Icy-Hot Visual Indicator [SciQua]🧊 Icy-Hot Visual Indicator

This indicator colors your price bars and/or chart background based on a normalized & smoothed transform of any price-based input (default: close). It gives you a quick “temperature map” of market momentum or volatility—cool blues for low readings, hot reds for high readings—without cluttering your chart.

🔍 Key Features

1. Dual Visual Layers

Candle Gradient: Applies a smooth, multi-color gradient to candle bodies and wicks based on normalized, smoothed input data

Background Gradient: Adds a semi-transparent gradient behind the candles to highlight broader trend zones or volatility regimes

2. Advanced Customization

Normalization Types: bounded, unbounded, z-score, MAD, percentile, sigmoid, tanh, rank, robust, and more

Smoothing Methods: EMA, SMA, WMA, RMA, HMA, TEMA, VWMA, Gaussian, LinReg, ExpReg, and others (12+ options)

3. Gradient Control: Choose 2–7 color stops, reverse direction, adjust display length

Flexible Source Inputs

Use any built-in price series (close, hl2, volume, etc.)

Feed outputs from external indicators (RSI, custom oscillators, moving averages) into either layer

❓How It Works

Inputs are normalized (z-score, bounded, etc.) then smoothed (EMA, LinReg, etc.) in the order you choose. The result is clamped to 0–1 and passed through a multi-stop gradient engine for precise color mapping.

✨ What Makes It Original

While many indicators apply colors or smoothing, this script combines multi-stage normalization, adaptive smoothing, and a modular gradient rendering engine in a highly customizable dual-layer system. It’s built using proprietary functions from the SciQua suite that are not available in public libraries and allow for advanced visual encoding without relying on alerts, signals, or extra panes.

This makes it original in both design and execution—offering a visual-first approach with unique depth, clarity, and flexibility.

🔐 Why This Script Is Closed-Source

While the underlying functions are published in the open-source SciQua library, this indicator’s specific implementation, configuration architecture, and visual behavior are proprietary. It combines multiple library utilities into a dual-layer adaptive system that handles advanced gradient rendering, multi-stage normalization, and smoothing pipelines in a unique way.

The source is closed to protect the design logic, interface abstraction, and fine-tuned behaviors that make this indicator commercially valuable. The building blocks are open to the Pine community, but this assembled product is not meant for replication or redistribution.

How to Use It

1. Highlight Trend Strength

Source: RSI percentile

Setup: 200-bar look-back, mild smoothing

Result: Warm tones when momentum is peaking; cool when it’s fading. Use as a quick filter for entries in the direction of the trend.

2. Visualize Volatility Regimes

Source: ATR or True Range

Setup: Bounded normalization with tighter smoothing bar color off, bg color on.

Result: Background bands that shade when volatility spikes. Helps you avoid low-volatility breakouts or throttle position sizing in choppy markets.

3. Combine with Other Indicators

Source: Output of your custom indicator (e.g., a Keltner Band width)

Setup: Match normalization period to your strategy’s timeframe

Result: Bars colored by your own logic—no extra panes, just enhanced candles.

4. Background Only Heatmap

Turn off bar coloring and dial in semi-transparent background shades—keeps candles crisp while still giving you a context heat-map behind price.

Trend

TrendBoxThis indicator is called "TrendBox," designed to help traders analyze daily price ranges using several technical indicators. Below is a breakdown of its functionality, purpose, and key components:

Purpose

The script overlays indicators on a chart to assess whether the price is above or below key levels and moving in a trend.

VIX-based expected range (index fund targeted)

- This helps calculate the expected dealers range based on VIX implications. You can expect to see ranges be bought on and sold on. Moving outside this range creates heightened volatility and most of the time a gamma squeeze follows.

VWAP (Volume Weighted Average Price)

- This allows you to understand the mid point or average pricing of the daily session. If you're paying a premium or getting a discount on the daily session.

Daily Market Open

- Identifying the market open price is a key level on a daily session and allows you to identify some level of intraday trend.

Daily 4-period VWMA

- This is a crucial role of our indicator and showing short term time frame bias. Seeing price move over the top of our daily 4 level establishes a short term trend and can be used as a distribution guide, closing positions when we see longer time frame candles close under it. Vice versa for shorting.

It also displays a status box (optional) summarizing whether the price is above or below these levels, helping traders quickly evaluate market conditions.

Market Shift Levels [ChartPrime]Market Shift Levels

This indicator detects trend shifts and visualizes key market structure turning points using Hull Moving Average logic. It highlights potential areas of support and resistance where price is likely to react, empowering traders to spot early trend transitions.

Market Shift Levels are horizontal zones that mark the moment of a directional change in market behavior. These shifts are based on crossovers between two smoothed Hull Moving Averages (HMA), allowing the indicator to detect potential reversals with minimal lag.

Once a shift is detected:

A dashed horizontal Market Shift Level is plotted at the low (for bullish shift) or high (for bearish shift) of the candle.

These levels often become key reaction points during pullbacks and trend retests.

Volume or price labels are added when price wicks into these levels, helping traders gauge the strength of rejection or acceptance.

⯁ KEY FEATURES

Uses HMA-based logic to detect when price momentum shifts.

Plots clean Market Shift Levels (MSLs) that act as dynamic support and resistance.

Automatically colors bars and candles based on the price positioning relative to levels.

Labels wick-based retests with either:

Volume data of the 3-bar cluster (default).

Price level if toggled.

⯁ HOW TO USE

Look for trend shifts where the HMA crossover triggers a new level — this marks a possible structural pivot .

Use the horizontal level as a dynamic support or resistance zone — especially when price returns with wick rejections.

Watch for volume labels near the level — higher values signal stronger rejection and potential continuation.

Combine with confluence tools like Smart Money concepts or Fibonacci levels for added edge.

⯁ EXAMPLE SETUPS

After a bullish shift, wait for price to return and wick into the level — if volume spikes and candle closes strong, it’s a retest confirmation entry .

After a bearish shift, bearish wick rejections with volume may signal short re-entry zones .

⯁ CONCLUSION

The Market Shift Levels indicator offers a visual and data-backed approach to spotting trend reversals and critical retest zones. It’s a simple yet powerful tool to structure your trades around objective, repeatable market behavior — all in real-time.

Global Risk Matrix [QuantAlgo]🟢 Overview

The Global Risk Matrix is a comprehensive macro risk assessment tool that aggregates multiple global financial indicators into a unified risk sentiment framework. It transforms diverse economic data streams (from currency strength and liquidity measures to volatility indices and commodity prices) into standardized Z-Score readings to identify market regime shifts across risk-on and risk-off conditions.

The indicator displays both a risk oscillator showing weighted average sentiment and a dynamic 2D matrix visualization that plots signal strength against momentum to reveal current market phase and historical evolution. This helps traders and investors understand broad market conditions, identify regime transitions, and align their strategies with prevailing macro risk environments across all asset classes.

🟢 How It Works

The indicator employs Z-Score normalization across various global macro components, each representing distinct aspects of market liquidity, sentiment, and economic health. Raw data from sources like DXY, S&P 500, Fed liquidity, global M2 money supply, VIX, and commodities undergoes statistical standardization. Several components are inverted (USDT.D, DXY, VIX, credit spreads, treasury bonds, gold) to align with risk-on interpretation, where positive values indicate bullish conditions.

This unique system applies configurable weights to each component based on selected asset class presets (Crypto Investor/Trader, Stock Trader, Commodity Trader, Forex Trader, Risk Parity, or Custom), creating a weighted average Z-Score. It then analyzes both signal strength and momentum direction to classify market conditions into four distinct phases: Risk-On (positive signal, rising momentum), Risk-Off (negative signal, falling momentum), Recovery (negative signal, rising momentum), and Weakening (positive signal, falling momentum). The 2D matrix visualization plots these dimensions with historical trail tracking to show regime evolution over time.

🟢 How to Use

1. Risk Oscillator Interpretation and Phase Analysis

Positive Territory (Above Zero) : Indicates risk-on conditions with capital flowing toward growth assets and higher risk tolerance

Negative Territory (Below Zero) : Signals risk-off sentiment with capital seeking safety and defensive positioning

Extreme Levels (±2.0) : Represent statistically significant deviations that often precede regime reversals or trend exhaustion

Zero Line Crosses : Mark critical transitions between risk regimes, providing early signals for portfolio rebalancing

Phase Color Coding : Green (Risk-On), Red (Risk-Off), Blue (Recovery), Yellow (Weakening) for immediate regime identification

2. Risk Matrix Visualization and Trail Analysis

Current Position Marker (⌾) : Shows real-time location in the risk/momentum space for immediate situational awareness

Historical Trail : Connected path showing recent market evolution and regime transition patterns

Quadrant Analysis : Risk-On (upper right), Risk-Off (lower left), Recovery (lower right), Weakening (upper left)

Trail Patterns : Clockwise rotation typically indicates healthy regime cycles, while erratic movement suggests uncertainty

3. Pro Tips for Trading and Investing

→ Portfolio Allocation Filter : Use Risk-On phases to increase exposure to growth assets, small caps, and emerging markets while reducing defensive positions during confirmed green phases

→ Entry Timing Enhancement : Combine Recovery phase signals with your technical analysis for optimal long entry points when macro headwinds are clearing but prices haven't fully recovered

→ Risk Management Overlay : Treat Weakening phase transitions as early warning systems to tighten stop losses, reduce position sizes, or hedge existing positions before full Risk-Off conditions develop

→ Sector Rotation Strategy : During Risk-On periods, favor cyclical sectors (technology, consumer discretionary, financials) while Risk-Off phases favor defensive sectors (utilities, consumer staples, healthcare)

→ Multi-Timeframe Confluence : Use daily matrix readings for strategic positioning while applying your regular technical analysis on lower timeframes for precise entry and exit execution

→ Divergence Detection : Watch for situations where your asset shows bullish technical patterns while the matrix shows Risk-Off conditions—these often provide the highest probability short opportunities and vice versa

Trend Direction (OTC)Trend Direction (OTC)

Welcome, and thank you for your interest in the Trend Direction (OTC) indicator. This is a private, invite-only tool designed to provide a clear and objective view of market structure and trend dynamics.

Overview

The primary goal of Trend Direction (OTC) is to declutter your charts and help you visually identify the prevailing market trend through a sophisticated analysis of swing points. By automatically plotting key structural points in the market, it helps traders see the bigger picture and make more informed decisions based on classic price action principles.

This indicator is suitable for all markets (Forex, Crypto, Stocks, Indices) and works on any timeframe.

Features

Intelligent Swing Detection: Automatically identifies and plots significant market swing points.

Market Structure Labels (HH, LL, LH, HL): Get instant context on the trend's health. The indicator clearly labels swing points as Higher Highs (HH), Lower Lows (LL), Lower Highs (LH), and Higher Lows (HL), allowing you to see trend continuation and potential reversals at a glance.

Trend Dashboard: A simple, color-coded dashboard in the corner of your chart provides a real-time assessment of the trend, classifying it as "Confirmed," "Unconfirmed". This helps filter out market noise and provides an extra layer of confirmation.

Customizable Display: You have full control over the visual elements.

Adjust the sensitivity of the swing detection to focus on either short-term or long-term trends.

Toggle the visibility of trend lines and labels.

Limit the number of historical swings shown on the chart to keep your workspace clean.

Customize all colors to match your chart's theme.

How to Use

The Trend Direction (OTC) indicator is designed to be intuitive. Here’s a simple guide to interpreting its signals:

Identifying an Uptrend: Look for a consistent series of HH (Higher Highs) and HL (Higher Lows). The dashboard will likely show a "Bullish" status. A break of this pattern (e.g., the formation of an LH or LL) could signal a potential change in trend.

Identifying a Downtrend: Look for a consistent series of LH (Lower Highs) and LL (Lower Lows). The dashboard will likely show a "Bearish" status. A break of this pattern (e.g., the formation of an HL or HH) could signal that the downtrend is weakening.

Ranging or Choppy Markets: In sideways markets, you will see an alternating series of swings without clear direction. The dashboard will likely read "Neutral" or flip between "Unconfirmed" states. This can be useful for avoiding low-probability setups.

Settings

Swing Detection:

Pivot Lookback: The core setting for sensitivity. Higher values = less sensitive (major swings). Lower values = more sensitive (minor swings).

Display Options:

Show Swing Labels: Toggles the HH/LL/etc. labels.

Show Trend Lines: Toggles the zig-zag lines connecting the swings.

Show Last Swings: Set to 0 to see all historical swings, or enter a number to see only the most recent ones.

Color Settings: Customize the colors of all lines and labels to your preference.

Disclaimer: The Trend Direction (OTC) indicator is a tool for analysis and should not be considered financial advice. It is designed to assist in your trading decisions, not to make them for you. Always use proper risk management. Past performance is not indicative of future results.

Aqua MTF Trend Oscillator——————————————————————————————————————————————————————————

The Aqua Multi-Timeframe (MTF) Trend Oscillator is a comprehensive momentum and trend analysis tool designed to synthesize

complex market dynamics into a single, intuitive oscillator. It moves beyond single-timeframe analysis by aggregating

trend information from up to five distinct, user-configurable sources—spanning different timeframes, symbols, and

moving average types.

--- CORE CONCEPT ---

The strength and direction of a trend are rarely uniform across all market perspectives. This indicator's core

principle is to quantify and weigh the trend's character from multiple angles simultaneously. By blending these

perspectives, it generates a composite score that reflects the overall "consensus" of trend momentum, providing

a more robust view than any single moving average could offer alone.

--- METHODOLOGY ---

The indicator's power lies in its sophisticated, multi-step normalization process for each analysis slot:

1. **MA Calculation:** A standard moving average (e.g., EMA, SMA) is calculated for the specified source, symbol, and timeframe.

2. **Volatility-Normalized Distance:** It first measures the deviation of price from its moving average in terms

of Average True Range (ATR) units. This volatility-normalization step is crucial for comparing trend strength

across different timeframes or instruments, as it measures distance in a context-aware manner.

3. **Magnitude Squashing:** This ATR-based distance is then passed through a hyperbolic tangent (`tanh`) squashing

function. This elegantly transforms the potentially unbounded measurement into a standardized score oscillating

between -1 (maximum bearish magnitude) and +1 (maximum bullish magnitude). This prevents extreme outliers in one

timeframe from disproportionately skewing the final result.

4. **Weighted Aggregation:** Each of these normalized (-1 to +1) scores is then combined based on a user-defined

weight. The weighted average of all enabled slots produces the final composite score.

5. **Final Scaling & Smoothing:** The composite score is scaled to oscillate between -100 and +100. An optional

final smoothing pass can be applied to this master line to reduce noise and clarify the overall trend.

All higher-timeframe calculations are performed correctly within their native context to ensure the indicator is

non-repainting and provides a stable, reliable output on the chart.

--- KEY FEATURES ---

• **Five Independent Analysis Slots:** Fully customize up to five sources, each with its own symbol, timeframe, MA type, period, and weight.

• **Advanced Normalization:** Utilizes ATR and the hyperbolic tangent function for robust, comparable trend magnitude scores.

• **Correct MTF Calculation:** Employs best practices for non-repainting data requests, ensuring historical and real-time results are consistent.

• **Weighted Composite Score:** Assign importance to different timeframes to tailor the oscillator to your specific analytical needs.

• **Optional Master Smoothing:** Apply a final MA to the composite score line for enhanced clarity and signal filtering.

• **Clear Visualization:** A simple, color-coded oscillator line shows the final trend score, while individual component trends can also be plotted.

--- HOW TO INTERPRET ---

• **Zero Line Cross:** A cross above 0 indicates that the weighted balance of trend components has shifted to bullish. A cross below 0 signals a shift to bearish.

• **Oscillator Magnitude:** Values approaching +100 suggest a strong, broad-based uptrend consensus. Values nearing -100 indicate a strong downtrend consensus.

• **Slope:** The slope of the oscillator line indicates the accelerating or decelerating nature of the aggregate trend momentum.

• **Divergence:** As with any oscillator, watch for divergences between price action and the oscillator, which can signal a potential exhaustion of the prevailing trend.

Author: Aquaritek

——————————————————————————————————————————————————————————

Step Channel Momentum Trend [ChartPrime]OVERVIEW

Step Channel Momentum Trend is a momentum-based price filtering system that adapts to market structure using pivot levels and ATR volatility. It builds a dynamic channel around a stepwise midline derived from swing highs and lows. The system colors price candles based on whether price remains inside this channel (low momentum) or breaks out (strong directional flow). This allows traders to clearly distinguish ranging conditions from trending ones and take action accordingly.

⯁ STRUCTURAL MIDLNE (STEP CHANNEL CORE)

The midline acts as the backbone of the trend system and is based on structure rather than smoothing.

Calculated as the average of the most recent confirmed Pivot High and Pivot Low.

The result is a step-like horizontal line that only updates when new pivot points are confirmed.

This design avoids lag and makes the line "snap" to recent structural shifts.

It reflects the equilibrium level between recent bullish and bearish control.

This unique step logic creates clear regime shifts and prevents noise from distorting trend interpretation.

⯁ DYNAMIC VOLATILITY BANDS (ATR FILTERING)

To detect momentum strength, the script constructs upper and lower bands using the ATR (Average True Range):

The distance from the midline is determined by ATR × multiplier (default: 200-period ATR × 0.6).

These bands adjust dynamically to volatility, expanding in high-ATR environments and contracting in calm markets.

The area between upper and lower bands represents a neutral or ranging market state.

Breakouts outside the bands are treated as significant momentum shifts.

This filtering approach ensures that only meaningful breakouts are visually emphasized — not every candle fluctuation.

⯁ MOMENTUM-BASED CANDLE COLORING

The system visually transforms price candles into momentum indicators:

When price (hl2) is above the upper band, candles are green → bullish momentum.

When price is below the lower band, candles are red → bearish momentum.

When price is between the bands, candles are orange → low or no momentum (range).

The candle body, wick, and border are all colored uniformly for visual clarity.

This gives traders instant feedback on when momentum is expanding or fading — ideal for breakout, pullback, or trend-following strategies.

⯁ PIVOT-BASED SWING ANCHORS

Each confirmed pivot is plotted as a label ⬥ directly on the chart:

They also serve as potential manual entry zones, SL/TP anchors, or confirmation points.

⯁ MOMENTUM STATE LABEL

To reinforce the current market mode, a live label is displayed at the most recent candle:

Displays either:

“ Momentum Up ” when price breaks above the upper band.

“ Momentum Down ” when price breaks below the lower band.

“ Range ” when price remains between the bands.

Label color matches the candle color for quick identification.

Automatically updates on each bar close.

This helps discretionary traders filter trades based on market phase.

USAGE

Use the green/red zones to enter with momentum and ride trending moves.

Use the orange zone to stay out or fade ranges.

The step midline can act as a breakout base, pullback anchor, or bias reference.

Combine with other indicators (e.g., order blocks, divergences, or volume) to build high-confluence systems.

CONCLUSION

Step Channel Momentum Trend gives traders a clean, adaptive framework for identifying trend direction, volatility-based breakouts, and ranging environments — all from structural logic and ATR responsiveness. Its stepwise midline provides clarity, while its dynamic color-coded candles make momentum shifts impossible to miss. Whether you’re scalping intraday momentum or managing swing entries, this tool helps you trade with the market’s rhythm — not against it.

RMSE Bollinger Bands + Loop | Lyro RSRMSE Bollinger Bands + Loops

Overview

The RMSE Bollinger Bands + Loops is a sophisticated technical analysis tool designed to identify and quantify market trends by combining dynamic moving averages with statistical measures. This indicator employs a multi-model approach, integrating Bollinger-style RMSE bands, momentum scoring, and a hybrid signal system to provide traders with adaptive insights across varying market conditions.

Indicator Modes

Bollinger-style RMSE Bands: this mode calculates dynamic volatility bands around the price using the following formula:

Upper Band = Dynamic Moving Average + (RMSE × Multiplier)

Lower Band = Dynamic Moving Average - (RMSE × Multiplier)

These bands adjust to market volatility, helping identify potential breakout or breakdown points.

For-Loop Momentum Scoring, momentum is assessed by analyzing recent price behavior through a looping mechanism. A rising momentum score indicates increasing bullish strength, while a declining score suggests growing bearish momentum.

Hybrid Combined Signal: this mode assigns a directional score to the other two modes:

+1 for bullish (green)

–1 for bearish (red)

An average of these scores is computed to generate a combined signal, offering a consolidated market trend indication.

Practical Application

Signal Interpretation: A buy signal is generated when both the RMSE Bands and For-Loop Momentum Scoring align bullishly. Conversely, a sell signal is indicated when both are bearish.

Trend Confirmation: The Hybrid Combined Signal provides a consolidated view, assisting traders in confirming the prevailing market trend.

Note: Always consider additional technical analysis tools and risk management strategies when making trading decisions.

⚠️Disclaimer

This indicator is a tool for technical analysis and does not provide guaranteed results. It should be used in conjunction with other analysis methods and proper risk management practices. The creators of this indicator are not responsible for any financial decisions made based on its signals.

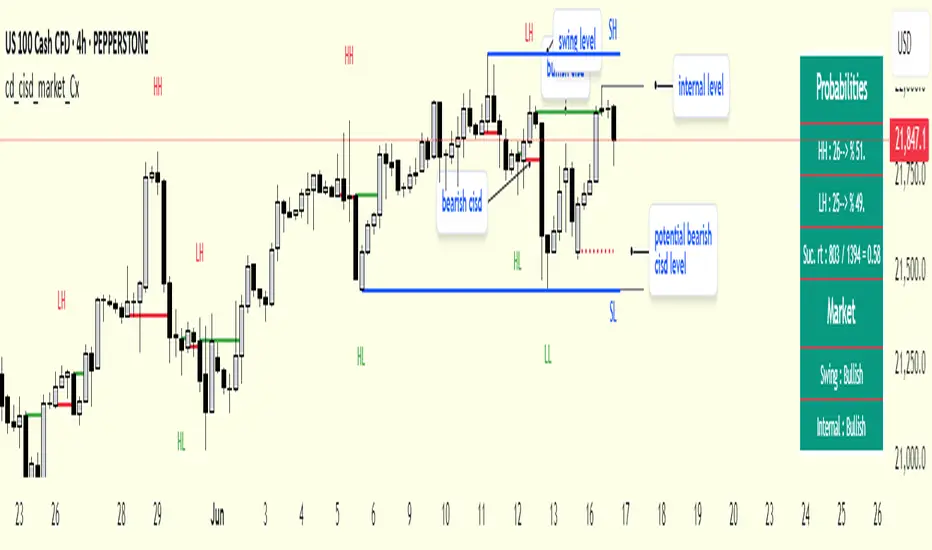

cd_cisd_market_CxHi Traders,

Overview:

Many traders follow market structure to identify the market direction and seek trade opportunities in line with the trend.

However, markings derived from user-defined inputs can create different structures, depending on personal choices. For instance, choosing a pivot distance of 3 instead of 2 alters the structure, even though the chart remains the same. Ideally, the structure should remain consistent.

"Change in State Delivery" ( CISD ) is a widely accepted concept among traders and is considered a significant indicator of market direction based on the gain/loss of CISD levels.

In this indicator, CISD is selected as the primary criterion for marking market structure, eliminating the influence of user-dependent variations.

Here is a summary of the key logic and rules applied:

• When the price forms a new high/low, that level is only considered a pivot if a CISD has occurred.

• A bullish CISD is always followed by a bearish CISD, and vice versa.

• Pivot points form the internal structure.

• The internal structure is used to interpret the swing structure.

• Probabilities are derived from internal structure patterns.

________________________________________

Details:

How is CISD determined?

As is commonly known:

• When price makes a new high, the opening level of the first candle in the consecutive bullish candle sequence is marked.

• When price makes a new low, the opening of the first candle in the consecutive bearish sequence is marked.

• If there’s only one candle in the sequence, its opening level is used.

In a bullish market, losing a bearish CISD level (i.e., a close below it) or in a bearish market, gaining a bullish CISD level (i.e., a close above it) is interpreted as a potential shift in buyer-seller dominance and a possible market reversal.

________________________________________

How are internal (pivot) levels determined?

• When price closes below a bearish CISD level, the highest candle's high becomes a pivot high (PH).

• When price closes above a bullish CISD level, the lowest candle's low becomes a pivot low (PL).

• If the new PH is above the previous PH, it’s labeled as HH (Higher High); otherwise, LH (Lower High).

• If the new PL is below the previous PL, it’s labeled as LL (Lower Low); otherwise, HL (Higher Low).

________________________________________

Internal Market Structure:

• A series of HHs indicates a bullish internal structure.

• A series of LLs indicates a bearish internal structure.

________________________________________

Swing (Main) Market Structure:

Using internal pivots and previous swing levels, the main market structure is derived.

• A new swing high (SH) requires the price to move above the previous SH.

• A new swing low (SL) requires the price to move below the previous SL.

________________________________________

Probability Calculation:

Pivot levels forming the internal structure are coded as five-element sequences.

There are 64 possible combinations of such sequences made from consecutive PH and PL values.

Each pattern’s frequency from its starting candle is tracked.

To make it more understandable:

For example, after the four-sequence “HH, LL, LH,HL”, either HH or LH might follow.

The table shows the statistical likelihood of both possible outcomes for the most recent four-element sequence on the chart.

________________________________________

How reliable is it?

To assess reliability, results are calculated from the beginning using:

Success Rate (Suc. Rt) = Number of Correct Predictions / Total Predictions

This value is added to the table for reference.

It’s important to note that no statistical outcome guarantees certainty—every result offers a different interpretation. What truly matters is to avoid getting stopped out 😊.

________________________________________

Menu Options:

Show/hide preferences and color selections can be customized via the indicator menu.

________________________________________

What’s Coming in Future Versions?

Features such as FVG (Fair Value Gaps) between swing levels, volume imbalances, order blocks / mitigation blocks, Fibonacci levels, and relevant trade suggestions will be added.

________________________________________

This is a BETA version that I believe will help simplify your market reading. I’d be happy to hear your feedback and suggestions.

Cheerful Trading!

Trend Blend

Trend blend is my new indicator. I use it to identify my bias when trading and filter out fake setups that are going in the wrong direction.

Trend blend utilises the 9 EMA (Red), 21 EMA (Black), and if you trade futures or Bitcoin, you can also use the VWAP (Blue).

There is also a table at the top right that displays the chart time frame bias

I prefer to use the 1-hour time frame for bias and execute the trades on 5-minute charts, mainly, and sometimes on the 1-minute for a smaller stoploss.

Here's an example of the trade I took during the London session on XAU/USD

1 hour bias was Bearish

Price broke out of the range

I waited for the London session to open, where I ended up taking a short on the 5-minute time frame as we broke out of the pre-London range

Entry was at the Fair Value Gap (5-minute bias was also Bearish as price traded into the FVG)

Stoploss was at the last high

Take Profit was the next major support level

Another set that I like to trade with the Trend blend is when price is trending bullish and price trades inside the 9 and 21 EMA, and there is a bullish candle closer above the 9 EMA with Stoploss below the low of the bullish candle and Take profit between 1-2 Risk to Reward

Same when there's a bearish trend, I wait for price to trade inside the 9 and 21 EMA, and I'll take sells when a bearish candle closes below the 9 EMA.

This setup works best in strong trends, or it can be used to enter a trade on a pullback or to scale into an existing trade.

Consolidation Zones[RanaAlgo]Overview

This indicator helps traders identify price consolidation zones (ranges) and potential breakouts in the market. It is useful for spotting periods of low volatility before significant price movements.

How It Works

Detects Consolidation Zones

Uses the ADX (Average Directional Index) to determine when the market is in a consolidation phase .

When ADX is below the threshold , the indicator marks the start of a consolidation zone.

Draws a semi-transparent box around the price range, adjusting its height as new highs/lows form.

Tracks Breakouts

When price breaks above/below the consolidation box, it signals a potential trend continuation.

Displays breakout arrows/labels (configurable shape & style) when price exits the range.

Visual Features

Boxes highlight consolidation areas (customizable color, border, and style).

Labels show real-time status ("CONSOLIDATING" or "TRENDING").

Breakout signals appear as arrows or shapes (up/down).

Usefulness in Trading

Range Trading: Helps traders identify sideways markets for buying low and selling high.

Breakout Trading: Signals potential trend entries when price exits consolidation.

Trend Confirmation: Low ADX + consolidation box = weak trend; breakout = possible trend start.

Example: If price stays in a blue box (consolidation) and then breaks above with an arrow, it suggests a bullish move.

RSI Buy Sell Signals+ with MFI Cloud [RanaAlgo]Indicator Overview

This indicator combines RSI (Relative Strength Index) with MFI (Money Flow Index) to generate trading signals with additional confirmation filters. The key features include:

RSI Analysis (14-period) with overbought/oversold levels

MFI Cloud (20-period default) showing trend direction via EMAs

Enhanced Signal Generation with volume and trend confirmation options

Visual Elements including colored zones, signal labels, and an information panel

How to Use This Indicator

Basic Interpretation:

Buy Signals (green labels) appear when:

RSI crosses above oversold level (30) OR

RSI shows a rising pattern from oversold zone with volume/trend confirmation (if enabled)

Sell Signals (red labels) appear when:

RSI crosses below overbought level (70) OR

RSI shows a falling pattern from overbought zone with volume/trend confirmation (if enabled)

MFI Cloud provides trend confirmation:

Green cloud = bullish trend (fast EMA > slow EMA)

Red cloud = bearish trend (fast EMA < slow EMA)

Recommended Usage:

For Conservative Trading:

Enable both volume and trend confirmation

Require MFI cloud to align with signal direction

Wait for RSI to clearly exit overbought/oversold zones

For Active Trading:

Combine with price action at key support/resistance levels

Watch for divergence between price and RSI

The Information Panel (top-right) shows:

Current RSI value and status

MFI trend direction

Last generated signal

Current momentum

Customization Options:

Adjust RSI/MFI lengths for sensitivity

Modify overbought/oversold levels

Toggle volume/trend confirmation requirements

Adjust visual elements like cloud opacity and zone visibility

MACD Support and Resistance [ChartPrime]⯁ OVERVIEW

MACD Support and Resistance is a dynamic support/resistance mapping tool powered by MACD crossover logic. Each time the MACD line crosses the signal line, the indicator scans for recent price extremes and locks them in as potential support or resistance zones. These levels are automatically cleaned up if price breaks them, keeping the chart focused on active market structure. The system includes a built-in MACD display with visual markers, along with contextual highs and lows to help define the current environment.

⯁ MACD-BASED SUPPORT/RESISTANCE GENERATION

The core logic uses the MACD oscillator crossover as a trigger event to generate structural levels:

When MACD crosses above its signal line:

→ The script scans the last 5 bars for the lowest low .

→ A support level is plotted at that price.

When MACD crosses below its signal line:

→ The script scans the last 5 bars for the highest high .

→ A resistance level is plotted at that price.

These dynamic levels reflect where price recently reversed or paused, making them prime zones for reaction, continuation, or invalidation.

⯁ LEVEL MANAGEMENT AND VALIDATION

To keep the chart clean and relevant:

A maximum of 20 active levels are allowed at once.

Older levels are automatically removed if the list exceeds the limit.

If price closes below a support level or above a resistance level , the corresponding line is deleted.

This ensures that only currently respected levels remain on the chart — a major advantage for active traders.

⯁ MACD VISUALIZATION + SIGNAL MARKERS

A full MACD system is rendered on the lower panel for visual confirmation:

The MACD line and Signal line are both plotted and color-coded dynamically.

A filled area] highlights the spread between them to emphasize momentum strength.

A diamond marker is drawn each time MACD crosses its signal line, alerting traders to potential trend shifts.

These visuals make it easy to understand the timing of the support/resistance updates.

⯁ LOCAL EXTREME REFERENCE LINES

To help contextualize current price position relative to recent market extremes:

A Local High line is plotted based on the highest MACD value over the past 100 bars].

A Local Low line is plotted based on the lowest MACD value over the past 100 bars].

These levels are rendered lightly and serve as dynamic range boundaries.

They assist traders in identifying overextended or compressed MACD behavior.

⯁ USAGE

Use the generated S/R levels as breakout or reversal zones.

Watch for MACD diamond markers to confirm the timing of new levels.

Combine these reactive zones with other ChartPrime confluence tools for higher-confidence entries.

Use the Local High/Low zones as a volatility envelope to guide risk and trend continuation potential.

⯁ CONCLUSION

MACD Support and Resistance takes a classic momentum indicator and adds real-time structural awareness. By linking MACD crossover events to recent price extremes, it identifies the zones where market sentiment shifted — and continues to monitor their strength. Whether you're a breakout trader or looking to fade key reaction points, this tool delivers clean, actionable levels based on momentum and structure — not guesswork.

ATR RopeATR Rope is inspired by DonovanWall's "Range Filter". It implements a similar concept of filtering out smaller market movements and adjusting only for larger moves. In addition, this indicator goes one step deeper by producing actionable zones to determine market state. (Trend vs. Consolidation)

> Background

When reading up on the Range Filter indicator, it reminded me exactly of a Rope stabilization drawing tool in a program I use frequently. Rope stabilization essentially attaches a fixed length "rope" to your cursor and an anchor point (Brush). As you move your cursor, you are pulling the brush behind it. The cursor (of course) will not pull the brush until the rope is fully extended, this behavior filters out jittery movements and is used to produce smoother drawing curves.

If compared visually side-by-side, you will notice that this indicator bears striking resemblance to its inspiration.

> Goal

Other than simply distinguishing price movements between meaningful and noise, this indicator strives to create a rigid structure to frame market movements and lack-there-of, such as when to anticipate trend, and when to suspect consolidation.

Since the indicator works based on an ATR range, the resulting ATR Channel does well to get reactions from price at its extremes. Naturally, when consolidating, price will remain within the channel, neither pushing the channel significantly up or down. Likewise, when trending, price will continue to push the channel in a single direction.

With the goal of keeping it quick and simple, this indicator does not do any smoothing of data feeds, and is simply based on the deviation of price from the central rope. Adjusting the rope when price extends past the threshold created by +/- ATR from the rope.

> Features & Behaviors

- ATR Rope

ATR Rope is displayed as a 3 color single line.

This can be considered the center line, or the directional line, whichever you'd prefer.

The main point of the Rope display is to indicate direction, however it also is factually the center of the current working range.

- ATR Rope Color

When the rope's value moves up, it changes to green (uptrend), when down, red (downtrend).

When the source crosses the rope, it turns blue (flat).

With these simple rules, we've formed a structure to view market movements.

- Consolidation Zones

Consolidation Zones generate from "Flat" areas, and extend into subsequent trend areas. Consolidation is simply areas where price has crossed the Rope and remains inside the range. Over these periods, the upper and lower values are accumulated and averaged together to form the "Consolidation Zone" values. These zones are draw live, so values are averaged as the flat areas progress and don't repaint, so all values seen historically are as they would appear live.

- ATR Channel

ATR Channel displays the upper and lower bounds of the working range.

When the source moves beyond this range, the rope is adjusted based on the distance from the source to the channel. This range can be extremely useful to view, but by default it is hidden.

> Application

This indicator is not created to provide signals, or serve as a "complete" system.

(People who didn't read this far will still comment for signals. :) )

This is created to be used alongside manual interpretation and intuition. This indicator is not meant to constrain any users into a box, and I would actually encourage an open mind and idea generation, as the application of this indicator can take various forms.

> Examples

As you would probably already know, price movement can be fast impulses, and movement can be slow bleeds. In the screenshot below, we are using movements from and to consolidation zones to classify weak trend and strong trend. As you can see, there are also areas of consolidation which get broken out of and confirmed for the larger moves.

Author's Note: In each of these examples, I have outlined the start and end of each session. These examples come from 1 Min Future charts, and have specifically been framed with day trading in mind.

"Breakout Retest" or "Support/Resistance Flips" or "Structure Retests" are all generally the same thing, with different traders referring to them by different names, all of which can be seen throughout these examples.

In the next example, we have a day which started with an early reversal leading into long, slow, trend. Notice how each area throughout the trend essentially moves slightly higher, then consolidates while holding support of the previous zone. This day had a few sharp movements, however there was a large amount of neutrality throughout this day with continuous higher lows.

In contrast to the previous example, next up, we have a very choppy day. Throughout which we see a significant amount of retests before fast directional movements. We also see a few examples of places where previous zones remained relevant into the future. While the zones only display into the resulting trend area, they do not become immediately meaningless once they stop drawing.

> Abstract

In the screenshot below, I have stacked 2 of these indicators, using the high as the source for one and the low as the source for the other. I've hidden lines of the high and low channels to create a 4 lined channel based on the wicks of price.

This is not necessary to use the indicator, but should help provide an idea of creative ways the simple indicator could be used to produce more complicated analysis.

If you've made it this far, I would hope it's clear to you how this indicator could provide value to your trading.

Thank you to DonovonWall for the inspiration.

Enjoy!

SimpleBiasSimpleBias - Multi-Timeframe Bias Analysis Indicator

Overview

SimpleBias is a comprehensive multi-timeframe bias analysis indicator designed to help traders make informed trading decisions by displaying market bias across multiple timeframes in a clean, organized table format.

Key Features

Multi-Timeframe Analysis

8 Timeframes Supported : 1M, 1W, 1D, 4H, 1H, 15m, 5m, 1m

Adaptive Display : Shows only relevant timeframes based on current chart timeframe

Real-time Bias Detection : Compares current open price with previous period's open price

Signal Generation

Day Trading Mode : Ideal for 15-minute timeframe analysis

Scalping Mode : Optimized for 5-minute timeframe trading

Signal OFF : Pure bias analysis without trade signals

Customization Options

Theme Support : Light mode and dark mode with automatic color adaptation

Position Control : Table can be positioned at top-right, middle-right, or bottom-right

Size Options : Tiny, small, or normal text size

Color Customization : Full control over bias colors, signal colors, and interface elements

Transparency : Optional transparent background for cleaner chart appearance

How It Works

Bias Calculation

The indicator determines market bias by comparing the current timeframe's open price with the previous period's open price:

BULLISH : Current open > Previous open

BEARISH : Current open < Previous open

NEUTRAL : Current open = Previous open

Adaptive Timeframe Display

The indicator intelligently shows only relevant timeframes based on your current chart:

On 1M chart: Shows 1M bias only

On 1W chart: Shows 1M, 1W bias

On 1D chart: Shows 1M, 1W, 1D bias

And so on...

Signal Logic

Day Trading : Compares current price with 4H open price

Scalping : Compares current price with 1H open price

Usage Instructions

Add to Chart : Apply the indicator to any timeframe chart

Configure Settings :

- Choose table position and text size

- Select signal mode (OFF/Day Trade/Scalping)

- Customize colors and theme

Interpret Results :

- Green/Blue text = Bullish bias

- Red text = Bearish bias

- Gray text = Neutral bias

Customization Guide

Theme Settings

Light Mode : Traditional white background with dark text

Dark Mode : Dark background with light text, optimized for dark charts

Transparent Background : Clean overlay without background color

Color Schemes

Bias Colors : Separate customization for bullish, bearish, and neutral bias

Signal Colors : Distinct colors for buy, sell, and neutral signals

Interface : Control table background and border colors

Best Practices

For Day Trading

Use 15-minute or 1-hour charts

Enable "Day Trade" signal mode

Focus on 4H and higher timeframe bias alignment

For Scalping

Use 5-minute charts

Enable "Scalping" signal mode

Watch for 1H and 4H bias alignment

For Swing Trading

Use 4H or daily charts

Keep signal mode OFF

Focus on weekly and monthly bias alignment

Important Notes

This indicator is for educational and analysis purposes only

Not financial advice - always do your own research

Past performance does not guarantee future results

Risk management is essential in all trading activities

Technical Specifications

Pine Script Version : v6

Overlay : True (displays on price chart)

Performance : Optimized with cached security requests

Compatibility : Works on all TradingView timeframes and instruments

---

SimpleBias - Indikator Analisis Bias Multi-Timeframe

Gambaran Umum

SimpleBias adalah indikator analisis bias multi-timeframe yang komprehensif, dirancang untuk membantu trader membuat keputusan trading yang tepat dengan menampilkan bias pasar di berbagai timeframe dalam format tabel yang bersih dan terorganisir.

Fitur Utama

Analisis Multi-Timeframe

8 Timeframe Didukung : 1M, 1W, 1D, 4H, 1H, 15m, 5m, 1m

Tampilan Adaptif : Hanya menampilkan timeframe yang relevan berdasarkan timeframe chart saat ini

Deteksi Bias Real-time : Membandingkan harga open saat ini dengan harga open periode sebelumnya

Mode Sinyal Trading

Mode Day Trading : Ideal untuk analisis timeframe 15 menit

Mode Scalping : Dioptimalkan untuk trading timeframe 5 menit

Mode OFF : Analisis bias murni tanpa sinyal trading

Opsi Kustomisasi

Dukungan Theme : Mode terang dan gelap dengan adaptasi warna otomatis

Kontrol Posisi : Tabel dapat diposisikan di kanan-atas, kanan-tengah, atau kanan-bawah

Opsi Ukuran : Ukuran teks kecil, sedang, atau normal

Kustomisasi Warna : Kontrol penuh atas warna bias, warna sinyal, dan elemen interface

Transparansi : Background transparan opsional untuk chart yang lebih bersih

Cara Kerja

Perhitungan Bias

Indikator menentukan bias pasar dengan membandingkan harga open timeframe saat ini dengan harga open periode sebelumnya:

BULLISH : Open saat ini > Open sebelumnya

BEARISH : Open saat ini < Open sebelumnya

NEUTRAL : Open saat ini = Open sebelumnya

Petunjuk Penggunaan

Tambahkan ke Chart : Terapkan indikator ke chart timeframe apapun

Konfigurasi Settings :

- Pilih posisi tabel dan ukuran teks

- Pilih mode sinyal (OFF/Day Trade/Scalping)

- Sesuaikan warna dan theme

Interpretasi Hasil :

- Teks hijau/biru = Bias bullish

- Teks merah = Bias bearish

- Teks abu-abu = Bias neutral

Best Practices

Untuk Day Trading

Gunakan chart 15 menit atau 1 jam

Aktifkan mode sinyal "Day Trade"

Fokus pada alignment bias timeframe 4H ke atas

Untuk Scalping

Gunakan chart 5 menit

Aktifkan mode sinyal "Scalping"

Perhatikan alignment bias 1H dan 4H

Catatan Penting

Indikator ini hanya untuk tujuan edukasi dan analisis

Bukan nasihat keuangan - selalu lakukan riset sendiri

Performa masa lalu tidak menjamin hasil masa depan

Manajemen risiko sangat penting dalam semua aktivitas trading

SimpleBias membantu trader mempertahankan kesadaran terhadap bias pasar di berbagai timeframe, mendukung timing dan pengambilan keputusan yang lebih baik dalam strategi trading mereka.

Hot Zones Indicator [ChartPrime]Hot Zones (Basic) is a precision-engineered confluence detection system that identifies statistically significant price reaction zones by mapping retracement levels enriched with structural, volumetric, and momentum-based overlays. In contrast to static Fibonacci tools, this system dynamically synchronizes a custom volume-weighted average price inspired overlay and localized oscillator signals to produce probabilistically favorable “hot zones” that respond to real-time market structure.

These zones are visually enhanced when multiple dimensions of market confluence align—such as volume-weighted price agreement, structural symmetry, and volatility-based momentum extremes—allowing for immediate prioritization of high-probability reaction areas.

Core Concept

The system autonomously detects impulse-correction phases within the price series using directional breakout logic and multi-bar structural analysis. Once a valid trend leg is established, standard retracement levels are plotted along the vector. These levels are continuously evaluated against live price interaction, volume alignment, and momentum state.

Swing Initialization Logic

Automated Structural Anchoring: Swing points are detected using fractal pivot analysis and breakout validation. The tool anchors retracement vectors to recent directional legs with the highest structural integrity.

Volume-Weighted Price Confluence

Two VWAP-derived overlays are applied:

Anchored Volume Level: Derived from the origin of the leg, reflecting the volume-weighted cost basis of major participants over the structural phase.

Internal VWAP: Triggered on intermediate pullbacks, mapping localized institutional activity through recursive anchoring logic.

When either curve aligns with a retracement level under live market conditions, the level is flagged as a high-confluence reaction zone.

Momentum & Volatility Filtering

A proprietary oscillator—optimized for mean deviation and multi-resolution smoothing—is integrated to quantify local volatility states and directional momentum.

The oscillator feeds into two distinct signal regimes:

Directional Crossovers: When a significant momentum shift occurs within a mapped levels, the zone is annotated accordingly with a directional labeling "⬆" or "⬇".

Momentum Extremes: OB/OS thresholds are used to detect compression or exhaustion states, enhancing zone validity under directional stress.

These signals are visually merged into the zone rendering, enabling contextual clarity at a glance.

Customization & Advanced Features

Individual fib levels can be toggled or styled per user preference.

Aesthetic properties (color, line width) are fully configurable.

An optional “Hacker Zone” region—highlighting retracement areas statistically associated with institutional accumulation also known as Golden Pocket — is available for advanced users.

Conclusion

Hot Zones by ChartPrime represents a multi-dimensional confluence engine, transforming traditional retracement mapping into a reactive, data-driven framework. By integrating structure, volume flow, and momentum analytics into a unified interface, it enhances discretionary and systematic trading decisions alike. Whether trading trend continuations, reversals, or liquidity anomalies, Hot Zones enables actionable clarity at structurally significant levels.

Volume Momentum [BackQuant]Volume Momentum

The Volume Momentum indicator is designed to help traders identify shifts in market momentum based on volume data. By analyzing the relative volume momentum, this indicator provides insights into whether the market is gaining strength (uptrend) or losing momentum (downtrend). The strategy uses a combination of percentile-based volume normalization, weighted moving averages (WMA), and exponential moving averages (EMA) to assess volume trends.

The system focuses on the relationship between price and volume, utilizing normalized volume data to highlight key market changes. This approach allows traders to focus on volume-driven price movements, helping them to capture momentum shifts early.

Key Features

1. Volume Normalization and Percentile Calculation:

The signed volume (positive when the close is higher than the open, negative when the close is lower) is normalized against the rolling average volume. This normalized volume is then subjected to a percentile interpolation, allowing for a robust statistical measure of how the current volume compares to historical data. The percentile level is customizable, with 50 representing the median.

2. Weighted and Smoothed Moving Averages for Trend Detection:

The normalized volume is smoothed using weighted moving averages (WMA) and exponential moving averages (EMA). These smoothing techniques help eliminate noise, providing a clearer view of the underlying momentum. The WMA filters out short-term fluctuations, while the EMA ensures that the most recent data points have a higher weight, making the system more responsive to current market conditions.

3. Trend Reversal Detection:

The indicator detects momentum shifts by evaluating whether the volume momentum crosses above or below zero. A positive volume momentum indicates a potential uptrend, while a negative momentum suggests a possible downtrend. These trend reversals are identified through crossover and crossunder conditions, triggering alerts when significant changes occur.

4. Dynamic Trend Background and Bar Coloring:

The script offers customizable background coloring based on the trend direction. When volume momentum is positive, the background is colored green, indicating a bullish trend. When volume momentum is negative, the background is colored red, signaling a bearish trend. Additionally, the bars themselves can be colored based on the trend, further helping traders quickly visualize market momentum.

5. Alerts for Momentum Shifts:

The system provides real-time alerts for traders to monitor when volume momentum crosses a critical threshold (zero), signaling a trend reversal. The alerts notify traders when the market momentum turns bullish or bearish, assisting them in making timely decisions.

6. Customizable Parameters for Flexible Usage:

Users can fine-tune the behavior of the indicator by adjusting various parameters:

Volume Rolling Mean: The period used to calculate the average volume for normalization.

Percentile Interpolation Length: Defines the range over which the percentile is calculated.

Percentile Level: Determines the percentile threshold (e.g., 50 for the median).

WMA and Smoothing Periods: Control the smoothing and response time of the indicator.

7. Trend Background Visualization and Trend-Based Bar Coloring:

The background fill is shaded according to whether the volume momentum is positive or negative, providing a visual cue to indicate market strength. Additionally, bars can be color-coded to highlight the trend, making it easier to see the trend’s direction without needing to analyze numerical data manually.

8. Note on Mean-Reversion Strategy:

If you take the inverse of the signals, this indicator can be adapted for a mean-reversion strategy. Instead of following the trend, the strategy would involve buying assets that are underperforming and selling assets that are overperforming, based on volume momentum. However, it’s important to note that this approach may not work effectively on highly correlated assets, as their price movements may be too similar, reducing the effectiveness of the mean-reversion strategy.

Final Thoughts

The Volume Momentum indicator offers a comprehensive approach to analyzing volume-based momentum shifts in the market. By using volume normalization, percentile interpolation, and smoothed moving averages, this system helps identify the strength and direction of market trends. Whether used for trend-following or adapted for mean-reversion, this tool provides traders with actionable insights into the market’s volume-driven movements, improving decision-making and portfolio management.

Candle Body TableCandle Body Table is a lightweight, easy-to-use indicator that displays a live summary of candle “body strength” across multiple timeframes, along with how much time is left on each candle. Simply choose up to five timeframes (1, 5, 15, 30, and 60 minutes by default), adjust the table’s corner and font size, and you’ll always have a quick, at-a-glance view of:

OC (Body %): The percentage of the candle that’s composed of its body (|open – close| divided by high–low).

Strength: A label (Weak, Balanced, or Strong) based on the body percentage.

Time Left: How many minutes and seconds remain before the current candle closes.

The table updates in real time (using lookahead), coloring each row background green if that timeframe’s current candle is bullish, or red if it’s bearish. That way, you can instantly see which timeframes have strong momentum, which are balanced or weak, and exactly when each candle will finish.

Use Cases

Multi-Timeframe Momentum Check:

If you want to confirm that both your 1m and 5m candles have “Strong” bodies before entering a trade, Candle Body Table shows you that instantly. No more switching back and forth between charts—just glance at the table.

Time-Sensitive Entries/Exits:

Suppose you trade breakouts only at the close of a 5-minute candle. The “Time Left” column counts down so you know exactly when that candle is about to close—down to the second—letting you prepare your order.

Quick Visual Scan:

When markets are choppy, you may want to see which timeframes are weak or balanced rather than diving into each timeframe separately. If the 15m row says “Weak” (small body %), you might avoid taking a trend-following position at that moment.

Session Overlaps & Volatility Windows:

During London/N.Y. overlap or U.S. cash close, traders often check for stronger bodies on higher timeframes (e.g., 30m or 60m). The table immediately highlights if that timeframe’s candle body heats up, indicating increased volatility.

Swing-to-Scalp Transition:

If you typically scalp on 1m but only when the 15m candle is “Strong,” this table gives a green/red cue and a strength label. That makes it easier to wait patiently until multiple timeframes align.

FAQ

Q1. What does “OC” mean, and why is it shown as a percentage?

A1. “OC” stands for Open/Close difference. So it reflects how much of the candle’s total range (high–low) is taken up by its body(open-close). A high OC% means the candle body is large relative to its wick. In other words a strong Bullish/Bearish candle.

Q2. How is “Strength” determined?

A2. The script uses three buckets:

Weak if OC% ≤ 30%

Balanced if 30% < OC% ≤ 55%

Strong if OC% > 55%

This gives you a quick label instead of having to interpret raw percentages every time.

Q3. Why do some rows have a green background and others red?

A3. If close > open (bullish candle), that entire row’s background is shaded green(70%). If close < open (bearish candle), it’s shaded red(70%). If open = close (doji), there’s no background shade. This lets you instantly spot bullish vs. bearish candles across your chosen timeframes.

Q4. Will this repaint?

A4. No. Because each OHLC value is requested with lookahead_on, you see the live developing OHLC. However, once a candle closes, those values are final. The “Time Left” column dynamically changes throughout the bar but does not redraw past values.

LRCLRC (Linear Regression Candle)

Overview

The LRC (Linear Regression Candle) indicator applies linear regression to the open, high, low, and close prices, creating smoothed "candles" that help filter market noise. It provides trend-confirmation signals and highlights potential reversal points based on regression crossovers.

Key Features

Smoothed Candles: Uses linear regression to calculate synthetic OHLC values, reducing noise.

Multi-Timeframe Support: Optional higher timeframe analysis for better trend confirmation.

Visual Signals: Color-coded candles and labels highlight bullish/bearish control zones.

Customizable Settings: Adjustable regression length, colors, and timeframe options.

How to Use

Signals & Interpretation

🟢 Bullish Signal (BUY): When the regression open crosses above the regression close (green candle).

🔴 Bearish Signal (SELL): When the regression open crosses below the regression close (red candle).

Control Zones:

Strong Bullish (Controlbull): Confirmed uptrend (bright green).

Bullish (Bull): Regular uptrend (light green).

Strong Bearish (Controlbear): Confirmed downtrend (dark red).

Bearish (Bear): Regular downtrend (orange).

Neutral (Gray): No clear trend.

Recommended Settings

Linear Regression Length: Default 8 (adjust for sensitivity).

Timeframe: Default current chart, but can switch to higher timeframes (e.g., 1D, 1W).

Bar Colors: Toggle on/off for visual clarity.

Labels: Displays "Control" markers at key reversal points.

Example Use Cases

Trend Confirmation: Use higher timeframe LRC to validate the primary trend.

Reversal Signals: Watch for BUY/SELL crossovers with strong color confirmation.

Noise Reduction: Helps avoid false breakouts in choppy markets.

FVG Trailing Stop [LuxAlgo]The FVG Trailing Stop indicator tracks unmitigated Fair Value Gaps (FVG) data to produce a Trailing Stop indicator able to determine if the market is uptrending or downtrending easily.

🔶 USAGE

The FVG Trailing Stop is intended to identify trend directions through its position relative to the closing price:

Bullish: Price is located above the Trailing Stop, indicating that all Bearish FVGs have been mitigated and the trend is anticipated to continue upwards.

Bearish State: Price is located below the Trailing Stop, indicating that all Bullish FVGs have been mitigated and the trend is anticipated to continue downwards.

The Trailing Stop originates from two extremities obtained from the average of respective unmitigated FVGs. The specific directional average is also displayed as a more transparent secondary line, however, the trailing stop is derived from this value and a new trend will not be detected until the opposite directional average is crossed.

Price reaching the Trailing Stop is caused by retracements and can lead to the following scenarios:

Outcome 1: The directional average is crossed next, indicating a new trend direction.

Outcome 2: The directional average is held as support or resistance, leading to a new impulse and a continuation of the trend.

🔹 Reset on Cross

While price crossing the Trailing Stop should be considered as a sign of an upcoming trend change; it is possible for the price to still evolve outside it.

As a solution, we have included the "Reset on Cross" feature, which (as the name suggests) hides and resets the Trailing Stop each time it is crossed, leading to a "Neutral" state.

This opens the opportunity for the Trailing Stop to be displayed again once the price moves again in the direction of the pre-established trend. A trader might use this to accumulate positions within a specific trend.

🔶 DETAILS

The script uses a typical identification method for FVGs. Once identified, the script collects the point of the FVG farthest from the current price when formed.

For Upwards FVGs this is the bottom of the FVG.

For Downwards FVGs this is the top of the FVG.

The data is managed only to use the last input lookback of FVGs. If an FVG is mitigated, it frees up a spot in the memory for a new FVG, however, if the lookback is full, the oldest will be deleted.

From there, it uses a "trailing" logic only to move the Trailing Stop in one direction until the trailing stop resets or the direction flips.

The extremities used to calculate the Trailing Stop are created from 2 calculation steps, the first step involves taking the raw average of the FVG mitigation levels, and the second step applies a simple moving average (SMA) smoothing of the precedent-obtained averages.

🔶 SETTINGS

Unmitigated FVG Lookback: Sets the maximum number of Unmitigated FVGs that the script will use.

Smoothing Length: Sets the smoothing length for the Trailing Stop to reduce erratic results.

Reset on Cross: When enabled, hide and reset the Trailing Stop until the price starts moving in the pre-established trend direction again.

MTF 5 Big Candles [RanaAlgo]Overview

This Pine Script indicator displays multiple timeframe (MTF) candlesticks from 5 different timeframes on your current chart. It helps traders quickly assess higher timeframe price action without switching charts.

Key Features

5 Customizable Timeframes

Displays candles from user-selected timeframes (e.g., 15m, 30m, 1H, 4H, Daily).

Each candle is offset to avoid clutter.

Visual Customization

Adjustable spacing, width, and colors for bullish/bearish candles.

Option to show/hide wicks, OHLC labels, and price guide lines.

Clear Price Reference

Dotted guide lines extend from the current price to the MTF candles for easy comparison.

OHLC labels (optional) show exact price levels.

and u can also check the remainig time of candles ..

Usefulness

✅ Multi-Timeframe Analysis – Compare trends across different timeframes at a glance.

✅ Avoid Chart Switching – See higher timeframe structure while trading lower TFs.

✅ Identify Key Levels – Spot support/resistance from higher timeframe candles.

✅ Customizable Layout – Adjust spacing and styling to fit your trading style.

Best For

Swing & position traders analyzing multiple timeframes.

Day traders looking for confluence from higher TFs.

Traders who prefer visual candlestick patterns over plain lines.

This script is particularly useful for confirming trends, spotting reversals, and aligning entries with higher timeframe structure.

Strategy Builder Pro [ChartPrime]ChartPrime Strategy Creator Overview

The ChartPrime Strategy Builder offers traders an innovative, structured approach to building and testing strategies. The Strategy Creator allows users to combine, test, and automate complex strategies with many parameters.

Key Features of the ChartPrime Strategy Builder

1. Customizable Buy and Sell Conditions

The Strategy Creator provides flexibility in establishing entry and exit rules, with separate sections for long and short strategies. Traders can combine multiple conditions in each section to fine-tune when positions are opened or closed. For instance, they might choose to only buy when the indicator signals a buy and the Dynamic Reactor (a low lag filter) indicator shows a bullish trend. Users are able to pick, mix and match the following list of features:

Signal Mode: Select the type of assistive signals you are requiring. Provided are both trend following signals with self optimization using backtest results as well as reversal signals, aiming to provide real time tops and bottoms in markets. Both these signal modes can be fine tuned using the tuning input to refine signals to a trader's liking. ChartPrime Trend Signals leverage audio engineering inspired techniques and low-pass filters in order to achieve and attempt to produce lower lag response times and therefore are designed to have a uniqueness when compared to more classical trend following approaches.

The Dynamic Reactor: provides a simple band passing through the chart. This can provide assistance in support and resistance locations as well as identifying the trend direction expressed via green and red colors. Taking a moving average and applying unique adaptivity calculations gives this plot a unique and fast behavior.

Candlestick structures: analyze candlestick formation putting a spin on classical candlestick patterns and provide the most relevant formations on the chart. These are not classical and are filtered by further analyzing market activity. A trader's classic with a spin.

The Prime Trend Assistant: provides a trend following dynamic support and resistance level. This makes it perfect to use in confluence or as a filter for other supporting indicators. This is an adaptive trend following system designed to handle volatility leveraging filter kernels as opposed to low pass filters.

Money Flow: with further filters applied for early response to money flow changes in the market. This can be a great filter in trends.

Oscillator reversals: are built in leveraging an oscillator focusing on market momentum allowing users to enter based on market shifts and trends along with reversals.

Volume-Inspired Signals: determine overbought and oversold conditions, adding another layer of analysis to the oscillator. These appear as orange labels, providing a simple reading into a possible reversal.

The Volume Matrix: is a volume oscillator that shows whether money is flowing into or out of the market. Green suggests an uptrend with buyers in control, while red indicates a majority of sellers. By incorporating smoothed volume analysis, it distinguishes between bullish and bearish volumes, offering an early indication of potential trend reversals.

The True 7: is a middle-ranking system that evaluates the strength of a move and the overall trend, offering a numeric or visual representation of trend strength. It can also indicate when a trend is starting to reverse, providing leading signals for potential market shifts. Rather than using an oscillator, this offers the unique edge of falling into set categories, making understanding it simple. This can be a great confluence point when designing a strategy.

Take profits: These offer real-time suggestions from our algorithm on when it might be a good time to take profit. Using these as part of a strategy allows for great entries at bottoms and tops of trends.

Using features such as the Dynamic reactor have dual purposes. Traders can use this as both a filter and an entry condition. This allows for true interoperability when using the Strategy Builder. The above conditions are duplicated for short entries too allowing for symmetrical trading systems. By disabling all of the entry conditions on either long or short areas of the settings will create a strategy that only takes a single type of position. For example; a trader that just wants to take longs can disable all short options.

2. Layered Entries

Layered entries, a feature to enhance the uniqueness in the tool. It allows traders to average into positions as the market moves, rather than committing all capital at once. This feature is particularly useful for volatile markets where prices may fluctuate substantially. The Strategy Builder lets users adjust the number of layered entries, which can help in managing risk and optimizing entry points as well as the aggressiveness of the safety orders. With each safety order placed the system will automatically and dynamically scale into positions reducing the average entry price and hence dynamically adjust the potential take profits. Due to the potential complexities of exiting during multiple orders, a smart system is employed to automatically take profits on the layered system aiming to take profits at peaks of trends.

Users are able to override this smart TP system at the bottom of the settings instead targeting percentage profits for both short and long positions.

Entries lowering average buy price

The ability to adjust how quickly the system layers into positions can also be adjusted via the layered entries drop down between fast and slow mode where the slow mode will be more cautious when producing new orders.

3. Flexible Take Profit (TP) and Stop Loss (SL) Options

Traders can set their TP and SL levels according to various parameters, including ATR (Average True Range), risk-reward ratio, trailing stops, or specific price changes. If layered entries are active, an automatic TP method is applied by default, though traders can manually specify TP values if they prefer. This setup allows for precise control over trade exits, tailored to the strategy’s risk profile.

Provided options

The ability to use external take profits and stop losses is also provided. By loading an indicator of your choice the plots will be added to the chart. By navigating to the external sources area of the settings, users can select this plot and use it as part of a wider trading system.

Example: Let’s say a user has entries based on the inbuilt trend signals and wishes to exit whenever the RSI crosses above 70, they can add RSI to the chart, select crossing up and enter the value of 70.

4. Integrated Reinvestment for Compounding Gains

The reinvestment option allows traders to reinvest a portion of their gains into future trades, increasing trade size over time and benefiting from compounding. For example, a user might set 30% of each trade's profit to reinvest, with the remaining 70% allocated for risk management or additional safety orders. This approach can enhance long-term growth while balancing risk.

Generally in trading it can be a good approach to take profits so we suggest a healthy balance. This setting is generally best used for slow steady strategies with the long term aim of accumulating as much of the asset as possible.

5. Leverage and Position Sizing

Users can configure leverage and position sizing to simulate varying risk levels and capital allocations. A dashboard on the interface displays margin requirements based on the selected leverage, allowing traders to estimate trade sizes relative to their available capital. Whenever using leverage especially with layered entries it’s important to keep a close eye on the position sizes to avoid potential liquidations.

6. Pre-Configured Strategies for Immediate Testing

For users seeking a starting point, ChartPrime includes a range of preset strategies. These were developed and backtested by ChartPrime’s team. This allows traders to start with a stable base and adapt it to their own preferences. It is vital to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. These pre-built configurations offer a structured way and base to design strategies off of. These are also subject to changing results as new price action arrives and they become outdated. They serve the purpose of simply being example use cases.

7. In-Depth Specific Backtesting Ranges

The Strategy Builder includes backtesting capabilities, providing a clear view of how different setups would have performed over specified time periods. Traders can select date ranges to target specific market conditions, then review results on TradingView to see how their strategies perform across different market trends.

Example Use Case: Developing a Strategy

Consider a trader who is focused on long positions only and prefers a lower-risk strategy (note these tools can be used for all assets; we are using an undisclosed asset as an example). Using the Strategy Builder, they could:

- Disable short conditions.

- Set long entry rules to trigger when both the ChartPrime oscillator and Quantum Reactor indicators show bullish signals.

- Enable layered entries to improve average entry prices by adding to positions during market dips.

- Run a backtest over a two-year period to see historical performance trends, making adjustments as needed.

The backtest will show where entries and exits would have occurred and how layered entries may have impacted profitability.

8. Iterative design