OpenCipher AOpenCipher A is an open-source and free to use Overlay.

Features:

EMA Ribbons (Lengths: 5, 11, 15, 18, 21, 25, 29, 33)

Symbols ("Be careful" and "attention required" signals)

EMA Ribbons

The EMA RIbbons are a set of exponential moving averages. Blue and white ribbons = uptrend, gray ribbons = downtrend. The ribbons can act as support in uptrends and as resistance in downtrends.

Lengths and source of the ribbons are customizable.

Symbols

Green Dots: The green dot is a bullish symbol that appears whenever the EMA 11 crosses over EMA 33.

Red Cross: The red cross is a bearish symbol that appears whenever the EMA 5 crosses under EMA 11.

Blue Triangle: The blue triangle marks a possible trend reversal that appears whenever the EMA 5 crosses over EMA 25 while EMA 29 is below EMA 33.

Red Diamond: The red diamond is a bearish symbol that marks a potential local top whenever a bearish wavecross occurs (fast wave crosses under slow wave).

Yellow X: The yellow X is a warning signal that appears whenever a bearish wavecross occurs while the slow wave of the wavetrend is below -40 and the moneyflow is in the red (below zero).

Blood Diamond: The blood diamond is a bearish symbol that highlights whenever the red diamond and the red cross appear on the same candle.

Usage

Treat the symbols as signs that your attention might be required and don't trade based on them.

ابحث في النصوص البرمجية عن "英国央行降息25个基点"

BB-RSI-ADX Entry PointsThis is a combination of indicators used to find oversold and overbought entry points for possible reversion.

A Green arrow will appear when all condition are met for an ENTER LONG position.

A Red arow will appear when all condition are met for an ENTER SHORT position.

You can modify all of these condition parameters from the indicator's settings.

How does the indicator work

The signals are using Bollinger Bands , BB %B , RSI and ADX indicators to try and find points of reversal

Enter LONG Conditions

Current candle low is below BB lower band.

The BB %B is more than 0.

RSI > 30

ADX > 25

Enter SHORT Conditions

Current candle high is above BB upper band.

The BB %B is less than 1.

RSI < 70

ADX > 25

Those are the default settings that seem to work for me but you can customize all of these from the indicator settings.

I find this strategy to best work on a 3 minute timeframe

Note: The bb %B is calculated for stDev - 1. This will help you see a change happening faster.

MTF RSI ScannerThis RSI scanner can be use to identify the relative strength of 10 symbols over multiple timeframes

it will give you a quick overview which pair is more bearish or more bullish and also signals tops and bottoms in the AVG row

light red/green cell = weak bearish (RSI = 45-35) / bullish (RSI = 55-65)

medium red/green cell = bearish (RSI = 35-25) / bullish (RSI = 65-75)

dark red/green cell = strong bearish (RSI <= 25) / bullish (RSI >= 75)

gray cell = neutral (RSI= 45-55)

Usage

If AVG (average of all 4 timeframes) falls below 30, the cell will get green, indicating a good time to enter long (buy)

If AVG (average of all 4 timeframes) rises above 70, the cell will get red, indicating a good time to enter short (sell)

Use the "MTF RSI Scanner" in combination with the "MTF Stochastic Scanner"

to find tops (RSI MTF avg >=70 AND Stochastic MTF avg >= 80)

or bottoms (RSI MTF avg <= 30 AND Stochastic MTF avg <= 20)

Here is how the two MTF scanners looked on Nov 08 2021 (ATH) »

and here how the MTF scanners looked on June 21 2022

use TradingViews Replay function to check how it would have worked in the past and when not.

As always… there NOT a single indicator that can show to the top & bottom 100% every single time. So use with caution, with other indicators and/or deeper understanding of technicals analysis ☝️☝️☝️

Settings

You can change the timeframes, symbols, RSI settings, overbought/oversold levels and colors to your liking

Drag the table onto the price chart, if you want to use it as an overlay.

NOTE:

Because of the 4x10 security requests, it can take up to 1 minute for changed settings to take effect! Please be patient 🙃

If you have any idea on how to optimise the code, please feel free to share 🙏

*** Inspired by "Binance CHOP Dashboard" from @Cazimiro and "RSI MTF Table" from @mobester16 ***

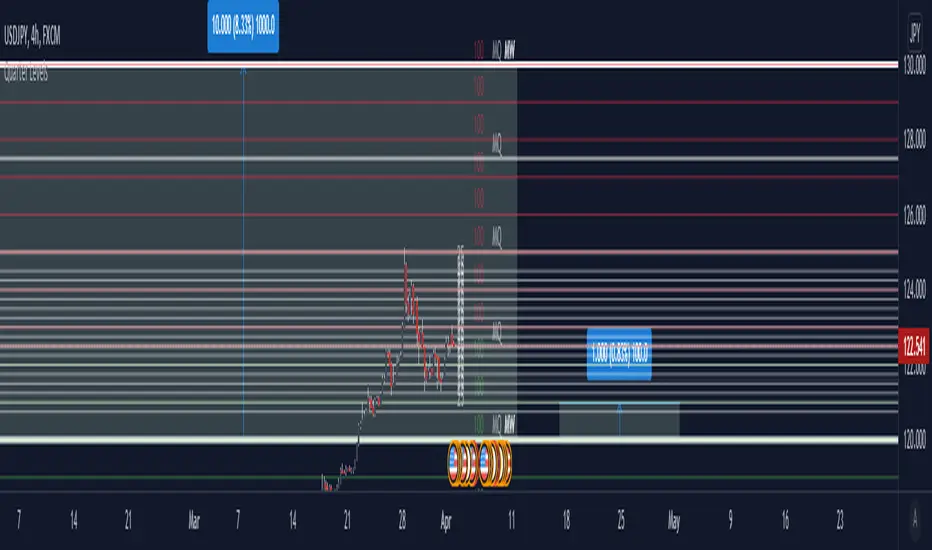

Quarter theory and whole numbersThis is an indicator that marks off Major whole/quarter levels

Between each major whole they are 1000 pips and that can be quarter and give you major quarter levels of 250 pips

Each of the major whole number can be divided into 10 - 100 pip ranges(giving you minor whole number), and you can in turn quarter these to give you 25 pips.

This is the lowest value you would need as price moves in 25 pip.

You can use this on any market as long as you can figure out the conversion from price into pips for you assets (This varies).

crypto futures hourly scalping with ma & rsi - ogcheckershi to all lovable traders,

hereby i want to share a combination of trade ideas for scalping

i've chosen hourly timeframe

indicators used: moving averages and rsi

moving averages:

ema 3, ema 5, ema 7

sma 3, sma 5, sma 7

daily_ema_3, daily_ema_5

daily_ema_5, daily_sma_5

rsi:

rsi 7, rsi 14, rsi 26

daily_rsi_7, daily_rsi_14, daily_rsi_26

as per the analysis over moving average behavioral patterns & rsi movements, useful points are given below which will be helpful while choosing good entry points & exit points,

strategical points for LONG:

* when ema3 crosses above sma3 - green candles start to form

* it's followed by ema5 > sma5 and ema7 > sma7

* when ema3 crosses down sma3 - it's considered as an indication of exit

* if rsi supports then can wait for ema5 crossing down sma5

* as similar, when daily_ema_3 crosses above daily_sma_3, its an higher timeframe bullish indication, so the lower timeframe entries inside this higher timeframe is a sure shot confident entry

* for LONG always take entries when rsi_14 < 30 or 25 else check rsi_7 < 25 or below

* as along the above, bullish CANDLE patterns like bullish engulfing , morning star is been used for entry at lower levels

* so here i've used OPEN as rsi_source in majority

* exit points also indicated at high_rsi and moving average crossunders or reverse crossovers

* for SHORTING, the above said ideas can be used in viceversa

* inputs in the indicator were tailored for users needs so that you will enjoy the magics of customization

if i am wrong in anyways regarding the above indicator strategy, please forgive me and help me improve in this aspect by commenting.

after few more studies and analysis and mainly QUERIES & COMMENTS, i'm planning to backtest these strategies here in tradingview.

also if these strategies are coded in python, we can link it to Binance Futures Algo or Bot Trading.

thankyou for this opportunity,

thanks to tradingview and pinecoders

thanks to Pranab (for 365MA)

thanks to Gandalf (for inspiring)

Special Thanks & Love to Chartbank for Everything

BTC Cap Dominance RSI StrategyThis strategy is based on the BTC Cap Dominance RSI indicator, which is a combination of the RSI of Bitcoin Market Cap and the RSI of Bitcoin Dominance. The concept of this strategy is to get a good grasp of the bitcoin market flow by combining bitcoin dominance as well as bitcoin market cap.

BTC Cap Dominance (BCD) RSI is defined as:

BCD RSI = (BTC Cap RSI + BTC Dominance RSI) / 2

Case 1 (Bull market):

Both Cap RSI and Dominance RSI values are high

Case 2 (Neutral market):

Cap RSI is high but Dominance RSI is low

Cap RSI is low but Dominance RSI is high

Case 3 (Bear market):

Both Cap RSI and Dominance RSI values are low

When the BCD RSI value closes the candle above the Bull level, it triggers a long signal and when the value closes below the Bear level, it triggers a short signal.

(Note) Please note that TradingView's market cap symbols (CRYPTOCAP:TOTAL and CRYPTOCAP:TOTAL2) started in January 2020, so strategy backtesting is possible from this point on.

(Note) Since the real-time BCD RSI value does not come out with this strategy, it is recommended to use it together because the current value can be known and the long-short signal can be predicted in advance by using a separate BCD RSI Index together.

If "Use Combination of dominance RSI ?" is not checked in addition to the recommended default value of the strategy, the recommended values are Length (14), Bull level (74), Bear level (25).

_______________________________________________________________________

이 전략은 비트코인 시가총액의 RSI와 비트코인 도미넌스 RSI를 조합하여 만든 BTC Cap Dominance RSI 지표를 기반으로 만들어졌습니다. 이 전략의 컨셉은 비트코인 시가총액뿐만 아니라 비트코인 도미넌스를 조합함으로써 비트코인 시장 흐름을 잘 파악할 수 있도록 하는 것입니다.

BTC Cap Dominance (BCD) RSI는 다음과 같이 정의하였습니다.

BCD RSI = (BTC Cap RSI + BTC Dominance RSI) / 2

Case 1 (강세 장):

Cap RSI와 Dominance RSI 값 모두 높은 경우

Case 2 (횡보 장):

Cap RSI는 높지만 Dominance RSI는 낮은 경우

Cap RSI는 낮지만 Dominance RSI는 높은 경우

Case 3 (약세 장):

Cap RSI와 Dominance RSI 값 모두 낮은 경우

BCD RSI 값이 Bull level 위에서 캔들 마감할 경우 long 신호를 트리거하고 Bear level 아래에서 캔들 마감할 경우 short 신호를 트리거합니다.

(주의) 트레이딩뷰의 시가총액 심볼들 (CRYPTOCAP:TOTAL과 CRYPTOCAP:TOTAL2)이 2020년 1월부터 시작하였으므로 이 시점부터 전략 백테스팅이 가능한 점을 유의하십시오.

(주의) 이 전략은 실시간 BCD RSI 값이 나오지 않기 때문에 별도의 BCD RSI Index를 함께 사용하면 현재 값을 알 수 있어 롱숏 신호를 사전에 예측할 수 있으므로 함께 사용하기를 권장합니다.

전략의 추천 기본값 외에 "Use Combination of dominance RSI ?"를 체크하지 않는 경우 권장하는 값은 Length (14), Bull level (74), Bear level (25) 입니다.

Margin Zones[kryptodude]This indicator is based on the margin requirements of the CME exchange.

Zones act as support and resistance levels, which are more likely to have a price reaction.

The recommended zones for entering a position, as well as taking profits, are zones 50 and 100.

For example, you decide to open a short position on the +100 zone,

in which case it is recommended to place a stop-loss behind the zone.

Take-profit part at -50 and -100, based on the zones from the formed maximum at the +100 zone.

Settings:

Select the currency pair and the exchange on which the indicator will work, For example BINANCE:BTCUSD

"Margin" (for example,now 68280, the next day the margin will be different)

"Tick cost" for BTC = 25 or 12.5

taken from the CME exchange.

"Price max"- High yesterday (for example 44451).

"Price min"- Low yesterday (for example 41280).

Please note, with strong volatility,

it is recommended to change the Tick cost instead of 25 to put 12.5

And also, only dots " . " not commas ", " work in the indicator.

Joint Conditions Strategy Suite + TradingConnector alerts bot"Please give us combined alerts with the possibility of having several conditions in place to trigger the alert." - was the top voted request from users under one of the recent blogposts by TradingView.

Ask and you shall receive ;)

TradingView is a great platform, with unmatched set of functionalities, yet this particular combo of features indeed seems not to be in place. Fortunately, TradingView is also very open platform, thanks to PineScript coding language, which enables developing combos like the requried one and plenty of other magic.

I have already published numerous "educational" scripts, showing how to code indicators and alerts with PineScript, but... this is not one of them. This one is for real. READY FOR USE on real markets, also by the non-coding traders. Just take my script, set parameters with dropdowns, backtest the strategy, fire the alerts and execute them.

HOW TO USE IT

In "Settings" popup I tried to mimic the CreateAlert popup dropdowns for selecting logic. Let's say you want to enter Long position at Stochastic KxD crossover. In first line of Long Entry conditions set "StochK" + "Crossing Up" + "StochD". Last field doesn't matter because in 3rd dropdown something else than "value" was selected. In second line you could set "maB" + "Greater Than" + "maC" to filter out those entries which are in direction of the uptrend. And yeah, add ADX>25 to make sure the market is actually moving: "ADX" + "Greater Than" + "value" + "25". All condition lines must be TRUE (or skipped) for the entry to be triggered. Toghether with an alert.

The same for Short entries. Combinations are limitless.

INDICATORS AND MTF (MULTI-TIMEFRAME)

In those dropdowns you can select candle values like open/close/high/low/ohlc4, but also some most popular indicators, which I have pre-built into this script: RSI, various Moving Averages, ADX-DMI, Stochastic and Bollinger Bands for start. You can configure parameters of those indicators also in "Settings" popup, in "Indicator Definitions" section. What's important, you can use any of these indicators from higher timeframe, setting MTF multiplier. So if you applied this indicator to 1h chart, but want to use rsi(close,14) from 4h chart, set MTF to 4. If you want to use current timeframe indicators, keep MTF at 1, which is a default setting here.

Note for coders: to keep focus of this script on joining conditions, entire logic for those indicators has been moved to external library, also open source. I encourage you to dig into the code and see how it's done. I love the addition of libraries concept in PineScript.

CUSTOM INDICATOR

Following the "openness" spirit of my master - which is TradingView itself - my work is also open, in 2 ways:

1. This script is open source. So you can grab it, modify or add any functionalities you want. I cannot and don't want to stop you from doing that. I'm asking for only one favor - please mention this source script in your credits.

2. You can import the plot (series) from any other indicator on TradingView. In Settings popup of my script, scroll down to "Indicator Definitions" section, and select the series of your choice in the first dropdown. Now it is ready to use in conditions dropdowns on top of the Settings popup.

Let me give you an example of that last scenario. Take another script of mine, "Pivot Points on SR lines DEMO". You can find it in "Indicators & Strategies" library or here: (). Attach it to your chart. Now come back to THIS script, open Settings popup and in "Custom Indicator aka Imported Source" select "Pivot Points on SR lines: ...". The way it works - it detects if a pivot point happened on Support/Resistance line from the past and returns 1 for PivotLow and -1 for Pivot High. Now in first Long Entry condition set: "custom indicator" + "Greater Than" + "value" + "0" and long entries will be marked on every pivot low noticed on Support/Resistance line.

ALERTS

Last but not least - the alerts. This script produces alerts on the entries calculated by strategy logic, as marked on the chart by the backtester. Moreover, syntax of those alerts is already prepared and fully compatible with TradingConnector - alerts executing tool (bot), if you want to auto-execute those trades. Apart from installing the tool, you need to set

up the alerts in TradingView, here is how:

open CreateAlert popup

in first dropdown select "Joint Conditions Strategy Template"

in second dropdown select "alert() function calls only"

And that's all. You only need to set one alert for the whole script, not one for Longs and one for Shorts as it was in the past. Also, you don't need to setup closing alerts, because stop-loss/take-profit/trailing-stop information is embedded in the entry alert so your broker receives it as early as possible. Alerts sent will look like this: "long sl=40 tp=80", which is exactly what TradingConnector expects.

Phew, that's all folks. If you think I should add something to this template (maybe other indicators?) please let me know in comments or via DM. Happy trading!

P.S. Pyramiding is not supported in this script.

Disclaimer : I'm not saying above combination of conditions will make you money. Actually none of this can be considered financial advice. It is only a software tool. Use it wisely, be aware of the risk and do your own research!

Kirill ChannelThis indicator shows overbought and oversold zones. Can be used on all time frames. I personally use 15m - 30m.

How to apply ?:

- There can be many strategies for use! I use this indicator to buy an asset in the green zone and then sell it in the middle of the channel or in the red zone.

- I strongly advise against entering counter-trend positions in a growing market if you have little trading experience and understanding of price action.

How do I place orders ?:

- I place orders in a grid.

- If the price is very close to the edge, but it is difficult to reach it, then it is better to open a position on the market and place orders deep into the grid.

- If the price is at the edge of the channel for a very long time, then you need to look at a higher timeframe.

Algorithm composition:

- ALMA

- Keltner Channel

- Fibonacci Retracement

- Custom price percent offset calculations and manipulations.

Settings:

- I strongly do not recommend changing ALMA. These numbers have been specially calculated.

- It's better not to change Borders either. The current algorithm dynamically changes the width of the extreme channels depending on the price movement.

- The Keltner Channel was specially selected.

- Fibonacci Retracement can be changed. This part of the algorithm can be modified to suit your needs. At the moment, there are settings for aggressive trading.

Channel type:

- Conservative: Fibonacci Retracement settings (100 ma, 100 atr, 8 mult, 100 smooth)

- Aggressive: Fibonacci Retracement settings (25 ma, 25 atr, 3.5 mult, 100 smooth)

Сonservative channel does not allow a large number of points to enter positions, however, it is more straightforward and safer for very large movements.

I prefer aggressive settings because they allow me to make more profit on the number of trades.

Try to use both modes and choose what is preferable for you.

[001] Entry_Test [TradeStand]Entry_Exit_Test .

------------------------------------

Function description

------------------------------------

You can automatically receive an entry alert when the conditions you specify are met.

Settlement alerts can be sent automatically when the conditions you specify are met.

Three types of moving averages can be displayed.

------------------------------------

Entry and Settlement Conditions

------------------------------------

Trade Mode: Select the trade you wish to execute.

Date and time: Enter the date and time you wish to execute the trade.

Number of seconds: If you want to specify the number of seconds, please enter it.

Daily MA: The 5, 25, and 75 day moving averages are displayed.

------------------------------------

------------------------------------

Entry_Exit_Test .

------------------------------------

■機能説明

------------------------------------

あなたが指定した条件を満たした時に、エントリーアラートを自動的に配信することが出来ます。

あなたが指定した条件を満たした時に、決済アラートを自動的に配信することが出来ます。

3種類の移動平均線を表示することが出来ます。

------------------------------------

■エントリー・決済条件

------------------------------------

・トレードモード:実行したいトレードを選択します

・日時:実行したい日時を入力、または選択します

・秒数:秒数まで指定したい場合は入力してください

・日足MA:5、25、75日移動平均線が表示できます

[002] DAY_MA_Pass [TradeStand]Cond_for_Day_MA

------------------------------------

Function description

------------------------------------

You can automatically receive an entry alert when the conditions you specify are met.

Settlement alerts can be sent automatically when the conditions you specify are met.

Three types of moving averages can be displayed.

------------------------------------

Entry and Settlement Conditions

------------------------------------

Trade Mode: Select the trade you wish to execute.

Date and time: Enter the date and time you wish to execute the trade.

Number of seconds: If you want to specify the number of seconds, please enter it.

Daily MA: The 5, 25, and 75 day moving averages are displayed.

Daily MA Trade: Select for this function

Select MA: Select the moving average you want to use as a reference.

Select conditions: Select the current position relative to the moving average

------------------------------------

------------------------------------

Cond_for_Day_MA

日足移動平均線を基準としたエントリー・決済

------------------------------------

■機能説明

------------------------------------

あなたが指定した条件を満たした時に、エントリーアラートを自動的に配信することが出来ます。

あなたが指定した条件を満たした時に、決済アラートを自動的に配信することが出来ます。

3種類の移動平均線を表示することが出来ます。

------------------------------------

■エントリー・決済条件

------------------------------------

選択した時間に、移動平均線を「超えているか」「割っているか」で

エントリー・決済を実行できます。

・トレードモード:実行したいトレードを選択します

・日足MA表示:5、25、75日移動平均線が表示できます

・実行日時:実行したい日時を入力、または選択します

・秒数:秒数まで指定したい場合は入力してください

・日足MA基準トレード:この機能の「OFF/ON」を選択します

・指定 日足移動平均線:基準となる日足移動平均を選択します

・条件:移動平均線に対する現在の位置関係を選択します

WMA Combo Crossover V2Before I begin I want to mention:

1. This is an upgrade of my indicator WMA Combo Crossover. (Link: www.tradingview.com)

2. The upgrade was inspired from the CCI and Bollinger Bands indicator by matsu_bitmex. (Link: www.tradingview.com)

3. I have combined the indictor with Bollinger Bands , coloring those sections as yellow, to increase winning trades as well as avoid losing trades by spotting potential reversals with the aid of news avoidance

4. This indicator is designed primarily for NNFX (No Nonsense Forex) though it can be used for any type of trading style

5. Also, I want to thank kurtisbu for helping me out. Thank you!

The indicator:

1. When WMA 25 is blue and is going upwards, it means there is an uptrend

2. When WMA 25 is red and is going down, it means there is a downtrend

3. During a trend, the color may switch to red and blue occasionally. When the color switches back to the direction of the trend, it can be used for re-entries

4. All trades based on the yellow color MUST be during a trend

5. When the color changes to yellow that means price is very volatile and only on the 1st candle is it advisable to enter a trade. (I have not backtested entering on the 2nd candle of a yellow color change)

6. During a trend, when the color changes to yellow and there is an incoming news event, then the chances of a reversal increase and I recommended avoid entering

Auto Fibonacci and Gann Fan/Retracements ComboIntroduction

This is a combination of Fibonacci and Gann fan/retracements.

The script can automatically draw as many:

Fibonacci Retracements

Fibonacci Fan

Gann Retracements

Gann Fan

as the user requires on the chart. Each level set or fan consists of 7 lines based on the most important ratios of Fibonacci/Gann.

Basics

What are Fibonacci retracements?

Fibonacci retracement levels are horizontal lines that indicate where support and resistance are likely to occur. They stem from Fibonacci’s sequence. Each level is associated with a percentage which is how much of a prior move the price has retraced. The Fibonacci retracement levels are 23.6%, 38.2%, 61.8%, and 78.6%. While not officially a Fibonacci ratio, 50% is also used. The indicator is useful because it can be drawn between any two significant price points, such as a high and a low. The indicator will then create the levels between those two points.

What are Gann retracements?

A developer of technical analysis and trading was W.D. Gann. Gann theory expects a normal retracement of 50 percent. This means that under normal selling pressure, the stock price will decline half the amount of its most recent rise, and vice versa. It also suggests that retracements occur at the halfway point of a move, such as 25 percent (half of 50 percent), 12.5 percent (half of 25 percent), and so on.

What is Fibonacci fan?

Fibonacci fan is a set of sequential trend lines drawn from a trough or peak through a set of points dictated by Fibonacci retracements. The first step to create it is to draw a trend line covering the local lowest and highest prices of a security. To reach retracement levels, the trader divides the difference in price at the low and high end by ratios determined by the Fibonacci series. The lines formed by connecting the starting point for the base trend line and each retracement level create the Fibonacci fan.

What is Gann fan?

A Gann fan consists of a series of lines called Gann angles. These angles are superimposed over a price chart to show potential support and resistance levels. The resulting image is supposed to help technical analysts predict price changes. Gann believed the 45-degree angle to be most important, but the Gann fan also draws angles at degrees like 75, 63.75, 26.25 and 15. The Gann fan originates at a low or high point. The resulting lines show areas of potential future support and resistance. The 45-degree line is known as the 1:1 line because the price will rise or fall at a 45-degree angle when the price moves up/down one unit for each unit of time. All other lines in the Gann fan are drawn above and below the 1:1 line. The other angles are associated with 2:1, 3:1, 4:1, 8:1 and 1:8, 1:4, 1:3, and 1:2 time-to-price moves.

Challenges

The most of the time I dedicated to writing this script has been spent on handling these problems:

1. Finding Local Highest/Lowest Prices

In order to draw Fibonacci and Gann fan/retracements, it's necessary to find local highest and lowest price points (Extrema) on the chart. As this could be so challenging, most traders and coders draw the lines covering the low and high prices over a given period of time or a limited number of bars back instead. I already wrote an indicator using this approach ( Auto Fibonacci Combo ).

In this new script I tried to find the exact highest and lowest prices based on this idea that: if a high point is formed lower than previous high which was after a lowest point, then that previous one was the local highest point, and vice versa if a low point is formed higher than previous low which was after a highest point, then that previous one was the local lowest point. So logically an extremum price on the chart won't be found until the next high/low point is formed.

2. Finding Proper Chart Scale for Gann Fan

Based on the theory, Gann angles are sensitive to the chart price scale and in order to have the right angles, the chart must be made with the proper scale. J.A. Hyerczyk in his book "Pattern, Price & Time - Using Gann Theory in Technical Analysis" suggests that the easiest way to determine the scale of a market is by taking the difference between top-to-top and bottom-to-bottom and dividing it by the time it took the market to move from top to top and bottom to bottom.

Thus on a properly constructed chart, the basic equation for calculating Gann angles is: Price * Time.

3. Drawing Fans and Relocating Fan Labels at Each New Bar in Pine (A Programming-Related Subject)

To do this, I used linear equations and line slopes. Of course it was so complicated and exhausting, but finally I overcame that thanks to my genius cousin.

Settings and Usage

By default, the script shows detected extremum points plus 1 Fibonacci fan, 1 Gann fan, 1 set of Fibonacci retracements and no Gann retracements on the chart. All of these could be changed in the indicator settings beside the color and transparency of each line.

Feel free to use this and send me your thoughts!

MA Deviation

Script description

A script that displays the deviation rate of the specified moving average line.

You can non-display the oscillator line by setting it.

Default setting

Moving average divergence rate : 25 SMA

Oscillator line (50) : display

Oscillator line (75) : non-display

Oscillator line (100) : non-display

スクリプトの説明

指定した移動平均線の乖離率を表示するスクリプトです。

設定によりオシレーター上の水平線の表示非表示を切り替えることができます。

デフォルト設定

移動平均乖離率:25 SMA

水平線(50):表示

水平線(75):非表示

水平線(100):非表示

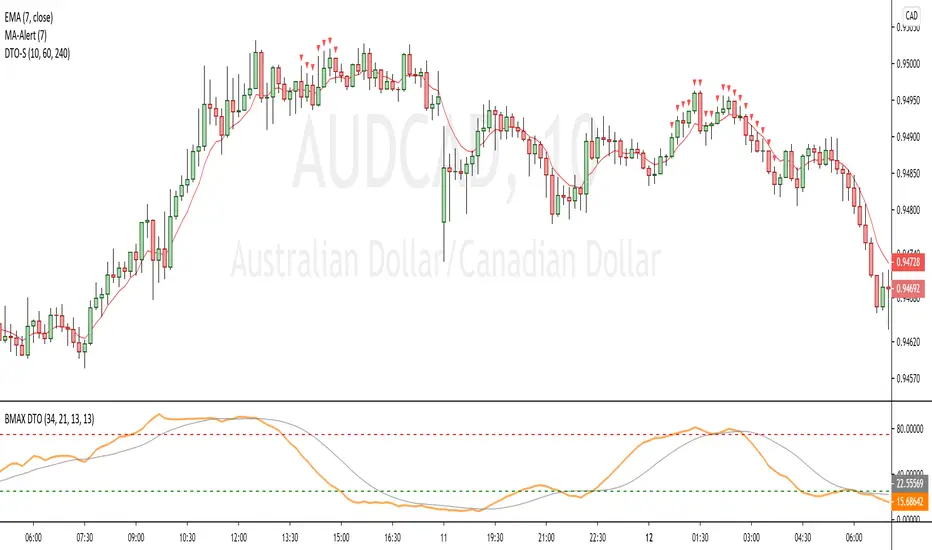

[BMAX] DTO Signal(ENGLISH)

This indicator is a variation of the original DT Oscillator that uses Stochastic and RSI calculations to find momentum opportunities. The purpose of it is to facilitate traking of multiple timeframes for overbought or oversold conditions.

As you can see on the example, we use the DT Oscillator in the selected timeframe, but in order to decide if we take a trade opportunity, we may want to see multiple timeframes in order to check a fractal scenario. DTO Signal indicates when 3 timeframes you select on the configurations are in the same condition, so overbought (above 75) or oversold (bellow 25).

(PORTUGUÊS)

Este indicador é uma variação do indicador DT Oscillator original que utiliza Estocástico e cálculos do RSI para encontrar oportunidades em "momentum". A proposta é facilitar o monitoramento de múltiplos tempos gráficos para condições de sobrecompra ou sobrevenda. Como você pode ver no example, com o uso do DT Oscillator no tempo gráfico escolhido, para que decidamos se tomamos uma posição no mercado, gostaríamos de verificar em múltiplos tempos gráficos uma condição fractal que construa um cenário provavel. DTO Signal indica quando 3 tempos gráficos escolhidos na configuração estão em uma mesma condição, de sobrecompra (acima de 75) ou de sobrevenda (abaixo de 25).

Percentile Nearest Rank Using Arrays [LuxAlgo]The new array feature is extremely powerful, as it will allow pinescript users to do more complex things, or compute existing calculations more efficiently, it will also be possible to shine some light to some already existing functions, one of them being percentile_nearest_rank .

We have been working on this new feature with our pal alexgrover, and made this script which computes a rolling percentile using the nearest rank method.

Settings

Length: Window of the rolling percentile, determine the number of past data to be used.

Percentage: Return the current value if Percentage % of the data fall below that value, the setting is in a range (0,100).

Src: Input source of the indicator.

Usage

A rolling percentile can have many usages when it comes to technical analysis, this is due to its ability to return the value of three common rolling statistics, the rolling median, which can be obtained using a percentage equal to 50, the rolling maximum, obtained with a percentage equal to 100, and the rolling minimum, obtained with a percentage equal to 0.

When we use our rolling percentile as a rolling median, we can obtain a robust estimation of the underlying trend in the price, while using it as a rolling maximum/minimum can allow us to determine if the market is trending, and at which direction. The rolling maximum/minimum is a rolling statistic used to calculate the well known stochastic oscillator and Donchian channel indicator.

We can also compute rolling quartiles, which can be obtained using a percentage of 25 or 75, with one of 25 returning the lower quartile and 75 the upper quartile.

In blue the upper rolling quartile (%75), in orange the lower rolling quartile (%25), both using a window size of 100.

Details

In order to compute a rolling percentile nearest rank, we must first take the most recent length closing prices, then order them in ascending order, we then return the value of the ordered observations at index (percentage/100*length) - 1 (we use - 1 because our array index starts at 0).

NIFTY Adv/Dec Live Count1) NIFTY Index Advance-Decline count

2) Each session, it reads the number of stock are +Ve or -Ve

3) Whichever the side +Ve or -Ve side moving stock is more than count will be plotted

4) at +/- 25 drawn a dotted line if Count is > = +/-25 Nifty is moving in a strong army

Eg:-

in the current session, 30 Stock is moving in +Ve direction & 10 are in -Ve direction

30 count will be plotted in the chart

[A618] Trend Tracker using Chandelier StopTrend Tacker

Works on ATR concepts and uses "Chandelier Stop by pipCharlie" as its main engine

How it is calculated

> 2 ATR stop plots are plotted

> #one ATR stop is of current time frame

> other one is the 5 times multiple of the current timeframe

> Their crossovers are analysed with the close of Current Timeframe

> This sort of methodology can help one with generating consistent entry signals over a particular timeframe

> My timeframe of choice is : 5 mins

> I have used resolution of 25, for 5 mins (see 5*5 =25)

Credits:

Chandelier Stop by pipCharlie

Hope this helps!!!

MARKET DYNAMICS HH LL BREAKOUTThis strategy is designed for Bank nifty and Nifty Indices on 5 min chart.This positional strategy ,go long when the long signal came and exit your buy position when sell signal generated by the strategy and again go short for next trade e g . when long signal came buy bank nifty 25 quantity ,book your profit or loss in next sell signal and again made SELL position with 25 quantity.

it is a non repainting strategy. this is just a breakout strategy and its accuracy is good. Slippages are not considered in the return.

mForex - Keltner channel + EMA Scalping systemTransaction setup parameters

Time frame: M5, M15

Currency pair: EUR / USD , GPB / USD

Transaction: London, USA

Number of orders / day: 10 - 15 orders

Trading strategies

=== BUY ===

Candles close on the upper Keltner

EMA10 crosses the upper Keltner range from below

Stop loss in the middle band or up to 12 pips

Profit target: 15-25 pips

=== SELL ===

Candles close below Keltner below

EMA10 crosses the Keltner range below from above

Stop loss in the middle band or up to 12 pips

Profit target: 15-25 pips

Vertical Horizontal Moving Average [AneoPsy & alexgrover] Moving average adapting to the strength of the trend, this is made possible by using the square of the vertical-horizontal filter as a smoothing factor. Alerts are included with two different types of conditions available to the user.

Settings

Length : Period of the moving average

Src : Input data for the indicator

Alerts : Types of conditions to be used in the alerts, when set to "VHMA Direction Change" alerts are triggered once the VHMA is either rising or declining, else the alerts are based on the crosses between Src and the VHMA

Usage

The VHMA can be used as a fast or slow-moving average in a moving average crossover system, or as input for other indicators.

VHMA of with length = 25 and sma with length = 200.

VHMA with length = 25 used as input for the RSI with length = 14.

Details

The vertical-horizontal filter is a measure of the strength of the trend and lay in a (0,1) range, to calculate it you just need to divide the rolling range over with the rolling sum of the absolute price changes, squaring the result allow to get lower results with higher values of length .

Squared vertical horizontal filter with length = 50, the value is low when the market is ranging and high when trending.

To set the alerts go in the alert panel, click on create alert, and select VHMA in "condition", choose between the buy or sell alert. If Src = closing price or another indicator dependant on the closing price select in options "once per bar close", if the indicator using the opening or lagged closing prices values as input select "One per bar" instead.

Thanks

Thanks to AneoPsy for adding the color change, the idea to use two kinds of conditions for the alert, and for its feedback, you can follow him

www.tradingview.com

and finally thanks to you for reading and for your support, only one last script left for the month, then we'll start July with some pretty interesting indicators, I hope you'll like them ^^/

Sto RSI and kijun-sen line to determine and follow the trend This script uses 25-75 treshold of stochastic RSI with the help of kijun-sen as confirmation, to find entry points to any trend either newly developed or an established one. I just realized it on the 1 hour SPX chart. Sure it can be used on other symbols. Crossing above/below 25/75 line of sto RSI is considered as buy/sell signal. Signals are evaluated whether price be above/below kijun-sen line. If a sell signal below kijun-sen is generated it is a continuation signal for downtrend, otherwise it is a countertrend signal (maybe a signal for a new downtrend). A countertrend signal must be evaluated carefully and only accepted in the right side of kijun-sen. e.g entering a sell signal generated above kijun-sen should be accepted only below the kijun-sen, vice-versa.

Terminal : USD Based Stock Markets Change (%)Hello.

This script is a simple USD Based Stock Markets Change (%) Data Terminal.

You can also set the period to look back manually in the menu.

In this way, an idea can be obtained about Countries' Stock Markets.

And you can observe the stock exchanges of relatively positive and negative countries from others.

Features

Value changes on a percentage basis (%)

Stock exchange values are calculated in dollar terms.

Due to the advantage of movement, future data were chosen instead of spot values on the required instruments.

Stock Markets

Usa : S&P 500 Futures

Japan: Nikkei 225 Futures

England: United Kingdom ( FTSE ) 100

Australia: Australia 200

Canada: S&P / TSX Composite

Switzerland: Swiss Market Index

New Zealand: NZX 50 Index

China: SSE Composite (000001)

Denmark: OMX Copenhagen 25 Index

Hong-Kong: Hang Seng Index Futures

India: Nifty 50

Norway: Oslo Bors All Share Index

Russia: MOEX Russia Index

Sweden: OMX Stockholm Index

Singapore: Singapore 30

Turkey: BIST 100

South Africa: South Africa Top 40 Index

Spain: IBEX 35

France: CAC 40

Italy: FTSE MIB Index

Netherlands: Netherlands 25

Germany : DAX

Regards.