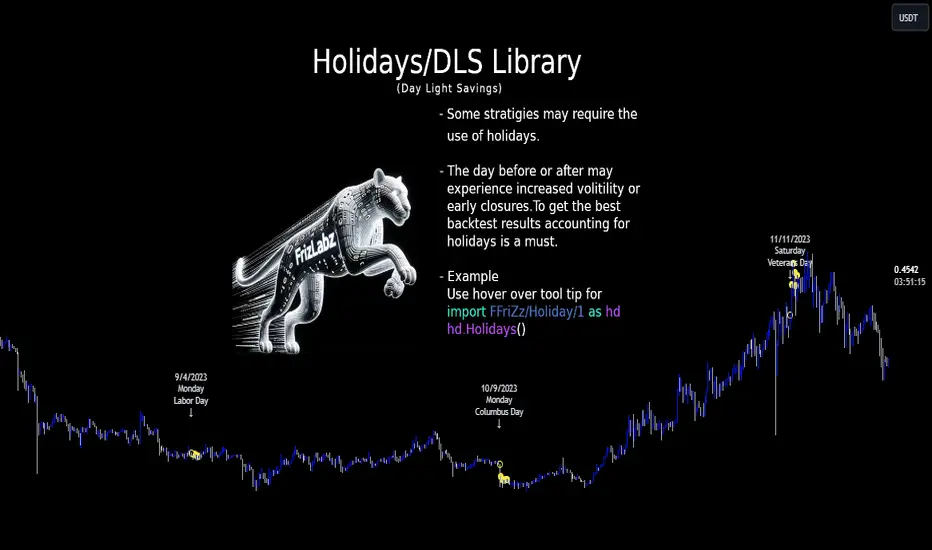

HolidayLibrary "Holiday"

- Full Control over Holidays and Daylight Savings Time (DLS)

The Holiday Library is an essential tool for traders and analysts who engage in backtesting and live trading . This comprehensive library enables the incorporation of crucial calendar elements - specifically Daylight Savings Time (DLS) adjustments and public holidays - into trading strategies and backtesting environments.

Key Features:

- DLS Adjustments: The library takes into account the shifts in time due to Daylight Savings. This feature is particularly vital for backtesting strategies, as DLS can impact trading hours, which in turn affects the volatility and liquidity in the market. Accurate DLS adjustments ensure that backtesting scenarios are as close to real-life conditions as possible.

- Comprehensive Holiday Metadata: The library includes a rich set of holiday metadata, allowing for the detailed scheduling of trading activities around public holidays. This feature is crucial for avoiding skewed results in backtesting, where holiday trading sessions might differ significantly in terms of volume and price movement.

- Customizable Holiday Schedules: Users can add or remove specific holidays, tailoring the library to fit various regional market schedules or specific trading requirements.

- Visualization Aids: The library supports on-chart labels, making it visually intuitive to identify holidays and DLS shifts directly on trading charts.

Use Cases:

1. Strategy Development: When developing trading strategies, it’s important to account for non-trading days and altered trading hours due to holidays and DLS. This library enables a realistic and accurate representation of these factors.

2. Risk Management: Trading around holidays can be riskier due to thinner liquidity and greater volatility. By integrating holiday data, traders can better manage their risk exposure.

3. Backtesting Accuracy: For backtesting to be effective, it must simulate the actual market conditions as closely as possible. Incorporating holidays and DLS adjustments contributes to more reliable and realistic backtesting results.

4. Global Trading: For traders active in multiple global markets, this library provides an easy way to handle different holiday schedules and DLS shifts across regions.

The Holiday Library is a versatile tool that enhances the precision and realism of trading simulations and strategy development . Its integration into the trading workflow is straightforward and beneficial for both novice and experienced traders.

EasterAlgo(_year)

Calculates the date of Easter Sunday for a given year using the Anonymous Gregorian algorithm.

`Gauss Algorithm for Easter Sunday` was developed by the mathematician Carl Friedrich Gauss

This algorithm is based on the cycles of the moon and the fact that Easter always falls on the first Sunday after the first ecclesiastical full moon that occurs on or after March 21.

While it's not considered to be 100% accurate due to rare exceptions, it does give the correct date in most cases.

It's important to note that Gauss's formula has been found to be inaccurate for some 21st-century years in the Gregorian calendar. Specifically, the next suggested failure years are 2038, 2051.

This function can be used for Good Friday (Friday before Easter), Easter Sunday, and Easter Monday (following Monday).

en.wikipedia.org

Parameters:

_year (int) : `int` - The year for which to calculate the date of Easter Sunday. This should be a four-digit year (YYYY).

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday for the given year.

easterInit()

Inits the date of Easter Sunday and Good Friday for a given year.

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday and Good Friday for the given year.

isLeapYear(_year)

Determine if a year is a leap year.

Parameters:

_year (int) : `int` - 4 digit year to check => YYYY

Returns: `bool` - true if input year is a leap year

method timezoneHelper(utc)

Helper function to convert UTC time.

Namespace types: series int, simple int, input int, const int

Parameters:

utc (int) : `int` - UTC time shift in hours.

Returns: `string`- UTC time string with shift applied.

weekofmonth()

Function to find the week of the month of a given Unix Time.

Returns: number - The week of the month of the specified UTC time.

dayLightSavingsAdjustedUTC(utc, adjustForDLS)

dayLightSavingsAdjustedUTC

Parameters:

utc (int) : `int` - The normal UTC timestamp to be used for reference.

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS).

Returns: `int` - The adjusted UTC timestamp for the given normal UTC timestamp.

getDayOfYear(monthOfYear, dayOfMonth, weekOfMonth, dayOfWeek, lastOccurrenceInMonth, holiday)

Function gets the day of the year of a given holiday (1-366)

Parameters:

monthOfYear (int)

dayOfMonth (int)

weekOfMonth (int)

dayOfWeek (int)

lastOccurrenceInMonth (bool)

holiday (string)

Returns: `int` - The day of the year of the holiday 1-366.

method buildMap(holidayMap, holiday, monthOfYear, weekOfMonth, dayOfWeek, dayOfMonth, lastOccurrenceInMonth, closingTime)

Function to build the `holidaysMap`.

Namespace types: map

Parameters:

holidayMap (map) : `map` - The map of holidays.

holiday (string) : `string` - The name of the holiday.

monthOfYear (int) : `int` - The month of the year of the holiday.

weekOfMonth (int) : `int` - The week of the month of the holiday.

dayOfWeek (int) : `int` - The day of the week of the holiday.

dayOfMonth (int) : `int` - The day of the month of the holiday.

lastOccurrenceInMonth (bool) : `bool` - Flag indicating whether the holiday is the last occurrence of the day in the month.

closingTime (int) : `int` - The closing time of the holiday.

Returns: `map` - The updated map of holidays

holidayInit(addHolidaysArray, removeHolidaysArray, defaultHolidays)

Initializes a HolidayStorage object with predefined US holidays.

Parameters:

addHolidaysArray (array) : `array` - The array of additional holidays to be added.

removeHolidaysArray (array) : `array` - The array of holidays to be removed.

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays.

Returns: `map` - The map of holidays.

Holidays(utc, addHolidaysArray, removeHolidaysArray, adjustForDLS, displayLabel, defaultHolidays)

Main function to build the holidays object, this is the only function from this library that should be needed. \

all functionality should be available through this function. \

With the exception of initializing a `HolidayMetaData` object to add a holiday or early close. \

\

**Default Holidays:** \

`DLS begin`, `DLS end`, `New Year's Day`, `MLK Jr. Day`, \

`Washington Day`, `Memorial Day`, `Independence Day`, `Labor Day`, \

`Columbus Day`, `Veterans Day`, `Thanksgiving Day`, `Christmas Day` \

\

**Example**

```

HolidayMetaData valentinesDay = HolidayMetaData.new(holiday="Valentine's Day", monthOfYear=2, dayOfMonth=14)

HolidayMetaData stPatricksDay = HolidayMetaData.new(holiday="St. Patrick's Day", monthOfYear=3, dayOfMonth=17)

HolidayMetaData addHolidaysArray = array.from(valentinesDay, stPatricksDay)

string removeHolidaysArray = array.from("DLS begin", "DLS end")

܂Holidays = Holidays(

܂ utc=-6,

܂ addHolidaysArray=addHolidaysArray,

܂ removeHolidaysArray=removeHolidaysArray,

܂ adjustForDLS=true,

܂ displayLabel=true,

܂ defaultHolidays=true,

܂ )

plot(Holidays.newHoliday ? open : na, title="newHoliday", color=color.red, linewidth=4, style=plot.style_circles)

```

Parameters:

utc (int) : `int` - The UTC time shift in hours

addHolidaysArray (array) : `array` - The array of additional holidays to be added

removeHolidaysArray (array) : `array` - The array of holidays to be removed

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS)

displayLabel (bool) : `bool` - Flag indicating whether to display a label on the chart

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays

Returns: `HolidayObject` - The holidays object | Holidays = (holidaysMap: map, newHoliday: bool, holiday: string, dayString: string)

HolidayMetaData

HolidayMetaData

Fields:

holiday (series string) : `string` - The name of the holiday.

dayOfYear (series int) : `int` - The day of the year of the holiday.

monthOfYear (series int) : `int` - The month of the year of the holiday.

dayOfMonth (series int) : `int` - The day of the month of the holiday.

weekOfMonth (series int) : `int` - The week of the month of the holiday.

dayOfWeek (series int) : `int` - The day of the week of the holiday.

lastOccurrenceInMonth (series bool)

closingTime (series int) : `int` - The closing time of the holiday.

utc (series int) : `int` - The UTC time shift in hours.

HolidayObject

HolidayObject

Fields:

holidaysMap (map) : `map` - The map of holidays.

newHoliday (series bool) : `bool` - Flag indicating whether today is a new holiday.

activeHoliday (series bool) : `bool` - Flag indicating whether today is an active holiday.

holiday (series string) : `string` - The name of the holiday.

dayString (series string) : `string` - The day of the week of the holiday.

ابحث في النصوص البرمجية عن "alert"

WHAlertCommandLibrary "WHAlertCommand"

f_WH_Risk(risk_Type_)

Parameters:

risk_Type_ (string)

f_WH_Open_Position(uuid_, enable_Buy_, enable_Sell, enable_All_Group_Members_, enable_Close_Opposite_Side_, enable_Risk_, risk_Type_, signal_Type_Buy_Or_Sell)

Parameters:

uuid_ (string)

enable_Buy_ (bool)

enable_Sell (bool)

enable_All_Group_Members_ (bool)

enable_Close_Opposite_Side_ (bool)

enable_Risk_ (bool)

risk_Type_ (string)

signal_Type_Buy_Or_Sell (string)

f_WH_TP(uuid_, position_Size_Percent_, side_)

Parameters:

uuid_ (string)

position_Size_Percent_ (float)

side_ (string)

f_WH_MARKET_CLOSE(uuid_, side_)

Parameters:

uuid_ (string)

side_ (string)

FinandyHookLibLibrary "FinandyHookLib"

TODO: add library description here

createOrderJson(model, hook_secret, options)

Parameters:

model (orderModel type from Hamster-Coder/OrderLib/7)

hook_secret (string)

options (textFormatOptions)

textFormatOptions

Fields:

price_format (series__string)

percent_format (series__string)

SAT_BACKTEST @description TODO: Regroupement of useful functionsLibrary "SAT_BACKTEST"

ex_timezone(tz)

switch case return exact @timezone for timezone input

Parameters:

tz (simple string)

Returns: syminfo.timezone or tz

if_in_date_range(usefromDate, fromDate, usetoDate, toDate, src_timezone, dst_timezone)

if_in_date_range : check if @time_close is range

Parameters:

usefromDate (simple bool)

fromDate (simple int)

usetoDate (simple bool)

toDate (simple int)

src_timezone (simple string)

dst_timezone (simple string)

Returns: true if @time_close is range

if_in_session(useSessionStart, sessionStartHour, sessionStartMinute, useSessionEnd, sessionEndHour, sessionEndMinute, useSessionDay, mon, tue, wed, thu, fri, sat, sun, src_timezone, dst_timezone)

if_in_session : check if @time_close is range

Parameters:

useSessionStart (simple bool)

sessionStartHour (simple int)

sessionStartMinute (simple int)

useSessionEnd (simple bool)

sessionEndHour (simple int)

sessionEndMinute (simple int)

useSessionDay (simple bool)

mon (simple bool)

tue (simple bool)

wed (simple bool)

thu (simple bool)

fri (simple bool)

sat (simple bool)

sun (simple bool)

src_timezone (simple string)

dst_timezone (simple string)

Returns: true if @time_close is range

Antares_messages_publicLibrary "Antares_messages_public"

This library add messages for yours strategy for use in Antares trading system for binance and bybit exchanges.

Данная библиотека позволяет формировать сообщения в алертах стратегий для Antares в более упрощенном для пользователя режиме, включая всплывающие подсказки и т.д.

set_leverage(token, market, ticker_id, leverage)

Set leverage for ticker on specified market.

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

leverage (float) : (float) leverage level. Устанавливаемое плечо.

Returns: 'Set leverage message'.

pause(time_pause)

Set pause in message. '::' -left and '::' -right included.

Parameters:

time_pause (int)

LongLimit(token, market, ticker_id, type_qty, quantity, price, orderId, leverageforqty)

Buy order with limit price and quantity.

Лимитный ордер на покупку(в лонг).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Buy order'. Лимитный ордер на покупку (лонг).

LongMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Market Buy order with quantity.

Рыночный ордер на покупку (в лонг).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Buy order'. Маркетный ордер на покупку (лонг).

ShortLimit(token, market, ticker_id, type_qty, quantity, price, leverageforqty, orderId)

Sell order with limit price and quantity.

Лимитный ордер на продажу(в шорт).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

Returns: 'Limit Sell order'. Лимитный ордер на продажу (шорт).

ShortMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Sell by market price and quantity.

Рыночный ордер на продажу(в шорт).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Sell order'. Маркетный ордер на продажу (шорт).

Cancel_by_ticker(token, market, ticker_id)

Cancel all orders for market and ticker in setups. Отменяет все ордера на заданной бирже и заданном токене(паре).

Parameters:

token (string)

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

Returns: 'Cancel all orders'. Отмена всех ордеров на заданной бирже и заданном токене(паре).

Cancel_by_id(token, market, ticker_id, orderId)

Cancel order by Id for market and ticker in setups. Отменяет ордер по Id на заданной бирже и заданном токене(паре).

Parameters:

token (string)

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

orderId (string)

Returns: 'Cancel order'. Отмена ордера по Id на заданной бирже и заданном токене(паре).

Close_positions(token, market, ticker_id)

Close all positions for market and ticker in setups. Закрывает все позиции на заданной бирже и заданном токене(паре).

Parameters:

token (string)

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

Returns: 'Close positions'

CloseLongLimit(token, market, ticker_id, type_qty, quantity, price, orderId, leverageforqty)

Close limit order for long position. (futures)

Лимитный ордер на продажу(в шорт) для закрытия лонговой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Sell order reduce only (close long position)'. Лимитный ордер на продажу для снижения текущего лонга(в шорт не входит).

CloseLongMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Close market order for long position.

Рыночный ордер на продажу(в шорт) для закрытия лонговой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Sell order reduce only (close long position)'. Ордер на снижение/закрытие текущего лонга(в шорт не входит) по рыночной цене.

CloseShortLimit(token, market, ticker_id, type_qty, quantity, price, orderId, leverageforqty)

Close limit order for short position.

Лимитный ордер на покупку(в лонг) для закрытия шортовой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order. Цена по которой должен быть установлен лимитный ордер.

orderId (string) : (string) if use order id you may change or cancel your order after or set it ''. Используйте OrderId если хотите изменить или отменить ордер в будущем.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Buy order reduce only (close short position)' . Лимитный ордер на покупку (лонг) для сокращения/закрытия текущего шорта.

CloseShortMarket(token, market, ticker_id, type_qty, quantity, leverageforqty)

Set Close limit order for long position.

Рыночный ордер на покупку(в лонг) для сокращения/закрытия шортовой позиции(reduceonly).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Market Buy order reduce only (close short position)'. Маркетного ордера на покупку (лонг) для сокращения/закрытия текущего шорта.

cancel_all_close(token, market, ticker_id)

Parameters:

token (string)

market (string)

ticker_id (string)

limit_tpsl_bybitfu(token, ticker_id, order_id, side, type_qty, quantity, price, tp_price, sl_price, leverageforqty)

Set multi order for Bybit : limit + takeprofit + stoploss

Выставление тройного ордера на Bybit лимитка со стоплоссом и тейкпрофитом

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

order_id (string)

side (bool) : (bool) "buy side" if true or "sell side" if false. true для лонга, false для шорта.

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order by 'side'. Цена лимитного ордера

tp_price (float) : (float) price for take profit order.

sl_price (float) : (float) price for stoploss order

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: Set multi order for Bybit : limit + takeprofit + stoploss.

replace_limit_tpsl_bybitfu(token, ticker_id, order_id, side, type_qty, quantity, price, tp_price, sl_price, leverageforqty)

Change multi order for Bybit : limit + takeprofit + stoploss

Изменение тройного ордера на Bybit лимитка со стоплоссом и тейкпрофитом

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

order_id (string)

side (bool) : (bool) "buy side" if true or "sell side" if false. true для лонга, false для шорта.

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size, see at 'type_qty'. Размер ордера, базы или % в соответствии с 'type_qty'

price (float) : (float) price for limit order by 'side'. Цена лимитного ордера

tp_price (float) : (float) price for take profit order.

sl_price (float) : (float) price for stoploss order

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: Set multi order for Bybit : limit + takeprofit + stoploss.

long_stop(token, market, ticker_id, type_qty, quantity, l_stop, leverageforqty)

Stop market order for long position

Рыночный стоп-ордер на продажу для закрытия лонговой позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

l_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Stop Market Sell order (close long position)'. Маркетный стоп-ордер на снижения/закрытия текущего лонга.

short_stop(token, market, ticker_id, type_qty, quantity, s_stop, leverageforqty)

Stop market order for short position

Рыночный стоп-ордер на покупку(в лонг) для закрытия шорт позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

s_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Stop Market Buy order (close short position)'. Маркетный стоп-ордер на снижения/закрытия текущего шорта.

change_stop_l(token, market, ticker_id, type_qty, quantity, l_stop, leverageforqty)

Change Stop market order for long position

Изменяем стоп-ордер на продажу(в шорт) для закрытия лонг позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

l_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Change Stop Market Buy order (close long position)'. Смещает цену активации Маркетного стоп-ордер на снижения/закрытия текущего лонга.

change_stop_s(token, market, ticker_id, type_qty, quantity, s_stop, leverageforqty)

Change Stop market order for short position

Смещает цену активации Рыночного стоп-ордера на покупку(в лонг) для закрытия шорт позиции.

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string)

quantity (float) : (float) orders size. Размер ордера.

s_stop (float) : (float) price for activation stop order. Цена активации стоп-ордера.

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Change Stop Market Buy order (close short position)'. Смещает цену активации Маркетного стоп-ордер на снижения/закрытия текущего шорта.

open_long_position(token, market, ticker_id, type_qty, quantity, l_stop, leverageforqty)

Cancel and close all orders and positions by ticker , then open Long position by market price with stop order

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает лонг по маркету с выставлением стопа (переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

l_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'command_all_close + LongMarket + long_stop.

open_short_position(token, market, ticker_id, type_qty, quantity, s_stop, leverageforqty)

Cancel and close all orders and positions , then open Short position by market price with stop order

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает шорт по маркету с выставлением стопа(переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) orders size. Размер ордера.

s_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

leverageforqty (int) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'command_all_close + ShortMarket + short_stop'.

open_long_trade(token, market, ticker_id, type_qty, quantity, l_stop, qty_ex1, price_ex1, qty_ex2, price_ex2, qty_ex3, price_ex3, leverageforqty)

Cancell and close all orders and positions , then open Long position by market price with stop order and take 1 ,take 2, take 3

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает лонг по маркету с выставлением стопа и 3 тейками (переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

quantity (float) : (float) enter order size, see at type_qty. Размер ордера входа, согласно type_qty.

l_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

qty_ex1 (float) : (float). Quantity for 1th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 1го тейка, согласно type_qty.. Если 0, то строка для этого тейка не формируется

price_ex1 (float) : (float). Price for 1th take , if = 0 string for order dont set. Цена лимитного ордера для 1го тейка. Если 0, то строка для этого тейка не формируется

qty_ex2 (float) : (float). Quantity for 2th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex2 (float) : (float). Price for 2th take, if = 0 string for order dont set. Цена лимитного ордера для 2го тейка. Если 0, то строка для этого тейка не формируется

qty_ex3 (float) : (float). Quantity for 3th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex3 (float) : (float). Price for 3th take, if = 0 string for order dont set. Цена лимитного ордера для 3го тейка. Если 0, то строка для этого тейка не формируется

leverageforqty (int)

Returns: 'cancel_all_close + LongMarket + long_stop + CloseLongLimit1 + CloseLongLimit2+CloseLongLimit3'.

open_short_trade(token, market, ticker_id, type_qty, quantity, s_stop, qty_ex1, price_ex1, qty_ex2, price_ex2, qty_ex3, price_ex3, leverageforqty)

Cancell and close all orders and positions , then open Short position by market price with stop order and take 1 and take 2

Отменяет все лимитки и закрывает все позы по тикеру, затем открывает шорт по маркету с выставлением стопа и 3 тейками (переворот позиции, при необходимости).

Parameters:

token (string)

market (string) : (string) 'binance' , 'binancefru' etc.. Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string)

quantity (float)

s_stop (float) : (float). Price for activation stop loss. Цена активации стоп-лосса.

qty_ex1 (float) : (float). Quantity for 1th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 1го тейка, согласно type_qty.. Если 0, то строка для этого тейка не формируется

price_ex1 (float) : (float). Price for 1th take , if = 0 string for order dont set. Цена лимитного ордера для 1го тейка. Если 0, то строка для этого тейка не формируется

qty_ex2 (float) : (float). Quantity for 2th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex2 (float) : (float). Price for 2th take, if = 0 string for order dont set. Цена лимитного ордера для 2го тейка. Если 0, то строка для этого тейка не формируется

qty_ex3 (float) : (float). Quantity for 3th take see at type_qty, if = 0 string for order dont set. Размер лимитного ордера для 2го тейка, согласно type_qty..Если 0, то строка для этого тейка не формируется

price_ex3 (float) : (float). Price for 3th take, if = 0 string for order dont set. Цена лимитного ордера для 3го тейка. Если 0, то строка для этого тейка не формируется

leverageforqty (int)

Returns: 'command_all_close + ShortMarket + short_stop + CloseShortLimit + CloseShortLimit(2)'.

Multi_LongLimit(token, market, ticker_id, type_qty, qty1, price1, qty2, price2, qty3, price3, qty4, price4, qty5, price5, qty6, price6, qty7, price7, qty8, price8, leverageforqty)

8 or less Buy orders with limit price and quantity.

До 8 Лимитных ордеров на покупку(в лонг).

Parameters:

token (string) : (integer or 0) token for trade in system, if = 0 then token part mess is empty. Токен, При значениb = 0 не включается в формирование строки алерта.

market (string) : (string) Spot 'binance' , 'bybit' . Futures ('binancefru','binancefro','bybitfu', 'bybitfi'). Строковая переменная названия биржи.

ticker_id (string) : (string) ticker in market ('btcusdt', 'ethusdt' etc...). Строковая переменная названия тикера (пары).

type_qty (string) : (string) type of quantity: 1. 'qty' or '' or na - standart (in coins), 2. 'quqty'- in assets (usdt,btc,etc..), 3.open% - open position(futures) or buy (spot) in % of base 4. close% - close in % of position (futures) or sell (spot) coins in % for current quantity

qty1 (float)

price1 (float)

qty2 (float)

price2 (float)

qty3 (float)

price3 (float)

qty4 (float)

price4 (float)

qty5 (float)

price5 (float)

qty6 (float)

price6 (float)

qty7 (float)

price7 (float)

qty8 (float)

price8 (float)

leverageforqty (bool) : (bool) use leverage in qty. Использовать плечо при расчете количества или нет.

Returns: 'Limit Buy order'. Лимитный ордер на покупку (лонг).

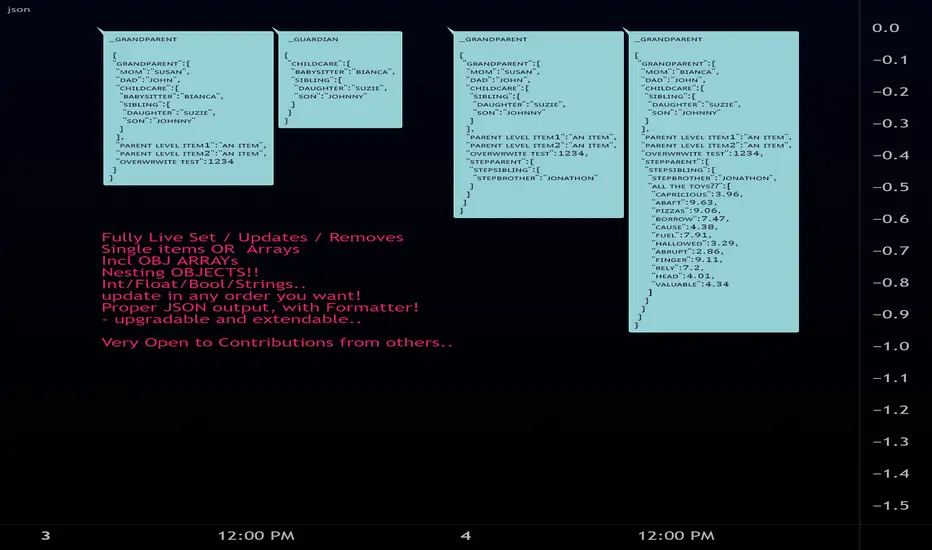

jsonLibrary "json"

JSON Easy Object Create/stringiffy

Functions to add/write JSON

new (name , kind) -> object

set (_item , _obj , _key ) -> key index for parent object's array

add (_obj , _key , _item ) -> key index for parent object's array

write (object , kind ) -> stringified object // (enter kind to cut off key )

============================================

obj

obj Object storage container/item

Fields:

key : (string ) item name

kind : (string ) item's type(for writing)

item : (string ) item (converted to string)

keys : (string ) keys of all sub-items and objects

items : (obj ) nested obj off individual subitems (for later...)

============================================

new(_name, _kind)

create multitype object

Parameters:

_name : (string) Name off object

_kind : (string) Preset Type (_OBJECT if a container item)

Returns: object container/item 2-in-1

============================================

add(_item, _obj, _key)

Set item to object obj item (same as set, prep for future Pine methods)

Parameters:

_item : ( int / float / bool / string )

_obj : (obj multi-type-item object)

_key : ( string )

set(_item, _obj, _key)

Set item to object obj item (same as add, prep for future Pine methods)

Parameters:

_item : ( int / float / bool / string )

_obj : (obj multi-type-item object)

_key : ( string )

addstore(_parent, _child)

Add a object as a subobject to storage (Future upgrade to write/edit)

Parameters:

_parent : to insert obj into

_child : to be inserted

setstore(_child, _parent)

Add a object as a subobject to storage (Future upgrade to write/edit)

Parameters:

_child : to be inserted

_parent : to insert obj into

add(_parent, _child)

Add a object as a string rendered item

Parameters:

_parent : to insert obj into

_child : to be inserted

set(_child, _parent)

Add a object as a string rendered item

Parameters:

_child : to be inserted

_parent : to insert obj into

============================================

write(_object, _key, _itemname)

Write object to string Object

Parameters:

_object : (obj)

_key : (array<(string/int)> )/(string)

_itemname : (string)

Returns: stringified flattened object.

clean_output(_str)

Clean JSON final output

Parameters:

_str : string json item

Returns: cleaned string

libcompressLibrary "libcompress"

numbers compressor for large output data compression

compress_fp24()

converts float to base64 (4 chars) | 24 bits: 1 sign + 5 exponent + 18 mantissa

Returns: 4-character base64_1/5/18 representation of x

compress_ufp18()

converts unsigned float to base64 (3 chars) | 18 bits: 5 exponent + 13 mantissa

Returns: 3-character base64_0/5/13 representation of x

compress_int()

converts int to base64

PineHelperLibrary "PineHelper"

This library provides various functions to reduce your time.

recent_opentrade_entry_bar_index()

get a recent opentrade entry bar_index

Returns: (int) bar_index

recent_closedtrade_entry_bar_index()

get a recent closedtrade entry bar_index

Returns: (int) bar_index

recent_closedtrade_exit_bar_index()

get a recent closedtrade exit bar_index

Returns: (int) bar_index

all_opnetrades_roi()

get all aopentrades roi

Returns: (float) roi

bars_since_recent_opentrade_entry()

get bars since recent opentrade entry

Returns: (int) number of bars

bars_since_recent_closedtrade_entry()

get bars since recent closedtrade entry

Returns: (int) number of bars

bars_since_recent_closedtrade_exit()

get bars since recent closedtrade exit

Returns: (int) number of bars

recent_opentrade_entry_id()

get recent opentrade entry ID

Returns: (string) entry ID

recent_closedtrade_entry_id()

get recent closedtrade entry ID

Returns: (string) entry ID

recent_closedtrade_exit_id()

get recent closedtrade exit ID

Returns: (string) exit ID

recent_opentrade_entry_price()

get recent opentrade entry price

Returns: (float) price

recent_closedtrade_entry_price()

get recent closedtrade entry price

Returns: (float) price

recent_closedtrade_exit_price()

get recent closedtrade exit price

Returns: (float) price

recent_opentrade_entry_time()

get recent opentrade entry time

Returns: (int) time

recent_closedtrade_entry_time()

get recent closedtrade entry time

Returns: (int) time

recent_closedtrade_exit_time()

get recent closedtrade exit time

Returns: (int) time

time_since_recent_opentrade_entry()

get time since recent opentrade entry

Returns: (int) time

time_since_recent_closedtrade_entry()

get time since recent closedtrade entry

Returns: (int) time

time_since_recent_closedtrade_exit()

get time since recent closedtrade exit

Returns: (int) time

recent_opentrade_size()

get recent opentrade size

Returns: (float) size

recent_closedtrade_size()

get recent closedtrade size

Returns: (float) size

all_opentrades_size()

get all opentrades size

Returns: (float) size

recent_opentrade_profit()

get recent opentrade profit

Returns: (float) profit

all_opentrades_profit()

get all opentrades profit

Returns: (float) profit

recent_closedtrade_profit()

get recent closedtrade profit

Returns: (float) profit

recent_opentrade_max_runup()

get recent opentrade max runup

Returns: (float) runup

recent_closedtrade_max_runup()

get recent closedtrade max runup

Returns: (float) runup

recent_opentrade_max_drawdown()

get recent opentrade maxdrawdown

Returns: (float) mdd

recent_closedtrade_max_drawdown()

get recent closedtrade maxdrawdown

Returns: (float) mdd

max_open_trades_drawdown()

get max open trades drawdown

Returns: (float) mdd

recent_opentrade_commission()

get recent opentrade commission

Returns: (float) commission

recent_closedtrade_commission()

get recent closedtrade commission

Returns: (float) commission

qty_by_percent_of_equity(percent)

get qty by percent of equtiy

Parameters:

percent : (series float) percent that you want to set

Returns: (float) quantity

qty_by_percent_of_position_size(percent)

get size by percent of position size

Parameters:

percent : (series float) percent that you want to set

Returns: (float) size

is_day_change()

get bool change of day

Returns: (bool) day is change or not

is_in_trade()

get bool using number of bars

Returns: (bool) allowedToTrade

discord_message(name, message)

get json format discord message

Parameters:

name : (string) name of bot

message : (string) message that you want to send

Returns: (string) json format string

telegram_message(chat_id, message)

get json format telegram message

Parameters:

chat_id : (string) chatId of bot

message : (string) message that you want to send

Returns: (string) json format string

Binance_Min_Limit_Order_amount_libraryLibrary "Binance_Min_Limit_Order_amount_library"

TODO: This library give us the minimum Limit Order amount for the contract in Binance.

m_qty(n_v, m_fee, t_fee, cost, m_t)

TODO: it give us the Minimum Qty for the trading in Binance

Parameters:

n_v : TODO: min_notional_value. 5 dollar is the minimum notional amount in Binance at the moment.

m_fee : TODO: maker_fee %

t_fee : TODO: taker_fee %

cost : TODO: your investing money

m_t : TODO: if you want Limit_Order, put the "T", if you want Market_Order, put the "M" defval="M"

Returns: TODO: for the coin of binance on your chart,

Reference: www.binance.com

LevelsManagerLibrary "LevelsManager"

TODO: Track up to 6 TakeProfits and 1 StopLoss achievement for one or many of your buy/sell conditions.

manageTrade(bool, bool, bool, string, string, float, float, bool, bool, bool, bool, bool, bool, float, float, float, float, float, float, float)

Track TakeProfits and StopLoss achievement for one or many of your buy/sell conditions. CHECK the commented section: "Function @manageTrade" for Description

Parameters:

bool : useSignal.

bool : b_gameOVer.

bool : b_gameOVer.

string : bName.

string : sName.

float : buyEntrySource.

float : sellEntrySource.

bool : useTp1.

bool : useTp2.

bool : useTp3.

bool : useTp4.

bool : useTp5.

bool : useTp6.

float : tp1x.

float : tp2x.

float : tp3x.

float : tp4x.

float : tp5x.

float : tp6x.

float : slx.

Returns: check commented section: "Function @manageTrade".

showOnlyFirstOccurence(booleanInput)

Single out the occurence of a bool series between to 2 bool series.

Parameters:

booleanInput : to activate or deactivate occurences filtering.

Returns: filterred or not bool series.

RouterOrdersIronLibrary "RouterOrdersIron"

Library for routing orders to the Binance exchange.

MsgDoLongMKT(id, symbol, balance)

Returns json for Iron to buy a symbol for the amount of the balance with market order.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

MsgDoShortMKT(id, symbol, balance)

Returns json for Iron to sell a symbol for the amount of the balance with market order.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

MsgDoLongLR(id, symbol, balance)

Returns json for Iron to buy a symbol for the amount of the balance. It is set at the best price and is re-set each time if a new price has risen before the application.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

MsgDoShortLR(id, symbol, balance)

Returns json for Iron to sell a symbol for the amount of the balance. It is set at the best price and is re-set each time if a new price has risen before the application.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

DoLongMKT(id, symbol, balance)

Buy a symbol for the amount of the balance. It is send market order to Iron.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

DoShortMKT(id, symbol, balance)

Sell a symbol for the amount of the balance. It is send market order to Iron.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

DoLongLR(id, symbol, balance)

Buy a symbol for the amount of the balance. It is set at the best price and is re-set each time if a new price has risen before the application.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

DoShortLR(id, symbol, balance)

Sell a symbol for the amount of the balance. It is set at the best price and is re-set each time if a new price has risen before the application.

Parameters:

id : ID of your Iron router.

symbol : Symbol for a trade, BTC example

balance : The amount for which to carry out the transaction.

Returns: true

GetQty(price, balance)

Get Qty for strategy on balance

Parameters:

price : Order price

balance : The amount for which to carry out the transaction.

Returns: Qty for strategy order TV

TradingHookLibrary "TradingHook"

This library is a client script for making a webhook signal formatted string to TradingHook webhook server.

buy_message(password, amount, order_name) Make a buy Message for TradingHook.

Parameters:

password : (string) password that you set in .env file.

amount : (float) amount. If not set, your strategy qty will be sent.

order_name : (string) order_name. The default name is "Order".

Returns: (string) A string containing the formatted webhook message.

sell_message(password, percent, order_name) Make a sell message for TradingHook.

Parameters:

password : (string) password that you set in .env file.

percent : (string) what percentage of your quantity you want to sell.

order_name : (string) order_name. The default name is "Order".

Returns: (string) A string containing the formatted webhook message.

You can use TradingHook WebServer open source code in github(github.com)

Timed_exit_alert_for_webhookLibrary "Timed_exit_alert_for_webhook"

TODO: add library description here

fun(x) TODO: add function description here

Parameters:

x : TODO: add parameter x description here

Returns: TODO: add what function returns

for exiting FCM like Tradovate and AMP using API and python MT5 and Webhooks

the writer take no responsibility for trades made using this script its written for informational purposes only

MakeLoveNotWarLibrary "MakeLoveNotWar"

Make Love Not War, place a flag of support on your chart!

flag(pos, text_size) Make Love Not War function.

Parameters:

pos : string, position.

text_size : string, text size.

Returns: table.

The Divergent LibraryLibrary "TheDivergentLibrary"

The Divergent Library is only useful when combined with the Pro version of The Divergent - Advanced divergence indicator . This is because the Basic (free) version of The Divergent does not expose the "Divergence Signal" value.

Usage instructions:

1. Create a new chart

2. Add The Divergent (Pro) indicator to your chart

3. Create a new strategy, import this library, add a "source" input, link it to "The Divergent: Divergence Signal", and use the library to decode the divergence signals from The Divergent (You can find example strategy code published in our profile)

4. Act on the divergences signalled by The Divergent

---

isRegularBullishEnabled(context) Returns a boolean value indicating whether Regular Bullish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Regular Bullish divergence detection is enabled in The Divergent.

isHiddenBullishEnabled(context) Returns a boolean value indicating whether Hidden Bullish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Hidden Bullish divergence detection is enabled in The Divergent.

isRegularBearishEnabled(context) Returns a boolean value indicating whether Regular Bearish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Regular Bearish divergence detection is enabled in The Divergent.

isHiddenBearishEnabled(context) Returns a boolean value indicating whether Hidden Bearish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Hidden Bearish divergence detection is enabled in The Divergent.

getPivotDetectionSource(context) Returns the 'Pivot Detection Source' setting of The Divergent. The returned value can be either "Oscillator" or "Price".

Parameters:

context : The context of The Divergent Library.

Returns: One of the following string values: "Oscillator" or "Price".

getPivotDetectionMode(context) Returns the 'Pivot Detection Mode' setting of The Divergent. The returned value can be either "Bodies" or "Wicks".

Parameters:

context : The context of The Divergent Library.

Returns: One of the following string values: "Bodies" or "Wicks".

isLinked(context) Returns a boolean value indicating the link status to The Divergent indicator.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating the link status to The Divergent indicator.

init(firstBarSignal, displayLinkStatus, debug) Initialises The Divergent Library's context with the signal produced by The Divergent on the first bar. The value returned from this function is called the "context of The Divergent Library". Some of the other functions of this library requires you to pass in this context.

Parameters:

firstBarSignal : The signal from The Divergent indicator on the first bar.

displayLinkStatus : A boolean value indicating whether the Link Status window should be displayed in the bottom left corner of the chart. Defaults to true.

debug : A boolean value indicating whether the Link Status window should display debug information. Defaults to false.

Returns: A bool array containing the context of The Divergent Library.

processSignal(signal) Processes a signal from The Divergent and returns a 5-tuple with the decoded signal: [ int divergenceType, int priceBarIndexStart, int priceBarIndexEnd, int oscillatorBarIndexStart, int oscillatorBarIndexEnd]. `divergenceType` can be one of the following values: na → No divergence was detected, 1 → Regular Bullish, 2 → Regular Bullish early, 3 → Hidden Bullish, 4 → Hidden Bullish early, 5 → Regular Bearish, 6 → Regular Bearish early, 7 → Hidden Bearish, 8 → Hidden Bearish early.

Parameters:

signal : The signal from The Divergent indicator.

Returns: A 5-tuple with the following values: [ int divergenceType, int priceBarIndexStart, int priceBarIndexEnd, int oscillatorBarIndexStart, int oscillatorBarIndexEnd].

DiscordWebhookFunctionLibrary "DiscordWebhookFunction"

discordMarkdown(_str, _italic, _bold, _code, _strike, _under) Convert string to markdown formatting User can combine any function at the same time.

Parameters:

_str : String input

_italic : Italic

_bold : Bold

_code : Code markdown

_strike : Strikethrough

_under : Underline

Returns: string Markdown formatted string.

discordWebhookJSON(_username, _avatarImgUrl, _contentText, _bodyTitle, _descText, _bodyUrl, _embedCol, _timestamp, _authorName, _authorUrl, _authorIconUrl, _footerText, _footerIconUrl, _thumbImgUrl, _imageUrl) Convert data to JSON format for Discord Webhook Integration.

Parameters:

_username : Override bot (webhook) username string / name,

_avatarImgUrl : Override bot (webhook) avatar by image URL,

_contentText : Main content page message,

_bodyTitle : Custom Webhook's embed message body title,

_descText : Webhook's embed message body description,

_bodyUrl : Webhook's embed body direct link URL,

_embedCol : Webhook's embed color,

_timestamp : Timestamp,

_authorName : Webhook's embed author name / title,

_authorUrl : Webhook's embed author direct link URL,

_authorIconUrl : Webhook's embed author icon by image URL,

_footerText : Webhook's embed footer text / title,

_footerIconUrl : Webhook's embed footer icon by image URL,

_thumbImgUrl : Webhook's embed thumbnail image URL,

_imageUrl : Webhook's embed body image URL.

Returns: string Single-line JSON format

FibonacciRetracementHi all!

This library will help you draw Fibonacci retracement levels (zones). The code is from my indicator "Fibonacci retracement" (). You can see that description for more information about the behaviour and example of how to use this library. The code is almost the same with the addition of alerts. If the alert frequency is 'alert.freq_once_per_bar_close' alert messages will be concatenated and have a header saying how many messages it contains (if it's more than 1).

Hope this is of help!

Library "FibonacciRetracement"

ConcateAlerts(context)

Concatenates all alerts from the bar to one string (separated by new lines) and clears alert messages on the current bar.

Parameters:

context (Context)

AddAlert(context, message, unshiftInsteadOfPush)

Parameters:

context (Context)

message (string)

unshiftInsteadOfPush (bool)

Range(context, structure, settings)

Will return values if new levels/zones should be drawn.

Parameters:

context (Context) : The 'Context' for the Fibonacci retracement.

structure (Structure type from mickes/PriceAction/1) : The current 'Structure' from the 'MarketStructure' library.

settings (Settings) : The 'Settings' object for the 'Context'.

Returns: A tuple with the start and end pivot if new zones should be drawn, ' ' otherwise.

DrawAll(context, settings, start, end)

Draws lines and labels for the zone. It will also set the 'Price' value that will be used for absolute positions.

Parameters:

context (Context) : The 'Context' for the Fibonacci retracement.

settings (Settings) : The 'Settings' object for the 'Context'.

start (Pivot type from mickes/PriceAction/1)

end (Pivot type from mickes/PriceAction/1)

AlertActive(context, settings)

Will alert for all zones that are active. If multiple alert messages are added they will be concatenated (separated by a new line) with a header saying how many messages the alert contains.

Parameters:

context (Context) : The 'Context' for the Fibonacci retracement. This contains the zones that will be alerted if price (wick or close according to the settings) enters it.

settings (Settings) : The 'Settings' object for the 'Context'.

TrendlineSettings

Holds all the values for 'TrendlineSettings'.

Fields:

Enabled (series bool) : If the trendline should be visible or not.

Color (series color) : The color of the trendline.

Style (series string) : The style of the trendline (as a string).

GenericZonesSettings

Holds all the values for 'GenericZonesSettings', that will be applicable to all drawn objects.

Fields:

ExtendRight (series bool) : If all lines should extend to the right or not.

Style (series string) : The style of all drawn lines

Reverse (series bool) : If true, all lines will be reversed.

Prices (series bool) : If price levels should be shown or not.

Levels (series bool) : If levels should be shown or not.

LevelsValue (series string) : Either 'Value' or 'Percent'. Defined if value or percentage should be shown.

FontSize (series int) : The for size of the text in labels drawn.

LabelsPosition (series string) : Coul be 'Left', 'Rigth' or 'Adapt'. 'Adapt' will try to adapt the labels position to the prices.

ZoneSettings

Holds all the values for 'ZoneSettings'.

Fields:

Enabled (series bool) : If this zone is enabled or not.

Level (series float) : The level of the zone.

Color (series color) : The color that will be displayed.

Price (series float) : The price of the level. Will be set internally.

Settings

Holds all the values for 'Settings'.

Fields:

PivotLeftLength (series int) : The left length used to find pivots through the 'MarketStructure' library.

PivotRightLength (series int) : The right length used to find pivots through the 'MarketStructure' library.

Trendline (TrendlineSettings) : The settings for the 'Trendline' object.

GenericZonesSettings (GenericZonesSettings) : The setting applicable to all zones.

AlertFrequency (series string) : The frequency for the alerts. If 'alert.freq_once_per_bar_close', alert messages will be concatenated and have a header saying how many messages it contains (if it's more than 1).

AlertPrice (series string) : The price that has to enter a zone. Can be 'Close' (the closing price) or 'Wick' (the whole candle needs to be in the zone).

Zone1 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone2 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone3 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone4 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone5 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone6 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone7 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone8 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone9 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone10 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone11 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone12 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone13 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone14 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone15 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone16 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone17 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone18 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone19 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone20 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone21 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone22 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone23 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Zone24 (ZoneSettings) : The 'ZoneSettings' that represents this zone.

Context

Holds all the values for 'Context'.

Fields:

Lines (array) : All the drawn lines for the current 'Context'.

Labels (array) : All the drawn labels for the current 'Context'.

Boxes (array) : All the drawn boxes for the current 'Context'.

Alerts (array) : All the alert messages on the current tick.

Start (series int) : The start bar index of the current 'Context'.

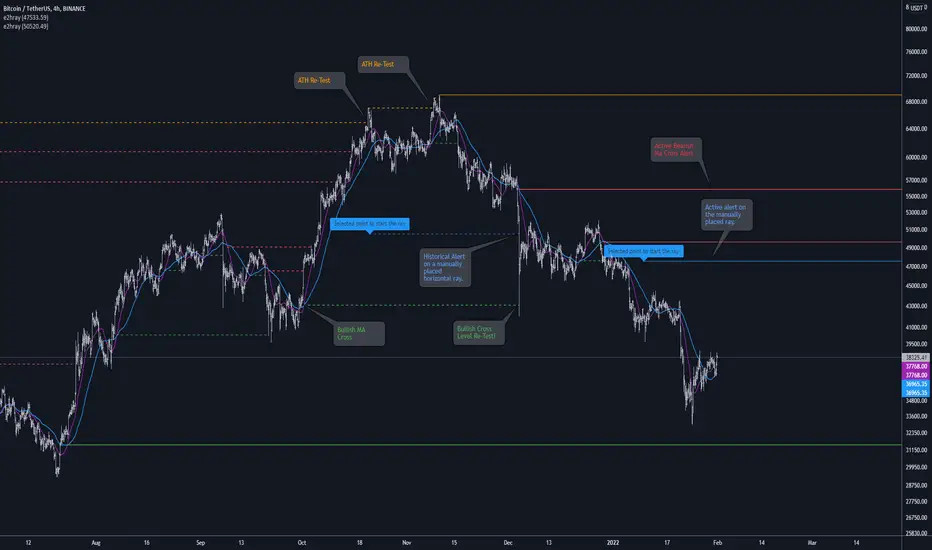

[e2] Drawing Library :: Horizontal Ray█ OVERVIEW

Library "e2hray"

A drawing library that contains the hray() function, which draws a horizontal ray/s with an initial point determined by a specified condition. It plots a ray until it reached the price. The function let you control the visibility of historical levels and setup the alerts.

█ HORIZONTAL RAY FUNCTION

hray(condition, level, color, extend, hist_lines, alert_message, alert_delay, style, hist_style, width, hist_width)

Parameters:

condition : Boolean condition that defines the initial point of a ray

level : Ray price level.

color : Ray color.

extend : (optional) Default value true, current ray levels extend to the right, if false - up to the current bar.

hist_lines : (optional) Default value true, shows historical ray levels that were revisited, default is dashed lines. To avoid alert problems set to 'false' before creating alerts.

alert_message : (optional) Default value string(na), if declared, enables alerts that fire when price revisits a line, using the text specified

alert_delay : (optional) Default value int(0), number of bars to validate the level. Alerts won't trigger if the ray is broken during the 'delay'.

style : (optional) Default value 'line.style_solid'. Ray line style.

hist_style : (optional) Default value 'line.style_dashed'. Historical ray line style.

width : (optional) Default value int(1), ray width in pixels.

hist_width : (optional) Default value int(1), historical ray width in pixels.

Returns: void

█ EXAMPLES

• Example 1. Single horizontal ray from the dynamic input.

//@version=5

indicator("hray() example :: Dynamic input ray", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

inputTime = input.time(timestamp("20 Jul 2021 00:00 +0300"), "Date", confirm = true)

inputPrice = input.price(54, 'Price Level', confirm = true)

e2draw.hray(time == inputTime, inputPrice, color.blue, alert_message = 'Ray level re-test!')

var label mark = label.new(inputTime, inputPrice, 'Selected point to start the ray', xloc.bar_time)

• Example 2. Multiple horizontal rays on the moving averages cross.

//@version=5

indicator("hray() example :: MA Cross", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

float sma1 = ta.sma(close, 20)

float sma2 = ta.sma(close, 50)

bullishCross = ta.crossover( sma1, sma2)

bearishCross = ta.crossunder(sma1, sma2)

plot(sma1, 'sma1', color.purple)

plot(sma2, 'sma2', color.blue)

// 1a. We can use 2 function calls to distinguish long and short sides.

e2draw.hray(bullishCross, sma1, color.green, alert_message = 'Bullish Cross Level Broken!', alert_delay = 10)

e2draw.hray(bearishCross, sma2, color.red, alert_message = 'Bearish Cross Level Broken!', alert_delay = 10)

// 1b. Or a single call for both.

// e2draw.hray(bullishCross or bearishCross, sma1, bullishCross ? color.green : color.red)

• Example 3. Horizontal ray at the all time highs with an alert.

//@version=5

indicator("hray() example :: ATH", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

var float ath = 0, ath := math.max(high, ath)

bool newAth = ta.change(ath)

e2draw.hray(nz(newAth ), high , color.orange, alert_message = 'All Time Highs Tested!', alert_delay = 10)

CCOMET_Scanner_LibraryLibrary "CCOMET_Scanner_Library"

- A Trader's Edge (ATE)_Library was created to assist in constructing CCOMET Scanners

Loc_tIDs_Col(_string, _firstLocation)

TickerIDs: You must form this single tickerID input string exactly as described in the scripts info panel (little gray 'i' that

is circled at the end of the settings in the settings/input panel that you can hover your cursor over this 'i' to read the

details of that particular input). IF the string is formed correctly then it will break up this single string parameter into

a total of 40 separate strings which will be all of the tickerIDs that the script is using in your CCOMET Scanner.

Locations: This function is used when there's a desire to print an assets ALERT LABELS. A set Location on the scale is assigned to each asset.

This is created so that if a lot of alerts are triggered, they will stay relatively visible and not overlap each other.

If you set your '_firstLocation' parameter as 1, since there are a max of 40 assets that can be scanned, the 1st asset's location

is assigned the value in the '_firstLocation' parameter, the 2nd asset's location is the (1st asset's location+1)...and so on.

Parameters:

_string (simple string) : (string)

A maximum of 40 Tickers (ALL joined as 1 string for the input parameter) that is formulated EXACTLY as described

within the tooltips of the TickerID inputs in my CCOMET Scanner scripts:

assets = input.text_area(tIDset1, title="TickerID (MUST READ TOOLTIP)", tooltip="Accepts 40 TICKERID's for each

copy of the script on the chart. TEXT FORMATTING RULES FOR TICKERID'S:

(1) To exclude the EXCHANGE NAME in the Labels, de-select the next input option.

(2) MUST have a space (' ') AFTER each TickerID.

(3) Capitalization in the Labels will match cap of these TickerID's.

(4) If your asset has a BaseCurrency & QuoteCurrency (ie. ADAUSDT ) BUT you ONLY want Labels

to show BaseCurrency(ie.'ADA'), include a FORWARD SLASH ('/') between the Base & Quote (ie.'ADA/USDT')", display=display.none)

_firstLocation (simple int) : (simple int)

Optional (starts at 1 if no parameter added).

Location that you want the first asset to print its label if is triggered to do so.

ie. loc2=loc1+1, loc3=loc2+1, etc.

Returns: Returns 40 output variables in the tuple (ie. between the ' ') with the TickerIDs, 40 variables for the locations for alert labels, and 40 Colors for labels/plots

TickeridForLabelsAndSecurity(_ticker, _includeExchange)

This function accepts the TickerID Name as its parameter and produces a single string that will be used in all of your labels.

Parameters:

_ticker (simple string) : (string)

For this parameter, input the varible named '_coin' from your 'f_main()' function for this parameter. It is the raw

Ticker ID name that will be processed.

_includeExchange (simple bool) : (bool)

Optional (if parameter not included in function it defaults to false ).

Used to determine if the Exchange name will be included in all labels/triggers/alerts.

Returns: ( )

Returns 2 output variables:

1st ('_securityTickerid') is to be used in the 'request.security()' function as this string will contain everything

TV needs to pull the correct assets data.

2nd ('lblTicker') is to be used in all of the labels in your CCOMET Scanner as it will only contain what you want your labels

to show as determined by how the tickerID is formulated in the CCOMET Scanner's input.

InvalID_LblSz(_barCnt, _close, _securityTickerid, _invalidArray, _tablePosition, _stackVertical, _lblSzRfrnce)

INVALID TICKERIDs: This is to add a table in the middle right of your chart that prints all the TickerID's that were either not formulated

correctly in the '_source' input or that is not a valid symbol and should be changed.

LABEL SIZES: This function sizes your Alert Trigger Labels according to the amount of Printed Bars the chart has printed within

a set time period, while also keeping in mind the smallest relative reference size you input in the 'lblSzRfrnceInput'

parameter of this function. A HIGHER % of Printed Bars(aka...more trades occurring for that asset on the exchange),

the LARGER the Name Label will print, potentially showing you the better opportunities on the exchange to avoid

exchange manipulation liquidations.

*** SHOULD NOT be used as size of labels that are your asset Name Labels next to each asset's Line Plot...

if your CCOMET Scanner includes these as you want these to be the same size for every asset so the larger ones dont cover the

smaller ones if the plots are all close to each other ***

Parameters:

_barCnt (float) : (float)

Get the 1st variable('barCnt') from the Security function's tuple and input it as this functions 1st input

parameter which will directly affect the size of the 2nd output variable ('alertTrigLabel') that is also outputted by this function.

_close (float) : (float)

Put your 'close' variable named '_close' from the security function here.

_securityTickerid (string) : (string)

Throughout the entire charts updates, if a '_close' value is never registered then the logic counts the asset as INVALID.

This will be the 1st TickerID variable (named _securityTickerid) outputted from the tuple of the TickeridForLabels()

function above this one.

_invalidArray (array) : (array string)

Input the array from the original script that houses all of the invalidArray strings.

_tablePosition (simple string) : (string)