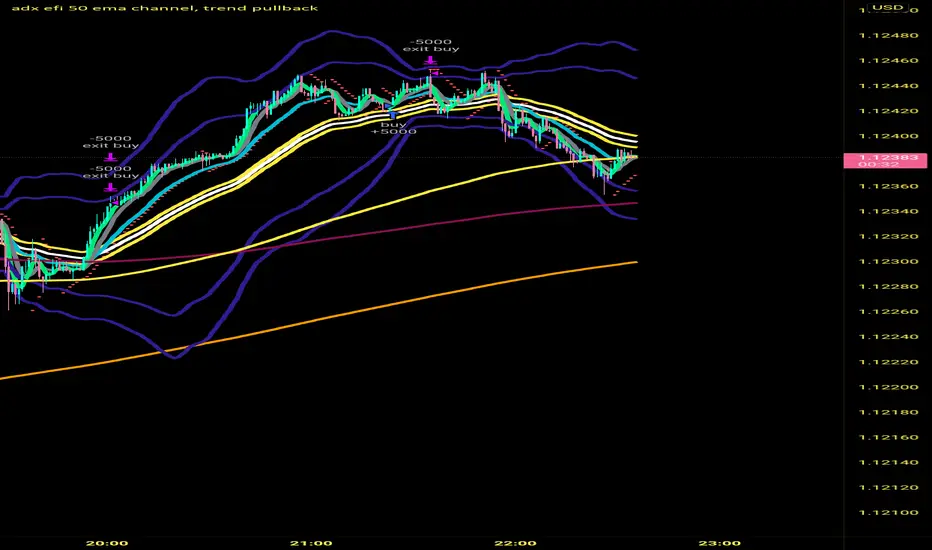

Mix1 : Ema Cross + Trend Channel [Gu5] - BacktestBacktest of the indicator "Mix1: Ema Cross + Trend Channel "

Trend indicator, by the crossing of moving averages

SMA200 with a channel as a filter confirms the trend.

The crossing of two moving averages, give alert only in trend.

استراتيجية Pine Script®