Triple VWAP: Anchored# Triple VWAP: Anchored + Last 2 Sessions

## 📊 Overview

**Triple VWAP** is a professional-grade Volume Weighted Average Price (VWAP) indicator designed for serious traders who need multi-timeframe volume analysis on a single chart. This indicator combines three powerful VWAP calculations: a custom **Anchored VWAP** from any historical date, a real-time **Current Session VWAP**, and **Previous Session VWAP** reference levels—all with configurable standard deviation bands.

Perfect for intraday traders, swing traders, and institutional-level analysis on Indian markets (Nifty, BankNifty) and global instruments.

***

## ✨ Key Features

### 🎯 Three Independent VWAP Calculations

**📍 Anchored VWAP (Long-term Reference)**

- Anchor VWAP from any specific date and time (year, month, day, hour, minute)

- Ideal for tracking price action from significant market events, earnings, or trend reversals

- Maintains accumulation from your chosen anchor point throughout the entire timeframe

**📅 Current Session VWAP (Real-Time)**

- Automatically resets at the start of each trading day

- Calculates dynamically as new bars form during the session

- Shows institutional trading levels and intraday fair value

**📆 Previous Session VWAP (Reference Levels)**

- Displays yesterday's final VWAP as horizontal reference lines

- Helps identify support/resistance zones from prior session

- Useful for gap analysis and opening range strategies

### 📐 Standard Deviation Bands

Each VWAP calculation includes optional standard deviation bands:

- **±1 SD** - Identifies normal price deviation zones

- **±2 SD** - Marks extreme price movements (high probability reversal zones)

- **±3 SD** - Ultra-extreme levels (rare price extensions)

Configure which SD levels to display for each VWAP type independently.

### 🎨 Customizable Visual Settings

- **Independent Color Schemes**: Assign unique colors to each VWAP type and its SD bands

- **Adjustable Line Widths**: Configure VWAP and SD line thickness (1-5 for VWAP, 1-3 for SD)

- **Plot Styles**: Previous session plots use cross-style for clear differentiation from real-time plots

- **Background Zones**: Optional colored zones when price extends beyond ±2 SD levels

- **Session Labels**: Automatic date labels marking each VWAP anchor point

### 📊 Information Dashboard

Real-time statistics table displaying:

- Current VWAP values for all three calculations

- Live standard deviation values

- ±1 SD levels for quick reference

- Distance from price to each VWAP (percentage format)

- Session tracking counter

- Color-coded proximity indicators

***

## 🔧 How to Use

### For Intraday Trading

1. **Current Session VWAP** acts as dynamic support/resistance—price above VWAP indicates bullish bias, below indicates bearish bias

2. Use **±1 SD bands** for profit targets and stop-loss placement

3. **±2 SD touches** often signal mean reversion opportunities

4. **Previous Session VWAP** provides overnight gap reference levels

### For Swing Trading

1. **Anchored VWAP** from significant events (breakouts, earnings, trend changes) shows institutional cost basis

2. Price trading consistently above/below anchored VWAP confirms trend strength

3. SD band rejections provide high-probability entry zones

### For Multi-Timeframe Analysis

1. Combine all three VWAPs to identify confluence zones

2. When current session VWAP aligns with previous session and anchored VWAP, expect strong support/resistance

3. Monitor distance percentage to gauge overextension

***

## ⚙️ Input Parameters

**📍 Anchored VWAP Configuration**

- `Enable Anchored VWAP` - Toggle on/off

- `Year, Month, Day, Hour, Minute` - Set your custom anchor point (requires confirmation)

**📅 Session VWAP Toggles**

- `Enable Current Session VWAP` - Toggle real-time daily VWAP

- `Enable Previous Session VWAP` - Toggle yesterday's reference VWAP

**General Settings**

- `VWAP Source` - Choose calculation source (default: HLC3)

- `Show ±1/2/3 SD` - Enable/disable each standard deviation level

**Visual Customization**

- Individual color pickers for each VWAP type and SD bands

- Line width adjustments

- `Show VWAP Labels` - Date labels at anchor points

- `Show Info Table` - Statistics dashboard toggle

- `Show SD Zones` - Background coloring beyond ±2 SD

***

## 💡 Trading Applications

✅ **Mean Reversion Trades**: Enter when price touches ±2 SD with reversal confirmation

✅ **Trend Following**: Trade in direction when price holds above/below VWAP

✅ **Institutional Levels**: Anchored VWAP reveals where large players accumulated positions

✅ **Gap Trading**: Use previous session VWAP to gauge gap fill probability

✅ **Volume Profile Analysis**: VWAP represents fair value based on actual volume traded

✅ **Support/Resistance Confluence**: Multiple VWAP alignment creates high-probability zones

***

## 🎓 Understanding VWAP

VWAP is the average price weighted by volume—representing the true average price paid by all market participants during a specific period. Unlike simple moving averages, VWAP gives more weight to price levels with higher trading volume, making it particularly valuable for:

- Institutional traders executing large orders

- Algorithmic trading systems

- Identifying fair value and overextended prices

- Minimizing market impact on large trades

***

## 📈 Chart Setup Recommendations

**Best Timeframes**: 1-minute to 15-minute charts for intraday; 1-hour to 4-hour for swing trading

**Compatible Markets**: Stocks, Indices (Nifty 50, Bank Nifty), Futures, Forex, Crypto

**Session Settings**: Works with standard daily sessions; automatically detects trading days (not calendar days)

***

## 🚀 What Makes This Indicator Unique

Unlike standard VWAP indicators that only show current session data, **Triple VWAP** provides:

- **Multi-session analysis** on a single chart without clutter

- **Historical anchoring** capability for event-driven analysis

- **Professional-grade statistics** dashboard

- **Independent customization** for each VWAP type

- **Optimized calculations** for real-time performance

***

## ⚠️ Important Notes

- **Anchored VWAP** requires manual date input (use significant market events like breakouts, earnings, trend reversals)

- **Session detection** based on daily timeframe changes—works on all chart timeframes

- **Previous Session VWAP** displays as static horizontal lines (reference only, not recalculated)

- **Standard Deviations** calculated using volume-weighted variance formula

- Works best on instruments with **consistent volume data**

***

## 📝 Credits & License

This indicator is published under **TradingView House Rules**. Code is original and follows Pine Script v6 best practices for performance and maintainability.

***

## 🤝 Support & Feedback

If you find this indicator valuable, please:

- ⭐ **Like** this publication

- 💬 **Comment** with your feedback or questions

- 🔔 **Follow** for updates and new releases

***

**Disclaimer**: This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always use proper risk management and combine with your own analysis before making trading decisions.

***

حجم التداول

VWAP Market FlowVWAP Flow Model

VWAP Flow Model is a VWAP-anchored market context indicator designed to help traders understand how price is behaving relative to fair value.

It evaluates the interaction between price, VWAP (Volume-Weighted Average Price), volatility, and momentum to classify prevailing market conditions such as trend continuation, expansion, mean reversion, and momentum decay.

Rather than issuing trade signals, the indicator focuses on identifying market state and execution quality.

Core framework:

-Adaptive VWAP with slope-based colouring

-VWAP acts as the central fair-value reference.

The VWAP line dynamically changes colour based on its slope:

-Rising VWAP → bullish pressure

-Falling VWAP → bearish pressure

-Flattening VWAP → balance, compression, or rotation

This allows traders to quickly assess directional bias and determine whether price movement is supported by underlying flow or occurring in a lower-quality environment.

Signal labels:

The indicator annotates key behavioural transitions to support visual interpretation of market state:

-IGN (Ignition) — Momentum expansion emerging from compression or balance, often marking the start of a directional move.

-CON (Continuation) — Price sustaining directional behaviour in alignment with VWAP slope.

-REV (Reversion) — Mean-reversion behaviour as price returns toward VWAP after extension.

-EXH (Exhaustion) — Loss of momentum or absorption after an extended move, often preceding rotation or regime change.

-MON (Displacement) — High-energy expansion bars indicating strong participation and structural shift.

These labels describe market behaviour, not trade instructions, and should be interpreted within the broader VWAP context.

Market behaviour classification:

The model continuously evaluates how price interacts with VWAP to determine whether the market is:

-directional and trending

-rotating around fair value

-accelerating away from value (expansion)

-losing momentum or showing signs of exhaustion

Classifications are derived from price displacement, volatility conditions, and momentum quality, rather than simple crossovers.

Filtering and control logic:

-Trend / Volatility Filter

Conditions market-state classification on the prevailing volatility and structural regime, helping prevent unstable or low-quality environments from producing misleading context shifts.

-Cooldown Filter

Enforces a minimum number of bars between classification updates to reduce rapid state-flipping in choppy conditions and keep context stable.

-Minimum Bars Between Signals

Controls the strictness of the cooldown logic.

Lower values increase responsiveness; higher values favour cleaner, more stable context changes.

-Tape Dominance Requirement (IGN)

Optional confirmation that requires directional signed-volume pressure to align with price behaviour before ignition-style classifications are allowed, helping distinguish genuine impulsive moves from weak or mechanically driven spikes.

-Tape Dominance Lookback

Defines the evaluation window used by the tape dominance filter.

Shorter lookbacks react faster; longer lookbacks require sustained participation.

Sensitivity and session controls:

Sensitivity modes adjust how responsive the model is to changing conditions:

-Aggressive — faster, more reactive (lower timeframes)

-Balanced — default intraday calibration

-Sniper — stricter thresholds, fewer but higher-quality classifications

Optional session filters allow the model to operate only during selected trading sessions, helping traders focus on higher-liquidity periods and avoid low-efficiency hours.

How to use it:

VWAP Flow Model is used as a context and confirmation layer, not a signal generator:

-Trade in the direction of VWAP slope during directional phases

-Expect mean reversion when price extends far from VWAP in balanced conditions

-Treat strong acceleration away from VWAP as expansion rather than chop

-Use flattening VWAP as an early warning of rotation or momentum loss

It integrates naturally with price action, structure-based analysis, and volume-aware workflows.

Indicator scope:

VWAP Flow Model provides objective market context and behavioural classification.

It does not generate direct trade signals and is designed to support discretionary decision-making.

Important notes:

Market classifications are probabilistic, not guarantees

Past behaviour does not imply future results

This indicator is a decision-support tool, not an automated trading system

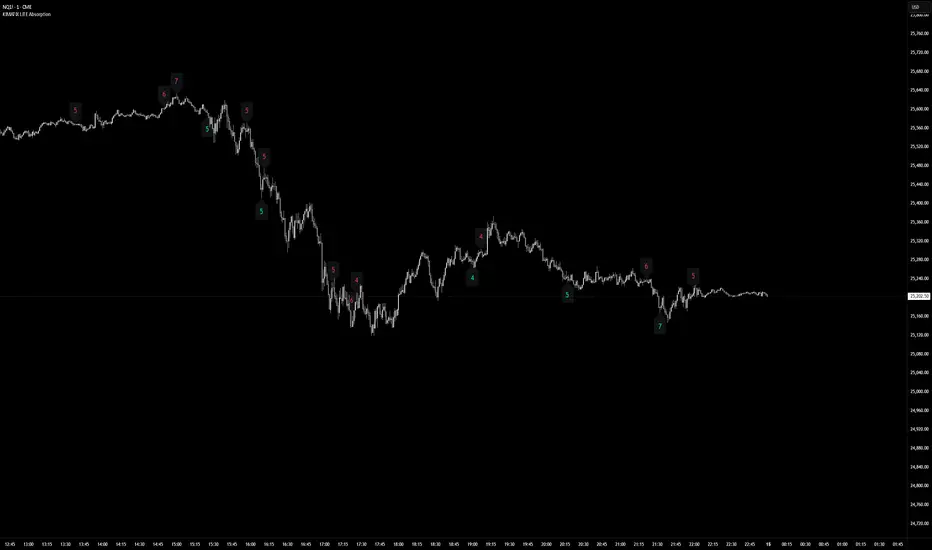

KIMATIX LITE AbsorptionThis indicator highlights absorption intensity directly on the chart using numeric sigma values only.

It is a deliberately reduced, signal-agnostic visualization designed to expose where significant absorption occurs, without adding levels, lines, or trade logic.

What you see

Numeric sigma values on candles

Each number represents the strength of absorption measured in standard deviations (σ).

Color-coded context

Green numbers below price → sell-side absorption

Red numbers above price → buy-side absorption

Only values that exceed the Minimum Sigma threshold are displayed.

No lines, zones, triangles, or alerts are shown — only the raw absorption magnitude.

How it works (LITE Version)

Absorption is derived from volume relative to candle structure

Values are normalized and filtered using:

A fixed statistical lookback

Wick dominance rules to avoid noise

Only statistically significant events (σ ≥ threshold) are visualized

All other calculations run silently in the background.

Intended use

This Lite version is meant to:

Identify areas of aggressive participation or defense

Spot potential absorption during trends or ranges

Provide context for liquidity, exhaustion, or hidden interest

It is not a trading system and does not generate entries or exits.

Use it as a contextual layer alongside your own execution logic.

The full version is distributed separately.

More information can be found here:

whop.com

KIMATIX LITE Delta ProfileThis indicator provides a clean, market-structure view of where participation concentrates and which side is in control across price levels.

The Lite version is intentionally reduced to focus on context over execution while keeping the visual identity of the full profile.

What is shown

Sentiment Profile (right side)

Displays directional dominance at each price level:

Bullish rows when buying pressure dominates

Bearish rows when selling pressure dominates

Point of Control (POC)

Value Area High / Low (VAH / VAL)

Lite Version

No left-side volume profile

No delta labels or historical delta tracking

No lower-timeframe or orderflow proxy

No alerts or event notifications

No visible-range logic or advanced controls

All calculations run on the chart timeframe only, making this version lighter and suitable for public use while preserving structural relevance.

Intended use

This indicator is designed to:

Identify high-interest price zones

Assess directional pressure at each level

Support bias and location decisions

Complement other execution or confirmation tools

It is not an entry or signal system and does not provide trade timing.

The full version is distributed separately.

More information can be found here:

whop.com

"VWAP Multi-Timeframe Pro - 6 VWAPs + Session Analysis"═════════════════════════════════════════════════════════════════════════════

VWAP MULTI-TIMEFRAME PRO - COMPLETE TUTORIAL

By Alphaomega18 (OA18)

═══════════════════════════════════════════════════════════════════════════════

📌 DESCRIPTION

VWAP Multi-Timeframe Pro is a professional trading tool that simultaneously

displays 6 different VWAPs with customizable sessions and dynamic standard

deviation bands. Ideal for day trading, swing trading, and institutional

order flow analysis.

═══════════════════════════════════════════════════════════════════════════════

🎯 KEY FEATURES

✅ 3 CUSTOMIZABLE SESSION VWAPS

• Asia Session: Configurable hours (default 0h-8h Paris time)

• London Session: Configurable hours (default 8h-16h Paris time)

• NY Session: Configurable hours (default 15h30-22h Paris time)

• Each session automatically stops at end time

• Customizable colors and thickness for each session

✅ 3 STANDARD TIMEFRAME VWAPS

• Daily VWAP (resets at midnight)

• Weekly VWAP (resets on Monday)

• Monthly VWAP (resets on 1st of month)

✅ ADVANCED STANDARD DEVIATION BANDS

• 3 levels of standard deviation (1σ, 2σ, 3σ)

• Timeframe selection for bands (Asia/London/NY/Daily/Weekly/Monthly)

• Colored zones for quick extreme identification

• Perfect for mean reversion trading

✅ DYNAMIC LABELS

• Real-time value display

• Labels visible only during active sessions

• Adjustable size (tiny/small/normal/large)

• Automatic positioning

✅ ALERT SYSTEM

• Price / Daily VWAP crossover

• Price reaching ±3σ bands

• Real-time notifications

═══════════════════════════════════════════════════════════════════════════════

📖 INSTALLATION GUIDE

STEP 1: Add the indicator

1. Open TradingView

2. Click on "Indicators" at the top of the chart

3. Search for "VWAP Multi-Timeframe Pro" or "Alphaomega18"

4. Click to add the indicator to your chart

STEP 2: Basic configuration

1. Click on the ⚙️ (settings) icon of the indicator

2. You will see 8 parameter groups

3. Start by enabling/disabling the VWAPs you want

═══════════════════════════════════════════════════════════════════════════════

⚙️ DETAILED CONFIGURATION

┌─────────────────────────────────────────────────────────────────────────────┐

│ GROUP 1: VWAP ASIA SESSION │

├─────────────────────────────────────────────────────────────────────────────┤

│ • Show VWAP Asia: YES/NO │

│ • Start Hour: 0 (24h format, 0-23) │

│ • Start Minute: 0 (minutes, 0-59) │

│ • End Hour: 8 │

│ • End Minute: 0 │

│ • Color: Yellow (customizable) │

│ • Line Width: 2 (1-5) │

│ │

│ 💡 EXAMPLE: For Tokyo 1h-9h Paris → Start: 1h00, End: 9h00 │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ GROUP 2: VWAP LONDON SESSION │

├─────────────────────────────────────────────────────────────────────────────┤

│ • Show VWAP London: YES/NO │

│ • Start Hour: 8 │

│ • Start Minute: 0 │

│ • End Hour: 16 │

│ • End Minute: 0 │

│ • Color: Aqua (customizable) │

│ • Line Width: 2 (1-5) │

│ │

│ 💡 EXAMPLE: For LSE 9h-17h30 Paris → Start: 9h00, End: 17h30 │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ GROUP 3: VWAP NY SESSION │

├─────────────────────────────────────────────────────────────────────────────┤

│ • Show VWAP NY: YES/NO │

│ • Start Hour: 15 │

│ • Start Minute: 30 │

│ • End Hour: 22 │

│ • End Minute: 0 │

│ • Color: Orange (customizable) │

│ • Line Width: 2 (1-5) │

│ │

│ 💡 NOTE: US RTH = 9h30-16h00 ET = 15h30-22h00 Paris time │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ GROUPS 4-6: VWAP DAILY, WEEKLY, MONTHLY │

├─────────────────────────────────────────────────────────────────────────────┤

│ Each group has the same options: │

│ • Show VWAP: YES/NO │

│ • Color: Customizable │

│ • Line Width: 1-5 │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ GROUP 7: STANDARD DEVIATION BANDS │

├─────────────────────────────────────────────────────────────────────────────┤

│ • Show Bands: YES/NO │

│ • Bands Timeframe: Asia/London/NY/Daily/Weekly/Monthly │

│ • Standard Deviation 1: 1.0 (recommended) │

│ • Standard Deviation 2: 2.0 (recommended) │

│ • Standard Deviation 3: 3.0 (recommended) │

│ • Upper Band Color: Green (customizable) │

│ • Lower Band Color: Red (customizable) │

│ │

│ 💡 Bands are calculated on the selected VWAP │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ GROUP 8: DISPLAY │

├─────────────────────────────────────────────────────────────────────────────┤

│ • Show Labels: YES/NO │

│ • Label Size: tiny/small/normal/large │

└─────────────────────────────────────────────────────────────────────────────┘

═══════════════════════════════════════════════════════════════════════════════

🎨 PRESET CONFIGURATIONS

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ CONFIGURATION 1: SCALPING / INTRADAY DAY TRADING ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Chart timeframe: 1min - 5min ┃

┃ ┃

┃ Active VWAPs: ┃

┃ ☑ VWAP Asia : YES (to see overnight range) ┃

┃ ☑ VWAP London : YES (if trading EU session) ┃

┃ ☑ VWAP NY : YES (main US session) ┃

┃ ☑ VWAP Daily : YES (daily reference) ┃

┃ ☐ VWAP Weekly : NO ┃

┃ ☐ VWAP Monthly : NO ┃

┃ ┃

┃ Bands: ┃

┃ Timeframe: NY (if trading US session) ┃

┃ Levels: 1σ, 2σ, 3σ ┃

┃ ┃

┃ Labels: YES, size SMALL ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ CONFIGURATION 2: STANDARD DAY TRADING ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Chart timeframe: 5min - 15min ┃

┃ ┃

┃ Active VWAPs: ┃

┃ ☐ VWAP Asia : NO ┃

┃ ☐ VWAP London : NO ┃

┃ ☑ VWAP NY : YES ┃

┃ ☑ VWAP Daily : YES ┃

┃ ☐ VWAP Weekly : NO ┃

┃ ☐ VWAP Monthly : NO ┃

┃ ┃

┃ Bands: ┃

┃ Timeframe: Daily ┃

┃ Levels: 1σ, 2σ, 3σ ┃

┃ ┃

┃ Labels: YES, size SMALL ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ CONFIGURATION 3: SWING TRADING ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Chart timeframe: 1H - 4H ┃

┃ ┃

┃ Active VWAPs: ┃

┃ ☐ VWAP Asia : NO ┃

┃ ☐ VWAP London : NO ┃

┃ ☐ VWAP NY : NO ┃

┃ ☑ VWAP Daily : YES ┃

┃ ☑ VWAP Weekly : YES ┃

┃ ☐ VWAP Monthly : NO ┃

┃ ┃

┃ Bands: ┃

┃ Timeframe: Weekly ┃

┃ Levels: 1σ, 2σ, 3σ ┃

┃ ┃

┃ Labels: YES, size NORMAL ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ CONFIGURATION 4: MULTI-SESSION TRADING (FOREX, 24H FUTURES) ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Chart timeframe: 15min - 1H ┃

┃ ┃

┃ Active VWAPs: ┃

┃ ☑ VWAP Asia : YES ┃

┃ ☑ VWAP London : YES ┃

┃ ☑ VWAP NY : YES ┃

┃ ☑ VWAP Daily : YES ┃

┃ ☐ VWAP Weekly : NO ┃

┃ ☐ VWAP Monthly : NO ┃

┃ ┃

┃ Bands: ┃

┃ Timeframe: Daily ┃

┃ Levels: 1σ, 2σ, 3σ ┃

┃ ┃

┃ Labels: YES, size SMALL ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

═══════════════════════════════════════════════════════════════════════════════

📊 SIGNAL INTERPRETATION

┌─────────────────────────────────────────────────────────────────────────────┐

│ PRICE POSITION RELATIVE TO VWAP │

├─────────────────────────────────────────────────────────────────────────────┤

│ Price > VWAP → BULLISH TREND (bulls in control) │

│ Price < VWAP → BEARISH TREND (bears in control) │

│ Price = VWAP → EQUILIBRIUM ZONE (indecision) │

│ Price oscillates → RANGE / CONSOLIDATION │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ STANDARD DEVIATION BANDS SIGNALS │

├─────────────────────────────────────────────────────────────────────────────┤

│ Price at +1σ → Normal bullish extension │

│ Price at +2σ → OVERBOUGHT - possible reversal │

│ Price at +3σ → EXTREME OVERBOUGHT - high probability return to VWAP │

│ │

│ Price at -1σ → Normal bearish extension │

│ Price at -2σ → OVERSOLD - possible reversal │

│ Price at -3σ → EXTREME OVERSOLD - high probability return to VWAP │

└─────────────────────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────────────────────┐

│ VWAP CONFLUENCE (POWERFUL SIGNALS) │

├─────────────────────────────────────────────────────────────────────────────┤

│ 3+ VWAPs aligned → VERY STRONG TREND │

│ VWAPs converging → MAJOR SUPPORT/RESISTANCE ZONE │

│ VWAPs diverging → CONSOLIDATION ZONE │

│ Price between 2 → CRITICAL DECISION ZONE │

└─────────────────────────────────────────────────────────────────────────────┘

═══════════════════════════════════════════════════════════════════════════════

💡 TRADING STRATEGIES

╔═════════════════════════════════════════════════════════════════════════════╗

║ STRATEGY 1: MEAN REVERSION ║

╠═════════════════════════════════════════════════════════════════════════════╣

║ TIMEFRAME: 5min - 15min ║

║ VWAP USED: Daily or NY Session ║

║ ║

║ LONG ENTRY RULES: ║

║ 1. Price touches -2σ or -3σ band ║

║ 2. Wait for rejection candle (hammer, pin bar) ║

║ 3. Volume above average ║

║ 4. Enter LONG above rejection candle high ║

║ ║

║ SHORT ENTRY RULES: ║

║ 1. Price touches +2σ or +3σ band ║

║ 2. Wait for rejection candle (shooting star, pin bar) ║

║ 3. Volume above average ║

║ 4. Enter SHORT below rejection candle low ║

║ ║

║ MANAGEMENT: ║

║ • Stop Loss: Beyond ±3σ band ║

║ • Take Profit: Return to VWAP (TP1), opposite VWAP (TP2) ║

║ • Risk/Reward: Minimum 1:2 ║

╚═════════════════════════════════════════════════════════════════════════════╝

╔═════════════════════════════════════════════════════════════════════════════╗

║ STRATEGY 2: TREND FOLLOWING ║

╠═════════════════════════════════════════════════════════════════════════════╣

║ TIMEFRAME: 15min - 1H ║

║ VWAP USED: Daily + Weekly ║

║ ║

║ LONG ENTRY RULES: ║

║ 1. Price > Daily VWAP AND > Weekly VWAP (confirmed trend) ║

║ 2. Wait for pullback to Daily VWAP ║

║ 3. Price rejects VWAP upward (doesn't break) ║

║ 4. Enter LONG on rejection ║

║ ║

║ SHORT ENTRY RULES: ║

║ 1. Price < Daily VWAP AND < Weekly VWAP (confirmed trend) ║

║ 2. Wait for pullback to Daily VWAP ║

║ 3. Price rejects VWAP downward (doesn't break) ║

║ 4. Enter SHORT on rejection ║

║ ║

║ MANAGEMENT: ║

║ • Stop Loss: Below/above Daily VWAP ║

║ • Take Profit: +1σ/+2σ bands or key support/resistance ║

║ • Trailing Stop: Use VWAP as dynamic trailing ║

╚═════════════════════════════════════════════════════════════════════════════╝

╔═════════════════════════════════════════════════════════════════════════════╗

║ STRATEGY 3: BREAKOUT CONFIRMATION ║

╠═════════════════════════════════════════════════════════════════════════════╣

║ TIMEFRAME: 5min - 30min ║

║ VWAP USED: NY Session + Daily ║

║ ║

║ LONG ENTRY RULES: ║

║ 1. Price consolidates around VWAP (range) ║

║ 2. Breakout above VWAP with HIGH VOLUME ║

║ 3. Simultaneous break of NY VWAP AND Daily VWAP ║

║ 4. Pullback test of VWAP (now support) ║

║ 5. Enter LONG on pullback rejection ║

║ ║

║ SHORT ENTRY RULES: ║

║ 1. Price consolidates around VWAP (range) ║

║ 2. Breakout below VWAP with HIGH VOLUME ║

║ 3. Simultaneous break of NY VWAP AND Daily VWAP ║

║ 4. Pullback test of VWAP (now resistance) ║

║ 5. Enter SHORT on pullback rejection ║

║ ║

║ MANAGEMENT: ║

║ • Stop Loss: Return to other side of VWAP ║

║ • Take Profit: ±2σ bands or measured move from range ║

║ • Failed breakout: Exit immediately if back in range ║

╚═════════════════════════════════════════════════════════════════════════════╝

╔═════════════════════════════════════════════════════════════════════════════╗

║ STRATEGY 4: SESSION HANDOFF ║

╠═════════════════════════════════════════════════════════════════════════════╣

║ TIMEFRAME: 5min - 15min ║

║ VWAP USED: Asia + London + NY ║

║ ║

║ CONCEPT: ║

║ Observe how each session respects or breaks the previous session's VWAP. ║

║ A break indicates sentiment change. ║

║ ║

║ LONG EXAMPLE: ║

║ 1. Asia Session: Price ranges around Asia VWAP ║

║ 2. London Open (8h): Price breaks Asia VWAP upward ║

║ 3. London VWAP forms above Asia VWAP ║

║ 4. NY Open (15h30): Price respects London VWAP (doesn't break) ║

║ 5. BULLISH SIGNAL: All 3 sessions aligned bullish ║

║ 6. Enter LONG on pullback to NY VWAP ║

║ ║

║ MANAGEMENT: ║

║ • Stop: Below current session VWAP ║

║ • Target: +2σ band or previous session high ║

║ • Invalid if: Price breaks below all session VWAPs ║

╚═════════════════════════════════════════════════════════════════════════════╝

═══════════════════════════════════════════════════════════════════════════════

🔔 ALERT CONFIGURATION

STEP 1: Create an alert

1. Click on "Alerts" button (alarm icon) top right

2. Click "Create alert"

3. In "Condition", select "VWAP Multi-Timeframe Pro"

STEP 2: Choose alert type

• Price > Daily VWAP: Alert when price crosses Daily VWAP upward

• Price < Daily VWAP: Alert when price crosses Daily VWAP downward

• Price at +3σ: Alert when price reaches extreme upper band

• Price at -3σ: Alert when price reaches extreme lower band

STEP 3: Configure alert

• Frequency: "Once per bar close" (recommended)

• Expiration: Set according to your needs

• Actions: Popup + Email + Mobile notification

RECOMMENDED ALERTS FOR DAY TRADING:

✓ Price crosses Daily VWAP (up and down)

✓ Price at ±3σ on NY Session VWAP

✓ Combine with other indicators for confirmation

═══════════════════════════════════════════════════════════════════════════════

💼 SPECIFIC USE CASES

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ TRADING MNQ (E-MINI NASDAQ 100) ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Optimal configuration: ┃

┃ • Timeframe: 5min ┃

┃ • VWAP Asia: 0h-8h (see overnight range) ┃

┃ • VWAP NY: 15h30-22h (RTH session) ┃

┃ • VWAP Daily: Active ┃

┃ • Bands: NY Session, 1σ/2σ/3σ ┃

┃ ┃

┃ Strategy: ┃

┃ 1. At 15h30: Observe if price respects or breaks Asia VWAP ┃

┃ 2. Enter in NY VWAP direction if confluence with Daily ┃

┃ 3. Use ±2σ bands for targets ┃

┃ 4. Stop below/above NY VWAP ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ TRADING FOREX EUR/USD ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Optimal configuration: ┃

┃ • Timeframe: 15min ┃

┃ • VWAP Asia: 0h-8h ┃

┃ • VWAP London: 8h-16h (most liquid EUR/USD session) ┃

┃ • VWAP NY: 14h-22h (US overlap) ┃

┃ • Bands: London Session ┃

┃ ┃

┃ Strategy: ┃

┃ 1. London Session (8h): Trade in Asia breakout direction ┃

┃ 2. NY Session (14h): Observe London/NY VWAP confluence ┃

┃ 3. Exit before 22h (end of liquidity) ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

┏━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┓

┃ TRADING US STOCKS (AAPL, TSLA, etc.) ┃

┣━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┫

┃ Optimal configuration: ┃

┃ • Timeframe: 5min or 15min ┃

┃ • VWAP NY: 15h30-22h (RTH only) ┃

┃ • VWAP Daily: Active ┃

┃ • VWAP Weekly: Active (for swing) ┃

┃ • Bands: Daily ┃

┃ ┃

┃ Strategy: ┃

┃ 1. Pre-market: Analyze sentiment vs Daily VWAP ┃

┃ 2. Open (15h30): Confirm direction with NY VWAP ┃

┃ 3. Institutional orders visible at Daily/Weekly VWAP confluence ┃

┗━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━┛

═══════════════════════════════════════════════════════════════════════════════

⚠️ COMMON MISTAKES TO AVOID

❌ MISTAKE 1: Trading against all VWAPs

→ If price < Daily, Weekly, Monthly VWAP → DON'T buy

→ Wait for confluence or trend change

❌ MISTAKE 2: Ignoring sessions

→ NY VWAP at 8am has NO validity

→ Respect session start/end times

❌ MISTAKE 3: Over-trading VWAP touches

→ Every VWAP touch is NOT a signal

→ Wait for confluence + volume + pattern

❌ MISTAKE 4: Wrong time configuration

→ Check your timezone

→ Adjust hours according to your location

❌ MISTAKE 5: Neglecting volume

→ VWAP crossover without volume is WEAK

→ Volume > average = more reliable signal

❌ MISTAKE 6: Forgetting HTF context

→ Always check higher timeframe

→ Daily chart for intraday, Weekly for swing

❌ MISTAKE 7: Too tight stop loss

→ Place stop BEYOND ±3σ band

→ Give position room to breathe

❌ MISTAKE 8: Using only VWAP

→ COMBINE with: RSI, Volume Profile, Support/Resistance

→ VWAP is a tool, not a complete strategy

═══════════════════════════════════════════════════════════════════════════════

📈 OPTIMIZATION & BACKTESTING

TIPS TO IMPROVE YOUR RESULTS:

1. JOURNAL YOUR TRADES

• Note which VWAP configuration worked

• Which session gives best results

• Which band level (1σ/2σ/3σ) is optimal

2. TEST DIFFERENT PERIODS

• Modify session hours according to your asset

• Crypto: Different 24h sessions

• EU Stocks: Adapt to XETRA/CAC hours

3. ADAPT BANDS

• Volatile assets: Use 1.5σ, 2.5σ, 3.5σ

• Calm assets: Keep standard 1σ, 2σ, 3σ

4. COMBINE WITH OTHER TOOLS

• Volume Profile (POC, VAH, VAL)

• Market Delta / Order Flow

• Horizontal Support/Resistance

• Fibonacci retracements

═══════════════════════════════════════════════════════════════════════════════

🆘 SUPPORT & FAQ

Q: Are times in local time or UTC?

A: Times are in your TradingView chart's timezone.

For Paris, use French local time.

Q: Can I use more than 3 sessions?

A: This version offers 3 customizable sessions. For more, duplicate

the indicator with different configurations.

Q: Does VWAP reset automatically?

A: Yes! Each VWAP resets automatically:

• Sessions: At defined start time

• Daily: At midnight

• Weekly: On Monday

• Monthly: On 1st of month

Q: Why isn't my session VWAP displaying?

A: Check:

1. Session is enabled in settings

2. You are WITHIN session time

3. Hours are correctly configured

Q: Can I export my configurations?

A: Yes, TradingView allows saving indicator templates.

Q: Compatible with free TradingView?

A: Yes, indicator works on all TradingView plans.

═══════════════════════════════════════════════════════════════════════════════

Version 1.0 | © 2025 Alphaomega18

Indicator developed for professional and passionate traders

═══════════════════════════════════════════════════════════════════════════════

TrendSurfer Pro

TrendSurfer Pro 🚀 - Advanced Multi-Signal Trading Indicator

TrendSurfer Pro is a comprehensive all-in-one trading system that combines multiple proprietary algorithms and technical indicators to identify high-probability trading opportunities across all timeframes.

**Key Features:**

🔹 **Master Trend System** - Identifies major trend reversals using a combination of EMAs, RSI, and custom filters

🔹 **Smart Money Analysis** - Order Blocks detection with Z-Score impulse identification and rejection signals

🔹 **Session-Based Trading** - Tokyo, London, and New York session analysis with automatic breakout/rejection detection

🔹 **IFVG Detection** - Institutional Fair Value Gap identification for precision entries

🔹 **Multi-Timeframe Signals** - Triangle signals with volume analysis and VWAP proximity filtering

🔹 **KCandle/Boost System** - Advanced engulfing pattern detection with golden area projections

🔹 **CCI Signals** - Commodity Channel Index crosses with MACD confirmation filter

🔹 **Take Profit System** 🎯 - Advanced exit system combining 8 technical indicators (RSI, MACD, Stochastic, Bollinger Bands, Supertrend, CCI, EMA Cross, Price Action) with customizable confirmation requirements

**Unique Advantages:**

✅ Yellow Box Filter - Proprietary reversal zone detection

✅ Time Filters - Trade only during your preferred hours

✅ VWAP Integration - All signals respect price position relative to VWAP

✅ Customizable Alerts - Get notified for every signal type

✅ Visual Dashboard - Real-time trend confirmation table

Perfect for day traders, swing traders, and scalpers seeking precise entries and optimal exits! 🚀

KIMATIX LITE Crypto ScannerKIMATIX Crypto Scanner

This indicator visualizes institutional demand and supply zones based on an automated volume profile calculation.

The Lite version is designed for context and market structure only:

Displays dynamic long and short zones

Helps identify high-interest price areas

Intended for bias and location, not execution

No signals, alerts, confirmations, or execution logic are included.

All advanced filters, timing logic, probability validation,

and trade management are reserved for the full version.

Use this tool to understand where price matters — not when to trade.

The full version is distributed separately.

More information can be found here:

whop.com

VP + Fib + AVWAP + Graded Signals An indicator for the discretionary trader

Avwap, Fib and VP is all you need.

Graded signals for conviction.

RSI WMA Crossover Momentum w/ HighlightRSI WMA Crossover Momentum

This is a momentum indicator that tracks the RSI. Its principle is to use the WMA line to determine the trend of the RSI, and from the RSI, the price trend can be determined.

Fed Balance Sheet vs GDP RatioThis indicator tracks the size of the Federal Reserve’s Balance Sheet relative to the total US Economy (Nominal GDP). It serves as a primary gauge for systemic liquidity and the extent of monetary intervention in the markets.

How it Works: The script calculates the ratio between:

Fed Total Assets (FRED:WALCL) - The total amount of bonds and assets held by the Fed.

US Nominal GDP (FRED:GDP) - The annualized economic output of the US.

How to Read the Levels: I have plotted historical reference lines to help contextualize the current cycle:

🔴 35% (Pandemic Peak): The absolute high of monetary stimulus (2020–2022). This represents maximum liquidity, where the Fed "printed" massive amounts of money to support the economy.

🟠 ~20% (The "Danger Zone"): This was the range established after the 2008 Financial Crisis (2014–2019). Watch this level closely. In late 2019, when the Fed tried to push the ratio below ~18%, the banking plumbing broke (the Repo Crisis), forcing them to restart QE. We are currently approaching this level again.

⚪ 6% (Pre-2008 Normal): The historical baseline before the era of Quantitative Easing (QE) began.

Why This Matters:

Rising Ratio: Suggests the Fed is expanding liquidity (QE) faster than the economy is growing. Historically, this is a tailwind for risk assets (Stocks, Crypto).

Falling Ratio: Suggests the Fed is tightening (QT) or the economy is outgrowing the money supply. This represents a headwind for liquidity and risk assets.

Methodology Note:

Data Source: Federal Reserve Economic Data (FRED).

Calculation: No manual annualization is applied to GDP, as FRED:GDP is already reported as a Seasonally Adjusted Annual Rate (SAAR).

NY Session Vol Entries (RB Trading)NY Session Vol Entries (RB Trading)

NY Session Vol Entries is an intraday analysis script designed to evaluate price behavior during U.S. market hours on the one hour chart. It focuses on the interaction between relative volume expansion, adaptive volatility structure, and directional momentum alignment to help users interpret active market conditions.

The script is intended specifically for liquid U.S. equities during the New York session and is not designed for use outside this context.

Intended Usage and Scope

• Timeframe: 1 hour only

• Market hours: New York session

• Asset class: U.S. equities with consistent volume

• Style: Intraday structure and momentum evaluation

• Alerts: Available for all signal types

Core Framework

The script evaluates market behavior through three interdependent components that must align before a setup is displayed:

Relative volume behavior

Volatility expansion and contraction

Directional momentum context

This structure helps filter low-participation periods and reduce noise.

Relative Volume Analysis

The script compares current volume to a rolling 14-period average to identify periods where participation meaningfully deviates from typical conditions.

Elevated volume often occurs during session opens or active repricing phases. When volume remains muted, the script suppresses signals to avoid low-quality environments.

Adaptive Volatility Structure

Volatility bands are calculated using an 8-period true range measurement. These bands adjust dynamically based on recent volatility rather than remaining static.

During elevated participation, the bands compress to reflect tighter price acceptance. As volatility expands, the bands trail price to help visualize directional structure.

Directional Momentum Context

Directional context is determined using a dual moving average relationship.

• When short-term momentum is above longer-term momentum, the script allows only bullish evaluations

• When short-term momentum is below longer-term momentum, the script allows only bearish evaluations

This alignment reduces counter-directional signals and helps maintain structural consistency. The filter can be disabled if users wish to study range behavior.

Signal Classification

The script displays two types of informational labels:

Volume-Aligned Signals

These appear only when directional momentum and relative volume expansion align at candle close.

Momentum Rotation Signals

These indicate directional shifts regardless of volume and are intended to provide context rather than standalone triggers.

All signals are confirmed only after the candle closes. No intrabar logic is used.

Stop and Target Reference Plotting

When conditions align, the script plots visual reference levels:

• A stop reference positioned beyond the momentum structure

• A projected target reference calculated using a fixed 2R multiple relative to the stop distance

These levels are provided for consistency and planning. They are not forecasts or guarantees.

Session and Timing Considerations

The script is designed specifically for New York market hours. Liquidity and participation outside this window often distort volume and volatility behavior.

Earnings sessions should be treated with caution, as event-driven price action can override normal structural behavior.

Opening Range Consideration

The first one hour candle of the New York session can display elevated volatility due to initial repricing. Allowing additional candles to form may provide clearer structural information before evaluating signals.

Why One Hour and New York Session

The one hour timeframe balances structure and responsiveness while reducing lower-timeframe noise. New York trading hours provide the most reliable volume profile for U.S. equities, making relative volume analysis more meaningful.

Settings Overview

• Volatility period: 8

• Volatility multiplier: 3.0

• Volume average period: 14

• Momentum averages: 8 and 21

• Trend filter: Enabled by default

• Alerts available for all signal types

Chart Usage Guidelines

• Use the script on a clean chart

• Avoid stacking additional momentum or volume indicators

• Drawings should only be used when they help interpret structure

Important Notes

This script analyzes historical price and volume behavior. It does not predict future price movement or ensure outcomes. Users should test the tool, understand its logic, and apply independent risk management.

4HR JRSX Swing Bias (RB Trading)4HR JRSX Swing Bias (RB Trading)

The 4HR JRSX Swing Bias is a higher timeframe swing analysis script designed to evaluate directional pressure, momentum decay, and price acceptance on the four hour chart. It is built specifically for GBPUSD and EURUSD and is not intended for use on other markets or timeframes.

It highlights conditions where directional pressure weakens, rotates, and is then confirmed by price behavior.

Intended Use and Scope

• Timeframe: 4 hour only

• Markets: GBPUSD and EURUSD

• Style: Swing bias and rotation analysis

• Signal frequency: Intentionally low, typically 10 to 15 setups per year per pair

• Alerts: Available for confirmed setups

• Not designed for Asia session conditions

Core Framework

The script operates through a sequential three-stage process. A setup can only appear when all stages align.

Directional pressure evaluation

Momentum exhaustion and rotation

Candle-based price confirmation

This structure prevents signals from appearing during noise or low-quality market conditions.

Directional Pressure Evaluation

The first stage measures directional pressure across multiple four hour candles using a smoothed strength calculation. This step evaluates whether bullish or bearish participation is dominant over time rather than reacting to isolated price spikes.

When directional pressure is unclear or neutral, the script remains inactive.

Momentum Exhaustion and Rotation

Once directional pressure is established, the script monitors for loss of momentum. Exhaustion is identified when pressure fails to expand despite continued price movement.

This decay often appears near the later stages of a directional move and signals increased probability of rotation rather than continuation.

Price Acceptance and Confirmation

The final stage requires price to confirm the rotation through candle behavior. No intrabar logic is used.

• Buy confirmation requires either

– a bullish candle close following downside pressure exhaustion

– or a pinbar showing strong rejection of lower prices

• Sell confirmation requires either

– a bearish candle close following upside pressure exhaustion

– or a pinbar showing strong rejection of higher prices

A setup is only confirmed after the four hour candle has fully closed.

Stop and Target Reference Plotting

When a setup is confirmed, the script plots visual reference levels:

• A stop reference beyond the exhaustion zone where the setup would be invalidated

• A projected target reference calculated using a fixed 4R multiple relative to the stop distance

These levels are provided for structural planning and consistency. They do not represent predictions or guarantees.

Why the Four Hour Chart Is Required

The pressure and exhaustion calculations are tuned to higher-timeframe behavior. On lower timeframes, momentum cycles occur too rapidly and lead to frequent false rotations.

The four hour chart provides the balance required for meaningful pressure, decay, and acceptance to develop.

Session Considerations

The script is not intended for Asia session evaluation. Reduced liquidity during those hours can distort momentum behavior and reduce signal quality. Best evaluation occurs during or after London and New York participation.

Chart Presentation Guidelines

• Use the script on a clean chart

• Avoid stacking other oscillators or momentum tools

• If drawings are used, they should be limited to swing structure or key price levels

All visual elements should support understanding of the script output.

Important Notes

This script analyzes historical price behavior to identify structural swing conditions. It does not predict future price movement or ensure outcomes. Users should test the tool, understand its confirmation rules, and apply independent risk management.

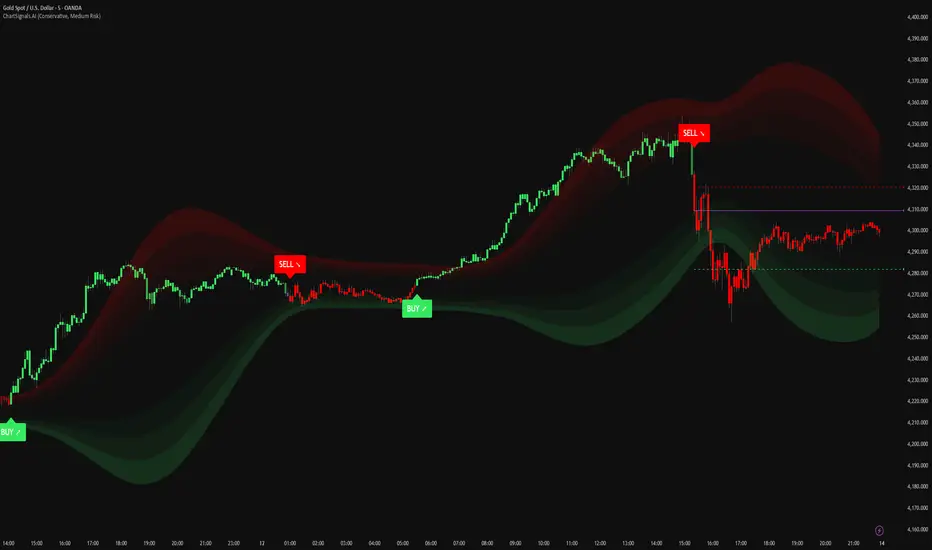

ChartSignals.AIChartSignals.AI is an overlay indicator designed to simplify chart reading by highlighting potential trade opportunities and providing optional visual context tools.

WHAT YOU’LL SEE

• Buy/Sell signals displayed directly on the chart

• Optional trade level guides (Entry / Take Profit / Stop Loss) to help structure a plan

• Optional trend and zone overlays to help interpret market conditions

• Optional key levels and breakout markers for additional context

• Dynamic candle coloring to help visualize momentum vs. quieter conditions

HOW TO USE (SIMPLE)

• Add ChartSignals.AI to your chart

• Choose a Signal Mode (controls how frequently signals appear)

• Enable/disable the optional overlays you want

• Use signals as chart assistance and confirm with your own analysis and risk management

ALERTS

This script includes alert conditions for:

• Buy, Sell, general signal notifications, and key level break events (when enabled).

DISCLAIMER

For educational and charting purposes only. Not financial advice. Trading involves risk and you are responsible for your own decisions.

Momentum Pulse Pro [MTF]# Momentum Pulse Pro

## What It Does

Detects when price momentum is stretched to extremes. The indicator analyzes momentum and highlights when the market is overextended — either too hot or too cold.

- **Green background** = Low momentum, potential bounce ahead

- **Red background** = High momentum, potential reversal ahead

- **Stronger color** = Stronger signal

## The Panel

Displays a Momentum Index from 0-100:

- **Below 30** = Stretched to the downside

- **30-70** = Neutral zone

- **Above 70** = Stretched to the upside

## How to Use

1. Wait for the background to change color

2. Stronger color = higher probability setup

3. Use as a filter for your strategy — don't trade it alone

## Settings

- **Colors** — Customize green/red

- **Transparency** — Background visibility

- **Confluence Intensity** — How fast color intensifies

- **Panel Position** — Move the info panel

## Alerts

- Momentum enters extreme zone

- Momentum strengthens or weakens inside extreme zone

## Good to Know

- Non-repainting

- Works on any market

- Best on 4H chart or lower

FTL Context Teaser - PublicFTL Context (Teaser) – Public

FTL Context (Teaser) is a visual market context layer designed to highlight periods of increased market risk and structural tension.

This script does NOT provide trading signals and is NOT intended for standalone trading decisions.

It serves as a contextual overlay only, helping traders visually identify when market conditions shift away from equilibrium.

The teaser version is intentionally limited and does not expose the underlying logic or decision framework.

Full functionality, advanced filters, and integrated decision logic are available in the invite-only FTL Context Layer (PRO).

📩 Contact / PRO access:

fairtradinglab@gmail.com

Educational & informational use only.

RSI+Breadth Multi-Factor# RSI+ Breadth Multi-Factor Indicator

**Multi-factor scoring system for US market timing | 美股多因子择时评分系统**

[! (img.shields.io)](www.tradingview.com)

[! (img.shields.io)](www.tradingview.com)

[! (img.shields.io)](LICENSE)

---

## Overview | 概述

A quantitative indicator that combines **RSI**, **market breadth** (% above 20/50-day MA), and **up/down volume ratio** to generate actionable buy/sell signals for SPY, QQQ, and IWM.

这是一个结合 **RSI**、**市场广度**(站上20/50日均线比例)和 **涨跌成交量比** 的量化指标,为 SPY、QQQ 和 IWM 生成可操作的买卖信号。

---

## Features | 功能特点

| Feature | 功能 |

|---------|------|

| 🎯 Multi-factor scoring (-10 to +10) | 多因子评分系统 (-10 到 +10) |

| 📊 RSI + Breadth + Volume integration | RSI + 广度 + 成交量三重验证 |

| 🔀 Three markets: SPY, QQQ, IWM | 三大市场:SPY、QQQ、IWM |

| 🔥 Cross-market resonance detection | 跨市场共振信号检测 |

| 📈 Trend filter (MA-based) | 趋势过滤(均线判断) |

| ⏰ Auto-adapts to intraday timeframes | 自动适配日内时间周期 |

| 🎚️ Three modes: Aggressive/Standard/Conservative | 三种模式:激进/标准/保守 |

---

## Signal Reference | 信号说明

| Score | Emoji | Signal | 中文 | Action |

|:-----:|:-----:|--------|:----:|--------|

| ≥ 6 | 🚀 | **PANIC LOW** | 恐慌低点 | Strong buy 强烈买入 |

| ≥ 4 | 📈 | **BUY ZONE** | 低吸区 | Accumulate 分批建仓 |

| -3~3 | - | **HOLD** | 持有 | Hold position 持仓观望 |

| ≤ -4↑ | ⭐ | **ELEVATED** | 高估 | Hold cautious 持有但谨慎 |

| ≤ -4↓ | ⚡ | **CAUTION** | 观望 | Take profit 止盈 |

| ≤ -6↓ | ⚠️ | **REDUCE** | 减仓 | Reduce position 减少仓位 |

> **↑ = Uptrend** (price > MA) | **↓ = Downtrend** (price < MA)

### Resonance Signals | 共振信号

| Emoji | Signal | Description |

|:-----:|--------|-------------|

| 🔥 | Resonance Buy | Multiple markets in buy zone 多市场同时低吸 |

| ❄️ | Resonance Risk | Multiple markets in risk zone 多市场同时高估 |

---

## Scoring Logic | 评分逻辑

### Factors | 因子

| Factor | Weight | Buy Score | Sell Score |

|--------|--------|-----------|------------|

| **RSI** | 1x | RSI < 30 → +2, < 40 → +1 | RSI > 75 → -2, > 65 → -1 |

| **FI (50D MA%)** | Bottom focus | < 25% → +3, < 35% → +2 | > 85% → -2, > 78% → -1 |

| **TW (20D MA%)** | Top focus | < 30% → +1 | > 82% → -3, > 72% → -2 |

| **Volume Ratio** | 1x | UVOL/DVOL < 0.5 → +2 | > 2.5 → -2 |

### Breadth Symbols | 广度数据

| Market | TW Symbol | FI Symbol | Volume |

|--------|-----------|-----------|--------|

| SPY (S&P 500) | INDEX:S5TW | INDEX:S5FI | USI:UVOL/DVOL |

| QQQ (NASDAQ) | INDEX:NCTW | INDEX:NCFI | USI:UVOLQ/DVOLQ |

| IWM (Russell 2000) | INDEX:R2TW | INDEX:R2FI | USI:UVOL/DVOL |

---

## Settings | 设置说明

### Mode | 模式

- **Aggressive**: Lower thresholds, shorter cooldown (5 bars)

- **Standard**: Balanced defaults (10 bar cooldown)

- **Conservative**: Higher thresholds, longer cooldown (15 bars)

### Key Parameters | 关键参数

| Parameter | Default | Description |

|-----------|---------|-------------|

| RSI Length | 14 | RSI calculation period |

| Trend MA Length | 10 | MA for trend filter |

| Cooldown Bars | 10 | Min bars between same signals |

| Resonance Window | 3 | Bars to check for multi-market agreement |

| Min Markets | 2 | # of markets needed for resonance |

---

## Usage | 使用方法

### Installation | 安装

1. Copy the indicator code

2. In TradingView: **Pine Editor** → **New** → Paste code → **Add to Chart**

### Recommended Setup | 推荐设置

- **Timeframe**: Daily (D) for best accuracy | 推荐日线图

- **Markets**: Apply on SPY, QQQ, or IWM | 应用于SPY/QQQ/IWM

- **Mode**: Start with "Standard" | 建议从"标准"模式开始

### Intraday Mode | 日内模式

The indicator automatically detects intraday timeframes and adjusts:

- Uses only RSI + Volume factors (TW/FI are daily-only data)

- Lowers signal thresholds accordingly

指标会自动检测日内周期并调整:

- 仅使用 RSI + 成交量因子(TW/FI 仅有日线数据)

- 相应降低信号触发阈值

---

## Dashboard | 仪表盘

Displays real-time factor breakdown:

```

┌────────┬───────┬────────┐

│ Factor │ Score │ Weight │

├────────┼───────┼────────┤

│ RSI │ 1.0 │ 1x │

│ FI(50D)│ 2.0 │ Bottom │

│ TW(20D)│ -1.0 │ Top │

│ Vol │ 1.0 │ 1x │

│ Trend │ ↑ │ 10MA │

├────────┼───────┼────────┤

│ Total │ 3.0 │ HOLD │

└────────┴───────┴────────┘

```

---

## Alerts | 警报

Available alerts for each market (SPY/QQQ/IWM):

- Panic Low / Buy Zone (entry signals)

- Reduce / Caution (exit signals)

- Resonance Buy / Risk (cross-market confirmation)

每个市场(SPY/QQQ/IWM)可设置以下警报:

- 恐慌低点 / 低吸区(入场信号)

- 减仓 / 观望(出场信号)

- 共振买入 / 风险(跨市场确认)

---

## Trend Filter | 趋势过滤

**Key feature**: Risk signals (CAUTION/REDUCE) only trigger when **price is below the trend MA**.

When price is above MA (uptrend), the indicator shows **ELEVATED** ⭐ instead, preventing premature exits during strong rallies.

**核心功能**:风险信号(观望/减仓)仅在 **价格跌破趋势均线** 时触发。

当价格在均线之上(上升趋势)时,指标显示 **高估** ⭐,避免在强势上涨中过早离场。

---

## Disclaimer | 免责声明

This indicator is for **educational and informational purposes only**. It is not financial advice. Past performance does not guarantee future results. Always do your own research and consider your risk tolerance before trading.

本指标仅供 **教育和参考用途**,不构成投资建议。历史表现不代表未来收益。交易前请自行研究并考虑风险承受能力。

---

## License | 许可

MIT License - Free to use and modify with attribution.

MIT 许可证 - 可自由使用和修改,请注明出处。

---

## Author | 作者

Built with ❤️ for the trading community.

为交易社区精心打造 ❤️

Smart WhaleOverview The Smart Whale Breakout System is a pure momentum strategy designed for Swing Traders who want to capture high-probability breakouts while managing risk with a mechanical trailing stop.

Unlike indicators that try to guess "bottoms," this system follows the "Smart Money" approach: buying strength when institutional volume enters, and riding the trend until the momentum breaks.

How it Works

1. The Entry (The Hunter) The system identifies a valid BREAKOUT signal only when four specific conditions align:

Trend Filter: Price must be above the 150 SMA. We only trade with the long-term trend.

Momentum: RSI > 50. Ensuring bulls are in control.

Volume Spike (Whale Activity): Current volume must be significantly higher than the average (Default: 1.5x). This filters out weak retail moves.

Price Action: A bullish candle closing higher than it opened.

2. The Exit (The Manager) Once in a trade, the system activates a dynamic Trailing Stop line. You never have to guess when to sell. You can choose between two exit logic modes in the settings:

ATR Trailing (Default): Adapts to volatility. The stop moves up based on a multiple of the Average True Range (ATR). Great for volatile stocks (e.g., TSLA, NVDA).

Percent Trailing: A fixed percentage drop from the highest high. (e.g., "Sell if price drops 10% from peak").

3. The Context (Optional Filter)

Squeeze Filter: Includes a built-in Bollinger/Keltner squeeze detection. If enabled in settings, the system will only signal a buy if the price recently broke out of a consolidation (squeeze). Default is OFF to catch all momentum moves.

Key Features

NO Repainting: Signals are confirmed at candle close.

Visual Risk Management: A Red Trailing Stop line clearly shows where your invalidation point is.

Fully Customizable: Adjust the Volume multiplier, ATR sensitivity, or Percentage drop to fit your asset class (Crypto/Stocks/Forex).

Clean Visuals: Only colors the Breakout and Sell candles to keep your chart clean.

Settings Guide

Trend SMA Length: Define the long-term trend baseline (Default: 150).

Volume Spike (xAvg): How much volume is needed to trigger a buy? (1.5 = 150% of average).

Exit Method: Choose between "ATR Trailing" or "Percent Trailing".

ATR Multiplier: Tighter stop (2.0) vs Looser stop (3.0).

Require Squeeze?: Check this to filter for breakouts that only happen after a consolidation period.

Disclaimer This tool is for educational purposes only. Always use proper risk management.

Custom Monthly Volume Profile [Multi-Timeframe]This indicator renders a high-precision Monthly Volume Profile designed for intraday traders and practitioners of Auction Market Theory. Unlike standard volume profiles, this script utilizes Multi-Timeframe (MTF) data request capability to build the profile from lower timeframe data (e.g., 5-minute bars) while displaying it on your trading timeframe.

This tool is optimized to keep your chart clean while providing critical developing levels (POC, VAH, VAL) and historical context from the previous month.

Key Features:

1. Dynamic "Auto-Scaling" Width One of the biggest issues with monthly profiles is visual clutter.

Early Month: The profile starts wide (default 10% width) so you can clearly see the developing structure when data is scarce.

Late Month: As volume accumulates, the profile automatically shrinks (scales down to 2% width) to prevent the histogram from obscuring price action.

Note: This can be toggled off for a static width.

2. Developing & Static Levels

Current Month: Displays real-time Developing Point of Control (dPOC), Value Area High (dVAH), and Value Area Low (dVAL).

Previous Month: Automatically locks in the levels from the previous month at the close, providing immediate support/resistance references for the new month.

3. Time-Filtered Alerts Avoid waking up to notifications during low-volume overnight sessions. This script includes a Session Filter (Default: 0830-1500).

Alerts for crossing POC, VAH, or VAL will only trigger if the price cross occurs within the user-defined time window.

4. Calculation Precision

Multi-Timeframe Data: The profile is built using lower timeframe data (Input: Calculation Precision) rather than just the current chart bars. This ensures the Volume Profile shape remains accurate even when viewing higher timeframes.

Row Size: Fully adjustable "Tick/Row Size" to control the resolution of the volume buckets.

Settings Overview:

Calculation Precision: Determine the granularity of the data (e.g., "5" for 5-minute data).

Row Size: Controls vertical resolution (Lower = higher detail).

Value Area %: Standard 70% default, fully adjustable.

Auto-Width: Set the Start % (Day 1) and End % (Day 31).

Alerts: Toggle Current or Previous month alerts and define the active time session.

Visual Customization:

Customize colors for the Histogram (Value Area vs. Outer Area).

Customize line width and colors for POC, VAH, and VAL.

Supports Right or Left alignment.

Disclaimer: This tool is for informational purposes only. Past performance and volume levels do not guarantee future price action.

Navigator Triple VolumeNavigator Triple Volume (VWAP + Fixed VP + Flexible VP)

**Navigator Triple Volume** combines three of the most practical volume-based tools into one clean overlay:

1. **VWAP (anchored) with optional deviation bands**

2. **Fixed Volume Profile** (auto-building by anchor timeframe, with optional developing/current profile)

3. **Flexible Volume Profile** (manual start/end window for custom range analysis)

The goal is simple: give you **institutional-grade context**—where price is “fair,” where volume is accepted, and where the real inventory is sitting—without stacking multiple indicators.

1) Anchored VWAP + Bands

This script plots an **anchored VWAP** and optional **±1 and ±2 standard deviation bands** to help you gauge:

* “Fair value” (VWAP)

* Stretch/extension zones (deviation bands)

* Mean reversion vs. trend strength around VWAP

Anchor period options include **Daily, Week, Month, Quarter, Year**, and event-based anchors like **Earnings, Dividends, and Splits** (where supported).

2) Fixed Volume Profile

The Fixed VP automatically builds a **completed profile each time the anchor timeframe rolls over** (ex: Daily). It can also display the **current/developing profile** for the active anchor period.

Includes:

* **PoC (Point of Control)**

* **Value Area (VAH/VAL)** based on a configurable % (default 68%)

* Adjustable **rows (resolution)**, **profile width**, and **bar thickness**

3) Flexible Volume Profile

Flexible VP lets you define a **custom range** using a manual **Start Calculation** and **End Calculation** time selection. This is ideal for:

* Single swing legs

* News/event reactions

* Range breaks

* “From low to high” campaign profiling

Includes:

* PoC + Value Area levels

* Adjustable profile resolution and styling

How traders use it

* Use **VWAP** as the “fair value” magnet and trend filter

* Use **Fixed VP** to identify session/period acceptance and key reference levels

* Use **Flexible VP** to profile *your chosen range* and locate the true battleground: PoC, VAH, and VAL

When all three agree, it’s a high-confidence area for decision-making. When they disagree, it often signals transition or rotation.

Notes

* This indicator draws profiles using TradingView line objects and includes controls to manage performance and display preferences.

* Built for chart clarity: one script, three volume lenses.

Navigator Volume Profil FixedLong Term Investing

Day Trading

Navigator Volume Profile Fixed (Fixed + Current Session)

**Navigator Volume Profile Fixed** plots a horizontal volume profile on your chart using a **fixed timeframe anchor** (ex: Daily) and optionally overlays a **live “current” profile** for the active session/period.

It’s designed to help you quickly see where volume is building (acceptance) vs. thinning out (rejection), and to identify the key reference levels traders watch most: **PoC, VAH, and VAL**.

### What it plots

**Fixed Volume Profile (anchored to a timeframe)**

Builds a completed profile each time the selected anchor timeframe rolls over (ex: each new day on a Daily anchor).

**Current Volume Profile (live)**

Continuously updates the developing profile for the current anchor period (optional toggle).

**Point of Control (PoC)**

Highlights the single price level with the highest traded volume.

**Value Area (VAH / VAL)**

Plots the Value Area boundaries using a configurable percentage (default **68%**), and visually differentiates the value area from the rest of the profile.

Key settings

* **Enable Fixed VP**: turn the fixed/anchored profile on/off

* **Timeframe Anchor**: choose the profile reset period (ex: 1D)

* **Show Current Fixed VP**: show/hide the developing (current) profile

* **Number of Rows**: controls profile resolution (price “bins”)

* **Profile Width (%)** and **Bar Thickness**: visual scaling controls

* **PoC + Value Area toggles**: show/hide PoC and VA boundaries

* **Extend PoC Line**: optionally extend the PoC into the future

How to use it (practical)

* Treat **PoC** as the most accepted price for the anchored period.

* Use **VAH/VAL** as reference boundaries for balance vs. imbalance.

* Compare **Fixed** vs **Current** profiles to see whether volume is migrating higher/lower during the session and where price is building acceptance.

**Note:** This script draws using TradingView line objects and is optimized to stay within platform limits while maintaining a clean profile display.

FTL Context - Public TeaserFTL Context (Teaser) – Public

FTL Context (Teaser) is a visual market context layer designed to highlight periods of increased market risk and structural tension.

This script does NOT provide trading signals and is NOT intended for standalone trading decisions.

It serves as a contextual overlay only, helping traders visually identify when market conditions shift away from equilibrium.

The teaser version is intentionally limited and does not expose the underlying logic or decision framework.

Full functionality, advanced filters, and integrated decision logic are available in the invite-only FTL Context Layer (PRO).

Educational & informational use only.

Golden Volume Lines📌 Golden Volume — Lines (Golden Team)

Golden Volume — Lines is an advanced volume-based indicator that detects Ultra High Volume candles using a statistical percentile model, then automatically draws and tracks key price levels derived from those candles.

The indicator highlights where real market interest and liquidity appear and shows how price reacts when those levels are broken.

🔍 How It Works

Volume Measurement

Choose between:

Units (raw volume)

Money (Volume × Average Price)

Average price can be calculated using HL2 or OHLC4.

Percentile-Based Classification

Volume is classified into:

Medium

High

Ultra High Volume

Thresholds are calculated using a rolling percentile window.

Ultra Volume candles are colored orange.

Dynamic High & Low Levels

For every Ultra Volume candle:

A High and Low dotted line is drawn.

Lines extend to the right until price breaks them.

Smart Line Break Detection (Wick-Based)

A line is considered broken when price wicks through it.

When a break occurs:

🟧 Orange line → broken by an Ultra Volume candle

⚪ White line → broken by a normal candle

The line stops exactly at the breaking candle.

🔔 Alerts

Alert on Ultra High Volume candles

Alert when a High or Low line is broken

Separate alerts for:

Break by Ultra Volume candle

Break by Normal candle

🎯 Use Cases

Breakout & continuation confirmation

Liquidity sweep detection

Volume-validated support & resistance

Market reaction after extreme participation

⚙️ Key Inputs

Volume display mode (Units / Money)

Percentile thresholds

Lookback window size

Maximum number of active Ultra levels

Optional dynamic alerts

⚠️ Disclaimer

This indicator is a volume and market structure tool, not a standalone trading system.

Always use proper risk management and additional confirmation.

PEAD ScreenerPEAD Screener - Post-Earnings Announcement Drift Scanner

═══════════════════════════════════════════════════════════════

WHY EARNINGS ANNOUNCEMENTS CREATE OPPORTUNITY

═══════════════════════════════════════════════════════════════

The days immediately following an earnings announcement are among the noisiest periods for any stock. Within hours, the market must digest new information about a company's profits, revenue, and future outlook. Analysts scramble to update their models. Institutions rebalance positions. Retail traders react to headlines.

This chaos creates a well-documented phenomenon called Post-Earnings Announcement Drift (PEAD): stocks that beat expectations tend to keep rising, while those that miss tend to keep falling - often for weeks after the initial announcement. Academic research has confirmed this pattern persists across decades and markets.

But not every earnings surprise is equal. A company that beats estimates by 5 cents might move very differently than one that beats by 5 cents with unusually high volume, or one where both earnings AND revenue exceeded expectations. Raw numbers alone don't tell the full story.

═══════════════════════════════════════════════════════════════

HOW "STANDARDIZED UNEXPECTED" METRICS CUT THROUGH THE NOISE

═══════════════════════════════════════════════════════════════

This screener uses a statistical technique to measure how "surprising" a result truly is - not just whether it beat or missed, but how unusual that beat or miss was compared to the company's own history.

The core idea: convert raw surprises into Z-scores.

A Z-score answers the question: "How many standard deviations away from normal is this result?"

- A Z-score of 0 means the result was exactly average

- A Z-score of +2 means the result was unusually high (better than ~95% of historical results)

- A Z-score of -2 means the result was unusually low

By standardizing surprises this way, we can compare apples to apples. A small-cap biotech's $0.02 beat might actually be more significant than a mega-cap's $0.50 beat, once we account for each company's typical variability.

This screener applies this standardization to three dimensions: earnings (SUE), revenue (SURGE), and volume (SUV).

═══════════════════════════════════════════════════════════════

THE 9 SCREENING CRITERIA

═══════════════════════════════════════════════════════════════

─────────────────────────────────────────

1. SUE (Standardized Unexpected Earnings)

─────────────────────────────────────────

WHAT IT IS:

SUE measures how surprising an earnings result was, adjusted for the company's historical forecast accuracy.

Calculation: Take the earnings surprise (actual EPS minus analyst estimate), then divide by the standard deviation of past forecast errors. This uses a rolling window of the last 8 quarters by default.

Formula: SUE = (Actual EPS - Estimated EPS) / Standard Deviation of Past Errors

HOW TO INTERPRET:

- SUE > +2.0: Strongly positive surprise - earnings beat expectations by an unusually large margin. These stocks often continue drifting higher.

- SUE between 0 and +2.0: Modest positive surprise - beat expectations, but within normal range.

- SUE between -2.0 and 0: Modest negative surprise - missed expectations, but within normal range.

- SUE < -2.0: Strongly negative surprise - significant miss. These stocks often continue drifting lower.

For long positions, look for SUE values above +2.0, ideally combined with positive SURGE.

─────────────────────────────────────────

2. SURGE (Standardized Unexpected Revenue)

─────────────────────────────────────────

WHAT IT IS:

SURGE applies the same standardization technique to revenue surprises. While earnings can be manipulated through accounting choices, revenue is harder to fake - it represents actual sales.

Calculation: Take the revenue surprise (actual revenue minus analyst estimate), then divide by the standard deviation of past revenue forecast errors.

Formula: SURGE = (Actual Revenue - Estimated Revenue) / Standard Deviation of Past Errors

HOW TO INTERPRET:

- SURGE > +1.5: Strongly positive revenue surprise - the company sold significantly more than expected.

- SURGE between 0 and +1.5: Modest positive surprise.

- SURGE < 0: Revenue missed expectations.

The most powerful signals occur when BOTH SUE and SURGE are positive and elevated (ideally SUE > 2.0 AND SURGE > 1.5). This indicates the company beat on both profitability AND top-line growth - a much stronger signal than either alone.

When SUE and SURGE diverge significantly (e.g., high SUE but negative SURGE), treat with caution - the earnings beat may have come from cost-cutting rather than genuine growth.

─────────────────────────────────────────

3. SUV (Standardized Unexpected Volume)

─────────────────────────────────────────

WHAT IT IS:

SUV detects unusual trading volume after accounting for how volatile the stock is. More volatile stocks naturally have higher volume, so raw volume comparisons can be misleading.

Calculation: This uses regression analysis to model the expected relationship between price volatility and volume. The "unexpected" volume is the residual - how much actual volume deviated from what the model predicted. This residual is then standardized into a Z-score.

In plain terms: SUV asks "Given how much this stock typically moves, is today's volume unusually high or low?"

HOW TO INTERPRET:

- SUV > +2.0: Exceptionally high volume relative to the stock's volatility. This often signals institutional activity - big players moving in or out.

- SUV between +1.0 and +2.0: Elevated volume - above normal interest.

- SUV between -1.0 and +1.0: Normal volume range.

- SUV < -1.0: Unusually quiet - less activity than expected.

High SUV combined with positive price movement suggests accumulation (buying). High SUV combined with negative price movement suggests distribution (selling).

─────────────────────────────────────────

4. % From D0 Close

─────────────────────────────────────────

WHAT IT IS:

This measures how far the current price has moved from the closing price on its initial earnings reaction day (D0). The "reaction day" is the first trading day that fully reflects the earnings news - typically the day after an after-hours announcement, or the announcement day itself for pre-market releases.

Calculation: ((Current Price - D0 Close) / D0 Close) × 100

HOW TO INTERPRET:

- Positive values: Stock has gained ground since earnings. The higher the percentage, the stronger the post-earnings drift.

- 0% to +5%: Modest positive drift - earnings were received well but momentum is limited.

- +5% to +15%: Strong drift - buyers continue accumulating.

- > +15%: Exceptional drift - significant institutional interest likely.