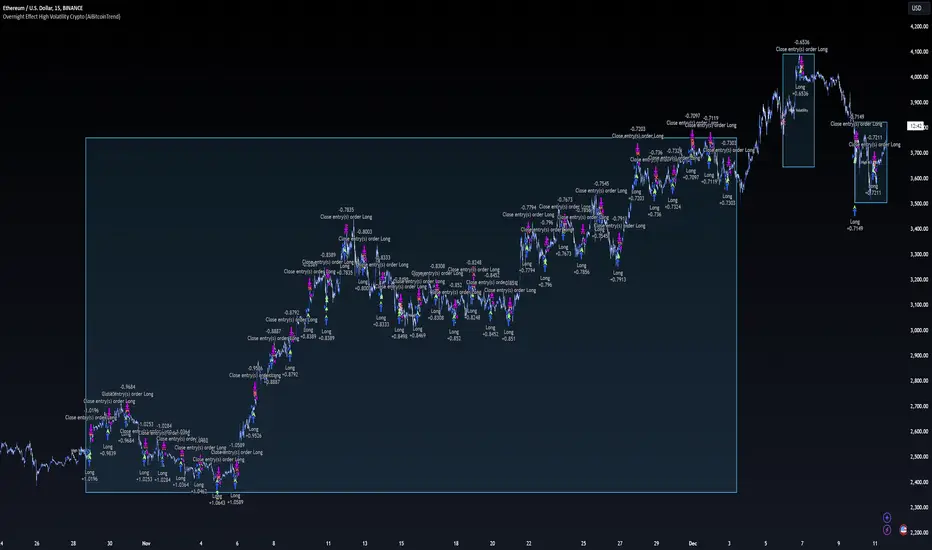

Overnight Effect High Volatility Crypto (AiBitcoinTrend)👽 Overview of the Strategy

This strategy leverages the overnight effect in the cryptocurrency market, specifically targeting the two-hour window from 21:00 UTC to 23:00 UTC. The strategy is designed to be applied only during periods of high volatility, which is determined using historical volatility data. This approach, inspired by research from Padyšák and Vojtko (2022), aims to capitalize on statistically significant return patterns observed during these hours.

Deep Backtesting with a High Volatility Filter

Deep Backtesting without a High Volatility Filter

👽 How the Strategy Works

Volatility Calculation:

Each day at 00:00 UTC, the strategy calculates the 30-day historical volatility of crypto returns (typically Bitcoin). The historical volatility is the standard deviation of the log returns over the past 30 days, representing the market's recent volatility level.

Median Volatility Benchmark:

The median of the 30-day historical volatility is calculated over a 365-day period (one year). This median acts as a benchmark to classify each day as either:

👾 High Volatility: When the current 30-day volatility exceeds the median volatility.

👾 Low Volatility: When the current 30-day volatility is below the median.

Trading Rule:

If the day is classified as a High Volatility Day, the strategy executes the following trades:

👾 Buy at 21:00 UTC.

👾 Sell at 23:00 UTC.

Trade Execution Details:

The strategy uses a 0.02% fee per trade.

Each trade is executed with 25% of the available capital. This allocation helps manage risk while allowing for compounding returns.

Rationale:

The returns during the 22:00 and 23:00 UTC hours have been found to be statistically significant during high volatility periods. The overnight effect is believed to drive this phenomenon due to the asynchronous closing hours of global financial markets. This creates unique trading opportunities in the cryptocurrency market, where exchanges remain open 24/7.

👽 Market Context and Global Time Zone Impact

👾 Why 21:00 to 23:00 UTC?

During this window, major traditional financial markets are closed:

NYSE (New York) closes at 21:00 UTC.

London and European markets are closed during these hours.

Asian markets (Tokyo, Hong Kong, etc.) open later, leaving this window largely unaffected by traditional trading flows.

This global market inactivity creates a period where significant moves can occur in the cryptocurrency market, particularly during high volatility.

👽 Strategy Parameters

Volatility Period: 30 days.

The lookback period for calculating historical volatility.

Median Period: 365 days.

The lookback period for calculating the median volatility benchmark.

Entry Time: 21:00 UTC.

Adjust this to your local time if necessary (e.g., 16:00 in New York, 22:00 in Stockholm).

Exit Time: 23:00 UTC.

Adjust this to your local time if necessary (e.g., 18:00 in New York, 00:00 midnight in Stockholm).

👽 Benefits of the Strategy

Seasonality Effect:

The strategy captures consistent patterns driven by the overnight effect and high volatility periods.

Risk Reduction:

Since trades are executed during a specific window and only on high volatility days, the strategy helps mitigate exposure to broader market risk.

Simplicity and Efficiency:

The strategy is moderately complex, making it accessible for traders while offering significant returns.

Global Applicability:

Suitable for traders worldwide, with clear guidelines on adjusting for local time zones.

👽 Considerations

Market Conditions: The strategy works best in a high-volatility environment.

Execution: Requires precise timing to enter and exit trades at the specified hours.

Time Zone Adjustments: Ensure you convert UTC times accurately based on your location to execute trades at the correct local times.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

David_30-Minute Boxes This indicator draws boxes for 30-minute intervals on the chart, highlighting significant price movements. The boxes begin at 00:00 and end at 22:00. Each box is color-coded according to price action:

Green Box: The closing price at the end of the 30-minute period is above the opening price.

Red Box: The closing price at the end of the 30-minute period is below the opening price.

Dark Green Box: The closing price at the end of the box is higher than the high of the previous box.

Dark Red Box: The closing price at the end of the box is lower than the low of the previous box.

The boxes dynamically adjust within each 30-minute interval to reflect the high and low of the period. The border of each box is fully transparent for a clean and uncluttered visual display.

Optional Candle Numbering

In the indicator settings, you can enable or disable the numbering of individual candles within each box. The numbering restarts at 1 for each new box, helping to track the progression of individual 30-minute intervals.

Use Cases

This indicator is particularly useful for traders who want to analyze short-term movements and the dynamics within 30-minute intervals. The color-coding of the boxes provides quick visual insights into the strength of price action within a time interval, making it easier to spot momentum shifts or important support and resistance levels.

Highest Volume* 지표 설명

이 지표는 다양한 기간 동안의 최대 거래량을 시각적으로 표시하여 거래자들이 중요한 거래량 패턴을 쉽게 식별할 수 있도록 도와줍니다. 30, 60, 90, 120 캔들 기간 동안의 최대 거래량을 감지하고, 이를 차트 상에 색상 코드로 표시합니다.

다중 기간 분석: 30, 60, 90, 120 캔들 기간에 대한 최대 거래량을 동시에 추적합니다.

기간에 따른 색상 표시: 기간이 길어질수록 표시되는 색상이 짙어집니다.

* 주요 기능

거래량 급증 감지: 갑작스러운 거래량 증가를 빠르게 포착할 수 있습니다.

* 부가 설명

초록색 배경: 최근 120 캔들 중 최대 거래량

노란색 배경: 최근 90 캔들 중 최대 거래량 (120 캔들 최대가 아닌 경우)

주황색 배경: 최근 60 캔들 중 최대 거래량 (90, 120 캔들 최대가 아닌 경우)

빨간색 배경: 최근 30 캔들 중 최대 거래량 (60, 90, 120 캔들 최대가 아닌 경우)

* Indicator Description

This indicator visually displays the maximum trading volume over various periods, helping traders easily identify important volume patterns. It detects the highest volume over 30, 60, 90, and 120 candle periods and represents this on the chart using color codes.

Multi-period analysis: Simultaneously tracks the maximum volume for 30, 60, 90, and 120 candle periods.

Color display according to period: The color becomes darker as the period gets longer.

* Key Features

Rapid volume surge detection: Quickly captures sudden increases in trading volume.

* Additional Explanation

Green background: Highest volume among the most recent 120 candles

Yellow background: Highest volume among the most recent 90 candles (when not the highest in 120 candles)

Orange background: Highest volume among the most recent 60 candles (when not the highest in 90 or 120 candles)

Red background: Highest volume among the most recent 30 candles (when not the highest in 60, 90, or 120 candles)

Moving Average Ratio [InvestorUnknown]Overview

The "Moving Average Ratio" (MAR) indicator is a versatile tool designed for valuation, mean-reversion, and long-term trend analysis. This indicator provides multiple display modes to cater to different analytical needs, allowing traders and investors to gain deeper insights into the market dynamics.

Features

1. Moving Average Ratio (MAR):

Calculates the ratio of the chosen source (close, open, ohlc4, hl2 …) to a longer-term moving average of choice (SMA, EMA, HMA, WMA, DEMA)

Useful for identifying overbought or oversold conditions, aiding in mean-reversion strategies and valuation of assets.

For some high beta asset classes, like cryptocurrencies, you might want to use logarithmic scale for the raw MAR, below you can see the visual difference of using Linear and Logarithmic scale on BTC

2. MAR Z-Score:

Computes the Z-Score of the MAR to standardize the ratio over chosen time period, making it easier to identify extreme values relative to the historical mean.

Helps in detecting significant deviations from the mean, which can indicate potential reversal points and buying/selling opportunities

3. MAR Trend Analysis:

Uses a combination of short-term (default 1, raw MAR) and long-term moving averages of the MAR to identify trend changes.

Provides a visual representation of bullish and bearish trends based on moving average crossings.

Using Logarithmic scale can improve the visuals for some asset classes.

4. MAR Momentum:

Measures the momentum of the MAR by calculating the difference over a specified period.

Useful for detecting changes in the market momentum and potential trend reversals.

5. MAR Rate of Change (ROC):

Calculates the rate of change of the MAR to assess the speed and direction of price movements.

Helps in identifying accelerating or decelerating trends.

MAR Momentum and Rate of Change are very similar, the only difference is that the Momentum is expressed in units of the MAR change and ROC is expressed as % change of MAR over chosen time period.

Customizable Settings

General Settings:

Display Mode: Select the display mode from MAR, MAR Z-Score, MAR Trend, MAR Momentum, or MAR ROC.

Color Bars: Option to color the bars based on the current display mode.

Wait for Bar Close: Toggle to wait for the bar to close before updating the MAR value.

MAR Settings:

Length: Period for the moving average calculation.

Source: Data source for the moving average calculation.

Moving Average Type: Select the type of moving average (SMA, EMA, WMA, HMA, DEMA).

Z-Score Settings:

Z-Score Length: Period for the Z-Score calculation.

Trend Analysis Settings:

Moving Average Type: Select the type of moving average for trend analysis (SMA, EMA).

Longer Moving Average: Period for the longer moving average.

Shorter Moving Average: Period for the shorter moving average.

Momentum Settings:

Momentum Length: Period for the momentum calculation.

Rate of Change Settings:

ROC Length: Period for the rate of change calculation.

Calculation and Plotting

Moving Average Ratio (MAR):

Calculates the ratio of the price to the selected moving average type and length.

Plots the MAR with a gradient color based on its Z-Score, aiding in visual identification of extreme values.

// Moving Average Ratio (MAR)

ma_main = switch ma_main_type

"SMA" => ta.sma(src, len)

"EMA" => ta.ema(src, len)

"WMA" => ta.wma(src, len)

"HMA" => ta.hma(src, len)

"DEMA" => ta.dema(src, len)

mar = (waitforclose ? src : src) / ma_main

z_col = color.from_gradient(z, -2.5, 2.5, color.green, color.red)

plot(disp_mode.mar ? mar : na, color = z_col, histbase = 1, style = plot.style_columns)

barcolor(color_bars ? (disp_mode.mar ? (z_col) : na) : na)

MAR Z-Score:

Computes the Z-Score of the MAR and plots it with a color gradient indicating the magnitude of deviation from the mean.

// MAR Z-Score

mean = ta.sma(math.log(mar), z_len)

stdev = ta.stdev(math.log(mar),z_len)

z = (math.log(mar) - mean) / stdev

plot(disp_mode.mar_z ? z : na, color = z_col, histbase = 0, style = plot.style_columns)

plot(disp_mode.mar_z ? 1 : na, color = color.new(color.red,70))

plot(disp_mode.mar_z ? 2 : na, color = color.new(color.red,50))

plot(disp_mode.mar_z ? 3 : na, color = color.new(color.red,30))

plot(disp_mode.mar_z ? -1 : na, color = color.new(color.green,70))

plot(disp_mode.mar_z ? -2 : na, color = color.new(color.green,50))

plot(disp_mode.mar_z ? -3 : na, color = color.new(color.green,30))

barcolor(color_bars ? (disp_mode.mar_z ? (z_col) : na) : na)

MAR Trend:

Plots the MAR along with its short-term and long-term moving averages.

Uses color changes to indicate bullish or bearish trends based on moving average crossings.

// MAR Trend - Moving Average Crossing

mar_ma_long = switch ma_trend_type

"SMA" => ta.sma(mar, len_trend_long)

"EMA" => ta.ema(mar, len_trend_long)

mar_ma_short = switch ma_trend_type

"SMA" => ta.sma(mar, len_trend_short)

"EMA" => ta.ema(mar, len_trend_short)

plot(disp_mode.mar_t ? mar : na, color = mar_ma_long < mar_ma_short ? color.new(color.green,50) : color.new(color.red,50), histbase = 1, style = plot.style_columns)

plot(disp_mode.mar_t ? mar_ma_long : na, color = mar_ma_long < mar_ma_short ? color.green : color.red, linewidth = 4)

plot(disp_mode.mar_t ? mar_ma_short : na, color = mar_ma_long < mar_ma_short ? color.green : color.red, linewidth = 2)

barcolor(color_bars ? (disp_mode.mar_t ? (mar_ma_long < mar_ma_short ? color.green : color.red) : na) : na)

MAR Momentum:

Plots the momentum of the MAR, coloring the bars to indicate increasing or decreasing momentum.

// MAR Momentum

mar_mom = mar - mar

// MAR Momentum

mom_col = mar_mom > 0 ? (mar_mom > mar_mom ? color.new(color.green,0): color.new(color.green,30)) : (mar_mom < mar_mom ? color.new(color.red,0): color.new(color.red,30))

plot(disp_mode.mar_m ? mar_mom : na, color = mom_col, histbase = 0, style = plot.style_columns)

MAR Rate of Change (ROC):

Plots the ROC of the MAR, using color changes to show the direction and strength of the rate of change.

// MAR Rate of Change

mar_roc = ta.roc(mar,len_roc)

// MAR ROC

roc_col = mar_roc > 0 ? (mar_roc > mar_roc ? color.new(color.green,0): color.new(color.green,30)) : (mar_roc < mar_roc ? color.new(color.red,0): color.new(color.red,30))

plot(disp_mode.mar_r ? mar_roc : na, color = roc_col, histbase = 0, style = plot.style_columns)

Summary:

This multi-purpose indicator provides a comprehensive toolset for various trading strategies, including valuation, mean-reversion, and trend analysis. By offering multiple display modes and customizable settings, it allows users to tailor the indicator to their specific analytical needs and market conditions.

PubLibTrendLibrary "PubLibTrend"

trend, multi-part trend, double trend and multi-part double trend conditions for indicator and strategy development

rlut()

return line uptrend condition

Returns: bool

dt()

downtrend condition

Returns: bool

ut()

uptrend condition

Returns: bool

rldt()

return line downtrend condition

Returns: bool

dtop()

double top condition

Returns: bool

dbot()

double bottom condition

Returns: bool

rlut_1p()

1-part return line uptrend condition

Returns: bool

rlut_2p()

2-part return line uptrend condition

Returns: bool

rlut_3p()

3-part return line uptrend condition

Returns: bool

rlut_4p()

4-part return line uptrend condition

Returns: bool

rlut_5p()

5-part return line uptrend condition

Returns: bool

rlut_6p()

6-part return line uptrend condition

Returns: bool

rlut_7p()

7-part return line uptrend condition

Returns: bool

rlut_8p()

8-part return line uptrend condition

Returns: bool

rlut_9p()

9-part return line uptrend condition

Returns: bool

rlut_10p()

10-part return line uptrend condition

Returns: bool

rlut_11p()

11-part return line uptrend condition

Returns: bool

rlut_12p()

12-part return line uptrend condition

Returns: bool

rlut_13p()

13-part return line uptrend condition

Returns: bool

rlut_14p()

14-part return line uptrend condition

Returns: bool

rlut_15p()

15-part return line uptrend condition

Returns: bool

rlut_16p()

16-part return line uptrend condition

Returns: bool

rlut_17p()

17-part return line uptrend condition

Returns: bool

rlut_18p()

18-part return line uptrend condition

Returns: bool

rlut_19p()

19-part return line uptrend condition

Returns: bool

rlut_20p()

20-part return line uptrend condition

Returns: bool

rlut_21p()

21-part return line uptrend condition

Returns: bool

rlut_22p()

22-part return line uptrend condition

Returns: bool

rlut_23p()

23-part return line uptrend condition

Returns: bool

rlut_24p()

24-part return line uptrend condition

Returns: bool

rlut_25p()

25-part return line uptrend condition

Returns: bool

rlut_26p()

26-part return line uptrend condition

Returns: bool

rlut_27p()

27-part return line uptrend condition

Returns: bool

rlut_28p()

28-part return line uptrend condition

Returns: bool

rlut_29p()

29-part return line uptrend condition

Returns: bool

rlut_30p()

30-part return line uptrend condition

Returns: bool

dt_1p()

1-part downtrend condition

Returns: bool

dt_2p()

2-part downtrend condition

Returns: bool

dt_3p()

3-part downtrend condition

Returns: bool

dt_4p()

4-part downtrend condition

Returns: bool

dt_5p()

5-part downtrend condition

Returns: bool

dt_6p()

6-part downtrend condition

Returns: bool

dt_7p()

7-part downtrend condition

Returns: bool

dt_8p()

8-part downtrend condition

Returns: bool

dt_9p()

9-part downtrend condition

Returns: bool

dt_10p()

10-part downtrend condition

Returns: bool

dt_11p()

11-part downtrend condition

Returns: bool

dt_12p()

12-part downtrend condition

Returns: bool

dt_13p()

13-part downtrend condition

Returns: bool

dt_14p()

14-part downtrend condition

Returns: bool

dt_15p()

15-part downtrend condition

Returns: bool

dt_16p()

16-part downtrend condition

Returns: bool

dt_17p()

17-part downtrend condition

Returns: bool

dt_18p()

18-part downtrend condition

Returns: bool

dt_19p()

19-part downtrend condition

Returns: bool

dt_20p()

20-part downtrend condition

Returns: bool

dt_21p()

21-part downtrend condition

Returns: bool

dt_22p()

22-part downtrend condition

Returns: bool

dt_23p()

23-part downtrend condition

Returns: bool

dt_24p()

24-part downtrend condition

Returns: bool

dt_25p()

25-part downtrend condition

Returns: bool

dt_26p()

26-part downtrend condition

Returns: bool

dt_27p()

27-part downtrend condition

Returns: bool

dt_28p()

28-part downtrend condition

Returns: bool

dt_29p()

29-part downtrend condition

Returns: bool

dt_30p()

30-part downtrend condition

Returns: bool

ut_1p()

1-part uptrend condition

Returns: bool

ut_2p()

2-part uptrend condition

Returns: bool

ut_3p()

3-part uptrend condition

Returns: bool

ut_4p()

4-part uptrend condition

Returns: bool

ut_5p()

5-part uptrend condition

Returns: bool

ut_6p()

6-part uptrend condition

Returns: bool

ut_7p()

7-part uptrend condition

Returns: bool

ut_8p()

8-part uptrend condition

Returns: bool

ut_9p()

9-part uptrend condition

Returns: bool

ut_10p()

10-part uptrend condition

Returns: bool

ut_11p()

11-part uptrend condition

Returns: bool

ut_12p()

12-part uptrend condition

Returns: bool

ut_13p()

13-part uptrend condition

Returns: bool

ut_14p()

14-part uptrend condition

Returns: bool

ut_15p()

15-part uptrend condition

Returns: bool

ut_16p()

16-part uptrend condition

Returns: bool

ut_17p()

17-part uptrend condition

Returns: bool

ut_18p()

18-part uptrend condition

Returns: bool

ut_19p()

19-part uptrend condition

Returns: bool

ut_20p()

20-part uptrend condition

Returns: bool

ut_21p()

21-part uptrend condition

Returns: bool

ut_22p()

22-part uptrend condition

Returns: bool

ut_23p()

23-part uptrend condition

Returns: bool

ut_24p()

24-part uptrend condition

Returns: bool

ut_25p()

25-part uptrend condition

Returns: bool

ut_26p()

26-part uptrend condition

Returns: bool

ut_27p()

27-part uptrend condition

Returns: bool

ut_28p()

28-part uptrend condition

Returns: bool

ut_29p()

29-part uptrend condition

Returns: bool

ut_30p()

30-part uptrend condition

Returns: bool

rldt_1p()

1-part return line downtrend condition

Returns: bool

rldt_2p()

2-part return line downtrend condition

Returns: bool

rldt_3p()

3-part return line downtrend condition

Returns: bool

rldt_4p()

4-part return line downtrend condition

Returns: bool

rldt_5p()

5-part return line downtrend condition

Returns: bool

rldt_6p()

6-part return line downtrend condition

Returns: bool

rldt_7p()

7-part return line downtrend condition

Returns: bool

rldt_8p()

8-part return line downtrend condition

Returns: bool

rldt_9p()

9-part return line downtrend condition

Returns: bool

rldt_10p()

10-part return line downtrend condition

Returns: bool

rldt_11p()

11-part return line downtrend condition

Returns: bool

rldt_12p()

12-part return line downtrend condition

Returns: bool

rldt_13p()

13-part return line downtrend condition

Returns: bool

rldt_14p()

14-part return line downtrend condition

Returns: bool

rldt_15p()

15-part return line downtrend condition

Returns: bool

rldt_16p()

16-part return line downtrend condition

Returns: bool

rldt_17p()

17-part return line downtrend condition

Returns: bool

rldt_18p()

18-part return line downtrend condition

Returns: bool

rldt_19p()

19-part return line downtrend condition

Returns: bool

rldt_20p()

20-part return line downtrend condition

Returns: bool

rldt_21p()

21-part return line downtrend condition

Returns: bool

rldt_22p()

22-part return line downtrend condition

Returns: bool

rldt_23p()

23-part return line downtrend condition

Returns: bool

rldt_24p()

24-part return line downtrend condition

Returns: bool

rldt_25p()

25-part return line downtrend condition

Returns: bool

rldt_26p()

26-part return line downtrend condition

Returns: bool

rldt_27p()

27-part return line downtrend condition

Returns: bool

rldt_28p()

28-part return line downtrend condition

Returns: bool

rldt_29p()

29-part return line downtrend condition

Returns: bool

rldt_30p()

30-part return line downtrend condition

Returns: bool

dut()

double uptrend condition

Returns: bool

ddt()

double downtrend condition

Returns: bool

dut_1p()

1-part double uptrend condition

Returns: bool

dut_2p()

2-part double uptrend condition

Returns: bool

dut_3p()

3-part double uptrend condition

Returns: bool

dut_4p()

4-part double uptrend condition

Returns: bool

dut_5p()

5-part double uptrend condition

Returns: bool

dut_6p()

6-part double uptrend condition

Returns: bool

dut_7p()

7-part double uptrend condition

Returns: bool

dut_8p()

8-part double uptrend condition

Returns: bool

dut_9p()

9-part double uptrend condition

Returns: bool

dut_10p()

10-part double uptrend condition

Returns: bool

dut_11p()

11-part double uptrend condition

Returns: bool

dut_12p()

12-part double uptrend condition

Returns: bool

dut_13p()

13-part double uptrend condition

Returns: bool

dut_14p()

14-part double uptrend condition

Returns: bool

dut_15p()

15-part double uptrend condition

Returns: bool

dut_16p()

16-part double uptrend condition

Returns: bool

dut_17p()

17-part double uptrend condition

Returns: bool

dut_18p()

18-part double uptrend condition

Returns: bool

dut_19p()

19-part double uptrend condition

Returns: bool

dut_20p()

20-part double uptrend condition

Returns: bool

dut_21p()

21-part double uptrend condition

Returns: bool

dut_22p()

22-part double uptrend condition

Returns: bool

dut_23p()

23-part double uptrend condition

Returns: bool

dut_24p()

24-part double uptrend condition

Returns: bool

dut_25p()

25-part double uptrend condition

Returns: bool

dut_26p()

26-part double uptrend condition

Returns: bool

dut_27p()

27-part double uptrend condition

Returns: bool

dut_28p()

28-part double uptrend condition

Returns: bool

dut_29p()

29-part double uptrend condition

Returns: bool

dut_30p()

30-part double uptrend condition

Returns: bool

ddt_1p()

1-part double downtrend condition

Returns: bool

ddt_2p()

2-part double downtrend condition

Returns: bool

ddt_3p()

3-part double downtrend condition

Returns: bool

ddt_4p()

4-part double downtrend condition

Returns: bool

ddt_5p()

5-part double downtrend condition

Returns: bool

ddt_6p()

6-part double downtrend condition

Returns: bool

ddt_7p()

7-part double downtrend condition

Returns: bool

ddt_8p()

8-part double downtrend condition

Returns: bool

ddt_9p()

9-part double downtrend condition

Returns: bool

ddt_10p()

10-part double downtrend condition

Returns: bool

ddt_11p()

11-part double downtrend condition

Returns: bool

ddt_12p()

12-part double downtrend condition

Returns: bool

ddt_13p()

13-part double downtrend condition

Returns: bool

ddt_14p()

14-part double downtrend condition

Returns: bool

ddt_15p()

15-part double downtrend condition

Returns: bool

ddt_16p()

16-part double downtrend condition

Returns: bool

ddt_17p()

17-part double downtrend condition

Returns: bool

ddt_18p()

18-part double downtrend condition

Returns: bool

ddt_19p()

19-part double downtrend condition

Returns: bool

ddt_20p()

20-part double downtrend condition

Returns: bool

ddt_21p()

21-part double downtrend condition

Returns: bool

ddt_22p()

22-part double downtrend condition

Returns: bool

ddt_23p()

23-part double downtrend condition

Returns: bool

ddt_24p()

24-part double downtrend condition

Returns: bool

ddt_25p()

25-part double downtrend condition

Returns: bool

ddt_26p()

26-part double downtrend condition

Returns: bool

ddt_27p()

27-part double downtrend condition

Returns: bool

ddt_28p()

28-part double downtrend condition

Returns: bool

ddt_29p()

29-part double downtrend condition

Returns: bool

ddt_30p()

30-part double downtrend condition

Returns: bool

ICT Killzones and Sessions W/ Silver Bullet + MacrosForex and Equity Session Tracker with Killzones, Silver Bullet, and Macro Times

This Pine Script indicator is a comprehensive timekeeping tool designed specifically for ICT traders using any time-based strategy. It helps you visualize and keep track of forex and equity session times, kill zones, macro times, and silver bullet hours.

Features:

Session and Killzone Lines:

Green: London Open (LO)

White: New York (NY)

Orange: Australian (AU)

Purple: Asian (AS)

Includes AM and PM session markers.

Dotted/Striped Lines indicate overlapping kill zones within the session timeline.

Customization Options:

Display sessions and killzones in collapsed or full view.

Hide specific sessions or killzones based on your preferences.

Customize colors, texts, and sizes.

Option to hide drawings older than the current day.

Automatic Updates:

The indicator draws all lines and boxes at the start of a new day.

Automatically adjusts time-based boxes according to the New York timezone.

Killzone Time Windows (for indices):

London KZ: 02:00 - 05:00

New York AM KZ: 07:00 - 10:00

New York PM KZ: 13:30 - 16:00

Silver Bullet Times:

03:00 - 04:00

10:00 - 11:00

14:00 - 15:00

Macro Times:

02:33 - 03:00

04:03 - 04:30

08:50 - 09:10

09:50 - 10:10

10:50 - 11:10

11:50 - 12:50

Latest Update:

January 15:

Added option to automatically change text coloring based on the chart.

Included additional optional macro times per user request:

12:50 - 13:10

13:50 - 14:15

14:50 - 15:10

15:50 - 16:15

Usage:

To maximize your experience, minimize the pane where the script is drawn. This minimizes distractions while keeping the essential time markers visible. The script is designed to help traders by clearly annotating key trading periods without overwhelming their charts.

Originality and Justification:

This indicator uniquely integrates various time-based strategies essential for ICT traders. Unlike other indicators, it consolidates session times, kill zones, macro times, and silver bullet hours into one comprehensive tool. This allows traders to have a clear and organized view of critical trading periods, facilitating better decision-making.

Credits:

This script incorporates open-source elements with significant improvements to enhance functionality and user experience.

Forex and Equity Session Tracker with Killzones, Silver Bullet, and Macro Times

This Pine Script indicator is a comprehensive timekeeping tool designed specifically for ICT traders using any time-based strategy. It helps you visualize and keep track of forex and equity session times, kill zones, macro times, and silver bullet hours.

Features:

Session and Killzone Lines:

Green: London Open (LO)

White: New York (NY)

Orange: Australian (AU)

Purple: Asian (AS)

Includes AM and PM session markers.

Dotted/Striped Lines indicate overlapping kill zones within the session timeline.

Customization Options:

Display sessions and killzones in collapsed or full view.

Hide specific sessions or killzones based on your preferences.

Customize colors, texts, and sizes.

Option to hide drawings older than the current day.

Automatic Updates:

The indicator draws all lines and boxes at the start of a new day.

Automatically adjusts time-based boxes according to the New York timezone.

Killzone Time Windows (for indices):

London KZ: 02:00 - 05:00

New York AM KZ: 07:00 - 10:00

New York PM KZ: 13:30 - 16:00

Silver Bullet Times:

03:00 - 04:00

10:00 - 11:00

14:00 - 15:00

Macro Times:

02:33 - 03:00

04:03 - 04:30

08:50 - 09:10

09:50 - 10:10

10:50 - 11:10

11:50 - 12:50

Latest Update:

January 15:

Added option to automatically change text coloring based on the chart.

Included additional optional macro times per user request:

12:50 - 13:10

13:50 - 14:15

14:50 - 15:10

15:50 - 16:15

ICT Sessions and Kill Zones

What They Are:

ICT Sessions: These are specific times during the trading day when market activity is expected to be higher, such as the London Open, New York Open, and the Asian session.

Kill Zones: These are specific time windows within these sessions where the probability of significant price movements is higher. For example, the New York AM Kill Zone is typically from 8:30 AM to 11:00 AM EST.

How to Use Them:

Identify the Session: Determine which trading session you are in (London, New York, or Asian).

Focus on Kill Zones: Within that session, focus on the kill zones for potential trade setups. For instance, during the New York session, look for setups between 8:30 AM and 11:00 AM EST.

Silver Bullets

What They Are:

Silver Bullets: These are specific, high-probability trade setups that occur within the kill zones. They are designed to be "one shot, one kill" trades, meaning they aim for precise and effective entries and exits.

How to Use Them:

Time-Based Setup: Look for these setups within the designated kill zones. For example, between 10:00 AM and 11:00 AM for the New York AM session .

Chart Analysis: Start with higher time frames like the 15-minute chart and then refine down to 5-minute and 1-minute charts to identify imbalances or specific patterns .

Macros

What They Are:

Macros: These are broader market conditions and trends that influence your trading decisions. They include understanding the overall market direction, seasonal tendencies, and the Commitment of Traders (COT) reports.

How to Use Them:

Understand Market Conditions: Be aware of the macroeconomic factors and market conditions that could affect price movements.

Seasonal Tendencies: Know the seasonal patterns that might influence the market direction.

COT Reports: Use the Commitment of Traders reports to understand the positioning of large traders and commercial hedgers .

Putting It All Together

Preparation: Understand the macro conditions and review the COT reports.

Session and Kill Zone: Identify the trading session and focus on the kill zones.

Silver Bullet Setup: Look for high-probability setups within the kill zones using refined chart analysis.

Execution: Execute the trade with precision, aiming for a "one shot, one kill" outcome.

By following these steps, you can effectively use ICT sessions, kill zones, silver bullets, and macros to enhance your trading strategy.

Usage:

To maximize your experience, shrink the pane where the script is drawn. This minimizes distractions while keeping the essential time markers visible. The script is designed to help traders by clearly annotating key trading periods without overwhelming their charts.

Originality and Justification:

This indicator uniquely integrates various time-based strategies essential for ICT traders. Unlike other indicators, it consolidates session times, kill zones, macro times, and silver bullet hours into one comprehensive tool. This allows traders to have a clear and organized view of critical trading periods, facilitating better decision-making.

Credits:

This script incorporates open-source elements with significant improvements to enhance functionality and user experience. All credit goes to itradesize for the SB + Macro boxes

[imba]lance algo🟩 INTRODUCTION

Hello, everyone!

Please take the time to review this description and source code to utilize this script to its fullest potential.

🟩 CONCEPTS

This is a trend indicator. The trend is the 0.5 fibonacci level for a certain period of time.

A trend change occurs when at least one candle closes above the level of 0.236 (for long) or below 0.786 (for short). Also it has massive amout of settings and features more about this below.

With good settings, the indicator works great on any market and any time frame!

A distinctive feature of this indicator is its backtest panel. With which you can dynamically view the results of setting up a strategy such as profit, what the deposit size is, etc.

Please note that the profit is indicated as a percentage of the initial deposit. It is also worth considering that all profit calculations are based on the risk % setting.

🟩 FEATURES

First, I want to show you what you see on the chart. And I’ll show you everything closer and in more detail.

1. Position

2. Statistic panel

3. Backtest panel

Indicator settings:

Let's go in order:

1. Strategies

This setting is responsible for loading saved strategies. There are only two preset settings, MANUAL and UNIVERSAL. If you choose any strategy other than MANUAL, then changing the settings for take profits, stop loss, sensitivity will not bring any results.

You can also save your customized strategies, this is discussed in a separate paragraph “🟩HOW TO SAVE A STRATEGY”

2. Sensitive

Responsible for the time period in bars to create Fibonacci levels

3. Start calculating date

This is the time to start backtesting strategies

4. Position group

Show checkbox - is responsible for displaying positions

Fill checkbox - is responsible for filling positions with background

Risk % - is responsible for what percentage of the deposit you are willing to lose if there is a stop loss

BE target - here you can choose when you reach which take profit you need to move your stop loss to breakeven

Initial deposit- starting deposit for profit calculation

5. Stoploss group

Fixed stoploss % checkbox - If choosed: stoploss will be calculated manually depending on the setting below( formula: entry_price * (1 - stoploss percent)) If NOT choosed: stoploss will be ( formula: fibonacci level(0.786/0.236) * (1 + stoploss percent))

6. Take profit group

This group of settings is responsible for how far from the entry point take profits will be and what % of the position to fix

7. RSI

Responsible for configuring the built-in RSI. Suitable bars will be highlighted with crosses above or below, depending on overbought/oversold

8. Infopanels group

Here I think everything is clear, you can hide or show information panels

9. Developer mode

If enabled, all events that occur will be shown, for example, reaching a take profit or stop loss with detailed information about the unfixed balance of the position

🟩 HOW TO USE

Very simple. All you need is to wait for the trend to change to long or short, you will immediately see a stop loss and four take profits, and you will also see prices. Like in this picture:

🟩 ALERTS

There are 3 types of alerts:

1. Long signal

2. Short signal

3. Any alert() function call - will be send to you json with these fields

{

"side": "LONG",

"entry": "64.454",

"tp1": "65.099",

"tp2": "65.743",

"tp3": "66.388",

"tp4": "67.032",

"winrate": "35.42%",

"strategy": "MANUAL",

"beTargetTrigger": "1",

"stop": "64.44"

}

🟩 HOW TO SAVE A STRATEGY

First, you need to make sure that the “MANUAL” strategy is selected in the strategy settings.

After this, you can start selecting parameters that will show the largest profit in the statistics panel.

I have highlighted what you need to pay attention to when choosing a strategy

Let's assume you have set up a strategy. The main question is how to preserve it?

Let’s say the strategy turned out with the following parameters:

Next we need to find this section of code:

// STRATS

selector(string strategy_name) =>

strategy_settings = Strategy_settings.new()

switch strategy_name

"MANUAL" =>

strategy_settings.sensitivity := 18

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"UNIVERSAL" =>

strategy_settings.sensitivity := 20

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

// "NEW STRATEGY" =>

// strategy_settings.sensitivity := 20

// strategy_settings.risk_percent := 1

// strategy_settings.break_even_target := "1"

// strategy_settings.tp1_percent := 1

// strategy_settings.tp1_percent_fix := 40

// strategy_settings.tp2_percent := 2

// strategy_settings.tp2_percent_fix := 30

// strategy_settings.tp3_percent := 3

// strategy_settings.tp3_percent_fix := 20

// strategy_settings.tp4_percent := 4

// strategy_settings.tp4_percent_fix := 10

// strategy_settings.fixed_stop := false

// strategy_settings.sl_percent := 0.0

strategy_settings

// STRATS

Let's uncomment on the latest strategy called "NEW STRATEGY" rename it to "SOL 5m" and change the sensitivity:

// STRATS

selector(string strategy_name) =>

strategy_settings = Strategy_settings.new()

switch strategy_name

"MANUAL" =>

strategy_settings.sensitivity := 18

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"UNIVERSAL" =>

strategy_settings.sensitivity := 20

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"SOL 5m" =>

strategy_settings.sensitivity := 15

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

strategy_settings

// STRATS

Now let's find this code:

strategy_input = input.string(title = "STRATEGY", options = , defval = "MANUAL", tooltip = "EN:\nTo manually configure the strategy, select MANUAL otherwise, changing the settings won't have any effect\nRU:\nЧтобы настроить стратегию вручную, выберите MANUAL в противном случае изменение настроек не будет иметь никакого эффекта")

And let's add our new strategy there, it turned out like this:

strategy_input = input.string(title = "STRATEGY", options = , defval = "MANUAL", tooltip = "EN:\nTo manually configure the strategy, select MANUAL otherwise, changing the settings won't have any effect\nRU:\nЧтобы настроить стратегию вручную, выберите MANUAL в противном случае изменение настроек не будет иметь никакого эффекта")

That's all. Our new strategy is now saved! It's simple! Now we can select it in the list of strategies:

HighLowBox+220MAs[libHTF]HighLowBox+220MAs

This is a sample script of libHTF to use HTF values without request.security().

import nazomobile/libHTFwoRS/1

HTF candles are calculated internally using 'GMT+3' from current TF candles by libHTF .

To calcurate Higher TF candles, please display many past bars at first.

The advantage and disadvantage is that the data can be generated at the current TF granularity.

Although the signal can be displayed more sensitively, plots such as MAs are not smooth.

In this script, assigned ➊,➋,➌,➍ for htf1,htf2,htf3,htf4.

HTF candles

Draw candles for HTF1-4 on the right edge of the chart. 2 candles for each HTF.

They are updated with every current TF bar update.

Left edge of HTF candles is located at the x-postion latest bar_index + offset.

DMI HTF

ADX/+DI/DI arrows(8lines) are shown each timeframes range.

Current TF's is located at left side of the HighLowBox.

HTF's are located at HighLowBox of HTF candles.

The top of HighLowBox is 100, The bottom of HighLowBox is 0.

HighLowBox HTF

Enclose in a square high and low range in each timeframe.

Shows price range and duration of each box.

In current timeframe, shows Fibonacci Scale inside(23.6%, 38.2%, 50.0%, 61.8%, 76.4%)/outside of each box.

Outside(161.8%,261.8,361.8%) would be shown as next target, if break top/bottom of each box.

In HTF, shows Fibonacci Level of the current price at latest box only.

Boxes:

1 for current timeframe.

4 for higher timeframes.(Steps of timeframe: 5, 15, 60, 240, D, W, M, 3M, 6M, Y)

HighLowBox TrendLine

Draw TrendLine for each HighLow Range. TrendLine is drawn between high and return high(or low and return low) of each HighLowBox.

Style of TrendLine is same as each HighLowBox.

HighLowBox RSI

RSI Signals are shown at the bottom(RSI<=30) or the top(RSI>=70) of HighLowBox in each timeframe.

RSI Signal is color coded by RSI9 and RSI14 in each timeframe.(current TF: ●, HTF1-4: ➊➋➌➍)

In case of RSI<=30, Location: bottom of the HighLowBox

white: only RSI9 is <=30

aqua: RSI9&RSI14; <=30 and RSI9RSI14

green: only RSI14 <=30

In case of RSI>=70, Location: top of the HighLowBox

white: only RSI9 is >=70

yellow: RSI9&RSI14; >=70 and RSI9>RSI14

orange: RSI9&RSI14; >=70 and RSI9=70

blue/green and orange/red could be a oversold/overbought sign.

20/200 MAs

Shows 20 and 200 MAs in each TFs(tfChart and 4 Higher).

TFs:

current TF

HTF1-4

MAs:

20SMA

20EMA

200SMA

200EMA

Physics CandlesPhysics Candles embed volume and motion physics directly onto price candles or market internals according to the cyclic pattern of financial securities. The indicator works on both real-time “ticks” and historical data using statistical modeling to highlight when these values, like volume or momentum, is unusual or relatively high for some periodic window in time. Each candle is made out of one or more sub-candles that each contain their own information of motion, which converts to the color and transparency, or brightness, of that particular candle segment. The segments extend throughout the entire candle, both body and wicks, and Thick Wicks can be implemented to see the color coding better. This candle segmentation allows you to see if all the volume or energy is evenly distributed throughout the candle or highly contained in one small portion of it, and how intense these values are compared to similar time periods without going to lower time frames. Candle segmentation can also change a trader’s perspective on how valuable the information is. A “low” volume candle, for instance, could signify high value short-term stopping volume if the volume is all concentrated in one segment.

The Candles are flexible. The physics information embedded on the candles need not be from the same price security or market internal as the chart when using the Physics Source option, and multiple Candles can be overlayed together. You could embed stock price Candles with market volume, market price Candles with stock momentum, market structure with internal acceleration, stock price with stock force, etc. My particular use case is scalping the SPX futures market (ES), whose price action is also dictated by the volume action in the associated cash market, or SPY, as well as a host of other securities. Physics allows you to embed the ES volume on the SPY price action, or the SPY volume on the ES price action, or you can combine them both by overlaying two Candle streams and increasing the Number of Overlays option to two. That option decreases the transparency levels of your coloring scheme so that overlaying multiple Candles converges toward the same visual color intensity as if you had one. The Candle and Physics Sources allows for both Symbols and Spreads to visualize Candle physics from a single ticker or some mathematical transformation of tickers.

Due to certain TradingView programming restrictions, each Candle can only be made out of a maximum of 8 candle segments, or an “8-bit” resolution. Since limits are just an opportunity to go beyond, the user has the option to stack multiple Candle indicators together to further increase the candle resolution. If you don’t want to see the Candles for some particular period of the day, you can hide them, or use the hiding feature to have multiple Candles calibrated to show multiple parts of the trading day. Securities tend to have low volume after hours with sharp spikes at the open or close. Multiple Candles can be used for multiple parts of the trading day to accommodate these different cycles in volume.

The Candles do not need be associated with the nominal security listed on the TV chart. The Candle Source allows the user to look at AAPL Candles, for instance, while on a TSLA or SPY chart, each with their respective volume actions integrated into the candles, for instance, to allow the user to see multiple security price and volume correlation on a single chart.

The physics information currently embeddable on Candles are volume or time, velocity, momentum, acceleration, force, and kinetic energy. In order to apply equations of motion containing a mass variable to financial securities, some analogous value for mass must be assumed. Traders often regard volume or time as inextricable variables to a securities price that can indicate the direction and strength of a move. Since mass is the inextricable variable to calculating the momentum, force, or kinetic energy of motion, the user has the option to assume either time or volume is analogous to mass. Volume may be a better option for mass as it is not strictly dependent on the speed of a security, whereas time is.

Data transformations and outlier statistics are used to color code the intensity of the physics for each candle segment relative to past periodic behavior. A million shares during pre-market or a million shares during noontime may be more intense signals than a typical million shares traded at the open, and should have more intense color signals. To account for a specific cyclic behavior in the market, the user can specify the Window and Cycle Time Frames. The Window Time Frame splits up a Cycle into windows, samples and aggregates the statistics for each window, then compares the current physics values against past values in the same window. Intraday traders may benefit from using a Daily Cycle with a 30-minute Window Time Frame and 1-minute Sample Time Frame. These settings sample and compare the physics of 1-minute candles within the current 30-minute window to the same 30-minute window statistics for all past trading days, up until the data limit imposed by TradingView, or until the Data Collection Start Date specified in the settings. Longer-term traders may benefit from using a Monthly Cycle with a Weekly Time Frame, or a Yearly Cycle with a Quarterly Time Frame.

Multiple statistics and data transformation methods are available to convey relative intensity in different ways for different trading signals. Physics Candles allows for both Normal and Log-Normal assumptions in the physics distribution. The data can then be transformed by Linear, Logarithmic, Z-Score, or Power-Law scoring, where scoring simply assigns an intensity to the relative physics value of each candle segment based on some mathematical transformation. Z-scoring often renders adequate detection by scoring the segment value, such as volume or momentum, according to the mean and standard deviation of the data set in each window of the cycle. Logarithmic or power-law transformation with a gamma below 1 decreases the disparity between intensities so more less-important signals will show up, whereas the power-law transformation with gamma values above 1 increases the disparity between intensities, so less more-important signals will show up. These scores are then converted to color and transparency between the Min Score and the Max Score Cutoffs. The Auto-Normalization feature can automatically pick these cutoffs specific to each window based on the mean and standard deviation of the data set, or the user can manually set them. Physics was developed with novices in mind so that most users could calibrate their own settings by plotting the candle segment distributions directly on the chart and fiddling with the settings to see how different cutoffs capture different portions of the distribution and affect the relative color intensities differently. Security distributions are often skewed with fat-tails, known as kurtosis, where high-volume segments for example, have a higher-probabilities than expected for a normal distribution. These distribution are really log-normal, so that taking the logarithm leads to a standard bell-shaped distribution. Taking the Z-score of the Log-Normal distribution could make the most statistical sense, but color sensitivity is a discretionary preference.

Background Philosophy

This indicator was developed to study and trade the physics of motion in financial securities from a visually intuitive perspective. Newton’s laws of motion are loosely applied to financial motion:

“A body remains at rest, or in motion at a constant speed in a straight line, unless acted upon by a force”.

Financial securities remain at rest, or in motion at constant speed up or down, unless acted upon by the force of traders exchanging securities.

“When a body is acted upon by a force, the time rate of change of its momentum equals the force”.

Momentum is the product of mass and velocity, and force is the product of mass and acceleration. Traders render force on the security through the mass of their trading activity and the acceleration of price movement.

“If two bodies exert forces on each other, these forces have the same magnitude but opposite directions.”

Force arises from the interaction of traders, buyers and sellers. One body of motion, traders’ capitalization, exerts an equal and opposite force on another body of motion, the financial security. A securities movement arises at the expense of a buyer or seller’s capitalization.

Volume

The premise of this indicator assumes that volume, v, is an analogous means of measuring physical mass, m. This premise allows the application of the equations of motion to the movement of financial securities. We know from E=mc^2 that mass has energy. Energy can be used to create motion as kinetic energy. Taking a simple hypothetical example, the interaction of one short seller looking to cover lower and one buyer looking to sell higher exchange shares in a security at an agreed upon price to create volume or mass, and therefore, potential energy. Eventually the short seller will actively cover and buy the security from the previous buyer, moving the security higher, or the buyer will actively sell to the short seller, moving the security lower. The potential energy inherent in the initial consolidation or trading activity between buy and seller is now converted to kinetic energy on the subsequent trading activity that moves the securities price. The more potential energy that is created in the consolidation, the more kinetic energy there is to move price. This is why point and figure traders are said to give price targets based on the level of volatility or size of a consolidation range, or why Gann traders square price and time, as time is roughly proportional to mass and trading activity. The build-up of potential energy between short sellers and buyers in GME or TSLA led to their explosive moves beyond their standard fundamental valuations.

Position

Position, p, is simply the price or value of a financial security or market internal.

Time

Time, t, is another means of measuring mass to discover price behavior beyond the time snapshots that simple candle charts provide. We know from E=mc^2 that time is related to rest mass and energy given the speed of light, c, where time ≈ distance * sqrt(mass/E). This relation can also be derived from F=ma. The more mass there is, the longer it takes to compute the physics of a system. The more energy there is, the shorter it takes to compute the physics of a system. Similarly, more time is required to build a “resting” low-volatility trading consolidation with more mass. More energy added to that trading consolidation by competing buyers and sellers decreases the time it takes to build that same mass. Time is also related to price through velocity.

Velocity = (p(t1) – p(t0)) / p(t0)

Velocity, v, is the relative percent change of a securities price, p, over a period of time, t0 to t1. The period of time is between subsequent candles, and since time is constant between candles within the same timeframe, it is not used to calculate velocity or acceleration. Price moves faster with higher velocity, and slower with slower velocity, over the same fixed period of time. The product of velocity and mass gives momentum.

Momentum = mv

This indicator uses physics definition of momentum, not finance’s. In finance, momentum is defined as the amount of change in a securities price, either relative or absolute. This is definition is unfortunate, pun intended, since a one dollar move in a security from a thousand shares traded between a few traders has the exact same “momentum” as a one dollar move from millions of shares traded between hundreds of traders with everything else equal. If momentum is related to the energy of the move, momentum should consider both the level of activity in a price move, and the amount of that price move. If we equate mass to volume to account for the level of trading activity and use physics definition of momentum as the product of mass and velocity, this revised definition now gives a thousand-times more momentum to a one-dollar price move that has a thousand-times more volume behind it. If you want to use finance’s volume-less definition of momentum, use velocity in this indicator.

Acceleration = v(t1) – v(t0)

Acceleration, a, is the difference between velocities over some period of time, t0 to t1. Positive acceleration is necessary to increase a securities speed in the positive direction, while negative acceleration is necessary to decrease it. Acceleration is related to force by mass.

Force = ma

Force is required to change the speed of a securities valuation. Price movements with considerable force have considerably more impact on future direction. A change in direction requires force.

Kinetic Energy = 0.5mv^2

Kinetic energy is the energy that a financial security gains from the change in its velocity by force. The built-up of potential energy in trading consolidations can be converted to kinetic energy on a breakout from the consolidation.

Cycle Theory and Relativity

Just as the physics of motion is relative to a point of reference, so too should the physics of financial securities be relative to a point of reference. An object moving at a 100 mph towards another object moving in the same direction at 100 mph will not appear to be moving relative to each other, nor will they collide, but from an outsider observer, the objects are going 100 mph and will collide with significant impact if they run into a stationary object relative to the observer. Similarly, trading with a hundred thousand shares at the open when the average volume is a couple million may have a much smaller impact on the price compared to trading a hundred thousand shares pre-market when the average volume is ten thousand shares. The point of reference used in this indicator is the average statistics collected for a given Window Time Frame for every Cycle Time Frame. The physics values are normalized relative to these statistics.

Examples

The main chart of this publication shows the Force Candles for the SPY. An intense force candle is observed pre-market that implicates the directional overtone of the day. The assumption that direction should follow force arises from physical observation. If a large object is accelerating intensely in a particular direction, it may be fair to assume that the object continues its direction for the time being unless acted upon by another force.

The second example shows a similar Force Candle for the SPY that counters the assumption made in the first example and emphasizes the importance of both motion and context. While it’s fair to assume that a heavy highly accelerating object should continue its course, if that object runs into an obstacle, say a brick wall, it’s course may deviate. This example shows SPY running into the 50% retracement wall from the low of Mar 2020, a significant support level noted in literature. The example also conveys Gann’s idea of “lost motion”, where the SPY penetrated the 50% price but did not break through it. A brick wall is not one atom thick and price support is not one tick thick. An object can penetrate only one layer of a wall and not go through it.

The third example shows how Volume Candles can be used to identify scalping opportunities on the SPY and conveys why price behavior is as important as motion and context. It doesn’t take a brick wall to impede direction if you know that the person driving the car tends to forget to feed the cats before they leave. In the chart below, the SPY breaks down to a confluence of the 5-day SMA, 20-day SMA, and an important daily trendline (not shown) after the bullish bounce from the 50% retracement days earlier. High volume candles on the SMA signify stopping volume that reverse price direction. The character of the day changes. Bulls become more aggressive than bears with higher volume on upswings and resistance, whiles bears take on a defensive position with lower volume on downswings and support. High volume stopping candles are seen after rallies, and can tell you when to take profit, get out of a position, or go short. The character change can indicate that its relatively safe to re-enter bullish positions on many major supports, especially given the overarching bullish theme from the large reaction off the 50% retracement level.

The last example emphasizes the importance of relativity. The Volume Candles in the chart below are brightest pre-market even though the open has much higher volume since the pre-market activity is much higher compared to past pre-markets than the open is compared to past opens. Pre-market behavior is a good indicator for the character of the day. These bullish Volume Candles are some of the brightest seen since the bounce off the 50% retracement and indicates that bulls are making a relatively greater attempt to bring the SPY higher at the start of the day.

Infrequently Asked Questions

Where do I start?

The default settings are what I use to scalp the SPY throughout most of the extended trading day, on a one-minute chart using SPY volume. I also overlay another Candle set containing ES future volume on the SPY price structure by setting the Physics Source to ES1! and the Number of Overlays setting to 2 for each Candle stream in order to account for pre- and post-market trading activity better. Since the closing volume is exponential-like up until the end of the regular trading day, adding additional Candle streams with a tighter Window Time Frame (e.g., 2-5 minute) in the last 15 minutes of trading can be beneficial. The Hide feature can allow you to set certain intraday timeframes to hide one Candle set in order to show another Candle set during that time.

How crazy can you get with this indicator?

I hope you can answer this question better. One interesting use case is embedding the velocity of market volume onto an internal market structure. The PCTABOVEVWAP.US is a market statistic that indicates the percent of securities above their VWAP among US stocks and is helpful for determining short term trends in the US market. When securities are rising above their VWAP, the average long is up on the day and a rising PCTABOVEVWAP.US can be viewed as more bullish. When securities are falling below their VWAP, the average short is up on the day and a falling PCTABOVEVWAP.US can be viewed as more bearish. (UPVOL.US - DNVOL.US) / TVOL.US is a “spread” symbol, in TV parlance, that indicates the decimal percent difference between advancing volume and declining volume in the US market, showing the relative flow of volume between stocks that are up on the day, and stocks that are down on the day. Setting PCTABOVEVWAP.US in the Candle Source, (UPVOL.US - DNVOL.US) / TVOL.US in the Physics Source, and selecting the Physics to Velocity will embed the relative velocity of the spread symbol onto the PCTABOVEVWAP.US candles. This can be helpful in seeing short term trends in the US market that have an increasing amount of volume behind them compared to other trends. The chart below shows Volume Candles (top) and these Spread Candles (bottom). The first top at 9:30 and second top at 10:30, the high of the day, break down when the spread candles light up, showing a high velocity volume transfer from up stocks to down stocks.

How do I plot the indicator distribution and why should I even care?

The distribution is visually helpful in seeing how different normalization settings effect the distribution of candle segments. It is also helpful in seeing what physics intensities you want to ignore or show by segmenting part of the distribution within the Min and Max Cutoff values. The intensity of color is proportional to the physics value between the Min and Max Cutoff values, which correspond to the Min and Max Colors in your color scheme. Any physics value outside these Min and Max Cutoffs will be the same as the Min and Max Colors.

Select the Print Windows feature to show the window numbers according to the Cycle Time Frame and Window Time Frame settings. The window numbers are labeled at the start of each window and are candle width in size, so you may need to zoom into to see them. Selecting the Plot Window feature and input the window number of interest to shows the distribution of physics values for that particular window along with some statistics.