CalendarCadLibrary "CalendarCad"

This library provides date and time data of the important events on CAD. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2023()

CAD high impact news date and time from 2015 to 2023

Timesessions

CalendarEurLibrary "CalendarEur"

This library provides date and time data of the important events on EUR. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2019()

EUR high impact news date and time from 2015 to 2019

HighImpactNews2020To2023()

EUR high impact news date and time from 2020 to 2023

CalendarGbpLibrary "CalendarGbp"

This library provides date and time data of the important events on GBP. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2019()

GBP high impact news date and time from 2015 to 2019

HighImpactNews2020To2023()

GBP high impact news date and time from 2020 to 2023

CalendarJpyLibrary "CalendarJpy"

This library provides date and time data of the important events on JPY. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2023()

JPY high impact news date and time from 2015 to 2023

CalendarUsdLibrary "CalendarUsd"

This library provides date and time data of the important events on USD. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2019()

USD high impact news date and time from 2015 to 2019

HighImpactNews2020To2023()

USD high impact news date and time from 2020 to 2023

NewsEventsGbpLibrary "NewsEventsGbp"

This library provides date and time data of the high imact news events on GBP. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

gbpNews2015To2019()

GBP high imact news date and time from 2015 to 2019

gbpNews2020To2023()

GBP high imact news date and time from 2020 to 2023

NewsEventsEurLibrary "NewsEventsEur"

This library provides date and time data of the high imact news events on EUR. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

eurNews2015To2019()

EUR high imact news date and time from 2015 to 2019

eurNews2020To2023()

EUR high imact news date and time from 2020 to 2023

NewsEventsJpyLibrary "NewsEventsJpy"

This library provides date and time data of the high imact news events on JPY. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

jpyNews2015To2023()

JPY high imact news date and time from 2015 to 2023

NewsEventsCadLibrary "NewsEventsCad"

This library provides date and time data of the high imact news events on CAD. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

cadNews2015To2023()

CAD high imact news date and time from 2015 to 2023

NewsEventsUsdLibrary "NewsEventsUsd"

This library provides date and time data of the high imact news events on USD. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

usdNews2015To2019()

USD high imact news date and time from 2015 to 2019

usdNews2020To2023()

USD high imact news date and time from 2020 to 2023

lib_trackingLibrary "lib_tracking"

tracking highest and lowest with anchor point to track over dynamic periods, e.g. to track a Session HH/LL live and get the bar/time of the LTF wick that matches the HTF HH/LL

// DESIGN DECISION

// why anchored replacements for ta.highest / ta.highestbars / ta.lowest / ta.lowestbars:

// 1. they require a fixed length/lookback which makes it easier to calculate, but

// 2. this prevents us from tracking the HH/LL of a changing timeframe, e.g. live tracking the HH/LL of a running session or unfinished higher timeframe

// 3. tracking with anchor/start/reset flag allows to persist values until the next start/reset, so no other external storage is required

track_highest(value, reset, track_this_bar)

Parameters:

value (float)

reset (bool) : boolean flag to restart tracking from this point (a.k.a anchor)

track_this_bar (bool) : allows enabling and disabling of tracking, e.g. before a session starts or after it ends, values can be kept until next reset.

track_lowest(value, reset, track_this_bar)

Parameters:

value (float)

reset (bool) : boolean flag to restart tracking from this point (a.k.a anchor)

track_this_bar (bool) : allows enabling and disabling of tracking, e.g. before a session starts or after it ends, values can be kept until next reset.

track_hl_htf(htf, value_high, value_low)

Parameters:

htf (string) : the higher timeframe in pinescript string notation

value_high (float)

value_low (float)

Returns:

RelativeValue█ OVERVIEW

This library is a Pine Script™ programmer's tool offering the ability to compute relative values, which represent comparisons of current data points, such as volume, price, or custom indicators, with their analogous historical data points from corresponding time offsets. This approach can provide insightful perspectives into the intricate dynamics of relative market behavior over time.

█ CONCEPTS

Relative values

In this library, a relative value is a metric that compares a current data point in a time interval to an average of data points with corresponding time offsets across historical periods. Its purpose is to assess the significance of a value by considering the historical context within past time intervals.

For instance, suppose we wanted to calculate relative volume on an hourly chart over five daily periods, and the last chart bar is two hours into the current trading day. In this case, we would compare the current volume to the average of volume in the second hour of trading across five days. We obtain the relative volume value by dividing the current volume by this average.

This form of analysis rests on the hypothesis that substantial discrepancies or aberrations in present market activity relative to historical time intervals might help indicate upcoming changes in market trends.

Cumulative and non-cumulative values

In the context of this library, a cumulative value refers to the cumulative sum of a series since the last occurrence of a specific condition (referred to as `anchor` in the function definitions). Given that relative values depend on time, we use time-based conditions such as the onset of a new hour, day, etc. On the other hand, a non-cumulative value is simply the series value at a specific time without accumulation.

Calculating relative values

Four main functions coordinate together to compute the relative values: `maintainArray()`, `calcAverageByTime()`, `calcCumulativeSeries()`, and `averageAtTime()`. These functions are underpinned by a `collectedData` user-defined type (UDT), which stores data collected since the last reset of the timeframe along with their corresponding timestamps. The relative values are calculated using the following procedure:

1. The `averageAtTime()` function invokes the process leveraging all four of the methods and acts as the main driver of the calculations. For each bar, this function adds the current bar's source and corresponding time value to a `collectedData` object.

2. Within the `averageAtTime()` function, the `maintainArray()` function is called at the start of each anchor period. It adds a new `collectedData` object to the array and ensures the array size does not exceed the predefined `maxSize` by removing the oldest element when necessary. This method plays an essential role in limiting memory usage and ensuring only relevant data over the desired number of periods is in the calculation window.

3. Next, the `calcAverageByTime()` function calculates the average value of elements within the `data` field for each `collectedData` object that corresponds to the same time offset from each anchor condition. This method accounts for cases where the current index of a `collectedData` object exceeds the last index of any past objects by using the last available values instead.

4. For cumulative calculations, the `averageAtTime()` function utilizes the `isCumulative` boolean parameter. If true, the `calcCumulativeSeries()` function will track the running total of the source data from the last bar where the anchor condition was met, providing a cumulative sum of the source values from one anchor point to the next.

To summarize, the `averageAtTime()` function continually stores values with their corresponding times in a `collectedData` object for each bar in the anchor period. When the anchor resets, this object is added to a larger array. The array's size is limited by the specified number of periods to be averaged. To correlate data across these periods, time indexing is employed, enabling the function to compare corresponding points across multiple periods.

█ USING THIS LIBRARY

The library simplifies the complex process of calculating relative values through its intuitive functions. Follow the steps below to use this library in your scripts.

Step 1: Import the library and declare inputs

Import the library and declare variables based on the user's input. These can include the timeframe for each period, the number of time intervals to include in the average, and whether the calculation uses cumulative values. For example:

//@version=5

import TradingView/RelativeValue/1 as TVrv

indicator("Relative Range Demo")

string resetTimeInput = input.timeframe("D")

int lengthInput = input.int(5, "No. of periods")

Step 2: Define the anchor condition

With these inputs declared, create a condition to define the start of a new period (anchor). For this, we use the change in the time value from the input timeframe:

bool anchor = timeframe.change(resetTimeInput)

Step 3: Calculate the average

At this point, one can calculate the average of a value's history at the time offset from the anchor over a number of periods using the `averageAtTime()` function. In this example, we use True Range (TR) as the `source` and set `isCumulative` to false:

float pastRange = TVrv.averageAtTime(ta.tr, lengthInput, anchor, false)

Step 4: Display the data

You can visualize the results by plotting the returned series. These lines display the non-cumulative TR alongside the average value over `lengthInput` periods for relative comparison:

plot(pastRange, "Past True Range Avg", color.new(chart.bg_color, 70), 1, plot.style_columns)

plot(ta.tr, "True Range", close >= open ? color.new(color.teal, 50) : color.new(color.red, 50), 1, plot.style_columns)

This example will display two overlapping series of columns. The green and red columns depict the current TR on each bar, and the light gray columns show the average over a defined number of periods, e.g., the default inputs on an hourly chart will show the average value at the hour over the past five days. This comparative analysis aids in determining whether the range of a bar aligns with its typical historical values or if it's an outlier.

█ NOTES

• The foundational concept of this library was derived from our initial Relative Volume at Time script. This library's logic significantly boosts its performance. Keep an eye out for a forthcoming updated version of the indicator. The demonstration code included in the library emulates a streamlined version of the indicator utilizing the library functions.

• Key efficiencies in the data management are realized through array.binary_search_leftmost() , which offers a performance improvement in comparison to its loop-dependent counterpart.

• This library's architecture utilizes user-defined types (UDTs) to create custom objects which are the equivalent of variables containing multiple parts, each able to hold independent values of different types . The recently added feature was announced in this blog post.

• To enhance readability, the code substitutes array functions with equivalent methods .

Look first. Then leap.

█ FUNCTIONS

This library contains the following functions:

calcCumulativeSeries(source, anchor)

Calculates the cumulative sum of `source` since the last bar where `anchor` was `true`.

Parameters:

source (series float) : Source used for the calculation.

anchor (series bool) : The condition that triggers the reset of the calculation. The calculation is reset when `anchor` evaluates to `true`, and continues using the values accumulated since the previous reset when `anchor` is `false`.

Returns: (float) The cumulative sum of `source`.

averageAtTime(source, length, anchor, isCumulative)

Calculates the average of all `source` values that share the same time difference from the `anchor` as the current bar for the most recent `length` bars.

Parameters:

source (series float) : Source used for the calculation.

length (simple int) : The number of reset periods to consider for the average calculation of historical data.

anchor (series bool) : The condition that triggers the reset of the average calculation. The calculation is reset when `anchor` evaluates to `true`, and continues using the values accumulated since the previous reset when `anchor` is `false`.

isCumulative (simple bool) : If `true`, `source` values are accumulated until the next time `anchor` is `true`. Optional. The default is `true`.

Returns: (float) The average of the source series at the specified time difference.

LibraryTimeframeHelperLibrary "LibraryTimeframeHelper"

Helper functions to work with timeframes: to get the next higher TF, and to make the string pretty for use in labels. Perhaps I'll add more later.

f_getHigherTF(_TF)

f_getHigherTF(): Converts the input timeframe into the next one up in the list of commonly used timeframes. NOTE: You can NOT use a TF from this function as input to a request.security() call if called from this library because it gets converted to a series (since there's nothing special about this function, I expect this probably goes for any library). However, you CAN copy the code and use it directly in your script, in which case the output is only a simple variable and thus suitable for the timeframe of a request.security() call.

Parameters:

_TF (string) - The timeframe to convert.

Returns: : A string in standard timeframe format.

f_prettifyTF(_TF)

f_prettifyTF(): Converts the input timeframe from standard timeframe format to the format shown by TradingView on a chart. The output is not suitable for use as an input timeframe of a request.security() call.

Parameters:

_TF (string) - The timeframe to convert.

Returns: : A string in prettified timeframe format.

SessionAndTimeFct_publicLibrary "SessionAndTimeFct_public"

is_in_session(sessionTime, sessionTimeZone)

: Check if actual bar is in specific session with specific time zone

Parameters:

sessionTime

sessionTimeZone

is_session_start(sessionTime, sessionTimeZone)

: Check if actual bar the first bar of a specific session

Parameters:

sessionTime

sessionTimeZone

is_new_day(timeZone)

: Check if a new day started

Parameters:

timeZone

is_new_week(timeZone)

: Check if a new week started

Parameters:

timeZone

is_new_month(timeZone)

: Check if a new month started

Parameters:

timeZone

is_element_to_show_with_tf_up(base, value)

: Check if an element is to show compared to a specific timeframe >

Parameters:

base

value

is_element_to_show_with_tf_down(base, value)

: Check if an element is to show compared to a specific timeframe <

Parameters:

base

value

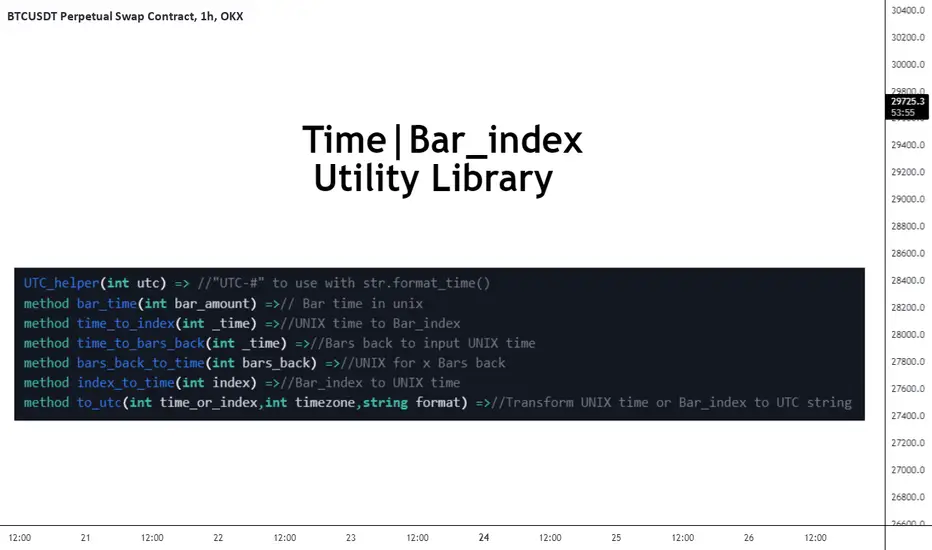

FrizLabz_Time_Utility_MethodsLibrary "FrizLabz_Time_Utility_Methods"

Some time to index and index to time helper methods made them for another library thought I would try to make

them as methods

UTC_helper(utc)

UTC helper function this adds the + to the positive utc times, add "UTC" to the string

and can be used in the timezone arg of for format_time()

Parameters:

utc : (int) | +/- utc offset

Returns: string | string to be added to the timezone paramater for utc timezone usage

bar_time(bar_amount)

from a time to index

Parameters:

bar_amount : (int) | default - 1)

Returns: int bar_time

time_to_index(_time)

from time to bar_index

Parameters:

_time : (int)

Returns: int time_to_index | bar_index that corresponds to time provided

time_to_bars_back(_time)

from a time quanity to bar quanity for use with .

Parameters:

_time : (int)

Returns: int bars_back | yeilds the amount of bars from current bar to reach _time provided

bars_back_to_time(bars_back)

from bars_back to time

Parameters:

bars_back

Returns: int | using same logic as this will return the

time of the bar = to the bar that corresponds to bars_back

index_time(index)

bar_index to UNIX time

Parameters:

index : (int)

Returns: int time | time in unix that corrresponds to the bar_index

to_utc(time_or_index, timezone, format)

method to use with a time or bar_index variable that will detect if it is an index or unix time

and convert it to a printable string

Parameters:

time_or_index : (int) required) | time in unix or bar_index

timezone : (int) required) | utc offset to be appled to output

format : (string) | default - "yyyy-MM-dd'T'HH:mm:ssZ") | the format for the time, provided string is

default one from str.format_time()

Returns: string | time formatted string

GET(line)

Gets the location paramaters of a Line

Parameters:

line : (line)

Returns: tuple

GET(box)

Gets the location paramaters of a Box

Parameters:

box : (box)

Returns: tuple

GET(label)

Gets the location paramaters and text of a Label

Parameters:

label : (label)

Returns: tuple

GET(linefill)

Gets line 1 and 2 from a Linefill

Parameters:

linefill : (linefill)

Returns: tuple

Format(line, timezone)

converts Unix time in time or index params to formatted time

and returns a tuple of the params as string with the time/index params formatted

Parameters:

line : (line) | required

timezone : (int) | default - na

Returns: tuple

Line(x1, y1, x2, y2, extend, color, style, width)

similar to line.new() with the exception

of not needing to include y2 for a flat line, y1 defaults to close,

and it doesnt require xloc.bar_time or xloc.bar_index, if no x1

Parameters:

x1 : (int) default - time

y1 : (float) default - close

x2 : (int) default - last_bar_time/last_bar_index | not required for line that ends on current bar

y2 : (float) default - y1 | not required for flat line

extend : (string) default - extend.none | extend.left, extend.right, extend.both

color : (color) default - chart.fg_color

style : (string) default - line.style_solid | line.style_dotted, line.style_dashed,

line.style_arrow_both, line.style_arrow_left, line.style_arrow_right

width

Returns: line

Box(left, top, right, bottom, extend, border_color, bgcolor, text_color, border_width, border_style, txt, text_halign, text_valign, text_size, text_wrap)

similar to box.new() but only requires top and bottom to create box,

auto detects if it is bar_index or time used in the (left) arg. xloc.bar_time and xloc.bar_index are not used

args are ordered by purpose | position -> colors -> styling -> text options

Parameters:

left : (int) default - time

top : (float) required

right : (int) default - last_bar_time/last_bar_index | will default to current bar index or time

depending on (left) arg

bottom : (float) required

extend : (string) default - extend.none | extend.left, extend.right, extend.both

border_color : (color) default - chart.fg_color

bgcolor : (color) default - color.new(chart.fg_color,75)

text_color : (color) default - chart.bg_color

border_width : (int) default - 1

border_style : (string) default - line.style_solid | line.style_dotted, line.style_dashed,

txt : (string) default - ''

text_halign : (string) default - text.align_center | text.align_left, text.align_right

text_valign : (string) default - text.align_center | text.align_top, text.align_bottom

text_size : (string) default - size.normal | size.tiny, size.small, size.large, size.huge

text_wrap : (string) default - text.wrap_auto | text.wrap_none

Returns: box

Label(x, y, txt, yloc, color, textcolor, style, size, textalign, text_font_family, tooltip)

similar to label.new() but only requires no args to create label,

auto detects if it is bar_index or time used in the (x) arg. xloc.bar_time and xloc.bar_index are not used

args are ordered by purpose | position -> colors -> styling -> text options

Parameters:

x : (int) default - time

y : (float) default - high or low | depending on bar direction

txt : (string) default - ''

yloc : (string) default - yloc.price | yloc.price, yloc.abovebar, yloc.belowbar

color : (color) default - chart.fg_color

textcolor : (color) default - chart.bg_color

style : (string) default - label.style_label_down | label.style_none

label.style_xcross,label.style_cross,label.style_triangleup,label.style_triangledown

label.style_flag, label.style_circle, label.style_arrowup, label.style_arrowdown,

label.style_label_up, label.style_label_down, label.style_label_left, label.style_label_right,

label.style_label_lower_left, label.style_label_lower_right, label.style_label_upper_left,

label.style_label_upper_right, label.style_label_center, label.style_square,

label.style_diamond

size : (string) default - size.normal | size.tiny, size.small, size.large, size.huge

textalign : (string) default - text.align_center | text.align_left, text.align_right

text_font_family : (string) default - font.family_default | font.family_monospace

tooltip : (string) default - na

Returns: label

EventsLibrary "Events"

events()

Returns the list of dates supported by this library as a string array.

Returns: array : Names of events supported by this library

fomcMeetings()

Gets the FOMC Meeting Dates. The FOMC meets eight times a year to determine the course of monetary policy. The FOMC announces its decision on the federal funds rate at the conclusion of each meeting and also issues a statement that provides information on the economic outlook and the Committee's assessment of the risks to the outlook.

Returns: array : FOMC Meeting Dates as timestamps

fomcMinutes()

Gets the FOMC Meeting Minutes Dates. The FOMC Minutes are released three weeks after each FOMC meeting. The Minutes provide information on the Committee's deliberations and decisions at the meeting.

Returns: array : FOMC Meeting Minutes Dates as timestamps

ppiReleases()

Gets the Producer Price Index (PPI) Dates. The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. The PPI is a leading indicator of CPI, and CPI is a leading indicator of inflation.

Returns: array : PPI Dates as timestamps

cpiReleases()

Gets the Consumer Price Index (CPI) Rekease Dates. The Consumer Price Index (CPI) measures changes in the price level of a market basket of consumer goods and services purchased by households. The CPI is a leading indicator of inflation.

Returns: array : CPI Dates as timestamps

csiReleases()

Gets the CSI release dates. The Consumer Sentiment Index (CSI) is a survey of consumer attitudes about the economy and their personal finances. The CSI is a leading indicator of consumer spending.

Returns: array : CSI Dates as timestamps

cciReleases()

Gets the CCI release dates. The Conference Board's Consumer Confidence Index (CCI) is a survey of consumer attitudes about the economy and their personal finances. The CCI is a leading indicator of consumer spending.

Returns: array : CCI Dates as timestamps

nfpReleases()

Gets the NFP release dates. Nonfarm payrolls is an employment report released monthly by the Bureau of Labor Statistics (BLS) that measures the change in the number of employed people in the United States.

Returns: array : NFP Dates as timestamps

eciReleases()

Gets the ECI The Employment Cost Index (ECI) is a measure of the change in the cost of labor,

SH_LibraryLibrary "SH_Library"

events()

Returns the list of dates supported by this library as a string array.

Returns: array : Names of events supported by this library

fomcMeetings()

Gets the FOMC Meeting Dates. The FOMC meets eight times a year to determine the course of monetary policy. The FOMC announces its decision on the federal funds rate at the conclusion of each meeting and also issues a statement that provides information on the economic outlook and the Committee's assessment of the risks to the outlook.

Returns: array : FOMC Meeting Dates as timestamps

fomcMinutes()

Gets the FOMC Meeting Minutes Dates. The FOMC Minutes are released three weeks after each FOMC meeting. The Minutes provide information on the Committee's deliberations and decisions at the meeting.

Returns: array : FOMC Meeting Minutes Dates as timestamps

ppiReleases()

Gets the Producer Price Index (PPI) Dates. The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. The PPI is a leading indicator of CPI, and CPI is a leading indicator of inflation.

Returns: array : PPI Dates as timestamps

cpiReleases()

Gets the Consumer Price Index (CPI) Rekease Dates. The Consumer Price Index (CPI) measures changes in the price level of a market basket of consumer goods and services purchased by households. The CPI is a leading indicator of inflation.

Returns: array : CPI Dates as timestamps

csiReleases()

Gets the CSI release dates. The Consumer Sentiment Index (CSI) is a survey of consumer attitudes about the economy and their personal finances. The CSI is a leading indicator of consumer spending.

Returns: array : CSI Dates as timestamps

cciReleases()

Gets the CCI release dates. The Conference Board's Consumer Confidence Index (CCI) is a survey of consumer attitudes about the economy and their personal finances. The CCI is a leading indicator of consumer spending.

Returns: array : CCI Dates as timestamps

nfpReleases()

Gets the NFP release dates. Nonfarm payrolls is an employment report released monthly by the Bureau of Labor Statistics (BLS) that measures the change in the number of employed people in the United States.

Returns: array : NFP Dates as timestamps

eciReleases()

Gets the ECI The Employment Cost Index (ECI) is a measure of the change in the cost of labor,

ISODateTimeLibrary "ISODateTime"

getDateParts(dateStr)

Get year, month, day from date string.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: array of int

getTimeParts(dateStr)

Get hour, minute, seconds from date string.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: array of int

getUTCTimezone(dateStr)

Get UTC timezone.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: string UTC timezone

Global_Economic_CalendarLibrary of economic events. Created to display events on the desired chart through the indicator.

Countries: USA, China, Eurozone, Russia

Importance: 3 stars

Source: Investing

Библиотека экономических событий. Создана для отображения событий на нужном графике через индикатор.

Страны: США, Китай, Еврозона, Россия

Важность: 3 звезды

Источник: Investing

Traders_Reality_LibLibrary "Traders_Reality_Lib"

This library contains common elements used in Traders Reality scripts

calcPvsra(pvsraVolume, pvsraHigh, pvsraLow, pvsraClose, pvsraOpen, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, darkGreyCandleColor, lightGrayCandleColor)

calculate the pvsra candle color and return the color as well as an alert if a vector candle has apperared.

Situation "Climax"

Bars with volume >= 200% of the average volume of the 10 previous chart TFs, or bars

where the product of candle spread x candle volume is >= the highest for the 10 previous

chart time TFs.

Default Colors: Bull bars are green and bear bars are red.

Situation "Volume Rising Above Average"

Bars with volume >= 150% of the average volume of the 10 previous chart TFs.

Default Colors: Bull bars are blue and bear are violet.

Parameters:

pvsraVolume : the instrument volume series (obtained from request.sequrity)

pvsraHigh : the instrument high series (obtained from request.sequrity)

pvsraLow : the instrument low series (obtained from request.sequrity)

pvsraClose : the instrument close series (obtained from request.sequrity)

pvsraOpen : the instrument open series (obtained from request.sequrity)

redVectorColor : red vector candle color

greenVectorColor : green vector candle color

violetVectorColor : violet/pink vector candle color

blueVectorColor : blue vector candle color

darkGreyCandleColor : regular volume candle down candle color - not a vector

lightGrayCandleColor : regular volume candle up candle color - not a vector

@return

adr(length, barsBack)

Parameters:

length : how many elements of the series to calculate on

barsBack : starting possition for the length calculation - current bar or some other value eg last bar

@return adr the adr for the specified lenght

adrHigh(adr, fromDo)

Calculate the ADR high given an ADR

Parameters:

adr : the adr

fromDo : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrHigh the position of the adr high in price

adrLow(adr, fromDo)

Parameters:

adr : the adr

fromDo : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrLow the position of the adr low in price

splitSessionString(sessXTime)

given a session in the format 0000-0100:23456 split out the hours and minutes

Parameters:

sessXTime : the session time string usually in the format 0000-0100:23456

@return

calcSessionStartEnd(sessXTime, gmt)

calculate the start and end timestamps of the session

Parameters:

sessXTime : the session time string usually in the format 0000-0100:23456

gmt : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return

drawOpenRange(sessXTime, sessXcol, showOrX, gmt)

draw open range for a session

Parameters:

sessXTime : session string in the format 0000-0100:23456

sessXcol : the color to be used for the opening range box shading

showOrX : boolean flag to toggle displaying the opening range

gmt : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return void

drawSessionHiLo(sessXTime, show_rectangleX, show_labelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle)

Parameters:

sessXTime : session string in the format 0000-0100:23456

show_rectangleX : show the session high and low lines

show_labelX : show the session label

sessXcolLabel : the color to be used for the hi/low lines and label

sessXLabel : the session label text

gmt : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle : the line stile for the session high low lines

@return void

calcDst()

calculate market session dst on/off flags

@return indicating if DST is on or off for a particular region

timestampPreviousDayOfWeek(previousDayOfWeek, hourOfDay, gmtOffset, oneWeekMillis)

Timestamp any of the 6 previous days in the week (such as last Wednesday at 21 hours GMT)

Parameters:

previousDayOfWeek : Monday or Satruday

hourOfDay : the hour of the day when psy calc is to start

gmtOffset : the gmt offset string usually in the format GMT+1 or GMT+2 etc

oneWeekMillis : the amount if time for a week in milliseconds

@return the timestamp of the psy level calculation start time

getdayOpen()

get the daily open - basically exchange midnight

@return the daily open value which is float price

newBar(res)

new_bar: check if we're on a new bar within the session in a given resolution

Parameters:

res : the desired resolution

@return true/false is a new bar for the session has started

toPips(val)

to_pips Convert value to pips

Parameters:

val : the value to convert to pips

@return the value in pips

rLabel(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry : series float the y coordinate of the lable

rtext : the text of the label

rstyle : the style for the lable

rcolor : the color for the label

valid : a boolean flag that allows for turning on or off a lable

labelXOffset : how much to offset the label from the current position

rLabelOffset(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry : series float the y coordinate of the lable

rtext : the text of the label

rstyle : the style for the lable

rcolor : the color for the label

valid : a boolean flag that allows for turning on or off a lable

labelXOffset : how much to offset the label from the current position

rLabelLastBar(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series only on the last bar

Parameters:

ry : series float the y coordinate of the lable

rtext : the text of the label

rstyle : the style for the lable

rcolor : the color for the label

valid : a boolean flag that allows for turning on or off a lable

labelXOffset : how much to offset the label from the current position

drawLine(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, labelXOffset, validTimeFrame)

a function that draws a line and a label for a series

Parameters:

xSeries : series float the y coordinate of the line/label

res : the desired resolution controlling when a new line will start

tag : the text for the lable

xColor : the color for the label

xStyle : the style for the line

xWidth : the width of the line

xExtend : extend the line

isLabelValid : a boolean flag that allows for turning on or off a label

labelXOffset : how much to offset the label from the current position

validTimeFrame : a boolean flag that allows for turning on or off a line drawn

drawLineDO(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, labelXOffset, validTimeFrame)

a function that draws a line and a label for the daily open series

Parameters:

xSeries : series float the y coordinate of the line/label

res : the desired resolution controlling when a new line will start

tag : the text for the lable

xColor : the color for the label

xStyle : the style for the line

xWidth : the width of the line

xExtend : extend the line

isLabelValid : a boolean flag that allows for turning on or off a label

labelXOffset : how much to offset the label from the current position

validTimeFrame : a boolean flag that allows for turning on or off a line drawn

drawPivot(pivotLevel, res, tag, pivotColor, pivotLabelColor, pivotStyle, pivotWidth, pivotExtend, isLabelValid, validTimeFrame, levelStart, pivotLabelXOffset)

draw a pivot line - the line starts one day into the past

Parameters:

pivotLevel : series of the pivot point

res : the desired resolution

tag : the text to appear

pivotColor : the color of the line

pivotLabelColor : the color of the label

pivotStyle : the line style

pivotWidth : the line width

pivotExtend : extend the line

isLabelValid : boolean param allows to turn label on and off

validTimeFrame : only draw the line and label at a valid timeframe

levelStart : basically when to start drawing the levels

pivotLabelXOffset : how much to offset the label from its current postion

@return the pivot line series

getPvsraFlagByColor(pvsraColor, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, lightGrayCandleColor)

convert the pvsra color to an internal code

Parameters:

pvsraColor : the calculated pvsra color

redVectorColor : the user defined red vector color

greenVectorColor : the user defined green vector color

violetVectorColor : the user defined violet vector color

blueVectorColor : the user defined blue vector color

lightGrayCandleColor : the user defined regular up candle color

@return pvsra internal code

updateZones(pvsra, direction, boxArr, maxlevels, pvsraHigh, pvsraLow, pvsraOpen, pvsraClose, transperancy, zoneupdatetype, zonecolor, zonetype, borderwidth, coloroverride, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, lightGrayCandleColor)

a function that draws the unrecovered vector candle zones

Parameters:

pvsra : internal code

direction : above or below the current pa

boxArr : the array containing the boxes that need to be updated

maxlevels : the maximum number of boxes to draw

pvsraHigh : the pvsra high value series

pvsraLow : the pvsra low value series

pvsraOpen : the pvsra open value series

pvsraClose : the pvsra close value series

transperancy : the transparencfy of the vecor candle zones

zoneupdatetype : the zone update type

zonecolor : the zone color if overriden

zonetype : the zone type

borderwidth : the width of the border

coloroverride : if the color overriden

redVectorColor : the user defined red vector color

greenVectorColor : the user defined green vector color

violetVectorColor : the user defined violet vector color

blueVectorColor : the user defined blue vector color

lightGrayCandleColor : the user defined regular up candle color

cleanarr(arr)

clean an array from na values

Parameters:

arr : the array to clean

@return if the array was cleaned

calcPsyLevels(oneWeekMillis, showPsylevels, psyType, sydDST)

calculate the psy levels

4 hour res based on how mt4 does it

mt4 code

int Li_4 = iBarShift(NULL, PERIOD_H4, iTime(NULL, PERIOD_W1, Li_0)) - 2 - Offset;

ObjectCreate("PsychHi", OBJ_TREND, 0, Time , iHigh(NULL, PERIOD_H4, iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)), iTime(NULL, PERIOD_W1, 0), iHigh(NULL, PERIOD_H4,

iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)));

so basically because the session is 8 hours and we are looking at a 4 hour resolution we only need to take the highest high an lowest low of 2 bars

we use the gmt offset to adjust the 0000-0800 session to Sydney open which is at 2100 during dst and at 2200 otherwize. (dst - spring foward, fall back)

keep in mind sydney is in the souther hemisphere so dst is oposite of when london and new york go into dst

Parameters:

oneWeekMillis : a constant value

showPsylevels : should psy levels be calculated

psyType : the type of Psylevels - crypto or forex

sydDST : is Sydney in DST

@return

NumberOfVisibleBarsLibrary "NumberOfVisibleBars"

This library calculates the number of visible bars on the user screen

NumberOfVisibleBars(No)

Calculates the number of visible bars on the user screen

Parameters:

No : paramters needed

Returns: The numbers of visible bars on the user screen (int)

EconomicCalendarLibrary "EconomicCalendar"

This library is a data provider for important dates and times from the Economic Calendar.

events()

Returns the list of dates supported by this library as a string array.

Returns: array : Names of events supported by this library

fomcMeetings()

Gets the FOMC Meeting Dates. The FOMC meets eight times a year to determine the course of monetary policy. The FOMC announces its decision on the federal funds rate at the conclusion of each meeting and also issues a statement that provides information on the economic outlook and the Committee's assessment of the risks to the outlook.

Returns: array : FOMC Meeting Dates as timestamps

fomcMinutes()

Gets the FOMC Meeting Minutes Dates. The FOMC Minutes are released three weeks after each FOMC meeting. The Minutes provide information on the Committee's deliberations and decisions at the meeting.

Returns: array : FOMC Meeting Minutes Dates as timestamps

ppiReleases()

Gets the Producer Price Index (PPI) Dates. The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. The PPI is a leading indicator of CPI, and CPI is a leading indicator of inflation.

Returns: array : PPI Dates as timestamps

cpiReleases()

Gets the Consumer Price Index (CPI) Rekease Dates. The Consumer Price Index (CPI) measures changes in the price level of a market basket of consumer goods and services purchased by households. The CPI is a leading indicator of inflation.

Returns: array : CPI Dates as timestamps

csiReleases()

Gets the CSI release dates. The Consumer Sentiment Index (CSI) is a survey of consumer attitudes about the economy and their personal finances. The CSI is a leading indicator of consumer spending.

Returns: array : CSI Dates as timestamps

cciReleases()

Gets the CCI release dates. The Conference Board's Consumer Confidence Index (CCI) is a survey of consumer attitudes about the economy and their personal finances. The CCI is a leading indicator of consumer spending.

Returns: array : CCI Dates as timestamps

nfpReleases()

Gets the NFP release dates. Nonfarm payrolls is an employment report released monthly by the Bureau of Labor Statistics (BLS) that measures the change in the number of employed people in the United States.

Returns: array : NFP Dates as timestamps