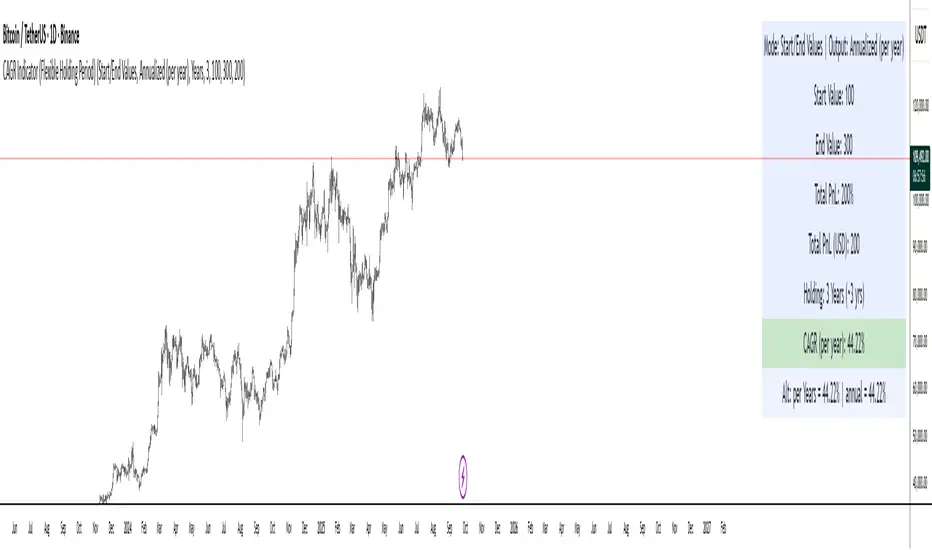

CAGR Indicator (Flexible Holding Period)CAGR Indicator (Flexible Holding Period)

The CAGR Indicator (Flexible Holding Period) is designed to convert any cumulative investment outcome into a standardized, annualized growth rate that can be compared across assets, strategies, and time horizons. Its core metric is the compound annual growth rate, which represents the constant yearly rate that, if compounded smoothly, transforms an initial value into a final value over a specified horizon. By annualizing returns, the indicator removes distortions caused by unequal test lengths and allows direct comparison with benchmarks such as index returns or risk-free rates.

Conceptually, the indicator proceeds in two stages: measuring growth and normalizing time. Growth is summarized by the growth multiple, which is the ratio of ending value to starting value when concrete values are provided, or equivalently 1 plus total percentage return divided by 100 when only a cumulative percent is known. Time is normalized by converting the user’s holding period into a year-equivalent, so that a 45-day, 30-week, 18-month, or multi-year interval can all be mapped onto a common annual scale. The conversions use widely accepted approximations: days divided by 365.25, weeks divided by approximately 52.1429, and months divided by 12, while years are used as entered.

Once growth and time are expressed in compatible units, the indicator applies the standard compounding identity: CAGR = (Growth Multiple)^(1/T) − 1, where T is the year-equivalent holding period. This transformation inverts the compounding process and yields the geometric mean rate of return per year. Because the geometric mean is path-independent, the CAGR summarizes start-to-finish performance without reference to the sequence of gains and losses. The output therefore reflects the constant annual rate that would have produced the observed terminal value from the initial value if returns had been smooth.

The indicator admits two data entry modes to accommodate common reporting practices. In Start/End Values mode, the user supplies initial and final portfolio values; the indicator computes the growth multiple as end divided by start and also displays absolute profit or loss in currency terms to aid practical interpretation. In Total PnL (%) mode, the user supplies a cumulative return percentage; the indicator converts this to a growth multiple and estimates a corresponding ending value for display, while the CAGR computation itself relies only on the multiple and the time horizon.

Validity checks ensure that reported numbers are meaningful. The growth multiple must be strictly positive; cumulative losses at or below minus one hundred percent make the multiple nonpositive and render the CAGR undefined. The holding period must be positive and convertible to a year-equivalent. In Start/End mode, the starting value must exceed zero to avoid division by zero and degenerate ratios. When these conditions are not met, the indicator withholds a numeric result and signals that the quantity is not well defined.

Interpreting the output requires recognizing both its strengths and its limits. The CAGR is a concise, comparable measure of long-run performance that abstracts from timing and volatility. It is particularly useful for benchmarking strategies of different durations, setting policy targets for funds, communicating results to stakeholders, and aligning outcomes with hurdle rates. However, because it is path-independent, the CAGR does not reflect interim drawdowns, variance, or tail risk. It also presumes a lump-sum investment with no intermediate cash flows; when deposits or withdrawals occur, internal rate of return methods such as IRR or XIRR are more appropriate.

Typical applications include comparing backtests with unequal sample lengths, reporting consolidated results from discrete projects on a common annual basis, and translating short-horizon event outcomes (for example, a multi-week campaign) into an annualized figure for decision-making. The indicator’s auxiliary displays, such as total profit or loss in currency and the explicit statement of the original holding period alongside its year-equivalent, improve transparency and auditability of the transformation.

Users should remain mindful of several caveats. Time conversions rely on conventional averages and may differ from calendar-exact counts by small amounts, which is usually immaterial but worth noting for edge cases. Selection bias can inflate reported CAGRs if intervals are cherry-picked; robust practice involves rolling windows, out-of-sample tests, and sensitivity analysis. Most importantly, the CAGR should be paired with risk and stability measures—such as maximum drawdown, Sharpe or Sortino ratios, downside deviation, or ulcer index—to form a complete assessment of a strategy’s quality.

In sum, the indicator operationalizes a simple but powerful idea: separate the measurement of growth from the normalization of time, then apply the compounding identity to express outcomes as a consistent per-year rate. By combining flexible period inputs with a rigorous geometric transformation, it enables fair, intelligible comparisons while encouraging the complementary use of risk diagnostics to avoid over-reliance on a single summary statistic.

Statistics

Mag 7 Weighted Performance % (Today Only)shows the cumulative weighted performance of mag 7 stocks as a percentage.

Stock Valuation Models - Professional Investment Analysis Tool📊 Overview

Stock Valuation Models is a comprehensive financial analysis indicator that combines multiple valuation methodologies to calculate intrinsic stock value. This professional-grade tool implements 7 different valuation methods , risk assessment framework, and financial health metrics to provide data-driven investment decisions.

🎯 Key Features

📈 Multiple Valuation Methods

Graham's Valuation - Conservative asset-based approach by Benjamin Graham

Multiples Valuation - Market-based P/E and P/B ratios from sector peers

Discounted Cash Flow (DCF) - Future cash flow projections with present value calculation

Dividend Discount Model - Gordon Growth Model for dividend-paying stocks

FCFF Model - Enterprise-level Free Cash Flow to Firm analysis

EVA Model - Economic Value Added measurement above cost of capital

Advanced Multiples - Enterprise Value ratios (EV/EBITDA, EV/Sales)

🏥 Financial Health Metrics

Altman Z-Score - Bankruptcy prediction and financial distress assessment

Piotroski F-Score - 9-point fundamental strength evaluation

Beneish M-Score - Earnings manipulation detection system

Magic Formula - Joel Greenblatt's combined quality and value scoring

⚖️ Risk Assessment Framework

Multi-Factor Risk Scoring - Fundamental, market, quality, and data quality risks

Risk-Adjusted Margin of Safety - Dynamic safety thresholds based on risk level

Position Sizing Guidance - Risk-appropriate investment allocation recommendations

🔍 Data Quality System

Real-Time Quality Tracking - Visual warnings for insufficient data

Fallback Methodology - Alternative calculations when primary data unavailable

Confidence Scoring - Method agreement and data quality assessment

⚙️ Settings & Parameters

Main Settings

Margin of Safety (%) - Minimum discount required before buying (Default: 15%)

Table Font Size - Choose between "Small" and "Normal" text size

Valuation Methods

Graham's Valuation - Best for mature, stable companies with strong fundamentals

Multiples Valuation - Compares to industry peers using dynamic sector ratios

Discounted Cash Flow - Ideal for growth companies with predictable cash flows

Dividend Discount Model - For consistent dividend-paying stocks (disabled by default)

FCFF Model - Enterprise approach for leveraged companies and M&A analysis

EVA Model - Measures value creation above cost of capital

Advanced Multiples - Wall Street standard EV ratios for professional analysis

Additional Metrics

Magic Formula - Combined quality and value scoring system

Altman Z-Score - Bankruptcy risk assessment (Safe >2.99, Distress <1.81)

Piotroski F-Score - Fundamental quality score (Excellent ≥8, Poor <4)

Beneish M-Score - Manipulation detector (High Risk >-2.22, Low Risk ≤-2.22)

🔧 How It Works

Dynamic Calculations

Sector-Based Ratios - Automatically detects company sector and applies appropriate valuation multiples

Economic Integration - Uses real-time risk-free rates, VIX volatility, and GDP growth data

Quality Weighting - Adjusts method weights based on company type (growth/mature/distressed) and market conditions

Negative Value Handling - Shows actual calculated values but excludes negative results from weighted average

Risk-Adjusted Analysis

VIX Integration - Higher market volatility increases required margin of safety

Sector Risk Premiums - Energy and Financial sectors get higher risk multipliers

Quality Adjustments - High Piotroski F-Score companies get lower risk ratings

Data Quality Impact - Insufficient data increases risk score and safety requirements

Visual Display

Horizontal Table Layout - Organized by method groups (Valuation → Results → Risk → Health)

Color-Coded Results - Green/Yellow/Red indicators for risk levels and recommendations

Warning Symbols - ⚠️ for data quality issues, ❌ for excluded negative values

Dollar Amounts - Both percentage and dollar-based margin of safety calculations

📈 Interpretation Guide

💎 Intrinsic Value Results

Weighted Average - Combines all enabled methods based on intelligent weighting

Confidence Level - High/Medium/Low based on method agreement and data quality

Method Count - Number of successful valuation calculations

🎯 Margin of Safety

Percentage - Current discount/premium to calculated intrinsic value

Dollar Amount - Absolute dollar difference per share

Buy Price - Risk-adjusted target purchase price

⚖️ Risk Assessment

Low Risk (Green) - Normal position sizing (3-5%)

Medium Risk (Yellow) - Reduced position sizing (1-3%)

High Risk (Red) - Minimal position sizing (<1%)

📊 Recommendations

STRONG BUY - Low risk + adequate margin + high confidence

BUY - Meets risk-adjusted margin requirements

HOLD - Positive margin but higher risk

SELL - Insufficient margin for risk level

🎓 Educational Tooltips

Every parameter includes detailed explanations accessible by hovering over the setting. Learn about:

When to use each valuation method

How different metrics are calculated

Interpretation thresholds and ratings

Risk factors and quality indicators

💡 Best Practices

🚀 For Growth Stocks

Enable DCF and Advanced Multiples

Focus on Piotroski F-Score for quality assessment

Use higher margin of safety due to volatility

💰 For Value Stocks

Enable Graham's and Multiples Valuation

Check Altman Z-Score for financial stability

Consider Magic Formula rating

📈 For Dividend Stocks

Enable Dividend Discount Model

Focus on sustainable dividend coverage

Check for consistent dividend history

⚠️ For Distressed Situations

Prioritize Graham's asset-based approach

Monitor Altman Z-Score closely

Use higher risk-adjusted margins

⚠️ Important Notes & Data Limitations

📅 Data Timing Considerations

Fundamental Data Lag - Company financial data (earnings, cash flows, balance sheet items) may be 1-3 months behind current market conditions

Quarterly Reporting Delays - Most recent available data reflects the company's situation as of the last filed quarterly/annual report

Market vs. Fundamentals Gap - Stock prices react instantly to news, while fundamental data updates occur periodically

Accuracy Impact - Recent business changes, market events, or company developments may not be reflected in current calculations

🔧 Technical Limitations

Data Dependencies - Requires fundamental data availability from TradingView

Quality Warnings - Pay attention to ⚠️ symbols indicating insufficient data

Risk Context - Always consider risk score in investment decisions

Market Conditions - Tool automatically adjusts for market volatility (VIX)

Sector Specificity - Ratios automatically adjust based on company's sector

💡 Best Practice Recommendations

Supplement with Current Analysis - Always combine with recent news, earnings calls, and management guidance

Monitor Data Quality - Check when the underlying financial data was last updated

Consider Market Context - Factor in recent market events that may affect company performance

Use as Starting Point - Treat calculations as baseline analysis requiring additional research

🔗 Methodology

Based on established academic research and professional practices:

Benjamin Graham - Security Analysis principles

Joel Greenblatt - Magic Formula methodology

Edward Altman - Z-Score bankruptcy prediction

Joseph Piotroski - Fundamental analysis scoring

Messod Beneish - Earnings manipulation detection

Modern Portfolio Theory - Risk-adjusted decision making

This indicator is designed for educational and analytical purposes. Always conduct additional research and consider consulting with financial professionals before making investment decisions.

Uptrick: Majors Directional BiasOverview

Uptrick: Majors Directional Bias is a trend-following indicator designed for higher timeframe markets, with a particular focus on the daily chart. It keeps a persistent bullish or bearish stance, highlights confirmed trend flips with one-time markers, and plots a slim, adaptive flow trail that often acts as dynamic support in bullish conditions and resistance in bearish conditions. It is purpose-built for BTC, ETH, and SOL, with safeguards to warn users if applied elsewhere.

Introduction

This indicator was created to simplify trend tracking on higher timeframes. Rather than layering multiple moving averages, oscillators, or external signals, it keeps everything on the price chart itself. Candles are colored by the active stance, a single marker shows the bar where a trend flip is confirmed, and the flow trail follows price closely while adjusting to volatility. For traders working with the daily chart, the trail becomes a practical tool: in an uptrend, it often serves as a natural stop placement zone or structural support, while in a downtrend it behaves like dynamic resistance. The combination of persistence, confirmation, and structure gives traders a clean map of market direction without noise or clutter.

Purpose

The tool is designed to help traders follow medium to long-term market trends rather than react to short intraday moves. Its focus is clarity and continuity — it latches onto a stance and only changes when a new confirmed flip occurs. This makes it suitable for swing traders and position traders who want to stay aligned with the prevailing trend on the daily chart.

Practical uses include identifying trend shifts, entering trades in the direction of the new stance, managing positions by trailing stops along the flow trail, and monitoring pullbacks for whether they respect or break the trail. In this way, the indicator supports both entry timing and ongoing trade management on higher timeframe markets.

Originality and uniqueness

The originality of this script lies in its blend of complexity and simplicity. Internally, it uses multiple filters and layered components to reduce market noise, smooth out erratic fluctuations, and avoid false flips that are common on higher timeframes. Externally, the presentation is deliberately simple: candles are colored by trend, a single marker identifies each confirmed flip, and a slim trail with soft fills shows where the trend structure sits. Many tools either overload traders with information or flicker constantly in uncertain conditions. This script strikes a balance — complex logic works in the background, but what the trader sees is minimal and actionable. Its ability to filter out noise, persist with confidence, and present direction in the simplest terms makes it unique among trend-following overlays.

Why these components were merged

Each component has a clear role in supporting higher timeframe trading. Persistent bias coloring ensures the dominant trend is always visible, making it easy to stay aligned with the market. Flip markers give clarity by identifying the exact bar where the stance shifts, allowing traders to backtest or audit trends quickly. The flow trail provides a structural guide that adapts to volatility: in bull phases it runs under price, often acting as support, while in bear phases it runs above price, often behaving as resistance. Together, these features provide three layers of information in one view — direction, confirmation, and structure — giving traders a reliable framework for swing and position trading on the daily chart.

Step-by-Step

The script determines the dominant trend and locks that stance until an opposite confirmation occurs.

On confirmation of a new trend, a single marker prints on the bar of the flip.

A slim, adaptive trail plots under price in bull phases and above price in bear phases, with a soft fill to reinforce the state.

Price candles are colored by the active stance so the overall direction is always clear.

If the indicator is loaded on assets outside BTC, ETH, or SOL, a warning panel appears to set expectations.

Features

Persistent trend stance

Candles are always bull or bear, with no neutral state. This reduces ambiguity and keeps the trend visible at all times.

One-time flip markers

Markers plot once at the confirmed flip bar, preventing repetitive clutter and making historical review straightforward.

Adaptive flow trail with soft fill

The trail tracks price while adjusting to volatility. In bull trends it acts like dynamic support, in bear trends like dynamic resistance. Traders can use it as a practical stop-loss reference, trailing their risk along the line as the trend progresses.

Noise filtering logic

Internally, the indicator applies multiple filters and components to dampen false signals and avoid unnecessary flips. This is particularly important on higher timeframes, where swings are larger and stability is critical.

Asset-aware design

The indicator is tuned for BTC, ETH, and SOL, with an internal mode that adapts its responsiveness to each. A warning panel appears when used outside these majors.

Overlay-only clarity

Everything is drawn directly on the main chart. The trail gaps at regime changes, fills are soft and non-obstructive, and the overall design emphasizes readability on higher timeframe candles.

Conclusion

The MDB is a higher timeframe trend-following overlay built for BTC, ETH, and SOL, with daily charts as its ideal setting. It combines persistent bias coloring, one-time flip markers, and an adaptive flow trail to give traders direction, confirmation, and structure in the simplest possible form. Internally, it uses complex filtering to reduce noise and maintain reliable signals, but externally it stays minimal and clean. For swing and position traders who want to follow the daily trend with clarity and discipline, this indicator provides a focused solution.

Disclaimer

This indicator is provided for educational and informational purposes only and does not constitute financial advice. Trading involves risk, including the risk of loss. Past performance does not guarantee future results. Always conduct your own analysis and use appropriate risk management.

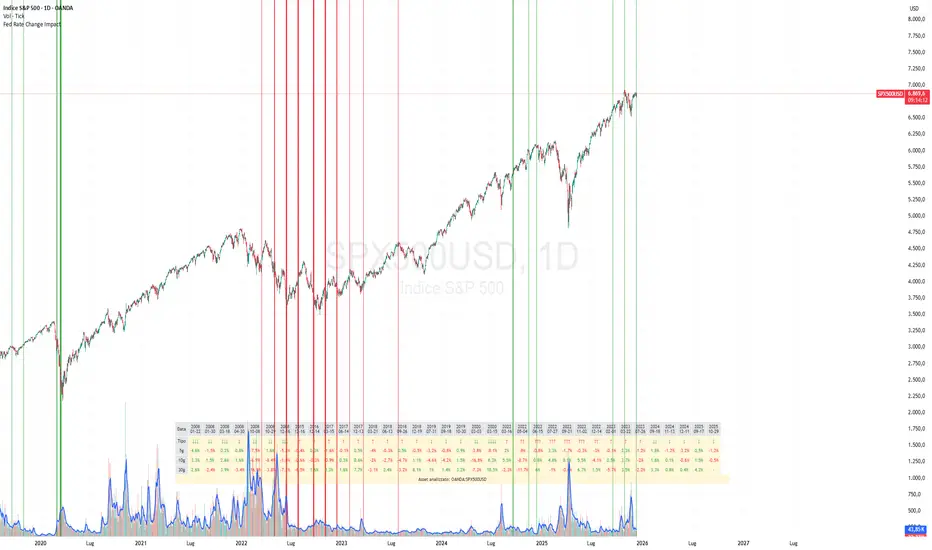

Fed Rate Change Impact📊 Fed Rate Change Impact — Macro Event-Driven Indicator

Fed Rate Change Impact is an advanced indicator designed to analyze the impact of Federal Reserve interest rate changes on financial markets. It integrates event-driven logic with dynamic visualization, percentage diagnostics, and multi-asset selection, offering a clear and customizable view of post-event effects.

🔍 Key Features 📅 Preloaded Fed Events : Includes over 30 historical rate cut (↓) and hike (↑) dates from 2008 to 2024.

📈 Post-Event Analysis : Calculates the percentage change of the selected asset 5, 10, and 30 days after each event.

📌 Vertical Chart Lines : Visually highlights each event directly on the chart, with dynamic coloring (red for hikes, green for cuts).

📋 Diagnostic Table : Displays real-time impact for each event, with color-coded values and a compact layout.

🧠 Interactive Filter: Choose to display only hikes, only cuts, or both.

🧭 Flexible Asset Selection : Analyze the current chart asset, pick from a predefined list, or manually input any ticker via input.symbol().

🎯 Contextual Highlighting : The table highlights the analyzed asset if it matches the active chart symbol.

⚙️ Customizable Parameters lookahead5, lookahead10, lookahead30: Define the time horizon for measuring post-event impact.

eventFilter : Choose which type of events to display.

presetAsset / customAsset : Select or input the asset to analyze.

🧪 Recommended Use Cases Macroeconomic analysis on indices, commodities, crypto, and forex

Studying delayed effects of rate changes on sensitive assets

Building event-driven strategies or diagnostic overlays

Visual backtesting and cross-asset comparison

🧠 Technical Notes The indicator is compatible with overlay=true and works best on Daily timeframe.

The table automatically adapts to the number of events and includes visual padding for improved readability.

All calculations are performed in real time and require no external data.

FOMC Policy Events[nakano]### FOMC Policy Events

#### Summary / 概要

This indicator plots the historical policy decisions of the U.S. Federal Open Market Committee (FOMC) directly onto your chart. It is an essential tool for traders and analysts who want to visualize how the market reacts to changes in monetary policy. All historical event data from 2000 onwards is hard-coded into the script for fast and reliable performance.

このインジケーターは、米国連邦公開市場委員会(FOMC)の過去の政策決定をチャート上に直接プロットします。金融政策の変更に対する市場の反応を視覚的に分析したいトレーダーやアナリストにとって不可欠なツールです。2000年以降の全ての過去イベントデータが含まれます。

---

#### Features / 主な機能

* **Comprehensive Historical Data / 包括的な過去データ**

Includes all historical scheduled and emergency FOMC rate decisions from January 2000.

2000年1月以降の、全ての定例および緊急のFOMC金利決定の履歴を含みます。

* **Detailed Event Labels / 詳細なイベントラベル**

Each event is marked with a clear label showing:

各イベントには、以下の情報を示す明確なラベルが表示されます:

* The exact date of the announcement.

発表の正確な日付

* The type of decision (Rate Hike, Rate Cut, Hold, or Emergency Cut).

決定内容(利上げ、利下げ、据え置き、緊急利下げ)

* The resulting Federal Funds Target Rate.

決定後の政策金利(FF金利ターゲット)

* **Fully Customizable Display / 柔軟な表示設定**

From the indicator's settings menu, you can:

インジケーターの設定画面から、以下の操作が可能です:

* Individually toggle the visibility of Rate Hikes, Rate Cuts, and Holds.

「利上げ」「利下げ」「据え置き」の表示・非表示を個別に切り替える

* Choose your preferred language for the labels (English or Japanese).

ラベルの表示言語を「英語」または「日本語」から選択する

* **Clear Visual Cues / 明確なビジュアル**

* **Rate Hikes:** Green labels positioned below the price bars.

**利上げ:** バーの下に緑色のラベル

* **Rate Cuts:** Red labels positioned above the price bars.

**利下げ:** バーの上に赤色のラベル

* **Holds:** Gray labels positioned above the price bars.

**据え置き:** バーの上に灰色のラベル

* **Emergency Events:** Specially highlighted in maroon for easy identification.

**緊急イベント:** 識別しやすいように特別な色(ワインレッド)で強調表示

---

#### How to Use / 使用方法

1. Add the indicator to your chart.

インジケーターをチャートに追加します。

2. Click the **Settings (gear icon)** next to the indicator name on your chart.

チャート上のインジケーター名の横にある**設定(歯車アイコン)**をクリックします。

3. In the "Display Settings" section, check or uncheck the boxes to show or hide different event types.

「Display Settings」セクションで、各イベントタイプの表示・非表示をチェックボックスで切り替えます。

4. In the "Language Settings" section, select your preferred language from the dropdown menu.

「Language Settings」セクションで、ドロップダウンメニューからお好みの言語を選択します。

---

#### A Note on Data / データについて

The event data included in this script is static and contains historical decisions up to September 2025. The script does not plot future scheduled meetings and will need to be manually updated as new policy decisions are made.

このスクリプトに含まれるイベントデータは静的なものであり、2025年9月までの過去の決定を含んでいます。未来のスケジュールをプロットする機能はなく、新しい金融政策が決定された場合は、スクリプトの手動更新が必要です。

Aggregated OI by MalexThis indicator aggregates Open Interest data from multiple major exchanges (Binance, Bybit, OKX) to provide a comprehensive view of market positioning across platforms.

Original idea by Alex Nikulin.

FEATURES:

Multi-exchange OI aggregation with customizable exchange selection

Choose between Sum or Average aggregation methods

Individual exchange OI display (optional)

Clean mode - show only aggregated data

Real-time status monitoring for each exchange

Candlestick visualization matching standard OI indicators

Information panel showing current values and active exchanges

USAGE:

Enable/disable specific exchanges in settings

Choose aggregation method (Average recommended for balanced view)

Toggle individual exchange display or use clean mode

Monitor the info panel for data availability status

COMPATIBILITY:

Works with any symbol that has Open Interest data available on the selected exchanges.

Best used on perpetual futures contracts (e.g., BTCUSDT, ETHUSDT, etc.)

Smarter Money Concepts Dashboard [PhenLabs]📊Smarter Money Concepts Dashboard

Version: PineScript™v6

📌Description

The Smarter Money Concepts Dashboard is a comprehensive institutional trading analysis tool that combines six of our most powerful smarter money concepts indicators into one unified suite. This advanced system automatically detects and visualizes Fair Value Gaps, Inverted FVGs, Order Blocks, Wyckoff Springs/Upthrusts, Wick Rejection patterns, and ICT Market Structure analysis.

Built for serious traders who need institutional-grade market analysis, this dashboard eliminates subjective interpretation by automatically identifying where smart money is likely positioned. The integrated real-time dashboard provides instant status updates on all active patterns, making it easy to monitor market conditions at a glance.

🚀Points of Innovation

● Multi-Module Integration: Six different SMC concepts unified in one comprehensive system

● Real-Time Dashboard Display: Live tracking of all active patterns with customizable positioning

● Advanced Volume Filtering: Institutional volume confirmation across all pattern types

● Automated Pattern Management: Smart memory system prevents chart clutter while maintaining relevant zones

● Probability-Based Wyckoff Detection: Mathematical probability calculations for spring/upthrust patterns

● Dual FVG System: Both standard and inverted Fair Value Gap detection with equilibrium analysis

🔧Core Components

● Fair Value Gap Engine: Detects standard FVGs with volume confirmation and equilibrium line analysis

● Inverted FVG Module: Advanced IFVG detection using RVI momentum filtering for inversion confirmation

● Order Block System: Institutional order block identification with customizable mitigation methods

● Wyckoff Pattern Recognition: Automated spring and upthrust detection with probability scoring

● Wick Rejection Analysis: High-probability reversal patterns based on wick-to-body ratios

● ICT Market Structure: Simplified institutional concepts with commitment tracking

🔥Key Features

● Comprehensive Pattern Detection: All major SMC concepts in one indicator with automatic identification

● Volume-Confirmed Signals: Multiple volume filters ensure only institutional-grade patterns are highlighted

● Interactive Dashboard: Real-time status display with active pattern counts and module status

● Smart Memory Management: Automatic cleanup of old patterns while preserving relevant market zones

● Full Alert System: Complete notification coverage for all pattern types and signal generations

● Customizable Display Options: Adjustable colors, transparency, and positioning for all visual elements

🎨Visualization

● Color-Coded Zones: Distinct color schemes for bullish/bearish patterns across all modules

● Dynamic Box Extensions: Automatically extending zones until mitigation or invalidation

● Equilibrium Lines: Fair Value Gap midpoint analysis with dotted line visualization

● Signal Markers: Clear spring/upthrust signals with directional arrows and probability indicators

● Dashboard Table: Professional-grade status panel with module activation and pattern counts

● Candle Coloring: Wick rejection highlighting with transparency-based visual emphasis

📖Usage Guidelines

Fair Value Gap Settings

● Days to Analyze: Default 15, Range 1-100 - Controls historical FVG detection period

● Volume Filter: Enables institutional volume confirmation for gap validity

● Min Volume Ratio: Default 1.5 - Minimum volume spike required for gap recognition

● Show Equilibrium Lines: Displays FVG midpoint analysis for precise entry targeting

Order Block Configuration

● Scan Range: Default 25 bars - Lookback period for structure break identification

● Volume Filter: Institutional volume confirmation for order block validation

● Mitigation Method: Wick or Close-based invalidation for different trading styles

● Min Volume Ratio: Default 1.5 - Volume threshold for significant order block formation

Wyckoff Analysis Parameters

● S/R Lookback: Default 20 - Support/resistance calculation period for spring/upthrust detection

● Volume Spike Multiplier: Default 1.5 - Required volume increase for pattern confirmation

● Probability Threshold: Default 0.7 - Minimum probability score for signal generation

● ATR Recovery Period: Default 5 - Price recovery calculation for pattern strength assessment

Market Structure Settings

● Auto-Detect Zones: Automatic identification of high-volume thin zones

● Proximity Threshold: Default 0.20% - Price proximity requirements for zone interaction

● Test Window: Default 20 bars - Time period for zone commitment calculation

Display Customization

● Dashboard Position: Four corner options for optimal chart layout

● Text Size: Scalable from Tiny to Large for different screen configurations

● Pattern Colors: Full customization of all bullish and bearish zone colors

✅Best Use Cases

● Swing Trading: Identify major institutional zones for multi-day position entries

● Day Trading: Precise intraday entries at Fair Value Gaps and Order Block boundaries

● Trend Analysis: Market structure confirmation for directional bias establishment

● Risk Management: Clear invalidation levels provided by all pattern boundaries

● Multi-Timeframe Analysis: Works across all timeframes from 1-minute to monthly charts

⚠️Limitations

● Market Condition Dependency: Performance varies between trending and ranging market environments

● Volume Data Requirements: Requires accurate volume data for optimal pattern confirmation

● Lagging Nature: Some patterns confirmed after initial price movement has begun

● Pattern Density: High-volatility markets may generate excessive pattern signals

● Educational Tool: Requires understanding of smart money concepts for effective application

💡What Makes This Unique

● Complete SMC Integration: First indicator to combine all major smart money concepts comprehensively

● Real-Time Dashboard: Instant visual feedback on all active institutional patterns

● Advanced Volume Analysis: Multi-layered volume confirmation across all detection modules

● Probability-Based Signals: Mathematical approach to Wyckoff pattern recognition accuracy

● Professional Memory Management: Sophisticated pattern cleanup without losing market relevance

🔬How It Works

1. Pattern Detection Phase:

● Multi-timeframe scanning for institutional footprints across all enabled modules

● Volume analysis integration confirms patterns meet institutional trading criteria

● Real-time pattern validation ensures only high-probability setups are displayed

2. Signal Generation Process:

● Automated zone creation with precise boundary definitions for each pattern type

● Dynamic extension system maintains relevance until mitigation or invalidation occurs

● Alert system activation provides immediate notification of new pattern formations

3. Dashboard Update Cycle:

● Live status monitoring tracks all active patterns and module states continuously

● Pattern count updates provide instant feedback on current market condition density

● Commitment tracking for market structure analysis shows institutional engagement levels

💡Note:

This indicator represents institutional trading concepts and should be used as part of a comprehensive trading strategy. Pattern recognition accuracy improves with understanding of smart money principles. Combine with proper risk management and multiple confirmation methods for optimal results.

PolyFilter [BackQuant]PolyFilter

A flexible, low-lag trend filter with three smoothing engines—optimized for clean bias, fewer whipsaws, and clear alerting.

What it does

PolyFilter draws a single “intelligent” baseline that adapts to price while suppressing noise. You choose the engine— Fractional MA , Ehlers 2-Pole Super Smoother , or a Multi-Kernel blend . The line can color itself by slope (trend) or by position vs price (above/below), and you get four ready-made alerts for flips and crosses.

What it plots

PolyFilter line — your smoothed trend baseline (width set by “Line Width”).

Optional candle & background coloring — choose: color by trend slope or by whether price is above/below the filter.

Signal markers — Arrows with L/S when the slope flips or when price crosses the line (if you enable shapes/alerts).

How the three engines differ

Fractional MA (experimental) — A power-law weighting of past bars (heavier focus on the most recent samples without throwing away history). The Adaptation Speed acts like the “fraction” exponent (default 0.618). Lower values lean more on recent bars; higher values spread weight further back.

Ehlers 2-Pole Super Smoother — Classic low-lag IIR smoother that aggressively reduces high-frequency noise while preserving turns. Great default when you want a steady, responsive baseline with minimal parameter fuss.

Multi-Kernel — A 70/30 blend of a Gaussian window and an exponential kernel. The Gaussian contributes smooth structure; the exponential adds a hint of responsiveness. Useful for assets that oscillate but still trend.

Reading the colors

Trend mode (default) — Line & candles turn green while the filter is rising (signal > signal ) and red while it’s falling.

Above/Below mode — Line & candles reflect price’s position relative to the filter: green when price > filter, red when price < filter. This is handy if you treat the filter like a dynamic “fair value” or bias line.

Inputs you’ll actually use

Calculation Settings

Price Source — Default HLC/3. Switch to Close for stricter trend, or HLC3/HL2 to soften single-print spikes.

Filter Length — Window/period for all engines. Shorter = snappier turns; longer = smoother line.

Adaptation Speed — Only affects Fractional MA . Lower it for faster, more local weighting; raise it for smoother, more global weighting.

Filter Type — Pick one of: Fractional MA, Ehlers 2-Pole, Multi-Kernel.

UI & Plotting

Color based off… — Choose Trend (slope) or > or < Close (position vs price).

Long/Short Colors — Customize bull/bear hues to your theme.

Show Filter Line / Paint candles / Color background — Visual toggles for the line, bars, and backdrop.

Line Width — Make the filter stand out (2–3 works well on most charts).

Signals & Alerts

PolyFilter Trend Up — Slope flips upward (the filter crosses above its prior value). Good for early continuation entries or stop-tightening on shorts.

PolyFilter Trend Down — Slope flips downward. Often used to scale out longs or rotate bias.

PolyFilter Above Price — The filter line crosses up through price (filter > price). This can confirm that mean has “caught up” after a pullback.

PolyFilter Below Price — The filter line crosses down through price (filter < price). Useful to confirm momentum loss on bounces.

Quick starts (suggested presets)

Intraday (5–15m, crypto or indices) — Ehlers 2-Pole, Length 55–80. Trend coloring ON, candle paint ON. Look for pullbacks to a rising filter; avoid fading a falling one.

Swing (1H–4H) — Multi-Kernel, Length 80–120. Background color OFF (cleaner), candle paint ON. Add a higher-TF confirmation (e.g., 4H filter rising when you trade 1H).

Range-prone FX — Fractional MA, Length 70–100, Adaptation ~0.55–0.70. Consider Above/Below mode to trade mean reversion to the line with a strict risk cap.

How to use it in practice

Bias line — Trade in the direction of the filter slope; stand aside when it flattens and color chops back and forth.

Dynamic support/resistance — Treat the line as a moving value area. In trends, entries often appear on shallow tags of the line with structure confluence.

Regime switch — When the filter flips and holds color for several bars, tighten stops on the opposing side and look for first pullback in the new color.

Stacking filters — Many users run PolyFilter on the active chart and a slower instance (longer length) on a higher timeframe as a “macro bias” guardrail.

Tuning tips

If you see too many flips, lengthen the filter or switch to Multi-Kernel.

If turns feel late, shorten the filter or try Ehlers 2-Pole for lower lag.

On thin or very noisy symbols, prefer HLC3 as the source and longer lengths.

Performance note: very large lengths increase computation time for the Multi-Kernel and Fractional engines. Start moderate and scale up only if needed.

Summary

PolyFilter gives you a single, trustworthy baseline that you can read at a glance—either as a pure trend line (slope coloring) or as a dynamic “above/below fair value” reference. Pick the engine that matches your market’s personality, set a sensible length, and let the color and alerts guide bias, entries on pullbacks, and risk on reversals.

Expected Value Monte CarloI created this indicator after noticing that there was no Expected Value indicator here on TradingView.

The EVMC provides statistical Expected Value to what might happen in the future regarding the asset you are analyzing.

It uses 2 quantitative methods:

Historical Backtest to ground your analysis in long-term, factual data.

Monte Carlo Simulation to project a cone of probable future outcomes based on recent market behavior.

This gives you a data-driven edge to quantify risk, and make more informed trading decisions.

The indicator includes:

Dual analysis: Combines historical probability with forward-looking simulation.

Quantified projections: Provides the Expected Value ($ and %), Win Rate, and Sharpe Ratio for both methods.

Asset-aware: Automatically adjusts its calculations for Stocks (252 trading days) and Crypto (365 days) for mathematical accuracy.

The projection cone shows the mean expected path and the +/- 1 standard deviation range of outcomes.

No repainting

Calculation:

1. Historical Expected Value:

This is a systematic backtest over thousands of bars. It calculates the return Rᵢ for N past trades (buy-and-hold). The Historical EV is the simple average of these returns, giving a baseline performance measure.

Historical EV % = (Σ Rᵢ) / N

2. Monte Carlo Projection:

This projection uses the Geometric Brownian Motion (GBM) model to simulate thousands of future price paths based on the market's recent behavior.

It first measures the drift (μ), or recent trend, and volatility (σ), or recent risk, from the Projection Lookback period. It then projects a final return for each simulation using the core GBM formula:

Projected Return = exp( (μ - σ²/2)T + σ√T * Z ) - 1

(Where T is the time horizon and Z is a random variable for the simulation.)

The purple line on the chart is the average of all simulated outcomes (the Monte Carlo EV). The cone represents one standard deviation of those outcomes.

The dashed lines represent one standard deviation (+/- 1σ) from the average, forming a cone of probable outcomes. Roughly 68% of the simulated paths ended within this cone.

This projection answers the question: "If the recent trend and volatility continue, where is the price most likely to go?"

Here's how to read the indicator

Expected Value ($/%): Is my average trade profitable?

Win Rate: How often can I expect to be right?

Sharpe Ratio: Am I being adequately compensated for the risk I'm taking?

User Guide

Max trade duration (bars): This is your analysis timeframe. Are you interested in the probable outcome over the next month (21 bars), quarter (63 bars), or year (252 bars)?

Position size ($): Set this to your typical trade size to see the Expected Value in real dollar terms.

Projection lookback (bars): This is the most important input for the Monte Carlo model. A short lookback (e.g., 50) makes the projection highly sensitive to recent momentum. Use this to identify potential recency bias. A long lookback (e.g., 252) provides a more stable, long-term projection of trend and volatility.

Historical Lookback (bars): For the historical backtest, more data is always better. Use the maximum that your TradingView plan allows for the most statistically significant results.

Use TP/SL for Historical EV: Check this box to see how the historical performance would have changed if you had used a simple Take Profit and Stop Loss, rather than just holding for the full duration.

I hope you find this indicator useful and please let me know if you have any suggestions. 😊

VIX Price BoxVIX Price Box (Customizable Colors)

This indicator displays the current VIX (CBOE Volatility Index) value in a fixed box on the top-right corner of the chart. It’s designed to give traders a quick, at-a-glance view of market volatility without needing to switch tickers.

Features

Pulls the live VIX price and updates automatically on every bar.

Displays the value inside a table box that stays fixed in the top-right corner.

Threshold-based coloring: the text color changes depending on whether the VIX is below, between, or above your chosen threshold levels.

5 built-in color modes:

Custom mode – choose your own colors for low, medium, and high volatility zones.

Adjustable threshold levels, background color, and frame color.

Use Cases

Monitor overall market risk sentiment while trading other instruments.

Identify periods of low vs. high volatility at a glance.

Pair with strategies that rely on volatility (options trading, hedging, breakout setups, etc.).

Cointegration IndicationThis indicator is inspired by Nobel Prize–winning research (Engle & Granger, 1987). The core idea is simple but powerful: even if two markets look noisy on their own, their relationship can be surprisingly stable over the long run. When they drift apart, history suggests they often snap back together and that’s exactly where opportunities arise.

What this tool does is bring that theory into practice. It estimates a long-run equilibrium between two assets (Y ~ α + βX), calculates the residual spread (ε), and then evaluates whether that spread behaves in a mean-reverting way. The Z-Score tells you when the spread has moved far from its historical mean. The Error Correction Model (ECM) adds a second layer: it checks whether the spread tends to close again, and how strong that adjustment pressure is. If λ is negative and stable, the relationship is cointegrated and mean-reverting. If not, the pair is unstable — even if the Z-Score looks attractive.

Signals are summarized clearly:

– Strong Setup appears when we see both extreme divergence and a stable, negative λ.

– Weak Setup means only partial confirmation.

– Invalid means the relationship is breaking down.

Why this matters

Cointegration analysis is widely used by institutional desks, especially in pairs trading, statistical arbitrage, and risk management. Classic cases include equity index futures vs ETFs (Alexander, 2001), oil vs energy stocks (Chen & Huang, 2010), or swap spreads in fixed income (Tsay, 2010). In crypto, temporary cointegration has been observed between BTC and ETH in periods of high liquidity (Corbet et al., 2018). With this indicator, you can explore these relationships directly on TradingView, test asset pairs, and see when divergences become statistically significant.

Limitations to keep in mind

– Timeframe choice matters: Daily calculations are usually more stable; weekly or intraday often show unstable signals. To avoid confusion, you can fix the calculation timeframe in the settings.

– Cointegration is not permanent. Structural breaks (earnings, regulation, macro shifts) can destroy old relationships.

– Results are approximate. Rolling regressions, Z-Scores, and ECM estimates are sensitive to the length of the chosen windows.

– This is a research tool — not a ready-made trading system. It should be used as one piece in a broader framework.

References

Alexander, C. (2001). Market models: A guide to financial data analysis. Wiley.

Chen, S. S., & Huang, C. W. (2010). Long-run equilibrium and short-run dynamics in energy stock prices and oil prices. Energy Economics, 32(1), 19–26.

Corbet, S., Meegan, A., Larkin, C., Lucey, B., & Yarovaya, L. (2018). Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters, 165, 28–34.

Engle, R. F., & Granger, C. W. J. (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica, 55(2), 251–276.

Tsay, R. S. (2010). Analysis of financial time series (3rd ed.). Wiley.

DCA Cost Basis (with Lump Sum)DCA Cost Basis (with Lump Sum) — Pine Script v6

This indicator simulates a Dollar Cost Averaging (DCA) plan directly on your chart. Pick a start date, choose how often to buy (daily/weekly/monthly), set the per-buy amount, optionally add a one-time lump sum on the first date, and visualize your evolving average cost as a VWAP-style line.

Features

Customizable DCA Plan — Set Start Date , buy Frequency (Daily / Weekly / Monthly), and Recurring Amount (in quote currency, e.g., USD).

Lump Sum Option — Add a one-time lump sum on the very first eligible date; recurring DCA continues automatically after that.

Cost Basis Line — Plots the live average price (Total Cost / Total Units) as a smooth, VWAP-style line for instant breakeven awareness.

Buy Markers — Optional triangles below bars to show when simulated buys occur.

Performance Metrics — Tracks:

Total Invested (quote)

Total Units (base)

Cost Basis (avg entry)

Current Value (mark-to-market)

CAGR (Annualized) from first buy to current bar

On-Chart Summary Table — Displays Start Date, Plan Type (Lump + DCA or DCA only), Total Invested, and CAGR (Annualized).

Data Window Integration — All key values also appear in the Data Window for deeper inspection.

Why use it?

Visualize long-term strategies for Bitcoin, crypto, or stocks.

See how a lump sum affects your average entry over time.

Gauge breakeven at a glance and evaluate historical performance.

Note: This tool is for educational/simulation purposes. Results are based on bar closes and do not represent live orders or fees.

Smart Index Levels — GSK-VIZAG-AP-INDIA📌 Smart Index Levels — GSK-VIZAG-AP-INDIA

Smart Index Levels is a versatile support and resistance plotting tool designed for intraday, weekly, and monthly analysis.

It automatically generates key price zones based on user-defined step sizes, helping traders visualize important market levels more clearly.

🔹 Features

Daily / Weekly / Monthly Modes

Switch easily between daily, weekly, or monthly reference levels.

Customizable Level Steps

Choose step intervals of 50 or 100 points for cleaner index-based zones.

Support & Resistance Zones

Auto-draws multiple support and resistance levels around the opening base price.

Mid-Level Marking

Highlights the nearest “mid” price level for balance reference.

Weekly High/Low Tracking (Optional)

Plots dynamic weekly high & low levels with dotted lines.

Monthly High/Low Tracking (Optional)

Displays monthly high & low levels for broader market context.

Custom Market Session Timing

Define your own market open and close times.

Line Style & Colors

Fully customizable line styles (solid, dashed, dotted) and colors.

⚙️ How It Works

At the start of the selected session (daily, weekly, or monthly), the script identifies the opening reference price.

From this base, it calculates and draws support and resistance levels at fixed step intervals.

Optionally, it overlays weekly and monthly high/low levels for additional perspective.

This provides a structured price map that helps you quickly spot potential reaction zones, without cluttering the chart.

🖥️ Best Use Cases

Intraday index traders who want quick reference levels (Nifty, BankNifty, etc.)

Swing traders who prefer weekly and monthly zones for context.

Anyone looking for clean, rule-based support/resistance plotting.

⚠️ Disclaimer

This indicator is for educational and informational purposes only.

It does not provide financial advice or trading signals. Always use in combination with your own analysis and risk management.

AWSA "Level Indicator with ATR" isn't a single, defined indicator but typically refers to a trading strategy or indicator that uses the Average True Range (ATR) to create dynamic levels on a price chart, such as support, resistance, or stop-loss levels. The ATR is a volatility indicator that measures market volatility; when high, it suggests the market has large price swings, and when low, small price swings. By using the ATR value with a multiplier, traders can set price levels that adapt to changing market volatility, providing more objective and dynamic trading signals than fixed-price levels.

Aggregated OI (Binance + Bybit + OKX)RU

Агрегатор Open Interest для крипты по трём биржам: Binance, Bybit, OKX/OKEX.

Показывает OI-свечи или дельту OI, есть мини-легенда (Open Interest, Rekt Longs/Shorts, Aggressive Longs/Shorts). Можно переключать биржи и единицы отображения (USD / COIN).

Данные зависят от доступности OI-тикеров в TradingView (…USDT.P_OI). Если по паре нет фида на бирже — она игнорируется. Основано на скрипте LeviathanCapital (MPL-2.0), модификация — SaneQ. Не является финсоветом.

EN

Aggregated Open Interest for crypto across Binance, Bybit, OKX/OKEX.

Plots OI candles or OI delta, plus a compact legend (Open Interest, Rekt Longs/Shorts, Aggressive Longs/Shorts). You can toggle exchanges and display units (USD / COIN).

Data depends on TV OI feeds (…USDT.P_OI). If a pair lacks a feed on an exchange, that source is skipped. Based on LeviathanCapital’s script (MPL-2.0), modified by SaneQ. Not financial advice.

OG OHLC MarkerDraws, OHLC for Previous day and Today with options to add alerts when any PD Array is swept

Volatility Momentum Score | Lyro RSVolatility Momentum Score | Lyro RS

Overview

The Volatility Momentum Score (VMS) combines price movement and volatility into a single, easy-to-read signal. Using z-scores, standard deviation bands, and flexible display modes, it helps traders identify trends, overbought/oversold conditions, and potential reversals quickly and effectively.

Key Features

Price + Volatility Blend

Tracks price action and volatility with separate z-scores and merges them into a unified momentum score.

Standard Deviation Bands

Upper and lower bands highlight extreme readings.

Adjustable multipliers allow for fine-tuning sensitivity.

Two Signal Modes

Trend Mode: Plots “Long” and “Short” signals when momentum crosses bands.

Reversion Mode: Colors the chart background when the score indicates stretched conditions.

Overbought & Oversold Alerts

▲ markers indicate oversold conditions.

▼ markers indicate overbought conditions.

Custom Colors

Four preset color themes or fully customizable bullish/bearish colors.

Clear Visuals

Dynamic line coloring based on momentum.

Candles recolored at signal points.

Background shading for quick visual assessment.

How It Works

Calculates z-scores for both price and volatility.

Blends the z-scores into a single average score.

Compares the score against dynamic upper and lower bands.

Triggers signals, markers, or background shading depending on the chosen display mode.

Practical Use

Ride trends: Follow Trend Mode signals to align with momentum.

Spot reversals: Watch ▲ and ▼ markers when markets are overextended.

Stay aware: Background shading highlights potentially overheated conditions.

Customization

Set lookback lengths for price, volatility, and bands.

Adjust band multipliers for more or less sensitive signals.

Choose between Trend or Reversion mode based on trading style.

Select color themes or create custom palettes.

⚠️ Disclaimer

This indicator is a technical analysis tool and does not guarantee results. It should be used alongside other methods and proper risk management. The creators are not responsible for any financial decisions based on its signals.

Pivot + Mean Reversion + RSI (Signals Only) by Shashwat KhuranaShow BUY labels below bars when a bullish reversal is detected.

Show SELL labels above bars when a bearish reversal is detected.

Uses pivot levels, mean reversion, big candle, RSI, and volume filters.

Moon Phase & Celestial Events TrackerMoon Phase & Celestial Events Tracker

Overview

A comprehensive astronomical and celestial event indicator that tracks and projects major cosmic events from 2011 to 2040. This indicator overlays important astronomical phenomena directly on your charts, allowing traders and researchers to analyze potential correlations between celestial events and market movements.

Key Features

Eclipse Tracking 🌑

Blood Moons (Total Lunar Eclipses) including 2014-2015 tetrad

Partial Lunar Eclipses with distinctive yellow markers

Solar Eclipses: Total, Annular, Partial, and Hybrid types with unique symbols

Optional eclipse season background highlighting

Moon Cycles 🌕

Supermoons at perigee (closest Earth approach)

Regular moon phases: New, First Quarter, Full, Last Quarter

Adjustable phase marking with day-offset capability

Mercury Retrograde ☿

Start and end dates clearly marked

Optional period highlighting for entire retrograde duration

Complete cycle tracking through 2040

Seasonal Transitions ✨

Spring Equinox, Summer Solstice, Autumn Equinox, Winter Solstice

Precise astronomical season changes

Future Projections 📊

Event forecasting up to 5 years ahead

Customizable projection range (30-1825 days)

Selective projection by event type

Adjustable visual styles and transparency

Interpretation Guide

Blood Moons

Total lunar eclipses where Earth's atmosphere creates the red appearance. In financial astrology, these are often watched as potential reversal or volatility periods, though correlations vary significantly.

Eclipse Seasons

Twice-yearly windows when Sun-Earth-Moon alignment allows eclipses. Some market practitioners note increased volatility during these periods, though empirical evidence remains debated.

Mercury Retrograde

The apparent backward motion of Mercury occurs 3-4 times yearly. In trading folklore, it's associated with communication issues, technical problems, and false signals. Many practitioners suggest extra caution with new positions during these periods.

Supermoons

Full or new moons at closest Earth approach. Some traders track these for potential short-term highs/lows, particularly in commodities and currencies, though effects are subtle if present.

Seasonal Markers

Astronomical season changes have been incorporated into various market timing systems, with some analysts noting clustering of trend changes around these dates.

Use Cases

Historical pattern analysis

Event-based research

Educational astronomy tracking

Market cycle studies

Long-term planning and observation

Technical Details ⚙️

Data Coverage: 2011-2040 (30 years of precise astronomical events)

Compatibility: All timeframes with smart filtering (Weekly/Monthly show only major events)

Performance: Lightweight with efficient calculations and minimal chart impact

Data Source: Based on NASA ephemeris data for precise event timing

Customization Options 🎨

Individual colors for each event type

Transparency controls for projections

Event visibility toggles

Optional date labels on events

Alert Options 🔔

Set custom alerts for any tracked event including all eclipse types, moon phases, Mercury retrograde start/end, and seasonal transitions.

⚠️ Important Note

This indicator displays astronomical events for research and educational purposes. Any perceived correlations with market movements should be thoroughly backtested. Financial astrology interpretations are included for historical context only and should not be considered trading advice. Always use proper risk management and multiple forms of analysis in trading decisions.

Best Suited For

Market researchers and analysts

Students of market cycles

Those interested in astronomical timing

Educational and observational purposes

Long-term pattern analysis

Position Sizing Calculator with ADR%, Account %, and RSILET ME KNOW IN COMMENTS IF YOU HAVE ANY ISSUES!

Overview

The Position Sizing Calculator with ADR% + RSI is a indicator that helps traders calculate position sizes based on risk management parameters (stop loss at low of day). It uses a fixed percentage of the account size, risk per trade, and stop loss distance (current price minus daily low) to determine the number of shares or contracts to trade. Additionally, it displays the Average Daily Range (ADR) as a percentage, the Relative Strength Index (RSI), and the price’s percentage distance from the daily low in a real-time table.

Features

Position Sizing: Calculates position size based on a fixed account percentage, risk per trade, and stop loss distance, ensuring the position value stays within the allocated capital.

ADR% Display: Shows the ADR as a percentage of the daily low, colored green if >5% or red if ≤5%.

RSI Display: Shows the RSI, colored green if oversold (<30), red if overbought (>70), or gray otherwise.

Distance from Low: Displays the current price’s percentage distance from the daily low for context.

Real-Time Table: Presents all metrics in a top-right table, updating in real-time.

Position Value Cap: Ensures the position value doesn’t exceed the allocated capital.

Minimum Stop Loss: Prevents oversized positions due to very small stop loss distances.

Customizable Parameters

Account Size ($): Set the total account balance (default: $1,000, min: $100, step: $100).

Risk Per Trade (%): The percentage of allocated capital to risk per trade (default: 1%, range: 0.1% to 10%, step: 0.1%).

Max % of Account: The fixed percentage of the account to allocate for the trade (default: 50%, range: 10% to 100%, step: 1%).

ADR Period: The number of days to calculate the ADR (default: 14, min: 1, step: 1).

RSI Length: The period for RSI calculation (default: 14, min: 1, step: 1).

Min Stop Loss Distance ($): The minimum stop loss distance to prevent oversized positions (default: $0.01, min: $0.001, step: $0.001).

Calculations

Stop Loss Distance: Current price minus daily low, with a minimum value set by the user.

Position Size: (Account Size * Max % of Account * Risk Per Trade %) / Stop Loss Distance, capped so the position value doesn’t exceed the allocated capital.

ADR%: 100 * (SMA(daily high / daily low, ADR Period) - 1), reflecting the average daily range relative to the low.

RSI: Calculated using the smoothed average of gains and losses over the RSI period, with special handling for zero gains or losses.

Distance from Low: (Current Price - Daily Low) / Daily Low * 100.

Table Display

Account Size: The input account balance.

Risk Per Trade: The risk percentage.

Stop Loss Distance: The price difference between the current price and daily low.

Distance from Low: The percentage distance from the daily low.

Account % Used: The fixed percentage of the account allocated.

Position Size: The calculated number of shares or contracts.

Position Value: The position size multiplied by the current price.

ADR %: The ADR percentage, colored green (>5%) or red (≤5%).

RSI: The RSI value, colored green (<30), red (>70), or gray (30–70).

Usage

Ideal for traders managing risk by allocating a fixed portion of their account and sizing positions based on stop loss distance.

The ADR% and RSI provide market context, with color coding to highlight high volatility or overbought/oversold conditions.

Adjust the customizable parameters to fit your trading style, such as increasing the risk percentage for aggressive trades or adjusting the ADR/RSI periods for different time horizons.

Earnings line & P/E Tracker# Earnings line & P/E Tracker

**A comprehensive fundamental analysis indicator that overlays earnings data and P/E ratios directly on your price charts.**

## 📊 Key Features

### Automatic Data Retrieval

- **Real-time financial data** pulled directly from TradingView's financial database

- **Multiple data sources**: Earnings Per Share (Basic/Diluted), Total Revenue, Net Income

- **Flexible periods**: TTM (Trailing Twelve Months), FQ (Quarterly), FY (Annual)

- **Live P/E ratio calculation** based on current price and TTM earnings

### Visual Display Options

- **Earnings progression line** overlaid on price chart for easy comparison

- **P/E ratio plot** with distinctive circle markers

- **Comprehensive data table** showing all key metrics in real-time

- **Dark mode optimized** with high-contrast colors for excellent readability

### Optional Event Tracking

- **Custom earnings dates** input for upcoming releases

- **Visual markers** on earnings announcement dates

- **Background highlighting** during earnings weeks

- **Smart alerts** for significant P/E changes and data updates

## 🎯 Perfect For

- **Fundamental analysts** comparing earnings growth vs stock price movement

- **Value investors** tracking P/E ratios and earnings trends

- **Earnings season trading** with visual release date markers

- **Long-term investors** monitoring fundamental health alongside technical analysis

## ⚙️ Customization Options

### Data Selection

- Choose between EPS Basic, EPS Diluted, Total Revenue, or Net Income

- Select TTM, quarterly, or annual reporting periods

- Toggle individual display elements on/off

### Visual Styling

- Customizable colors for earnings line, P/E ratio, and event markers

- Adjustable line width and styling options

- Moveable data table with size and position controls

### Event Management

- Input custom earnings release dates

- Enable/disable earnings event markers

- Background highlighting for earnings periods

- Configurable alert thresholds

## 📈 How It Works

1. **Automatic Detection**: The indicator automatically detects available fundamental data for your selected symbol

2. **Real-time Updates**: Financial metrics update as new data becomes available

3. **Visual Integration**: Earnings data is scaled and overlaid directly on your price chart

4. **Status Monitoring**: Clear indicators show data availability and freshness

## 🔧 Setup Instructions

1. Add the indicator to your chart

2. Select your preferred data source (EPS recommended for P/E tracking)

3. Choose time period (TTM recommended for most analyses)

4. Customize colors and display options to your preference

5. Optionally add upcoming earnings dates for event tracking

## 💡 Pro Tips

- **Use TTM EPS** for the most accurate P/E ratio calculations

- **Compare earnings line slope** with price movement to spot divergences

- **Enable earnings events** to prepare for volatility around announcements

- **Works best on daily/weekly timeframes** for fundamental analysis

## ⚠️ Data Availability

- Requires stocks with available fundamental data in TradingView's database

- Most major US stocks, ETFs, and international equities supported

- Limited data may be available for small-cap or recently listed companies

- Clear "No Data" indicator when fundamental data is unavailable

## 🎨 Display Features

- **High contrast colors** optimized for both light and dark chart themes

- **Clean, professional table** displaying all key metrics

- **Intuitive visual markers** for earnings events and data points

- **Responsive design** that adapts to different chart sizes

---

**Perfect for traders and investors who want to combine fundamental analysis with technical charting in a single, comprehensive view.**

## ⚠️ Important Disclaimer

**This indicator is provided for educational and informational purposes only. The author (raptor2030) is not responsible for:**

- **Data accuracy or completeness** - Financial data is sourced from TradingView's database and may contain errors, delays, or omissions

- **Trading decisions** - This tool should not be used as the sole basis for investment decisions

- **Financial losses** - Past performance does not guarantee future results

- **Data reliability** - Third-party data sources may experience outages or provide incorrect information

- **Market timing** - Earnings dates and projections may be inaccurate or outdated

**Always verify critical information from official company sources and consult with qualified financial professionals before making investment decisions.**

**Use this indicator at your own risk. The author disclaims all liability for any direct, indirect, or consequential damages arising from the use of this script.**