Enhanced BTC Order Block IndicatorThe script you provided is an "Enhanced BTC Order Block Indicator" written in Pine Script v5 for TradingView. It is designed to identify and visually mark Order Blocks (OBs) on a Bitcoin (BTC) price chart, specifically tailored for a high-frequency scalping strategy on the 5-minute (M5) timeframe. Order Blocks are key price zones where institutional traders are likely to have placed significant buy or sell orders, making them high-probability areas for reversals or continuations. The script incorporates customizable filters, visual indicators, and alert functionality to assist traders in executing the strategy outlined earlier.

Key Features and Functionality

Purpose:

The indicator detects bullish Order Blocks (buy zones) and bearish Order Blocks (sell zones) based on a predefined percentage price movement (default 0.5–1%) and volume confirmation.

It marks these zones on the chart with colored boxes and provides alerts when an OB is detected.

User-Configurable Inputs:

Price Move Range: minMovePercent (default 0.5%) and maxMovePercent (default 1.0%) define the acceptable price movement range for identifying OBs.

Volume Threshold: volumeThreshold (default 1.5x average volume) ensures OB detection is backed by significant trading activity.

Lookback Period: lookback (default 10 candles) determines how many previous candles are analyzed to find the last candle before a strong move.

Wick/Body Option: useWick (default false) allows users to choose whether the OB zone is based on the candle’s wick or body.

Colors: bullishOBColor (default green) and bearishOBColor (default red) set the visual appearance of OB boxes.

Box Extension: boxExtension (default 100 bars) controls how far the OB box extends to the right on the chart.

RSI Filter: useRSI (default true) enables an RSI filter, with rsiLength (default 14), rsiBullishThreshold (default 50), and rsiBearishThreshold (default 50) for trend confirmation.

M15 Support/Resistance: useSR (default true) and srLookback (default 20) integrate M15 timeframe swing highs and lows for additional OB validation.

Core Logic:

Bullish OB Detection: Identifies a strong upward move (0.5–1%) with volume above the threshold. It then looks back to the last bearish candle before the move to define the OB zone. RSI > 50 and proximity to M15 support/resistance (optional) enhance confirmation.

Bearish OB Detection: Identifies a strong downward move (0.5–1%) with volume confirmation, tracing back to the last bullish candle. RSI < 50 and M15 resistance proximity (optional) add validation.

The OB zone is drawn as a rectangle from the high to low of the identified candle, extended rightward.

Visual Output:

Boxes: Uses box.new to draw OB zones, with left set to the previous bar (bar_index ), right extended by boxExtension, top and bottom defined by the OB’s high and low prices. Each box includes a text label ("Bullish OB" or "Bearish OB") and is semi-transparent.

Colors distinguish between bullish (green) and bearish (red) OBs.

Alerts:

Global alertcondition definitions trigger notifications for "Bullish OB Detected" and "Bearish OB Detected" when the respective conditions are met, displaying the current close price in the message.

Helper Functions:

f_priceChangePercent: Calculates the percentage price change between open and close prices.

isNearSR: Checks if the price is within 0.2% of M15 swing highs or lows for support/resistance confluence.

How It Works

The script runs on each candle, evaluating the current price action against the user-defined criteria.

When a bullish or bearish move is detected (meeting the percentage, volume, RSI, and S/R conditions), it identifies the preceding candle to define the OB zone.

The OB is then visualized on the chart, and an alert is triggered if configured in TradingView.

Use Case

This indicator is tailored for your BTC scalping strategy, where trades last 1–15 minutes targeting 0.3–0.5% gains. It helps traders spot institutional order zones on the M5 chart, confirmed by secondary M1 analysis, and integrates with your use of EMAs, RSI, and volume. The customizable settings allow adaptation to varying market conditions or personal preferences.

Limitations

The M15 S/R detection is simplified (using swing highs/lows), which may not always align perfectly with manual support/resistance levels.

Alerts depend on TradingView’s alert system and require manual setup.

Performance may vary with high volatility or low-volume periods, necessitating parameter adjustments.

ابحث في النصوص البرمجية عن "通达信+选股公式+换手率+0.5+源码"

Entropy Chart Analysis [PhenLabs]📊 Entropy Chart analysis -

Version: PineScript™ v6

📌 Description

The Entropy Chart indicator analysis applies Approximate Entropy (ApEn) to identify zones of potential support and resistance on your price chart. It is designed to locate changes in the market’s predictability, with a focus on zones near significant psychological price levels (e.g., multiples of 50). By quantifying entropy, the indicator aims to identify zones where price action might stabilize (potential support) or become randomized (potential resistance).

This tool automates the visualization of these key areas for traders, which may have the effect of revealing reversal levels or consolidation zones that would be hard to discern through traditional means. It also filters the signals by proximity to key levels in an attempt to reduce noise and highlight higher-probability setups. These dynamic zones adapt to changing market conditions by stretching, merging, and expiring based on user-inputted rules.

🚀 Points of Innovation

Combines Approximate Entropy (ApEn) calculation with price action near significant levels.

Filters zone signals based on proximity (in ticks) to predefined significant price levels (multiples of 50).

Dynamically merges overlapping or nearby zones to consolidate signals and reduce chart clutter.

Uses ApEn crossovers relative to its moving average as the core trigger mechanism.

Provides distinct visual coloring for bullish, bearish, and merged (mixed-signal) zones.

Offers comprehensive customization for entropy calculation, zone sensitivity, level filtering, and visual appearance.

🔧 Core Components

Approximate Entropy (ApEn) Calculation : Measures the regularity or randomness of price fluctuations over a specified window. Low ApEn suggests predictability, while high ApEn suggests randomness.

Zone Trigger Logic : Creates potential support zones when ApEn crosses below its average (indicating increasing predictability) and potential resistance zones when it crosses above (indicating increasing randomness).

Significant Level Filter : Validates zone triggers only if they occur within a user-defined tick distance from significant price levels (multiples of 50).

Dynamic Zone Management : Automatically creates, extends, merges nearby zones based on tick distance, and removes the oldest zones to maintain a maximum limit.

Zone Visualization : Draws and updates colored boxes on the chart to represent active support, resistance, or mixed zones.

🔥 Key Features

Entropy-Based S/R Detection : Uses ApEn to identify potential support (low entropy) and resistance (high entropy) areas.

Significant Level Filtering : Enhances signal quality by focusing on entropy changes near key psychological price points.

Automatic Zone Drawing & Merging : Visualizes zones dynamically, merging close signals for clearer interpretation.

Highly Customizable : Allows traders to adjust parameters for ApEn calculation, zone detection thresholds, level filter sensitivity, merging distance, and visual styles.

Integrated Alerts : Provides built-in alert conditions for the formation of new bullish or bearish zones near significant levels.

Clear Visual Output : Uses distinct, customizable colors for buy (support), sell (resistance), and mixed (merged) zones.

🎨 Visualization

Buy Zones : Represented by greenish boxes (default: #26a69a), indicating potential support areas formed during low entropy periods near significant levels.

Sell Zones : Represented by reddish boxes (default: #ef5350), indicating potential resistance areas formed during high entropy periods near significant levels.

Mixed Zones : Represented by bluish/purple boxes (default: #8894ff), formed when a buy zone and a sell zone merge, indicating areas of potential consolidation or conflict.

Dynamic Extension : Active zones are automatically extended to the right with each new bar.

📖 Usage Guidelines

Calculation Parameters

Window Length

Default: 15

Range: 10-100

Description: Lookback period for ApEn calculation. Shorter lengths are more responsive; longer lengths are smoother.

Embedding Dimension (m)

Default: 2

Range: 1-6

Description: Length of patterns compared in ApEn calculation. Higher values detect more complex patterns but require more data.

Tolerance (r)

Default: 0.5

Range: 0.1-1.0 (step 0.1)

Description: Sensitivity factor for pattern matching (as a multiple of standard deviation). Lower values require closer matches (more sensitive).

Zone Settings

Zone Lookback

Default: 5

Range: 5-50

Description: Lookback period for the moving average of ApEn used in threshold calculations.

Zone Threshold

Default: 0.5

Range: 0.5-3.0

Description: Multiplier for the ApEn average to set crossover trigger levels. Higher values require larger ApEn deviations to create zones.

Maximum Zones

Default: 5

Range: 1-10

Description: Maximum number of active zones displayed. The oldest zones are removed first when the limit is reached.

Zone Merge Distance (Ticks)

Default: 5

Range: 1-50

Description: Maximum distance in ticks for two separate zones to be merged into one.

Level Filter Settings

Tick Size

Default: 0.25

Description: The minimum price increment for the asset. Must be set correctly for the specific instrument to ensure accurate level filtering.

Max Ticks Distance from Levels

Default: 40

Description: Maximum allowed distance (in ticks) from a significant level (multiple of 50) for a zone trigger to be valid.

Visual Settings

Buy Zone Color : Default: color.new(#26a69a, 83). Sets the fill color for support zones.

Sell Zone Color : Default: color.new(#ef5350, 83). Sets the fill color for resistance zones.

Mixed Zone Color : Default: color.new(#8894ff, 83). Sets the fill color for merged zones.

Buy Border Color : Default: #26a69a. Sets the border color for support zones.

Sell Border Color : Default: #ef5350. Sets the border color for resistance zones.

Mixed Border Color : Default: color.new(#a288ff, 50). Sets the border color for mixed zones.

Border Width : Default: 1, Range: 1-3. Sets the thickness of zone borders.

✅ Best Use Cases

Identifying potential support/resistance near significant psychological price levels (e.g., $50, $100 increments).

Detecting potential market turning points or consolidation zones based on shifts in price predictability.

Filtering entries or exits by confirming signals occurring near significant levels identified by the indicator.

Adding context to other technical analysis approaches by highlighting entropy-derived zones.

⚠️ Limitations

Parameter Dependency : Indicator performance is sensitive to parameter settings ( Window Length , Tolerance , Zone Threshold , Max Ticks Distance ), which may need optimization for different assets and timeframes.

Volatility Sensitivity : High market volatility or erratic price action can affect ApEn calculations and potentially lead to less reliable zone signals.

Fixed Level Filter : The significant level filter is based on multiples of 50. While common, this may not capture all relevant levels for every asset or market condition. Accurate Tick Size input is essential.

Not Standalone : Should be used in conjunction with other analysis methods (price action, volume, other indicators) for confirmation, not as a sole basis for trading decisions.

💡 What Makes This Unique

Entropy + Level Context : Uniquely combines ApEn analysis with a specific filter for proximity to significant price levels (multiples of 50), adding locational context to entropy signals.

Intelligent Zone Merging : Automatically consolidates nearby buy/sell zones based on tick distance, simplifying visual analysis and highlighting stronger confluence areas.

Targeted Signal Generation : Focuses alerts and zone creation on specific market conditions (entropy shifts near key levels).

🔬 How It Works

Calculate Entropy : The script computes the Approximate Entropy (ApEn) of the closing prices over the defined Window Length to quantify price predictability.

Check Triggers : It monitors ApEn relative to its moving average. A crossunder below a calculated threshold (avg_apen / zone_threshold) indicates potential support; a crossover above (avg_apen * zone_threshold) indicates potential resistance.

Filter by Level : A potential zone trigger is confirmed only if the low (for support) or high (for resistance) of the trigger bar is within the Max Ticks Distance of a significant price level (multiple of 50).

Manage & Draw Zones : If a trigger is confirmed, a new zone box is created. The script checks for overlaps with existing zones within the Zone Merge Distance and merges them if necessary. Zones are extended forward, and the oldest are removed to respect the Maximum Zones limit. Active zones are drawn and updated on the chart.

💡 Note:

Crucially, set the Tick Size parameter correctly for your specific trading instrument in the “Level Filter Settings”. Incorrect Tick Size will make the significant level filter inaccurate.

Experiment with parameters, especially Window Length , Tolerance (r) , Zone Threshold , and Max Ticks Distance , to tailor the indicator’s sensitivity to your preferred asset and timeframe.

Always use this indicator as part of a comprehensive trading plan, incorporating risk management and seeking confirmation from other analysis techniques.

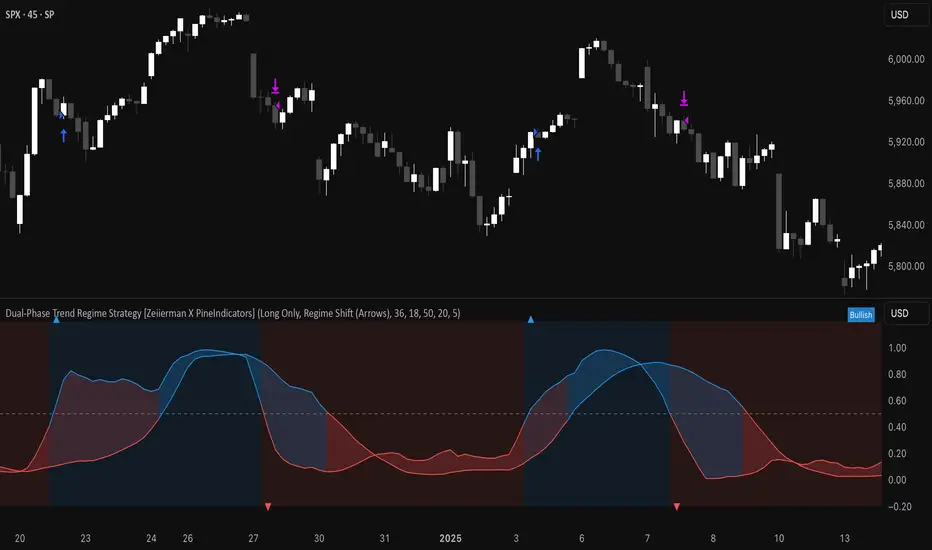

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

Dskyz (DAFE) Adaptive Regime - Quant Machine ProDskyz (DAFE) Adaptive Regime - Quant Machine Pro:

Buckle up for the Dskyz (DAFE) Adaptive Regime - Quant Machine Pro, is a strategy that’s your ultimate edge for conquering futures markets like ES, MES, NQ, and MNQ. This isn’t just another script—it’s a quant-grade powerhouse, crafted with precision to adapt to market regimes, deliver multi-factor signals, and protect your capital with futures-tuned risk management. With its shimmering DAFE visuals, dual dashboards, and glowing watermark, it turns your charts into a cyberpunk command center, making trading as thrilling as it is profitable.

Unlike generic scripts clogging up the space, the Adaptive Regime is a DAFE original, built from the ground up to tackle the chaos of futures trading. It identifies market regimes (Trending, Range, Volatile, Quiet) using ADX, Bollinger Bands, and HTF indicators, then fires trades based on a weighted scoring system that blends candlestick patterns, RSI, MACD, and more. Add in dynamic stops, trailing exits, and a 5% drawdown circuit breaker, and you’ve got a system that’s as safe as it is aggressive. Whether you’re a newbie or a prop desk pro, this strat’s your ticket to outsmarting the markets. Let’s break down every detail and see why it’s a must-have.

Why Traders Need This Strategy

Futures markets are a gauntlet—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional traps that punish the unprepared. Meanwhile, platforms are flooded with low-effort scripts that recycle old ideas with zero innovation. The Adaptive Regime stands tall, offering:

Adaptive Intelligence: Detects market regimes (Trending, Range, Volatile, Quiet) to optimize signals, unlike one-size-fits-all scripts.

Multi-Factor Precision: Combines candlestick patterns, MA trends, RSI, MACD, volume, and HTF confirmation for high-probability trades.

Futures-Optimized Risk: Calculates position sizes based on $ risk (default: $300), with ATR or fixed stops/TPs tailored for ES/MES.

Bulletproof Safety: 5% daily drawdown circuit breaker and trailing stops keep your account intact, even in chaos.

DAFE Visual Mastery: Pulsing Bollinger Band fills, dynamic SL/TP lines, and dual dashboards (metrics + position) make signals crystal-clear and charts a work of art.

Original Craftsmanship: A DAFE creation, built with community passion, not a rehashed clone of generic code.

Traders need this because it’s a complete, adaptive system that blends quant smarts, user-friendly design, and DAFE flair. It’s your edge to trade with confidence, cut through market noise, and leave the copycats in the dust.

Strategy Components

1. Market Regime Detection

The strategy’s brain is its ability to classify market conditions into five regimes, ensuring signals match the environment.

How It Works:

Trending (Regime 1): ADX > 20, fast/slow EMA spread > 0.3x ATR, HTF RSI > 50 or MACD bullish (htf_trend_bull/bear).

Range (Regime 2): ADX < 25, price range < 3% of close, no HTF trend.

Volatile (Regime 3): BB width > 1.5x avg, ATR > 1.2x avg, HTF RSI overbought/oversold.

Quiet (Regime 4): BB width < 0.8x avg, ATR < 0.9x avg.

Other (Regime 5): Default for unclear conditions.

Indicators: ADX (14), BB width (20), ATR (14, 50-bar SMA), HTF RSI (14, daily default), HTF MACD (12,26,9).

Why It’s Brilliant:

Regime detection adapts signals to market context, boosting win rates in trending or volatile conditions.

HTF RSI/MACD add a big-picture filter, rare in basic scripts.

Visualized via gradient background (green for Trending, orange for Range, red for Volatile, gray for Quiet, navy for Other).

2. Multi-Factor Signal Scoring

Entries are driven by a weighted scoring system that combines candlestick patterns, trend, momentum, and volume for robust signals.

Candlestick Patterns:

Bullish: Engulfing (0.5), hammer (0.4 in Range, 0.2 else), morning star (0.2), piercing (0.2), double bottom (0.3 in Volatile, 0.15 else). Must be near support (low ≤ 1.01x 20-bar low) with volume spike (>1.5x 20-bar avg).

Bearish: Engulfing (0.5), shooting star (0.4 in Range, 0.2 else), evening star (0.2), dark cloud (0.2), double top (0.3 in Volatile, 0.15 else). Must be near resistance (high ≥ 0.99x 20-bar high) with volume spike.

Logic: Patterns are weighted higher in specific regimes (e.g., hammer in Range, double bottom in Volatile).

Additional Factors:

Trend: Fast EMA (20) > slow EMA (50) + 0.5x ATR (trend_bull, +0.2); opposite for trend_bear.

RSI: RSI (14) < 30 (rsi_bull, +0.15); > 70 (rsi_bear, +0.15).

MACD: MACD line > signal (12,26,9, macd_bull, +0.15); opposite for macd_bear.

Volume: ATR > 1.2x 50-bar avg (vol_expansion, +0.1).

HTF Confirmation: HTF RSI < 70 and MACD bullish (htf_bull_confirm, +0.2); RSI > 30 and MACD bearish (htf_bear_confirm, +0.2).

Scoring:

bull_score = sum of bullish factors; bear_score = sum of bearish. Entry requires score ≥ 1.0.

Example: Bullish engulfing (0.5) + trend_bull (0.2) + rsi_bull (0.15) + htf_bull_confirm (0.2) = 1.05, triggers long.

Why It’s Brilliant:

Multi-factor scoring ensures signals are confirmed by multiple market dynamics, reducing false positives.

Regime-specific weights make patterns more relevant (e.g., hammers shine in Range markets).

HTF confirmation aligns with the big picture, a quant edge over simplistic scripts.

3. Futures-Tuned Risk Management

The risk system is built for futures, calculating position sizes based on $ risk and offering flexible stops/TPs.

Position Sizing:

Logic: Risk per trade (default: $300) ÷ (stop distance in points * point value) = contracts, capped at max_contracts (default: 5). Point value = tick value (e.g., $12.5 for ES) * ticks per point (4) * contract multiplier (1 for ES, 0.1 for MES).

Example: $300 risk, 8-point stop, ES ($50/point) → 0.75 contracts, rounded to 1.

Impact: Precise sizing prevents over-leverage, critical for micro contracts like MES.

Stops and Take-Profits:

Fixed: Default stop = 8 points, TP = 16 points (2:1 reward/risk).

ATR-Based: Stop = 1.5x ATR (default), TP = 3x ATR, enabled via use_atr_for_stops.

Logic: Stops set at swing low/high ± stop distance; TPs at 2x stop distance from entry.

Impact: ATR stops adapt to volatility, while fixed stops suit stable markets.

Trailing Stops:

Logic: Activates at 50% of TP distance. Trails at close ± 1.5x ATR (atr_multiplier). Longs: max(trail_stop_long, close - ATR * 1.5); shorts: min(trail_stop_short, close + ATR * 1.5).

Impact: Locks in profits during trends, a game-changer in volatile sessions.

Circuit Breaker:

Logic: Pauses trading if daily drawdown > 5% (daily_drawdown = (max_equity - equity) / max_equity).

Impact: Protects capital during black swan events (e.g., April 27, 2025 ES slippage).

Why It’s Brilliant:

Futures-specific inputs (tick value, multiplier) make it plug-and-play for ES/MES.

Trailing stops and circuit breaker add pro-level safety, rare in off-the-shelf scripts.

Flexible stops (ATR or fixed) suit different trading styles.

4. Trade Entry and Exit Logic

Entries and exits are precise, driven by bull_score/bear_score and protected by drawdown checks.

Entry Conditions:

Long: bull_score ≥ 1.0, no position (position_size <= 0), drawdown < 5% (not pause_trading). Calculates contracts, sets stop at swing low - stop points, TP at 2x stop distance.

Short: bear_score ≥ 1.0, position_size >= 0, drawdown < 5%. Stop at swing high + stop points, TP at 2x stop distance.

Logic: Tracks entry_regime for PNL arrays. Closes opposite positions before entering.

Exit Conditions:

Stop-Loss/Take-Profit: Hits stop or TP (strategy.exit).

Trailing Stop: Activates at 50% TP, trails by ATR * 1.5.

Emergency Exit: Closes if price breaches stop (close < long_stop_price or close > short_stop_price).

Reset: Clears stop/TP prices when flat (position_size = 0).

Why It’s Brilliant:

Score-based entries ensure multi-factor confirmation, filtering out weak signals.

Trailing stops maximize profits in trends, unlike static exits in basic scripts.

Emergency exits add an extra safety layer, critical for futures volatility.

5. DAFE Visuals

The visuals are pure DAFE magic, blending function with cyberpunk flair to make signals intuitive and charts stunning.

Shimmering Bollinger Band Fill:

Display: BB basis (20, white), upper/lower (green/red, 45% transparent). Fill pulses (30–50 alpha) by regime, with glow (60–95 alpha) near bands (close ≥ 0.995x upper or ≤ 1.005x lower).

Purpose: Highlights volatility and key levels with a futuristic glow.

Visuals make complex regimes and signals instantly clear, even for newbies.

Pulsing effects and regime-specific colors add a DAFE signature, setting it apart from generic scripts.

BB glow emphasizes tradeable levels, enhancing decision-making.

Chart Background (Regime Heatmap):

Green — Trending Market: Strong, sustained price movement in one direction. The market is in a trend phase—momentum follows through.

Orange — Range-Bound: Market is consolidating or moving sideways, with no clear up/down trend. Great for mean reversion setups.

Red — Volatile Regime: High volatility, heightened risk, and larger/faster price swings—trade with caution.

Gray — Quiet/Low Volatility: Market is calm and inactive, with small moves—often poor conditions for most strategies.

Navy — Other/Neutral: Regime is uncertain or mixed; signals may be less reliable.

Bollinger Bands Glow (Dynamic Fill):

Neon Red Glow — Warning!: Price is near or breaking above the upper band; momentum is overstretched, watch for overbought conditions or reversals.

Bright Green Glow — Opportunity!: Price is near or breaking below the lower band; market could be oversold, prime for bounce or reversal.

Trend Green Fill — Trending Regime: Fills between bands with green when the market is trending, showing clear momentum.

Gold/Yellow Fill — Range Regime: Fills with gold/aqua in range conditions, showing the market is sideways/oscillating.

Magenta/Red Fill — Volatility Spike: Fills with vivid magenta/red during highly volatile regimes.

Blue Fill — Neutral/Quiet: A soft blue glow for other or uncertain market states.

Moving Averages:

Display: Blue fast EMA (20), red slow EMA (50), 2px.

Purpose: Shows trend direction, with trend_dir requiring ATR-scaled spread.

Dynamic SL/TP Lines:

Display: Pulsing colors (red SL, green TP for Trending; yellow/orange for Range, etc.), 3px, with pulse_alpha for shimmer.

Purpose: Tracks stops/TPs in real-time, color-coded by regime.

6. Dual Dashboards

Two dashboards deliver real-time insights, making the strat a quant command center.

Bottom-Left Metrics Dashboard (2x13):

Metrics: Mode (Active/Paused), trend (Bullish/Bearish/Neutral), ATR, ATR avg, volume spike (YES/NO), RSI (value + Oversold/Overbought/Neutral), HTF RSI, HTF trend, last signal (Buy/Sell/None), regime, bull score.

Display: Black (29% transparent), purple title, color-coded (green for bullish, red for bearish).

Purpose: Consolidates market context and signal strength.

Top-Right Position Dashboard (2x7):

Metrics: Regime, position side (Long/Short/None), position PNL ($), SL, TP, daily PNL ($).

Display: Black (29% transparent), purple title, color-coded (lime for Long, red for Short).

Purpose: Tracks live trades and profitability.

Why It’s Brilliant:

Dual dashboards cover market context and trade status, a rare feature.

Color-coding and concise metrics guide beginners (e.g., green “Buy” = go).

Real-time PNL and SL/TP visibility empower disciplined trading.

7. Performance Tracking

Logic: Arrays (regime_pnl_long/short, regime_win/loss_long/short) track PNL and win/loss by regime (1–5). Updated on trade close (barstate.isconfirmed).

Purpose: Prepares for future adaptive thresholds (e.g., adjust bull_score min based on regime performance).

Why It’s Brilliant: Lays the groundwork for self-optimizing logic, a quant edge over static scripts.

Key Features

Regime-Adaptive: Optimizes signals for Trending, Range, Volatile, Quiet markets.

Futures-Optimized: Precise sizing for ES/MES with tick-based risk inputs.

Multi-Factor Signals: Candlestick patterns, RSI, MACD, and HTF confirmation for robust entries.

Dynamic Exits: ATR/fixed stops, 2:1 TPs, and trailing stops maximize profits.

Safe and Smart: 5% drawdown breaker and emergency exits protect capital.

DAFE Visuals: Shimmering BB fill, pulsing SL/TP, and dual dashboards.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

How to Use

Add to Chart: Load on a 5min ES/MES chart in TradingView.

Configure Inputs: Set instrument (ES/MES), tick value ($12.5/$1.25), multiplier (1/0.1), risk ($300 default). Enable ATR stops for volatility.

Monitor Dashboards: Bottom-left for regime/signals, top-right for position/PNL.

Backtest: Run in strategy tester to compare regimes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see regime shifts and stops.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance does not guarantee future results. Backtest results may differ from live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Slippage: 3

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Adaptive Regime - Quant Machine Pro is more than a strategy—it’s a revolution. Crafted with DAFE’s signature precision, it rises above generic scripts with adaptive regimes, quant-grade signals, and visuals that make trading a thrill. Whether you’re scalping MES or swinging ES, this system empowers you to navigate markets with confidence and style. Join the DAFE crew, light up your charts, and let’s dominate the futures game!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

[blackcat] L3 Breakout IndicatorOVERVIEW

This script provides a breakout detection system ( L3 Breakout Indicator) analyzing price momentum across timeframes. It identifies market entry/exit zones through dynamically scaled thresholds and visual feedback layers.

FEATURES

Dual momentum visualization: • Price Momentum Ratio Plot ( yellow ) • Filtered Signal Value Plot ( fuchsia )

Adjustable trade boundaries: ▪ Lower Threshold (default: 0.5) ▪ Upper Threshold (default: 2.9) ▪ Central boundary ( fixed at 2.0 )

Real-time visual feedback: ☀ Buy zone highlights ( lime ) on momentum crossover ⚠ Sell zone highlights ( red ) on momentum cross-under ♦ Dynamic convergence area between plots ( colored gradient )

HOW TO USE

Interpretation Flow

Monitor momentum plots relative to threshold lines

Actionable signals occur when momentum crosses thresholds

Persistent movement above/below central boundary indicates trend continuation

Key Zones

• Below 0.5: Potential buying opportunity zone

• Above 2.0: Cautionary selling region

• Between 0.5-2.0: Neutral consolidation phase

Optimization Tips

Adjust thresholds based on asset volatility

Combine with volume metrics for confirmation

Backtest parameters using historical data

LIMITATIONS

• Lag induced by 4-period EMA smoothing

• Historical dependency in calculating extremes (lowest(100)/highest(250))

• No built-in risk management protocols (stop loss take profit)

• Performance variability during sideways markets

Fuzzy SMA Trend Analyzer (experimental)[FibonacciFlux]Fuzzy SMA Trend Analyzer (Normalized): Advanced Market Trend Detection Using Fuzzy Logic Theory

Elevate your technical analysis with institutional-grade fuzzy logic implementation

Research Genesis & Conceptual Framework

This indicator represents the culmination of extensive research into applying fuzzy logic theory to financial markets. While traditional technical indicators often produce binary outcomes, market conditions exist on a continuous spectrum. The Fuzzy SMA Trend Analyzer addresses this limitation by implementing a sophisticated fuzzy logic system that captures the nuanced, multi-dimensional nature of market trends.

Core Fuzzy Logic Principles

At the heart of this indicator lies fuzzy logic theory - a mathematical framework designed to handle imprecision and uncertainty:

// Improved fuzzy_triangle function with guard clauses for NA and invalid parameters.

fuzzy_triangle(val, left, center, right) =>

if na(val) or na(left) or na(center) or na(right) or left > center or center > right // Guard checks

0.0

else if left == center and center == right // Crisp set (single point)

val == center ? 1.0 : 0.0

else if left == center // Left-shoulder shape (ramp down from 1 at center to 0 at right)

val >= right ? 0.0 : val <= center ? 1.0 : (right - val) / (right - center)

else if center == right // Right-shoulder shape (ramp up from 0 at left to 1 at center)

val <= left ? 0.0 : val >= center ? 1.0 : (val - left) / (center - left)

else // Standard triangle

math.max(0.0, math.min((val - left) / (center - left), (right - val) / (right - center)))

This implementation of triangular membership functions enables the indicator to transform crisp numerical values into degrees of membership in linguistic variables like "Large Positive" or "Small Negative," creating a more nuanced representation of market conditions.

Dynamic Percentile Normalization

A critical innovation in this indicator is the implementation of percentile-based normalization for SMA deviation:

// ----- Deviation Scale Estimation using Percentile -----

// Calculate the percentile rank of the *absolute* deviation over the lookback period.

// This gives an estimate of the 'typical maximum' deviation magnitude recently.

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

// ----- Normalize the Raw Deviation -----

// Divide the raw deviation by the estimated 'typical max' magnitude.

normalized_diff = raw_diff / diff_abs_percentile

// ----- Clamp the Normalized Deviation -----

normalized_diff_clamped = math.max(-3.0, math.min(3.0, normalized_diff))

This percentile normalization approach creates a self-adapting system that automatically calibrates to different assets and market regimes. Rather than using fixed thresholds, the indicator dynamically adjusts based on recent volatility patterns, significantly enhancing signal quality across diverse market environments.

Multi-Factor Fuzzy Rule System

The indicator implements a comprehensive fuzzy rule system that evaluates multiple technical factors:

SMA Deviation (Normalized): Measures price displacement from the Simple Moving Average

Rate of Change (ROC): Captures price momentum over a specified period

Relative Strength Index (RSI): Assesses overbought/oversold conditions

These factors are processed through a sophisticated fuzzy inference system with linguistic variables:

// ----- 3.1 Fuzzy Sets for Normalized Deviation -----

diffN_LP := fuzzy_triangle(normalized_diff_clamped, 0.7, 1.5, 3.0) // Large Positive (around/above percentile)

diffN_SP := fuzzy_triangle(normalized_diff_clamped, 0.1, 0.5, 0.9) // Small Positive

diffN_NZ := fuzzy_triangle(normalized_diff_clamped, -0.2, 0.0, 0.2) // Near Zero

diffN_SN := fuzzy_triangle(normalized_diff_clamped, -0.9, -0.5, -0.1) // Small Negative

diffN_LN := fuzzy_triangle(normalized_diff_clamped, -3.0, -1.5, -0.7) // Large Negative (around/below percentile)

// ----- 3.2 Fuzzy Sets for ROC -----

roc_HN := fuzzy_triangle(roc_val, -8.0, -5.0, -2.0)

roc_WN := fuzzy_triangle(roc_val, -3.0, -1.0, -0.1)

roc_NZ := fuzzy_triangle(roc_val, -0.3, 0.0, 0.3)

roc_WP := fuzzy_triangle(roc_val, 0.1, 1.0, 3.0)

roc_HP := fuzzy_triangle(roc_val, 2.0, 5.0, 8.0)

// ----- 3.3 Fuzzy Sets for RSI -----

rsi_L := fuzzy_triangle(rsi_val, 0.0, 25.0, 40.0)

rsi_M := fuzzy_triangle(rsi_val, 35.0, 50.0, 65.0)

rsi_H := fuzzy_triangle(rsi_val, 60.0, 75.0, 100.0)

Advanced Fuzzy Inference Rules

The indicator employs a comprehensive set of fuzzy rules that encode expert knowledge about market behavior:

// --- Fuzzy Rules using Normalized Deviation (diffN_*) ---

cond1 = math.min(diffN_LP, roc_HP, math.max(rsi_M, rsi_H)) // Strong Bullish: Large pos dev, strong pos roc, rsi ok

strength_SB := math.max(strength_SB, cond1)

cond2 = math.min(diffN_SP, roc_WP, rsi_M) // Weak Bullish: Small pos dev, weak pos roc, rsi mid

strength_WB := math.max(strength_WB, cond2)

cond3 = math.min(diffN_SP, roc_NZ, rsi_H) // Weakening Bullish: Small pos dev, flat roc, rsi high

strength_N := math.max(strength_N, cond3 * 0.6) // More neutral

strength_WB := math.max(strength_WB, cond3 * 0.2) // Less weak bullish

This rule system evaluates multiple conditions simultaneously, weighting them by their degree of membership to produce a comprehensive trend assessment. The rules are designed to identify various market conditions including strong trends, weakening trends, potential reversals, and neutral consolidations.

Defuzzification Process

The final step transforms the fuzzy result back into a crisp numerical value representing the overall trend strength:

// --- Step 6: Defuzzification ---

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10 // Use small epsilon instead of != 0.0 for float comparison

fuzzyTrendScore := (strength_SB * STRONG_BULL +

strength_WB * WEAK_BULL +

strength_N * NEUTRAL +

strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1 (strong bearish) to +1 (strong bullish), providing a smooth, continuous evaluation of market conditions that avoids the abrupt signal changes common in traditional indicators.

Advanced Visualization with Rainbow Gradient

The indicator incorporates sophisticated visualization using a rainbow gradient coloring system:

// Normalize score to for gradient function

normalizedScore = na(fuzzyTrendScore) ? 0.5 : math.max(0.0, math.min(1.0, (fuzzyTrendScore + 1) / 2))

// Get the color based on gradient setting and normalized score

final_color = get_gradient(normalizedScore, gradient_type)

This color-coding system provides intuitive visual feedback, with color intensity reflecting trend strength and direction. The gradient can be customized between Red-to-Green or Red-to-Blue configurations based on user preference.

Practical Applications

The Fuzzy SMA Trend Analyzer excels in several key applications:

Trend Identification: Precisely identifies market trend direction and strength with nuanced gradation

Market Regime Detection: Distinguishes between trending markets and consolidation phases

Divergence Analysis: Highlights potential reversals when price action and fuzzy trend score diverge

Filter for Trading Systems: Provides high-quality trend filtering for other trading strategies

Risk Management: Offers early warning of potential trend weakening or reversal

Parameter Customization

The indicator offers extensive customization options:

SMA Length: Adjusts the baseline moving average period

ROC Length: Controls momentum sensitivity

RSI Length: Configures overbought/oversold sensitivity

Normalization Lookback: Determines the adaptive calculation window for percentile normalization

Percentile Rank: Sets the statistical threshold for deviation normalization

Gradient Type: Selects the preferred color scheme for visualization

These parameters enable fine-tuning to specific market conditions, trading styles, and timeframes.

Acknowledgments

The rainbow gradient visualization component draws inspiration from LuxAlgo's "Rainbow Adaptive RSI" (used under CC BY-NC-SA 4.0 license). This implementation of fuzzy logic in technical analysis builds upon Fermi estimation principles to overcome the inherent limitations of crisp binary indicators.

This indicator is shared under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Remember that past performance does not guarantee future results. Always conduct thorough testing before implementing any technical indicator in live trading.

Low Liquidity Zones [PhenLabs]📊 Low Liquidity Zones

Version: PineScript™ v6

📌 Description

Low Liquidity Zones identifies and highlights periods of unusually low trading volume on your chart, marking areas where price movement occurred with minimal participation. These zones often represent potential support and resistance levels that may be more susceptible to price breakouts or reversals when revisited with higher volume.

Unlike traditional volume analysis tools that focus on high volume spikes, this indicator specializes in detecting low liquidity areas where price moved with minimal resistance. Each zone displays its volume delta, providing insight into buying vs. selling pressure during these thin liquidity periods. This combination of low volume detection and delta analysis helps traders identify potential price inefficiencies and weak structures in the market.

🚀 Points of Innovation

• Identifies low liquidity zones that most volume indicators overlook but which often become significant technical levels

• Displays volume delta within each zone, showing net buying/selling pressure during low liquidity periods

• Dynamically adjusts to different timeframes, allowing analysis across multiple time horizons

• Filters zones by maximum size percentage to focus only on precise price levels

• Maintains historical zones until they expire based on your lookback settings, creating a cumulative map of potential support/resistance areas

🔧 Core Components

• Low Volume Detection: Identifies candles where volume falls below a specified threshold relative to recent average volume, highlighting potential liquidity gaps.

• Volume Delta Analysis: Calculates and displays the net buying/selling pressure within each low liquidity zone, providing insight into the directional bias during low participation periods.

• Dynamic Timeframe Adjustment: Automatically scales analysis periods to match your selected timeframe preference, ensuring consistent identification of low liquidity zones regardless of chart settings.

• Zone Management System: Creates, tracks, and expires low liquidity zones based on your configured settings, maintaining visual clarity on the chart.

🔥 Key Features

• Low Volume Identification: Automatically detects and highlights candles where volume falls below your specified threshold compared to the moving average.

• Volume Delta Visualization: Shows the net volume delta within each zone, providing insight into whether buyers or sellers were dominant despite the low overall volume.

• Flexible Timeframe Analysis: Analyze low liquidity zones across multiple predefined timeframes or use a custom lookback period specific to your trading style.

• Zone Size Filtering: Filters out excessively large zones to focus only on precise price levels, improving signal quality.

• Automatic Zone Expiration: Older zones are automatically removed after your specified lookback period to maintain a clean, relevant chart display.

🎨 Visualization

• Volume Delta Labels: Each zone displays its volume delta with “+” or “-” prefix and K/M suffix for easy interpretation, showing the strength and direction of pressure during the low volume period.

• Persistent Historical Mapping: Zones remain visible for your specified lookback period, creating a cumulative map of potential support and resistance levels forming under low liquidity conditions.

📖 Usage Guidelines

Analysis Timeframe

Default: 1D

Range/Options: 15M, 1HR, 3HR, 4HR, 8HR, 16HR, 1D, 3D, 5D, 1W, Custom

Description: Determines the historical period to analyze for low liquidity zones. Shorter timeframes provide more recent data while longer timeframes offer a more comprehensive view of significant zones. Use Custom option with the setting below for precise control.

Custom Period (Bars)

Default: 1000

Range: 1+

Description: Number of bars to analyze when using Custom timeframe option. Higher values show more historical zones but may impact performance.

Volume Analysis

Volume Threshold Divisor

Default: 0.5

Range: 0.1-1.0

Description: Maximum volume relative to average to identify low volume zones. Example: 0.5 means volume must be below 50% of the average to qualify as low volume. Lower values create more selective zones while higher values identify more zones.

Volume MA Length

Default: 15

Range: 1+

Description: Period length for volume moving average calculation. Shorter periods make the indicator more responsive to recent volume changes, while longer periods provide a more stable baseline.

Zone Settings

Zone Fill Color

Default: #2196F3 (80% transparency)

Description: Color and transparency of the low liquidity zones. Choose colors that stand out against your chart background without obscuring price action.

Maximum Zone Size %

Default: 0.5

Range: 0.1+

Description: Maximum allowed height of a zone as percentage of price. Larger zones are filtered out. Lower values create more precise zones focusing on tight price ranges.

Display Options

Show Volume Delta

Default: true

Description: Toggles the display of volume delta within each zone. Enabling this provides additional insight into buying vs. selling pressure during low volume periods.

Delta Text Position

Default: Right

Options: Left, Center, Right

Description: Controls the horizontal alignment of the delta text within zones. Adjust based on your chart layout for optimal readability.

✅ Best Use Cases

• Identifying potential support and resistance levels that formed during periods of thin liquidity

• Spotting price inefficiencies where larger players may have moved price with minimal volume

• Finding low-volume consolidation areas that may serve as breakout or reversal zones when revisited

• Locating potential stop-hunting zones where price moved on minimal participation

• Complementing traditional support/resistance analysis with volume context

⚠️ Limitations

• Requires volume data to function; will not work on symbols where the data provider doesn’t supply volume information

• Low volume zones don’t guarantee future support/resistance - they simply highlight potential areas of interest

• Works best on liquid instruments where volume data has meaningful fluctuations

• Historical analysis is limited by the maximum allowed box count (500) in TradingView

• Volume delta in some markets may not perfectly reflect buying vs. selling pressure due to data limitations

💡 What Makes This Unique

• Focus on Low Volume: Unlike some indicators that highlight high volume events particularly like our very own TLZ indicator, this tool specifically identifies potentially significant price zones that formed with minimal participation.

• Delta + Low Volume Integration: Combines volume delta analysis with low volume detection to reveal directional bias during thin liquidity periods.

• Flexible Lookback System: The dynamic timeframe system allows analysis across any timeframe while maintaining consistent zone identification criteria.

• Support/Resistance Zone Generation: Automatically builds a visual map of potential technical levels based on volume behavior rather than just price patterns.

🔬 How It Works

1. Volume Baseline Calculation:

The indicator calculates a moving average of volume over your specified period to establish a baseline for normal market participation. This adaptive baseline accounts for natural volume fluctuations across different market conditions.

2. Low Volume Detection:

Each candle’s volume is compared to the moving average and flagged when it falls below your threshold divisor. The indicator also filters zones by maximum size to ensure only precise price levels are highlighted.

3. Volume Delta Integration:

For each identified low volume candle, the indicator retrieves the volume delta from a lower timeframe. This delta value is formatted with appropriate scaling (K/M) and displayed within the zone.

4. Zone Management:

New zones are created and tracked in a dynamic array, with each zone extending rightward until it expires. The system automatically removes expired zones based on your lookback period to maintain a clean chart.

💡 Note:

Low liquidity zones often represent areas where price moved with minimal participation, which can indicate potential market inefficiencies. These zones frequently become important support/resistance levels when revisited, especially if approached with higher volume. Consider using this indicator alongside traditional technical analysis tools for comprehensive market context. For best results, experiment with different volume threshold settings based on the specific instrument’s typical volume patterns.

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

Uptrick: Fisher Eclipse1. Name and Purpose

Uptrick: Fisher Eclipse is a Pine version 6 extension of the basic Fisher Transform indicator that focuses on highlighting potential turning points in price data. Its purpose is to allow traders to spot shifts in momentum, detect divergence, and adapt signals to different market environments. By combining a core Fisher Transform with additional signal processing, divergence detection, and customizable aggressiveness settings, this script aims to help users see when a price move might be losing momentum or gaining strength.

2. Overview

This script uses a Fisher Transform calculation on the average of each bar’s high and low (hl2). The Fisher Transform is designed to amplify price extremes by mapping data into a different scale, making potential reversals more visible than they might be with standard oscillators. Uptrick: Fisher Eclipse takes this concept further by integrating a signal line, divergence detection, bar coloring for momentum intensity, and optional thresholds to reduce unwanted noise.

3. Why Use the Fisher Transform

The Fisher Transform is known for converting relatively smoothed price data into a more pronounced scale. This transformation highlights where markets may be overextended. In many cases, standard oscillators move gently, and traders can miss subtle hints that a reversal might be approaching. The Fisher Transform’s mathematical approach tightens the range of values and sharpens the highs and lows. This behavior can allow traders to see clearer peaks and troughs in momentum. Because it is often quite responsive, it can help anticipate areas where price might change direction, especially when compared to simpler moving averages or traditional oscillators. The result is a more evident signal of possible overbought or oversold conditions.

4. How This Extension Improves on the Basic Fisher Transform

Uptrick: Fisher Eclipse adds multiple features to the classic Fisher framework in order to address different trading styles and market behaviors:

a) Divergence Detection

The script can detect bullish or bearish divergences between price and the oscillator over a chosen lookback period, helping traders anticipate shifts in market direction.

b) Bar Coloring

When momentum exceeds a certain threshold (default 3), bars can be colored to highlight surges of buying or selling pressure. This quick visual reference can assist in spotting periods of heightened activity. After a bar color like this, usually, there is a quick correction as seen in the image below.

c) Signal Aggressiveness Levels

Users can choose between conservative, moderate, or aggressive signal thresholds. This allows them to tune how quickly the indicator flags potential entries or exits. Aggressive settings might suit scalpers who need rapid signals, while conservative settings may benefit swing traders preferring fewer, more robust indications.

d) Minimum Movement Filter

A configurable filter can be set to ensure that the Fisher line and its signal have a sufficient gap before triggering a buy or sell signal. This step is useful for traders seeking to minimize signals during choppy or sideways markets. This can be used to eliminate noise as well.

By combining all these elements into one package, the indicator attempts to offer a comprehensive toolkit for those who appreciate the Fisher Transform’s clarity but also desire more versatility.

5. Core Components

a) Fisher Transform

The script calculates a Fisher value using normalized price over a configurable length, highlighting potential peaks and troughs.

b) Signal Line

The Fisher line is smoothed using a short Simple Moving Average. Crossovers and crossunders are one of the key ways this indicator attempts to confirm momentum shifts.

c) Divergence Logic

The script looks back over a set number of bars to compare current highs and lows of both price and the Fisher oscillator. When price and the oscillator move in opposing directions, a divergence may occur, suggesting a possible upcoming reversal or weakening trend.

d) Thresholds for Overbought and Oversold

Horizontal lines are drawn at user-chosen overbought and oversold levels. These lines help traders see when momentum readings reach particular extremes, which can be especially relevant when combined with crossovers in that region.

e) Intensity Filter and Bar Coloring

If the magnitude of the change in the Fisher Transform meets or exceeds a specified threshold, bars are recolored. This provides a visual cue for significant momentum changes.

6. User Inputs

a) length

Defines how many bars the script looks back to compute the highest high and lowest low for the Fisher Transform. A smaller length reacts more quickly but can be noisier, while a larger length smooths out the indicator at the cost of responsiveness.

b) signal aggressiveness

Adjusts the buy and sell thresholds for conservative, moderate, and aggressive trading styles. This can be key in matching the indicator to personal risk preferences or varying market conditions. Conservative will give you less signals and aggressive will give you more signals.

c) minimum movement filter

Specifies how far apart the Fisher line and its signal line must be before generating a valid crossover signal.

d) divergence lookback

Controls how many bars are examined when determining if price and the oscillator are diverging. A larger setting might generate fewer signals, while a smaller one can provide more frequent alerts.

e) intensity threshold

Determines how large a change in the Fisher value must be for the indicator to recolor bars. Strong momentum surges become more noticeable.

f) overbought level and oversold level

Lets users define where they consider market conditions to be stretched on the upside or downside.

7. Calculation Process

a) Price Input

The script uses the midpoint of each bar’s high and low, sometimes referred to as hl2.

hl2 = (high + low) / 2

b) Range Normalization

Determine the maximum (maxHigh) and minimum (minLow) values over a user-defined lookback period (length).

Scale the hl2 value so it roughly fits between -1 and +1:

value = 2 * ((hl2 - minLow) / (maxHigh - minLow) - 0.5)

This step highlights the bar’s current position relative to its recent highs and lows.

c) Fisher Calculation

Convert the normalized value into the Fisher Transform:

fisher = 0.5 * ln( (1 + value) / (1 - value) ) + 0.5 * fisher_previous

fisher_previous is simply the Fisher value from the previous bar. Averaging half of the new transform with half of the old value smooths the result slightly and can prevent erratic jumps.

ln is the natural logarithm function, which compresses or expands values so that market turns often become more obvious.

d) Signal Smoothing

Once the Fisher value is computed, a short Simple Moving Average (SMA) is applied to produce a signal line. In code form, this often looks like:

signal = sma(fisher, 3)

Crossovers of the fisher line versus the signal line can be used to hint at changes in momentum:

• A crossover occurs when fisher moves from below to above the signal.

• A crossunder occurs when fisher moves from above to below the signal.

e) Threshold Checking

Users typically define oversold and overbought levels (often -1 and +1).

Depending on aggressiveness settings (conservative, moderate, aggressive), these thresholds are slightly shifted to filter out or include more signals.

For example, an oversold threshold of -1 might be used in a moderate setting, whereas -1.5 could be used in a conservative setting to require a deeper dip before triggering.

f) Divergence Checks

The script looks back a specified number of bars (divergenceLookback). For both price and the fisher line, it identifies:

• priceHigh = the highest hl2 within the lookback

• priceLow = the lowest hl2 within the lookback

• fisherHigh = the highest fisher value within the lookback

• fisherLow = the lowest fisher value within the lookback

If price forms a lower low while fisher forms a higher low, it can signal a bullish divergence. Conversely, if price forms a higher high while fisher forms a lower high, a bearish divergence might be indicated.

g) Bar Coloring

The script monitors the absolute change in Fisher values from one bar to the next (sometimes called fisherChange):

fisherChange = abs(fisher - fisher )

If fisherChange exceeds a user-defined intensityThreshold, bars are recolored to highlight a surge of momentum. Aqua might indicate a strong bullish surge, while purple might indicate a strong bearish surge.

This color-coding provides a quick visual cue for traders looking to spot large momentum swings without constantly monitoring indicator values.

8. Signal Generation and Filtering

Buy and sell signals occur when the Fisher line crosses the signal line in regions defined as oversold or overbought. The optional minimum movement filter prevents triggering if Fisher and its signal line are too close, reducing the chance of small, inconsequential price fluctuations creating frequent signals. Divergences that appear in oversold or overbought regions can serve as additional evidence that momentum might soon shift.

9. Visualization on the Chart

Uptrick: Fisher Eclipse plots two lines: the Fisher line in one color and the signal line in a contrasting shade. The chart displays horizontal dashed lines where the overbought and oversold levels lie. When the Fisher Transform experiences a sharp jump or drop above the intensity threshold, the corresponding price bars may change color, signaling that momentum has undergone a noticeable shift. If the indicator detects bullish or bearish divergence, dotted lines are drawn on the oscillator portion to connect the relevant points.

10. Market Adaptability

Because of the different aggressiveness levels and the optional minimum movement filter, Uptrick: Fisher Eclipse can be tailored to multiple trading styles. For instance, a short-term scalper might select a smaller length and more aggressive thresholds, while a swing trader might choose a longer length for smoother readings, along with conservative thresholds to ensure fewer but potentially stronger signals. During strongly trending markets, users might rely more on divergences or large intensity changes, whereas in a range-bound market, oversold or overbought conditions may be more frequent.

11. Risk Management Considerations

Indicators alone do not ensure favorable outcomes, and relying solely on any one signal can be risky. Using a stop-loss or other protections is often suggested, especially in fast-moving or unpredictable markets. Divergence can appear before a market reversal actually starts. Similarly, a Fisher Transform can remain in an overbought or oversold region for extended periods, especially if the trend is strong. Cautious interpretation and confirmation with additional methods or chart analysis can help refine entry and exit decisions.

12. Combining with Other Tools

Traders can potentially strengthen signals from Uptrick: Fisher Eclipse by checking them against other methods. If a moving average cross or a price pattern aligns with a Fisher crossover, the combined evidence might provide more certainty. Volume analysis may confirm whether a shift in market direction has participation from a broad set of traders. Support and resistance zones could reinforce overbought or oversold signals, particularly if price reaches a historical boundary at the same time the oscillator indicates a possible reversal.

13. Parameter Customization and Examples

Some short-term traders run a 15-minute chart, with a shorter length setting, aggressively tight oversold and overbought thresholds, and a smaller divergence lookback. This approach produces more frequent signals, which may appeal to those who enjoy fast-paced trading. More conservative traders might apply the indicator to a daily chart, using a larger length, moderate threshold levels, and a bigger divergence lookback to focus on broader market swings. Results can differ, so it may be helpful to conduct thorough historical testing to see which combination of parameters aligns best with specific goals.

14. Realistic Expectations

While the Fisher Transform can reveal potential turning points, no mathematical tool can predict future price behavior with full certainty. Markets can behave erratically, and a period of strong trending may see the oscillator pinned in an extreme zone without a significant reversal. Divergence signals sometimes appear well before an actual trend change occurs. Recognizing these limitations helps traders manage risk and avoids overreliance on any one aspect of the script’s output.

15. Theoretical Background

The Fisher Transform uses a logarithmic formula to map a normalized input, typically ranging between -1 and +1, into a scale that can fluctuate around values like -3 to +3. Because the transformation exaggerates higher and lower readings, it becomes easier to spot when the market might have stretched too far, too fast. Uptrick: Fisher Eclipse builds on that foundation by adding a series of practical tools that help confirm or refine those signals.

16. Originality and Uniqueness

Uptrick: Fisher Eclipse is not simply a duplicate of the basic Fisher Transform. It enhances the original design in several ways, including built-in divergence detection, bar-color triggers for momentum surges, thresholds for overbought and oversold levels, and customizable signal aggressiveness. By unifying these concepts, the script seeks to reduce noise and highlight meaningful shifts in market direction. It also places greater emphasis on helping traders adapt the indicator to their specific style—whether that involves frequent intraday signals or fewer, more robust alerts over longer timeframes.

17. Summary

Uptrick: Fisher Eclipse is an expanded take on the original Fisher Transform oscillator, including divergence detection, bar coloring based on momentum strength, and flexible signal thresholds. By adjusting parameters like length, aggressiveness, and intensity thresholds, traders can configure the script for day-trading, swing trading, or position trading. The indicator endeavors to highlight where price might be shifting direction, but it should still be combined with robust risk management and other analytical methods. Doing so can lead to a more comprehensive view of market conditions.

18. Disclaimer

No indicator or script can guarantee profitable outcomes in trading. Past performance does not necessarily suggest future results. Uptrick: Fisher Eclipse is provided for educational and informational purposes. Users should apply their own judgment and may want to confirm signals with other tools and methods. Deciding to open or close a position remains a personal choice based on each individual’s circumstances and risk tolerance.

13W High/Low/Fibs w/100D SMAIndicator: 13 Week High/100 Day SMA/13 Week Low with 0.382, 0.5, and 0.618 Fibonacci Levels

Description:

This indicator for TradingView, written in Pine Script version 6

It displays a table on the chart that provides a visual analysis of key price levels based on a 13-week timeframe and a 100-day Simple Moving Average (SMA).

Core Calculations:

100-Day SMA: The indicator calculates the 100-day Simple Moving Average of the closing price using daily data. The SMA is a widely used trend-following indicator.

13-Week High and Low: The indicator calculates the highest high and lowest low over the past 13 weeks using weekly data. This provides a longer-term perspective on the price range.

13-Week Fibonacci Retracement Levels: Based on the calculated 13-week high and low, the script determines the 0.382, 0.5, and 0.618 Fibonacci retracement levels.

The table includes the following information:

13W High: The highest price reached over the last 13 weeks.

100D SMA: The calculated 100-day Simple Moving Average value.

13W Low: The lowest price reached over the last 13 weeks.

Fibonacci Levels: The 0.382, 0.5, and 0.618 Fibonacci retracement levels, labeled as "↗," "|," and "↘," respectively.

Global Market Strength IndicatorThe Global Market Strength Indicator is a powerful tool for traders and investors. It helps compare the strength of various global markets and indices. This indicator uses the True Strength Index (TSI) to measure market strength.

The indicator retrieves price data for different markets and calculates their TSI values. These values are then plotted on a chart. Each market is represented by a different colored line, making it easy to distinguish between them.

One of the main benefits of this indicator is its comprehensive global view. It covers major indices and country-specific ETFs, giving users a broad perspective on global market trends. This wide coverage allows for easy comparison between different markets and regions.

The indicator is highly customizable. Users can adjust the TSI smoothing period to suit their preferences. They can also toggle the visibility of individual markets. This feature helps reduce chart clutter and allows for more focused analysis.

To use the indicator, apply it to your chart in TradingView. Adjust the settings as needed, and observe the relative positions and movements of the TSI lines. Lines moving higher indicate increasing strength in that market, while lines moving lower suggest weakening markets.

The chart includes reference lines at 0.5 and -0.5. These help identify potential overbought and oversold conditions. Markets with TSI values above 0.5 may be considered strong or potentially overbought. Those below -0.5 may be weak or potentially oversold.

By comparing the movements of different markets, users can identify which markets are leading or lagging. They can also spot potential divergences between related markets. This information can be valuable for identifying sector rotations or shifts in global market sentiment.

A dynamic legend automatically updates to show only the visible markets. This feature improves chart readability and makes it easier to interpret the data.

The Global Market Strength Indicator is a versatile tool that provides valuable insights into global market performance. It helps traders and investors identify trends, compare market performances, and make more informed decisions. Whether you're looking to spot emerging global trends or identify potential trading opportunities, this indicator offers a comprehensive solution for global market analysis.

Sharpe Ratio Z-ScoreThe "Sharpe Ratio Z-Score" indicator is a powerful tool designed to measure risk-adjusted returns in financial assets. This script helps investors evaluate the performance of a security relative to its risk, using a Z-score based modification of the Sharpe Ratio. The indicator is suitable for assessing market environments and understanding periods of underperformance or overperformance relative to historical standards.

Features:

Risk Assessment and Scaling: The indicator calculates a modified version of the Sharpe Ratio

over a user-defined period. By using scaling and mean offset adjustments, it allows for better

fitting to different market conditions.

Customizable Settings:

Period Length: The number of bars used to calculate the Sharpe Ratio.

Mean Adjustment: Offset value to adjust the average return of the calculated Sharpe ratio.

Scale Factor: A multiplier for emphasizing or reducing the calculated score's impact.

Line Color: Easily customize the plot's appearance.

Visual Cues:

Plots horizontal lines and fills specific regions to visually represent significant Z-score levels.

Highlighted zones include risk thresholds, such as overbought (positive Z-scores) and oversold

(negative Z-scores) areas, using intuitive color fills:

Green for areas below -0.5 (potential buy opportunities).

Red for areas above 0.5 (potential sell opportunities).

Yellow for neutral zones between -0.5 and 0.5.

Use Cases:

Risk-Adjusted Decision Making: Understand when returns are favorable compared to risk, especially during volatile market conditions.

Timing Reversion to Mean: Use highlighted zones to identify potential reversion-to-mean scenarios.

Trend Analysis: Identify times when an asset's performance is significantly deviating from its

average risk-adjusted return.

How It Works:

The script computes the daily returns over a set period, calculates the standard deviation of

those returns, and then applies a modified Sharpe Ratio approach. The Z-score transformation

helps to visualize how far an asset's risk-adjusted return deviates from its historical average.

This "Sharpe Ratio Z-Score" indicator is well-suited for investors seeking to combine quantitative metrics with visual cues, enhancing decision-making for long and short positions while maintaining a risk-adjusted perspective.

Altcoins vs BTC Market Cap HeatmapAltcoins vs BTC Market Cap Heatmap

"Ground control to major Tom" 🌙 👨🚀 🚀

This indicator provides a visual heatmap for tracking the relationship between the market cap of altcoins (TOTAL3) and Bitcoin (BTC). The primary goal is to identify potential market cycle tops and bottoms by analyzing how the TOTAL3 market cap (all cryptocurrencies excluding Bitcoin and Ethereum) compares to Bitcoin’s market cap.

Key Features:

• Market Cap Ratio: Plots the ratio of TOTAL3 to BTC market caps to give a clear visual representation of altcoin strength versus Bitcoin.