RSI W Pattern strategyThis strategy is similar to RSI V pattern strategy, but it looks for W pattern in RSI chart.

RULES

======

BUY

1. ema20 is above ema50

2. RSI5 crossing up 30 from oversold area

3. and RSI5 must be below overbought area (default value set to 65)

Add to existing Position

1. You can add on the next W pattern OR

2. if RSI5 is crossing up from below 20

Exit

1. when RSI5 reaches 75

Note: This is for short term/swing trading . which gets on when price dip in trending and quickly gets you out on RSI overbought area

Strategy!

TSI CCI Hull with profit$$$This is a modified version of @SeaSide420 TSI CCI Hull with profits exit on long and short order

ORIGINAL SCRIPT:

/// /// feel free to edit/improve and comment

Options Decay Speed for 0DTEUse only for:

SPX, 5 minutes time frame

This indicator is complementing options 0DTE strategy - selling options for SPX index in the same day as they are expiring. Output of the indicator (red or green color of the curve) indicates whether is profitable to sell options at given moment at delta and VIX specified in the parameters. Changing parameter "Candles" is not recommended.

Main thought is that options expire with certain speed (theta decay) when stock doesnt move. When stock moves in unfavorable direction slowly enough, decay speed can compensate for disadvantage coming from option delta. Intuitively there must be certain speed of stock value change (expressed in stock value per 5 minutes) that is exactly compensating theta decay. This indicator calculates those two values (details below) and shows, where theta decay is faster than stock movement in the last hour and thus favorable to sell options.

Indicator gets its result from comparing two values:

1) volatility in the form of highest high and lowest low for past 12 candles (one hour in total) divided by 12 - meaning average movement of stock expressed in

2) speed of options value decay in form of combination of theta decay and option delta. Formulas are approximation of Black-Scholes model as Pine script doesnt allow for advanced functions. Approximations are accurate to 2 decimal points from market open to one hour before market close and will not indicate green when accuracy is not sufficient. Its value is also expressed in so its mutualy comparable.

My focus was not on code elegance but on practical usability.

Written by Ondřej Škop.

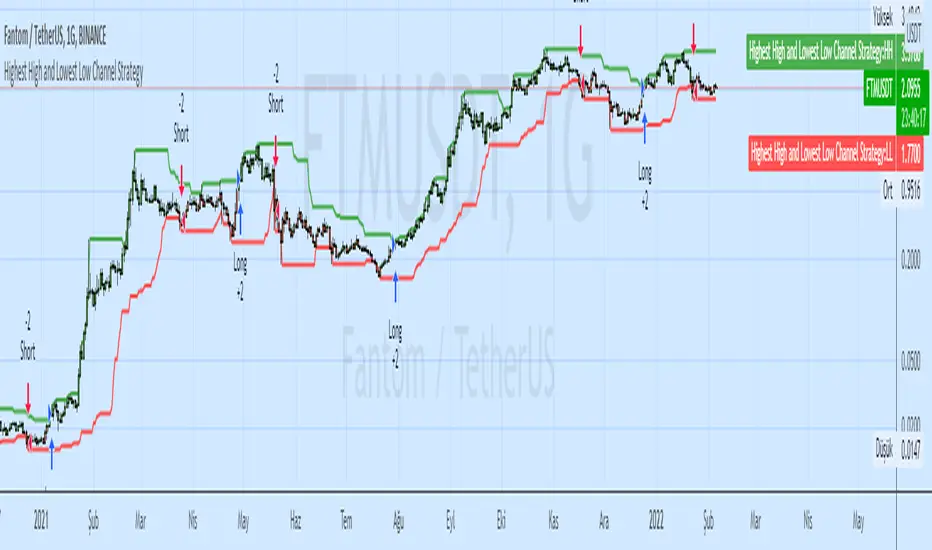

Highest High and Lowest Low Channel StrategyHighest / Highest High Highest (Data) - HHV (Data, Period)

Lowest / Lowest Low Lowest (Data) LLV (Data, Period)

These functions calculate the highest / lowest value of a selected data.

Highest High and Lowest Low options are mostly used.

The Highest function calculates the highest value of the selected data in the past.

The Lowest function calculates the lowest value of the selected data in the past.

Pivot Point V2 Strategy Pivot points simply took the high, low, and closing price from the previous period and

divided by 3 to find the pivot. From this pivot, traders would then base their

calculations for three support, and three resistance levels. The calculation for the most

basic flavor of pivot points, known as ‘floor-trader pivots’, along with their support and

resistance levels.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Elder Ray (Bear Power) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bull Power measures the ability of buyers to

drive prices above the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

EMA Slope Trend Follower StrategyThis strategy is based on the slope of the EMA130.

Over that slope, the script calculates two EMAs (9,21) which are used to generate the main entry and exit signal.

In particular, the strategy enters a LONG position when EMA9 > EMA21. On the contrary, it closes the LONG and opens a SHORT when EMA9 < EMA21.

When the slope of the EMA130 is rising, it means that the price is accelerating upwards, fueling an uptrend. Conversely, when the slope is falling, it means that the price is slowing down, falling into a possible downtrend.

Calculating and analyzing two EMAs (fast and slow) over the slope of a medium length EMA instead of the price anticipates a lot the signal. In this way, the strategy never miss a trend.

In order to minimize false positives (entering useless positions), I included two filters, which can be optionally turned on:

- Trend Filter: When the price is above EMA200, the strategy opens ONLY LONG positions. If price < EMA200, only shorts allowed. If the slope gives a long signal and price is below EMA200, for example, the eventual SHORT position is closed, but the LONG entry is postponed to the moment when both conditions (slope uptrending and price > ema200) are met.

I recommend always turning on this filter, as it dramatically decreases drawdown.

- Volatility Filter: When the standard deviation of the last 20 candles is below its 50 samples moving average, no positions are opened, as market is going sideways. The purpose of this filter is to prevent false positives (positions which open and close in a matter of candles due to false signals in sideways market).

I recommend turning on this filter only on low time frames.

This strategy works great on medium time frames (like 4h, 6h, daily), since it spends way less in fees, opening less positions.

It works good on low TFs too (up to 1h, didn't test lower ones), provided Volatility filter is turned on and parameters are set according to the asset.

Commission included in calculations: 0.06% (it's the taker commission on BitMEX with the 10% discount obtainable with any referral link)

Slippage included in calculations: 2 ticks (BitMEX has very liquid order books, and slippage doesn't happen very often unless a huge position size is used).

Hull Suite StrategyConverted the hull suite into a strategy script for easy backtesting and added ability to specify a time periods to backtest over.

RSI5_50 with DivergenceThis is variation of RSI Divergence strategy.

I have added a filter (long term RSI) to the Rules. strategy BUYs when RSI 50 period is above 50 line and there is divergence on the short term RSI

settings

=========

short term RSI period 5

long term RSI period 50

stopLoss is 8% --- if setting is enabled

BUY Rule

========

RSI 50 is above 50 line

short term RSI is showing divergence

Add to existing

==============

if already in position, BUY when shorTermRSI is crossing above 20

TakeProfit

=========

when longTermRSI reaches 60,65, 70 and 75 level , take partial profits .

(not when crossing down --- This may affect on profits , because when price goes down , it goes very fast )

Exit

=====

when longTermRSI is crossing down 30

OR stopLoss value hits

Note: When I tested this with GOOGL stock , I have got excellent results ... any experts there , please check everything is good with scripting ...

Happy Trading

RSI V Pattern strategyThis strategy based on RSI for swing trading or short term trading

Strategy Rules

=============

LONG

1. ema20 is above ema50 --- candles are colored green on the chart

2. RSI value sharply coming up

previous candle1 low is previous candle2 low and previous candle1 RSI value is less than previous candle2

current candle RSI value is greater than previous candle1 and crossing above 30

above which makes a V shape on RSI indicator, colored in yellow on the chart , price bar is colored in yellow

3. Enter Long when the above V pattern occurs

EXIT LONG

1. when the RSI reaches 70 , close half position and move stop loss to up

2. when RSI reaches high value 90, close 3/4 position

3. when RSI crossing below 10 OR stopLoss hit , whichever happens first , close whole position

Note : take profit levels are colored in blue on RSI and Price candles

I have tested SPY , QQQ on daily chart , performance results are with 80% win rate and more than 3 profit factor

Happy Trading

KD compare strategy (交易策略對照組)This is a base and easy trading strategy for comparing my other strategy.

The strategy consider K >= 80 is strong target in the last high period,

and consider K <=20 is the weak target in the last low period.

In the strong target, the strategy may increase long at the first day when K < 50, until 2/3 max order limitation or strong target become to weak.

In the weak target, the strategy may increase short at the first day when K > 50, until 2/3 max order limitation or strong target become to strong.

there are three orders for this strategy.

when the strong become to weak, it may use the remain 1/3 to save itself, and change the direction at the next k > 50

when the weak become to weak, it may use the remain 1/3 to save itself, and change the direction at the next k < 50

這是一個簡單的雙向交易策略,用來對照我其他的策略。

當 K>=80 它會認為目前是強勢股,偏多操作

當 K<=20 它會認為目前是強勢股,偏空操作

當標的為強勢股時,當第一次 K<50 會加碼多單,最多買進2/3的持股,直到轉弱

當標的為弱勢股時,當第一次 K>50 會加碼空單,最多買進2/3的持股,直到轉強

當強勢轉弱勢時,會使用剩下的1/3來拯救持股,在下次 k > 50 出清持股

當弱勢轉強勢時,會使用剩下的1/3來拯救持股,在下次 k < 50 出清持股

Ranged Volume Strategy - evoThis is the strategy version for the ranged volume indicator I published a few days ago.

Long : First yellow break-out after red

Short : First red break-out after yellow

Because this is volume, you want to be using this on an exchange with high volume for the best results. Default settings are not optimized but work great on bitcoins daily chart.

A short explanation of the indicator below:

[FN] Session Range & Date Range For BacktestingThis has been done before in different ways, however, my goal is to publish a single, simplified copy/paste version of the idea so you can quickly and easily incorporate it into your strategy backtesting.

You can designate weekdays, weekdays + weekends for 24/7 markets, and also session range.

So, you trade bitcoin? It works. CME futures? It works. You are a discretionary trader so the only signals that matter are the ones that happen when you're awake? It works. Copy and paste.

The goal is that its that easy. You'll have to let me know if it is. glhf everyone.

If I'm not mistaken, you should be able to copy/paste this directly into your strategy script (Paste it in before your entry declarations). Just leave out the last 2 lines where the bgcolor() is declared... unless you want the background color lit up, that's up to you. It's just for demonstration purposes in this script.

After you've pasted it in, then in your strategy.entry() function you are adding: to the strategy.entry() function.

e.g:

strategy.entry("Long", strategy.long, qty=1, when = ENTRY_SIGNAL and signal_backtest())

Shoutouts to @zenandtheartoftrading and @allanster for providing the basis of this code that I put together here. We stand on the shoulders of giants.

Camarilla Pivot Points V2 Strategy Camarilla pivot point formula is the refined form of existing classic pivot point formula.

The Camarilla method was developed by Nick Stott who was a very successful bond trader.

What makes it better is the use of Fibonacci numbers in calculation of levels.

Camarilla equations are used to calculate intraday support and resistance levels using

the previous days volatility spread. Camarilla equations take previous day’s high, low and

close as input and generates 8 levels of intraday support and resistance based on pivot points.

There are 4 levels above pivot point and 4 levels below pivot points. The most important levels

are L3 L4 and H3 H4. H3 and L3 are the levels to go against the trend with stop loss around H4 or L4 .

While L4 and H4 are considered as breakout levels when these levels are breached its time to

trade with the trend.

WARNING:

- For purpose educate only

- This script to change bars colors.

Ichimoku Kinko Hyo: ETH 3h Strategy by tobunoIchimoku Kinko Hyo strategy for long term trend trades of Ethereum . Optimized for 3H ticks.

Camarilla Pivot Points Strategy Pivot point studies highlight prices considered to be a likely turning point

when looking at values from a previous period, whether it be daily, weekly,

quarterly or annual. Each pivot point study has its own characteristics on

how these points are calculated.

Red color = Sell

Green color = Buy

WARNING:

- For purpose educate only

- This script to change bars colors.

Super Z strategy - Thanks to Rafael Zioni//Original script

//https://www.tradingview.com/script/wYknDlLx-super-Z/

This is a test for verifying if this interesting study works well.

The author, thanks to him!!!, advise a possible repaint because the script uses security function.

Refer to tradingview.com for more info on repainting:

www.tradingview.com

QUOTE:

We can see repainting in the following cases:

1- Strategies using calc_on_every_tick=true. A strategy with parameter calc_on_every_tick = false may also be prone to repainting, but to a lesser degree.

(this is not the case, ndr).

2- Using security for requesting data from a resolution higher than the resolution of the chart’s main symbol (i.e. do not use ion weelky chart if you set 1440 (1Day) in inputs)

NOTE: Thanks again to Rafael Zioni. If he requires to delete this strategy, I'll do immediately.

Mean Reversion w/ Bollinger BandsThis is a more advanced version of my original mean reversion script.

It employs the famous Bollinger Bands.

This robot will buy when price falls below the lower Bollinger Band, and sell when price moves above the upper Bollinger Band.

I've only tested it on the S&P 500, though you could try it out on other assets to see the backtest performance.

During the recent COVID-19 bear market drop, it produced several buy signals on the S&P which I followed, and made some nice gains so far.

I still think this would make a better investing strategy (buy undervalued / sell over-valued), rather than a trading strategy.

I use this robot for my long term portfolio.

Combo Strategy 123 Reversal & Elder Ray (Bear Power) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bear Power measures the ability of sellers to

drive prices below the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

VPTbollfib & Camarilla (Danarilla)I do not own the original indicators. This is just a combination of the two because of their nature to work in a similar way.

Camarilla Pivots run on the basis of intraday range trading. Usually after daily open you look the fade whatever move happened before. by shorting R3/H3 levels or longing R3/L3. Targeting the other side of the range. This is the infamous PivotBoss level calculations and you would want to activate camarilla and turn off the normal pivots. They use the previous days volatility to plot the next days levels.

But what about some confirmation?

Well RafaelIzoni (who made it open source for improvement) threw together this VPTbollfib. It is volume price trend crossing down a fib line using bollinger bands as price envelope. The beauty of this is that It will signal usually counter to current price action based on selling into uptrends or vise versa. Meaning you get signals to counter price. Which is what you might be looking for on range day trade scalps for camarilla. A wick reversal or engulfing + volume based signal is a very happy pairing together. And those signals are usually suitable for the target of the range you are day trading. Hourly time frame works quite well for both. And camarilla should also be on daily settings.

Special Thanks to Nanda (who published the pivotboss indicator AND) Helped to merge the scripts together.

This indicator alone is an entire trade system. Camarilla already is. If you know the rules. it can be used for entries, exits, risk management to trade the range on TREND, COUNTER TREND, and BREAKOUT plays. The bollinger band fibs add confirmation to the trends levels. And the VPT adds a secondary confirmation to take a camarilla trade.

Try it out. I think you will find both the levels on camarilla and the VPT signals quite suprising.

Strategy Follow Line MTF Any MM AverageThe objective is only to evaluate different configurations of the indicator "Follow Line MTF Any MM Average".

The strategy does not have position management, it's very basic, this indicator should be used to see trend, range zones, evaluate the best areas to enter the market, use higher time frames to confirm a direction can be useful.

I do not recommend using only this indicator to trade, because you can lose all your money if you do not know what you are doing.

I hope you find it useful.

Successes