TradeBuilderOverview

TradeBuilder is an ever-growing toolbox that lets you combine and compound any number of bundled indicators and algorithms to create a compound strategy. At launch, we're including two Moving Averages (SMA, EMA), RSI, and Stochastic Oscillator, with many more to come. You can use any combination of indicators, be it just one, two, or all.

Key Concepts

Indicator Integration: Tradebuilder allows the use of Moving Averages, RSI, and Stochastic Oscillators, with customizable parameters for each. More indicators to come.

Mode Selection : Choose between Confirm Trend Mode (using indicators to confirm trends) and Momentum Mode (using indicators to spot reversals).

Trade Flexibility : Offers options for both long and short trades, enabling diverse trading strategies.

Customizable Inputs : Easily toggle indicators on or off and adjust specific settings like periods and thresholds.

Signal Generation : Combines multiple conditions to generate entry and exit signals.

Input Parameters:

Moving Average (MA):

use_ma : Enable this to include the Moving Average in your strategy.

ma_cross_type : Choose between "Close/MA" (price crossing the MA) or "MA/MA" (one MA crossing another).

ma_length : Set the period for the primary MA.

ma_type : Choose between "SMA" (Simple Moving Average) or "EMA" (Exponential Moving Average).

ma_length2 : Set the period for the secondary MA if using the "MA/MA" cross type.

ma_type2 : Set the type for the secondary MA.

Relative Strength Index (RSI):

use_rsi : Enable this to include RSI in your strategy.

rsi_length : Set the period for RSI calculation.

rsi_overbought : Define the overbought level.

rsi_oversold : Define the oversold level.

Stochastic Oscillator:

use_stoch : Enable this to include the Stochastic Oscillator in your strategy.

stoch_k : Set the %K period.

stoch_d : Set the %D period.

stoch_smooth : Define the smoothing factor.

stoch_overbought : Set the overbought level.

stoch_oversold : Set the oversold level.

Confirmation or Momentum Mode:

confirm_trend : Set this to true to use RSI and Stochastic Oscillator to confirm trends (long when above overbought, short when below oversold). Set to false to trade on momentum (short when above overbought, long when below oversold).

Tip: When set to false and used with just momentum oscillators like Stochastic or RSI, it's geared toward scalping as it essentially becomes momentum trading.

Trade Directions:

trade_long : Enable to allow long trades.

trade_short : Enable to allow short trades.

Example Strategy on E-mini S&P 500 Index Futures ( CME_MINI:ES1! ), 1-minute Chart

Let’s say you want to create a strategy to go long when:

A 5-period SMA crosses above a 100-period EMA.

RSI is above 20.

The Stochastic Oscillator is above 95.

Trend Confirmation Mode is on.

For short:

A 5-period SMA crosses below a 100-period EMA.

RSI is below 45.

The Stochastic Oscillator is below 5.

Trend Confirmation Mode is on.

Here’s how you would set it up in Tradebuilder:

use_ma = true

ma_cross_type = "MA/MA"

ma_length = 5

ma_type = "SMA"

ma_length2 = 100

ma_type2 = "EMA"

use_rsi = true

rsi_length = 14

rsi_overbought = 20

rsi_oversold = 45

use_stoch = true

stoch_k = 8

stoch_d = 1

stoch_smooth = 1

stoch_overbought = 95

stoch_oversold = 5

confirm_trend = true

trade_long = true

trade_short = false

Alerts

Here is how to set TradeBuilder alerts: open a TradingView chart, attach TradeBuilder, right-click on chart -> Add Alert. Condition: Symbol (e.g. NQ) >> TradeBuilder >> Open-Ended Alert >> Once Per Bar Close.

Development Roadmap

We plan to add many more compoundable indicators to TradeBuilder over the coming months from all walks of technical analysis, including Volume, Volatility, Trend Detection/Validation, Momentum, Divergences, Chart Patterns, Support/Resistance Analysis. etc.

Trendfollowing

AlgoBuilder [Trend-Following] | FractalystWhat's the strategy's purpose and functionality?

This strategy is designed for both traders and investors looking to rely on and trade based on historical and backtested data using automation. The main goal is to build profitable trend-following strategies that outperform the underlying asset in terms of returns while minimizing drawdown. For example, as for a benchmark, if the S&P 500 (SPX) has achieved an estimated 10% annual return with a maximum drawdown of -57% over the past 20 years, using this strategy with different entry and exit techniques, users can potentially seek ways to achieve a higher Compound Annual Growth Rate (CAGR) while maintaining a lower maximum drawdown.

Although the strategy can be applied to all markets and timeframes, it is most effective on stocks, indices, future markets, cryptocurrencies, and commodities and JPY currency pairs given their trending behaviors.

In trending market conditions, the strategy employs a combination of moving averages and diverse entry models to identify and capitalize on upward market movements. It integrates market structure-based trailing stop-loss mechanisms across different timeframes and provides exit techniques, including percentage-based and risk-reward (RR) based take profit levels.

Additionally, the strategy has also a feature that includes a built-in probability and sentiment function for traders who want to implement probabilities and market sentiment right into their trading strategies.

Performance summary, weekly, and monthly tables enable quick visualization of performance metrics like net profit, maximum drawdown, compound annual growth rate (CAGR), profit factor, average trade, average risk-reward ratio (RR), and more. This aids optimization to meet specific goals and risk tolerance levels effectively.

-----

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

Trading:

1. Trading (1x):

- Designed for traders looking to capitalize on bullish trending markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for active trading with a focus on trend-following and risk management.

- (1x) This mode ensures no stacking of positions, allowing for only one running position or trade at a time.

◓: Mode | %: Risk percentage per trade

2. Trading (2x):

Similar to the 1x mode but allows for two pyramiding entries.

This approach enables traders to increase their position size as the trade moves in their favor, potentially enhancing profits during strong bullish trends.

◓: Mode | %: Risk percentage per trade

3. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes 100% of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully investing in the asset during bullish conditions.

- ◓: Mode | %: Risk not applied (In investing mode, the strategy uses 100% of equity to buy the asset)

-----

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

This comparison filter can be turned on (>/<) or off.

For example, you can set the filter so that MA#1 > MA#2, meaning the first moving average must be above the second one before the script looks for entry conditions. This adds an extra layer of trend confirmation, ensuring that trades are only taken in more favorable market conditions.

MA #1: Fast MA | MA #2: Medium MA | MA #3: Slow MA

⍺: MA Period | Σ: MA Timeframe

-----

What entry modes are used in this strategy? What are the underlying calculations?

The strategy by default uses two different techniques for the entry criteria with user-adjustable left and right bars: Breakout and Fractal.

1. Breakout Entries :

- The strategy looks for pivot high points with a default period of 3.

- It stores the most recent high level in a variable.

- When the price crosses above this most recent level, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot high left bars period | ◨: Pivot high right bars period

2. Fractal Entries :

- The strategy looks for pivot low points with a default period of 3.

- When a pivot low is detected, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot low left bars period | ◨: Pivot low right bars period

By utilizing these entry modes, the strategy aims to capitalize on bullish price movements while ensuring that the necessary conditions are met to validate the entry points.

-----

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

Initial Stop-Loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14).

Example - ATR (14) * 1.5

⍺: ATR period | Σ: ATR Multiplier

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

Example - ADR (14) * 1.5

⍺: ADR period | Σ: ADR Multiplier

Application in Strategy:

- The strategy calculates the current bar's ADR/ATR with a user-defined period.

- It then multiplies the ADR/ATR by a user-defined multiplier to determine the initial stop-loss level.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Trailing Stop-Loss:

One of the key elements of this strategy is its ability to detec buyside and sellside liquidity levels across multiple timeframes to trail the stop-loss once the trade is in running profits.

By utilizing this approach, the strategy allows enough room for price to run.

There are two built-in trailing stop-loss (SL) options you can choose from while in a trade:

1. External Trailing Stop-Loss:

- Uses sell-side liquidity to trail your stop-loss, allowing price to consolidate before continuation. This method is less aggressive and provides more room for price fluctuations.

Example - External - Wick below the trailing SL - 12H trailing timeframe

⍺: Exit type | Σ: Trailing stop-loss timeframe

2. Internal Trailing Stop-Loss:

- Uses the most recent swing low with a period of 2 to trail your stop-loss. This method is more aggressive compared to the external trailing stop-loss, as it tightens the stop-loss closer to the current price action.

Example - Internal - Close below the trailing SL - 6H trailing timeframe

⍺: Exit type | Σ: Trailing stop-loss timeframe

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

-----

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

- You can choose to set a break-even level at which your initial stop-loss moves to the entry price as soon as it hits, and your trailing stop-loss gets activated (if enabled).

- You can select either a percentage (%) or risk-to-reward (RR) based break-even, allowing you to set your break-even level as a percentage amount above the entry price or based on RR.

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

The underlying calculations involve determining the price levels at which these actions are triggered. For break-even, it moves the initial stop-loss to the entry price and activate the trailing stop-loss once the break-even level is reached.

For TP1 and TP2, it's specifying the price levels at which the position is partially or fully closed based on the chosen method (percentage or RR) above the entry price.

These calculations are crucial for managing risk and optimizing profitability in the strategy.

⍺: BE/TP type (%/RR) | Σ: how many RR/% above the current price

-----

What's the ADR filter? What does it do? What are the underlying calculations?

The Average Day Range (ADR) measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

The period of the ADR filter used in this strategy is tied to the same period you've used for your initial stop-loss.

Users can define the minimum ADR they want to be met before the script looks for entry conditions.

ADR Bias Filter:

- Compares the current bar ADR with the ADR (Defined by user):

- If the current ADR is higher, it indicates that volatility has increased compared to ADR (DbU).(⬆)

- If the current ADR is lower, it indicates that volatility has decreased compared to ADR (DbU).(⬇)

Calculations:

1. Calculate ADR:

- Average the high prices over the specified period.

- Average the low prices over the same period.

- Find the difference between these average values in %.

2. Current ADR vs. ADR (DbU):

- Calculate the ADR for the current bar.

- Calculate the ADR (DbU).

- Compare the two values to determine if volatility has increased or decreased.

By using the ADR filter, the strategy ensures that trades are only taken in favorable market conditions where volatility meets the user's defined threshold, thus optimizing entry conditions and potentially improving the overall performance of the strategy.

>: Minimum required ADR for entry | %: Current ADR comparison to ADR of 14 days ago.

-----

What's the probability filter? What are the underlying calculations?

The probability filter is designed to enhance trade entries by using buyside liquidity and probability analysis to filter out unfavorable conditions.

This filter helps in identifying optimal entry points where the likelihood of a profitable trade is higher.

Calculations:

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside, Sellside and Equilibrium levels.

3. Understanding probability calculations

1. Upon the formation of a new range, the script waits for the price to reach and tap into equilibrium or the 50% level. Status: "⏸" - Inactive

2. Once equilibrium is tapped into, the equilibrium status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

5. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

Example - BSL > 50%

-----

What's the sentiment Filter? What are the underlying calculations?

Sentiment filter aims to calculate the percentage level of bullish or bearish fluctuations within equally divided price sections, in the latest price range.

Calculations:

This filter calculates the current sentiment by identifying the highest swing high and the lowest swing low, then evenly dividing the distance between them into percentage amounts. If the price is above the 50% mark, it indicates bullishness, whereas if it's below 50%, it suggests bearishness.

Sentiment Bias Identification:

Bullish Bias: The current price is trading above the 50% daily range.

Bearish Bias: The current price is trading below the 50% daily range.

Example - Sentiment Enabled | Bullish degree above 50% | Bullish sentimental bias

>: Minimum required sentiment for entry | %: Current sentimental degree in a (Bullish/Bearish) sentimental bias

-----

What's the range length Filter? What are the underlying calculations?

The range length filter identifies the price distance between buyside and sellside liquidity levels in percentage terms. When enabled, the script only looks for entries when the minimum range length is met. This helps ensure that trades are taken in markets with sufficient price movement.

Calculations:

Range Length (%) = ( ( Buyside Level − Sellside Level ) / Current Price ) ×100

Range Bias Identification:

Bullish Bias: The current range price has broken above the previous external swing high.

Bearish Bias: The current range price has broken below the previous external swing low.

Example - Range length filter is enabled | Range must be above 5% | Price must be in a bearish range

>: Minimum required range length for entry | %: Current range length percentage in a (Bullish/Bearish) range

-----

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

Increased Flexibility: The filter provides increased flexibility, allowing traders to adapt the strategy to their specific needs and preferences.

Example - Day filter | Session Filter

θ: Session time | Exchange time-zone

-----

What tables are available in this script?

Table Type:

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades, Compound Annual Growth Rate (CAGR), MAR and more.

CAGR: It calculates the 'Compound Annual Growth Rate' first and last taken trades on your chart. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two strategies. Since it annualizes values, it requires a minimum 4H timeframe to display the CAGR value. annualizing returns over smaller periods of times doesn't produce very meaningful figures.

MAR: Measure of return adjusted for risk: CAGR divided by Max Drawdown. Indicates how comfortable the system might be to trade. Higher than 0.5 is ideal, 1.0 and above is very good, and anything above 3.0 should be considered suspicious and you need to make sure the total number of trades are high enough by running a Deep Backtest in strategy tester. (available for TradingView Premium users.)

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most trend-following successful strategies have a percent profitability of 15-40% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- OFF: Hides the performance table.

Labels:

- OFF: Hides labels in the performance table.

- PnL: Shows the profit and loss of each trade individually, providing detailed insights into the performance of each trade.

- Range: Shows the range length and Average Day Range (ADR), offering additional context about market conditions during each trade.

Profit Color:

- Allows users to set the color for representing profit in the performance table, helping to quickly distinguish profitable periods.

Loss Color:

- Allows users to set the color for representing loss in the performance table, helping to quickly identify loss-making periods.

These customizable tables provide traders with flexible and detailed performance analysis, aiding in better strategy evaluation and optimization.

-----

User-input styles and customizations:

To facilitate studying historical data, all conditions and rules can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

-----

How to Use This Algobuilder to Create a Profitable Edge and System:

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker or prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 100 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade value is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, MAR (Mar Ratio), CAGR (Compound Annual Growth Rate), and net profit with minimum drawdown. Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

Automation:

- Once you’re confident in your strategy, you can use the automation section to connect the algorithm to your broker or prop firm.

- Trade a fully automated and backtested trading strategy, allowing for hands-free execution and management.

-----

What makes this strategy original?

1. Incorporating direct integration of probabilities into the strategy.

2. Leveraging market sentiment to construct a profitable approach.

3. Utilizing built-in market structure-based trailing stop-loss mechanisms across various timeframes.

4. Offering both investing and trading strategies, facilitating optimization from different perspectives.

5. Automation for efficient execution.

6. Providing a summary table for instant access to key parameters of the strategy.

-----

How to use automation?

For Traders:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Enter your PineConnector License ID in the designated field.

3. Specify the desired risk level.

4. Provide the Metatrader symbol.

5. Check for chart updates to ensure the automation table appears on the top right corner, displaying your License ID, risk, and symbol.

6. Set up an alert with the strategy selected as Condition and the Message as {{strategy.order.alert_message}}.

7. Activate the Webhook URL in the Notifications section, setting it as the official PineConnector webhook address.

8. Double-check all settings on PineConnector to ensure the connection is successful.

9. Create the alert for entry/exit automation.

For Investors:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Choose "Investing" in the user-input settings.

3. Create an alert with a specified name.

4. Customize the notifications tab to receive alerts via email.

5. Buying/selling alerts will be triggered instantly upon entry or exit order execution.

----

Strategy Properties

This script backtest is done on 4H COINBASE:BTCUSD , using the following backtesting properties:

Balance: $5000

Order Size: 10% of the equity

Risk % per trade: 1%

Commission: 0.04% (Default commission percentage according to TradingView competitions rules)

Slippage: 75 ticks

Pyramiding: 2

-----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Long EMA Strategy with Advanced Exit OptionsThis strategy is designed for traders seeking a trend-following system with a focus on precision and adaptability.

**Core Strategy Concept**

The essence of this strategy lies in use of Exponential Moving Averages (EMAs) to identify potential long (buy) positions based on the relative positions of short-term, medium-term, and long-term EMAs. The use of EMAs is a classic yet powerful approach to trend detection, as these indicators smooth out price data over time, emphasizing the direction of recent price movements and potentially signaling the beginning of new trends.

**Customizable Parameters**

- **EMA Periods**: Users can define the periods for three EMAs - long-term, medium-term, and short-term - allowing for a tailored approach to capture trends based on individual trading styles and market conditions.

- **Volatility Filter**: An optional Average True Range (ATR)-based volatility filter can be toggled on or off. When activated, it ensures that trades are only entered when market volatility exceeds a user-defined threshold, aiming to filter out entries during low-volatility periods which are often characterized by indecisive market movements.

- **Trailing Stop Loss**: A trailing stop loss mechanism, expressed as a percentage of the highest price achieved since entry, provides a dynamic way to manage risk by allowing profits to run while cutting losses.

- **EMA Exit Condition**: This advanced exit option enables closing positions when the short-term EMA crosses below the medium-term EMA, serving as a signal that the immediate trend may be reversing.

- **Close Below EMA Exit**: An additional exit condition, which is disabled by default, allows positions to be closed if the price closes below a user-selected EMA. This provides an extra layer of flexibility and risk management, catering to traders who prefer to exit positions based on specific EMA thresholds.

**Operational Mechanics**

Upon activation, the strategy evaluates the current price in relation to the set EMAs. A long position is considered when the current price is above the long-term EMA, and the short-term EMA is above the medium-term EMA. This setup aims to identify moments where the price momentum is strong and likely to continue.

The strategy's versatility is further enhanced by its optional settings:

- The **Volatility Filter** adjusts the sensitivity of the strategy to market movements, potentially improving the quality of the entries during volatile market conditions.

The Average True Range (ATR) is a key component of this filter, providing a measure of market volatility by calculating the average range between the high and low prices over a specified number of periods. Here's how you can adjust the volatility filter settings for various market conditions, focusing on filtering out low-volatility markets:

Setting Examples for Volatility Filter

1. High Volatility Markets (e.g., Cryptocurrencies, Certain Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: Setting the multiplier to a lower value, such as 1.0 or 1.2, can be beneficial in high-volatility markets. This sensitivity allows the strategy to react to volatility changes more quickly, ensuring that you're entering trades during periods of significant movement.

2. Medium Volatility Markets (e.g., Major Equity Indices, Medium-Volatility Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: A multiplier of 1.5 (default) is often suitable for medium volatility markets. It provides a balanced approach, ensuring that the strategy filters out low-volatility conditions without being overly restrictive.

3. Low Volatility Markets (e.g., Some Commodities, Low-Volatility Forex Pairs):

ATR Periods: Increasing the ATR period to 20 or 25 can smooth out the volatility measure, making it less sensitive to short-term fluctuations. This adjustment helps in focusing on more significant trends in inherently stable markets.

ATR Multiplier: Raising the multiplier to 2.0 or even 2.5 increases the threshold for volatility, effectively filtering out low-volatility conditions. This setting ensures that the strategy only triggers trades during periods of relatively higher volatility, which are more likely to result in significant price movements.

How to Use the Volatility Filter for Low-Volatility Markets

For traders specifically interested in filtering out low-volatility markets, the key is to adjust the ATR Multiplier to a higher level. This adjustment increases the threshold required for the market to be considered sufficiently volatile for trade entries. Here's a step-by-step guide:

Adjust the ATR Multiplier: Increase the ATR Multiplier to create a higher volatility threshold. A multiplier of 2.0 to 2.5 is a good starting point for very low-volatility markets.

Fine-Tune the ATR Periods: Consider lengthening the ATR calculation period if you find that the strategy is still entering trades in undesirable low-volatility conditions. A longer period provides a more averaged-out measure of volatility, which might better suit your needs.

Monitor and Adjust: Volatility is not static, and market conditions can change. Regularly review the performance of your strategy in the context of current market volatility and adjust the settings as necessary.

Backtest in Different Conditions: Before applying the strategy live, backtest it across different market conditions with your adjusted settings. This process helps ensure that your approach to filtering low-volatility conditions aligns with your trading objectives and risk tolerance.

By fine-tuning the volatility filter settings according to the specific characteristics of the market you're trading in, you can enhance the performance of this strategy

- The **Trailing Stop Loss** and **EMA Exit Conditions** provide two layers of exit strategies, focusing on capital preservation and profit maximization.

**Visualizations**

For clarity and ease of use, the strategy plots the three EMAs and, if enabled, the ATR threshold on the chart. These visual cues not only aid in decision-making but also help in understanding the market's current trend and volatility state.

**How to Use**

Traders can customize the EMA periods to fit their trading horizon, be it short, medium, or long-term trading. The volatility filter and exit options allow for further customization, making the strategy adaptable to different market conditions and personal risk tolerance levels.

By offering a blend of trend-following principles with advanced risk management features, this strategy aims to cater to a wide range of trading styles, from cautious to aggressive. Its strength lies in its flexibility, allowing traders to fine-tune settings to their specific needs, making it a potentially valuable tool in the arsenal of any trader looking for a disciplined approach to navigating the markets.

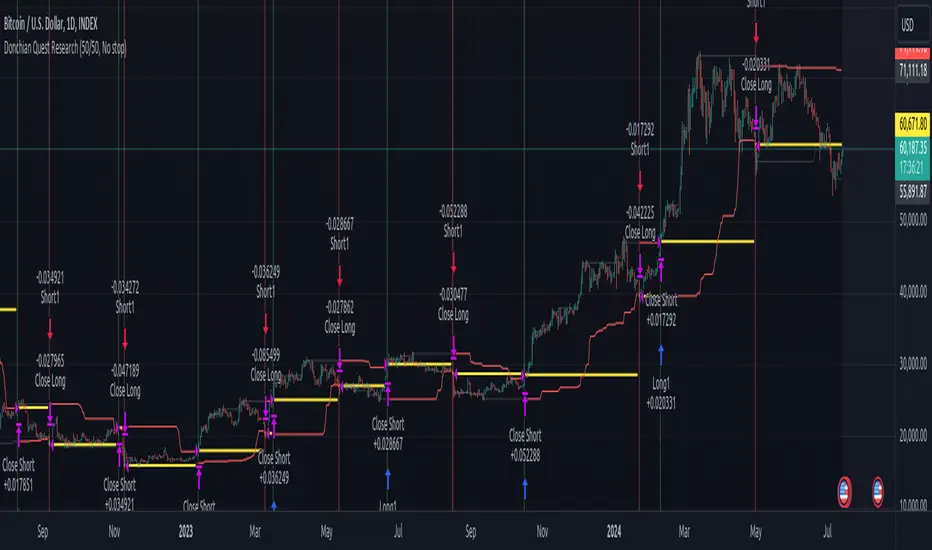

Donchian Quest Research// =================================

Trend following strategy.

// =================================

Strategy uses two channels. One channel - for opening trades. Second channel - for closing.

Channel is similar to Donchian channel, but uses Close prices (not High/Low). That helps don't react to wicks of volatile candles (“stop hunting”). In most cases openings occur earlier than in Donchian channel. Closings occur only for real breakout.

// =================================

Strategy waits for beginning of trend - when price breakout of channel. Default length of both channels = 50 candles.

Conditions of trading:

- Open Long: If last Close = max Close for 50 closes.

- Close Long: If last Close = min Close for 50 closes.

- Open Short: If last Close = min Close for 50 closes.

- Close Short: If last Close = max Close for 50 closes.

// =================================

Color of lines:

- black - channel for opening trade.

- red - channel for closing trade.

- yellow - entry price.

- fuchsia - stoploss and breakeven.

- vertical green - go Long.

- vertical red - go Short.

- vertical gray - close in end, don't trade anymore.

// =================================

Order size calculated with ATR and volatility.

You can't trade 1 contract in BTC and 1 contract in XRP - for example. They have different price and volatility, so 1 contract BTC not equal 1 contract XRP.

Script uses universal calculation for every market. It is based on:

- Risk - USD sum you ready to loss in one trade. It calculated as percent of Equity.

- ATR indicator - measurement of volatility.

With default setting your stoploss = 0.5 percent of equity:

- If initial capital is 1000 USD and used parameter "Permit stop" - loss will be 5 USD (0.5 % of equity).

- If your Equity rises to 2000 USD and used parameter "Permit stop"- loss will be 10 USD (0.5 % of Equity).

// =================================

This Risk works only if you enable “Permit stop” parameter in Settings.

If this parameter disabled - strategy works as reversal strategy:

⁃ If close Long - channel border works as stoploss and momentarily go Short.

⁃ If close Short - channel border works as stoploss and momentarily go Long.

Channel borders changed dynamically. So sometime your loss will be greater than ‘Risk %’. Sometime - less than ‘Risk %’.

If this parameter enabled - maximum loss always equal to 'Risk %'. This parameter also include breakeven: if profit % = Risk %, then move stoploss to entry price.

// =================================

Like all trend following strategies - it works only in trend conditions. If no trend - slowly bleeding. There is no special additional indicator to filter trend/notrend. You need to trade every signal of strategy.

Strategy gives many losses:

⁃ 30 % of trades will close with profit.

⁃ 70 % of trades will close with loss.

⁃ But profit from 30% will be much greater than loss from 70 %.

Your task - patiently wait for it and don't use risky setting for position sizing.

// =================================

Recommended timeframe - Daily.

// =================================

Trend can vary in lengths. Selecting length of channels determine which trend you will be hunting:

⁃ 20/10 - from several days to several weeks.

⁃ 20/20 or 50/20 - from several weeks to several months.

⁃ 50/50 or 100/50 or 100/100 - from several months to several years.

// =================================

Inputs (Settings):

- Length: length of channel for trade opening/closing. You can choose 20/10, 20/20, 50/20, 50/50, 100/50, 100/100. Default value: 50/50.

- Permit Long / Permit short: Longs are most profitable for this strategy. You can disable Shorts and enable Longs only. Default value: permit all directions.

- Risk % of Equity: for position sizing used Equity percent. Don't use values greater than 5 % - it's risky. Default value: 0.5%.

⁃ ATR multiplier: this multiplier moves stoploss up or down. Big multiplier = small size of order, small profit, stoploss far from entry, low chance of stoploss. Small multiplier = big size of order, big profit, stop near entry, high chance of stoploss. Default value: 2.

- ATR length: number of candles to calculate ATR indicator. It used for order size and stoploss. Default value: 20.

- Close in end - to close active trade in the end (and don't trade anymore) or leave it open. You can see difference in Strategy Tester. Default value: don’t close.

- Permit stop: use stop or go reversal. Default value: without stop, reversal strategy.

// =================================

Properties (Settings):

- Initial capital - 1000 USD.

- Script don't uses 'Order size' - you need to change 'Risk %' in Inputs instead.

- Script don't uses 'Pyramiding'.

- 'Commission' 0.055 % and 'Slippage' 0 - this parameters are for crypto exchanges with perpetual contracts (for example Bybit). If use on other markets - set it accordingly to your exchange parameters.

// =================================

Big dataset used for chart - 'BITCOIN ALL TIME HISTORY INDEX'. It gives enough trades to understand logic of script. It have several good trends.

// =================================

SOFEX Strong Volatility Trend Follower + BacktestingWhat is the SOFEX Strong Volatility Trend Follower + Backtesting script?

🔬 Trading Philosophy

This script is trend-following, attempting to avoid choppy markets.

It has been developed for Bitcoin and Ethereum trading, on 1H timeframe.

The strategy does not aim to make a lot of trades, or to always remain in a position and switch from long to short. Many times there is no direction and the market is in "random walk mode", and chasing trades is futile.

Expectations of performance should be realistic.

The script focuses on a balanced take-profit to stop-loss ratio. In the default set-up of the script, that is a 2% : 2% (1:1) ratio. A relatively low stop loss and take profit build onto the idea that positions should be exited promptly. There are many options to edit these values, including enabling trailing take profit and stop loss. Traders can also completely turn off TP and SL levels, and rely on opposing signals to exit and enter new trades.

Extreme scenarios can happen on the cryptocurrency markets, and disabling stop-loss levels completely is not recommended. The position size should be monitored since all of it is at risk with no stop-loss.

⚙️ Logic of the indicator

The Strong Volatility Trend Follower indicator aims at evading ranging market conditions. It does not seek to chase volatile, yet choppy markets. It aims at aggressively following confirmed trends. The indicator works best during strong, volatile trends, however, it has the downside of entering trades at trend tops or bottoms.

This indicator also leverages proprietary adaptive moving averages to identify and follow strong trend volatility effectively. Furthermore, it uses the Average Directional Index, Awesome Oscillator, ATR and a modified version of VWAP, to categorize trends into weak or strong ones. The VWAP indicator is used to identify the monetary (volume) inflow into a given trend, further helping to avoid short-term manipulations. It also helps to distinguish choppy-market volatility with a trending market one.

📟 Parameters Menu

The script has a comprehensive parameter menu:

Preset Selection : Choose between Bitcoin or Ethereum presets to tailor the indicator to your preferred cryptocurrency market.

Indicator Sensitivity Parameter : Adjust the sensitivity to adapt the indicator, particularly to make it seek higher-strength trends.

Indicator Signal Direction : Set the signal direction as Long, Short, or Both, depending on your preference.

Exit of Signals : You have options regarding Take-Profit (TP) and Stop-Loss (SL) levels. Enable TP/SL levels to exit trades at predetermined levels, or disable them to rely on direction changes for exits. Be aware that removing stop losses can introduce additional risk, and position sizing should be carefully monitored.

By enabling Trailing TP/SL, the system switches to a trailing approach, allowing you to:

- Place an initial customizable SL.

- Specify a level (%) for the Trailing SL to become active.

- When the activation level is reached, the system moves the trailing stop by a given Offset (%).

Additionally, you can enable exit at break-even, where the system places an exit order when the trail activation level is reached, accounting for fees and slippage.

Alert Messages : Define the fields for alert messages based on specific conditions. You can set up alerts to receive email, SMS, and in-app notifications. If you use webhooks for alerts, exercise caution, as these alerts can potentially execute trades without human supervision.

Backtesting : Default backtesting parameters are set to provide realistic backtesting performance:

- 0.04% Commission per trade (for both entries and exits)

- 3 ticks Slippage (highly dependent on exchange)

- Initial capital of $1000

- Order size of $1000

While the order size is equal to the initial capital, the script employs a 2% stop-loss order to limit losses and attempts to prevent risky trades from creating big losses. The order size is a set dollar value, so that the backtesting performance is linear, instead of using % of capital which may result in unrealistic backtesting performance.

Risk Disclaimer

Please be aware that backtesting results, while valuable for statistical overview, do not guarantee future performance in any way. Cryptocurrency markets are inherently volatile and risky. Always trade responsibly and do not risk more than you can afford to lose.

Blockunity Divinetrend (BDT)A formidable trend-following indicator, based on an ATR combined with a trailing stop mechanism. Divinetrend’s aim is to offer a simple and efficient alternative to Supertrend, another highly reputed indicator of the same type. It comes with a trading strategy that can be activated in its parameters. You can also change a number of design parameters.

Divinetrend is pretty straightforward in its approach. It calculates a base moving average taking into account the asset’s volatility, multiplies it with an ATR, then displays a line representing a trailing stop. When a red line is broken, the asset is considered to be moving back into an uptrend. Inversely, when a green line is broken, a bearish signal is sent. In the parameters, you can also activate a trend contestation period. If this parameter is activated, the price must have been trending for at least 5 days for the trend change to be validated.

Usage Advice

We recommend that you do not use this indicator with a time unit of less than 2 hours. Ideally in 4 hours or daily, or even 3 days. Otherwise, there’s nothing special about the use of this indicator. We still recommend that you use your logarithmic chart for a better visualization, but this is optional.

This indicator was designed in particular for the crypto market, but it also works on traditional market assets.

The Different Signals

Divinetrend gives buy and sell signals based on trailing stop line breaks and trend orientation. In particular, it can be used for trend identification and following. If the Contested Trend option is activated in the settings, the indicator will also display a contested period in blue. In this case, it is necessary to wait 5 days for the trend to be validated.

Integrated Strategy

In addition, a trading strategy is integrated into the Divinetrend indicator. This can be activated in the parameters. This is mainly there to see the results and the relevance of the indicator in the TradingView Strategy Tester. We do not recommend using it alone. As this strategy is used to study the indicator's performance, we use the following default parameters: An initial capital of 2,000 USDT with 100% of equity in order size. In other words, we'll bet the entire portfolio on each trade. To do this, we use a default stop loss of 10%, to avoid risking heavy losses. We also use a commission of 0.01% and a slippage of 3 ticks to reflect more reality.

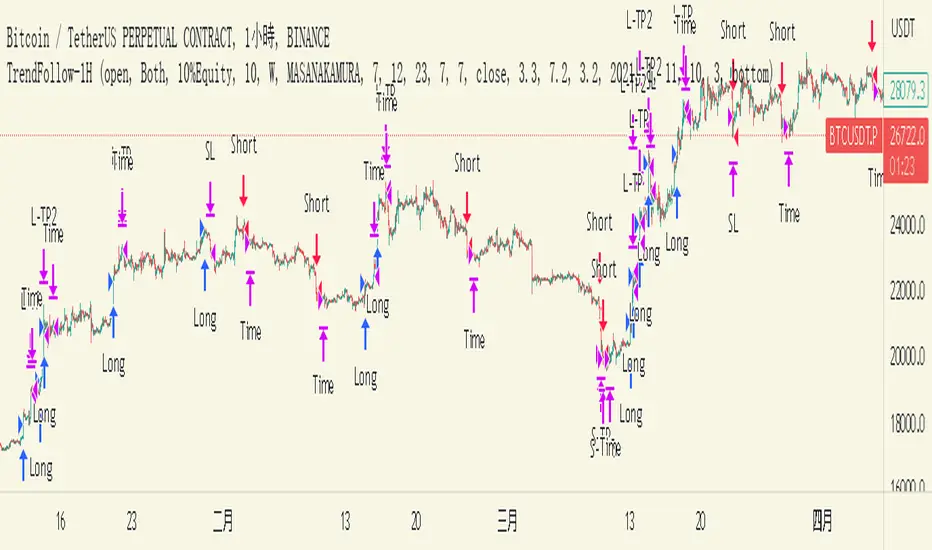

TrendFollow-1HThis is a trading strategy specially used on btcusdtperp in binance 1H chart

The most important part of this strategy is to use Support and Resistance with trading volume

Auxiliary indicators are include Directional Movement Index, trading volume, Commodity Channel Index,volume-weighted average price,Range Filter

Why is it not applicable to other trading varieties or exchanges?

Because the activity of each trading target is different from the trading volume, this strategy is very focused on the change of trading volume, so it may not be applicable to every trading variety

The idea of this strategy is to chase when the trend in the market is clear

Determine whether to break support or resistance to identify trends

But the market is full of false breakouts

Therefore, trading volume is an important indicator for judging the true and false.

Therefore, when the price breaks through support or resistance, accompanied by a huge trading volume, and forms a resonance with auxiliary indicators, the strategy will follow the trend, a time stop loss is also set. After entering the market, if there is no immediate profit to the stop profit, you will leave the market first.

But the market is always random, so the profit and loss ratio must be taken into account

Use a fixed stop loss space in exchange for a larger profit space, and ensure that the expected value is positive to make stable profits in the market

Therefore, this strategy uses 3.2% stop loss, 3.3% Take profit1 and 7.2% take profit2

About 1.5:1 profit and loss ratio to ensure positive expected value

Because the market has a clear trend only about 10% of the time

So the trading frequency of this strategy is very low

According to the backtest of up to 2021-01-01 till now , it takes about 5 days to make a transaction

User can choose their own leverage to obtain higher returns. But be sure to prioritize risk.

In order to prevent you from using this strategy without knowing it, the trading date of this strategy is only executed until the release date, and positions will not be opened and closed for subsequent markets.

You can contact me if you want to know more about this strategy

這是專門用於幣安1H圖表中btcusdtperp的交易策略

本策略最重要的部分是將支撐和阻力與交易量一起使用

輔助指標包括ADX,成交量,CCI,VWAP,Range Filter等

為什麼不適用於其他交易品種或交易所?

由於每個交易標的的活躍度與交易量不同,本策略非常注重交易量的變化,因此不一定適用於每個交易品種

這個策略的方法是在趨勢明朗的時候進行趨勢跟隨

確定是否打破支撐或阻力以識別趨勢

但市場充滿假突破

因此,成交量是判斷真假的重要指標。

當價格突破支撐位或阻力位,伴隨著巨大的成交量,並與輔助指標形成共振時,策略會順勢而為,同時設置時間止損。進場後,如果沒有立即獲利到止盈,就離場。

但市場總是隨機的,所以必須考慮盈虧比

用固定的止損空間換取更大的盈利空間,保證預期值為正,才能在市場中穩定獲利

因此,該策略使用 3.2% 止損、3.3% 止盈1 和 7.2% 止盈2

約1.5:1盈虧比,確保正期望值

因為市場只有大約 10% 的時間有明顯的趨勢

所以這個策略的交易頻率很低

根據2021-01-01至今的回測,交易頻率大約5天一次

用戶也可以選擇適合自己的槓桿以獲得更高的收益。但一定要優先考慮風險。

為防止您在不知情的情況下使用本策略,本策略的運行交易的日期僅至2023-05-30止,後續日期將不開倉和平倉。

如果您想了解更多有關此策略的信息,可以聯繫我。

Lorentzian Classification Strategy Based in the model of Machine learning: Lorentzian Classification by @jdehorty, you will be able to get into trending moves and get interesting entries in the market with this strategy. I also put some new features for better backtesting results!

Backtesting context: 2022-07-19 to 2023-04-14 of US500 1H by PEPPERSTONE. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

Machine learning: Lorentzian Classification by @jdehorty

One Ema of 200 periods for identifying the trend

Supertrend indicator as a filter for some exits

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is above 200 Ema

Lorentzian Classification indicates a buying signal

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 1:1 and take profit of 3:1 where half position will be closed. This will be showed as buy.

The other half will be closed when the model indicates a selling signal or Supertrend indicator gives a bearish signal. This will be showed as cl buy.

For shorts:

Close price is under 200 Ema

Lorentzian Classification indicates a selling signal

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 1:1 and take profit of 3:1 where half position will be closed. This will be showed as sell.

The other half will be closed when the model indicates a buying signal or Supertrend indicator gives a bullish signal. This will be showed as cl sell.

Risk management

To calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss or last swing for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss or last swing is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

> In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

> You can also choose a fixed amount, so you will have to activate fixed amount in risk management for trades and set the fixed amount for backtesting.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, a table of some stats from backtesting, etc.

You will find the settings for risk management at the end of the script if you want to change something or trying new values for other assets for backtesting.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

I also added a function for backtesting if you had added or withdrawn money frequently:

Adding money: You can choose how often you want to add money (Monthly, yearly, daily or weekly). Then a fixed amount of money and activate or deactivate this function

Withdraw money: You can choose if you want to withdraw a fixed amount or a percentage of earnings. Then you can choose a fixed amount of money, the period of time and activate or deactivate this function. Also, the percentage of earnings if you choosed this option.

Some other assets where strategy has worked

BTCUSD 4H, 1D

ETHUSD 4H, 1D

BNBUSD 4H

SPX 1D

BANKNIFTY 4H, 15 min

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!. If you have problems loading the script reduce max bars back number in general settings

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

Please, visit the post from @jdehorty called Machine Learning: Lorentzian Classification for a better understanding of his script!

Any support and boosts will be well received. If you have any question, do not doubt to ask!

Strategy for UT Bot Alerts indicator Using the UT Bot alerts indicator by @QuantNomad, this strategy was designed for showing an example of how this indicator could be used, also, it has the goal to help some people from a group that use to use this indicator for their trading. Under any circumstance I recommend to use it without testing it before in real time.

Backtesting context: 2020-02-05 to 2023-02-25 of BTCUSD 4H by Tvc. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

UT Bot Alerts indicator by Quantnomad

One Ema of 200 periods for indicate the trend

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is higher than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as buy (open long position)

The other half will be closed when close price is lower than Atr and Ema from UT Bot cross under Atr. This will be showed as cl buy (close long position)

For shorts:

Close price is lower than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as sell (open short position)

The other half will be closed when close price is higher than Atr and Ema from UT Bot cross over Atr. This will be showed as cl sell (close short position)

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

---> Do not forget to deactivate Trades on chart option in style settings for a cleaner look of the chart <---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

---> The strategy can still be improved, you can change some parameters depending of the asset and timeframe like risk/reward for taking profits, for break even, also the main parameters of the UT Bot Alerts <----

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

Rocket Grid Algorithm - The Quant ScienceThe Rocket Grid Algorithm is a trading strategy that enables traders to engage in both long and short selling strategies. The script allows traders to backtest their strategies with a date range of their choice, in addition to selecting the desired strategy - either SMA Based Crossunder or SMA Based Crossover.

The script is a combination of trend following and short-term mean reversing strategies. Trend following involves identifying the current market trend and riding it for as long as possible until it changes direction. This type of strategy can be used over a medium- to long-term time horizon, typically several months to a few years.

Short-term mean reversing, on the other hand, involves taking advantage of short-term price movements that deviate from the average price. This type of strategy is usually applied over a much shorter time horizon, such as a few days to a few weeks. By rapidly entering and exiting positions, the strategy seeks to capture small, quick gains in volatile market conditions.

Overall, the script blends the best of both worlds by combining the long-term stability of trend following with the quick gains of short-term mean reversing, allowing traders to potentially benefit from both short-term and long-term market trends.

Traders can configure the start and end dates, months, and years, and choose the length of the data they want to work with. Additionally, they can set the percentage grid and the upper and lower destroyers to manage their trades effectively. The script also calculates the Simple Moving Average of the chosen data length and plots it on the chart.

The trigger for entering a trade is defined as a crossunder or crossover of the close price with the Simple Moving Average. Once the trigger is activated, the script calculates the total percentage of the side and creates a grid range. The grid range is then divided into ten equal parts, with each part representing a unique grid level. The script keeps track of each grid level, and once the close price reaches the grid level, it opens a trade in the specified direction.

The equity management strategy in the script involves a dynamic allocation of equity to each trade. The first order placed uses 10% of the available equity, while each subsequent order uses 1% less of the available equity. This results in the allocation of 9% for the second order, 8% for the third order, and so on, until a maximum of 10 open trades. This approach allows for risk management and can help to limit potential losses.

Overall, the Rocket Grid Algorithm is a flexible and powerful trading strategy that can be customized to meet the specific needs of individual traders. Its user-friendly interface and robust backtesting capabilities make it an excellent tool for traders looking to enhance their trading experience.

Simple SuperTrend Strategy for BTCUSD 4HHello guys!, If you are a swing trader and you are looking for a simple trend strategy, you should check this one. Based in the supertrend indicator, this strategy will help you to catch big movements in BTCUSD 4H and avoid losses as much as possible in consolidated situations of the market

This strategy was designed for BTCUSD in 4H timeframe

Backtesting context: 2020-01-02 to 2023-01-05 (The strategy has also worked in previous years)

Trade conditions:

Rules are actually simple, the most important thing is the risk and position management of this strategy

For long:

Once Supertrend changes from a downtrend to a uptrend, you enter into a long position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Now, just will be there two situations:

Once Supertrend changes from a uptrend to a downtrend, you close the other half of the initial long position.

If price goes againts the position, the position will be closed due to breakeven.

For short:

Once Supertrend changes from a uptrend to a downtrend, you enter into a short position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Like in the long position, just will be there two situations:

Once Supertrend changes from a downtrend to a uptrend, you close the other half of the initial short position.

If price goes againts the position, the position will be closed due to breakeven.

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, supertrend or positions.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

Signals meanings:

L for long position. CL for close long position.

S for short position. CS for close short position.

Tp for take profit (it also appears when the position is closed due to stop loss, this due to the script uses two kind of positions)

Exit due to break even or due to stop loss

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

The amount of trades closed in the backtest are not exactly the real ones. If you want to know the real ones, go to settings and change % of trade for first take profit to 100 for getting the real ones. In the backtest, the real amount of opened trades was of 194.

Indicators used:

Supertrend

Atr stop loss by garethyeo

This is the fist strategy that I publish in tradingview, I will be glad with you for any suggestion, support or advice for future scripts. Do not doubt in make any question you have and if you liked this content, leave a boost. I plan to bring more strategies and useful content for you!

EURUSD COT Trend StrategyThis is a long term/investment type of strategy designed to have a good idea about where the big trend direction is headed.

Its logic, its made entirely on the COT report, mainly from looking into the net non comercial positions aka the speculators.

For bullish trend we look that the difference between long non comercial vs short non comercial is higher than 0

For bearish trend we look that the difference between long non comercial vs short non comercial is lower than 0.

This is mainly as an educational tool, for a full strategy, I recommend implement other things into it, like technical analysis or risk management.

If you have any questions, please let me know !

Trend Following based on Trend ConfidenceThis is a Trend Following strategy based on the Trend Confidence indicator.