Multi-TimeCycles SMT Live DetectorThis indicator is a multi-asset, multi-timeframe SMT Live detector designed to work on any symbol (indices, futures, FX, crypto, stocks).

It compares your chart symbol against up to two custom comparison symbols and automatically detects bullish and bearish SMT divergences across:

90-minute session blocks (Asia, London, NY – with internal 90m sessions)

60-minute (hourly) cycles

30-minute cycles

10-minute cycles

3-minute cycles

Each SMT is plotted as a line between the reference high/low and the current high/low, with a clear text label showing:

Timecycle (90m / 60m / 30m / 10m / 3m)

Which comparison asset(s) created the divergence (e.g., ES, YM, ES/YM or your custom labels)

The 90-minute SMT module is session-aware using New York time:

Asia: 18:00 – 02:29 NY time

London A/M/D

NY AM A/M/D

NY PM A/M/D

ابحث في النصوص البرمجية عن "Cycle"

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Gann Seasonal Dates - CEGann Seasonal Dates - Community Edition

Welcome to the Gann Seasonal Dates V1.61 - Community Edition, a powerful tool designed to enhance time-based trading with W.D. Gann’s seasonal date methodology. This feature-complete indicator allows traders to plot critical seasonal dates on charts for equities, forex, commodities, and cryptocurrencies. It empowers traders to anticipate market turning points with precision.

Overview

The Gann Seasonal Dates plots Gann’s major and minor seasonal dates, which are rooted in the cyclical nature of solstices, equinoxes, and their midpoints. Major dates include the vernal equinox (March 21st), summer solstice (June 22nd), autumnal equinox (September 23rd), and winter solstice (December 22nd). Minor dates mark the halfway points between these events (February 4th, May 6th, July 23rd, August 8th, November 7th, and November 22nd). With customizable styling and historical data up to 50 years, this script helps traders identify key time-based market events.

Key Features

Major and Minor Seasonal Dates : Plot four major dates (solstices and equinoxes) and six minor dates (midpoints) to highlight potential market turning points.

Customizable Date Selection : Enable or disable individual major and minor dates to focus on specific cycles relevant to your analysis.

Historical Data Range : Adjust the lookback period up to 50 years, with recommendations for optimal performance based on your TradingView plan (5 years for Basic, 20 for Pro/Pro+/Premium).

Styling Options : Customize line styles (solid, dotted, dashed) and colors for major and minor dates to enhance chart clarity.

Labeled Visuals : Each plotted date includes a label with a tooltip (e.g., "Vernal equinox") for easy identification and context.

How It Works

Configure Settings : Enable major and/or minor dates and select specific dates (e.g., March 21st, February 4th) to display on your chart.

Set Historical Range : Adjust the years of data (up to 50) to plot historical seasonal dates, ensuring compatibility with your TradingView plan’s processing limits.

Customize Styling : Choose line styles and colors for major and minor dates to differentiate them visually.

Analyze and Trade : Use the plotted vertical lines and labels to identify potential market turning points, integrating Gann’s time-based cycles into your strategy.

Get Started

As a gift to the TradingView community and Gann traders, the Gann Seasonal Dates - Community Edition is provided free of charge. With no features locked, this tool offers full access to Gann’s seasonal date methodology for precise time-based analysis. Trade wisely and leverage the power of seasonal cycles!

Vibration BoxFirst Public release of the Vibration Box

WARNING - THESE CYCLES CANNOT PREDICT PERFECT "UP & DOWN" MOTION

There is absolutely no guarantee that these cycles will predict perfect "up & down" motion for the markets

Please be aware that this tool is to be used with a robust risk management system

These cycles are representative of "circle geometry within a square of price & time"

Slowly, I will build up some ideas to go along with this script so that you can learn to apply it to many different markets in many different ways

Those familiar with the work of W.D. Gann should be able to utilize this tool in many different ways

Instructions:

Place the box down with 2 mouse clicks (first is for bottom left corner & second is for top right corner)

NOTE: DUE TO TRADINGVIEW LIMITATIONS

-There is a maximum of 12 divisions for your box/vibration (I will work on increasing this number)

-You MUST choose a coordinate that is within the price action that has already occurred

-You CANNOT initially place the box BEFORE THE FIRST BAR of data

-You CANNOT initially place the box BEYOND THE LAST BAR of data

THEN, ONCE YOU HAVE PLACED THE BOX FOR THE FIRST TIME

YOU CAN MANUALLY ADJUST THE DATES WITHIN THE SETTINGS TO PLACE THE BOX IN ANYWAY YOU WOULD LIKE!

ALT Risk Metric StrategyHere's a professional write-up for your ALT Risk Strategy script:

ALT/BTC Risk Strategy - Multi-Crypto DCA with Bitcoin Correlation Analysis

Overview

This strategy uses Bitcoin correlation as a risk indicator to time entries and exits for altcoins. By analyzing how your chosen altcoin performs relative to Bitcoin, the strategy identifies optimal accumulation periods (when alt/BTC is oversold) and profit-taking opportunities (when alt/BTC is overbought). Perfect for traders who want to outperform Bitcoin by strategically timing altcoin positions.

Key Innovation: Why Alt/BTC Matters

Most traders focus solely on USD price, but Alt/BTC ratios reveal true altcoin strength:

When Alt/BTC is low → Altcoin is undervalued relative to Bitcoin (buy opportunity)

When Alt/BTC is high → Altcoin has outperformed Bitcoin (take profits)

This approach captures the rotation between BTC and alts that drives crypto cycles

Key Features

📊 Advanced Technical Analysis

RSI (60% weight): Primary momentum indicator on weekly timeframe

Long-term MA Deviation (35% weight): Measures distance from 150-period baseline

MACD (5% weight): Minor confirmation signal

EMA Smoothing: Filters noise while maintaining responsiveness

All calculations performed on Alt/BTC pairs for superior market timing

💰 3-Tier DCA System

Level 1 (Risk ≤ 70): Conservative entry, base allocation

Level 2 (Risk ≤ 50): Increased allocation, strong opportunity

Level 3 (Risk ≤ 30): Maximum allocation, extreme undervaluation

Continuous buying: Executes every bar while below threshold for true DCA behavior

Cumulative sizing: L3 triggers = L1 + L2 + L3 amounts combined

📈 Smart Profit Management

Sequential selling: Must complete L1 before L2, L2 before L3

Percentage-based exits: Sell portions of position, not fixed amounts

Auto-reset on re-entry: New buy signals reset sell progression

Prevents premature full exits during volatile conditions

🤖 3Commas Automation

Pre-configured JSON webhooks for Custom Signal Bots

Multi-exchange support: Binance, Coinbase, Kraken, Bitfinex, Bybit

Flexible quote currency: USD, USDT, or BUSD

Dynamic order sizing: Automatically adjusts to your tier thresholds

Full webhook documentation compliance

🎨 Multi-Asset Support

Pre-configured for popular altcoins:

ETH (Ethereum)

SOL (Solana)

ADA (Cardano)

LINK (Chainlink)

UNI (Uniswap)

XRP (Ripple)

DOGE

RENDER

Custom option for any other crypto

How It Works

Risk Metric Calculation (0-100 scale):

Fetches weekly Alt/BTC price data for stability

Calculates RSI, MACD, and deviation from 150-period MA

Normalizes MACD to 0-100 range using 500-bar lookback

Combines weighted components: (MACD × 0.05) + (RSI × 0.60) + (Deviation × 0.35)

Applies 5-period EMA smoothing for cleaner signals

Color-Coded Risk Zones:

Green (0-30): Extreme buying opportunity - Alt heavily oversold vs BTC

Lime/Yellow (30-70): Accumulation range - favorable risk/reward

Orange (70-85): Caution zone - consider taking initial profits

Red/Maroon (85-100+): Euphoria zone - aggressive profit-taking

Entry Logic:

Buys execute every candle when risk is below threshold

As risk decreases, position sizing automatically scales up

Example: If risk drops from 60→25, you'll be buying at L1 rate until it hits 50, then L2 rate, then L3 rate

Exit Logic:

Sells only trigger when in profit AND risk exceeds thresholds

Sequential execution ensures partial profit-taking

If new buy signal occurs before all sells complete, sell levels reset to L1

Configuration Guide

Choosing Your Altcoin:

Select crypto from dropdown (or use CUSTOM for unlisted coins)

Pick your exchange

Choose quote currency (USD, USDT, BUSD)

Risk Metric Tuning:

Long Term MA (default 150): Higher = more extreme signals, Lower = more frequent

RSI Length (default 10): Lower = more volatile, Higher = smoother

Smoothing (default 5): Increase for less noise, decrease for faster reaction

Buy Settings (Aggressive DCA Example):

L1 Threshold: 70 | Amount: $5

L2 Threshold: 50 | Amount: $6

L3 Threshold: 30 | Amount: $7

Total L3 buy = $18 per candle when deeply oversold

Sell Settings (Balanced Exit Example):

L1: 70 threshold, 25% position

L2: 85 threshold, 35% position

L3: 100 threshold, 40% position (final exit)

3Commas Setup

Bot Configuration:

Create Custom Signal Bot in 3Commas

Set trading pair to your altcoin/USD (e.g., ETH/USD, SOL/USDT)

Order size: Select "Send in webhook, quote" to use strategy's dollar amounts

Copy Bot UUID and Secret Token

Script Configuration:

Paste credentials into 3Commas section inputs

Check "Enable 3Commas Alerts"

Save and apply to chart

TradingView Alert:

Create Alert → Condition: "alert() function calls only"

Webhook URL: api.3commas.io

Enable "Webhook URL" checkbox

Expiration: Open-ended

Strategy Advantages

✅ Outperform Bitcoin: Designed specifically to beat BTC by timing alt rotations

✅ Capture Alt Seasons: Automatically accumulates when alts lag, sells when they pump

✅ Risk-Adjusted Sizing: Buys more when cheaper (better risk/reward)

✅ Emotional Discipline: Systematic approach removes fear and FOMO

✅ Multi-Asset: Run same strategy across multiple altcoins simultaneously

✅ Proven Indicators: Combines RSI, MACD, and MA deviation - battle-tested tools

Backtesting Insights

Optimal Timeframes:

Daily chart: Best for backtesting and signal generation

Weekly data is fetched internally regardless of display timeframe

Historical Performance Characteristics:

Accumulates heavily during bear markets and BTC dominance periods

Captures explosive altcoin rallies when BTC stagnates

Sequential selling preserves capital during extended downtrends

Works best on established altcoins with multi-year history

Risk Considerations:

Requires capital reserves for extended accumulation periods

Some altcoins may never recover if fundamentals deteriorate

Past correlation patterns may not predict future performance

Always size positions according to personal risk tolerance

Visual Interface

Indicator Panel Displays:

Dynamic color line: Green→Lime→Yellow→Orange→Red as risk increases

Horizontal threshold lines: Dashed lines mark your buy/sell levels

Entry/Exit labels: Green labels for buys, Orange/Red/Maroon for sells

Real-time risk value: Numerical display on price scale

Customization:

All threshold lines are adjustable via inputs

Color scheme clearly differentiates buy zones (green spectrum) from sell zones (red spectrum)

Line weights emphasize most extreme thresholds (L3 buy and L3 sell)

Strategy Philosophy

This strategy is built on the principle that altcoins move in cycles relative to Bitcoin. During Bitcoin rallies, alts often bleed against BTC (high sell, accumulate). When Bitcoin consolidates, alts pump (take profits). By measuring risk on the Alt/BTC chart instead of USD price, we time these rotations with precision.

The 3-tier system ensures you're always averaging in at better prices and scaling out at better prices, maximizing your Bitcoin-denominated returns.

Advanced Tips

Multi-Bot Strategy:

Run this on 5-10 different altcoins simultaneously to:

Diversify correlation risk

Capture whichever alt is pumping

Smooth equity curve through rotation

Pairing with BTC Strategy:

Use alongside the BTC DCA Risk Strategy for complete portfolio coverage:

BTC strategy for core holdings

ALT strategies for alpha generation

Rebalance between them based on BTC dominance

Threshold Calibration:

Check 2-3 years of historical data for your chosen alt

Note where risk metric sat during major bottoms (set buy thresholds)

Note where it peaked during euphoria (set sell thresholds)

Adjust for your risk tolerance and holding period

Credits

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Technical Analysis Framework: RSI, MACD, Moving Average theory

Implementation: pommesUNDwurst

Disclaimer

This strategy is for educational purposes only. Cryptocurrency trading involves substantial risk of loss. Altcoins are especially volatile and many fail completely. The strategy assumes liquid markets and reliable Alt/BTC price data. Always do your own research, understand the fundamentals of any asset you trade, and never risk more than you can afford to lose. Past performance does not guarantee future results. The authors are not financial advisors and assume no liability for trading decisions.

Additional Warning: Using leverage or trading illiquid altcoins amplifies risk significantly. This strategy is designed for spot trading of established cryptocurrencies with deep liquidity.

Tags: Altcoin, Alt/BTC, DCA, Risk Metric, Dollar Cost Averaging, 3Commas, ETH, SOL, Crypto Rotation, Bitcoin Correlation, Automated Trading, Alt Season

Feel free to modify any sections to better match your style or add specific backtesting results you've observed! 🚀Claude is AI and can make mistakes. Please double-check responses. Sonnet 4.5

IPDA Time High/L🧭 IPDA Time Pivot High/Low (3•6•9)

Precision timing meets liquidity delivery.

🔹 Concept

This tool is built on the idea that price is delivered by time, not structure — a core belief in Zeussy/Smart Money–style analysis.

Certain time signatures, known as IPDA times (where the digits of hour and minute reduce to 3, 6, or 9), often align with reversals, traps, or accelerations in market delivery.

These times represent rhythmic energy cycles in algorithmic delivery, marking when liquidity is often redistributed.

🔹 What the Indicator Does

Scans your selected time window (default: 9:00–11:00, New York).

Identifies candles forming micro pivots — a candle that’s higher or lower than both its immediate neighbors.

Filters only those pivots that occur at IPDA times (digital roots of 3, 6, or 9).

Prints a clean, minimal time label (HH:MM) above or below each qualifying candle.

Labels dynamically adjust to your chart’s timezone and vertical spacing for clarity.

🔹 Why It’s Useful

These moments often align with:

Engineered traps during liquidity hunts.

Session transitions (e.g., London → NY Open).

Delivery shifts where price changes direction into the Draw on Liquidity (DOL).

By highlighting only precise, time-based pivots, this indicator helps traders:

Anticipate timing-based reversals,

Align narrative with smart-money delivery cycles,

And build refined entries within the NY AM session.

🔹 How to Use

Apply the indicator to your chart.

Set the timezone (default: America/New_York).

Focus on your session window (e.g., 09:00–11:00).

Observe when price reaches your POI or liquidity pool during an IPDA time — those candles are often where manipulation or delivery begins.

Combine with your own narrative tools (SMT, CISD, DOL, POI) for confirmation.

🔹 Features

Automatic timezone alignment

Adjustable session hours

Transparent, minimalistic time labels

Custom label size & offset for clean chart aesthetics

Works on all intraday timeframes

🔹 Philosophy

“Price is delivered by time, not structure.”

— Zeussy

This indicator was designed for traders who study timing as a function of delivery,

not just structure — allowing you to see when the algorithm intends to act.

Nancy's All-In-One [Private] [Institutional]A Private Institutional Tool by Design

PRIVATE ACCESS ONLY

This script is not for public usage or those casually scrolling through the indicator library. This is a private tool, built for precision, and extremely powerful in the wrong hands. Used properly, it can unlock financial freedom yes, it’s that potent.

“This is the closest you’ll get to peeking behind the curtain of institutional strategy without having a Bloomberg terminal or a Wall Street badge.”

– KC Research

What It Does

The Nancy All-In-One is the culmination of thousands of hours of backtesting, real-world application, and tactical insights drawn from elite strategies used at places like Renaissance Technologies, proprietary desks, and private equity firms.

This version fuses:

DTT Root Candles & Time-Zone Price Levels (including NY Judas, Kyoto, Osaka, etc.)

Intraday Sessions & Micro Box Models (Turncoat, Bishop, Knight, Big Ben, etc.)

Quarterly Micro Cycles — breaks down time into high-probability 90-minute blocks

Fib-Based Inner Intervals — ideal for sniper-level scalps or early entries

SMT Divergences, PD High/Low, NWOG/NDOG/EHPDA setups

Multi-Timeframe Visualization (with user control over display resolution)

Every line, label, and box drawn has a purpose, engineered to expose fractal imbalances, liquidity traps, and premium/discount zones with surgical accuracy.

How to Use It

Use the 1M or 5M chart — This script was optimized with lower-timeframe precision in mind. It works higher up, but that’s not its primary edge.

Turn on sessions you want under Turn Modules On group. Each session represents a model with its own behavior (e.g. Osaka Model = Asia liquidity expansion).

Price Lines — The "DTT Root Candles" levels are critical. These are not random timestamps—they represent algorithmic triggers derived from real volume and timing analysis.

Quarterly Cycles — Use these to trade from zone-to-zone with context. Each 90-minute block often contains a reversal, breakout, or liquidity sweep.

SMT, PDHL, NWOG, NDOG — These are best used with confluence. The more boxes and lines that agree, the higher your confidence.

Built for Traders Who Know the Game

This is not a magic button. It’s a complex system that assumes you're willing to study it, adapt it, and integrate it into your own strategy. It’s a tool—not a signal generator. It won't tell you when to buy or sell, but it will show you exactly where institutions are hunting.

Settings & Customization

You can toggle each element on/off to declutter your chart.

Change label sizes, opacity, and styles to suit your preferences.

Adjust session times if you're not in EST (UTC-5 default).

Works Best With:

1M to 15M charts (although elements scale up)

Liquid FX pairs, indices (SPX, NAS100), BTC, and ETH

Time-sensitive entries (news, killzones, session opens)

Final Note

This was developed internally by Nancy and private anon entities, and is still being actively expanded. Portions of the code are open-source, but most logic is proprietary and reverse-engineering resistant.

If you don’t know what NWOG, EQH/PDH, or SMT are—this isn’t for you. If you do... welcome to the other side.

Planetary Speed - CEPlanetary Speed - Community Edition

Welcome to the Planetary Speed - Community Edition , a specialized tool designed to enhance W.D. Gann-inspired trading by plotting the speed of selected planets. This indicator measures changes in planetary ecliptic longitudes, which may correlate with market timing and volatility, making it ideal for traders analyzing equities, forex, commodities, and cryptocurrencies.

Overview

The Planetary Speed - Community Edition calculates the speed of a chosen planet (Mercury, Venus, Mars, Jupiter, Saturn, Uranus, Neptune, or Pluto) by comparing its ecliptic longitude across time. Supporting heliocentric and geocentric modes, the script plots speed data with high precision across various chart timeframes, particularly for markets open 24/7 like cryptocurrencies. Traders can customize line colors and add multiple instances for multi-planet analysis, aligning with Gann’s belief that planetary cycles influence market trends.

Key Features

Plots the speed of eight planets (Mercury, Venus, Mars, Jupiter, Saturn, Uranus, Neptune, Pluto) based on ecliptic longitude changes

Supports heliocentric and geocentric modes for flexible analysis

Customizes line colors for clear visualization of planetary speed data

Projects future speed data up to 250 days with daily resolution

Works across default TradingView timeframes (except monthly) for continuous markets

Enables multiple script instances for tracking different planets on the same chart

How to Use

Access the script’s settings to configure preferences

Choose a planet from Mercury, Venus, Mars, Jupiter, Saturn, Uranus, Neptune, or Pluto

Select heliocentric or geocentric mode for calculations

Customize the line color for speed data visualization

Review plotted speed data to identify potential market timing or volatility shifts

Add multiple instances to track different planets simultaneously

Get Started

The Planetary Speed - Community Edition provides full functionality for astrological market analysis. Designed to highlight Gann’s planetary cycles, this tool empowers traders to explore celestial influences. Trade wisely and harness the power of planetary speed!

Time Block with Current K-Line TimeThis indicator divides the market into fixed time blocks (daily, three-day, weekly, monthly, and yearly) and displays 1/4, 1/2, and 3/4 dividing lines within each block, indicating key price positions within the block.

————————————

Description:

1. Generally speaking, the duration of a market period is one time block within the corresponding period.

2. Supports display of the current candlestick time, the dividing line for the next block, and a countdown.

3. Multi-time zone support: Shanghai, New York, London, Tokyo, and UTC. Time display automatically adapts to the selected time zone.

4. Time block visualization: Select the time block length based on the observation period and draw dividers at the time block boundaries.

5. Real-time time display: Detailed time of the current candlestick chart (year/month/day, hour:minute, day of the week).

6. Future time prediction: Displays the next time block's start position with a future divider. A countdown function displays the time until the next block, helping to determine the remaining duration of the current trend.

————————————

Use scenarios:

Day trading: Identify trading day boundaries (1-day blocks)

Swing trading: Optimize weekly/monthly time frame transitions (1-week/1-month blocks)

Long-term investment: Observe annual market cycles (1-year blocks)

Cross-time zone trading: Seamlessly switch between major global trading time zones.

————————————

Functions:

- Time block division to observe market cycles

- Draw 1/4, 1/2, and 3/4 dividers to assist in trading decisions

- Current K-line Time Display

- Future Block Divider and Countdown Indicator

————————————

How to Use:

Can be combined with trend lines or other trend-following tools to identify trend-following entry opportunities near the dividing line and follow the main trend.

——————————————————————————————————————————————————————————

本指标将行情划分为固定时间区块(日、三日、周、月、年),并在每个区块内显示1/4、1/2、3/4分割线,标示区块内关键价格位置

————————————

描述:

1. 通常而言,一段行情的持续时间为对应周期下的一个时间区块

2. 支持显示当前K线时间及下一个区块的分割线和倒计时。

3. 多时区支持,支持上海、纽约、伦敦、东京、UTC五大交易时区,自适应所选时区的时间显示

4. 时间区块可视化:根据观测周期选择时间区块长度,在时间区块边界绘制分隔线

5. 实时时间显示:当前K线详细时间(年/月/日 时:分 星期)

6. 未来时间预测,下一个时间区块开始位置显示未来分割线,倒计时功能显示距离下个区块的时间,用于辅助判断当前趋势的剩余持续时间

————————————

使用场景:

日内交易:识别交易日边界(1日区块)

波段交易:把握周/月时间框架转换(1周/1月区块)

长期投资:观察年度市场周期(1年区块)

跨时区交易:无缝切换全球主要交易时区

————————————

功能:

- 时间区块划分,观察行情周期

- 绘制1/4、1/2、3/4分割线,辅助交易判断

- 当前K线时间显示

- 未来区块分割线及倒计时提示

————————————

使用方法:

可结合趋势线或其他趋势跟随工具,在分割线附近寻找顺势进场机会,追随主趋势

CVDD Z-ScoreCumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Now with the automatic Z-Score calculation for ease of classification of Bitcoin's valuation according to this metric.

Created for TRW.

Risk On/Off Index [SwissAlgo]Risk On/Off Index - Sector Rotation Analysis

----------------------------------------------------

What it does:

This indicator estimates market risk appetite by comparing the weighted performance of growth/cyclical sectors (Risk-On) against defensive sectors (Risk-Off).

It provides a normalized oscillator that ranges from -1 (extreme risk-off) to +1 (extreme risk-on), which may help traders identify potential shifts in market sentiment and sector rotation patterns.

The analysis examines whether institutional money flows favor aggressive growth assets or seek safety in defensive positions, potentially offering insights into the underlying risk tolerance that drives market movements. When properly interpreted alongside other analyses, this information could assist in understanding broader market cycles and sentiment transitions.

----------------------------------------------------

How it works:

The indicator analyzes 11 major sector ETFs weighted by their actual market capitalization representation:

Risk-On sectors (70% weight) : Technology (28%), Financials (11%), Consumer Discretionary (10%), Communication (9%), Industrials (8%), Energy (4%), Materials (2.5%), Real Estate (2%)

Risk-Off sectors (30% weight) : Healthcare (13%), Consumer Staples (6%), Utilities (2.5%)

The algorithm calculates the weighted performance difference over your selected timeframe (7 days to 12 months) and normalizes it using three methods: Simple Difference, Tanh Normalized, or Historical Range. A 7-period EMA smooths the signal, while a longer signal line (default 50) provides trend context.

----------------------------------------------------

Visual Features:

Main curve (Risk Appetite Delta) : The primary line shows the smoothed (7-period EMA) risk appetite reading. When above zero, growth sectors are outperforming defensive sectors (risk-on sentiment). When below zero, defensive sectors are outperforming growth sectors (risk-off sentiment).

Signal line : A longer EMA (default 50-period) of the risk appetite data that represents the underlying trend. Crossovers between the main curve and signal line may indicate potential momentum shifts in market sentiment (potential long signal when the crossover happens in extreme risk-off zones, and potential short signal when the crossunder occurs in extreme risk-on zones)

Dynamic color coding : The main curve color reflects both position and momentum:

Red : Risk-on territory (>0) with strengthening momentum (above signal line)

Green : Risk-on territory (>0) but weakening momentum (below signal line) - potential reversal warning

Maroon : Risk-off territory (<0) but strengthening momentum (above signal line) - potential reversal warning

Lime : Risk-off territory (<0) with strengthening momentum (below signal line)

Gradient background zones : Subtle fills indicate risk appetite intensity levels from moderate (0 to ±0.25) through strong (±0.25 to ±0.5) to extreme (±0.5 to ±1.0)

Sector breakdown table : Shows individual sector performance with clear Risk-On/Risk-Off categorization

Reference levels : Horizontal lines mark neutral (0), strong (±0.5), and extreme (±1) risk appetite zones

This color system allows traders to quickly assess not just current sentiment (above/below zero) but also whether that sentiment is strengthening or potentially reversing based on the relationship with the signal line.

----------------------------------------------------

Who may benefit:

Portfolio managers rotating between growth and defensive allocations

Swing traders timing sector rotation plays

Risk managers monitoring overall market sentiment

Asset allocators adjusting exposure based on risk appetite cycles

----------------------------------------------------

Key applications:

Identify when markets transition from growth-seeking to risk-averse behavior

Time entries into cyclical sectors during risk-on phases

Rotate to defensive sectors when risk appetite weakens

Spot divergences between individual stocks and broader market sentiment

----------------------------------------------------

Limitations:

This indicator reflects US equity sector dynamics and may not capture risk sentiment in other asset classes or geographic regions. ETF-based analysis introduces slight tracking differences from underlying sector performance. Past performance patterns do not guarantee future results.

----------------------------------------------------

Disclaimer:

This indicator is for educational and analytical purposes only. It does not constitute financial advice or trading recommendations. Users should conduct their own analysis and risk assessment before making investment decisions. SwissAlgo assumes no responsibility for trading losses or investment outcomes based on this indicator's signals.

Goichi Hosoda TheoryGreetings to traders. I offer you an indicator for trading according to the Ichimoku Kinho Hyo trading system. This indicator determines possible time cycles of price reversal and expected asset price values based on the theory of waves and time cycles by Goichi Hosoda.

The indicator contains classic price levels N, V, E and NT, and is supplemented with intermediate levels V+E, V+N, N+NT and x2, x3, x4 for levels V and E, which are used in cases where the wave does not contain corrections and there is no possibility to update the impulse-corrective wave.

A function for counting bars from points A B and C has also been added.

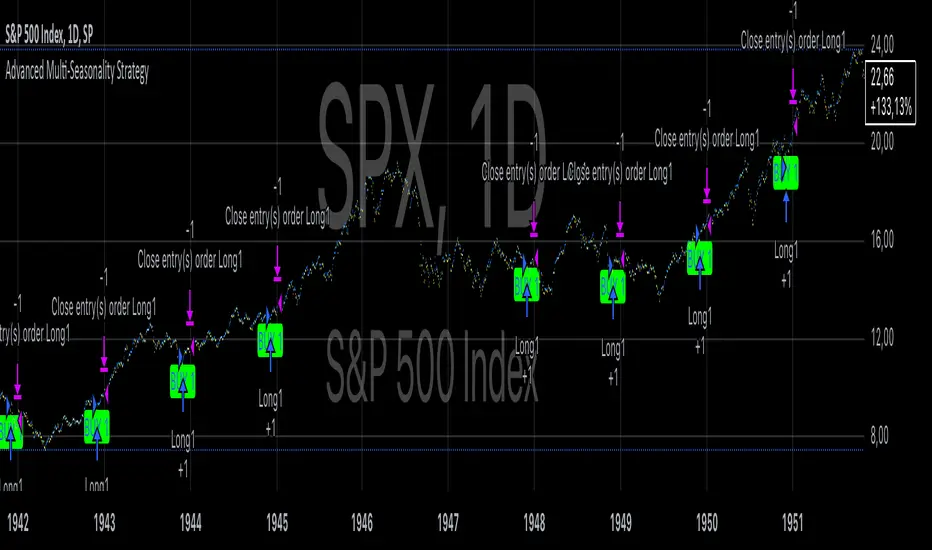

Advanced Multi-Seasonality StrategyThe Multi-Seasonality Strategy is a trading system based on seasonal market patterns. Seasonality refers to recurring market trends driven by predictable calendar-based events. These patterns emerge due to economic cycles, corporate activities (e.g., earnings reports), and investor behavior around specific times of the year. Studies have shown that such effects can influence asset prices over defined periods, leading to opportunities for traders who exploit these patterns (Hirshleifer, 2001; Bouman & Jacobsen, 2002).

How the Strategy Works:

The strategy allows the user to define four distinct periods within a calendar year. For each period, the trader selects:

Entry Date (Month and Day): The date to enter the trade.

Holding Period: The number of trading days to remain in the trade after the entry.

Trade Direction: Whether to take a long or short position during that period.

The system is designed with flexibility, enabling the user to activate or deactivate each of the four periods. The idea is to take advantage of seasonal patterns, such as buying during historically strong periods and selling during weaker ones. A well-known example is the "Sell in May and Go Away" phenomenon, which suggests that stock returns are higher from November to April and weaker from May to October (Bouman & Jacobsen, 2002).

Seasonality in Financial Markets:

Seasonal effects have been documented across different asset classes and markets:

Equities: Stock markets tend to exhibit higher returns during certain months, such as the "January effect," where prices rise after year-end tax-loss selling (Haugen & Lakonishok, 1987).

Commodities: Agricultural commodities often follow seasonal planting and harvesting cycles, which impact supply and demand patterns (Fama & French, 1987).

Forex: Currency pairs may show strength or weakness during specific quarters based on macroeconomic factors, such as fiscal year-end flows or central bank policy decisions.

Scientific Basis:

Research shows that market anomalies like seasonality are linked to behavioral biases and institutional practices. For example, investors may respond to tax incentives at the end of the year, and companies may engage in window dressing (Haugen & Lakonishok, 1987). Additionally, macroeconomic factors, such as monetary policy shifts and holiday trading volumes, can also contribute to predictable seasonal trends (Bouman & Jacobsen, 2002).

Risks of Seasonal Trading:

While the strategy seeks to exploit predictable patterns, there are inherent risks:

Market Changes: Seasonal effects observed in the past may weaken or disappear as market conditions evolve. Increased algorithmic trading, globalization, and policy changes can reduce the reliability of historical patterns (Lo, 2004).

Overfitting: One of the risks in seasonal trading is overfitting the strategy to historical data. A pattern that worked in the past may not necessarily work in the future, especially if it was based on random chance or external factors that no longer apply (Sullivan, Timmermann, & White, 1999).

Liquidity and Volatility: Trading during specific periods may expose the trader to low liquidity, especially around holidays or earnings seasons, leading to slippage and larger-than-expected price swings.

Economic and Geopolitical Shocks: External events such as pandemics, wars, or political instability can disrupt seasonal patterns, leading to unexpected market behavior.

Conclusion:

The Multi-Seasonality Strategy capitalizes on the predictable nature of certain calendar-based patterns in financial markets. By entering and exiting trades based on well-established seasonal effects, traders can potentially capture short-term profits. However, caution is necessary, as market dynamics can change, and seasonal patterns are not guaranteed to persist. Rigorous backtesting, combined with risk management practices, is essential to successfully implementing this strategy.

References:

Bouman, S., & Jacobsen, B. (2002). The Halloween Indicator, "Sell in May and Go Away": Another Puzzle. American Economic Review, 92(5), 1618-1635.

Fama, E. F., & French, K. R. (1987). Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. Journal of Business, 60(1), 55-73.

Haugen, R. A., & Lakonishok, J. (1987). The Incredible January Effect: The Stock Market's Unsolved Mystery. Dow Jones-Irwin.

Hirshleifer, D. (2001). Investor Psychology and Asset Pricing. Journal of Finance, 56(4), 1533-1597.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Sullivan, R., Timmermann, A., & White, H. (1999). Data-Snooping, Technical Trading Rule Performance, and the Bootstrap. Journal of Finance, 54(5), 1647-1691.

This strategy harnesses the power of seasonality but requires careful consideration of the risks and potential changes in market behavior over time.

US Presidential Elections (Names & Dates)US Presidential Elections (Names & Dates)

Description :

This indicator marks key dates in US presidential history, highlighting both election days and inauguration dates. It's designed to provide historical context to your charts, allowing you to see how major political events align with market movements.

Key Features:

• Displays US presidential elections from 1936 to 2052

• Shows inauguration dates for each president

• Customizable colors and styles for both election and inauguration markers

• Toggle visibility of election and inauguration labels separately

• Adapts to different timeframes (daily, weekly, monthly)

• Includes president names for historical context

The indicator uses yellow labels for election days and blue labels for inauguration dates. Election labels show the year and "Election", while inauguration labels display the name of the incoming president.

Customization options include:

• Colors for election and inauguration labels and text

• Line widths for both types of events

• Label placement styles

This tool is perfect for traders and analysts who want to correlate political events with market trends over long periods. It provides a unique perspective on how presidential cycles might influence financial markets.

Note: Future elections (2024 onwards) are marked with a placeholder (✅) as the presidents are not yet known.

Use this indicator to:

• Identify potential market patterns around election cycles

• Analyze historical market reactions to specific presidencies

• Add political context to your long-term chart analysis

Enhance your chart analysis with this comprehensive view of US presidential history!

CVDD - Coin Value Days Destroyed for Bitcoin (BTC) [Logue]Cumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Cycle Position TradingTitle: Cycle Position Trading Strategy v1.0

Description: Cycle Position Trading Strategy is a simple yet effective trading strategy based on a 200-day Simple Moving Average (SMA). Users can select between two modes, "Buy Uptrend" and "Buy Downtrend," to customize the strategy according to their trading preferences. The strategy allows users to set their own stop loss (SL) and take profit (TP) levels, providing more flexibility and control over their trades.

Features:

Choose between two trading modes: "Buy Uptrend" and "Buy Downtrend."

Customize your stop loss (SL) and take profit (TP) levels.

Clear visual representation of the 200-day Simple Moving Average (SMA) on the chart.

How to use:

Add the strategy to your chart by searching for "Cycle Position Trading Strategy" in the TradingView "Indicators & Strategies" section.

Configure the strategy settings according to your preferences:

Select the trading mode from the dropdown menu. "Buy Uptrend" will open long positions when the closing price is above the 200-day SMA. "Buy Downtrend" will open long positions when the closing price is below the 200-day SMA.

Set your desired stop loss (SL) and take profit (TP) levels. The default values are 0.9 (10% below the entry price) for the stop loss and 1.1 (10% above the entry price) for the take profit.

Monitor the chart for trade signals based on the chosen mode and settings. The strategy will enter and exit trades automatically based on the selected mode and the configured stop loss and take profit levels.

Analyze the performance of the strategy by checking the TradingView strategy performance summary or by viewing individual trades in the "Trades" list.

Disclaimer: This strategy is intended for educational and illustrative purposes only. Use it at your own risk. Past performance is not indicative of future results. Trading stocks, cryptocurrencies, or any other financial instrument involves significant risk and may result in the loss of capital.

Version: v1.0

Release date: 2023-03-25

Author: I11L

License: Mozilla Public License 2.0 (mozilla.org)

Cycle Channel Oscillator [LazyBear]Here's an oscillator derived from my previous script, Cycle Channel Clone ().

There are 2 oscillator plots - fast & slow. Fast plot shows the price location with in the medium term channel, while slow plot shows the location of short term midline of cycle channel with respect to medium term channel.

Usage of this is similar to %b oscillator. The slow plot can be considered as the signal line.

Bar colors can be enabled via options page. When short plot is above 1.0 or below 0, they are marked purple (both histo and the bar color) to highlight the extreme condition.

This makes use of the default 10/30 values of Cycle Channel, but may need tuning for your instrument.

More info:

List of my free indicators: bit.ly

List of my app-store indicators: blog.tradingview.com (More info: bit.ly)

Days Of The Week📌 Indicator Description

Days of the Week (Color + UTC-5 Auto) is a visual time-structure indicator designed to clearly separate trading days on the chart and highlight the day of the week using customizable colors.

It is especially useful for traders who analyze market behavior by weekday or who want a clean and intuitive way to identify weekly cycles, weekend transitions, and session-based structure.

🔹 Key Features

1. Automatic New York Timezone (UTC-5 / UTC-4 with DST)

The indicator automatically calculates time using the America/New_York timezone with full daylight saving time support.

This ensures that day changes, weekdays, and labels always align with the New York trading session regardless of the chart’s local timezone.

2. Day Separator Background (Vertical Highlighting)

A vertical background separator is drawn at the beginning of each New York trading day.

Users can independently customize:

-Weekday separator color

-Saturday separator color

-Sunday separator color

-Separator transparency

This makes weekends and weekly boundaries instantly visible on any timeframe.

3. Day-of-Week Text Labels at NY 09:00

At exactly 09:00 New York time, the indicator displays a text label at the bottom of the chart showing the current day of the week.

Sunday displays “Beginning of week – Sunday”

Monday through Friday display their respective weekday names

Saturday displays “Saturday”

This timing aligns with the New York session open, making it useful for intraday and session-based traders.

4. Separate Color Control for Weekdays vs Weekends

Text colors are fully customizable and separated into:

Weekday text color

Saturday text color

Sunday text color

Additionally, the script supports dark-background and light-background text modes, allowing the user to toggle which version is displayed depending on their chart theme.

5. Minimal, Non-Intrusive Design

No repainting

No future-looking logic

No impact on price data

Lightweight and optimized

The indicator is purely visual and does not interfere with other studies or trading systems.

🔹 Customization Options

Users can control:

Whether the day separator is shown

Separator colors for weekdays, Saturday, and Sunday

Separator transparency

Whether dark or light background text is displayed

Individual text colors for weekdays, Saturday, and Sunday

All settings update instantly from the indicator’s settings panel.

Momentum Structural AnalysisMomentum Structural Analysis (MSA‑style Oscillator)

This indicator implements a simple, MSA‑style momentum oscillator that measures how far price has moved above or below its own long‑term trend on the active timeframe, expressed in percentage terms. Instead of looking at raw price, it "oscillates" price around a timeframe‑appropriate simple moving average (SMA) and plots the percentage distance from that SMA as an orange line around a zero baseline. Zero means price is exactly at its structural trend; positive values mean price is extended above trend; negative values mean it is trading below trend.

The script automatically selects the SMA length based on the chart timeframe:

On daily charts it uses the configurable Daily SMA Length (default 252 trading days, roughly 1 year).

On weekly charts it uses Weekly SMA Length (default 208 weeks).

On monthly charts it uses Monthly SMA Length (default 120 months).

This approach is inspired by the ideas behind Momentum Structural Analysis (MSA), which studies where a market trades relative to long‑term moving averages and then treats the momentum line (the oscillator) as the primary object of analysis. The goal is to highlight structural overbought/oversold conditions and regime changes that are often clearer on momentum than on the raw price chart.

--------------------------------------------------

What the script computes and how it works

For each bar, the indicator:

Chooses an SMA length based on the current timeframe (daily/weekly/monthly).

Calculates the SMA of the close.

Computes the percentage distance:

\text{Diff %} = \frac{\text{Close} - \text{SMA}}{\text{SMA}} \times 100

Plots this Diff % as an orange line, with a dashed horizontal zero line as the base.

This produces a momentum oscillator that oscillates around zero and reflects the "structural" position of price versus its own long‑term mean.

--------------------------------------------------

How to use it on index charts (e.g., NIFTY50)

On indices like NIFTY50, use the indicator to see how stretched the index is versus its structural trend.

Typical uses:

Identify extremes: a). Historically high positive readings can signal euphoric, late‑stage conditions where risk is elevated. b). Deep negative readings can highlight panic/capitulation zones where downside may be exhausted.

Draw structural levels: a). Mark horizontal bands on the oscillator where past turns have occurred (e.g., +15%, −10%, etc. specific to NIFTY50). b). Watch how price behaves when the oscillator revisits these zones: repeated rejections can validate them as structural bounds; clean breaks can indicate a change of regime.

This is not a buy/sell signal generator by itself; it is a framework to understand where the index sits within its long‑term momentum structure and to support risk‑management decisions.

--------------------------------------------------

How to use it on ratio charts

Apply the same indicator to ratio symbols such as NIFTY50/GOLD, BANKNIFTY/NIFTY50, sector vs index, or any spread you plot as a ratio.

On a ratio chart:

The oscillator now measures relative momentum: how far that ratio is above or below its own long‑term mean.

High positive readings = strong outperformance of the numerator vs the denominator (e.g., equities strongly outperforming gold).

Deep negative readings = strong underperformance (e.g., equities structurally lagging gold).

This is very much in the spirit of MSA’s work on spreads between asset classes: it helps visualize major rotations (equities → gold, financials → commodities, etc.) and whether a relative‑performance trend is stretched, reverting, or breaking into a new phase.

--------------------------------------------------

Using multiple timeframes for better decisions

You can stack information across timeframes to get a more robust view:

Monthly : a). Use monthly charts to see secular/structural phases. b). Long multi‑year stretches above or below zero, and large bases or trendline breaks on the monthly oscillator, can mark major bull or bear cycles and big rotations between asset classes.

Weekly : a). Use weekly charts for the primary trend. b). Weekly structures (multi‑month highs/lows, channels, or trendlines on the oscillator) are useful for medium‑term positioning and for confirming or rejecting signals seen on the monthly view.

Daily : a). Use daily charts mainly for timing entries/exits once the higher‑timeframe direction is clear. b). Short‑term extremes on the daily oscillator that align with the larger weekly/monthly structure can offer better‑timed opportunities, while signals that contradict higher‑timeframe momentum are more likely to be noise.

--------------------------------------------------

LJ Parsons Adjustable expanding MRT Fibpapers.ssrn.com

Market Resonance Theory (MRT) reinterprets financial markets as structured multiplicative, recursive systems rather than linear, dollar-based constructs. By mapping price growth as a logarithmic lattice of intervals, MRT identifies the deep structural cycles underlying long-term market behaviour. The model draws inspiration from the proportional relationships found in musical resonance, specifically the equal temperament system, revealing that markets expand through recurring octaves of compounded growth. This framework reframes volatility, not as noise, but as part of a larger self-organising structure.

Extended SOPR Indicator - SSOPR Tops (A/B toggle)Extended SOPR Indicator — SSOPR Tops and Lows (A/B toggle)

Observation-only. Data: Glassnode SOPR.

Overview

This indicator extends the classical SOPR (Spent Output Profit Ratio) to improve readability and reduce noise on charts. SOPR measures whether coins moved on-chain were spent at a profit or at a loss. In brief: SOPR > 1 → spending at profit; SOPR < 1 → spending at loss. SSOPR (from "Smoothed SOPR") applies optional log transform (centers baseline at 0), smoothing (standard or adaptive), and adds structured signals: Z‑score lows (capitulation), buy zones , and top detection after prolonged elevation.

Why extend SOPR? (SSOPR vs classical SOPR)

• Noise reduction: Raw daily SOPR can whipsaw around its baseline. SSOPR uses smoothing and (optionally) adaptive smoothing so regimes are visible without overfitting.

• Better readability: The log transform shifts the break-even line to 0, making “profit territory” (above 0) and “loss territory” (below 0) visually intuitive on oscillators.

• Actionable context: Z‑score highlights extreme lows (capitulation risk), a simple buy-zone threshold marks potential accumulation, and a structured top pattern (with a time factor) helps frame distribution phases after sustained elevation.

What the script plots

• Smoothed SOPR (SSOPR): An orange line representing the smoothed SOPR (with optional log transform and optional adaptive smoothing).

• Top markers: A red triangle appears once at the onset of a confirmed top pattern.

• Background shading:

– Soft green: Buy zone when SSOPR falls below the “Buy Threshold.” (+ Z‑score capitulation zones (extreme lows)).

– Soft red: Top‑zone shading when the top criteria are met but before the single triangle fires.

Inputs & parameters

• Smoothing Length (default 14): Base window for smoothing SSOPR. Higher values = smoother, slower response.

• Apply Log Transform (default ON): Uses log(SOPR) so the baseline is 0 (log(1)=0). Above 0 → net profit regime; below 0 → net loss regime.

• Adaptive Smoothing (default OFF): Expands smoothing length as volatility rises using a standard deviation proxy; reduces whipsaws while preserving structure.

• Z‑score Threshold for Lows (default −2.5): Highlights capitulation zones when SSOPR deviates far below its rolling mean.

• SSOPR Buy Threshold (default −0.02): Simple rule-of-thumb level for potential accumulation context when below (log scale).

• SSOPR Top Threshold (default +0.005): Minimum elevation required for “profit territory” when assessing tops (log scale).

• Min Bars Above Threshold Before Top (default 50): Ensures prolonged elevation before calling a top.

• Lookback for Peak Detection (default 50): Window used to locate the recent high.

• Drop % from Peak to Confirm Top (default 5%): Confirms the start of distribution from a local high.

• Highlight Background : Toggles shaded zones.

Top detection (indicator-only)

A top fires when ALL of the following are true:

SSOPR spent at least Min Bars Above Threshold above the Top Threshold (sustained elevation).

The rising phase test passes (Option A or B; see below).

A drop from the local peak exceeds Drop % within the Lookback window.

The peak occurred in profit territory (SSOPR > Top Threshold).

To avoid repeated signals during the decline, the script emits the triangle once, at onset.

Rising‑phase switch: Option A vs Option B

• Option A — Up‑step ratio : Over the last A: Bars for Rising Check (default 50), it requires that at least A: Required Up‑Step Ratio (default 60%) of bars were rising (each bar compared to the previous). This favors gradual, persistent advances and filters out “choppy” lifts.

• Option B — Net slope : Compares current SSOPR to its value B: Bars Back for Net Slope ago (default 50). If higher, the series is considered rising. This is simpler and reacts faster in volatile phases but can admit brief pseudo‑trends.

Guidance : Prefer A for conservative confirmation in slow, persistent cycles; use B when trend moves are strong and you need timely detection.

Interpretation guide

• Regimes (log view): Above 0 → spending at profit; below 0 → spending at loss.

• Capitulation lows: When Z‑score < threshold, conditions often reflect forced/liquidity‑driven spending. Treat as context, not signals.

• Buy zone: SSOPR < Buy Threshold flags potential accumulation conditions (combine with price structure).

• Tops: After prolonged elevation, a confirmed top often coincides with profit‑taking/distribution phases.

Recommended timeframes

• Daily : Code optimized for daily timeframe.

Method summary

• SSOPR source: GLASSNODE:BTC_SOPR (via request.security ).

• Optional log transform: sopr → log(sopr) to normalize around 0.

• Smoothing: SMA over Smoothing Length , optionally adaptive using local volatility (std dev).

• Z‑score: (SSOPR − mean) / std dev, highlighting extreme lows.

• Top: Requires long elevation above Top Threshold , rising‑phase (A/B), and a subsequent drop > Drop % from recent high.

Limitations & notes

• SOPR reflects on‑chain movements; some activity occurs off‑chain (exchanges, internal transfers). Not all moves imply sale; aggregation makes it a usable proxy for profit/loss realization.

• Higher smoothing reduces noise but delays signals; adaptive smoothing can help but is still a trade‑off.

• Treat thresholds as context markers. They are not entry/exit signals by themselves.

• Use with price structure, volume, and other on‑chain indicators (e.g., realized price bands, dormancy/CDD) for confluence.

How to use (examples)

• Advance holding above 0 (log view): Retests of 0 from above that hold—while SSOPR remains elevated—often mark absorption; look for Top conditions only after sustained elevation and a confirmed drop from peak.

• Downtrend below 0: Rejections near 0 can align with continued loss realization; extreme Z‑score lows suggest capitulation risk—context for accumulation, not a blind buy.

Recommended settings

• Weekly: Log ON, Smoothing Length 14–30, Adaptive ON, Buy Threshold −0.02, Top Threshold +0.005, Rising Method A, Min Bars 50.

• Daily: Log ON, Smoothing Length 14–20, Adaptive OFF or ON (depending on noise), Rising Method B for timely slope checks.

Credits & references

• SOPR metric: Renato Shirakashi; documentation: Glassnode , CryptoQuant , overview: Bitbo .

Disclaimer

This script is for research/education on market behavior. It is not financial advice. Indicators provide context; decisions remain your responsibility.

Tags

bitcoin, btc, on‑chain, sopr, ssopr, glassnode, oscillator, regime, distribution, capitulation

Stochastic Hash Strat [Hash Capital Research]# Stochastic Hash Strategy by Hash Capital Research

## 🎯 What Is This Strategy?

The **Stochastic Slow Strategy** is a momentum-based trading system that identifies oversold and overbought market conditions to capture mean-reversion opportunities. Think of it as a "buy low, sell high" approach with smart mathematical filters that remove emotion from your trading decisions.

Unlike fast-moving indicators that generate excessive noise, this strategy uses **smoothed stochastic oscillators** to identify only the highest-probability setups when momentum truly shifts.

---

## 💡 Why This Strategy Works

Most traders fail because they:

- **Chase prices** after big moves (buying high, selling low)

- **Overtrade** in choppy, directionless markets

- **Exit too early** or hold losses too long

This strategy solves all three problems:

1. **Entry Discipline**: Only trades when the stochastic oscillator crosses in extreme zones (oversold for longs, overbought for shorts)

2. **Cooldown Filter**: Prevents revenge trading by forcing a waiting period after each trade

3. **Fixed Risk/Reward**: Pre-defined stop-loss and take-profit levels ensure consistent risk management

**The Math Behind It**: The stochastic oscillator measures where the current price sits relative to its recent high-low range. When it's below 25, the market is oversold (time to buy). When above 70, it's overbought (time to sell). The crossover with its moving average confirms momentum is shifting.

---

## 📊 Best Markets & Timeframes

### ⭐ OPTIMAL PERFORMANCE:

**Crude Oil (WTI) - 12H Timeframe**

- **Why it works**: Oil markets have predictable volatility patterns and respect technical levels

**AAVE/USD - 4H to 12H Timeframe**

- **Why it works**: DeFi tokens exhibit strong momentum cycles with clear extremes

### ✅ Also Works Well On:

- **BTC/USD** (12H, Daily) - Lower frequency but high win rate

- **ETH/USD** (8H, 12H) - Balanced volatility and liquidity

- **Gold (XAU/USD)** (Daily) - Classic mean-reversion asset

- **EUR/USD** (4H, 8H) - Lower volatility, requires patience

### ❌ Avoid Using On:

- Timeframes below 4H (too much noise)

- Low-liquidity altcoins (wide spreads kill performance)

- Strongly trending markets without pullbacks (Bitcoin in 2021)

- News-driven instruments during major events

---

## 🎛️ Understanding The Settings

### Core Stochastic Parameters

**Stochastic Length (Default: 16)**

- Controls the lookback period for price comparison

- Lower = faster reactions, more signals (10-14 for volatile markets)

- Higher = smoother signals, fewer trades (16-21 for stable markets)

- **Pro tip**: Use 10 for crypto 4H, 16 for commodities 12H

**Overbought Level (Default: 70)**

- Threshold for short entries

- Lower values (65-70) = more trades, earlier entries

- Higher values (75-80) = fewer but higher-conviction trades

- **Sweet spot**: 70 works for most assets

**Oversold Level (Default: 25)**

- Threshold for long entries

- Higher values (25-30) = more trades, earlier entries

- Lower values (15-20) = fewer but stronger bounce setups

- **Sweet spot**: 20-25 depending on market conditions

**Smooth K & Smooth D (Default: 7 & 3)**

- Additional smoothing to filter out whipsaws

- K=7 makes the indicator slower and more reliable

- D=3 is the signal line that confirms the trend

- **Don't change these unless you know what you're doing**

---

### Risk Management

**Stop Loss % (Default: 2.2%)**

- Automatically exits losing trades

- Should be 1.5x to 2x your average market volatility

- Too tight = death by a thousand cuts

- Too wide = uncontrolled losses

- **Calibration**: Check ATR indicator and set SL slightly above it

**Take Profit % (Default: 7%)**

- Automatically exits winning trades

- Should be 2.5x to 3x your stop loss (reward-to-risk ratio)

- This default gives 7% / 2.2% = 3.18:1 R:R

- **The golden rule**: Never have R:R below 2:1

---

### Trade Filters

**Bar Cooldown Filter (Default: ON, 3 bars)**

- **What it does**: Forces you to wait X bars after closing a trade before entering a new one

- **Why it matters**: Prevents emotional revenge trading and overtrading in choppy markets

- **Settings guide**:

- 3 bars = Standard (good for most cases)

- 5-7 bars = Conservative (oil, slow-moving assets)

- 1-2 bars = Aggressive (only for experienced traders)

**Exit on Opposite Extreme (Default: ON)**

- Closes your long when stochastic hits overbought (and vice versa)

- Acts as an early profit-taking mechanism

- **Leave this ON** unless you're testing other exit strategies

**Divergence Filter (Default: OFF)**

- Looks for price/momentum divergences for additional confirmation

- **When to enable**: Trending markets where you want fewer but higher-quality trades

- **Keep OFF for**: Mean-reverting markets (oil, forex, most of the time)

---

## 🚀 Quick Start Guide

### Step 1: Set Up in TradingView

1. Open TradingView and navigate to your chart

2. Click "Pine Editor" at the bottom

3. Copy and paste the strategy code

4. Click "Add to Chart"

5. The strategy will appear in a separate pane below your price chart

### Step 2: Choose Your Market

**If you're trading Crude Oil:**

- Timeframe: 12H

- Keep all default settings

- Watch for signals during London/NY overlap (8am-11am EST)

**If you're trading AAVE or crypto:**

- Timeframe: 4H or 12H

- Consider these adjustments:

- Stochastic Length: 10-14 (faster)

- Oversold: 20 (more aggressive)

- Take Profit: 8-10% (higher targets)

### Step 3: Wait for Your First Signal

**LONG Entry** (Green circle appears):

- Stochastic crosses up below oversold level (25)

- Price likely near recent lows

- System places limit order at take profit and stop loss

**SHORT Entry** (Red circle appears):

- Stochastic crosses down above overbought level (70)

- Price likely near recent highs

- System places limit order at take profit and stop loss

**EXIT** (Orange circle):

- Position closes either at stop, target, or opposite extreme

- Cooldown period begins

### Step 4: Let It Run

The biggest mistake? **Interfering with the system.**

- Don't close trades early because you're scared

- Don't skip signals because you "have a feeling"

- Don't increase position size after a big win

- Don't revenge trade after a loss

**Follow the system or don't use it at all.**

---

### Important Risks:

1. **Drawdown Pain**: You WILL experience losing streaks of 5-7 trades. This is mathematically normal.

2. **Whipsaw Markets**: Choppy, range-bound conditions can trigger multiple small losses.

3. **Gap Risk**: Overnight gaps can cause your actual fill to be worse than the stop loss.

4. **Slippage**: Real execution prices differ from backtested prices (factor in 0.1-0.2% slippage).

---

## 🔧 Optimization Guide

### When to Adjust Settings:

**Market Volatility Increased?**

- Widen stop loss by 0.5-1%

- Increase take profit proportionally

- Consider increasing cooldown to 5-7 bars

**Getting Too Few Signals?**

- Decrease stochastic length to 10-12

- Increase oversold to 30, decrease overbought to 65

- Reduce cooldown to 2 bars

**Getting Too Many Losses?**

- Increase stochastic length to 18-21 (slower, smoother)

- Enable divergence filter

- Increase cooldown to 5+ bars

- Verify you're on the right timeframe

### A/B Testing Method:

1. **Run default settings for 50 trades** on your chosen market

2. Document: Win rate, profit factor, max drawdown, emotional tolerance

3. **Change ONE variable** (e.g., oversold from 25 to 20)

4. Run another 50 trades

5. Compare results

6. Keep the better version

**Never change multiple settings at once** or you won't know what worked.

---

## 📚 Educational Resources

### Key Concepts to Learn:

**Stochastic Oscillator**

- Developed by George Lane in the 1950s

- Measures momentum by comparing closing price to price range

- Formula: %K = (Close - Low) / (High - Low) × 100

- Similar to RSI but more sensitive to price movements

**Mean Reversion vs. Trend Following**

- This is a **mean reversion** strategy (price returns to average)

- Works best in ranging markets with defined support/resistance

- Fails in strong trending markets (2017 Bitcoin, 2020 Tech stocks)

- Complement with trend filters for better results

**Risk:Reward Ratio**

- The cornerstone of profitable trading

- Winning 40% of trades with 3:1 R:R = profitable

- Winning 60% of trades with 1:1 R:R = breakeven (after fees)

- **This strategy aims for 45% win rate with 2.5-3:1 R:R**

### Recommended Reading:

- *"Trading Systems and Methods"* by Perry Kaufman (Chapter on Oscillators)

- *"Mean Reversion Trading Systems"* by Howard Bandy

- *"The New Trading for a Living"* by Dr. Alexander Elder

---

## 🛠️ Troubleshooting

### "I'm not seeing any signals!"

**Check:**

- Is your timeframe 4H or higher?

- Is the stochastic actually reaching extreme levels (check if your asset is stuck in middle range)?

- Is cooldown still active from a previous trade?

- Are you on a low-liquidity pair?

**Solution**: Switch to a more volatile asset or lower the overbought/oversold thresholds.

---

### "The strategy keeps losing money!"

**Check:**

- What's your win rate? (Below 35% is concerning)

- What's your profit factor? (Below 0.8 means serious issues)

- Are you trading during major news events?

- Is the market in a strong trend?

**Solution**:

1. Verify you're using recommended markets/timeframes

2. Increase cooldown period to avoid choppy markets

3. Reduce position size to 5% while you diagnose

4. Consider switching to daily timeframe for less noise

---

### "My stop losses keep getting hit!"

**Check:**

- Is your stop loss tighter than the average ATR?

- Are you trading during high-volatility sessions?

- Is slippage eating into your buffer?

**Solution**:

1. Calculate the 14-period ATR

2. Set stop loss to 1.5x the ATR value

3. Avoid trading right after market open or major news

4. Factor in 0.2% slippage for crypto, 0.1% for oil

---

## 💪 Pro Tips from the Trenches

### Psychological Discipline

**The Three Deadly Sins:**

1. **Skipping signals** - "This one doesn't feel right"

2. **Early exits** - "I'll just take profit here to be safe"

3. **Revenge trading** - "I need to make back that loss NOW"

**The Solution:** Treat your strategy like a business system. Would McDonald's skip making fries because the cashier "doesn't feel like it today"? No. Systems work because of consistency.

---

### Position Management

**Scaling In/Out** (Advanced)

- Enter 50% position at signal

- Add 50% if stochastic reaches 10 (oversold) or 90 (overbought)

- Exit 50% at 1.5x take profit, let the rest run

**This is NOT for beginners.** Master the basic system first.

---

### Market Awareness

**Oil Traders:**

- OPEC meetings = volatility spikes (avoid or widen stops)

- US inventory reports (Wed 10:30am EST) = avoid trading 2 hours before/after

- Summer driving season = different patterns than winter

**Crypto Traders:**

- Monday-Tuesday = typically lower volatility (fewer signals)

- Thursday-Sunday = higher volatility (more signals)

- Avoid trading during exchange maintenance windows

---

## ⚖️ Legal Disclaimer

This trading strategy is provided for **educational purposes only**.

- Past performance does not guarantee future results

- Trading involves substantial risk of loss

- Only trade with capital you can afford to lose

- No one associated with this strategy is a licensed financial advisor

- You are solely responsible for your trading decisions

**By using this strategy, you acknowledge that you understand and accept these risks.**

---

## 🙏 Acknowledgments

Strategy development inspired by:

- George Lane's original Stochastic Oscillator work

- Modern quantitative trading research

- Community feedback from hundreds of backtests

Built with ❤️ for retail traders who want systematic, disciplined approaches to the markets.

---

**Good luck, stay disciplined, and trade the system, not your emotions.**

Systemic Net Liquidity (Macro Fuel for Crypto & Stocks)This indicator tracks Systemic Net Liquidity, the single most important macro factor for determining the long-term trend of risk assets like Bitcoin (BTC) and major indices (S&P 500). It measures the amount of actual cash available in the financial system to chase speculative assets, distinguishing between money that is circulating and money that is locked up at the Federal Reserve.

Mechanism (What It Measures)

The script uses direct data from the FRED (Federal Reserve Economic Data) to calculate the true state of market funding:

\text{Net Liquidity} = \text{Fed Assets (WALCL)} - \text{Treasury General Account (TGA)} - \text{Reverse Repo (RRP)}

1. Fed Assets (WALCL): The total balance sheet of the Fed (The overall supply of money).

2. Treasury General Account (TGA): Funds the US Treasury collects via bond issuance. When the TGA rises, liquidity is actively drained from the banking system (A major bearish pressure).

3. Overnight Reverse Repo (RRP): Cash parked by banks and money market funds at the Fed, effectively frozen and not contributing to market activity.

How to Interpret Signals

Treat the Net Liquidity line as the market's "Fuel Gauge":

📈 BULLISH SIGNAL (Liquidity Injection): When the Net Liquidity line is rising, money is flowing back into the system, signalling a tailwind for risk assets.

📉 BEARISH SIGNAL (Liquidity Drain): When the line is falling (often due to high TGA balances), cash is being removed. This signals major friction and pressure on price action.

⚠️ DIVERGENCE WARNING: A strong signal is generated when Price (e.g., BTC) rises, but Net Liquidity falls. This macro divergence strongly suggests a major trend reversal or correction is imminent.

Important Notes

Data Source: Data is directly sourced from FRED and updates daily/weekly. This tool is best used for macro analysis and identifying high-level cycles, not short-term scalping.

Disclaimer: Use this indicator as a confirmation tool within your broader strategy. It is not a standalone trading signal.