Super-AO with Risk Management Strategy Template - 11-29-25Super-AO Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to the Super-AO Strategy. This is more than just a buy/sell indicator; it is a complete, open-source Risk Management (RM) Template designed for the Pine Script community.

At its core, this script implements a robust swing-trading strategy combining the SuperTrend (for macro direction) and the Awesome Oscillator (for momentum). However, the real power lies under the hood: a custom-built Risk Management Engine that handles trade states, prevents repainting, and manages complex exit conditions like Staged Take Profits and Advanced Adaptive Trailing Stops (AATS).

We are releasing this code to help traders transition from simple indicators to professional-grade strategy structures.

2. Quick Action Guide (TL;DR)

Best Timeframe: 4 Hours (H4) and above. Designed for Swing Trading.

Best Assets: "Well-behaved" assets with clear liquidity (Major Forex pairs, BTC, ETH, Indices).

Strategy Type: Trend Following + Momentum Confirmation.

Key Feature: The Risk Management Engine is modular. You can strip out the "Super-AO" logic and insert your own strategy logic into the template easily.

Repainting: Strictly Non-Repainting. The engine calculates logic based on confirmed candle closes.

3. Detailed Report: How It Works

A. The Strategy Logic: Super-AO

The entry logic is based on the convergence of two classic indicators:

SuperTrend: Determines the overall trend bias (Green/Red).

Awesome Oscillator (AO): Measures market momentum.

The Signal:

LONG (+2): SuperTrend is Green AND AO is above the Zero Line AND AO is Rising.

SHORT (-2): SuperTrend is Red AND AO is below the Zero Line AND AO is Falling.

By requiring momentum to agree with the trend, this system filters out many false signals found in ranging markets.

B. The Risk Management (RM) Engine

This script features a proprietary State Machine designed by Signal Lynx. Unlike standard strategies that simply fire orders, this engine separates the Signal from the Execution.

Logic Injection: The engine listens for a specific integer signal: +2 (Buy) or -2 (Sell). This makes the code a Template. You can delete the Super-AO section, write your own logic, and simply pass a +2 or -2 to the RM_EngineInput variable. The engine handles the rest.

Trade States: The engine tracks the state of the trade (Entry, In-Trade, Exiting) to prevent signal spamming.

Aggressive vs. Conservative:

Conservative Mode: Waits for a full trend reversal before taking a new trade.

Aggressive Mode: Allows for re-entries if the trend is strong and valid conditions present themselves again (Pyramiding Type 1).

C. Advanced Exit Protocols

The strategy does not rely on a single exit point. It employs a "Layered Defense" approach:

Hard Stop Loss: A fixed percentage safety net.

Staged Take Profits (Scaling Out): The script allows you to set 3 distinct Take Profit levels. For example, you can close 10% of your position at TP1, 10% at TP2, and let the remaining 80% ride the trend.

Trailing Stop: A standard percentage-based trailer.

Advanced Adaptive Trailing Stop (AATS): This is a highly sophisticated volatility stop. It calculates market structure using Hirashima Sugita (HSRS) levels and Bollinger Bands to determine the "floor" and "ceiling" of price action.

If volatility is high: The stop loosens to prevent wicking out.

If volatility is low: The stop tightens to protect profit.

D. Repainting Protection

Many Pine Script strategies look great in backtesting but fail in live trading because they rely on "real-time" price data that disappears when the candle closes.

This Risk Management engine explicitly pulls data from the previous candle close (close , high , low ) for its calculations. This ensures that the backtest results you see match the reality of live execution.

4. For Developers & Modders

We encourage you to tear this code apart!

Look for the section titled // Super-AO Strategy Logic.

Replace that block with your own RSI, MACD, or Price Action logic.

Ensure your logic outputs a 2 for Buy and -2 for Sell.

Connect it to RM_EngineInput.

You now have a fully functioning Risk Management system for your custom strategy.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

This code has been in action since 2022 and is a known performer in PineScript v5. We provide this open source to help the community build better, safer automated systems.

If you are looking to automate your strategies, please take a look at Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source). If you make beneficial modifications, please release them back to the community!

ابحث في النصوص البرمجية عن "backtesting"

Double MOST with Pivot and EMAMOST Long Strategy with Multi-Filter Confirmation (Pivot + VAR Trend Filter)

This strategy combines a custom MOST stop-line structure with a moving average trend filter (EMA / VAR / ZLMA), daily pivot levels, and a 9-period VAR filter to generate clean long-only entries.

It aims to capture early trend continuations while avoiding reversals and false breakouts.

✔ Buy Conditions

A long position is opened only if all of the conditions below occur simultaneously:

MA (ort) > MOST Line (s2)

– Confirms that momentum is on the long side.

Price > Daily Pivot (pvt_gun)

– Ensures the market is trading above the day’s fair-value level.

Price > VAR(9)

– Short-term VAR filter to confirm trend strength and reduce noise.

Only the first bar where all conditions turn true generates a position.

✔ Sell Condition

A long position is closed when:

MOST Line (s2) crosses above MA (ort)

– Indicates a momentum shift against the long position.

✔ Execution Style (MetaStock-like)

Strategy operates long-only

Orders are filled on the next bar open, not on the signal bar

Commission: 0.03% (3 bps / on-binde 3)

Position size: 100% of equity per trade

This makes the behavior comparable to classical MetaStock backtesting logic.

✔ Chart Markers

Only actual trade entries and exits are drawn

No repeated signals or overlapping markers

Clean visual trade history

Purpose

This strategy is ideal for traders who want:

A structured long-only trend model

A multi-layer confirmation filter

Clean execution without repaint

High-quality entries above market structure levels

Dual MTF Confirmed Trend Strategy (5m Entry / 15m MACD & RSI) v1That is a detailed Dual Multi-Timeframe (MTF) Confirmed Trend Strategy written in Pine Script for TradingView. The core idea of this strategy is to only take entry signals on a faster timeframe (5-minute) when the trend is strongly confirmed on a slower, higher timeframe (15-minute). This aims to reduce false signals and trade in the direction of the dominant trend. Here is an explanation of how the strategy works, broken down by section:

1. 5-Minute Entry Filters 🚀This section calculates several indicators on the current 5-minute chart to identify potential trade setups. A position is only considered if all 5-minute conditions align.

Supertrend: A trend-following indicator based on Average True Range (ATR).

Long Condition: The closing price must be above the Supertrend line.

Short Condition: The closing price must be below the Supertrend line.

Gann Hi-Lo (GHL): A trend indicator using Simple Moving Averages (SMA) of the high and low prices. GHL Line: Switches between the SMA of the Highs and the SMA of the Lows based on price action.

Long Condition: The closing price must be above the GHL line.

Short Condition: The closing price must be below the GHL line.

Exponential Moving Averages (EMAs): It uses a 50-period EMA and a 100-period EMA to confirm the short-term trend direction.

Long Condition: The closing price must be above both the 50 EMA and the 100 EMA.

Short Condition: The closing price must be below both the 50 EMA and the 100 EMA.

2. 15-Minute MTF Confirmation Filters ⏳This is the crucial step where the strategy verifies the trend on the slower, 15-minute timeframe using the request security function. This step acts as a gatekeeper to ensure the 5-minute trade aligns with the larger trend.

MACD Histogram (12, 26, 9): The difference between the MACD Line and the Signal Line.

Long Confirmation: The 15m MACD Histogram must be greater than 0 (MACD line is above the Signal line, indicating bullish momentum).

Short Confirmation: The 15m MACD Histogram must be less than 0 (MACD line is below the Signal line, indicating bearish momentum).

RSI (Relative Strength Index) (14): A momentum oscillator. The 50 level is often used to determine the general market trend.

Long Confirmation: The 15m RSI must be greater than 50 (indicating stronger bullish momentum).

Short Confirmation: The 15m RSI must be less than 50 (indicating stronger bearish momentum).

The Total 15m Confirmation is only true if both the MACD and the RSI confirmation signals align.

3. Trade Orders (Entry Logic) ⚖️

The strategy only executes a trade when the 5-minute entry conditions are met AND the 15-minute confirmation conditions are met.

Final Long Condition:

5m Conditions (Supertrend, GHL, EMA alignment) AND

15m Confirmation (MACD Hist > 0 AND RSI > 50)

Final Short Condition:

5m Conditions (Supertrend, GHL, EMA alignment) AND

15m Confirmation (MACD Hist < 0 AND RSI < 50)

When a trade signal is generated, the strategy:

Closes any opposite position (e.g., closes a "Short" trade if a "Long" signal appears).

Enters the new position (e.g., enters a "Long" trade).

This is designed as a reversal strategy where a new entry automatically closes the previous opposing trade.

In Summary

The strategy operates on a principle of Trend Alignment:

5-Minute Chart: Is used for Signal Timing (when exactly to enter the market).

15-Minute Chart: Is used for Trend Validation (is the overall market momentum supporting the signal?).

It's an attempt to capture short-term moves (5m signals) that are backed by strong medium-term momentum (15m confirmation), thereby aiming for higher probability trades.

This is not investment advice; it is recommended to perform optimization and backtesting for the assets intended for implementation.

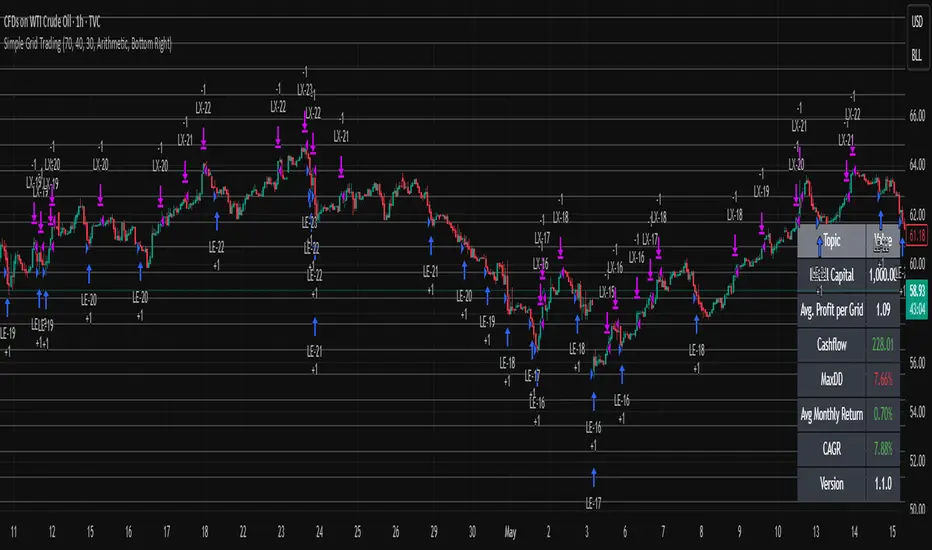

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

15m ORB Breakout NAS100 (5m Mgmt) v6 - OptimizedOpening Range Breakout Strategy

Buy and sell signals are given upon break of market session opening range. Best utilized for 30 minute NY opening range, managed on 5 min timeframe on NAS100. Tweak the settings for higher win rate on backtesting dashboard before implementing strategy.

Oracle Protocol — Arch Public (Testing Clone) Oracle Protocol — Arch Public Series (testing clone)

This model implements the Arch Public Oracle structure: a systematic accumulation-and-distribution engine built around a dynamic Accumulation Cost Base (ACB), strict profit-gate exit logic, and a capital-bounded flywheel reinvestment system.

It is designed for transparent execution, deterministic behaviour, and rule-based position management.

Core Function Set

1. Accumulation Framework (ACB-Driven)

The accumulation engine evaluates market movement against defined entry conditions, including:

Percentage-based entry-drop triggers

Optional buy-below-ACB mode

Capital-gated entries tied to available ledger balance

Fixed-dollar and min-dollar entry rules (as seen in Arch public materials)

Automated sizing through flywheel capital

Range-bounded ledger for controlled backtesting input

Each qualifying buy updates the live ACB, maintains the internal ledger, and forms the next reference point for exit evaluation.

No forecasting mechanisms are included.

2. Profit-Gate Exit System

Exits are governed by the standard Arch public approach:

A sealed ACB reference for threshold evaluation

Optional live-ACB visibility

Profit-gate triggers defined per asset class

Candle-confirmation integration (“ProfitGate + Candle” mode)

Distribution only when the smallest active threshold is met

This provides a consistent cadence with published Arch diagrams and PDFs.

3. Once-Per-Rally Governance

After a distribution, the algorithm locks until price retraces below the most recent accumulation base.

Only after re-arming can the next profit gate activate.

This prevents over-frequency selling and aligns with the public-domain Oracle behaviour.

4. Quiet-Bars & Threshold Cluster Control

A volatility-stabilisation layer prevents multiple exits from micro-fluctuations or transient spikes.

This ensures clean execution during fast markets and high volatility.

5. Flywheel Reinvestment

Distribution proceeds automatically return to the capital pool where permitted, creating a closed system of:

Entry sizing

Exit proceeds

Ledger-managed capital state

All sizing respects capital boundaries and does not breach dollar floors or overrides.

6. Automation Hooks and Integration

The script exposes:

3Commas-compatible JSON sizing

Entry/exit signalling via alertcondition()

Deterministic event reporting suitable for external automation

This allows consistent deployment across automated execution environments.

7. Visual Tooling

Optional displays include:

Live ACB line

Exit-guide markers

Capital, state, and ledger panels

Realized/unrealized outcome tracking based on internal logic only

Visual components do not influence execution rules.

Operating Notes

This model is rule-based, deterministic, and non-predictive.

It executes only according to the explicit thresholds, capital limits, and state transitions defined within the script.

No discretionary or forward-looking logic is included.

Paulinho Signals – Cripto 5m/15m com Filtro de LateralidadeThis script is an automated Pine Script v6 strategy designed for short-term cryptocurrency trading, especially on 5-minute and 15-minute timeframes. It combines moving average crossovers, trend strength (ADX), volatility (ATR), and candlestick patterns to generate buy and sell signals with a fixed risk/reward management system.

How to Use:

- Apply to cryptocurrency charts on 5m or 15m timeframes.

- Adjust parameters to fit your preferences (EMA, RSI, ADX, ATR).

- Use for backtesting or as a decision-support tool.

Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Always test on demo accounts before applying to live trading.

MTF Scalper - alemicihanMulti-Timeframe Scalper Strategy: Aligning the Big Picture for Quick Gains

This article presents a robust futures trading strategy designed for high-frequency scalping in the crypto market. It’s built on the principle of minimizing risk by ensuring that short-term entries are always aligned with the dominant, higher-timeframe trend.

The Core Concept: Alignment is Key

A Balanced Trend Follower approach, now refined for rapid scalping, uses a Multi-Timeframe (MTF) confirmation system to filter out market noise and increase the probability of a successful trade.

The strategy operates on a Low Timeframe (LTF) chart (e.g., 3m, 5m, or 15m) but only executes trades if the direction is validated by three Higher Timeframes (HTF).

ComponentPurposeFunctionHTF (D, 4h, 1h) EMA => Trend Confirmation =>Checks if the current price is above/below all three Exponential Moving Averages (EMA 20). This provides a strong directional bias.

LTF (5m) Stochastic RSI => Momentum Entry => Generates the actual buy/sell signal by spotting a swift crossover, indicating fresh momentum in the direction of the confirmed HTF trend.

How The Signal Is Generated

Trend Alignment: The system first confirms the trend. If the price is trading above the Daily, 4-Hour, and 1-Hour EMAs, the market is deemed to be in a Strong LONG Trend. Only LONG signals are permitted.

Momentum Trigger: Once the trend is confirmed, a Long Signal is generated only when the Stochastic K-Line crosses above the D-Line, indicating a momentum shift (a pullback ending) towards the main trend direction.

Short Signal: The inverse logic applies to the Short Trend confirmation and entry signal.

Mandatory Risk Management: ATR-Based Exit

Given the high leverage nature of futures and scalping, static Stop-Loss (SL) and Take-Profit (TP) levels are inefficient. This strategy uses the Average True Range (ATR) indicator to dynamically set profit and loss targets based on current market volatility.

Stop Loss (SL): Set dynamically at 1.5 x ATR below (for long) or above (for short) the entry price. This gives the trade enough room to breathe without risking excessive capital.

Take Profit (TP): Set dynamically at 3.0 x ATR, establishing a robust Risk-to-Reward Ratio of 1:2.

Final Thoughts on Testing

This sophisticated approach combines the reliability of MTF analysis with the speed of momentum indicators. However, data analysis is key. Backtesting these parameters (EMA, ATR Multipliers, RSI/Stochastic lengths) on your chosen asset (like BTC/USDT or ETH/USDT) and timeframe is crucial to achieving optimal performance.

Macketings 1min ScalpingThis is a hyper-reactive scalping strategy designed for the 1-minute chart. It utilizes a strict four-EMA hierarchy (80/90/340/500) to ensure trades are only taken in the strongest aligned market trend. The strategy is built to be extremely tight on risk and focuses on capturing the immediate, high-momentum swing that follows a confirmed EMA retest or breakout.

Key Mechanics (How it Works):

Strict Trend Alignment: Entry is only permitted when the faster EMA band (80/90) and the price action are correctly aligned with the slow trend (340/500).

Long: EMA 80/90 must be above EMA 340/500, AND EMA 340 must be above EMA 500. (And vice-versa for Short.)

Expanded Retest Entry: The strategy waits for the price to retest or briefly enter the 80/90 band, then immediately enters upon the confirmed momentum breakout from that band.

Dynamic Risk Management (Tight Ride): The strategy is engineered to ride the wave aggressively while protecting capital immediately:

Extremely Tight Initial Stop Loss (0.2% default): Limits initial risk instantly.

Break-Even Security: Once profit hits 0.3%, the Stop Loss is automatically trailed to secure 0.2% profit (a risk-free trade).

Aggressive Exit Logic: Positions are closed not only upon hitting the Take Profit target (2.5%) but also immediately if the 80/90 EMA band crosses the 340 EMA, signaling a critical loss of momentum.

Disclaimer:

This strategy requires high-liquidity instruments and is best used on low timeframes (1-minute) due to its dependency on fast momentum shifts and tight stops. Backtesting and forward testing are crucial before deployment.

Any Strategy BacktestA simple script for backtesting your strategies with TP and SL settings. For this to work, your indicators must have sources for long and short conditions.

Range Oscillator Strategy + Stoch Confirm🔹 Short summary

This is a free, educational long-only strategy built on top of the public “Range Oscillator” by Zeiierman (used under CC BY-NC-SA 4.0), combined with a Stochastic timing filter, an EMA-based exit filter and an optional risk-management layer (SL/TP and R-multiple exits). It is NOT financial advice and it is NOT a magic money machine. It’s a structured framework to study how range-expansion + momentum + trend slope can be combined into one rule-based system, often with intentionally RARE trades.

────────────────────────

0. Legal / risk disclaimer

────────────────────────

• This script is FREE and public. I do not charge any fee for it.

• It is for EDUCATIONAL PURPOSES ONLY.

• It is NOT financial advice and does NOT guarantee profits.

• Backtest results can be very different from live results.

• Markets change over time; past performance is NOT indicative of future performance.

• You are fully responsible for your own trades and risk.

Please DO NOT use this script with money you cannot afford to lose. Always start in a demo / paper trading environment and make sure you understand what the logic does before you risk any capital.

────────────────────────

1. About default settings and risk (very important)

────────────────────────

The script is configured with the following defaults in the `strategy()` declaration:

• `initial_capital = 10000`

→ This is only an EXAMPLE account size.

• `default_qty_type = strategy.percent_of_equity`

• `default_qty_value = 100`

→ This means 100% of equity per trade in the default properties.

→ This is AGGRESSIVE and should be treated as a STRESS TEST of the logic, not as a realistic way to trade.

TradingView’s House Rules recommend risking only a small part of equity per trade (often 1–2%, max 5–10% in most cases). To align with these recommendations and to get more realistic backtest results, I STRONGLY RECOMMEND you to:

1. Open **Strategy Settings → Properties**.

2. Set:

• Order size: **Percent of equity**

• Order size (percent): e.g. **1–2%** per trade

3. Make sure **commission** and **slippage** match your own broker conditions.

• By default this script uses `commission_value = 0.1` (0.1%) and `slippage = 3`, which are reasonable example values for many crypto markets.

If you choose to run the strategy with 100% of equity per trade, please treat it ONLY as a stress-test of the logic. It is NOT a sustainable risk model for live trading.

────────────────────────

2. What this strategy tries to do (conceptual overview)

────────────────────────

This is a LONG-ONLY strategy designed to explore the combination of:

1. **Range Oscillator (Zeiierman-based)**

- Measures how far price has moved away from an adaptive mean.

- Uses an ATR-based range to normalize deviation.

- High positive oscillator values indicate strong price expansion away from the mean in a bullish direction.

2. **Stochastic as a timing filter**

- A classic Stochastic (%K and %D) is used.

- The logic requires %K to be below a user-defined level and then crossing above %D.

- This is intended to catch moments when momentum turns up again, rather than chasing every extreme.

3. **EMA Exit Filter (trend slope)**

- An EMA with configurable length (default 70) is calculated.

- The slope of the EMA is monitored: when the slope turns negative while in a long position, and the filter is enabled, it triggers an exit condition.

- This acts as a trend-protection exit: if the medium-term trend starts to weaken, the strategy exits even if the oscillator has not yet fully reverted.

4. **Optional risk-management layer**

- Percentage-based Stop Loss and Take Profit (SL/TP).

- Risk/Reward (R-multiple) exit based on the distance from entry to SL.

- Implemented as OCO orders that work *on top* of the logical exits.

The goal is not to create a “holy grail” system but to serve as a transparent, configurable framework for studying how these concepts behave together on different markets and timeframes.

────────────────────────

3. Components and how they work together

────────────────────────

(1) Range Oscillator (based on “Range Oscillator (Zeiierman)”)

• The script computes a weighted mean price and then measures how far price deviates from that mean.

• Deviation is normalized by an ATR-based range and expressed as an oscillator.

• When the oscillator is above the **entry threshold** (default 100), it signals a strong move away from the mean in the bullish direction.

• When it later drops below the **exit threshold** (default 30), it can trigger an exit (if enabled).

(2) Stochastic confirmation

• Classic Stochastic (%K and %D) is calculated.

• An entry requires:

- %K to be below a user-defined “Cross Level”, and

- then %K to cross above %D.

• This is a momentum confirmation: the strategy tries to enter when momentum turns up from a pullback rather than at any random point.

(3) EMA Exit Filter

• The EMA length is configurable via `emaLength` (default 70).

• The script monitors the EMA slope: it computes the relative change between the current EMA and the previous EMA.

• If the slope turns negative while the strategy holds a long position and the filter is enabled, it triggers an exit condition.

• This is meant to help protect profits or cut losses when the medium-term trend starts to roll over, even if the oscillator conditions are not (yet) signalling exit.

(4) Risk management (optional)

• Stop Loss (SL) and Take Profit (TP):

- Defined as percentages relative to average entry price.

- Both are disabled by default, but you can enable them in the Inputs.

• Risk/Reward Exit:

- Uses the distance from entry to SL to project a profit target at a configurable R-multiple.

- Also optional and disabled by default.

These exits are implemented as `strategy.exit()` OCO orders and can close trades independently of oscillator/EMA conditions if hit first.

────────────────────────

4. Entry & Exit logic (high level)

────────────────────────

A) Time filter

• You can choose a **Start Year** in the Inputs.

• Only candles between the selected start date and 31 Dec 2069 are used for backtesting (`timeCondition`).

• This prevents accidental use of tiny cherry-picked windows and makes tests more honest.

B) Entry condition (long-only)

A long entry is allowed when ALL the following are true:

1. `timeCondition` is true (inside the backtest window).

2. If `useOscEntry` is true:

- Range Oscillator value must be above `entryLevel`.

3. If `useStochEntry` is true:

- Stochastic condition (`stochCondition`) must be true:

- %K < `crossLevel`, then %K crosses above %D.

If these filters agree, the strategy calls `strategy.entry("Long", strategy.long)`.

C) Exit condition (logical exits)

A position can be closed when:

1. `timeCondition` is true AND a long position is open, AND

2. At least one of the following is true:

- If `useOscExit` is true: Oscillator is below `exitLevel`.

- If `useMagicExit` (EMA Exit Filter) is true: EMA slope is negative (`isDown = true`).

In that case, `strategy.close("Long")` is called.

D) Risk-management exits

While a position is open:

• If SL or TP is enabled:

- `strategy.exit("Long Risk", ...)` places an OCO stop/limit order based on the SL/TP percentages.

• If Risk/Reward exit is enabled:

- `strategy.exit("RR Exit", ...)` places an OCO order using a projected R-multiple (`rrMult`) of the SL distance.

These risk-based exits can trigger before the logical oscillator/EMA exits if price hits those levels.

────────────────────────

5. Recommended backtest configuration (to avoid misleading results)

────────────────────────

To align with TradingView House Rules and avoid misleading backtests:

1. **Initial capital**

- 10 000 (or any value you personally want to work with).

2. **Order size**

- Type: **Percent of equity**

- Size: **1–2%** per trade is a reasonable starting point.

- Avoid risking more than 5–10% per trade if you want results that could be sustainable in practice.

3. **Commission & slippage**

- Commission: around 0.1% if that matches your broker.

- Slippage: a few ticks (e.g. 3) to account for real fills.

4. **Timeframe & markets**

- Volatile symbols (e.g. crypto like BTCUSDT, or major indices).

- Timeframes: 1H / 4H / **1D (Daily)** are typical starting points.

- I strongly recommend trying the strategy on **different timeframes**, for example 1D, to see how the behaviour changes between intraday and higher timeframes.

5. **No “caution warning”**

- Make sure your chosen symbol + timeframe + settings do not trigger TradingView’s caution messages.

- If you see warnings (e.g. “too few trades”), adjust timeframe/symbol or the backtest period.

────────────────────────

5a. About low trade count and rare signals

────────────────────────

This strategy is intentionally designed to trade RARELY:

• It is **long-only**.

• It uses strict filters (Range Oscillator threshold + Stochastic confirmation + optional EMA Exit Filter).

• On higher timeframes (especially **1D / Daily**) this can result in a **low total number of trades**, sometimes WELL BELOW 100 trades over the whole backtest.

TradingView’s House Rules mention 100+ trades as a guideline for more robust statistics. In this specific case:

• The **low trade count is a conscious design choice**, not an attempt to cherry-pick a tiny, ultra-profitable window.

• The goal is to study a **small number of high-conviction long entries** on higher timeframes, not to generate frequent intraday signals.

• Because of the low trade count, results should NOT be interpreted as statistically strong or “proven” – they are only one sample of how this logic would have behaved on past data.

Please keep this in mind when you look at the equity curve and performance metrics. A beautiful curve with only a handful of trades is still just a small sample.

────────────────────────

6. How to use this strategy (step-by-step)

────────────────────────

1. Add the script to your chart.

2. Open the **Inputs** tab:

- Set the backtest start year.

- Decide whether to use Oscillator-based entry/exit, Stochastic confirmation, and EMA Exit Filter.

- Optionally enable SL, TP, and Risk/Reward exits.

3. Open the **Properties** tab:

- Set a realistic account size if you want.

- Set order size to a realistic % of equity (e.g. 1–2%).

- Confirm that commission and slippage are realistic for your broker.

4. Run the backtest:

- Look at Net Profit, Max Drawdown, number of trades, and equity curve.

- Remember that a low trade count means the statistics are not very strong.

5. Experiment:

- Tweak thresholds (`entryLevel`, `exitLevel`), Stochastic settings, EMA length, and risk params.

- See how the metrics and trade frequency change.

6. Forward-test:

- Before using any idea in live trading, forward-test on a demo account and observe behaviour in real time.

────────────────────────

7. Originality and usefulness (why this is more than a mashup)

────────────────────────

This script is not intended to be a random visual mashup of indicators. It is designed as a coherent, testable strategy with clear roles for each component:

• Range Oscillator:

- Handles mean vs. range-expansion states via an adaptive, ATR-normalized metric.

• Stochastic:

- Acts as a timing filter to avoid entering purely on extremes and instead waits for momentum to turn.

• EMA Exit Filter:

- Trend-slope-based safety net to exit when the medium-term direction changes against the position.

• Risk module:

- Provides practical, rule-based exits: SL, TP, and R-multiple exit, which are useful for structuring risk even if you modify the core logic.

It aims to give traders a ready-made **framework to study and modify**, not a black box or “signals” product.

────────────────────────

8. Limitations and good practices

────────────────────────

• No single strategy works on all markets or in all regimes.

• This script is long-only; it does not short the market.

• Performance can degrade when market structure changes.

• Overfitting (curve fitting) is a real risk if you endlessly tweak parameters to maximise historical profit.

Good practices:

- Test on multiple symbols and timeframes.

- Focus on stability and drawdown, not only on how high the profit line goes.

- View this as a learning tool and a basis for your own research.

────────────────────────

9. Licensing and credits

────────────────────────

• Core oscillator idea & base code:

- “Range Oscillator (Zeiierman)”

- © Zeiierman, licensed under CC BY-NC-SA 4.0.

• Strategy logic, Stochastic confirmation, EMA Exit Filter, and risk-management layer:

- Modifications by jokiniemi.

Please respect both the original license and TradingView House Rules if you fork or republish any part of this script.

────────────────────────

10. No payments / no vendor pitch

────────────────────────

• This script is completely FREE to use on TradingView.

• There is no paid subscription, no external payment link, and no private signals group attached to it.

• If you have questions, please use TradingView’s comment system or private messages instead of expecting financial advice.

Use this script as a tool to learn, experiment, and build your own understanding of markets.

────────────────────────

11. Example backtest settings used in screenshots

────────────────────────

To avoid any confusion about how the results shown in screenshots were produced, here is one concrete example configuration:

• Symbol: BTCUSDT (or similar major BTC pair)

• Timeframe: 1D (Daily)

• Backtest period: from 2018 to the most recent data

• Initial capital: 10 000

• Order size type: Percent of equity

• Order size: 2% per trade

• Commission: 0.1%

• Slippage: 3 ticks

• Risk settings: Stop Loss and Take Profit disabled by default, Risk/Reward exit disabled by default

• Filters: Range Oscillator entry/exit enabled, Stochastic confirmation enabled, EMA Exit Filter enabled

If you change any of these settings (symbol, timeframe, risk per trade, commission, slippage, filters, etc.), your results will look different. Please always adapt the configuration to your own risk tolerance, market, and trading style.

CDC BACKTEST (MACD) FIX AMOUNT $200k per trade This strategy implements an Exponential Moving Average (EMA) Crossover System designed for backtesting and performance evaluation. EMA 12,26 (MACD)

The trading logic is based on the crossover between two EMAs — a short-term EMA (12) and a long-term EMA (26) — which serves as a momentum-based signal for trend identification.

Buy Condition:

A long (buy) position is entered when the 12-period EMA crosses above the 26-period EMA, indicating a potential upward trend or bullish momentum.

Sell Condition:

A position is closed, or a short (sell) position is opened, when the 12-period EMA crosses below the 26-period EMA, signaling a potential downward trend or bearish momentum.

Position Sizing:

Each trade with a fixed position size of 200,000 USD (default), while the starting account balance is set at 400,000 (USD).

Both the fixed trade amount and the initial balance are user-adjustable parameters, allowing flexibility for different risk preferences and portfolio sizes.

Tristan's Tri-band StrategyTristan's Tri-band Strategy - Confluence Trading System

Strategy Overview:

This strategy combines three powerful technical indicators - RSI, Williams %R, and Bollinger Bands - into a single visual trading system. Instead of cluttering your chart with separate indicator panels, all signals are displayed directly on the price chart using color-coded gradient overlays, making it easy to spot high-probability trade setups at a glance.

How It Works:

The strategy identifies trading opportunities when multiple indicators align (confluence), suggesting strong momentum shifts:

📈 Long Entry Signals:

RSI drops to 30 or below (oversold)

Williams %R reaches -80 to -100 range (oversold)

Price touches or breaks below the lower Bollinger Band

All three conditions must align during your selected trading session

📉 Short Entry Signals:

RSI rises to 70 or above (overbought)

Williams %R reaches 0 to -20 range (overbought)

Price touches or breaks above the upper Bollinger Band

All three conditions must align during your selected trading session

Visual Indicators:

(faint) Green gradients below candles = Bullish oversold conditions (buying opportunity)

(faint) Red/Orange gradients above candles = Bearish overbought conditions (selling opportunity)

Stacked/brighter gradients = Multiple indicators confirming the same signal (higher probability) will stack and show brighter / less faint

Blue Bollinger Bands = Volatility boundaries and mean reversion zones

Exit Strategy:

Long trades exit when price reaches the upper Bollinger Band OR RSI becomes overbought (≥70)

Short trades exit when price reaches the lower Bollinger Band OR RSI becomes oversold (≤30)

Key Features:

✅ Session Filters - Trade only during NY (9:30 AM-4 PM), London (3 AM-11:30 AM), or Asia (7 PM-1 AM EST) sessions

✅ No Repainting - Signals are confirmed on candle close for realistic backtesting and live trading

✅ Customizable Parameters - Adjust RSI levels, BB standard deviations, Williams %R periods, and gradient visibility

✅ Visual Clarity - See all three indicators at once without switching between panels

✅ Built-in Alerts - Get notified when entry and exit conditions are met

How to Use Effectively:

Choose Your Trading Session - For day trading US stocks, enable only the NY session. For forex or 24-hour markets, select the sessions that match your schedule.

Look for Gradient Stacking - The brightest, most visible gradients occur when both RSI and Williams %R signal together. These are your highest-probability setups.

Confirm with Price Action - Wait for the candle to close before entering. The strategy enters on the next bar's open to prevent repainting.

Respect the Bollinger Bands - Entries occur at the outer bands (price extremes), and exits occur at the opposite band or when momentum reverses.

Backtest First - Test the strategy on your preferred instruments and timeframes. Works best on liquid assets with clear trends and mean reversion patterns (stocks, major forex pairs, indices).

Adjust Gradient Visibility - Use the "Gradient Strength" slider (lower = more visible) to make signals stand out on your chart style.

Best Timeframes: 5-minute to 1-hour charts for intraday trading; 4-hour to daily for swing trading (I have also found the 3 hour timeframe to work really well for some stocks / ETFs.)

Best Markets: Liquid instruments with volatility - SPY, QQQ, major stocks, EUR/USD, GBP/USD, major indices

Risk Management: This is a mean reversion strategy that works best in ranging or choppy markets. In strong trends, signals may appear less frequently. Always use proper position sizing and stop losses based on your risk tolerance.

----------------------------------------------

Note: Past performance does not guarantee future results. This strategy is provided for educational purposes. Always backtest thoroughly and practice proper risk management before live trading.RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5

v2.0—Tristan's Multi-Indicator Reversal Strategy🎯 Multi-Indicator Reversal Strategy - Optimized for High Win Rates

A powerful confluence-based strategy that combines RSI, MACD, Williams %R, Bollinger Bands, and Volume analysis to identify high-probability reversal points . Designed to let winners run with no stop loss or take profit - positions close only when opposite signals occur.

Also, the 3 hour timeframe works VERY well—just a lot less trades.

📈 Proven Performance

This strategy has been backtested and optimized on multiple blue-chip stocks with 80-90%+ win rates on 1-hour timeframes from Aug 2025 through Oct 2025:

✅ V (Visa) - Payment processor

✅ MSFT (Microsoft) - Large-cap tech

✅ WMT (Walmart) - Retail leader

✅ IWM (Russell 2000 ETF) - Small-cap index

✅ NOW (ServiceNow) - Enterprise software

✅ WM (Waste Management) - Industrial services

These stocks tend to mean-revert at extremes, making them ideal candidates for this reversal-based approach. I only list these as a way to show you the performance of the script. These values and stock choices may change over time as the market shifts. Keep testing!

🔑 How to Use This Strategy Successfully

Step 1: Apply to Chart

Open your desired stock (V, MSFT, WMT, IWM, NOW, WM recommended)

Set timeframe to 1 Hour

Apply this strategy

Check that the Williams %R is set to -20 and -80, and "Flip All Signals" is OFF (can flip this for some stocks to perform better.)

Step 2: Understand the Signals

🟢 Green Triangle (BUY) Below Candle:

Multiple indicators (RSI, Williams %R, MACD, Bollinger Bands) show oversold conditions

Enter LONG position

Strategy will pyramid up to 10 entries if more buy signals occur

Hold until red triangle appears

🔴 Red Triangle (SELL) Above Candle:

Multiple indicators show overbought conditions

Enter SHORT position (or close existing long)

Strategy will pyramid up to 10 entries if more sell signals occur

Hold until green triangle appears

🟣 Purple Labels (EXIT):

Shows when positions close

Displays count if multiple entries were pyramided (e.g., "Exit Long x5")

Step 3: Let the Strategy Work

Key Success Principles:

✅ Be Patient - Signals don't occur every day, wait for quality setups

✅ Trust the Process - Don't manually close positions, let opposite signals exit

✅ Watch Pyramiding - The strategy can add up to 10 positions in the same direction

✅ No Stop Loss - Positions ride through drawdowns until reversal confirmed

✅ Session Filter - Only trades during NY session (9:30 AM - 4:00 PM ET)

⚙️ Winning Settings (Already Set as Defaults)

INDICATOR SETTINGS:

- RSI Length: 14

- RSI Overbought: 70

- RSI Oversold: 30

- MACD: 12, 26, 9 (standard)

- Williams %R Length: 14

- Williams %R Overbought: -20 ⭐ (check this! And adjust to your liking)

- Williams %R Oversold: -80 ⭐ (check this! And adjust to your liking)

- Bollinger Bands: 20, 2.0

- Volume MA: 20 periods

- Volume Multiplier: 1.5x

SIGNAL REQUIREMENTS:

- Min Indicators Aligned: 2

- Require Divergence: OFF

- Require Volume Spike: OFF

- Require Reversal Candle: OFF

- Flip All Signals: OFF ⭐

RISK MANAGEMENT:

- Use Stop Loss: OFF ⭐⭐⭐

- Use Take Profit: OFF ⭐⭐⭐

- Allow Pyramiding: ON ⭐⭐⭐

- Max Pyramid Entries: 10 ⭐⭐⭐

SESSION FILTER:

- Trade Only NY Session: ON

- NY Session: 9:30 AM - 4:00 PM ET

**⭐ = Critical settings for success**

## 🎓 Strategy Logic Explained

### **How It Works:**

1. **Multi-Indicator Confluence**: Waits for at least 2 out of 4 technical indicators to align before generating signals

2. **Oversold = Buy**: When RSI < 30, Williams %R < -80, price below lower Bollinger Band, and/or MACD turning bullish → BUY signal

3. **Overbought = Sell**: When RSI > 70, Williams %R > -20, price above upper Bollinger Band, and/or MACD turning bearish → SELL signal

4. **Pyramiding Power**: As trend continues and more signals fire in the same direction, adds up to 10 positions to maximize gains

5. **Exit Only on Reversal**: No arbitrary stops or targets - only exits when opposite signal confirms trend change

6. **Session Filter**: Only trades during liquid NY session hours to avoid overnight gaps and low-volume periods

### **Why No Stop Loss Works:**

Traditional reversal strategies fail because they:

- Get stopped out too early during normal volatility

- Miss the actual reversal that happens later

- Cut winners short with tight take profits

This strategy succeeds because it:

- ✅ Rides through temporary noise

- ✅ Captures full reversal moves

- ✅ Uses multiple indicators for confirmation

- ✅ Pyramids into winning positions

- ✅ Only exits when technical picture completely reverses

---

## 📊 Understanding the Display

**Live Indicator Counter (Top Corner / end of current candles):**

Bull: 2/4

Bear: 0/4

(STANDARD)

Shows how many indicators currently align bullish/bearish

"STANDARD" = normal reversal mode (buy oversold, sell overbought)

"FLIPPED" = momentum mode if you toggle that setting

Visual Indicators:

🔵 Blue background = NY session active (trading window)

🟡 Yellow candle tint = Volume spike detected

💎 Aqua diamond = Bullish divergence (price vs RSI)

💎 Fuchsia diamond = Bearish divergence

⚡ Advanced Tips

Optimizing for Different Stocks:

If Win Rate is Low (<50%):

Try toggling "Flip All Signals" to ON (switches to momentum mode)

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Test on different timeframe (4-hour or daily)

If Too Few Signals:

Decrease "Min Indicators Aligned" to 2

Turn OFF all requirement filters

Widen Williams %R bands to -15 and -85

If Too Many False Signals:

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Reduce Max Pyramid Entries to 5

Stock Selection Guidelines:

Best Suited For:

Large-cap stable stocks (V, MSFT, WMT)

ETFs (IWM, SPY, QQQ)

Stocks with clear support/resistance

Mean-reverting instruments

Avoid:

Ultra low-volume penny stocks

Extremely volatile crypto (try traditional settings first)

Stocks in strong one-directional trends lasting months

🔄 The "Flip All Signals" Feature

If backtesting shows poor results on a particular stock, try toggling "Flip All Signals" to ON:

STANDARD Mode (OFF):

Buy when oversold (reversal strategy)

Sell when overbought

May work best for: V, MSFT, WMT, IWM, NOW, WM

FLIPPED Mode (ON):

Buy when overbought (momentum strategy)

Sell when oversold

May work best for: Strong trending stocks, momentum plays, crypto

Test both modes on your stock to see which performs better!

📱 Alert Setup

Create alerts to notify you of signals:

📊 Performance Expectations

With optimized settings on recommended stocks:

Typical results we are looking for:

Win Rate: 70-90%

Average Winner: 3-5%

Average Loser: 1-3%

Signals Per Week: 1-3 on 1-hour timeframe

Hold Time: Several hours to days

Remember: Past performance doesn't guarantee future results. Always use proper risk management.

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

USDJPY Fair Value Gap + Session Strategy🎯 Overview

This strategy combines Fair Value Gaps (FVGs) with session-based order flow analysis, specifically optimized for USDJPY. It identifies price inefficiencies left behind by institutional order flow during high-volatility trading sessions, offering a modern alternative to traditional lagging indicators.

🔬 What Are Fair Value Gaps?

Fair Value Gaps represent areas where aggressive institutional buying or selling created "gaps" in the market structure:

Bullish FVG: Price moves up so aggressively that it leaves unfilled buy orders behind

Bearish FVG: Price moves down so quickly that it leaves unfilled sell orders behind

Research shows approximately 80% of FVGs get "filled" (price returns to the gap) within 20-60 bars, making them highly predictable trading zones.

(see the generated image above)

(see the generated image above)

FVG Detection Logic:

text

// Bullish FVG: Gap between high and current low

bullishFVG = low > high and high > high

// Bearish FVG: Gap between low and current high

bearishFVG = high < low and low < low

🌏 Session-Based Trading

Why Sessions Matter for USDJPY

(see the generated image above)

Tokyo Session (00:00-09:00 UTC)

Highest volatility during first hour (00:00-01:00 UTC)

Average movement: 51-60 pips

Best for breakout strategies

London/NY Overlap (13:00-16:00 UTC)

Maximum liquidity and institutional participation

Tightest spreads and most reliable FVG formations

Optimal for continuation trades

Monday Premium Effect

USDJPY moves 120+ pips on Mondays due to weekend positioning

Enhanced FVG formation during session opens

📊 Strategy Components

(see the generated image above)

1. Fair Value Gap Detection

Identifies bullish and bearish FVGs automatically

Age limit: FVGs expire after 20 bars to avoid stale setups

Size filter: Minimum gap size to filter out noise

2. Session Filtering

Tokyo Open focus: Trades during first hour of Asian session

London/NY Overlap: Captures high-liquidity institutional flows

Weekend gap strategy: Enhanced signals on Monday opens

3. Volume Confirmation

Requires 1.5x average volume spike

Confirms institutional participation

Reduces false signals

4. Trend Alignment

50 EMA filter ensures trades align with higher timeframe trend

Long trades above EMA, short trades below

Prevents costly counter-trend trades

5. Risk Management

2:1 Risk/Reward minimum ensures profitability with 40%+ win rate

Percentage-based stops adapt to USDJPY volatility (0.3% default)

Configurable position sizing

🎯 Entry Conditions

(see the generated image above)

Long Entry (BUY)

✅ Bullish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price above 50 EMA (trend confirmation)

✅ Bullish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

Short Entry (SELL)

✅ Bearish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price below 50 EMA (trend confirmation)

✅ Bearish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

📈 Expected Performance

Backtesting Results (Based on Similar Strategies):

Win Rate: 44-59% (profitable due to high R:R ratio)

Average Winner: 60-90 pips during London/NY sessions

Average Loser: 30-40 pips (tight stops at FVG boundaries)

Risk/Reward: 2:1 minimum, often 3:1 during strong trends

Best Performance: Monday Tokyo opens and Wednesday London/NY overlaps

Why This Works for USDJPY:

90% correlation with US-Japan bond yield spreads

High volatility provides sufficient pip movement

Heavy institutional/central bank participation creates clear FVGs

Consistent volatility patterns across trading sessions

⚙️ Configurable Parameters

Session Settings:

Trade Tokyo Session (Enable/Disable)

Trade London/NY Overlap (Enable/Disable)

FVG Settings:

FVG Minimum Size (Filter small gaps)

Maximum FVG Age (20 bars default)

Show FVG Markers (Visual display)

Volume Settings:

Use Volume Filter (Enable/Disable)

Volume Multiplier (1.5x default)

Volume Average Period (20 bars)

Trend Settings:

Use Trend Filter (Enable/Disable)

Trend EMA Period (50 default)

Risk Management:

Risk/Reward Ratio (2.0 default)

Stop Loss Percentage (0.3% default)

🎨 Visual Indicators

🟡 Yellow Line: 50 EMA trend filter

🟢 Green Triangles: Long entry signals

🔴 Red Triangles: Short entry signals

🟢 Green Dots: Bullish FVG zones

🔴 Red Dots: Bearish FVG zones

🟦 Blue Background: Tokyo open session

🟧 Orange Background: London/NY overlap

📊 Recommended Settings

Optimal Timeframes:

Primary: 5-minute charts (scalping)

Secondary: 15-minute charts (swing trading)

Parameter Optimization:

Conservative: Stop Loss 0.2%, R:R 2:1, Volume 2.0x

Balanced: Stop Loss 0.3%, R:R 2:1, Volume 1.5x (default)

Aggressive: Stop Loss 0.4%, R:R 1.5:1, Volume 1.2x

Risk Management:

Maximum 1-2% of account per trade

Daily loss limit: Stop after 3-5 consecutive losses

Use fixed percentage position sizing

⚠️ Important Considerations

Avoid Trading During:

Major news events (BOJ interventions, NFP, FOMC)

Holiday periods with reduced liquidity

Low volatility Asian afternoon sessions

When US-Japan yield differential narrows sharply

Best Practices:

Limit to 2-3 trades per session maximum

Always respect the 50 EMA trend filter

Never risk more than planned per trade

Paper trade for 2-4 weeks before live implementation

Track performance by session and day of week

🚀 How to Use

Add the script to your USDJPY chart

Set timeframe to 5-minute or 15-minute

Adjust parameters based on your risk tolerance

Enable strategy alerts for automated notifications

Wait for visual signals (triangles) to appear

Enter trades according to your risk management rules

📚 Strategy Foundation

This strategy is based on:

Smart Money Concepts (SMC): Institutional order flow tracking

Market Microstructure: Understanding how FVGs form in electronic trading

Quantified Risk Management: Statistical edge through proper R:R ratios

Session Liquidity Patterns: Exploiting predictable volatility cycles

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

Bitcoin Halving Strategy

A systematic, data-driven trading strategy based on Bitcoin's 4-year halving cycles. This strategy capitalizes on historical price patterns that emerge around halving events, providing clear entry and exit signals for both accumulation and profit-taking phases.

🎯 Strategy Overview

This automated trading system identifies optimal buy and sell zones based on the predictable Bitcoin halving cycle that occurs approximately every 4 years. By analyzing historical data from all previous halvings (2012, 2016, 2020, 2024), the strategy pinpoints high-probability trading opportunities.

📊 Key Features

Automated Signal Generation: Buy signals at halving events and DCA zones, sell signals at profit-taking peaks

Multi-Phase Analysis: Tracks Accumulation, Profit Taking, Bear Market, and DCA phases

Visual Dashboard: Real-time performance metrics, phase countdown, and position tracking

Backtesting Enabled: Comprehensive historical performance analysis with configurable parameters

Risk Management: Built-in position sizing, slippage control, and optional short trading

⚙️ Strategy Logic

Buy Signals:

At halving event (Week 0)

DCA zone entry (Week 135 post-halving)

Sell Signals:

Profit-taking zone (Week 80 post-halving)

Optional short position entry for advanced traders

📈 Performance Highlights

Captures major bull run profits while avoiding prolonged bear markets

Clear visual indicators for all phases and transitions

Customizable timing parameters for personalized risk tolerance

Professional dashboard with live P&L, win rate, and drawdown metrics

🛠️ Customization Options

Adjustable phase timing (profit start/end, DCA timing)

Position sizing control

Enable/disable short trading

Visual customization (colors, labels, zones)

Table positioning and transparency

⚠️ Risk Disclosure

Past performance does not guarantee future results. This strategy is based on historical halving cycle patterns and should be used as part of a comprehensive trading plan. Always conduct your own research and consider your risk tolerance before trading.

💡 Ideal For

Long-term Bitcoin investors seeking systematic entry/exit points

Swing traders capitalizing on multi-month trends

Portfolio managers implementing cycle-based allocation strategies

Twisted Forex's Doji + Area StrategyTitle

Twisted Forex’s Doji + Area Strategy

Description

What this strategy does

This strategy looks for doji candles forming inside or near supply/demand areas . Areas are built from swing pivots and sized with ATR, then tracked for retests (“confirmations”). When a doji prints close to an area and quality checks pass, the strategy places a trade with the stop beyond the doji and a configurable R:R target.

How areas (zones) are built

• Swings are detected with a user-set pivot length.

• Each swing spawns a horizontal area centered at the pivot price with half-height = zoneHalfATR × ATR .

• Duplicates are de-duplicated by center distance (ATR-scaled).

• Areas fade when broken beyond a buffer or after an optional age (expiry).

• Retests are recorded when price touches and then bounces away from the area; repeated reactions increase the zone’s “strength”.

Signal logic (summary)

Doji detection: strict or loose body criteria with optional minimum wick fractions and ATR-scaled minimum range.

Proximity: price must be inside/near a supply or demand area (proxATR × ATR).

Side resolution: overlap is resolved by (a) which side price penetrates more, (b) fast/slow EMA trend, or (c) nearest distance. Optional “previous candle flip” can bias long after a bearish candle and short after a bullish one.

Optional 1-bar confirmation: the bar after the doji must close away from the area by confirmATR × ATR .

Quality filter (Off/Soft/Strict): four checks—(i) wick rejection past the edge, (ii) doji closes in an edge “band” of the area, (iii) fresh touch (cooldown), (iv) approach impulse over a short lookback. In Strict , thresholds auto-tighten.

Orders & exits

• Long: stop below doji low minus buffer; Short: above doji high plus buffer.

• Target = rrMultiple × risk distance .

• Pyramiding is off by default.

Position sizing

You can size from the script or from Strategy Properties:

• Script-driven (default): set Position sizing = “Risk % of equity” and choose riskPercent (e.g., 1.0%). The script applies safe floors/rounding (FX micro-lots by default) so quantity never rounds to zero.

• Properties-driven : toggle Use TV Properties → Order size ON, then pick “Percent of equity” in Properties (e.g., 1%). The header includes safe defaults so trades still place.

Key inputs to explore

• Zone building : pivotLen, zoneHalfATR, minDepartureATR, expiryBars, breakATR, leftBars, dedupeATR.

• Doji & proximity : strictDoji, dojiBodyFrac, minWickFrac, minRangeATR, proxATR, minBarsBetween.

• Overlap resolution : usePenetration, useTrend (EMA 21/55), “previous candle flip”, needNextBarConf & confirmATR.

• Quality : qualityMode (Off/Soft/Strict), minQualPass/kStrict, wickPenATR, edgeBandFrac, approachLookback, approachMinATR, freshTouchBars.

• Zone strength gating : minStrengthSoft / minStrengthStrict.

• HTF confluence (optional) : useHTFTrend (HTF EMA 34/89) and/or useHTFZoneProx (HTF swing bands).

Tips to make it cleaner / higher quality

• Turn needNextBarConf ON and use confirmATR = 0.10–0.15 .

• Increase approachMinATR (e.g., 0.35–0.45) to require a stronger pre-touch impulse.

• Raise minStrengthSoft/Strict (e.g., 4–6) so only well-reacted zones can signal.

• Use signalsOnlyConfirmed ON if you prefer trades only from zones with retests (the script falls back gracefully when none exist yet).

• Nudge proxATR to 0.5–0.6 to demand tighter proximity to the level.

• Optional: enable useHTFTrend to filter counter-trend setups.

Default settings used in this publication

• Initial capital: 100,000 (illustrative).

• Slippage: 1 tick; Commission: 0% (you can raise commission if you prefer—spread is partly modeled by slippage).

• Sizing: Risk % of equity via inputs; riskPercent = 1.0% ; FX uses micro-lot floors by default.

• Quality: Off by default (Soft/Strict available).

• HTF trend gate: Off by default.

Backtesting notes

For a meaningful sample size, test on liquid symbols/timeframes that yield 100+ trades (e.g., majors on 5–15m over 1–2 years). Backtests are modelled and broker costs/spread vary—validate on your feed and forward-test.

How to read the chart

Shaded bands are supply (above) and demand (below). Brighter bands are the nearest K per side (visual aid). BUY/SELL labels mark entries; colored dots show entry/SL/TP levels. You can hide zones or unconfirmed zones for a cleaner view.

Disclaimer

This is educational material, not financial advice. Trading involves risk. Always test and size responsibly.

BTC 5-MA Multi Cross Strategy By Hardik Prajapati Ai TradelabThis strategy is built around the five most powerful and commonly used moving averages in crypto trading — 5, 20, 50, 100, and 200-period SMAs (Simple Moving Averages) — applied on a 1-hour Bitcoin chart.

Core Idea:

The strategy aims to identify strong bullish trends by confirming when the price action crosses above all key moving averages. This alignment of multiple MAs indicates momentum shift and helps filter out false breakouts.

⸻

⚙️ How It Works:

1. Calculates 5 Moving Averages:

• 5 MA → Short-term momentum (fastest signal)

• 20 MA → Near-term trend confirmation

• 50 MA → Mid-term trend filter

• 100 MA → Long-term trend foundation

• 200 MA → Macro-trend direction (strongest support/resistance)

2. Buy Condition (Entry):

• A Buy is triggered when:

• The price crosses above the 5 MA, and

• The closing price remains above all other MAs (20, 50, 100, 200)

This signals that momentum is aligned across all time horizons — a strong uptrend confirmation.

3. Sell Condition (Exit):

• The position is closed when price crosses below the 20 MA, showing weakness in short-term momentum.

4. Visual Signals:

• 🟢 BUY triangle below candles → Entry signal

• 🔴 SELL triangle above candles → Exit signal

• Colored MAs plotted for trend clarity.

⸻

📈 Recommended Usage:

• Chart: BTC/USDT

• Timeframe: 1 Hour

• Type: Trend-following crossover strategy

• Ideal for: Identifying major breakout moves and confirming trend reversals.

⸻

⚠️ Notes:

• This script is meant for educational and backtesting purposes only.

• Always apply additional confirmation tools (like RSI, Volume, or VIX-style filters) before live trading.

• Works best during trending markets; may produce whipsaws in sideways zones.

PG DMean & Price Sync ver 9.4 - ConsolidatedPG DMean & Price Sync Strategy (SD Filter)

This strategy combines the momentum-oscillator properties of the Detrended Mean (DMean) with a Standard Deviation (SD) Price Filter for confirming trend direction, aiming to isolate high-conviction trades while actively managing risk.

🔑 Core Logic

DMean Momentum Signal: The strategy's primary engine is the DMean, which measures the percentage difference between the current closing price and a longer-term Moving Average (price_ma). It is then smoothed by a DMean Signal line (MA of the DMean).

Entry Signal: A trade is triggered when the DMean line crosses above (for Long) or below (for Short) its Signal Line, but it must clear a user-defined Dead Zone Threshold to confirm momentum commitment.

SD Filter Confirmation (Price Sync): A Standard Deviation Channel, based on a separate user-defined price source and period, is used to filter trades.

Long Filter: Allows Long entries only when the price is trading above the lower SD band, suggesting the current price action is stronger than the recent average volatility to the downside.

Short Filter: Allows Short entries only when the price is currently below the Filter Basis (SMA), confirming a bearish stance within the SD channel.

🛡️ Risk & Exit Management

Primary Exit: All trades are exited by reverse DMean Crossover/Crossunder, meaning the position is closed when the DMean momentum reverses against the open trade (e.g., DMean crosses under the Signal to exit a Long).

Hard Stop Loss (Short Trades): A mandatory percentage-based Hard Stop Loss is implemented only for short positions to protect against sudden upward price spikes, closing the trade if the loss exceeds the set percentage. (Note: This version does not include a Hard SL for Long trades).

📊 Performance Dashboard

A custom Performance Dashboard Table is displayed at the bottom right of the chart to provide real-time, at-a-glance comparison of the strategy's equity performance versus a simple Buy & Hold over the selected backtesting date range.

AVGO Advanced Day Trading Strategy📈 Overview

The AVGO Advanced Day Trading Strategy is a comprehensive, multi-timeframe trading system designed for active day traders seeking consistent performance with robust risk management. Originally optimized for AVGO (Broadcom), this strategy adapts well to other liquid stocks and can be customized for various trading styles.

🎯 Key Features

Multiple Entry Methods

EMA Crossover: Classic trend-following signals using fast (9) and medium (16) EMAs

MACD + RSI Confluence: Momentum-based entries combining MACD crossovers with RSI positioning

Price Momentum: Consecutive price action patterns with EMA and RSI confirmation

Hybrid System: Advanced multi-trigger approach combining all methodologies

Advanced Technical Arsenal

When enabled, the strategy analyzes 8+ additional indicators for confluence:

Volume Price Trend (VPT): Measures volume-weighted price momentum

On-Balance Volume (OBV): Tracks cumulative volume flow

Accumulation/Distribution Line: Identifies institutional money flow

Williams %R: Momentum oscillator for entry timing

Rate of Change Suite: Multi-timeframe momentum analysis (5, 14, 18 periods)

Commodity Channel Index (CCI): Cyclical turning points

Average Directional Index (ADX): Trend strength measurement

Parabolic SAR: Dynamic support/resistance levels

🛡️ Risk Management System

Position Sizing

Risk-based position sizing (default 1% per trade)

Maximum position limits (default 25% of equity)

Daily loss limits with automatic position closure

Multiple Profit Targets

Target 1: 1.5% gain (50% position exit)

Target 2: 2.5% gain (30% position exit)

Target 3: 3.6% gain (20% position exit)

Configurable exit percentages and target levels

Stop Loss Protection

ATR-based or percentage-based stop losses

Optional trailing stops

Dynamic stop adjustment based on market volatility

📊 Technical Specifications

Primary Indicators

EMAs: 9 (Fast), 16 (Medium), 50 (Long)

VWAP: Volume-weighted average price filter

RSI: 6-period momentum oscillator

MACD: 8/13/5 configuration for faster signals

Volume Confirmation

Volume filter requiring 1.6x average volume

19-period volume moving average baseline

Optional volume confirmation bypass

Market Structure Analysis

Bollinger Bands (20-period, 2.0 multiplier)

Squeeze detection for breakout opportunities

Fractal and pivot point analysis

⏰ Trading Hours & Filters

Time Management

Configurable trading hours (default: 9:30 AM - 3:30 PM EST)

Weekend and holiday filtering

Session-based trade management

Market Condition Filters

Trend alignment requirements

VWAP positioning filters

Volatility-based entry conditions

📱 Visual Features

Information Dashboard

Real-time display of:

Current entry method and signals

Bullish/bearish signal counts

RSI and MACD status

Trend direction and strength

Position status and P&L

Volume and time filter status

Chart Visualization

EMA plots with customizable colors

Entry signal markers

Target and stop level lines

Background color coding for trends

Optional Bollinger Bands and SAR display

🔔 Alert System

Entry Alerts

Customizable alerts for long and short entries

Method-specific alert messages

Signal confluence notifications

Advanced Alerts

Strong confluence threshold alerts