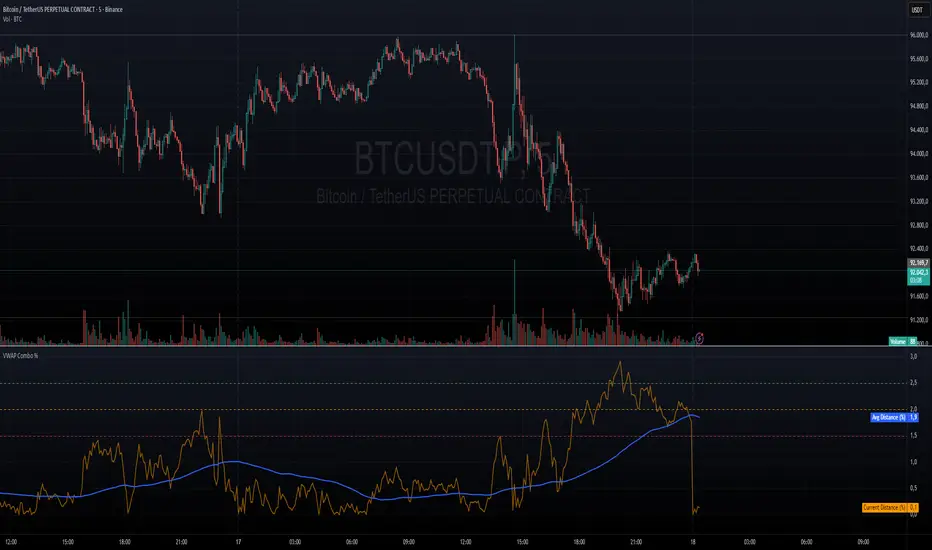

VWAP + VWAP Distance Avg + Alert Lines (%)VWAP Distance & Average Distance Indicator – Detailed Description

The VWAP + VWAP Distance Avg + Alert Lines (%) indicator is designed to measure the distance of the current price from the VWAP (Volume Weighted Average Price), as well as the average distance over a specified period. This tool is particularly useful for traders who use the VWAP as a magnet for price, helping to identify potential trend changes and areas where price may revert toward the VWAP.

Key Features

Current Distance (%)

Calculates the absolute percentage difference between the current price and the VWAP

This line shows how far the price has moved away from the VWAP at any given moment.

Average Distance (%)

Calculates a simple moving average (SMA) of the distance over a specified lookback period.

This provides a reference for typical price deviations from the VWAP, helping traders assess whether the current distance is unusually high or low.

Alert Lines (%)

Allows up to three customizable horizontal alert lines, which can be turned on or off individually.

Each line can be configured with:

Value in percent.

Color.

Line thickness.

These lines serve as visual thresholds, helping traders detect extreme deviations from the VWAP that may precede trend reversals.

Use Case – Detecting Potential Trend Changes

Traders often treat the VWAP as a price magnet, where price tends to revert after significant deviations.

When the current distance exceeds typical average levels or crosses an alert line, it can signal that the price may revert toward the VWAP, potentially indicating a shift in trend or a high-probability mean-reversion scenario.

Disclaimer

This indicator is provided for educational and analytical purposes only. It does not constitute financial advice, and trading decisions are always the sole responsibility of the individual trader. Users should carefully evaluate market conditions and their own risk tolerance before taking any trade.

Better used with VWAP on chart , and be careful around the end of session, for now this works just for session...

still improving on this....

التقلب

Swing Wicks + Bodies; Stolen from LeviathanSwing Wicks + Bodies — Stolen from Leviathan

This indicator automatically detects swing highs and lows by separating wick swings from body swings, providing a precise view of liquidity zones on the chart.

It draws:

• wick-based swing levels

• body-based swing levels

• dynamic liquidity boxes showing unfilled price zones

• touch counters (T1, T2, T3…)

• optional HTF levels (H1/H4…) for multi-timeframe context

Included features:

• hide filled levels

• keep only the most recent unfilled levels

• full customization (colors, line styles, text size, minimum box height)

• optional “extend until filled” mode

• volume threshold filter

• lookback limitation (history in days)

ATR or % Based Trailing Stop for Delta Exchange (trade_crush)This indicator calculates and visually displays a dynamic trailing stop line on the chart based on either the Average True Range (ATR) or a fixed percentage of the current close price. Designed especially for futures or crypto traders using Delta Exchange, it helps determine where to place trailing stop loss orders to manage risk effectively.

DCA Bot v7 - Cryptosa Nostra 1.0Technical Overview: Adaptive RSI DCA Bot

This is a sophisticated DCA (Dollar Cost Averaging) indicator designed for accumulating assets and managing portfolio distribution. It does not trade on simple RSI crosses. Instead, it combines multi-zone RSI analysis with ATR-based volatility triggers to execute staggered, dynamically-sized trades.

Its core feature is a "learning" engine that adapts its own settings over time. This "brain" can be trained on historical data and then applied to your real-time portfolio holdings via a "Live Override" feature.

Core Logic: How It Works

A trade is only executed when two conditions are met simultaneously:

The RSI Condition: The RSI must be inside one of the four pre-defined zones.

The Price Condition: The price must cross a "trigger line" (the green or red line) that is dynamically calculated based on volatility.

1. The Four RSI Zones

This script uses four distinct zones to determine the intent to trade:

Deep Buy Zone (Default: RSI <= 35 & Downtrend): This is the primary "value" buy signal. It only activates if the RSI is deeply oversold and the price is below the 200-period Trend MA.

Reload Buy Zone (Default: RSI 40-50 & Uptrend): This is a "buy the dip" signal. It looks for minor pullbacks during an established uptrend (price above the 200-period Trend MA).

Profit-Taking Zone (Default: RSI 70-80): Triggers a standard, small sell when the market is overbought.

Euphoria Zone (Default: RSI >= 80): Triggers a larger, more aggressive sell during extreme "blow-off" tops.

2. Dynamic Trade Sizing

The amount to buy or sell is not fixed. It scales dynamically based on how high or low the RSI is:

Buy Sizing: Spends a higher percentage of available cash when RSI is at its lowest (e.g., 35) and a smaller percentage when it's at the top of the reload zone (e.g., 50).

Sell Sizing: Sells a smaller percentage of holdings when RSI just enters the overbought zone (e.g., 70) and a much larger percentage when it's in the euphoria zone (e.g., 80+).

3. The "Adaptive Brain" (ATR Multipliers)

This is the script's learning mechanism. The green/red trigger lines are calculated as: Last Trade Price +/- (ATR * Multiplier).

This "Multiplier" is the brain. It adapts based on trade performance.

After a successful trade (as defined by profit_target_multiplier), the bot gets more confident and reduces the multiplier. This places the next trigger line closer to the price, making it more aggressive.

After a losing trade (as defined by loss_limit_multiplier), the bot gets more cautious and increases the multiplier. This places the next trigger line further away, making it more patient.

How to Use This Indicator

This script is designed to be "trained" on historical data to provide relevant signals for today.

To Train the Brain: In the settings, go to "1. Backtest Settings". Set the "Start Date (For Learning)" to a date in the past (e.g., 6 months or 1 year ago). The script will run a simulation from that date, allowing its Adaptive Multipliers (the "brain") to adjust to the market's volatility.

To See Live Signals: In "2. Live Portfolio Override", check the box "Override Backtest Balance?" and enter your real current coin and USD holdings.

Result: The "Live Status" table (top-right) will now display signals from the trained brain but will calculate the "Potential Buy %" and "Potential Sell %" based on your real portfolio. The "Buy Multi" and "Sell Multi" fields show you the brain's current learned values.

Daily ATR vs Move (black & white) + PipsTop of Chart, Mid. Gives the user an idea of what trend is doing and how the current price compares to daily ATR.

Used on this example below to indicate we are within the bottom range for the day, and price has potential to move up without worry of exhaustion.

Bollinger Bands Regression Forecast [BigBeluga]🔵 OVERVIEW

The Bollinger Bands Regression Forecast combines volatility envelopes from Bollinger Bands with a linear regression-based projection model .

It visualizes both current and future price zones by extrapolating the Bollinger channel forward in time, giving traders a statistical forecast of probable support and resistance behavior.

🔵 CONCEPTS

Classic Bollinger Bands use a moving average (basis) and standard deviation (deviation) to form dynamic envelopes around price.

This indicator enhances them with linear regression slope detection , allowing it to forecast how the band may expand or contract in the future.

Regression is applied to both the band’s basis and deviation components to predict their trajectory for a user-defined number of Forecast Bars .

The resulting forecast creates a smoothed, funnel-shaped projection that dynamically adapts to volatility.

▲ and ▼ markers highlight potential mean reversion points when price crosses the outer bounds of the bands.

🔵 FEATURES

Forecast Engine : Uses linear regression to project Bollinger Band movement into the future.

Dynamic Channel Width : Adapts standard deviation and slope for realistic volatility modeling.

Auto-Labeled Levels : Displays live upper and lower forecast values for quick reference.

Cross Signals : Marks potential overbought and oversold zones with ▲/▼ signals when price exits the band.

Trend-Adaptive Basis Color : Basis line automatically switches color to represent short-term trend direction.

Customizable Colors and Widths for complete visual control.

🔵 HOW TO USE

Apply the indicator to visualize both current Bollinger structure and its forward projection.

Use ▲/▼ breakout markers to identify short-term reversals or volatility shifts.

When price consistently rides the upper band forecast, the trend is strong and likely continuing.

When regression shows narrowing bands ahead, expect a volatility contraction or consolidation period.

For range traders, outer projected bands can be used as potential mean reversion entry points .

Combine with volume or momentum filters to confirm whether breakouts are genuine or fading.

🔵 CONCLUSION

Bollinger Bands Regression Forecast transforms classic Bollinger analysis into a predictive forecasting model .

By merging volatility dynamics with regression-based extrapolation, it provides traders with a forward-looking visualization of likely price boundaries — revealing not only where volatility is but also where it’s heading next.

2-Stage Dashboard (SQZPRO Wide + EMA)Dashboard for Darvas Box EMA momentum traders, located in the bottom right, mostly for quickly screening if a setup is viable.

- EMAs are 9 & 21

- SQZPRO set to wide squeezes

Long setup:

- Green SQZPRO row

- Green EMA row

Short setup:

- Green SQZPRO row

- Red EMA row

Price Drop CounterThe Price Drop Counter is a very basic statistical indicator.

See it as an analytical tool that tracks how many times an asset's price has dropped by a specified percentage from its recent peak within a defined date range.

The indicator monitors the highest price reached and counts each occurrence when the price falls by your chosen threshold, then resets its peak tracking point after each drop is registered.

Uses

Volatility Assessment: Measure how frequently significant price corrections occur during specific periods

Market Behavior Analysis: Compare drop frequency across different timeframes or market conditions

Risk Evaluation: Identify assets or periods with higher downside volatility

Historical Pattern Recognition: Study how often major pullbacks happened during bull or bear markets

Backtesting Support: Analyze how your strategy would perform based on the frequency of drawdowns

How to use it

Add the indicator to your TradingView chart

Configure the Percent Drop (%) to define your threshold (default: 10%). The indicator will count each time price falls by this percentage from the most recent high

IMPORTANT Set your Start Date and End Date to analyze a specific period of interest

The blue step-line plot shows the cumulative count of drops within your date range

Adjust the percentage threshold based on your analysis needs - use smaller values (2-5%) for more frequent signals or larger values (15-20%) for major corrections only

The counter resets its high-water mark after each qualifying drop, allowing it to track multiple sequential drops within the same period.

ZFX Prime Trend Matrix PRO – Zumiko FX📌 ZFX Prime Trend Matrix PRO – Zumiko FX

ZFX Prime Trend Matrix PRO is a multi-timeframe trend dashboard designed by Zumiko FX to give traders an instant, complete market overview.

It analyzes six key timeframes simultaneously and displays trend direction, band positioning, momentum, volatility and alignment — all in one clean, horizontal table.

This matrix is made to simplify decision-making and help traders instantly identify when multiple timeframes agree on a market direction.

🔹 What the Matrix Shows

The dashboard updates in real time and displays:

1. Trend Direction

UP / DOWN / Neutral for each timeframe (M1, M5, M15, H1, H4, D1).

2. Bands Position (Prime Bands)

Shows whether price is:

Above Fast Band

Below Fast Band

Above Slow Band

Below Slow Band

Inside range

Perfect for spotting breakouts and trend continuation zones.

3. RSI (Momentum Strength)

Color-coded RSI readings help detect overbought/oversold and neutral momentum.

4. Stochastic (Timing Tool)

Reads market timing with Stoch K/D movements.

Highlights when a trend aligns with momentum.

5. ATR Bias

Instant view of volatility pressure:

LONG

SHORT

Neutral

Great for filtering entries.

6. HTF Alignment

Shows whether each timeframe is aligned with the next higher timeframe.

A powerful trend continuation filter used by advanced traders.

7. Trading Signal Zone

Final synthesised signal:

BUY ZONE → Strong bullish alignment

SELL ZONE → Strong bearish alignment

NO TRADE → Conditions not optimal

This allows traders to quickly identify “green light” moments across the trend structure.

🔹 Why This Matrix Is Powerful

✔ Shows 6 timeframes at once

✔ Helps confirm entries from other indicators

✔ Reveals hidden contradictions in trend

✔ Perfect for scalpers and day traders who need fast confirmation

✔ Works with any strategy as a high-level filter

✔ Clean, minimalistic, professional UI

🔹 Who Is It For?

Scalpers

Day traders

Swing traders

Traders using trend-following strategies

Traders who want a clean, high-level overview

🔹 About Zumiko FX

Developed by Zumiko FX, known for precision-based systems and advanced multi-timeframe tools for serious traders.

ATR Risk Display - Multi FuturesWhat This Does

I got tired of manually calculating my ATR stops and risk for different futures contracts, especially when switching between ES, NQ, and their micro versions. This indicator automatically detects what futures symbol you're trading and shows you the exact tick count and dollar risk for your stop loss.

The Problem It Solves

If you trade futures with ATR-based stops, you know the hassle:

Different contracts have different tick values

You need to calculate position risk in dollars

Switching between symbols means redoing all the math

Renko charts make it even more confusing since ATR needs to come from regular candles

This handles all of that automatically.

Key Features

Auto-detects futures symbols - ES, NQ, YM, RTY, GC, CL, and all the micros (MES, MNQ, etc.)

Shows everything you need in one line: ATR(timeframe) × multiplier = X ticks ($XXX)

Works on Renko charts - pulls ATR from regular timeframe charts (super important if you use Renko)

Adjustable position sizing - set your contract count and see total risk instantly

Clean, minimal display - just the info you need, no clutter

How to Use

Add it to any futures chart

Set your preferred ATR timeframe (I use 5-minute)

Set your ATR multiplier (I use 1.5x for my stops)

Set your contract size

That's it - the indicator handles the rest

The display will show something like: "ES ATR(5) × 1.5 = 12 ticks ($150)"

Settings Explained

ATR Timeframe: What timeframe to calculate ATR from (always uses regular candles, even on Renko)

ATR Multiplier: How many ATRs for your stop (1.5 is common, 2.0 for wider stops)

Number of Contracts: Your position size for risk calculation

Auto-Detect Symbol: Leave on unless you want to manually override

Supported Futures

Full size: ES, NQ, YM, RTY, GC, CL, ZB, ZN, 6E, 6J

Micros: MES, MNQ, MYM, M2K, MGC, MCL

Notes

Made this primarily for my own ES trading but figured others might find it useful

The tick values are based on standard CME specs

If you trade other futures, you can modify the code to add them

Works great alongside level indicators for risk management

Why This Exists

I use ATR trailing stops on all my trades and got tired of doing mental math every time I switched between charts or contracts. Especially useful if you trade both full-size and micro contracts - the risk difference is huge and easy to mess up.

Hope this helps your trading! Feel free to suggest improvements.

Turtle 20-Day Breakout (Donchian)Yes, the most important indicator used in the Turtle Rules (Turtle Trading Strategy) for finding breakouts above previous highs is the Donchian Channel. 🐢📈

Donchian Channel

The Donchian Channel is a trend-following indicator composed of three lines plotted on the chart:

Shutterstock

Upper Band: The highest high over the defined number of periods.

Lower Band: The lowest low over the defined number of periods.

Middle Line: The average of the Upper and Lower bands (not always used, but sometimes added for orientation).

The Turtle Rules use the following periods for the entry signals (breakouts) you mentioned in your query:

Short-Term (System 1): Crossing the 20-day high (this corresponds to the upper band of a Donchian Channel with a 20-period setting).

Mid-Term/Long-Term (System 2): Crossing the 55-day high (this corresponds to the upper band of a Donchian Channel with a 55-period setting).

Crossing the upper band signals a breakout and serves as the buy signal for a long position (for short positions, crossing below the lower band is used).

Is there anything else I can translate for you, or would you like me to elaborate on the Average True Range (ATR), the other key indicator used by the Turtles?

Session Range Boxes GR v2.1This indicator draws intraday range boxes for the main Forex sessions based on Europe/Budapest time (CET/CEST).

Tracked sessions (Budapest time):

Asia: 01:00 – 08:00

Frankfurt (pre-London): 08:00 – 09:00

London: 09:00 – 18:00

New York: 14:30 – 23:00

For each session, the script:

Detects the session start and session end using the current chart timeframe and the Europe/Budapest time zone.

Tracks the high and low of price during the session.

Draws a colored box from session open to session close, covering the full price range between the session high and low.

Draws a white midline inside every box at the midpoint between the session high and low (and keeps it visible for all past sessions).

Optionally plots a small label (“Asia”, “Fra”, “London”, “NY”) above the first bar of each session.

Color scheme:

Asia: soft orange box

Frankfurt: light aqua box

London: darker blue box

New York: light lime box

Use this tool to:

Quickly see which session created the high or low of the day,

Highlight important liquidity zones and prior session ranges that price may revisit,

Visually separate Asia, Frankfurt, London and New York volatility profiles on intraday charts.

Optimized for intraday trading (Forex / indices), but it works on any symbol where session behavior and time-of-day structure matter.

Session Range Boxes (Budapest time) GR V2.0Session Range Boxes (Budapest time)

This indicator draws intraday range boxes for the main Forex sessions based on Europe/Budapest time (CET/CEST).

Tracked sessions (Budapest time):

Asia: 01:00 – 08:00

Frankfurt (pre-London): 08:00 – 09:00

London: 09:00 – 18:00

New York: 14:30 – 23:00

For each session, the script:

Detects the session start and session end using the current chart timeframe and the Europe/Budapest time zone.

Tracks the high and low of price during the entire session.

Draws a box (rectangle) from session open to session close, covering the full price range between session high and low.

Optionally prints a small label above the first bar of each session (Asia, Fra, London, NY).

Color scheme:

Asia: soft orange box

Frankfurt: light aqua box

London: darker blue box

New York: light lime box

Use this tool to:

Quickly see which session created the high/low of the day,

Identify liquidity zones and session ranges that price may revisit,

Visually separate Asia, Frankfurt, London and New York volatility on intraday charts.

Optimized for intraday trading (Forex / indices), but it works on any symbol where session behavior matters.

Average True Range with MAKey features

ATR calculation: true range (ta.tr(true)) is smoothed using a selectable method to produce the ATR.

ATR smoothing options: RMA, SMA, EMA, or WMA for the ATR calculation.

MA-on-ATR: a separate moving average computed on the ATR values with its own length and smoothing method.

Display controls: toggles to show/hide the ATR and the ATR MA independently.

Appearance controls: separate color inputs for the ATR and the ATR MA, and a thicker line for the MA (linewidth=2).

Inputs

ATR Length (default 14): length used to smooth true range into the ATR.

ATR Smoothing (default RMA): smoothing method applied to the true range to form ATR.

MA Length (on ATR) (default 14): length for the moving average applied to the ATR series.

MA Smoothing (default SMA): smoothing method used for the MA applied to ATR.

Show ATR / Show ATR MA: booleans to toggle visibility.

ATR Color / ATR MA Color: choose plot colors.

How to interpret

ATR line: shows current volatility (average true range). Rising ATR indicates increasing volatility; falling ATR indicates decreasing volatility.

ATR MA line: smooths the ATR to reveal trend direction and reduce noise.

Use crossovers: ATR crossing above its MA may signal volatility is picking up; ATR crossing below its MA suggests volatility is subsiding.

Combine with price action or other indicators (e.g., breakout systems, position sizing rules) to make decisions based on volatility regime.

XAUUSD Pro Setup Suite manuel_lnt.fx is an advanced Pine Script v6 indicator designed exclusively for XAUUSD, built to automatically detect the 5 highest-probability setups in gold day trading.

It combines institutional price action, volatility patterns, mean reversion logic, and momentum confirmation to generate clean, filtered, and actionable signals.

The indicator automatically detects:

⸻

1️⃣ Break & Retest Premium (BR)

Identifies valid breaks of key levels and signals the retest with rejection wick, EMA20 trend confirmation, and neutral RSI.

→ Excellent for trend continuation.

⸻

2️⃣ Fakeout Liquidity Trap (FO)

Detects liquidity grabs above highs or below lows with an opposite close + engulfing candle confirmation.

→ The strongest setup for fast and explosive reversals on gold.

⸻

3️⃣ MACD Zero-Line Shift (MACD)

Signals when the MACD crosses the zero line while price breaks micro-structure.

→ Perfect for spotting the start of a new trend.

⸻

4️⃣ Bollinger Squeeze → Breakout (BB)

Recognizes volatility compression and signals when a breakout is likely to explode.

→ Ideal for clean breakout trades.

⸻

5️⃣ Mean Reversion on EMA50 (MR)

Highlights price extensions far away from the EMA50 with ATR confirmation and a reversal candle.

→ Great for pullbacks back toward the mean value.

orb cody hoskinscody orb designed a 15 min range orb indicator for people to use dur8ng market open in asian and new york

ORB + INMERELO ADR + ATRThis indicator provides **two completely different but complementary lines of information** for intraday traders:

# **1. The ORB Line (ADR-Based Context Line)**

The ORB portion of the script focuses on **range expansion** relative to typical daily behavior.

### **What it measures**

* **20-day ADR (Average Daily Range)**

* **Today’s range as a % of ADR**

* **How much of the average range has been “used”** by the time you’re considering an Opening Range Breakout

### **Why it matters for ORB trading**

Successful ORBs thrive when:

* **ADR used% is low** (green) → plenty of fuel left for expansion

* **ADR used% is moderate** (orange) → breakout still possible but less explosive

* **ADR used% is high** (red) → breakout attempts often fail or reverse

### **What the indicator gives you**

A clean, color-coded readout of:

* ADR

* Today’s range

* Used%

* A simple green/orange/red evaluation of ORB quality

This allows a trader to quickly judge whether **conditions favor ORB continuation or mean-reversion reversal**—without manually calculating ranges or switching charts.

---

# **2. The INMERELO Line (ATR Stretch + MA Interaction)**

The INMERELO portion of the script is built around **mean-reversion mechanics**:

the market tends to revert back toward the **first daily MA it crosses under**.

### **How it determines the active MA**

At the start of each session, the script waits for price to cross under:

* **EMA10**

* **EMA21**

* **SMA50**

Whichever MA is crossed first becomes the **active MA** for the day.

If no cross has occurred yet, the indicator shows the **nearest MA**, so traders know exactly what the likely “INMERELO magnet” will be.

### **What it measures**

* **Stretch from the active MA (in ATR units)**

* **20-day ATR regime direction (expanding or contracting)**

* **Daily MA context: E10, E21, or S50**

### **Why it matters for INMERELOs**

This provides:

* The **target MA**

* The **distance to that MA in ATRs**

* A color-coded stretch score:

* **0.6–1.2 ATR** → prime INMERELO zone (Green)

* Moderately stretched → Orange

* Overstretched or dead zone → Red

An up/down arrow shows whether **volatility is expanding or compressing**, which affects expected retrace behavior.

### **What the indicator gives you**

All INMERELO data is displayed in a second compact line:

* Stretch to MA

* Active MA label (E10/E21/S50)

* ATR regime arrow

This allows fast identification of high-probability **mean-reversion trades back to the MA**.

---

# **Summary**

This indicator shows:

### **Line 1 → ORB Context (ADR)**

* Is the stock setup for a powerful breakout?

* How much ADR is left?

* Are you early (good) or late (risky)?

### **Line 2 → INMERELO Context (ATR + MA Stretch)**

* Which MA is in control today (EMA10, EMA21, or SMA50)?

* How many ATRs away from that MA are we?

* Is volatility expanding or contracting?

* Is this a clean INMERELO setup or not?

Together, these two lines give traders the **two most important intraday lenses**:

**range expansion (ORB)** and **mean reversion (INMERELO)**—updated every bar, without clutter.

VWAP D/W/M + MA100 & EMA100 albanThis TradingView indicator displays three independent VWAPs (Volume Weighted Average Prices) along with MA100 (Simple Moving Average) and EMA100 (Exponential Moving Average) on the chart.

Key Features:

VWAP #1, VWAP #2, VWAP #3: Each VWAP can be configured independently with:

Source (hlc3, close, etc.)

Anchor period (Session, Week, Month, Quarter, Year, Decade, Century, Earnings, Dividends, Splits)

Offset

Option to hide on daily or higher timeframes

MA100: 100-period Simple Moving Average

EMA100: 100-period Exponential Moving Average

Purpose:

This script is ideal for traders who want to track multiple VWAP levels simultaneously while also monitoring the 100-period moving averages for trend analysis. It provides a clean setup without bands or fills, focusing solely on price averages.

Use Cases:

Identify intraday or multi-timeframe VWAP levels

Combine VWAP levels with MA100/EMA100 for support/resistance analysis

Analyze trend direction and momentum using moving averages

Long Term indicator for financial marketsIts the indicator that i have made for my friends following the learnings which i have learnt over the last few years for momentum traders

GEX / Gamma - SPX Indicator Description – GEX / Gamma (SPX)

This indicator allows you to manually plot your daily +GEX, TRANS-GEX, and –GEX levels on SPX and visualize how price reacts around key gamma zones.

You enter the three levels each morning, and the script automatically draws:

+GEX / TRANS / –GEX zones with an adjustable buffer

Clean labels (e.g., “+GEX: 6850”) pinned to the right side of the chart

Today-only candle coloring (green above TRANS-GEX, red below)

Zones extend from yesterday’s session through the current session, helping highlight areas where dealer hedging flows may influence volatility, compression, or acceleration.

How to Use

Add the indicator to any intraday SPX chart.

Open settings and enter your +GEX, TRANS-GEX, and –GEX levels for the day.

Adjust the buffer, colors, and label style as needed.

Watch how price behaves as it moves above or below TRANS-GEX and interacts with +/- GEX zones.

Best For

Intraday SPX / ES / SPY

Options traders

Volatility and gamma-aware strategies

Strategy Behind It (Tight Version)

GEX levels help identify where dealer hedging flows can influence SPX price behavior.

+GEX (Positive Gamma)

Market tends to stabilize here. Dealers hedge against price moves, creating mean-reversion and lower volatility.

TRANS-GEX (Transition Level)

Key pivot where gamma flips. Price crossing this level often signals a shift in volatility or intraday direction.

–GEX (Negative Gamma)

Market becomes more reactive. Dealers hedge with price, increasing volatility, momentum, and trend potential.

How traders use it:

Expect resistance or slowdown into +GEX

Watch for potential bottoming or increased volatility –GEX

Use TRANS-GEX as a bias line or trigger for intraday shifts

A move outside of either the +GEX or -GEX will likely result in some type of high volume move.