Average Daily RangeRe-Re-upload!

There are a handful of decent Average Daily Range indicators out there.

Often they are built using Pinescript v2 (severely outdated) or have no customization or are "Closed Source"

In this version, you can select two multipliers to display on chart

Primary Mult - Large Green or Red crosses, by default set to 1 or 100% of ADR

Secondary Mult - Small Aqua or Maroon crosses, by default set to 0.5 or 50% of ADR

Cheers,

EFX

ابحث في النصوص البرمجية عن "通达信+选股公式+换手率+0.5+源码"

MathStatisticsKernelDensityEstimationLibrary "MathStatisticsKernelDensityEstimation"

(KDE) Method for Kernel Density Estimation

kde(observations, kernel, bandwidth, nsteps)

Parameters:

observations : float array, sample data.

kernel : string, the kernel to use, default='gaussian', options='uniform', 'triangle', 'epanechnikov', 'quartic', 'triweight', 'gaussian', 'cosine', 'logistic', 'sigmoid'.

bandwidth : float, bandwidth to use in kernel, default=0.5, range=(0, +inf), less will smooth the data.

nsteps : int, number of steps in range of distribution, default=20, this value is connected to how many line objects you can display per script.

Returns: tuple with signature: (float array, float array)

draw_horizontal(distribution_x, distribution_y, distribution_lines, graph_lines, graph_labels) Draw a horizontal distribution at current location on chart.

Parameters:

distribution_x : float array, distribution points x value.

distribution_y : float array, distribution points y value.

distribution_lines : line array, array to append the distribution curve lines.

graph_lines : line array, array to append the graph lines.

graph_labels : label array, array to append the graph labels.

Returns: void, updates arrays: distribution_lines, graph_lines, graph_labels.

draw_vertical(distribution_x, distribution_y, distribution_lines, graph_lines, graph_labels) Draw a vertical distribution at current location on chart.

Parameters:

distribution_x : float array, distribution points x value.

distribution_y : float array, distribution points y value.

distribution_lines : line array, array to append the distribution curve lines.

graph_lines : line array, array to append the graph lines.

graph_labels : label array, array to append the graph labels.

Returns: void, updates arrays: distribution_lines, graph_lines, graph_labels.

style_distribution(lines, horizontal, to_histogram, line_color, line_style, linewidth) Style the distribution lines.

Parameters:

lines : line array, distribution lines to style.

horizontal : bool, default=true, if the display is horizontal(true) or vertical(false).

to_histogram : bool, default=false, if graph style should be switched to histogram.

line_color : color, default=na, if defined will change the color of the lines.

line_style : string, defaul=na, if defined will change the line style, options=('na', line.style_solid, line.style_dotted, line.style_dashed, line.style_arrow_right, line.style_arrow_left, line.style_arrow_both)

linewidth : int, default=na, if defined will change the line width.

Returns: void.

style_graph(lines, lines, horizontal, line_color, line_style, linewidth) Style the graph lines and labels

Parameters:

lines : line array, graph lines to style.

lines : labels array, graph labels to style.

horizontal : bool, default=true, if the display is horizontal(true) or vertical(false).

line_color : color, default=na, if defined will change the color of the lines.

line_style : string, defaul=na, if defined will change the line style, options=('na', line.style_solid, line.style_dotted, line.style_dashed, line.style_arrow_right, line.style_arrow_left, line.style_arrow_both)

linewidth : int, default=na, if defined will change the line width.

Returns: void.

ColorExtensionLibrary "ColorExtension"

Color Extension methods.

hsl(hue, saturation, lightness, transparency) HSL color transform.

Parameters:

hue : float, hue color component, hue is a degree on the color wheel from 0 to 360. 0 is red, 120 is green, 240 is blue.

saturation : float, saturation color component, saturation is a percentage value, 0 means a shade of gray and 100 is the full color.

lightness : float, lightness color component, Lightness is also a percentage; 0 is black, 100 is white.

transparency : float, transparency color component, transparency is also a percentage; 0 is opaque, 100 is transparent.

Returns: color

rgb_to_hsl(red, green, blue) Convert RGB to HSL color values

Parameters:

red : float, red color component.

green : float, green color component.

blue : float, blue color component.

Returns: tuple with 3 float values, hue, saturation and lightness.

complement(primary) Complementary of selected color

Parameters:

primary : color, the primary

Returns: color.

invert(primary) Inverts selected color.

Parameters:

primary : color, the primary.

Returns: color.

is_cool(base) Color is cool or warm.

Parameters:

base : color, the color to check.

Returns: bool.

temperature(base) Color temperature.

Parameters:

base : color, the color to check.

Returns: bool.

is_high_key(base) Color is high key (orange yellow green).

Parameters:

base : color, the color to check.

Returns: bool.

mix(base, mix, rate) Mix two colors together.

Parameters:

base : color, the base color.

mix : color, the color to mix.

rate : float, default=0.5, the rate of mixture, range within 0.0 and 1.0.

Returns: color.

analog(primary) Selects 2 near spectrum colors (H +/- 45).

Parameters:

primary : color, the base color.

Returns: tuple with 2 colors.

triadic(primary) Selects 2 far spectrum colors (H +/- 120).

Parameters:

primary : color, the base color.

Returns: tuple with 2 colors.

tetradic(primary) Uses primary and the complementary color, + 60º to form a rectangular pattern on the color wheel.

Parameters:

primary : color, the base color.

Returns: tuple with 3 colors.

square(primary) Uses primary and generate 3 equally spaced (90º) colors.

Parameters:

primary : color, the base color.

Returns: tuple with 3 colors.

Inverse Fisher Transform on Williams %RInverse Fisher Transform On Williams %R

Since Williams R indicator produces negative values, I preferred to add 50 instead of subtracting 50.

It produces values between 0.5 and -0.5.

Generates clear buy and sell signals.

Williams %R determines overbought and oversold levels.

You can see more softly.

0_dteUSAGE

This script guages the probability of an underlying moving a certain amount on expiration day, to aid the popular "0 dte" strategy. The script counts how many next-day moves exceeded a given magnitude in the past, under similar conditions. The inputs are:

mark_mode:

- "open": measures the magnitude as "open to close"--a true 0 dte.

- "previous close": for lazy people who don't want to wake up early. measures magnitude from the previous day's close.

move_mode:

- "percent": measures moves that exceed a given percentage.

- "absolute": measures moves that exceed a point value.

move-dir: measure only up moves, down moves, or both.

vol_model: the model for realized volatility. (may add more later).

min_vol: only measure moves when realized vol is above this value.

max_vol: only measure moves when realized vol is below this value.

precision: number of digits printed in the output table.

EXAMPLE:

- mark_mode: "previous close"

- move_mode: "percent"

- move_dir: "up"

- move_mag: 0.07

- vol_model: hv30

- min_vol: 0.2

- max_vol: 0.5

These settings will count the number of trading days that closed 7% higher than the previous day's close, when the previous day's realized volatility (annualized) was between 20% and 50%. The outputs are:

- current vol: green plot. Today's realized vol. Shown for convenience.

- max and min vol: red plots. Also shown for convenience.

- count: the number of days that exceeded the chosen magnitude, when the previous day's realized volatility was within the chosen bounds.

- total: the total number of days where realized volatility was within the chosen bounds

- probability: count / total. the percentage of days that exceeded the move when volatility was within the bounds.

- move: plotted as a purple line. purple "X" labels are plotted above

- bars where the move exceeded the magnitude threshold and volatility was in-bounds. a "hit".

CONCLUSION

This script is based on the idea that realized volatility has some bearing on future volatility. By seeing what happened in the past when volatility was close to its current value, we may be able to assess the probability that our short put will be in the money, tomorrow, and our account devastated.

NOTE: Unlike many of my other scripts, all percentages--both inputs and outputs--are given in fractional form. E.g., 0.01 means 1%.

3Commas BotBjorgum 3Commas Bot

A strategy in a box to get you started today

With 3rd party API providers growing in popularity, many are turning to automating their strategies on their favorite assets. With so many options and layers of customization possible, TradingView offers a place no better for young or even experienced coders to build a platform from to meet these needs. 3Commas has offered easy access with straight forward TradingView compatibility. Before long many have their brokers hooked up and are ready to send their alerts (or perhaps they have been trying with mixed success for some time now) only they realize there might just be a little bit more to building a strategy that they are comfortable letting out of their sight to trade their money while they eat, sleep, etc. Many may have ideas for entry criteria they are excited to try, but further questions arise... "What about risk mitigation?" "How can I set stop or limit orders?" "Is there not some basic shell of a strategy that has laid some of this out for me to get me going?"

Well now there is just that. This strategy is meant for those that have begun to delve into the world of algorithmic trading providing a template that offers risk defined positions complete with stops, limit orders, and even trailing stops should one so choose to employ any of these criteria. It provides a framework that is easily manipulated (with some basic working knowledge of pine coding) to encompass ones own ideas and entry criteria, while also providing an already functioning strategy.

The default settings have a basic 1:1 risk to reward ratio, which sets a limit and a stop equal distance from the entry. The entry is a simple MA cross (up for long, down for short). There a variety of MA's to choose from and the user can define the lengths of the averages. The ratio can be adjusted from the menu along with a volatility based adder (ATR) that helps to distance a stop from support or resistance. These values are calculated off the swing low/high of the user defined lookback period. Risk is calculated from position entry to stop, and projected upwards to the limit as a function of the desired risk to reward ratio. Of note: the default settings include 0.05% commissions. Competitive commissions of the leading cryptocurrency exchanges are .1% round trip (one buy and one sell) for market orders. There is also some slippage to allow time for alerts to be sent and orders to fill giving the back test results a more accurate representation of real time conditions. Its recommended to research the going rates for your exchange and set them to default for the strategy you use or build.

To get started a user would:

1) Make a copy of the code and paste in their bot keys in the area provided under the "3Comma Keys" section

- eg. Long bot "start deal" copied from 3commas in to define "Long" etc. (code is commented)

2) Place alert on desired asset with desired settings ensuring to select "Order fills and alert() function calls"

3) Paste webhook into the webhook box and select webhook URL alerts (3rd party provided webhook)

3) Delete contents of alert message box and replace with {{strategy.order.alert_message}} and nothing else

- the codes will be sent to the webhook appropriately as the strategy enters and exits positions. Only 1 alert is needed

settings used for the display image:

1hr chart on BTCUSD

-ATR stop

-Risk adjustment 1.2

-ATR multiplier 1.3

-RnR 0.6

-MAs HEMA/SMA

-MA Length 50/100

-Order size percent of equity

-Trail trigger 60% of target

Experiment with your own settings on your crypto of choice or implement your own code!

Implementing your trailing stop (optional)

Among the options for possible settings is a trailing stop. This stop will ratchet higher once triggered as a function of the Average True Range (ATR). There is a variable level to choose where the user would like to begin trailing the stop during the trade. The level can be assigned with a decimal between 0 and 1 (eg. 0.5 = 50% of the distance between entry and the target which must be exceeded before the trail triggers to begin). This can allow for some dips to occur during the trade possibly keeping you in the trade for longer, while potentially reducing risk of drawdown over time. The default for this setting is 0 meaning unless adjusted, the trail will trigger on entry if the trailing stop exit method is selected. An example can be seen below:

Again, optional as well is the choice to implement a limit order. If one were to select a trailing stop they could choose not to set a limit, which could allow a trail to run further until hit. Drawdowns of this strategy would be foregoing locking gains at highs on target on other trades. This is a trade-off the user can decide on and test. An example of this working in favor can be observed below:

Conclusion

Although a simple strategy is implemented here, the benefits of this script allow a user a starting platform to build their strategies from with built in risk mitigation. This allows the user to sidestep some of the potential difficulties' that can arise while learning Pine and taking on the endeavor of automating their trading strategies. It is meant as an aid, a structure, and an educational piece that can be seen as a "pick-up-and-go" strategy with easy 3Commas compatibility. Additionally, this can help users become more comfortable with strategy alert messages and sending strings in the form of alerts from Pine. As well, FAQs are often littered with questions regarding "strategy.exit" calls, how to implement stops. how to properly set a trailing stop based on ATR, and more. The time this can save an individual to get started is likely of the best "take-aways" here.

Happy trading

Unusual Time Frame VolumeThis script plots the ratio of each volume bar to the average daily volume of that specific bar (at that specific time of day).

You can see what the volume at the 09:30 (or whenever) bar looks like compared to the average volume at the same time during the previous X number of days.

The output can be read like a normal volume chart; however, you can see at a glance whether these is more volume than "normal" for that time of day.

A value of "2" would be 2x the "normal" volume; a value of "0.5" would be half.

Thus, if bars exceed the value of "1", you know that there is more volume than normal.

If the bar exceeds an adjustable threshold, it will change the color of the bar to yellow; otherwise it will be orange for values exceeding "1".

As a consequence to this approach, the plot is effectively normalized such that it obviates the need to scale up or down as volume changes throughout the day.

Notes:

If the settings are not set appropriately for your mode and time frame, the output will be incorrect/invalid!

Make sure you set the "Asset Mode" and "Time Frame (minutes)" to values that match your asset and chart setting. For example, if you are trading Futures on a 2m chart, set the Asset Mode to Futures and Time Frame to 2m. If you are trading crypto on a 5m chart, set the Asset Mode to 24/7 and Time Frame to 5m.

If you choose a "Look-back (Days)" setting that is too far back given the time frame, the script will produce an error. I suggest playing with settings from 1 (compares volume to the previous day's volume) to the highest number that doesn't break the script. For example, at a 2m time frame, the maximum look-back will be 6-7 depending on which mode you are using. Longer time frames allow larger look-back values. I find that the default value (6 Days) does a decent job in general.

Multi Level ZigZag Harmonic PatternsLets make things bit complicated.

Main difference between this script and the earlier Multi Zigzag Harmonic Pattern is the calculation logic of Zigzag 2, 3 and 4

In the earlier script, all zigzags were plain and were calculated on the basis of different lengths. (Such as 5, 10, 15, 20). These were derived on the basis of Multi Zigzag indicator

In this script, Zigzag 2, 3 and 4 are calculated in slightly different way. They are calculated on the basis of previous zigzag. This means, Zigzag 1 will be the input for Zigzag2 calculation and Zigzag 2 will be the input for Zigzag3 and so on. This is demonstrated in the script - Multi Level Zigzag

One important parameter which is specific to this script is: UseZigZagChain

If checked:

Zigzag2 is formed based on Zigzag1

Zigzag3 is formed based on Zigzag2

Zigzag4 is formed based on Zigzag3

This can lead to patterns covering huge number of candles as this chaining causes exponential effect in each levels. (Effective length grows exponentially in each level)

If unchecked:

Zigzag2 is formed based on Zigzag1 (Same as when checked)

Zigzag3 is formed based on Zigzag1. But, length is set to zigzag2Length + zigzag3Length

Zigzag4 is formed based on Zigzag1. But, length is set to zigzag2Length + zigzag3Length + zigzag4Length

This reduces exponential increase of zigzag lengths over next levels.

Logical ratios of patterns are coded as below:

Notations:

Lines XABCD forms the pattern in all cases. (OXABCD in case of Three drives )

abc = BC retacement of AB, xab = AB retracement of XA and so on

ABCD Classic

0.618 <= abc <= 0.786

1.272 <= bcd <= 1.618

AB=CD

Price difference between AB and CD are equal

Time difference between AB and CD are equal

ABCD Extension

0.618 <= abc <= 0.786

1.272 <= AD/ BC (price) <= 1.618

Gartley

xab = 0.618

0.382 <= abc <= 0.886

1.272 <= bcd <= 1.618 OR xad = 0.786

Crab

0.382 <= xab <= 0.618

0.382 <= abc <= 0.886

2.24 <= bcd <= 3.618 OR xad = 1.618

Deep Crab

xab = 0.886

0.382 <= abc <= 0.886

2.0 <= bcd <= 3.618 OR xad = 1.618

Bat

0.382 <= xab <= 0.50

0.382 <= abc <= 0.886

1.618 <= bcd <= 2.618 OR xad = 0.886

Butterfly

xab = 0.786

0.382 <= abc <= 0.886

1.618 <= bcd <= 2.618 OR 1.272 <= xad <= 2.618

Shark

xab = 0.786

1.13 <= abc <= 1.618

1.618 <= bcd <= 2.24 OR 0.886 <= xad <= 1.13

Cypher

0.382 <= xab <= 0.618

1.13 <= abc <= 1.414

1.272 <= bcd <= 2.0 OR xad = 0.786

Three Drives

oxa = 0.618

1.27 <= xab <= 1.618

abc = 0.618

1.27 <= bcd <= 1.618

5-0

1.13 <= xab <= 1.618

1.618 <= abc <= 2.24

bcd = 0.5

Double Bottom

Last two pivot High Lows make W shape

Last Pivot Low is higher than previous Last Pivot Low.

Last Pivot High is lower than previous last Pivot High.

Price has not gone below Last Pivot Low

Price breaks out of last Pivot High to complete W shape

Double Top

Last two pivot High Lows make M shape

Last Pivot Low is higher than previous Last Pivot Low.

Last Pivot High is lower than previous last Pivot High.

Price has not gone above Last Pivot High

Price breaks out of last Pivot Low to complete M shape

Multi ZigZag Harmonic PatternsCombining Multizigzag with harmonic patterns - this script generates harmonic patterns based on multiple deapth zigzags.

Input parameter allows to chose which Zigzag to be included in pattern identification and set different length, line color, width and style for each Zigzag combinations.

Pattern rules are as below:

Gartley

xab = 0.618

0.382 <= abc <= 0.886

1.272 <= bcd <= 1.618 OR xad = 0.786

Crab

0.382 <= xab <= 0.618

0.382 <= abc <= 0.886

2.24 <= bcd <= 3.618 OR xad = 1.618

Deep Crab

xab = 0.886

0.382 <= abc <= 0.886

2.0 <= bcd <= 3.618 OR xad = 1.618

Bat

0.382 <= xab <= 0.50

0.382 <= abc <= 0.886

1.618 <= bcd <= 2.618 OR xad = 0.886

Butterfly

xab = 0.786

0.382 <= abc <= 0.886

1.618 <= bcd <= 2.618 OR 1.272 <= xad <= 2.618

Shark

xab = 0.786

1.13 <= abc <= 1.618

1.618 <= bcd <= 2.24 OR 0.886 <= xad <= 1.13

Cypher

0.382 <= xab <= 0.618

1.13 <= abc <= 1.414

1.272 <= bcd <= 2.0 OR xad = 0.786

Three Drives

oxa = 0.618

1.27 <= xab <= 1.618

abc = 0.618

1.27 <= bcd <= 1.618

5-0

1.13 <= xab <= 1.618

1.618 <= abc <= 2.24

bcd = 0.5

Related scripts are present here:

quarter level 0.5 to 2.0This script could help to see edged level for a reverse on forex, not for yen pairs and is based on quarter and round number theory.

I suggest to use it on H4 timeframe or lower to have a confermation on support or resistance level.

Auto Harmonic Patterns - Open SourceI may not be able to spend much time on the harmonic patterns and realized that there are not much open source scripts on them either. Hence, decided to release open source version which can be used by other developers for reference and build things on top of it.

Original script is protected and can be found here:

Logical ratios of patterns are coded as below:

Notations:

Lines XABCD forms the pattern in all cases. (OXABCD in case of Three drives )

abc = BC retacement of AB, xab = AB retracement of XA and so on

ABCD Classic

0.618 <= abc <= 0.786

1.272 <= bcd <= 1.618

AB=CD

Price difference between AB and CD are equal

Time difference between AB and CD are equal

ABCD Extension

0.618 <= abc <= 0.786

1.272 <= AD/ BC (price) <= 1.618

Gartley

xab = 0.618

0.382 <= abc <= 0.886

1.272 <= bcd <= 1.618 OR xad = 0.786

Crab

0.382 <= xab <= 0.618

0.382 <= abc <= 0.886

2.24 <= bcd <= 3.618 OR xad = 1.618

Deep Crab

xab = 0.886

0.382 <= abc <= 0.886

2.0 <= bcd <= 3.618 OR xad = 1.618

Bat

0.382 <= xab <= 0.50

0.382 <= abc <= 0.886

1.618 <= bcd <= 2.618 OR xad = 0.886

Butterfly

xab = 0.786

0.382 <= abc <= 0.886

1.618 <= bcd <= 2.618 OR 1.272 <= xad <= 2.618

Shark

xab = 0.786

1.13 <= abc <= 1.618

1.618 <= bcd <= 2.24 OR 0.886 <= xad <= 1.13

Cypher

0.382 <= xab <= 0.618

1.13 <= abc <= 1.414

1.272 <= bcd <= 2.0 OR xad = 0.786

Three Drives

oxa = 0.618

1.27 <= xab <= 1.618

abc = 0.618

1.27 <= bcd <= 1.618

5-0

1.13 <= xab <= 1.618

1.618 <= abc <= 2.24

bcd = 0.5

This script contains everything which original script has apart from stats. Use the original script if you are not developer looking for code reference and prefer having stats table.

I have also developed a strategy based on harmonic patterns which can be found here:

Kifier's MFI/STOCH Hidden Divergence/Trend BeaterMFI/STOCH Hidden Divergence/Trend Beater

General Idea:

My premise around this strategy was to make a general strategy for crypto that would help out with finding entry positions for when you’re bullish on a crypto and want to hold on for a while, and at the same time avoiding massive drops. Essentially a way to mix long term/ swing trading; I somewhat achieved my goal however it still requires a lot of logic tuning of the trend averages.

I’m a huge proponent of volume indicators and coupled with average closing price, I think this gives a really good idea of what is happening with the market. It gives an idea on the market and retail investor sentiment. This generally gives you logical entry positions (Although I don’t know how amazing that will work with all cryptos, there’s a fine line between a good strategy and one that just rides bubble market conditions, some would argue that’s still a success and others not)

How it works:

There are many components to the strategy that try to do different things:

First of all there are two types of entries, a MFI hidden divergence with a STOCH check, essentially it will only fire when a divergence is detected while STOCH is above 50%, however this might be changed in the future as due to the volatile nature of cryptos, the STOCH is not too effective. The second entry is a simple MFI/STOCH trend, if STOCH is above 50% and the trend is detected to be in a trending long, once a MFI crossover over the 50% line is detected an entry is placed, this is designed to get out profit where the divergence would otherwise be less accurate during strongly trending conditions.

-MFI is a great indicator, as a volume weighted momentum indicator I find it the most accurate of all, the STOCH however is a great indicator to get a general picture of simple market conditions and can filter out the emotional noise of retail investors.

-VWMA and an SMA (The bottom oscillator) gives an idea of the trend tacking into account of the volume, this serves as a more short term filter of the trend for filters.

-OBV checks are done between the OBV and an EMA of the OBV, to get the idea of a volume weighted long trend, which is important for crypto as there are massive rallies to go up due to retail greed, it’s great to jump onto it at the beginning, and get off before the stack of cards fall apart.

-ATR is used to detect when the market is relatively just ranging or moving sideways, which is where the hidden divergence entries are done, during predictable and profitable market conditions.

- Stop loss is based on the closest support of the entry, this is a nice medium of room to breath but also an actual stop loss.

Future plans and improvements:

Currently there’s a lot I want to improve, mostly the divergence detection and the overall sharpe ratio could be much better, but the current value of 0.5 gives me hope that the strategy is onto something. I also want to change TP from a percentage stop to something more dynamic but that might be too optimistic. The current plan is to paper trade test this either by manual or by a python bot, to see how it performs with some user input as well.

BTC top bottom weekly bandsThis indicator is based on the 20 weekly simple moving average and it could be used to help finding potential tops and bottoms on a weekly BTC chart.

When using the provided "coef" parameter set to the default of 0.5 it shows how most bottoms since 2013 have hit the lower band of this indicator.

The lower band is calculated as exp(coef) * sma(close)

Instructions:

- Use with the symbol INDEX:BTCUSD so you can see the price since 2010

- Set the timeframe to weekly

- Use logarithmic chart (toggle "log" on)

Optionals:

- change the coef to 0.6 for a more conservative bottom

- change the coef to 0.4 for a more conservative top

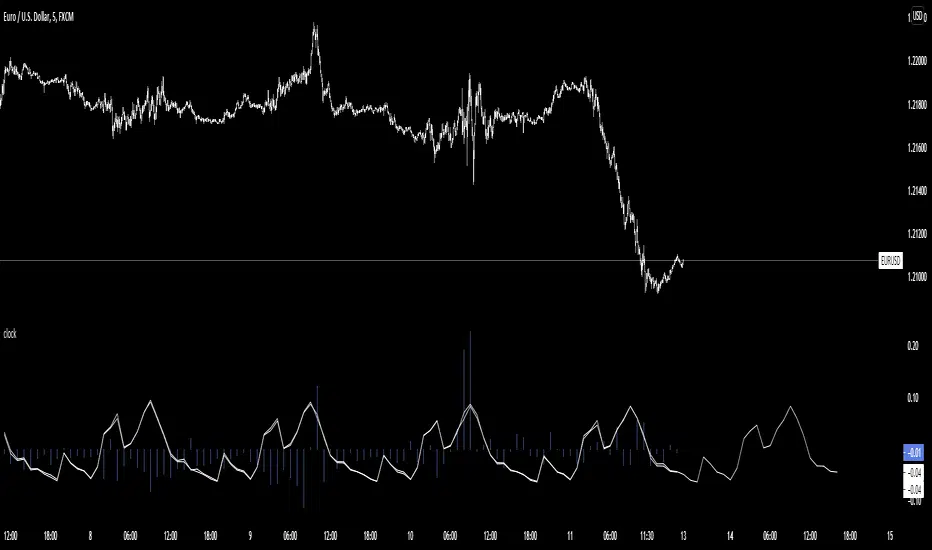

CUSTOM intraday volatility chart clockChart clock showing an overview of the day's expected and actual intraday volatility.

In white are only the expected volatility scores. The expected increase or decrease in volatility at any given hour of day compared to the average of the whole day's expected volatility. A 0.5 score two hours from now means that you can expect that hour to be 0.5% more volatile than the average of whole day's volatility.

In blue are the actual or realized volatility scores; the difference between that hour's volatility and what was expected to be its volatility is displayed as a blue bar. If two three hours ago was expected to be a more volatile hour of the day but no movement occurred, a large down bar will print for that hour.

Large swings of daily volatility (i.e. this month is much more or much less volatility than the last) will bias the clock usually only a little higher or lower, although historical volatility peaks/depressions will show the blue realized volatility score to be consistently high/low.

If requested I can change the look of the indicator or add input settings for the input length of clock, which for now is set to 20 bars, which is an approximation of the last month's realized volatility.

PineGIF - Display Gifs & Images In Tradingview [LuxAlgo]Pinescript is not designed to create or display images, let alone gifs, but it's very fun to try, and that's what this script does. This script allows the user to display three different gifs. In this post, we explain how we managed to display images/gif's using pinescript tables.

1. Image Pre-Processing

Due to pinescript limitations, we can't possibly display images with an excessively high resolution. As such we targeted pixel art as a primary image source. We used a pixel art gif of the magnificent Octocat (the mascot for the source-code hosting service GitHub) for our first try.

We first extract each frame from the gif and resize them to a 50x50 resolution which returns frames made of 2500 pixels. This process was done using python.

Getting Individual Pixels RGBA Values

Python can easily return a matrix containing each pixel's rgba value. For convenience, we converted the rgba values to hex.

We then create a simple code allowing us to return a pinescript array containing the 2500 pixel hex colors. We do this process for each frame.

2. Defining Table Cell Color

In the code, each frame is its own array. We create a new table with dimensions equal to len(frame1)^2 (we assume height = width).

The color of a cell is defined by the color of the image pixel at the same exact location. When a new bar is created, we do this exact process using a different frame which ultimately allows a new frame to be displayed.

3. Playing The GIFs

By default, the script will play the gif of the Tradingview cloud logo raining. In order to play the gif, simply use the replay mode. The replay speed allows the user to determine the frame rate (0.1 for the raining cloud and Nyan cat works best, 0.5 for Octocat).

We included the frames of the Octocat and Nyan cat gifs in the script.

4. Some Other Cool Images

Displaying static images is possible and involves the same process described above.

An original idea of the lizard, implemented by the wizard.

Bear & Bull Zone Signal StrategySince I love to mix and match, here is something fresh and that actually works on the breakout of Ethereum without losing your ass on lagging indicators.

It blends some of the nice parts of my previous scripts while moving to big boy pants with a twist on the Fibonacci retracement using SMA and EMA at multiple levels to do a sanity check.

Is it too good to be true? Nope, just what happens when a Solution Architect starts messing around with crypto and applies engineering and mathematics to the mix. You get a strategy that really doesn't have high profit losses when you tweak it just the right way.

What's the right tweak you ask?

1. Start with a 30 minute timeframe and set your window start date to the date the market began the bear or bull run

2. Make sure you can see your strategy performance window (not the graph one)

3. Set Stop Loss and Target Profit to 50%

4. Use your mouse wheel or up and down arrows and mess around with the RSI, go down one at a time but no lower than 7. Whichever value displayed the highest long or short gain is the one to pick.

5. Now select long or short only based on whichever one shows the highest gain.

6. Now go to K and D, leave K as 3 and check what happens when D is 4 or 5. Leave D at the value that gives you the highest gain.

7. Now go to EMA Fast and Slow Lengths. Leave Fast at 5 and check what happens when the Slow is moved up to 11 or 12, do the gains go up. If not, check what happens when Slow is moved down to 9, 8, or 7. Whichever gives you the highest gain, leave it there. Now go mess with the fast length, keep in mind that fast must always be less than slow. So check values down to 3 and up to 6. Same concept, mo money...leave it be.

8. Now go mess with the Target Profit, I start at 5, hit enter, then go to 7, hit enter, then 9...up by 2 until I get to 21 to make sure I don't hastily pick a low one and always keep in mind between which values the gain switched from high to low. For example, in this example I published at 11 it was $5k and at 13 it was $3700 for the gains. So after I got up to 21 I went back to 11 and started going up by 0.01 steps until the value dropped, which was at 11.19 so I set it at 11.18.

9. Now stop loss is trickier, you've maximized the gains, which means if you set the stop loss at a low value you will sacrifice gains. Typically by this point your loss is less than 10% with this script. So, my approach is to find the value where the stop loss doesn't change what I've tweaked already. In this example, I did the same start at 5 and go up by 2 and saw that when I went to 17 it stopped changing. So I started going back down by 0.5 and saw at 15.5 the gains went lower again. Now I started going back up in steps of 0.01 and at 15.98 it went back to the high gain I already tweaked for. I kept stop loss there and unleashed the strategy on ETH.

So far so good, no bad trades and it's been behaving pretty well.

Hammers & Stars StrategyOverview

This script trades basic hammer and shooting star candlestick patterns.

It's an extremely simple strategy with minimal filters, and according to my personal manual backtesting and automated trading results, performs best on the Daily chart on certain forex pairs.

It is intended to be traded on the forex markets but theoretically should work on all markets (especially if you optimize the settings).

The script also comes with complete AutoView automation for Oanda.

Make sure you've connected AutoView to TradingView and Oanda, then simply set an alert using the "alert() function calls only" condition and it will automatically execute trades based on whatever settings you've selected (only recommended for experienced traders - use at your own risk!)

If you're not sure how to set up AutoView, search "The Art of Trading AutoView Guide" on YouTube to find my detailed video guide.

Check out my website and YouTube channel for more information, scripts, resources and free Pine Script & trading lessons (link in my profile).

Best of luck with your trading!

- Matt / The Art of Trading

Settings Menu

Tooltips are included explaining what the various settings do, but here's a quick summary:

Strategy Settings

>= ATR Filter: Minimum size of entry candle compared to ATR

<= ATR Filter: Maximum size of entry candle compared to ATR

Stop Loss ATR: Stop loss multiplier (x ATR)

R:R: Risk:Reward profile

Fib Level: Used to calculate upper/lower third of candle. (For example, setting it to 0.5 will mean hammers must close >= 50% mark of the total candle size)

Start Date Filter: Date & time to begin trading from

End Date Filter: Date & time to stop trading

AutoView Oanda Settings

Use Oanda Demo: If turned on then oandapractice broker prefix will be used for AutoView alerts (demo account). If turned off then live account will be used

Use Limit Order: If turned on then AutoView will use limit orders. If turned off then market orders will be used (recommended to use limit order to mitigate spread issues)

Days To Leave Limit Order: This is your GTD setting (good til day)

Account Balance: Your account balance (used for calculating position size)

Account Currency: Your account balance currency (used for calculating position size)

Risk Per Trade %: Your risk per trade as a % of your account balance

Linear Stoch trendJust hybrid of Stoch RSI with linear regression trend indicator

to control linear regression -length set to 100 and deviation set to 0.5 (can be from 0 to any)

the stoch controlled by by the regukar way

Fibonacci levels alerted as Support and Resistance lvlsThis script is another Fibonacci script however this script gives select signals indicating when a resistance level is hit aswell as a support level.

A resistance level is calculated by price action failing to close or open above a fib level yet its high crossing the level. This essentially means price action was too weak to break this level.

The same goes for support levels where the price open and closes above the fib level yet the price low was below. This means the bears where unable to break the support level and may potentially rebound.

This script uses the 0.764, 0.618, 0.5, 0.382 and 0.236 levels. More can be added to script if asked.

From personal use I use the script to help guide the entry and exit for potential trades aswell as helping mark price targets and exit levels. However i never use this script alone and actively ensure it is used alongside other technical indicators.

Within the script there is also a plotted Fibonacci retracement chart which can help visually aid the trader.

Monte Carlo Range Forecast [DW]This is an experimental study designed to forecast the range of price movement from a specified starting point using a Monte Carlo simulation.

Monte Carlo experiments are a broad class of computational algorithms that utilize random sampling to derive real world numerical results.

These types of algorithms have a number of applications in numerous fields of study including physics, engineering, behavioral sciences, climate forecasting, computer graphics, gaming AI, mathematics, and finance.

Although the applications vary, there is a typical process behind the majority of Monte Carlo methods:

-> First, a distribution of possible inputs is defined.

-> Next, values are generated randomly from the distribution.

-> The values are then fed through some form of deterministic algorithm.

-> And lastly, the results are aggregated over some number of iterations.

In this study, the Monte Carlo process used generates a distribution of aggregate pseudorandom linear price returns summed over a user defined period, then plots standard deviations of the outcomes from the mean outcome generate forecast regions.

The pseudorandom process used in this script relies on a modified Wichmann-Hill pseudorandom number generator (PRNG) algorithm.

Wichmann-Hill is a hybrid generator that uses three linear congruential generators (LCGs) with different prime moduli.

Each LCG within the generator produces an independent, uniformly distributed number between 0 and 1.

The three generated values are then summed and modulo 1 is taken to deliver the final uniformly distributed output.

Because of its long cycle length, Wichmann-Hill is a fantastic generator to use on TV since it's extremely unlikely that you'll ever see a cycle repeat.

The resulting pseudorandom output from this generator has a minimum repetition cycle length of 6,953,607,871,644.

Fun fact: Wichmann-Hill is a widely used PRNG in various software applications. For example, Excel 2003 and later uses this algorithm in its RAND function, and it was the default generator in Python up to v2.2.

The generation algorithm in this script takes the Wichmann-Hill algorithm, and uses a multi-stage transformation process to generate the results.

First, a parent seed is selected. This can either be a fixed value, or a dynamic value.

The dynamic parent value is produced by taking advantage of Pine's timenow variable behavior. It produces a variable parent seed by using a frozen ratio of timenow/time.

Because timenow always reflects the current real time when frozen and the time variable reflects the chart's beginning time when frozen, the ratio of these values produces a new number every time the cache updates.

After a parent seed is selected, its value is then fed through a uniformly distributed seed array generator, which generates multiple arrays of pseudorandom "children" seeds.

The seeds produced in this step are then fed through the main generators to produce arrays of pseudorandom simulated outcomes, and a pseudorandom series to compare with the real series.

The main generators within this script are designed to (at least somewhat) model the stochastic nature of financial time series data.

The first step in this process is to transform the uniform outputs of the Wichmann-Hill into outputs that are normally distributed.

In this script, the transformation is done using an estimate of the normal distribution quantile function.

Quantile functions, otherwise known as percent-point or inverse cumulative distribution functions, specify the value of a random variable such that the probability of the variable being within the value's boundary equals the input probability.

The quantile equation for a normal probability distribution is μ + σ(√2)erf^-1(2(p - 0.5)) where μ is the mean of the distribution, σ is the standard deviation, erf^-1 is the inverse Gauss error function, and p is the probability.

Because erf^-1() does not have a simple, closed form interpretation, it must be approximated.

To keep things lightweight in this approximation, I used a truncated Maclaurin Series expansion for this function with precomputed coefficients and rolled out operations to avoid nested looping.

This method provides a decent approximation of the error function without completely breaking floating point limits or sucking up runtime memory.

Note that there are plenty of more robust techniques to approximate this function, but their memory needs very. I chose this method specifically because of runtime favorability.

To generate a pseudorandom approximately normally distributed variable, the uniformly distributed variable from the Wichmann-Hill algorithm is used as the input probability for the quantile estimator.

Now from here, we get a pretty decent output that could be used itself in the simulation process. Many Monte Carlo simulations and random price generators utilize a normal variable.

However, if you compare the outputs of this normal variable with the actual returns of the real time series, you'll find that the variability in shocks (random changes) doesn't quite behave like it does in real data.

This is because most real financial time series data is more complex. Its distribution may be approximately normal at times, but the variability of its distribution changes over time due to various underlying factors.

In light of this, I believe that returns behave more like a convoluted product distribution rather than just a raw normal.

So the next step to get our procedurally generated returns to more closely emulate the behavior of real returns is to introduce more complexity into our model.

Through experimentation, I've found that a return series more closely emulating real returns can be generated in a three step process:

-> First, generate multiple independent, normally distributed variables simultaneously.

-> Next, apply pseudorandom weighting to each variable ranging from -1 to 1, or some limits within those bounds. This modulates each series to provide more variability in the shocks by producing product distributions.

-> Lastly, add the results together to generate the final pseudorandom output with a convoluted distribution. This adds variable amounts of constructive and destructive interference to produce a more "natural" looking output.

In this script, I use three independent normally distributed variables multiplied by uniform product distributed variables.

The first variable is generated by multiplying a normal variable by one uniformly distributed variable. This produces a bit more tailedness (kurtosis) than a normal distribution, but nothing too extreme.

The second variable is generated by multiplying a normal variable by two uniformly distributed variables. This produces moderately greater tails in the distribution.

The third variable is generated by multiplying a normal variable by three uniformly distributed variables. This produces a distribution with heavier tails.

For additional control of the output distributions, the uniform product distributions are given optional limits.

These limits control the boundaries for the absolute value of the uniform product variables, which affects the tails. In other words, they limit the weighting applied to the normally distributed variables in this transformation.

All three sets are then multiplied by user defined amplitude factors to adjust presence, then added together to produce our final pseudorandom return series with a convoluted product distribution.

Once we have the final, more "natural" looking pseudorandom series, the values are recursively summed over the forecast period to generate a simulated result.

This process of generation, weighting, addition, and summation is repeated over the user defined number of simulations with different seeds generated from the parent to produce our array of initial simulated outcomes.

After the initial simulation array is generated, the max, min, mean and standard deviation of this array are calculated, and the values are stored in holding arrays on each iteration to be called upon later.

Reference difference series and price values are also stored in holding arrays to be used in our comparison plots.

In this script, I use a linear model with simple returns rather than compounding log returns to generate the output.

The reason for this is that in generating outputs this way, we're able to run our simulations recursively from the beginning of the chart, then apply scaling and anchoring post-process.

This allows a greater conservation of runtime memory than the alternative, making it more suitable for doing longer forecasts with heavier amounts of simulations in TV's runtime environment.

From our starting time, the previous bar's price, volatility, and optional drift (expected return) are factored into our holding arrays to generate the final forecast parameters.

After these parameters are computed, the range forecast is produced.

The basis value for the ranges is the mean outcome of the simulations that were run.

Then, quarter standard deviations of the simulated outcomes are added to and subtracted from the basis up to 3σ to generate the forecast ranges.

All of these values are plotted and colorized based on their theoretical probability density. The most likely areas are the warmest colors, and least likely areas are the coolest colors.

An information panel is also displayed at the starting time which shows the starting time and price, forecast type, parent seed value, simulations run, forecast bars, total drift, mean, standard deviation, max outcome, min outcome, and bars remaining.

The interesting thing about simulated outcomes is that although the probability distribution of each simulation is not normal, the distribution of different outcomes converges to a normal one with enough steps.

In light of this, the probability density of outcomes is highest near the initial value + total drift, and decreases the further away from this point you go.

This makes logical sense since the central path is the easiest one to travel.

Given the ever changing state of markets, I find this tool to be best suited for shorter term forecasts.

However, if the movements of price are expected to remain relatively stable, longer term forecasts may be equally as valid.

There are many possible ways for users to apply this tool to their analysis setups. For example, the forecast ranges may be used as a guide to help users set risk targets.

Or, the generated levels could be used in conjunction with other indicators for meaningful confluence signals.

More advanced users could even extrapolate the functions used within this script for various purposes, such as generating pseudorandom data to test systems on, perform integration and approximations, etc.

These are just a few examples of potential uses of this script. How you choose to use it to benefit your trading, analysis, and coding is entirely up to you.

If nothing else, I think this is a pretty neat script simply for the novelty of it.

----------

How To Use:

When you first add the script to your chart, you will be prompted to confirm the starting date and time, number of bars to forecast, number of simulations to run, and whether to include drift assumption.

You will also be prompted to confirm the forecast type. There are two types to choose from:

-> End Result - This uses the values from the end of the simulation throughout the forecast interval.

-> Developing - This uses the values that develop from bar to bar, providing a real-time outlook.

You can always update these settings after confirmation as well.

Once these inputs are confirmed, the script will boot up and automatically generate the forecast in a separate pane.

Note that if there is no bar of data at the time you wish to start the forecast, the script will automatically detect use the next available bar after the specified start time.

From here, you can now control the rest of the settings.

The "Seeding Settings" section controls the initial seed value used to generate the children that produce the simulations.

In this section, you can control whether the seed is a fixed value, or a dynamic one.

Since selecting the dynamic parent option will change the seed value every time you change the settings or refresh your chart, there is a "Regenerate" input built into the script.

This input is a dummy input that isn't connected to any of the calculations. The purpose of this input is to force an update of the dynamic parent without affecting the generator or forecast settings.

Note that because we're running a limited number of simulations, different parent seeds will typically yield slightly different forecast ranges.

When using a small number of simulations, you will likely see a higher amount of variance between differently seeded results because smaller numbers of sampled simulations yield a heavier bias.

The more simulations you run, the smaller this variance will become since the outcomes become more convergent toward the same distribution, so the differences between differently seeded forecasts will become more marginal.

When using a dynamic parent, pay attention to the dispersion of ranges.

When you find a set of ranges that is dispersed how you like with your configuration, set your fixed parent value to the parent seed that shows in the info panel.

This will allow you to replicate that dispersion behavior again in the future.

An important thing to note when settings alerts on the plotted levels, or using them as components for signals in other scripts, is to decide on a fixed value for your parent seed to avoid minor repainting due to seed changes.

When the parent seed is fixed, no repainting occurs.

The "Amplitude Settings" section controls the amplitude coefficients for the three differently tailed generators.

These amplitude factors will change the difference series output for each simulation by controlling how aggressively each series moves.

When "Adjust Amplitude Coefficients" is disabled, all three coefficients are set to 1.

Note that if you expect volatility to significantly diverge from its historical values over the forecast interval, try experimenting with these factors to match your anticipation.

The "Weighting Settings" section controls the weighting boundaries for the three generators.

These weighting limits affect how tailed the distributions in each generator are, which in turn affects the final series outputs.

The maximum absolute value range for the weights is . When "Limit Generator Weights" is disabled, this is the range that is automatically used.

The last set of inputs is the "Display Settings", where you can control the visual outputs.

From here, you can select to display either "Forecast" or "Difference Comparison" via the "Output Display Type" dropdown tab.

"Forecast" is the type displayed by default. This plots the end result or developing forecast ranges.

There is an option with this display type to show the developing extremes of the simulations. This option is enabled by default.

There's also an option with this display type to show one of the simulated price series from the set alongside actual prices.

This allows you to visually compare simulated prices alongside the real prices.

"Difference Comparison" allows you to visually compare a synthetic difference series from the set alongside the actual difference series.

This display method is primarily useful for visually tuning the amplitude and weighting settings of the generators.

There are also info panel settings on the bottom, which allow you to control size, colors, and date format for the panel.

It's all pretty simple to use once you get the hang of it. So play around with the settings and see what kinds of forecasts you can generate!

----------

ADDITIONAL NOTES & DISCLAIMERS

Although I've done a number of things within this script to keep runtime demands as low as possible, the fact remains that this script is fairly computationally heavy.

Because of this, you may get random timeouts when using this script.

This could be due to either random drops in available runtime on the server, using too many simulations, or running the simulations over too many bars.

If it's just a random drop in runtime on the server, hide and unhide the script, re-add it to the chart, or simply refresh the page.

If the timeout persists after trying this, then you'll need to adjust your settings to a less demanding configuration.

Please note that no specific claims are being made in regards to this script's predictive accuracy.

It must be understood that this model is based on randomized price generation with assumed constant drift and dispersion from historical data before the starting point.

Models like these not consider the real world factors that may influence price movement (economic changes, seasonality, macro-trends, instrument hype, etc.), nor the changes in sample distribution that may occur.

In light of this, it's perfectly possible for price data to exceed even the most extreme simulated outcomes.

The future is uncertain, and becomes increasingly uncertain with each passing point in time.

Predictive models of any type can vary significantly in performance at any point in time, and nobody can guarantee any specific type of future performance.

When using forecasts in making decisions, DO NOT treat them as any form of guarantee that values will fall within the predicted range.

When basing your trading decisions on any trading methodology or utility, predictive or not, you do so at your own risk.

No guarantee is being issued regarding the accuracy of this forecast model.

Forecasting is very far from an exact science, and the results from any forecast are designed to be interpreted as potential outcomes rather than anything concrete.

With that being said, when applied prudently and treated as "general case scenarios", forecast models like these may very well be potentially beneficial tools to have in the arsenal.

FIBS S/R IndicatorHello,

I've decided to publish a new script. The previous version of this script was removed by admins for breaking community rules.

So I present to you the Fibonacci Support / Resistance.

1. How does it work

Ratio plots

I first take the input of pivot look back and search for pivots high and low.

And then it takes a second look back to search highest high and lowest low to establish the top bottom range.

Then using the top and bottom I plot ratios provided as input. Defaults to most relevant 5 ratios I've found (Fibonacci):

Ratio 0 = 0 - can't be changed

Ratio 1 = 0.5

Ratio 2 = 0.618

Ratio 3 = 1

Ratio 4 = 1.618

Ratio 5 = 2.618

Any changes done to these ratios should be in order, otherwise conditions could get messed up. So R1 needs to the lowest and R5 the highest.

Also the same ratios are used in reverse as negative ratios.

There is a option to plot all ratios but gets really confusing for me but maybe for you it works. By default there are certain conditions set so that as we go up new resistance ratio get displayed and as we go down we see new resistance plots.

Trendlines

I've also added some automatic trendline plots with breakout warning labels based on the pivots high and low. Start and end for trendlines can be changed via inputs.

Labels can be deactivated via input. On a older version the trendlines and labels where not removed from the chart but I felt like there was to much information.

Overcooked/Undercooked

I've also added some fills and background colors that indicate if the price action is over R5 or under Negative R5 ratios. This usually indicates some "overcooking" or "undecooking".

I've notices that after "crossunder"/"crossover" top bottom ratios it goes in consolidation or it dumps. So then I plot a bgcolor to signal that.

2. How to use it

Using plot lines we can determine where we have support and resistance. I found that the best way to use the default ratios values is on the 1H chart. Very good for trading on crypto because of current situation in the market where there is a lot of new people entering the space and volatility and sentiment make swings respect the Fibonacci ratios.

3. Examples

For instance lets look at BINANCE:BTCUSDT .

On the left we see that the price action between 20 and 21 February was "overcooked". So after we got the signal that we "crossunder" the R5 the signal was triggered and we got a small red candle followed by a small dip and after that we got a small bounce and a dump.

If we also look at MF-RSI we can also see we got multiple bear divs.

Lets entertain the idea that we went short at ~57.1k as soon as we get signaled and it starts dumping.

Where does it stop ?

We can see it went all the way down to Negative R5 ratio. Normally that should signal "undercooking" but this was not triggered as it did not close under it (signaled in green).

We can also see that previous support now becomes resistance (signaled in red).

If we take a look at BINANCE:ETHUSDT , we do see that the "undercooking" was triggered here.

I will be publishing a more detailed Idea with examples of using this on the BINANCE:BTCUSDT chart in combination with Volume and other technical analysis.

Use with caution, this is not 100% signal indicator as the markets do what they want. But by using this in combination with other indicators like MF-RSI, EMAs and regular patterns we can get some targets for Support/Resistance.

I'm trying to create a strategy based on this indicator but I'm not getting very good results. Best results were on the 15 min chart with gross profits around ~50%.

Please try to play around with the inputs and let me know if you find something interesting, maybe I can incorporate new features in the indicator.

You can find the MF-RSI indicator here

Spitznagel ROICThis is a rough version of the Return on Invested Capital metric that Mark Spitznagel presents in The Dao of Capital. The purpose is to calculate the return on real invested capital, conservatively calculated. Over a medium term horizon, the theory is that companies which have a high ROIC (presented here as a decimal value where 0.5 = 50%, 1 = 100%, etc., and color coded as a general guide) combined with a low Faustmann Ratio (see my other script) should generally outperform. Please don't take this short summary as an excuse to not read the full book. It's well worth your time. (I am not affiliated with the author in any way.)

ABUs EurorampThis strategy backtests the opening ramp of Europe at 9am European time, which is 2am Chicago time ( CME ES timezone ) on the ES Futures Contract.

The following conditions are embedded in the strategy:

- Market entry at 2 am Chicago time

- Size = 2 contracts

- Stop = -5 points

- TP 1 = +3 points (1 Contract)

- Stop to Break even (entry + 0.5) after TP 1 is reached

- Set a TP 2 stop to +5 if entry is +10 points

- Close all positions EOD RTH

As the script entry / stops / TPs work on candle closes, best is to use the strategy on the 5min chart.