VWAP Kalman FilterOverview

This indicator applies Kalman filtering techniques to Volume Weighted Average Price (VWAP) calculations, providing a statistically optimized approach to VWAP analysis. The Kalman filter reduces noise while maintaining responsiveness to genuine price movements, addressing common VWAP limitations in volatile or low-volume conditions.

Technical Implementation

Kalman Filter Mathematics

The indicator implements a state-space model for VWAP estimation:

- Prediction Step: x̂(k|k-1) = x̂(k-1|k-1) + v(k-1)

- Update Step: x̂(k|k) = x̂(k|k-1) + K(k)

- Kalman Gain: K(k) = P(k|k-1) / (P(k|k-1) + R)

Where:

- x̂ = estimated VWAP state

- K = Kalman gain (adaptive weighting factor)

- P = error covariance

- R = measurement noise

- Q = process noise

- v = optional velocity component

Core Components

Dual VWAP System

- Standard VWAP: Traditional volume-weighted calculation

- Kalman-filtered VWAP: Noise-reduced estimation with optional velocity tracking

- Real-time divergence measurement between filtered and unfiltered values

Adaptive Filtering

- Process Noise (Q): Controls adaptation to price changes (0.001-1.0)

- Measurement Noise (R): Determines smoothing intensity (0.01-5.0)

- Optional velocity tracking for momentum-based filtering

Multi-Timeframe Anchoring

- Session, Weekly, Monthly, Quarterly, and Yearly anchor periods

- Automatic Kalman state reset on anchor changes

- Maintains VWAP integrity across timeframes

Features

Visual Components

- Dual VWAP Lines: Compare filtered vs. unfiltered in real-time

- Dynamic Bands: Three-level deviation bands (1σ, 2σ, 3σ)

- Trend Coloring: Automatic color adaptation based on price position

- Cloud Visualization: Highlights divergence between standard and Kalman VWAP

- Signal Markers: Crossover and band-touch indicators

Trading Signals

- VWAP crossover detection with Kalman filtering

- Band touch alerts at multiple standard deviation levels

- Velocity-based momentum confirmation (optional)

- Divergence warnings when filtered/unfiltered values separate

Information Display

- Real-time VWAP values (both standard and filtered)

- Trend direction indicator

- Velocity/momentum reading (when enabled)

- Divergence percentage calculation

- Anchor period display

Input Parameters

VWAP Settings

- Anchor Period: Choose calculation reset period

- Band Multipliers: Customize deviation band distances

- Display Options: Toggle standard VWAP and bands

Kalman Parameters

- Length: Base period for calculations (5-200)

- Process Noise (Q: Higher values increase responsiveness

- Measurement Noise (R): Higher values increase smoothing

- Velocity Tracking: Enable momentum-based filtering

Visual Controls

- Toggle filtered/unfiltered VWAP display

- Band visibility options

- Signal markers on/off

- Cloud fill between VWAPs

- Bar coloring by trend

Use Cases

Noise Reduction

Particularly effective during:

- Low volume periods (pre-market, lunch hours)

- Volatile market conditions

- Fast-moving markets where standard VWAP whipsaws

Trend Identification

- Cleaner trend signals with reduced false crosses

- Earlier trend detection through velocity component

- Confirmation through divergence analysis

Support/Resistance

- Filtered VWAP provides more stable S/R levels

- Bands adapt to filtered values for better zone identification

- Reduced false breakout signals

Technical Advantages

1. Optimal Estimation: Mathematically optimal under Gaussian noise assumptions

2. Adaptive Response: Self-adjusting to market conditions

3. Predictive Element: Velocity component provides forward-looking insight

4. Noise Immunity: Superior noise rejection vs. simple moving average smoothing

Limitations

- Assumes linear price dynamics

- Requires parameter optimization for different instruments

- May lag during sudden volatility regime changes

- Not suitable as standalone trading system

Mathematical Background

Based on control systems theory, the Kalman filter provides recursive Bayesian estimation originally developed for aerospace applications. This implementation adapts the algorithm specifically for financial time series, maintaining VWAP's volume-weighted properties while adding statistical filtering.

Comparison with Standard VWAP

Standard VWAP Issues Addressed:

- Choppy behavior in low volume

- Whipsaws around VWAP line

- Lag in trend identification

- Noise in deviation bands

Kalman VWAP Benefits:

- Smooth yet responsive line

- Fewer false signals

- Optional momentum tracking

- Statistically optimized filtering

Alert Conditions

The indicator includes several pre-configured alert conditions:

- Bullish/Bearish VWAP crosses

- Upper/Lower band touches

- High divergence warnings

- Velocity shifts (if enabled)

---

This open-source indicator is provided as-is for educational and trading purposes. No guarantees are made regarding trading performance. Users should conduct their own testing and validation before using in live trading.

Statistics

Dynamic S/R Levels - MTF (1-Week, Strong/Spaced)dynamic support and resistance levels based on timeframe

Info de Vela 1m1-Minute Candle Info Dashboard (Real-Time)

Overview

This is a lightweight, real-time dashboard designed specifically for 1-minute (1m) scalping. It provides critical, non-lagging data about the current 1-minute candle, helping you make split-second decisions on stop-loss placement and risk assessment.The table updates on every tick without flickering or repainting.

Key Features (Real-Time Table)

The dashboard displays three key metrics about the current 1m candle:Time Remaining: A simple countdown timer showing the exact seconds remaining until the current candle closes (e.g., "00:34").Dist. to Extreme (Ticks): This is the core function for scalping. It calculates the distance (in ticks) from the current price to the furthest extreme of the candle (i.e., max(high - close, close - low)). This is ideal for traders who base their stop-loss on the current candle's range.Total Candle Range (Ticks): Displays the full high-to-low range of the current candle in ticks, giving you an instant read on volatility.

How to Use

This tool is designed to solve one problem: speed.Instead of manually measuring the distance for your stop-loss on every candle, you can instantly read the exact tick value from the table. This allows you to calculate your position size (lotage) much faster, which is essential in a fast-moving 1m environment.

REQUIREMENT:This indicator is designed to work ONLY on the 1-minute (1m) timeframe. It will display an error and show no data on any other chart.

[AA] - Market Valuation (Mean Based) - Market Valuation (Mean Based)

What it does

This indicator estimates whether price is overvalued, undervalued, or fairly valued relative to its structural mean across multiple lookback windows. It builds a single normalized oscillator from short-, mid-, and long-term ranges so traders can quickly see when price is stretched away from equilibrium.

This is not a mashup of existing tools. It’s a custom mean-deviation model that aggregates multi-window range positioning into one score.

How it works (concepts)

For each lookback length (13, 25, 30, 50, 100, 200):

Range & midpoint:

Highest high H and lowest low L.

Structural midpoint Mid = (H + L)/2.

Normalized deviation:

Dev = (Close − Mid) / (H − L) → location of price within its own range.

Aggregation:

The oscillator z_struct is the average of the deviations from the five windows.

Result: a smoothed, dimensionless value (roughly −1 to +1 in typical markets) showing multi-horizon displacement from the mean.

Plots & levels

Oscillator (area): z_struct

Reference lines: +0.40 (OB), 0.00 (equilibrium), −0.30 (OS)

Coloring:

Red when z_struct > OB (extended above mean)

Blue when z_struct < OS (extended below mean)

White in between

Suggested use

Mean reversion context: Fade extremes in range-bound conditions; take profits into OB/OS.

Trend awareness: In strong trends, extremes can persist—use levels as exhaustion context rather than standalone entry.

Filter/confirm: Combine with your trend filter or structure tools to time pullbacks and avoid chasing extended moves.

Inputs

Lookbacks: 13, 25, 30, 50, 100, 200

Thresholds: OB = 0.40, OS = −0.30

Notes & limitations

Works on the current symbol/timeframe only; no security() calls and no repainting beyond normal bar completion.

In very tight or flat ranges (H ≈ L), normalized deviations can become sensitive; consider longer windows or higher timeframes.

This is an indicator, not a strategy. No signals are generated; use with risk management.

Originality statement

This script implements an original, multi-window mean-deviation aggregation. It does not replicate a built-in or a public indicator; its purpose is to quantify cross-horizon valuation in a single, normalized measure.

Dashboard — Vol & PriceDashboard for traders

Indicator Description

1. Prev Day High

What it shows: the previous trading day's high.

Why it shows: a resistance level. Many traders watch to see if the price will hold above or below this level. A breakout can signal buying strength.

2. Prev Day Low

What it shows: the previous day's low.

Why it shows: a support level. If the price breaks downwards, it signals weakness and a possible continuation of the decline.

3. Today

What it shows:

The difference between the current price and yesterday's close (in absolute values and as a percentage).

Color: green for an increase, red for a decrease.

Why it shows: immediately shows how strong a gap or movement is today relative to yesterday. This is an indicator of current momentum.

4. ADR, % (Average Daily Range)

What it shows: Average daily range (High – Low), expressed as a percentage of the closing price, for the selected period (default 7 days).

Why it's useful: To understand the "normal" volatility of an instrument. For example, if the ADR is 3%, then a 1% move is small, while a 6% move is very large.

5. ATR (Average True Range)

What it shows: Average fluctuation range (including gaps), in absolute points, for the specified period (default 7 days).

Why it's useful: A classic volatility indicator. Useful for setting stops, calculating position sizes, and identifying "noise" movements.

6. ATR (Today), %

What it shows: How much the current movement today (from yesterday's close to the current price) represents in % of the average ATR.

Why it shows: Shows whether the instrument has "played out" its average range. If the value is already >100%, there is a high probability that the movement will begin to slow.

7. Vol (Today)

What it shows:

Current trading volume for the day (in millions/billions).

Comparison with yesterday as a percentage (for example: 77.32M (-52.78%)).

Color: green if the volume is higher than yesterday; red if lower.

Why it shows:Quickly shows whether the market is active today. Volume = fuel for price movement.

8. Avg Vol (20d)

What it shows: Average daily volume over the last 20 trading days.

Why it's useful:"normal" activity level. It's a convenient backdrop for assessing today's turnover.

9. Rel. Vol (Today), % (Relative Volume)

What it shows: Deviation of the current volume from the average (20 days).

Formula: `(today / average - 1)` * 100`.

+30% = volume 30% above average, -40% = 40% below average.

Color: green for +, red for –.

Why it's useful:A key indicator for a trader. If RelVol > 100% (green), the market is "charged," and the movement is more significant. If low, activity is weak and movements are less reliable.

10. Normalized RS (Relative Strength)

What it shows: the relative strength of a stock to a selected benchmark (e.g., SPY), normalized by the period (default 7 days).

100 = same result as the market.

> 100 = the stock is stronger than the index.

<100 = weaker than the index.

Why it's needed: filtering ideas. Strong stocks rise faster when the market rises, weak stocks fall more sharply. This helps trade in the direction of the trend and select the best candidates.

In summary:

Prev High / Low — key support and resistance levels.

Today — an instant understanding of the current momentum.

ADR and ATR — volatility and potential movement.

ATR (Today) — how much the instrument has already "run."

Vol + Rel.Vol — activity and confirmation of the movement's strength.

RS — selecting strong/weak leaders against the market.

Price Action Bar Counter for Crypto Traders标注美股开收盘时间的K线辅助指标,自动调整夏令时与冬令时,适用于5m、15m、30m与1h级别。

Highlights U.S. stock market open and close times with automatic DST adjustment.

Best used on 5m, 15m, 30m, and 1h charts.

Trading ScorecardChecklist, note, scorecard, custom table. I originally created the table for currency strength analysis, but it can be used as a checklist. You can also create your own scoring system. The number of columns and rows can be changed. The color and size of the table are customizable.

Index Weighted Returns [SS]This is the index weighted return indicator.

It supports a few ETFs, including:

SPY/SPX

QQQ/NDX

ARKK

SMH

UFO

XBI

QTUM

What it does is it takes the top, approximately 40, of the most heavily weighted tickers on the ETF, monitors their returns using the request security function, and then uses their weight to calculate the synthetic returns of the ETF of interest.

For example, in the chart we have SMH.

The indicator is looking at the top weighted tickers of SMH, calculating their returns, adjusting it for their individual weight on SMH and then predicting the expected return of SMH based on the weighing and holding's returns themselves.

How to Use it

The indicator is pretty straight forward, you select which ever index you are on and your desired timeframe (you can do as low as 30-Minutes or as high as monthly or quarterly).

The indicator will then retrieve the top holdings for that ticker, their corresponding weights and calculate the expected daily return based on the weight and return of these tickers.

It will plot this return for you on the chart.

Other Options

There is an optional table for you to view the actual weight, ticker composition and period returns for each of the top x tickers for an index. You can simply toggle "Show Table" in the settings menu, and it will show you the list of all tickers included, their period returns and their weight on the ETF.

Tips for Use

Works well to see when an index may be over the actual top weighted tickers, implying a pullback/sell, or under. For example:

SPY today fell well below its top tickers and is currently rallying back up to the expected close range.

You can see in the primary chart, SMH fell below and returned to its balance, being at the expected close range based on its component tickers.

That is the indicator!

Its simple but powerful!

Hope you enjoy and as always, safe trades!

Full Floating Dashboard YUJiDisplay information on top right corner.

Info shown:

High and Low

Current Price

24 Hour Change

Smart Flow Tracker [The_lurker]

Smart Flow Tracker (SFT): Advanced Order Flow Tracking Indicator

Overview

Smart Flow Tracker (SFT) is an advanced indicator designed for real-time tracking and analysis of order flows. It focuses on detecting institutional patterns, massive orders, and potential reversals through analysis of lower timeframes (Lower Timeframe) or live ticks. It provides deep insights into market behavior using a multi-layered intelligent detection system and a clear visual interface, giving traders a competitive edge.

SFT focuses on trade volumes, directions, and frequencies to uncover unusual activity that may indicate institutional intervention, massive orders, or manipulation attempts (traps).

Indicator Operation Levels

SFT operates on three main levels:

1. Microscopic Monitoring: Tracks every trade at precise timeframes (down to one second), providing visibility not available in standard timeframes.

2. Advanced Statistical Analysis: Calculates averages, deviations, patterns, and anomalies using precise mathematical algorithms.

3. Behavioral Artificial Intelligence: Recognizes behavioral patterns such as hidden institutional accumulation, manipulation attempts and traps, and potential reversal points.

Key Features

SFT features a set of advanced functions to enhance the trader's experience:

1. Intelligent Order Classification System: Classifies orders into six categories based on size and pattern:

- Standard: Normal orders with typical size.

- Significant 💎: Orders larger than average by 1.5 times.

- Major 🔥: Orders larger than average by 2.5 times.

- Massive 🐋: Orders larger than average by 3 times.

- Institutional 🏛️: Consistent patterns indicating institutional activity.

- Reversal 🔄: Large orders indicating direction change.

- Trap ⚠️: Patterns that may be price traps.

2. Institutional Patterns Detection: Tracks sequences of similar-sized orders, detects organized institutional activity, and is customizable (number of trades, variance ratio).

3. Reversals Detection: Compares recent flows with previous ones, detects direction shifts from up to down or vice versa, and operates only on large orders (Major/Massive/Institutional).

4. Traps Detection: Identifies sequences of large orders in one direction, followed by an institutional order in the opposite direction, with early alerts for false moves.

5. Flow Delta Bar: Displays the difference between buy and sell volumes as a percentage for balance, with instant updates per trade.

6. Dynamic Statistics Panel: Displays overall buy and sell ratios with real-time updates and interactive colors.

How It Works and Understanding

SFT relies on logical sequential stages for data processing:

A. Data Collection: Uses the `request.security_lower_tf()` function to extract data from a lower timeframe (like 1S) even on a higher timeframe (like 5D). For each time unit, it calculates:

- Adjusted Volume: Either normal volume or "price-weighted volume" (hlc3 * volume) based on user choice.

- Trade Direction: Compared to previous close (rise → buy, fall → sell).

B. Building Temporary Memory: Maintains a dynamic list (sizeHistory) of the last 100 trade sizes, continuously calculating the moving average (meanSize).

C. Intelligent Classification: Compares each new trade to the average:

- > 1.5 × average → Significant.

- > 2.5 × average → Major.

- > 3.0 × average → Massive.

- Institutional Patterns Check: A certain number of trades (e.g., 5) with a specified variance ratio (±5%) → Institutional.

D. Advanced Detection:

- Reversal: Compares buy/sell totals in two consecutive periods.

- Trap: Sequence of large trades in one direction followed by an opposite institutional trade.

E. Display and Alerts: Results displayed in an automatically updated table, with option to enable alerts for notable events.

Settings (Fully Customizable)

SFT offers extensive options to adapt to the trader's needs:

A. Display Settings:

- Language: English / Arabic.

- Table Position: 9 options (e.g., Top Right, Middle Right, Bottom Left).

- Display Size: Tiny / Small / Normal / Large.

- Max Rows: 10–100.

- Enable Flow Delta Bar: Yes / No.

- Enable Statistics Panel: Yes / No (displays buy/sell % ratio).

B.- Technical Settings:

- Data Source: Lower Timeframe / Live Tick (simulation).

- Timeframe: Optional (e.g., 1S, 5S, 1).

- Calculation Type: Volume / Price Volume.

C. Intelligent Detection System:

- Enable Institutional Patterns Detection.

- Pattern Length: 3–20 trades.

- Allowed Variance Ratio: 1%–20%.

- Massive Orders Detection Factor: 2.0–10.0.

D. Classification Criteria:

- Significant Orders Factor: 1.2–3.0.

- Major Orders Factor: 2.0–5.0.

E. **Advanced Detection**:

- Enable Reversals Detection (with review period).

- Enable Traps Detection (with minimum sequence limit).

F. Alerts System:

- Enable for each type: Massive orders, institutional patterns, reversals, traps, severe imbalance (60%–90%).

G. Color System: Manual customization for each category:

- Standard Buy 🟢: Dark gray green.

- Standard Sell 🔴: Dark gray red.

- Significant Buy 🟢: Medium green.

- Significant Sell 🔴: Medium red.

- Major Orders 🟣: Purple.

- Massive Orders 🟠: Orange.

- Institutional 🟦: Sky blue.

- Reversal 🔵: Blue.

- Trap 🟣: Pink-purple.

Target Audiences

SFT benefits a wide range of traders and investors:

1. Scalpers: Instant detection of large orders, liquidity points identification, avoiding traps in critical moments.

2. Day Traders: Tracking smart money footprint, determining real session direction, early reversals detection.

3. Swing Traders: Confirming trend strength, detecting institutional accumulation/distribution, identifying optimal entry points.

4. Investors: Understanding true market sentiments, avoiding entry at false peaks, identifying real value zones.

⚠️ Disclaimer:

This indicator is for educational and analytical purposes only. It does not constitute financial, investment, or trading advice. Use it in conjunction with your own strategy and risk management. Neither TradingView nor the developer is liable for any financial decisions or losses.

Smart Flow Tracker (SFT): مؤشر متقدم لتتبع تدفقات الأوامر

نظرة عامة

Smart Flow Tracker (SFT) مؤشر متقدم مصمم لتتبع وتحليل تدفقات الأوامر في الوقت الفعلي. يركز على كشف الأنماط المؤسسية، الأوامر الضخمة، والانعكاسات المحتملة من خلال تحليل الأطر الزمنية الأقل (Lower Timeframe) أو التيك الحي. يوفر رؤية عميقة لسلوك السوق باستخدام نظام كشف ذكي متعدد الطبقات وواجهة مرئية واضحة، مما يمنح المتداولين ميزة تنافسية.

يركز SFT على حجم الصفقات، اتجاهها، وتكرارها لكشف النشاط غير العادي الذي قد يشير إلى تدخل مؤسسات، أوامر ضخمة، أو محاولات تلاعب (فخاخ).

مستويات عمل المؤشر

يعمل SFT على ثلاثة مستويات رئيسية:

1. المراقبة المجهرية: يتتبع كل صفقة على مستوى الأطر الزمنية الدقيقة (حتى الثانية الواحدة)، مما يوفر رؤية غير متوفرة في الأطر الزمنية العادية.

2. التحليل الإحصائي المتقدم: يحسب المتوسطات، الانحرافات، الأنماط، والشذوذات باستخدام خوارزميات رياضية دقيقة.

3. الذكاء الاصطناعي السلوكي: يتعرف على أنماط سلوكية مثل التراكم المؤسسي المخفي، محاولات التلاعب والفخاخ، ونقاط الانعكاس المحتملة.

الميزات الرئيسية

يتميز SFT بمجموعة من الوظائف المتقدمة لتحسين تجربة المتداول:

1. نظام تصنيف الأوامر الذكي: يصنف الأوامر إلى ست فئات بناءً على الحجم والنمط:

- Standard (قياسي)**: أوامر عادية بحجم طبيعي.

- Significant 💎 (مهم)**: أوامر أكبر من المتوسط بـ1.5 ضعف.

- Major 🔥 (كبير)**: أوامر أكبر من المتوسط بـ2.5 ضعف.

- Massive 🐋 (ضخم)**: أوامر أكبر من المتوسط بـ3 أضعاف.

- Institutional 🏛️ (مؤسسي)**: أنماط متسقة تشير إلى نشاط مؤسسي.

- Reversal 🔄 (انعكاس)**: أوامر كبيرة تشير إلى تغيير اتجاه.

- Trap ⚠️ (فخ)**: أنماط قد تكون فخاخًا سعرية.

2. كشف الأنماط المؤسسية: يتتبع تسلسل الأوامر المتشابهة في الحجم، يكشف النشاط المؤسسي المنظم، وقابل للتخصيص (عدد الصفقات، نسبة التباين).

3. كشف الانعكاسات: يقارن التدفقات الأخيرة بالسابقة، يكشف تحول الاتجاه من صعود إلى هبوط أو العكس، ويعمل فقط على الأوامر الكبيرة (Major/Massive/Institutional).

4. كشف الفخاخ: يحدد تسلسل أوامر كبيرة في اتجاه واحد، يليها أمر مؤسسي في الاتجاه المعاكس، مع تنبيه مبكر للحركات الكاذبة.

5. شريط دلتا التدفق: يعرض الفرق بين حجم الشراء والبيع كنسبة مئوية للتوازن، مع تحديث فوري لكل صفقة.

6. لوحة إحصائيات ديناميكية: تعرض نسبة الشراء والبيع الإجمالية مع تحديث لحظي وألوان تفاعلية.

طريقة العمل والفهم

يعتمد SFT على مراحل منطقية متسلسلة لمعالجة البيانات:

أ. جمع البيانات: يستخدم دالة `request.security_lower_tf()` لاستخراج بيانات من إطار زمني أدنى (مثل 1S) حتى على إطار زمني أعلى (مثل 5D). لكل وحدة زمنية، يحسب:

- الحجم المعدّل: إما الحجم العادي (volume) أو "الحجم المرجّح بالسعر" (hlc3 * volume) حسب الاختيار.

- اتجاه الصفقة: مقارنة الإغلاق الحالي بالسابق (ارتفاع → شراء، انخفاض → بيع).

ب. بناء الذاكرة المؤقتة: يحتفظ بقائمة ديناميكية (sizeHistory) لآخر 100 حجم صفقة، ويحسب المتوسط المتحرك (meanSize) باستمرار.

ج. التصنيف الذكي: يقارن كل صفقة جديدة بالمتوسط:

- > 1.5 × المتوسط → Significant.

- > 2.5 × المتوسط → Major.

- > 3.0 × المتوسط → Massive.

- فحص الأنماط المؤسسية: عدد معين من الصفقات (مثل 5) بنسبة تباين محددة (±5%) → Institutional.

د. الكشف المتقدم:

- الانعكاس: مقارنة مجموع الشراء/البيع في فترتين متتاليتين.

- الفخ: تسلسل صفقات كبيرة في اتجاه واحد يتبعها صفقة مؤسسية معاكسة.

هـ. العرض والتنبيه: عرض النتائج في جدول محدّث تلقائيًا، مع إمكانية تفعيل تنبيهات للأحداث المميزة.

لإعدادات (قابلة للتخصيص بالكامل)

يوفر SFT خيارات واسعة للتكييف مع احتياجات المتداول:

أ. إعدادات العرض:

- اللغة: English / العربية.

- موقع الجدول: 9 خيارات (مثل Top Right, Middle Right, Bottom Left).

- حجم العرض: Tiny / Small / Normal / Large.

- الحد الأقصى للصفوف: 10–100.

- تفعيل شريط دلتا التدفق: نعم / لا.

- تفعيل لوحة الإحصائيات: نعم / لا (تعرض نسبة الشراء/البيع %).

ب. الإعدادات التقنية:

- مصدر البيانات: Lower Timeframe / Live Tick (محاكاة).

- الإطار الزمني: اختياري (مثل 1S, 5S, 1).

- نوع الحساب: Volume / Price Volume.

ج. نظام الكشف الذكي:

- تفعيل كشف الأنماط المؤسسية.

- طول النمط: 3–20 صفقة.

- نسبة التباين: 1%–20%.

- عامل كشف الأوامر الضخمة: 2.0–10.0.

د. معايير التصنيف:

- عامل الأوامر المهمة: 1.2–3.0.

- عامل الأوامر الكبرى: 2.0–5.0.

هـ. الكشف المتقدم:

- تفعيل كشف الانعكاسات (مع فترة مراجعة).

- تفعيل كشف الفخاخ (مع حد أدنى للتسلسل).

و. نظام التنبيهات:

- تفعيل لكل نوع: أوامر ضخمة، أنماط مؤسسية، انعكاسات، فخاخ، عدم توازن شديد (60%–90%).

ز. نظام الألوان**: تخصيص يدوي لكل فئة:

- شراء قياسي 🟢: أخضر رمادي داكن.

- بيع قياسي 🔴: أحمر رمادي داكن.

- شراء مهم 🟢: أخضر متوسط.

- بيع مهم 🔴: أحمر متوسط.

- أوامر كبرى 🟣: بنفسجي.

- أوامر ضخمة 🟠: برتقالي.

- مؤسسي 🟦: أزرق سماوي.

- انعكاس 🔵: أزرق.

- فخ 🟣: وردي-أرجواني.

الفئات المستهدفة

يستفيد من SFT مجموعة واسعة من المتداولين والمستثمرين:

1. السكالبرز (Scalpers): كشف لحظي للأوامر الكبيرة، تحديد نقاط السيولة، تجنب الفخاخ في اللحظات الحرجة.

2. المتداولون اليوميون (Day Traders): تتبع بصمة الأموال الذكية، تحديد اتجاه الجلسة الحقيقي، كشف الانعكاسات المبكرة.

3. المتداولون المتأرجحون (Swing Traders): تأكيد قوة الاتجاه، كشف التراكم/التوزيع المؤسسي، تحديد نقاط الدخول المثلى.

4. المستثمرون: فهم معنويات السوق الحقيقية، تجنب الدخول في قمم كاذبة، تحديد مناطق القيمة الحقيقية.

⚠️ إخلاء مسؤولية:

هذا المؤشر لأغراض تعليمية وتحليلية فقط. لا يُمثل نصيحة مالية أو استثمارية أو تداولية. استخدمه بالتزامن مع استراتيجيتك الخاصة وإدارة المخاطر. لا يتحمل TradingView ولا المطور مسؤولية أي قرارات مالية أو خسائر.

Risk & Position DashboardRisk & Position Dashboard

Overview

The Risk & Position Dashboard is a comprehensive trading tool designed to help traders calculate optimal position sizes, manage risk, and visualize potential profit/loss scenarios before entering trades. This indicator provides real-time calculations for position sizing based on account size, risk percentage, and stop-loss levels, while displaying multiple take-profit targets with customizable risk-reward ratios.

Key Features

Position Sizing & Risk Management:

Automatic position size calculation based on account size and risk percentage

Support for leveraged trading with maximum leverage limits

Fractional shares support for brokers that allow partial share trading

Real-time fee calculation including entry, stop-loss, and take-profit fees

Break-even price calculation including trading fees

Multi-Target Profit Management:

Support for up to 3 take-profit levels with individual portion allocations

Customizable risk-reward ratios for each take-profit target

Visual profit/loss zones displayed as colored boxes on the chart

Individual profit calculations for each take-profit level

Visual Dashboard:

Clean, customizable table display showing all key metrics

Configurable label positioning and styling options

Real-time tracking of whether stop-loss or take-profit levels have been reached

Color-coded visual zones for easy identification of risk and reward areas

Advanced Configuration:

Comprehensive input validation and error handling

Support for different chart timeframes and symbols

Customizable colors, fonts, and display options

Hide/show individual data fields for personalized dashboard views

How to Use

Set Account Parameters: Configure your account size, maximum risk percentage per trade, and trading fees in the "Account Settings" section.

Define Trade Setup: Use the "Entry" time picker to select your entry point on the chart, then input your entry price and stop-loss level.

Configure Take Profits: Set your desired risk-reward ratios and portion allocations for each take-profit level. The script supports 1-3 take-profit targets.

Analyze Results: The dashboard will automatically calculate and display position size, number of shares, potential profits/losses, fees, and break-even levels.

Visual Confirmation: Colored boxes on the chart show profit zones (green) and loss zones (red), with lines extending to current price levels.

Reset Entry and SL:

You can easily reset the entry and stop-loss by clicking the "Reset points..." button from the script's "More" menu.

This is useful if you want to quickly clear your current trade setup and start fresh without manually adjusting the points on the chart.

Calculations

The script performs sophisticated calculations including:

Position size based on risk amount and price difference between entry and stop-loss

Leverage requirements and position amount calculations

Fee-adjusted risk-reward ratios for realistic profit expectations

Break-even price including all trading costs

Individual profit calculations for partial position closures

Detailed Take-Profit Calculation Formula:

The take-profit prices are calculated using the following mathematical formula:

// Core variables:

// risk_amount = account_size * (risk_percentage / 100)

// total_risk_per_share = |entry_price - sl_price| + (entry_price * fee%) + (sl_price * fee%)

// shares = risk_amount / total_risk_per_share

// direction_factor = 1 for long positions, -1 for short positions

// Take-profit calculation:

net_win = total_risk_per_share * shares * RR_ratio

tp_price = (net_win + (direction_factor * entry_price * shares) + (entry_price * fee% * shares)) / (direction_factor * shares - fee% * shares)

Step-by-step example for a long position (based on screenshot):

Account Size: 2,000 USDT, Risk: 2% = 40 USDT

Entry: 102,062.9 USDT, Stop Loss: 102,178.4 USDT, Fee: 0.06%

Risk per share: |102,062.9 - 102,178.4| + (102,062.9 × 0.0006) + (102,178.4 × 0.0006) = 115.5 + 61.24 + 61.31 = 238.05 USDT

Shares: 40 ÷ 238.05 = 0.168 shares (rounded to 0.17 in display)

Position Size: 0.17 × 102,062.9 = 17,350.69 USDT

Position Amount (with 9x leverage): 17,350.69 ÷ 9 = 1,927.85 USDT

For 2:1 RR: Net win = 238.05 × 0.17 × 2 = 80.94 USDT

TP1 price = (80.94 + (1 × 102,062.9 × 0.17) + (102,062.9 × 0.0006 × 0.17)) ÷ (1 × 0.17 - 0.0006 × 0.17) = 101,464.7 USDT

For 3:1 RR: TP2 price = 101,226.7 USDT (following same formula with RR=3)

This ensures that after accounting for all fees, the actual risk-reward ratio matches the specified target ratio.

Risk Management Features

Maximum Trade Amount: Optional setting to limit position size regardless of account size

Leverage Limits: Built-in maximum leverage protection

Fee Integration: All calculations include realistic trading fees for accurate expectations

Validation: Automatic checking that take-profit portions sum to 100%

Historical Tracking: Visual indication when stop-loss or take-profit levels are reached (within last 5000 bars)

Understanding Max Trade Amount - Multiple Simultaneous Trades:

The "Max Trade Amount" feature is designed for traders who want to open multiple positions simultaneously while maintaining proper risk management. Here's how it works:

Key Concept:

- Risk percentage (2%) always applies to your full Account Size

- Max Trade Amount limits the capital allocated per individual trade

- This allows multiple trades with full risk on each trade

Example from Screenshot:

Account Size: 2,000 USDT

Max Trade Amount: 500 USDT

Risk per Trade: 2% × 2,000 = 40 USDT per trade

Stop Loss Distance: 0.11% from entry

Result: Position Size = 17,350.69 USDT with 35x leverage

Total Risk (including fees): 40.46 USDT

Multiple Trades Strategy:

With this setup, you can open:

Trade 1: 40 USDT risk, 495.73 USDT position amount (35x leverage)

Trade 2: 40 USDT risk, 495.73 USDT position amount (35x leverage)

Trade 3: 40 USDT risk, 495.73 USDT position amount (35x leverage)

Trade 4: 40 USDT risk, 495.73 USDT position amount (35x leverage)

Total Portfolio Exposure:

- 4 simultaneous trades = 4 × 495.73 = 1,982.92 USDT position amount

- Total risk exposure = 4 × 40 = 160 USDT (8% of account)

Position Size & Drawdown ManagerThis tool is designed to help traders dynamically adjust their position size and drawdown expectations as their trading capital changes over time. It provides a simple and intuitive way to translate backtest results into real-world position sizing decisions.

Purpose and Functionality

The indicator uses your original backtest parameters — including base capital, base drawdown percentage, and base position size — and your current account balance to calculate how your risk profile changes. It presents two main scenarios:

Lock Drawdown %: Keeps your original drawdown percentage fixed and calculates the new position size required.

Lock Position Size: Keeps your position size unchanged and shows how your drawdown percentage will shift.

Why it’s useful

Many traders face the challenge of scaling their strategies as their account grows or shrinks. This tool makes it easy to visualize the relationship between position sizing, capital, and drawdown. It’s particularly valuable for risk management, portfolio rebalancing, and maintaining consistent exposure when transitioning from backtest conditions to live trading.

How it works

The calculations are displayed in a clean, color-coded table that updates dynamically. This allows you to instantly see how capital fluctuations impact your expected drawdown or position size. You can toggle between light and dark themes and highlight important cells for clarity.

Practical use case

Combine this tool with your TradingView strategy results to better interpret your backtests and adjust your real-world trade sizes accordingly. It bridges the gap between simulated performance and actual account management.

Chart example

The chart included focuses only on this indicator, showing the output table and visual layout clearly without additional scripts or overlays.

Machine Learning Moving Average [BackQuant]Machine Learning Moving Average

A powerful tool combining clustering, pseudo-machine learning, and adaptive prediction, enabling traders to understand and react to price behavior across multiple market regimes (Bullish, Neutral, Bearish). This script uses a dynamic clustering approach based on percentile thresholds and calculates an adaptive moving average, ideal for forecasting price movements with enhanced confidence levels.

What is Percentile Clustering?

Percentile clustering is a method that sorts and categorizes data into distinct groups based on its statistical distribution. In this script, the clustering process relies on the percentile values of a composite feature (based on technical indicators like RSI, CCI, ATR, etc.). By identifying key thresholds (lower and upper percentiles), the script assigns each data point (price movement) to a cluster (Bullish, Neutral, or Bearish), based on its proximity to these thresholds.

This approach mimics aspects of machine learning, where we “train” the model on past price behavior to predict future movements. The key difference is that this is not true machine learning; rather, it uses data-driven statistical techniques to "cluster" the market into patterns.

Why Percentile Clustering is Useful

Clustering price data into meaningful patterns (Bullish, Neutral, Bearish) helps traders visualize how price behavior can be grouped over time.

By leveraging past price behavior and technical indicators, percentile clustering adapts dynamically to evolving market conditions.

It helps you understand whether price behavior today aligns with past bullish or bearish trends, improving market context.

Clusters can be used to predict upcoming market conditions by identifying regimes with high confidence, improving entry/exit timing.

What This Script Does

Clustering Based on Percentiles : The script uses historical price data and various technical features to compute a "composite feature" for each bar. This feature is then sorted and clustered based on predefined percentile thresholds (e.g., 10th percentile for lower, 90th percentile for upper).

Cluster-Based Prediction : Once clustered, the script uses a weighted average, cluster momentum, or regime transition model to predict future price behavior over a specified number of bars.

Dynamic Moving Average : The script calculates a machine-learning-inspired moving average (MLMA) based on the current cluster, adjusting its behavior according to the cluster regime (Bullish, Neutral, Bearish).

Adaptive Confidence Levels : Confidence in the predicted return is calculated based on the distance between the current value and the other clusters. The further it is from the next closest cluster, the higher the confidence.

Visual Cluster Mapping : The script visually highlights different clusters on the chart with distinct colors for Bullish, Neutral, and Bearish regimes, and plots the MLMA line.

Prediction Output : It projects the predicted price based on the selected method and shows both predicted price and confidence percentage for each prediction horizon.

Trend Identification : Using the clustering output, the script colors the bars based on the current cluster to reflect whether the market is trending Bullish (green), Bearish (red), or is Neutral (gray).

How Traders Use It

Predicting Price Movements : The script provides traders with an idea of where prices might go based on past market behavior. Traders can use this forecast for short-term and long-term predictions, guiding their trades.

Clustering for Regime Analysis : Traders can identify whether the market is in a Bullish, Neutral, or Bearish regime, using that information to adjust trading strategies.

Adaptive Moving Average for Trend Following : The adaptive moving average can be used as a trend-following indicator, helping traders stay in the market when it’s aligned with the current trend (Bullish or Bearish).

Entry/Exit Strategy : By understanding the current cluster and its associated trend, traders can time entries and exits with higher precision, taking advantage of favorable conditions when the confidence in the predicted price is high.

Confidence for Risk Management : The confidence level associated with the predicted returns allows traders to manage risk better. Higher confidence levels indicate stronger market conditions, which can lead to higher position sizes.

Pseudo Machine Learning Aspect

While the script does not use conventional machine learning models (e.g., neural networks or decision trees), it mimics certain aspects of machine learning in its approach. By using clustering and the dynamic adjustment of a moving average, the model learns from historical data to adjust predictions for future price behavior. The "learning" comes from how the script uses past price data (and technical indicators) to create patterns (clusters) and predict future market movements based on those patterns.

Why This Is Important for Traders

Understanding market regimes helps to adjust trading strategies in a way that adapts to current market conditions.

Forecasting price behavior provides an additional edge, enabling traders to time entries and exits based on predicted price movements.

By leveraging the clustering technique, traders can separate noise from signal, improving the reliability of trading signals.

The combination of clustering and predictive modeling in one tool reduces the complexity for traders, allowing them to focus on actionable insights rather than manual analysis.

How to Interpret the Output

Bullish (Green) Zone : When the price behavior clusters into the Bullish zone, expect upward price movement. The MLMA line will help confirm if the trend remains upward.

Bearish (Red) Zone : When the price behavior clusters into the Bearish zone, expect downward price movement. The MLMA line will assist in tracking any downward trends.

Neutral (Gray) Zone : A neutral market condition signals indecision or range-bound behavior. The MLMA line can help track any potential breakouts or trend reversals.

Predicted Price : The projected price is shown on the chart, based on the cluster's predicted behavior. This provides a useful reference for where the price might move in the near future.

Prediction Confidence : The confidence percentage helps you gauge the reliability of the predicted price. A higher percentage indicates stronger market confidence in the forecasted move.

Tips for Use

Combining with Other Indicators : Use the output of this indicator in combination with your existing strategy (e.g., RSI, MACD, or moving averages) to enhance signal accuracy.

Position Sizing with Confidence : Increase position size when the prediction confidence is high, and decrease size when it’s low, based on the confidence interval.

Regime-Based Strategy : Consider developing a multi-strategy approach where you use this tool for Bullish or Bearish regimes and a separate strategy for Neutral markets.

Optimization : Adjust the lookback period and percentile settings to optimize the clustering algorithm based on your asset’s characteristics.

Conclusion

The Machine Learning Moving Average offers a novel approach to price prediction by leveraging percentile clustering and a dynamically adapting moving average. While not a traditional machine learning model, this tool mimics the adaptive behavior of machine learning by adjusting to evolving market conditions, helping traders predict price movements and identify trends with improved confidence and accuracy.

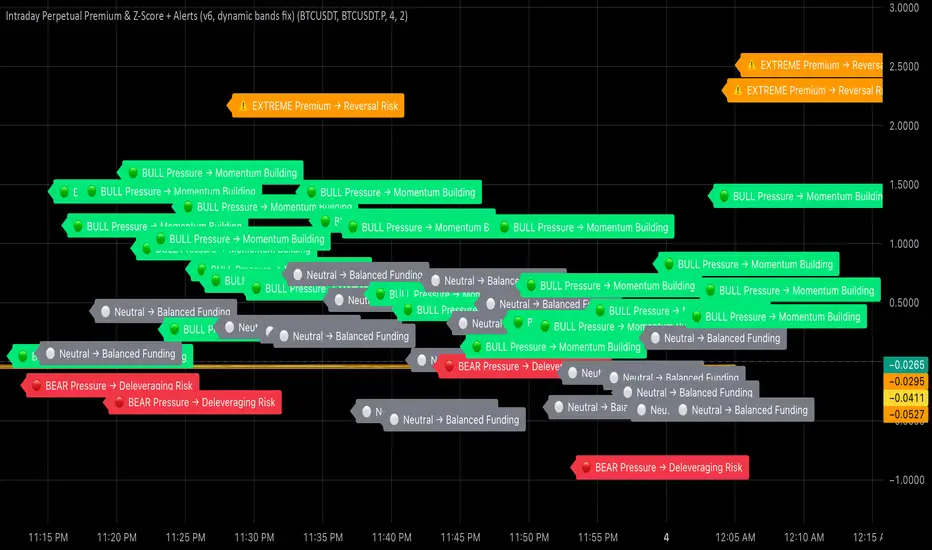

Intraday Perpetual Premium & Z-ScoreThis indicator measures the real-time premium of a perpetual futures contract relative to its spot market and interprets it through a statistical lens.

It helps traders detect when funding pressure is building, when leverage is being unwound, and when crowding in the futures market may precede volatility.

How it works

• Premium (%) = (Perp – Spot) ÷ Spot × 100

The script fetches both spot and perpetual prices and calculates their percentage difference each minute.

• Rolling Mean & Z-Score

Over a 4-hour look-back, it computes the average premium and standard deviation to derive a Z-Score, showing how stretched current sentiment is.

• Dynamic ±2σ Bands highlight statistically extreme premiums or discounts.

• Rate of Change (ROC) over one hour gauges the short-term directional acceleration of funding flows.

Colour & Label Interpretation

Visual cue Meaning Trading Implication

🟢 Green bars + “BULL Pressure” Premium rising faster than mean Leverage inflows → momentum strengthening

🔴 Red bars + “BEAR Pressure” Premium shrinking Leverage unwind → pull-back or consolidation

⚠️ Orange “EXTREME Premium/Discount” Crowded trade → heightened reversal risk

⚪ Grey bars Neutral Balanced conditions

Alerts

• Bull Pressure Alert → funding & premium rising (momentum building)

• Bear Pressure Alert → premium falling (deleveraging)

• Extreme Premium Alert → crowded longs; potential top

• Extreme Discount Alert → capitulation; possible bottom

Use case

Combine this indicator with your Heikin-Ashi, RSI, and MACD confluence rules:

• Enter only when your oscillators are low → curling up and Bull Pressure triggers.

• Trim or exit when Bear Pressure or Extreme Premium appears.

• Watch for Extreme Discount during flushes as an early bottoming clue.

korea time with 200 korea time

start time

08

09

17

18

23

00

This script makes it easier to look at the charts

The time automatically displays even if you don't bother to bring the mouse by hand

Now you can see the time intuitively

Run a very happy trading session

India Vix based Strangle StrikesA clean Nifty–VIX dashboard that converts India VIX into expected daily moves, price ranges, and suggested strangle strikes. Includes VIX %, expanded 1.2× range, and smart rounded strike levels for options trading.

This script provides a professional on-chart dashboard that converts India VIX into actionable trading levels for Nifty. It calculates the VIX-based expected daily move, projected price ranges, expanded 1.2× ranges, and suggested strangle strike prices. Includes clean formatting, color-coded sections, and real-time updates.

Ideal for traders using straddles, strangles, intraday volatility models, range-bound setups, and options-based risk management.

1.2x expanded range is better success probability, may keep 20% of strangle value as stop loss.

The vix based system is intended to give approx. 70%+ success rate.

JiNFOJiNFO is a clean, data-driven overlay that displays key information about the current symbol directly on your chart — without clutter.

🧭 What it shows

Company & Symbol Info – Name, ticker, sector, industry, market cap

Timeframe Label – Current chart timeframe (auto-formatted)

ATR (14) & % Volatility – With color dots for low 🟢 / medium 🟡 / high 🔴 volatility

Moving Average Status – Indicates if price is above or below the selected MA (default 150)

RSI & RSI-SMA (14) – Compact line with live values and color dot for overbought/neutral/oversold zones

Distance from SMA (50) – Shows how far price is from the 50 MA (+/- %) and grades it A–D by distance 🟢🟠🔴

Earnings Countdown – Days remaining until the next earnings date (if available)

⚙️ Customization

Position (top/middle/bottom, left/center/right)

Text size (default Small), color, opacity (100 %)

Toggle any data row on or off

Choose compact or verbose labels

🧩 Purpose

JiNFO replaces bulky data panels with a lightweight, transparent information layer — perfect for traders who want essential fundamentals, volatility, and technical context at a glance.

Custom Horizontal Lines | Trade Symmetry📊 Custom Horizontal Lines

🔍 Overview

The Custom Horizontal Lines is a precision utility designed for traders who perform manual higher-timeframe analysis and want to preserve their marked price levels directly on the chart.

It doesn’t calculate or detect anything automatically — instead, it acts as your personal level memory, preserving your analyzed zones and reference prices throughout the session.

Ideal for traders who manually mark the High, Low, Open, Close, Mean Thresholds, and Quarter Levels of Order Blocks, Fair Value Gaps, Inversion Fair Value Gaps and Wicks before the trading day begins.

⚙️ Key Features

✅ Manual Level Entry — Input your analyzed price levels (OB, FVG, WICK,etc) directly into the indicator settings.

✅ Preserved Levels — Once entered, your lines stay visible and consistent — even after switching symbols, timeframes, or reloading the chart.

✅ Supports All Level Types — Store any kind of manually defined level: OB highs/lows, FVG boundaries, Wicks, Mean Thresholds, Quarter levels, or custom reference prices.

✅ Clean Visualization — Customize line color, style, and labels for easy visual organization.

✅ Session-Ready Workflow — Built for pre-market preparation — enter your HTF levels once, and trade around them all day.

✅ No Auto Calculations — 100% manual by design — ensuring only your analyzed levels are shown, exactly as you defined them.

💡 How to Use

Open the indicator’s settings and manually enter those price values.

The indicator will plot and preserve those exact levels on your chart.

Switch to your lower timeframe and observe how price reacts around them — without ever needing to redraw.

🎯 Why It’s Useful

Keeps your HTF levels organized and persistent across sessions.

Saves time by avoiding redrawing.

Fits perfectly into ICT / Smart Money trading workflows.

Ensures full manual control and precision over what’s displayed on your chart.

🧩 Ideal For

ICT and Smart Money traders

Institutional-style manual analysts

Traders marking Mean Thresholds, or Quarter Levels of OBs, FVGs, Wicks etc

Anyone who wants a clean, reliable way to preserve their manual analysis

Scientific Correlation Testing FrameworkScientific Correlation Testing Framework - Comprehensive Guide

Introduction to Correlation Analysis

What is Correlation?

Correlation is a statistical measure that describes the degree to which two assets move in relation to each other. Think of it like measuring how closely two dancers move together on a dance floor.

Perfect Positive Correlation (+1.0): Both dancers move in perfect sync, same direction, same speed

Perfect Negative Correlation (-1.0): Both dancers move in perfect sync but in opposite directions

Zero Correlation (0): The dancers move completely independently of each other

In financial markets, correlation helps us understand relationships between different assets, which is crucial for:

Portfolio diversification

Risk management

Pairs trading strategies

Hedging positions

Market analysis

Why This Script is Special

This script goes beyond simple correlation calculations by providing:

Two different correlation methods (Pearson and Spearman)

Statistical significance testing to ensure results are meaningful

Rolling correlation analysis to track how relationships change over time

Visual representation for easy interpretation

Comprehensive statistics table with detailed metrics

Deep Dive into the Script's Components

1. Input Parameters Explained-

Symbol Selection:

This allows you to select the second asset to compare with the chart's primary asset

Default is Apple (NASDAQ:AAPL), but you can change this to any symbol

Example: If you're viewing a Bitcoin chart, you might set this to "NASDAQ:TSLA" to see if Bitcoin and Tesla are correlated

Correlation Window (60): This is the number of periods used to calculate the main correlation

Larger values (e.g., 100-500) provide more stable, long-term correlation measures

Smaller values (e.g., 10-50) are more responsive to recent price movements

60 is a good balance for most daily charts (about 3 months of trading days)

Rolling Correlation Window (20): A shorter window to detect recent changes in correlation

This helps identify when the relationship between assets is strengthening or weakening

Default of 20 is roughly one month of trading days

Return Type: This determines how price changes are calculated

Simple Returns: (Today's Price - Yesterday's Price) / Yesterday's Price

Easy to understand: "The asset went up 2% today"

Log Returns: Natural logarithm of (Today's Price / Yesterday's Price)

More mathematically elegant for statistical analysis

Better for time-additive properties (returns over multiple periods)

Less sensitive to extreme values.

Confidence Level (95%): This determines how certain we want to be about our results

95% confidence means we accept a 5% chance of being wrong (false positive)

Higher confidence (e.g., 99%) makes the test more strict

Lower confidence (e.g., 90%) makes the test more lenient

95% is the standard in most scientific research

Show Statistical Significance: When enabled, the script will test if the correlation is statistically significant or just due to random chance.

Display options control what you see on the chart:

Show Pearson/Spearman/Rolling Correlation: Toggle each correlation type on/off

Show Scatter Plot: Displays a scatter plot of returns (limited to recent points to avoid performance issues)

Show Statistical Tests: Enables the detailed statistics table

Table Text Size: Adjusts the size of text in the statistics table

2.Functions explained-

calcReturns():

This function calculates price returns based on your selected method:

Log Returns:

Formula: ln(Price_t / Price_t-1)

Example: If a stock goes from $100 to $101, the log return is ln(101/100) = ln(1.01) ≈ 0.00995 or 0.995%

Benefits: More symmetric, time-additive, and better for statistical modeling

Simple Returns:

Formula: (Price_t - Price_t-1) / Price_t-1

Example: If a stock goes from $100 to $101, the simple return is (101-100)/100 = 0.01 or 1%

Benefits: More intuitive and easier to understand

rankArray():

This function calculates the rank of each value in an array, which is used for Spearman correlation:

How ranking works:

The smallest value gets rank 1

The second smallest gets rank 2, and so on

For ties (equal values), they get the average of their ranks

Example: For values

Sorted:

Ranks: (the two 2s tie for ranks 1 and 2, so they both get 1.5)

Why this matters: Spearman correlation uses ranks instead of actual values, making it less sensitive to outliers and non-linear relationships.

pearsonCorr():

This function calculates the Pearson correlation coefficient:

Mathematical Formula:

r = (nΣxy - ΣxΣy) / √

Where x and y are the two variables, and n is the sample size

What it measures:

The strength and direction of the linear relationship between two variables

Values range from -1 (perfect negative linear relationship) to +1 (perfect positive linear relationship)

0 indicates no linear relationship

Example:

If two stocks have a Pearson correlation of 0.8, they have a strong positive linear relationship

When one stock goes up, the other tends to go up in a fairly consistent proportion

spearmanCorr():

This function calculates the Spearman rank correlation:

How it works:

Convert each value in both datasets to its rank

Calculate the Pearson correlation on the ranks instead of the original values

What it measures:

The strength and direction of the monotonic relationship between two variables

A monotonic relationship is one where as one variable increases, the other either consistently increases or decreases

It doesn't require the relationship to be linear

When to use it instead of Pearson:

When the relationship is monotonic but not linear

When there are significant outliers in the data

When the data is ordinal (ranked) rather than interval/ratio

Example:

If two stocks have a Spearman correlation of 0.7, they have a strong positive monotonic relationship

When one stock goes up, the other tends to go up, but not necessarily in a straight-line relationship

tStatistic():

This function calculates the t-statistic for correlation:

Mathematical Formula: t = r × √((n-2)/(1-r²))

Where r is the correlation coefficient and n is the sample size

What it measures:

How many standard errors the correlation is away from zero

Used to test the null hypothesis that the true correlation is zero

Interpretation:

Larger absolute t-values indicate stronger evidence against the null hypothesis

Generally, a t-value greater than 2 (in absolute terms) is considered statistically significant at the 95% confidence level

criticalT() and pValue():

These functions provide approximations for statistical significance testing:

criticalT():

Returns the critical t-value for a given degrees of freedom (df) and significance level

The critical value is the threshold that the t-statistic must exceed to be considered statistically significant

Uses approximations since Pine Script doesn't have built-in statistical distribution functions

pValue():

Estimates the p-value for a given t-statistic and degrees of freedom

The p-value is the probability of observing a correlation as strong as the one calculated, assuming the true correlation is zero

Smaller p-values indicate stronger evidence against the null hypothesis

Standard interpretation:

p < 0.01: Very strong evidence (marked with **)

p < 0.05: Strong evidence (marked with *)

p ≥ 0.05: Weak evidence, not statistically significant

stdev():

This function calculates the standard deviation of a dataset:

Mathematical Formula: σ = √(Σ(x-μ)²/(n-1))

Where x is each value, μ is the mean, and n is the sample size

What it measures:

The amount of variation or dispersion in a set of values

A low standard deviation indicates that the values tend to be close to the mean

A high standard deviation indicates that the values are spread out over a wider range

Why it matters for correlation:

Standard deviation is used in calculating the correlation coefficient

It also provides information about the volatility of each asset's returns

Comparing standard deviations helps understand the relative riskiness of the two assets.

3.Getting Price Data-

price1: The closing price of the primary asset (the chart you're viewing)

price2: The closing price of the secondary asset (the one you selected in the input parameters)

Returns are used instead of raw prices because:

Returns are typically stationary (mean and variance stay constant over time)

Returns normalize for price levels, allowing comparison between assets of different values

Returns represent what investors actually care about: percentage changes in value

4.Information Table-

Creates a table to display statistics

Only shows on the last bar to avoid performance issues

Positioned in the top right of the chart

Has 2 columns and 15 rows

Populating the Table

The script then populates the table with various statistics:

Header Row: "Metric" and "Value"

Sample Information: Sample size and return type

Pearson Correlation: Value, t-statistic, p-value, and significance

Spearman Correlation: Value, t-statistic, p-value, and significance

Rolling Correlation: Current value

Standard Deviations: For both assets

Interpretation: Text description of the correlation strength

The table uses color coding to highlight important information:

Green for significant positive results

Red for significant negative results

Yellow for borderline significance

Color-coded headers for each section

=> Practical Applications and Interpretation

How to Interpret the Results

Correlation Strength

0.0 to 0.3 (or 0.0 to -0.3): Weak or no correlation

The assets move mostly independently of each other

Good for diversification purposes

0.3 to 0.7 (or -0.3 to -0.7): Moderate correlation

The assets show some tendency to move together (or in opposite directions)

May be useful for certain trading strategies but not extremely reliable

0.7 to 1.0 (or -0.7 to -1.0): Strong correlation

The assets show a strong tendency to move together (or in opposite directions)

Can be useful for pairs trading, hedging, or as a market indicator

Statistical Significance

p < 0.01: Very strong evidence that the correlation is real

Marked with ** in the table

Very unlikely to be due to random chance

p < 0.05: Strong evidence that the correlation is real

Marked with * in the table

Unlikely to be due to random chance

p ≥ 0.05: Weak evidence that the correlation is real

Not marked in the table

Could easily be due to random chance

Rolling Correlation

The rolling correlation shows how the relationship between assets changes over time

If the rolling correlation is much different from the long-term correlation, it suggests the relationship is changing

This can indicate:

A shift in market regime

Changing fundamentals of one or both assets

Temporary market dislocations that might present trading opportunities

Trading Applications

1. Portfolio Diversification

Goal: Reduce overall portfolio risk by combining assets that don't move together

Strategy: Look for assets with low or negative correlations

Example: If you hold tech stocks, you might add some utilities or bonds that have low correlation with tech

2. Pairs Trading

Goal: Profit from the relative price movements of two correlated assets

Strategy:

Find two assets with strong historical correlation

When their prices diverge (one goes up while the other goes down)

Buy the underperforming asset and short the outperforming asset

Close the positions when they converge back to their normal relationship

Example: If Coca-Cola and Pepsi are highly correlated but Coca-Cola drops while Pepsi rises, you might buy Coca-Cola and short Pepsi

3. Hedging

Goal: Reduce risk by taking an offsetting position in a negatively correlated asset

Strategy: Find assets that tend to move in opposite directions

Example: If you hold a portfolio of stocks, you might buy some gold or government bonds that tend to rise when stocks fall

4. Market Analysis

Goal: Understand market dynamics and interrelationships

Strategy: Analyze correlations between different sectors or asset classes

Example:

If tech stocks and semiconductor stocks are highly correlated, movements in one might predict movements in the other

If the correlation between stocks and bonds changes, it might signal a shift in market expectations

5. Risk Management

Goal: Understand and manage portfolio risk

Strategy: Monitor correlations to identify when diversification benefits might be breaking down

Example: During market crises, many assets that normally have low correlations can become highly correlated (correlation convergence), reducing diversification benefits

Advanced Interpretation and Caveats

Correlation vs. Causation

Important Note: Correlation does not imply causation

Example: Ice cream sales and drowning incidents are correlated (both increase in summer), but one doesn't cause the other

Implication: Just because two assets move together doesn't mean one causes the other to move

Solution: Look for fundamental economic reasons why assets might be correlated

Non-Stationary Correlations

Problem: Correlations between assets can change over time

Causes:

Changing market conditions

Shifts in monetary policy

Structural changes in the economy

Changes in the underlying businesses

Solution: Use rolling correlations to monitor how relationships change over time

Outliers and Extreme Events

Problem: Extreme market events can distort correlation measurements

Example: During a market crash, many assets may move in the same direction regardless of their normal relationship

Solution:

Use Spearman correlation, which is less sensitive to outliers

Be cautious when interpreting correlations during extreme market conditions

Sample Size Considerations

Problem: Small sample sizes can produce unreliable correlation estimates

Rule of Thumb: Use at least 30 data points for a rough estimate, 60+ for more reliable results

Solution:

Use the default correlation length of 60 or higher

Be skeptical of correlations calculated with small samples

Timeframe Considerations

Problem: Correlations can vary across different timeframes

Example: Two assets might be positively correlated on a daily basis but negatively correlated on a weekly basis

Solution:

Test correlations on multiple timeframes

Use the timeframe that matches your trading horizon

Look-Ahead Bias

Problem: Using information that wouldn't have been available at the time of trading

Example: Calculating correlation using future data

Solution: This script avoids look-ahead bias by using only historical data

Best Practices for Using This Script

1. Appropriate Parameter Selection

Correlation Window:

For short-term trading: 20-50 periods

For medium-term analysis: 50-100 periods

For long-term analysis: 100-500 periods

Rolling Window:

Should be shorter than the main correlation window

Typically 1/3 to 1/2 of the main window

Return Type:

For most applications: Log Returns (better statistical properties)

For simplicity: Simple Returns (easier to interpret)

2. Validation and Testing

Out-of-Sample Testing:

Calculate correlations on one time period

Test if they hold in a different time period

Multiple Timeframes:

Check if correlations are consistent across different timeframes

Economic Rationale:

Ensure there's a logical reason why assets should be correlated

3. Monitoring and Maintenance

Regular Review:

Correlations can change, so review them regularly

Alerts:

Set up alerts for significant correlation changes

Documentation:

Keep notes on why certain assets are correlated and what might change that relationship

4. Integration with Other Analysis

Fundamental Analysis:

Combine correlation analysis with fundamental factors

Technical Analysis:

Use correlation analysis alongside technical indicators

Market Context:

Consider how market conditions might affect correlations

Conclusion

This Scientific Correlation Testing Framework provides a comprehensive tool for analyzing relationships between financial assets. By offering both Pearson and Spearman correlation methods, statistical significance testing, and rolling correlation analysis, it goes beyond simple correlation measures to provide deeper insights.

For beginners, this script might seem complex, but it's built on fundamental statistical concepts that become clearer with use. Start with the default settings and focus on interpreting the main correlation lines and the statistics table. As you become more comfortable, you can adjust the parameters and explore more advanced applications.

Remember that correlation analysis is just one tool in a trader's toolkit. It should be used in conjunction with other forms of analysis and with a clear understanding of its limitations. When used properly, it can provide valuable insights for portfolio construction, risk management, and pair trading strategy development.

Central Limit Theorem Reversion IndicatorDear TV community, let me introduce you to the first-ever Central Limit Theorem indicator on TradingView.

The Central Limit Theorem is used in statistics and it can be quite useful in quant trading and understanding market behaviors.

In short, the CLT states: "When you take repeated samples from any population and calculate their averages, those averages will form a normal (bell curve) distribution—no matter what the original data looks like."

In this CLT indicator, I use statistical theory to identify high-probability mean reversion opportunities in the markets. It calculates statistical confidence bands and z-scores to identify when price movements deviate significantly from their expected distribution, signaling potential reversion opportunities with quantifiable probability levels.

Mathematical Foundation

The Central Limit Theorem (CLT) says that when you average many data points together, those averages will form a predictable bell-curve pattern, even if the original data is completely random and unpredictable (which often is in the markets). This works no matter what you're measuring, and it gets more reliable as you use more data points.

Why using it for trading?

Individual price movements seem random and chaotic, but when we look at the average of many price movements, we can actually predict how they should behave statistically. This lets us spot when prices have moved "too far" from what's normal—and those extreme moves tend to snap back (mean reversion).

Key Formula:

Z = (X̄ - μ) / (σ / √n)

Where:

- X̄ = Sample mean (average return over n periods)

- μ = Population mean (long-term expected return)

- σ = Population standard deviation (volatility)

- n = Sample size

- σ/√n = Standard error of the mean

How I Apply CLT

Step 1: Calculate Returns

Measures how much price changed from one bar to the next (using logarithms for better statistical properties)

Step 2: Average Recent Returns

Takes the average of the last n returns (e.g., last 100 bars). This is your "sample mean."

Step 3: Find What's "Normal"

Looks at historical data to determine: a) What the typical average return should be (the long-term mean) and b) How volatile the market usually is (standard deviation)

Step 4: Calculate Standard Error

Determines how much sample averages naturally vary. Larger samples = smaller expected variation.

Step 5: Calculate Z-Score

Measures how unusual the current situation is.

Step 6: Draw Confidence Bands

Converts these statistical boundaries into actual price levels on your chart, showing where price is statistically expected to stay 95% and 99% of the time.

Interpretation & Usage

The Z-Score:

The z-score tells you how statistically unusual the current price deviation is:

|Z| < 1.0 → Normal behavior, no action

|Z| = 1.0 to 1.96 → Moderate deviation, watch closely

|Z| = 1.96 to 2.58 → Significant deviation (95%+), consider entry

|Z| > 2.58 → Extreme deviation (99%+), high probability setup

The Confidence Bands

- Upper Red Bands: 95% and 99% overbought zones → Expect mean reversion downward as the price is not likely to cross these lines.

- Center Gray Line: Statistical expectation (fair value)

- Lower Blue Bands: 95% and 99% oversold zones → Expect mean reversion upward

Trading Logic:

- When price exceeds the upper 95% band (z-score > +1.96), there's only a 5% probability this is random noise → Strong sell/short signal

- When price falls below the lower 95% band (z-score < -1.96), there's a 95% statistical expectation of upward reversion → Strong buy/long signal

Background Gradient

The background color provides real-time visual feedback:

- Blue shades: Oversold conditions, expect upward reversion

- Red shades: Overbought conditions, expect downward reversion

- Intensity: Darker colors indicate stronger statistical significance

Trading Strategy Examples

Hypothetically, this is how the indicator could be used:

- Long: Z-score < -1.96 (below 95% confidence band)

- Short: Z-score > +1.96 (above 95% confidence band)

- Take profit when price returns to center line (Z ≈ 0)

Input Parameters

Sample Size (n) - Default: 100

Lookback Period (m) - Default: 100

You can also create alerts based on the indicator.

Final notes:

- The indicator uses logarithmic returns for better statistical properties

- Converts statistical bands back to price space for practical use

- Adaptive volatility: Bands automatically widen in high volatility, narrow in low volatility

- No repainting: yay! All calculations use historical data only

Feedback is more than welcome!

Henri

Stablecoin Liquidity Delta (Aggregate Market Cap Flow)Hi All,

This indicator visualizes the bar-to-bar change in the aggregate market capitalization of major stablecoins, including USDT, USDC, DAI, and others. It serves as a proxy for monitoring on-chain liquidity and measuring capital inflows or outflows across the crypto market.

Stablecoins are the primary liquidity layer of the crypto economy. Their combined market capitalization acts as a mirror of the available fiat-denominated liquidity in digital markets:

🟩 An increase in the total stablecoin market capitalization indicates new issuance (capital entering the market).

🟥 A decrease reflects redemption or burning (liquidity exiting the system).

Tracking these flows helps anticipate macro-level liquidity trends that often lead overall market direction, providing context for broader price movements.

All values are derived from TradingView’s public CRYPTOCAP tickers, which represent the market capitalization of each stablecoin. While minor deviations can occur due to small price fluctuations around the $1 peg, these figures serve as a proxy for circulating supply and net issuance across the stablecoin ecosystem.

Continuation Probability (0–100)This indicator helps measure how likely the current candle trend will continue or reverse, giving a probability score between 0–100.

It combines multiple market factors trend, candle strength, volume, and volatility to create a single, intuitive signal.