Easy Directional Movement IndexNothing more than a graphical tweak for the integrated Directional movement index (DMI). The purpose is to make the reading of the DMI easier and more immediate.

The area between DI+ and DI- is filled, and the indicator's range in divided into 4 sections, each of them representing a different price tendency:

- When ADX line is inside the red colored area (0-25), the market is in a ranging phase.

- When inside the aqua colored area (25-50), there is a trend.

- When inside the blue colored area (50-75), there is a strong trend

- When inside the navy colored area (75-100), there is an extremely strong trend.

However keep in mind that these are default levels that may be not always significant. You can change them from the script settings as you prefer, to better tweak your analysis.

Please support my work and follow me if you like my scripts. Many more of them are coming in the future.

@Bezzus

ابحث في النصوص البرمجية عن "英国央行降息25个基点"

Ichimoku with Correct DisplacementThe default Ichimoku Cloud by TradingView is strange. The kumo is only displaced 25 periods forward, and the chikou is displaced 25 periods back. This is because TradingView had the correct value for displacement (26), but they decided to subtract this displacement by 1 when actually drawing the kumo and add 1 when drawing the chikou. This script fixes this and allows for easier customization of each line in the Ichimoku.

MACD At Scales with AlertsI use the horizontal scale lines on the MACD indicator as part of my scalping strategy along with other indicators like RSI/EMA and Market Cipher B when trading BTC

I am looking for a cross above or below the 12.5 and 25 horizontal scale lines, along with lining up other indicators

I set my alerts on the 5 min TF and look to the 15 and 30 min TF's for further confirmation.

I have find the scale lines to be very useful for visual reference of the crosses, above/below 25 lines is mostly a safer trade, crosses above/below 12.5 lines can have more risk, crosses between 0 baseline and 12.5 can have a higher return but have much more risk.

Don't ever use just this indicator by itself, you must always have at least 2 indicators running

This is an example of the TF's not lining up, so a entry here would be high risk

This is an example of the TF's lining up, so a entry here would be less risk

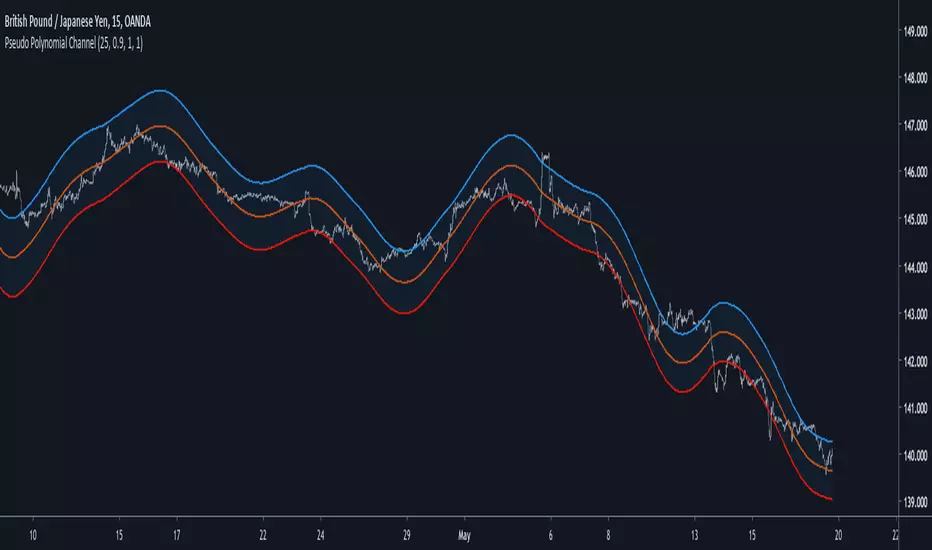

Pseudo Polynomial ChannelIntroduction

Back when i started using pine i made a script called periodic channel who aimed to rescale an average correlated sine wave to the price...don't worked very well. So i tried to fix problems induced by the indicator without much success, i had to redo it from scratch while abandoning the idea of rescaling correlated smooth functions to the price, at that time i also received requests regarding polynomial channel, some plateformes included this indicator, this led me to the idea to estimate it in order to both respond to the periodic channel problems and the requests i received, i have tried many many things and recently i tweaked a linear extrapolation to have an approximation.

Linear Extrapolation To Pseudo Polynomial Regression

I could be wrong but a polynomial regression must use constant parameters in order to provide a really smooth output, at least constant for a set of time. The moving averages forms (Savitzky-Golay moving average) who smooth polynomials across a window to the data don't have such smoothness, so how to estimate a polynomial regression while having a parameter providing control over the smoothness, a response to this is by using a recursive linear extrapolation. I posted a linear extrapolation indicator long ago, i used the same formula while adding a function to morph the output and the input in the form of :

morph * output + (1-morph) * input

How can this provide an estimate of a polynomial regression ? Well i'm not even sure myself but if you use the output as input (morph = 1) for the linear extrapolation function you should get a rough estimate of a line, this is what i thought at first and it proved to be right

Based on this observation i thought that it would be possible to get polynomial results by lowering morph, and as expected it worked well but showed a periodic pattern, this is why i smooth k in line 10.

0.9 for morph work well, higher values create sometimes smoother results but damage heavily the estimation.

Parameters

Morph have been introduced earlier, it control the amount of output and input the linear extrapolation should process, lower values create rougher but more stables results, if you see that the estimation is going nuts lower morph or change length, also lower length if you increase morph .

High overshoot, morph to 0.8 can help have a better estimation at the cost of less smoothness.

Length control the indicator smoothing, this parameter differ heavily from other filters, therefore low values can create mid/long term smoothing, it can also depend on which market instrument you are applying it, so there are no fixed optimal length.

Mult control how spread the bands are, to do so mult multiply the cumulative mean error, you can change this error measurement by anything you want like standard deviation/atr/range but take into account that you may create a separate parameter to control the error instead of length . Mult can be a float and like length can have different optimal values depending on the market the indicator is applied to.

Flatten do exactly what is name imply, it flatten the overall output to have a better estimation, can be a float. The result is less smooth.

Flatten = 2

More Exemples

BTCUSD length = 25 and mult = 4

XPDUSD length = 25 and mult = 1

ALPHABET length = 6 and morph = 0.99

Conclusion

I tried to estimate a polynomial channel by using recursion in the linear extrapolation function. This build is way more stable than the periodic channel but its still a bit inaccurate in my opinion. I hope this code can still help someone build something really nice, if so share your results :)

I apologize for those expecting a legit polynomial channel build but i really don't know how to do that, as i said parameters for the regression must be constants, i hope it still fine :)

Thanks for reading !

Modified Gann HiLo ActivatorIntroduction

The gann hilo activator is a trend indicator developed by Robert Krausz published into W. D. Gann Treasure Discovered: Simple Trading Plans for Stocks & Commodities . This indicator crate a trailing stop aiming to show the direction of the trend.

This indicator is fairly easy to compute and dont require lot of skills to understand. First we calculate the simple moving average of both price high and price low, when the close price is higher than the moving average of the price high the indicator return the moving average of the price low, else the indicator return the moving average of the price high if the close price is lower than the moving average of the price low.

My indicator add a different calculation method in order to avoid whipsaw trades as well as adding significance to the moving average length. A Median method has been added to provide more robustness.

The Indicator

The indicator is a simple trailing stop aiming to show the direction of the trend. The indicator use a different source instead of the price high/low for its calculation. The first method is the "SMA" method which like the classic hilo indicator use a simple moving average for the calculation of the indicator.

Sma Method with length = 25

The "Median" use a moving median instead of a simple moving average, this provide more robustness.

Median Method with length = 25

The shape is less curved and the indicator can sometimes avoid whipsaw with high's length periods.

Mult Parameter

The mult parameter is a parameter set to be lower or equal to 1 and greater or equal to 0. High values allow the indicator to be far from the price thus avoiding whipsaw trades, lower ones lower the distance from the price. A mult parameter of 0.1 approximate the original hilo indicator.

In blue the indicator with mult = 0.1 and in radical red the original hilo activator.

Conclusion

The modifications allow more control over the indicator as well as adding more robustness while the original one is destined to fail when market price is more complex.

Thanks for reading :)

For any questions/suggestions feel free to pm me

Average Candle LengthThis script is designed to show you the average candle size in pips (wick to wick) for however many bars you choose (20 is default).

The idea is that if the average candle size for the last 20 bars is, let's say 25, you would probably not want to set your stop loss less than 25 because it is more likely to get hit.

if you find this script helpful, tips and donations are always appreciated (venmo @rick-munoz) :)

Future Least Squares Moving Average//+------------------------------------------------------------------+

// | Future Least Squares Moving Average |

// | 未来予測LSMA |

// | Ver.1.0 |

// | Copyright Sakura |

//+------------------------------------------------------------------+

//LSMAは一時回帰直線の現在地の点の集合であるということは、未来の点を使えば未来を描けるはずというアホなことを無理やり考えました。

//結論はうまくいかなかったですので、パラメーターをいじって誤魔化しという結果に。

//それでも、先に書いてますので急激な価格変動に対処できる訳もなくといった感じになっています。

//displacementは一目に合わせたいので26固定の方向でとしたいところですが厳しいですね。

//

//設定例

//SMA(25)≒FLSMA(25,7,13)

//SMA(50)≒FLSMA(50,13,26)

//SMA(75)≒FLSMA(75,20,26)

How to automate this strategy for free using a chrome extension.Hey everyone,

Recently we developed a chrome extension for automating TradingView strategies using the alerts they provide. Initially we were charging a monthly fee for the extension, but we have now decided to make it FREE for everyone. So to display the power of automating strategies via TradingView, we figured we would also provide a profitable strategy along with the custom alert script and commands for the alerts so you can easily cut and paste to begin trading for profit while you sleep.

Step 1:

You are going to need to download the Chrome Extension called AutoView. You can get the extension for free by following this link: bit.ly ( I had to shorten the link as it contains Google and TV automatically converts it to a symbol)

Step 2: Go to your chrome extension page, and under the new extension you'll see a "settings" button. In the setting you will have to connect and give permission to the exchange 1broker allowing the extension to place your orders automatically when triggered by an alert.

Step 3: Setup the strategy and custom script for the alerts in TradingView. The attached script is the strategy, you can play with the settings yourself to try and get better numbers/performance if you please.

This following script is for the custom alerts:

//@version=2

study("4All-Alert", shorttitle="Alerts")

src = close

len = input(4, minval=1, title="Length")

up = rma(max(change(src), 0), len)

down = rma(-min(change(src), 0), len)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

rsin = input(5)

sn = 100 - rsin

ln = 0 + rsin

short = crossover(rsi, sn) ? 1 : 0

long = crossunder(rsi, ln) ? 1 : 0

plot(long, "Long", color=green)

plot(short, "Short", color=red)

Now that you have the extension installed, the custom strategy and alert scripts in place, you simply need to create the alerts.

To get the alerts to communicate with the extension properly, there is a specific syntax that you will need to put in the message of the alert. You can find more details about the syntax here : gist.github.com

For this specific strategy, I use the Alerts script, long/short greater than 0.9 on close.

In the message for a long place this as your message:

Long

c=order b=short

c=position b=short l=200 t=market

b=long q=0.01 l=200 t=market tp=13 sl=25

and for the short...

Short

c=order b=long

c=position b=long l=200 t=market

b=short q=0.01 l=200 t=market tp=13 sl=25

If you'll notice in my above messages, compared to the strategy my tp and sl (take profit and stop loss) vary by a few pips. This is to cover the market opens and spread on 1broker. You can change the tp and sl in the strategy to the above and see that the overall profit will not vary much at all.

I hope this all makes sense and it is enough to not only make some people money, but to show the power of coming up with your own strategy and automating it using TradingView alerts and the free Chrome Extension AutoView.

ps. I highly recommend upgrading your TradingView account so you have access to back testing and multiple alerts.

There is really no reason you won't cover the cost and then some on a monthly basis using the tools provided.

Best of luck and happy trading.

Note: The extension currently allows for automation on 2 exchanges; 1broker and Okcoin. If you do not have accounts there, we'd appreciate you signing up using our referral links.

www.okcoin.com

1broker.com

dhruv private 91400//@version=5

//

VERSION = '7.9-X'// 2024.3.20

strategy(

'LE VAN DO® - Swing Signals & Overlays Private™ 7.9-X',

shorttitle = 'LE VAN DO® - Swing Signals & Overlays Private™ 7.9-X' + VERSION,

overlay = true,

explicit_plot_zorder = true,

pyramiding = 0,

default_qty_type = strategy.percent_of_equity,

default_qty_value = 50,

calc_on_every_tick = false,

process_orders_on_close = true,

max_bars_back = 500,

initial_capital = 5000,

commission_type = strategy.commission.percent,

commission_value = 0.02,

max_lines_count = 500

)

//Truncate Function

truncate(number, decimals) =>

factor = math.pow(10, decimals)

int(number * factor) / factor

//

// === INPUTS ===

TPSType = input.string('Trailing', 'What TPS should be taken : ', options = )

setupType = input.string('Open/Close', title='What Trading Setup should be taken : ', options= )

scolor = input(true, title='Show coloured Bars to indicate Trend?')

almaRibbon = input(false, title='Enable Ribbon?')

//tradeType = input.string('BOTH', title='What trades should be taken : ', options= )

// === /INPUTS ===

// Display the probabilities in a table

//text01_ = str.tostring(timeframe.multiplier * intRes, '####')

//t = timenow + math.round(ta.change(time) * 25)

//var label lab01 = na

//label.delete(lab01)

//lab01 := label.new(t, close, text=text01_, style=label.style_label_left, yloc=yloc.price, xloc=xloc.bar_time, textalign=text.align_left, textcolor=color.white)

// Constants colours that include fully non-transparent option.

green100 = #008000FF

lime100 = #66bb6a

red100 = #f7525f

blue100 = #0000FFFF

aqua100 = #00FFFFFF

darkred100 = #8B0000FF

gray100 = #808080FF

/////////////////////////////////////////////

// Create non-repainting security function

rp_security(_symbol, _res, _src) =>

request.security(_symbol, _res, _src )

//

f_tfInMinutes() =>

_tfInMinutes = timeframe.period == '1' ? '3' : timeframe.period == '3' ? '5' : timeframe.period == '5' ? '15' : timeframe.period == '15' ? '30' : timeframe.period == '30' ? '60' : timeframe.period == '60' ? '240' : 'D'

_tfInMinutes

my_time1 = f_tfInMinutes()

tfmult = 18 //input.int(18, "Input Timeframe Multiplier")

f_resInMinutes() =>

_resInMinutes = timeframe.multiplier * (

timeframe.isseconds ? 1. / 60. :

timeframe.isminutes ? 1. :

timeframe.isdaily ? 1440. :

timeframe.isweekly ? 10080. :

timeframe.ismonthly ? 43800. : na)

my_time = str.tostring(f_resInMinutes()*tfmult)

useSource = close //input.string('Close', 'What Source to be used?', options = )

enableFilter = input(true, "Enable Backtesting Range Filtering")

fromDate = input.time(timestamp("01 Jan 2023 00:00 +0300"), "Start Date")

toDate = input.time(timestamp("31 Dec 2099 00:00 +0300"), "End Date")

tradeDateIsAllowed = not enableFilter or (time >= fromDate and time <= toDate)

filter1 = 'Filter with Atr'

filter2 = 'Filter with RSI'

filter3 = 'Atr or RSI'

filter4 = 'Atr and RSI'

filter5 = 'No Filtering'

filter6 = 'Entry Only in sideways market(By ATR or RSI)'

filter7 = 'Entry Only in sideways market(By ATR and RSI)'

typefilter = input.string(filter5, title='Sideways Filtering Input', options= , group='Strategy Options')

RSI = truncate(ta.rsi(close, input.int(7, group='RSI Filterring')), 2)

toplimitrsi = input.int(45, title='TOP Limit', group='RSI Filterring')

botlimitrsi = input.int(10, title='BOT Limit', group='RSI Filterring')

//ST = input.bool(true, title='Show Supertrend?', group='Supertrend Indicator')

//period = input.int(1440, group='Supertrend Indicator')

//mult = input.float(2.612, group='Supertrend Indicator')

atrfiltLen = 5 //input.int(5, minval=1, title='atr Length', group='Sideways Filtering Input')

atrMaType = 'EMA' //input.string('EMA', options= , group='Sideways Filtering Input', title='atr Moving Average Type')

atrMaLen = 5 //input.int(5, minval=1, title='atr MA Length', group='Sideways Filtering Input')

//filtering

atra = request.security(syminfo.tickerid, '', ta.atr(atrfiltLen))

atrMa = atrMaType == 'EM' ? ta.ema(atra, atrMaLen) : ta.sma(atra, atrMaLen)

updm = ta.change(high)

downdm = -ta.change(low)

plusdm = na(updm) ? na : updm > downdm and updm > 0 ? updm : 0

minusdm = na(downdm) ? na : downdm > updm and downdm > 0 ? downdm : 0

cndSidwayss1 = atra >= atrMa

cndSidwayss2 = RSI > toplimitrsi or RSI < botlimitrsi

cndSidways = cndSidwayss1 or cndSidwayss2

cndSidways1 = cndSidwayss1 and cndSidwayss2

Sidwayss1 = atra <= atrMa

Sidwayss2 = RSI < toplimitrsi and RSI > botlimitrsi

Sidways = Sidwayss1 or Sidwayss2

Sidways1 = Sidwayss1 and Sidwayss2

trendType = typefilter == filter1 ? cndSidwayss1 : typefilter == filter2 ? cndSidwayss2 : typefilter == filter3 ? cndSidways : typefilter == filter4 ? cndSidways1 : typefilter == filter5 ? RSI > 0 : typefilter == filter6 ? Sidways : typefilter == filter7 ? Sidways1 : na

// === /INPUTS ===

tf = my_time //input('15')

r = ticker.heikinashi(syminfo.tickerid)

openSeriesAlt = request.security(r, tf, open, lookahead=barmerge.lookahead_on)

closeSeriesAlt = request.security(r, tf, close, lookahead=barmerge.lookahead_on)

//openP = plot(almaRibbon ? openSeriesAlt : na, color=color.new(color.lime, 0), linewidth=3)

//closeP = plot(almaRibbon ? closeSeriesAlt : na, color=color.new(color.red, 0), linewidth=3)

BUYOC = ta.crossover(closeSeriesAlt, openSeriesAlt) and setupType == "Open/Close" and trendType

SELLOC = ta.crossunder(closeSeriesAlt, openSeriesAlt) and setupType == "Open/Close" and trendType

//strategy.entry('sell', direction=strategy.short, qty=trade_size, comment='sell', when=sel_entry)

//strategy.entry('buy', direction=strategy.long, qty=trade_size, comment='buy', when=buy_entry)

//trendColour = closeSeriesAlt > openSeriesAlt ? color.green : color.red

//bcolour = closeSeriesAlt > openSeriesAlt ? lime100 : red100

//barcolor(scolor ? bcolour : na, title='Bar Colours')

//closeP = plot(almaRibbon ? closeSeriesAlt : na, title='Close Series', color=color.new(trendColour, 20), linewidth=2, style=plot.style_line)

//openP = plot(almaRibbon ? openSeriesAlt : na, title='Open Series', color=color.new(trendColour, 20), linewidth=2, style=plot.style_line)

//fill(closeP, openP, color=color.new(trendColour, 80))

//

//rt = input(true, title="ATR Based REnko is the Default, UnCheck to use Traditional ATR?")

atrLen = 3 //input.int(3, title="RENKO_ATR", group = "Renko Settings")

isATR = true //input.bool(true, title="RENKO_USE_RENKO_ATR", group = "Renko Settings")

tradLen1 = 1000 //input.int(1000, title="RENKO_TRADITIONAL", group = "Renko Settings")

//Code to be implemented in V2

//mul = input(1, "Number Of minticks")

//value = mul * syminfo.mintick

tradLen = tradLen1 * 1

param = isATR ? ticker.renko(syminfo.tickerid, "ATR", atrLen) : ticker.renko(syminfo.tickerid, "Traditional", tradLen)

renko_close = request.security(param, my_time, close, lookahead=barmerge.lookahead_on)

renko_open = request.security(param, my_time, open, lookahead=barmerge.lookahead_on)

//============================================

//Sniper------------------------------------------------------------------------------------------------------------------------------------- // Signal 2

//============================================

//============================================

//EMA_CROSS-------------------------------------------------------------------------------------------------------------------------------- // Signal 4

//============================================

EMA1_length=input.int(2, "EMA1_length", group = "Renko Settings")

EMA2_length=input.int(10, "EMA2_length", group = "Renko Settings")

a = ta.ema(renko_close, EMA1_length)

b = ta.ema(renko_close, EMA2_length)

//BUY = ta.cross(a, b) and a > b and renko_open < renko_close

//SELL = ta.cross(a, b) and a < b and renko_close < renko_open

///////////////////////////////

// Determine long and short conditions

BUYR = ta.crossover(a, b) and setupType == "Renko" and trendType

SELLR = ta.crossunder(a, b) and setupType == "Renko" and trendType

sel_color = setupType == "Open/Close" ? closeSeriesAlt < openSeriesAlt : setupType == "Renko" ? renko_close < renko_open : na

buy_color = setupType == "Open/Close" ? closeSeriesAlt > openSeriesAlt : setupType == "Renko" ? renko_close > renko_open : na

sel_entry = setupType == "Open/Close" ? SELLOC : setupType == "Renko" ? SELLR : na

buy_entry = setupType == "Open/Close" ? BUYOC : setupType == "Renko" ? BUYR : na

trendColour = buy_color ? color.green : color.red

bcolour = buy_color ? lime100 : red100

barcolor(scolor ? bcolour : na, title='Bar Colours')

p11=plot(almaRibbon and setupType == "Open/Close" ? closeSeriesAlt : almaRibbon and setupType == "Renko" ? renko_close : na, style=plot.style_circles, linewidth=1, color=color.new(trendColour, 80), title="RENKO_1")

p22=plot(almaRibbon and setupType == "Open/Close" ? openSeriesAlt : almaRibbon and setupType == "Renko" ? renko_open : na, style=plot.style_circles, linewidth=1, color=color.new(trendColour, 80), title="RENKO_2")

fill(p11, p22, color=color.new(trendColour, 50), title="RENKO_fill")

//

lxTrigger = false

sxTrigger = false

leTrigger = buy_entry

seTrigger = sel_entry

// === /ALERT conditions.

buy = leTrigger //ta.crossover(closeSeriesAlt, openSeriesAlt)

sell = seTrigger //ta.crossunder(closeSeriesAlt, openSeriesAlt)

varip wasLong = false

varip wasShort = false

if barstate.isconfirmed

wasLong := false

else

if buy

wasLong := true

if barstate.isconfirmed

wasShort := false

else

if sell

wasShort := true

plotshape(wasLong, color = color.yellow)

plotshape(wasShort, color = color.yellow)

//plotshape(almaRibbon ? buy : na, title = "Buy", text = 'Buy', style = shape.labelup, location = location.belowbar, color= #39ff14, textcolor = #FFFFFF, size = size.tiny)

//plotshape(almaRibbon ? sell : na, title = "Exit", text = 'Exit', style = shape.labeldown, location = location.abovebar, color= #ff1100, textcolor = #FFFFFF, size = size.tiny)

// === STRATEGY ===

i_alert_txt_entry_long = "Short Exit" //input.text_area(defval = "Short Exit", title = "Long Entry Message", group = "Alerts")

i_alert_txt_exit_long = "Long Exit" //input.text_area(defval = "Long Exit", title = "Long Exit Message", group = "Alerts")

i_alert_txt_entry_short = "Go Short" //input.text_area(defval = "Go Short", title = "Short Entry Message", group = "Alerts")

i_alert_txt_exit_short = "Go Long" //input.text_area(defval = "Go Long", title = "Short Exit Message", group = "Alerts")

// Entries and Exits with TP/SL

//tradeType

if buy and TPSType == "Trailing" and tradeDateIsAllowed

strategy.close("Short" , alert_message = i_alert_txt_exit_short)

strategy.entry("Long" , strategy.long , alert_message = i_alert_txt_entry_long)

if sell and TPSType == "Trailing" and tradeDateIsAllowed

strategy.close("Long" , alert_message = i_alert_txt_exit_long)

strategy.entry("Short" , strategy.short, alert_message = i_alert_txt_entry_short)

//tradeType

if buy and TPSType == "Options" and tradeDateIsAllowed

// strategy.close("Short" , alert_message = i_alert_txt_exit_short)

strategy.entry("Long" , strategy.long , alert_message = i_alert_txt_entry_long)

if sell and TPSType == "Options" and tradeDateIsAllowed

strategy.close("Long" , alert_message = i_alert_txt_exit_long)

// strategy.entry("Short" , strategy.short, alert_message = i_alert_txt_entry_short)

G_RISK = '■ ' + 'Risk Management'

//#region ———— <↓↓↓ G_RISK ↓↓↓> {

//ATR SL Settings

atrLength = 20 //input.int(20, minval=1, title='ATR Length')

profitFactor = 2.5 //input(2.5, title='Take Profit Factor')

stopFactor = 1 //input(1.0, title='Stop Loss Factor')

// Calculate ATR

tpatrValue = ta.atr(atrLength)

// Calculate take profit and stop loss levels for buy signals

takeProfit1_buy = 1 * profitFactor * tpatrValue //close + profitFactor * atrValue

takeProfit2_buy = 2 * profitFactor * tpatrValue //close + 2 * profitFactor * atrValue

takeProfit3_buy = 3 * profitFactor * tpatrValue //close + 3 * profitFactor * atrValue

stopLoss_buy = close - takeProfit1_buy //stopFactor * tpatrValue

// Calculate take profit and stop loss levels for sell signals

takeProfit1_sell = 1 * profitFactor * tpatrValue //close - profitFactor * atrValue

takeProfit2_sell = 2 * profitFactor * tpatrValue //close - 2 * profitFactor * atrValue

takeProfit3_sell = 3 * profitFactor * tpatrValue //close - 3 * profitFactor * atrValue

stopLoss_sell = close + takeProfit1_sell //stopFactor * tpatrValue

// ———————————

//Tooltip

T_LVL = '(%) Exit Level'

T_QTY = '(%) Adjust trade exit volume'

T_MSG = 'Paste JSON message for your bot'

//Webhook Message

O_LEMSG = 'Long Entry'

O_LXMSGSL = 'Long SL'

O_LXMSGTP1 = 'Long TP1'

O_LXMSGTP2 = 'Long TP2'

O_LXMSGTP3 = 'Long TP3'

O_LXMSG = 'Long Exit'

O_SEMSG = 'Short Entry'

O_SXMSGSL = 'Short SL'

O_SXMSGA = 'Short TP1'

O_SXMSGB = 'Short TP2'

O_SXMSGC = 'Short TP3'

O_SXMSGX = 'Short Exit'

// on whole pips) for forex currency pairs.

pip_size = syminfo.mintick * (syminfo.type == "forex" ? 10 : 1)

// On the last historical bar, show the instrument's pip size

//if barstate.islastconfirmedhistory

// label.new(x=bar_index + 2, y=close, style=label.style_label_left,

// color=color.navy, textcolor=color.white, size=size.large,

// text=syminfo.ticker + "'s pip size is:\n" +

// str.tostring(pip_size))

// ——————————— | | | Line length guide |

i_lxLvlTP1 = leTrigger ? takeProfit1_buy : seTrigger ? takeProfit1_sell : na //input.float (1, 'Level TP1' , group = G_RISK, tooltip = T_LVL)

i_lxQtyTP1 = input.float (50, 'Qty TP1' , group = G_RISK, tooltip = T_QTY)

i_lxLvlTP2 = leTrigger ? takeProfit2_buy : seTrigger ? takeProfit2_sell : na //input.float (1.5, 'Level TP2' , group = G_RISK, tooltip = T_LVL)

i_lxQtyTP2 = input.float (30, 'Qty TP2' , group = G_RISK, tooltip = T_QTY)

i_lxLvlTP3 = leTrigger ? takeProfit3_buy : seTrigger ? takeProfit3_sell : na //input.float (2, 'Level TP3' , group = G_RISK, tooltip = T_LVL)

i_lxQtyTP3 = input.float (20, 'Qty TP3' , group = G_RISK, tooltip = T_QTY)

i_lxLvlSL = leTrigger ? takeProfit1_buy : seTrigger ? takeProfit1_sell : na //input.float (0.5, 'Stop Loss' , group = G_RISK, tooltip = T_LVL)

i_sxLvlTP1 = i_lxLvlTP1

i_sxQtyTP1 = i_lxQtyTP1

i_sxLvlTP2 = i_lxLvlTP2

i_sxQtyTP2 = i_lxQtyTP2

i_sxLvlTP3 = i_lxLvlTP3

i_sxQtyTP3 = i_lxQtyTP3

i_sxLvlSL = i_lxLvlSL

G_MSG = '■ ' + 'Webhook Message'

i_leMsg = O_LEMSG //input.string (O_LEMSG ,'Long Entry' , group = G_MSG, tooltip = T_MSG)

i_lxMsgSL = O_LXMSGSL //input.string (O_LXMSGSL ,'Long SL' , group = G_MSG, tooltip = T_MSG)

i_lxMsgTP1 = O_LXMSGTP1 //input.string (O_LXMSGTP1,'Long TP1' , group = G_MSG, tooltip = T_MSG)

i_lxMsgTP2 = O_LXMSGTP2 //input.string (O_LXMSGTP2,'Long TP2' , group = G_MSG, tooltip = T_MSG)

i_lxMsgTP3 = O_LXMSGTP3 //input.string (O_LXMSGTP3,'Long TP3' , group = G_MSG, tooltip = T_MSG)

i_lxMsg = O_LXMSG //input.string (O_LXMSG ,'Long Exit' , group = G_MSG, tooltip = T_MSG)

i_seMsg = O_SEMSG //input.string (O_SEMSG ,'Short Entry' , group = G_MSG, tooltip = T_MSG)

i_sxMsgSL = O_SXMSGSL //input.string (O_SXMSGSL ,'Short SL' , group = G_MSG, tooltip = T_MSG)

i_sxMsgTP1 = O_SXMSGA //input.string (O_SXMSGA ,'Short TP1' , group = G_MSG, tooltip = T_MSG)

i_sxMsgTP2 = O_SXMSGB //input.string (O_SXMSGB ,'Short TP2' , group = G_MSG, tooltip = T_MSG)

i_sxMsgTP3 = O_SXMSGC //input.string (O_SXMSGC ,'Short TP3' , group = G_MSG, tooltip = T_MSG)

i_sxMsg = O_SXMSGX //input.string (O_SXMSGX ,'Short Exit' , group = G_MSG, tooltip = T_MSG)

i_src = close

G_DISPLAY = 'Display'

//

i_alertOn = true //input.bool (true, 'Alert Labels On/Off' , group = G_DISPLAY)

i_barColOn = true //input.bool (true, 'Bar Color On/Off' , group = G_DISPLAY)

// ———————————

// @function Calculate the Take Profit line, and the crossover or crossunder

f_tp(_condition, _conditionValue, _leTrigger, _seTrigger, _src, _lxLvlTP, _sxLvlTP)=>

var float _tpLine = 0.0

_topLvl = _src + _lxLvlTP //TPSType == "Fixed %" ? _src + (_src * (_lxLvlTP / 100)) : _src + _lxLvlTP

_botLvl = _src - _lxLvlTP //TPSType == "Fixed %" ? _src - (_src * (_sxLvlTP / 100)) : _src - _sxLvlTP

_tpLine := _condition != _conditionValue and _leTrigger ? _topLvl :

_condition != -_conditionValue and _seTrigger ? _botLvl :

nz(_tpLine )

// @function Similar to "ta.crossover" or "ta.crossunder"

f_cross(_scr1, _scr2, _over)=>

_cross = _over ? _scr1 > _scr2 and _scr1 < _scr2 :

_scr1 < _scr2 and _scr1 > _scr2

// ———————————

//

var float condition = 0.0

var float slLine = 0.0

var float entryLine = 0.0

//

entryLine := leTrigger and condition <= 0.0 ? close :

seTrigger and condition >= 0.0 ? close : nz(entryLine )

//

slTopLvl = TPSType == "Fixed %" ? i_src + (i_src * (i_lxLvlSL / 100)) : i_src + i_lxLvlSL

slBotLvl = TPSType == "Fixed %" ? i_src - (i_src * (i_sxLvlSL / 100)) : i_src - i_lxLvlSL

slLine := condition <= 0.0 and leTrigger ? slBotLvl :

condition >= 0.0 and seTrigger ? slTopLvl : nz(slLine )

slLong = f_cross(low, slLine, false)

slShort = f_cross(high, slLine, true )

//

= f_tp(condition, 1.2,leTrigger, seTrigger, i_src, i_lxLvlTP3, i_sxLvlTP3)

= f_tp(condition, 1.1,leTrigger, seTrigger, i_src, i_lxLvlTP2, i_sxLvlTP2)

= f_tp(condition, 1.0,leTrigger, seTrigger, i_src, i_lxLvlTP1, i_sxLvlTP1)

tp3Long = f_cross(high, tp3Line, true )

tp3Short = f_cross(low, tp3Line, false)

tp2Long = f_cross(high, tp2Line, true )

tp2Short = f_cross(low, tp2Line, false)

tp1Long = f_cross(high, tp1Line, true )

tp1Short = f_cross(low, tp1Line, false)

switch

leTrigger and condition <= 0.0 => condition := 1.0

seTrigger and condition >= 0.0 => condition := -1.0

tp3Long and condition == 1.2 => condition := 1.3

tp3Short and condition == -1.2 => condition := -1.3

tp2Long and condition == 1.1 => condition := 1.2

tp2Short and condition == -1.1 => condition := -1.2

tp1Long and condition == 1.0 => condition := 1.1

tp1Short and condition == -1.0 => condition := -1.1

slLong and condition >= 1.0 => condition := 0.0

slShort and condition <= -1.0 => condition := 0.0

lxTrigger and condition >= 1.0 => condition := 0.0

sxTrigger and condition <= -1.0 => condition := 0.0

longE = leTrigger and condition <= 0.0 and condition == 1.0

shortE = seTrigger and condition >= 0.0 and condition == -1.0

longX = lxTrigger and condition >= 1.0 and condition == 0.0

shortX = sxTrigger and condition <= -1.0 and condition == 0.0

longSL = slLong and condition >= 1.0 and condition == 0.0

shortSL = slShort and condition <= -1.0 and condition == 0.0

longTP3 = tp3Long and condition == 1.2 and condition == 1.3

shortTP3 = tp3Short and condition == -1.2 and condition == -1.3

longTP2 = tp2Long and condition == 1.1 and condition == 1.2

shortTP2 = tp2Short and condition == -1.1 and condition == -1.2

longTP1 = tp1Long and condition == 1.0 and condition == 1.1

shortTP1 = tp1Short and condition == -1.0 and condition == -1.1

// ——————————— {

//

if strategy.position_size <= 0 and longE and TPSType == "ATR" and tradeDateIsAllowed

strategy.entry( 'Long', strategy.long, alert_message = i_leMsg, comment = 'LE')

if strategy.position_size > 0 and condition == 1.0 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'LXTP1', from_entry = 'Long', qty_percent = i_lxQtyTP1, limit = tp1Line, stop = slLine, comment_profit = 'LXTP1', comment_loss = 'SL', alert_profit = i_lxMsgTP1, alert_loss = i_lxMsgSL)

if strategy.position_size > 0 and condition == 1.1 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'LXTP2', from_entry = 'Long', qty_percent = i_lxQtyTP2, limit = tp2Line, stop = slLine, comment_profit = 'LXTP2', comment_loss = 'SL', alert_profit = i_lxMsgTP2, alert_loss = i_lxMsgSL)

if strategy.position_size > 0 and condition == 1.2 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'LXTP3', from_entry = 'Long', qty_percent = i_lxQtyTP3, limit = tp3Line, stop = slLine, comment_profit = 'LXTP3', comment_loss = 'SL', alert_profit = i_lxMsgTP3, alert_loss = i_lxMsgSL)

if longX and tradeDateIsAllowed

strategy.close( 'Long', alert_message = i_lxMsg, comment = 'LX')

//

if strategy.position_size >= 0 and shortE and TPSType == "ATR" and tradeDateIsAllowed

strategy.entry( 'Short', strategy.short, alert_message = i_leMsg, comment = 'SE')

if strategy.position_size < 0 and condition == -1.0 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'SXTP1', from_entry = 'Short', qty_percent = i_sxQtyTP1, limit = tp1Line, stop = slLine, comment_profit = 'SXTP1', comment_loss = 'SL', alert_profit = i_sxMsgTP1, alert_loss = i_sxMsgSL)

if strategy.position_size < 0 and condition == -1.1 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'SXTP2', from_entry = 'Short', qty_percent = i_sxQtyTP2, limit = tp2Line, stop = slLine, comment_profit = 'SXTP2', comment_loss = 'SL', alert_profit = i_sxMsgTP2, alert_loss = i_sxMsgSL)

if strategy.position_size < 0 and condition == -1.2 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'SXTP3', from_entry = 'Short', qty_percent = i_sxQtyTP3, limit = tp3Line, stop = slLine, comment_profit = 'SXTP3', comment_loss = 'SL', alert_profit = i_sxMsgTP3, alert_loss = i_sxMsgSL)

if shortX and tradeDateIsAllowed

strategy.close( 'Short', alert_message = i_sxMsg, comment = 'SX')

// ———————————

c_tp = leTrigger or seTrigger ? na :

condition == 0.0 ? na : color.green

c_entry = leTrigger or seTrigger ? na :

condition == 0.0 ? na : color.blue

c_sl = leTrigger or seTrigger ? na :

condition == 0.0 ? na : color.red

p_tp1Line = plot ( condition == 1.0 or condition == -1.0 ? tp1Line : na, title = "TP Line 1", color = c_tp, linewidth = 1, style = plot.style_linebr)

p_tp2Line = plot ( condition == 1.0 or condition == -1.0 or condition == 1.1 or condition == -1.1 ? tp2Line : na, title = "TP Line 2", color = c_tp, linewidth = 1, style = plot.style_linebr)

p_tp3Line = plot ( condition == 1.0 or condition == -1.0 or condition == 1.1 or condition == -1.1 or condition == 1.2 or condition == -1.2 ? tp3Line : na, title = "TP Line 3", color = c_tp, linewidth = 1, style = plot.style_linebr)

p_entryLine = plot ( condition >= 1.0 or condition <= -1.0 ? entryLine : na, title = "Entry Line", color = c_entry, linewidth = 1, style = plot.style_linebr)

p_slLine = plot ( condition == 1.0 or condition == -1.0 or condition == 1.1 or condition == -1.1 or condition == 1.2 or condition == -1.2 ? slLine : na, title = "SL Line", color = c_sl, linewidth = 1, style = plot.style_linebr)

//fill( p_tp3Line, p_entryLine, color = leTrigger or seTrigger ? na :color.new(color.green, 90))

fill( p_entryLine, p_slLine, color = leTrigger or seTrigger ? na :color.new(color.red, 90))

//

plotshape( i_alertOn and longE, title = 'Long', text = 'Long', textcolor = color.white, color = color.green, style = shape.labelup, size = size.tiny, location = location.belowbar)

plotshape( i_alertOn and shortE, title = 'Short', text = 'Short', textcolor = color.white, color = color.red, style = shape.labeldown, size = size.tiny, location = location.abovebar)

plotshape( i_alertOn and (longX or shortX) ? close : na, title = 'Close', text = 'Close', textcolor = color.white, color = color.gray, style = shape.labelup, size = size.tiny, location = location.absolute)

l_tp = i_alertOn and (longTP1 or shortTP1) ? close : na

plotshape( l_tp, title = "TP1 Cross", text = "TP1", textcolor = color.white, color = #ec407a, style = shape.labelup, size = size.tiny, location = location.absolute)

plotshape( i_alertOn and (longTP2 or shortTP2) ? close : na, title = "TP2 Cross", text = "TP2", textcolor = color.white, color = #ec407a, style = shape.labelup, size = size.tiny, location = location.absolute)

plotshape( i_alertOn and (longTP3 or shortTP3) ? close : na, title = "TP3 Cross", text = "TP3", textcolor = color.white, color = #ec407a, style = shape.labelup, size = size.tiny, location = location.absolute)

plotshape( i_alertOn and (longSL or shortSL) ? close : na, title = "SL Cross", text = "SL", textcolor = color.white, color = color.maroon, style = shape.labelup, size = size.tiny, location = location.absolute)

//

plot( na, title = "─── ───", editable = false, display = display.data_window)

plot( condition, title = "condition", editable = false, display = display.data_window)

plot( strategy.position_size * 100, title = ".position_size", editable = false, display = display.data_window)

//#endregion }

// ——————————— <↑↑↑ G_RISK ↑↑↑>

//#region ———— <↓↓↓ G_SCRIPT02 ↓↓↓> {

// @function Queues a new element in an array and de-queues its first element.

f_qDq(_array, _val) =>

array.push(_array, _val)

_return = array.shift(_array)

_return

var line a_slLine = array.new_line(1)

var line a_entryLine = array.new_line(1)

var line a_tp3Line = array.new_line(1)

var line a_tp2Line = array.new_line(1)

var line a_tp1Line = array.new_line(1)

var label a_slLabel = array.new_label(1)

var label a_tp3label = array.new_label(1)

var label a_tp2label = array.new_label(1)

var label a_tp1label = array.new_label(1)

var label a_entryLabel = array.new_label(1)

newEntry = longE or shortE

entryIndex = 1

entryIndex := newEntry ? bar_index : nz(entryIndex )

lasTrade = bar_index >= entryIndex

l_right = 10

if TPSType == "ATR"

line.delete( f_qDq(a_slLine, line.new( entryIndex, slLine, last_bar_index + l_right, slLine, style = line.style_solid, color = c_sl)))

if TPSType == "ATR"

line.delete( f_qDq(a_entryLine, line.new( entryIndex, entryLine, last_bar_index + l_right, entryLine, style = line.style_solid, color = color.blue)))

if TPSType == "ATR"

line.delete( f_qDq(a_tp3Line, line.new( entryIndex, tp3Line, last_bar_index + l_right, tp3Line, style = line.style_solid, color = c_tp)))

if TPSType == "ATR"

line.delete( f_qDq(a_tp2Line, line.new( entryIndex, tp2Line, last_bar_index + l_right, tp2Line, style = line.style_solid, color = c_tp)))

if TPSType == "ATR"

line.delete( f_qDq(a_tp1Line, line.new( entryIndex, tp1Line, last_bar_index + l_right, tp1Line, style = line.style_solid, color = c_tp)))

if TPSType == "ATR"

label.delete( f_qDq(a_slLabel, label.new( last_bar_index + l_right, slLine, 'SL: ' + str.tostring(slLine, '##.###'), style = label.style_label_left, textcolor = color.white, color = c_sl)))

if TPSType == "ATR"

label.delete( f_qDq(a_entryLabel, label.new( last_bar_index + l_right, entryLine, 'Entry: ' + str.tostring(entryLine, '##.###'), style = label.style_label_left, textcolor = color.white, color = color.blue)))

if TPSType == "ATR"

label.delete( f_qDq(a_tp3label, label.new( last_bar_index + l_right, tp3Line, 'TP3: ' + str.tostring(tp3Line, '##.###') + " - Target Pips : - " + str.tostring(longE ? tp3Line - entryLine : entryLine - tp3Line, "#.##"), style = label.style_label_left, textcolor = color.white, color = c_tp)))

if TPSType == "ATR"

label.delete( f_qDq(a_tp2label, label.new( last_bar_index + l_right, tp2Line, 'TP2: ' + str.tostring(tp2Line, '##.###'), style = label.style_label_left, textcolor = color.white, color = c_tp)))

if TPSType == "ATR"

label.delete( f_qDq(a_tp1label, label.new( last_bar_index + l_right, tp1Line, 'TP1: ' + str.tostring(tp1Line, '##.###'), style = label.style_label_left, textcolor = color.white, color = c_tp)))

//#endregion }

// ——————————— <↑↑↑ G_SCRIPT02 ↑↑↑>

c_barCol = close > open ? color.rgb(120, 9, 139) : color.rgb(69, 155, 225)

barcolor(

i_barColOn ? c_barCol : na)

// ———————————

//

if longE or shortE or longX or shortX

alert(message = 'Any Alert', freq = alert.freq_once_per_bar_close)

if longE

alert(message = 'Long Entry', freq = alert.freq_once_per_bar_close)

if shortE

alert(message = 'Short Entry', freq = alert.freq_once_per_bar_close)

if longX

alert(message = 'Long Exit', freq = alert.freq_once_per_bar_close)

if shortX

alert(message = 'Short Exit', freq = alert.freq_once_per_bar_close)

//#endregion }

// ——————————— <↑↑↑ G_SCRIPT03 ↑↑↑>

// This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © TraderHalai

// This script was born out of my quest to be able to display strategy back test statistics on charts to allow for easier backtesting on devices that do not natively support backtest engine (such as mobile phones, when I am backtesting from away from my computer). There are already a few good ones on TradingView, but most / many are too complicated for my needs.

//

//Found an excellent display backtest engine by 'The Art of Trading'. This script is a snippet of his hard work, with some very minor tweaks and changes. Much respect to the original author.

//

//Full credit to the original author of this script. It can be found here: www.tradingview.com

//

// This script can be copied and airlifted onto existing strategy scripts of your own, and integrates out of the box without implementation of additional functions. I've also added Max Runup, Average Win and Average Loss per trade to the orignal script.

//

//Will look to add in more performance metrics in future, as I further develop this script.

//

//Feel free to use this display panel in your scripts and strategies.

//Thanks and enjoy! :)

//@version=5

//strategy("Strategy BackTest Display Statistics - TraderHalai", overlay=true, default_qty_value= 5, default_qty_type = strategy.percent_of_equity, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.1)

//DEMO basic strategy - Use your own strategy here - Jaws Mean Reversion from my profile used here

//source = input(title = "Source", defval = close)

///////////////////////////// --- BEGIN TESTER CODE --- ////////////////////////

// COPY below into your strategy to enable display

////////////////////////////////////////////////////////////////////////////////

// Declare performance tracking variables

drawTester = input.bool(false, "Strategy Performance", group='Dashboards', inline="Show Dashboards")

var balance = strategy.initial_capital

var drawdown = 0.0

var maxDrawdown = 0.0

var maxBalance = 0.0

var totalWins = 0

var totalLoss = 0

// Prepare stats table

var table testTable = table.new(position.top_right, 5, 2, border_width=1)

f_fillCell(_table, _column, _row, _title, _value, _bgcolor, _txtcolor) =>

_cellText = _title + "\n" + _value

table.cell(_table, _column, _row, _cellText, bgcolor=_bgcolor, text_color=_txtcolor)

// Custom function to truncate (cut) excess decimal places

//truncate(_number, _decimalPlaces) =>

// _factor = math.pow(10, _decimalPlaces)

// int(_number * _factor) / _factor

// Draw stats table

var bgcolor = color.new(color.black,0)

if drawTester and tradeDateIsAllowed

if barstate.islastconfirmedhistory

// Update table

dollarReturn = strategy.netprofit

f_fillCell(testTable, 0, 0, "Total Trades:", str.tostring(strategy.closedtrades), bgcolor, color.white)

f_fillCell(testTable, 0, 1, "Win Rate:", str.tostring(truncate((strategy.wintrades/strategy.closedtrades)*100,2)) + "%", bgcolor, color.white)

f_fillCell(testTable, 1, 0, "Starting:", "$" + str.tostring(strategy.initial_capital), bgcolor, color.white)

f_fillCell(testTable, 1, 1, "Ending:", "$" + str.tostring(truncate(strategy.initial_capital + strategy.netprofit,2)), bgcolor, color.white)

f_fillCell(testTable, 2, 0, "Avg Win:", "$"+ str.tostring(truncate(strategy.grossprofit / strategy.wintrades, 2)), bgcolor, color.white)

f_fillCell(testTable, 2, 1, "Avg Loss:", "$"+ str.tostring(truncate(strategy.grossloss / strategy.losstrades, 2)), bgcolor, color.white)

f_fillCell(testTable, 3, 0, "Profit Factor:", str.tostring(truncate(strategy.grossprofit / strategy.grossloss,2)), strategy.grossprofit > strategy.grossloss ? color.green : color.red, color.white)

f_fillCell(testTable, 3, 1, "Max Runup:", str.tostring(truncate(strategy.max_runup, 2 )), bgcolor, color.white)

f_fillCell(testTable, 4, 0, "Return:", (dollarReturn > 0 ? "+" : "") + str.tostring(truncate((dollarReturn / strategy.initial_capital)*100,2)) + "%", dollarReturn > 0 ? color.green : color.red, color.white)

f_fillCell(testTable, 4, 1, "Max DD:", str.tostring(truncate((strategy.max_drawdown / strategy.equity) * 100 ,2)) + "%", color.red, color.white)

// --- END TESTER CODE --- ///////////////

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © niceGear68734

//@version=5

//strategy("Table to filter trades per day", overlay=true, use_bar_magnifier = true, initial_capital = 5000, calc_on_every_tick = true, calc_on_order_fills = true, commission_type = strategy.commission.cash_per_contract)

//~ ___________________________________________________________________________

//~ !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

//~ !!!!!!!!!!!!!!!_________________ START _________________!!!!!!!!!!!!!!!!!

i_showweeklyPerformance = input.bool(false, 'Weekly Performance', group='Dashboards', inline="Show Dashboards")

//__________________________ User Inputs ___________________________________

var const string g_table = "Table Settings"

i_table_pos = "Top Left" //input.string(defval = "Top Left", title = "Position", options = , group = g_table, inline = "1", tooltip = "It sets the location of the table")

i_text_size = "Normal" //input.string(defval = "Normal", title = "Set the size of text", options = , tooltip = "This option is used to change the size of the text in the table")

var const string g_general = "General Settings"

i_check_open_close = "Opened" //input.string("Opened", "Check when the trade :", , group = g_general, tooltip = "This parameter defines what to check for. If opened is selected, the results will show the trades that opened on that day. If closed is selected, the results will show the trades that closed on that day")

i_timezone = "Exchange" //input.string("Exchange", title = "Set the Timezone", options = , group = g_general, tooltip = "You can use this setting whenever you want to change the time that the trade has closed/opened")

//~_____________________________ Switches ___________________________________

table_pos = switch i_table_pos

"Bottom Right" => position.bottom_right

"Bottom Left" => position.bottom_left

"Top Right" => position.top_right

"Top Left" => position.top_left

timezone_setting = i_timezone == "Exchange" ? syminfo.timezone : i_timezone

text_size = switch i_text_size

"Small" => size.small

"Normal" => size.normal

"Large" => size.large

//__________________________ Array Declaration _____________________________

var string t_column_names = array.from( "", "Sun", "Mon", "Tue", "Wed", "Thur", "Fri", "Sat") // Columns header names

var string t_row_names = array.from("", "Total Trades", "Loss", "Win", "Win Rate" ) // Rows header names

var t_column_size = array.size(t_column_names)

var t_row_size = array.size(t_row_names)

var string a_closed_trades = array.new_string() // Save the total number of trades

var string a_loss_trades = array.new_string() // Save the number of losing trades

var string a_win_trades = array.new_string() // Save the number of winning trades

var _a_day_week = array.new_int() // Save the day of the week to split data

// __________________________ Custom Functions ________________________________

//~ create a counter so that it gives a number to strategy.closed_trades.entry_time(counter)

var trade_number = -1

if strategy.closedtrades > strategy.closedtrades

trade_number += 1

f_strategy_closedtrades_hour() =>

switch

i_check_open_close =="Closed" => dayofweek(strategy.closedtrades.exit_time(trade_number), timezone_setting)

i_check_open_close =="Opened" => dayofweek(strategy.closedtrades.entry_time(trade_number), timezone_setting)

f_data(_i) =>

var _closed_trades = 0

var _loss_trades = 0

var _win_trades = 0

var _txt_closed_trades = ""

var _txt_loss_trades = ""

var _txt_win_trades = ""

if strategy.closedtrades > strategy.closedtrades and f_strategy_closedtrades_hour() == _i

_closed_trades += 1

_txt_closed_trades := str.tostring(_closed_trades)

if strategy.losstrades > strategy.losstrades and f_strategy_closedtrades_hour() == _i

_loss_trades += 1

_txt_loss_trades := str.tostring(_loss_trades)

if strategy.wintrades > strategy.wintrades and f_strategy_closedtrades_hour() == _i

_win_trades += 1

_txt_win_trades := str.tostring(_win_trades)

//__________________________

var string array1 = array.new_string(5)

var string array2 = array.new_string(5)

var string array3 = array.new_string(5)

var string array4 = array.new_string(5)

var string array5 = array.new_string(5)

var string array6 = array.new_string(5)

var string array7 = array.new_string(5)

f_pass_data_to_array(_i, _array) =>

= f_data(_i)

array.set(_array,1 , cl)

array.set(_array,2,loss)

array.set(_array,3,win)

if cl != ""

array.set(_array,4,str.tostring(str.tonumber(win) / str.tonumber(cl) * 100 , "##") + " %")

if cl != "" and win == ""

array.set(_array,4,"0 %")

for i = 1 to 7

switch

i == 1 => f_pass_data_to_array(i,array1)

i == 2 => f_pass_data_to_array(i,array2)

i == 3 => f_pass_data_to_array(i,array3)

i == 4 => f_pass_data_to_array(i,array4)

i == 5 => f_pass_data_to_array(i,array5)

i == 6 => f_pass_data_to_array(i,array6)

i == 7 => f_pass_data_to_array(i,array7)

f_retrieve_data_to_table(_i, _j) =>

switch

_i == 1 => array.get(array1, _j)

_i == 2 => array.get(array2, _j)

_i == 3 => array.get(array3, _j)

_i == 4 => array.get(array4, _j)

_i == 5 => array.get(array5, _j)

_i == 6 => array.get(array6, _j)

_i == 7 => array.get(array7, _j)

//~ ___________________________ Create Table ________________________________

create_table(_col, _row, _txt) =>

var table _tbl = table.new(position = table_pos, columns = t_column_size , rows = t_row_size, border_width=1)

color _color = _row == 0 or _col == 0 ? color.rgb(3, 62, 106) : color.rgb(2, 81, 155)

table.cell(_tbl, _col, _row, _txt, bgcolor = _color, text_color = color.white, text_size = text_size)

//~___________________________ Fill With Data _______________________________

if barstate.islastconfirmedhistory and i_showweeklyPerformance and tradeDateIsAllowed

for i = 0 to t_column_size - 1 by 1

for j = 0 to t_row_size - 1 by 1

_txt = ""

if i >= 0 and j == 0

_txt := array.get(t_column_names, i)

if j >= 0 and i == 0

_txt := array.get(t_row_names, j)

if i >= 1 and j >= 1 and j <= 5

_txt := f_retrieve_data_to_table( i , j)

create_table(i ,j , _txt)

//~ ___________________________ Notice ______________________________________

if timeframe.in_seconds() > timeframe.in_seconds("D")

x = table.new(position.middle_center,1,1,color.aqua)

table.cell_set_text(x,0,0,"Please select lower timeframes (Daily or lower)")

//~ !!!!!!!!!!!!!!!_________________ STOP _________________!!!!!!!!!!!!!!!!!!

//~ !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

//~ ___________________________________________________________________________

// Global Dashboard Variables

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

// Dashboard Table Text Size

i_tableTextSize = "Normal" //input.string(title="Dashboard Size", defval="Normal", options= , group="Dashboards")

table_text_size(s) =>

switch s

"Auto" => size.auto

"Huge" => size.huge

"Large" => size.large

"Normal" => size.normal

"Small" => size.small

=> size.tiny

tableTextSize = table_text_size(i_tableTextSize)

// Monthly Table Performance Dashboard By @QuantNomad

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

i_showMonthlyPerformance = input.bool(false, 'Monthly Performance', group='Dashboards', inline="Show Dashboards")

i_monthlyReturnPercision = 2

if i_showMonthlyPerformance and tradeDateIsAllowed

new_month = month(time) != month(time )

new_year = year(time) != year(time )

eq = strategy.equity

bar_pnl = eq / eq - 1

cur_month_pnl = 0.0

cur_year_pnl = 0.0

// Current Monthly P&L;

cur_month_pnl := new_month ? 0.0 :

(1 + cur_month_pnl ) * (1 + bar_pnl) - 1

// Current Yearly P&L;

cur_year_pnl := new_year ? 0.0 :

(1 + cur_year_pnl ) * (1 + bar_pnl) - 1

// Arrays to store Yearly and Monthly P&Ls;

var month_pnl = array.new_float(0)

var month_time = array.new_int(0)

var year_pnl = array.new_float(0)

var year_time = array.new_int(0)

last_computed = false

if (not na(cur_month_pnl ) and (new_month or barstate.islastconfirmedhistory))

if (last_computed )

array.pop(month_pnl)

array.pop(month_time)

array.push(month_pnl , cur_month_pnl )

array.push(month_time, time )

if (not na(cur_year_pnl ) and (new_year or barstate.islastconfirmedhistory))

if (last_computed )

array.pop(year_pnl)

array.pop(year_time)

array.push(year_pnl , cur_year_pnl )

array.push(year_time, time )

last_computed := barstate.islastconfirmedhistory ? true : nz(last_computed )

// Monthly P&L; Table

var monthly_table = table(na)

if (barstate.islastconfirmedhistory)

monthly_table := table.new(position.bottom_right, columns = 14, rows = array.size(year_pnl) + 1, border_width = 1)

table.cell(monthly_table, 0, 0, "", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 1, 0, "Jan", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 2, 0, "Feb", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 3, 0, "Mar", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 4, 0, "Apr", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 5, 0, "May", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 6, 0, "Jun", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 7, 0, "Jul", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 8, 0, "Aug", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 9, 0, "Sep", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 10, 0, "Oct", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 11, 0, "Nov", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 12, 0, "Dec", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 13, 0, "Year", bgcolor = #999999, text_size=tableTextSize)

for yi = 0 to array.size(year_pnl) - 1

table.cell(monthly_table, 0, yi + 1, str.tostring(year(array.get(year_time, yi))), bgcolor = #cccccc, text_size=tableTextSize)

y_color = array.get(year_pnl, yi) > 0 ? color.new(color.teal, transp = 40) : color.new(color.gray, transp = 40)

table.cell(monthly_table, 13, yi + 1, str.tostring(math.round(array.get(year_pnl, yi) * 100, i_monthlyReturnPercision)), bgcolor = y_color, text_color=color.new(color.white, 0),text_size=tableTextSize)

for mi = 0 to array.size(month_time) - 1

m_row = year(array.get(month_time, mi)) - year(array.get(year_time, 0)) + 1

m_col = month(array.get(month_time, mi))

m_color = array.get(month_pnl, mi) > 0 ? color.new(color.teal, transp = 40) : color.new(color.maroon, transp = 40)

table.cell(monthly_table, m_col, m_row, str.tostring(math.round(array.get(month_pnl, mi) * 100, i_monthlyReturnPercision)), bgcolor = m_color, text_color=color.new(color.white, 0), text_size=tableTextSize)

hide = timeframe.isintraday

// Input for EMA period

emaPeriod = 48 //input.int(48, title="EMA Period")

emaPeriod2 = 2 //input.int(2, title="EME Period 2")

emaPeriod3 = 21 //input.int(21, title="EMA Period")

// Input to toggle EMA Cloud

showcloud = input.bool(false, title="Plot EMA?", group='EMA & ATR', inline="Show EMA's & ATR")

useHTF = input.bool(true, title = "Use Higher Time Frame?")

matimeframe = useHTF ? my_time1 : ''

// EMA calculations

ema = request.security(syminfo.tickerid, matimeframe, ta.ema(close, emaPeriod))

ema2 = request.security(syminfo.tickerid, matimeframe, ta.ema(close,emaPeriod2))

ema3 = request.security(syminfo.tickerid, matimeframe,ta.ema(close, emaPeriod3))

emaColor = close > ema3 ? color.new(color.rgb(56, 142, 60, 63), 50) : color.new(color.rgb(147, 40, 51, 38), 50)

// Plotting EMA's

// plot_ema1 = plot(hide ? ema : na, style=plot.style_line, color=color.new(color.rgb(255, 255, 255, 100), 50), title="EMA", linewidth=2)

// plot_ema2 = plot(hide ? ema2 : na, style=plot.style_line, color=color.new(color.rgb(255, 255, 255, 100), 50), title="EMA", linewidth=1)

// plot_ema3 = plot(ema3, style=plot.style_line, color=emaColor, title="EMA", linewidth=1)

// EMA Cloud

cloudColor = ema2 > ema ? color.new(#0f8513, 80) : color.new(#a81414, 80)

cloudColor2 = ema2 > ema3 ? color.new(#0f8513, 50) : color.new(#a81414, 50)

cloudColor := showcloud ? cloudColor : na

// fill(plot_ema1, plot_ema2, color=cloudColor, title="EMA Cloud")

// fill(plot_ema3, plot_ema2, color=cloudColor, title="EMA Cloud")

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © BackQuant

import TradingView/ta/4 as ta

//@version=5

//indicator(

// title="DEMA Adjusted Average True Range ",

// shorttitle = "DEMA ATR ",

// overlay=true,

// timeframe="",

// timeframe_gaps=true

// )

// Define User Inputs

simple bool showAtr = input.bool(false, "Plot Dema?", group='EMA & ATR', inline="Show EMA's & ATR")

simple bool haCandles = true //input.bool(true, "Use HA Candles?")

simple int periodDema = 7 //input.int(7, "Dema Period", group = "Dema Atr")

series float sourceDema = close //input.source(close, "Calculation Source", group = "Dema Atr")

simple int periodAtr = 14 //input.int(14, "Period", group = "Dema Atr")

simple float factorAtr = 1.7 //input.float(1.7, "Factor", step = 0.01, group = "Dema Atr")

simple color longColour = #66bb6a

simple color shortColour = #f23645

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// Use HA Candles?

heikinashi_close = request.security(

symbol = ticker.heikinashi(syminfo.tickerid),

timeframe = timeframe.period,

expression = close,

gaps = barmerge.gaps_off,

lookahead = barmerge.lookahead_on

)

var series float source = close

if haCandles == true

source := heikinashi_close

if haCandles == false

source := sourceDema

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// Function

DemaAtrWithBands(periodDema, source, lookback, atrFactor)=>

ema1 = ta.ema(source, periodDema)

ema2 = ta.ema(ema1, periodDema)

demaOut = 2 * ema1 - ema2

atr = ta.atr(lookback)

trueRange = atr * atrFactor

DemaAtr = demaOut

DemaAtr := nz(DemaAtr , DemaAtr)

trueRangeUpper = demaOut + trueRange

trueRangeLower = demaOut - trueRange

if trueRangeLower > DemaAtr

DemaAtr := trueRangeLower

if trueRangeUpper < DemaAtr

DemaAtr := trueRangeUpper

DemaAtr

// Function Out

DemaAtr = DemaAtrWithBands(periodDema, source, periodAtr, factorAtr)

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// Conditions

DemaAtrLong = DemaAtr > DemaAtr

DemaAtrShort = DemaAtr < DemaAtr

// Colour Condtions

var color Trendcolor = #ffffff

if DemaAtrLong

Trendcolor := longColour

if DemaAtrShort

Trendcolor := shortColour

// Plotting

plot( showAtr ? DemaAtr : na, "ATR", color=Trendcolor, linewidth = 2 )

import DevLucem/ZigLib/1 as ZigZag

////////

// Fetch Ingredients

//

// ////////

// // Bake it with a simple oven this time

= ZigZag.zigzag(low, high, Depth, Deviation, Backstep)

string nowPoint = ""

var float lastPoint = z1.price

if bool(ta.change(direction))

lastPoint := z1.price

// ////////

// // Let it Cool And Serve

line zz = na

label point = na

if repaint

zz := line.new(z1, z2, xloc.bar_time, extend? extend.right: extend.none, color.new(direction>0? upcolor: dncolor, lines), width=line_thick)

nowPoint := direction<0? (z2.pricelastPoint? "HH": "LH")

point := label.new(z2, nowPoint, xloc.bar_time, yloc.price,

color.new(direction<0? upcolor: dncolor, labels), direction>0? label.style_label_down: label.style_label_up, color.new(direction>0? upcolor: dncolor, labels), label_size)

if direction == direction

line.delete(zz )

label.delete(point )

else

line.set_extend(zz , extend.none)

else

if direction != direction

zz := line.new(z1 , z2 , xloc.bar_time, extend.none, color.new(direction>0? upcolor: dncolor, lines), width=line_thick)

nowPoint := direction <0? (z2.price lastPoint ? "HH": "LH")

point := label.new(z2 , nowPoint, xloc.bar_time, yloc.price,

color.new(direction <0? upcolor: dncolor, labels), direction >0? label.style_label_down: label.style_label_up, color.new(direction >0? upcolor: dncolor, labels), label_size)

bgcolor(direction<0? color.new(dncolor, background): color.new(upcolor, background), title='Direction Background', display = display.none)

plotarrow(direction, "direction", display=display.status_line)

// ////////

// // Declare Meal Was Sweet By Force

alertcondition(nowPoint == "HH" and z2.price != z2.price , "New Higher High", 'Zigzag on {{ticker}} higher higher high detected at {{time}}')

alertcondition(nowPoint == "LH" and z2.price != z2.price , "New Lower High", 'Zigzag on {{ticker}} higher lower high detected at {{time}}')

alertcondition(nowPoint == "HL" and z2.price != z2.price , "New Higher Low", 'Zigzag on {{ticker}} higher lower low detected at {{time}}')

alertcondition(nowPoint == "LL" and z2.price != z2.price , "New Lower Low", 'Zigzag on {{ticker}} lower low detected at {{time}}')

alertcondition(direction != direction , 'Direction Changed', 'Zigzag on {{ticker}} direction changed at {{time}}')

alertcondition(direction != direction and direction>0, 'Bullish Direction', 'Zigzag on {{ticker}} bullish direction at {{time}}')

alertcondition(direction != direction and direction<0, 'Bearish Direction', 'Zigzag on {{ticker}} bearish direction at {{time}}')

if direction != direction

alert((direction<0? "Bearish": "Bullish") + " Direction Final ", alert.freq_once_per_bar_close)

MSG = "MARKET STRUCTURE"

VBG = "VOLUMETRIC ORDER BLOCKS"

MST = "Limit market structure calculation to improve memory speed time"

SLT = " Limit swing structure to tot bars back"

IDT = " Start date of the internal structure"

CST = "Color candle based on trend detection system"

OBT = "Display internal buy and sell activity"

OBD = "Show Last number of orderblock"

OBMT = " Use Length to adjust cordinate of the orderblocks\n Use whole candle body"

_ ='

------------

–––––––––––––––––––––––––– INPUTS –––––––––––––––––––––––––––

------------ '//{

bool windowsis = input.bool(true, "Window", inline="kla", group=MSG)

int mswindow = input.int(5000, "", tooltip=MST,group=MSG, inline="kla", minval=1000)

bool showSwing = input.bool(true, "Swing", inline="scss", group=MSG)

int swingLimit = input.int(100, "", tooltip=SLT, inline="scss", group=MSG, minval=10, maxval=200)

color swingcssup = input.color(#f7525f, "", inline="scss", group=MSG)

color swingcssdn = input.color(#66bb6a, "", inline="scss", group=MSG)

bool showMapping = input.bool(false, "Mapping Structure", inline="mapping", group=MSG)

string mappingStyle = input.string("----", "", options= , inline="mapping", group=MSG)

color mappingcss = input.color(color.silver, "", tooltip="Display Mapping Structure", inline="mapping", group=MSG)

bool candlecss = input.bool(false, "Color Candles", tooltip=CST, group=MSG, inline="txt")

string mstext = input.string("Tiny", "", options= ,

inline="txt", group=MSG)

string msmode = input.string("Adjusted Points", "Algorithmic Logic", options=

, inline="node", group=MSG)

int mslen = input.int(5, "", inline="node", group=MSG, minval=2)

bool buildsweep = input.bool(true, "Build Sweep (x)", "Build sweep on market structure", "znc", MSG)

bool msbubble = input.bool(true, "Bubbles", tooltip="Display Circle Bubbles", inline="bubbles", group=MSG)

bool obshow = input.bool(true, "Show Last", tooltip=OBD, group=VBG, inline="obshow")

int oblast = input.int(5, "", group=VBG, inline="obshow", minval=0)

color obupcs = input.color(color.new(#089981, 90), "", inline="obshow", group=VBG)

color obdncs = input.color(color.new(#f23645, 90), "", inline="obshow", group=VBG)

bool obshowactivity = input.bool(true, "Show Buy/Sell Activity", inline="act", group=VBG, tooltip=OBT)

color obactup = input.color(color.new(#089981, 50), "", inline="act", group=VBG)

color obactdn = input.color(color.new(#f23645, 50), "", inline="act", group=VBG)

obshowbb = input.bool(false, "Show Breakers", inline="bb", group=VBG, tooltip="Display Breakers")

color bbup = input.color(color.new(#089981, 100), "", inline="bb", group=VBG)

color bbdn = input.color(color.new(#f23645, 100), "", inline="bb", group=VBG)

obmode = input.string("Length", "Construction", options= , tooltip=OBMT, inline="atr", group=VBG)

len = input.int(5, "", inline="atr", group=VBG, minval=1)

obmiti = input.string("Close", "Mitigation Method", options= ,

tooltip="Mitigation method for when to trigger order blocks", group=VBG)

obtxt = input.string("Normal", "Metric Size", options= ,

tooltip="Order block Metrics text size", inline="txt", group=VBG)

showmetric = input.bool(true, "Show Metrics", group=VBG)

showline = input.bool(true, "Show Mid-Line", group=VBG)

overlap = input.bool(true, "Hide Overlap", group=VBG, inline="ov")

wichlap = input.string("Recent", "", options= , inline="ov", group=VBG)

fvg_enable = input.bool(false, "", inline="1", group="FAIR VALUE GAP", tooltip="Display fair value gap")

what_fvg = input.string("FVG", "", inline="1", group="FAIR VALUE GAP", tooltip="Display fair value gap",

options= )

fvg_num = input.int(5, "Show Last", inline="1a", group="FAIR VALUE GAP", tooltip="Number of fvg to show", minval=0)

fvg_upcss = input.color(color.new(#089981, 80), "", inline="1", group="FAIR VALUE GAP")

fvg_dncss = input.color(color.new(#f23645, 80), "", inline="1", group="FAIR VALUE GAP")

fvgbbup = input.color(color.new(#089981, 100), "", inline="1", group="FAIR VALUE GAP")

fvgbbdn = input.color(color.new(#f23645, 100), "", inline="1", group="FAIR VALUE GAP")

fvg_src = input.string("Close", "Mitigation",

inline="3",

group="FAIR VALUE GAP",

tooltip=" Use the close of the body as trigger\n\n Use the extreme point of the body as trigger",

options= )

fvgthresh = input.float(0, "Threshold", tooltip="Filter out non significative FVG", group="FAIR VALUE GAP",

inline="asd", minval=0, maxval=2, step=0.1)

fvgoverlap = input.bool(true, "Hide Overlap", "Hide overlapping FVG", group="FAIR VALUE GAP")

fvgline = input.bool(true, "Show Mid-Line", group="FAIR VALUE GAP")

fvgextend = input.bool(false, "Extend FVG", group="FAIR VALUE GAP")

dispraid = input.bool(false, "Display Raids", inline="raid", group="FAIR VALUE GAP")

//}

_ ='

------------

–––––––––––––––––––––––––– UDT –––––––––––––––––––––––––––

------------ '//{

type hqlzone

box pbx

box ebx

box lbx

label plb

label elb

label lbl

type Zphl

line top

line bottom

label top_label

label bottom_label

bool stopcross

bool sbottomcross

bool itopcross

bool ibottomcross

string txtup

string txtdn

float topy

float bottomy

float topx

float bottomx

float tup

float tdn

int tupx

int tdnx

float itopy

float itopx

float ibottomy

float ibottomx

float uV

float dV

type entered

bool normal = false

bool breaker = false

type store

line ln

label lb

box bx

linefill lf

type structure

int zn

float zz

float bos

float choch

int loc

int temp

int trend

int start

float main

int xloc

bool upsweep

bool dnsweep

string txt = na

type drawms

int x1

int x2

float y

string txt

color css

string style

type ob

bool bull

float top

float btm

float avg

int loc

color css

float vol

int dir

int move

int blPOS

int brPOS

int xlocbl

int xlocbr

bool isbb = false

int bbloc

type FVG

float top = na

float btm = na

int loc = bar_index

bool isbb = false

int bbloc = na

bool israid = false

float raidy = na

int raidloc = na

int raidx2 = na

bool active = false

color raidcs = na

type SFP

float y

int loc

float ancor

type sfpbuildlbl

int x

float y

string style

color css

string txt

type sfpbuildline

int x1

int x2

float y

color css

float ancor

int loc

type equalbuild

int x1

float y1

int x2

float y2

color css

string style

type equalname

int x

float y

string txt

color css

string style

type ehl

float pt

int t

float pb

int b

type sellbuyside

float top

float btm

int loc

color css

string txt

float vol

type timer

bool start = false

int count = 0

//}

_ ='

------------

–––––––––––––––––––––––––– SETUP –––––––––––––––––––––––––––

------------ '//{

var store bin = store.new(

array.new< line >()

, array.new< label >()

, array.new< box >()

, array.new()

)

var entered blobenter = entered.new()

var entered brobenter = entered.new()

var entered blfvgenter = entered.new()

var entered brfvgenter = entered.new()

var entered blarea = entered.new()

var entered brarea = entered.new()

var timer lc = timer.new ()

if barstate.islast

for obj in bin.ln

obj.delete()

for obj in bin.lb

obj.delete()

for obj in bin.bx

obj.delete()

for obj in bin.lf

obj.delete()

bin.ln.clear()

bin.lb.clear()

bin.bx.clear()

bin.lf.clear()

invcol = #ffffff00

float atr = (ta.atr(200) / (5/len))

//}

_ ='

------------

–––––––––––––––––––––––––– UTILITY –––––––––––––––––––––––––––

------------ '//{

method txSz(string s) =>

out = switch s

"Tiny" => size.tiny

"Small" => size.small

"Normal" => size.normal

"Large" => size.large

"Huge" => size.huge

"Auto" => size.auto

out

method lstyle(string style) =>

out = switch style

'⎯⎯⎯⎯' => line.style_solid

'----' => line.style_dashed

'····' => line.style_dotted

ghl() => [high , low , close , open , close, open, high, low, high , low , ta.atr(200)]

method IDMIDX(bool use_max, int loc) =>

min = 99999999.

max = 0.

idx = 0

if use_max

for i = 0 to (bar_index - loc)

max := math.max(high , max)

min := max == high ? low : min

idx := max == high ? i : idx

else

for i = 0 to (bar_index - loc)

min := math.min(low , min)

max := min == low ? high : max

idx := min == low ? i : idx

idx

SFPData() => [high, high , high , low, low , low , close, volume, time, bar_index , time ]

SFPcords() =>

RealTF = barstate.isrealtime ? 0 : 1

= SFPData()

[h , h1 , h2 , l , l1 , l2 , c , v , t , n , t1 ]

method find(structure ms, bool use_max, bool sweep, bool useob) =>

min = 99999999.

max = 0.

idx = 0

if not sweep

if ((bar_index - ms.loc) - 1) > 0

if use_max

for i = 0 to (bar_index - ms.loc) - 1

max := math.max(high , max)

min := max == high ? low : min

idx := max == high ? i : idx

if useob

if high

ICT Smart Money - PremiumCME_MINI:NQ1!

✅ Detecting FVG boxes (green/red) for A+ setups

✅ When price taps back into the FVG, it triggers an entry

✅ Shows the position boxes (green profit zone, red SL zone)

✅ Calculates SL (25-35 points auto or fixed)

✅ Sets TP1, TP2, TP3 based on liquidity levels (swing highs/lows)

✅ Shows labels with entry price, SL in points, and TP levels with R:R

OsMA by A8/4 - Limited Edition🌟 **OsMA by A8/4 — The Ultimate Indicator for XAUUSD Trading** 🌟

An intelligent **automated system** designed exclusively for **gold trading**, equipped with everything you need in one tool 🔥

💡 **Key Features of OsMA by A8/4**

✅ **Auto Entry Signals**

Automatically detects trade opportunities using a **refined MACD Histogram formula** for enhanced accuracy.

Displays **LONG/SHORT arrows only on the first bar** to keep your chart clean and readable.

✅ **Auto Take Profit & Stop Loss System (Auto TP/SL)**

Once a signal appears, the system automatically sets:

* **TP1 = +15 USD**

* **TP2 = +25 USD**

* **SL = -10 USD**

These levels are displayed as **dashed lines** on the chart — clear and updated in real-time.

✅ **Smart DCA System (3 Orders)**

Works for both LONG and SHORT positions:

* **Order 1:** Entry upon signal confirmation (after candle close)

* **Order 2:** Entry at 5 USD below/above Order 1

* **Order 3:** Entry at another 5 USD below/above Order 2

The system automatically **calculates the average entry price** and **adjusts the SL** to -10 USD from the average cost.

This helps **spread risk** and **increase recovery potential** when prices rebound 💰

✅ **Specially Designed for XAUUSD Trading**